Interbank Mobile Payment Service. Interbank Mobile Payment Services Instant!!!! ^

Upload

sachin-kajaveCategory

view

106download

0

A

PROJECT REPORT

ON

“A Study of Foreign Exchange Remittances

And

Interbank Dealings”

FOR

NKGSB CO-OP.BANK LTD.

MASTER OF MANAGEMENT STUDIES (MMS)

UNIVERSITY OF MUMBAI

SUBMITTED TO

MARATHA MANDIR’S

BABASAHEB GAWDE INSTITUTE OF

MANAGEMENT STUDIES

MUMBAI CENTRAL

SUBMITTED BY: SACHIN KAJAVE

BATCH:

ROLL NO: 19

DECLARATION

I, Sachin P. Kajave student of Masters of Management Studies (Semester III) of

Babasaheb Gawde Institute of Management Studies (BGIMS), hereby declare that I have

successfully completed this project on “STUDY OF FOREIGN EXCHANGE

REMITTANCES AND INTERBANK DEALINGS” as a part of my ‘Summer

Internship’. The information incorporated in this project is true and original to the best of

my knowledge.

____________________________________

Signature

CERTIFICATE

ACKNOWLEDGEMENT

My sincere gratitude to NKGSB Co-op Bank Ltd for providing me with an

opportunity to work in the Banking Sector. I take this opportunity to acknowledge the

efforts of all those individuals who have helped me in making the project.

First and foremost, I am highly indebted to my Industry guide and Mentor Mr. Nirmal

Parekh, Assistant Manager and Mrs. Poonam Madam, Forex Department, NKGSB

for their guidance and constant supervision as well as for providing necessary

information regarding the project & completion of the project. Without their vision and

support this project would not have been so beneficial to me in which I had worked.

I would also like to express my gratitude to Ms. Sanchita and Ms. Shambhavi

Forex Dept., NKGSB Co-op Bank Ltd, Girgaum Branch for their timely guidance and

valuable experience that they shared with me during my project and sincerely appreciate

their suggestions, encouragement and approachability from day one through the end and

for making the one and half month period a memory to cherish.

I gratefully thank our Director and all the faculty members and my friends for adding

value to my knowledge base by providing with valuable insights into the completion of

this project and sharpening me for the corporate world.

INDEXChapter

No CONTENTS Page No.

1. Executive Summary 1

2. Introduction to project 2

3. Objectives of Study 10

4. Research methodology 11

5. NKGSB profile 13

6. Foreign exchange market

7. Forex Department & their functions

8. Remittance overview

8.1 Benefits of remittances 14

8.2 Types of remittances 21

8.3 Operating model in remittance business 23

8.4 Remittance transaction process

9. NKGSB’s AD II activities 25

9.1 Purposes of Remittances

10. Inter Bank dealings 69

10.1 Procedure & Documentation required 71

10.2 Purchase and Sale of Foreign Currency Travelers cheques (FTC)

10.3 Purchase and Sale of Foreign Currency notes (FC)

11. Travel Currency card

Advantages Of Travel Currency Cards

12. Recommendation and suggestions 78

13. Conclusion 79

14. Bibliography 80

Executive Summary

During one and half month period, NKGSB bank has given greater opportunity to work

with Forex Department and learn how Banks play an important role in Foreign Exchange

Remittances, Trade Finance activities and also Foreign Exchange currency convertibility

transaction. Though the process can be done without banks but for the security of the

payment and assurance of the Credit worthiness of the parties’ banks plays a major role to

it.

In this globalizing world, migration of people from one country to another

for employment opportunities h a s b e c o m e a c o m m o n phenomenon.

Dominant migration corridors have been formed between various countries/regions.

Documentary Credits mainly Letter of Credit is involved in the process of the importing

and exporting of goods through Banks, as some of the foreign exchange transactions and

applications are studies. It is universal processes accepted by all the countries dealing in

forex and adheres to terms and agreement from WTO and strict guidelines given by

Reserve Bank of India for trading in India. This work gives brief information about

Benefits of remittances and various purposes of remittances.

During this study, I have found out Foreign Remittance business may follow the

conventional banking model or any of the non-banking models. As studying there are

their views regarding the LC process and charges relating to it. There are too many banks

who are dealing with Forex so there is intense competition among all of them for

providing better services to the customers. However the margin or Credit given by all the

banks differs from each other. RBI is playing a very important role in maintaining strict

guidelines for Banks in India, Traders in India, Traders outside India and Foreign Banks.

Since my project states Trade Finance activities and foreign exchange currency dealing

especially inward remittance and Outward remittance which has given a new scenario to

all the New Traders on how to function in import/export activities and Various Tariffs

regarding import/export of goods into India and what all Process has to be followed with

what sort of documents, Licenses required.

1.1 Introduction to project

Globalization and financial liberalization in India have brought about enormous changes

in the financial functioning of the economy, as a result of which, the resultant gain of the

global integration of domestic and foreign financial markets has thrown open new

opportunities but at the same time exposed the financial system to significant risks.

Until 1991 before liberalization, India was isolated from the world markets, to protect its

economy as they fear of the colonization and to achieve self-reliance. Foreign trade was

highly difficult as import tariffs were extremely high around 300%, export taxes was also

levied and also quantitative restrictions, while foreign direct investment(FDI) was

restricted by high-limit equity participation, there were restrictions on technology

transfer, and government approvals.

This could be explained by the invoicing of imports in India in US dollars (80-90 per

cent) and the presence of menu cost in changing invoice price. For small exchange rate

change, it is not worthwhile to change the invoice price of imports in its own currency

due to the menu cost (a fixed cost involved in altering invoice price). Thus, the import

price in local currency (domestic prices) would change by the extent of the exchange rate

change, i.e., a higher pass-through. Invoicing pattern of trade, exchange rate movements

and exchange rate pass-through to domestic prices, thus, have implications for exchange

rate management and trade competitiveness.

It recommended that banks be allowed to initiate cross currency positions abroad and to

lend or borrow short-term funds up to six months, subject to a specified ceiling. Another

important suggestion related to allowing exporters and importers to retain 100 per cent of

their earnings in any foreign currency with an Authorised Dealer (AD) in India, subject to

liquidation of outstanding advances against export bills.

There are possibilities that the visible cost advantage apparently gained by the firm may

erode if the export or import risk factors were not properly identified and managed.

This project has been prepared with such focus on the issues faced to types of foreign

exchange dealing and techniques to resolves the issues faced by export/import

International trade and finance.

1.2 Objective of Research/Study

Study the operation of foreign exchange markets and alternative exchange rate systems.

Acquire essential skills for managing foreign exchange risks and operating exposure.

Operations for the bank in an informed and effective manner.

To utilize new process improvements for operational efficiency.

To understand the Operating model in remittance business.

To equip participants with the updated acknowledge for Trade Finance.

To acquire skills to understand how Interbank Dealings is done in the bank.

1.3 Research Methodology

Historical Research Design –

The purpose is to collect, verify, synthesize evidence to establish facts that defend or

refute your hypothesis. It uses primary sources, secondary sources, and lots of

qualitative data sources such as logs, diaries, official records, reports, etc. The limitation

is that the sources must be both authentic and valid.

Sources of Data

Data Collections from various sources like,

RBI circulars

Bank’s Forex Management Guide Book.

Banks official website

Journals on Foreign Exchange

Indian Institute of Banking and Finance’s book on

Practitioners of Trade Finance

Statistical Tools used in the study- Presentations in Graphical Form.

Limitations

(a) Unavailability of the data from the Bank.

(b) The study is limited to period to one and half months only

Introduction

Migrant remittances are a steadily growing external source of capital for

developing countries. While foreign direct investments and capital market flows fell

sharply in the last years due to the recession in the high income countries, migrant

remittances continued to grow, reaching USD 149.4 billion in 2002. The importance of

remittances in compensating the human capital loss of developing countries through

Migration and their potential in boosting economic growth was already recognised in the

beginning of the 1980s. A wide range of issues related to remittances became the subject

of political debate, as well as of more in-depth research. These topics include the

determinants of remittances, the transfer channels used and their economic impact on the

remittance receiving countries. Over the past years, partly because of the sharp increase

in remittance flows, the research on these issues gained momentum, resulting in a

mushrooming of scientific literature.

