SUCCEEDING IN EMERGING MARKETS - NASBITE

71

SUCCEEDING IN EMERGING MARKETS Michael Pacurar Global Director, Trade & Government Raymond Clark Development Executive, Trade & Government

Transcript of SUCCEEDING IN EMERGING MARKETS - NASBITE

SUCCEEDING IN EMERGING MARKETS

Michael Pacurar

Global Director, Trade & Government

Raymond Clark

Development Executive, Trade & Government

PART I: WHY EMERGING MARKETS?

PART II: CHOOSING THE RIGHT MARKET

PART I: WHY EMERGING MARKETS?

INTRODUCTION

ASSESSING MARKET POTENTIAL

STRATEGIES FOR SUCCESS

CONCLUSION

PART I: WHY EMERGING MARKETS?

INTRODUCTION

ASSESSING MARKET POTENTIAL

STRATEGIES FOR SUCCESS

CONCLUSION

© Euromonitor International

5

Emerging markets still hold the key INTRODUCTION

Source: Euromonitor International from national statistics/OECD/IMF.

© Euromonitor International

6

Emerging markets still hold the key INTRODUCTION

Source: Euromonitor International from national statistics/OECD/IMF.

© Euromonitor International

7

Emerging markets still hold the key INTRODUCTION

Source: Euromonitor International from national statistics/OECD/IMF.

© Euromonitor International

8

Emerging markets still hold the key INTRODUCTION

Source: Euromonitor International from national statistics/OECD/IMF.

© Euromonitor International

9

What does this mean on the ground? INTRODUCTION

Source: Euromonitor International from national statistics/OECD/IMF.

Between 2013 and 2025 Emerging Markets Will See:

PART I: WHY EMERGING MARKETS?

