Style selection model - NOMURA · Style selection model ... Universe is based on MSCI AC...

28

QUANTITATIVE 15 March 2011 Nomura 1 Any authors named on this report are research analysts unless otherwise indicated. See the important disclosures and analyst certifications on pages 25 to 28. Style selection model ASIA PACIFIC Sandy Lee +852 2252 2101 [email protected] Rico Kwan, CFA +852 2252 2102 [email protected] Action We show that a methodical approach for style selection works in both the Asia and China universes. We exploit a style-switching model to provide short-term views on style performance based on long-term relative value of styles, short-term relative strength of styles, plus we use a risk-aversion proxy to enhance style timing. Our Asian model delivers a return of 11.8% pa with an information ratio of 2.35. A systematic style-switching approach Investment styles matter Active fund managers may have either a transient or a permanent style bias in managing portfolios. But different style strategies tend to cycle in and out of favor pertinent to the investment environment and macro circumstances. The significant changes in factor leadership in recent years exhibit the importance of style allocation. In this report, we examine a rules-based approach to select investment styles, with the objective of seeking consistent performance in the long run. Define style indices and develop the Asia style selection model Our style selection model starts from creating portfolios from bottom-up stock screening on various style themes. We create eight style indices, calculated by tracking performance of the long-short portfolios of a given style theme. In line with the behavioural finance literature, we study three main drivers of style rotation: long-term relative value of styles; short-term style performance; and the use of a risk-aversion proxy to enhance style timing. To measure the relative value of styles, we compare median E/P and B/P spread of the long-short style portfolios relative to the history in order to identify the mean reversion opportunity. We gauge the short-term relative strength of styles using latest-six-month style returns. Further, we apply market return as a risk-aversion proxy to improve the style timing. When the previous month’s market return is positive, our style-switching model will assign a greater weighting to the relative-strength approach, and vice versa. By combining the style ranking scores based on the three drivers, we pick the top two ranking styles and track the average style performance over time. Performance of Asia style selection model The Asia style-switching model delivers a long-short return of 11.8% pa since end- 2000 with an information ratio of 2.35. We show that our style model yields a better return than alternative style selectors. The model offers short-term views on style performance and is effective using either a monthly or quarterly rebalance. Our Asian model recommends revision and profitability styles in March. Does our style selection model work in China A-shares? A trend-following (momentum) approach to pick styles appears to yield far better returns in China in the observed period, compared with one looking solely at long- term relative value of styles. We believe, however, such a pure relative-strength approach tends to suffer at turning points. Our preferred style selection model for the China CSI universe delivers a moderately better return and lower risk leading to a much better risk-adjusted performance, compared with a style selector that focuses on only short-term style momentum. The model is more effective when applied on a monthly basis. In March, our China model recommends revision and momentum styles. NOMURA INTERNATIONAL (HK) LIMITED Analysts Sandy Lee +852 2252 2101 [email protected] Rico Kwan, CFA +852 2252 2102 [email protected] Performance of style selection model for Asia Pacific ex Japan (50) 0 50 100 150 200 250 Nov-00 Nov-01 Nov-02 Nov-03 Nov-04 Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 (%) (30) 0 30 60 90 120 150 (%) Long return (LHS) Short return (LHS) Long-short return (RHS) Note: Cumulative performance represents the combined style returns of the styles selected in our style selection model. The styles are equal-weighted and rebalanced monthly. Source: Nomura Quantitative Strategies

Transcript of Style selection model - NOMURA · Style selection model ... Universe is based on MSCI AC...

Q U A N T I T A T I V E

15 March 2011 Nomura 1

Any authors named on this report are research analysts unless otherwise indicated. See the important disclosures and analyst certifications on pages 25 to 28.

Style selection model ASIA PACIFIC

Sandy Lee +852 2252 2101 [email protected]

Rico Kwan, CFA +852 2252 2102 [email protected]

Action We show that a methodical approach for style selection works in both the Asia and

China universes. We exploit a style-switching model to provide short-term views on style performance based on long-term relative value of styles, short-term relative strength of styles, plus we use a risk-aversion proxy to enhance style timing. Our Asian model delivers a return of 11.8% pa with an information ratio of 2.35.

A systematic style-switching approach Investment styles matter

Active fund managers may have either a transient or a permanent style bias in managing portfolios. But different style strategies tend to cycle in and out of favor pertinent to the investment environment and macro circumstances. The significant changes in factor leadership in recent years exhibit the importance of style allocation. In this report, we examine a rules-based approach to select investment styles, with the objective of seeking consistent performance in the long run.

Define style indices and develop the Asia style selection model

Our style selection model starts from creating portfolios from bottom-up stock screening on various style themes. We create eight style indices, calculated by tracking performance of the long-short portfolios of a given style theme. In line with the behavioural finance literature, we study three main drivers of style rotation: long-term relative value of styles; short-term style performance; and the use of a risk-aversion proxy to enhance style timing. To measure the relative value of styles, we compare median E/P and B/P spread of the long-short style portfolios relative to the history in order to identify the mean reversion opportunity. We gauge the short-term relative strength of styles using latest-six-month style returns. Further, we apply market return as a risk-aversion proxy to improve the style timing. When the previous month’s market return is positive, our style-switching model will assign a greater weighting to the relative-strength approach, and vice versa. By combining the style ranking scores based on the three drivers, we pick the top two ranking styles and track the average style performance over time.

Performance of Asia style selection model

The Asia style-switching model delivers a long-short return of 11.8% pa since end-2000 with an information ratio of 2.35. We show that our style model yields a better return than alternative style selectors. The model offers short-term views on style performance and is effective using either a monthly or quarterly rebalance. Our Asian model recommends revision and profitability styles in March.

Does our style selection model work in China A-shares?

A trend-following (momentum) approach to pick styles appears to yield far better returns in China in the observed period, compared with one looking solely at long-term relative value of styles. We believe, however, such a pure relative-strength approach tends to suffer at turning points. Our preferred style selection model for the China CSI universe delivers a moderately better return and lower risk leading to a much better risk-adjusted performance, compared with a style selector that focuses on only short-term style momentum. The model is more effective when applied on a monthly basis. In March, our China model recommends revision and momentum styles.

N O M U R A I N T E R N A T I O N A L ( H K ) L I M I T E D

Analysts Sandy Lee

+852 2252 2101

Rico Kwan, CFA

+852 2252 2102

Performance of style selection model for Asia Pacific ex Japan

(50)

0

50

100

150

200

250

Nov

-00

Nov

-01

Nov

-02

Nov

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Nov

-08

Nov

-09

Nov

-10

(%)

(30)

0

30

60

90

120

150(%)Long return (LHS)

Short return (LHS)Long-short return (RHS)

Note: Cumulative performance represents the combined style returns of the styles selected in our style selection model. The styles are equal-weighted and rebalanced monthly.

Source: Nomura Quantitative Strategies

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 2

Contents

Investment styles matter 3

Defining the style themes 5 Building eight style indices 5 Performance and return correlation between style indices 6

Style selection model 7 Identify the key drivers of style rotation 7 Methodology to combine style ranking scores 8

Performance of style selection model 10 Styles that are selected in Asia Pacific ex Japan historically 12 Stock ideas from Asia style selection model 13

Does style selection model work in China? 17 Which styles are opted for in China historically? 19 Stock ideas from China style selection model 20

Definition of factors 23

All returns in this report are calculated exclusive of transaction costs unless otherwise stated.

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 3

A review of recent performance of styles

Investment styles matter In the previous versions of Quantitative Insight (last published on 9 February, 2011), we show that both value investing and earnings-revision indicators have worked well in the Asia Pacific ex-Japan region in the long run. But no one screen factor works well all the time in the region. Active fund managers may have either a transient or a permanent style bias in managing portfolios. Static investment styles are pretty much destined to short-term volatility — as the effectiveness of quantitative factors differs over the cycle, different style strategies tend to cycle in and out of favor pertinent to the investment environment and macro circumstances. Quantitative investing requires rigorous analysis and scientific method to find out what style themes or screen factors offer opportunities, when and where.

We have seen significant changes in style leadership since the credit crisis (Exhibit 1). During the crisis, low-risk and high-dividend yield stocks outperformed, while B/P and E/P suffered. In early 2009, the equity market was dominated by a risk-relief value rally; value and high-risk stocks recovered, whereas price momentum factors suffered badly when markets faced dramatic reversals. Looking at the 2010 factor return, value factors saw a mixed performance, with a change in leadership of value to forecast E/P and dividend yield, from B/P and CF/P in 2009. Earnings revision indicators are seeing a rising factor impact since early 2010 and have outperformed most value factors in delivering a better risk-adjusted return, whereas mid-term price momentum factor has shown improved performance.

Exhibit 1. Performance of major factors since summer 2007

(20)(15)(10)(5)05

101520253035

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

(%) Dividend yield E/P B/P CF/P

(40)

(30)

(20)

(10)

0

10

20

30

40

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

(%) Mid-term price momentum (12M-1M)

Revision index

Estimates dispersion

Default probability *

Note: Universe is based on MSCI AC Asia-Pacific ex-Japan. Factor returns are generated by calculating the subsequent performance of an equal-weighted portfolio that is long the highest quintile and short the quintile with the lowest scores (rebalanced monthly), except for the factor marked *, which is computed reverse-based.. Data run to 28 February.

Source: Worldscope, I/B/E/S, MSCI, Nomura Quantitative Strategies

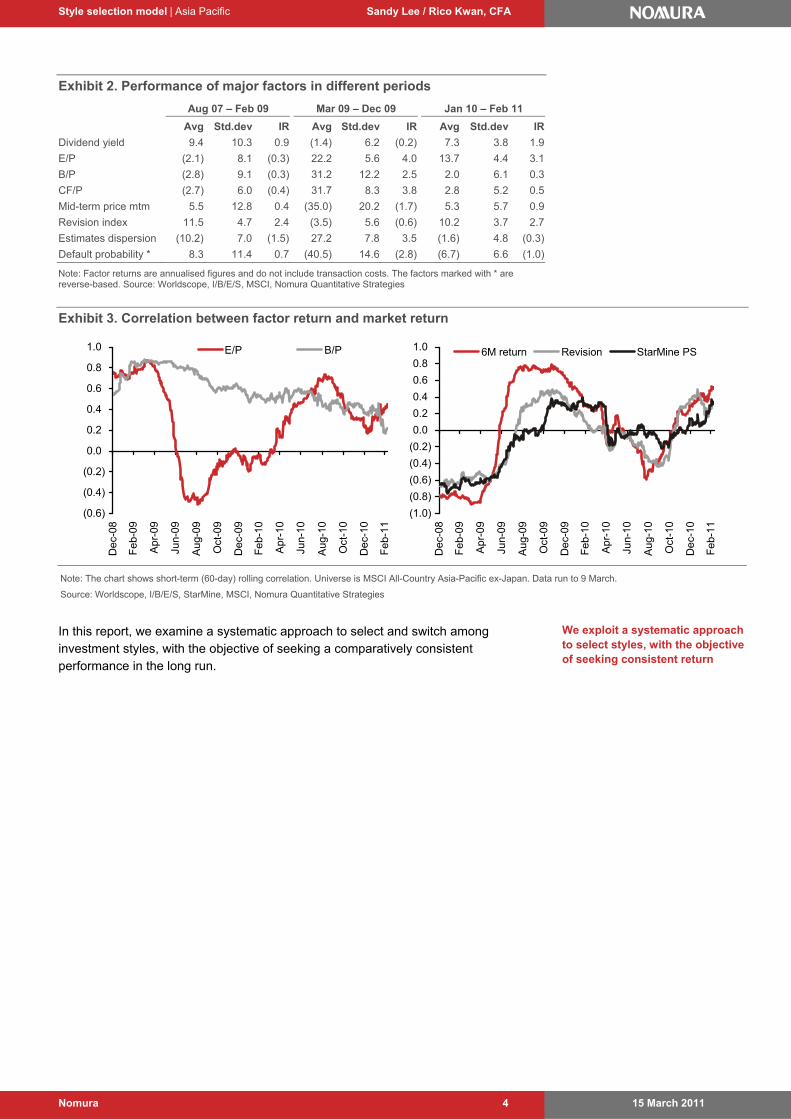

In Exhibit 2, we present the performance of major factors between August 2007 and February 2009, from March 2009 to December 2009, and since January 2010. Consistency of the factor performance has been affected by an ongoing swing in market sentiment and risk appetite. Likewise, short-term correlation between factor return and market return has changed over time (Exhibit 3). This illustrates the importance of style investing and selecting the right investment styles over the cycle.