This introduction presents a critical overview of the state-of-art literature on

remittances and is organized as follows: in the following section, the data on migrant

remittances, methods of estimating the amounts of remittance flows, global and regional

trends in remittance flows, and their importance as a source of capital for developing

countries, are discussed. The third section gives an overview of the theoretical and

empirical research on the determinants of remittances and the following section outlines

the transfer channels, the cost involved with international money transfers and the

evolutions of money transfer markets. The last two sections examine the literature on the

effects of remittances on inequality, growth and the balance of payments, and present the

conclusions.

Banking Sector: An overview

Banking Regulation Act of India, 1949 defines Banking as “accepting, for the

Purpose of lending or investment of deposits of money from the public, repayable on

demand or otherwise and withdraw able by cheques, drafts, and order or otherwise.”

Most of activities a Bank performs are derived from the above definition. In

addition, Banks are allowed to perform certain activities which are ancillary to this

business of accepting deposits and lending. A bank’s relationship with the public,

therefore, revolves around accepting deposits and lending money. Another activity which

is assuming increasing importance is transfer of money –both domestic and foreign –

from one place to another. This activity is generally known as “remittance business” in

banking parlance. The so called forex (foreign exchange) business is largely a part of

remittance albeit it involves buying and selling of foreign currencies.

The law governing Banking Activities in India is called “Negotiation Instruments

Act 1881”. The banking activities can be classified as:

Accepting Deposits from public/others (Deposits)

Lending money to public (Loans)

Transferring money from one place to another (Remittances)

Acting as trustees

Acting as intermediaries

Keeping valuables in safe custody

Collecting Business

Government business

Co-operative Banks Defined

A co-operative bank is a financial entity which belongs to its members, who are at the

same time the owners and the customers of their bank. Co-operative banks are often

created by persons belonging to the same local or professional community or sharing a

common interest.

Co-operative banks generally provide their members with a wide range of banking and

financial services (loans, deposits, banking accounts).

Introduction of Cooperative Bank

Cooperative banking is retail and commercial banking organized on a cooperative basis.

Cooperative banking institutions take deposits and lend money in most parts of the world.

Cooperative banking (for the purposes of this article), includes retail banking, as carried

out by credit unions, mutual savings and loan associations, building societies and

cooperatives, as well as commercial banking services provided by mutual organizations

(such as cooperative federations) to cooperative businesses. Co-operative banks differ

from stockholder banks by their organization, their goals, their values and their

governance. In most countries, they are supervised and controlled by banking authorities

and have to respect prudential banking regulations, which put them at a level playing

field with stockholder banks. Depending on countries, this control and supervision can be

implemented directly by state entities or delegated to a co-operative federation or central

body. Even if their organizational rules can vary according to their respective national

legislations, co-operative banks share common features Customer-owned entities in a co-

operative bank, the needs of the customers meet the needs of the owners, as co-operative

bank members are both. As a consequence, the first aim of a co-operative bank is not to

maximize profit but to provide the best possible products and services to its members.

Some co-operative banks only operate with their members but most of them also admit

non-member clients to benefit from their banking and financial services. Democratic

member control: co-operative banks are owned and controlled by their members, who

democratically elect the board of directors. Members usually have equal voting rights,

according to the co-operative principle of “one person, one vote”. Profit allocation: in a

co-operative bank, a significant part of the yearly profit, benefits or surplus is usually

allocated to constitute reserves. A part of this profit can also be distributed to the co-

operative members, with legal or statutory limitations in most cases. Profit is usually

allocated to members either through a patronage dividend, which is related to the use of

the co-operatives products and services by each member, or through an interest or a

dividend, which is related to the number of shares subscribed by each member.

NKGSB Profile NKGSB was founded by a great visionary Sheth Shantaram Mangesh Kulkarni on

26th September, 1917.

The Bank with a modest beginning in 1917, is now a Multi-State Bank having its

area of operation in the States of Maharashtra, Karnataka, Goa, Gujarat and Union

territories of Daman, Diu, Dadra and Nagar Haveli.

Today the Bank has 64 branches spread over in the state of Maharashtra, Goa ,

Karnataka & Gujarat.

Mumbai - 34 branches

Navi Mumbai – Vashi, CBD Belapur, Panvel, Nerul, Kharghar & Kamothe (6

branches)

Maharashtra other than Mumbai - Pune – (Kothrud, Aundh, Chikhli, Chakan,

Bhosari & Magarpatta), Kolhapur – (Kolhapur Main & Uma talkies. These are

take over of Shahu Co-operative Bank, Ichalkaranji), Nashik – (Nashik & Am-

bad) & Sindhudurg – (Kudal) and Ratnagiri

Goa- Ponda, Panaji, Madgaon & Mapusa

Karnataka – Karwar- Main. Karwar -Baad, Hubli, Belgaum & Sirsi.

Gujarat – Vadodara, Surat.

Over the years, the Bank has consistently shown robust growth both quantitatively

and qualitatively. The Bank has not only grown in size of deposits and advances,

but has multiplied its net worth making the institution financially sound and fun-

damentally strong.

The Board of Directors of the Bank consists of well qualified professionals en-

riched with varied experience in the strategic fields of Finance, Technology, Busi-

ness and Management. Being driven by the co-operative principles, management

lays emphasis on profits but with focus on the welfare of our stakeholders.

As a part of good governance practice, the Bank has adopted code of good busi-

ness principles and accepted the responsibility to ensure that they are observed

down the line as a work culture in its true spirit. The business philosophy is based

on four core values i.e. pillars of service excellence, customer focus, product in-

novation and resourceful people.

In terms of our commitment for harnessing the state of art technology, networking

all 64 branches counter under ‘Core banking solution’, customers can access their

accounts and perform banking operations ‘anywhere anytime’ with value added

services.

The Bank has varied Deposit products to suit every needs of customers, so also

the bank has occupied a place of pride with those who are financed for offering

tailor-made complete credit solutions under one roof packaged at liberal, compet-

itive and flexible terms, let it be personal finance or loan facilities for Short term

as well Long term requirement of Small Businessman, Professionals, Small &

Medium Enterprises and Corporates.

The Bank has always been in the forefront to add on value to its products and has

entered into correspondent relationship and strategic alliances to offer best of the

services to its customers efficiently and with convenience such as:

Tied-up with Insurance Companies to sell both the insurance products, life insurance

with “Max New York Life” and non-life with “Oriental Insurance Company Ltd.”

A member of payment & settlement gateways of RBI through INFINET and

RTGS system by way of Electronic Fund Transfer (EFT) and Electronic Cheque

Clearing (ECC), which provides instant realization of funds & speedy remittances

including Electronic Clearing System (ECS) both account debit & credit.

Provides Demand Draft facility under arrangement with private sector bank

Amongst few Co-operative banks, having secured License as Authorised Dealer

Category II of RBI which offers sale and purchase of foreign exchange, foreign

remittances, etc.

Also caters to Forex business needs through foreign exchange arrangement made

with private sector bank.

Tied up with UAEXchange for fast inward remittance of foreign exchange.

Providing facilities - Pension a/cs, ‘SMS Banking’ and also ‘iConnect’ for hassle

free payment of taxes.

Tied up with NSDL as a Depository Participant offering Demat services at all our

branches

Management

Board of Directors is composed of eminent, well qualified professionals enriched

with varied experience in the strategic fields of Finance, Technology, Business and

Management. Being driven by the Co-operative principles, the management lays

emphasis on profits but with entire focus on the welfare of stakeholders.

As a part of good governance practice, the bank has adopted code of good business

principles and accepted the responsibility to ensure that they are observed down the

line as a work culture in its true spirit. The business philosophy is based on four

core value pillars of service excellence, customer focus, product innovation and

resourceful people.

Vision A premier co-operative bank

Operating Principles

We will make our Customers, Shareholders and Community at large very proud

We will always strive to provide Customers the best products and services that

leads to their progress and prosperity

We shall act with high level of integrity, achieving the set goals with active in-

volvement, devotion and commitment of our employees

SWOT Analysis:

Strengths:

Online Services: NEFT, RTGS, Online Login.

Advanced Infrastructure: Branches at NKGSB are well equipped that provide the

customers with taster banking services. All the computerized machines are located in

suitable manner & are very useful to the customers & staff of the bank.

Friendly Staff: The staff at NKGSB in all branches is very friendly & help the

customers in all cases. They provide faster services along with bonding & personal

relationship with the customers.

Banking Hours: It has Banking Hours from 8am to 8pm. It is more convenient to

customers.

Other Facilities to the Customers & Employees: NKGSB also provides other

facilities like drinking water facilities, proper sitting arrangements to the customers.

Money Transfer Banking: Newly introduced “Money Gram” by NKGSB to

facilitate all money transfers electronically can be wire transfer through this services,

hence provide greater value to customers in preference of time saving..

