Case Studies UNDP: SRI LANKA WILDLIFE CONSERVATION SOCIETY, Sri Lanka

David Haigh CEOBrand Finance plc

Superbrands Sri Lanka ‘Value Based Marketing’

20th March 2007

Brand Finance plc

• world’s leading independent brand valuation and strategy consultancy

• maximise shareholder valuethrough effective management

• extensive global experience of intangible asset valuation, transaction support, brand management and licensing

• specialists with unique combination of strategy, finance and marketing expertise

Brand Due Diligence

Value BasedMarketing

BrandValuation

AustraliaBrazil

USA

Canada

RussiaLondon

(HQ)

France

Holland

Croatia

Turkey

Barcelona

Madrid India

Sri Lanka

Singapore

Brand Finance: Network

Hong Kong

Dubai

Switzerland

The Intangible Revolution

‘Understanding the hidden 70% of corporate value’

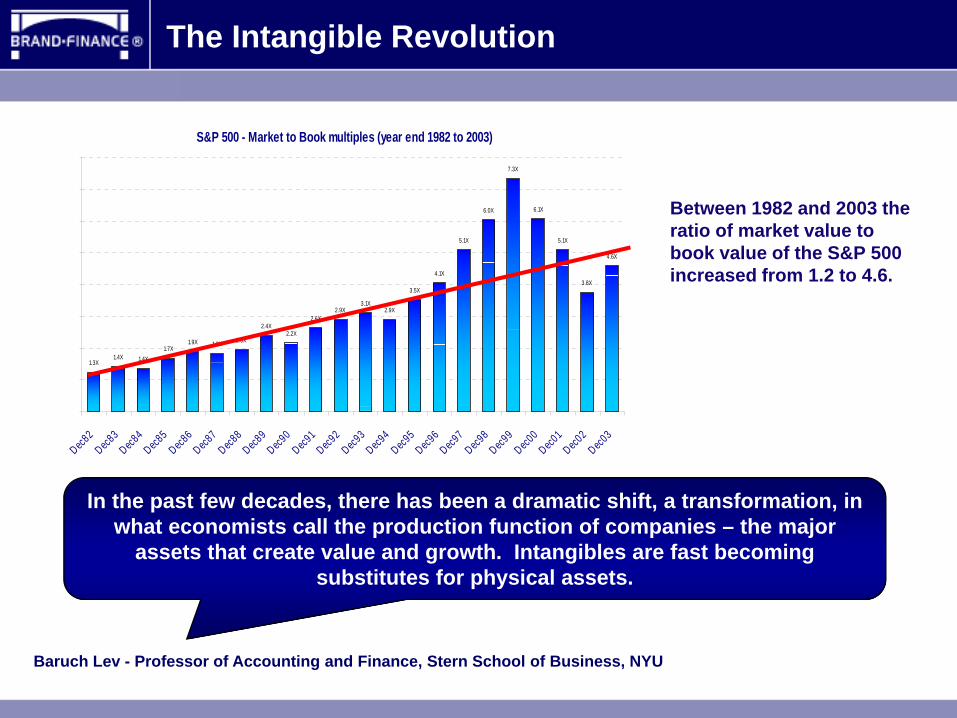

In the past few decades, there has been a dramatic shift, a transformation, in what economists call the production function of companies – the major

assets that create value and growth. Intangibles are fast becoming substitutes for physical assets.

The Intangible Revolution

Baruch Lev - Professor of Accounting and Finance, Stern School of Business, NYU

Between 1982 and 2003 the ratio of market value to book value of the S&P 500 increased from 1.2 to 4.6.

S&P 500 - Market to Book multiples (year end 1982 to 2003)

