Supplementary Appendix for Liquidity, Volume, and Price ...

20

Supplementary Appendix for Liquidity, Volume, and Price Behavior: The Impact of Order vs. Quote Based Trading –not for publication– Katya Malinova * University of Toronto Andreas Park † University of Toronto March 16, 2009 Abstract This document contains an extensive number of tables and graphs to support the numerical analysis in Sections 5 and 6 of the main text; these figures are num- bered consecutively following those in the main text. This document also provides additional information about the institutional background of trading mechanisms, technical details of the information structure used in the main text and, a detailed description of the simulation process that we employed to obtain our results in Section 8 of the main text. * Email: [email protected]; web: http://individual.utoronto.ca/kmalinova/. † Email: [email protected]; web: http://www.chass.utoronto.ca/∼apark/.

Transcript of Supplementary Appendix for Liquidity, Volume, and Price ...

Supplementary Appendix for

Liquidity, Volume, and Price Behavior:

The Impact of Order vs. Quote Based Trading

–not for publication–

Katya Malinova∗

University of Toronto

Andreas Park†

University of Toronto

March 16, 2009

Abstract

This document contains an extensive number of tables and graphs to support

the numerical analysis in Sections 5 and 6 of the main text; these figures are num-

bered consecutively following those in the main text. This document also provides

additional information about the institutional background of trading mechanisms,

technical details of the information structure used in the main text and, a detailed

description of the simulation process that we employed to obtain our results in

Section 8 of the main text.

∗Email: [email protected]; web: http://individual.utoronto.ca/kmalinova/.†Email: [email protected]; web: http://www.chass.utoronto.ca/∼apark/.

C Appendix: The Institutional Background

Our treatment of price formation in the dealer market is stylized: effectively, people sub-

mit their market orders without knowing the price and there are no standing quotes from

dealers. Of course, in real markets dealers do post quotes, but they usually quote only

a single bid and a single ask price. Moreover, for most markets, dealers are commonly

required to trade a guaranteed minimum number of units at this price (for instance,

on Nasdaq a quote‘must be “good” for 1000 shares for most stocks). Alternatively, on

exchanges such as the TSX or Paris Bourse, the upstairs dealers are required to trade at

the best bid or offer (BBO) that is currently on the book, unless the size of the trade is

very large. Finally, trading systems or exchanges that include small-order routing (i.e.

small orders are given to different dealers according to a pre-determined set of routing

rules) require dealers to do price improvement, that is they require dealers to give small

size orders the best price that is currently quoted.

None of these institutional details contradict our setup. First, the defining feature of

dealer markets is that the dealer will know the size of the trade when quoting the uniform

price for the order. Thus the dealer quotes cannot be ‘hit’ in the same way as a standing

limit order in a consolidated limit order book. Next, in the theoretical analysis of our

paper we describe that the dealer charges different prices for different quantities. The

bid- and ask-prices that she quotes would be for the minimum quantity that she must

trade — and this quantity may well be “large”; in other words, the quoted ask price may

be ask2

D, but when facing a small order, the dealer may offer ask1

D. Third, in our model

traders accurately anticipate the price that they will be quoted. Consequently, quotes

will be self-fulfilling. Finally, the BBO requirement in upstairs-downstairs markets is

trivially satisfied in the hybrid market.

D Appendix: Quality and Belief Distributions

Financial market microstructure models with binary signals and states typically employ

a constant signal quality q ∈ [1/2, 1], with Pr(S = v|V = v) = q. Our framework has

a continuum of possible qualities with a continuous density function and, as outlined

above, we will map investors’ signals and their qualities into a continuous private belief

on [0, 1]. The quality parametrization on [1/2, 1] is very natural, as a trader who receives

a high signal h will update his prior in favor of the high liquidation value, V = 1, and a

trader who receives a low signal l will update his prior in favor of V = 0. We thus use

the conventional parametrization on [1/2, 1] in the main text.

1 Appendix for Trading Mechanisms & Market Dynamics

However, to characterize the map from investors’ signal and qualities into their pri-

vate beliefs and to derive the distributions of the latter, it is mathematically convenient

to normalize the signal quality so that its domain coincides with that of the private

belief. We will denote the distribution function of this normalized quality on [0, 1] by G

and its density by g, whereas the distribution and density functions of original qualities

on [1/2, 1] will be denoted by G̃ and g̃ respectively.

The normalization proceeds as follows. Without loss of generality, we will employ

the density function g that is symmetric around 1/2. For q ∈ [0, 1/2], we then have

g(q) = g̃(1 − q)/2 and for q ∈ [1/2, 1], we have g(q) = g̃(q)/2.

Under this specification, signal qualities q and 1−q are equally useful for the individ-

ual: if someone receives signal h and has quality 1/4, then this signal has ‘the opposite

meaning’, i.e. it has the same meaning as receiving signal l with quality 3/4. Signal

qualities are assumed to be independent across agents, and independent of the security’s

liquidation value V .

Beliefs are derived by Bayes Rule, given signals and signal-qualities. Specifically, if

a trader is told that his signal quality is q and receives a high signal h then his belief

is q/[q + (1 − q)] = q (respectively 1 − q if he receives a low signal l), because the prior

is 1/2. The belief π is thus held by people who receive signal h and quality q = π and by

those who receive signal l and quality q = 1−π. Consequently, the density of individuals

with belief π is given by f1(π) = π[g(π) + g(1 − π)] in state V = 1 and analogously by

f0(π) = (1 − π)[g(π) + g(1 − π)] in state V = 0.

Smith and Sorensen (2008) prove the following property of private beliefs (Lemma 2

in their paper):

Lemma 1 (Symmetric beliefs, Smith and Sorensen (2008))

With the above the signal quality structure, private belief distributions satisfy F1(π) =

1 − F0(1 − π) for all π ∈ (0, 1).

Proof: Since f1(π) = π[g(π) + g(1 − π)] and f0(π) = (1 − π)[g(π) + g(1 − π)], we have

f1(π) = f0(1 − π). Integrating, F1(π) =∫ π

0f1(x)dx =

∫ π

0f0(1 − x)dx =

∫1

1−πf0(x)dx =

1 − F0(1 − π). �

A direct implication of this lemma is that with symmetric thresholds, πb = 1− πs, a

buy in state V = 1 is as likely as a sale in state V = 0, because

β1 = (1− µ)/2 + µ(1− F1(πb)) = (1− µ)/2 + µF0(1− πbb) = (1− µ)/2 + µF0(πs) = σ0.

Similarly, β0 = σ1. Next, the belief densities satisfy the monotone likelihood ratio

2 Appendix for Trading Mechanisms & Market Dynamics

property becausef1(π)

f0(π)=

π[g(π) + g(1 − π)]

(1 − π)[g(π) + g(1 − π)]=

π

1 − π

is increasing in π.

One can recover the distribution of qualities on [1/2, 1], denoted by G̃, from G by

combining qualities that yield the same beliefs for opposing signals (e.g q = 1/4 and

signal h is combined with q = 3/4 and signal l). With symmetric g, G(1/2) = 1/2, and

G̃(q) =

∫ q

1

2

g(s)ds +

∫ 1

2

1−q

g(s)ds = 2

∫ q

1

2

g(s)ds = 2G(q) − 2G(1/2) = 2G(q) − 1. (1)

E Simulation Procedure for Price Efficiency

We employed the following data generation procedure for the simulations: We ob-

tained 500,000 observations of trading days for each of the Poisson arrival rates ρ ∈

{5, 10, 15, 20, 25, 30, 35, 40, 45, 50} and levels of informed trading µ ∈ {.1, .2, .3, .4, .5, .6,

.7, .8, .9}. Here, the Poisson arrival rate ρ implies that, on average, there are ρ traders

(though some may choose not to trade). Fixing the true value to V = 1, prices are closer

to the true value if they are larger. To get a better sense of the effect of a small ρ for

transparent vs. opaque hybrid markets, we also ran ρ ∈ {1, 2, . . . , 14} for µ ∈ {.2, .5, .8},

as outlined in the main text.

