Strengthening governance, risk and compliance in the insurance industry

14

Strengthening governance, risk and compliance in the insurance industry An Economist Intelligence Unit report Sponsored by SAP

-

Upload

jordi-planas-manzano -

Category

Documents

-

view

2.025 -

download

2

description

EIU

Transcript of Strengthening governance, risk and compliance in the insurance industry

Strengthening governance, risk and compliance in the insurance industry An Economist Intelligence Unit reportSponsored by SAP

© Economist Intelligence Unit Limited 2009 Strengthening governance, risk and compliance in the insurance industry

1

Strengthening governance, risk and compliance in the insurance industry is an Economist Intelligence Unit report sponsored by SAP. The Economist Intelligence Unit bears sole responsibility for this report. The Economist Intelligence Unit’s editorial team conducted the interviews and wrote the report. The fi ndings and views expressed in this report do not necessarily refl ect the views of the sponsor. Dan Armstrong was the editor of the report and Mike Kenny was responsible for layout and design. Our thanks are due to all of the survey respondents and interviewees for their time and insights.

February 2009

Preface

© Economist Intelligence Unit Limited 2009Strengthening governance, risk and compliance in the insurance industry

2

Strengthening governance, risk and compliance in the insurance industry

Insurance companies have long struggled to gain greater effi ciency and transparency in their fi nancial processes through automation and process redesign. Their efforts have generally been focused on the

negative goals of controlling costs, reducing sudden fi nancial shocks and avoiding regulatory sanctions. However, some companies are discovering that a more integrated approach to managing fi nancial processes can be a source not only of effi ciency but also of strategic advantage.

Many companies are aiming at achieving that added value through governance, risk and compliance (GRC) initiatives, which embed rules, processes and controls in keeping with a carrier’s operating policies and strategic objectives. These measures provide greater transparency into day-to-day operations, help to identify potential risk exposures, and enable companies to react in a timely fashion to emerging risks. GRC is characterised by effi ciency and accuracy, but can also add the dimension of providing a synoptic picture of risk to support strategic decision-making.

That sort of insight has become suddenly much more important in 2009, in the wake of a fi nancial crisis that could just as accurately be termed a risk management crisis. While strict solvency requirements helped the insurance industry to weather the crisis better than their counterparts in banking and securities, some insurers did encounter unforeseen exposures in their investment portfolios, the consequences of which are yet to be fully realised. There is little question that many insurers lacked the capability to develop a comprehensive picture of risk exposure at a corporate level, comprising credit, market and operational risk.

Moreover, insurers operating in the European Union face challenges stemming from the updated set of regulatory requirements known as Solvency II. The Supervisory Review Process of Solvency II aims to identify institutions with fi nancial, organisational or other features that result in a higher risk profi le. Because the authorities will review fi nancial processes as well as governance and capital reserves, it will be necessary to know who know who participates in each process, what the person does, and the results of the process.

The problem with autonomyAchieving a unifi ed enterprise view of fi nancial process remains an almost quixotic goal in much of the insurance industry because of the operational autonomy of business units. Even in companies that enjoy a high degree of process automation, consistent use of practices and tools across the enterprise

© Economist Intelligence Unit Limited 2009 Strengthening governance, risk and compliance in the insurance industry

3

is rare. As Figure 1 shows, insurers struggle with complex procedures, inconsistent methodologies and incompatible technology. In order to produce a complete fi nancial picture on which to base decisions, survey respondents report the need to reconcile inconsistent or redundant data from disparate sources.

To some degree insurers are more concerned about the risks of improving their processes than the risks those processes can reveal, as illustrated by Figure 2. Nearly half of the respondents cited high cost as a barrier to standardising and automating fi nancial processes. They also reported diffi culties caused by the complexity of modeling fi nancial process and the incommensurability of regulatory regimes within different lines of business. Responses also showed that the siloed organisational structure of insurance companies made securing buy-in from line-of-business managers more diffi cult than corporate-level leadership.

Securian Financial, a $2.8 billion US life insurer based in Minnesota, eased its transition to an economic capital-based approach to risk management by enlisting business managers into working

About the survey

In 2008 and early 2009, on behalf of SAP, the Economist Intelligence Unit surveyed 446 senior executives from ten industries about their views on their fi nancial processes and their attempts to improve them. Of this total, 58 came from the insurance industry (both life and property and casualty). It is

these insurance executives upon which this paper is based. Of these respondents, 30% hailed from Europe, 25% from North America and 20% from the Asia/Pacifi c region. Over half worked for companies with annual revenues in excess of $1bn. One-third have positions in the C-suite and another 24% came from the VP level or higher. Most respondents served in the fi nance, risk management, strategy, business development or operations functions.

