SUMMARISED STATEMENT OF CASH FLOWS - CLHG · Cash (outf low)/infl ow from fi nancing acti viti es...

2

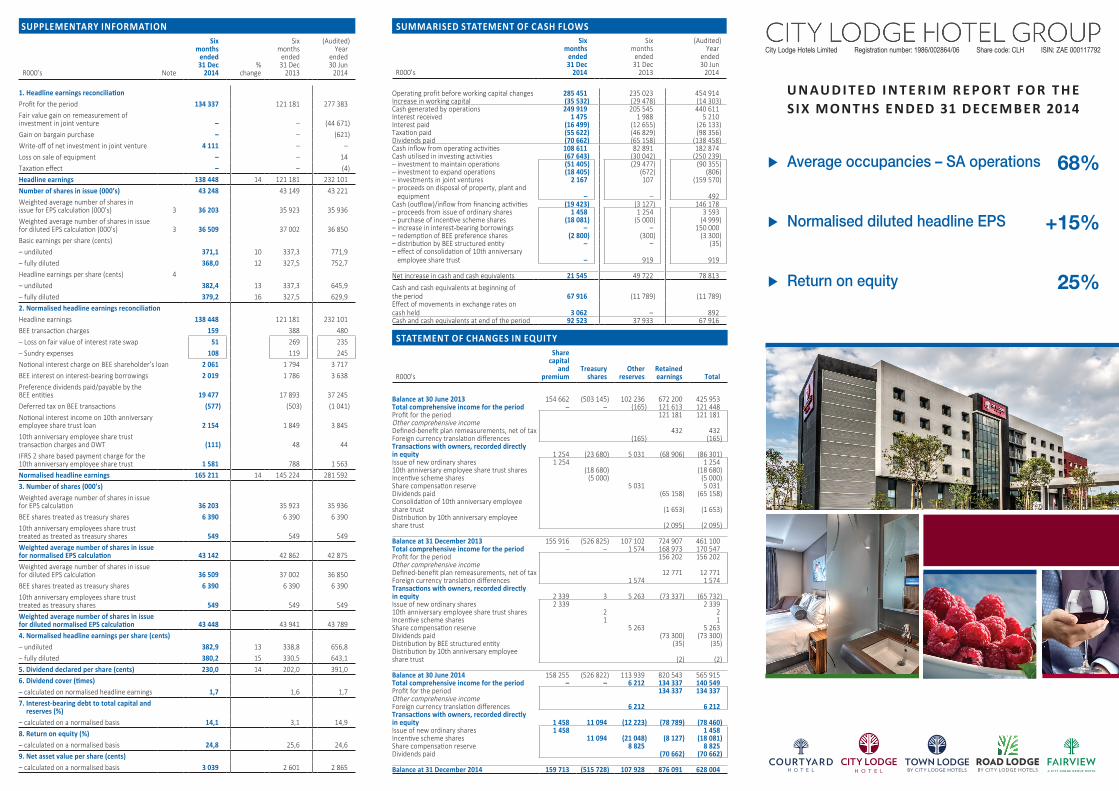

FOR THE SIX MONTHS ENDED Average occupancies – SA operations 68% Normalised diluted headline EPS +15% Return on equity 25% City Lodge Hotels Limited Registration number: 1986/002864/06 Share code: CLH ISIN: ZAE 000117792 UNAUDITED INTERIM REPORT FOR THE SIX MONTHS ENDED 31 DECEMBER 2014 SUMMARISED STATEMENT OF CASH FLOWS R000’s Six months ended 31 Dec 2014 Six months ended 31 Dec 2013 (Audited) Year ended 30 Jun 2014 Operating profit before working capital changes 285 451 235 023 454 914 Increase in working capital (35 532) (29 478) (14 303) Cash generated by operations 249 919 205 545 440 611 Interest received 1 475 1 988 5 210 Interest paid (16 499) (12 655) (26 133) Taxaon paid (55 622) (46 829) (98 356) Dividends paid (70 662) (65 158) (138 458) Cash inflow from operang acvies 108 611 82 891 182 874 Cash utilised in investing activities (67 643) (30 042) (250 239) – investment to maintain operaons (51 405) (29 477) (90 355) – investment to expand operaons (18 405) (672) (806) – investments in joint ventures 2 167 107 (159 570) – proceeds on disposal of property, plant and equipment – – 492 Cash (oulow)/inflow from financing acvies (19 423) (3 127) 146 178 – proceeds from issue of ordinary shares 1 458 1 254 3 593 – purchase of incenve scheme shares (18 081) (5 000) (4 999) – increase in interest-bearing borrowings – – 150 000 – redempon of BEE preference shares (2 800) (300) (3 300) – distribuon by BEE structured enty – – (35) – effect of consolidaon of 10th anniversary employee share trust – 919 919 Net increase in cash and cash equivalents 21 545 49 722 78 813 Cash and cash equivalents at beginning of the period 67 916 (11 789) (11 789) Effect of movements in exchange rates on cash held 3 062 – 892 Cash and cash equivalents at end of the period 92 523 37 933 67 916 STATEMENT OF CHANGES IN EQUITY R000’s Share capital and premium Treasury shares Other reserves Retained earnings Total Balance at 30 June 2013 154 662 (503 145) 102 236 672 200 425 953 Total comprehensive income for the period – – (165) 121 613 121 448 Profit for the period 121 181 121 181 Other comprehensive income Defined-benefit plan remeasurements, net of tax 432 432 Foreign currency translaon differences (165) (165) Transacons with owners, recorded directly in equity 1 254 (23 680) 5 031 (68 906) (86 301) Issue of new ordinary shares 1 254 1 254 10th anniversary employee share trust shares (18 680) (18 680) Incenve scheme shares (5 000) (5 000) Share compensaon reserve 5 031 5 031 Dividends paid (65 158) (65 158) Consolidaon of 10th anniversary employee share trust (1 653) (1 653) Distribuon by 10th anniversary employee share trust (2 095) (2 095) Balance at 31 December 2013 155 916 (526 825) 107 102 724 907 461 100 Total comprehensive income for the period – – 1 574 168 973 170 547 Profit for the period 156 202 156 202 Other comprehensive income Defined-benefit plan remeasurements, net of tax 12 771 12 771 Foreign currency translaon differences 1 574 1 574 Transacons with owners, recorded directly in equity 2 339 3 5 263 (73 337) (65 732) Issue of new ordinary shares 2 339 2 339 10th anniversary employee share trust shares 2 2 Incenve scheme shares 1 1 Share compensaon reserve 5 263 5 263 Dividends paid (73 300) (73 300) Distribuon by BEE structured enty (35) (35) Distribuon by 10th anniversary employee share trust (2) (2) Balance at 30 June 2014 158 255 (526 822) 113 939 820 543 565 915 Total comprehensive income for the period – – 6 212 134 337 140 549 Profit for the period 134 337 134 337 Other comprehensive income Foreign currency translaon differences 6 212 6 212 Transacons with owners, recorded directly in equity 1 458 11 094 (12 223) (78 789) (78 460) Issue of new ordinary shares 1 458 1 458 Incenve scheme shares 11 094 (21 048) (8 127) (18 081) Share compensaon reserve 8 825 8 825 Dividends paid (70 662) (70 662) Balance at 31 December 2014 159 713 (515 728) 107 928 876 091 628 004 SUPPLEMENTARY INFORMATION R000’s Note Six months ended 31 Dec 2014 % change Six months ended 31 Dec 2013 (Audited) Year ended 30 Jun 2014 1. Headline earnings reconciliaon Profit for the period 134 337 121 181 277 383 Fair value gain on remeasurement of investment in joint venture – – (44 671) Gain on bargain purchase – – (621) Write-off of net investment in joint venture 4 111 – – Loss on sale of equipment – – 14 Taxaon effect – – (4) Headline earnings 138 448 14 121 181 232 101 Number of shares in issue (000’s) 43 248 43 149 43 221 Weighted average number of shares in issue for EPS calculaon (000’s) 3 36 203 35 923 35 936 Weighted average number of shares in issue for diluted EPS calculaon (000’s) 3 36 509 37 002 36 850 Basic earnings per share (cents) – undiluted 371,1 10 337,3 771,9 – fully diluted 368,0 12 327,5 752,7 Headline earnings per share (cents) 4 – undiluted 382,4 13 337,3 645,9 – fully diluted 379,2 16 327,5 629,9 2. Normalised headline earnings reconciliaon Headline earnings 138 448 121 181 232 101 BEE transacon charges 159 388 480 – Loss on fair value of interest rate swap 51 269 235 – Sundry expenses 108 119 245 Noonal interest charge on BEE shareholder’s loan 2 061 1 794 3 717 BEE interest on interest-bearing borrowings 2 019 1 786 3 638 Preference dividends paid/payable by the BEE enes 19 477 17 893 37 245 Deferred tax on BEE transacons (577) (503) (1 041) Noonal interest income on 10th anniversary employee share trust loan 2 154 1 849 3 845 10th anniversary employee share trust transacon charges and DWT (111) 48 44 IFRS 2 share based payment charge for the 10th anniversary employee share trust 1 581 788 1 563 Normalised headline earnings 165 211 14 145 224 281 592 3. Number of shares (000’s) Weighted average number of shares in issue for EPS calculaon 36 203 35 923 35 936 BEE shares treated as treasury shares 6 390 6 390 6 390 10th anniversary employees share trust treated as treated as treasury shares 549 549 549 Weighted average number of shares in issue for normalised EPS calculaon 43 142 42 862 42 875 Weighted average number of shares in issue for diluted EPS calculaon 36 509 37 002 36 850 BEE shares treated as treasury shares 6 390 6 390 6 390 10th anniversary employees share trust treated as treasury shares 549 549 549 Weighted average number of shares in issue for diluted normalised EPS calculaon 43 448 43 941 43 789 4. Normalised headline earnings per share (cents) – undiluted 382,9 13 338,8 656,8 – fully diluted 380,2 15 330,5 643,1 5. Dividend declared per share (cents) 230,0 14 202,0 391,0 6. Dividend cover (mes) – calculated on normalised headline earnings 1,7 1,6 1,7 7. Interest-bearing debt to total capital and reserves (%) – calculated on a normalised basis 14,1 3,1 14,9 8. Return on equity (%) – calculated on a normalised basis 24,8 25,6 24,6 9. Net asset value per share (cents) – calculated on a normalised basis 3 039 2 601 2 865