INTRODUCTION

ASSESSING MARKET POTENTIAL

STRATEGIES FOR SUCCESS

CONCLUSION

© Euromonitor International

11

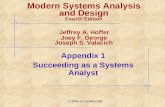

Market

Macroeconomic stability

Middle class

Consumer market size and

growth

Openness

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Access

Infrastructure

Internet

Partners

Retail landscape

Business Environment

Ease of doing business

Government

Corruption

Human capital

Factors affecting market selection ASSESSING MARKET POTENTIAL

© Euromonitor International

12

Market

Macroeconomic stability

Middle class

Consumer market size and

growth

Openness

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Access

Infrastructure

Internet

Partners

Retail landscape

Business Environment

Ease of doing business

Government

Corruption

Human capital

Factors affecting market selection ASSESSING MARKET POTENTIAL

© Euromonitor International

13

Market

Macroeconomic stability

Middle class

Consumer market size and

growth

Openness

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Access

Infrastructure

Internet

Partners

Retail landscape

Business Environment

Ease of doing business

Government

Corruption

Human capital

Factors affecting market selection ASSESSING MARKET POTENTIAL

© Euromonitor International

14

Market

Macroeconomic stability

Middle class

Consumer market size and

growth

Openness

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Access

Infrastructure

Internet

Partners

Retail landscape

Business Environment

Ease of doing business

Government

Corruption

Human capital

Factors affecting market selection ASSESSING MARKET POTENTIAL

© Euromonitor International

15

Market

Macroeconomic stability

Middle class

Consumer market size and

growth

Openness

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Access

Infrastructure

Internet

Partners

Retail landscape

Business Environment

Ease of doing business

Government

Corruption

Human capital

Factors affecting market selection ASSESSING MARKET POTENTIAL

© Euromonitor International

16

Market

Macroeconomic stability

Middle class

Consumer market size and

growth

Openness

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Access

Infrastructure

Internet

Partners

Retail landscape

Business Environment

Ease of doing business

Government

Corruption

Human capital

Factors affecting market selection ASSESSING MARKET POTENTIAL

© Euromonitor International

17

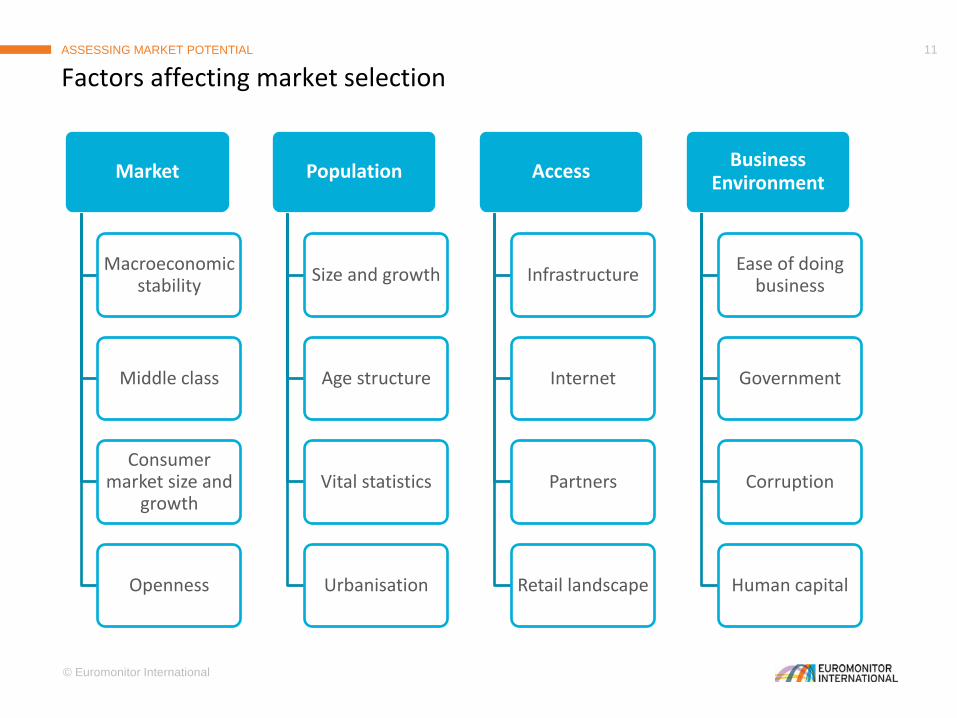

A granular strategy: Across countries

ASSESSING MARKET POTENTIAL

Source: Euromonitor International from national statistics/UN/OECD/IMF. Note: Data refer to a ranking of consumer expenditure growth in 120 major cities globally.

© Euromonitor International

18

A granular strategy: Across countries

ASSESSING MARKET POTENTIAL

• Chinese and Indian cities dominate the rankings of fastest-growing consumer markets

Source: Euromonitor International from national statistics/UN/OECD/IMF. Note: Data refer to a ranking of consumer expenditure growth in 120 major cities globally.

© Euromonitor International

19

A granular strategy: Across countries

ASSESSING MARKET POTENTIAL

• Other more surprising entrants into the list include:

• Minsk • Ho Chi Minh City • Almaty

• Nairobi

Source: Euromonitor International from national statistics/UN/OECD/IMF. Note: Data refer to a ranking of consumer expenditure growth in 120 major cities globally.

© Euromonitor International

20

A granular strategy: Within a country ASSESSING MARKET POTENTIAL

Source: Euromonitor International from national statistics.

© Euromonitor International

21

A granular strategy: Within a country ASSESSING MARKET POTENTIAL

Source: Euromonitor International from national statistics.

© Euromonitor International

22

A granular strategy: Within a country ASSESSING MARKET POTENTIAL

Source: Euromonitor International from national statistics.

© Euromonitor International

23

Young, fast-growing populations

Rapid urbanisation

Strong economic growth Weak infrastructure

Corruption and poor governance

Widespread poverty

Frontier markets offer potential on a vast scale ASSESSING MARKET POTENTIAL

Opportunities

Challenges

PART I: WHY EMERGING MARKETS?

