Strategy Note India Strategy- Disruption series IV ... THIS REPORT IS DISTRIBUTED IN THE UNITED...

30

India│May 2, 2017 Strategy Note IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH. Powered by the EFA Platform India Strategy- Disruption series IV Proposed APLM + e-NAM: Rise in farm income ■ Proposed Agricultural Produce and Livestock Marketing (APLM) Act and electronic National Agricultural Market (e-NAM) could raise farmers’ income. ■ In the past, such acts were not easily adopted by states but things are different with APLM, as states with 75% agricultural production appear willing to adopt it. ■ e-NAM and APLM could raise farmers’ income, reduce middlemen commissions and lower retail prices of agricultural commodities. ■ Positive for consumer staples, two-wheelers, agrochemicals and users of agri commodities. Britannia, HUVR, Marico and Hero Motocorp are our top picks. Proposed APLM & e-NAM to increase farm income & lower inflation The proposed APLM Act, which most states have agreed to adopt, along with e-NAM could lift farmers’ earnings and reduce the retail prices of food grains. e-NAM has not gone truly national yet as the current act has no provision for a pan-India licence to trade. The APLM will remove tax and market levy inefficiencies, with a single pan-India trading licence for e-NAM, leading to a unified agricultural market in India. Consequently, farmer’s income will go up and retail prices of agri products will come down in our view. APLM necessary for unified national agricultural market e-NAM suffers from serious bottlenecks: 1) absence of a unified national trading licence, 2) multiple taxes in agricultural produce market committee (APMC) markets, and 3) requirement that traders have a stall in an APMC market leads to black marketing of space and higher commission rates. APLM proposes: 1) single unified national licences, 2) first point-of-sale to be located anywhere, removing APMC requirement, 3) setting up Markets of National Importance (MNI), and 4) limiting levies to 5% of selling price Unlike previous APMC laws, APLM has high chance of success Agriculture is a state subject and hence, state governments have the choice not to implement the APLM. However, we believe the APLM will succeed where past acts failed, as: 1) almost 75% of India’s agricultural production is carried out in BJP-ruled or friendly states, 2) there is single point levy for market fees, 3) the commission rates are well defined, with commission and market fees capped at 5%, and 4) it proposes the MNI, interstate markets with a more professional market committee than the APMC. Korean example shows that APLM & e-NAM can be game changers APLM and e-NAM constitute direct marketing of agricultural goods, enabling farmers to take advantage of favourable prices, lower marketing cost and widen net margins. Now, farmers are forced to sell via middlemen in regulated markets and the markets are not equipped with appropriate services and facilities, resulting in marketing inefficiency. In South Korea, direct marketing caused retail prices to fall 20-30% and farmers’ profits to rise 10-20% (Report of Inter-Ministerial Task Force on Agricultural Marketing Reforms). Consumer names and users of agri products stand to benefit Rising farm income would benefit consumption themes. We like makers of small-ticket consumer items like Britannia and HUVR. Manufacturers of two-wheelers also stand to gain, with Hero Motocorp as our top pick. Users of agri commodities like Marico and Britannia would also benefit as their costs may come down. Figure 1: APLM Act has high chance of success as the BJP (the ruling party at centre) controls/ has friendly relations with the states that produce ~75% of India’s agricultural output SOURCES: CIMB, COMPANY REPORTS ▎ India Highlighted companies Hero Motocorp ADD, TP Rs3,708, Rs3,319 close Improvement in retail sales volume mom in and frequent price hikes make Hero Motocorp well placed to handle cost pressures. Given its favourable FY17F P/BV of 5.3x, close to -1 s.d. historical mean, we reiterate our Add rating. Analyst(s) Satish KUMAR T (91) 22 6602 5185 E [email protected] Siddharth GADEKAR T (91) 22 6602 5171 E [email protected] 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% AP Assam Chhattisgarh Gujarat Haryana J&K Jharkhand MP Maharashtra Rajasthan UP Uttarakhand Orissa TN Bihar HP Karnataka Kerala Punjab WB Others Total % Indian agricultural production

Transcript of Strategy Note India Strategy- Disruption series IV ... THIS REPORT IS DISTRIBUTED IN THE UNITED...

India│May 2, 2017

Strategy Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

India Strategy- Disruption series IV Proposed APLM + e-NAM: Rise in farm income ■ Proposed Agricultural Produce and Livestock Marketing (APLM) Act and electronic

National Agricultural Market (e-NAM) could raise farmers’ income.

■ In the past, such acts were not easily adopted by states but things are different with APLM, as states with 75% agricultural production appear willing to adopt it.

■ e-NAM and APLM could raise farmers’ income, reduce middlemen commissions and lower retail prices of agricultural commodities.

■ Positive for consumer staples, two-wheelers, agrochemicals and users of agri commodities. Britannia, HUVR, Marico and Hero Motocorp are our top picks.

Proposed APLM & e-NAM to increase farm income & lower inflation The proposed APLM Act, which most states have agreed to adopt, along with e-NAM could lift farmers’ earnings and reduce the retail prices of food grains. e-NAM has not gone truly national yet as the current act has no provision for a pan-India licence to trade. The APLM will remove tax and market levy inefficiencies, with a single pan-India trading licence for e-NAM, leading to a unified agricultural market in India. Consequently, farmer’s income will go up and retail prices of agri products will come down in our view.

APLM necessary for unified national agricultural market e-NAM suffers from serious bottlenecks: 1) absence of a unified national trading licence, 2) multiple taxes in agricultural produce market committee (APMC) markets, and 3) requirement that traders have a stall in an APMC market leads to black marketing of space and higher commission rates. APLM proposes: 1) single unified national licences, 2) first point-of-sale to be located anywhere, removing APMC requirement, 3) setting up Markets of National Importance (MNI), and 4) limiting levies to 5% of selling price

Unlike previous APMC laws, APLM has high chance of success Agriculture is a state subject and hence, state governments have the choice not to implement the APLM. However, we believe the APLM will succeed where past acts failed, as: 1) almost 75% of India’s agricultural production is carried out in BJP-ruled or friendly states, 2) there is single point levy for market fees, 3) the commission rates are well defined, with commission and market fees capped at 5%, and 4) it proposes the MNI, interstate markets with a more professional market committee than the APMC.

Korean example shows that APLM & e-NAM can be game changers APLM and e-NAM constitute direct marketing of agricultural goods, enabling farmers to take advantage of favourable prices, lower marketing cost and widen net margins. Now, farmers are forced to sell via middlemen in regulated markets and the markets are not equipped with appropriate services and facilities, resulting in marketing inefficiency. In South Korea, direct marketing caused retail prices to fall 20-30% and farmers’ profits to rise 10-20% (Report of Inter-Ministerial Task Force on Agricultural Marketing Reforms).

Consumer names and users of agri products stand to benefit Rising farm income would benefit consumption themes. We like makers of small-ticket consumer items like Britannia and HUVR. Manufacturers of two-wheelers also stand to gain, with Hero Motocorp as our top pick. Users of agri commodities like Marico and Britannia would also benefit as their costs may come down.

Figure 1: APLM Act has high chance of success as the BJP (the ruling party at centre) controls/ has friendly relations with the states that produce ~75% of India’s agricultural output

SOURCES: CIMB, COMPANY REPORTS

Figure 2: [Add Table/Chart Title]

▎ India

Highlighted companies

Hero Motocorp ADD, TP Rs3,708, Rs3,319 close

Improvement in retail sales volume mom in and frequent price hikes make Hero Motocorp well placed to handle cost pressures. Given its favourable FY17F P/BV of 5.3x, close to -1 s.d. historical mean, we reiterate our Add rating.

