Structuring Demystifying the African Continent - step.org · highly integrated basis. ... In Kenya...

26

Anjarwalla Collins & Haidermota, Legal Consultants 1 Structuring – Demystifying the African Continent 11 th April, 2018

Transcript of Structuring Demystifying the African Continent - step.org · highly integrated basis. ... In Kenya...

Anjarwalla Collins & Haidermota, Legal Consultants

1

Structuring – Demystifying the African Continent 11th April, 2018

Presenter 2

Atiq S. Anjarwalla

Managing Partner, Anjarwalla Collins & Haidermota,

Legal Consultants

INTRODUCTION TO AC&H AND ALN AC&H at a Glance

3

Regulated legal consultancy firm in Dubai, UAE Regional office of ALN (Africa Legal Network) - ALN network is

highly integrated basis. AC&H acts as the point of contact for all aspects of multi-jurisdictional deals across the entire ALN network through a seamless “one-stop shop” approach

Affiliated with Haidermota BNR – Pakistani’s premier corporate firm

Able to leverage expertise of over 700 lawyers in Africa Strategically based in Dubai, connecting Asia to Africa

4

ALN at a Glance Cont. 4

* Regional Office

** Associate Firm

United Arab

Emirates*

Anjarwalla, Collins &

Haidermota

South Africa**

Webber Wentzel

United Arab

Emirates*

Anjarwalla, Collins &

Haidermota

South Africa**

Webber Wentzel

ALN at a Glance

5

Founded in 2004 Leading independent African alliance of top tier law firms. ALN firms are recognised in international legal directories

and many have advised on ground breaking, first-of-a-kind deals in their markets

ALN is the largest grouping of its kind in Africa, with close working relationships across its members and an established network of Best Friends across the continent

ALN has the widest coverage and is the most integrated group of law firms operating on the continent

Present in 16 African countries Regional office in the UAE and Associate Firm in South Africa Over 700 lawyers on the ground

Understanding Africa – Macro issues for service providers to consider

9

REMEMBER… Africa is a CONTINENT

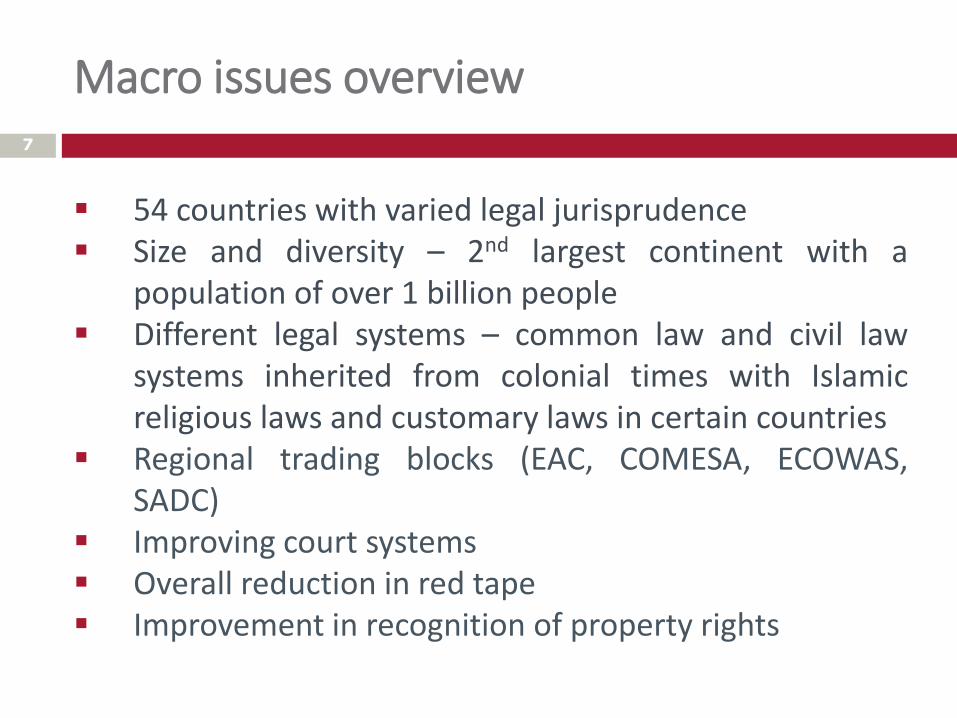

Macro issues overview 7

54 countries with varied legal jurisprudence Size and diversity – 2nd largest continent with a

population of over 1 billion people Different legal systems – common law and civil law

systems inherited from colonial times with Islamic religious laws and customary laws in certain countries

Regional trading blocks (EAC, COMESA, ECOWAS, SADC)

Improving court systems Overall reduction in red tape Improvement in recognition of property rights

Snapshot of opportunities in Africa 8

In 2016, total external flows to Africa were estimated at USD 177.7 billion (The Africa Economic Outlook 2017 - AfDB, OECD, and UNDP)

USD 5.6 Trillion in African business opportunities by 2025 (Mckinsey & Company – Lions on the move II, 2016)