For each series, we first drew the number of traders for the session and performed

the random allocation of traders into noise and informed. Thus overall there were, for

instance, approximately 25,000,000 trades for ρ = 50. The informed traders were then

equipped with a signal quality and a draw of the high or low signal for that quality,

conditional on V = 1. Noise traders were assigned a random trading role. We then

determined a random entry order and for the hybrid market performed an additional

random draw to determine in which market the respective trader will be placing this

order. Finally, we computed the end-prices that would result for each trading sessions

under each of the four trading regimes. One can think of these prices at the prices that

would obtain at the end of a trading day. Our results are for the distribution of these

final prices. Our descriptions on properties of the empirical distributions are based on

the case with ρ = 50. The rule of thumb is that the larger is ρ, the diverse the outcomes

of trading rounds are and the closer are the distributions of end prices to a smooth

continuous function (for small values of ρ they resemble step functions).

3 Appendix for Trading Mechanisms & Market Dynamics

mu

Ask

(lim

it)-A

sk(hyb

rid)

0.005

0.010

0.015

0.020

mu

Ask(hyb

rid)-A

sk(dealer)

0.01

0.02

0.03

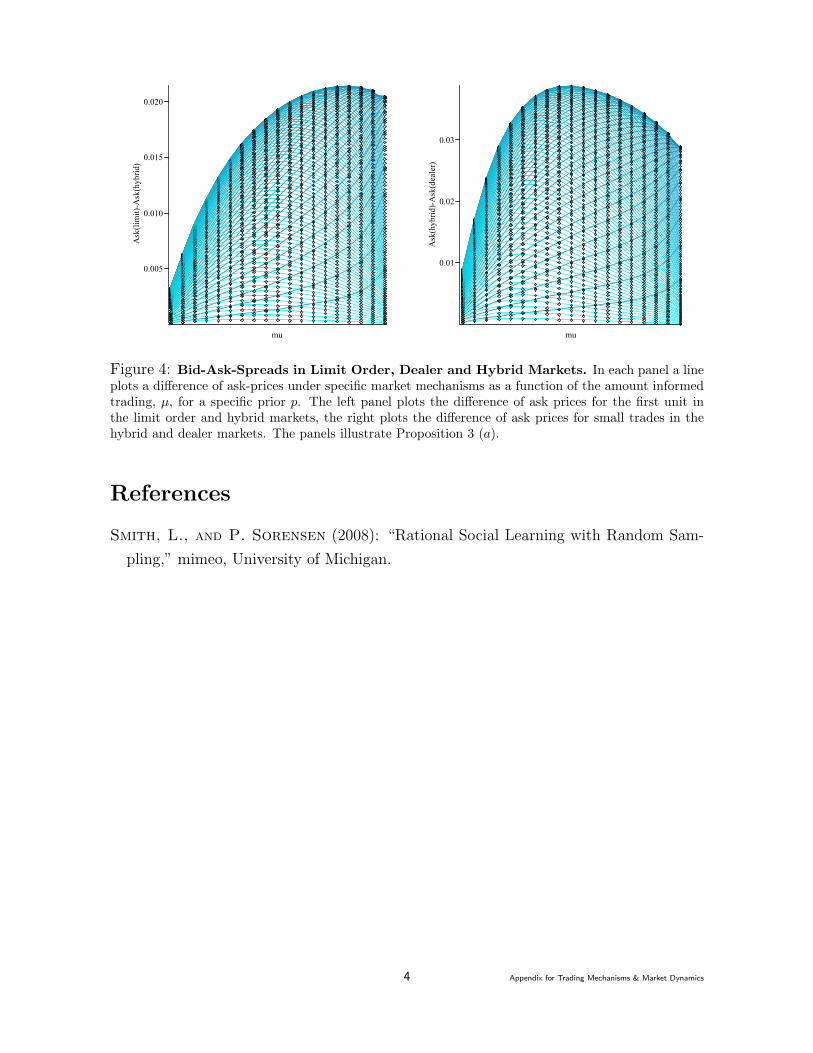

Figure 4: Bid-Ask-Spreads in Limit Order, Dealer and Hybrid Markets. In each panel a lineplots a difference of ask-prices under specific market mechanisms as a function of the amount informedtrading, µ, for a specific prior p. The left panel plots the difference of ask prices for the first unit inthe limit order and hybrid markets, the right plots the difference of ask prices for small trades in thehybrid and dealer markets. The panels illustrate Proposition 3 (a).

References

Smith, L., and P. Sorensen (2008): “Rational Social Learning with Random Sam-

pling,” mimeo, University of Michigan.

4 Appendix for Trading Mechanisms & Market Dynamics

m

Cos

t(lim

it)-C

ost(hy

brid)

K0.0150

K0.0125

K0.0100

K0.0075

K0.0050

K0.0025

m

Cos

t(hy

brid)-Cos

t(de

aler)

K0.03

K0.02

K0.01

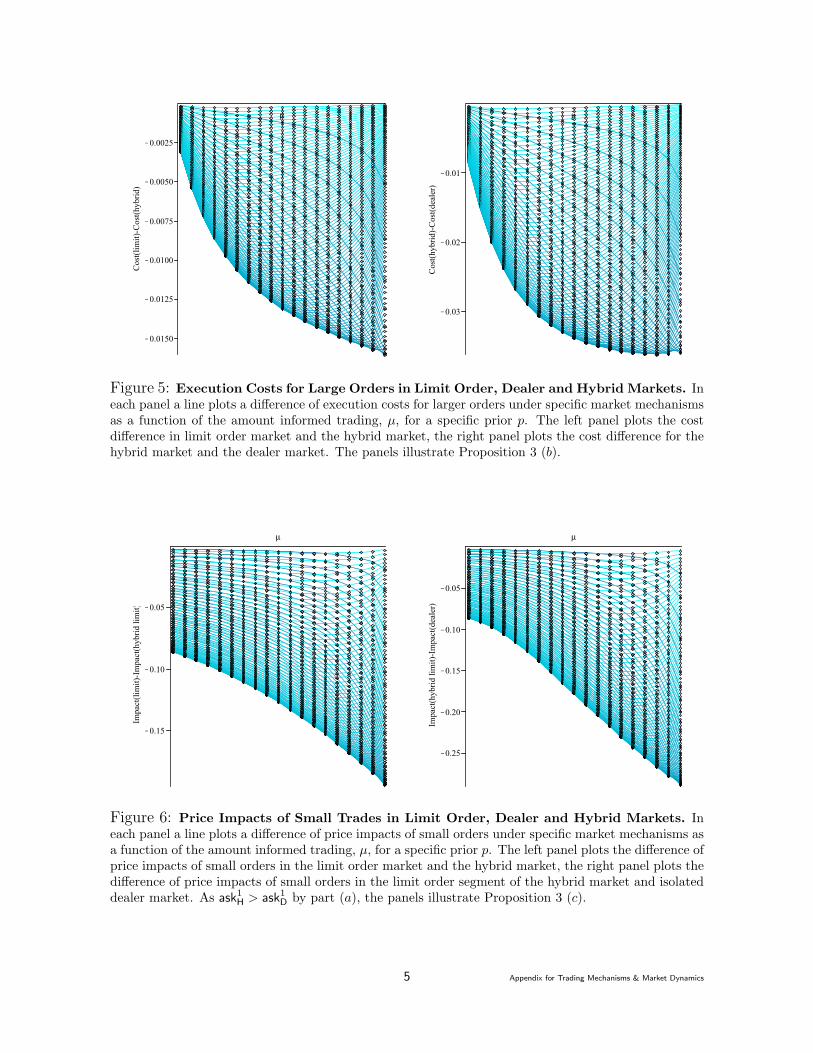

Figure 5: Execution Costs for Large Orders in Limit Order, Dealer and Hybrid Markets. Ineach panel a line plots a difference of execution costs for larger orders under specific market mechanismsas a function of the amount informed trading, µ, for a specific prior p. The left panel plots the costdifference in limit order market and the hybrid market, the right panel plots the cost difference for thehybrid market and the dealer market. The panels illustrate Proposition 3 (b).