Analyst(s)

Satish KUMAR

T (91) 22 6602 5185 E [email protected]

Siddharth GADEKAR T (91) 22 6602 5171 E [email protected]

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AP

Assa

m

Ch

hatt

isg

arh

Gu

jara

t

Ha

rya

na

J&

K

Jh

ark

han

d

MP

Ma

hara

sh

tra

Ra

jasth

an

UP

Utt

ara

kh

an

d

Orissa

TN

Bih

ar

HP

Ka

rna

taka

Ke

rala

Pu

nja

b

WB

Oth

ers

To

tal

% I

nd

ian

ag

ricu

ltu

ral

pro

du

cti

on

India│Strategy Note│May 2, 2017

2

KEY CHARTS

Traditional marketing model for agricultural products hampered by many inefficiencies Under the traditional model, farmers must pay high ‘mandi’ (agricultural market) fees, agents’ commission charges and payments may not be made on time. In many cases, farmers earn less than Minimum Support Prices (MSP). By law, bids in the Agricultural Produce Market Committee (APMC) markets cannot be at prices lower than MSP.

e-NAM is a way to promote direct marketing of agricultural products e-NAM is a novel approach that allows farmers to reach the end-consumers directly. The middlemen have no role in this system. To date, ~Rs160bn (mostly intra-state) transactions have taken place on the platform. Given the introduction of nationwide trading licences (as proposed by the APLM Act 2017), we expect a significant rise in e-NAM trades in coming years.

APLM Act has higher chance of success than Model APMC Act of 2003 The Model APMC Act was introduced in 2003 but many states did not implement it. This time around, things are different for the APLM Act, as ~75% of India’s agricultural production is concentrated in BJP-ruled or friendly states. The central government also has an ace up its sleeve in the form of the Markets of National Importance (MNI). MNI will be interstate agricultural markets that will have professional management.

At present APMC market taxes vary widely across states and can be as high as 13% selling price The various taxes for APMC markets, including market levy and commissions, vary widely across states. This is the biggest impediment to a unified national market for agricultural products.

SOURCE: CIMB RESEARCH, COMPANY REPORTS

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

AP

Assam

Ch

hatt

isgarh

Guja

rat

Ha

ryan

a

J&

K

Jhark

han

d

MP

Ma

hara

sh

tra

Ra

jasth

an

UP

Utt

ara

khan

d

Orissa

TN

Bih

ar

HP

Karn

ata

ka

Kera

la

Punja

b

WB

Oth

ers

% o

f A

ll I

nd

ia a

gri

cu

ltu

ral

pro

du

cti

on

Page 2 key charts to be inserted into in your report

No chart title and source statement are needed

0

2

4

6

8

10

12

14

16

Andh

ra P

rad

esh

Assa

m

Bih

ar

Ch

att

isg

arh

Gu

jara

t

Ha

rya

na

Jh

ark

ha

nd

Ka

rna

taka

Ke

rala

Ma

dh

ya

Pra

desh

Ma

ha

rash

tra

NC

T o

f D

elh

i

Orissa

Pu

nja

b

Ra

jasth

an

TN

/ T

ela

ng

an

a

Utta

r P

rad

esh

Utt

rakh

an

d

We

st B

en

ga

l

AP

MC

ta

xe

s in

dif

fere

nt s

tate

s

India│Strategy Note│May 2, 2017

3

APLM Act strives to make taxes uniform across the country The APLM Act aims to rationalise market taxes and make them uniform across the country, making pan-India trade easier.

Even before APLM, volumes and registered farmers were rising on e-NAM platform In the absence of uniform taxes across the country and a single trading licence, the e-NAM mainly operates as an intra-state market. Following the implementation of the APLM Act, we expect to see a significant increase in volumes and farmers’ participation.

e-NAM leading to increase in farmers’ profits In the past 12 months, trading on e-NAM has led to higher average selling prices vis-à-vis Minimum Support Prices (MSP). In our view, the implementation of APLM will increase average selling prices for all agricultural commodities.

e-NAM prices are lower than wholesale prices for most commodities though An efficient market is still some time away (will only emerge after the APLM Act is implemented) but right now, we observe that e-NAM prices are much lower than the wholesale prices of APMC markets. This is good news for bulk users. Limited Indian experience with e-NAM is in line with the Korean case that saw wholesale prices fall by 10-20%, after direct marketing was introduced.

SOURCE: CIMB RESEARCH, COMPANY REPORTS

Page 2 key charts to be inserted into in your report

No chart title and source statement are needed

0%

1%

2%

3%

4%

5%

Perishable goods Non perishable goods

Market levy Commission

Page 2 key charts to be inserted into in your report

No chart title and source statement are needed

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0

20

40

60

80

100

120

140

160

180

Oct-16 Nov-Dec16 Jan- Mar17 Apr-17 Till date

In m

illio

ns

In b

illi

on

s

Turnover in e-NAM ( LHS) Incremnetal Turnover

Registered Farmers ( RHS)

Page 2 key charts to be inserted into in your report

No chart title and source statement are needed

0%

5%

10%

15%

20%

25%

Paddy Wheat Jowar Bajra Maize

E-NAM prices higher than MSP

Page 2 key charts to be inserted into in your report

No chart title and source statement are needed

-20%

-15%

-10%

-5%

0%

5%

10%

Paddy Wheat Jowar Bajra Maize

Difference Between E-NAM & Wholesale Prices

India│Strategy Note│May 2, 2017

`

4

Proposed APLM + e-NAM: Rise in farm income

The Model APLM Act, if implemented by all states, will produce a national agricultural market that is likely to lead to great success for e-NAM. The e-NAM platform is already resulting in above-MSP (minimum support price) average selling prices for farmers. However, e-NAM trade prices are lower than APMC wholesale prices in most cases. The proposed reforms are likely to lead to higher farmer income due to the removal of middlemen and consequently, wholesale prices would come down.

Model APMC Act needs drastic changes

e-NAM is the agricultural e-marketplace established by the government of India to facilitate interstate and inter-APMC market trades of agricultural goods. However, e-NAM suffers from the serious handicaps of different taxes in different state agricultural markets and the lack of single nationwide trading licence. These problems are relics of the old APMC Act that must be changed, in our view. The APMC Act creates market inefficiencies and hence, lowers farmers’ income and causes food inflation.

To date, the buying and selling of agricultural goods in India has been determined by the provisions of the APMC Act

The Model APMC Act 2003 is restrictive to farmers in many ways. In the paragraphs below, we identify the restrictions imposed by the Model APMC Act on farmers.

Contract farming allowed in model Act but impractical due to restrictive laws 1. The Model APMC Act circulated to the states/union territories (UTs) in 2003

allowed for contract farming agreements and model specifications.

2. 20 states amended the APMC Act to make provisions for contract farming but only 12 states notified the rules.

3. Farming contracts require registration with the APMC and payment of market fees and other levies to the APMC although no services are rendered by the committee.

Direct selling of agricultural goods to processing industries, exporters or bulk buyers is restricted by the APMC Act 2003 The APMC Act 2003 prohibits farmers from selling their produce to processors, manufacturers, bulk processors, exporters and bulk retailers outside the market yard and the produce must be channelled through regulated markets.

Shop/stall in APMC market requirement for registration of traders/market functionaries is another restrictive practice At present, only the traders/commission agents who own a shop or godown

(warehouse) in an APMC-regulated market are allowed to purchase produce in the market.

This practice of compulsory licensing of commission agents/traders in the regulated markets has led to these licensed traders creating a monopoly that acts as a major barrier to new entrepreneurs entering the existing APMCs.

India│Strategy Note│May 2, 2017

`

5

Extremely difficult to set up private ‘mandis’ under Model APMC Act 2003 The Model APMC Act 2003 allows the setting up of markets by private players but the provision is not adequate to promote healthy competition with APMCs. The owner of the private market will have to collect the APMC taxes/fees for and on behalf of the APMC, in addition to the fees it wants to charge. This makes private markets practically untenable in most cases. Apart from the above criterion, many state governments put other stringent criteria, such as minimum investment requirement etc.

Single-point levy on agriculture produce absent APMCs charge multiple fees which are of substantial magnitude. This artificially raises the prices of agri commodities without the benefit accruing to the end-consumers. These multiple taxes only fill the coffers of middlemen and create inefficiency in the system.

E-trading not facilitated in the old system E-trading of agri commodities requires certain basic infrastructure and laws which are not facilitated in the model APMC Act 2003. They are:

A unified licence across the states

Clarity on interstate taxation

Single-point levy of market taxes.