The significant changes in factor leadership over the cycle demonstrate the importance of style investing

Picking the right style themes matters in seeking alpha

Quantitative investing requires rigorous analysis to find out what investment styles or screen factors offer opportunities

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 4

Exhibit 2. Performance of major factors in different periods

Aug 07 – Feb 09 Mar 09 – Dec 09 Jan 10 – Feb 11

Avg Std.dev IR Avg Std.dev IR Avg Std.dev IR

Dividend yield 9.4 10.3 0.9 (1.4) 6.2 (0.2) 7.3 3.8 1.9

E/P (2.1) 8.1 (0.3) 22.2 5.6 4.0 13.7 4.4 3.1

B/P (2.8) 9.1 (0.3) 31.2 12.2 2.5 2.0 6.1 0.3

CF/P (2.7) 6.0 (0.4) 31.7 8.3 3.8 2.8 5.2 0.5

Mid-term price mtm 5.5 12.8 0.4 (35.0) 20.2 (1.7) 5.3 5.7 0.9

Revision index 11.5 4.7 2.4 (3.5) 5.6 (0.6) 10.2 3.7 2.7

Estimates dispersion (10.2) 7.0 (1.5) 27.2 7.8 3.5 (1.6) 4.8 (0.3)

Default probability * 8.3 11.4 0.7 (40.5) 14.6 (2.8) (6.7) 6.6 (1.0)

Note: Factor returns are annualised figures and do not include transaction costs. The factors marked with * are reverse-based. Source: Worldscope, I/B/E/S, MSCI, Nomura Quantitative Strategies

Exhibit 3. Correlation between factor return and market return

(0.6)

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

De

c-08

Fe

b-09

Ap

r-09

Jun-

09

Au

g-09

Oct

-09

De

c-09

Fe

b-10

Ap

r-10

Jun-

10

Au

g-10

Oct

-10

De

c-10

Fe

b-11

E/P B/P

(1.0)

(0.8)

(0.6)

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

De

c-08

Fe

b-09

Ap

r-09

Jun-

09

Au

g-09

Oct

-09

De

c-09

Fe

b-10

Ap

r-10

Jun-

10

Au

g-10

Oct

-10

De

c-10

Fe

b-11

6M return Revision StarMine PS

Note: The chart shows short-term (60-day) rolling correlation. Universe is MSCI All-Country Asia-Pacific ex-Japan. Data run to 9 March.

Source: Worldscope, I/B/E/S, StarMine, MSCI, Nomura Quantitative Strategies

In this report, we examine a systematic approach to select and switch among investment styles, with the objective of seeking a comparatively consistent performance in the long run.

We exploit a systematic approach to select styles, with the objective of seeking consistent return

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 5

Identifying the major styles that are relevant in Asia

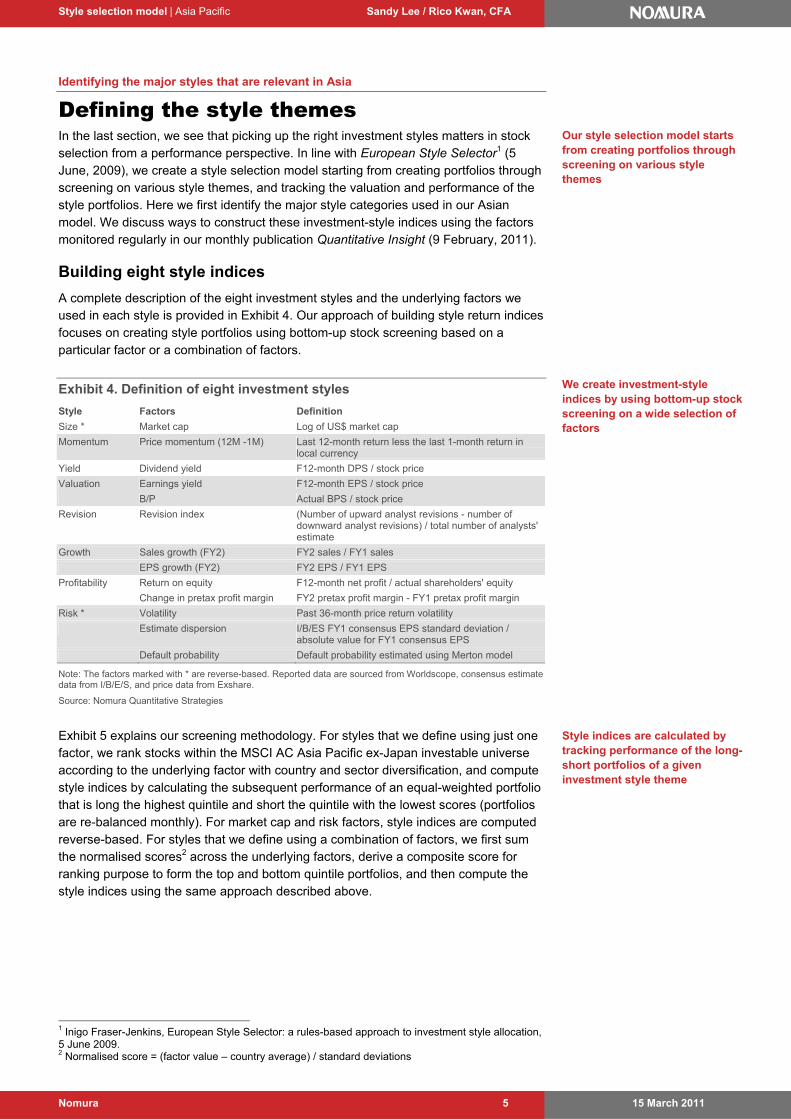

Defining the style themes In the last section, we see that picking up the right investment styles matters in stock selection from a performance perspective. In line with European Style Selector1 (5 June, 2009), we create a style selection model starting from creating portfolios through screening on various style themes, and tracking the valuation and performance of the style portfolios. Here we first identify the major style categories used in our Asian model. We discuss ways to construct these investment-style indices using the factors monitored regularly in our monthly publication Quantitative Insight (9 February, 2011).

Building eight style indices

A complete description of the eight investment styles and the underlying factors we used in each style is provided in Exhibit 4. Our approach of building style return indices focuses on creating style portfolios using bottom-up stock screening based on a particular factor or a combination of factors.

Exhibit 4. Definition of eight investment styles

Style Factors Definition

Size * Market cap Log of US$ market cap

Momentum Price momentum (12M -1M) Last 12-month return less the last 1-month return in local currency

Yield Dividend yield F12-month DPS / stock price

Valuation Earnings yield F12-month EPS / stock price

B/P Actual BPS / stock price

Revision Revision index (Number of upward analyst revisions - number of downward analyst revisions) / total number of analysts' estimate

Growth Sales growth (FY2) FY2 sales / FY1 sales

EPS growth (FY2) FY2 EPS / FY1 EPS

Profitability Return on equity F12-month net profit / actual shareholders' equity

Change in pretax profit margin FY2 pretax profit margin - FY1 pretax profit margin

Risk * Volatility Past 36-month price return volatility

Estimate dispersion I/B/ES FY1 consensus EPS standard deviation / absolute value for FY1 consensus EPS

Default probability Default probability estimated using Merton model

Note: The factors marked with * are reverse-based. Reported data are sourced from Worldscope, consensus estimate data from I/B/E/S, and price data from Exshare.

Source: Nomura Quantitative Strategies

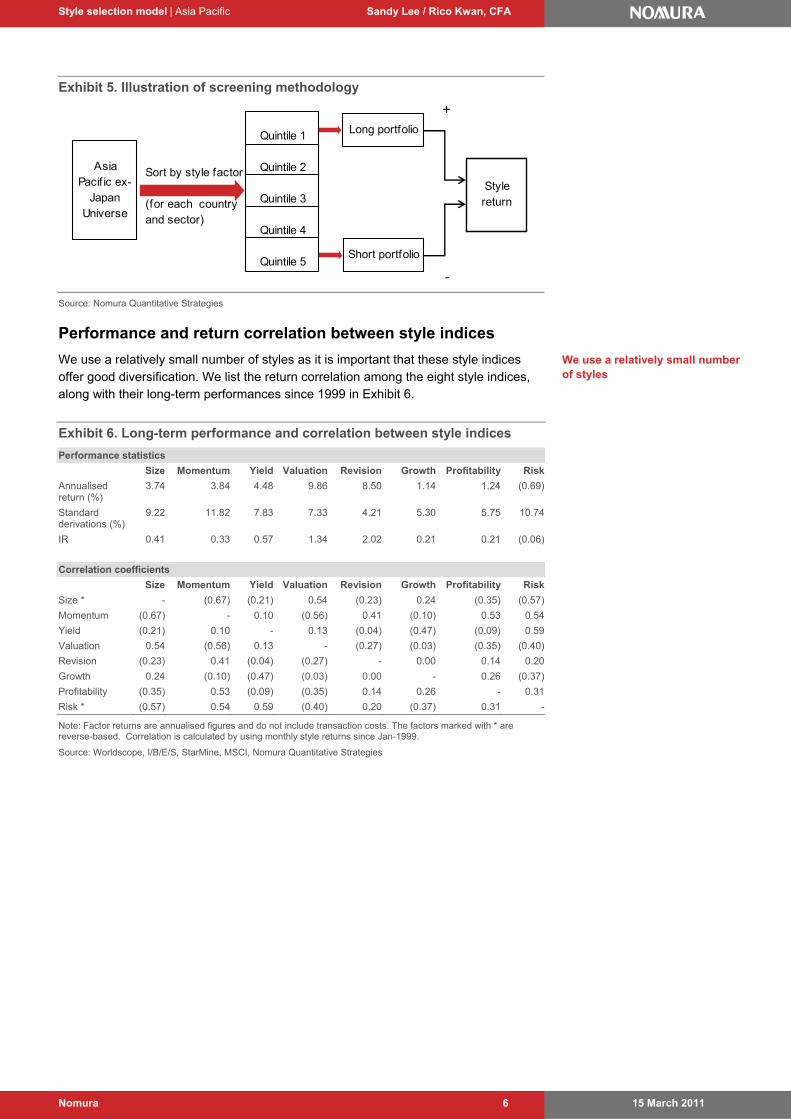

Exhibit 5 explains our screening methodology. For styles that we define using just one factor, we rank stocks within the MSCI AC Asia Pacific ex-Japan investable universe according to the underlying factor with country and sector diversification, and compute style indices by calculating the subsequent performance of an equal-weighted portfolio that is long the highest quintile and short the quintile with the lowest scores (portfolios are re-balanced monthly). For market cap and risk factors, style indices are computed reverse-based. For styles that we define using a combination of factors, we first sum the normalised scores2 across the underlying factors, derive a composite score for ranking purpose to form the top and bottom quintile portfolios, and then compute the style indices using the same approach described above.

1 Inigo Fraser-Jenkins, European Style Selector: a rules-based approach to investment style allocation, 5 June 2009. 2 Normalised score = (factor value – country average) / standard deviations

Our style selection model starts from creating portfolios through screening on various style themes

We create investment-style indices by using bottom-up stock screening on a wide selection of factors

Style indices are calculated by tracking performance of the long-short portfolios of a given investment style theme

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 6

Exhibit 5. Illustration of screening methodology

Sort by style factor

(for each country and sector)

Asia Pacif ic ex-

Japan Universe

Quintile 1

Quintile 2

Quintile 3

Quintile 4

Quintile 5

Long portfolio

Short portfolio

Style return

+

‐

Source: Nomura Quantitative Strategies

Performance and return correlation between style indices

We use a relatively small number of styles as it is important that these style indices offer good diversification. We list the return correlation among the eight style indices, along with their long-term performances since 1999 in Exhibit 6.

Exhibit 6. Long-term performance and correlation between style indices

Performance statistics

Size Momentum Yield Valuation Revision Growth Profitability Risk

Annualised return (%)

3.74 3.84 4.48 9.86 8.50 1.14 1.24 (0.69)

Standard derivations (%)

9.22 11.82 7.83 7.33 4.21 5.30 5.75 10.74

IR 0.41 0.33 0.57 1.34 2.02 0.21 0.21 (0.06)

Correlation coefficients

Size Momentum Yield Valuation Revision Growth Profitability Risk

Size * - (0.67) (0.21) 0.54 (0.23) 0.24 (0.35) (0.57)

Momentum (0.67) - 0.10 (0.56) 0.41 (0.10) 0.53 0.54

Yield (0.21) 0.10 - 0.13 (0.04) (0.47) (0.09) 0.59

Valuation 0.54 (0.56) 0.13 - (0.27) (0.03) (0.35) (0.40)

Revision (0.23) 0.41 (0.04) (0.27) - 0.00 0.14 0.20

Growth 0.24 (0.10) (0.47) (0.03) 0.00 - 0.26 (0.37)

Profitability (0.35) 0.53 (0.09) (0.35) 0.14 0.26 - 0.31

Risk * (0.57) 0.54 0.59 (0.40) 0.20 (0.37) 0.31 -

Note: Factor returns are annualised figures and do not include transaction costs. The factors marked with * are reverse-based. Correlation is calculated by using monthly style returns since Jan-1999.

Source: Worldscope, I/B/E/S, StarMine, MSCI, Nomura Quantitative Strategies

We use a relatively small number of styles

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 7

Methodology of style-switching model

Style selection model In this section, we attempt to develop a systematic approach to allocate style exposure over time in a dynamic way, with the objective to deliver comparatively consistent performance in the long run. We first look into two attributes of style performance: the relative value of style portfolios versus the long-term average, and the recent short-term momentum of style performance. This is to say, styles that are seeing wider value spread on the long-short style portfolios relative to the historical average (relative value of styles) are relatively ‘inexpensive’ and would tend to see mean reversion, thus having greater opportunities to outperform in the future. In addition, style performance tends to be persistent in the short term (relative strength of styles). Further, we attempt to apply a risk-aversion proxy to distinguish the potential of relative-value and relative-strength approach and improve the potential rewards of style timing.

Identify the key drivers of style rotation

Academic researchers and investment professionals alike have found evidence to support the long-term relative-value and short-term relative-strength approach for selecting styles. One example of academic literature is “Style Timing: Value versus Growth” by Clifford S. Asness et al (2000)3, which concluded that value spread has predictive power for value strategy return versus growth. Beckers and Thomas4 (2010) focus on the persistence and predictability of the Barra style returns in the U.S., Europe and Japan. They show that actively investing based on the persistence of historically significant style returns leads to outperformance, although precisely capturing the style returns is not simple.