1.3X1.4X 1.4X

1.7X1.9X 1.8X 2.0X

2.4X2.2X

2.6X2.9X

3.1X2.9X

3.5X

4.1X

5.1X

6.0X

7.3X

6.1X

5.1X

3.8X

4.6X

0X

1X

2X

3X

4X

5X

6X

7X

8X

Dec82

Dec83

Dec84

Dec85

Dec86

Dec87

Dec88

Dec89

Dec90

Dec91

Dec92

Dec93

Dec94

Dec95

Dec96

Dec97

Dec98

Dec99

Dec00

Dec01

Dec02

Dec03

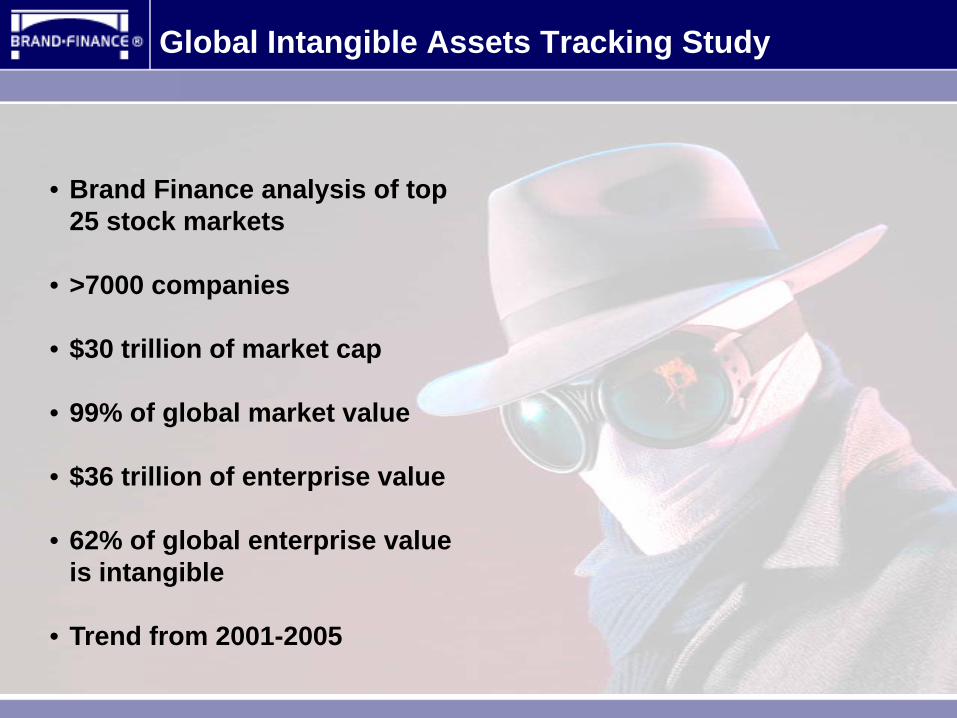

Global Intangible Assets Tracking Study

• Brand Finance analysis of top 25 stock markets

• >7000 companies

• $30 trillion of market cap

• 99% of global market value

• $36 trillion of enterprise value

• 62% of global enterprise value is intangible

• Trend from 2001-2005

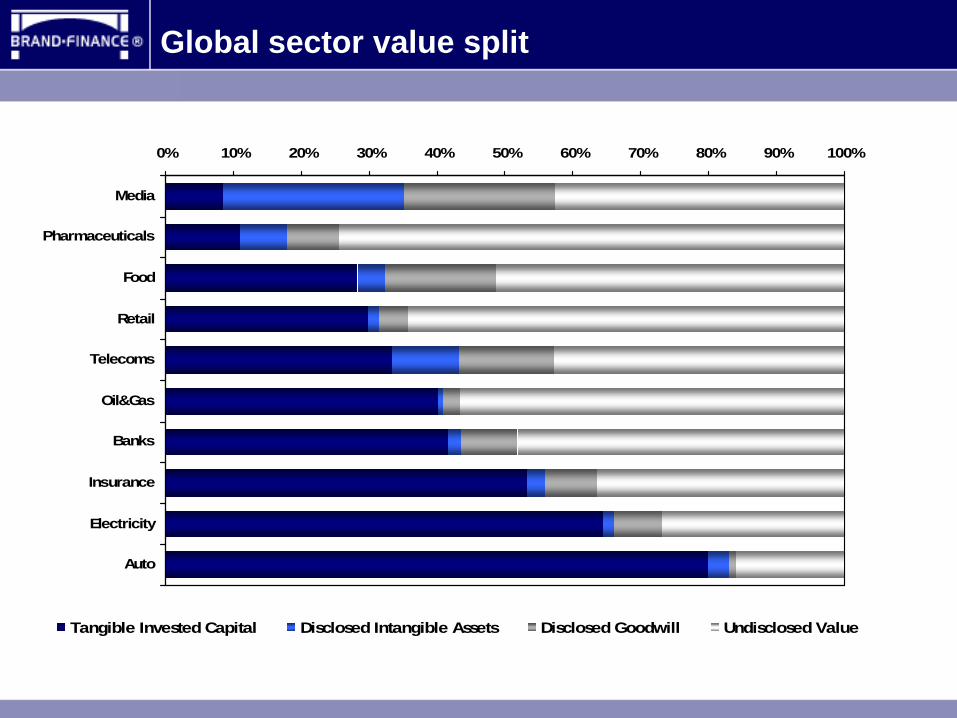

Global sector value split

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Media

Pharmaceuticals

Food

Retail

Telecoms

Oil&Gas

Banks

Insurance

Electricity

Auto

Tangible Invested Capital Disclosed Intangible Assets Disclosed Goodwill Undisclosed Value

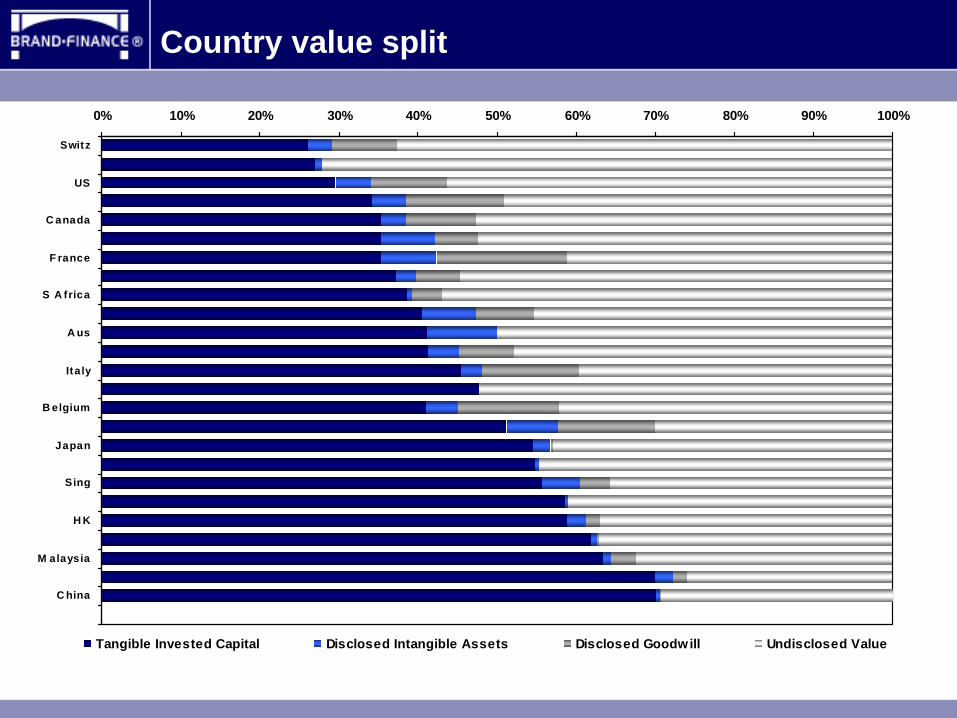

Country value split

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Switz

US

C anada

F rance

S A frica

A us

Italy

B elgium

Japan

Sing

H K

M alaysia

C hina

Tangible Invested Capital Disclosed Intangible Assets Disclosed Goodwill Undisclosed Value

