STRUCTURING THE TRIBAL BUSINESS ENTITY - Law …lawseminars.com/materials/07TRIBWA/tribwa m 21...

28

STRUCTURING THE TRIBAL BUSINESS ENTITY October 23, 2007 Brett Kenney, Tribal Attorney Coquille Indian Tribe

Transcript of STRUCTURING THE TRIBAL BUSINESS ENTITY - Law …lawseminars.com/materials/07TRIBWA/tribwa m 21...

1

STRUCTURING THE TRIBALBUSINESS ENTITY

October 23, 2007

Brett Kenney, Tribal AttorneyCoquille Indian Tribe

2

This presentation covers basicconsiderations when forming a Tribal

business.

Why separate tribal businesses from Tribe?• liability reasons• financing reasons• management reasons

3

OVERVIEW

Business Entities in General

Possible Ways to Structure Relationships Among Entities

Issues Regarding Corporate Formation

Federally Chartered Corporations (Section 17 Corps.)

Tribal Law Corporations

4

POSSIBLE ENTITIES

State chartered corporationsState chartered limited liability companiesTribally chartered corporationsTribally chartered limited liability companiesUnincorporated arms or entities of the TribeFederally chartered corporations (Section 17)

5

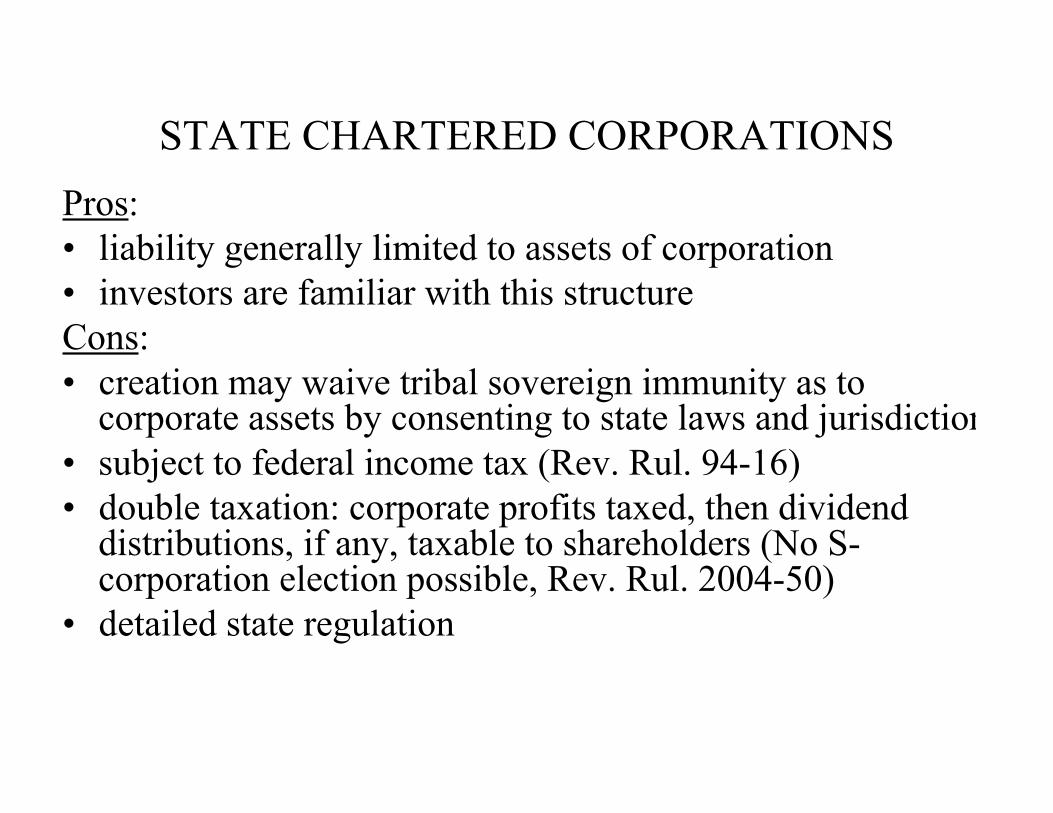

STATE CHARTERED CORPORATIONSPros:• liability generally limited to assets of corporation• investors are familiar with this structureCons:• creation may waive tribal sovereign immunity as to

