Strategy & Overview - ceoclub.eu · Strategy & Overview March 2005 You & Us. 1 ... NNM Invested...

23

Strategy & Overview March 2005 You & Us

Transcript of Strategy & Overview - ceoclub.eu · Strategy & Overview March 2005 You & Us. 1 ... NNM Invested...

Strategy & Overview

March 2005

You & Us

1

Caution regarding forward-looking statementsThis communication contains statements that constitute “forward-looking statements”,including, but not limited to, statements relating to the implementation of strategic initiatives,such as the European wealth management business, and other statements relating to ourfuture business development and economic performance.

While these forward-looking statements represent our judgments and future expectationsconcerning the development of our business, a number of risks, uncertainties and otherimportant factors could cause actual developments and results to differ materially from ourexpectations.

These factors include, but are not limited to, (1) general market, macro-economic,governmental and regulatory trends, (2) movements in local and international securitiesmarkets, currency exchange rates and interest rates, (3) competitive pressures, (4) technologicaldevelopments, (5) changes in the financial position or credit worthiness of our customers,obligors and counterparties and developments in the markets in which they operate, (6)legislative developments, (7) management changes and changes to our Business Groupstructure and (8) other key factors that we have indicated could adversely affect our businessand financial performance which are contained in other parts of this document and in our pastand future filings and reports, including those filed with the SEC.

More detailed information about those factors is set forth elsewhere in this document and indocuments furnished by UBS and filings made by UBS with the SEC, including UBS’s AnnualReport on Form 20-F for the year ended 31 December 2003. UBS is not under any obligation to(and expressly disclaims any such obligations to) update or alter its forward-looking statementswhether as a result of new information, future events, or otherwise.

2

Agenda

♦ Facts & Figures

♦ Achievements & Track Record

♦ Growth Plan & Challenges

♦ Conclusion: Attractive Investment Case

Facts & Figures

4

♦ World's largestprivate bank

♦ CHF 918bninvested assets

♦ 4mn individualand corporateclients

♦ 25-35% of Swissbanking market

♦ 4th largest fullservice US broker

♦ 2mn privateclients

♦ 15% marketshare, 369 officesacross USA

♦ #1 muni franchise(15% marketshare)

♦ Top 5 globalbulge bracketposition

♦ #1 global Equityhouse (11%market share)

♦ #1 FX house (12%market share)