-

Upload

trinhduong -

Category

Documents

-

view

213 -

download

0

Transcript of SUMMARISED STATEMENT OF CASH FLOWS - CLHG · Cash (outf low)/infl ow from fi nancing acti viti es...

UNAUDITED INTERIM REPORT FOR THE S IX MONTHS ENDED

31 DECEMBER 2014

� Average occupancies – SA operations 68%

� Normalised diluted headline EPS +15%

� Return on equity 25%

City Lodge Hotels Limited Registration number: 1986/002864/06 Share code: CLH ISIN: ZAE 000117792

U N AU D I T E D I N T E R I M R E P O R T F O R T H E S IX MONTHS ENDED 31 DECEMBER 2014

8

ROAD LODGECORPORATE IDENTITY GUIDELINES

STACKED 1The first stacked logo is the preferred logo version and should be used wherever possible in print. It features the two words of the logotype in a single line, with the symbol centred directly above. The decriptor line is always placed below the logotype.

STACKED 2The second stacked option has the word “LODGE” centred below the first line of logotype. This version should only be used when the available space is close to a square shape (typically signage).

LOGO

STACKED VERSIONS

SUMMARISED STATEMENT OF CASH FLOWS

R000’s

Six months

ended31 Dec

2014

Six months

ended31 Dec

2013

(Audited)Year

ended30 Jun

2014

Operating profit before working capital changes 285 451 235 023 454 914 Increase in working capital (35 532) (29 478) (14 303)Cash generated by operations 249 919 205 545 440 611 Interest received 1 475 1 988 5 210 Interest paid (16 499) (12 655) (26 133)Taxati on paid (55 622) (46 829) (98 356)Dividends paid (70 662) (65 158) (138 458)Cash infl ow from operati ng acti viti es 108 611 82 891 182 874 Cash utilised in investing activities (67 643) (30 042) (250 239)– investment to maintain operati ons (51 405) (29 477) (90 355)– investment to expand operati ons (18 405) (672) (806)– investments in joint ventures 2 167 107 (159 570)– proceeds on disposal of property, plant and

equipment – – 492 Cash (outf low)/infl ow from fi nancing acti viti es (19 423) (3 127) 146 178 – proceeds from issue of ordinary shares 1 458 1 254 3 593 – purchase of incenti ve scheme shares (18 081) (5 000) (4 999)– increase in interest-bearing borrowings – – 150 000 – redempti on of BEE preference shares (2 800) (300) (3 300)– distributi on by BEE structured enti ty – – (35)– eff ect of consolidati on of 10th anniversary

employee share trust – 919 919

Net increase in cash and cash equivalents 21 545 49 722 78 813

Cash and cash equivalents at beginning of the period 67 916 (11 789) (11 789)Effect of movements in exchange rates on cash held 3 062 – 892 Cash and cash equivalents at end of the period 92 523 37 933 67 916