corporate assets by consenting to state laws and jurisdiction• subject to federal income tax (Rev. Rul. 94-16)• double taxation: corporate profits taxed, then dividend

distributions, if any, taxable to shareholders (No S-corporation election possible, Rev. Rul. 2004-50)

• detailed state regulation

6

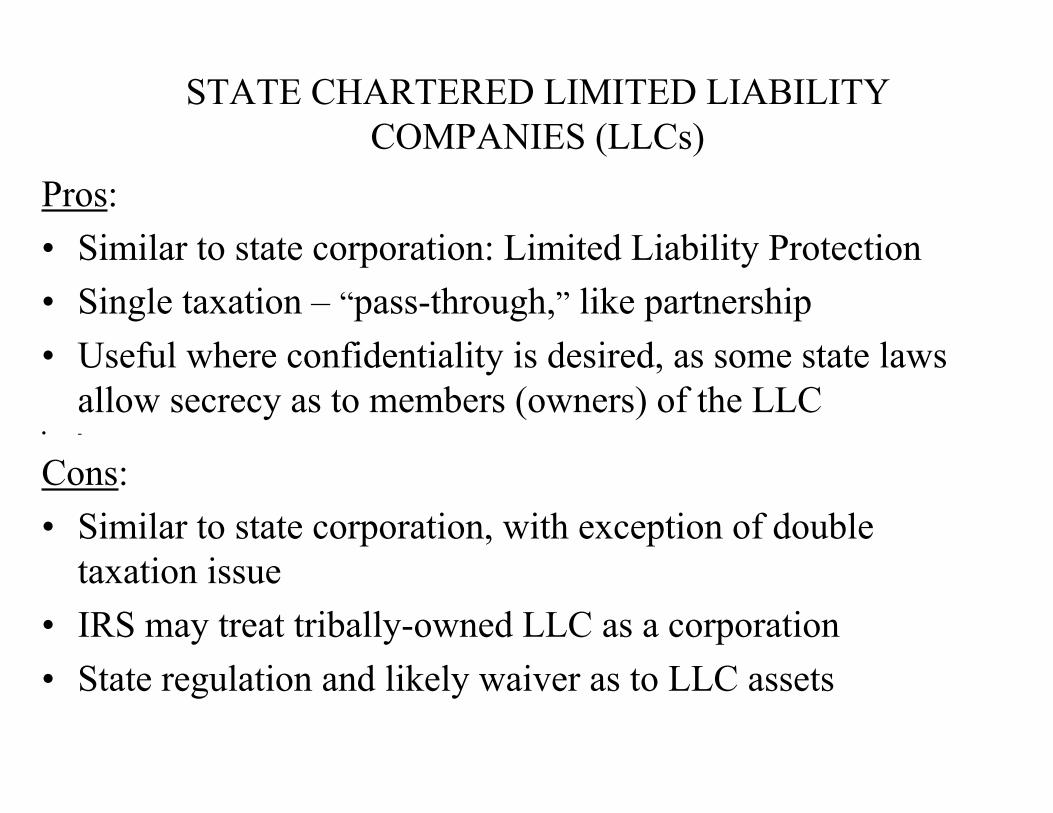

STATE CHARTERED LIMITED LIABILITYCOMPANIES (LLCs)

Pros:• Similar to state corporation: Limited Liability Protection• Single taxation – “pass-through,” like partnership• Useful where confidentiality is desired, as some state laws

allow secrecy as to members (owners) of the LLC• -

Cons:• Similar to state corporation, with exception of double

taxation issue• IRS may treat tribally-owned LLC as a corporation• State regulation and likely waiver as to LLC assets