♦ 6'000corporations/institutions/clients

♦ Leadinginstitutional andwholesale assetmanager

♦ CHF 601bninvested assets

♦ Broad basedcapabilities

♦ Second largestEuropean mutualfund manager

Facts and figures

CHF 2.3 trillion invested assetsCHF 113.9 billion market capitalization1

CHF 34.5 billion equityOver 67'000 employees

UBS Group

WealthManagement &

Business Banking

WealthManagement

USAInvestment Bank Global Asset

Management

Note:1 Market capitalisation as per 9.2.2005

5

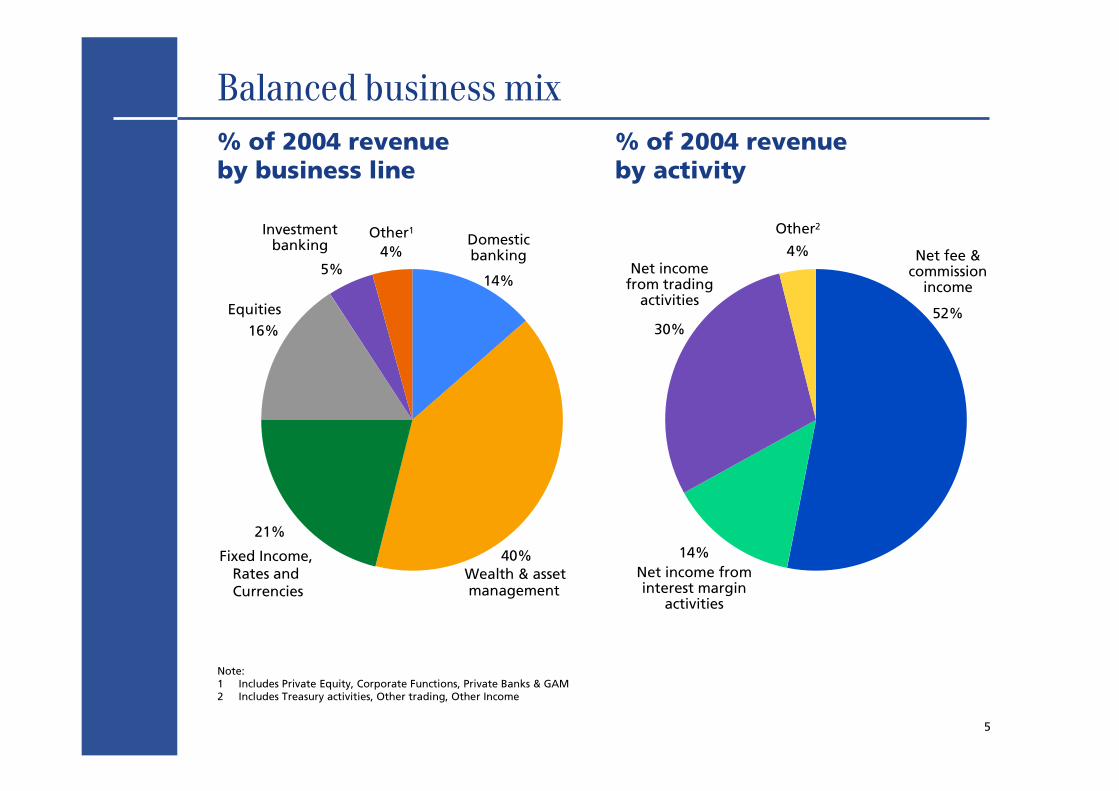

Balanced business mix% of 2004 revenueby business line

Net fee &commission

income

Net income frominterest margin

activities

Net incomefrom trading

activities

% of 2004 revenueby activity

Other2

52%

14%

4%

30%

14%

40%

21%

16%

5%4%

Domesticbanking

Equities

Investmentbanking

Wealth & assetmanagement

Fixed Income,Rates andCurrencies

Other1

Note:1 Includes Private Equity, Corporate Functions, Private Banks & GAM2 Includes Treasury activities, Other trading, Other Income

6

High margin businesses, with significant barriers to entry

1 2004 pre-tax profit margin pre goodwill2 Group profit before tax pre goodwill 20043 Includes Corporate Functions performance before tax