INTRODUCTION

ASSESSING MARKET POTENTIAL

STRATEGIES FOR SUCCESS

CONCLUSION

© Euromonitor International

25

Knowledge is power STRATEGIES FOR SUCCESS

© Euromonitor International

26

A tale of two markets STRATEGIES FOR SUCCESS

Source: Euromonitor International from national statistics. Note: All data refer to 2013.

© Euromonitor International

27

A tale of two markets STRATEGIES FOR SUCCESS

Source: Euromonitor International from national statistics. Note: All data refer to 2013.

© Euromonitor International

28

A tale of two markets STRATEGIES FOR SUCCESS

Source: Euromonitor International from national statistics. Note: All data refer to 2013.

PART I: WHY EMERGING MARKETS?

INTRODUCTION

ASSESSING MARKET POTENTIAL

STRATEGIES FOR SUCCESS

CONCLUSION

© Euromonitor International

30

Choose wisely – remembering the market, population, access and business environment factors affecting selection:

Look beyond the usual suspects

Think granular

Learn from others – winning strategies are based on knowledge:

Differentiate between and within markets

Localisation

Sales strategies

Price and features

Winning in emerging markets requires staying power CONCLUSION

PART I: WHY EMERGING MARKETS?

PART II: CHOOSING THE RIGHT MARKET

PART II: CHOOSING THE RIGHT MARKET

INTRODUCTION

MARKET

POPULATION

ACCESS

BUSINESS ENVIRONMENT

CONCLUSION

PART II: CHOOSING THE RIGHT MARKET

INTRODUCTION

MARKET

POPULATION

ACCESS

BUSINESS ENVIRONMENT

CONCLUSION

© Euromonitor International

34

The First and Most Important Step to Success

INTRODUCTION

© Euromonitor International

35

Market

Macroeconomic stability

Consumer market size and

growth

Middle class

Openness

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Access

Infrastructure

Internet

Retail landscape

Partners

Business Environment

Ease of doing business

Regulations

Corruption

Human capital

Factors Affecting Market Selection

ASSESSING MARKET POTENTIAL

PART II: CHOOSING THE RIGHT MARKET

INTRODUCTION

MARKET

POPULATION

ACCESS

BUSINESS ENVIRONMENT

CONCLUSION

© Euromonitor International

37

Market

MARKET

Market

Macroeconomic stability

Consumer market size and

growth

Middle class

Openness

Is the country sizeable and stable

enough to do business in?

Are consumers/companies well-off

enough to buy my products and

services?

Is the potential growth of the market

attractive enough to offset any risk?

Are the conditions for foreign

businesses right?

© Euromonitor International

38

Macroeconomic Stability – Look Below the Surface

MARKET

Source: Euromonitor International from IMF/national statistics/OECD

© Euromonitor International

39

There is Usually a Trade-Off Between Size and Growth

MARKET

Source: Euromonitor International from IMF/national statistics/Eurostat/OECD

© Euromonitor International

40

- 50 100 150

Panama

China

Ghana

Qatar

Ethiopia

Sierra Leone

Turkmenistan

Mongolia

Macau

Nauru

Real % growth

There is Usually a Trade-Off Between Size and Growth

MARKET

The World’s Fastest-growing Economies: 2009-2014

Source: Euromonitor International from IMF/national statistics/Eurostat/OECD

© Euromonitor International

41

Openness is Central to Success

MARKET

Trade Investment New Ideas

© Euromonitor International

42

0

40

80

120

160

UAE MalaysiaThailand Poland Qatar SaudiArabia

Mexico Chile SouthAfrica

Turkey

% o

f G

DP

Openness is Central to Success

MARKET

Trade Investment New Ideas

Total Trade as % of GDP: 2014

Source: Euromonitor International from national statistics/OECD/IMF

© Euromonitor International

43

0.0

2.0

4.0

6.0

8.0

Chile Turkmenistan

% o

f G

DP

Chile Turkmenistan

Overall

Score

78.5 41.4

Investment

Freedom

90.0 0.0

Business

Freedom

69.3 30.0

Financial

Freedom

70.0 10.0

Openness is Central to Success

MARKET

Trade Investment New Ideas

Source: UNCTAD/2015 Index of Economic Freedom, The Heritage Foundation

Note: The index is based on 10 quantitative and qualitative factors, grouped into four broad categories of economic

freedom: rule of law; limited government, regulatory efficiency, and open markets.