7

TRIBALLY CHARTERED CORPORATIONSPros:• May retain sovereign immunity• Have been held exempt from federal income tax

where corporation meets IRS two-pronged“integral part” test (to be discussed in a moment)

Cons:• Federal tax status is unsettled

8

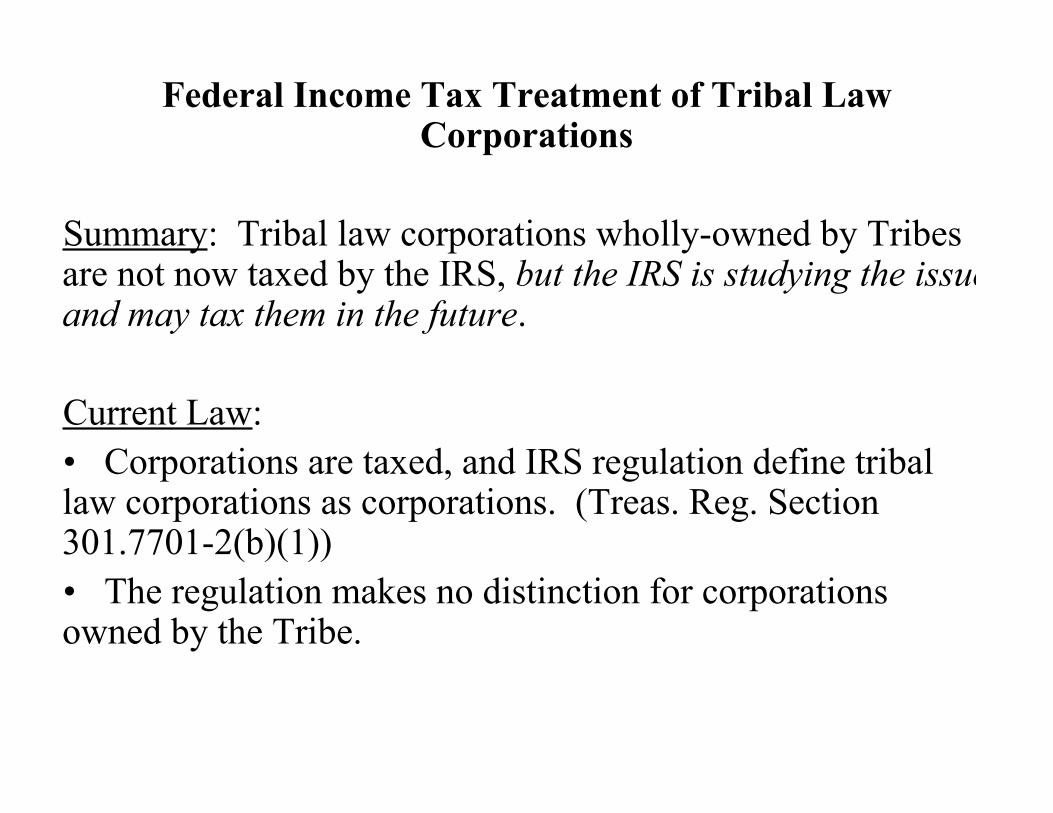

Federal Income Tax Treatment of Tribal LawCorporations

Summary: Tribal law corporations wholly-owned by Tribesare not now taxed by the IRS, but the IRS is studying the issueand may tax them in the future.

Current Law:• Corporations are taxed, and IRS regulation define triballaw corporations as corporations. (Treas. Reg. Section301.7701-2(b)(1))• The regulation makes no distinction for corporationsowned by the Tribe.