31% 5% 18% 6% 42% 4% 100%3

% of group profit before tax2

Pre-tax margin1

0

10

20

30

40

5046%

41%

33%30%

15%

46%

30%

WealthManagement

BusinessBanking

Switzerland

Global AssetManagement

InvestmentBank

WealthManagement

USA*

PrivateBanks &

GAM

UBS

%

Achievements & Track Record

8

Achievements & track record

Franchise growth

Attractive and consistent financial results

One-firm concept

9

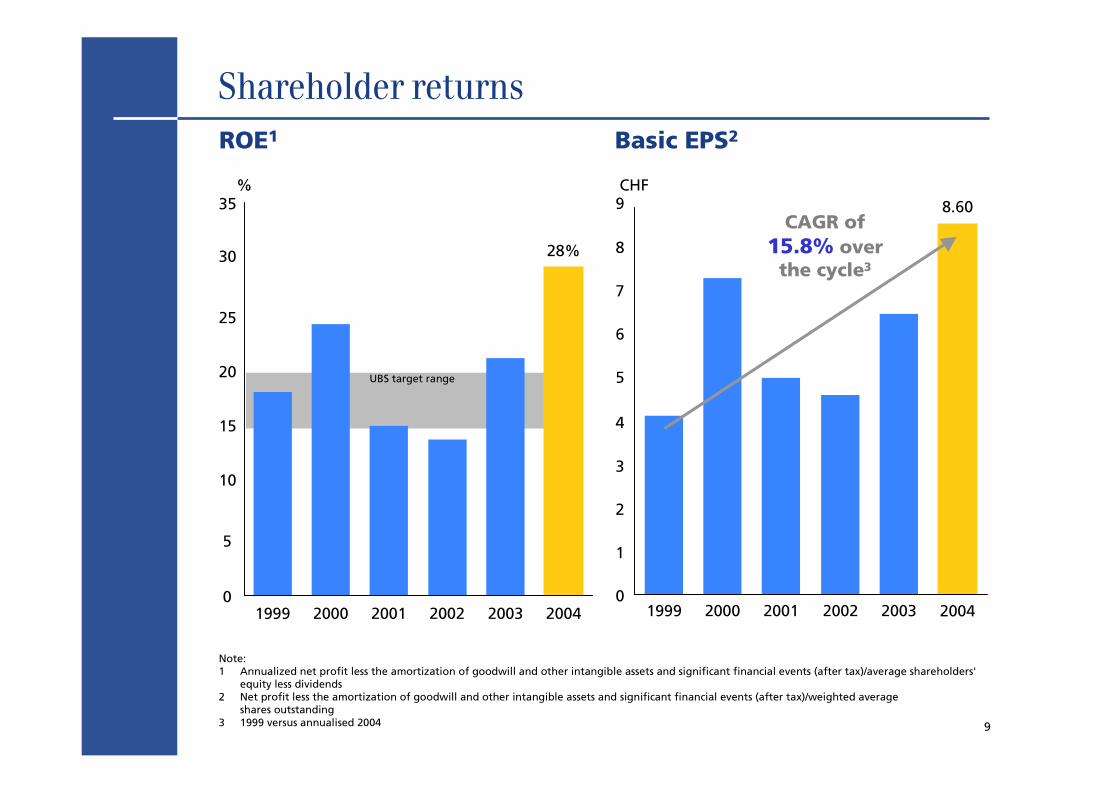

Shareholder returnsROE1 Basic EPS2

Note:1 Annualized net profit less the amortization of goodwill and other intangible assets and significant financial events (after tax)/average shareholders'

equity less dividends2 Net profit less the amortization of goodwill and other intangible assets and significant financial events (after tax)/weighted average