Model APMC Act only resulted in heavy taxation & inefficiency in the system

The APMC Act resulted in heavy taxation which inflated the retail prices of agri commodities, with the middlemen gaining at the expense of farmers and end-consumers.

Figure 3: The high rate of APMC taxes and other charges created inefficiency in the system; middlemen gained at the expense of farmers and consumers

SOURCES: CIMB, COMPANY REPORTS

APMC set on premise of not selling below MSP; but many farmers do not even know the concept of MSP

Both the government's annual Economic Survey and the National Sample Survey Office (NSSO) have documented many cases where farmers do not even know about the existence of MSP; this defeats the purpose of APMC markets. Please note that in APMC markets, produce cannot be sold below MSP but if the farmers are unaware of MSP, they can easily be conned by the middlemen.

Title:

Source:

Please fill in the values above to have them entered in your report

0

2

4

6

8

10

12

14

16

An

dh

ra P

rade

sh

Assa

m

Bih

ar

Cha

ttis

ga

rh

Gu

jara

t

Hary

an

a

Jh

ark

ha

nd

Ka

rna

taka

Ke

rala

Ma

dh

ya

Pra

de

sh

Ma

ha

rashtr

a

NC

T o

f D

elh

i

Ori

ssa

Pu

nja

b

Raja

sth

an

TN

/ T

ela

nga

na

Utta

r P

rad

esh

Uttra

kh

an

d

We

st

Ben

gal

AP

MC

ta

xe

s in

d

iffe

ren

t s

tate

s

India│Strategy Note│May 2, 2017

`

6

Figure 4: Some 19% of Indian farmers do not even know about the existence of MSP and hence can be manipulated by middlemen in mandis

SOURCES: CIMB, Indian Economic Survey

Higher APMC wholesale prices only due to tax inefficiency; farmers do not gain

Ostensibly, wholesale prices are much higher than MSP. However, if we adjust for APMC taxes etc., then wholesale prices of commodities are only marginally ahead of MSP. This again proves that to a large extent, farmers are not gaining from the high food prices. Only middlemen are gaining, instead of Indian consumers and farmers.

Figure 5: Adjusted for taxes & commissions at APMC markets, wheat wholesale prices are only 4.5% higher than MSP

Figure 6: Against headline number of 10%, adjusted for APMC charge, paddy wholesale price is higher by only 5.5% over MSP

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

AP

Bih

ar

Guja

rat

Ka

rna

taka

MP

Ma

hara

sh

tra

Od

ish

a

Punja

b

Ra

jasth

an

UP

Utt

ara

kh

an

d

0%

20%

40%

60%

80%

100%

%

Po

pu

lati

on

un

aw

are

ab

ou

t M

SP

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Whole sale prices higher thanMSP

Adjusted for APMC taxeswholesale prices higher than MSP

Wh

eat

pri

ces %

hig

her

than

MS

P

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Whole sale prices higher thanMSP

Adjusted for APMC taxeswholesale prices higher than

MSP

Pad

dy p

rices %

hig

her

than

MS

P

India│Strategy Note│May 2, 2017

`

7

APMC Act 2.0 or APML - The game-changing law

The Indian central government has proposed a new model APMC Act called Agricultural Produce and Livestock Marketing Act (APLM) and is discussing the proposed legislation with the state governments. If the contours of the implemented law remain broadly in line with what has been proposed, it can change the way agricultural produce are being sold in India. Middlemen will be removed from most of the marketplaces and farmers’ income will likely rise.

New model APMC Act dubbed APLM

The central government has discussed the proposed Agricultural Produce and Livestock Marketing (APLM) Act 2017 with the chief ministers of several states on 25 April and many of them have agreed to adopt the proposed law.

APLM strives to change the way agricultural products are sold

Abolish market fragmentation within the states/UTs by removing the concept of notified market areas in so far as enforcement of APMC regulations is concerned (state-level single market).

Create a conducive environment for the setting up and operation of private wholesale market yards and farmer-consumer market yards so as to enhance the competition for the farmer's produce, to the advantage of the farmer.

Create a direct market for bulk-buyers/end-users in order to reduce the price spread, which would be advantageous for both the producers and consumers.

Enable warehouses/silos/cold storages and other structures/spaces to be declared as market sub-yards to provide better access/linkages to the farmers.

Give agriculturalists the freedom to sell their produce to whomever they want at the place and time of their choice, to get better prices.

Promotion of e-trading to enhance transparency in trade operations and integration of markets across geographies.

Provisions for single-point levy of market fees across the state and a unified single trading licence to realise cost-effective transactions.

Promotion of a national market for agricultural produce through interstate trading licence grading and standardisation, and quality certification.

Rationalisation of market fees and commission charges.

Provision for Special Commodity Market yards and Market yards of National Importance (MNI).

Licensees of private market yards, market sub-yards, electronic trading and direct marketing will have a level playing field with APMC market yards.

If implemented as per the draft bill, it will limit the market fee and commission charges

Currently, market fee and commission charges differ across the different states. The Bill proposes to limit the overcharges on non-perishables goods at 4% and perishable goods at 5% of selling prices

Proposed Act will curtail the power of APMCs; they will no longer have any monopoly powers

The government's aim is to set up a wholesale market every 80 km. The proposed law will end the monopoly of APMCs and allow more players to set up markets and create competition so that farmers have a wider choice on where they can sell their produce.

India│Strategy Note│May 2, 2017

`

8

The APMC markets will be one type of market. APMC will no longer have monopoly powers. The law promotes multiple market channels like private market yards and direct marketing; even godowns and silos can be declared as markets.

Even an individual keen to buy agri-produce in bulk for a big event like marriage can take up a licence and buy the produce, but not more than three times in six months.

Multiple avenues to sell products will ensure better realisation for farmers

Currently, there is a regularised market every 462 sq km, but the National Commission recommends that ideally, a regulated market should be available to farmers every 5 km radius.

To achieve this, and to provide farmers markets at their farm gates, APLM has a provision to allow godowns and cold storages to be declared as markets.

If the state governments would implement APLM diligently, farmers will be empowered to decide who to sell to and at what price.

One of the important points of this legislation is that the farmers would get the price of their yields based on the quality of their produce. This is because the quality of their goods will be tested before electronic bidding commences on e-NAM.

Declaring a warehouse/godown as a market is an effort to bring markets closer to the farmers and facilitate them with pledge loans. Emphasis is being given by the government to the investment in the agriculture sector.

Market of national importance (MNI) another game-changing proposition

The government may, by notification, declare any market yard as Market of National Importance (MNI) after consideration of such aspects as total throughput, value, upstream catchment area, downstream number of consumers served and special infrastructure requirements.

These MNI will be completely controlled by the state government but have a more professional set-up than the traditional APMC market.

MNI is likely to be more efficient and transaction costs are likely to be lower than APMC.

Interstate trading licences another innovative provision

A single licence nationwide for interstate trade will be issued for traders to operate on the e-platform. With a single, pan-India licence, a trader would be allowed to operate in APMC markets, principal market yards, submarket yards, private market yards or any 'place' identified for the purpose in the country.

Absence of interstate trading licence one of the key impediments in wide adoption of e-market The absence of interstate trading licences was one of the main impediments to the development of a national agricultural market. In the first 12 months of operations, the value of goods traded on the electronic national agricultural market (e-NAM) platform rose to 3% of the overall agricultural goods market. However, this volume was mostly intra-state. We expect volumes to increase significantly when interstate transactions start.