9

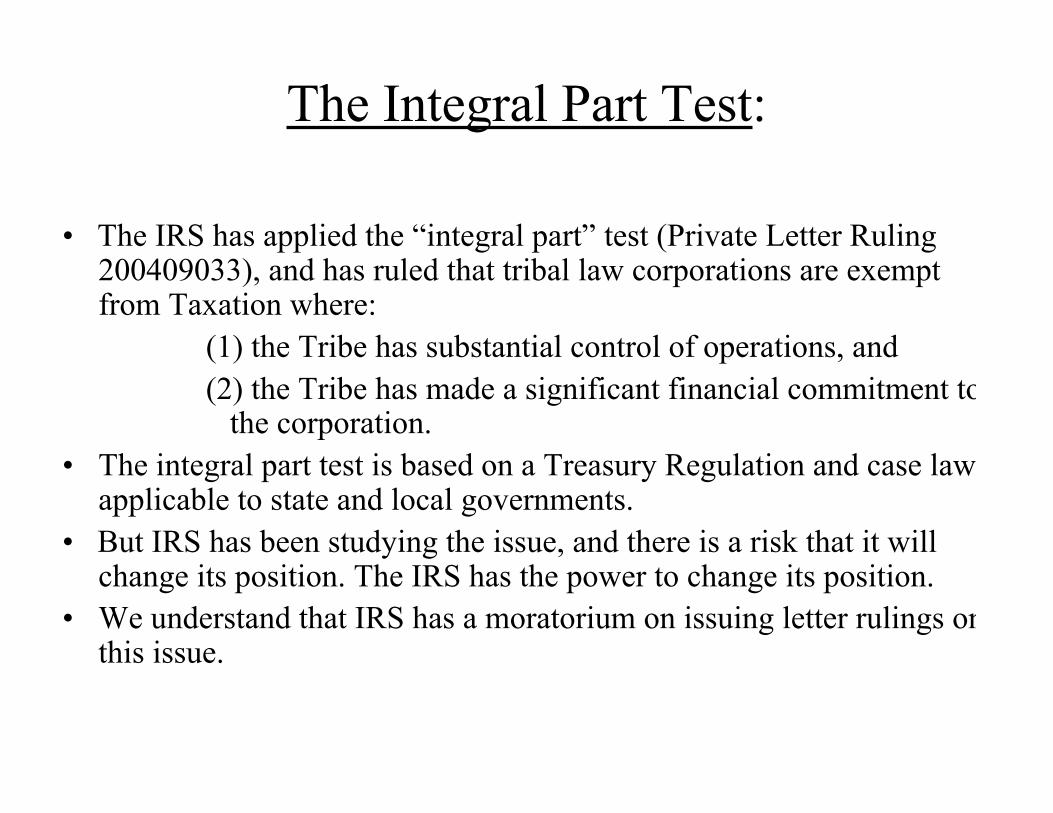

The Integral Part Test:

• The IRS has applied the “integral part” test (Private Letter Ruling200409033), and has ruled that tribal law corporations are exemptfrom Taxation where:

(1) the Tribe has substantial control of operations, and(2) the Tribe has made a significant financial commitment to

the corporation.• The integral part test is based on a Treasury Regulation and case law

applicable to state and local governments.• But IRS has been studying the issue, and there is a risk that it will

change its position. The IRS has the power to change its position.• We understand that IRS has a moratorium on issuing letter rulings on

this issue.

10

IRS Listening Session• Listening Meetings

The office of Indian Tribal Governments conducts Consultation Listeningmeetings, which afford tribal and village representatives the opportunity to raisequestions, and to offer suggestions on methods to enhance federal taxadministration for tribal and village governments.

• The next meeting will be held on Thursday November 8, 2007 from 1:00pm-4:00pm at:

Doubletree Hotel (at SeaTac Airport) 18740 International Boulevard Seattle, Washington 98188

• The meeting is open to anyone that a tribe or village may wish to designate toattend.