shares outstanding3 1999 versus annualised 2004

28%

UBS target range

0

5

10

15

20

25

30

35

1999 2000 2001 2002 2003 2004

CHF8.60

1999 2000 2001 2002 2003 2004

CAGR of15.8% over

the cycle3

0

1

2

3

4

5

6

7

8

9%

10

Return of capital to shareholders1

Note:1 Dividend is shown in the year of performance

60% of Operating cash flow returned to shareholders since1999

Buy-back program Dividend/par value reduction

CHF bn

0

5

10

15

20

25

30

35

1999 2000 2001 2002 2003 2004 Total

2

6

4

8

7

7 35

11

Net new moneyNNM UBS1 NNM wealth management

businesses

Note:1 Numbers from 1999 to 2001 have not been restated for definitional change

WM-US WM

0

10

20

30

40

50

60

70

16

2000

56

2001

36

2002

51

2003

CHF bn

1999

4 17

42

2004

59

-46-60

-40

-20

0

20

40

60

80

100

120

1999

-50

2000

102

2001

37

2002

69

2003

89

2004

CHF bn

12

The integrated business model at work

Corporate Center

WealthManagement

USA

Global AssetManagement

InvestmentBanking

WealthManagement &

Business Banking

Tradeflows

Funds

Tradeflows

Structured productsCorporate finance advice

NNMinflow

NNMinflow

Funds

DerivativesResearch

Tradeflows

Sales &Market-

ing

Productexper-

tise

ITI Controlling Communication Human ResourcesRisk Management Treasury

Structured productsCorporate finance advice

13

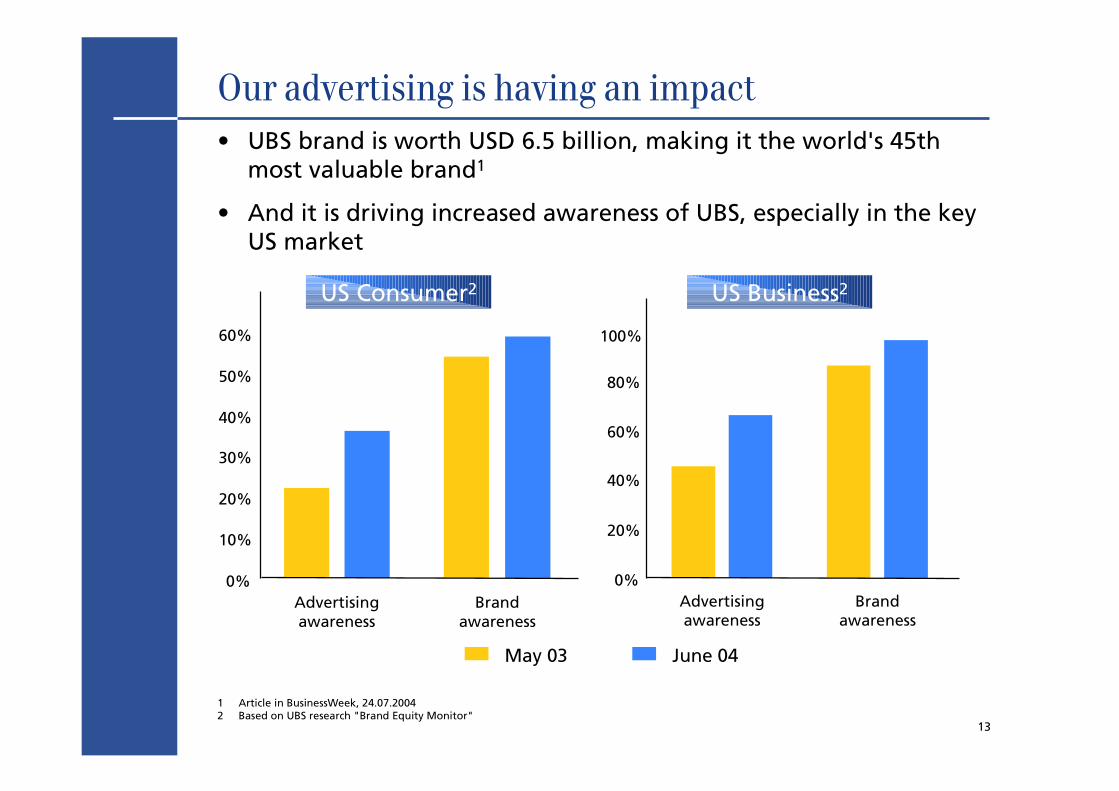

Our advertising is having an impact

US Consumer2 US Business2

May 03 June 04

• UBS brand is worth USD 6.5 billion, making it the world's 45thmost valuable brand1