The short-term persistence of style performance is also explained by a large amount of behavioural finance literature. Owain ap Gwilym et al (2010)5, for instance, find that momentum strategies are profitable in a global portfolio. Such behavioural effect could be applied to style portfolios that consist of stocks with similar characteristics. In an environment of falling interest rates, for instance, returns of high-yield stocks may start to improve. Since investors may need time to reallocate style exposure, such under-reaction to news in the short term may thus produce a momentum effect, causing high-yield stocks to consistently outperform in the short run.

In emerging markets, Stéphanie Desrosiers et al (2006)6 find that a strategy using a relative-value indicator following negative market performance and a relative-strength measure after positive market performance presents consistent return that is better than that resulting from either the relative-value or relative-strength approaches. This is to say, there is psychological evidence to support that prior performance results tend to affect subsequent risk-taking behaviour. Such behavioural effect could also be applied to style selection. When previous market return is positive and risk appetite is steady or high, for instance, investors could be more willing to invest on styles that show good short-term momentum, and vice versa. As such, market performance could potentially be used as a risk-aversion proxy to increase the effectiveness of style timing.

3 Clifford S. Asness, Jacques A. Friedman, Robert J. Krail, and John M. Liew (2000), Style Timing: Value versus Growth, The Journal of Portfolio Management Vol. 26, pp 50-60. 4 Stan Beckers and Jolly Ann Thomas (2010), On the Persistence of Style Returns, The Journal of Portfolio Management Vol. 37, pp 15-30. 5 Owain ap Gwilym , Andrew Clare , James Seaton , and Stephen Thomas, Price and Momentum as Robust Tactical Approaches to Global Equity Investing, The Journal of Investing Vol. 19, pp 80-91. 6 Stéphanie Desrosiers , Mohamed Kortas , Jean-François L'her , Jean-François Plante , and Mathieu Roberge, Style Timing in Emerging Markets, The Journal of Investing Vol. 15, pp 29-37.

We study three main drivers of style rotation: relative value of the style compared with history; short-term persistence of style performance; and the use of a risk-aversion proxy to enhance style timing

There is strong academic evidence to support the notion of long-term relative-value approach in style timing – value spread has predictive power for value strategy return versus growth

Investors may need time to reallocate style exposure. Such under-reaction to news in the short-term may thus produce a momentum effect

There is psychological evidence to support that prior performance results tend to affect subsequent risk-taking behaviour, thus a risk-aversion proxy may increase the effectiveness of style timing

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 8

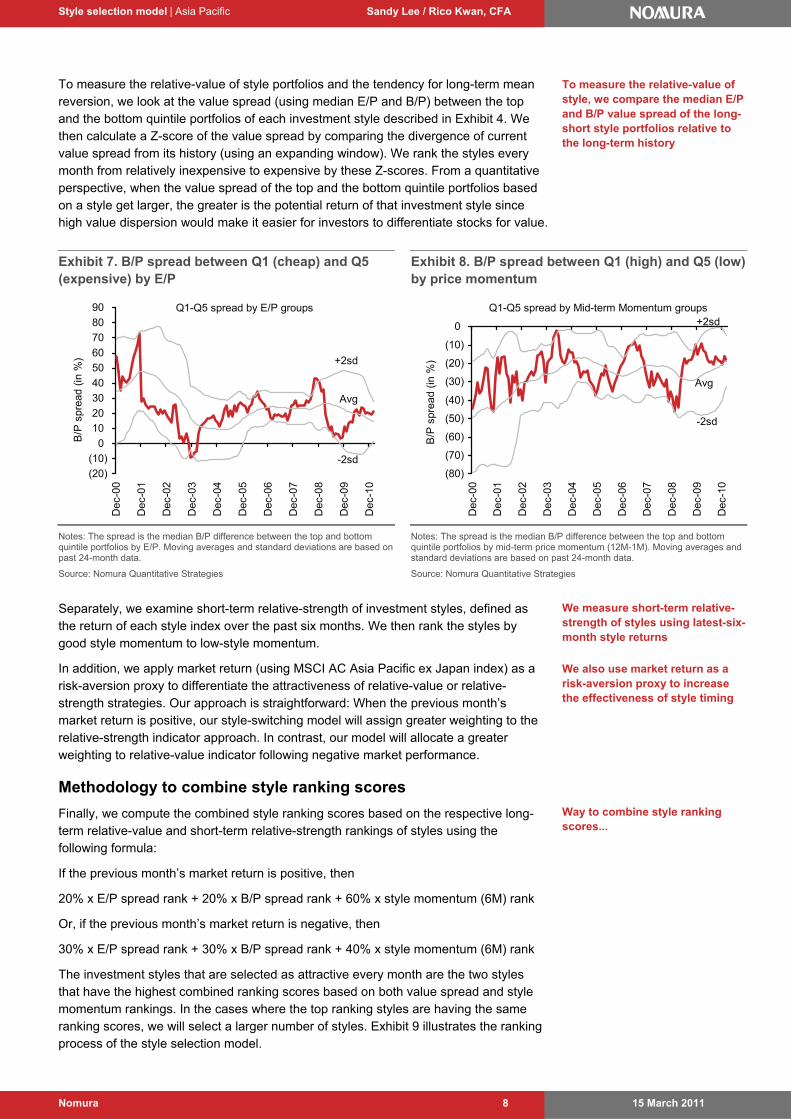

To measure the relative-value of style portfolios and the tendency for long-term mean reversion, we look at the value spread (using median E/P and B/P) between the top and the bottom quintile portfolios of each investment style described in Exhibit 4. We then calculate a Z-score of the value spread by comparing the divergence of current value spread from its history (using an expanding window). We rank the styles every month from relatively inexpensive to expensive by these Z-scores. From a quantitative perspective, when the value spread of the top and the bottom quintile portfolios based on a style get larger, the greater is the potential return of that investment style since high value dispersion would make it easier for investors to differentiate stocks for value.

Exhibit 7. B/P spread between Q1 (cheap) and Q5 (expensive) by E/P

Q1-Q5 spread by E/P groups

(20)

(10)

0

10

20

30

40

50

60

70

80

90

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

B/P

spr

ead

(in

%) +2sd

-2sd

Avg

Notes: The spread is the median B/P difference between the top and bottom quintile portfolios by E/P. Moving averages and standard deviations are based on past 24-month data.

Source: Nomura Quantitative Strategies

Exhibit 8. B/P spread between Q1 (high) and Q5 (low) by price momentum

Q1-Q5 spread by Mid-term Momentum groups

(80)

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

B/P

spr

ead

(in

%)

+2sd

Avg

-2sd

Notes: The spread is the median B/P difference between the top and bottom quintile portfolios by mid-term price momentum (12M-1M). Moving averages and standard deviations are based on past 24-month data.

Source: Nomura Quantitative Strategies

Separately, we examine short-term relative-strength of investment styles, defined as the return of each style index over the past six months. We then rank the styles by good style momentum to low-style momentum.

In addition, we apply market return (using MSCI AC Asia Pacific ex Japan index) as a risk-aversion proxy to differentiate the attractiveness of relative-value or relative-strength strategies. Our approach is straightforward: When the previous month’s market return is positive, our style-switching model will assign greater weighting to the relative-strength indicator approach. In contrast, our model will allocate a greater weighting to relative-value indicator following negative market performance.

Methodology to combine style ranking scores

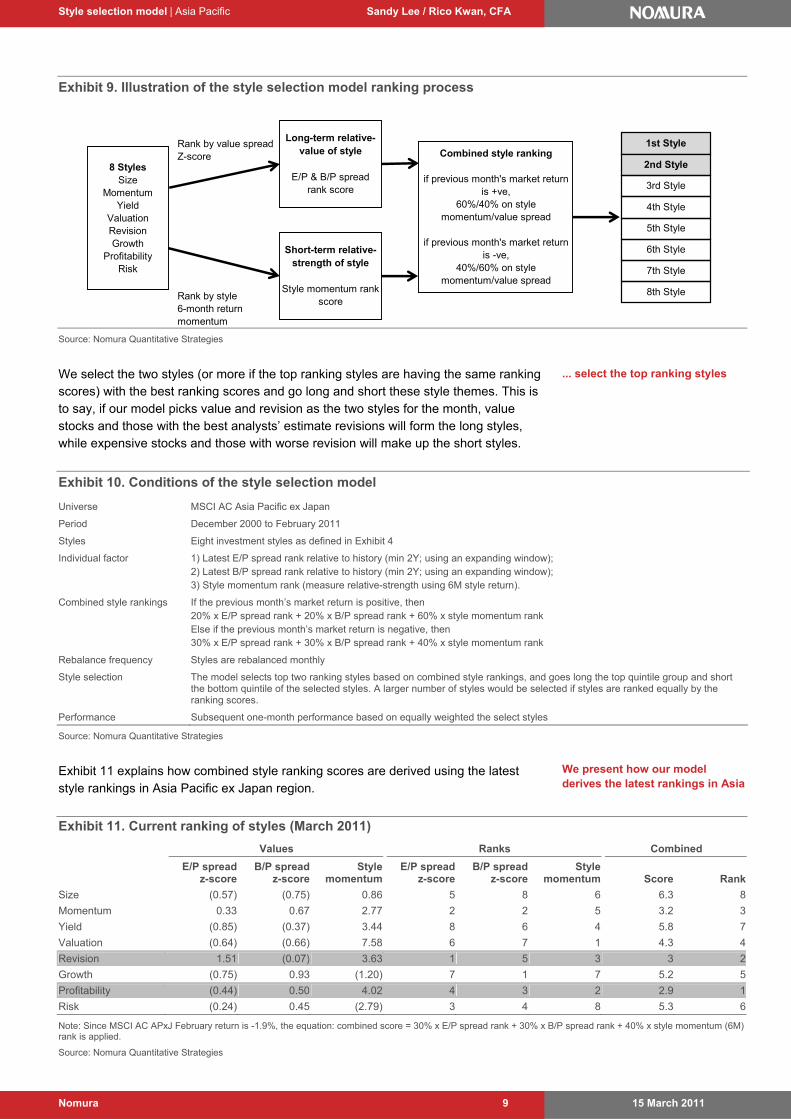

Finally, we compute the combined style ranking scores based on the respective long-term relative-value and short-term relative-strength rankings of styles using the following formula:

If the previous month’s market return is positive, then

20% x E/P spread rank + 20% x B/P spread rank + 60% x style momentum (6M) rank

Or, if the previous month’s market return is negative, then

30% x E/P spread rank + 30% x B/P spread rank + 40% x style momentum (6M) rank

The investment styles that are selected as attractive every month are the two styles that have the highest combined ranking scores based on both value spread and style momentum rankings. In the cases where the top ranking styles are having the same ranking scores, we will select a larger number of styles. Exhibit 9 illustrates the ranking process of the style selection model.

To measure the relative-value of style, we compare the median E/P and B/P value spread of the long-short style portfolios relative to the long-term history

We measure short-term relative-strength of styles using latest-six-month style returns

We also use market return as a risk-aversion proxy to increase the effectiveness of style timing

Way to combine style ranking scores...

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 9

Exhibit 9. Illustration of the style selection model ranking process

Rank by value spread Z-score

Rank by style 6-month return momentum

8 StylesSize

MomentumYield

ValuationRevisionGrowth

ProfitabilityRisk

Long-term relative-value of style

E/P & B/P spread rank score

1st Style

Short-term relative-strength of style

Style momentum rank score

2nd Style

3rd Style

4th Style

5th Style

6th Style

7th Style

8th Style

Combined style ranking

if previous month's market return is +ve,

60%/40% on style momentum/value spread

if previous month's market return is -ve,

40%/60% on style momentum/value spread

Source: Nomura Quantitative Strategies

We select the two styles (or more if the top ranking styles are having the same ranking scores) with the best ranking scores and go long and short these style themes. This is to say, if our model picks value and revision as the two styles for the month, value stocks and those with the best analysts’ estimate revisions will form the long styles, while expensive stocks and those with worse revision will make up the short styles.

Exhibit 10. Conditions of the style selection model

Universe MSCI AC Asia Pacific ex Japan

Period December 2000 to February 2011

Styles Eight investment styles as defined in Exhibit 4

Individual factor 1) Latest E/P spread rank relative to history (min 2Y; using an expanding window); 2) Latest B/P spread rank relative to history (min 2Y; using an expanding window); 3) Style momentum rank (measure relative-strength using 6M style return).

Combined style rankings If the previous month’s market return is positive, then 20% x E/P spread rank + 20% x B/P spread rank + 60% x style momentum rank Else if the previous month’s market return is negative, then 30% x E/P spread rank + 30% x B/P spread rank + 40% x style momentum rank

Rebalance frequency Styles are rebalanced monthly

Style selection The model selects top two ranking styles based on combined style rankings, and goes long the top quintile group and short the bottom quintile of the selected styles. A larger number of styles would be selected if styles are ranked equally by the ranking scores.

Performance Subsequent one-month performance based on equally weighted the select styles

Source: Nomura Quantitative Strategies

Exhibit 11 explains how combined style ranking scores are derived using the latest style rankings in Asia Pacific ex Japan region.