STATEMENT OF CHANGES IN EQUITY

R000’s

Sharecapital

and premium

Treasuryshares

Otherreserves

Retainedearnings Total

Balance at 30 June 2013 154 662 (503 145) 102 236 672 200 425 953 Total comprehensive income for the period – – (165) 121 613 121 448 Profi t for the period 121 181 121 181 Other comprehensive incomeDefi ned-benefi t plan remeasurements, net of tax 432 432 Foreign currency translati on diff erences (165) (165)Transacti ons with owners, recorded directly in equity 1 254 (23 680) 5 031 (68 906) (86 301)Issue of new ordinary shares 1 254 1 254 10th anniversary employee share trust shares (18 680) (18 680)Incenti ve scheme shares (5 000) (5 000)Share compensati on reserve 5 031 5 031 Dividends paid (65 158) (65 158)Consolidati on of 10th anniversary employee share trust (1 653) (1 653)Distributi on by 10th anniversary employee share trust (2 095) (2 095)

Balance at 31 December 2013 155 916 (526 825) 107 102 724 907 461 100 Total comprehensive income for the period – – 1 574 168 973 170 547 Profi t for the period 156 202 156 202 Other comprehensive incomeDefi ned-benefi t plan remeasurements, net of tax 12 771 12 771 Foreign currency translati on diff erences 1 574 1 574 Transacti ons with owners, recorded directly in equity 2 339 3 5 263 (73 337) (65 732)Issue of new ordinary shares 2 339 2 339 10th anniversary employee share trust shares 2 2Incenti ve scheme shares 1 1Share compensati on reserve 5 263 5 263 Dividends paid (73 300) (73 300)Distributi on by BEE structured enti ty (35) (35)Distributi on by 10th anniversary employee share trust (2) (2)

Balance at 30 June 2014 158 255 (526 822) 113 939 820 543 565 915 Total comprehensive income for the period – – 6 212 134 337 140 549 Profi t for the period 134 337 134 337 Other comprehensive incomeForeign currency translati on diff erences 6 212 6 212 Transacti ons with owners, recorded directly in equity 1 458 11 094 (12 223) (78 789) (78 460)Issue of new ordinary shares 1 458 1 458 Incenti ve scheme shares 11 094 (21 048) (8 127) (18 081)Share compensati on reserve 8 825 8 825 Dividends paid (70 662) (70 662)

Balance at 31 December 2014 159 713 (515 728) 107 928 876 091 628 004

SUPPLEMENTARY INFORMATION

R000’s Note

Six months

ended31 Dec

2014 %

change

Six months

ended31 Dec

2013

(Audited)Year

ended30 Jun

2014

1. Headline earnings reconciliati onProfi t for the period 134 337 121 181 277 383 Fair value gain on remeasurement of investment in joint venture – – (44 671)Gain on bargain purchase – – (621)Write-off of net investment in joint venture 4 111 – – Loss on sale of equipment – – 14 Taxati on eff ect – – (4)Headline earnings 138 448 14 121 181 232 101 Number of shares in issue (000’s) 43 248 43 149 43 221Weighted average number of shares inissue for EPS calculati on (000’s) 3 36 203 35 923 35 936Weighted average number of shares in issue for diluted EPS calculati on (000’s) 3 36 509 37 002 36 850Basic earnings per share (cents)– undiluted 371,1 10 337,3 771,9– fully diluted 368,0 12 327,5 752,7Headline earnings per share (cents) 4– undiluted 382,4 13 337,3 645,9 – fully diluted 379,2 16 327,5 629,9 2. Normalised headline earnings reconciliati onHeadline earnings 138 448 121 181 232 101 BEE transacti on charges 159 388 480 – Loss on fair value of interest rate swap 51 269 235 – Sundry expenses 108 119 245 Noti onal interest charge on BEE shareholder’s loan 2 061 1 794 3 717 BEE interest on interest-bearing borrowings 2 019 1 786 3 638 Preference dividends paid/payable by the BEE enti ti es 19 477 17 893 37 245 Deferred tax on BEE transacti ons (577) (503) (1 041)Noti onal interest income on 10th anniversary employee share trust loan 2 154 1 849 3 845 10th anniversary employee share trust transacti on charges and DWT (111) 48 44 IFRS 2 share based payment charge for the 10th anniversary employee share trust 1 581 788 1 563 Normalised headline earnings 165 211 14 145 224 281 592 3. Number of shares (000’s)Weighted average number of shares in issue for EPS calculati on 36 203 35 923 35 936 BEE shares treated as treasury shares 6 390 6 390 6 390 10th anniversary employees share trust treated as treated as treasury shares 549 549 549Weighted average number of shares in issue for normalised EPS calculati on 43 142 42 862 42 875Weighted average number of shares in issue for diluted EPS calculati on 36 509 37 002 36 850 BEE shares treated as treasury shares 6 390 6 390 6 390 10th anniversary employees share trust treated as treasury shares 549 549 549Weighted average number of shares in issue for diluted normalised EPS calculati on 43 448 43 941 43 789 4. Normalised headline earnings per share (cents)– undiluted 382,9 13 338,8 656,8 – fully diluted 380,2 15 330,5 643,1 5. Dividend declared per share (cents) 230,0 14 202,0 391,06. Dividend cover (ti mes)– calculated on normalised headline earnings 1,7 1,6 1,7 7. Interest-bearing debt to total capital and