Complex procedures which are difficult to model or automate

Inconsistent methodologies around the organisation

Incompatible technology (eg, customised spreadsheets, databases and commercial products)

The need to reconcile inconsistent or redundant data from multiple sources

Boundaries between departments, with departmental managers trying to hold on to authority

Too many manual processes

Controls which are too numerous or restrictive

Portions of the process depend on individuals who are not always available

Lack of visibility and accountability

The need to document audit trails

Other

Figure 1: Insurers struggle with complexity, inconsistency and incompatibilityWhat are the biggest problems with your current financial processes? Select up to three. (% respondents)

Source: Economist Intelligence Unit survey, 2009.

36

36

33

33

29

29

21

19

16

12

5

© Economist Intelligence Unit Limited 2009Strengthening governance, risk and compliance in the insurance industry

4

groups on key topics. “Our approach was to work with them to achieve ‘quick wins’ demonstrating the advantages of the new way of measuring risk and value,” says Vice President and Chief Actuary Leslie Chapman. “For example, we formed an asset/liability management group. We have found that by having every business line actively engaging in dialogue has help drive buy-in.”

Chapman credits a combination of corporate risk management culture and the power of automation in enabling Securian to more precisely measure and project risk exposure. By building a platform allowing a view of risk from an economic capital perspective, the company is able to see the impact of decisions from multiple perspectives, which simultaneously enables more secure and more opportunistic management of risk.

“We have enhanced our fi nancial processes and reporting over the years so that we can spend less time quantifying and more time analysing,” comments Chapman. “We couldn’t do this at all without automation. But the value is multiplied as we get faster, enabling us to spend more time on decision-making, which results in higher-quality decisions.”

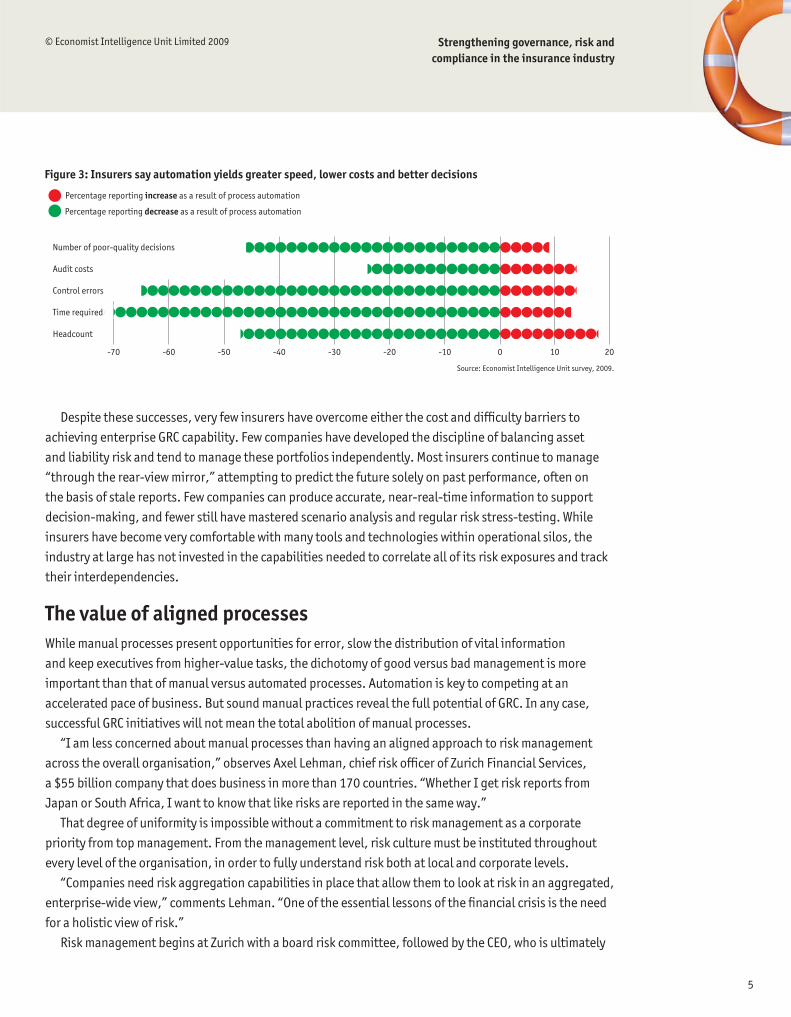

Securian is clearly not alone in its appreciation of the potential benefi ts of more automated fi nancial processes as demonstrated by survey respondents’ reports of the benefi ts their companies have enjoyed (Fig. 3). Respondents say that higher levels of automation have yielded faster processes with fewer errors while at the same time requiring less staff to manage them. By embedding risk assessments into fi nancial processes, two-thirds of respondents’ enjoyed greater effi ciency and over 80% reported higher-quality decisions.