India│Strategy Note│May 2, 2017

`

9

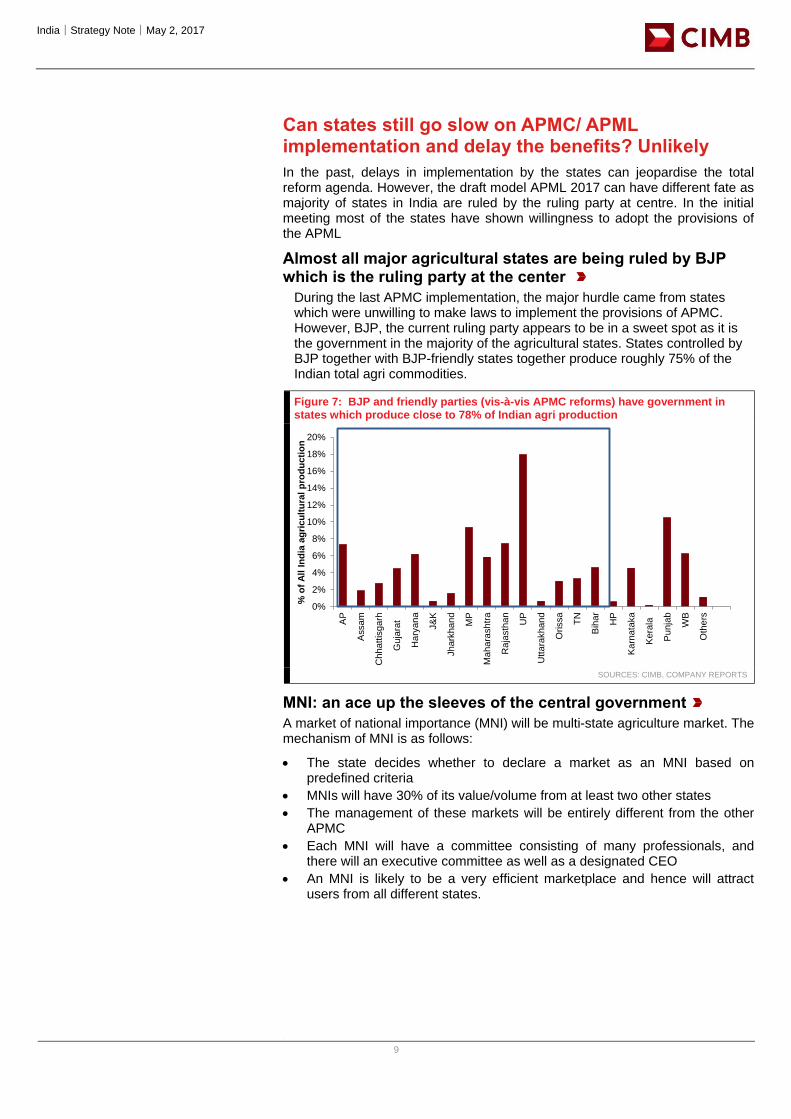

Can states still go slow on APMC/ APML implementation and delay the benefits? Unlikely

In the past, delays in implementation by the states can jeopardise the total reform agenda. However, the draft model APML 2017 can have different fate as majority of states in India are ruled by the ruling party at centre. In the initial meeting most of the states have shown willingness to adopt the provisions of the APML

Almost all major agricultural states are being ruled by BJP which is the ruling party at the center

During the last APMC implementation, the major hurdle came from states which were unwilling to make laws to implement the provisions of APMC. However, BJP, the current ruling party appears to be in a sweet spot as it is the government in the majority of the agricultural states. States controlled by BJP together with BJP-friendly states together produce roughly 75% of the Indian total agri commodities.

Figure 7: BJP and friendly parties (vis-à-vis APMC reforms) have government in states which produce close to 78% of Indian agri production

SOURCES: CIMB, COMPANY REPORTS

MNI: an ace up the sleeves of the central government

A market of national importance (MNI) will be multi-state agriculture market. The mechanism of MNI is as follows:

The state decides whether to declare a market as an MNI based on predefined criteria

MNIs will have 30% of its value/volume from at least two other states

The management of these markets will be entirely different from the other APMC

Each MNI will have a committee consisting of many professionals, and there will an executive committee as well as a designated CEO

An MNI is likely to be a very efficient marketplace and hence will attract users from all different states.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

AP

Assa

m

Ch

hatt

isg

arh

Gu

jara

t

Ha

rya

na

J&

K

Jh

ark

han

d

MP

Ma

hara

sh

tra

Ra

jasth

an

UP

Utt

ara

kh

an

d

Orissa

TN

Bih

ar

HP

Ka

rna

taka

Kera

la

Pu

nja

b

WB

Oth

ers

% o

f A

ll I

nd

ia a

gri

cu

ltu

ral

pro

du

cti

on

India│Strategy Note│May 2, 2017

`

10

e-NAM can flourish only in APML environement and is a big game changer

The success of the electronic national agricultural market (e-NAM) is dependent on the successful implementation of APML. With many states already agreeing on the implementation APML and provision of unified national trading licenses, e-NAM is likely to be a success, in our view.

What is the traditional selling model for farmers?

Figure 8: As per old APMC rules, farmers can sell their products only in APMC markets through the process depicted below

SOURCES: CIMB, COMPANY REPORTS

However, it was a lose- lose proposition for farmers

India│Strategy Note│May 2, 2017

`

11

Figure 9: The traditional marketing channel had become a lose-lose proposition for farmers due to low realisations, high commissions, long gestation period, wastage etc.

SOURCES: CIMB, COMPANY REPORTS

What is e-NAM on the selling of farm goods?

Figure 10: e-NAM is an online trading platform designed to benefit the farmers, but is bad news for middlemen

SOURCES: CIMB, COMPANY REPORTS

India│Strategy Note│May 2, 2017

`

12

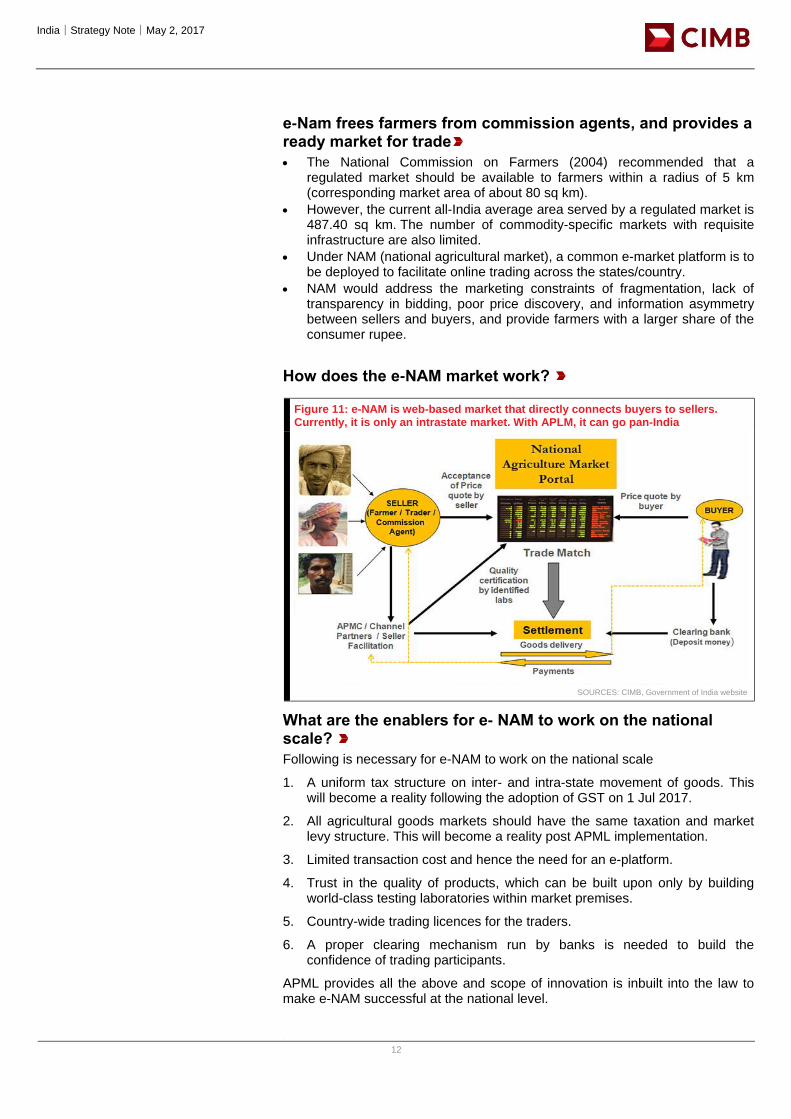

e-Nam frees farmers from commission agents, and provides a ready market for trade

The National Commission on Farmers (2004) recommended that a regulated market should be available to farmers within a radius of 5 km (corresponding market area of about 80 sq km).