m

Impa

ct(l

imit)

-Im

pact

(hyb

rid

limit)

K0.15

K0.10

K0.05

m

Impa

ct(h

ybri

d lim

it)-I

mpa

ct(d

eale

r)

K0.25

K0.20

K0.15

K0.10

K0.05

Figure 6: Price Impacts of Small Trades in Limit Order, Dealer and Hybrid Markets. Ineach panel a line plots a difference of price impacts of small orders under specific market mechanisms asa function of the amount informed trading, µ, for a specific prior p. The left panel plots the difference ofprice impacts of small orders in the limit order market and the hybrid market, the right panel plots thedifference of price impacts of small orders in the limit order segment of the hybrid market and isolateddealer market. As ask

1

H > ask1

D by part (a), the panels illustrate Proposition 3 (c).

5 Appendix for Trading Mechanisms & Market Dynamics

m

Impa

ct(h

ybri

d lim

it)-I

mpa

ct(l

imit)

, lar

ge tr

ades

0.01

0.02

0.03

m

Impa

ct(d

eale

r)-I

mpa

ct(h

ybri

d de

aler

), la

rge

trad

es

0.005

0.010

0.015

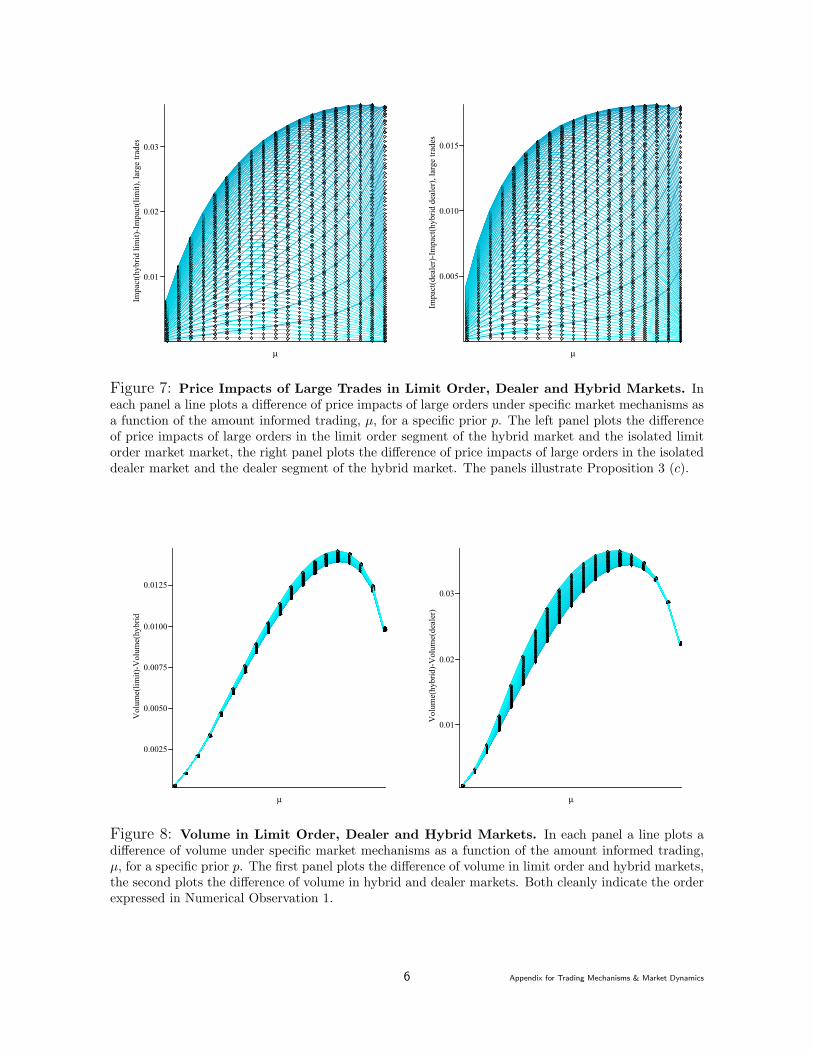

Figure 7: Price Impacts of Large Trades in Limit Order, Dealer and Hybrid Markets. Ineach panel a line plots a difference of price impacts of large orders under specific market mechanisms asa function of the amount informed trading, µ, for a specific prior p. The left panel plots the differenceof price impacts of large orders in the limit order segment of the hybrid market and the isolated limitorder market market, the right panel plots the difference of price impacts of large orders in the isolateddealer market and the dealer segment of the hybrid market. The panels illustrate Proposition 3 (c).

m

Volum

e(lim

it)-V

olum

e(hy

brid)

0.0025

0.0050

0.0075

0.0100

0.0125

m

Volum

e(hy

brid)-Volum

e(de

aler)

0.01

0.02

0.03

Figure 8: Volume in Limit Order, Dealer and Hybrid Markets. In each panel a line plots adifference of volume under specific market mechanisms as a function of the amount informed trading,µ, for a specific prior p. The first panel plots the difference of volume in limit order and hybrid markets,the second plots the difference of volume in hybrid and dealer markets. Both cleanly indicate the orderexpressed in Numerical Observation 1.

6 Appendix for Trading Mechanisms & Market Dynamics

Closing Price Limit Order Market - Dealer Market5 10 15 20 25 30 35 40 45 50

0.1 0.0003 0.0006 0.0009 0.0012 0.0014 0.0016 0.0019 0.0020 0.0022 0.0024+ + + + + + + + + +

0.2 0.0029 0.0051 0.0069 0.0083 0.0095 0.0104 0.0111 0.0116 0.0120 0.0125+ + + + + + + + + +

0.3 0.0074 0.0119 0.0148 0.0170 0.0180 0.0188 0.0192 0.0193 0.0189 0.0186+ + + + + + + + + +

0.4 0.0116 0.0170 0.0198 0.0207 0.0207 0.0205 0.0194 0.0185 0.0171 0.0159+ + + + + + + + + +

0.5 0.0132 0.0180 0.0193 0.0191 0.0178 0.0161 0.0145 0.0125 0.0110 0.0096+ + + + + + + + + +

0.6 0.0121 0.0150 0.0145 0.0135 0.0117 0.0096 0.0079 0.0064 0.0052 0.0043+ + + + + + + + + +

0.7 0.0076 0.0090 0.0086 0.0070 0.0053 0.0042 0.0033 0.0024 0.0019 0.0014+ + + + + + + + + +

0.8 0.0014 0.0019 0.0017 0.0013 0.0011 0.0008 0.0005 0.0003 0.0002 0.0002+ + + + + + + + + +

0.9 -0.0081 -0.0062 -0.0045 -0.0032 -0.0019 -0.0013 -0.0008 -0.0004 -0.0003 -0.0002- - - - - - - - - -

Table 1: Difference of Average Closing Prices: Limit Order vs. Dealer Market. Thistable is based upon the simulations described in the main text. Columns denote the entry rateρ, rows the level of informed trading µ. Thus each entry denotes the difference of the averageclosing prices in Limit Order and Dealer markets for a specific (ρ, µ)-combination. As theunderlying true value is V = 1, the higher a price is, the closer it is to the true value and thusthe more efficient it is. Thus a positive difference of the average closing prices indicates thatthe Limit Order Market is more efficient. As the table indicates, this is always the case butfor the largest values of µ that we considered. This table relates to Numerical Observation 2.

