submarine telecoms INDUSTRY REPORT - SubTel · PDF file9/7/2012 · 6 Key Submarine...

59

submarine telecoms INDUSTRY REPORT 2012

Transcript of submarine telecoms INDUSTRY REPORT - SubTel · PDF file9/7/2012 · 6 Key Submarine...

1

submarine te lecoms

INDUSTRYREPORT

2012

2

Submarine Cable Industry ReportIssue 1July 2012

Copyright © 2012 by Submarine Telecoms Forum, Inc.

All rights reserved. No part of this book may be used or reproduced by any means, graphic, electronic, or mechanical, including photocopying, recording, taping or by any information storage retrieval system without the written permission of the publisher except in the case of brief quotations embodied in critical articles and reviews.

Submarine Telecoms Forum, Inc.21495 Ridgetop CircleSuite 201Sterling, Virginia 20166USAwww.subtelforum.com

ISSN: applied for

3

Disclaimer:Whileeverycareistakeninpreparationofthispublication,thepublisherscannotbeheldresponsiblefortheaccuracyoftheinformationherein,oranyerrorswhichmayoccurinadvertisingoreditorialcontent,oranyconsequencearisingfromanyerrorsoromissions,andtheeditorreservestherighttoeditanyadvertisingoreditorialmaterialsubmittedforpublication.Ifyouhaveasuggestion,[email protected].

4

TableofContents

1.0 Introduction 132.0 Worldwide Market Analysis and Outlook 142.1 Connecting the Unconnected 142.2 Overview of Historical System Investment 152.3 2008 to 2012 Systems in Review 162.4 Systems Investment Beyond 2012 172.5 Decommissioning 183.0 Supplier Analysis 203.1 System Suppliers 203.2 Upgrade Suppliers 204.0 Ownership Analysis 234.1 Financing of Current Submarine Systems 234.2 Financing of Proposed Submarine Systems 235.0 Recent Events and Potential Impact on Submarine Cables 265.1 Macroeconomic Environment 265.2 Cable Protection Rules and International Water Rulings 266.0 Technology 326.1 Overview 326.2 Upgrades 326.3 Terminal Equipment 326.4 Wet Plant 336.5 Other Advances 347.0 Regional Market Analysis and Capacity Outlook 367.1 Transatlantic 36

7.1.1 Bandwidth and Capacity 367.1.2 New Systems 38

7.2 Transpacific 397.2.1 Bandwidth and Capacity 397.2.2 New Systems 41

7.3 North America-South America 427.3.1 Bandwidth and Capacity 42

5

7.3.2 New Systems 437.4 Sub-Saharan Africa 46

7.4.1 Bandwidth and Capacity 467.4.2 New Systems 48

7.5 South Asia and Middle East 487.5.1 Bandwidth and Capacity 487.5.2 New Systems 51

7.6 Australia and New Zealand 537.6.1 Bandwidth and Capacity 537.6.2 New Systems 54

7.7 Polar Route 558.0 Conclusion 58

List of Figures

Investment in New Submarine Fiber Optic Projects, 1987-2012 15Investment in New Submarine Fiber Optic Projects by Region, 2008-2012

16

Proposed Submarine Fiber Optic Projects 17Credible (“High-Activity” and “Medium-Activity”) Proposed Submarine Fiber Optic Projects by Region

18

Financing of New Submarine Fiber Optic Systems, 2008-2012 23Financing of Credible (“High-Activity” and “Medium-Activity”) Proposed Submarine Fiber Optic Projects

24

Forecasted Lit Capacity Requirement vs. Current Demonstrated Design Capacity of Transatlantic Systems

37

Forecasted Lit Capacity Requirement vs. Current Demonstrated Design Capacity of Transpacific Systems

39

Chinese International Internet Bandwidth by Operator, Year-End 2011 42

List of Tables

Civilian-Inhabited Sovereign States and Territories Without International Fiber Optic Connectivity as of Mid-2012

14

Market Share for Supply of New Submarine Fiber Optic Systems, 2012 and Beyond

20

6

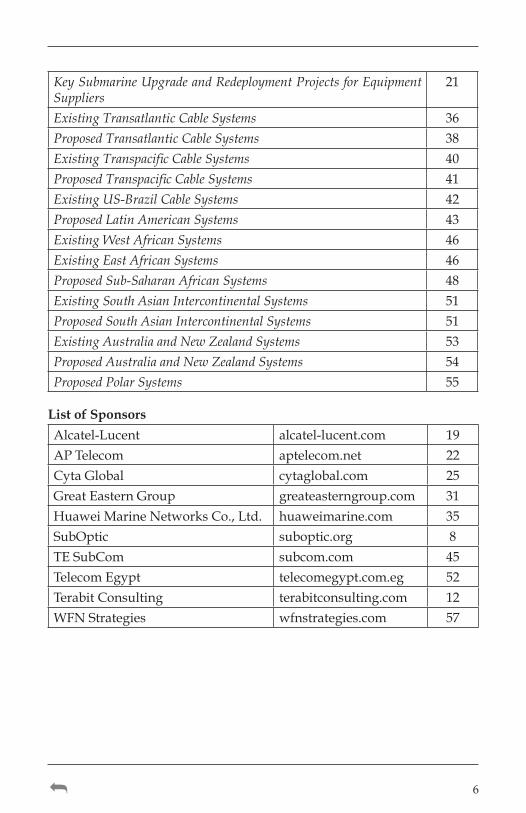

Key Submarine Upgrade and Redeployment Projects for Equipment Suppliers

21

Existing Transatlantic Cable Systems 36Proposed Transatlantic Cable Systems 38Existing Transpacific Cable Systems 40Proposed Transpacific Cable Systems 41Existing US-Brazil Cable Systems 42Proposed Latin American Systems 43Existing West African Systems 46Existing East African Systems 46Proposed Sub-Saharan African Systems 48Existing South Asian Intercontinental Systems 51Proposed South Asian Intercontinental Systems 51Existing Australia and New Zealand Systems 53Proposed Australia and New Zealand Systems 54Proposed Polar Systems 55

List of Sponsors

Alcatel-Lucent alcatel-lucent.com 19APTelecom aptelecom.net 22CytaGlobal cytaglobal.com 25GreatEasternGroup greateasterngroup.com 31HuaweiMarineNetworksCo.,Ltd. huaweimarine.com 35SubOptic suboptic.org 8TESubCom subcom.com 45TelecomEgypt telecomegypt.com.eg 52TerabitConsulting terabitconsulting.com 12WFNStrategies wfnstrategies.com 57

7

Foreword

ForanumberofyearsSubOptichasbeenlookingtoundertakeinterimactivitiesbetweenourconferenceevents,whichare typicallyheldeverythreeyears,toprovideabetterservicetoourentirecommunity

ofinterest.

Whilstwehavemaintainedtheintervalbetweenoureventsataperiodlongenoughfortheretobesignificantdevelopmentstodiscuss,wehavelongrecognisedthatanannualreportwhichprovidesasnapshotofthestateofthemanysectorswithinourindustry,couldbeofmajorinterestandvaluetoourentirecommunity,especiallyifitweretobefreelyavailable.

We are therefore very happy to support this initiative fromSubmarineTelecoms Forum along with Terabit Consulting, which we hope willprovideagood,credible indicatorofhowtheindustryisdevelopingtomeetnewchallenges,bothfromthedemandandthesupplyareas,andfromexternalfactorsbothnaturalandmanmade.

Thereare,of course, risks in trying toproducesucha report,and Iamsuretherewillbesomediscussionastowhetheritistotallyaccurateorwhetherithasmanagedtocapturethekeyactivitiesanddecisionswhicharehelpingtoshapeourindustry,whichissocriticaltotheeconomyoftheglobe.

We think, however, that the debate that such a report will stimulatecouldbegoodfortheindustryandhelptoraiseourprofileamongstthemanyoutsideourimmediatecommunity,whostilldonotrecognisehowimportantUnderseaFibreOpticCommunicationcablesaretoourglobaleconomy.

AndofcoursetherewillalwaysbethenextAnnualIndustryReportwheresuchmatterscanbeadjustedastheinevitablechangesoccur.Therewillalsobenextspring,SubOptic2013inParis,wheretheindustryasawholecomes together todiscussanddebate the futureofour industry,whichwillformthefoundation,wehope,forfutureAnnualIndustryReports.

WelldonetoSubmarineTelecomsForumfortakingthisinitiative.

FionaBeckPresident of the SubOptic Executive Committee and President and CEO of Southern Cross Cable Network

9

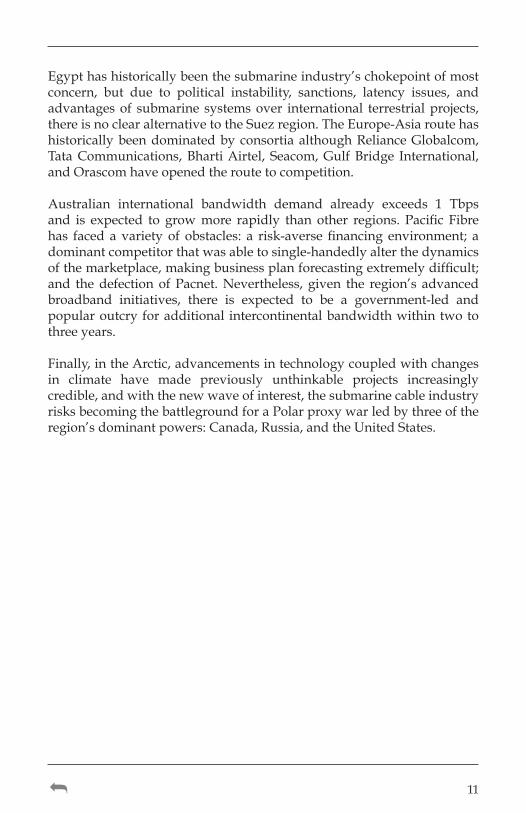

ExecutiveSummary

Astheworld has become increasingly connected since the dawnof the internet age in themid-1990s, there has been amassiveundertaking to “plug-in” every nation. As of mid-2012, only

21 nations and territories remain isolated fromfibre optic connectivity,thoughprojects areunderway inmanyof thesemarkets at the timeofthiswriting.Since2008, thesubmarinecablemarkethasbeen inanewcycle,thethirdofthefiberopticera,dominatedbycarriersinvestingindevelopingmarketssuchasAfrica,India,andChina.Approximately$10billionworthofinvestmentinnewprojectshasoccurredduringthisfive-yearperiod, and there are currently $25.6billion innewprojectsbeingactivelypursuedbyvarioussponsors.

Althoughmarketsharewassomewhatuneveninrecentyears,thenear-term outlook is more equitable, with each of four major new-systemsuppliers garnering a 20 to 25 percent share of credible projects in thenear-term.Meanwhile,capacityupgradeshavebecomeoneof themostimportantaspectsoftheindustry,providingaconsistentsourceofgrowth.

Carriers,bothinconsortiaandontheirown,havebeenthegreatestsourceof capital for cable projects, but private investors have returned andgovernment/Development Finance Institution (DFI) interest is steadilygrowing.

Macroeconomicshockshavehadremarkablylittleimpactondemandforinternationalcapacityfortheenduser,butatthecarrierlevel,theabilitytopurchasebandwidthandinvestinnewsystemshasbeenimpacted.Themostprofoundimpactofmacroeconomicdevelopmentsonthedemandfornewsystemshasbeenthetighteningofcapitalfromtheprojectfinancecommunity.Other events such as the strengthening of cable protectionlawsandthegrowingimportanceoftheUnitedNationsConventionontheLawoftheSeahavealsoimpactedthesubmarinecableindustry.