High: Low ‘Intangible Value’ Countries

100%0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Switzerland

India

US

Malaysia

South Korea

China

Tangible Invested Capital

Disclosed Intangible Assets (ex Goodwill)

Disclosed Goodwill

Undisclosed Value

Top Three

Bottom Three

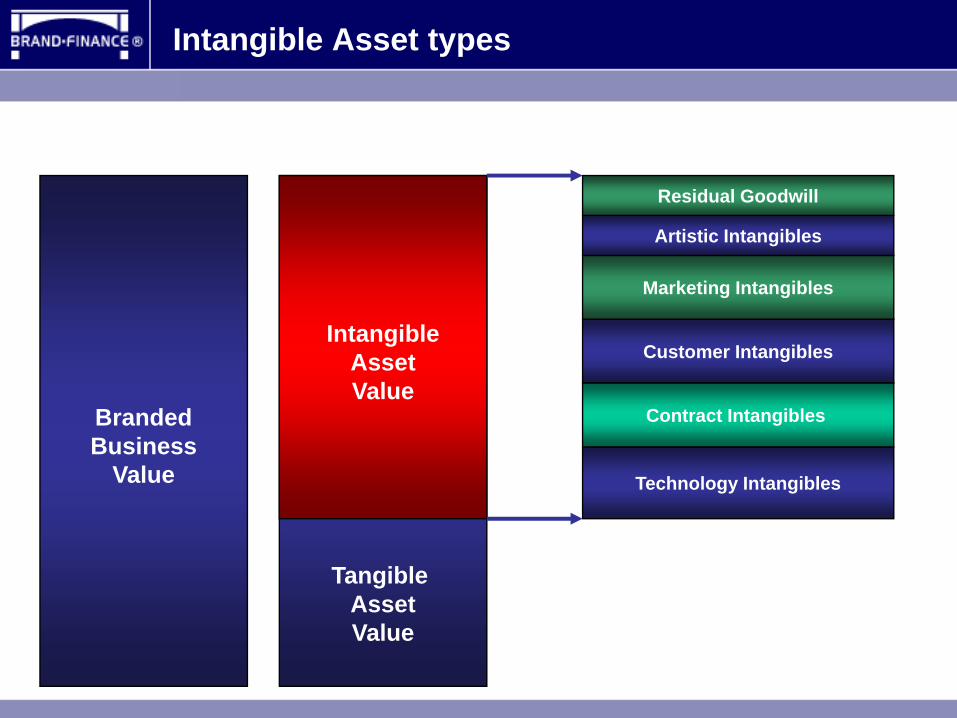

Intangible Asset types

BrandedBusiness

Value

Tangible AssetValue

IntangibleAssetValue

Technology Intangibles

Residual Goodwill

Customer Intangibles

Marketing Intangibles

Contract Intangibles

Artistic Intangibles

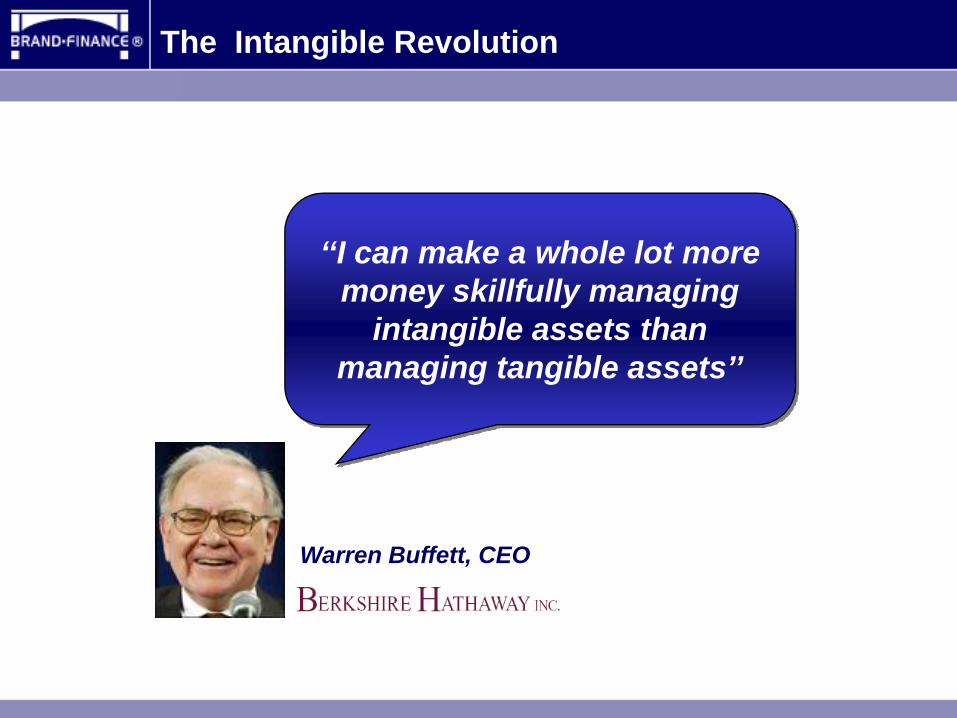

The Intangible Revolution

‘‘I can make a whole lot more money skillfully managing

intangible assets than managing tangible assets’’

Warren Buffett, CEO

P&G acquisition of Gillette

Intangible Assets

Tangible Assets

Technology

Relationships

Brands

Purchase Price Allocation:

Gillette

Purchase price 53.4

$ billion

Total Intangible Assets 29.7

Intangible Assets :

Brands 25.6

Patents and technology 2.7

Customer relationships 1.4

Residual Goodwill 34.9

Tangible Fixed Assets 4.5

Working Capital 0.6

L-t liabilities assumed (16.2)