7 Appendix for Trading Mechanisms & Market Dynamics

Closing Price Limit Order Market - Hybrid Market5 10 15 20 25 30 35 40 45 50

0.1 -0.0004 -0.0009 -0.0012 -0.0015 -0.0019 -0.0021 -0.0024 -0.0028 -0.0029 -0.0032- - - - - - - - - -

0.2 -0.0010 -0.0018 -0.0023 -0.0028 -0.0031 -0.0036 -0.0037 -0.0039 -0.0041 -0.0043- - - - - - - - - -

0.3 -0.0011 -0.0018 -0.0023 -0.0025 -0.0029 -0.0028 -0.0027 -0.0030 -0.0030 -0.0027- - - - - - - - - -

0.4 -0.0009 -0.0015 -0.0016 -0.0019 -0.0019 -0.0017 -0.0016 -0.0015 -0.0016 -0.0011- - - - - - - - - -

0.5 -0.0010 -0.0014 -0.0014 -0.0013 -0.0012 -0.0011 -0.0009 -0.0008 -0.0006 -0.0006- - - - - - - - - -

0.6 -0.0013 -0.0014 -0.0014 -0.0011 -0.0010 -0.0009 -0.0008 -0.0006 -0.0005 -0.0004- - - - - - - - - -

0.7 -0.0022 -0.0022 -0.0018 -0.0015 -0.0012 -0.0009 -0.0005 -0.0005 -0.0003 -0.0002- - - - - - - - - -

0.8 -0.0034 -0.0032 -0.0027 -0.0021 -0.0013 -0.0009 -0.0006 -0.0004 -0.0003 -0.0002- - - - - - - - - -

0.9 -0.0061 -0.0051 -0.0038 -0.0027 -0.0016 -0.0011 -0.0007 -0.0004 -0.0002 -0.0002- - - - - - - - - -

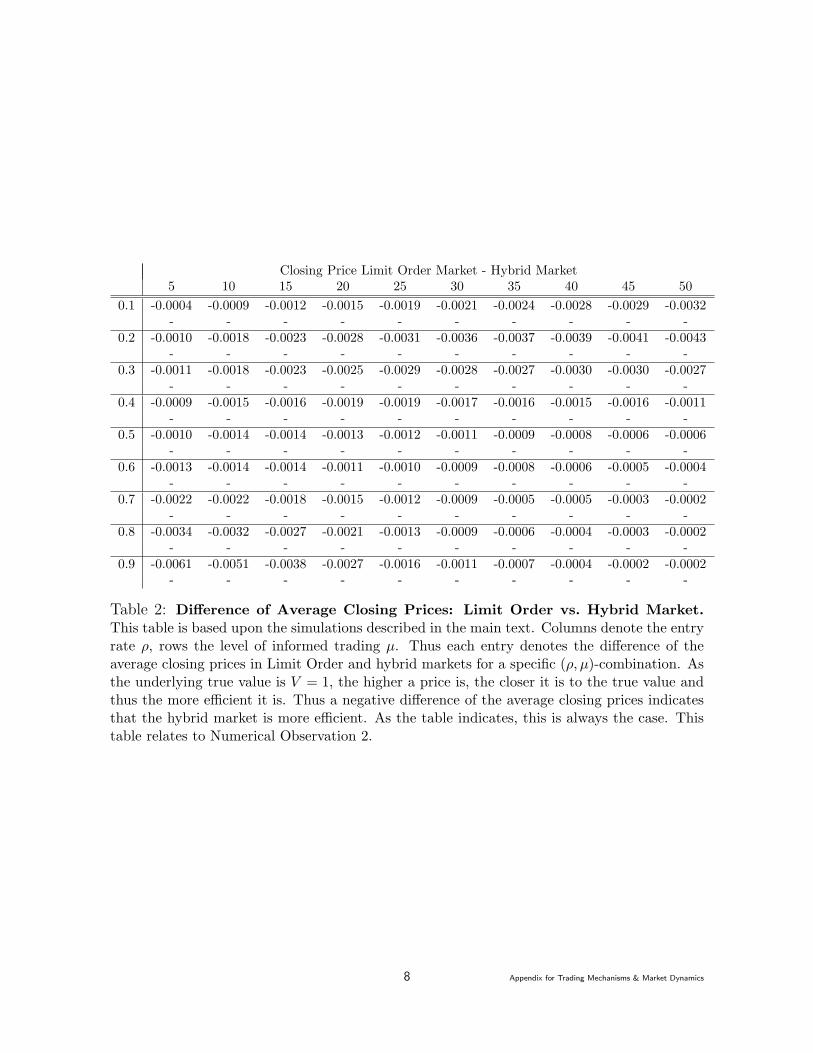

Table 2: Difference of Average Closing Prices: Limit Order vs. Hybrid Market.

This table is based upon the simulations described in the main text. Columns denote the entryrate ρ, rows the level of informed trading µ. Thus each entry denotes the difference of theaverage closing prices in Limit Order and hybrid markets for a specific (ρ, µ)-combination. Asthe underlying true value is V = 1, the higher a price is, the closer it is to the true value andthus the more efficient it is. Thus a negative difference of the average closing prices indicatesthat the hybrid market is more efficient. As the table indicates, this is always the case. Thistable relates to Numerical Observation 2.