Advances in optical transmission technology have recently returnedto amore natural pattern after the burst of the dot-combubble.Manytechnologies offering the ability to increase data rate, channel countand overall capacity have come tomarket. Owners and purchasers ofsubmarinecablesystemsmustconsiderpotentialupgrades,newterminalequipmenttechnology,newwetplanttechnology,andseveralotherrecentadvances.

10

Breaking submarine investment into regions provides useful marketinsight.The transatlanticmarket is overwhelminglywholesale-orientedandwill soon have gone ten yearswithout a new, direct cable systembetweenNorthAmerica andEurope. It hasbecome commoditizedanddemocratized,butitsreputedoversupplyisnotasdireaswidelyclaimed.Thebusinesscaseforanewtransatlanticwholesalecablecontinuestobeatoughselltofinanciers;todifferentiatethemselves,newprojectsrelyonlowlatency,renewableenergysources,andtheexpansionofconnectivitybeyondNorthAmericaandWesternEurope.

The transpacific market suffered a shock with the activation of threenew systems between 2008 and 2010, andwithout new deployment, atranspacific capacity shortage is a real possibility within three years.ChinaandJapanwillbethepillarsofEastAsianbandwidthdemandasnext-generation intra-Asian systems (SJC, ASE, andAPG) will changetranspacificmarketdynamics.

TheNorthAmerica-SouthAmericacapacitymarketisheavilydependentonthreecables:GlobeNet,SAM-1,andSouthAmericanCrossing,butawaveofatleasteightnewprojectshopestochangethisdynamic.LatinAmericastill commandssomeof thehighestpremiumsofanycapacitymarket,with10GbpswavelengthsbetweenBrazilandtheUnitedStatesremainingwellover$100,000permonth.TheBrazilianmarkethasalsobeentargetedbydevelopersofinterregionalsystemsthathopetoreroutethe region’s traditional Miami-centric traffic patterns away from theUnitedStatesandtowardothermarkets.

TotalinternationalInternetbandwidthinSub-SaharanAfricais300Gbpsasof2012.Thedesigncapacityofsystemsinserviceasofyear-endwillbe15TbpsonAfrica’swestcoastand7.5Tbpsonitseastcoast.

India’s international bandwidth demand, which exceeds 1 Tbps as of2012, is the primary driver of the region’s submarine investment andIndianbandwidthdemandtotheUnitedStateshasgrownconsiderably,with India having becomeUnited States’ leading voice correspondent.Despitedecreases in extremepoverty and the expansionof themiddleclass,Indianincomeinequalityremainsasignificantobstacletogrowthofthecountry’stelecommunicationsandInternetmarkets.Althoughgrowthin Indian Internetbandwidthhasbeen strong, the sustainabilityof thisdemandwillbedependentuponincreasesinsubscribership(particularlyforbroadbandservices)whichwillonlybepossiblethroughanexpansionofconsumerspendingpower.

11

Egypthashistoricallybeenthesubmarineindustry’schokepointofmostconcern, but due to political instability, sanctions, latency issues, andadvantagesof submarine systemsover international terrestrialprojects,thereisnoclearalternativetotheSuezregion.TheEurope-AsiaroutehashistoricallybeendominatedbyconsortiaalthoughRelianceGlobalcom,TataCommunications,BhartiAirtel, Seacom,GulfBridge International,andOrascomhaveopenedtheroutetocompetition.

Australian international bandwidth demand already exceeds 1 Tbpsand is expected to growmore rapidly than other regions. Pacific Fibrehas faced a variety of obstacles: a risk-aversefinancing environment; adominantcompetitorthatwasabletosingle-handedlyalterthedynamicsofthemarketplace,makingbusinessplanforecastingextremelydifficult;and thedefectionofPacnet.Nevertheless, given the region’s advancedbroadband initiatives, there is expected to be a government-led andpopularoutcryforadditional intercontinentalbandwidthwithintwotothreeyears.

Finally,intheArctic,advancementsintechnologycoupledwithchangesin climate have made previously unthinkable projects increasinglycredible,andwiththenewwaveofinterest,thesubmarinecableindustryrisksbecomingthebattlegroundforaPolarproxywarledbythreeoftheregion’sdominantpowers:Canada,Russia,andtheUnitedStates.

The Undersea Cable Report 2013From Terabit Consulting

Publication Date: September, 2012

Intelligent intelligence -go beyond the numbers!

The most diligent quantitative and qualitative analysis of the undersea cable market - 1,600 pages of data, intelligence, and forecasts that can be found nowhere else.

Terabit Consulting analysts led by Director of International Research Michael Ruddy tell you what’s real and what’s not, where we’ve been and where we’re headed.

YOUR KEY TO UNDERSTANDING AND HARNESSING THE $20 BILLION UNDERSEA MARKET OPPORTUNITY

The Undersea Cable Report capitalizes on Terabit Consulting’s global on-site experience working with carriers, cable operators, financiers, and governments in over 70 countries on dozens of leading projects (e.g. AJC, BRICS, EASSy, Hibernia, SEAS, TBI) - a world of experience, at your fingertips in a single resource!

For more information visit www.terabitconsulting.com

Limited time re-introductory offer to celebrate the return of the Undersea Cable Report! Reserve your copy today.

SAVE 50% UNTIL SEPTEMBER 7, 2012Single-user license $10,995 limited-time re-introductory offer $5,500

Multi-user site license $24,990 limited-time re-introductory offer $12,495 Global organizational intranet licenses also available

The Undersea Cable Report 2013 is your single source of information for top-level decision-making - with the most detailed profiles, data, market analysis, and forecasts available.

• accurate, reliable data• valuable intelligence• innovative modeling• thoughtful insight• global perspective• respected expertise

• 680+ detailed undersea cable profi les • Capacity demand, capacity supply, and capacity pricing• Ownership, system supply, fi nancing, and project costs• The upgrade market • Global, region-by-region, and route-by-route analysis • Reliable, detailed forecasts

13

1.0 IntroductionWelcometothefirsteditionoftheSubmarineTelecomsIndustryReport,whichwasauthoredbythesubmarineindustry’sleadingmarketanalysisfirm, Terabit Consulting, with research overseen by Terabit’s directorof international research,MichaelRuddy. It servesas thefinal chapterin a trilogyof products beginningwith the SubmarineCableMap andincludingtheSubmarineCableAlmanac.

TheSubmarineTelecomsIndustryReportfeaturesin-depthanalysisandprognosesof thesubmarinecable industry,andservesasan invaluableresourceforallwhoareseekingtounderstandthehealthofthesubmarineindustry.Itexaminesboththeworldwideandregionalsubmarinecablemarkets, including issues such as thenew-systemandupgrade supplyenvironments,ownership,technologiesandgeopolitical/economiceventsthatmayimpactinthefuture.

Inthisreport,TerabitConsultingidentifiedmorethan$25billioninnewprojectsthatarecurrentlybeingactivelypursuedbytheirsponsors. Ofthose,more than $5 billionworth of newprojects are considered to beinanadvancedstateofdevelopmentandwell-positionedfornear-termdeployment.

Whilethecrystalballwillrarelybecompletelyclear,onefactremains–thatour150+yearoldinternationalenterprisecontinuestobeathriving,excitingandever-evolvingindustry.

Ouraimistomakethisinformationastimelyandavailableaspossible.Asalways,wefeelthataninformedindustryisaproductiveindustry.

14

2.0 Worldwide Market Analysis and Outlook

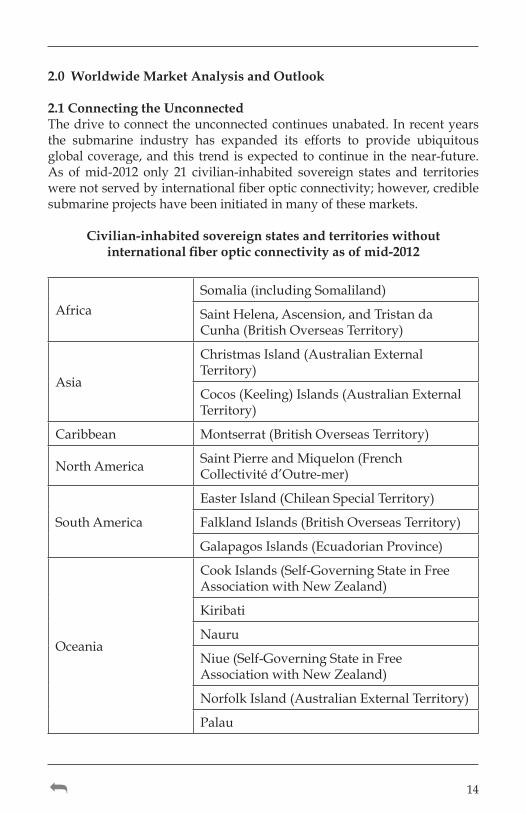

2.1 Connecting the UnconnectedThedrivetoconnecttheunconnectedcontinuesunabated.Inrecentyearsthe submarine industry has expanded its efforts to provide ubiquitousglobalcoverage,andthis trendisexpectedtocontinue in thenear-future.As ofmid-2012 only 21 civilian-inhabited sovereign states and territorieswerenotservedbyinternationalfiberopticconnectivity;however,crediblesubmarineprojectshavebeeninitiatedinmanyofthesemarkets.

Civilian-inhabited sovereign states and territories without international fiber optic connectivity as of mid-2012

AfricaSomalia(includingSomaliland)

SaintHelena,Ascension,andTristandaCunha(BritishOverseasTerritory)

Asia

ChristmasIsland(AustralianExternalTerritory)

Cocos(Keeling)Islands(AustralianExternalTerritory)

Caribbean Montserrat(BritishOverseasTerritory)

NorthAmerica SaintPierreandMiquelon(FrenchCollectivitéd’Outre-mer)

SouthAmerica

EasterIsland(ChileanSpecialTerritory)

FalklandIslands(BritishOverseasTerritory)

GalapagosIslands(EcuadorianProvince)

Oceania

CookIslands(Self-GoverningStateinFreeAssociationwithNewZealand)

Kiribati

Nauru

Niue(Self-GoverningStateinFreeAssociationwithNewZealand)

NorfolkIsland(AustralianExternalTerritory)

Palau

15

Oceania

PitcairnIslands(BritishOverseasTerritory)

SolomonIslands

Tokelau(NewZealandDependentTerritory)

Tonga

Vanuatu

WallisandFutuna(FrenchCollectivitéd’Outre-mer)

2.2 Overview of Historical System InvestmentByyear-end2012therewillhavebeen$56.1billionworthofinvestmentinfiberopticsubmarinesystems,comprising1.253millionroutekilometers.Overits25-yearhistorythemarketwillhaveaveraged$2billionworthofinvestmentand48,200kilometersofdeploymentperyear.

Investment in New Submarine Fiber Optic Projects, 1987-2012(Including Projects Under Construction) ($Millions by RFS Date)

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

16

Submarine cable deployment can be broken down into three distinctcycles:

1. The first, lasting ten years from 1987 to 1997, marked the adventof transoceanic fiber optic communications and a predictable,consortium-dominatedmarket.

2. The second cycle was characterized by unprecedented levels ofinvestmentfrom1998to2002,fueledbythedawningoftheInternetandWDMerasandthearrivalofspeculativeinvestment,followedbyadisastrousmarketcollapsethat ledtowhatwaseffectivelyafive-yeardormancyofthemarket.

