Stress testing - Strategy& - the global strategy … 5 Regulatory pressure Stress testing, both...

20

From regulatory burden to strategic capability Stress testing

Transcript of Stress testing - Strategy& - the global strategy … 5 Regulatory pressure Stress testing, both...

From regulatory burden to strategic capability

Stress testing

2 Strategy&

Contacts

Amsterdam

Marijn StrubenPwC Netherlands+31-6-2219-5670marijn.struben @strategyand.nl.pwc.com

Jeroen CrijnsPwC Netherlands+31-6-5156-6470jeroen.crijns @strategyand.nl.pwc.com

Brussels

Alex van Tuykom PwC Belgium+32-4-7554-9795alex.van.tuykom @be.pwc.com

Düsseldorf

Peter Gassmann PwC Strategy& Germany+49-170-2238-470peter.gassmann @strategyand.de.pwc.com

Frankfurt

Martin NeisenPwC Strategy& Germany+49-69-9585-3328martin.neisen @de.pwc.com

Ullrich Hartmann PwC Strategy& Germany+49-69-9585-2115ullrich.hartmann @de.pwc.com

Istanbul

Mehmet Eryilmaz PwC Turkey +90-530-370-5703mehmet.eryilmaz @strategyand.tr.pwc.com

London

Joerg RuetschiPwC UK+44-79-0016-3597joerg.ruetschi @strategyand.uk.pwc.com

Miles KennedyPwC UK+44-77-3831-3619miles.x.kennedy @strategyand.uk.pwc.com

Madrid

Raquel Garces Sañudo PwC Spain +34-91-411-8450raquel.garces.sanudo @strategyand.es.pwc.com

Milan

Roberto Bartocetti PwC Italy +39-34-8260-7297roberto.bartocetti @strategyand.it.pwc.com

Munich

Philipp Wackerbeck PwC Strategy& Germany+49-170-2238-659philipp.wackerbeck @strategyand.de.pwc.com

New York

Steve PearsonPwC US +1-646-471-0080 [email protected]

Arjun SaxenaPwC US [email protected]

São Paulo

Ivan de Souza PwC Brazil +55-11-999-781-541ivan.de.souza @strategyand.br.pwc.com

Singapore

Winston NesfieldPwC Singapore +65-9159-1425winston.nesfield @strategyand.sg.pwc.com

Sydney

Peter Burns PwC Australia +34-91-411-8450peter.burns @strategyand.au.pwc.com

Sarah Butler PwC Australia +61-2-8266-5001sarah.m.butler @strategyand.au.pwc.com

Tokyo

Vanessa Wallace PwC Japan +81-80-5881-7959vanessa.wallace @strategyand.jp.pwc.com

Vienna

Andreas Putz PwC Strategy& Austria +43-664-5152-908andreas.putz @strategyand.at.pwc.com

Zurich

Daniel Diemers PwC Strategy& Switzerland+41-79-6200-929daniel.diemers @strategyand.ch.pwc.com

3Strategy&

About the authors

Dr. Philipp Wackerbeck is an advisor to executives in financial services for Strategy&, PwC’s strategy consulting business. Based in Munich, he is a partner with PwC Strategy& Germany. He leads the risk and regulation team in Europe, the Middle East, and Africa and the financial-services team in Germany, Switzerland, and Austria. He has led numerous assignments in stress testing, financial stability, and banking-sector restructuring throughout Europe, the U.S., and the Middle East.

Arjun Saxena is an advisor to executives in financial services for Strategy&. Based in New York, he is a principal with PwC US. He serves global financial-services clients in the U.S., Europe, and Canada, focusing on risk, regulation, and business strategy. He has led numerous engagements on enterprise risk management, stress testing, capital planning, resolution planning, and related topics for large U.S. and global financial institutions.

Jeroen Crijns is a specialist in risk, capital, and regulation for Strategy&. He is a director with PwC Netherlands based in Amsterdam. Within the European financial-services practice, he focuses on stress testing and integrated financial planning. He has led many stress-testing assignments from both a supervisory and bank perspective.

Dr. Christel Karsten is a recognized innovator with Strategy& based in Amsterdam. She is a manager with PwC Netherlands. She specializes in risk and regulatory reporting, risk management, and valuation in the financial-services sector. She has supported multiple banks with executing and enhancing their stress-testing approach as well as improving their risk management.

The following people also contributed to this report: Benjamin Baur, Renée van der Mijle, Harman Korte, Robert Steemers, and Mark Tissot.