Exhibit 11. Current ranking of styles (March 2011)

Values Ranks Combined

E/P spread

z-scoreB/P spread

z-score Style

momentumE/P spread

z-scoreB/P spread

z-scoreStyle

momentum Score Rank

Size (0.57) (0.75) 0.86 5 8 6 6.3 8

Momentum 0.33 0.67 2.77 2 2 5 3.2 3

Yield (0.85) (0.37) 3.44 8 6 4 5.8 7

Valuation (0.64) (0.66) 7.58 6 7 1 4.3 4

Revision 1.51 (0.07) 3.63 1 5 3 3 2

Growth (0.75) 0.93 (1.20) 7 1 7 5.2 5

Profitability (0.44) 0.50 4.02 4 3 2 2.9 1

Risk (0.24) 0.45 (2.79) 3 4 8 5.3 6

Note: Since MSCI AC APxJ February return is -1.9%, the equation: combined score = 30% x E/P spread rank + 30% x B/P spread rank + 40% x style momentum (6M) rank is applied.

Source: Nomura Quantitative Strategies

... select the top ranking styles

We present how our model derives the latest rankings in Asia

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 10

Performance and results for Asia Pacific ex Japan

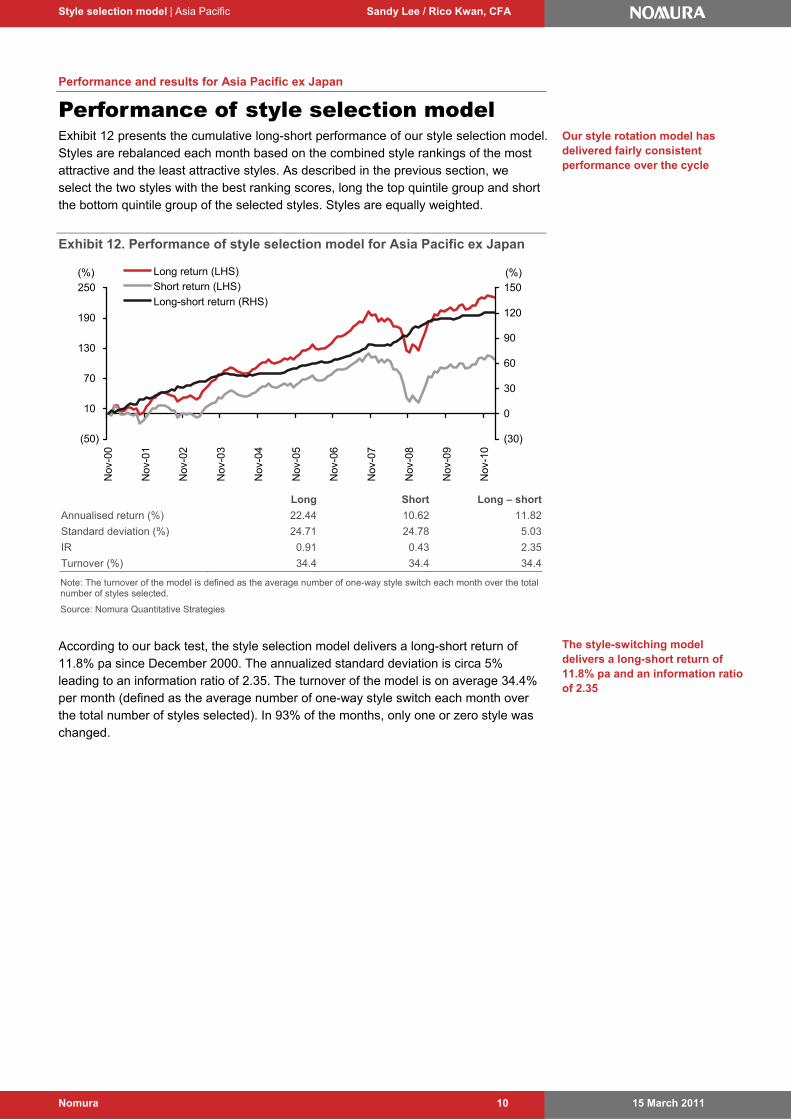

Performance of style selection model Exhibit 12 presents the cumulative long-short performance of our style selection model. Styles are rebalanced each month based on the combined style rankings of the most attractive and the least attractive styles. As described in the previous section, we select the two styles with the best ranking scores, long the top quintile group and short the bottom quintile group of the selected styles. Styles are equally weighted.

Exhibit 12. Performance of style selection model for Asia Pacific ex Japan

(50)

10

70

130

190

250

Nov

-00

Nov

-01

Nov

-02

Nov

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Nov

-08

Nov

-09

Nov

-10

(%)

(30)

0

30

60

90

120

150

(%)Long return (LHS)

Short return (LHS)

Long-short return (RHS)

Long Short Long – short

Annualised return (%) 22.44 10.62 11.82

Standard deviation (%) 24.71 24.78 5.03

IR 0.91 0.43 2.35

Turnover (%) 34.4 34.4 34.4

Note: The turnover of the model is defined as the average number of one-way style switch each month over the total number of styles selected.

Source: Nomura Quantitative Strategies

According to our back test, the style selection model delivers a long-short return of 11.8% pa since December 2000. The annualized standard deviation is circa 5% leading to an information ratio of 2.35. The turnover of the model is on average 34.4% per month (defined as the average number of one-way style switch each month over the total number of styles selected). In 93% of the months, only one or zero style was changed.

Our style rotation model has delivered fairly consistent performance over the cycle

The style-switching model delivers a long-short return of 11.8% pa and an information ratio of 2.35

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 11

Exhibit 13. Performance of Asia style selection model versus alternative style selectors

(20)

0

20

40

60

80

100

120

140

No

v-00

No

v-01

No

v-02

No

v-03

No

v-04

No

v-05

No

v-06

No

v-07

No

v-08

No

v-09

No

v-10

(%) Our style selection model

Relative-value only

Short-term style mtm only

50-50 value & style mtm

Average of 8 styles

Long – short performance

Our style model (relative-value +

style momentum + risk proxy)

Relative-value only

Short-term style

momentum only

50-50 between relative-value

& style momentum

Average of eight style

indices

Annualised return (%) 11.82 7.78 9.96 10.56 3.94

Standard deviation (%) 5.03 4.59 5.80 4.79 2.45

IR 2.35 1.69 1.72 2.21 1.61

Turnover (%) 34.4 40.9 21.7 32.4 -

Note: The turnover of the model is defined as the average number of one-way style switch each month over the total number of styles selected.

Source: Nomura Quantitative Strategies

In Exhibit 13, we compare performance of our style selection model with alternative style selectors using criterion based on: 1) solely long-term relative value; 2) only short-term style momentum approach, 3) a 50-50 allocation between relative value and style momentum; and 4) the average performance of the eight investment style indices. We note that in Asia Pacific ex Japan region, an approach using solely relative value or only relative strength to select styles will bring similar information ratios, suggesting both strategies provide a reliable source of alpha. However, using just relative-value approach to select styles will convey a lower return but a lower risk compared with a pure style-momentum approach to simply go long the recent outperforming styles and short the recent underperforming styles. We observe that the correlation of monthly returns between relative-value and relative-strength strategies is -0.03, indicating the source of alpha generated by style-momentum approach is not correlated with the alpha from picking styles based on relative value. Thus, we believe combining these strategies offers diversification opportunity.

Our style selection model that combines relative-value and relative-strength signals plus adding on a risk-aversion proxy delivers a comparatively consistent return and higher information ratio compared with alternate style selectors that focus on only relative value or style momentum. We thus conclude that this systematic style rotation model to allocate the factor exposure over time in a dynamic way works in the Asia region.

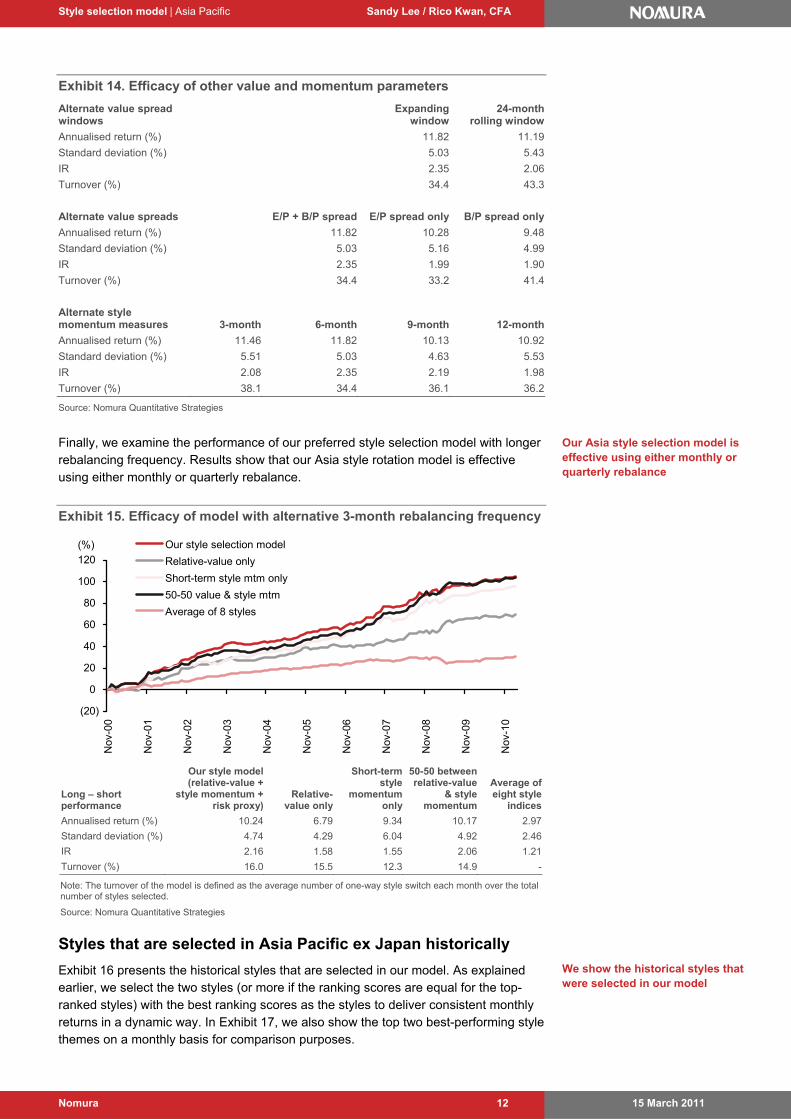

We also have examined the effectiveness of alternative parameters to define relative value and relative strength of styles. Exhibit 14 reviews the style selection model performance using different parameters. On relative value, for instance, currently our style selection model considers the Z score of E/P and B/P spread using an expanding window, but here we show the results that apply a 24-month rolling window and use either the E/P or B/P value spread. In addition, we display results that use alternative time periods to define the short-term relative-strength of styles, including 3, 6, 9, and 12 months. Results confirm that our preferred style selection model yields a better information ratio than these alternatives.

In the region, using just relative-value approach to select styles will convey a lower return but a lower risk compared with a pure style-momentum approach

Our model to combine relative-value and relative-strength signals plus adding on a risk-aversion proxy yields higher information ratio

Our preferred style selection model yields a better information ratio than other alternatives using different parameters to define relative value and relative strength of styles

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 12

Exhibit 14. Efficacy of other value and momentum parameters

Alternate value spread windows

Expanding window

24-month rolling window

Annualised return (%) 11.82 11.19

Standard deviation (%) 5.03 5.43

IR 2.35 2.06

Turnover (%) 34.4 43.3

Alternate value spreads E/P + B/P spread E/P spread only B/P spread only

Annualised return (%) 11.82 10.28 9.48

Standard deviation (%) 5.03 5.16 4.99

IR 2.35 1.99 1.90

Turnover (%) 34.4 33.2 41.4

Alternate style momentum measures 3-month 6-month 9-month 12-month

Annualised return (%) 11.46 11.82 10.13 10.92

Standard deviation (%) 5.51 5.03 4.63 5.53

IR 2.08 2.35 2.19 1.98

Turnover (%) 38.1 34.4 36.1 36.2

Source: Nomura Quantitative Strategies

Finally, we examine the performance of our preferred style selection model with longer rebalancing frequency. Results show that our Asia style rotation model is effective using either monthly or quarterly rebalance.

Exhibit 15. Efficacy of model with alternative 3-month rebalancing frequency

(20)

0

20

40

60

80

100

120

Nov

-00

Nov

-01

Nov

-02

Nov

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Nov

-08

Nov

-09

Nov

-10

(%) Our style selection model

Relative-value only

Short-term style mtm only

50-50 value & style mtm

Average of 8 styles

Long – short performance

Our style model (relative-value +

style momentum + risk proxy)

Relative-value only

Short-term style

momentum only

50-50 between relative-value

& style momentum

Average of eight style

indices

Annualised return (%) 10.24 6.79 9.34 10.17 2.97

Standard deviation (%) 4.74 4.29 6.04 4.92 2.46

IR 2.16 1.58 1.55 2.06 1.21

Turnover (%) 16.0 15.5 12.3 14.9 -

Note: The turnover of the model is defined as the average number of one-way style switch each month over the total number of styles selected.