3. Thethirdcycle,lastingfrom2008tothepresent,representstheeraofcarrier-dominatedinvestmentindevelopingmarkets.Todate,mostofthatinvestmenthasbeendirectedtowardAfrica,India,andChina.

2.3 2008 to 2012 Systems in ReviewDuring thefive-yearperiod from2008 toyear-end2012 therewillhavebeenapproximately$10billionworthofinvestmentinnewprojects,foranaverageof$2billionand54,000routekilometersperyear.Morethantwo thirds of that investment has been in three regions: Sub-SaharanAfrica,SouthAsiaandtheMiddleEast,andthetranspacific,withmostinvestmenttargetedtowardthe“anchor”marketsofSouthAfrica,India,andChinarespectively.

Investment in New Submarine Fiber Optic Projects by Region, 2008-2012

Africa32%

South Asia/Middle East19%

Transpacific17%

Europe/North Africa

9%

East Asia8%

Australia4%

South Pacific4%

Latin America/Caribbean

4%

North America3%

17

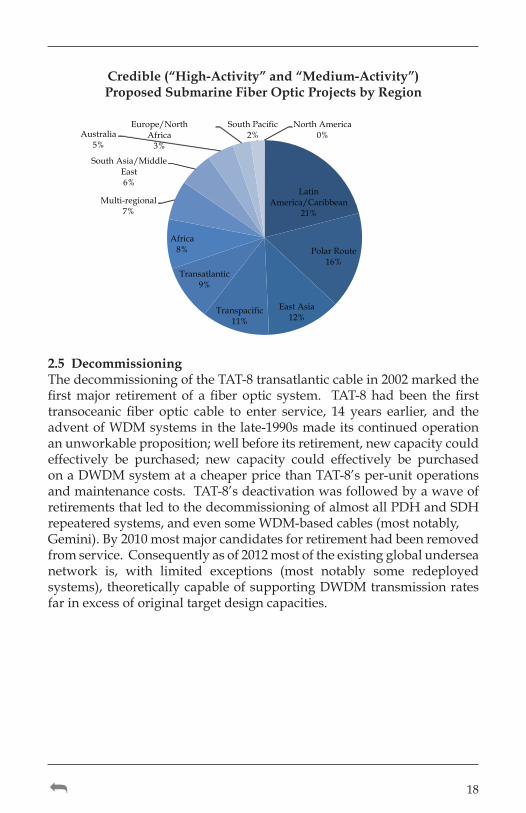

2.4 Systems Investment Beyond 2012TerabitConsultingidentifiedatotalof$25.6billioninnewprojectsthatarecurrentlybeingactivelypursuedbytheirsponsors.Theseprojectswereeach classified into one of three categories: “HighActivity,” “MediumActivity,”and“LowActivity”basedonvariouscriteriaincludingsupplycontracts, funding, licenses,carriercommitments,marketopportunities,marinesurveys,desktopstudies,andfeasibilitystudies.

Theanalysisfoundthatapproximately$5billionworthofprojectscanbeconsidered tobe in an advanced state ofdevelopment (“HighActivity”)and an additional $15 billion havemade significant progress (“MediumActivity”).Afurther$5.6billionworthofprojectswereconfirmedasbeingunderseriousconsiderationbuthadyettodemonstratetheirtruecredibility.

TerabitConsultingalsoclassifiedmorethan$25billionworthofprojectsaseitherofficiallyoreffectively“cancelled.”

Proposed Submarine Fiber Optic Projects (Excluding Systems Under Construction) ($Millions)

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

High Activity Projects Medium Activity Projects Low Activity Projects

Credibleproposedinvestment,i.e.projectsfallingintothe“HighActivity”and“MediumActivity”categories,ischaracterizedbythewhatwouldbethegreatestgeographicdiversityofinvestmentinthesubmarinemarketsinceitsinception,withatleastthree-quartersdirectedtowarddevelopingmarketsandnewroutes.

18

Credible (“High-Activity” and “Medium-Activity”) Proposed Submarine Fiber Optic Projects by Region

Latin America/Caribbean

21%

Polar Route16%

East Asia12%

Transpacific11%

Transatlantic9%

Africa8%

Multi-regional7%

South Asia/Middle East6%

Australia5%

Europe/North Africa

3%

South Pacific2%

North America0%

2.5 DecommissioningThedecommissioningoftheTAT-8transatlanticcablein2002markedthefirstmajor retirementof afiberoptic system. TAT-8hadbeen thefirsttransoceanic fiber optic cable to enter service, 14 years earlier, and theadventofWDMsystemsinthelate-1990smadeitscontinuedoperationanunworkableproposition;wellbeforeitsretirement,newcapacitycouldeffectively be purchased; new capacity could effectively be purchasedonaDWDMsystematacheaperpricethanTAT-8’sper-unitoperationsandmaintenancecosts.TAT-8’sdeactivationwasfollowedbyawaveofretirementsthatledtothedecommissioningofalmostallPDHandSDHrepeateredsystems,andevensomeWDM-basedcables(mostnotably,Gemini).By2010mostmajorcandidatesforretirementhadbeenremovedfromservice.Consequentlyasof2012mostoftheexistingglobalunderseanetwork is, with limited exceptions (most notably some redeployedsystems),theoreticallycapableofsupportingDWDMtransmissionratesfarinexcessoforiginaltargetdesigncapacities.

Realizing the potential of a connected world

Realizing the potential of a connected world

20

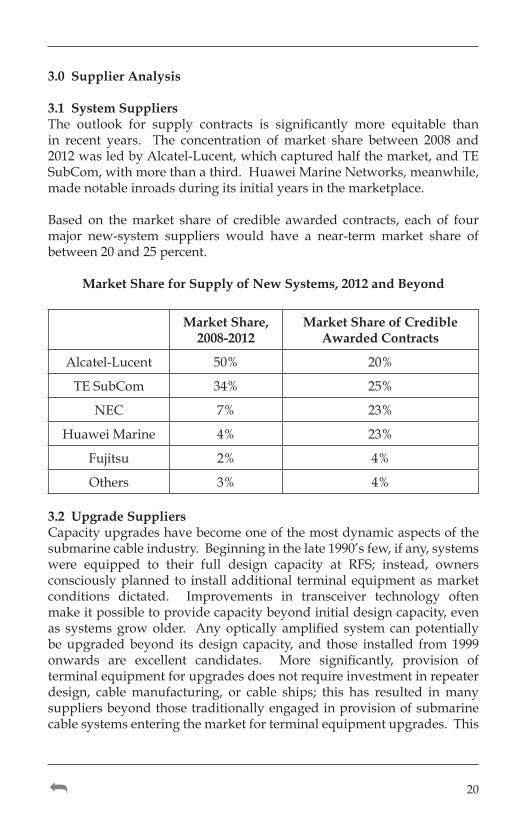

3.0 Supplier Analysis

3.1 System SuppliersThe outlook for supply contracts is significantly more equitable thanin recent years. The concentration ofmarket share between 2008 and2012wasledbyAlcatel-Lucent,whichcapturedhalfthemarket,andTESubCom,withmorethanathird.HuaweiMarineNetworks,meanwhile,madenotableinroadsduringitsinitialyearsinthemarketplace.

Based on themarket share of credible awarded contracts, each of fourmajor new-system suppliers would have a near-term market share ofbetween20and25percent.

Market Share for Supply of New Systems, 2012 and Beyond

Market Share, 2008-2012

Market Share of Credible Awarded Contracts

Alcatel-Lucent 50% 20%

TESubCom 34% 25%

NEC 7% 23%

HuaweiMarine 4% 23%

Fujitsu 2% 4%

Others 3% 4%

3.2 Upgrade SuppliersCapacityupgradeshavebecomeoneofthemostdynamicaspectsofthesubmarinecableindustry.Beginninginthelate1990’sfew,ifany,systemswere equipped to their full design capacity at RFS; instead, ownersconsciouslyplannedto installadditional terminalequipmentasmarketconditions dictated. Improvements in transceiver technology oftenmakeitpossibletoprovidecapacitybeyondinitialdesigncapacity,evenas systemsgrowolder. Anyopticallyamplified systemcanpotentiallybeupgradedbeyond its design capacity, and those installed from1999onwards are excellent candidates. More significantly, provision ofterminalequipmentforupgradesdoesnotrequireinvestmentinrepeaterdesign, cablemanufacturing, or cable ships; this has resulted inmanysuppliersbeyondthosetraditionallyengagedinprovisionofsubmarinecablesystemsenteringthemarketforterminalequipmentupgrades.This

21

dynamicmaybeuncomfortableforsomesuppliers,buthas let tosomestrikingbenefitsforsystemowners.

The upgrademarket and its technology suppliers are a relatively newniche to the industry, increasing the utility and longevity of a numberof submarine cable systems. Several key submarine upgrades andredeploymentshavebeenaccomplishedinrecentyears,encompassinginscopebothregionalandtransoceanicsystems.

The upgrademarket,meanwhile,will arguably be themost consistentsourceofgrowthandhasbeentargetedbyfourequipmentsuppliers,inadditiontothetraditionalsubmarinesystemsuppliers.

Key Upgrade and Redeployment Projects for Equipment Suppliers

Ciena Southern Cross Cable Network, TGN Atlantic, Japan-USCableNetwork,NorthAsianLoop,Australia-JapanCable,FLAGEurope-Asia

Infinera PacificCrossing-1,NorthAsianLoop,Transatlanticcable,MedNautilus,Kodiak-Kenai,Pacnet

Mitsubishi Asia-AmericaGateway,TAT-14

Xtera EAC/C2C,AC-1, Gulf Bridge International, GlobeNet,Arcos,PAC,SHEFA-2,GOKI,Columbus-2,Columbus-3,GeminiBermuda,C-BUS,East-WestCable

23

4.0 Ownership Analysis

4.1 Financing of Current Submarine SystemsThe financing of current submarine systems consists of consortium,carrier,investorandgovernmentbackedmodels.Projectsledbycarrierspredominate, but private investors have returned and government/DevelopmentFinanceInstitution(DFI)interestissteadilygrowing.Also,despiteglobalfinancialuncertainty,thereare$8billionworthofcredibleinvestor-ledprojectfinanceopportunitieson the table in thesubmarinemarket.

From2008to2012four-fifthsofprojectswerefinancedbycarriers,eitheralone,insmallgroups,orinlargeconsortia,asprivateinvestorsremainedcautious.Governmentsanddevelopmentfinancialinstitutionsincreasedtheirshareoffundingto5percentofallprojects.

Financing of New Submarine Fiber Optic Systems, 2008-2012

Consortium49%

Carrier32%

Investor14%

Government/DFI5%

4.2 Financing of Proposed Submarine SystemsOfthe$20billionincredibleprojects,roughlyhalfwouldbefinancedbycarriers,and interestamonggovernmentandDFIsources is increasing.Notably,40percent,or$8billionofcredibleproposedprojectswouldbefinanced by private sources, although privately-financed projects alsoshowthegreatestriskofnotcomingtofruition.