Total Goodwill 64.5

The Brand Finance Global Top 250

‘Tracking the strongest and most valuable brands in the world’

BF250 – top 10 brands by value

Source: BrandFinance250©

BF250 – top 10 brands by Brand Strength

Source: BrandFinance250©

Brand Rating

Number of Brands

Brands

AAA+ AAA AAA-

12 8 17

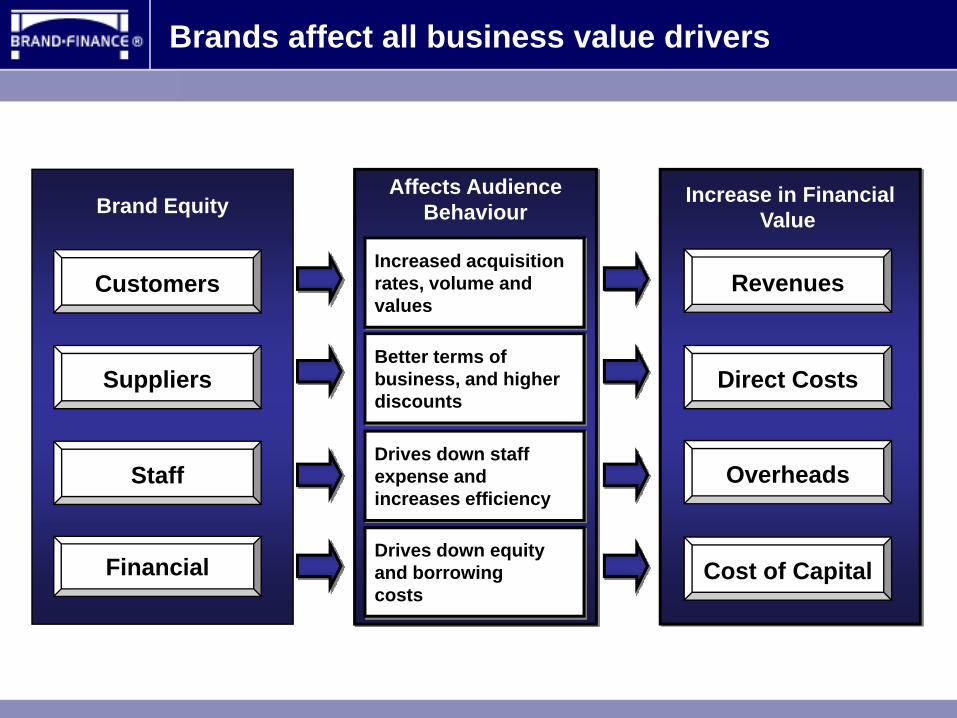

Brand Equity

Financial

Staff

Customers

Brands affect all business value drivers

Suppliers

Affects AudienceBehaviour

Drives down equity and borrowing costs

Drives down staff expense andincreases efficiency

Increased acquisitionrates, volume and values

Better terms of business, and higher discounts

Increase in FinancialValue

Revenues

Direct Costs

Overheads

Cost of Capital

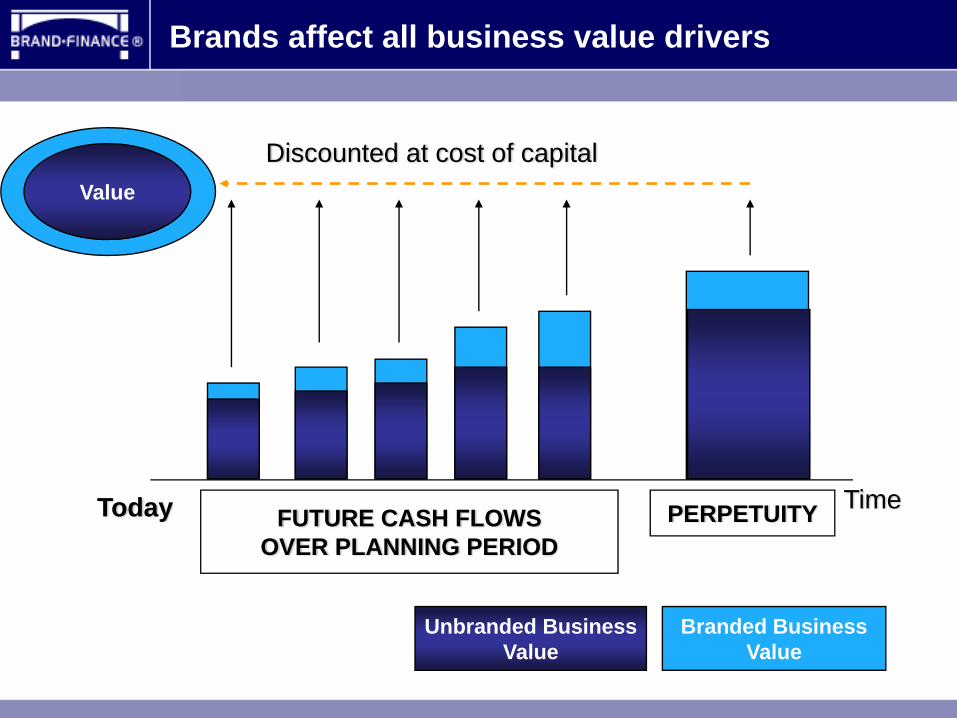

FutureValue

Discounted at cost of capital

FUTURE CASH FLOWSOVER PLANNING PERIOD

PERPETUITY

Value

Today Time

Yr.5

Branded BusinessValue

Unbranded BusinessValue

Brands affect all business value drivers

Case Study

Taking the global brand war seriously

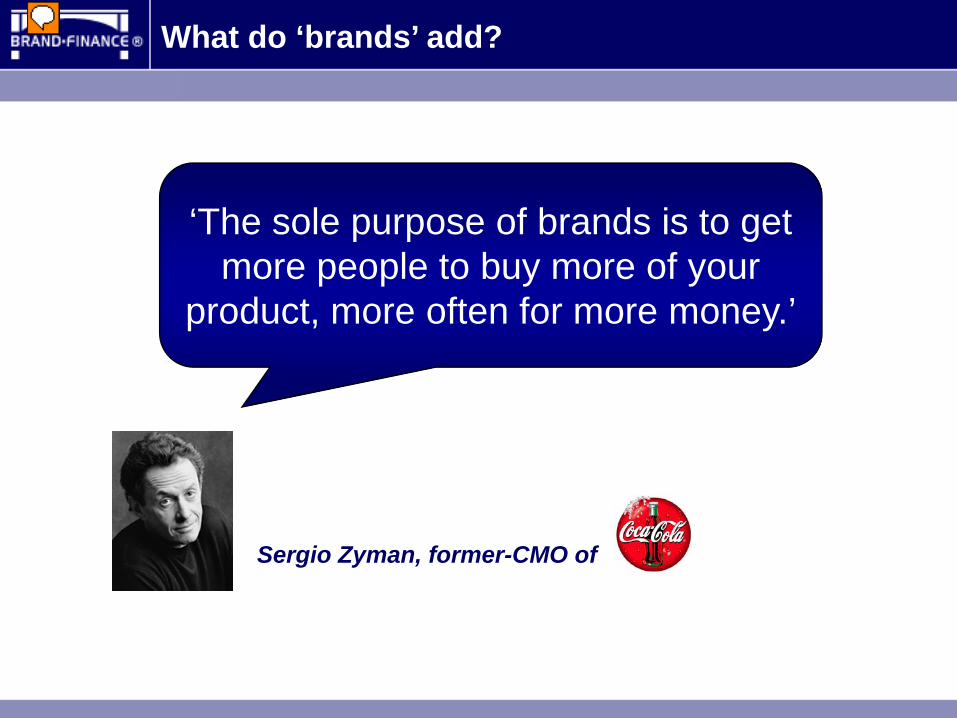

‘The sole purpose of brands is to get more people to buy more of your

product, more often for more money.’

What do ‘brands’ add?