Source: Nomura Quantitative Strategies

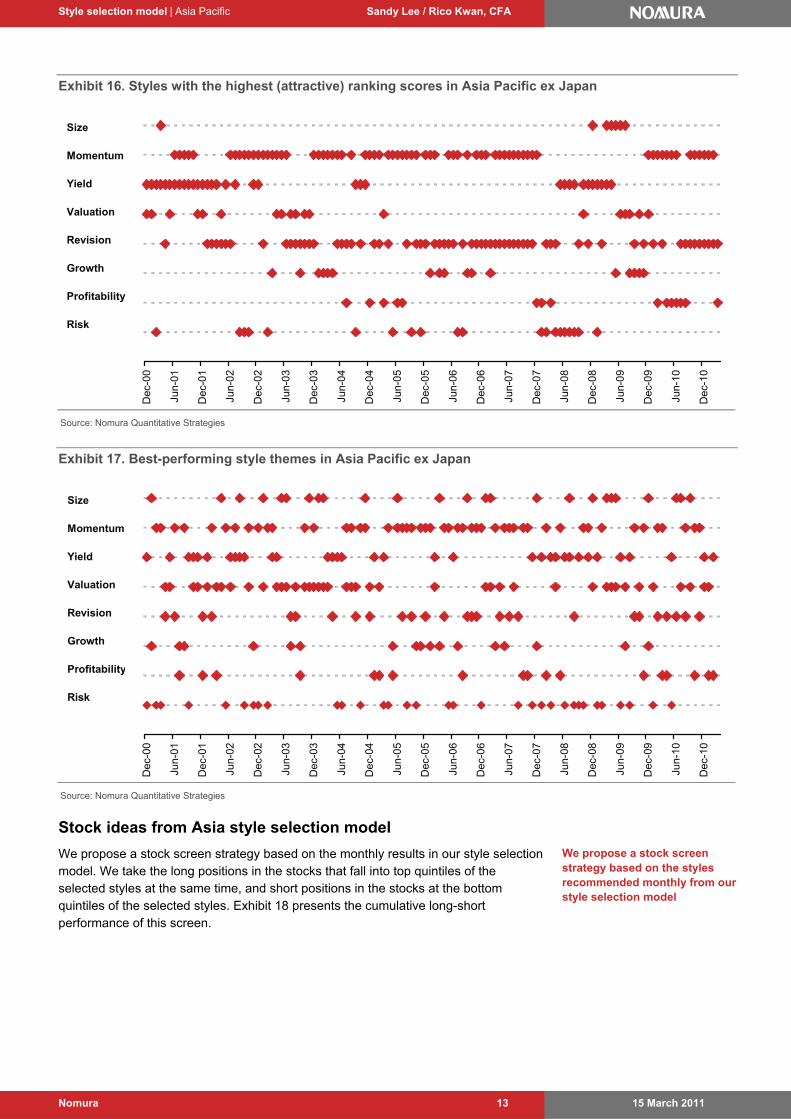

Styles that are selected in Asia Pacific ex Japan historically

Exhibit 16 presents the historical styles that are selected in our model. As explained earlier, we select the two styles (or more if the ranking scores are equal for the top-ranked styles) with the best ranking scores as the styles to deliver consistent monthly returns in a dynamic way. In Exhibit 17, we also show the top two best-performing style themes on a monthly basis for comparison purposes.

Our Asia style selection model is effective using either monthly or quarterly rebalance

We show the historical styles that were selected in our model

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 13

Exhibit 16. Styles with the highest (attractive) ranking scores in Asia Pacific ex Japan

Dec

-00

Jun-

01

Dec

-01

Jun-

02

Dec

-02

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Size

Momentum

Yield

Valuation

Revision

Growth

Profitability

Risk

Source: Nomura Quantitative Strategies

Exhibit 17. Best-performing style themes in Asia Pacific ex Japan

Dec

-00

Jun-

01

Dec

-01

Jun-

02

Dec

-02

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Size

Momentum

Yield

Valuation

Revision

Growth

Profitability

Risk

Source: Nomura Quantitative Strategies

Stock ideas from Asia style selection model

We propose a stock screen strategy based on the monthly results in our style selection model. We take the long positions in the stocks that fall into top quintiles of the selected styles at the same time, and short positions in the stocks at the bottom quintiles of the selected styles. Exhibit 18 presents the cumulative long-short performance of this screen.

We propose a stock screen strategy based on the styles recommended monthly from our style selection model

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 14

Exhibit 18. Performance of stock screen based on the results of style selection model for Asia Pacific ex Japan

(50)

0

50

100

150

200

250

300

Nov

-00

Nov

-01

Nov

-02

Nov

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Nov

-08

Nov

-09

Nov

-10

(%)

(50)

0

50

100

150

200

250

(%)Long portfolio

Short portfolio

Asia Pacific ex-Japan

Long-short return (RHS)

Long Short APxJ Long – short

Annualised return (%) 25.48 4.71 16.03 20.77

Standard deviation (%) 24.99 24.64 24.59 9.37

IR 1.02 0.19 0.65 2.22

Turnover (%) 69.2 69.0 4.8 138.2

Number of stocks 46 40 605 85

Note: Asia Pacific ex-JP benchmark is the equal weighted return of the MSCI AC Asia Pacific ex-Japan universe, rebalanced monthly.

Source: Nomura Quantitative Strategies

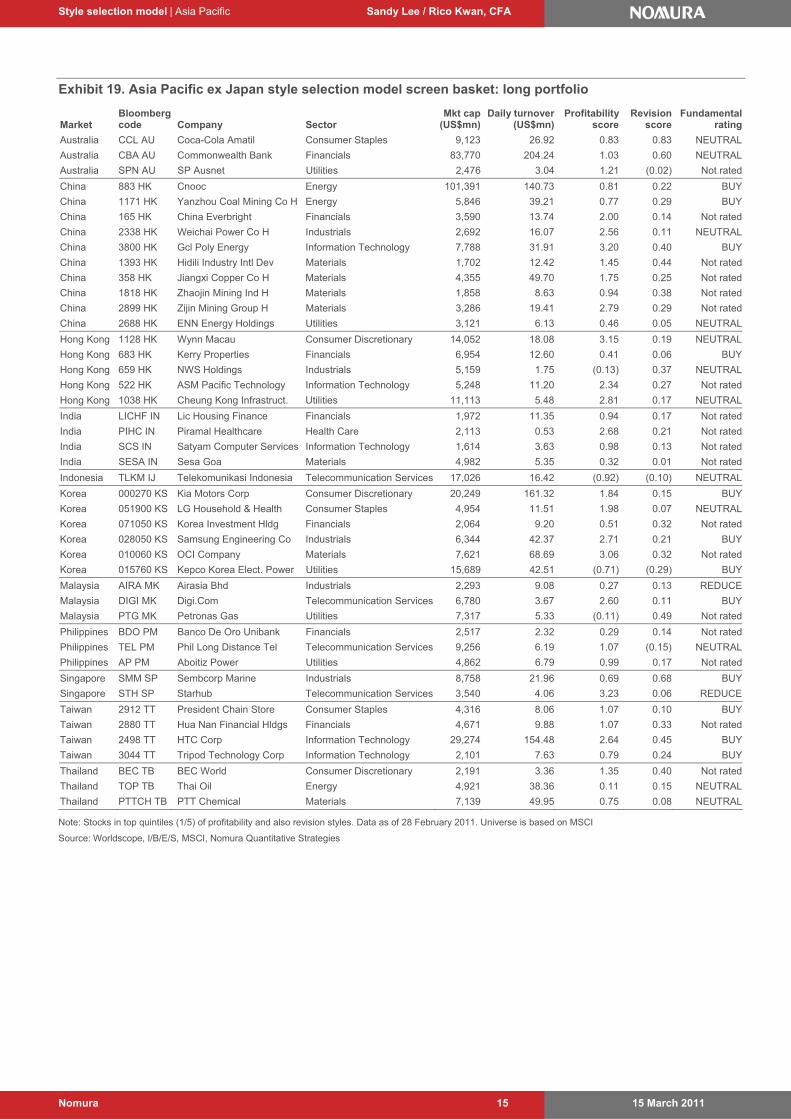

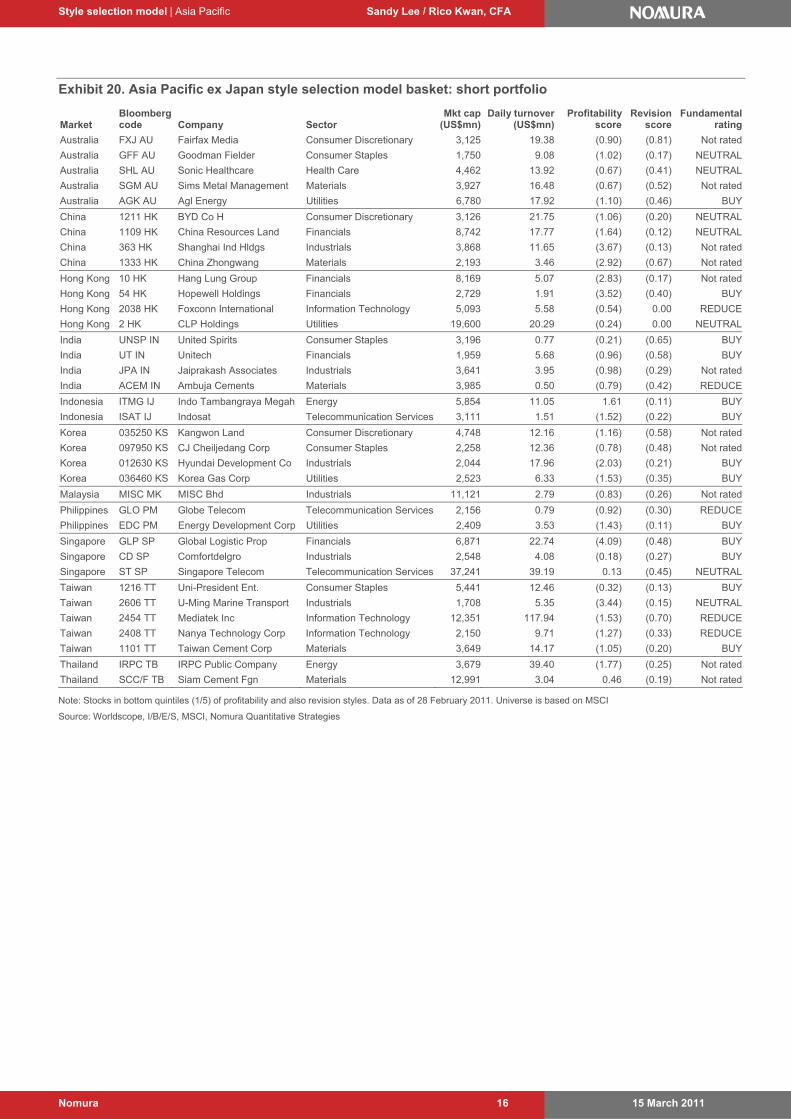

Our model selects Profitability and Revision as the most attractive styles in March. Exhibits 19 and 20 present a stock screen based on the underlying factors in these two styles. We take the long positions in the stocks with best profitability scores and with good earnings revisions, and short positions in the stocks with the worst profitability scores and with the worst earnings revisions.

We present stock screen ideas based on the latest styles recommended from our style selection model

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 15

Exhibit 19. Asia Pacific ex Japan style selection model screen basket: long portfolio

Market Bloomberg code Company Sector

Mkt cap (US$mn)

Daily turnover (US$mn)

Profitability score

Revision score

Fundamental rating

Australia CCL AU Coca-Cola Amatil Consumer Staples 9,123 26.92 0.83 0.83 NEUTRAL

Australia CBA AU Commonwealth Bank Financials 83,770 204.24 1.03 0.60 NEUTRAL

Australia SPN AU SP Ausnet Utilities 2,476 3.04 1.21 (0.02) Not rated

China 883 HK Cnooc Energy 101,391 140.73 0.81 0.22 BUY

China 1171 HK Yanzhou Coal Mining Co H Energy 5,846 39.21 0.77 0.29 BUY

China 165 HK China Everbright Financials 3,590 13.74 2.00 0.14 Not rated

China 2338 HK Weichai Power Co H Industrials 2,692 16.07 2.56 0.11 NEUTRAL

China 3800 HK Gcl Poly Energy Information Technology 7,788 31.91 3.20 0.40 BUY

China 1393 HK Hidili Industry Intl Dev Materials 1,702 12.42 1.45 0.44 Not rated

China 358 HK Jiangxi Copper Co H Materials 4,355 49.70 1.75 0.25 Not rated

China 1818 HK Zhaojin Mining Ind H Materials 1,858 8.63 0.94 0.38 Not rated

China 2899 HK Zijin Mining Group H Materials 3,286 19.41 2.79 0.29 Not rated

China 2688 HK ENN Energy Holdings Utilities 3,121 6.13 0.46 0.05 NEUTRAL

Hong Kong 1128 HK Wynn Macau Consumer Discretionary 14,052 18.08 3.15 0.19 NEUTRAL

Hong Kong 683 HK Kerry Properties Financials 6,954 12.60 0.41 0.06 BUY

Hong Kong 659 HK NWS Holdings Industrials 5,159 1.75 (0.13) 0.37 NEUTRAL

Hong Kong 522 HK ASM Pacific Technology Information Technology 5,248 11.20 2.34 0.27 Not rated

Hong Kong 1038 HK Cheung Kong Infrastruct. Utilities 11,113 5.48 2.81 0.17 NEUTRAL

India LICHF IN Lic Housing Finance Financials 1,972 11.35 0.94 0.17 Not rated

India PIHC IN Piramal Healthcare Health Care 2,113 0.53 2.68 0.21 Not rated

India SCS IN Satyam Computer Services Information Technology 1,614 3.63 0.98 0.13 Not rated

India SESA IN Sesa Goa Materials 4,982 5.35 0.32 0.01 Not rated

Indonesia TLKM IJ Telekomunikasi Indonesia Telecommunication Services 17,026 16.42 (0.92) (0.10) NEUTRAL

Korea 000270 KS Kia Motors Corp Consumer Discretionary 20,249 161.32 1.84 0.15 BUY

Korea 051900 KS LG Household & Health Consumer Staples 4,954 11.51 1.98 0.07 NEUTRAL

