Summary of CFPB Final Small-Dollar Lending Rule I. II. III...

30

1 A special thanks to Andrew Smith and the Covington team for providing this information. Summary of CFPB Final Small-Dollar Lending Rule I. Major Changes from the Proposed Rule ........................................................................ 1 II. Scope of Coverage and Related Definitions .................................................................... 2 III. Underwriting Requirements ............................................................................................ 6 IV. Payments .......................................................................................................................... 13 V. Information Furnishing, Recordkeeping, Anti-Evasion, and Severability................ 22 I. Major Changes from the Proposed Rule • No ability-to-repay requirement for covered longer-term loans, except for covered longer-term balloon-payment loans. • No credit reporting or registered information system requirements for covered longer- term loans, except for covered longer-term balloon-payment loans. • Coverage triggered by the “cost of credit” using the TILA APR of 36 percent, not the “total cost of credit” or all-in APR/military APR methodology. • Flexibility to assess ability-to-repay using either a debt-to-income ratio test or a residual income test. • Ability to rely on stated income in certain circumstances. • Ability to rely on household income and shared payment of expenses. • Ability to rely on stated rent for housing expenses. • No presumption of inability to repay. • New exemptions for: o Accommodations loans (fewer than 2,500 per year and less than 10 percent of revenue); o Certain no-cost wage advance programs; and o Certain no-cost advances (e.g., no-cost overdrafts).

Transcript of Summary of CFPB Final Small-Dollar Lending Rule I. II. III...

1

A special thanks to Andrew Smith and the Covington team for providing this information.

Summary of CFPB Final Small-Dollar Lending Rule

I. Major Changes from the Proposed Rule ........................................................................ 1

II. Scope of Coverage and Related Definitions .................................................................... 2

III. Underwriting Requirements ............................................................................................ 6

IV. Payments .......................................................................................................................... 13

V. Information Furnishing, Recordkeeping, Anti-Evasion, and Severability ................ 22

I. Major Changes from the Proposed Rule

• No ability-to-repay requirement for covered longer-term loans, except for covered

longer-term balloon-payment loans.

• No credit reporting or registered information system requirements for covered longer-

term loans, except for covered longer-term balloon-payment loans.

• Coverage triggered by the “cost of credit” using the TILA APR of 36 percent, not the

“total cost of credit” or all-in APR/military APR methodology.

• Flexibility to assess ability-to-repay using either a debt-to-income ratio test or a residual

income test.

• Ability to rely on stated income in certain circumstances.

• Ability to rely on household income and shared payment of expenses.

• Ability to rely on stated rent for housing expenses.

• No presumption of inability to repay.

• New exemptions for:

o Accommodations loans (fewer than 2,500 per year and less than 10 percent of

revenue);

o Certain no-cost wage advance programs; and

o Certain no-cost advances (e.g., no-cost overdrafts).

2

II. Scope of Coverage and Related Definitions

• The CFPB’s final small-dollar lending rule applies to “a lender that extends credit by

making covered loans.” (Section 1041.3(a))

• A lender is defined as “a person who regularly extends loans to a consumer primarily for

personal, family, or household purposes.” (Section 1041.2(13))

o The test for determining whether a person is a lender is based on making 25 non-

home secured loans or five home-secured loans in the previous calendar year, as

set forth in Section 1026.2(a)(17)(v) of Regulation Z. (Comment 1041.2(13)-1)

o In addition, any loan to a consumer for personal, family, or household purposes,

not just covered loans, counts toward the numerical threshold for determining

whether a person is a lender. (Comment 1041.2(13)-1)

• A covered loan is closed-end or open-end credit that is extended to a consumer primarily

for personal, family, or household purposes that is not excluded by, or conditionally

exempted from, the rule and that falls within one of the following categories of covered

loans:

o Covered short-term loans.

▪ Closed-end credit that does not provide for multiple advances to

consumers where the consumer is required to repay substantially the entire

amount of the loan within 45 days of consummation; or

▪ For all other loans (open-end credit), the consumer is required to repay

substantially the entire amount of the advance within 45 days of the

advance under the loan. (Section 1041.2(10) and .3(b)(1)).

o Covered longer-term balloon-payment loan.

▪ Closed-end credit that does not provide for multiple advances to

consumers where the consumer is required to repay substantially the entire

balance of the loan in a single payment more than 45 days after

consummation or to repay the loan through at least one payment that is

more than twice as large as any other payment.

▪ For all other loans (open-end credit),

• The consumer is required to repay substantially the entire amount

of an advance in a single payment more than 45 days after the

advance is made or is required to make at least one payment on the

advance more than twice as large as any other payment; or

• A multiple advance loan is structured such that the required

minimum payments may not fully amortize the outstanding

balance by a specified date or time, and the amount of the final

payment could be more than twice the amount of other minimum

payments under the plan. (Section 1041.2(a)(7) and .3(b)(2)).

3

o Covered longer-term loans.

▪ For loans that are not covered short-term loans or covered longer-term

balloon-payment loans, a loan is a covered loan if:

• The cost of credit for the loan exceeds 36 percent per annum:

o For closed-end credit, measured at consummation;

o For open-end credit, measured at consummation, and if not

more than 36 percent, again at the end of each billing cycle

for open-end credit, except that—

▪ Open-end credit meets the 36 percent threshold in

any billing cycle in which a lender imposes a

finance charge, and the principal balance is $0; and

▪ Once open-end credit exceeds the 36 percent

threshold for any billing cycle, it meets the

condition for the duration of the plan; and

• The lender or service provider obtains a leveraged payment

mechanism, as discussed below. (Section 1041.2(a)(8) and

.3(b)(3)).

▪ The cost of credit is the cost of consumer credit expressed as a per annum

rate calculated in accordance with the requirements of Regulation Z

standards for APR calculations. (Section 1041.2(a)(6)). It includes all

finance charges set forth in Section 1026.4 of Regulation Z, but without

regard to whether the credit is consumer credit, or is extended to a

consumer. Calculation of the cost of credit works as follows:

• For closed-end credit, calculate the cost of credit in accordance

with Section 1026.22 of Regulation Z; and

• For open-end credit, calculate the cost of credit in accordance with

the rules for calculating the effective APR for a billing cycle in

Section 1026.14(c) and (d) of Regulation Z. (Section

1041.2(a)(6)).

• A leveraged payment mechanism gives a lender or servicer the right to initiate a transfer

of money, through any means, from a consumer’s account to satisfy an obligation on a

loan.

o A lender or service provider does not obtain a leveraged payment mechanism by

initiating a single immediate transfer at the consumer’s request after the consumer

authorizes the transfer. (Section 1041.3(c)).

• Covered loans include open-end credit, which is defined as an extension of credit to a

consumer that is an open-end credit plan as defined in Regulation Z, 12 CFR

1026.2(a)(20), but without regard to several elements of open-end credit under

Regulation Z, including whether the credit is consumer credit or whether it permits a

finance to be imposed from time to time on an outstanding balance. (Section

1041.2(a)(16)). In addition, the final rule substitutes:

o The defined term “lender” in Section 1041.2(a)(13) for the Regulation Z

definition of “creditor” in 12 CFR 1026.2(a)(17); and

4

o The defined term “consumer” in Section 1041.2(a) (4) for the Regulation Z

definition of “consumer” in 12 CFR 1026.2(a)(11). (Section 1041.2(a)(16)).