24

Financing of Credible (“High-Activity” and “Medium-Activity”) Proposed Submarine Fiber Optic Projects

Investor40%

Consortium33%

Carrier16%

Government/DFI6%

Other (Research Networks, Suppliers,

etc.)5%

26

5.0 Recent Events and Potential Impact on Submarine Cables

5.1 Macroeconomic EnvironmentThe global economic environment’s impact on the submarine industryisincreasinglycomplex.Attheend-userdemandlevel,macroeconomicshocks have had remarkably little impact on demand for internationalcapacity.Atthecarrierlevel,however,theyhaveunquestionablyimpactedcarriers’abilitytopurchasebandwidthaswellascarriers’propensitytoinvestinnewsystems.Butthemostprofoundimpactofmacroeconomicdevelopments on the demand for new systems (i.e. from the supplierperspective) has been the tighteningof capital from theprojectfinancecommunity.

Increasingly,theindustryhassoughttotemperthiseffectbylookingtomorestable,alternativesourcesofcapital,particularlyfromdevelopmentfinancialinstitutions,andbyshiftingitsattentiontowardareasofgrowthin the developing world. Nevertheless the submarine industry willundoubtedlyfeeltheimpactoftheEuropeansovereign-debtcrisis,mostimmediatelyinthegrowingreluctanceoftheprivatefinancecommunitytofundsubmarineprojects.

5.2 Cable Protection Rules and International Water RulingsThe rulesgoverning the survey, installation,maintenanceand repairofsubmarine cableswithin territorialwaters aredefinedby the sovereignstategovernmentsconcerned. WithinExclusiveEconomicZones (EEZ)andoutintointernationalwaterstheyarecoveredbytheUnitedNationsConventionontheLawoftheSea(UNCLOS).IntheEEZ,theUNCLOSArticles 58 & 113 – 115 apply; in international waters the relevant theUNCLOSArticlesare86,87&112–115.Todate162countriesplustheEuropeanUnionhavesignedtheconvention,althoughanumberhavestilltoratifyit.MostnotableoftheseisUnitedStateswhichonlyrecognizestheUNCLOSasacodificationof“customaryinternationallaw”.

In thepastdecade the importanceof international submarine cables toworldtradeandindividualcountryeconomieshasgrownexponentially,as connection to the internet has become a prerequisite for conductingbusiness. Major disruptions to the submarine network and the failureof the internet, asexemplifiedby theHengchunsubseaearthquake,offTaiwan,in2006,hasincreasedpressureongovernmentsaroundtheworldtorecognizetheimportanceofsubmarinecablesandtheneedtoimprovelegislationfortheirimplementationandprotection.

27

Atthe65thSessionoftheUNGeneralAssembly,on29thofMarch2010,the Secretary-General addressed the subject of the world’s submarinecablenetworks. Inhisreporthestated:“Submarinecables.Aneedhasbeen expressedby someStates, including in recentworkshops, to con-sidergapsintheexistinglegalregimeregardingsubmarinecablesattheinternationalandnational levels, inparticular in the implementationofarticle113oftheUnitedNationsConventionontheLawoftheSea.Viewshavebeenexpressed that thecurrent legal regime isnotadequatewithrespecttotheoperationof,andthreatsto,submarinecables.Inparticular,aneedforacodeofbestpracticeswithregardtothelayingandrepairofsubmarinecablesandtheconductofcableroutingsurveyswasmentioned,amongotherthings.Inthatcontext,aneedforcapacitybuildingactivitiesfacilitatingthereviewofthelegalregimeandpossiblegapsthereincouldbeconsidered.”

Following this report, in 2010, the International Cable ProtectionCommittee (ICPC) announced that it had changed its rules to allownational governments and companies that were key players in thesubmarinecableindustrytoberepresentedwithinitsmembership.TheICPC’sstatedobjectiveinmakingthischangewastofosterimprovedco-operationbetweengovernmentandindustry,whichwasdeemedessentialtoenhancethesecurityofsubmarinecablesworldwide.

FromstudiesconductedbyICPCandothers,followingsuchdisruptionsastheHengchunearthquake,akeyfactorthatemergedwasthatnationalgovernments were often in the critical path for the installation of andremedialworktosubmarinecables.Itwasthereforeanticipatedthathavinggovernments represented within the ICPC would facilitate improvededucation and awareness, strengthening of legislative protections andrightsforcableowners,inaccordancewiththeUNCLOS.Thelatterwasconsideredessentialtohelpeliminatepermittingdelaysandtofacilitateprovisionofurgentassistanceintheeventthatthesecurityofasubmarinecablewasthreatenedbyillegalaction.

InDecember 2010, theUnitedNationsGeneralAssembly approved anOmnibusResolutionontheOceansandLawoftheSea.Forthefirsttimethisresolutionrecognizedthecriticalimportanceofsubmarinecablestotheglobaleconomyandthesecurityofnations. Italsorecognizedthattheyaresusceptibletoaccidentalandintentionaldamage.Theresolutionwas originally proposed by the Singaporean Government and wassupportedbydiplomats fromothercountrieswhohadbeenbriefedbytheirrespectiveICPCMembers.

28

Importantly, the resolution called for states to takemeasures toprotectcables, in accordance with international law. It encouraged greaterdialogueandcooperationbetweenstatesandrelevantregionalandglobalorganizations to promote the security of the critical communicationsinfrastructure.However, theUNprocess requiresunanimity among allmember countries for any provision to be included, and further hardworkwasrequiredtoeducatethediplomatsastotheimportanceoftheresolutionlanguageonsubmarinecables.

In the autumnof 2011, the nationmembers of theUNmet once againto define the Omnibus Resolution on Oceans and the Law of the Sea.The result of this meeting was another positive step forward. In the2011 Omnibus Resolution on Oceans and the Law of the Sea, for thefirst time, the inclusionof theword“repair”wasagreedbyallnationstobe included in the textconcerningmaintenanceofsubmarinecables.However, theproposed languageonexpeditingrepairs in theEEZwasdilutedinordertobeacceptabletosomenations.Theagreedlanguagestatesthatrepairsshouldbecompletedinaccordancewithinternationallawwithout reference tomaritime boundaries. The resolution stronglyencouragesnationstoimplementorupdatenationallawstoprotectcablesinfulfilmentofnationalobligationsundertheUNCLOS.

Therelevantlanguagefromthe2011OmnibusResolutiononOceansandtheLawoftheSeaisasfollows:

PP22: Recognising that fibre optic submarine cables transmit most of the world’s data and communications and, hence, are vitally important to the global economy and the national security of all States, conscious that these cables are susceptible to intentional and accidental damage from shipping and other activities, and that the maintenance, including the repair, of these cables is important, noting that these matters have been brought to the attention of States at various workshops and seminars, and conscious of the need for States to adopt national laws and regulations to protect submarine cables and render their wilful damage or damage by culpable negligence punishable offences,

OP 121a: Calls upon States to take measures to protect fibre optic submarine cables and to fully ad-dress issues relating to these cables, in accordance with international law, as reflected in the Convention;

OP 121b: Encourages greater dialogue and cooperation through workshops and seminars among States and the relevant regional and global organizations

29

on the protection and maintenance of fibre optic submarine cables to promote the security of such critical communications infrastructure;

OP 121c: Encourages the adoption by States of laws and regulations addressing the breaking or injury of submarine cables or pipelines beneath the high seas done wilfully or through culpable negligence by a ship flying its flag or by a person subject to its jurisdiction, in accordance with international law, as reflected in the Convention;

OP 121d: Affirms the importance of the maintenance, including the repair, of submarine cables, undertaken in conformity with international law, as reflected in the Convention; This language clearly and specifically encourages Nation States to adopt laws and regulations addressing obligations to enact modern domestic laws under UNCLOS article 113 and for the first time uses the word “repair” in the text.

However, as the final language on repair is the result of compromiserequiredbyvariousnations,it isunderstoodthatICPCwillcontinuetosupportcontinuedeffortsbySingaporeandotherlike-mindednationsinanattempttoexpandthelanguageintheresolutiontoincludeexpeditiousrepairswhentheUNmeetsagaintodefinetheOmnibusResolutiononOceansandtheLawoftheSeain2012.

TheAustralianGovernmenthasbeenanearlyadopteroflegislationrelatedtosubmarinecables,itwasoneofthefirstsignatoriestotheUNCLOS,whichcameintoforcein1994,andisthefirstgovernmenttobecomeamemberof ICPC. TheAustralianTelecommunicationsAct (1997) coversunderSchedule3AalltheprinciplesoftheUNCLOS;inparticular,Schedule3AempowerstheAustralianCommunicationsandMediaAuthority(ACMA)thatadministerstheacttoestablishProtectionsZonesaroundsubmarinecables.However,the1997Actisdesignedonlytoaddressinternationalanddomestic submarine ‘telecommunication’cables. At the timeof itsdrafting the legislators did not have in contemplation the offshoreOil&Gas industry that has since emerged. Muchof the continental shelfaroundAustraliaisrichinoilandnaturalgasandoverthenextdecade,major offshore production facilities will be constructed, outside ofterritorialwatersbutwithintheAustralianEEZ.Submarinefibreopticcables,betweentheseplatformsandthemainlandwillbeessentialtotheiroperation. TheAustralianGovernmenthasenactedlegislationtocovertheseoffshoreproductionfacilitiesintheformoftheOffshorePetroleumandGreenhouseGasStorageAct(2006)(OPGGSA);unfortunately,onceagainitdoesnotaddresssubmarinecables.TheOPGGSAisadministered

30

by the Department of Resource, Energy and Tourism. TheAustralianGovernmenthasadilemmatoresolveinthenextyearorsoastowhichlegislationshouldbeapplicabletothesetypesofcablesandhowthiswillapplyifthecableisownedbyanAustraliancarrierprovidingaservicetotheOil&GascompanyorthecableisanintegralpartoftheoffshorefacilityownedandoperatedbytheOil&Gascompany.

LikeAustralia,manynationstateshave,orareintheprocessof,dividingtheir EEZ into leasable blocks for Oil & Gas exploration and laterproduction. The challenge in drafting the legislation for the necessaryleases and licences will be to protect the rights of the lessee whilemaintainingtherequirementsoftheUNCLOStoallowsubmarinecablesfree access to cross these blocks andpermitmaintenance and repair ofcableswithin the blocks,when required. TheAustralianGovernmentmay well be leading the way in developing appropriate legislation toprotectsubmarinetelecommunicationscableandwillshortlyneedtore-address this legislation,as it relates tosubmarinecable for theoffshoreOil&Gasindustry.Therefore,anopportunityexistsforrestoftheworldtoconsidertheAustralianapproach,learnfromitandwhereappropriateadopttheirrulesandregulations.

32

6.0 Technology

6.1 OverviewAdvancesinopticaltransmissiontechnologyexperiencedabriefhiatusintheaftermathofthedot-combubble,buthaverecentlyreturnedtoamorenaturalpattern.Theperiodfrom2009to2010sawmanylabexperimentsdemonstratingincreasesindatarate,channelcountandoverallcapacity,soitisnosurprisethatthreeyearslaterweseemanyofthesecapabilitiescomingtomarket. Ownersandpurchasersofsubmarinecablesystemsmustconsiderpotentialupgrades,newterminalequipment technology,newwetplanttechnology,andseveralotherrecentadvances.

6.2 UpgradesUpgrades may utilize 10Gb/s, 40Gb/s or 100Gb/s transmissiontechnology. 10Gb/stranspondersmaybeusedwhenlowcostorrapiddeploymentisrequired;typicallyfrom1to1½timestheoriginaldesigncapacitymaybeachieved; forexampleasystemdesignedfor32wavesperfiberpairmightbeexpandedto40or48waves. 40Gb/supgradeshavebeenoffered forseveralyears,butarerapidlybeingovertakenby100Gb/s upgrades. 40Gb/s upgradesmay deliver 2 to 2 ½ times theoriginaldesigncapacity;itisnotusuallypossibletoreplaceeach10Gb/schannelwitha40Gb/schannel,thustheimprovementfactorislessthan4.100Gb/supgradeshaverecentlybeenannounced,withthepotentialtoachieve4timestheoriginaldesigncapacityonsomewetplant.