Korea 071050 KS Korea Investment Hldg Financials 2,064 9.20 0.51 0.32 Not rated

Korea 028050 KS Samsung Engineering Co Industrials 6,344 42.37 2.71 0.21 BUY

Korea 010060 KS OCI Company Materials 7,621 68.69 3.06 0.32 Not rated

Korea 015760 KS Kepco Korea Elect. Power Utilities 15,689 42.51 (0.71) (0.29) BUY

Malaysia AIRA MK Airasia Bhd Industrials 2,293 9.08 0.27 0.13 REDUCE

Malaysia DIGI MK Digi.Com Telecommunication Services 6,780 3.67 2.60 0.11 BUY

Malaysia PTG MK Petronas Gas Utilities 7,317 5.33 (0.11) 0.49 Not rated

Philippines BDO PM Banco De Oro Unibank Financials 2,517 2.32 0.29 0.14 Not rated

Philippines TEL PM Phil Long Distance Tel Telecommunication Services 9,256 6.19 1.07 (0.15) NEUTRAL

Philippines AP PM Aboitiz Power Utilities 4,862 6.79 0.99 0.17 Not rated

Singapore SMM SP Sembcorp Marine Industrials 8,758 21.96 0.69 0.68 BUY

Singapore STH SP Starhub Telecommunication Services 3,540 4.06 3.23 0.06 REDUCE

Taiwan 2912 TT President Chain Store Consumer Staples 4,316 8.06 1.07 0.10 BUY

Taiwan 2880 TT Hua Nan Financial Hldgs Financials 4,671 9.88 1.07 0.33 Not rated

Taiwan 2498 TT HTC Corp Information Technology 29,274 154.48 2.64 0.45 BUY

Taiwan 3044 TT Tripod Technology Corp Information Technology 2,101 7.63 0.79 0.24 BUY

Thailand BEC TB BEC World Consumer Discretionary 2,191 3.36 1.35 0.40 Not rated

Thailand TOP TB Thai Oil Energy 4,921 38.36 0.11 0.15 NEUTRAL

Thailand PTTCH TB PTT Chemical Materials 7,139 49.95 0.75 0.08 NEUTRAL

Note: Stocks in top quintiles (1/5) of profitability and also revision styles. Data as of 28 February 2011. Universe is based on MSCI

Source: Worldscope, I/B/E/S, MSCI, Nomura Quantitative Strategies

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 16

Exhibit 20. Asia Pacific ex Japan style selection model basket: short portfolio

Market Bloomberg code Company Sector

Mkt cap (US$mn)

Daily turnover (US$mn)

Profitability score

Revision score

Fundamental rating

Australia FXJ AU Fairfax Media Consumer Discretionary 3,125 19.38 (0.90) (0.81) Not rated

Australia GFF AU Goodman Fielder Consumer Staples 1,750 9.08 (1.02) (0.17) NEUTRAL

Australia SHL AU Sonic Healthcare Health Care 4,462 13.92 (0.67) (0.41) NEUTRAL

Australia SGM AU Sims Metal Management Materials 3,927 16.48 (0.67) (0.52) Not rated

Australia AGK AU Agl Energy Utilities 6,780 17.92 (1.10) (0.46) BUY

China 1211 HK BYD Co H Consumer Discretionary 3,126 21.75 (1.06) (0.20) NEUTRAL

China 1109 HK China Resources Land Financials 8,742 17.77 (1.64) (0.12) NEUTRAL

China 363 HK Shanghai Ind Hldgs Industrials 3,868 11.65 (3.67) (0.13) Not rated

China 1333 HK China Zhongwang Materials 2,193 3.46 (2.92) (0.67) Not rated

Hong Kong 10 HK Hang Lung Group Financials 8,169 5.07 (2.83) (0.17) Not rated

Hong Kong 54 HK Hopewell Holdings Financials 2,729 1.91 (3.52) (0.40) BUY

Hong Kong 2038 HK Foxconn International Information Technology 5,093 5.58 (0.54) 0.00 REDUCE

Hong Kong 2 HK CLP Holdings Utilities 19,600 20.29 (0.24) 0.00 NEUTRAL

India UNSP IN United Spirits Consumer Staples 3,196 0.77 (0.21) (0.65) BUY

India UT IN Unitech Financials 1,959 5.68 (0.96) (0.58) BUY

India JPA IN Jaiprakash Associates Industrials 3,641 3.95 (0.98) (0.29) Not rated

India ACEM IN Ambuja Cements Materials 3,985 0.50 (0.79) (0.42) REDUCE

Indonesia ITMG IJ Indo Tambangraya Megah Energy 5,854 11.05 1.61 (0.11) BUY

Indonesia ISAT IJ Indosat Telecommunication Services 3,111 1.51 (1.52) (0.22) BUY

Korea 035250 KS Kangwon Land Consumer Discretionary 4,748 12.16 (1.16) (0.58) Not rated

Korea 097950 KS CJ Cheiljedang Corp Consumer Staples 2,258 12.36 (0.78) (0.48) Not rated

Korea 012630 KS Hyundai Development Co Industrials 2,044 17.96 (2.03) (0.21) BUY

Korea 036460 KS Korea Gas Corp Utilities 2,523 6.33 (1.53) (0.35) BUY

Malaysia MISC MK MISC Bhd Industrials 11,121 2.79 (0.83) (0.26) Not rated

Philippines GLO PM Globe Telecom Telecommunication Services 2,156 0.79 (0.92) (0.30) REDUCE

Philippines EDC PM Energy Development Corp Utilities 2,409 3.53 (1.43) (0.11) BUY

Singapore GLP SP Global Logistic Prop Financials 6,871 22.74 (4.09) (0.48) BUY

Singapore CD SP Comfortdelgro Industrials 2,548 4.08 (0.18) (0.27) BUY

Singapore ST SP Singapore Telecom Telecommunication Services 37,241 39.19 0.13 (0.45) NEUTRAL

Taiwan 1216 TT Uni-President Ent. Consumer Staples 5,441 12.46 (0.32) (0.13) BUY

Taiwan 2606 TT U-Ming Marine Transport Industrials 1,708 5.35 (3.44) (0.15) NEUTRAL

Taiwan 2454 TT Mediatek Inc Information Technology 12,351 117.94 (1.53) (0.70) REDUCE

Taiwan 2408 TT Nanya Technology Corp Information Technology 2,150 9.71 (1.27) (0.33) REDUCE

Taiwan 1101 TT Taiwan Cement Corp Materials 3,649 14.17 (1.05) (0.20) BUY

Thailand IRPC TB IRPC Public Company Energy 3,679 39.40 (1.77) (0.25) Not rated

Thailand SCC/F TB Siam Cement Fgn Materials 12,991 3.04 0.46 (0.19) Not rated

Note: Stocks in bottom quintiles (1/5) of profitability and also revision styles. Data as of 28 February 2011. Universe is based on MSCI

Source: Worldscope, I/B/E/S, MSCI, Nomura Quantitative Strategies

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 17

Applying the same model for CSI 300 universe

Does style selection model work in China? We attempt to apply the same style selection model to the domestic China-A stock universe. As we have shorter factor history for China and need to consider long-term relative value of styles, we start the back testing since April 2007. Exhibit 21 presents the cumulative long-short performance of our style selection model using the CSI 300 universe and Exhibit 22 compares the model results with alternative style selectors. We note that short-selling activities are restricted for foreign investors in China, but investors can consider our results as an input in style allocation, as well as to adjust stock weights in their investment portfolios.

Exhibit 21. Performance of style selection model for China CSI 300

(30)

0

30

60

90

120

150

180

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

(%)

(10)

0

10

20

30

40

50

60

(%)Long return (LHS)

Short return (LHS)

Long-short return (RHS)

Long Short Long – short

Annualised return (%) 34.33 21.33 13.00

Standard deviation (%) 43.15 43.68 7.06

IR 0.80 0.49 1.84

Turnover (%) 41.3 41.3 41.3

Note: The turnover of the model is defined as the average number of one-way style switch each month over the total number of styles selected.

Source: Nomura Quantitative Strategies

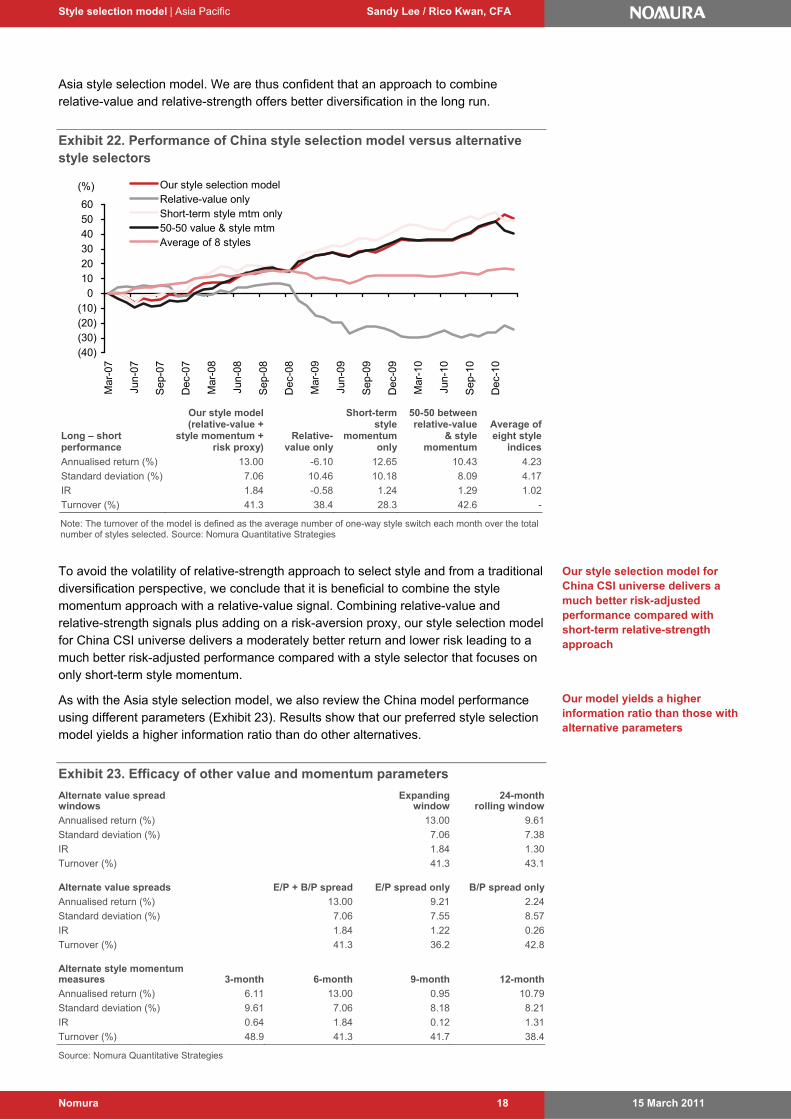

Despite the relatively shorter back-testing horizon, similar to our Asian model, our analysis of China shows that the style selection model also works for China companies. The model delivers a long-short return of 13.0% pa since April 2007. The annualized standard deviation is 7.1%, leading to an information ratio of 1.84.

Comparing Exhibit 22 with the results of Asia style selection model in Exhibit 13, we observe a notable difference between use of relative-value or relative-strength approach in the Asia Pacific ex Japan and China universes. A pure style-momentum approach – that goes long the outperforming styles in the past six months and short the underperforming styles – works best in the China CSI 300 universe. In fact, relying on just the relative value of styles does a poor job in selecting style themes during the observed period with a return of circa -6.1% pa. As such, a trend-following approach results in far better returns in China in the observed period compared with the one looking at long-term relative value of styles.

As a trend-following approach is much more effective in the back test, should we only employ such an approach to pick styles in China? First, we note that the back-testing period is quite short. Second, a pure relative-strength approach tends to suffer at turning points and when the market experiences a dramatic reversal. The underperformance of the relative-strength approach in the recent months is an obvious example. Further, notably the correlation of monthly returns between relative-value and relative-strength strategies is -0.37, which is more negatively correlated than is our

Applying the same model to the CSI 300 universe also sees good performance

A pure trend-following approach to select styles work well in China during the observed period, albeit with volatility especially at turning points

The correlation of monthly returns between relative-value and relative-strength strategies is -ve 0.37, implying diversification opportunity

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 18

Asia style selection model. We are thus confident that an approach to combine relative-value and relative-strength offers better diversification in the long run.

Exhibit 22. Performance of China style selection model versus alternative style selectors

(40)(30)(20)(10)

0102030405060

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

(%) Our style selection modelRelative-value onlyShort-term style mtm only50-50 value & style mtmAverage of 8 styles

Long – short performance

Our style model (relative-value +

style momentum + risk proxy)

Relative-value only

Short-term style

momentum only

50-50 between relative-value

& style momentum

Average of eight style

indices

Annualised return (%) 13.00 -6.10 12.65 10.43 4.23

Standard deviation (%) 7.06 10.46 10.18 8.09 4.17

IR 1.84 -0.58 1.24 1.29 1.02

Turnover (%) 41.3 38.4 28.3 42.6 -

Note: The turnover of the model is defined as the average number of one-way style switch each month over the total number of styles selected. Source: Nomura Quantitative Strategies

To avoid the volatility of relative-strength approach to select style and from a traditional diversification perspective, we conclude that it is beneficial to combine the style momentum approach with a relative-value signal. Combining relative-value and relative-strength signals plus adding on a risk-aversion proxy, our style selection model for China CSI universe delivers a moderately better return and lower risk leading to a much better risk-adjusted performance compared with a style selector that focuses on only short-term style momentum.