Family-owned businesses account for 10 to 20 percent of large companies (700 companies with annual revenue of more than $500 million each) (Mckinsey & Company – Lions on the move II, 2016)

Key issues affecting structuring 9

Taxation Use of DTAs and BITS (Mauritius, Netherlands and UAE have 16,

9 and 8 DTAs respectively in force with African countries) Antitrust – treaty based (COMESA) and individual country

regimes Foreign exchange controls Local content requirements Legal systems Application of Sharia Laws Forced heirship right CRS (countries presently signed up are South Africa, Ghana,

Seychelles, Nigeria, Mauritius etc.) Recognition of customary marriage Dependency roles

Taxation 10

Capital Gains Tax and Stamp duty exemptions

Tax residency Taxation systems (Source / Worldwide) Thin capitalisation and deemed interest Transfer pricing Management and control Tax Amnesty Generally no inheritance taxes Use of DTAs and BITs

11

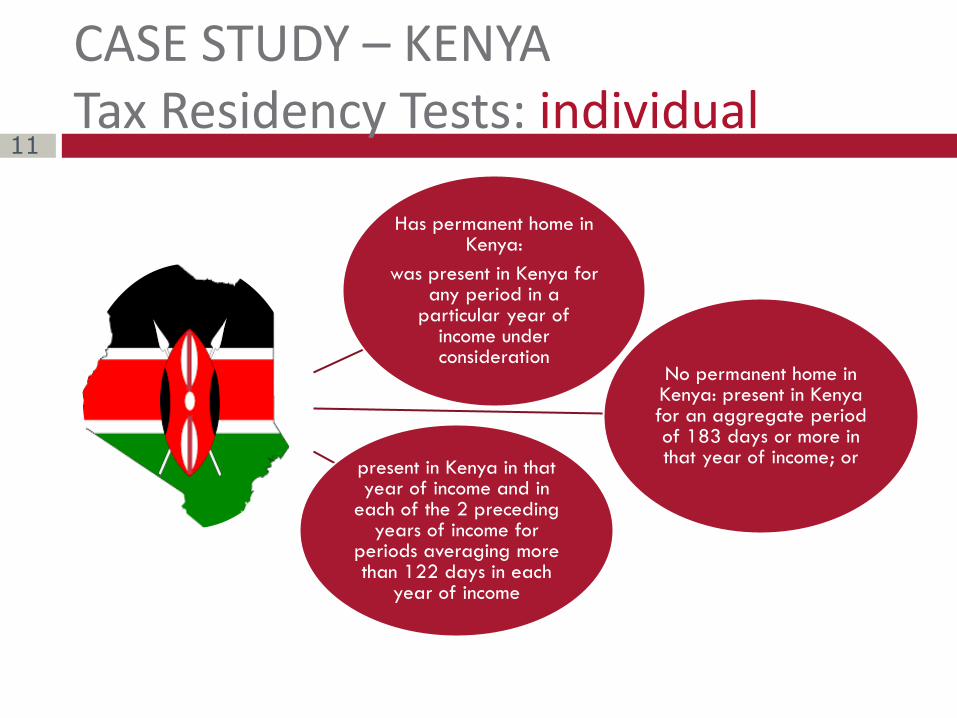

CASE STUDY – KENYA Tax Residency Tests: individual

Has permanent home in Kenya:

was present in Kenya for any period in a

particular year of income under consideration

No permanent home in Kenya: present in Kenya for an aggregate period of 183 days or more in that year of income; or

present in Kenya in that year of income and in

each of the 2 preceding years of income for

periods averaging more than 122 days in each

year of income

12

A body of persons is considered resident if:

its a company incorporated under a law of Kenya;

the management and control of the affairs of the body was exercised in Kenya in a particular year of income under consideration; or

the body has been declared by the Minister, to be resident for any year of income.

Kenya cont’d

13

According to OECD:

Source based - taxable income is income arising within its jurisdiction regardless of the residence of the taxpayer, i.e. residents and non-residents are taxed on income derived from the country (e.g. Kenya).

Worldwide system - resident persons are taxed on their worldwide income (e.g. Tanzania)

Source based v Worldwide taxation system

14

A company is thinly capitalised when a company is foreign controlled its debt exceeds equity beyond certain thresholds.

In Kenya this limits the deductibility of interest on loans for any year of income where the company is in the control of a non-resident person alone or together with four or fewer.

Control defined to be shareholding of 25% or more by non-resident persons.

Relating to offshore structures

Thin Capitalisation and Transfer pricing

15

Where a non-resident shareholder has extended a loan to a resident company on an interest-free basis, the resident company is required to compute a deemed-interest charge based on the prevailing Treasury Bill rates and the withholding tax of 15% remitted to the KRA.