4 Strategy&

Executive summary

The 2008–09 financial crisis triggered a significant increase in bank regulation and supervision around the world. Basel III was enacted to fortify regulation, introducing new capital buffers, increasing liquidity, and expanding the scope of risk management. Meanwhile, bank supervisors in Europe and the U.S. have shifted their focus toward trying to determine whether individual banks could survive another negative economic environment. They have put in place a series of stress tests to evaluate bank performance and capital under a range of challenging scenarios.

Whereas some banks perceive these increased regulatory demands as a burden, others have successfully leveraged the capabilities they have developed in response to this in their daily business activities and decision-making processes. Having analyzed the stress-testing capabilities of 27 banks throughout Europe and the U.S., we have found that banks that effectively use their stress-test findings in their day-to-day activities show higher performance across several key dimensions, including earnings strength, capital adequacy, and asset quality. This could be because fully embedding these insights enables banks to make more efficient use of capital, optimize their risk–return profiles, and intervene earlier and more effectively to mitigate downside risk.

However, to ensure an effective process and reliable results, banks must enhance their internal stress-testing capabilities. That means making certain that their results come from high-quality data, accurate models, efficient testing processes, and proper risk scenario coverage, and that they develop consistent processes for making use of those results. This report describes what banks can learn from their best-in-class peers that have incorporated the insights from stress testing into their risk management and business decision making.

We strongly advise all banks to adopt and develop these stress test capabilities to make the performance gains that many leading banks have already achieved.

5Strategy&

Regulatory pressure

Stress testing, both regulatory and internal, is aimed at providing a detailed picture of a bank’s current risk position, its key risk drivers, and the main sensitivities of its portfolio. These tests offer a comprehensive, forward-looking perspective on a bank’s full balance sheet and profit-and-loss statements, giving the bank an assessment of the combined impact of all the risks it might face.

Because a bank’s assets and liabilities are generally highly diverse and complex, its aggregated risk profile is often not fully understood, especially by senior management or the board of directors. Stress testing can be a powerful tool to increase this understanding. By using the results to evaluate the bank’s business strategy, financial plans, and risk management, senior management can better assess tactical decisions, such as product pricing and divesting a portfolio, against strategic perspectives and targets.

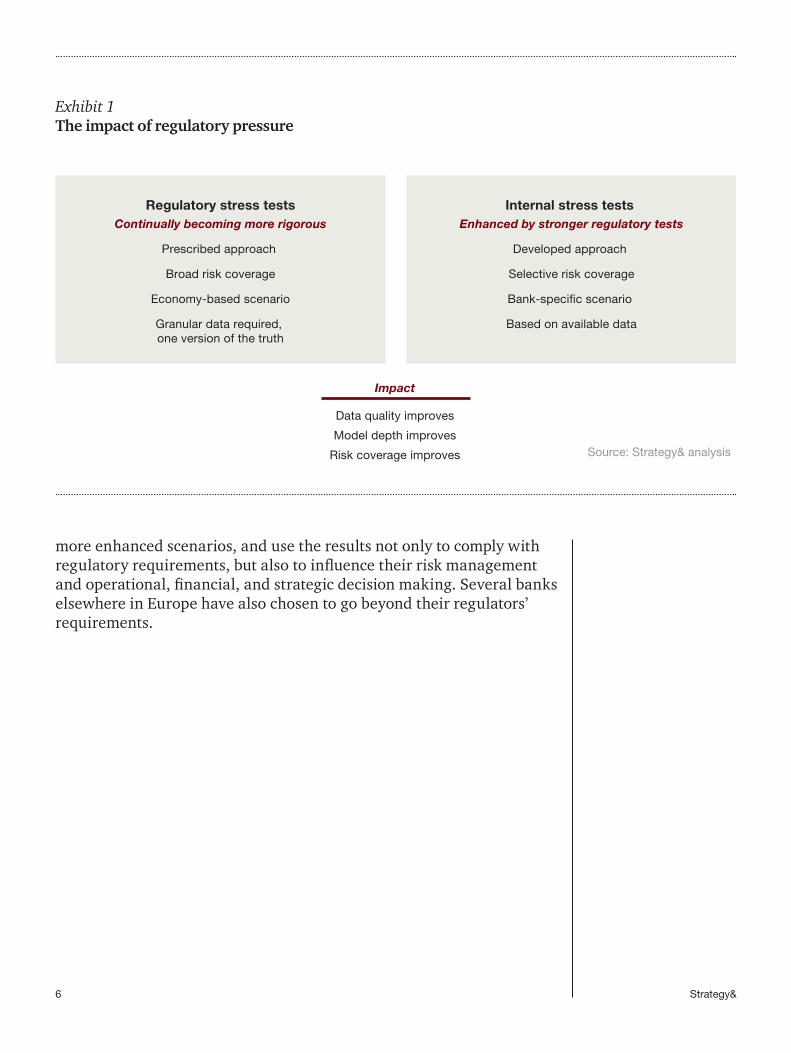

Bank supervisors in different countries and regions, however, take different approaches to how they test their banks. (See “Stress-testing approaches vary,” page 8.) Since banks have generally developed their internal stress-testing models in line with their particular regulatory requirements, they have in turn taken different approaches to how they conduct their internal tests, the models they use, and what they do with the results (see Exhibit 1, next page).