Enhancing data integrity

Cutting back on manual processes, decreasing risk of error

Freeing staff from routine number-crunching, redeploying into higher-value activities

Meeting compressed deadlines/improve response time

Reducing costs

Better visibility into origin of numbers and how they are calculated

Standardisation of methodologies around the enterprise

Higher productivity

Able to set risk thresholds, data access and other controls centrally

Better compliance with regulatory requirements

Able to identify and resolve bottlenecks

Fewer opportunities for fraud

Other

Figure 2: Insurers want to improve data integrity and cut back on manual processesWhat would be the biggest benefits of an initiative to standardise and automate your financial processes? Select up to three. (% respondents)

Source: Economist Intelligence Unit survey, 2009.

50

48

43

34

24

17

16

16

12

10

9

3

2

© Economist Intelligence Unit Limited 2009 Strengthening governance, risk and compliance in the insurance industry

5

Despite these successes, very few insurers have overcome either the cost and diffi culty barriers to achieving enterprise GRC capability. Few companies have developed the discipline of balancing asset and liability risk and tend to manage these portfolios independently. Most insurers continue to manage “through the rear-view mirror,” attempting to predict the future solely on past performance, often on the basis of stale reports. Few companies can produce accurate, near-real-time information to support decision-making, and fewer still have mastered scenario analysis and regular risk stress-testing. While insurers have become very comfortable with many tools and technologies within operational silos, the industry at large has not invested in the capabilities needed to correlate all of its risk exposures and track their interdependencies.

The value of aligned processesWhile manual processes present opportunities for error, slow the distribution of vital information and keep executives from higher-value tasks, the dichotomy of good versus bad management is more important than that of manual versus automated processes. Automation is key to competing at an accelerated pace of business. But sound manual practices reveal the full potential of GRC. In any case, successful GRC initiatives will not mean the total abolition of manual processes.

“I am less concerned about manual processes than having an aligned approach to risk management across the overall organisation,” observes Axel Lehman, chief risk offi cer of Zurich Financial Services, a $55 billion company that does business in more than 170 countries. “Whether I get risk reports from Japan or South Africa, I want to know that like risks are reported in the same way.”

That degree of uniformity is impossible without a commitment to risk management as a corporate priority from top management. From the management level, risk culture must be instituted throughout every level of the organisation, in order to fully understand risk both at local and corporate levels.

“Companies need risk aggregation capabilities in place that allow them to look at risk in an aggregated, enterprise-wide view,” comments Lehman. “One of the essential lessons of the fi nancial crisis is the need for a holistic view of risk.”

Risk management begins at Zurich with a board risk committee, followed by the CEO, who is ultimately

-70 -60 -50 -40 -30 -20 -10 0 10 20

Number of poor-quality decisions

Audit costs

Control errors

Time required

Headcount

Figure 3: Insurers say automation yields greater speed, lower costs and better decisions

Percentage reporting decrease as a result of process automation

Percentage reporting increase as a result of process automation

Source: Economist Intelligence Unit survey, 2009.

© Economist Intelligence Unit Limited 2009Strengthening governance, risk and compliance in the insurance industry

6

responsible for risk management. As chief risk offi cer, Lehman shares risk management with other members of the executive team, who in turn work with business unit leaders, who are responsible for observing risk management procedures and standards while retaining the independence they need to function as business managers.

Zurich has implemented a Risk Modeling Platform with the ability to tap into other information systems and reconcile information. That gives the insurer the ability to understand local risks and aggregate them up through various levels of the organisation. Zurich has also instituted what it calls Total Risk Profi ling, which identifi es and records risk at all levels of the organisation, and it has implemented an economic capital framework to project return on risk-based capital in the company’s strategic decision-making.

Too often insurers limit their risk management activities to the negative goals of protection, reducing earnings volatility, protecting the capital base and otherwise insulating the franchise from negative surprises, Lehman believes. He regards that approach as necessary but not suffi cient. “Risk management in a well-managed company is used to support profi table risk-taking and growth,” he says. “It is not only about being aware of the risk exposure, but strategically shaping the risk/return profi le of the organisation.