Sergio Zyman, former-CMO of

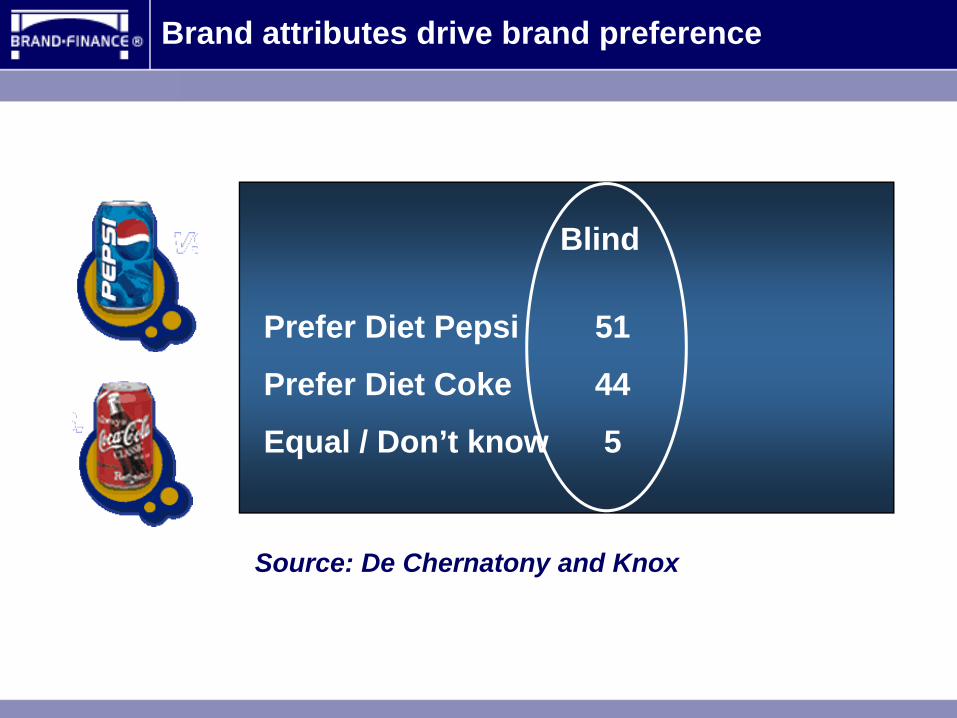

Source: De Chernatony and Knox

Blind

Prefer Diet Pepsi 51

Prefer Diet Coke 44

Equal / Don’t know 5

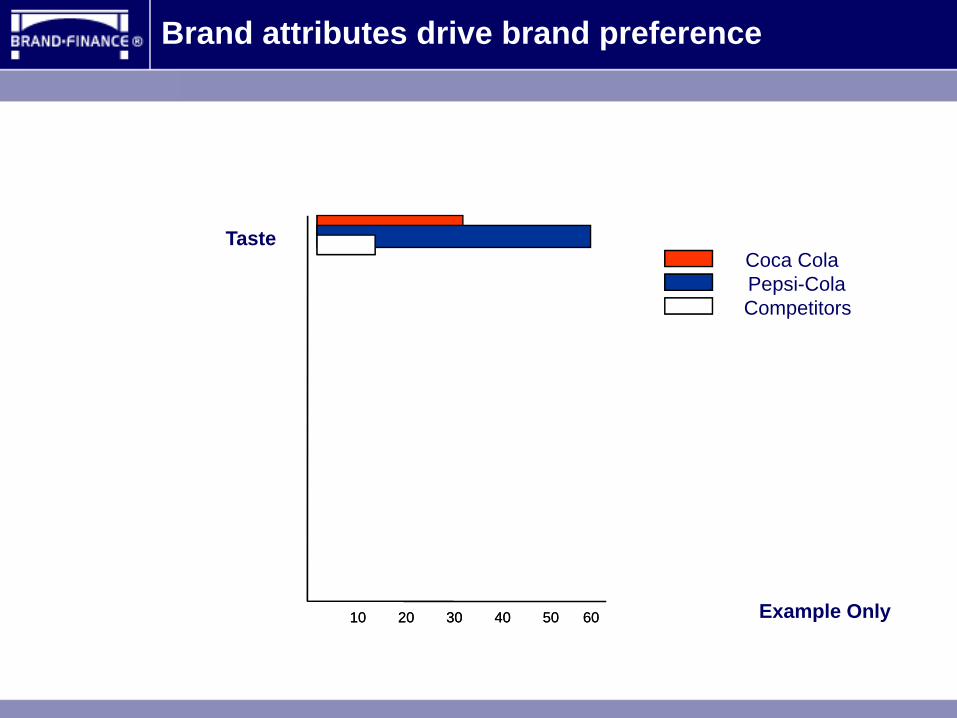

Brand attributes drive brand preference

Coca Cola

10 20 30 40 50 60

Taste

CompetitorsPepsi-Cola

10 20 30 40 50 60 Example Only

Brand attributes drive brand preference

Source: De Chernatony and Knox

Blind

Prefer Diet Pepsi 51

Prefer Diet Coke 44

Equal / Don’t know 5

23

65

12

Named

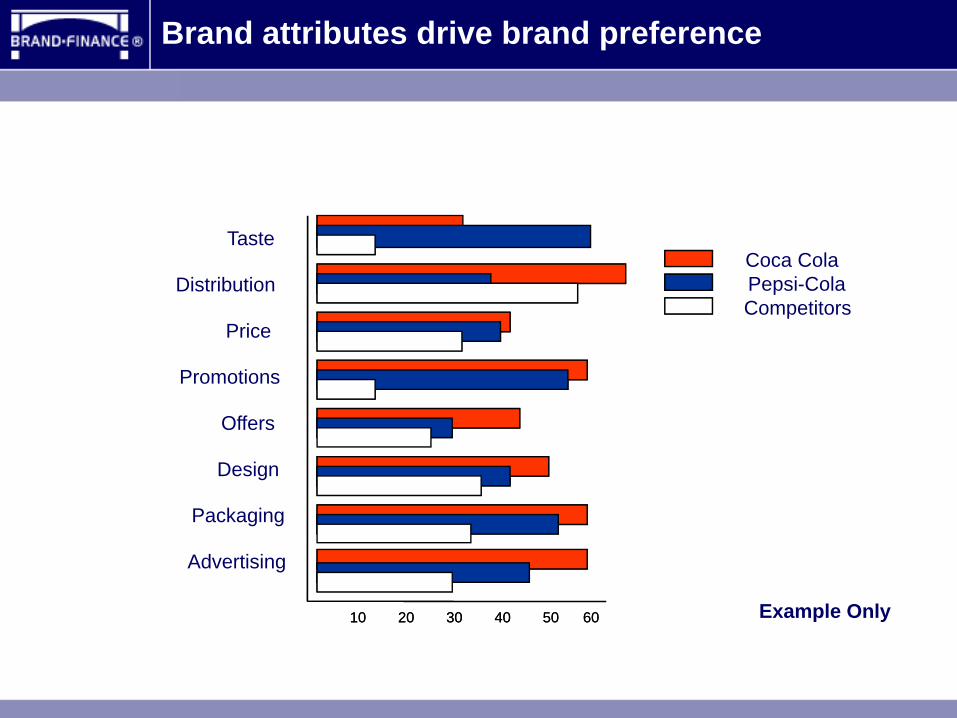

Brand attributes drive brand preference

Coca Cola

10 20 30 40 50 60

Taste

Distribution

Price

Offers

Design

CompetitorsPepsi-Cola

10 20 30 40 50 60

Promotions

Packaging

Advertising

Example Only

Brand attributes drive brand preference

Pepsico – emotional connection with consumers

Pepsico – emotional connection with consumers

$ 2.4 B

$ 1.5 B

$ 5.9 B

$ 5.0 B

$ 3.6 B

$ 3.8 B

$ 2.4 B $ 1.5 B

$ 1.6 B

$ 1.6 B

$ 1.3 B

$ 1.3 B

$ 1.1 B

$ 1.9 B*

Source: Estimate of 2002 Global Sales at Retail

$ 14.8 B

* International only.

$ 1.0 B

Sixteen Billion $ Global Brands (2005)