SMS Banking: NKGSB sends sms to its customers for their new products and

services and can be access from any place any where.

Weakness

No Proper Facilities to Uneducated customers: NKGSB provides all services

through electronic computerized machines. This creates problems to the less educated

people. But this threat falls in the 4th quadrant so it’s negligible. The company can

avoid this threat.

Opportunities

Increase in percentage of Returns on increase: The bank should provide

higher returns on deposits in comparison of the present situation. This will also

upto large extent help the bank earn profits & popularity.

Popularity in Investments in Capital Markets: As an on going situation as

market capitalization of NKGSB increases, it should increase its investments in

capital markets such as securities market, mutual fund and insurance.

Threats

Competition from Other already established Nationalized Banks.

Competition from Private Banks which provide more Speedy Transactions.

Net Services: NKGSB provides all kind of services on-line. There can be a

Threat of Hacking. The confidential information of the customers can be leaked

easily through the e-mail ids.

Foreign Exchange Market:

An Overview

The Foreign Exchange Regulation Act, 1973 (FERA) was repealed and a new Act called

the Foreign Exchange Management Act, 1999 (FEMA) came into force with effect from

June 1, 2000, with a view to facilitating external trade and payments and promoting

orderly development and maintenance of foreign exchange market in India.

The foreign exchange market exists wherever one currency is traded for another. It is by

far the largest market in the world, in terms of cash value traded, and includes trading

between large banks, central banks, currency

speculators, multinational corporations,

governments, and other financial markets and

institutions. The trade happening in the forex

markets across the globe currently exceeds

US$1.9 trillion/day (on average). Retail traders

(individuals) are currently a very small part of

this market and may only participate indirectly through brokers or banks.

The foreign exchange market provides the physical and institutional structure through

which the money of one country is exchanged for that of another country, the rate of

exchange between currencies is determined, and foreign exchange transactions are

physically completed.

The retail market for foreign exchange deals with transactions involving travelers and

tourists exchanging one currency for another in the form of currency notes or travelers’

cheques. The wholesale market often referred to as the interbank market is entirely

different and the participants in this market are commercial banks, corporations and

central banks.

Authorised Persons for Foreign Exchange Transaction

Foreign Exchange Management Act (FEMA) stipulates that all foreign exchange

transactions are required to be routed only through the entities that are licenced by the

Reserve Bank to undertake such transactions. Such entities are defined as Authorised

persons in Section 10 of the Act. Under current dispensation, such authorised person may

be:

a. A Commercial bank (AD), or

b. A Money changer (FFMC), or

c. Any financial institution authorized for limited kind of transactions, depending on their activity, or

d. Any other entity authorized by the Reserve Bank.

Foreign Exchange Market participants:

The foreign exchange market consists of two tiers:

The client or retail market and

The interbank or wholesale market

Five broad categories of participants operate within these two tiers:

1. Bank and nonbank foreign exchange dealers

Banks and a few nonbank foreign exchange dealers operate in both the interbank and

client markets. They profit from buying foreign exchange at a ‘bid’ price and reselling it

at a slightly higher ‘ask’ price. Dealers in the foreign exchange departments of large

international banks often function as market makers.

Currency trading is quite profitable for commercial and investment banks. Small to

medium sized banks are likely to participate but not as market makers in the interbank

market. Instead of maintaining significant inventory positions, they buy from and sell to

large banks to offset retail transactions with their own customers.

2. Individuals and firms conducting commercial or investment Transactions

Importers and exporters, international portfolio investors, Multi National Enterprises,

tourists, and others use the foreign exchange market to facilitate execution of commercial

or investment transactions. Some of these participants use the market to ‘hedge’ foreign

exchange risk.

3. Speculators and arbitragers

Speculators and arbitragers seek to profit from trading in the market itself. They operate

in their own interest, without a need or obligation to serve clients or to ensure a

continuous market. A large proportion of speculation and arbitrage is conducted on behalf

of major banks by traders employed by those banks. Thus banks act both as exchange

dealers and as speculators and arbitrages.

4. Central banks and treasuries

Central bank and treasuries use the market to acquire or spend their country’s foreign

exchange reserves as well as to influence the price at which their own currency is traded.

They may act to support the value of their own currency because of policies adopted at

the national level or because of commitments entered into through membership in joint

float agreements.

5. Foreign exchange brokers

Foreign exchange brokers are agents who facilitate trading between dealers. Brokers

charge small commission for the service provided to dealers. They maintain instant

access to hundreds of dealers world wide via open telephone lines.

Foreign Exchange Department

Vision

To evolve appropriate environment in discharging the basic objective of the For-

eign Exchange Management Act (FEMA), 1999;

To facilitate external trade and payments and to promote orderly development and

maintenance of foreign exchange market in India; and

To frame prompt and pro-active policy responses, as part of active capital account

management, within the evolving macroeconomic conditions.

Mission

To effectively integrate the needs of the users, both resident and non-resident, with the

evolving market dynamics and external sector developments by:

Evolving and disseminating rules and regulations in a user friendly language;

Moving towards fuller capital account convertibility in a calibrated manner;

Having regular interface with the users to assess their needs with greater focus on

the requirements of resident individuals / entities;

Rendering effective and efficient customer service with greater transparency;

Empowering authorized persons and enlarging their role as a conduit to create

awareness about the developments;

Facilitating hassle-free cross-border transactions;

Capturing data on a real time basis to dynamically induce policy changes; and

Disseminating data in a transparent manner.

Foreign Exchange department in a bank has following functions:

1. EXPORTS

Pre-shipment Advances

Post-shipment Advances

Export Guarantees

Advising/Confirming Letter of Credit

Facilitating project exports

Bills for collection

2. IMPORTS

Opening letters of credit

Advance bills

Import loans and guarantees.

3. EXCHANGE DEALINGS

Rate computation

Nostro/Vostro Accounts

Forward contracts

Derivatives

Exchange position and cover operations

4. REMITTANCES

Issue of DD, MT, TT etc.

Encashment of cheques, DD, MT, TT etc.

Issue and encashment of travelers' cheques

Sale and encashment of foreign currency notes

Non-resident deposits

5. STATISTICS

Submission of returns

Collection of credit information

Under the FEMA, foreign exchange transactions are divided into two broad categories -

current account and capital account transactions. Transactions that alter the assets or

liabilities, including contingent liabilities outside India, of persons resident in India or

assets or liabilities in India of persons resident outside India are classified as capital

account transactions. All other transactions are current account transactions.

Capital Account Transactions

Capital account transaction is defined as a transaction which:- Alters the assets or liabilities, including contingent liabilities, outside India of per-

sons resident in India. In other words, it includes those transactions which are

undertaken by a resident of India such that his/her assets or liabilities outside In-

dia are altered (either increased or decreased). For example: - (i) a resident of

India acquire an immovable property outside India or acquire shares of a foreign

company. This way his/her overseas assets are increased; or (ii) a resident of In-

dia borrows from a non-resident through External commercial Borrowings

(ECBs). This way he/she has created a liability outside India.

Alters the assets or liabilities in India of persons resident outside the India. In

other words, it includes those transactions which are undertaken by a non-resi-

dent such that his/her assets or liabilities in India are altered (either increased

or decreased). For example, (i) a non-resident acquire immovable property in

India or acquires shares of an Indian company or invest in a Wholly Owned

Subsidiary or a Joint Venture with a resident of India. This way his/her assets

in India are increased; or (ii) a non-resident borrows from Indian housing fi-

nance institute for acquiring a house in India. This way he/she has created a li-

ability in India.

The Act also contains a list of some of the most common capital account

transactions:-

Transfer or issue of any foreign security by a person resident in India;

Transfer or issue of any security by a person resident outside India;

Transfer or issue of any security or foreign security by any branch, of-

fice or agency in India of a person resident outside India;

Any borrowing or lending in rupees in whatever form or by whatever

name called;

Any borrowing or lending in rupees in whatever form or by whatever

name called between a person resident in India and a person resident

outside India;

Deposits between persons resident in India and persons resident out-

side India;

Export, import or holding of currency or currency notes;

Transfer of immovable property outside India, other than a lease not

exceeding five years, by a person resident in India;

Acquisition or transfer of immovable property in India, other than a

lease not exceeding five years, by a person resident outside India;

Giving of a guarantee or surety in respect of any debt, obligation or

other liability incurred-

(i) By a person resident in India and owed to a person resident outside

India; or

(ii) By a person resident outside India.