Ownersmay choose from these solutions tomeet their specific needs:maximizingcapacity,rapiddeployment,lowestcostorsomecombination.The exact results depend on amplifier bandwidth, equalization, thechromatic dispersion map, and other factors. A typical upgrade willinvolveteststocharacterizeafiberpairfollowedbytrialsoftheequipmentbefore a supplier commitment is made. Many upgrade designs nowpermitnewchannelstobeaddedalongsideexistingchannels,avoidingtheneedtoremoveexistingterminalequipmentfromservice.

6.3 Terminal EquipmentBoth40Gb/sand100Gb/sterminalequipment isnowbeingofferedbysystem suppliers. 10Gb/s continues to be offered to support existingcustomers andwheremarket demanddoes not yet justify the jump tohigher bit rates. 40Gb/s equipment is immediately available andmaynowbeconsideredmainstream.Therearesigns,however,that40Gb/swillquicklybesupersededby100Gb/s.Theadoptionof100Gb/stechnologyin terrestrial networks and pressure from non-traditional suppliers

33

willdrive thedeployment of 100Gb/s technologyon submarine cablesystems.Theuseof100Gb/sclientsignalswillfurthercement100Gb/sasthestandardbitrateforthenextgenerationofcablesystems.

Theadvances in terminal equipment technologyachievedover the lastfewyearsinclude:

• Coherentdetectiontoimprovereceiversensitivity

• Quadrature Phase Shift Keying (QPSK) tomodulate 2 bits persymbol

• Increasesinthebaudrateto14or28Gbaud(symbolspersecond)

• Digitalsignalprocessingofthereceivedsignaltopermitpartialcompensation of linear impairments in the electrical domainreducingtheneedforexternaldispersioncompensation

• Dualpolarizationtotransmittwosignalsperwavelength

• Frequency division multiplexing, in which two closely spacedopticalchannelsoccupyasingle50GHzchannelslot

• ImprovedForwardErrorCorrection(FEC)algorithms

40Gb/s systems typically employ several of these, while 100Gb/stransceiversmustusealmostallofthem.(Ifallwereused,theresultingbitratewouldbe200Gb/s.)

To achieve high channel counts over trans-oceanic distances, someadditionalimprovementswillbeadded;thesemayincludefurtherchangestothemodulationformatandfullcompensationaccumulatedCD.

6.4 Wet Plant TechnologyImprovementsintransceiverdesigncanincreasethecapacityofexistingwetplant.However,themostdramaticbenefitscanbeachievedthroughsynergiesbetweentransceiverandwetplantdesign.Theabilitytoperformdispersioncompensationintheelectricaldomaineliminatestheneedfordispersionmanagementintheopticalline.Thisinturnpermitstheuseofhigheffectivearea,lowlossfiberwhichreducesnon-linearimpairmentsandimprovesend-to-endperformance.Systemsusingcoherentdetectionand suitably optimized wet plant will support 80 or more 100Gb/schannels,or8Tb/s,perfiberpairovertrans-Pacificdistances.

34

The need for additional capacity, opportunities to reducemaintenancecosts, and the age of existing systemsmeans that a new round ofwetplantinstallationonmajortrans-oceanicrouteswilleventuallybeneeded.Whenthattimecomes,thestageissetforcapacitiestentimesgreaterthanthoseavailablepreviously.

6.5 Other AdvancesAmongthemanychangesintechnology,twootheradvancesareworthyofnote.Thefirstisanewclientinterfacestandardintheformof40Gb/sand 100Gb/s Ethernet. As with previous generations of technology,muxponders will fill the gap between the adoption of new line sideinterfacesandtheavailabilityofclientinterfaces.Routerswith100Gb/sinterfaces entered field trials by mid 2011, so widespread adoption isprobablystillayearorsoaway.Nevertheless,as100Gb/sbecomesmoreprevalent,100Gb/sEthernetislikelytobetheclientinterfaceofchoice.IEEE802bawasratifiedinJune2010andupdatedinMarch2011.40Gb/sand100Gb/sEthernetinterfacesareavailableinformatsforcoppercable,multi-modefiberandsinglemodefiber.

The second advance of note is Reconfigurable Optical Add DropMultiplexers (ROADM). ROADM have seen adoption in terrestrialnetworksandarenaturallysuitedtomanagingcapacityonatrunkandspurconfiguration commonly encountered in submarinenetworks. The risksandchallengesassociatedwithanynewwetplanttechnologyshouldnotbeunderestimated,howeverROADMisatechnologythatbearswatching.

36

7.0 Regional Market Analysis and Capacity Outlook

7.1 Transatlantic

7.1.1 Bandwidth and CapacityNo transoceanicmarket has experienced amore precipitous decline ininvestmentthanthetransatlanticmarket,whichiscurrentlyenduringitslongestdeploymentdrought inhistory. Between1993and2003,anewtransatlanticcablesystementeredserviceeverytenmonths,onaverage.Bythetimethenexttransatlanticcablesystemisactivated,themarketwillhavegonemorethanadecadewithoutanew,directcablesystem.

Existing Transatlantic Cable Systems

RFS System Owner(s)

1999 AtlanticCrossing-1(AC-1) Level3

1999 Columbus-3 Internationalconsortiumofcarriers

2000Yellow(Level-3)/AtlanticCrossing-2(AC-2)

Level3

2000 Atlantis-2 Internationalconsortiumofcarriers

2001 FLAGAtlantic-1(FA-1) RelianceGlobalcom

2001 HiberniaAtlantic ColumbiaVenturesCorp.

2001 TAT-14 Internationalconsortiumofcarriers

2001 TGN-Atlantic TataCommunications

2003 Apollo Cable&Wireless/Alcatel-Lucent

ThesevenlitDWDMsystemsbetweenNorthAmericaandEuropeareownedbysixentities:ApolloSCSLtd.(a jointventurebetweenCable&WirelessWorldwideandAlcatel-Lucent),Level3(formerlyGlobalCrossing,whichoperatestwosystems),HiberniaAtlantic(an85-percentownedsubsidiaryofColumbiaVentures),RelianceGlobalcom,TataCommunications,andtheTAT-14consortium.Consequently,thetransatlanticmarketcanbedescribedas an overwhelmingly “wholesale” market, where operators have optedto lease capacity from network operators (as opposed to making directinvestmentintheirowncapacityinfrastructure).

37

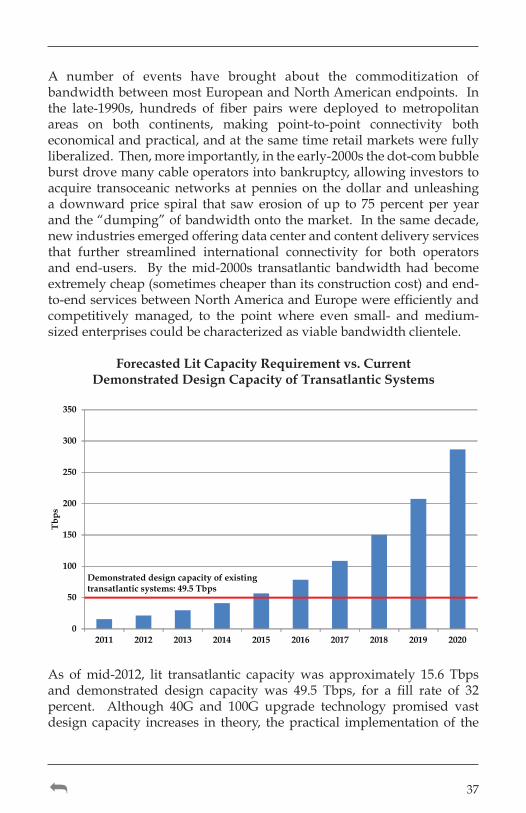

A number of events have brought about the commoditization ofbandwidthbetweenmostEuropeanandNorthAmericanendpoints.Inthe late-1990s, hundreds of fiber pairs were deployed to metropolitanareas on both continents, making point-to-point connectivity botheconomicalandpractical,andatthesametimeretailmarketswerefullyliberalized.Then,moreimportantly,intheearly-2000sthedot-combubbleburstdrovemanycableoperatorsintobankruptcy,allowinginvestorstoacquire transoceanicnetworks at pennies on thedollar andunleashingadownwardprice spiral that sawerosionofup to 75percentperyearandthe“dumping”ofbandwidthontothemarket.Inthesamedecade,newindustriesemergedofferingdatacenterandcontentdeliveryservicesthat further streamlined international connectivity for both operatorsand end-users. By themid-2000s transatlantic bandwidth had becomeextremelycheap(sometimescheaperthanitsconstructioncost)andend-to-endservicesbetweenNorthAmericaandEuropewereefficientlyandcompetitively managed, to the point where even small- and medium-sizedenterprisescouldbecharacterizedasviablebandwidthclientele.

Forecasted Lit Capacity Requirement vs. Current Demonstrated Design Capacity of Transatlantic Systems

0

50

100

150

200

250

300

350

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Tb

ps

Demonstrated design capacity of existing transatlantic systems: 49.5 Tbps

As ofmid-2012, lit transatlantic capacitywas approximately 15.6 Tbpsand demonstrated design capacity was 49.5 Tbps, for a fill rate of 32percent. Although 40G and 100G upgrade technology promised vastdesign capacity increases in theory, thepractical implementationof the

38

technology in ten- to fifteen-year old systems has not shown uniformsuccess, and even themost optimistic estimates of transatlantic designcapacity using existing systemsdo not exceed 80 Tbps. Consequently,therequiredleveloflittransatlanticcapacityisforecastedtoexhaustthedesigncapacityofexistingsystemswithinthreetofouryears.

7.1.2 New SystemsConsortia of operators were rumored to have been considering theconstructionofaTAT-15systemasearlyas2002,andthefirsttenyearsofinconclusivediscussionsseemtohaveservedprimarilyasanongoingpressuretacticonwholesalerstolowerprices.Withpriceerosionhavingleveled off at between 10 and 15 percent annually and the long-termviabilityofTAT-14 inquestion,aclearercasecanbemade that tier-oneoperatorsoughttoinvestdirectlyintheirowninfrastructureratherthancontinuepurchasingbandwidthfromwholesalers.

Planned Transatlantic Fiber Systems(Europe to the Americas)

System Owner(s)

ACSea-EURCableSystem Telebras

EmeraldExpress EmeraldNetworks

EuropeLinkwithLatinAmerica(ELLA) Researchcommunity

ProjectExpress ColumbiaVenturesCorp.