• IRS requests advance email registration: [email protected]

11

TRIBALLY CHARTERED LIMITED LIABILITYCOMPANIES

Pros:• Member liability limited to amount of investment• “Pass-through” taxation• Flexible management structure• Useful for creating partnership-like or joint-venture-like entities under

tribal law with non-tribal parties so as to not fall under state law.Cons:• Tax status unclear under “integral part” test above• Limited ability to transfer LLC's assets to Tribe or corporation• Tribe must draft, enact and administer a tribal Limited Liability

Code.

12

UNINCORPORATED ARMS OR ENTITIESOF THE TRIBE: TRIBAL AUTHORITIES

Pros:• If set up and operated correctly, it will possess sovereign immunity• Maximizes tribal government control over entity• Shares tribal government’s tax status because of direct control

Cons:• Lack of independence from tribe means politics may interfere with

business judgment• Need to carefully structure waivers of immunity to insulate tribe from

judgments against entity on a contract by contract basis• Significantly greater time demands on tribal governing body.

13

FEDERALLY CHARTERED CORPORATION(SECTION 17)

Pros:• Section 17 Corporation is exempt from federal taxes (Rev.

Rule 94-16, 81-295) and may possess immunity from suit• Federally-issued charter may provide greater assurance to

investors/lenders than a tribal charter• Charter cannot be revoked by tribal government.Cons:• Subject to Congressional jurisdiction

14

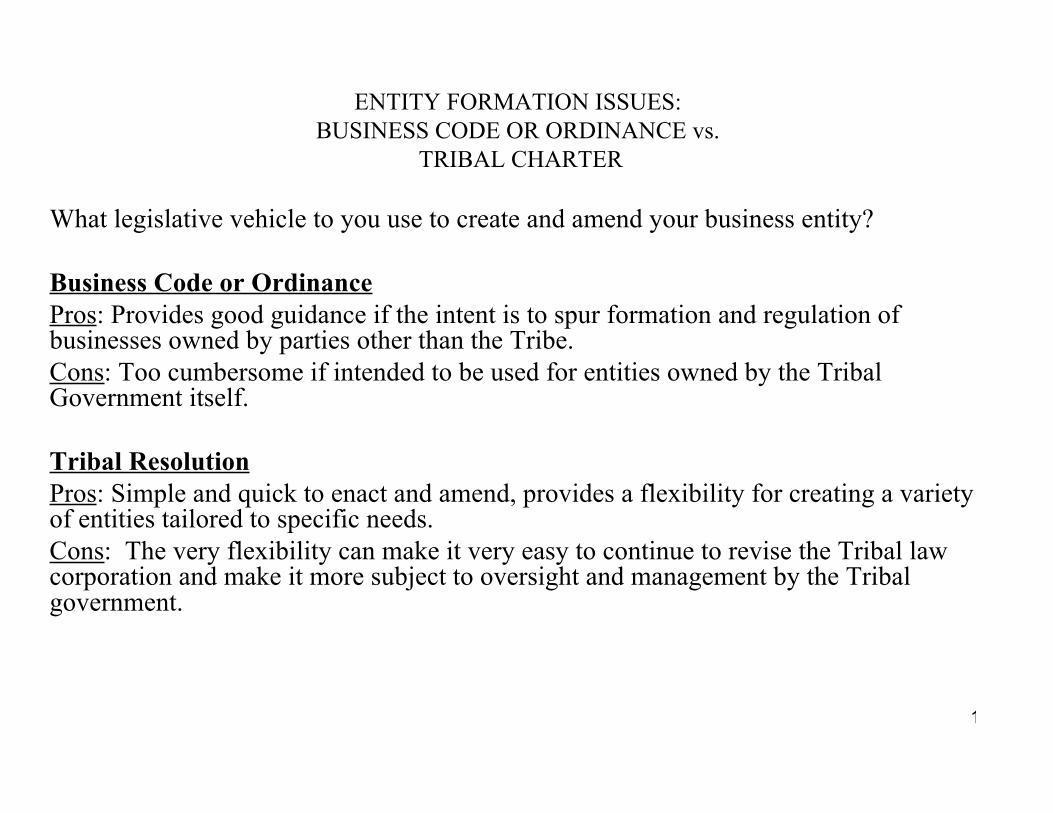

ENTITY FORMATION ISSUES:BUSINESS CODE OR ORDINANCE vs.