The Act has empowered the Reserve Bank of India (RBI) to specify, in consultation with

the Central Government, the permissible capital account transactions and the limits up to

which foreign exchange may be drawn for these transactions. But it shall not impose any

restriction on the drawal of foreign exchange for payments due on account of

amortization of loans or for depreciation of direct investments in the ordinary course of

business.

The FEMA Notification contains the list of permissible capital account transactions as

well as list of prohibited capital account transactions. The permitted capital account

transactions have been classified into two categories:-

Capital account transactions by persons resident in India includes,

Investment in foreign securities;

Foreign currency loans raised in India and abroad;

Acquisition and transfer of immovable property outside India;

Guarantees issued in favour of a person resident outside India;

Export, import and holding of currency or currency notes;

Loans and overdrafts (borrowings) from a person resident outside India;

Maintenance of foreign currency accounts in India and outside India;

Taking out the insurance policy from an insurance company outside India;

Remittance outside India of capital assets of a person resident in India;

Sale and purchase of foreign exchange derivatives in India and abroad and

commodity derivatives abroad.

Capital account transactions by non- residents includes,

Investment in India such as (i) issue of security by a body corporate or an

entity in India and investment therein by a non-resident and (ii) investment

by way of contribution to the capital of a firm or a proprietary concern or

an association of persons in India;

Acquisition and transfer of immovable property in India;

Guarantee in favour of, or on behalf of, a person resident in India;

Import and export of currency/currency notes into/from India;

Deposits between a person resident in India and a person resident outside

India;

Foreign currency accounts in India of a non-resident;

Remittance of the assets in India held by a non-resident.

There are generally two types of prohibitions on capital account transactions:-

General Prohibition: - A person shall not undertake or sell or draw foreign ex-

change to or from an authorized person for any capital account transaction. This

prohibition is subjected to the conditions specified by Reserve Bank in its circu-

lars and notifications. For example, Reserve Bank of India has issued an AP

(DIR) Circular, wherein a resident individual can draw from an authorized person

foreign exchange up to US$ 25,000 per calendar year for a capital account trans-

action specified in Schedule I to the Notification.

Special Prohibition:- A non resident person shall not make investment in India in

any form, in any company or partnership firm or proprietary concern or any en-

tity, whether incorporated or not, which is engaged or proposes to engage:- (i) in

the business of chit fund, or (ii) as Nidhi Company, or (iii) in agricultural or plan-

tation activities or (iv) in real estate business, or construction of farm houses or

(v) in trading in Transferable Development Rights (TDRs).

Current Account Transactions

The Act defines the term 'current account transaction' as a transaction other than a capital

account transaction and without prejudice to the generality of the foregoing such

transaction includes,

Payments due in connection with

Foreign trade,

Other current business,

Services and

Short-term banking and credit facilities in the ordinary course of business;

Payments due as

Interest on loans and

Net income from investments,

Remittances for living expenses of parents, spouse and children residing abroad and

Expenses in connection with

Foreign travel,

Education and Medical care of parents, spouse and children.

Medical care of parents, spouse and children.

Above definition implies that even if the transactions listed above may fit into the

definition of capital account transactions, such transactions shall be treated current

account transactions. For example, resident of India imports goods from outside India on

a short term credit (for a period of less than 6 months), he is creating a liability outside

India and thus, it can be treated a capital account transaction but, it is specifically

included in the above definition as a current account transaction. As a general rule, any

person may sell or draw foreign exchange if such sale or drawal is a current account

transaction. Under the Act, Central Government may, in public interest and in

consultation with the Reserve Bank, impose such reasonable restrictions for current

account transactions as may be prescribed. Accordingly, the Central Government has

issued the Foreign Exchange Management (Current Account Transaction) Rules. It

contains the list of current account transactions for which drawal of foreign exchange is:-

Totally prohibited;

Permitted, subject to the prior approval of concerned Ministry, Central

Government;

Permitted, subject to prior approval of the Reserve Bank of India;

No restrictions or limits are applicable for undertaking the transactions that are

not covered by the above rules and the authorized dealers are free to release

foreign exchange upon the satisfaction that the transactions will not involve and is

not designed for the purpose of, violation of the Act, or any rules, regulations

made there under.

In today's changed scenario, Indian rupee has become fully convertible so far as current

account transactions are concerned. This implies that foreign exchange is freely available

to the residents for remittance on account of current account transactions for the various

purposes like foreign travel, foreign education, and medical treatment abroad etc. The

non-residents are also freely allowed to remit outside India the income or capital gain

generated in India. But, even today, the Indian rupee, in respect of capital account

transactions, is not fully convertible.

REMITTANCE Overview

“Remittance is the act of transmitting money to a distant location to fulfill an obli-

gation”. A remittance is a transfer of money by a foreign worker to his or her home

country.

Money sent home by migrants constitutes the second largest financial inflow to many de-

veloping countries, exceeding international aid. Estimates of remittances to developing

countries vary from International Fund for Agricultural Development's US$301 billion

(including informal flows) to the World Bank's US$250 billion for 2006 (excluding infor-

mal flows). Remittances contribute to economic growth and to the livelihoods of people

worldwide. Moreover, remittance transfers can also promote access to financial ser-

vices for the sender and recipient, thereby increasing financial and social inclusion. Re-

mittances also foster, in the receiving countries, a further economic dependence on the

global economy instead of building sustainable, local economies.

Apart from accepting deposits and lending money, Banks also carry out, on behalf of

their customers the act of transfer of money - both domestic and foreign from one place

to another. This activity is known as "remittance business". Banks issue Demand Drafts,

Banker's Cheques and Money Orders etc. for transferring the money. Banks also have the

facility of quick transfer of money also know as Telegraphic Transfer or Tele Cash Or-

ders.

In Remittance business, Bank 'A' at a place 'a' accepts money from customer 'C' and

makes arrangement for payment of the same amount of money to either the customer 'C'

or his "order" i.e. a person or entity, designated by 'C' as the recipient, through either a

Branch of Bank 'A' or any other entity at place 'b'. In return for having rendered this ser-

vice, the Banks charge a pre-decided sum known as exchange or commission or service

charge. This sum can differ from bank to bank. This also differs depending upon the

mode of transfer and the time available for affecting the transfer of money.

Faster the mode of transfer, higher the charges.

Reasons:

In this globalizing world, migration of people from one country to another for

employment opportunities h a s b e c o m e a c o m m o n phenomenon. Dominant

migration corridors have been formed between various countries/regions. This is primar-

ily due to the socio-economic conditions prevailing in the migrants’ countries of origin

and destination. A few examples:

Migrant-sending country:

Lack of job opportunity

Lower wage rates

Social insecurity

Political instability

Extreme geographical conditions

Migrant-receiving country:

Availability of employment

Friendly migration policies

Shortage of skilled resources

Financial liberalization

Abundance of natural resources

A few examples of such corridors (sender country-receiving country) are Mexico-

US, South Asia-UAE and India-US.

Benefits of Remittances

Remittances are playing an increasingly large role in the economies of many countries,

contributing to economic growth and to the livelihoods of less prosperous people (though

generally not the poorest of the poor). According to World Bank estimates, remittances

totaled US$414 billion in 2009, of which US$316 billion went to developing countries

that involved 192 million migrant workers. For some individual recipient countries, re-

mittances can be as high as a third of their GDP. As remittance receivers often have a

higher propensity to own a bank account, remittances promote access to financial ser-

vices for the sender and recipient, an essential aspect of leveraging remittances to pro-

mote economic development

It’s easy to look at the numbers surrounding money sent overseas and realize that

there are a very large number of people who leave their home and families behind to pur-

sue better wages and opportunities in other countries. It is estimated that over $350 bil-

lion was sent to home countries from foreign lands in 2007 alone, most of it in monthly

installments of between $100 and $250.

In several countries with developing economies, remittances can make up as much as

one-third of a nation’s gross domestic product. When we look at the remittance market on

a macro level, we get an understanding of the sheer size of the money flowing to devel-

oping nations.

What we can’t get by looking at the numbers, however, is a sense of the decision making

process that goes into leaving one’s home, family, and country to pursue opportunities

overseas. Migrant workers often leave home with no guarantees or promises of jobs, only

hope that they will find something that suits them when they arrive at their destination.

Many leave home knowing that they will not see their children again for up to several

years. These workers leave home for a variety of reasons. For some, it is to escape the

clutches of poverty that pass from generation to generation in many developing countries.