Pepsico – satisfying consumer tastes

Pepsi International vs Coke International CSD Growth vs PY

Source: KO earnings releases, PI analysis

3.9% 4.1%

6.4%

10.7%

9.7%

2.4%1.7%

2.6% 2.3% 2.40%

2001 2002 2003 2004 2005

2002-2005 International Volume Growth

+9% +12% +11% +20%

Pepsico – delivering outstanding growth

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

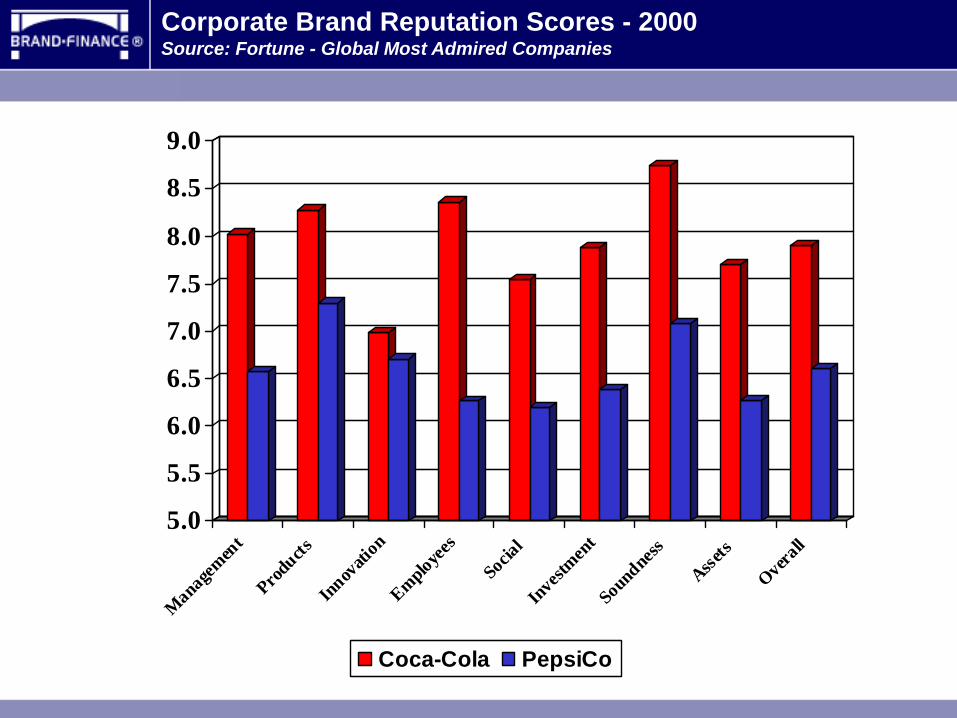

Manag

emen

tProd

uctsInn

ovati

onEmplo

yees

Socia

lInv

estmen

tSo

undne

ss

Assets

Overall

Coca-Cola PepsiCo

Corporate Brand Reputation Scores - 2000Source: Fortune - Global Most Admired Companies

5.0

5.5

6.0

6.5

7.0

7.5

8.0

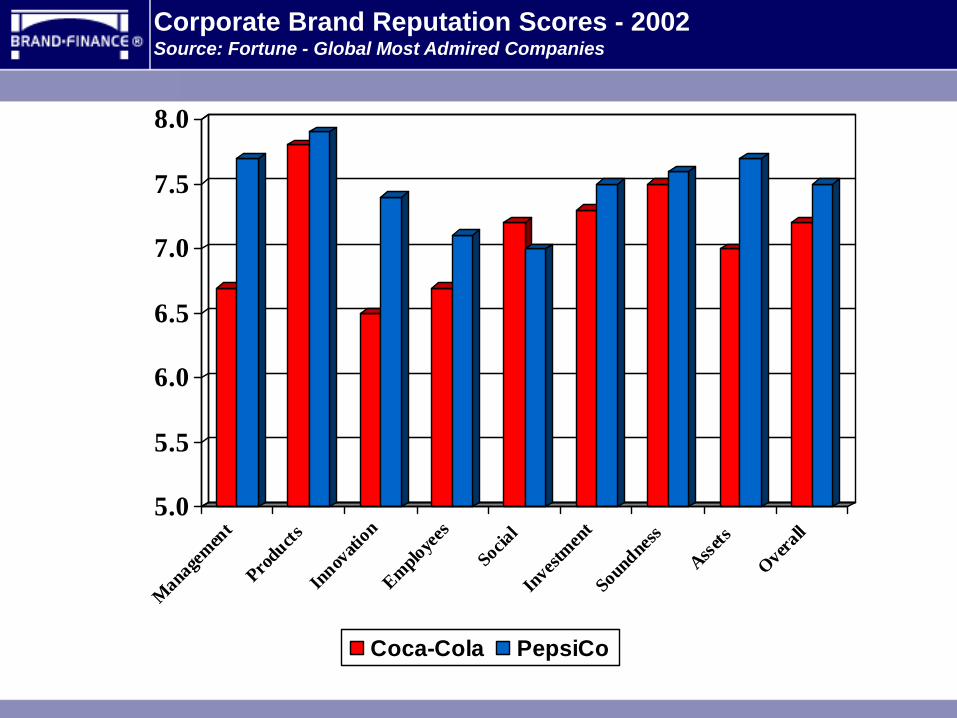

Manag

emen

tProd

uctsInn

ovati

onEmplo

yees

Socia

lIn

vestm

ent

Soun

dness

Assets

Overall

Coca-Cola PepsiCo

Corporate Brand Reputation Scores - 2002Source: Fortune - Global Most Admired Companies