Notional – not a tax deductible expense

Compliance with Transfer Pricing Rules

Deemed Interest

16

Finance Act 2016 introduced a provision in the Tax Procedures Act, 2015 (the TPA)

Section 37B of the TPA (as amended by the Finance Act, 2017) provides:

…the Commissioner shall refrain from assessing or recovering taxes, penalties or interest in respect of any year of income ending on or before the 31st December 2016, and from following up on the sources of income under the amnesty where –

a. that income has been declared for the year 2016 by a person earning taxable income outside Kenya; and

Tax Amnesty (Kenya)

17

b. The returns and accounts for the year 2016 are submitted on or before the 30th June 2018:

c. the voluntarily declared funds have been transferred back to Kenya.

d. where the funds are not remitted back to Kenya within the period of the amnesty, there shall be a 5yr period of remittance and a penalty of 10% shall apply on the remittance.

Tax Amnesty (Kenya) Cont’d.

18

Kenyan tax resident persons in the following circumstances:

Foreign assets and income acquired using untaxed income.

Inheritance from Kenyan sources where no clarity on tax status.

Salary splitting arrangements

Who should consider the Tax Amnesty?

19

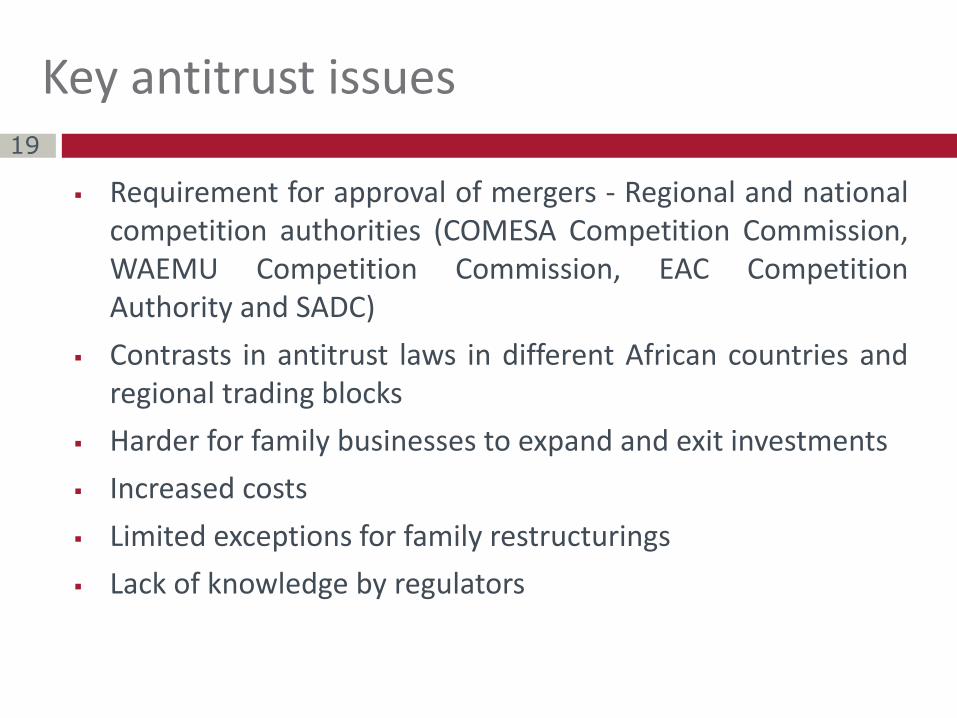

Requirement for approval of mergers - Regional and national competition authorities (COMESA Competition Commission, WAEMU Competition Commission, EAC Competition Authority and SADC)

Contrasts in antitrust laws in different African countries and regional trading blocks

Harder for family businesses to expand and exit investments

Increased costs

Limited exceptions for family restructurings

Lack of knowledge by regulators

Key antitrust issues

20

Certain African countries have foreign exchange controls – South Africa, Zimbabwe, Ethiopia, etc.

Hard currency shortage

Not easy to repatriate funds

Exposure to weak currency risks

Lack of derivatives markets (or young and untested derivatives market) for hedging foreign exchange risks

Local content requirements mostly in energy, oil & gas and mining sectors – need for Africa countries to strike the right balance between incentives to attract foreign capital and developing local content

Foreign Exchange controls and foreign ownership restrictions issues

21

KYC and AML Challenges

Lack of robust laws on KYC and AML

Lack of government records on physical and postal address of persons

Lack of collaboration between government, non governmental organisations and financial institutions in information sharing

Increased costs on KYC and AML compliance

CRS – in line with the rest of the world, African countries are agreeing to sharing of financial information under CRS with certain countries (such as Kenya, South Africa, Ghana, Seychelles, Nigeria, Mauritius etc.) already signatories.

KYC and AML Challenges

22

Risk factors

Corruption

Restrictive policies and regulatory framework

Weak institutions

Unstable political environment

Weak security

Is it really high risk?

Not a high risk – Africa risks are not unique and they are similar to risks in other emerging markets

Risk Factors – Is it really high risk?

23

Each country is very different and there is no one size fits all approach which will work.

It is important to get your hands dirty by being on the ground. You cannot work in Africa by remote control.

Transparency in information is an issue so spend time to verify facts and information.

Final remarks

Questions 24

The contents of this presentation are intended to be for

general use only and should not be relied upon without

seeking specific legal advice on any matter.

The End 26