For others, they leave a country with a corrupt or violent government in hopes of eventu-

ally building a new life abroad and then sending for their family to join them. No matter

the reason, the decision to leave is usually a difficult one that calls for great sacrifice both

for the worker moving abroad and the family staying behind.

Remittances do a great deal of good for developing economies, and their reach is more

powerful than helping family members buy groceries, clothing, and medicine.

The money that is sent in the form of remittances often is more than sufficient to meet the

daily needs of living in these small countries and it allows family members to save and

invest in themselves and their community. Developing nations would be wise to make the

remittance process as easy as possible to encourage even more money to be sent by citi-

zens working abroad.

In the United States, many migrant workers from the same home country have banded to-

gether to make the money they send home even more powerful. In addition to sending

money to their individual families, many workers will contribute to funds that are pooled

and used in times of need, such as after natural disasters.

For instance, Mexican immigrants in the United States have formed thousands of groups

to pool funds and send money to those who need it most. The Mexican government, real-

izing the potential for more money to flow into their country, has encouraged action such

as this by matching remittances sent through these organizations

Types of Remittances:

Foreign remittance can be defined as ‘the purchase and sale of freely convertible foreign

currencies as admissible under Exchange Control Regulations of the country’.

A looser translation is the sending of money home while working in a foreign country.

Thousands of people are currently working and living in a country that is not their home,

and sending funds regularly back to their families in their home country.

There are two types of remittances:

Foreign Inward Remittance: The receiving country, where the beneficiary resides.

The bank receives the money that has been sent from the sending person in the coun-

try in which the money has been earned. The term 'inward remittance" means pur-

chase of foreign currencies in whatever form and includes not only remittances by

M.T., T.T., draft etc., but also purchase of travellers cheques, drafts under travellers

letters of credit, bills of exchange, currency notes and coin etc. Debit to banks' non-

resident Rupee accounts also constitutes an inward remittance.

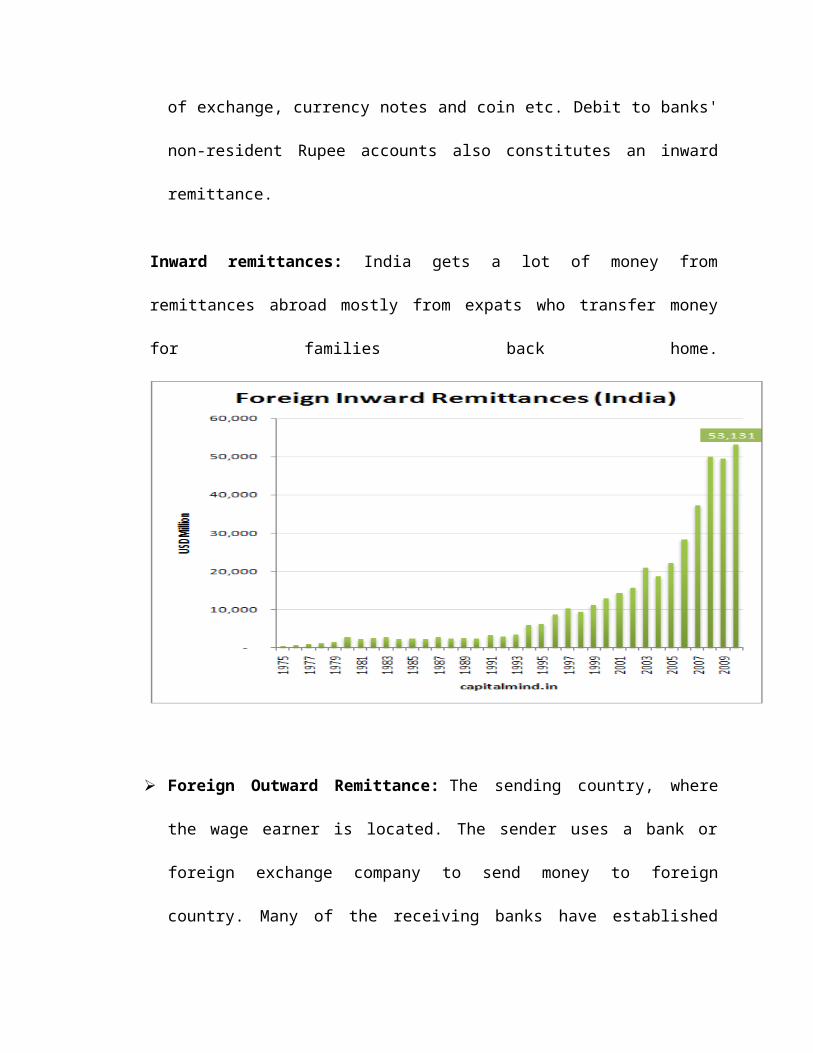

Inward remittances: India gets a lot of money from remittances abroad mostly from

expats who transfer money for families back home.

Foreign Outward Remittance: The sending country, where the wage earner is lo-

cated. The sender uses a bank or foreign exchange company to send money to foreign

country. Many of the receiving banks have established remittance relationships with

currency houses and banks in other countries to better facilitate the flow of remit-

tances into the country.

There is no restriction on receipt of remittances from abroad either in foreign currency

or by debit to non-resident Rupee accounts of banks' overseas branches or correspon-

dents. Authorised Dealers may freely purchase T.Ts, M.Ts, drafts, bills etc., expressed

and payable in foreign currencies or drawn in Rupees on banks' non-resident Rupee

accounts. There is also no objection to their obtaining reimbursement in foreign cur-

rency from their overseas branches and correspondents in respect of Rupee bills and

drafts which are purchased by them under letters of credit opened by non-resident

banks or under other arrangements.

Outward remittances: Indians like to give gifts to people abroad. They also like to

invest in international equity and debt. But they invest less in overseas deposits.

According to RBI data, money sent abroad by resident Indians crossed the $1 billion

mark for the first time in 2010-11. Between April and November of the current fiscal,

such outward remittances stood at $628 million or around Rs 3,000 crore, down 15 per

cent over a similar period in 2010-11. The dip was mainly on account of a drop in money

sent for maintenance of close relatives living abroad.

The RBI's liberalized remittance scheme currently allows residents to remit up to

$2,00,000 in a financial year for various purposes, both for capital and current account

transactions. From $25,000 in 2004, this limit has been increased over the years.

Investment made abroad in deposits, immovable property, equity or debt instruments are

all included under the scheme. Gift, donations, money spent on travel or for medical

treatment abroad, money sent for maintenance of close relatives living abroad as well as

funds used for studying overseas also fall under the scheme.

Investments abroad: Of these, well over a fifth of total remittances were made for

investing in equity and debt instruments abroad, both in 2010-11 and till November this

fiscal. This could be due to better performance by some of the markets and because of the

products or vehicles offered by portfolio/wealth management firms, for Indian investors

to diversify internationally.

Investments made in these overseas instruments expanded at a compounded annual rate

of 22 per cent in the last three years to $266 million in 2010-11. The same stood at $148

million for the eight months ending November 2011.

Although purchase of property rose to $66.3 million in 2010-11 after a dip in 2009-10, it

is still not as popular as investing in equity or debt.

Value of gifts: Indians also seem to splurge in gifting. At $242 million in 2010-11 and

$166.5 million till November 2011 of this fiscal, the value of gifts rose from 20 per cent

of total outward remittances last fiscal to 25 per cent this financial year so far. The RBI,

through a notification in September 2011, allowed gifts in the form of shares, debentures

or any security up to $50,000 in a financial year. This limit was earlier $25,000 a year.

Interestingly, money sent for maintenance of close relatives saw a sharp increase in 2010-

11 but has declined in 2011-12 thus far. For the eight months ending November 2011,

Indians sent $95 million under this category, down 46 per cent over a similar period a

year ago. Improved employment numbers in countries such as the US may have resulted

in Indians sending less money to their relatives abroad.

Operating Models In the Remittance Business

An International Remittance business may follow the conventional banking model or any

of the non-banking models.

Conventional Banking Model

In this model, an end-to-end remittance transaction involves the following parties:

• Remitter’s B a n k - Th e b a n k w h e r e t h e remitter has an account that is

debited for transferring money to the beneficiary

• Beneficiary’s Bank - The bank where the beneficiary of the remittance has

an account that is credited for the remittance money received

• Correspondent Bank (only in cases where the above-mentioned entities do

not have a direct business tie-up) - an intermediary bank which has

associated with various banks globally, through which remittance

transactions are routed

Figure 4 Nostro-based setup

Figure 4 illustrates the Nostro-based setup, wherein the Beneficiary Bank has an account with the Correspondent Bank, while

Figure 5 shows the generic process involved in a remittance transaction based on a Nostro account model.