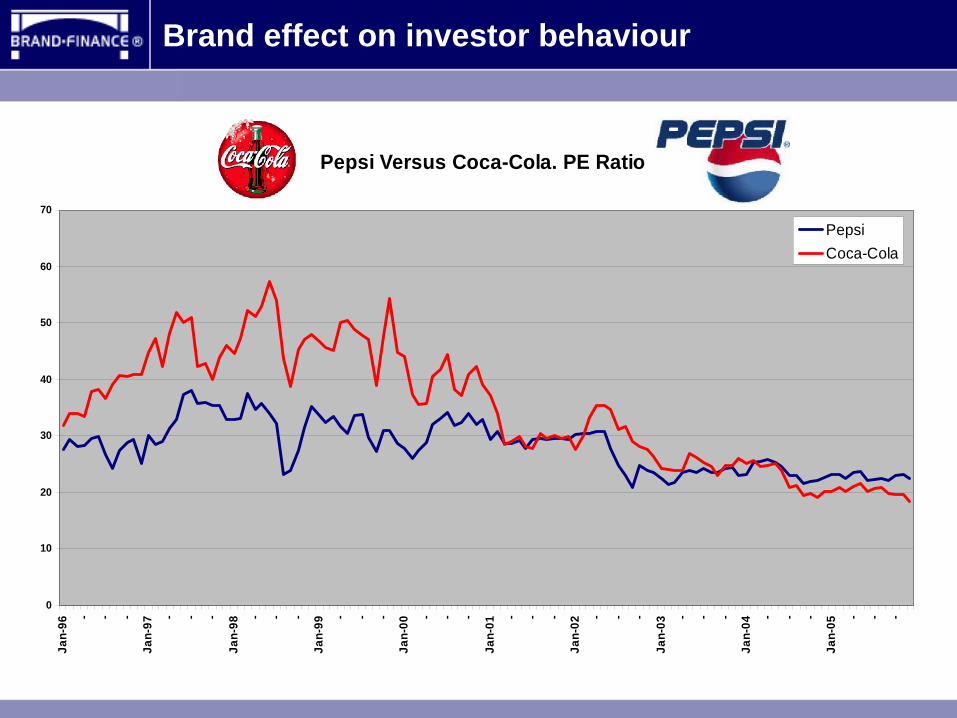

Brand effect on investor behaviour

Pepsi Versus Coca-Cola. PE Ratio

0

10

20

30

40

50

60

70

Jan-

96

- - -

Jan-

97

- - -

Jan-

98

- - -

Jan-

99

- - -

Jan-

00

- - -

Jan-

01

- - -

Jan-

02

- - -

Jan-

03

- - -

Jan-

04

- - -

Jan-

05

- - -

PepsiCoca-Cola

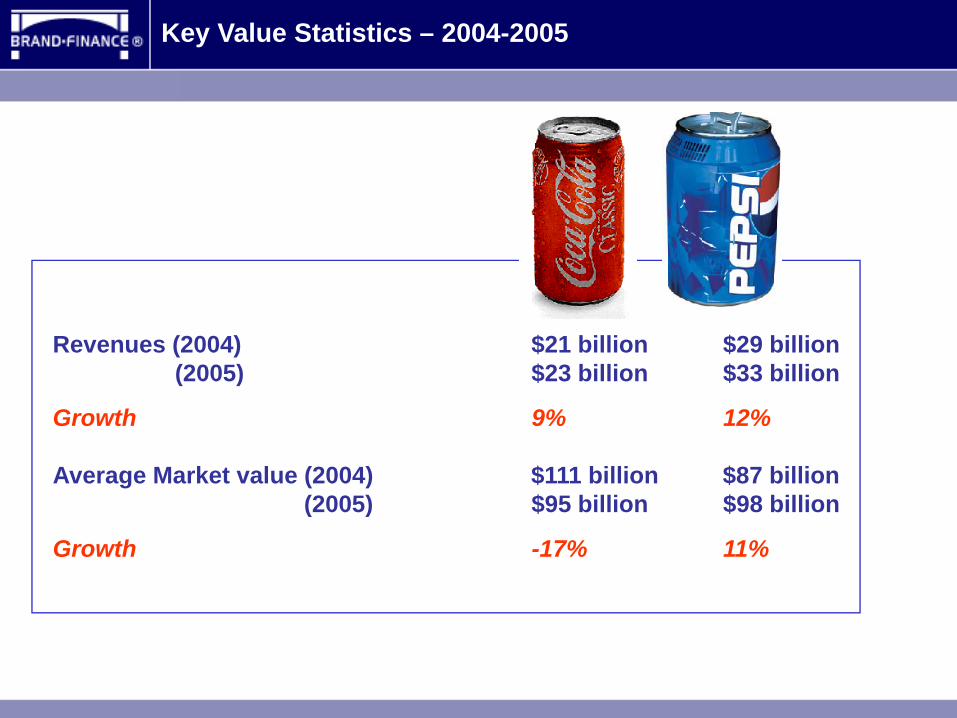

Revenues (2004) $21 billion $29 billion(2005) $23 billion $33 billion

Growth 9% 12%

Average Market value (2004) $111 billion $87 billion(2005) $95 billion $98 billion

Growth -17% 11%111

234

162

Key Value Statistics – 2004-2005

The Brand Finance Sri Lanka Top 50

‘Tracking the strongest and most valuable brands in Sri Lanka’

The Brand Challenge

The Brand

ChallengeCorporate Individual

Governmental

The Governmental Brand Challenge

Tourism

People

Products / Services

Investment

The four dimensions of Nation Branding(Simon Anholt, CEO GMI Index)

Governmental branding campaigns in tourism

• Geographic denomination of origin powerful ‘branding’ local products

• Consumers are willing to pay more "authentic" and of "high quality"

• ‘Protected name’ products attract a price premium of up to 20-30%. For example: Champagne, Parma Ham, Feta cheese, Patna Rice, Darjeeling Tea

• Governments are increasingly standing up for their producers

• Ethiopia versus Starbucks

Governmental branding campaigns in produce

Direct support (Grants and Initiatives)

• USA• EU• China• Singapore• Malaysia

Indirect support (Fiscal and Regulatory)

• Switzerland• Ireland• Singapore• Dubai• Maldives!

Government support for brand owners

Winning the war in a world of free trade

Competing to be thehome of choice

The Brand

ChallengeCorporate Individual

Governmental

Top 10 Sri Lanka brands by value

• Dialog• DCSL• Cargills Food City• Ceylinco Insurance• SLT• Singer• Nestle• Commercial Bank• Lion• CTC

The Corporate Brand Challenge

The Corporate Brand Challenge

Vodafone global brand footprint

The Corporate Brand Challenge

The Corporate Brand Challenge

The Brand

ChallengeCorporate Individual

Governmental

Brand Equity

Financial

Staff

Customers

Brands affect all business value drivers

Suppliers

Affects AudienceBehaviour

Drives down equity and borrowing costs

Drives down staff expense andincreases efficiency

Increased acquisitionrates, volume and values

Better terms of business, and higher discounts

Increase in FinancialValue

Revenues

Direct Costs

Overheads

Cost of Capital

Visual Identity Valuable Proposition

Cost Centre Revenue Source

Shareholder ValueImposition

Shareholder Value Improvement

From Brand = To Brand =

The Individual Brand Challenge

Contact Details:

David HaighCEOBrand Finance plc8 Oak LaneTwickenhamTW1 3PA UK

Tel: +44 208 607 0300Fax: +44 208 607 0301