TransatlanticConsortiumSystem/TAT-15 Internationalconsortiumofcarriers

WASACENorth WASACECableCompany

Although financiers have shown continued commitment to submarineinvestments in general, they have shown a strong aversion to thetransatlantic bandwidth market since its meltdown and subsequentcommoditization in the early-2000s. In an effort to attract privateinvestmentandovercomethiscommoditization,thethreenewannouncedNorthAmerica-to-Europeprojectseachdrawonspecialcharacteristicstodifferentiatetheirbandwidthofferings.HiberniaAtlantic’sProjectExpresshopestoshavefivetotenmillisecondsoffofcurrentroundtriptransatlanticlatency,witha targetof59msbetweenNewYorkandLondonandthe

39

hope of attracting the patronage of the high-frequency trading (HFT)community. EmeraldNetworks’EmeraldExpresswouldalsooffer lowlatencybutwouldpositionaccesstoIcelandicdatacenters,poweredbylow-cost,renewableenergy,asacornerstoneofitsmarketstrategy.Athirdproject,WASACEEurope,wouldbeafollow-onphaseofdevelopmentfortheambitiousWASACEnetwork,withearlierphasesconnectingAfrica,SouthAmerica,CentralAmerica, andNorthAmerica;WASACEwouldthuspromoteitswidegeographicreachasadifferentiator.Despitethesestrategies, each of the proposed wholesale projects will face an uphillbattlewithoutstrongcommitmentsfromtier-oneoperators,particularlyifforcedtocompeteagainstanext-generationconsortium-ledsystem.7.2 Transpacific

7.2.1 Bandwidth and CapacityThedemonstrateddesigncapacityofexistingtranspacificsystemsisjustabove40Tbps, andalthoughadditional capacitymaybepossiblewith100Gbpslinerates,thelengthoftranspacificspansisexpectedtoposeapracticalobstacletothefullrealizationoftargetedupgradecapacities.Itisthereforeagenuinepossibilitythatlitcapacityrequirementswillexceedthe design capacity of existing systemswithin three years. Given theextended time-to-marketof transpacificnetworks, anynewprojectwilllikelyneedtobefinalizedbeforeyear-end2012.

Forecasted Lit Capacity Requirement vs. Current Demonstrated Design Capacity of Transpacific Systems

0

50

100

150

200

250

300

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Tb

ps

Demonstrated design capacity of existing transpacific systems: 40.8 Tbps

40

Thetranspacificmarketsufferedashockwiththeactivationofthreenewsystemsbetween2008and2010.Eachofthethreenewsystemstargeteditsownmarketsegment:TransPacificExpress (TPE)catered toChina’stranspacificdemand;Asia-AmericaGateway(AAG)wasthefirstcabletoconnectNorthAmericadirectlytoSoutheastAsianmarkets;andUnity/EACPacific,ledbyPacnetandGoogle,positioneditselfasacomplementtodatacenterinfrastructureintheUnitedStatesandJapan.Between2008and2010thenumberofactivetranspacificsystemsincreaseddramatically,from four to seven. Furthermore, theUnity/EACPacific project,withmorethantwo-thirdsofitscapacitycontrolledbynon-operators,openeduptheJapan-USwholesalemarket,whichuntilthenhadbeendominatedbyTGNPacificandPacificCrossing-1.Asaresult,transpacificpricesfellbyasmuchas50percentinoneyear.

Existing Transpacifc Cable Systems

RFS System Owner(s)

2000 PacificCrossing-1(PC-1) NTT

2001 China-USCableNetwork Internationalconsortiumofcarriers

2001 Japan-USCableNetwork Internationalconsortiumofcarriers

2002 TGN-Pacific TataCommunications

2008 TransPacificExpress(TPE) Internationalconsortiumofcarriers

2010 Asia-AmericaGateway(AAG) Internationalconsortiumofcarriers

2010 Unity/EACPacificPacnet/Google/Bharti/GlobalTransit/KDDI/Singtel

Chinashowsthestrongestprospectsforgrowthintheregionandalreadyclaims the status of being the world’s largest broadband market: thecountryhastentimesmorefixedbroadbandsubscribersthanIndiaandsurpassed the United States in 2008. The number of fixed-broadbandsubscribers is expected to exceed 200millionwithin two years. ADSLremains the country’s dominant fixed-broadband technology, althoughtheChinesegovernmenthascalled for increasedFTTHinvestmentand

41

currentfiberdeploymentalreadytotalsmore than8millionkilometers.Japanese bandwidth demand, meanwhile, remains the largest in theregionandis50percentlargerthanChina’s,althoughforthenearfuturethe transpacific bandwidth demand of the country’s leading operatorsNTTandKDDIwilllikelybeaccommodatedbytheirinvestmentsinthePC-1andUnitysystems,respectively.

7.2.2 New SystemsMost of East Asia’s 20 largest operators will have equity in next-generation intra-Asian submarine capacity infrastructure by 2014following the expected activation of the Southeast Asia-Japan Cable,AsiaSubmarine-cableExpress, andAsiaPacificGateway systems. Themesh of connectivityprovidedby the networkswill allow the region’slargestcapacitypurchaserstohavemorecost-effectiveaccesstoeachofthecompetingtranspacificsystems.

Planned TranspacificFiberSystems

System Owner(s)

China-US-2 Internationalconsortiumofcarriers

Malaysia-US Internationalconsortiumofcarriers

TransPacificExpress(TPE)Expansion Internationalconsortiumofcarriers

Thailand-US Internationalconsortiumofcarriers

China’s international Internet bandwidth was 1.4 Tbps as of year-end2011.AlthoughChinaTelecomandChinaUnicomhaverespectivesharesof13and26percentintheTransPacificExpresssystem,sourcesindicatedthattheconfirmeddesigncapacityofthesystemasof2012wasonly2.5Tbps.Iffurtherupgradescannotbeeffected,ChinaTelecom’sallotmentofdesigncapacitywillbelessthanhalfofitstotalinternationalInternetbandwidthdemandasofyear-end2011. Furthermore,ChinaMobile isreportedlyseekingitsowninvestment-leveltranspacificbandwidth.Asaresult,anewChina-USsystemisexpectedtoenterservicein2015.

42

Chinese International Internet Bandwidth by Operator, Year-End 2011

China Telecom 810 Gbps

China Unicom 467 Gbps

China Mobile 83 Gbps

Other 30 Gbps

7.3 North America-South America

7.3.1 Bandwidth and CapacityTheNorthAmerica-SouthAmericacapacitymarketisheavilydependentonthreecables:GlobeNet,SAM-1,andSouthAmericanCrossing.

Existing US-Brazil Cable Systems

RFS System Owners

2000 Americas-II Consortium

2001 GlobeNet BrasilTelecom(Oi)

2001 SAM-1 Telefonica

2001 SouthAmericanCrossing(SAC) GlobalCrossingLatinAmerica has commanded some of the highest premiums of anycapacitymarket,with10GbpswavelengthsbetweenBrazilandtheUnitedStatesstillwellover$100,000permonth.

Pricing on the NorthAmerica-SouthAmerica route is as much as tentimeshigher than transatlanticpricing. This isdue in largepart to thethreewholesalers’relativelytightcontroloverthemarketplace,aswellas

43

unforeseenbandwidthgrowth in theregion’smajormarkets,especiallyBrazil.

TheBrazilian telecommunicationsmarket is strong,withhigh levels ofinvestmentonthepartofOiandforeigninvestorsincludingTelefonica,America Movil, Vivendi, and Portugal Telecom. The Plano Nacionalde Banda Larga (PNBL), administered by state-owned Telebras, aimstoprovide1Mbpshigh-speed Internetconnections forbetweenUSD$8and USD$20 per month and has attracted commitments from mostmajor operators. The country’s economic growth has been strong andmore equitable than in other developingmarkets, resulting in a largeraddressablebase for telecommunicationsand Internet services, and the2014WorldCup and 2016 SummerOlympics are expected to result inevengreaterincreasesinbandwidthdemand.

7.3.2 New SystemsAccording to most of the sources interviewed for this analysis, twomajorNorthAmerica-LatinAmericaprojects are in advancedplanningstages: AMX1, led by America Movil, and Transamericas BroadbandInfrastructure,ledbyaconsortiumofoperatorsandinvestors.AmericaMovil is one of the world’s five-largest mobile operators in terms ofsubscribers,anditsClarosubsidiaryoperatesthroughoutLatinAmerica;its takeoverofTelmexwasapprovedbyMexicanregulatoryauthoritiesin 2010, giving it control of the Brazilian fixed-line and long-distanceoperator Embratel (as of 2010ClarowasBrazil’s second-largestmobileoperatorandEmbratelhadamajorityshareofthecountry’sinternationallong distance market). TBI, meanwhile, is reportedly led by AT&T,Google, France Telecom, and least a dozen LatinAmerican operators,possiblyincludingTelefonica,whichisalsoconsideringtheconstructionofthePacificCaribbeanCommunicationsSystemtothenorthwestcornerofSouthAmerica.

Proposed Latin American Systems

RFS System Owners

2013/14 AmericaMovil-1(AMX1) AmericaMovil

2013/14 PacificCaribbeanCommunicationsSystem(PCCS)

Consortium

44

2013/14 TransamericasBroadbandInfrastructure(TBI)

Consortium

2014 AtlanticCableSystem(ACSea)

Telebras/Odebrecht/AngolaCable

2014 BRICSCable ImphandzeSubtelServices(S.Africa)

2014 Seabras-1 SeabornNetworks(USA)

2014 SouthAtlanticExpress(SAEx)

eFive(S.Africa)/Globenet(Oi)

2014 WASACE WASACECableWorlwide/AteriosCapital

TheSeabras-1projectwasunveiledinMarchof2012bySeabornNetworks,agroupofBoston,USA-basedbusinessmen;unlikeotherLatinAmericancableprojects,Seaborn-1wouldconnectonlytheUnitedStatesandBrazil.Theprojectwouldpursue a “carriers carrier”businessplan, andgiventherelativelyhighconcentrationofBrazilianmarketshare inthehandsofafewoperators(especiallyOiandTelefonica,whichoperatetheirownnetworks),thisstrategyisnotwithoutrisks.AMay,2012announcementthat Tata Communications would become an “anchor tenant” on thesystemwas a significant step forward although Tata is not currently amajorplayerintheregion’send-usermarkets.Nevertheless,ifSeabras-1orsimilarinvestor-ledprojectssuchasProjectExpressorEmeraldExpresssucceed, it could embolden future “carriers’ carrier” projects in otherregions.

In addition to the threemajor projects thatwould primarily target theNorthAmerica-SouthAmerica route (i.e.AMX1, Seabras-1, andTBI), agrowinglistofprojectswouldattempttocapitalizeonBrazil’seconomicemergence inorder topromote ties todevelopingeconomies includingsub-SaharanAfricaandBRICSmarkets. Someof thesewouldalso linkBrazil,theworld’slargestPortuguese-speakingcountry,withtheworld’sthird-largest Lusophone community, which is located inAngola. Theoverall strategy of these projects, which include the Telebras’ AtlanticCableSystem(ACSea),theBRICSCable,SouthAtlanticExpress(SAEx),and WASACE, would be to capitalize from the perceived shift in thebalanceofpowerawayfromthetraditionalG7economies.

TE SubCom (SubCom), a TE Connectivity

Limited company, is an industry pioneer

in undersea communications technology

and marine services and a leading

global supplier for today’s undersea

communications requirements. Drawing

on its heritage of technical innovation and

industry recognized performance, SubCom

designs, manufactures and installs the

most reliable, high-quality solutions for

telecommunications companies, internet

providers and offshore and science customers

with undersea communications needs vital

to their core mission. With its industry-leading

research and development laboratories,

manufacturing facilities, installation and

maintenance ships and depots, SubCom

has manufactured, and installed more than

100 undersea fiber optic systems and

deployed enough subsea communications

cable to circle the earth more than 12 times

at the equator. For more information

visit www.SubCom.com.