Modes of Remittance

There are various Origination Modes, which are used by the remitter to transfer

money. The remitter can issue a remittance request to his bank either;

a. By visiting the branch and furnishing a Remittance Instruction Form

prescribed by the Remitting Bank, bearing all details necessary for effecting the

remittance along with an account debit mandate

or

b. By dropping a cheque from an account with the Remitting Bank along with the

Remittance Instruction Form. Based on the details in the form, the Remitter’s

Bank debits his bank account and sends a SWIFT message to transfer the

money to the Beneficiary’s Bank.

Listed below are the various Disbursement Modes of remittance using which the

money can be tendered to the beneficiary.

1. Direct Credit to the beneficiary’s account with the Beneficiary Bank

2. Disbursement of Cash to the beneficiary on furnishing appropriate photo -

identification/ address proof in the event of his not having a bank account

3. Transfer of Money by the Beneficiary Bank to the beneficiary’s

account with some other local bank using the local payment mechanism

4. DD issuance in the name of the beneficiary

Non-Banking Channels

Non-banking players play a vital role in the remittance space and have a larger share in

the Global Remittance business than conventional banks. These entities operate in

various forms:

Money Transfer Operators

MTOs (Money transfer Operators) like Western Union and Money Gram have a

network of agents across the globe and serve as non-bank remittance channels. The

remitter can visit an MTO outlet and pay cash in foreign currency to send money to any

part of the globe where the MTO’s agent is present. The receiver can visit the MTO

agent at his location and collect the money in local currency.

Following depicts the process for an International Remittance

transaction effected through an MTO:

The settlement between the MTOs in the two countries takes place through their

partner banks. On receiving the remittance amount in cash from the remitter, MTOs

deposit those funds in their local bank accounts. MTOs request their bank to

transfer the consolidated amount to the bank account of the MTO agent in the

receiving country. In order to minimize costs, only the net amount (total amount to

be sent to the recipient country minus total amount to be received from that country) is

sent. Please note that the beneficiary receives the money much before the settlement

between the MTOs

Costs

The fixed costs incurred by an MTO are listed below:

1. Origination and Disbursement Agent Network Costs

Setting up agency networks/outlets in the country of origination and disbursement forms

a significant portion of an MTO’s costs. Though traditionally, MTOs have had

proprietary agents, of late, third party agents have also been appointed by Western

Union and Money Gram. While these agents receive a fixed minimum compensation,

major incentives are linked to the number and value of transactions. The MTOs thus

share the risk of expanding their network with these partners.

2. Processing and Money Transfer Costs

These are the fees to be paid to the local bank which buys and sells various

international currencies, on behalf of the remittance service provider. These costs are

linked to the aggregate transaction value and MTOs with large volume transactions

could negotiate lower fees.

3. Marketing Costs

This simple transaction processing business has now become commoditized and players

have started spending on advertising and brand building.

4. Compliance and Regulatory Costs

Various mandatory compliance/regulatory procedures in the remittance business are

listed below. Expenses involved in following them form a sizeable part of the total

cost.

• KYC of Remitter / Beneficiary:

To prevent practices like transfer of money between anti-social elements, the

“Know Your Customer” checks are done by the Remitter ’s and the

Beneficiary’s Bank. KYC would typically involve obtaining documents such as

photo-ID, address proof, passport details, driving license details etc.

• Regular Reporting of Transaction: Details to the Central Bank

Central Banks place limits on the value of an individual’s remittances within a

certain time frame. Additionally, institutions are also supposed to comply

with Anti-Money Laundering requirements and report any suspicious/fraudulent

transactions to the Central Bank.

5. Administrative and IT costs

The MTO will also have to bear office maintenance expenses as well as system

development and maintenance costs.

Salient Features of the MTO model-

1. It is the fastest mode of transfer since the beneficiary can receive the money

within seconds after it is sent.

2. People without b a n k a c c o u n t s c a n a l s o transact in this model.

3. The cost per transaction is lower compared to other models.

4. MTOs have the biggest market share in the remittance business.

5. Setup costs are high, acting as a barrier for new entrants.

E-mail: The exchange house sends e-mail to the Beneficiary Bank instructing

it to transfer the amount to the furnished beneficiary account.

Integration of exchange house and Beneficiary Bank systems

B e n e f i c i a r y B a n k ’s p r o p r i e t a r y remittance platform

Exchange Houses:

Exchange Houses are extensively used for remittances from the Middle East. Unlike the

banking channel, this channel is based on Vostro accounts i.e. the accounts

maintained by exchange houses with various banks in the beneficiary countries.

These accounts are pre-funded by the exchange houses.

Salient Features of the Exchange House Channel

1. Since the Vostro accounts are pre-funded, the beneficiary amount is

paid based on the funding in this account. Hence o n r e c e i v i n g

t h e E x c h a n g e H o u s e’s instruction, the beneficiary

receives the amount almost instantaneously.

2. The Exchange House has to fund its account with the Beneficiary

Bank hence the latter enjoys the float.

3. The Exchange House can draw a DD on its Vostro account in favor of the

beneficiary and hand it over to the remitter over the counter, which can then

be dispatched by courier or even sent along with a friend travelling back

home. Alternatively, the DD can also be drawn in favor of the remitter,

who can then carry it back to his home country on his return and get it

cleared there. This is a secure option for blue collar workers who would

otherwise have to travel with hard cash.

The Remittance T ransaction Process

Step 1 The remitter deposits the remittance money in the overseas currency in cash

at the Exchange House counter.

Step 2 The exchange rate and the transaction fee are communicated and confirmed

over the counter.

Step 3 The beneficiary account details are provided by the remitter.

Step 4 The exchange house instructs the Beneficiary Bank with whom it has a

tie-up for transferring the requisite amount in the beneficiary country’s

local currency using one of the following modes:

Figure depicts the Vostro-based setup wherein the Correspondent Bank has an account with the Beneficiary Bank

Impact on Global economy

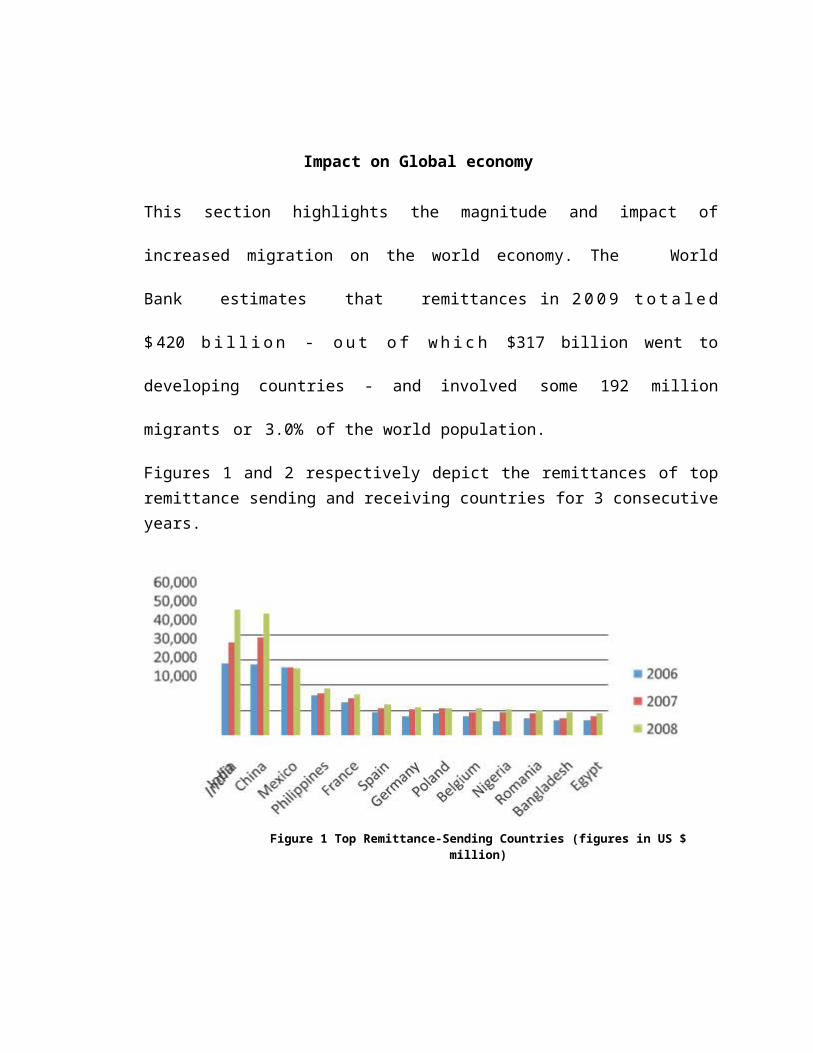

This section highlights the magnitude and impact of increased migration on the world

economy. The World Bank estimates that remittances in 2 0 0 9 t o t a l e d $ 420

b i l l i o n - o u t o f w h i c h $317 billion went to developing countries - and involved

some 192 million migrants or 3.0% of the world population.