TRIBAL CHARTER

What legislative vehicle to you use to create and amend your business entity?

Business Code or OrdinancePros: Provides good guidance if the intent is to spur formation and regulation ofbusinesses owned by parties other than the Tribe.Cons: Too cumbersome if intended to be used for entities owned by the TribalGovernment itself.

Tribal ResolutionPros: Simple and quick to enact and amend, provides a flexibility for creating a varietyof entities tailored to specific needs.Cons: The very flexibility can make it very easy to continue to revise the Tribal lawcorporation and make it more subject to oversight and management by the Tribalgovernment.

15

COMPANY STRUCTURE

Issue: Place all tribal businesses under one roof, or have asseparate entities entirely?

Advantages of placing under one roof:• Uniform development• Economies of scale and maximizes resource utilization• Minimizes competition for financial resources, personnel

or business opportunities between different businessventures

Disadvantages:• Can limit diversity and create a monolithic, uniform

scheme of economic development.• Risks and Liabilities of one business can affect others

16

ASSET TRANSFERS — TAX ISSUE

Issue: Transfer of assets from taxable corporation to tax-exempt entity(Tribe or Section 17 Corporation) can create a taxable event

Ramifications: Can create a large unintended taxable event based on thefair market value of the asset transferred.• Tribes must ensure that transfer of existing tribal businessesto new entity is not taxable• Attorney’s advice is critical.

17

THE WAY YOUR BUSINESS IS STRUCTURED CAN HAVEFINANCE CONSEQUENCES

• Legally distinct entities not liable for each others debts & mayhave different credit risks/ratings

• But if different businesses grouped under one roof, then diversityof businesses could have beneficial effect on credit rating iffinanced as a unified credit

• But, similarly, if different businesses are grouped under oneroof, weakest business could impact upon financing of strongerbusinesses

• Lenders are generally more comfortable working with Triballyowned corporations than to Tribal governments as suchcorporations more neatly fit their lending models