FDI Inflows as % of GDP: 2013 Index of Economic Freedom: 2015

© Euromonitor International

44

0% 20% 40% 60% 80% 100%

China

Russia

Brazil

India

Agree

Neither agree nor disagree

Disagree

Openness is Crucial

MARKET

Percentage of Respondents who Describe Themselves as Liking to

Try New Products and Services: 2013

Source: Euromonitor International's Global Consumer Trends Survey 2013

Note: Between 1,800-2,000 consumers in each market are surveyed

Trade Investment New Ideas

IKEA CHINA

Local FLAVOUR

Granular STRATEGY

PART II: CHOOSING THE RIGHT MARKET

INTRODUCTION

MARKET

POPULATION

ACCESS

BUSINESS ENVIRONMENT

CONCLUSION

© Euromonitor International

47

Population Matters

POPULATION

Population

Size and growth

Age structure

Vital statistics

Urbanisation

Where do my target customers live?

Where will they live in the future?

Which age segment offers most

opportunities?

Is my target audience growing and will

it continue to do so?

Is it geographically dispersed or

concentrated?

© Euromonitor International

48

Size and Growth: India and China Compared

POPULATION

247 million increase in the Indian

population to 2030

India

© Euromonitor International

49

Size and Growth: India and China Compared

POPULATION

247 million increase in the Indian

population to 2030

50 million increase in the Chinese

population to 2030

Source: Euromonitor International from national statistics/UN

India

China

© Euromonitor International

50

-10 0 10 20 30 40

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-14

5-90-4

Change in millions

9.4 million fewer children

aged 0-9 years in

2030

45%

35-54 year olds as

a % of total

population growth

Age Structure

POPULATION

Population Growth in India by Age Group: 2012-2030

Source: Euromonitor International from national statistics/UN

© Euromonitor International

51

Vital statistics - births, deaths and migration - are the building blocks of population

change.

Growth driven by migration leads to a different

demographic make-up to a population driven by

natural increase.

Life expectancy impacts consumption trends and

varies dramatically from region-to-region and even

within a region.

Life expectancy at birth in Nigeria in 2014: 53 years

Life expectancy at birth in Chile in 2014: 80 years

Vital Statistics Are…Vital!

POPULATION

Average Fertility

Rates 2014-2030

Population Change

2014-2030

Japan 1.6 -8%

UAE 1.6 +25%

Source: Euromonitor International from national statistics/UN

© Euromonitor International

52

0 20 40 60 80

Angola

Ghana

Côte d'Ivoire

Senegal

Mozambique

Tanzania

Ethiopia

Uganda

% of total population

0 20 40 60

Angola

Ghana

Côte d'Ivoire

Senegal

Mozambique

Tanzania

Ethiopia

Uganda

% of urban population

Urbanisation and City Configurations

POPULATION

Urbanisation in African

Markets of the Future: 2014

% of the Population Residing in the Largest

Cities in African Markets of the Future:

2014

Source: Euromonitor International from national statistics and

www.citypopulation.de

© Euromonitor International

53

Mexico City in Focus

POPULATION

Source: Euromonitor International from national statistics/OECD/IMF

© Euromonitor International

54

Mexico City in Focus

POPULATION

Source: Euromonitor International from national statistics/OECD/IMF

© Euromonitor International

55

Mexico City in Focus

POPULATION

Source: Euromonitor International from national statistics/OECD/IMF

PART II: CHOOSING THE RIGHT MARKET

INTRODUCTION

MARKET

POPULATION

ACCESS

BUSINESS ENVIRONMENT

CONCLUSION

© Euromonitor International

57

Access All Areas

ACCESS

Access

Infrastructure

Internet

Partners

Retail landscape

Will it be difficult to get products to market?