As with the Asia style selection model, we also review the China model performance using different parameters (Exhibit 23). Results show that our preferred style selection model yields a higher information ratio than do other alternatives.

Exhibit 23. Efficacy of other value and momentum parameters

Alternate value spread windows

Expanding window

24-month rolling window

Annualised return (%) 13.00 9.61

Standard deviation (%) 7.06 7.38

IR 1.84 1.30

Turnover (%) 41.3 43.1 Alternate value spreads E/P + B/P spread E/P spread only B/P spread only

Annualised return (%) 13.00 9.21 2.24

Standard deviation (%) 7.06 7.55 8.57

IR 1.84 1.22 0.26

Turnover (%) 41.3 36.2 42.8 Alternate style momentum measures 3-month 6-month 9-month 12-month

Annualised return (%) 6.11 13.00 0.95 10.79

Standard deviation (%) 9.61 7.06 8.18 8.21

IR 0.64 1.84 0.12 1.31

Turnover (%) 48.9 41.3 41.7 38.4

Source: Nomura Quantitative Strategies

Our style selection model for China CSI universe delivers a much better risk-adjusted performance compared with short-term relative-strength approach

Our model yields a higher information ratio than those with alternative parameters

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 19

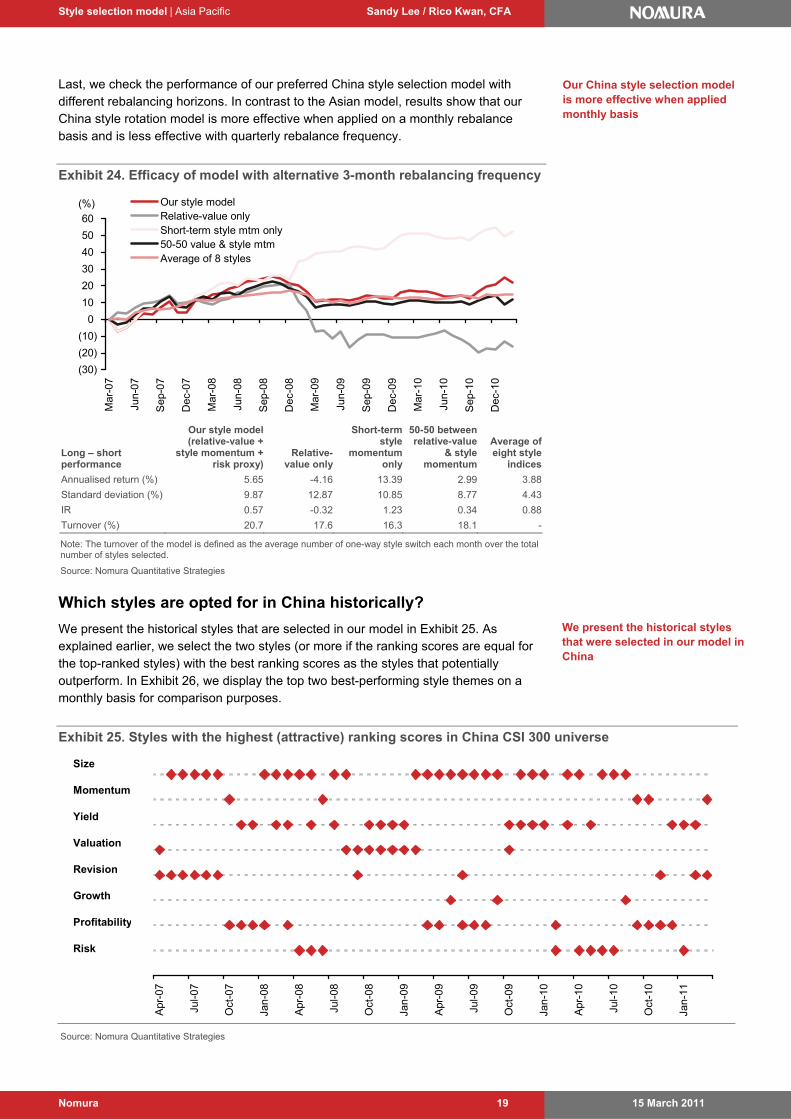

Last, we check the performance of our preferred China style selection model with different rebalancing horizons. In contrast to the Asian model, results show that our China style rotation model is more effective when applied on a monthly rebalance basis and is less effective with quarterly rebalance frequency.

Exhibit 24. Efficacy of model with alternative 3-month rebalancing frequency

(30)

(20)

(10)

0

10

20

30

40

50

60

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

(%) Our style modelRelative-value onlyShort-term style mtm only50-50 value & style mtmAverage of 8 styles

Long – short performance

Our style model (relative-value +

style momentum + risk proxy)

Relative-value only

Short-term style

momentum only

50-50 between relative-value

& style momentum

Average of eight style

indices

Annualised return (%) 5.65 -4.16 13.39 2.99 3.88

Standard deviation (%) 9.87 12.87 10.85 8.77 4.43

IR 0.57 -0.32 1.23 0.34 0.88

Turnover (%) 20.7 17.6 16.3 18.1 -

Note: The turnover of the model is defined as the average number of one-way style switch each month over the total number of styles selected.

Source: Nomura Quantitative Strategies

Which styles are opted for in China historically?

We present the historical styles that are selected in our model in Exhibit 25. As explained earlier, we select the two styles (or more if the ranking scores are equal for the top-ranked styles) with the best ranking scores as the styles that potentially outperform. In Exhibit 26, we display the top two best-performing style themes on a monthly basis for comparison purposes.

Exhibit 25. Styles with the highest (attractive) ranking scores in China CSI 300 universe

Apr

-07

Jul-0

7

Oct

-07

Jan

-08

Apr

-08

Jul-0

8

Oct

-08

Jan

-09

Apr

-09

Jul-0

9

Oct

-09

Jan

-10

Apr

-10

Jul-1

0

Oct

-10

Jan

-11

Size

Momentum

Yield

Valuation

Revision

Growth

Profitability

Risk

Source: Nomura Quantitative Strategies

We present the historical styles that were selected in our model in China

Our China style selection model is more effective when applied monthly basis

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 20

Exhibit 26. Best-performing style themes in China CSI 300 universe

Apr

-07

Jul-0

7

Oct

-07

Jan

-08

Apr

-08

Jul-0

8

Oct

-08

Jan

-09

Apr

-09

Jul-0

9

Oct

-09

Jan

-10

Apr

-10

Jul-1

0

Oct

-10

Jan

-11

Size

Momentum

Yield

Valuation

Revision

Growth

Profitability

Risk

Source: Nomura Quantitative Strategies

Stock ideas from China style selection model

The stock screen strategy we proposed also works well in the China CSI 300 universe. We take long positions in the stocks that fall into the top two quintiles of the selected styles simultaneously and short positions in the stocks at the bottom two quintiles of the selected styles. We use two quintiles instead of one, such that our China CSI 300 screen contains a reasonable number of stocks. Exhibit 27 presents the cumulative long-short performance of this screen.

Exhibit 27. Performance of stock screen based on the results of style selection model for China CSI 300 universe

(50)

0

50

100

150

200

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

(%)

(25)

0

25

50

75

100

(%)Long portfolio Short portfolio

CSI 300 Long-short return (RHS)

Long Short CSI 300 Long – short

Annualised return (%) 40.00 19.18 25.88 20.83

Standard deviation (%) 42.07 44.65 44.26 12.88

IR 0.95 0.43 0.58 1.62

Turnover (%) 64.3 60.3 5.6 124.6

Number of stocks 39 40 300 78

Note: CSI 300 is the equal weighted return of the China CSI 300 Index universe, rebalanced monthly.

Source: Nomura Quantitative Strategies

The stock screen strategy we proposed also works well in China

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 21

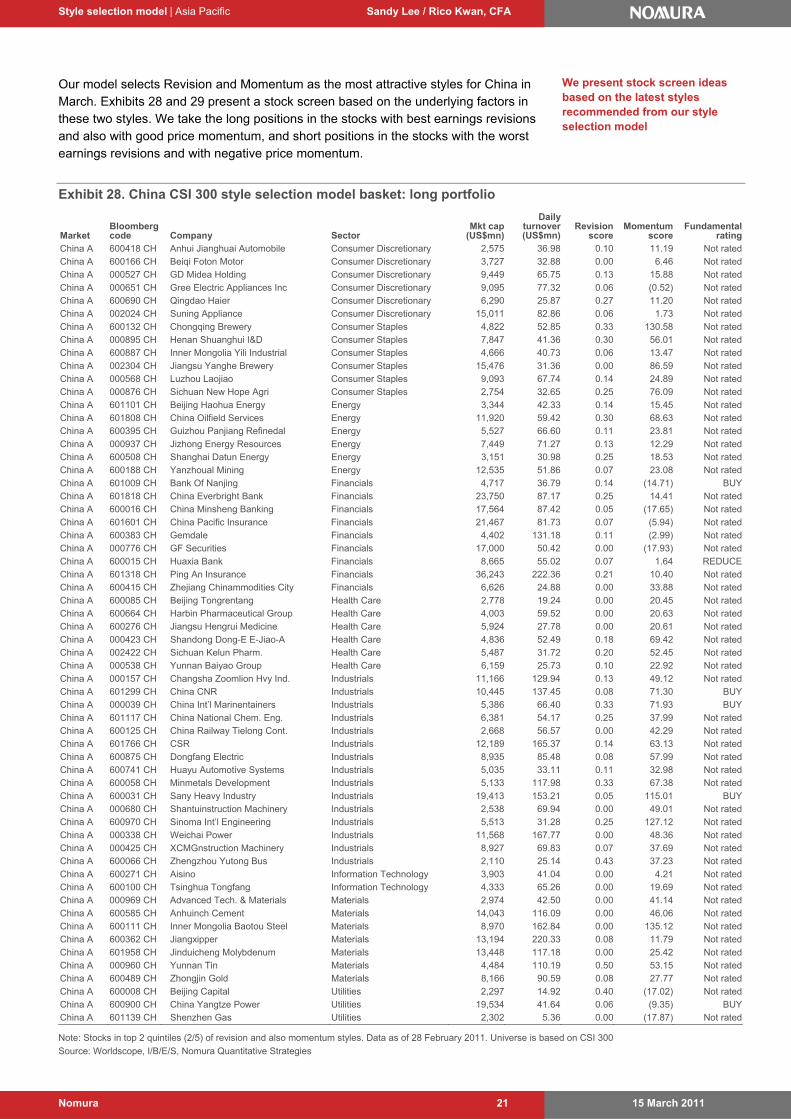

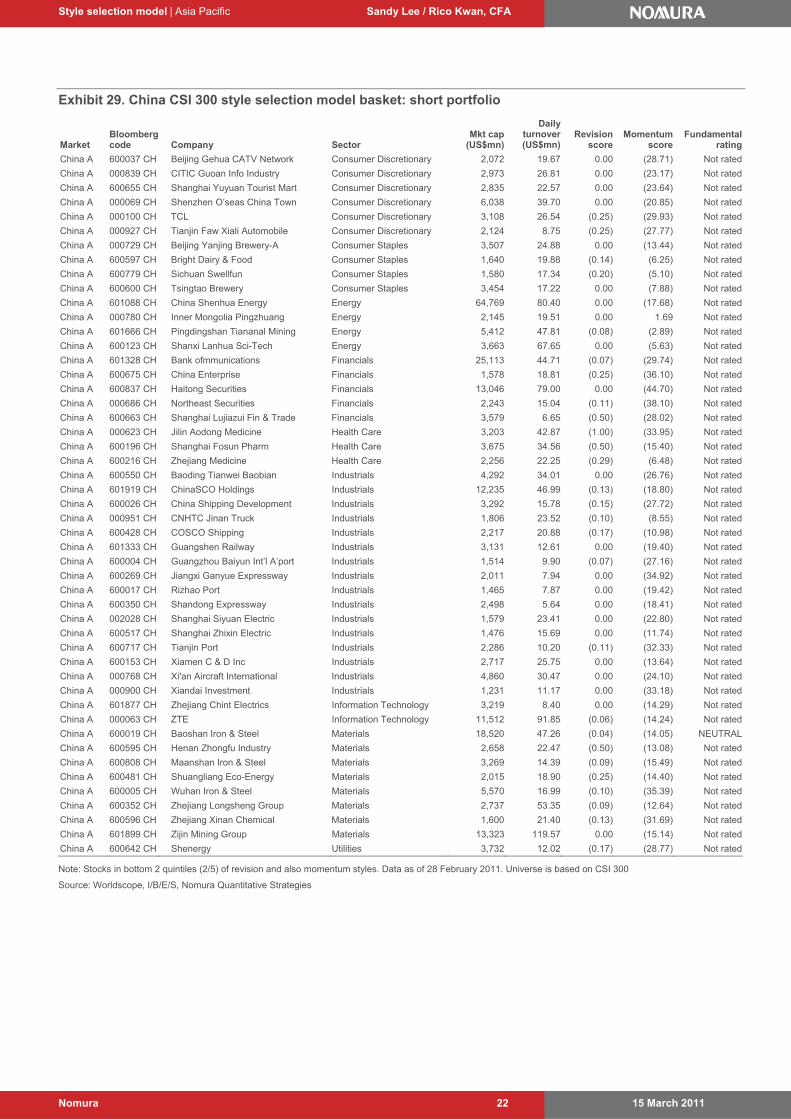

Our model selects Revision and Momentum as the most attractive styles for China in March. Exhibits 28 and 29 present a stock screen based on the underlying factors in these two styles. We take the long positions in the stocks with best earnings revisions and also with good price momentum, and short positions in the stocks with the worst earnings revisions and with negative price momentum.