18

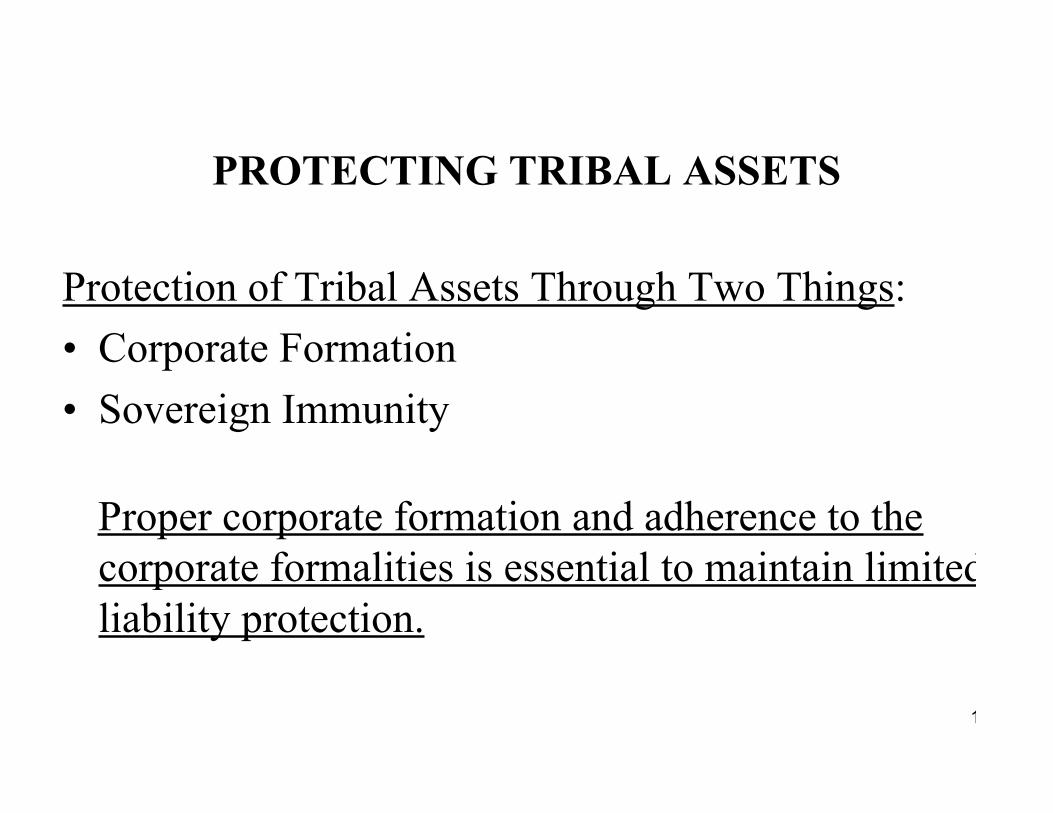

PROTECTING TRIBAL ASSETS

Protection of Tribal Assets Through Two Things:• Corporate Formation• Sovereign Immunity

Proper corporate formation and adherence to thecorporate formalities is essential to maintain limitedliability protection.

19

CORPORATE FORMALITIES: Piercing the corporate veil.

Normally, corporations and LLCs provide “limitedliability” protection.– This means that a court judgment against a corporation

or LLC can only recover the assets actually owned bythat corporation or LLC.

However, if corporate formalities are disregarded,resulting in fraud or injustice, court may “piercethe corporate veil” and hold owner (Tribe) liable forthe debts of the corporation.