8 Appendix for Trading Mechanisms & Market Dynamics

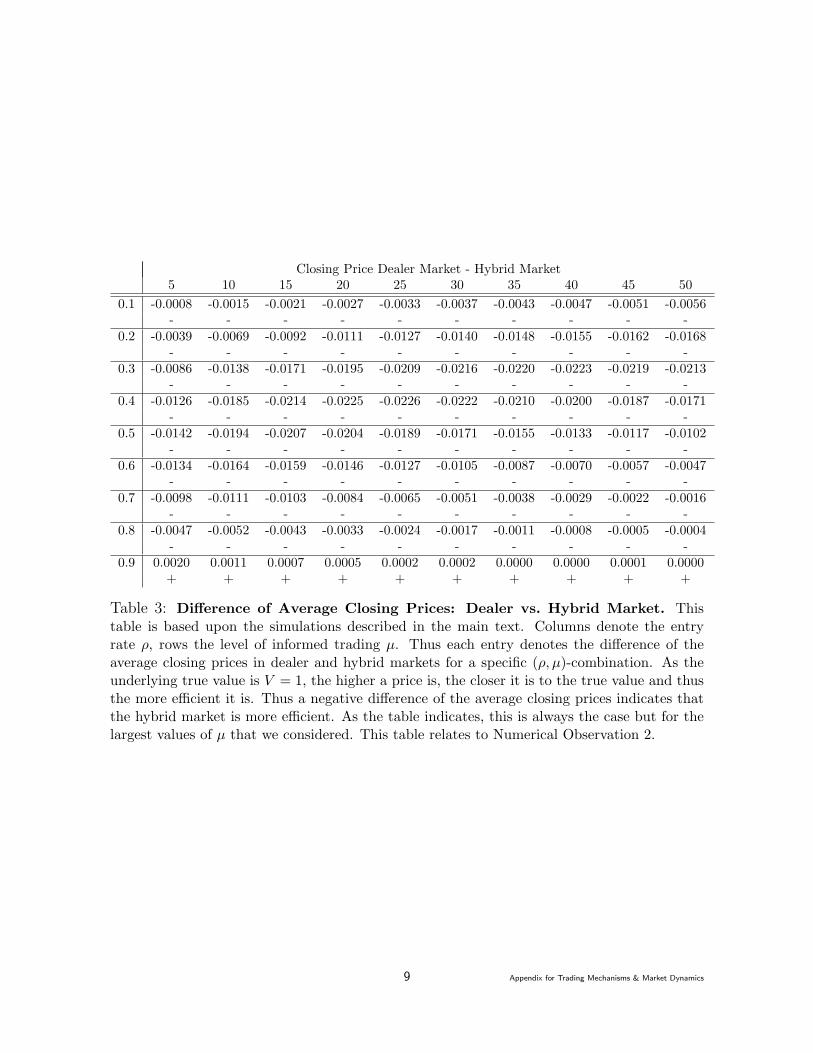

Closing Price Dealer Market - Hybrid Market5 10 15 20 25 30 35 40 45 50

0.1 -0.0008 -0.0015 -0.0021 -0.0027 -0.0033 -0.0037 -0.0043 -0.0047 -0.0051 -0.0056- - - - - - - - - -

0.2 -0.0039 -0.0069 -0.0092 -0.0111 -0.0127 -0.0140 -0.0148 -0.0155 -0.0162 -0.0168- - - - - - - - - -

0.3 -0.0086 -0.0138 -0.0171 -0.0195 -0.0209 -0.0216 -0.0220 -0.0223 -0.0219 -0.0213- - - - - - - - - -

0.4 -0.0126 -0.0185 -0.0214 -0.0225 -0.0226 -0.0222 -0.0210 -0.0200 -0.0187 -0.0171- - - - - - - - - -

0.5 -0.0142 -0.0194 -0.0207 -0.0204 -0.0189 -0.0171 -0.0155 -0.0133 -0.0117 -0.0102- - - - - - - - - -

0.6 -0.0134 -0.0164 -0.0159 -0.0146 -0.0127 -0.0105 -0.0087 -0.0070 -0.0057 -0.0047- - - - - - - - - -

0.7 -0.0098 -0.0111 -0.0103 -0.0084 -0.0065 -0.0051 -0.0038 -0.0029 -0.0022 -0.0016- - - - - - - - - -

0.8 -0.0047 -0.0052 -0.0043 -0.0033 -0.0024 -0.0017 -0.0011 -0.0008 -0.0005 -0.0004- - - - - - - - - -

0.9 0.0020 0.0011 0.0007 0.0005 0.0002 0.0002 0.0000 0.0000 0.0001 0.0000+ + + + + + + + + +

Table 3: Difference of Average Closing Prices: Dealer vs. Hybrid Market. Thistable is based upon the simulations described in the main text. Columns denote the entryrate ρ, rows the level of informed trading µ. Thus each entry denotes the difference of theaverage closing prices in dealer and hybrid markets for a specific (ρ, µ)-combination. As theunderlying true value is V = 1, the higher a price is, the closer it is to the true value and thusthe more efficient it is. Thus a negative difference of the average closing prices indicates thatthe hybrid market is more efficient. As the table indicates, this is always the case but for thelargest values of µ that we considered. This table relates to Numerical Observation 2.

9 Appendix for Trading Mechanisms & Market Dynamics

−.0

2−

.01

0.0

1.0

2.0

3cd

f(de

aler

)−cd

f(LO

B)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

−.0

20

.02

.04

.06

cdf(

deal

er)−

cdf(

LOB

)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

0.0

2.0

4.0

6.0

8cd

f(de

aler

)−cd

f(LO

B)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

µ = .1 µ = .2 µ = .3

0.0

2.0

4.0

6.0

8.1

cdf(

deal

er)−

cdf(

LOB

)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

0.0

5.1

cdf(

deal

er)−

cdf(

LOB

)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

0.0

2.0

4.0

6.0

8.1

cdf(

deal

er)−

cdf(

LOB

)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

µ = .4 µ = .5 µ = .6

0.0

1.0

2.0

3.0

4.0

5cd

f(de

aler

)−cd

f(LO

B)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

0.0

05.0

1.0

15.0

2cd

f(de

aler

)−cd

f(LO

B)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

−.0

04−

.003

−.0

02−

.001

0.0

01cd

f(de

aler

)−cd

f(LO

B)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

µ = .7 µ = .8 µ = .9

Figure 9: First Order Stochastic Dominance of Closing Prices Dealer Market vs. Limit

Order Book. The panels plot differences of empirical distributions as a functions of the price FD(p)−FL(p) and illustrates Numerical Observation 3 (a).

10 Appendix for Trading Mechanisms & Market Dynamics

−.0

20

.02

.04

cdf(

deal

er)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD dealer vs hybrid

−.0

20

.02

.04

.06

cdf(

deal

er)−

cdf(

LOB

)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

0.0

2.0

4.0

6.0

8cd

f(de

aler

)−cd

f(LO

B)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

µ = .1 µ = .2 µ = .3

0.0

2.0

4.0

6.0

8.1

cdf(

deal

er)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD dealer vs hybrid

0.0

5.1

.15

cdf(

deal

er)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD dealer vs hybrid

0.0

2.0

4.0

6.0

8.1

cdf(

deal

er)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD dealer vs hybrid

µ = .4 µ = .5 µ = .6

0.0

2.0

4.0

6cd

f(de

aler

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD dealer vs hybrid

0.0

05.0

1.0

15.0

2cd

f(de

aler

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD dealer vs hybrid

0.0

01.0

02.0

03cd

f(de

aler

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD dealer vs hybrid

µ = .7 µ = .8 µ = .9

Figure 10: First Order Stochastic Dominance of Closing Prices Dealer Market vs. Hybrid

Market. The panels plot differences of empirical distributions as a functions of the price FD(p)−FH(p)and illustrates Numerical Observation 3 (b).