reserves (%)– calculated on a normalised basis 14,1 3,1 14,9 8. Return on equity (%)– calculated on a normalised basis 24,8 25,6 24,6 9. Net asset value per share (cents)– calculated on a normalised basis 3 039 2 601 2 865

STATEMENT OF COMPREHENSIVE INCOME

R000’s Note

Six months

ended31 Dec

2014 %

change

Six months

ended31 Dec

2013

(Audited)Year

ended30 Jun

2014

Revenue 642 394 20 533 949 1 062 749 Administration and marketing costs (48 025) (42 220) (83 300)BEE transaction charges 2 (159) (388) (480)Operating costs excluding depreciation (328 721) (267 220) (542 816)

265 489 18 224 121 436 153 Depreciation and amortisation (42 386) (40 574) (78 421)Results from operating activities 223 103 22 183 547 357 732 Interest income 1 475 1 988 5 210 Total interest expense (30 891) (23 856) (50 349)Interest expense (7 334) (2 383) (5 749)Notional interest on BEE shareholder’s loan 2 (2 061) (1 794) (3 717)BEE interest expense 2 (2 019) (1 786) (3 638)BEE preference dividend 2 (19 477) (17 893) (37 245)Fair value gain on remeasurement of investment in joint venture – – 44 671 Share of profit from joint ventures 1 029 11 847 21 327 – Courtyard Hotels 1 029 1 818 2 895 – East Africa (after tax) – 10 029 18 432

Profit before taxation 194 716 12 173 526 378 591 Taxation (60 379) (52 345) (101 208)Profit for the period 134 337 11 121 181 277 383 Other comprehensive incomeItems that will never be reclassified to profit and lossDefined benefit plan remeasurements – 600 18 337 Income tax on other comprehensive income – (168) (5 134)Items that are or may be reclassified to profit and lossForeign currency translation differences 6 212 (165) 1 409 Total comprehensive income for the period 140 549 16 121 448 291 995

STATEMENT OF FINANCIAL POSITION

R000’s31 Dec

201431 Dec

2013

(Audited)30 Jun

2014

ASSETSNon-current assets 1 533 778 1 271 752 1 512 124 Property, plant and equipment 1 478 566 1 058 216 1 457 426 Intangible assets 21 581 – 15 297 Investments in joint ventures 29 484 209 138 35 762 Deferred taxation 4 147 4 398 3 639 Current assets 223 611 132 176 191 785 Inventories 6 828 3 261 6 551 Trade receivables 74 504 63 091 66 330 Other receivables 42 939 25 660 32 539 Taxation 1 869 2 231 4 065 Cash and cash equivalents 97 471 37 933 82 300