20

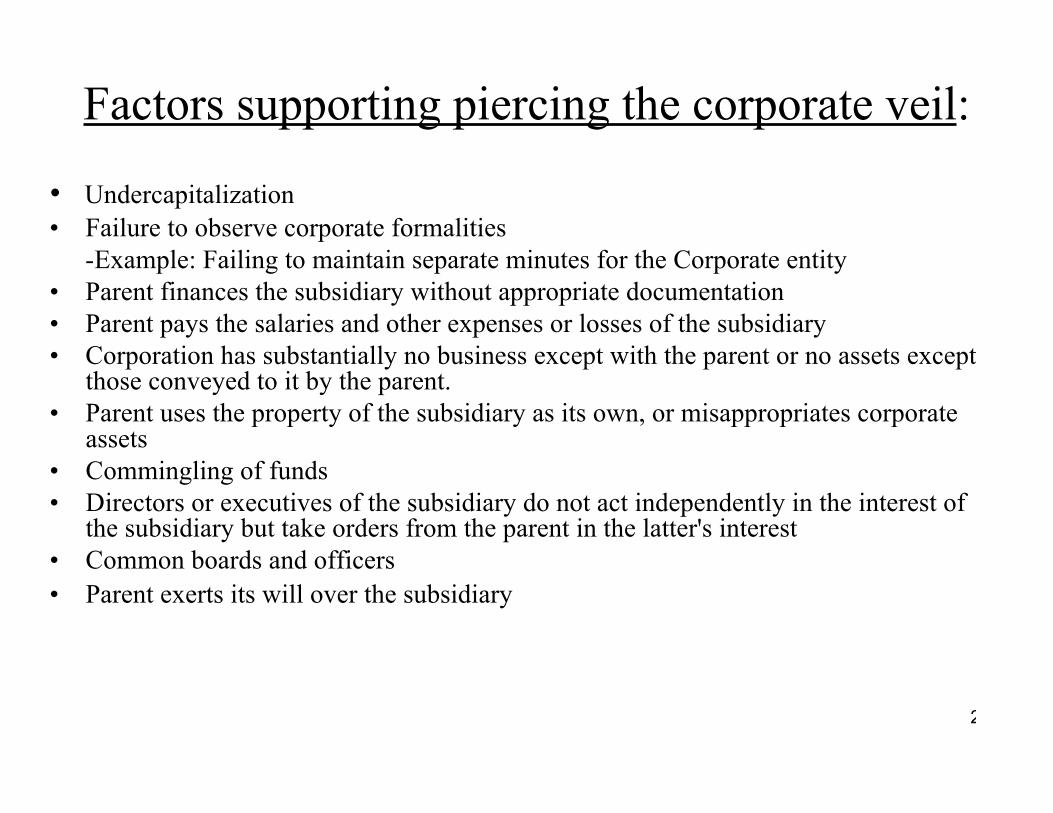

Factors supporting piercing the corporate veil:

• Undercapitalization• Failure to observe corporate formalities

-Example: Failing to maintain separate minutes for the Corporate entity• Parent finances the subsidiary without appropriate documentation• Parent pays the salaries and other expenses or losses of the subsidiary• Corporation has substantially no business except with the parent or no assets except

those conveyed to it by the parent.• Parent uses the property of the subsidiary as its own, or misappropriates corporate

assets• Commingling of funds• Directors or executives of the subsidiary do not act independently in the interest of

the subsidiary but take orders from the parent in the latter's interest• Common boards and officers• Parent exerts its will over the subsidiary

21

Factors minimizing risk of corporate veil piercing:

• Charter or Articles identifies corporation as separatelegal entity

• Managerial and operational independence from parent• Observation of corporate formalities as set forth in

Articles and Bylaws. This last factor is critical.• e.g. notification, meeting, and voting requirements• secretary must maintain minutes and other records

22

SOVEREIGN IMMUNITY

Tribe is immune from suit.

Tribal Entities: May share Tribe’s immunity, depending onvarious factors: intent of Tribe, ownership, control, purpose,etc.

23

Section 17 Corporation: Sovereign Immunity Very Likely If . . .

• Record shows that tribe clearly intended to share its immunitywith the Section 17 Corporation and the articles of incorporationso clearly provided for such immunity.

• Section 17 Corporation is wholly owned by tribe.

• Documents demonstrate strong tribal control: directors appointedby Tribal Council.

• Federal government approves of charter or other organicdocument recognizing Section 17 sovereign immunity:endorsement of Tribe's intent that courts will likely respect

24

Tribal Law Corporations: Immunity Likely

• If tribe clearly intended to share its immunity with thecorporation and the articles of incorporation so clearlyprovided for such immunity.

• Possible exception to immunity: Federal income taxliability

25

Issues Regarding Corporate Formation

• Initial investments or contributions from tribe• Loans from tribe; real property leases from tribe• Allocation of profits or corporate distributions• Management issues• Tribal preference• Structural issues• Control issues

26

CONTROL ISSUES

Policy decision: how much control is tribe willing to cede tocorporation?

Will the tribal governing body be the same as the business entitygoverning body (e.g. the corporate board of directors)?

Competing mandates of government (expend resources, create jobs,provide services, be popular) and business (generate resources(profit), create efficiencies, be profitable).

Cornell & Kalt (Harvard 1998): Highly recommend separation ofpolitics from business management—four times as likely to beprofitable. Insulate day-to-day operations from politicalinterference.

27

Section 17 Corporation

Is governed by Section 17 of the Indian Reorganization Act(IRA)Charter is issued by Secretary of the Interior• to be ratified later by a tribal council resolutionCharter cannot be rescinded by Secretary of the Interior ortribe

28

IRS Circular 230 NOTICE:

To ensure compliance with requirementsimposed by the IRS, we inform you that anyU.S. federal tax advice contained in thiscommunication (including any attachments) isnot intended or written to be used, and cannotbe used, for the purpose of (i) avoidingpenalties under the Internal Revenue Code or(ii) promoting, marketing or recommending toanother party any transaction or matteraddressed herein.