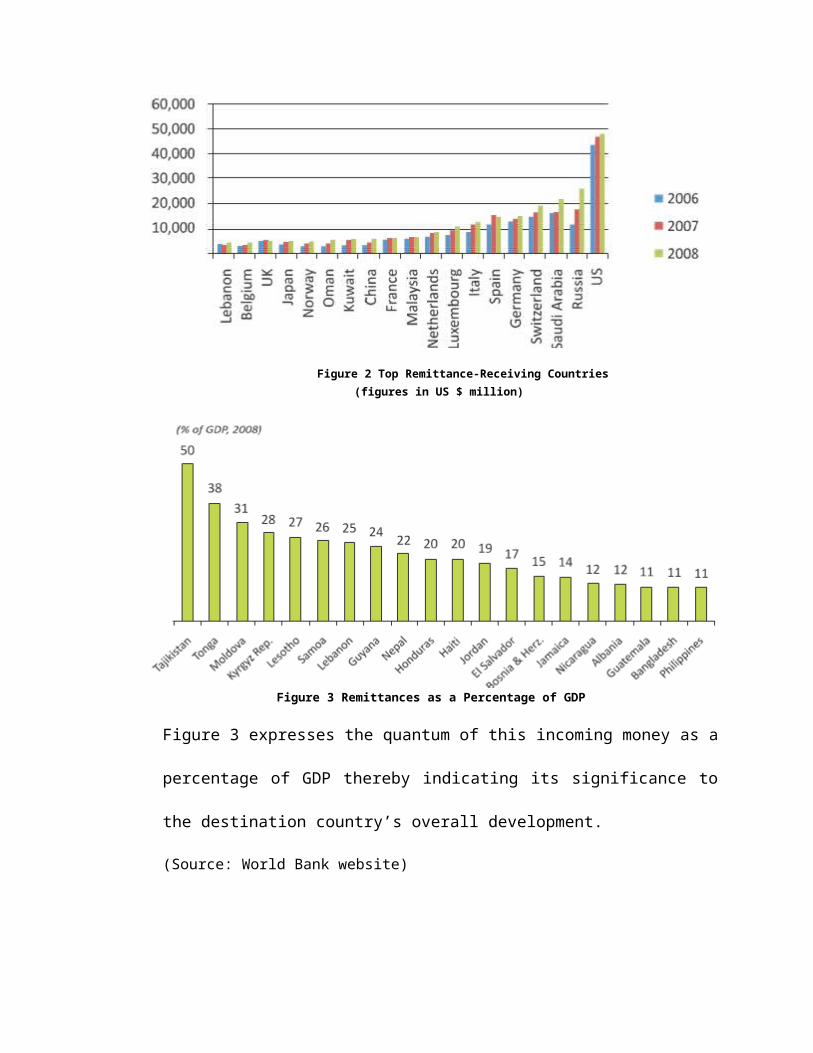

Figures 1 and 2 respectively depict the remittances of top remittance sending and receiving countries for 3 consecutive years.

Figure 1 Top Remittance-Sending Countries (figures in US $ million)

Figure 2 Top Remittance-Receiving Countries (figures in US $ million)

Figure 3 Remittances as a Percentage of GDP

Figure 3 expresses the quantum of this incoming money as a percentage of GDP

thereby indicating its significance to the destination country’s overall development.

(Source: World Bank website)

NKGSB’s AD-II Activities:

Reserve Bank of India has renewed NKGSB’s AD II license and also given a

permission to start AD II activities in all branches. At present following

Branches are doing the AD – II Activity and acting as a focal point for

designated branches.

Forex Dept; Girgaum, Dadar, Dindoshi, Mulund (East), Thane.

Under AD-II License following activities can be carried out by NKGSB bank –

Foreign Demand Draft remittances

Telegraphic Transfers

Purchase & Sale of Foreign Currency Notes

Purchase & Sale of Foreign Travellers Cheque

Under Telegraphic Transfer and Demand Draft remittances only clean

remittances are allowed. The above mentioned activities can be carried out for

the purpose mentioned as under:

(a) Private visits,

(b) Remittance by tour operators/travel agents to overseas

agents/principals/hotels,

(c) Business Travel,

(d) Fee for participation in global conferences and specialised training,

(e) Remittance for participation in international events/ competitions

(towards training, sponsorship and prize money,

(f) Film shooting,

(g) Medical Treatment abroad,

(h) Disbursement of crew wages,

(i) Overseas Education,

(j) Remittance under educational tie up arrangements with universities

abroad,

(k) Remittance towards fees for examinations held in India and abroad

and additional score sheets for GRE, TOEFL, etc,

(l) Employment and processing, assessment fees for overseas job

applications,

(m)Emigration and Emigration Consultancy fees,

(n) Skills/ credential assessment fees for intending migrants,

(o) Visa fees,

(p) Processing fees for registration of documents as required by the

Portuguese/ other Governments, Registration/Subscription/

Membership fees to International Organisations,

(q) Registration / Subscription/ Membership fees to International

Organisations.

Personal/ Private/ Leisure Visits

Foreign exchange for private visit can also be released to a person who is availing of

foreign exchange for travel outside India for any purpose up to the limits specified in

Schedule III to the Rules.

Eligibility:

Resident Indian Nationals.

Foreign Nationals permanently resident in India are also eligible to avail of this

quota provided the applicant is not availing of facilities for remittance of his salary,

savings etc .abroad in terms of the existing

FEMA regulations.

Foreign born wife of Indian nationals.

Children endorsed on parent’s passport are

also eligible for full entitlement.

Quantum of Exchange:

UptoatotalofUS$10000orits equivalent per resident individual on a financial year ba-

sis.

Out of which maximum of US$3000or its equivalent in Currency notes per visit

and resting Travelers Cheques for all the countries except for travel to Iraq, Libya,

Islamic Republic of Iran, Russian Federation and other Republics of Common

wealth of Independent States.

Individual traveling to countries like Nepal & Bhutan are not eligible to withdraw

foreign exchange under this scheme.

For Travelers proceeding to Iraq or Libya exchange in the form of currency notes

may be sold up to limit not exceeding USD 5000orits equivalent per resident indi-

vidual on a financial year basis.

For Travelers proceeding to the Islamic Republic of Iran, Russian Federation and

other Republics of Commonwealth of Independent States entire exchange can

be released in the form of currency notes.

Foreign exchange quota for personal visit can be availed over & above the

specified amount under all other schemes for release of foreign exchange.

Documentation:

Request cum FEMA Declaration form for release of exchange under personal

visit scheme.

Form A2 or Simplified Application cum Declaration up to USD 5000

Equivalent

Original passport for pages showing name, address, valid visa & passport num-

ber and validity should be verified by the Counter Staff & details to be note don

their quest form Confirmed ticket-showing travel within 60days of taking for-

eign exchange should be verified & details of the ticket number should be noted

on their quest form by Counter Staff.

Request form should have the undertaking from the Counter Staff that all

originals including the passport &he/she has dully verified the ticket. Photo-

copies need to be kept.

Photocopy of the crossed account payee cheque /draft or pay order along with

debit advice.

If the applicant is a foreign national permanently resident in India, he/she

should give an undertaking on the application itself that he/she is perma-

nently resident in India and is not availing of facilities for remittance of his/her

salary. Saving etc. abroad in terms of existing FEMA Regulations.

Exceptions to be noted by Counter Staff:

o Visa may not be insisted up on in cases where travel is to a country-offering visa

on arrival. However, undertaking for the same may be obtained

o For Airline staff open ticket may be accepted. Proof of Airline staff may be kept

in record.

Sales to Business Visit

Foreign exchange may be released for undertaking

business travel or attending a conference or specialised

training or for maintenance expenses of a patient going

abroad for medical treatment or check up abroad or for accompanying as attendant

to a patient going abroad for medical treatment / check up to the limits specified in

Schedule III to the Rules.