Watch our videos on YouTube:

www.youtube.com/user/SubComChannel

46

7.4 Sub-Saharan Africa

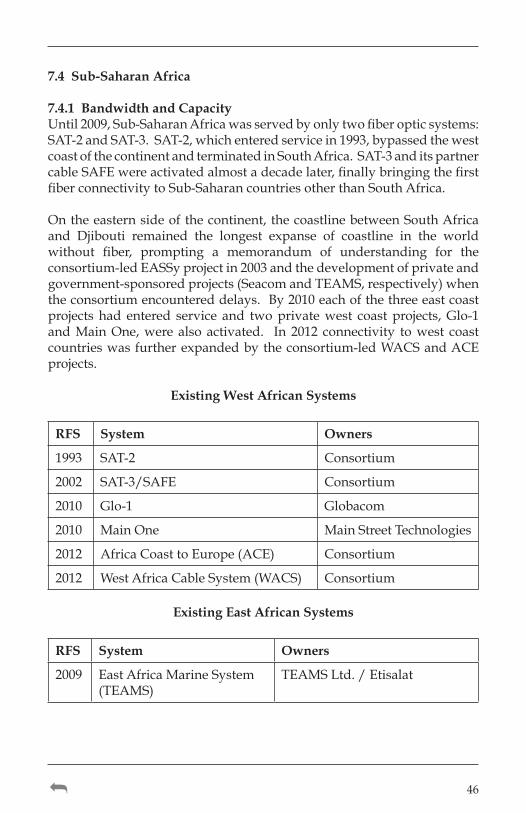

7.4.1 Bandwidth and CapacityUntil2009,Sub-SaharanAfricawasservedbyonlytwofiberopticsystems:SAT-2andSAT-3.SAT-2,whichenteredservicein1993,bypassedthewestcoastofthecontinentandterminatedinSouthAfrica.SAT-3anditspartnercableSAFEwereactivatedalmostadecadelater,finallybringingthefirstfiberconnectivitytoSub-SaharancountriesotherthanSouthAfrica.

Ontheeasternsideofthecontinent,thecoastlinebetweenSouthAfricaand Djibouti remained the longest expanse of coastline in the worldwithout fiber, prompting a memorandum of understanding for theconsortium-ledEASSyprojectin2003andthedevelopmentofprivateandgovernment-sponsoredprojects(SeacomandTEAMS,respectively)whentheconsortiumencountereddelays.By2010eachofthethreeeastcoastprojects had entered service and twoprivatewest coast projects,Glo-1andMainOne,werealsoactivated. In 2012 connectivity towest coastcountrieswasfurtherexpandedbytheconsortium-ledWACSandACEprojects.

Existing West African Systems

RFS System Owners

1993 SAT-2 Consortium

2002 SAT-3/SAFE Consortium

2010 Glo-1 Globacom

2010 MainOne MainStreetTechnologies

2012 AfricaCoasttoEurope(ACE) Consortium

2012 WestAfricaCableSystem(WACS) Consortium

Existing East African Systems

RFS System Owners

2009 EastAfricaMarineSystem(TEAMS)

TEAMSLtd./Etisalat

47

2009 Seacom IPS/Remgro/Herakles/Convergence/Shanduka

2010 EastAfricanSubmarineCableSystem(EASSy)

Consortium

Sub-Saharan Africa has 47 markets and dozens of operators withinternational bandwidth demand, none of whom are dominant on acontinentalbasis,andmanyofwhomwereuntilrecentlypayinginflatedsatellitecapacityprices–sothebuildoutofmultiplefibersystemsoneachcoastmaynothavebeenasirrationalasmanyobserversassert.

Although the design capabilities of sub-Saharan Africa’s submarinecablesystemswillgreatlyexceeddemandfortheforeseeablefuture,thedynamicsoftheAfricantelecommunicationsmarketallowittosupportmultiplesubmarinecableprojects.Submarineconnectivityoffersthemostcost-effectivesolutionforthecontinent’smajormarkets,andmostAfricanoperators are financially healthy and willing to invest in or purchasesubmarinecablecapacity.

Priortothebuildoutofnext-generationAfricanfiberbetween2009and2012,mostsub-SaharanAfricanoperatorswerelimitedtoeitherunreliable,expensivesatellitebandwidthoroverpricedcapacityonthemonopolisticSAT-3 system. Operators’ investments in the next-generation fiberprovidesthemwithmanytimesmorebandwidthatafractionofthecosttheyhadbeenpaying.

AlthoughtheAfricanmarketmaybefertilegroundformultiplesubmarinecable projects, governments’ investment in incumbent operators andthose operators’ control over international gateways and terrestrialinfrastructure make it difficult for wholesale cable projects to succeedwithouttheequityparticipationofoperatorswithineachlandingcountry.

TheperceivedoverbuildofSub-SaharanAfricancapacityisnotsimilartotheoverbuildofcapacityonthetransatlanticrouteinthelate-1990s.

Unlike the transatlantic route, only two of the next-generationAfricansystemsareconsideredtobeinvestor-led(asopposedtoconsortium-orcarrier-led), andboth reportedly received commitments fromoperatorsprior to their construction. Any bankruptcies ofAfrican cableswouldhaveamorelimitedimpactthanintheNorthAtlantic,duetothemoredirectparticipationofoperatorsinsubmarineinfrastructure.Furthermore

48

the complexities of the African market make the commoditization ofinternationalcapacityintheregionunlikely.

7.4.2 New SystemsThe success of the newestAfrican cables will be dependent upon thebuildoutofinfrastructurethroughouttheterrestrialnetwork,particularlyatitsextremities:backhaulandlocalaccess.Currently,botharegenerallycontrolled by former monopolies; their insulation from competitionhas arguably been the biggest obstacle to the full exploitation of next-generationinternationalbandwidth.

FortheretobesignificantSouthAtlanticdemandbetweenAfricaandSouthAmerica,theremayneedtobegreaterprogressineconomicdevelopment,geopolitical relations, Internet routing patterns, and Internet contentdevelopment;inthemeantimethereisamoreimmediateopportunityforsingle-systemconnectivitybetweenAfricaandtheUnitedStates.

AtleastfourcredibleproposalsareonthetableforconnectivitybetweenSub-SaharanAfricaandSouthAmerica;themostsuccessfulofthesewillfocusonprovidingconnectivityonwardtotheUnitedStates.

Proposed Sub-Saharan African Systems

RFS System Owners

2014 AtlanticCableSystem(ACSea) Telebras/Odebrecht/AngolaCable

2014 BRICSCable ImphandzeSubtelServices(S.Africa)

2014 SouthAtlanticExpress(SAEx) eFive(S.Africa)/Globenet(Oi)

2014 WASACE WASACECableWorlwide/AteriosCapital

7.5 South Asia and Middle East

7.5.1 Bandwidth and CapacityIndia, with international Internet bandwidth in excess of 1 Tbps as of2012, is the leadinggeneratorofbandwidthdemand inSouthAsiaandtheMiddleEast.India’sdemandfarexceedsthecombineddemandofthe

49

nextfourlargestbandwidthmarkets,whichindescendingorderareSaudiArabia,theUnitedArabEmirates,Pakistan,andIran.

Asof2012IndiaistheUnitedStates’leadingvoicecorrespondent,withthe number of international minutes between the two countries far inexcessofthesecond-andthird-placecorrespondents,MexicoandCanada.DirectandconnectinginternationalInternetbandwidthbetweenthetwocountriesisgreaterthan500Gbps.

In less than ten years, between 2002 and 2010, the Indianmiddle- andupper-class (characterized as households with incomes in excess ofUSD$4,000peryear)grewfrom13.8millionhouseholdsto46.7million.Extremelyimpoverishedhouseholdsearninglessthan$1,000peryearfellfrom65.2millionto41million. Yetdespitethecountry’sincomegains,middle-andupper-classhouseholdsstillaccountforlessthan20percentofthepopulation.Thesizeofthecountry’sso-called“in-betweenclass,”classifiedasthosehouseholdswithincomeofbetween$1,000and$4,000per year and thus considered to be relatively poor but not explicitlyliving in poverty, has remained steady atmore than three-fifths of thepopulation.Specifically,asof2010therewere140.7millionhouseholdsinthe“in-betweenclass,”representing61percentofallIndianhouseholds.

Althoughmobilevoiceservicesareaffordable–IndianARPUisamongthelowestintheworldatapproximately113INR(USD$2)–broadbandInternet services have failed to achieve significant penetration outsideof the country’s upper class. A primary obstacle is the country’s lowcomputerownership,atonly6percentofhouseholds.AffordableADSLpackagesexistbutfiber-basedbroadbandservicesaresignificantlymoreexpensive than in the rest of the world; the country’s largest Internetserviceproviderrecently launchedafiber-to-the-homeservicepricedatINR2,999(USD$53)permonthforthelowestbandwidthofjust1Mbps.Onthemobileside,3Gadoptionhasbeenweakerthanexpected,andhasbeen affected by widespread consumer complaints about high prices,weakcoverage,incompatiblehandsets,and“billshock.”Thelatterwasexperienced by “a majority of customers who are subscribing to 3G,”accordingtotelecomanalystsatGoldmanSachs.Theanalystsobservedthatwatchingonehourofasportingeventvia3Gtypicallycosts300INR(USD$6),farinexcessofwhatmostconsumerswerewillingtopay.

The concentration of Europe-to-Asia cable systems in theGulf of Suezwas a concern of telecommunications operators since the 1990s. Fearsofcatastrophiccableoutageswererealizedmultipletimes,mostnotably

50

in 2008 when Sea-Me-We and FLAG cables were cut simultaneously,promptingspeculationofapoliticalormilitaryconspiracy. FrustrationincreasedwhenEgyptian authorities delayed the landing of new cablesystemsinordertoallegedlyaccommodatesurveillancerequirementsputinplacebytheEgyptianOfficeofMilitaryServicesandReconnaissance.Cable operators’ concern was further heightened by the politicaluncertaintyaccompanyingtheEgyptianRevolutionof2011.SimultaneouscableoutagesinEgypthaveresultedinthelossofasmuchas80percentofIndia’sinternationalbandwidth.

Variousroutingshavebeenconstructedorproposedinordertocompeteagainst cables passing through Egypt. One of the first submarinealternativeswastheSAT-3/SAFEprojectwhichin2002providedthefirstEurope-AsiaconnectivityviaSouthAfricabutwithgreaterlatency.FiberopticsystemsconnectingIndiaeastwardstartedtoappearatapproximatelythe same time but created an equally-risky chokepoint in the Strait ofMalacca.Thenin2011,largelyasaresultofpoliticaluncertaintyinEgypt,planswere finalized formultiple terrestrial networks bypassing Egyptto the east includingEuropePersiaExpressGateway (EPEG),RegionalCable Network (RCN), and Jeddah-Amman-Damascus-Istanbul (JADILink).Notably,optionsforAmericanoperatorswishingtobypassEgyptare restrictedbyU.S.Government-imposed economic sanctions againstIran,Syria, andSudanso thatAmericanoperatorswishing to invest inprojectsbypassingEgyptareeffectivelylimitedtotworelativelynarrowpassagesacrossthe4,700-kilometerexpansebetweenwesternSudanandeasternIran:a200-kilometer-widecorridorintheKurdish-inhabitedareaalongtheIraq-Turkeyborder,anda400-kilometer-widecorridorthroughJordanwhichwouldrequireasubmarineconnectionviaLebanon,Israel,ortheGazaStrip.