• Exclusions. The term covered loan does not apply to the following types of credit:

o Certain purchase money security interest loans. Credit extended for the sole and

express purpose of financing a consumer’s initial purchase of a good when the

credit is secured by the property being purchased, whether or not the security

interest is perfected or recorded. (Section 1041.3(d)(1)).

o Real estate secured credit. Credit that is secured by any real property, or by

personal property used or expected to be used as a dwelling, and the lender

records or otherwise perfects the security interest within the term of the loan.

(Section 1041.3(d)(2)).

o Credit cards. Any credit card account under an open-end (not home-secured)

consumer credit plan as defined in Regulation Z, 12 CFR 1026.2(a)(15)(ii).

(Section 1041.3(d)(3)).

o Student loans. Credit made, insured, or guaranteed pursuant to a program

authorized by subchapter IV of the Higher Education Act of 1965, 20 U.S.C. 1070

through 1099d, or a private education loan as defined in Regulation Z, 12 CFR

1026.46(b)(5). (Section 1041.3(d)(4)).

o Non-recourse pawn loans. Credit in which the lender has sole physical possession

and use of the property securing the credit for the entire term of the loan and for

which the lender’s sole recourse if the consumer does not elect to redeem the

pawned item and repay the loan is the retention of the property securing the

credit. (Section 1041.3(d)(5)).

o Overdraft services and overdraft lines of credit. Overdraft services as defined in

Regulation E, 12 CFR 1005.17(a), and overdraft lines of credit otherwise

excluded from the definition of overdraft services under Regulation E, 12 CFR

1005.17(a)(1). (Section 1041.3(d)(6)).

o Wage advance programs. Advances of wages that constitute credit if made by an

employer, as defined in the Fair Labor Standards Act, 29 U.S.C. 203(d), or by the

employer’s business partner, to the employer’s employees, provided that the

advance is made only against the accrued cash value of any wages the employee

has earned up to the date of the advance, and before any advance, the entity

advancing the funds warrants to the consumer as part of the contract between the

parties on behalf of itself and any business partners, that it or they, as applicable:

▪ Will not require the consumer to pay any charges or fees in connection

with the advance, other than a charge for participating in the wage

advance program;

▪ Has no legal or contractual claim or remedy against the consumer based

on the consumer’s failure to repay in the event the amount advanced is not

repaid in full; and

▪ With respect to the amount advanced to the consumer, will not engage in

any debt collection activities if the advance is not deducted directly from

wages or otherwise repaid on the scheduled date, place the amount

advanced as a debt with a debt collector or sell it to a debt buyer, or report

5

to a consumer reporting agency concerning the amount advanced.

(Section 1041.3(d)(7)).

o No-cost advances. Advances of funds that constitute credit if the consumer is not

required to pay any charge or fee to be eligible to receive or in return for receiving

the advance, provided that before any amount is advanced, the entity advancing

the funds warrants to the consumer as part of the contract between the parties that:

▪ It has no legal or contractual claim or remedy against the consumer based

on the consumer’s failure to repay in the event the amount advanced is not

repaid in full; and

▪ With respect to the amount advanced to the consumer, such entity will not

engage in any debt collection activities if the advance is not repaid on the

scheduled date, place the amount advanced as a debt with a debt collector

or sell it to a debt buyer, or report to a consumer reporting agency

concerning the amount advanced. (Section 1041.3(d)(8)).

• Conditional exemption for alternative loans.

o Alternative loans are conditionally exempt from the final rule. (Section

1041.3(e)).

o An alternative loan must satisfy the following five loan term conditions:

▪ The loan is not structured as open-end credit;

▪ The loan has a term of not less than one month and not more than six

months;

▪ The loan has a principal loan amount of not less than $200 and not more

than $1,000;

▪ The loan is repayable in two or more payments, all of which are

substantially equal in amount and fall due in substantially equal intervals,

and amortizes completely during the term of the loan; and

▪ The lender does not impose any charges other than the rate and application

fees permissible for Federal credit unions under NCUA regulations at 12

CFR 701.21(c)(7)(iii). (Section 1041.3(e)(1)).

o In addition, a lender must satisfy a borrower history condition and an income

documentation condition to qualify for the conditional exemption:

▪ Borrower history condition. Prior to making an alternative loan, the

lender must determine from its records that the loan would not result in the

consumer being indebted on more than three outstanding loans made

under this section from the lender within a period of 180 days. The lender

must also make no more than one alternative loan at a time to a consumer.

(Section 1041.3(e)(2)).

▪ Income documentation condition. The lender must maintain and comply

with policies and procedures for documenting proof of recurring income.

(Section 1041.3(e)(3)).

o Loans made by Federal credit unions in compliance with the conditions set forth

by the National Credit Union Administration at 12 CFR 701.21(c)(7)(iii) for a

Payday Alternative Loan are deemed to be in compliance with the requirements

and conditions for alternative loans. (Section 1041.3(e)(4)).

6

• Conditional exemption for accommodation loans.

o Accommodation loans are conditionally exempt from the final rule. (Section

1041.3(f)).

o An accommodation loan is a covered loan if at the time the loan is consummated:

▪ The lender and its affiliates collectively have made 2,500 or fewer covered

loans during the current calendar year, and made 2,500 or fewer such

covered loans in the preceding calendar year; and

▪ During the most recent completed tax year in which the lender was in

operation, the lender and any affiliates that were in operation and use the

same tax year derived no more than 10 percent of their receipts (total

income + cost of goods sold) from covered loans during the current tax

year. If the lender was not in operation in a prior tax year, the lender

reasonably anticipates that the lender and any of its affiliates that use the

same tax year will derive no more than 10 percent of their receipts from

covered loans during the current tax year.

▪ Provided, however, that covered longer-term loans for which all transfers

meet the conditions in Section 1041.8(a)(1)(ii) (conditional exclusion for

certain transfers by account-holding institutions), and receipts from such

loans, are not included for the purpose of determining whether the

conditions for accommodation loans, described above, have been satisfied.

(Section 1041.3(f)).

o The terms “receipts” (total income + cost of goods sold) and “tax year” are

defined with reference to Internal Revenue Service rules. (Sections 1041.3(g) and

(h)).

III. Underwriting Requirements

It is an abusive and unfair practice for a lender to make covered short-term loans or covered

longer-term balloon-payment loans without reasonably determining that the consumer will have

the ability to repay the loans according to their terms. (Section 1041.4)

Ability-to-Repay Requirement (Section 1041.5)

• Definitions (Section 1041.5(a)).

o Basic living expenses = expenses for goods and services necessary to maintain

health, welfare and ability to produce income of the consumer and members of his

or her household who are financially dependent on the consumer. (Section

1041.5(a)(1)).

o Debt-to-income ratio – the ratio, expressed as a percentage, of

▪ The sum of the amounts that the lender projects will be payable by the

consumer for major financial obligations during the relevant monthly

period and the payments under the covered short-term loan or covered

longer-term balloon-payment loan during the relevant monthly period, to

▪ The net income that the lender projects the consumer will receive during

the relevant monthly period. (Section 1041.5(a)(2)).