However, the current all-India average area served by a regulated market is 487.40 sq km. The number of commodity-specific markets with requisite infrastructure are also limited.

Under NAM (national agricultural market), a common e-market platform is to be deployed to facilitate online trading across the states/country.

NAM would address the marketing constraints of fragmentation, lack of transparency in bidding, poor price discovery, and information asymmetry between sellers and buyers, and provide farmers with a larger share of the consumer rupee.

How does the e-NAM market work?

Figure 11: e-NAM is web-based market that directly connects buyers to sellers. Currently, it is only an intrastate market. With APLM, it can go pan-India

SOURCES: CIMB, Government of India website

What are the enablers for e- NAM to work on the national scale?

Following is necessary for e-NAM to work on the national scale

1. A uniform tax structure on inter- and intra-state movement of goods. This will become a reality following the adoption of GST on 1 Jul 2017.

2. All agricultural goods markets should have the same taxation and market levy structure. This will become a reality post APML implementation.

3. Limited transaction cost and hence the need for an e-platform.

4. Trust in the quality of products, which can be built upon only by building world-class testing laboratories within market premises.

5. Country-wide trading licences for the traders.

6. A proper clearing mechanism run by banks is needed to build the confidence of trading participants.

APML provides all the above and scope of innovation is inbuilt into the law to make e-NAM successful at the national level.

India│Strategy Note│May 2, 2017

`

13

e-NAM implementation successful to date

e-NAM was launched in Apr 2016 with the aim of integrating ~250 markets by the end of Mar 2017. However, by the end of that period, it had integrated close to 400 markets. The target is to integrate a total of 585 APMC markets by 2018. Going by its pace of progress, this can be achieved much earlier, in our view.

In past 12 months, transaction volumes have been close to Rs160bn which is ~3% of overall market

In the first 12 months of e-NAM's existence, the overall volume on the platform has reached Rs160bn, which is ~3% of overall agricultural market. Please note that most of these are intrastate volumes as the unified single trading licence is still not available. As the unified single licence become available (as per the new APLM law), then e-NAM volumes will jump.

Till date ~450 mandis have been integrated on e- NAM

Figure 12: The best part is that states like WB which were initially reluctant to take part in e-NAM are coming forward

SOURCES: CIMB, COMPANY REPORTS

e-NAM has been mostly an intrastate market; a unified national licence will change things

To date, e-NAM has mostly been an intrastate market. Few states have taken the lead in this market. For the rest, e-NAM has mostly been a nonstarter. We believe e-NAM will only truly develop when single licences are issues for trading nationwide. Following the implementation of GST, interstate transportation of goods will no longer be an issue anyway.

State

Proposal Received From

States to Integrate Mandis

with E-NAM

Total No of Mandis

Integrated with E-Nam

Mandis Yet To Be

Integrated

Andhra Pradesh 22 22 0

Chandigarh 1 0 1

Chattisgarh 14 14 0

Gujrat 90 40 50

Haryana 54 54 0

Himachal Pradesh 41 17 24

Jharkhand 19 19 0

Madhya Pradesh 58 58 0

Maharashtra 60 44 16

Odisha 10 9 1

Rajasthan 25 25 0

Telengana 60 44 16

Uttar Pradesh 100 66 34

Uttarakhand 5 5 0

West Bengal 17 0 17

TamilNadu 100 0 100

Total 676 417 259

India│Strategy Note│May 2, 2017

`

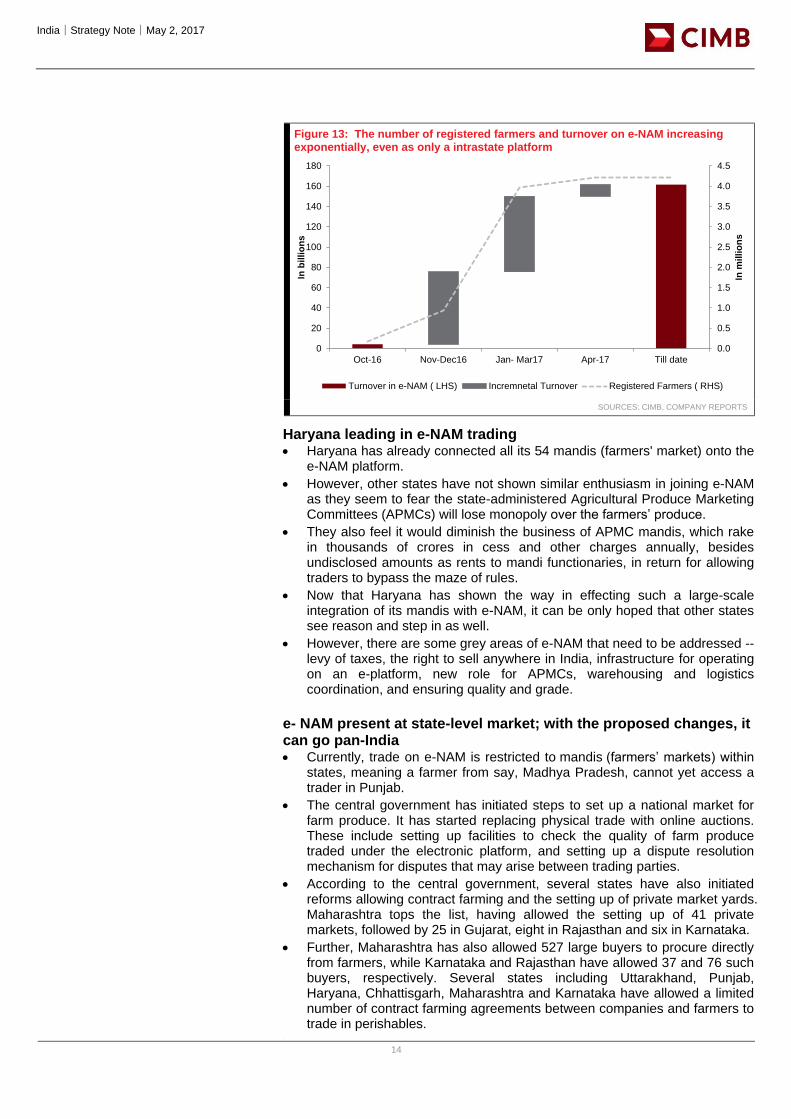

14

Figure 13: The number of registered farmers and turnover on e-NAM increasing exponentially, even as only a intrastate platform

SOURCES: CIMB, COMPANY REPORTS

Haryana leading in e-NAM trading Haryana has already connected all its 54 mandis (farmers' market) onto the

e-NAM platform.

However, other states have not shown similar enthusiasm in joining e-NAM as they seem to fear the state-administered Agricultural Produce Marketing Committees (APMCs) will lose monopoly over the farmers’ produce.

They also feel it would diminish the business of APMC mandis, which rake in thousands of crores in cess and other charges annually, besides undisclosed amounts as rents to mandi functionaries, in return for allowing traders to bypass the maze of rules.

Now that Haryana has shown the way in effecting such a large-scale integration of its mandis with e-NAM, it can be only hoped that other states see reason and step in as well.

However, there are some grey areas of e-NAM that need to be addressed -- levy of taxes, the right to sell anywhere in India, infrastructure for operating on an e-platform, new role for APMCs, warehousing and logistics coordination, and ensuring quality and grade.

e- NAM present at state-level market; with the proposed changes, it can go pan-India Currently, trade on e-NAM is restricted to mandis (farmers’ markets) within

states, meaning a farmer from say, Madhya Pradesh, cannot yet access a trader in Punjab.

The central government has initiated steps to set up a national market for farm produce. It has started replacing physical trade with online auctions. These include setting up facilities to check the quality of farm produce traded under the electronic platform, and setting up a dispute resolution mechanism for disputes that may arise between trading parties.

According to the central government, several states have also initiated reforms allowing contract farming and the setting up of private market yards. Maharashtra tops the list, having allowed the setting up of 41 private markets, followed by 25 in Gujarat, eight in Rajasthan and six in Karnataka.