11 Appendix for Trading Mechanisms & Market Dynamics

−.0

4−

.02

0.0

2.0

4cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

−.0

10

.01

.02

.03

cdf(

LOB

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

−.0

050

.005

.01

.015

.02

cdf(

LOB

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

µ = .1 µ = .2 µ = .3

0.0

05.0

1cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

0.0

02.0

04.0

06.0

08.0

1cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

0.0

01.0

02.0

03.0

04.0

05cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

µ = .4 µ = .5 µ = .6

0.0

02.0

04.0

06cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

0.0

01.0

02.0

03.0

04cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

0.0

02.0

04.0

06cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD LOB vs hybrid

µ = .7 µ = .8 µ = .9

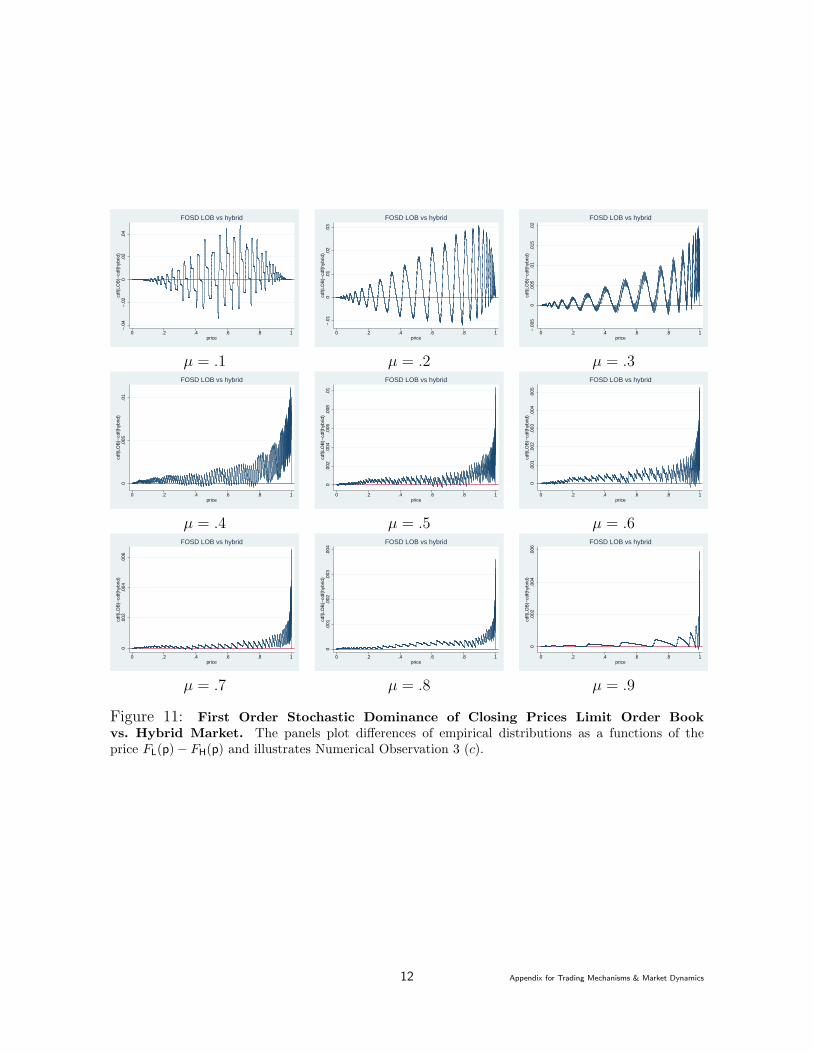

Figure 11: First Order Stochastic Dominance of Closing Prices Limit Order Book

vs. Hybrid Market. The panels plot differences of empirical distributions as a functions of theprice FL(p) − FH(p) and illustrates Numerical Observation 3 (c).

12 Appendix for Trading Mechanisms & Market Dynamics

010

2030

ccdf

(dea

ler)

−cc

df(L

OB

)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

050

100

150

ccdf

(dea

ler)

−cc

df(L

OB

)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

050

100

150

200

ccdf

(dea

ler)

−cc

df(L

OB

)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

µ = .1 µ = .2 µ = .3

050

100

150

ccdf

(dea

ler)

−cc

df(L

OB

)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

020

4060

8010

0cc

df(d

eale

r)−

ccdf

(LO

B)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

010

2030

40cc

df(d

eale

r)−

ccdf

(LO

B)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

µ = .4 µ = .5 µ = .6

05

1015

ccdf

(dea

ler)

−cc

df(L

OB

)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

0.5

11.

5cc

df(d

eale

r)−

ccdf

(LO

B)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

−.0

04−

.003

−.0

02−

.001

0.0

01cd

f(de

aler

)−cd

f(LO

B)

0 .2 .4 .6 .8 1price

FOSD dealer vs LOB

µ = .7 µ = .8 µ = .9

Figure 12: Second Order Stochastic Dominance of Closing Prices Dealer Market vs. Limit

Order Book. The panels plot differences of empirical distributions as a functions of the price∫ p

0[FD(s)−

FL(s)]ds and illustrates Numerical Observation 4 (a).

13 Appendix for Trading Mechanisms & Market Dynamics

−20

020

4060

ccdf

(dea

ler)

−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

050

100

150

200

ccdf

(dea

ler)

−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

050

100

150

200

ccdf

(dea

ler)

−cc

df(L

OB

)

0 .2 .4 .6 .8 1price

SOSD dealer vs LOB

µ = .1 µ = .2 µ = .3

050

100

150

200

ccdf

(dea

ler)

−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

020

4060

8010

0cc

df(d

eale

r)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

010

2030

4050

ccdf

(dea

ler)

−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

µ = .4 µ = .5 µ = .6

05

1015

ccdf

(dea

ler)

−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

01

23

4cc

df(d

eale

r)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

−.4

−.3

−.2

−.1

0cc

df(d

eale

r)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD dealer vs hybrid

µ = .7 µ = .8 µ = .9

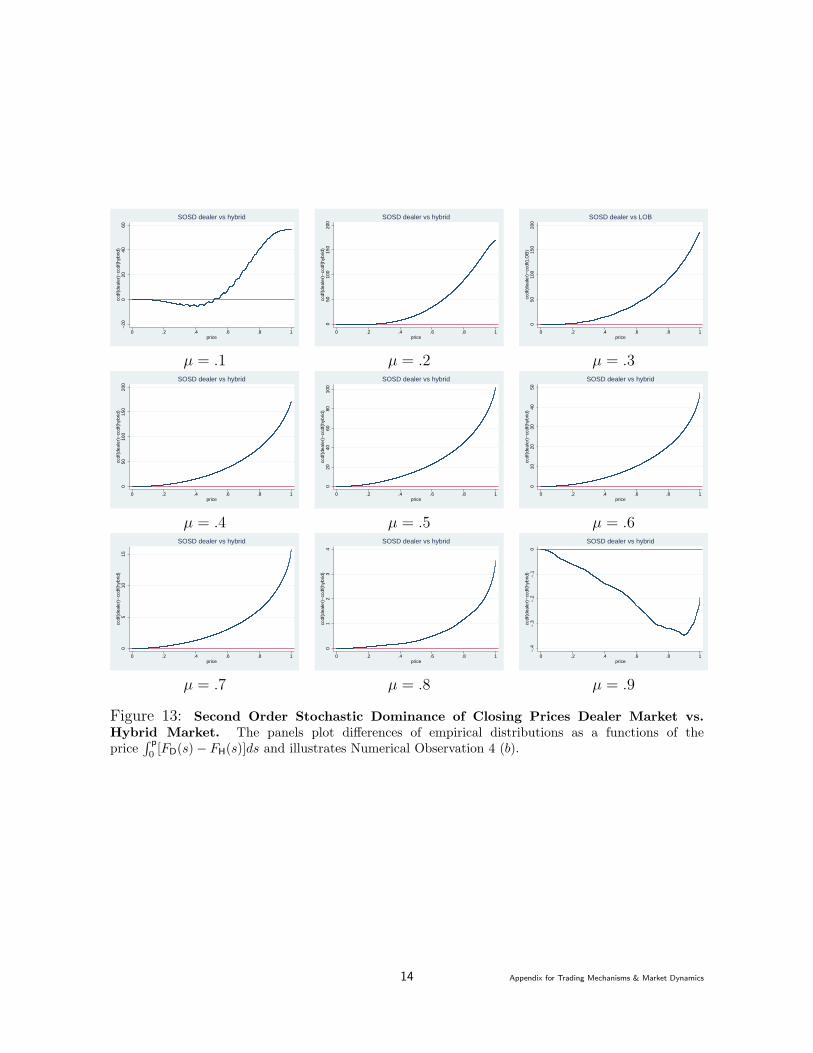

Figure 13: Second Order Stochastic Dominance of Closing Prices Dealer Market vs.

Hybrid Market. The panels plot differences of empirical distributions as a functions of theprice

∫ p

0[FD(s) − FH(s)]ds and illustrates Numerical Observation 4 (b).