7

o Major financial obligations = housing expense + required payments under debt

obligations + child support obligations + alimony obligations. (Section

1041.5(a)(3)).

o National consumer report – a consumer report from a nationwide consumer

reporting agency. (Section 1041.5(a)(4)).

o Net income – total amount that a consumer receives after the payer deducts

amounts for taxes withheld, voluntary contributions (such as consumer

contributions to 401(k) and similar plans), and “other obligations” (such as

premiums for employer-sponsored health insurance plans). Net income may

include income to which a consumer has a reasonable expectation of access, as

well as irregular or seasonal income, but does not include one-time payments such

as tax refunds or legal settlements, unless verified as to amount and timing.

(Section 1041.5(a)(5)).

o Payment under the covered short-term loan or covered longer-term balloon-

payment loan –

▪ includes all principal, interest, charges and fees; and

▪ for a line of credit is calculated assuming that the consumer draws down

the full amount and makes only the minimum required payments. (Section

1041.5(a)(6)).

o Relevant monthly period – the calendar month in which the highest sum of

payments is due under the covered short-term or covered longer-term balloon-

payment loan. (Section 1041.5(a)(7)).

o Residual income – projected net income during the relevant monthly period, less

amounts payable for major financial obligations during the relevant monthly

period and payment under the covered short-term loan or covered longer-term

balloon payment loan during the relevant monthly period. (Section 1041.5(a)(8)).

• Reasonable determination required (Section 1041.5(b)).

o A lender must not make a covered short-term loan or covered longer-term

balloon-payment loan or increase the credit available such loans, unless the lender

first makes a reasonable determination that the consumer will have the ability to

repay the loan according to its terms. (Section 1041.5(b)(1)).

▪ Special rule for lines of credit: A lender must not permit a consumer to

obtain an advance under a line of credit more than 90 days after the

original ability to repay determination, unless the lender makes a new

ability to repay determination.

o A lender’s determination of a consumer’s ability to repay a covered short-term

loan or covered longer-term balloon-payment loan is reasonable only if the lender

reasonably concludes that either:

▪ Debt-to-income ratio test. The consumer’s debt-to-income ratio calculated

by the lender for the relevant monthly period and the lender’s estimates of

the consumer’s basic living expenses for the relevant monthly period

indicate that the consumer will be able to make payments for major

financial obligations, make all payments under the loan, and meet basic

living expenses:

8

• For covered short-term loans, during the shorter of the term of the

loan or the period ending 45 days after consummation of the loan,

and for 30 days after having made the highest payment under the

loan; or

• For covered longer-term balloon-payment loans, during the

relevant monthly period, and for 30 days after having made the

highest payment under the loan.

▪ Residual income test. The consumer’s residual income calculated by the

lender for the relevant monthly period and estimates of the consumer’s

basic living expenses for the relevant monthly period enables the

consumer to make payments for major financial obligations, make all

payments under the loan, and meet basic living expenses:

• For covered short-term loans, during the shorter of the term of the

loan or the period ending 45 days after consummation of the loan,

and for 30 days after having made the highest payment under the

loan; or

• For covered longer-term balloon-payment loans, during the

relevant monthly period, and for 30 days after having made the

highest payment under the loan. (Section 1041.5(b)(2)).

• Projecting consumer net income and payments for major financial obligations required

(Section 1041.5(c)).

o A lender must make a “reasonable projection of the amount and timing of a

consumer’s net income and payments for major financial obligations during the

relevant monthly period” using:

▪ The consumer’s written statement, including the major financial

obligations listed on the statement;

▪ Verification evidence to the extent required; and

▪ Information about rental housing expense. (Section 1041.5(c)(1)).

o A lender may reasonably consider other reliable evidence obtained from or about

the consumer, including any consumer explanations. (Section 1041.5(c)(1).

o A lender must obtain a written statement from the consumer of:

▪ The amount of net income, which may include the income of another

person to which the consumer has a reasonable expectation of access; and

▪ The amount of payments required for the consumer’s major financial

obligations. (Section 1041.5(c)(2)(i).

o A lender must obtain verification evidence for the consumer’s net income and

payments for major financial obligations (other than rental housing expense) as

follows:

▪ For the consumer’s net income:

• The lender must obtain a reliable record (or records) of an income

payment (or payments) directly to the consumer covering sufficient

history to support the lender’s projection if a reliable record (or

records) is reasonably available.

o A reliable record includes a facially genuine original,

photocopy, or image of a document, or electronic or paper

9

compilation of data included in such a document, stating

the amount and date of the income paid to the consumer, as

well as or electronic or paper record of transactions

showing the amount and date of receipt of income.

o A sufficient history typically is one biweekly or monthly

pay cycle for a covered short-term loan and two biweekly

or two monthly pay cycles for a covered longer-term

balloon-payment loan, depending on how often the

consumer is paid.

o Income records are reasonably available if the consumer

has access to a pay stub or can provide a bank account

deposit history of direct deposits.

• If a lender determines that a reliable record (or records) of some or

all of the consumer’s net income is not reasonably available, the

lender may reasonably rely on the stated income in the consumer’s

written statement for that portion of the consumer’s net income.

o Must be consistent with lender’s written policies and

procedures.

o Must be no indication that stated income is implausibly

high.

o Must not engage in pattern of systematically overestimating

consumers’ income.

• If the lender elects to include in the consumer’s net income for the

relevant monthly period any income of another person to which the

consumer has a reasonable expectation of access, the lender must

obtain verification evidence demonstrating that the consumer has

reasonable expectation of access to that income. (Section

1041.5(c)(2)(ii)).

▪ For the consumer’s required payments under debt obligations:

• The lender must obtain a credit report from a nationwide consumer

reporting agency, the records of the lender and its affiliates, and a

consumer report from a CFPB-registered information system that

has been registered for 180 days or more.

• If such reports and records do not include a debt obligation listed

in the consumer’s written statement, the lender may reasonably

rely on the consumer’s written statement in determining the

amount of the required payment. (Section 1041.5(c)(2)(ii)).

▪ For child support and alimony obligations:

• A lender must obtain a credit report from a nationwide consumer

reporting agency.

• If the report does not include a child support or alimony obligation

listed in the consumer’s written statement, the lender may

reasonably rely on the written statement in determining the amount

of the required payment. (Section 1041.5(c)(2)(ii)).

▪ Exception to verification of obligations: A lender is not required to obtain

a credit report from a nationwide consumer reporting agency to verify the

10

consumer’s debt, alimony, and child support obligation if during the

preceding 90 days:

• The lender or an affiliate obtained a national consumer report for

the consumer, retained the report under Section 1041.12(b)(1)(ii),

and checked the report again in connection with the new loan; and

• The consumer did not complete a loan sequence of three loans

covered by Section 1041.5 and trigger the prohibition on and

cooling-off period for making additional covered short-term or

longer-term balloon-payment loans since the previous report was

obtained.

▪ For rental housing expenses (i.e., housing expenses other than a payment

for a debt obligation that appears on a credit report), the lender may

reasonably rely on the stated housing expense in the consumer’s written

statement. (Section 1041.5(c)(2)(iii)).