© Economist Intelligence Unit Limited 2009 Strengthening governance, risk and compliance in the insurance industry

7

Insurance companies were among the original adopters of information technology, and their actuaries, underwriters and accountants have demonstrated interest and even mastery in the use of a broad

range of technological tools in recent times. However, the traditional independence of business lines and the functions within them have contrived to render the insurance industry a laggard in process automation even in the core functions of governance, risk management and compliance that have special importance in a highly regulated industry dedicated to the profi table transfer of risk. Moreover, when insurers have adopted technology to upgrade governance, risk and compliance processes, the focus has been on reducing costs and increasing effi ciency rather than providing an integrated picture of risk to support better decisions. Cost reduction is still a compelling argument for moving forward, especially in a stagnant economy. But the less heralded benefi ts—which ultimately may be more important—have to do with improving the quality of decisions.

Companies have managed to be profi table despite their dependence on manual processes, but as the pace of business accelerates, the speed and effi ciency afforded by automation becomes more important. Even more important is the need to have an enterprise-wide picture of risk and the ability to identify and react to emerging risks. Risk is opportunity for insurers, but they need a tighter grip on their overall portfolio of risk with the emergence of new and imperfectly understood risks, such as those associated with the fi nancial markets, rapid change in laws and regulations, information security vulnerability, climate change, political instability and terrorism.

An example of how fi nancial process integration can generate returns rather than simply reduce costs might be the effort by property and casualty insurers to target home and auto insurance policies by location. Underwriting guidelines have long distinguished among risks in different postal codes. Adding precise elevation data by latitude and longitude allows insurers to go further and target, for instance, high-elevation addresses in a postal code dominated by a fl ood plain. Similarly, a life insurance company might be able to quickly model and price the actuarial effects of, for instance, a widespread outbreak of avian fl u. Companies that integrate risk, pricing, location and sales activities should be able to “cherry pick” high-margin, low-risk underwriting opportunities.

Ultimately risk management is about management, not modeling. In the end, technology supplies input for decision-making, not the decisions themselves. Nevertheless, with a holistic implementation of GRC, governance risk and compliance are consistently defi ned, closely linked and embedded throughout the organisation through end-to-end processes and controls. Well-designed automated processes effi ciently integrate fi nancial reporting, compliance and risk monitoring into daily operations. Furthermore, they afford greater ease of modifi cation, giving insurers the ability to react to changes in the marketplace. Finally, they not only reinforce the protective aspects of risk management but they also provide the basis for strategic risk management as an engine of profi tability.

Conclusion

8

Economist Intelligence Unit 2009AppendixSurvey results: Insurance respondents only

Strengthening governance, risk and compliance in the insurance industry

AppendixSurvey results: Insurance respondents only

Complex procedures which are difficult to model or automate

Inconsistent methodologies around the organisation

Incompatible technology (eg, customised spreadsheets, databases and commercial products)

The need to reconcile inconsistent or redundant data from multiple sources

Boundaries between departments, with departmental managers trying to hold on to authority

Too many manual processes

Controls which are too numerous or restrictive

Portions of the process depend on individuals who are not always available

Lack of visibility and accountability

The need to document audit trails

Other

What are the biggest problems with your current financial processes? Select up to three. (% respondents)

36

36

33

33

29

29

21

19

16

12

5

High level of investment required

Difficulty of getting buy-in from business lines/regions

Difficulty of modeling complex financial processes

Multiple regulatory regimes make compliance rules unique by business and/or region

Difficulty of getting buy-in from senior management

Organisation is too diverse in its business lines

Business model and operations are unique

Financial processes are sufficiently fast, efficient and accurate now

What would be the biggest drawbacks of an initiative to standardise and automate financial processes? Select up to two.(% respondents)

47

28

26

24

21

17

14

7

Enhancing data integrity

Cutting back on manual processes, decreasing risk of error

Freeing staff from routine number-crunching, redeploying into higher-value activities

Meeting compressed deadlines/improve response time

Reducing costs

Better visibility into origin of numbers and how they are calculated

Standardisation of methodologies around the enterprise

Higher productivity

Able to set risk thresholds, data access and other controls centrally

Better compliance with regulatory requirements

Able to identify and resolve bottlenecks

Fewer opportunities for fraud

Other

What would be the biggest benefits of an initiative to standardise and automate your financial processes? Select up to three. (% respondents)