Further, Maharashtra has also allowed 527 large buyers to procure directly from farmers, while Karnataka and Rajasthan have allowed 37 and 76 such buyers, respectively. Several states including Uttarakhand, Punjab, Haryana, Chhattisgarh, Maharashtra and Karnataka have allowed a limited number of contract farming agreements between companies and farmers to trade in perishables.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0

20

40

60

80

100

120

140

160

180

Oct-16 Nov-Dec16 Jan- Mar17 Apr-17 Till date

In m

illio

ns

In b

illio

ns

Turnover in e-NAM ( LHS) Incremnetal Turnover Registered Farmers ( RHS)

India│Strategy Note│May 2, 2017

`

15

Farmers' have gained realisations higher than wholesale prices Farmers can gain in multiple ways from e-NAM. Higher realisations and ease of selling are direct outcomes. The complete elimination of commission fee is another big gain. As we have pointed out earlier, commission and market levy varies from 0% to 13.5% across states, and these are effectively borne by the farmers.

Figure 14: The realised price for many commodities on e-NAM much higher than MSP for farmers

SOURCES: CIMB, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Pad

dy

Wh

eat

Jo

war

Bajr

a

Ma

ize

Tu

r (A

rhar)

Mo

on

g

Ura

d

Soya

be

an

Co

tto

n

Barl

ey

Gra

m

e-Nam prices higher than MSP

India│Strategy Note│May 2, 2017

`

16

Farmers' income to rise because of new APMC law and e-NAM

The farmer’s income is set to rise because of the unified agricultural market and removal of commission agents. APMC provided a trade settlement security which can be taken over by a clearing house on the e-NAM platform. Revision of the APMC is necessary for a successful implementation of e-NAM and if the APLM is passed, this will be a big shot in the arm to the farmers' income in India.

As per old practice, Indian famers heavily dependent on middlemen

As per the old APMC Act, the first point of sales has to be in an APMC market. Famers have to pay multiple charges for selling in an APMC market which includes market levy, commission, usage fee, lab free, storage charges etc. Overall, farmers lose at least 7-8% sales realisation to middlemen and the APMC market.

Old APMC markets have become a bastion of corruption and political inference

As per the old APMC Act, if the sales happen in private market, certain fees still have to be paid to the concerned APMC.

Only those with office/godowns in an APMC market can work as a commission agent in that market. With limited space in the APMC market, this has led to exorbitant prices for the offices/ godowns.

While traders claim that they work for the benefit of farmers, in many cases, they charge arbitrary commission rates. Money is also not paid on time; sometimes it takes months before sale proceeds reach the farmers.

The election of market committee becomes a totally political process and in many cases, the legitimate voice of the farmers remains unheard.

e-NAM, even when just on an intrastate level, has removed much inefficiency in the market

On e-Nam, farmers are not dependent on commission agents or traders to sell their products

All APMC markets with e-trading facilities will have certified testing laboratories that can be used by farmers for a nominal fee.

A bank-backed clearing mechanism provides comfort to the seller, and proceeds from transactions are also dispensed pretty quickly.

Post GST and APLM, things will be even better for farmers

The farmer's selling zone will not be limited to a single state

All APMC markets that provide e-trading facilities will have certified testing labs that can be used by formers for a nominal fee

A bank-backed clearing mechanism provides comfort to the seller and proceeds from transactions would also be dispensed quickly.

If the APLM is implemented, the resulting national market would enable better price discovery as buyers and sellers will have a wide range of offerings to choose from.

GST implementation will lead to the removal of many procedural issues in the transport of agri products

Most importantly, a unified trading licence will help buyer’s source products from anywhere in India, resulting in a much more efficient market.

As middlemen commissions are eliminated, e-NAM prices are lower than APMC wholesale prices

In e-NAM, middlemen commissions are miniscule; this brings down wholesale prices on the platform. Please note that current e-NAM prices are below APMC

India│Strategy Note│May 2, 2017

`

17

wholesale prices. Falling wholesale prices are a win-win for all, end-consumers, industries users etc.

Figure 15: In many cases, e-NAM prices (though still inefficient) is way below APMC wholesale prices

SOURCES: CIMB, COMPANY REPORTS

Exact gain for farmers difficult to estimate; evidence suggest substantial gain

Due to the number of variables, we are unable to estimate the extent of increase in farmer income arising from the nationwide adoption of APLM and e-NAM. However, it is apparent that their income will rise over MSP. Eliminating the middlemen will also lower wholesale prices as well, benefiting the industries.

-20%

-15%

-10%

-5%

0%

5%

10%

Paddy Wheat Jowar Bajra Maize

Difference Between E-NAM & Wholesale Prices

India│Strategy Note│May 2, 2017

`

18

Consumption themes, agrochemicals to benefit from the rise in farm income

e-NAM is already showing falling wholesale prices and rising farmer realisation. Both of these are drivers of increased consumer spending and hence corporate earnings

Most corporate agri product users have high raw material costs, which could decline post APLM and e-NAM

Figure 16: Most of the consumer companies that use agri products as input can see a margin expansion as wholesale prices are slated to fall in the coming years

SOURCES: CIMB, COMPANY REPORTS

Rising farm income another positive for consumer products companies

Companies that have a wider reach (in terms of distribution network) and lower Rs/SKU (stock-keeping unit) are likely to gain the most in the coming years. Two-wheelers are both aspirational products and necessities for most villagers and hence, are likely to see an increase in sales. We do not cover any consumer staples companies but from a strategy perspective, we like Britannia (Not Rated) , HUVR(Not Rated) and Marico (Not Rated)

Among consumer names, Britannia remains our top pick

We like Britannia as its SKU sizes are smaller, it has a wide reach (~3.6m outlets) and uses agri products as input and we expect these prices to come down over medium term

Title:

Source:

Please fill in the values above to have them entered in your report

30%

35%

40%

45%

50%

55%

60%

65%

70%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Ra

w m

ate

ria

l c

os

t a

s %

of

sa

les

Britannia Industries Ltd. Hindustan Unilever Ltd. ITC Ltd. Marico Ltd.

India│Strategy Note│May 2, 2017

`

19

Figure 17: Biscuits form almost 90% of the Britannia's sales; we expect biscuit consumption to go up as farm income rises

Figure 18: Most importantly, the price range of Britannia products makes them easily purchasable once income rises

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Valuations are high but high ROE, ROIC, likelihood of growth and high incremental ROIC is a heady mixture for valuations Britannia is currently trading at extremely high valuations. However, given the likelihood of margin expansion and hence even higher return ratios and earnings growth, it can sustain these heady valuation levels, in our view.

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY15 FY16

Biscuits Bread etc Cake Others Britannia SKU (gm) Price (Rs) Rs/Kg

Bourbon 60 10 167

Bourbon 150 26 173

Little Heatrs 39 10 256

Jim Jam 100 15 150

NutriChoice - Simply Lite 100 15 150

NutriChoice - High Fibre 100 20 200

NutriChoice - Heavens 100 40 400

Good Day 200 30 150

Good Day 120 20 167

Good Day 75 10 133

Nice Time 150 22 147

Nice Time - Sugar Showered 73 10 137

Marie Gold 89 10 112

Marie Gold - Vita 75 10 133

50:50 33 5 152

50:50 - Maska Chaska 120 25 208

Milk Bikis 100 20 200

Tiger - Krunch Choco Chips 70 10 143

Tiger - Krunch Butter 45 5 111

Tiger - Glucose 66 5 76

Tiger - Cream - Chocolate 50 5 100

Pure magic 100 20 200

Pure magic - Chocolush 75 30 400

Treat 64 10 156

India│Strategy Note│May 2, 2017

`

20

Figure 19: Britannia has stellar return ratios Figure 20: Britannia has shown 33% EPS CAGR in the past 7 years, and ~10% yoy EPS growth in 9MFY17

SOURCES: COMPANY REPORTS SOURCES: COMPANY REPORTS

Figure 21: Britannia's P/E chart- Luxurious valuation (based on current year earnings) is a common theme across all the consumer names in India and Britannia is no exception.