Exhibit 2, page 7, lays out the results of our survey regarding the degree to which 27 banks across Europe and the U.S. have succeeded in embedding their internal stress test results into their overall management practices. For the most part, banks in Europe conduct stress tests primarily to comply with regulatory requirements. As a result, these banks derive only limited insights into how the results should affect their business decision-making and risk management processes.

Meanwhile, banks in the U.S. and in Sweden have leveraged their supervisors’ more complete and individualized approach to stress testing to perform stress tests more frequently than required, apply

6 Strategy&

more enhanced scenarios, and use the results not only to comply with regulatory requirements, but also to influence their risk management and operational, financial, and strategic decision making. Several banks elsewhere in Europe have also chosen to go beyond their regulators’ requirements.

Exhibit 1The impact of regulatory pressure

Source: Strategy& analysis

Regulatory stress testsContinually becoming more rigorous

Prescribed approach

Broad risk coverage

Economy-based scenario

Granular data required, one version of the truth

Internal stress tests Enhanced by stronger regulatory tests

Developed approach

Selective risk coverage

Bank-speci�c scenario

Based on available data

Impact

Data quality improves

Model depth improves

Risk coverage improves

7Strategy&

Exhibit 2Geographic differences in stress-testing capabilities

Note: All of these banks have been subjected to regulatory stress tests in the past two years. Their stress-testing capabilities were assessed against standardized criteria. For each criterion, a score from 1 to 5 has been granted, and those scores have been aggregated into scores for stress-testing embeddedness and several other stress-testing dimensions. The information was derived from interviews with experts who have worked with or at these banks during their regulatory stress tests.

Source: Strategy& analysis

2

4

5

3

1

U.K.

U.S. and Sweden

Europe

High

Medium

Low

Level of embedding of stress test insights

Asset size(in € billions)

10 100 1,000 10,000

8 Strategy&

Stress-testing approaches vary

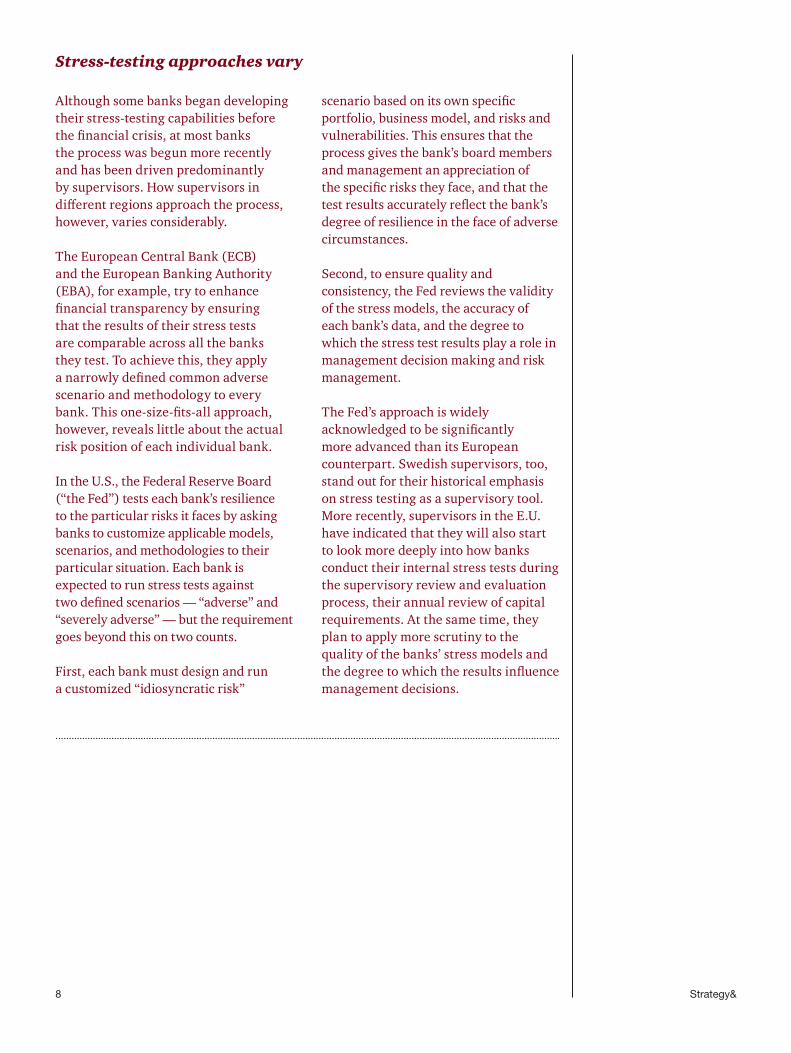

Although some banks began developing their stress-testing capabilities before the financial crisis, at most banks the process was begun more recently and has been driven predominantly by supervisors. How supervisors in different regions approach the process, however, varies considerably.