• And it is driving increased awareness of UBS, especially in the keyUS market

1 Article in BusinessWeek, 24.07.20042 Based on UBS research "Brand Equity Monitor"

0%

10%

20%

30%

40%

50%

60%

Advertisingawareness

Brandawareness

Advertisingawareness

Brandawareness

100%

0%

20%

40%

60%

80%

Growth Plan & Challenges

15

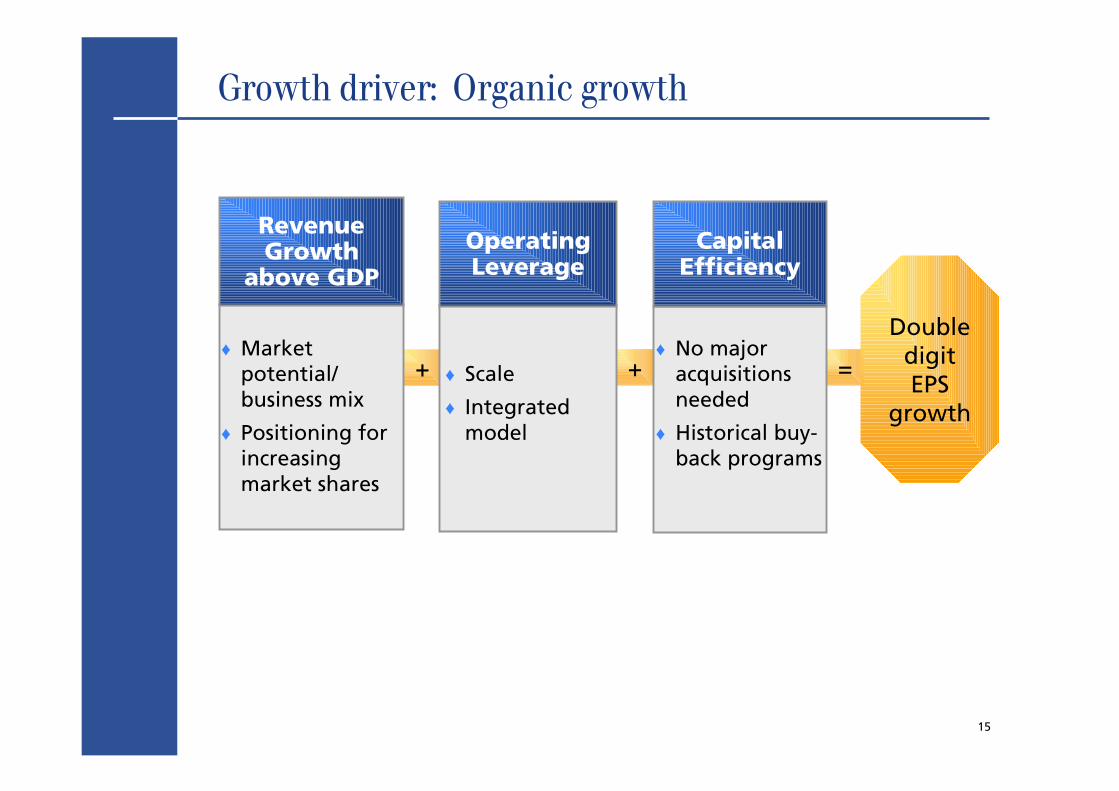

Growth driver: Organic growth

+ + =

RevenueGrowth

above GDP

♦ Marketpotential/business mix

♦ Positioning forincreasingmarket shares

OperatingLeverage

♦ Scale

♦ Integratedmodel

CapitalEfficiency

♦ No majoracquisitionsneeded

♦ Historical buy-back programs

DoubledigitEPS

growth

16

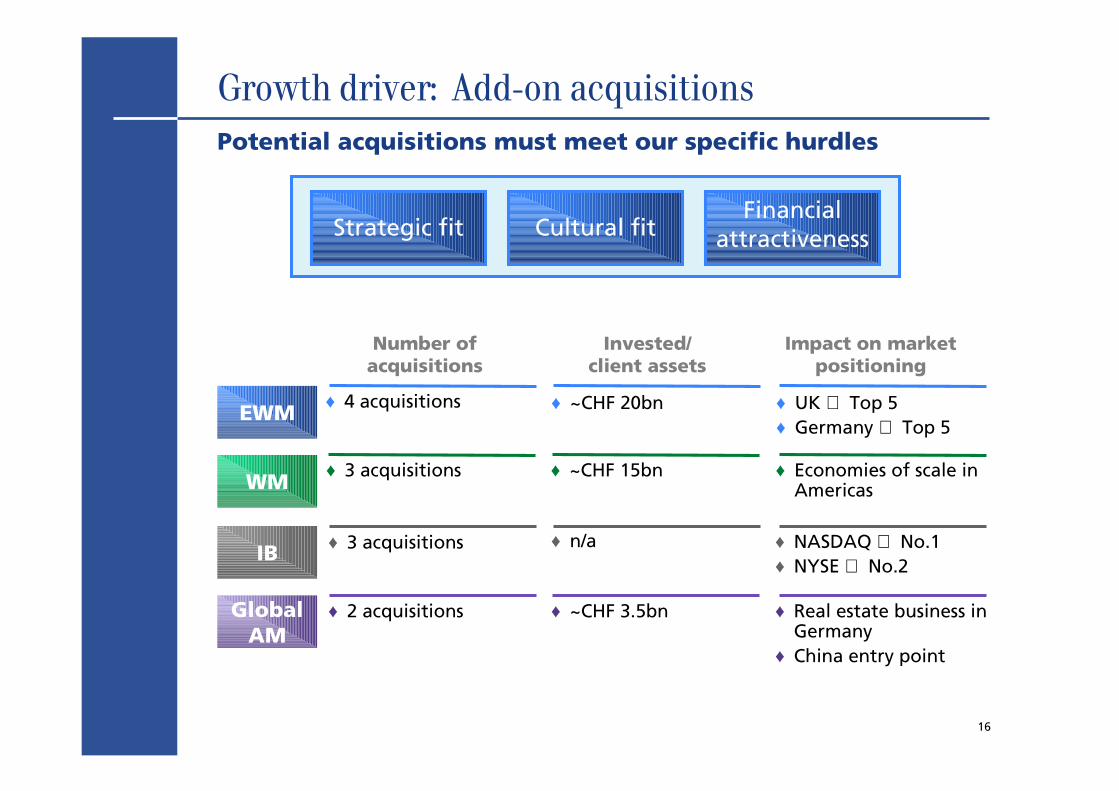

Growth driver: Add-on acquisitionsPotential acquisitions must meet our specific hurdles