Inthemid-2000sitappearedthatthestringofSea-Me-Wesystems,ledbymostofthedominantoperatorsalongtheroute,wouldcontinue.In2007theSea-Me-We-5consortiumheldameeting inGibraltarbutBT,whichhadoriginallyemergedasaleadingproponentofSea-Me-We-5,reportedlycalledforthedissolutionoftheconsortiumwhenitperceivedthatFranceTelecomwas not fully committed to the project andwould instead bedevotingitsefforttotheI-Me-Weproject.BythefollowingyearSea-Me-We-5’smembershadchosenbetweeneither I-Me-WeandEurope IndiaGateway,withthemajorityoptingforthelatter.AlthoughbothI-Me-WeandEIGencountereddifficultiesintheirdevelopment,EIG’sweremoresevereandwhenthesystemwasactivatedin2011itsconnectionsthroughEgyptremainedincomplete.

51

Existing South Asian Intercontinental Systems

RFS System Owners

1997 FLAGEurope-Asia(FEA) RelianceGlobalcom

1999 Sea-Me-We-3 Consortium

2002 i2i BhartiAirtel

2002 SAT-3/SAFE Consortium

2004 TGN-TIC TataCommunications

2005 Sea-Me-We-4 Consortium

2006 Falcon RelianceGlobalcom

2009 Seacom/TGNEurasia IPS/Remgro/Herakles/Convergence/Shanduka

2010 I-Me-We Consortium

2011 EuropeIndiaGateway(EIG) Consortium

2012 GulfBridgeInternational(GBI)/MENA

GulfBridgeInternational/OrascomHoldings

7.5.2 New SystemsBharti Airtel, China Mobile, China Telecom, France Telecom, SaudiTelecomCompany,andSingtelhavebeenidentifiedastheleadersofthenewSea-Me-We-5consortium,whichisreportedlyconsideringoptionstobypassEgypt.TheprojectwouldbethefirstSea-Me-WeendeavorwithstronginfluencefromChineseoperators,andwouldcompeteagainsttheroughlyonedozeninternationalcablesalreadyservingIndia,aswellastwootherproposedsystems: theBRICScable,whichwouldbethefirstsystemtoprovideadirectlinkbetweenIndiaandtheUnitedStates,andtheproposed“TagareCable.”

Proposed South Asian Intercontinental Systems

RFS System Owners

2014 BRICSCable ImphandzeSubtelServices(S.Africa)

2014 Sea-Me-We-5 Consortium

2014-2015 TagareCable NeilTagare/Consortium

53

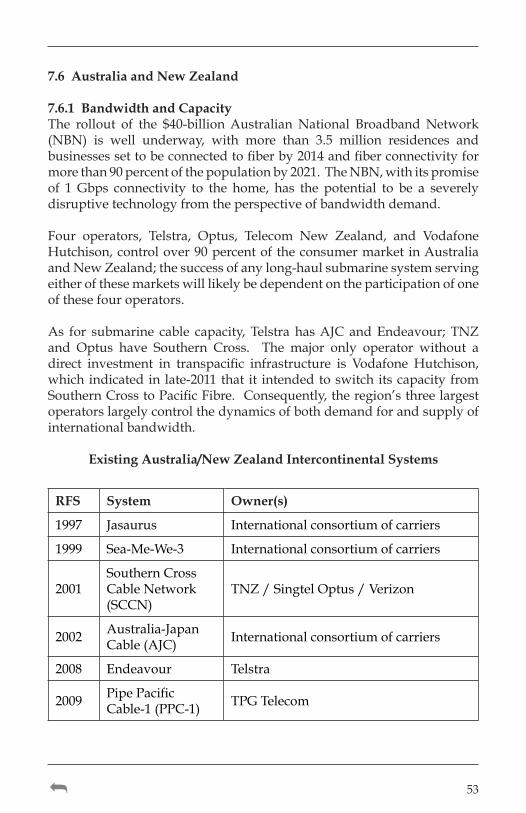

7.6 Australia and New Zealand

7.6.1 Bandwidth and CapacityThe rollout of the $40-billionAustralianNational BroadbandNetwork(NBN) is well underway, with more than 3.5 million residences andbusinessessettobeconnectedtofiberby2014andfiberconnectivityformorethan90percentofthepopulationby2021.TheNBN,withitspromiseof 1Gbps connectivity to the home, has the potential to be a severelydisruptivetechnologyfromtheperspectiveofbandwidthdemand.

Four operators, Telstra, Optus, Telecom New Zealand, and VodafoneHutchison,controlover90percentoftheconsumermarketinAustraliaandNewZealand;thesuccessofanylong-haulsubmarinesystemservingeitherofthesemarketswilllikelybedependentontheparticipationofoneofthesefouroperators.

As for submarine cable capacity, Telstra hasAJC andEndeavour; TNZand Optus have Southern Cross. The major only operator without adirect investment in transpacific infrastructure is Vodafone Hutchison,which indicatedin late-2011that it intendedtoswitch itscapacityfromSouthernCrosstoPacificFibre.Consequently,theregion’sthreelargestoperatorslargelycontrolthedynamicsofbothdemandforandsupplyofinternationalbandwidth.

Existing Australia/New Zealand Intercontinental Systems

RFS System Owner(s)

1997 Jasaurus Internationalconsortiumofcarriers

1999 Sea-Me-We-3 Internationalconsortiumofcarriers

2001SouthernCrossCableNetwork(SCCN)

TNZ/SingtelOptus/Verizon

2002 Australia-JapanCable(AJC) Internationalconsortiumofcarriers

2008 Endeavour Telstra

2009 PipePacificCable-1(PPC-1) TPGTelecom

54

7.6.2 New SystemsPacific Fibre has faced a variety of obstacles: a risk-averse financingenvironment;adominantcablesystemthatwasabletosingle-handedlyalterthedynamicsofthemarketplace,makingbusinessplanforecastingextremelydifficult;andthedefectionofPacnet.

ThebusinessplanofPacificFibrewereimpactedbyothercableoperators’simple ability to “move thegoalposts,”particularlywith respect to thepricingofcapacity.Thefinancingofanyprivatecablesystemisincreasinglydifficultinthecurrenteconomicenvironment,butPacificFibre’shead-to-headfaceoffwithincumbentswasexceedinglychallenging.

Oncethenext-generationnetworksbegintoachievesignificantlevelsofpenetration,governmentsupportandpopularexpectationsforAustralia’sNBNandNewZealand’sUltraFastBroadbandInitiativewilllikelyleadtodemandformoreabundantinternationalbandwidthinordertoensureaqualityexperienceforthenetworks’customers.BecausethemajorityofinternationaldemandintheregionisstilldirectedtowardNorthAmerica,itisexpectedthattherewillbeastrongbusinesscaseforanewtranspacificsystemtoAustraliaandNewZealandinthenear-future.

Sources have indicated that the Pacific Transit Cable, first proposedapproximately 12 years ago as a South Pacific link betweenAustralia,NewZealand,andChile,isonceagainunderconsideration.

Proposed Australia/New Zealand Intercontinental Systems

System Owner(s)

Australia-SingaporeCable(ASC) LeightonContractorsTelecom

Australia-SingaporeSubmarineCable(ASSC-1) JPCInternational

MatrixCableSystemExpansion MatrixNetworks

PacificFibre PacificFibreLtd.

PacificTransitCable Internationalconsortiumofcar-riers

SouthernCross-2 TNZ/SingtelOptus/Verizon

55

7.7 Polar RouteLongconsideredoutsidetherealmofpracticalpossibility,theconceptofatrans-Polarcablehasneverbeenmorecrediblewithrespecttoeachofthemajorconsiderations:technology,economics,andgeopolitics.Cableprojectshavebeenproposedbyinvestorsfromeachofthethreelargestpowers present in the Arctic, although each has varying degrees ofsupportfromtheirhomegovernments.GiventhestrategicimportanceoftheArcticregionwithregardtopetroleumandgasdeposits,freshwater,seafood,andtransport, it isexpectedthatgovernmentsupport foreachprospectiveprojectwillincrease,withtheprojectsallowingforincreasedinfluenceintheregionandalsoexpandingsurveillancecapabilities.

Proposed Polar Systems

RFS System Owners

2014 ArcticFibre ArcticFibre,Inc.

2014 ArcticLink Kodiak-KenaiCableCo./KhanjeeHoldings

2014 RussianOpticalTransArcticCableSystem(ROTACS)

GovernmentofRussia/PolarnetProjectLtd.

TheArcticFibresystem,ledbyCanadianinvestorDouglasCunningham,would connect Japan, Alaska, and the United Kingdom via northernCanada,with thepossibilityof future expansion toChina. Theprojectwould provide a route between North Asian and European markets,avoidingwhatcompanyrepresentativesidentifiedas“problematicareas”includingtheLuzonStrait,theSouthChinaSea,theSuezCanal,andtheMediterranean.Alow-latencypathof168millisecondswouldbecreatedbetween London and Asian destinations including Tokyo, Seoul, andShanghai. Theprojectwouldalsoseekgovernmentsupport toprovideconnectivitytoArcticcommunitiesinbothCanadaandAlaskaaswellastheproposedCanadianHighArcticResearchStation.

Arctic Link, led by the Kodiak-Kenai Cable Company and KhanjeeHoldings,wasoriginallyproposedasanextensionofaproposedAlaskandomestic network, Northern Fiber Optic Link, which unsuccessfullyapplied for stimulus fundingunder theBroadbandUSA component oftheAmericanRecoveryandReinvestmentAct.TheprojectwouldconnectAlaskatotheUnitedKingdomandJapan.

56

ROTACS and its predecessor, Polarnet, have been under considerationsinceatleast2002,andcanbeconsideredasthefirstseriousproposalforArcticconnectivity,havingcompletedroutesurveysin2003.Theprojectwas effectively shelved between 2005 and 2011, but comments fromthe Russian government in 2011 indicated that the system, connectingEngland,northernRussia,andJapan,wouldreceiveitssupport.

58

8.0 ConclusionWith$10billionofnewinvestmentoverthelastfiveyears,thesubmarineindustrysuccessfullyrecoveredfromitscrisisperiodof2003to2007(whenthemarketcontractedtoone-eighthof itsvalueovertheprecedingfiveyears).$20billionworthofcredibleprojectsareonthedrawingboard;thequestionthatwillshapetheindustryis:aretheyqualityprojects?

Onpaper,itwouldseemthatmostofthemare.Developingmarkets,longdeprivedofaffordableandabundantinternationalbandwidth,continueto be targeted and LatinAmerica has been of particular interest in aneffort to compensate for more than a decade without a new Brazilianintercontinentalsystem.BoldnewendeavorstotransitandservetheArcticare gaining credibility. Vast interregional systems look to interconnectmarkets that could previously only reach each other via costly transitpathsthroughdevelopedmarkets.

Ontheonehand,theindustryseemstobereturningtoitsrootsascarrierparticipationisthenewkeytoprojectsuccess.Ontheotherhand,newplayerscontinuetoappear.Googleconfoundedmarketobserversin2007whendetails of its investment in a transpacific cable began to emerge.FiveyearslaterFacebookhasenteredthefray,andanewwaveofover-the-top(OTT)contentprovidersseemreadytouseinternationalbandwidthinfrastructuretodirectlytackleoneofthemajorthreatstotheirbusinessmodels:poornetworkperformance.

As with all industries, the global economic crisis has slowed thedevelopmentofmanyprojects,notonlythoseseekingprivatefinancingbut operator-led systems as well. However the case for increasedconnectivityandanewwayof connectingmarkets is aviableoneandsolidopportunitiesexist,particularlywiththerightlocalpartners.

59