• Additional limitations on lending imposed (Section 1041.5(d)).

o Borrowing history review. Prior to making a covered short-term or longer-term

balloon-payment loan, a lender must review the consumer’s borrowing history

from the records of the lender and its affiliates, and review credit report from one

of the CFPB-registered information system, if available. (Section 1041.5(d)(1).

o Sequence of three loans plus cooling-off period. A lender must not make a

covered short-term loan or covered longer-term balloon-payment loan during the

period in which the consumer already has such a covered loan outstanding and for

30 days thereafter if the new covered short-term loan or covered longer-term

balloon-payment loan would be the fourth loan in a sequence of covered short-

term loans, covered longer-term balloon-payment loans, or a combination of such

loans. (Section 1041.5(d)(2)).

o Single loan plus cooling-off period. A lender must not make a covered short-term

loan or covered longer-term balloon-payment loan during the period in which the

consumer has a covered short-term loan outstanding under Section 1041.6 (the

conditional exemption for certain covered short-term loans) and for 30 days

thereafter. (Section 1041.5(d)(3)).

• Prohibition against evasion (Section 1041.5(e)).

o A lender must not take any action with the intent of evading the requirements of

the ability-to-repay section.

Conditional Exemption for Certain Covered Short-Term Loans in a Loan Sequence with a

Principal-Payoff Option (Section 1041.6)

• The ability to repay requirements do not apply to covered short-term loans in a three-loan

sequence that provide for a principal-payoff option and meet certain loan term

11

requirements, borrowing history requirements, cooling-off requirement, and disclosure

requirements. (Section 1041.6(a)).

• Loan term requirements. A covered short-term loan must satisfy the following loan term

requirements to be eligible for the conditional exemption:

o The first loan in a three-loan sequence is for a principal amount of no more than

$500, with the second loan in the sequence being for principal amount of no more

than two thirds of the first loan, and the third loan in the sequence being for a

principal amount of no more than one third of the first loan;

o Fully amortizing, and the payment schedule provides for the lender allocating a

consumer’s payments to the outstanding principal and interest and fees as they

accrue only by applying a fixed periodic rate of interest to the outstanding balance

of the unpaid loan principal during every scheduled repayment period for the term

of the loan;

o No vehicle security;

▪ The term “vehicle security” is an interest a lender or service provider

obtains in a consumer’s motor vehicle as a condition of credit, regardless

of how the transaction is characterized under State law, and includes:

• Any security interest in the motor vehicle, motor vehicle title, or

motor vehicle registration whether or not the security interest is

perfected or recorded; or

• A pawn transaction in which the consumer’s motor vehicle is the

pledged good and the consumer retains use of the motor vehicle

during the period of the pawn agreement. (Section 1041.2(a)(19)).

o Not structured as open-end credit. (Section 1041.6(b)).

• Borrowing history requirements. Prior to making a covered short-term loan, the lender

must review the consumer’s borrowing history in the records of the lender and its

affiliates, as well as obtain credit report from a CFPB-registered information system to

ensure that

o The consumer has not had in the past 30 days an outstanding covered short-term

loan or covered longer-term balloon-payment loan from any lender;

o The loan would not result in the consumer having a loan sequence of more than

three covered short-term loans made by any lender; and

o The loan would not result in the consumer having more than six covered short-

term loans outstanding, or more than an aggregate of 90 days of outstanding

indebtedness on covered short-term loans, during any consecutive twelve-month

period. (Section 1041.6(c)).

• Cooling-off requirement. If a lender makes a covered short-term loan under this

conditional exemption to a consumer, the lender or its affiliate must not subsequently

make a covered loan, except for a covered short-term loan that is part of the three-loan

sequence, or a non-covered loan to the consumer while the covered short-term loan made

under this section is outstanding and for 30 days thereafter. (Section 1041.6(d)).

12

• Disclosure requirements. Before the loan is consummated, the lender must provide clear

and conspicuous disclosure of the amounts of the first, second and third loan amounts; a

notice of the required cooling-off period; and a warning that the consumer should be able

to repay the total amount of principal and finance charges on the contractual due date.

(Section 1041.6(e)).

o These disclosures may be in writing or electronically (but not orally or by a

recorded message), must be segregated from all other information except

information necessary for product identification, branding, and navigation, must

be made in a retainable, machine readable format, and must be substantially

similar to the CFPB’s model form:

o Before providing a third loan in a sequence, the lender must make a disclosure

substantially similar to the CFPB’s model form:

13

IV. Payments

• It is an unfair and abusive practice for a lender to attempt to withdraw payment from a

consumer’s account in connection with a covered loan after the lender’s second

consecutive attempt to withdraw payment from the account has failed due to a lack of

sufficient funds, unless the lender obtains the consumer’s new and specific authorization

to make further withdrawals from the account. (Section 1041.7).

o Prohibited Payment Transfer Attempts (Section 1041.8).

o A payment transfer is defined as any lender-initiated debit or withdrawal of funds

from a consumer’s account for the purpose of collecting any amount due or

purported to be due in connection with a covered loan, regardless of the means

through which the lender initiates the debit or withdrawal. (Section 1041.8(a)(1)).

▪ Payment transfers include, without limitation, a debit or withdrawal of

funds initiated through any of the following means:

• Electronic fund transfer, including a preauthorized electronic fund

transfer as defined in Regulation E, 12 CFR 1005.2(k);

• Signature check, regardless of whether the transaction is processed

through the check network or another network, such as the

automated clearing house (ACH) network;

• Remotely created check as defined in Regulation CC, 12 CFR

229.2(fff);

• Remotely created payment order as defined in 16 CFR 310.2(cc);

or

• An account-holding institution’s transfer of funds from a

consumer’s account that is held at the same institution. (Section

1041.8(a)(1)(i)).

▪ Conditional exclusion for certain transfers by account-holding institutions.

When the lender is also the account-holding institution, the institution’s

transfer of funds from a consumer’s account held at the same institution is

14

not a payment transfer if the lender, pursuant to the terms of the loan

agreement or account agreement, does not:

• Charge the consumer any fee, other than a late fee under the loan

agreement, in the event that the lender initiates a transfer of funds

from the consumer’s account in connection with the covered loan

for an amount that the account lacks sufficient funds to cover; or

• Close the consumer’s account in response to a negative balance

that results from a transfer of funds initiated in connection with the

covered loan. (Section 1041.8(a)(1)(ii)).

o General prohibition. A lender must not initiate a payment transfer from a

consumer’s account in connection with a covered loan after the lender has

attempted to initiate two consecutive failed payment transfers from the

consumer’s account in connection with any covered loan the consumer has with

the lender.

▪ A payment transfer is deemed to have failed when it results in a return

indicating that the consumer’s account lacks sufficient funds or, for a

lender that is the consumer’s account-holding institution, the transfer is for

an amount that the account lacks sufficient funds to cover. (Section

1041.8(b)(1)).