Are consumers easily accessible for sales,

marketing and promotional activities?

Would a local partner facilitate market

entry?

Is the retail landscape modern or

traditional?

© Euromonitor International

58

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

-

1.0

2.0

3.0

4.0

5.0

6.0

La

nd

are

a, ‘0

00

sq

. km

Qua

lity o

f in

fra

str

uctu

re, 0

-7

Quality of overall infrastructure Land area

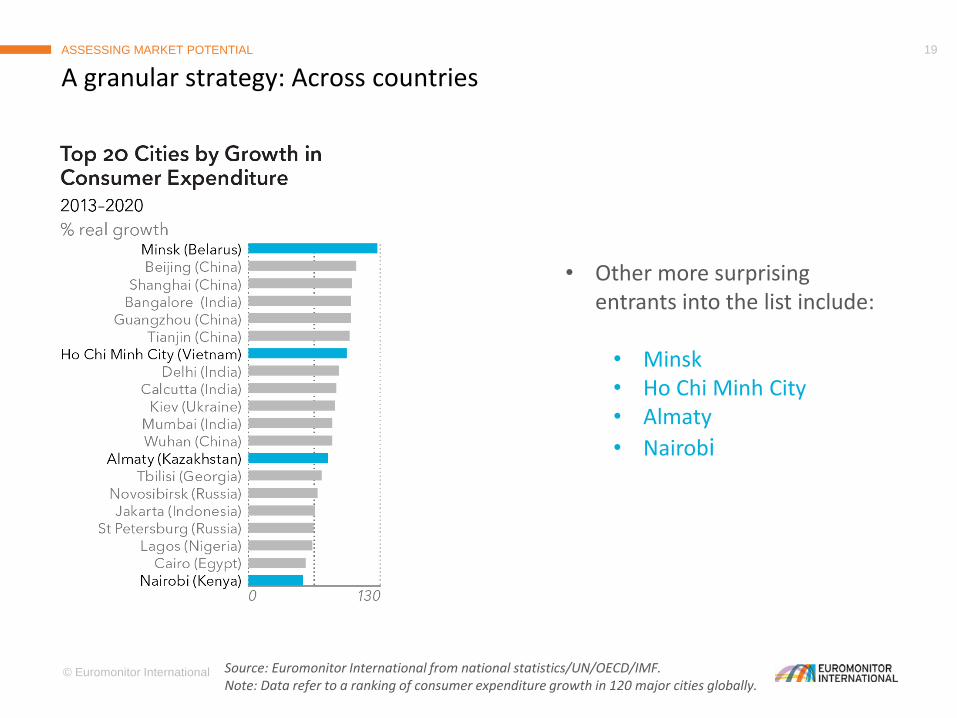

Infrastructure Can Add Significant Costs

ACCESS

Quality of Infrastructure v Land Area: 2014-2015

Source: FAOSTAT/WEF Global Competitiveness Report 2014-2015.

Note: Quality of overall infrastructure is based on responses from an executive survey.

Respondents were asked ”How would you assess general infrastructure (e.g. transport,

telephony, and energy) in your country? 1 = extremely underdeveloped; 7 = well developed and

efficient by international standards.”

© Euromonitor International

59

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

-

1.0

2.0

3.0

4.0

5.0

6.0

La

nd

are

a, ‘0

00

sq

. km

Qua

lity o

f in

fra

str

uctu

re, 0

-7

Quality of overall infrastructure Land area

Infrastructure Can Add Significant Costs

ACCESS

Quality of Infrastructure v Land Area: 2014-2015

Russia has weak

infrastructure

combined with

a huge land

area

Source: FAOSTAT/WEF Global Competitiveness Report 2014-2015.

Note: Quality of overall infrastructure is based on responses from an executive survey.

Respondents were asked ”How would you assess general infrastructure (e.g. transport,

telephony, and energy) in your country? 1 = extremely underdeveloped; 7 = well developed and

efficient by international standards.”