Eligibility:

Executive’s sponsored by firms/companies/ organizations in India.

Participation in international conferences /seminars which are of a scientific,

technical or educational nature.

Specialized training/study tour sponsored by institutions or undertaken by pro-

fessionals like Doctors.

Quantum of Exchange:

Up to USD25000 per business trip irrespective of period of stay

Release of exchange beyond USD 25000 for a single business visit requires prior

approval of RBI.

Exchange may also released to foreign nationals if the visit is sponsored by the

company/firm/organization in India where they are employed on regular basis.

If a passenger plans to club both Conference and business visit together the enti-

tlement remains only up to a maximum of USD25000.

Personal Visit entitlement can be availed over and above the specified amount

under this scheme

Documentation:

Request cum FEMA Declaration form for release of exchange under business

visit scheme on company’s letter head, duly signed by Authorized official of the

company.

A -2 form (Only for the amounts exceedingUSD 5000equivalent.)

In case of Travel for a conference/ seminars the brochure giving full particulars

of the Conference/seminar shall also be submitted along with the application.

In case of Travel related to Training/ Study tours the details of training/study tour

along with a letter from the overseas institutions agreeing to provide necessary fa-

cilities for the training /study tour, and certifying that the expenses are being

borne by the organization.

All the above documents to be kept on record along with Copy of Cash Memo.

Medical treatment abroad Resident Indian proceeding for permanent emigra-

tion abroad (needs to be confirmed)

With a view to enable residents to avail of foreign exchange for medical treatment

abroad without any hassles and any loss of time, Authorised Dealers may release for-

eign exchange up to an amount of USD 100,000 or its equivalent, on the basis of

self declaration that the applicant is buying exchange for medical treatment outside

India, without insisting on any estimate from a hospital/doctor. For amount exceeding

the above limit, estimate from the doctor in India or hospital/ doctor abroad, is re-

quired to be

submitted to

the Authorised

Dealers. A

person who

has fallen sick

after proceeding abroad may also be released foreign exchange by an Authorised

Dealer for medical treatment outside India.

Eligibility:

Resident Indian

must be suffering from an ailment requiring specialized treatment abroad.

Resident I n d i a n f a l l e n s i c k a f t e r proceeding abroad

Going abroad for Medical Check Up.

Quantum of exchange: USD 100,000

Documentation:

Request cum FEMA Declaration form for release of exchange by filling the

relevant portion as per the type of remittance.

Photocopy o f t h e p a s s p o r t h a v i n g valid visa in case the remittance is for

employment, education abroad, and medical treatment and for permanent

emigration.

A - 2 form (Only for the amounts exceeding USD 5000 equivalent.)

For application fees in case of foreign education or processing fees for

immigration, valid visa is not required.

Medical treatment abroad for Resident Indian:

Quantum of exchange: Exceeding U S D 1 0 0 0 0 0 o n submission to AD of an

estimate from the Doctor in India or hospital/ doctor abroad.

Cultural Tours

Dance troupes, artistes, etc., who wish to undertake tours abroad for cultural purposes

should apply to the Ministry of Human Resources Development (Department of

Education and Culture), Government of India, for their foreign exchange requirements.

Authorised Dealers may release foreign exchange, on the strength of the sanction from

the Ministry concerned, to the extent and subject to conditions indicated therein.

Emigration:

Eligibility:

USD 100,000 or amount prescribed by country of Emigration (lower of the two)

Quantum of exchange:

Resident Indian Proceeding for permanent emigration abroad

Documentation:

Request cum FEMA Declaration form for release of exchange by filling the

relevant portion as per the type of remittance.

Photocopy of t h e p a s s p o r t h a v i n g valid visa in case the remittance is for

employment, education abroad, and medical treatment and for permanent

emigration.

A - 2 form (Only for the amounts exceeding USD 5000 equivalent.)

For application fees in case of foreign education or processing fees for

immigration, valid visa is not required.

Remittances for Tour Arrangements (At the request of the traveler)

Authorised Dealers may remit foreign exchange up to a reasonable limit, at the

request of a traveler towards his hotel accommodation, tour arrangements, etc., in the

countries proposed to be visited by him or for making other tour arrangements for

travelers from India, provided in each case the Authorised Dealer is satisfied that the

remittance is being made out of the foreign exchange purchased by the traveler

concerned from an Authorised Person (including exchange drawn for private travel

abroad), in accordance with the Rules, Regulations and Directions in force.

Authorised Dealers may effect remittances at the request of agents in India who have

tie-up arrangements with hotels / agents, etc., abroad for providing hotel accommodation

or making other tour

arrangements for travel from

India, provided the Authorised

Dealer is satisfied that the

remittance is being made out

of the foreign exchange

purchased by the traveler concerned from an Authorised Person(including exchange

drawn for private travel abroad) in accordance with the Rules, Regulations and

Directions in force.

Eligibility:

Traveler traveling abroad on personal/Leisure visit or business visit can remit up to a

reasonable limit towards his hotel accommodation, tour arrangements, etc., in the

countries proposed to be visited by him, provided it is out of foreign exchange

purchased by the traveler from us (including exchange drawn for private travel abroad)

Quantum of exchange:

Quantum of Exchange is not specified in the RBI Circulars

Documentation:

Letter from the Client duly signed by their authorized signatories clearly

indicating the following details/particulars : -

Request for the remittance with the currency, amount and date of remittance. [In

case of difference in amount between underlying document/s against the actual

remittance amount, such adjustments should be explicitly stated along with the

reason and final net amount to be remitted should be specified]

Purpose of Remittance

Debit authority – a u t h o r i z i n g t h e bank to debit their INR/EEFC account with us

towards the amount of remittance and our charges / commission and

Beneficiary & Bank details for remittance.

Form A2 – Dully filled – in and signed by authorized signatories

FEMA Declaration format duly signed by authorized signatories

Remittances for Tour Arrangements (At the request of the Agent)

Eligibility:

Agents in India, having a good track record and s a t i s f y i n g a l l KYC norms, and

have tie up arrangements with hotels/agents etc., abroad for providing hotel

accommodation or making other tour arrangements for travelers from India, provided

the remittance is made out of foreign exchange purchased by the concerned

traveler from us or from an authorized person (including exchange drawn

for private travel abroad)

Quantum of exchange:

Amount as per the invoice of the overseas hotels/agent within the prescribed limits of

personal / business visit Forex quota as mentioned above.

Documentation:

Agent’s Declaration from the client to the effect that the remittance is being

made out of the foreign exchange purchased by the concerned traveler from an

authorized person (including exchange drawn for private travel abroad) in

accordance with the Rules, Regulations and Directions in force.

That he (agents) has received the undertaking from the travelers in addition

to the normal required conditions applicable for release of foreign exchange that

the traveler has/will purchase the foreign exchange from the Authorized person only

and within the prescribed limits (including the amount now being remitted abroad

as advance payment) in accordance with the Rules, Regulation and Direction in

force.

That he will take care and follow up that t h e tour/services for which the advance

is being/has b e e n remitted should be executed and ensure that the beneficiary

of advance remittance has fulfilled his obligation under the Contract/agreement/tie-

up and will inform the Bank within reasonable time from the completion of

the Tour and undertake to repatriate the unspent advance remittance, if any.

Employment abroad

Eligibility: USD 100,000

Quantum of Exchange:

Resident Indians

Employment Visa / Work P e r m i t and letter from the overseas employer

Documentation:

Request cum FEMA Declaration form for release of exchange by filling the

relevant portion as per the type of remittance.

Photocopy of the passport having valid visa in case the remittance is for

employment, education abroad, and medical treatment and for permanent emigration.

A -2 form (Only for the amounts exceeding USD 5000 equivalent.)

For application fees in case of foreign education or processing fees for immigration,

valid visa is not required.

Maintenance of close relatives abroad ( by resident Indian)

Eligibility:

Resident Indians can remit to their close relative who are Nonresident and require

funds abroad for their maintenance.

Quantum of exchange:

USD 100,000 (per year, per recipient)

Documentation:

Request cum FEMA Declaration form for release of exchange by filling the

relevant portion as per the type of remittance.

Photocopy of the p a s s p o r t h a v i n g valid visa in case the remittance is for

employment, education abroad, and medical treatment and for permanent

emigration.

A - 2 form (Only for the amounts exceeding USD 5000 equivalent.)

For application fees in case of foreign education or processing fees for

immigration, valid visa is not required.

Maintenance of Close relative abroad (By resident but not permanently resi-

dent in india)