▪ A payment transfer the fails for another reason, such as an administrative

return, is not a “failed payment transfer” for the purposes of these payment

restrictions. (Comment 1041.8(b)(1)-3.)

o Consecutive failed payment transfers are described in terms of a:

▪ First failed payment transfer occurs when the lender has initiated no other

payment transfer for the covered loan or any other covered loan the

consumer has with the lender, the immediately preceding payment transfer

was successful (regardless of whether a previous payment transfer failed),

or the transfer is the first to fail after the consumer’s authorization for

additional payment transfers; and

▪ Second consecutive failed payment transfer occurs if the immediately

preceding payment transfer was a first failed payment transfer, including

transfers initiated at the same time or on the same day as the first failed

payment transfer and transfers initiated through a different channel than

the first failed payment transfer. (Section 1041.8(b)(2)).

o Exception for additional payment transfers authorized by the consumer (Section

1041.8(c)). A lender may initiate additional payment transfers from a consumer’s

account after two consecutive failed payment transfers if:

▪ The additional payment transfers are authorized by the consumer in

accordance with the requirements and conditions in Section 1041.8(c)(2)

and (3); or

15

▪ The lender executes a single immediate payment transfer at the

consumer’s request in accordance with Section 1041.8(d). (Section

1041.8(c)(1)).

o General authorization requirements and conditions (Section 1041.8(c)(2)). The

consumer must authorize the specific date, amount, and payment channel of each

additional payment transfer, except if:

▪ The additional payment transfer authorized by the consumer is returned

for nonsufficient funds, in which case the lender may re-initiate the

payment transfer, such as by re-presenting it once through the ACH

system, on or after the date authorized by the consumer, provided that the

returned payment transfer has not triggered the prohibition on consecutive

failed payment transfers.

▪ The lender initiates an additional payment transfer solely to collect a late

fee or returned item fee if the consumer has authorized the lender to

initiate such payment transfers in advance of the withdrawal attempt. The

consumer authorizes such payment transfers only if the consumer’s

authorization for additional payment transfers includes a clear and readily

understandable statement that payment transfers may be initiated solely to

collect a late fee or returned item fee and specifies the highest amount for

such fees that may be charged and the payment channel to be used.

o Requirements and conditions for obtaining authorization of additional transfers

(Section 1041.8(c)(3)). The lender may request that the consumer authorize

additional payment transfers by:

▪ Providing the consumer with the consumer rights notice required by

Section 1041.9(c) and requesting authorization no earlier than the date the

lender provides the notice to the consumer; and

▪ Including in the request the payment transfer term and, if applicable, the

statements regarding the collection of a late fee or returned item fee in

Section 1041.8(c)(2); and

▪ Providing the terms and statements to the consumer

• In writing, or in retainable form by email if the consumer consents

or agrees to email delivery; or

• By oral telephone communication if the consumer affirmatively

contacts the lender in response to the consumer rights notice and

agrees to receive the terms and statement orally as part of the same

communication; and

▪ After the consumer’s receipt of the consumer right notice, obtaining a

signed authorization from the consumer, in writing or electronically in

accordance with the signature requirements of the E-Sign Act (for

example, consumer enters a code on a telephone keypad) and in a

retainable format (not satisfied by a telephone recording) that includes the

specific date, amount, and payment channel of each additional payment

transfer the consumer is authorizing and any special authorization required

for collection of a late fee or returned item fee.

16

• The lender must record and retain any authorization obtained by

oral telephone communication.

• When authorization is granted in a recorded telephone

conversation or is otherwise not immediately retainable by the

consumer at the time of signature, the lender must provide a

memorialization in retainable form to the consumer no later than

the date on which the first payment transfer authorized by the

consumer is initiated.

▪ Expiration. The authorization expires if the lender subsequently obtains a

new authorization or if two consecutive payment transfers initiated

pursuant to the authorization fail. (Section 1041.8(c)(4)).

o Exception for single immediate payment transfer at the consumer’s request

(Section 1041.8(d)). After a lender’s second consecutive payment transfer has

failed, the lender may initiate a payment transfer from the consumer’s account

without obtaining authorization for additional payment transfers if:

▪ The payment is a single immediate payment transfer at the consumer’s

request; and

▪ The consumer authorizes the one-time electronic fund transfer or provides the

underlying signature check to the lender no earlier than the date the lender

provides the consumer with the consumer rights notice or on the date the

consumer affirmatively contacts the lender to discuss repayment options,

whichever is earlier. (Section 1041.8(d)).

o For purposes of this exception, a single immediate payment transfer at the

consumer’s request is:

▪ A payment transfer initiated by a one-time electronic fund transfer within

one business day after the lender obtains the consumer’s authorization for

the one-time electronic fund transfer; or

▪ A payment transfer initiated by means of processing the consumer’s

signature check through the check system or through the ACH system

within one business day after the consumer provides the check to the

lender. (Section 1041.8(a)(2)).

o Prohibition against evasion (Section 1041.8(e)). A lender must not take any

action with the intent of evading the requirements of the section governing

prohibited payment transfer attempts.

• Disclosure of Payment Transfer Attempts (Section 1041.9). The final rule requires a

number of consumer disclosures that must be:

o Clear and conspicuous;

o Provided in writing or electronically, if the consumer affirmatively consents in

writing or electronically to the particular electronic delivery method;

17

▪ Valid consumer consent to electronic delivery requires a lender to give the

consumer the option to select email as the method of electronic delivery,

separate and apart from any other electronic delivery methods, such as

mobile application or text message;

▪ A lender may not provide disclosures via a method of electronic delivery

if the consumer revokes consent to receive disclosures through that

delivery method or notifies the lender that the consumer is unable to

receive disclosures through that delivery method at the address or number

used;

o Provided in a retainable form (except for certain short-form disclosures provided

by text or mobile app);

o Be segregated from all other materials or notices, other than information

necessary for product identification, branding, and navigation;

o Contain machine readable text accessible via both web browsers and screen

readers if the disclosure is provided electronically;

o Be substantially similar to the CFPB’s model forms; and

o May be in a language other than English, provided they are available in English

upon request. (Section 1041.9(a)).

o Payment notice (Section 1041.9(b)). Prior to initiating a payment transfer from a

consumer’s account, a lender must provide to the consumer a payment notice:

▪ For a first payment withdrawal, no earlier than when the lender obtains

payment authorization and no later than three business days prior to

initiating the transfer (if the notice is provided electronically or in person)

or six business days prior to initiating the transfer (if the notice is provided

by mail).

▪ For an unusual withdrawal, no earlier than seven business day and no later

than three business day prior to initiating the transfer (if the notice is

provided electronically or in person), and no earlier than 10 business days

and no later than six business day prior to initiating the transfer (if the

notice is provided by mail). If the unusual withdrawal notice is for open-

end credit, the lender may provide the notice with the periodic statement

in accordance with the timing requirements of Regulation Z, 12 C.F.R.

1026.7(b).

▪ Exceptions. A payment notice is not required when the lender initiates:

• The initial payment transfer from a consumer’s account after

obtaining the consumer’s authorization for additional payment

transfers under Section 1041.8(c); or

• A single immediate payment transfer at the consumer’s request

under Section 1041.8(a)(2).

o Contents of payment notice (Section 1041.9(b)). Each payment notice must

contain:

▪ An identifying statement, such as “Upcoming Withdrawal Notice” or, if

the amount, timing, or channel will vary from the regularly scheduled

18

payments, “Alert: Unusual Withdrawal”, and the name of the lender

providing the notice;

▪ Transfer terms, including: the transfer date; amount; identification of the

consumer account; loan identification information; payment channel;

check number if the transfer will be by check, remotely created check, or

remotely created payment order;

▪ Payment breakdown, in tabular form, including:

• a heading, “Payment Breakdown”;

• amount of payment applied to principal;

• amount of payment applied to accrued interest, fees, other charges;

• the “Total Payment Amount” using that phrase; and

• an explanation of any interest-only or negatively amortizing

payment;

▪ Lender name, the name under which the transfer will be initiated, if

different, and two different forms of lender contact information; and

▪ Additional content for unusual withdrawal attempts, such as varying

amounts (but for open-end credit, required only if amount deviates from

scheduled minimum payment disclosed on periodic statement), transfer

date other than a regularly scheduled payment due date, different payment

channel, or purpose of re-initiation of a returned transfer.