Total assets 1 757 389 1 403 928 1 703 909 EQUITYCapital and reserves 628 004 461 100 565 915 Share capital and premium 159 713 155 916 158 255 BEE investment and incentive scheme shares (515 728) (526 825) (526 822)Retained earnings 876 091 724 907 820 543 Other reserves 107 928 107 102 113 939 LIABILITIESNon-current liabilities 1 035 212 820 050 1 016 917 Interest-bearing borrowings 185 000 – 185 000 BEE interest-bearing borrowings 44 120 44 120 44 120 BEE preference shares 418 100 423 900 420 900 BEE shareholder’s loan 30 779 26 795 28 718 BEE preference share dividend accrual 154 179 127 765 141 010 Fair value of BEE interest rate swap – 151 –Other non-current liabilities 108 509 116 454 105 905 Deferred taxation 94 525 80 865 91 264 Current liabilities 94 173 122 778 121 077 Interest-bearing borrowings – 35 000 –BEE preference share dividend accrual 3 146 4 869 3 144 Fair value of BEE interest rate swap 365 2 508 1 210 Trade and other payables 85 714 80 401 102 339 Bank overdraft 4 948 – 14 384

Total liabilities 1 129 385 942 828 1 137 994 Total equity and liabilities 1 757 389 1 403 928 1 703 909 Note: The company has authorised capital commitments of R704 million of which approximately R71 million has been contracted. It is anticipated that approximately R178 million of the authorised commitments will be spent by 30 June 2015.

SEGMENT REPORTPrimary segment City Lodge Town Lodge Road Lodge Central office and other Total

R000’s 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013Revenue 334 186 302 915 108 444 97 601 129 839 117 489 69 925 15 944 642 394 533 949

EBITDAR 201 849 184 801 52 427 46 510 71 705 65 913 (25 312) (42 721) 300 669 254 503Land and hotel building rental (35 180) (30 382) (35 180) (30 382)EBITDA 265 489 224 121 Depreciation and amortisation (11 330) (12 427) (3 744) (3 348) (6 460) (5 750) (20 852) (19 049) (42 386) (40 574)Results from operating activities 223 103 183 547 Share of profit from joint ventures 1 029 11 847 1 029 11 847

South Africa Rest of Africa TotalGeographic information 2014 2013 2014 2013 2014 2013Revenue 583 155 527 119 59 239 6 830 642 394 533 949Share of profit from joint ventures 1 029 1 818 – 10 029 1 029 11 847Non-current assets – property, plant and equipment 1 074 520 1 043 808 404 046 14 408 1 478 566 1 058 216

EBITDAR represents earnings after BEE transaction charges but before interest, taxation, depreciation and rental. EBITDA represents earnings after BEE transaction charges but before interest, taxation and depreciation.

Average occupancies at the group’s South African hotels rose to 68% in the six months to 31 December 2014, an increase of 4 percentage points from the 64% achieved in the previous interim reporting period.

Revenue at the South African operations increased by 10,6% to R583,2 million due to the higher occupancies and a below inflation increase in achieved room rates. Total revenue, including the Kenyan operations, which weren’t consolidated in the prior year, rose by 20,3% to R642,4 million. Kenyan occupancies were lower than in the previous year as a result of the perceived Ebola threat and numerous foreign travel advisories in relation to the terror threat in the region.

Unlike the previous year, the Road Lodge brand also achieved higher occupancies, whilst occupancies at the Courtyard Hotel brand were lower, reflecting the ongoing over-supply in the four star market.

South African operating costs, on a normalised basis, increased by 6,7% on a per room sold basis, resulting in a 0,8 percentage point decrease in the normalised EBITDA margin for the South African operations to 42,0%. Total normalised EBITDA increased by 20,4% to R271,4 million. Depreciation was slightly higher, interest income was lower and interest expense was higher as a result of additional borrowings for the Kenyan operations acquired in May 2014.

As a consequence of lower occupancies, the contribution from the Courtyard joint venture fell to R1,0 million from R1,8 million. This performance was also affected by the closure of Courtyard Hotel Cape Town.

Profit before tax on a normalised basis rose by 14% to R226,3 million, while normalised headline earnings also increased by 14% to R165,2 million. Fully diluted normalised headline earnings per share increased by 15% to 380,2 cents.

In line with the group’s policy of paying out 60% of normalised earnings, an interim dividend of 230 cents has been declared, 14% higher than the previous year’s interim dividend.

DEVELOPMENT ACTIVITY Several major refurbishments have been completed or are underway, which is in keeping with the group’s ongoing commitment to maintaining and upgrading its portfolio across all locations and brands.

The first 35 rooms of the 149-room City Lodge Hotel Waterfall City were opened in mid-December, with the rest of the hotel becoming operational at the beginning of February 2015.