© Euromonitor International

60

Sharing the Risks and Rewards

ACCESS

Tata Starbucks Ltd

• Launched in Mumbai and opened its

50th store in Chennai in July 2014

• In 2013, Tata Starbucks had a 2.2%

brand share in Chained Cafés/Bars,

way behind the market leader Café

Coffee Day

• Looking at moving into second and third

tier cities

• Its alliance with Tata has enabled it to

grow its business at a faster rate than

would otherwise have been the case

Go it alone Strategic

partnership Acquisition

© Euromonitor International

61

0

5

10

15

20

25

30

% o

f to

tal re

tail

sa

les fro

m to

p 5

re

taile

rs

The Nature of Retailing

ACCESS

Concentration of Retailing Sector in Selected

Emerging Asian Economies: 2014

• Modern v traditional

retail sector

• Distribution challenges:

• Micro-distributors

• Direct distribution

Source: Euromonitor International from trade sources

Colgate CAMEROON

Distribution THREE-WHEELED MOTORCYCLES

500% INCREASE IN DELIVERIES

PART II: CHOOSING THE RIGHT MARKET

INTRODUCTION

MARKET

POPULATION

ACCESS

BUSINESS ENVIRONMENT

CONCLUSION

© Euromonitor International

64

A Business Environment Fit for Purpose

BUSINESS ENVIRONMENT

Business Environment

Ease of doing business

Regulations

Corruption

Human capital

Is there a level playing field between

domestic and foreign investors?

Is the rule of law sufficient?

How can business beat corruption?

© Euromonitor International

65

Mexico ranks 39th of 189 economies

6 days to start a business

11 days to import

85 days to get electricity

Nigeria is ranked at 170th of 189 economies

28 days to start a business

33 days to import

260 days to get electricity

Easy Does it

BUSINESS ENVIRONMENT

Source: World Bank Doing Business

© Euromonitor International

66

Regulations can be an effective barrier to entry:

Financial cost

Reduced productivity

Opportunity cost

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

Mexico Turkey Brazil Indonesia China Russia India Nigeria

Regulatory Burden can be a Barrier to Entry

BUSINESS ENVIRONMENT

Regulatory Quality Index in BRIC and MINT: 2013

Source: World Bank

Note: Regulatory quality index captures perceptions of the ability of the government to

formulate and implement sound policies and regulations that permit and promote private

sector development. The index ranges between -2.5 and 2.5 with higher values

corresponding to better governance,

© Euromonitor International

67

Corruption has an impact on:

Economic growth

FDI inflows

Business risk

A two-fold impact on business:

Subdues market demand

Supresses economic development 0.0 2.0 4.0 6.0

Russia

Nigeria

Indonesia

Mexico

China

India

Brazil

Italy

Turkey

USA

Germany

Corruption Costs

BUSINESS ENVIRONMENT

Corruption Perceptions Index in

Selected Economies: 2014

Source: Transparency International

Note: perceptions of the degree of corruption as seen by

business people and country analysts, and ranges between

10 (highly clean) and 0 (highly corrupt).

PART II: CHOOSING THE RIGHT MARKET

INTRODUCTION

MARKET

POPULATION

ACCESS

BUSINESS ENVIRONMENT

CONCLUSION

© Euromonitor International

69

The four pillar model offers methodological clarity to emerging market selection:

The first pillar, market, incorporates the most fundamental concerns of any emerging

market strategy.

Many of the most important decisions that planners must make should be shaped by

the factors within the second pillar – population.

To Sum Up

CONCLUSION

The factors within the third pillar,

access, concern the realities of

market entry.

The fourth pillar, business

environment, incorporates the

practicalities of doing business.

© Euromonitor International

70

Can you afford not to be in emerging markets? CONCLUSION

THANK YOU FOR LISTENING

Michael Pacurar

Global Director, Trade & Government

Raymond Clark

Development Executive, Trade & Government

http://blog.euromonitor.com/economic-and-consumer-insight/