▪ The notices must be substantially similar to the CFPB’s model forms:

19

▪ A short notice is permitted when the consumer has consented to receive

electronic disclosures. The short notice contains abbreviated content, and

must be substantially similar to the CFPB’s model form:

20

o Consumer rights notice (Section 1041.8(c)). After a lender initiates two

consecutive failed payment transfers from a consumer’s account, the lender must

provide to the consumer a consumer rights notice no later than three business days

after it receives information that the second consecutive attempt has failed.

▪ Each consumer rights notice must contain:

• A statement that the named lender is no longer permitted to

withdraw loan payments from the consumer’s account;

• A statement that the last two payment transfer attempts were

returned due to insufficient funds, or, if applicable to payments

initiated by the consumer’s account-holding institution, caused the

account to go into overdraft status;

• Consumer account information—sufficient information to permit

the consumer to identify the account from which unsuccessful

payment attempts were made, but without providing the complete

account number;

• Loan identification information—sufficient information to permit

the consumer to identify any covered loans associated with the

unsuccessful payment attempts;

• A statement that Federal law prohibits the lender from initiating

further payment transfers without the consumer’s permission;

• A statement that the lender may be in contact with the consumer

about payment choices;

• A tabular breakdown of previous unsuccessful payment attempts,

including

o a heading stating “previous payment attempts”;

o the scheduled payment due date of each previous

unsuccessful payment transfer attempted by the lender; the

date of each previous attempt;

o the amount of each previous unsuccessful payment transfer;

o the fees charged by the lender for each unsuccessful

payment attempt, if applicable, with an indication that the

fees were charged by the lender; and

21

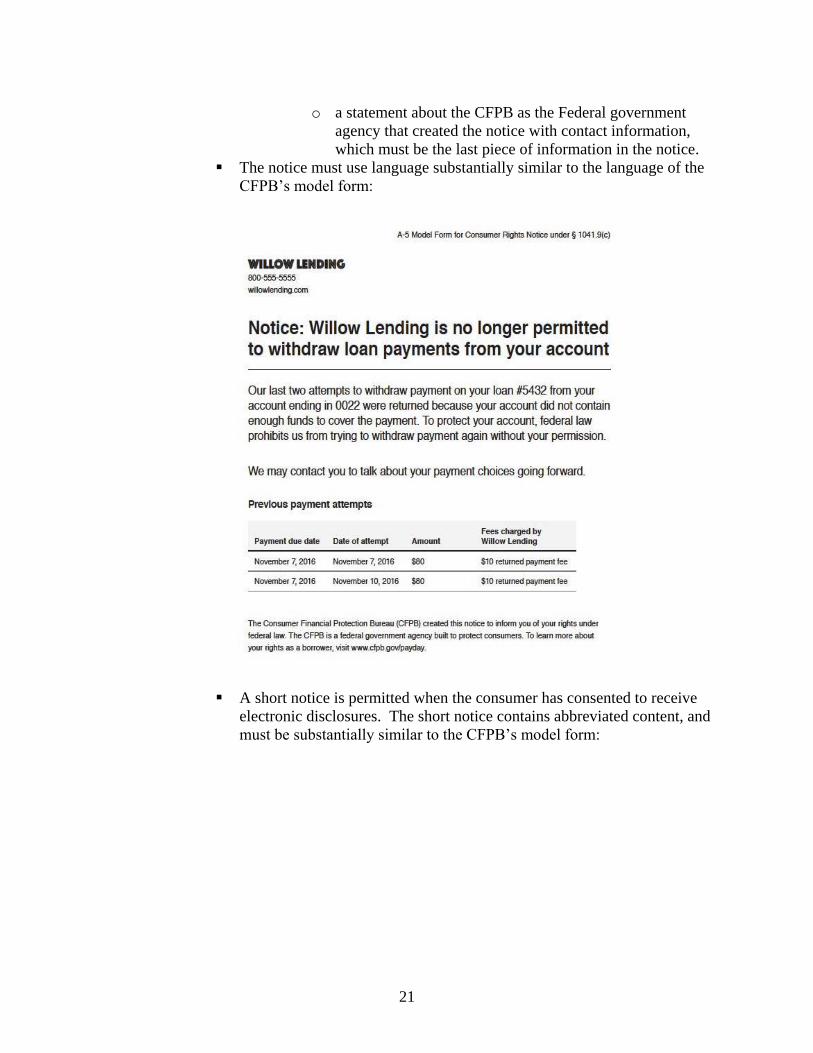

o a statement about the CFPB as the Federal government

agency that created the notice with contact information,

which must be the last piece of information in the notice.

▪ The notice must use language substantially similar to the language of the

CFPB’s model form:

▪ A short notice is permitted when the consumer has consented to receive

electronic disclosures. The short notice contains abbreviated content, and

must be substantially similar to the CFPB’s model form:

22

V. Information Furnishing, Recordkeeping, Anti-Evasion, and Severability

• Furnishing to Information Systems (Section 1041.10(a) and (b)). For each covered short-

term loan and covered longer-term balloon-payment loan a lender makes, the lender must

furnish specified loan information to each information system that, as of the date the loan

is consummated, has been registered with the CFPB for 180 days or more, or has been

provisionally registered with the CFPB for 180 days or more.

o The CFPB will publish on its website and in the Federal Register notice of

provisional registrations, registrations, and suspensions or revocations of

provisional registrations and registrations.

o The CFPB will maintain on its website a current list of provisionally registered

and registered information systems.

o A provisional registration, registration, suspension, or revocation is effective on

the date the CFPB publishes notice of such status on its website.

o The CFPB will provide instructions on its website concerning the scope and terms

of any suspension of revocation of a provisional registration or registration of an

information system.

• Information to Be Furnished (Section 1041.10(c)). A lender must furnish the following

information about each covered short-term loan and covered longer-term balloon-

payment loan in a format acceptable to each information system at the following stages:

o At consummation, the lender must furnish on the date of consummation or as

close in time as feasible to the date of consummation:

▪ Unique loan identifying information;

▪ Information to identify the specific consumer(s) responsible for the loan;

▪ Whether the loan is a covered short-term loan or a covered longer-term

balloon-payment loan;

▪ Whether the loan is made under the short-term loan ability to repay

standard in Section 1041.5 or under the conditional exemption for loan

sequencing for certain covered short-term loans in Section § 1041.6, as

applicable;

23

▪ The loan consummation date;

▪ For a loan made under the conditional exemption for loan sequencing in

Section 1041.6, the principal amount borrowed;

▪ For a loan that is closed-end credit:

• The fact that the loan is closed-end credit;

• The date that each payment on the loan is due; and

• The amount due on each payment date.

▪ For a loan that is open-end credit:

• The fact that the loan is open-end credit;

• The credit limit on the loan;

• The date that each payment on the loan is due; and

• The minimum amount due on each payment date. (Section

1041.10(c)(1)).

o When a covered loan is outstanding, the lender must furnish updates within a

reasonable period of time of the event which causes the information previously

furnished to be out of date. (Section 1041.10(c)(2)).

o When a loan ceases to be outstanding, the lender must furnish no later than the

date the loan ceases to be outstanding or as close in time as feasible to that date:

▪ The date as of which the loan ceased to be an outstanding loan; and

▪ Whether all amounts owed were paid in full, including the amount

financed, charges included in the cost of credit, and charges excluded from

the cost of credit. (Section 1041.10(c)(3)).