City Lodge Hotel Newtown is progressing well and is on track to open its 148 rooms towards the end of calendar 2015. Construction of the 90-room Road Lodge Pietermaritzburg will commence next week, with completion scheduled for early November.

Detailed design work is at an advanced stage for the development of the 169-room City Lodge Hotel Two Rivers, Nairobi and the 147-room City Lodge Hotel Dar es Salaam, and it is expected that earthworks will commence at each of the locations during the second quarter of 2015. Both hotels are expected to open during the fourth quarter of 2016.

A memorandum of understanding (MOU), which is subject to finalisation of a financial feasibility study, has been signed regarding a land and building lease in Kampala, Uganda, for the development of a 150-room City Lodge Hotel.

Similarly, an MOU, which is subject to certain conditions, has been signed in respect of a land and building lease for a 140 to 150-room Town Lodge in Windhoek, Namibia. Negotiations are at an advanced stage for the acquisition of land in Maputo, Mozambique, with a view to constructing a 150 to 160-room City Lodge Hotel.

OUTLOOK The trend of higher than previous year occupancies extended into January and the first half of February. It is expected that this trend will continue given the combined effect of gradual GDP growth and limited supply of new hotel capacity.

DIRECTORATE Mr Nigel Matthews retired from the board effective 31 December 2014 after 25 years of distinguished service.The board thanks Nigel for his leadership and valued contribution and wishes him well in his retirement.

The board was pleased to announce the appointment of Mr Deon Huysamer as an independent non-executive director with effect from 1 January 2015 and welcomes him to the team.

In addition, a number of changes to the various committees were announced on SENS on 17 December 2014.

www.clhg.comRegistered office: “The Lodge”, Bryanston Gate Office Park, cnr. Homestead Avenue and

Main Road, Bryanston, 2191. Transfer secretaries: Computershare Investor Services Proprietary Limited, 70 Marshall Street, Johannesburg, 2001. Directors: BT Ngcuka (Chairman),

C Ross (Chief executive)*, GG Huysamer, FWJ Kilbourn, N Medupe, SG Morris, Dr KIM Shongwe, W Tlou, AC Widegger* Company secretary: MC van Heerden

Sponsor: JP Morgan Equities South Africa Proprietary Limited *executive

COMMENTARY BASIS OF PREPARATIONThe condensed consolidated interim financial statements are prepared in accordance with International Financial Reporting Standard, IAS 34 Interim Financial Reporting, the SAICA Financial Reporting Guides issued by the Accounting Practices Committee and Financial Pronouncements as issued by the Financial Reporting Standards Council and the requirements of the Companies Act of South Africa.

The accounting policies applied in the preparation of these interim financial statements are in terms of International Financial Reporting Standards and are consistent with those applied in the previous annual financial statements.

The condensed group financial information has been presented on the historical cost basis, except for financial instruments carried at fair value, and are presented in Rand thousands, which is City Lodge’s functional and presentation currency.

These condensed interim financial statements were prepared under the supervision of Mr AC Widegger CA(SA), in his capacity as group financial director.

DECLARATION OF DIVIDENDThe board has approved and declared interim dividend number 52 of 230 cents per ordinary share (gross) in respect of the six months ended 31 December 2014.

The dividend will be subject to Dividends Withholding Tax (DWT). In accordance with paragraphs 11.17 (a) (i) to (x) and 11.17(c) of the JSE Listings Requirements, the following additional information is disclosed:

The dividend has been declared out of income reserves.

The local Dividends Tax rate is 15% (fifteen per centum).

There are no Secondary Tax on Companies (STC) credits utilised.

The gross local dividend amount is 230 cents per ordinary share for shareholders exempt from the Dividends Tax.

The net local dividend amount is 195,5 cents per ordinary share for shareholders liable to pay the Dividends Tax.

The Company currently has 43 247 993 ordinary shares in issue.

The Company’s income tax reference number is 9041001711.

Shareholders are advised of the following dates:

Last date to trade cum dividend Friday, 6 March 2015Shares commence trading ex dividend Monday, 9 March 2015Record date Friday, 13 March 2015Payment of dividend Monday, 16 March 2015

Share certificates may not be dematerialised or rematerialised between Monday, 9 March 2015 and Friday, 13 March 2015, both days inclusive.

For and on behalf of the board

Bulelani Ngcuka Clifford RossChairman Chief executive

17 February 2015