The European Central Bank (ECB) and the European Banking Authority (EBA), for example, try to enhance financial transparency by ensuring that the results of their stress tests are comparable across all the banks they test. To achieve this, they apply a narrowly defined common adverse scenario and methodology to every bank. This one-size-fits-all approach, however, reveals little about the actual risk position of each individual bank.

In the U.S., the Federal Reserve Board (“the Fed”) tests each bank’s resilience to the particular risks it faces by asking banks to customize applicable models, scenarios, and methodologies to their particular situation. Each bank is expected to run stress tests against two defined scenarios — “adverse” and “severely adverse” — but the requirement goes beyond this on two counts.

First, each bank must design and run a customized “idiosyncratic risk”

scenario based on its own specific portfolio, business model, and risks and vulnerabilities. This ensures that the process gives the bank’s board members and management an appreciation of the specific risks they face, and that the test results accurately reflect the bank’s degree of resilience in the face of adverse circumstances.

Second, to ensure quality and consistency, the Fed reviews the validity of the stress models, the accuracy of each bank’s data, and the degree to which the stress test results play a role in management decision making and risk management.

The Fed’s approach is widely acknowledged to be significantly more advanced than its European counterpart. Swedish supervisors, too, stand out for their historical emphasis on stress testing as a supervisory tool. More recently, supervisors in the E.U. have indicated that they will also start to look more deeply into how banks conduct their internal stress tests during the supervisory review and evaluation process, their annual review of capital requirements. At the same time, they plan to apply more scrutiny to the quality of the banks’ stress models and the degree to which the results influence management decisions.

9Strategy&

What’s in it for the banks?

As important as it is for banks to bring their stress test results into their daily operations, the institutions vary considerably in the degree to which they have done so — which could have a considerable impact on their operating and financial performance. Banks that have more completely incorporated stress test findings into their daily activities are better able to assess tactical decisions such as product pricing and portfolio management. These banks typically show better performance across a number of indicators.