♦ UK ⇒ Top 5♦ Germany ⇒ Top 5

Strategic fit Cultural fitFinancial

attractiveness

EWM

WM♦ Economies of scale in

Americas

♦ 4 acquisitions ♦ ~CHF 20bn

♦ ~CHF 15bn♦ 3 acquisitions

IB ♦ NASDAQ ⇒ No.1♦ NYSE ⇒ No.2

♦ n/a♦ 3 acquisitions

Number ofacquisitions

Invested/client assets

Impact on marketpositioning

GlobalAM

♦ Real estate business inGermany

♦ China entry point

♦ ~CHF 3.5bn♦ 2 acquisitions

17

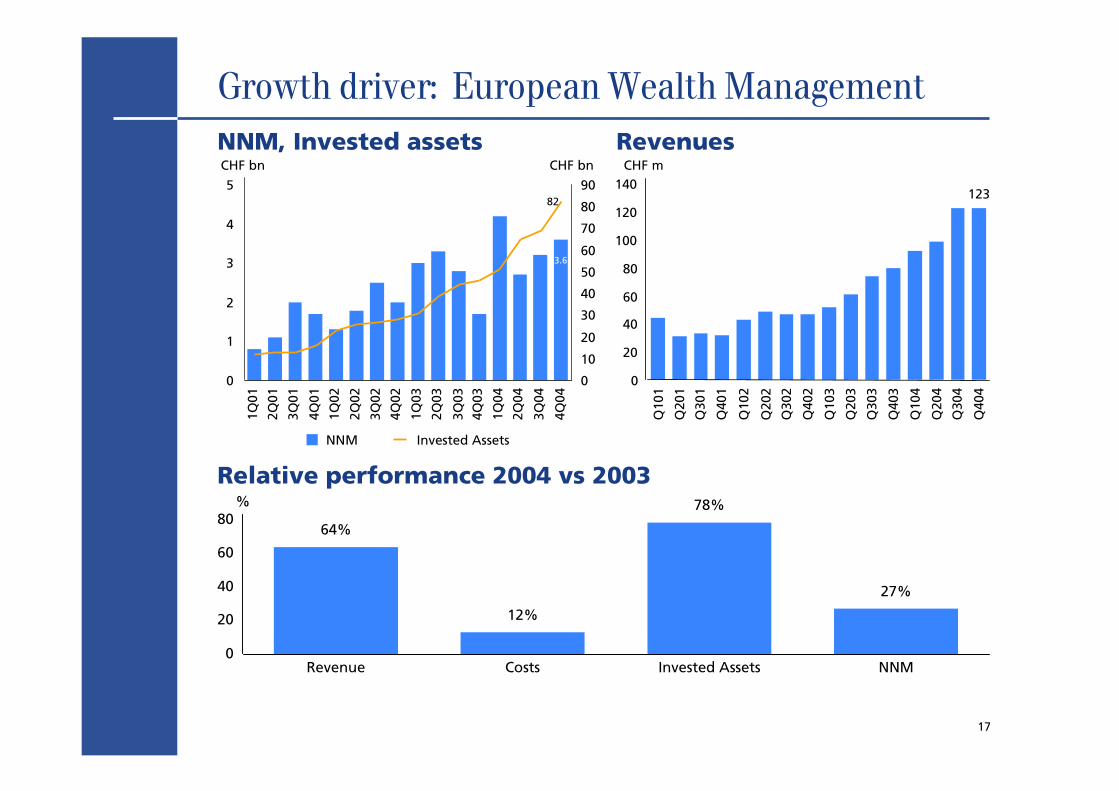

Growth driver: European Wealth ManagementNNM, Invested assets Revenues

Relative performance 2004 vs 2003

NNM Invested Assets

0

1

2

3

4

5

1Q01

2Q01

3Q01

4Q01

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

CHF bn

0

10

20

30

40

50

60

70

80

90

CHF bn

82

3.6

0

20

40

60

80

100

120

140

Q10

1

Q20

1

Q30

1

Q40

1

Q10

2

Q20

2

Q30

2

Q40

2

Q10

3

Q20

3

Q30

3

Q40

3

Q10

4

Q20

4

Q30

4

Q40

4

CHF m

123

64%

12%

78%