▪ A loan ceases to be outstanding if no payments have been made for the

prior 180 days. (Section 1041.2(a)(17)).

• Registered Information Systems (Section 1041.11).

o Eligibility criteria (Section 1041.11(b)). An entity must satisfy each of the

following eight conditions to be eligible for CFPB designation as a provisionally

registered information system or a registered information system:

▪ Receiving capability. Possess the technical capability to receive

information lenders must furnish under Section 1041.10 immediately upon

the furnishing of such information, and use reasonable data standards that

facilitate the timely and accurate transmission and processing of

information in a manner that does not impose unreasonable costs or

burdens on lenders.

▪ Reporting capability. Possess the technical capability to generate a

consumer report containing, as applicable for each unique consumer, all

information required to be furnished by a lender under Section 1041.10

substantially simultaneous to receiving the information from a lender.

▪ Performance. Perform in a manner that facilitates compliance with and

furthers the purposes of Part 1041.

▪ Federal consumer financial law compliance program. Has developed,

implemented, and maintains a compliance program reasonably designed to

24

ensure compliance with all applicable Federal consumer financial laws,

which includes written policies and procedures, comprehensive training,

and monitoring to detect and to promptly correct compliance weaknesses.

▪ Independent assessment of compliance program. Provide to the CFPB in

its application for provisional registration or registration a written

assessment of its Federal consumer financial law compliance program

that:

• Sets forth a detailed summary of the Federal consumer financial

law compliance program that the entity has implemented and

maintains;

• Explains how the Federal consumer financial law compliance

program is appropriate for the entity’s size and complexity, the

nature and scope of its activities, and risks to consumers presented

by such activities;

• Certifies that, in the opinion of the assessor, the Federal consumer

financial law compliance program is operating with sufficient

effectiveness to provide reasonable assurance that the entity is

fulfilling its obligations under all Federal consumer financial laws;

and

• Certifies that the assessment has been conducted by a qualified,

objective, independent third-party individual or entity that uses

procedures and standards generally accepted in the profession,

adheres to professional and business ethics, performs all duties

objectively, and is free from any conflicts of interest that might

compromise the assessor’s independent judgment in performing

assessments.

▪ Information security program. Has developed, implemented, and

maintains a comprehensive information security program that complies

with the Standards for Safeguarding Customer Information, 16 CFR part

314.

▪ Independent assessment of information security program. Provide to the

CFPB in its application for provisional registration or registration and on

at least a biennial basis thereafter, a written assessment of its information

security program. Each written assessment must be completed and

provided to the CFPB within 60 days after the end of the period to which

the assessment applies. Each written assessment shall:

• Set forth the administrative, technical, and physical safeguards that

the entity has implemented and maintains;

• Explain how such safeguards are appropriate to the entity’s size

and complexity, the nature and scope of its activities, and the

sensitivity of the customer information at issue;

• Explain how the safeguards that have been implemented meet or

exceed the protections required by the Standards for Safeguarding

Customer Information, 16 CFR part 314;

• Certify that, in the opinion of the assessor, the information security

program is operating with sufficient effectiveness to provide

25

reasonable assurance that the entity is fulfilling its obligations

under the Standards for Safeguarding Customer Information, 16

CFR part 314; and

• Certify that the assessment has been conducted by a qualified,

objective, independent third-party individual or entity that uses

procedures and standards generally accepted in the profession,

adheres to professional and business ethics, performs all duties

objectively, and is free from any conflicts of interest that might

compromise the assessor’s independent judgment in performing

assessments.

o Professionals qualified to make such assessments include: a

person qualified as a Certified Information System Security

Professional (CISSP) or as a Certified Information Systems

Auditor (CISA); a person holding Global Information

Assurance Certification (GIAC) from the SysAdmin, Audit,

Network, Security (SANS) Institute; and an individual or

entity with a similar qualification or certification

▪ Consent to CFPB supervisory authority. Acknowledge that the entity is,

or consents to being, subject to the CFPB’s supervisory authority.

o Registration Process and Timing (Sections 1041.11(c) through (g)).

▪ Preliminary Approval. Prior to the effective date of the furnishing

requirements in Section 1041.10:

• Effective Dates.

o The effective date of the furnishing requirements in Section

1041.10 is 21 months after the date of the rule’s publication

in the Federal Register [approximately August 1, 2019].

o The effective date of these registration requirements in

Section 1041.11 is two months after the date of the rule’s

publication in the Federal Register [approximately January

1, 2018].

• The CFPB may preliminarily approve an entity for registration as

an information system only if the entity submits an application to

the CFPB within 90 days from the effective date of Section

1041.11 [150 days after publication of the rule and the Federal

Register, or approximately April 1, 2018] containing information

sufficient for the CFPB to determine that the entity is reasonably

likely to satisfy the conditions for eligibility as a registered

information system within 120 days from the date preliminary

approval is granted.

o The Federal consumer financial law compliance and

information security assessments do not need to be

included with an application for preliminary approval for

registration or completed prior to the submission of the

application.

26

• The CFPB may approve an application to be a registered

information system only if the entity:

o Received preliminary approval; and

o Submits an application to the CFPB within 120 days from

the date preliminary approval for registration is granted

containing information and documentation sufficient for the

CFPB to determine that the entity satisfies the conditions

for eligibility as a registered information system.

• The CFPB may waive the above deadlines.

• The CFPB may require additional information and documentation

to:

o Facilitate a preliminary approval determination; or

o Facilitate a determination on an application or assess

whether registration of the entity would pose an

unreasonable risk to consumers.

▪ Provisional Registration. On or after the effective date of the furnishing

requirements in Section 1041.10:

• The CFPB may approve an entity to be a provisionally registered

information system only if the entity submits an application that

contains information and documentation sufficient for the CFPB to

determine that the entity satisfies the conditions for eligibility.

• The CFPB may require additional information and documentation

to facilitate this determination or otherwise to assess whether

provisional registration of the entity would pose an unreasonable

risk to consumers.

• An information system that is provisionally registered on or after

the effective date of the furnishing requirements in Section

1041.10 automatically becomes a registered information system

upon the expiration of the 240-day period commencing on the date

the information system is provisionally registered.

• An information system is provisionally registered on the date that

the CFPB publishes notice of the provisional registration on the

Bureau’s website.

▪ Applications for preliminary approval, registration, and provisional registration

must be submitted in the form required by the CFPB and must include, in addition

to the other information required in Section 1041.10, the following information:

• The name under which the applicant does business, including any

“doing business as” or other trade name;

• The applicant’s main business address, mailing address if different

from the main business address, telephone number, email address,

and Internet website; and

• The name and contact information (including telephone number

and email address) of the person authorized to communicate with

the CFPB on the applicant’s behalf concerning the application.