50

48

43

34

24

17

16

16

12

10

9

3

2

Economist Intelligence Unit 2009 AppendixSurvey results: Insurance

respondents only

Strengthening governance, risk and compliance in the insurance industry

9

Increase level of automation for processes in general

Prioritise controls based on risk assessments

Increase level of automation for internal controls

Realign segregation of duties

Reduce redundancies

Other

We have not attempted to improve our financial processes

In the past five years, which of the following tasks has your organisation attempted to address by improving its financial processes? Select all that apply.(% respondents)

76

50

48

43

34

3

2

Much higher Higher No change Lower Much lower Don’t know

Headcount

Time required

Control errors

Audit costs

Number of poor-quality decisions

What improvements, if any, have resulted from these attempts? Increase level of automation for processes in general(% respondents)

7 11 32 48 2

2 11 14 57 14 2

7 7 16 56 9 5

5 9 43 25 5 14

2 7 25 45 7 14

Much higher Higher No change Lower Much lower Don’t know

Headcount

Time required

Control errors

Audit costs

Number of poor-quality decisions

What improvements, if any, have resulted from these attempts? Increase level of automation for internal controls (% respondents)

4 19 31 42 4

19 19 48 15 0

19 11 44 22 4

4 11 44 22 7 11

8 20 48 8 16

Much higher Higher No change Lower Much lower Don’t know

Headcount

Time required

Control errors

Audit costs

Number of poor-quality decisions

What improvements, if any, have resulted from these attempts? Reduce redundancies (% respondents)

11 11 21 53 5 0

11 11 11 53 11 5

6 11 17 56 6 6

6 11 50 17 17

6 28 39 6 22

10

Economist Intelligence Unit 2009AppendixSurvey results: Insurance respondents only

Strengthening governance, risk and compliance in the insurance industry

Much higher Higher No change Lower Much lower Don’t know

Headcount

Time required

Control errors

Audit costs

Number of poor-quality decisions

What improvements, if any, have resulted from these attempts? Realign segregation of duties(% respondents)

4 25 38 25 8

21 33 38 8

22 30 39 4 4

22 57 17 4

5 55 32 5 5

Much higher Higher No change Lower Much lower Don’t know

Headcount

Time required

Control errors

Audit costs

Number of poor-quality decisions

What improvements, if any, have resulted from these attempts? Prioritise controls based on risk assessments (% respondents)

21 59 14 7

28 28 41 3 0

11 25 61 4 0

3 17 31 31 3 14

7 17 59 3 14

79

17

3

Yes

No

Don’t know

Does your organisation regularly include risk evaluations as part of its financial processes? (% respondents)

Much better Better No change Worse Much worse Don’t know

Quality of decisions

Efficiency of processes

Prioritisation of controls

What are the results of these risk evaluations? (% respondents)

11 72 17

6 53 36 6

17 53 28 3

Economist Intelligence Unit 2009 AppendixSurvey results: Insurance

respondents only

Strengthening governance, risk and compliance in the insurance industry

11

United States of America

United Kingdom

South Korea

Canada

Nigeria

Brazil

China

India

Netherlands

Switzerland

Australia

Belgium

Croatia

Czech Republic

Denmark

Germany

Ghana

Hong Kong

Hungary

Israel

Kenya

Latvia

Mexico

Poland

Puerto Rico

South Africa

Spain

Thailand

Turkey

Zimbabwe

In which country are you personally located?(% respondents)

20

9

7

5

5

4

4

4

4

4

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

4

4

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

2

30

25

20

14

7

4

Western Europe

North America

Asia-Pacific

Middle East and Africa

Latin America

Eastern Europe

In which region are you personally based? (% respondents)

100Financial services

What is your primary industry? (% respondents)

100Insurance

In which sub-sector of financial services does your organisation belong? (% respondents)

12

Economist Intelligence Unit 2009AppendixSurvey results: Insurance respondents only

Strengthening governance, risk and compliance in the insurance industry

26

19

16

19

19

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your job title?(% respondents)

2

10

16

0

5

24

12

14

12

5

Finance

Risk

General management

Strategy and business development

Marketing and sales

Operations and production

Customer service

IT

Human resources

R&D

Information and research

Legal

Procurement

Supply-chain management

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

45

40

34

29

16

14

12

7

5

5

3

0

0

0

3

Whilst every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsors of this report can accept any responsibility or liability for reliance by any person on this white paper or any of the information, opinions or conclusions set out in the white paper.

LONDON26 Red Lion SquareLondon WC1R 4HQUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8476E-mail: [email protected]

NEW YORK111 West 57th StreetNew York NY 10019United StatesTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchai Hong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]