27%

0

20

40

60

80

Revenue Costs Invested Assets NNM

%

18

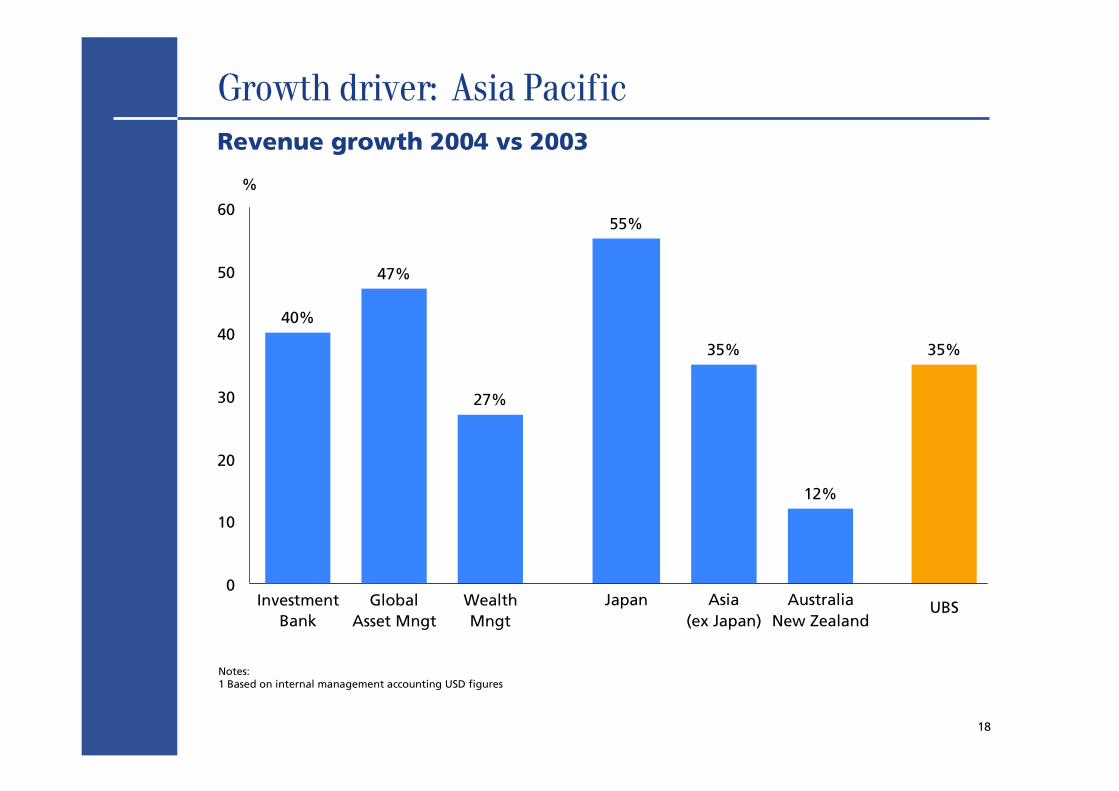

Growth driver: Asia Pacific

Notes:1 Based on internal management accounting USD figures

0

10

20

30

40

50

60

27%

WealthMngt

55%

Japan

12%

AustraliaNew Zealand

35%

UBS

35%

Asia(ex Japan)

40%

InvestmentBank

47%

GlobalAsset Mngt

%

Revenue growth 2004 vs 2003

19

Overall UBS challenges

Additional add-on acquisitions to supplement organicgrowth

Further increase our Asia-Pacific footprint

Group wide emphasis on operational risk

Maintain positive NNM momentum

Continue to build IB client franchise and executionexcellence

Conclusion: Attractive Investment Case

21

UBS investment case

Proven performance across cycles

Focused strategy

High margin businesses

Significant barriers to entry

Strong, integrated culture and brand

Attractive growth opportunities

Strategy & Overview

March 2005

You & Us