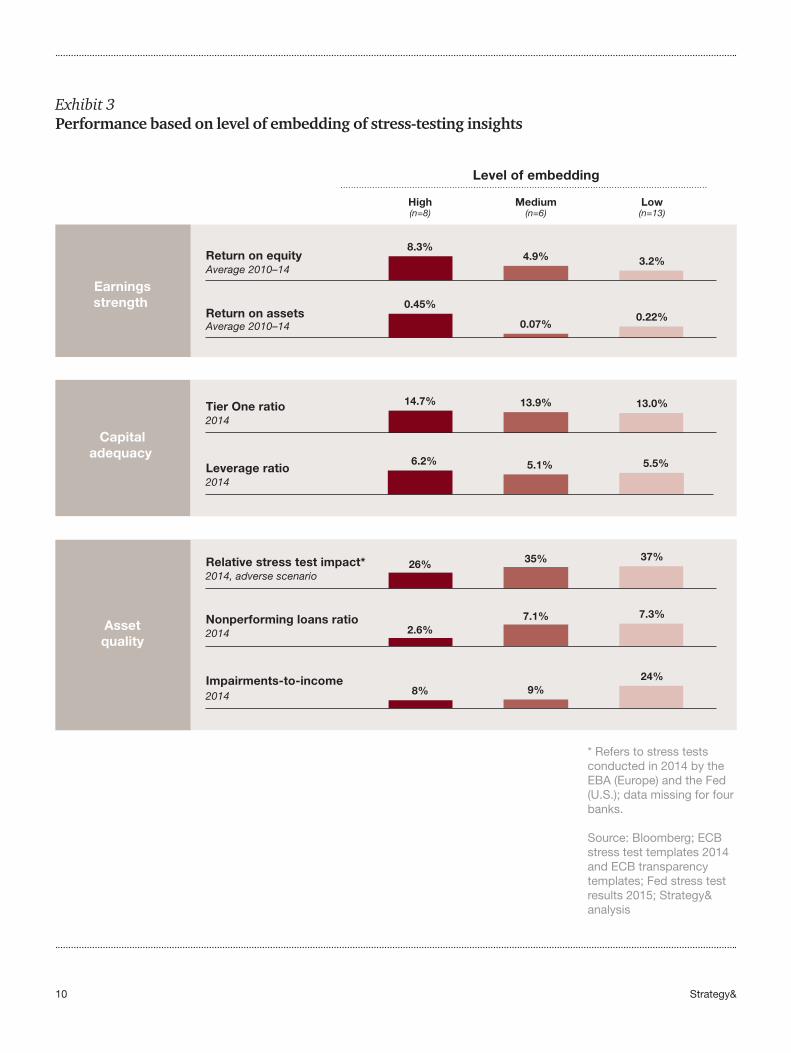

Exhibit 3, next page, shows the correlation between performance and the use of stress test data on several financial metrics. On average, banks that have embedded the findings more deeply show better earnings strength, as indicated by their return on equity and return on assets. And they tend to have a higher Tier One ratio and leverage ratio, which indicates that their higher returns are not achieved by increasing their risk profile. Instead, the quality of their assets is verifiably better, as shown by the relatively low impact they experienced during their regulatory stress test. Their credit risk is lower, too, as indicated by their lower ratio of nonperforming loans and ratio of impairments to income.

10 Strategy&

Exhibit 3Performance based on level of embedding of stress-testing insights

* Refers to stress tests conducted in 2014 by the EBA (Europe) and the Fed (U.S.); data missing for four banks.

Source: Bloomberg; ECB stress test templates 2014 and ECB transparency templates; Fed stress test results 2015; Strategy& analysis

3.2% 4.9% 8.3%

0.07% 0.45%

0.22%

Return on equity Average 2010–14

Medium(n=6)

Low(n=13)

High(n=8)

Earningsstrength

Capitaladequacy

Level of embedding

Return on assets Average 2010–14

13.9% 13.0% 14.7% Tier One ratio 2014

Assetquality

8% 9% 24%

Relative stress test impact* 2014, adverse scenario

Nonperforming loans ratio2014

Impairments-to-income2014

5.5% 5.1% 6.2% Leverage ratio 2014

2.6% 7.1% 7.3%

26% 35% 37%

11Strategy&

Learn from the best

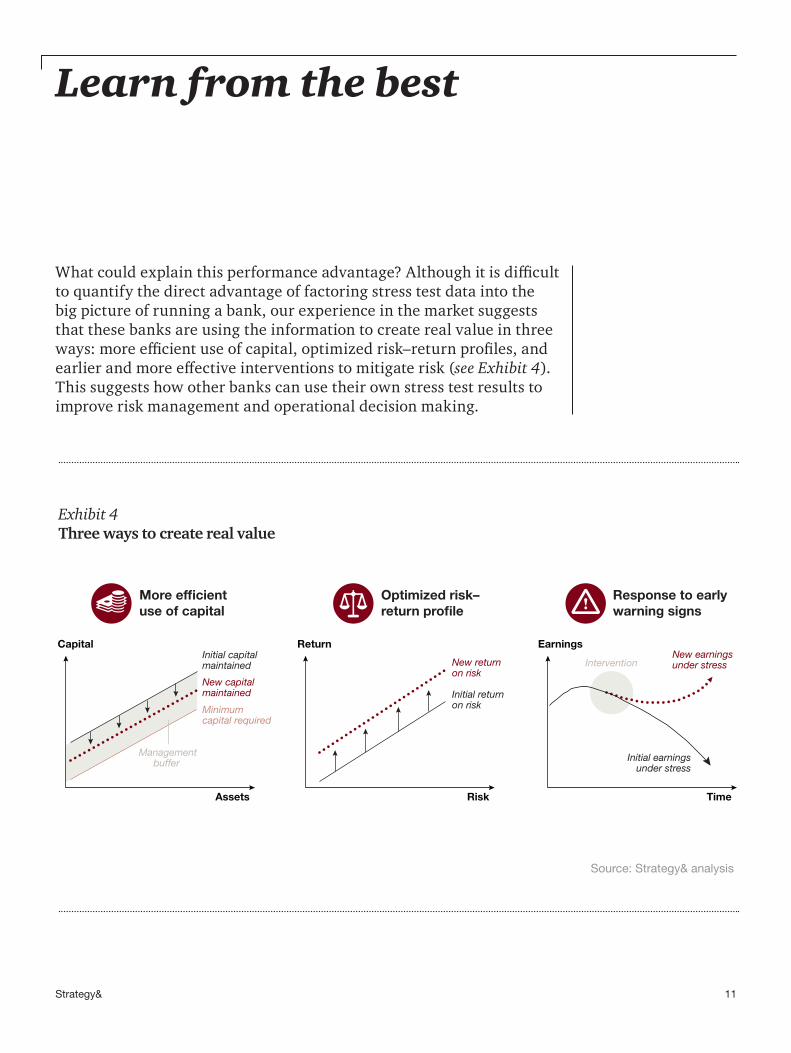

What could explain this performance advantage? Although it is difficult to quantify the direct advantage of factoring stress test data into the big picture of running a bank, our experience in the market suggests that these banks are using the information to create real value in three ways: more efficient use of capital, optimized risk–return profiles, and earlier and more effective interventions to mitigate risk (see Exhibit 4). This suggests how other banks can use their own stress test results to improve risk management and operational decision making.