27

▪ The CFPB will deny an application for preliminary approval, registration, or

provisional registration if:

• The entity does not satisfy the conditions for eligibility, or, in the

case of an entity seeking preliminary approval, is not reasonably

likely to satisfy the conditions within 120 days from the date

preliminary approval is granted;

• The application is untimely, materially inaccurate, or incomplete;

or

• Preliminary approval, provisional registration, or registration

would pose an unreasonable risk to consumers.

▪ A provisionally registered or registered information system must notify the CFPB

in writing of any material change to information in its application or previously

provided to the CFPB for purposes of registration within 14 days of such change.

o Suspension or Revocation (Section 1041.10(h)).

▪ The CFPB will suspend or revoke a preliminary approval, provisional registration,

or registration if it determines that the entity:

• Has not satisfied or no longer satisfies the conditions for eligibility;

• Has not notified the CFPB of a material change to the information

in its application or information previously provided to the CFPB;1

or

• Poses an unreasonable risk to consumers.

▪ The CFPB may require additional information and documentation if it has reason

to believe that suspension or revocation may be warranted.

▪ Except in cases of willfulness or where the public interest requires otherwise, the

CFPB will provide written notice of the facts or conduct that may warrant

suspension or revocation and give the entity or information system an opportunity

to demonstrate or achieve compliance or address the CFPB’s concerns.

▪ If an entity submits a written request to the CFPB that its preliminary approval,

provisional registration, or registration be revoked, the CFPB will revoke the

entity’s preliminary approval, provisional registration, or registration.

▪ Suspension or revocation of an information system’s revocation is effective:

• For purposes of the ability-to-repay and conditional exemption for

certain loan sequences in Sections 1041.5 and .6, five days after

the date the CFPB publishes notice of the suspension or revocation

on its website; and

• For purposes of the lender furnishing obligations in Section

1041.10(b), on the date the CFPB publishes notice of the

suspension or revocation in its website.

1 The regulatory text cites to a provision dealing with the denial of an application, not with the material change provision. However, this appears to be a typographical error, as the denial of application provision is largely duplicative of the other bases for suspension or revocation.

28

o Administrative Appeals (Section 1041.10(i)).

▪ An entity may appeal a CFPB determination that:

• Denies the entity’s application for preliminary approval for

registration, registration, or provisional registration; or

• Suspends or revokes the entity’s preliminary approval for

registration, registration, or provisional registration.

▪ An appeal must be submitted within 30 business days of the date of the

determination, but the CFPB may extend this time for good cause.

▪ An appeal must be submitted by electronic means in the manner set forth on the

CFPB’s website, and must:

• Be labeled “Information System Registration Appeal.”

• Set forth contact information for the appellant including, to the

extent available, a mailing address, telephone number, or email

address at which the Bureau may contact the appellant regarding

the appeal;

• Specify the date of the letter of determination, and enclose a copy

of the determination being appealed; and

• Include a description of the issues in dispute, specify the legal and

factual basis for appealing the determination, and include

appropriate supporting information.

▪ The filing and pendency of an appeal does not suspend the determination that is

the subject of the appeal during the appeals process; however, the CFPB may, in

its discretion, suspend the determination that is the subject of the appeal during

the appeals process.

▪ The CFPB will decide whether to affirm the determination (in whole or in part) or

to reverse the determination (in whole or in part) and will notify the appellant of

this decision in writing.

• Lender Compliance Program and Record Retention (Section 1041.12).

o Lender compliance program (Section 1041.12(a)). A lender making a covered

loan must develop and follow written policies and procedures that are reasonably

designed to ensure compliance with the requirements in Part 1041. These policies

and procedures must be appropriate to the size and complexity of the lender and

its affiliates, and the nature and scope of the covered loan lending activities of the

lender and its affiliates.

o Record retention (Section 1041.12(b)). A lender must retain evidence of

compliance with Part 41 for 36 months after the date on which a covered loan

ceases to be an outstanding loan.

• Record retention for covered short-term and covered longer-term balloon-payment

loans (Section 1041.12(b)(1)-(3)).

o Origination documents. A lender must retain or be able to reproduce an image of

the loan agreement and documentation obtained in connection with a covered

29

short-term or covered longer-term balloon-payment loan, including the following

as applicable:

o Consumer report from an information system registered with the CFPB;

o Verification evidence; and

o Written statement obtained from the consumer.

• Calculation and ability-to-repay determination documents. For covered short-term or

covered longer-term balloon-payment loans subject to the ability-to-repay

requirements in Section 1041.5, a lender must retain electronic records in tabular

format that include the following information:

o The projection made by the lender of the amount of a consumer’s net income

during the relevant monthly period;

o The projections made by the lender of the amounts of a consumer’s major

financial obligations during the relevant monthly period;

o Calculated residual income or debt-to-income ratio during the relevant

monthly period;

o Estimated basic living expenses for the consumer during the relevant monthly

period; and

o Other consumer-specific information considered in making the ability-to-

repay determination.

• Type, terms, and performance documents. For covered short-term or covered longer-

term balloon-payment loans, a lender also must retain electronic records in tabular

format that include the following information:

o As applicable, the information the lender furnished to each information

system at loan consummation and while the loan is outstanding, listed in

Sections 1041.10(c)(1)(i) through (viii) and 1041.10(c)(2);

o Whether the lender obtained vehicle security from the consumer;

o The loan number in a loan sequence of covered short-term loans, covered

longer-term balloon-payment loans, or a combination thereof.

o For any full payment on the loan that was not received or transferred by the

contractual due date, the number of days such payment was past due, up to a

maximum of 180 days;

o For a loan with vehicle security, whether repossession of the vehicle was

initiated;

o Date of last or final payment received; and

o The date the loan ceased to be an outstanding loan and whether all amounts

owed in connection with the loan were paid in full.

• Record retention for payment practices (Section 1041.12(b)(4)-(5)).

o A lender must retain or be able to reproduce an image of the following

documentation, as applicable, in connection with a covered loan:

▪ Leveraged payment mechanism(s) obtained by the lender from the

consumer;

▪ Authorization of additional payment transfer, as described in Section

1041.8(c)(3)(iii); and

30

▪ Underlying one-time electronic transfer authorization or underlying

signature check, as described in § 1041.8(d)(2).

o A lender must retain electronic records in tabular format that include the

following information for all covered loans:

▪ History of payments received and attempted payment transfers, as

defined in Section 1041.8(a)(1), including: date of receipt of payment

or attempted payment transfer; amount of payment due; amount of

attempted payment transfer; amount of payment received or

transferred; and payment channel used for attempted payment transfer.

▪ If an attempt to transfer funds from a consumer’s account is subject to

the prohibition on initiating such transfers after two consecutive failed

payment transfers, whether the lender or service provider obtained

authorization to initiate additional payment transfers from the

consumer in accordance with Sections 1041.8(c) or (d).

• Prohibition Against Evasion (Section 1041.13). A lender is prohibited from taking

any action with intent to evade the requirements of part 1041. The commentary states

that the actual substance of the lender’s action as well as other relevant facts and

circumstances will determine whether the lender’s action was taken with the intent of

evading the requirements. The commentary emphasizes that evasion is not an issue

for lender actions “taken solely for legitimate business purposes,” but that fraud,

deceit, or other unlawful or illegitimate activity may contribute to a finding of

evasion.

• Severability (Section 1041.20). The provisions of the rule are separate and severable

from one another. If any provision is stayed or determined to be invalid, the CFPB’s

intention is that the remaining provisions shall continue in effect.