SOURCES: Bloomberg, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

FY11 FY12 FY13 FY14 FY15 FY16

RoE RoIC RoCE

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

10

20

30

40

50

60

70

80

FY11 FY12 FY13 FY14 FY15 FY16

EPS( LHS) growth in EPS (RHS)

Title:

Source:

Please fill in the values above to have them entered in your report

-5

5

15

25

35

45

55

65

Apr-

09

Au

g-0

9

De

c-0

9

Apr-

10

Au

g-1

0

De

c-1

0

Apr-

11

Au

g-1

1

De

c-1

1

Apr-

12

Au

g-1

2

De

c-1

2

Apr-

13

Au

g-1

3

De

c-1

3

Apr-

14

Au

g-1

4

De

c-1

4

Apr-

15

Au

g-1

5

De

c-1

5

Apr-

16

Au

g-1

6

De

c-1

6

Apr-

17

PE Average +1 stdev -1 stdev +2 Stdev -2 Stdev

India│Strategy Note│May 2, 2017

`

21

Hindustan Unilever (Not Rated) is one of the most attractive plays on rising rural income and fall in input costs

Figure 22: We expect HUVR's overall sales to rise with rising income. Meanwhile, food and refreshment margins could increase with falling commodity prices

Figure 23: HUVR has the largest distribution network and hence is in perfect position to capture any rise in farm income

SOURCES: COMPANY REPORTS SOURCES: COMPANY REPORTS

Figure 24: Like Britannia, HUVR's valuation (on current year Bloomberg earnings) is very high. However given likely increased spending tailwinds, wide reach and product range, a de-rating is unlikely

SOURCES: Bloomberg, COMPANY REPORTS

Marico (Not Rated) could be positively impacted by falling wholesale APMC prices

One of Marico’s key raw materials is Copra. Corpa is not currently in the approved commodities list but we believe that once APLM comes into force, this critical commodity is likey to be a part of the list. As witnessed in other commodities, the integration of markets removes inefficiencies and lowers the prices for producers.

Title:

Source:

Please fill in the values above to have them entered in your report

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Q1 FY16 Q2 FY16 Q3 FY16 Q4 FY16 Q1 FY17 Q2 FY17 Q3 FY17

Home Care Personal Care Foods Refreshments Others 0

2

4

6

8

10

12

Britannia Parle HUVR

Dis

trib

uti

on

po

int

in m

illio

ns

Title:

Source:

Please fill in the values above to have them entered in your report

20

25

30

35

40

45

50

55

60

Ap

r-1

0

Ju

l-1

0

Oct-

10

Jan-1

1

Ap

r-1

1

Ju

l-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-12

Oct-

12

Ja

n-1

3

Apr-

13

Jul-13

Oct-

13

Ja

n-1

4

Apr-

14

Jul-14

Oct-

14

Ja

n-1

5

Ap

r-1

5

Ju

l-1

5

Oct-

15

Ja

n-1

6

Ap

r-1

6

Ju

l-1

6

Oct-

16

Ja

n-1

7

Ap

r-1

7

HUVR PE Average +1 stdev -1 stdev +2 Stdev -2 Stdev

India│Strategy Note│May 2, 2017

`

22

Figure 25: Marco's P/E chart. Based on Bloomberg numbers, Marco is working out to be costliest among our top three picks. However, we believe given the raw materail fall tailwinds, a significant and sustained unerperformance is unlikely

SOURCES: CIMB, COMPANY REPORTS

Agrochemicals companies to gain from the rise in farm income

We do not cover agrochemicals or consumer staple companies. However, from a strategic perspective, we like PI Industries (Not Rated), Rallis (Not Rated), Insecticide India (Not Rated), HUVR(Not Rated) and Britannia(Not Rated). We believe that hybrid seed companies are also likely to do well.

Indian agrochemical companies in a sweet spot With rising farmers’ income, Indian agrochemical companies will be in a sweet spot. Indian agrochemical consumption is one of the lowest in the world. Hence, it can only go higher with the expected rise in farmers’ income, in our view. We like PI Industries, Rallis India and Insecticide India in this space.

Figure 26: Agrochemical usage in India one of the lowest in the world

Figure 27: Rising rural wage (courtesy of MGNREGA) likely to drive the usage of herbicides in India

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

PI Industries: Multiple revenue sources; valuation not cheap, but then never cheap to begin with PI Industries has two business segments: contract synthesis and manufacturing (CRAMS) and agrochemicals. CRAMS now contributes about 60% of its overall

15

20

25

30

35

40

45

50

55

60

65

Apr-

09

Au

g-0

9

De

c-0

9

Apr-

10

Au

g-1

0

De

c-1

0

Apr-

11

Au

g-1

1

De

c-1

1

Apr-

12

Au

g-1

2

De

c-1

2

Apr-

13

Au

g-1

3

De

c-1

3

Apr-

14

Au

g-1

4

De

c-1

4

Apr-

15

Au

g-1

5

De

c-1

5

Apr-

16

Au

g-1

6

De

c-1

6

Apr-

17

Marico PE Average +1 stdev -1 stdev +2 Stdev -2 Stdev

Title:

Source:

Please fill in the values above to have them entered in your report

0

2

4

6

8

10

12

14

16

18

20

India US Korea China Japan

Kg

/He

cta

re

Title:

Source:

Please fill in the values above to have them entered in your report

65%

16%

15%

4%

Insecticides Herbicides Fungicides Others

India│Strategy Note│May 2, 2017

`

23

sales (FY16). The company is focused on R&D. In the past five years, it has consistently introduced two or more new products/molecules per year in its CRAMS and agrochemicals businesses.

Figure 28: PI Industries: high revenue visibility leads to premium valuation which we find sustainable given its large CRAMS order book and domestic growth potential

SOURCES: Bloomberg

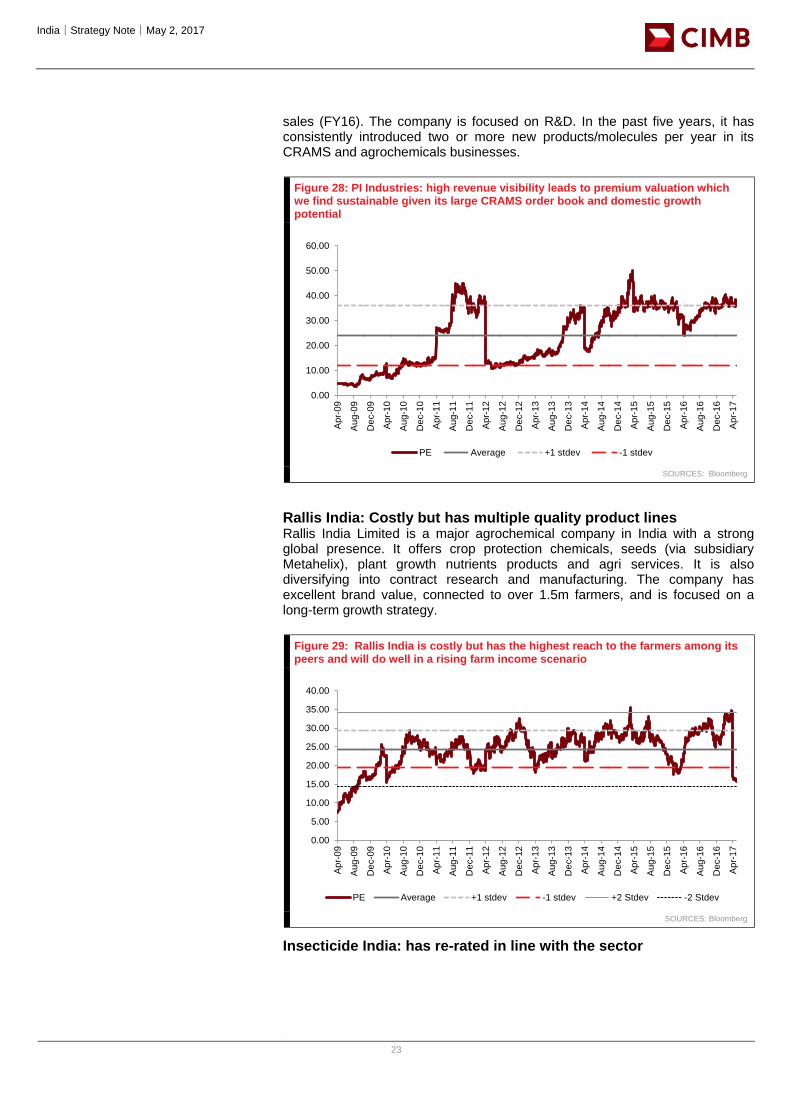

Rallis India: Costly but has multiple quality product lines Rallis India Limited is a major agrochemical company in India with a strong global presence. It offers crop protection chemicals, seeds (via subsidiary Metahelix), plant growth nutrients products and agri services. It is also diversifying into contract research and manufacturing. The company has excellent brand value, connected to over 1.5m farmers, and is focused on a long-term growth strategy.