14 Appendix for Trading Mechanisms & Market Dynamics

−10

010

2030

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

010

2030

40cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD LOB vs. hybrid

010

2030

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

µ = .1 µ = .2 µ = .3

05

10cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

02

46

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

01

23

4cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

µ = .4 µ = .5 µ = .6

0.5

11.

52

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

0.5

11.

52

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

0.5

11.

52

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD LOB vs. Hybrid

µ = .7 µ = .8 µ = .9

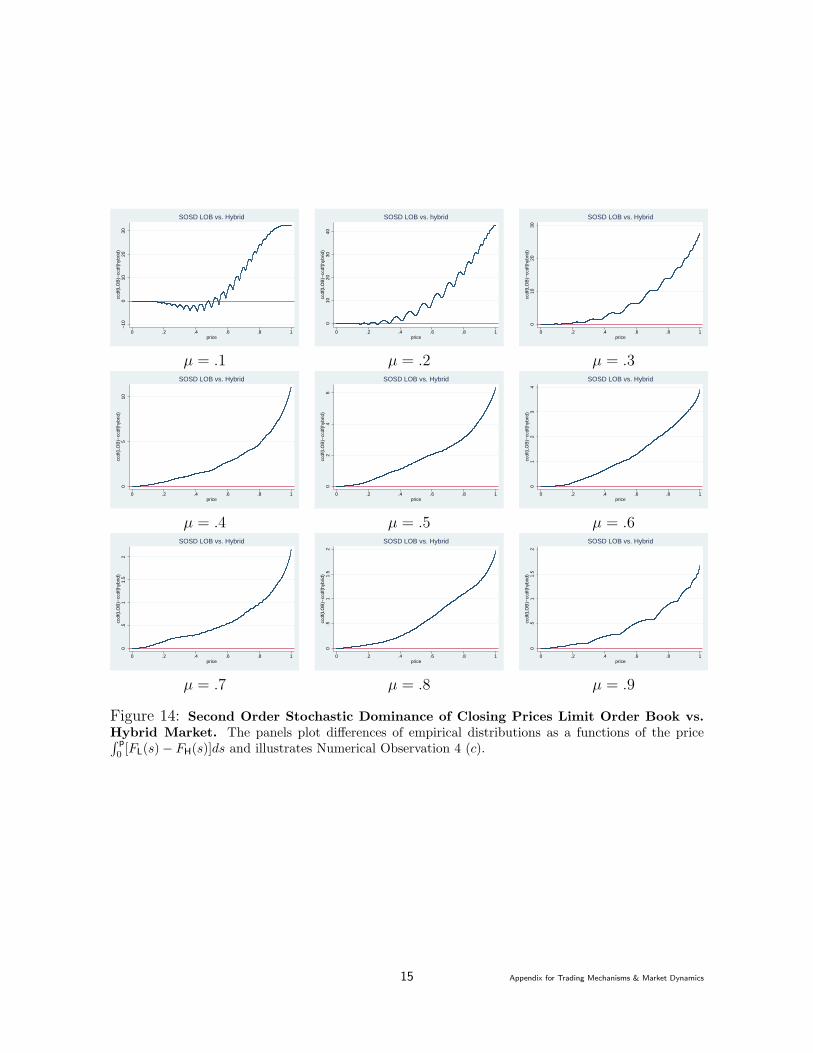

Figure 14: Second Order Stochastic Dominance of Closing Prices Limit Order Book vs.

Hybrid Market. The panels plot differences of empirical distributions as a functions of the price∫ p

0[FL(s) − FH(s)]ds and illustrates Numerical Observation 4 (c).

15 Appendix for Trading Mechanisms & Market Dynamics

Closing Price Hybrid Transparent - Hybrid Opaque5 10 15 20 25 30 35 40 45 50

0.1 0.0000 0.0001 0.0000 0.0003 0.0004 0.0006 0.0007 0.0011 0.0013 0.0013- + + + + + + + + +

0.2 0.0002 0.0007 0.0012 0.0022 0.0029 0.0038 0.0045 0.0050 0.0056 0.0062+ + + + + + + + + +

0.3 0.0001 0.0012 0.0027 0.0041 0.0052 0.0060 0.0072 0.0077 0.0079 0.0081+ + + + + + + + + +

0.4 -0.0001 0.0019 0.0037 0.0050 0.0060 0.0066 0.0071 0.0071 0.0068 0.0065- + + + + + + + + +

0.5 -0.0003 0.0018 0.0039 0.0049 0.0055 0.0054 0.0053 0.0045 0.0044 0.0040- + + + + + + + + +

0.6 -0.0011 0.0016 0.0029 0.0037 0.0038 0.0034 0.0031 0.0026 0.0022 0.0019- + + + + + + + + +

0.7 -0.0017 0.0006 0.0019 0.0022 0.0021 0.0019 0.0015 0.0012 0.0009 0.0007- + + + + + + + + +

0.8 -0.0027 -0.0003 0.0007 0.0010 0.0009 0.0008 0.0006 0.0004 0.0003 0.0002- - + + + + + + + +

0.9 -0.0034 -0.0014 -0.0003 0.0001 0.0002 0.0002 0.0002 0.0001 0.0001 0.0001- - - + + + + + + +

Table 4: Difference of Average Closing Prices: Transparent vs. Opaque Hybrid

Market. This table is based upon the simulations described in the main text. Columnsdenote the entry rate ρ, rows the level of informed trading µ. Thus each entry denotes thedifference of the average closing prices in transparent and opaque hybrid markets for a specific(ρ, µ)-combination. As the underlying true value is V = 1, the higher a price is, the closer itis to the true value and thus the more efficient it is. Thus a positive difference of the averageclosing prices indicates that the transparent hybrid market is more efficient. As the tableindicates, this is always the case but for small values of ρ that we considered; see also Table 5.This table support Numerical Observation 5 (a).

16 Appendix for Trading Mechanisms & Market Dynamics

Closing Price Hybrid Transparent - Hybrid Opaque for small rho1 2 3 4 5 6 7

0.2 -0.0001 -0.0001 0.0000 0.0000 0.0001 0.0002 0.0003- - + - + + +

0.5 -0.0009 -0.0011 -0.0011 -0.0010 -0.0005 -0.0001 0.0006- - - - - - +

0.8 -0.0028 -0.0035 -0.0035 -0.0031 -0.0026 -0.0021 -0.0017- - - - - - -

8 9 10 11 12 13 14

0.2 0.0002 0.0005 0.0006 0.0009 0.0009 0.0011 0.0012+ + + + + + +

0.5 0.0009 0.0015 0.0019 0.0025 0.0029 0.0031 0.0034+ + + + + + +

0.8 -0.0012 -0.0008 -0.0005 0.0000 0.0002 0.0003 0.0007- - - - + + +

Table 5: Difference of Average Closing Prices: Transparent vs. Opaque Hybrid

Market — small values of ρ. This table complements Table 5 and considers small valuesof ρ. is based upon the simulations described in the main text. Columns denote the entry rateρ, rows the level of informed trading µ. Thus each entry denotes the difference of the averageclosing prices in transparent and opaque hybrid markets for a specific (ρ, µ)-combination. Asthe underlying true value is V = 1, the higher a price is, the closer it is to the true value andthus the more efficient it is. Thus a positive difference of the average closing prices indicatesthat the transparent hybrid market is more efficient. As the table indicates, for small valuesof ρ, the opaque market may be more efficient. Further, for larger µ, the set of entry rates forwhich this applies is larger. This table support Numerical Observation 5 (a).