Exhibit 28. China CSI 300 style selection model basket: long portfolio

Market Bloomberg code Company Sector

Mkt cap (US$mn)

Daily turnover (US$mn)

Revision score

Momentum score

Fundamental rating

China A 600418 CH Anhui Jianghuai Automobile Consumer Discretionary 2,575 36.98 0.10 11.19 Not ratedChina A 600166 CH Beiqi Foton Motor Consumer Discretionary 3,727 32.88 0.00 6.46 Not ratedChina A 000527 CH GD Midea Holding Consumer Discretionary 9,449 65.75 0.13 15.88 Not rated

China A 000651 CH Gree Electric Appliances Inc Consumer Discretionary 9,095 77.32 0.06 (0.52) Not ratedChina A 600690 CH Qingdao Haier Consumer Discretionary 6,290 25.87 0.27 11.20 Not ratedChina A 002024 CH Suning Appliance Consumer Discretionary 15,011 82.86 0.06 1.73 Not rated

China A 600132 CH Chongqing Brewery Consumer Staples 4,822 52.85 0.33 130.58 Not ratedChina A 000895 CH Henan Shuanghui I&D Consumer Staples 7,847 41.36 0.30 56.01 Not ratedChina A 600887 CH Inner Mongolia Yili Industrial Consumer Staples 4,666 40.73 0.06 13.47 Not rated

China A 002304 CH Jiangsu Yanghe Brewery Consumer Staples 15,476 31.36 0.00 86.59 Not ratedChina A 000568 CH Luzhou Laojiao Consumer Staples 9,093 67.74 0.14 24.89 Not ratedChina A 000876 CH Sichuan New Hope Agri Consumer Staples 2,754 32.65 0.25 76.09 Not rated

China A 601101 CH Beijing Haohua Energy Energy 3,344 42.33 0.14 15.45 Not ratedChina A 601808 CH China Oilfield Services Energy 11,920 59.42 0.30 68.63 Not ratedChina A 600395 CH Guizhou Panjiang Refinedal Energy 5,527 66.60 0.11 23.81 Not rated

China A 000937 CH Jizhong Energy Resources Energy 7,449 71.27 0.13 12.29 Not ratedChina A 600508 CH Shanghai Datun Energy Energy 3,151 30.98 0.25 18.53 Not ratedChina A 600188 CH Yanzhoual Mining Energy 12,535 51.86 0.07 23.08 Not rated

China A 601009 CH Bank Of Nanjing Financials 4,717 36.79 0.14 (14.71) BUYChina A 601818 CH China Everbright Bank Financials 23,750 87.17 0.25 14.41 Not ratedChina A 600016 CH China Minsheng Banking Financials 17,564 87.42 0.05 (17.65) Not rated

China A 601601 CH China Pacific Insurance Financials 21,467 81.73 0.07 (5.94) Not ratedChina A 600383 CH Gemdale Financials 4,402 131.18 0.11 (2.99) Not ratedChina A 000776 CH GF Securities Financials 17,000 50.42 0.00 (17.93) Not rated

China A 600015 CH Huaxia Bank Financials 8,665 55.02 0.07 1.64 REDUCEChina A 601318 CH Ping An Insurance Financials 36,243 222.36 0.21 10.40 Not ratedChina A 600415 CH Zhejiang Chinammodities City Financials 6,626 24.88 0.00 33.88 Not rated

China A 600085 CH Beijing Tongrentang Health Care 2,778 19.24 0.00 20.45 Not ratedChina A 600664 CH Harbin Pharmaceutical Group Health Care 4,003 59.52 0.00 20.63 Not ratedChina A 600276 CH Jiangsu Hengrui Medicine Health Care 5,924 27.78 0.00 20.61 Not rated

China A 000423 CH Shandong Dong-E E-Jiao-A Health Care 4,836 52.49 0.18 69.42 Not ratedChina A 002422 CH Sichuan Kelun Pharm. Health Care 5,487 31.72 0.20 52.45 Not ratedChina A 000538 CH Yunnan Baiyao Group Health Care 6,159 25.73 0.10 22.92 Not rated

China A 000157 CH Changsha Zoomlion Hvy Ind. Industrials 11,166 129.94 0.13 49.12 Not ratedChina A 601299 CH China CNR Industrials 10,445 137.45 0.08 71.30 BUYChina A 000039 CH China Int’l Marinentainers Industrials 5,386 66.40 0.33 71.93 BUY

China A 601117 CH China National Chem. Eng. Industrials 6,381 54.17 0.25 37.99 Not ratedChina A 600125 CH China Railway Tielong Cont. Industrials 2,668 56.57 0.00 42.29 Not ratedChina A 601766 CH CSR Industrials 12,189 165.37 0.14 63.13 Not rated

China A 600875 CH Dongfang Electric Industrials 8,935 85.48 0.08 57.99 Not ratedChina A 600741 CH Huayu Automotive Systems Industrials 5,035 33.11 0.11 32.98 Not ratedChina A 600058 CH Minmetals Development Industrials 5,133 117.98 0.33 67.38 Not rated

China A 600031 CH Sany Heavy Industry Industrials 19,413 153.21 0.05 115.01 BUYChina A 000680 CH Shantuinstruction Machinery Industrials 2,538 69.94 0.00 49.01 Not ratedChina A 600970 CH Sinoma Int’l Engineering Industrials 5,513 31.28 0.25 127.12 Not rated

China A 000338 CH Weichai Power Industrials 11,568 167.77 0.00 48.36 Not ratedChina A 000425 CH XCMGnstruction Machinery Industrials 8,927 69.83 0.07 37.69 Not ratedChina A 600066 CH Zhengzhou Yutong Bus Industrials 2,110 25.14 0.43 37.23 Not rated

China A 600271 CH Aisino Information Technology 3,903 41.04 0.00 4.21 Not ratedChina A 600100 CH Tsinghua Tongfang Information Technology 4,333 65.26 0.00 19.69 Not ratedChina A 000969 CH Advanced Tech. & Materials Materials 2,974 42.50 0.00 41.14 Not rated

China A 600585 CH Anhuinch Cement Materials 14,043 116.09 0.00 46.06 Not ratedChina A 600111 CH Inner Mongolia Baotou Steel Materials 8,970 162.84 0.00 135.12 Not ratedChina A 600362 CH Jiangxipper Materials 13,194 220.33 0.08 11.79 Not rated

China A 601958 CH Jinduicheng Molybdenum Materials 13,448 117.18 0.00 25.42 Not ratedChina A 000960 CH Yunnan Tin Materials 4,484 110.19 0.50 53.15 Not ratedChina A 600489 CH Zhongjin Gold Materials 8,166 90.59 0.08 27.77 Not rated

China A 600008 CH Beijing Capital Utilities 2,297 14.92 0.40 (17.02) Not ratedChina A 600900 CH China Yangtze Power Utilities 19,534 41.64 0.06 (9.35) BUYChina A 601139 CH Shenzhen Gas Utilities 2,302 5.36 0.00 (17.87) Not rated

Note: Stocks in top 2 quintiles (2/5) of revision and also momentum styles. Data as of 28 February 2011. Universe is based on CSI 300

Source: Worldscope, I/B/E/S, Nomura Quantitative Strategies

We present stock screen ideas based on the latest styles recommended from our style selection model

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 22

Exhibit 29. China CSI 300 style selection model basket: short portfolio

Market Bloomberg code Company Sector

Mkt cap (US$mn)

Daily turnover (US$mn)

Revision score

Momentum score

Fundamental rating

China A 600037 CH Beijing Gehua CATV Network Consumer Discretionary 2,072 19.67 0.00 (28.71) Not rated

China A 000839 CH CITIC Guoan Info Industry Consumer Discretionary 2,973 26.81 0.00 (23.17) Not rated

China A 600655 CH Shanghai Yuyuan Tourist Mart Consumer Discretionary 2,835 22.57 0.00 (23.64) Not rated

China A 000069 CH Shenzhen O’seas China Town Consumer Discretionary 6,038 39.70 0.00 (20.85) Not rated

China A 000100 CH TCL Consumer Discretionary 3,108 26.54 (0.25) (29.93) Not rated

China A 000927 CH Tianjin Faw Xiali Automobile Consumer Discretionary 2,124 8.75 (0.25) (27.77) Not rated

China A 000729 CH Beijing Yanjing Brewery-A Consumer Staples 3,507 24.88 0.00 (13.44) Not rated

China A 600597 CH Bright Dairy & Food Consumer Staples 1,640 19.88 (0.14) (6.25) Not rated

China A 600779 CH Sichuan Swellfun Consumer Staples 1,580 17.34 (0.20) (5.10) Not rated

China A 600600 CH Tsingtao Brewery Consumer Staples 3,454 17.22 0.00 (7.88) Not rated

China A 601088 CH China Shenhua Energy Energy 64,769 80.40 0.00 (17.68) Not rated

China A 000780 CH Inner Mongolia Pingzhuang Energy 2,145 19.51 0.00 1.69 Not rated

China A 601666 CH Pingdingshan Tiananal Mining Energy 5,412 47.81 (0.08) (2.89) Not rated

China A 600123 CH Shanxi Lanhua Sci-Tech Energy 3,663 67.65 0.00 (5.63) Not rated

China A 601328 CH Bank ofmmunications Financials 25,113 44.71 (0.07) (29.74) Not rated

China A 600675 CH China Enterprise Financials 1,578 18.81 (0.25) (36.10) Not rated

China A 600837 CH Haitong Securities Financials 13,046 79.00 0.00 (44.70) Not rated

China A 000686 CH Northeast Securities Financials 2,243 15.04 (0.11) (38.10) Not rated

China A 600663 CH Shanghai Lujiazui Fin & Trade Financials 3,579 6.65 (0.50) (28.02) Not rated

China A 000623 CH Jilin Aodong Medicine Health Care 3,203 42.87 (1.00) (33.95) Not rated

China A 600196 CH Shanghai Fosun Pharm Health Care 3,675 34.56 (0.50) (15.40) Not rated

China A 600216 CH Zhejiang Medicine Health Care 2,256 22.25 (0.29) (6.48) Not rated

China A 600550 CH Baoding Tianwei Baobian Industrials 4,292 34.01 0.00 (26.76) Not rated

China A 601919 CH ChinaSCO Holdings Industrials 12,235 46.99 (0.13) (18.80) Not rated

China A 600026 CH China Shipping Development Industrials 3,292 15.78 (0.15) (27.72) Not rated

China A 000951 CH CNHTC Jinan Truck Industrials 1,806 23.52 (0.10) (8.55) Not rated

China A 600428 CH COSCO Shipping Industrials 2,217 20.88 (0.17) (10.98) Not rated

China A 601333 CH Guangshen Railway Industrials 3,131 12.61 0.00 (19.40) Not rated

China A 600004 CH Guangzhou Baiyun Int’l A’port Industrials 1,514 9.90 (0.07) (27.16) Not rated

China A 600269 CH Jiangxi Ganyue Expressway Industrials 2,011 7.94 0.00 (34.92) Not rated

China A 600017 CH Rizhao Port Industrials 1,465 7.87 0.00 (19.42) Not rated

China A 600350 CH Shandong Expressway Industrials 2,498 5.64 0.00 (18.41) Not rated

China A 002028 CH Shanghai Siyuan Electric Industrials 1,579 23.41 0.00 (22.80) Not rated

China A 600517 CH Shanghai Zhixin Electric Industrials 1,476 15.69 0.00 (11.74) Not rated

China A 600717 CH Tianjin Port Industrials 2,286 10.20 (0.11) (32.33) Not rated

China A 600153 CH Xiamen C & D Inc Industrials 2,717 25.75 0.00 (13.64) Not rated

China A 000768 CH Xi'an Aircraft International Industrials 4,860 30.47 0.00 (24.10) Not rated

China A 000900 CH Xiandai Investment Industrials 1,231 11.17 0.00 (33.18) Not rated

China A 601877 CH Zhejiang Chint Electrics Information Technology 3,219 8.40 0.00 (14.29) Not rated

China A 000063 CH ZTE Information Technology 11,512 91.85 (0.06) (14.24) Not rated

China A 600019 CH Baoshan Iron & Steel Materials 18,520 47.26 (0.04) (14.05) NEUTRAL

China A 600595 CH Henan Zhongfu Industry Materials 2,658 22.47 (0.50) (13.08) Not rated

China A 600808 CH Maanshan Iron & Steel Materials 3,269 14.39 (0.09) (15.49) Not rated

China A 600481 CH Shuangliang Eco-Energy Materials 2,015 18.90 (0.25) (14.40) Not rated

China A 600005 CH Wuhan Iron & Steel Materials 5,570 16.99 (0.10) (35.39) Not rated

China A 600352 CH Zhejiang Longsheng Group Materials 2,737 53.35 (0.09) (12.64) Not rated

China A 600596 CH Zhejiang Xinan Chemical Materials 1,600 21.40 (0.13) (31.69) Not rated

China A 601899 CH Zijin Mining Group Materials 13,323 119.57 0.00 (15.14) Not rated

China A 600642 CH Shenergy Utilities 3,732 12.02 (0.17) (28.77) Not rated

Note: Stocks in bottom 2 quintiles (2/5) of revision and also momentum styles. Data as of 28 February 2011. Universe is based on CSI 300

Source: Worldscope, I/B/E/S, Nomura Quantitative Strategies

Style selection model | Asia Pacific Sandy Lee / Rico Kwan, CFA

15 March 2011 Nomura 23

Appendix

Definition of factors