Exhibit 4Three ways to create real value

Source: Strategy& analysis

Capital

Assets

Minimumcapital required

New capitalmaintained

New returnon risk

New earningsunder stress

Initial returnon risk

Initial earningsunder stress

Managementbuffer

Initial capitalmaintained

Return

Risk

Intervention

Earnings

Time

More efficientuse of capital

Optimized risk–return profile

Response to earlywarning signs

12 Strategy&

1. More efficient use of capital. Proper stress testing increases the transparency of a bank’s aggregate risk position, offering the possibility that banks could reduce their margin of

conservatism and hold less capital in their portfolio than they currently do. As the frequency of internal stress tests increases, the accuracy of the results typically improves as well. By incorporating these results into the limits they place on risky capital levels, defaults, loans, and the like, for example, senior managers can gain a more accurate and up-to-date perspective on their banks’ performance and risks. Moreover, they can assess how close these risks are to their risk limits, and whether those limits are set properly. This transparency allows banks to potentially reduce required capital in two main ways.

First, as the test models become more stable and reliable, and the risk parameters better substantiated, the assumptions used to generate the capital projection models can be more accurate and targeted, and thus allow for less conservative capital buffers. That increases the predictability of a bank’s capital requirements, allowing management to hold capital closer to target levels.

Second, conducting internal stress tests can provide a comprehensive perspective on a bank’s performance, and thus facilitates communication with external parties, including regulators, of course, but also investors, customers, and rating agencies. This can increase investors’ confidence and reduce the minimum return they demand on their investment. Rating agencies, too, may grant better ratings on the basis of improved transparency and risk management.

2. Optimized risk–return profiles. With a deeper understanding of key risk drivers, banks can better focus their portfolio composition on assets with high returns relative to

risk. There are several ways to optimize:

• Capital allocation. Greater understanding of sensitivities, portfolio interrelations, and even client types allows banks to allocate funds across portfolios more efficiently. More capital could, for example, be allocated to clients or products that face a relatively low impact under stress while earning the same return, or to parts of the portfolio whose level of risk is not closely correlated to the portfolio as a whole. This kind of detail can also be used to identify less risky products, clients, and markets to invest in for further growth, and to assess the degree to which such investments can grow before a predetermined level of risk is reached.

Stress tests can facilitate communication with external parties, which can increase investors’ confidence.

13Strategy&

• Portfolio transactions. In response to changing regulation, banks have been more actively evaluating their plans for acquisitions and divestitures. Stress testing can provide guidance through a calculation of the impact on a bank’s overall risk profile in the event of a business or portfolio acquisition or sale. Such insights help not only to identify appropriate portfolios, but also to value them more accurately.

For example, the managers at one bank with a portfolio focused primarily on commercial banking used stress testing to better understand the effect of the potential acquisition of a retail depository in various macroeconomic environments. With the foresight derived from this exercise, they improved the price they were willing to pay for the acquisition. Similarly, another bank looking to make an acquisition ran a stress test to analyze the impact of stress on the hypothetical balance sheet of the combined bank after the acquisition. By determining the effect of the deal on the post-acquisition risk profile, the bank’s management could more accurately value the synergies with the target bank.

• Product pricing. Determining the right price for a financial instrument, such as a loan, invariably involves assessing the risk involved. By incorporating an assessment of the instrument’s performance under stress, banks can determine a more accurate price. This is especially valuable if risk parameters such as probability of default and loss given default are expected to change drastically under stress.

At one large U.S. bank, for example, managers combined several different measures of risk capital in their estimation of the bank portfolio’s return on required capital, which is used in pricing decisions. These measures included the capital required under a stress test, in addition to that required by more traditional regulations. As a result, the bank was able to assign a more competitive price to the products that would be less risky under stress, while earning a better return on the riskier ones.

• Funding requirements. Aside from adjusting the composition of their assets, banks can also apply stress test results to optimize their funding mix. Stress tests can provide estimates of the margins a bank might earn from different types of loans in times of stress. Moreover, stress tests show the extent to which such margins fluctuate depending on funding mixes with different characteristics, such as the average maturity and whether the interest rates are fixed or floating. Armed with this information, banks can identify the optimal funding mix that ensures high margins within reasonable risk constraints.