17 Appendix for Trading Mechanisms & Market Dynamics

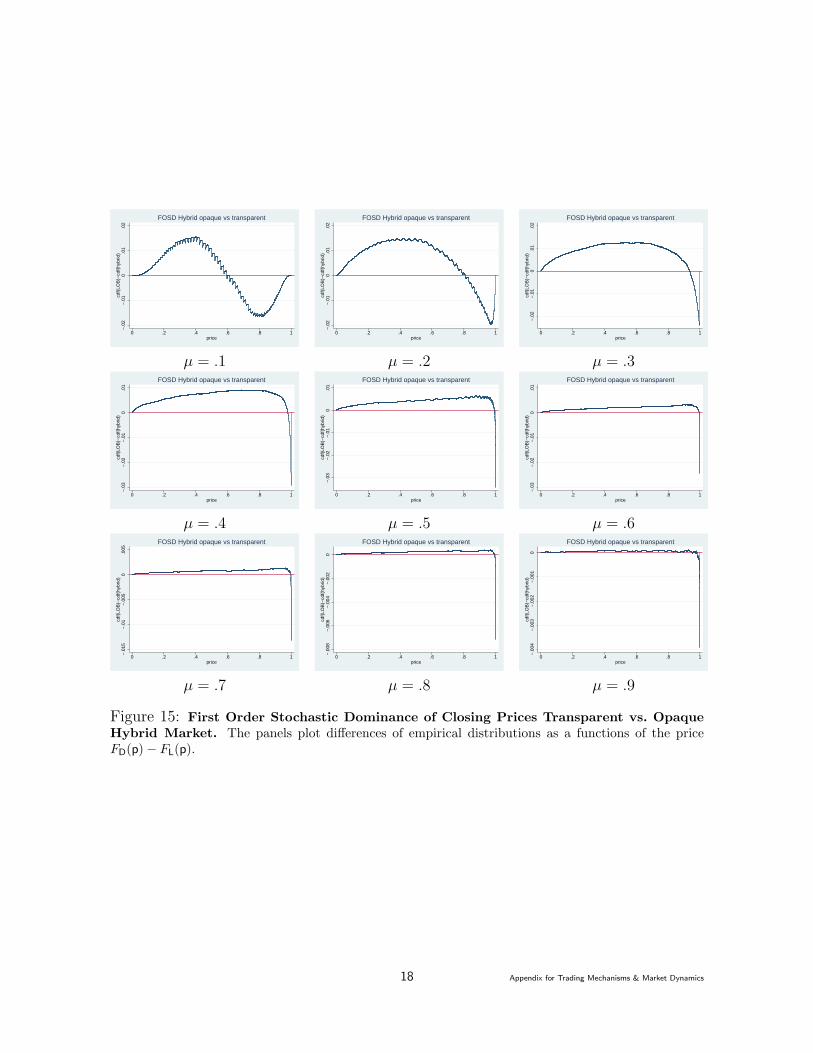

−.0

2−

.01

0.0

1.0

2cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

−.0

2−

.01

0.0

1.0

2cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

−.0

2−

.01

0.0

1.0

2cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

µ = .1 µ = .2 µ = .3

−.0

3−

.02

−.0

10

.01

cdf(

LOB

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

−.0

3−

.02

−.0

10

.01

cdf(

LOB

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

−.0

3−

.02

−.0

10

.01

cdf(

LOB

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

µ = .4 µ = .5 µ = .6

−.0

15−

.01

−.0

050

.005

cdf(

LOB

)−cd

f(hy

brid

)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

−.0

08−

.006

−.0

04−

.002

0cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

−.0

04−

.003

−.0

02−

.001

0cd

f(LO

B)−

cdf(

hybr

id)

0 .2 .4 .6 .8 1price

FOSD Hybrid opaque vs transparent

µ = .7 µ = .8 µ = .9

Figure 15: First Order Stochastic Dominance of Closing Prices Transparent vs. Opaque

Hybrid Market. The panels plot differences of empirical distributions as a functions of the priceFD(p) − FL(p).

18 Appendix for Trading Mechanisms & Market Dynamics

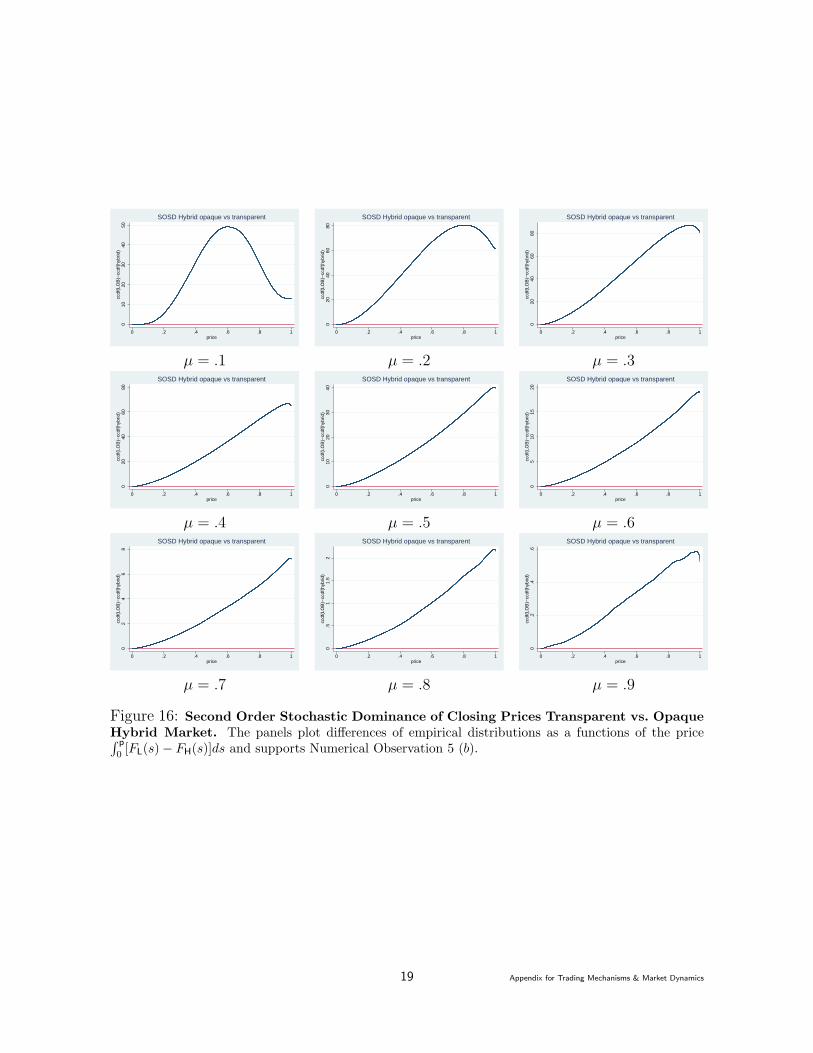

010

2030

4050

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

020

4060

80cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

020

4060

80cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

µ = .1 µ = .2 µ = .3

020

4060

80cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

010

2030

40cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

05

1015

20cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

µ = .4 µ = .5 µ = .6

02

46

8cc

df(L

OB

)−cc

df(h

ybrid

)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

0.5

11.

52

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

0.2

.4.6

ccdf

(LO

B)−

ccdf

(hyb

rid)

0 .2 .4 .6 .8 1price

SOSD Hybrid opaque vs transparent

µ = .7 µ = .8 µ = .9

Figure 16: Second Order Stochastic Dominance of Closing Prices Transparent vs. Opaque

Hybrid Market. The panels plot differences of empirical distributions as a functions of the price∫ p

0[FL(s) − FH(s)]ds and supports Numerical Observation 5 (b).

19 Appendix for Trading Mechanisms & Market Dynamics