Stress testing can provide guidance in the event of a business acquisition or sale.

14 Strategy&

3. Response to early warning signs. A thorough understanding of the external risks banks might face under stress scenarios can enable the institutions to identify

potential losses and better prepare for their possibility by analyzing the effectiveness of mitigating measures. Actions to reduce risk leading into such an environment might include reducing exposure to specific financial instruments, markets, or customers; improving collateral levels; strengthening efforts to collect on the most exposed loans; adjusting the funding mix; and implementing hedges.

To illustrate, the recent decline in oil and gas prices has significantly affected the operating performance of banks with a high share of customers dependent on the oil and gas sector. In the case of one U.S. bank with significant exposure to this sector, an early analysis of the potential impact of such a decline enabled the bank to quantify the effects on its balance sheet and take corrective action beforehand. Upon facing the actual decline in prices, the bank quickly responded by instituting a macroeconomic hedge through actively managed short positions. As a result, the bank was able to continue supporting its customers in this industry without being hamstrung by further deterioration in its credit profiles. As the decline in oil prices continued, the incremental credit risk from serving oil and gas clients was largely offset by the increase in the value of the hedge position.

15Strategy&

How to get there

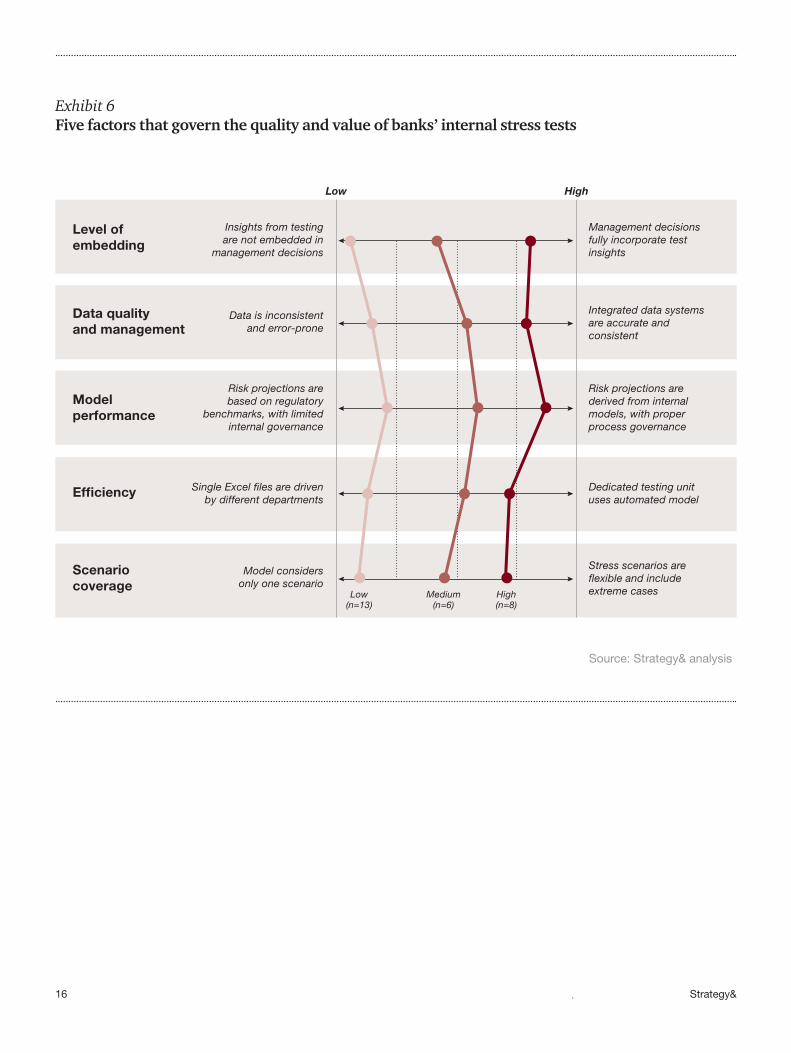

Banks can derive the benefits from their internal stress testing only if they have an effective process for incorporating the results into the relevant management decision making (see Exhibit 5). The results must also be of sufficiently high quality to be reliable and informative. To achieve this, banks should ensure high data quality, model performance, efficiency, and scenario coverage. Exhibit 6, next page, illustrates the

Exhibit 5How to get there

Source: Strategy& analysis

Data qualityand management

Model performance

Efficiency Scenariocoverage

Level ofembedding

16 Strategy&

Exhibit 6Five factors that govern the quality and value of banks’ internal stress tests

Source: Strategy& analysis

Data qualityand management

Model performance

Scenariocoverage

Efficiency

Level of embedding

Insights from testingare not embedded in

management decisions

Data is inconsistentand error-prone

Risk projections are based on regulatory

benchmarks, with limited internal governance

Single Excel files are driven by different departments

Model considers only one scenario

Management decisions fully incorporate test insights

Integrated data systems are accurate and consistent

Risk projections are derived from internal models, with proper process governance

Dedicated testing unit uses automated model

Stress scenarios are flexible and include extreme casesMedium

(n=6)Low

(n=13)High

Low High

(n=8)

17Strategy&

level of embedding and the range of proficiency in each of these five factors among the banks we studied.

Level of embedding. Banks with highly embedded stress-testing approaches typically apply the test results in two ways: through formalized processes and in ad hoc decision making. In terms of formalized processes, stress-testing analyses are applied as part of various core banking activities, such as allocating capital across divisions, setting operational budgets and targets, defining risk appetite and monitoring the resulting performance, and capital and liquidity planning. For major investments or strategic decisions such as M&A transactions or a change in pricing strategy, banks typically conduct ad hoc stress test analyses to determine the impact.

Data quality and management. High-quality data that provides an accurate picture of the bank’s current position is essential in ensuring that the results of the test are meaningful and useful. As a rule, banks proficient at conducting internal stress tests have developed integrated databases that contain reliable and consistent historical information. Their databases typically align data from both finance and risk, including such data as loan-level exposure and collateral values, combined with volumes, interest rates, and contract duration information, allowing for a complete assessment of their portfolios.

Model performance. The models and risk projections used to conduct stress tests are not perfect representations of reality and therefore will contain some degree of uncertainty. Expert judgment should supplement all scenario modeling, and at times might provide a better evaluation. However, the models that a bank uses must be sensitive to potential future scenarios. Strong banks have accomplished this goal in two ways. First, they base the estimates of their models’ risk parameters on statistical models rather than on expert judgment. These include both credit risk parameters, such as the probability of default and losses given default, and interest rate parameters, such as the rates at which banks can borrow or lend under stress scenarios. Second, they put in place strong governance and quality assurance processes that ensure full transparency and accountability for each modeling step, and they double-check the tests’ results against the models themselves.

Efficiency. If banks are to make better use of stress-testing results, the tests should be performed frequently and quickly. Many strong banks have invested in integrating their estimation models and reorganized their stress-testing efforts into a centralized function. Some have developed systems that allow stress tests to be run automatically, with the calculations performed in short order. At one bank, for instance, a dedicated stress-testing team has developed a tool that rapidly extracts

18 Strategy&

data directly from the internal systems and automatically estimates the impact of multiple scenarios.

Scenario coverage. Banks that take into account a wide range of stress scenarios are better able to manage their current and future operations. Such scenarios should include macroeconomic developments, management decisions such as divesting a specific portfolio, industry-specific risks like the entrance of a new competitor into the bank’s market, and geopolitical changes, such as a breakup of the eurozone.

19Strategy&

Don’t wait for the supervisors

Supervisors around the world will most likely push banks to further develop their capabilities and embed stress testing in their decision-making processes. Therefore, banks are strongly advised to adopt and develop such capabilities before they are required to do so. This is especially true of European banks: Having just completed their 2016 regulatory stress tests, they have some breathing room before the next round.

Banks that have not yet done so should push hard to improve their data quality, model performance, efficiency, and scenario flexibility. The investment required is only a small portion of the structural benefits they can capture. Banks that already have strong stress-testing capabilities should make the insights a key factor in their strategic and day-to-day decisions by broadening the scenario coverage of their stress tests and integrating the findings into their existing processes, including risk assessment, operational planning, and capital planning.

The benefits, both strategic and tactical, are real. Now is the time to move forward.

© 2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. Mentions of Strategy& refer to the global team of practical strategists that is integrated within the PwC network of firms. For more about Strategy&, see www.strategyand.pwc.com. No reproduction is permitted in whole or part without written permission of PwC. Disclaimer: This content is for general purposes only, and should not be used as a substitute for consultation with professional advisors.

www.strategyand.pwc.com

Strategy& is a global team of practical strategists committed to helping you seize essential advantage.

We do that by working alongside you to solve your toughest problems and helping you capture your greatest opportunities.

These are complex and high-stakes undertakings — often game-changing transformations. We bring 100 years of strategy consulting experience and the unrivaled industry and functional capabilities of the PwC network to the task. Whether you’re

charting your corporate strategy, transforming a function or business unit, or building critical capabilities, we’ll help you create the value you’re looking for with speed, confidence, and impact.

We are part of the PwC network of firms in 157 countries with more than 223,000 people committed to delivering quality in assurance, tax, and advisory services. Tell us what matters to you and find out more by visiting us at strategyand.pwc.com.