Figure 29: Rallis India is costly but has the highest reach to the farmers among its peers and will do well in a rising farm income scenario

SOURCES: Bloomberg

Insecticide India: has re-rated in line with the sector

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Ap

r-0

9

Au

g-0

9

De

c-0

9

Ap

r-1

0

Au

g-1

0

De

c-1

0

Ap

r-1

1

Aug-1

1

De

c-1

1

Ap

r-1

2

Au

g-1

2

De

c-1

2

Ap

r-1

3

Au

g-1

3

De

c-1

3

Ap

r-1

4

Au

g-1

4

De

c-1

4

Ap

r-1

5

Au

g-1

5

De

c-1

5

Ap

r-1

6

Au

g-1

6

De

c-1

6

Ap

r-1

7

PE Average +1 stdev -1 stdev

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

Ap

r-0

9

Au

g-0

9

De

c-0

9

Ap

r-1

0

Au

g-1

0

De

c-1

0

Ap

r-1

1

Aug-1

1

De

c-1

1

Ap

r-1

2

Au

g-1

2

De

c-1

2

Ap

r-1

3

Au

g-1

3

De

c-1

3

Ap

r-1

4

Au

g-1

4

De

c-1

4

Ap

r-1

5

Au

g-1

5

De

c-1

5

Ap

r-1

6

Au

g-1

6

De

c-1

6

Ap

r-1

7

PE Average +1 stdev -1 stdev +2 Stdev -2 Stdev

India│Strategy Note│May 2, 2017

`

24

Figure 30: Insecticide India is a domestic player with no CRAMS presence currently. It is likely to grow in line with the sector.

SOURCES: COMPANY REPORTS

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oct-

11

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oct-

12

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oct-

13

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oct-

14

Ja

n-1

5

Ap

r-1

5

Ju

l-1

5

Oct-

15

Ja

n-1

6

Ap

r-1

6

Ju

l-1

6

Oct-

16

Ja

n-1

7

Insecticide India PE Average +1 stdev

-1 stdev +2 Stdev -2 Stdev

India│Strategy Note│May 2, 2017

25

DISCLAIMER #03

The content of this report (including the views and opinions expressed therein, and the information comprised therein) has been prepared by and belongs to CIMB and is distributed by CIMB.

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the “Restrictions on Distributions” set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CIMB may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. CIMB is under no obligation to update this report in the event of a material change to the information contained in this report. CIMB has no, and will not accept any, obligation to (i) check or ensure that the contents of this report remain current, reliable or relevant, (ii) ensure that the content of this report constitutes all the information a prospective investor may require, (iii) ensure the adequacy, accuracy, completeness, reliability or fairness of any views, opinions and information, and accordingly, CIMB, or any of their respective affiliates, or its related persons (and their respective directors, associates, connected persons and/or employees) shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof. In particular, CIMB disclaims all responsibility and liability for the views and opinions set out in this report.

Unless otherwise specified, this report is based upon sources which CIMB considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research.

Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CIMB or its affiliates to any person to buy or sell any investments.

CIMB, its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMB, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

CIMB or its affiliates may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CIMB may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure.

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. CIMB prohibits the analyst(s) who prepared this research report from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request.

Reports relating to a specific geographical area are produced by the corresponding CIMB entity as listed in the table below. The term “CIMB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, CIMB Group Holdings Berhad ("CIMBGH") and its affiliates, subsidiaries and related companies.

Country CIMB Entity Regulated by

Hong Kong CIMB Securities Limited Securities and Futures Commission Hong Kong

India CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI)

Indonesia PT CIMB Securities Indonesia Financial Services Authority of Indonesia

Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia

Singapore CIMB Research Pte. Ltd. Monetary Authority of Singapore

South Korea CIMB Securities Limited, Korea Branch Financial Services Commission and Financial Supervisory Service

Taiwan CIMB Securities Limited, Taiwan Branch Financial Supervisory Commission

Thailand CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

India│Strategy Note│May 2, 2017

26

(i) As of May 1, 2017, CIMB has a proprietary position in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report:

(a) Hero Motocorp

(ii) As of May 2, 2017, the analyst(s) who prepared this report, and the associate(s), has / have an interest in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report:

(a) -

This report does not purport to contain all the information that a prospective investor may require. CIMB or any of its affiliates does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CIMB nor any of its affiliates nor its related persons shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

This report is general in nature and has been prepared for information purposes only. It is intended for circulation amongst CIMB and its affiliates’ clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments or any derivative instrument, or any rights pertaining thereto.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report.

The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CIMB Securities (Singapore) Pte. Ltd. and CIMB Securities Limited. This research is only available in Australia to persons who are “wholesale clients” (within the meaning of the Corporations Act 2001 (Cth) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. You represent and warrant that if you are in Australia, you are a “wholesale client”. This research is of a general nature only and has been prepared without taking into account the objectives, financial situation or needs of the individual recipient. CIMB Securities (Singapore) Pte. Ltd. and CIMB Securities Limited do not hold, and are not required to hold an Australian financial services licence. CIMB Securities (Singapore) Pte. Ltd. and CIMB Securities Limited rely on “passporting” exemptions for entities appropriately licensed by the Monetary Authority of Singapore (under ASIC Class Order 03/1102) and the Securities and Futures Commission in Hong Kong (under ASIC Class Order 03/1103).

Canada: This research report has not been prepared in accordance with the disclosure requirements of Dealer Member Rule 3400 – Research Restrictions and Disclosure Requirements of the Investment Industry Regulatory Organization of Canada. For any research report distributed by CIBC, further disclosures related to CIBC conflicts of interest can be found at https://researchcentral.cibcwm.com .

China: For the purpose of this report, the People’s Republic of China (“PRC”) does not include the Hong Kong Special Administrative Region, the Macau Special Administrative Region or Taiwan. The distributor of this report has not been approved or licensed by the China Securities Regulatory Commission or any other relevant regulatory authority or governmental agency in the PRC. This report contains only marketing information. The distribution of this report is not an offer to buy or sell to any person within or outside PRC or a solicitation to any person within or outside of PRC to buy or sell any instruments described herein. This report is being issued outside the PRC to a limited number of institutional investors and may not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose.

France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument.

Germany: This report is only directed at persons who are professional investors as defined in sec 31a(2) of the German Securities Trading Act (WpHG). This publication constitutes research of a non-binding nature on the market situation and the investment instruments cited here at the time of the publication of the information.

The current prices/yields in this issue are based upon closing prices from Bloomberg as of the day preceding publication. Please note that neither the German Federal Financial Supervisory Agency (BaFin), nor any other supervisory authority exercises any control over the content of this report.

Hong Kong: This report is issued and distributed in Hong Kong by CIMB Securities Limited (“CHK”) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at CIMB Securities Limited. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CHK.

CIMB Securities Limited does not make a market on other securities mentioned in the report.

India: This report is issued and distributed in India by CIMB Securities (India) Private Limited (“CIMB India”) which is registered with the National Stock Exchange of India Limited and BSE Limited as a trading and clearing member under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992. In accordance with the provisions of Regulation 4(g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CIMB India is not required to seek registration with the Securities and Exchange Board of India (“SEBI”) as an Investment Adviser. CIMB India is registered with SEBI as a Research Analyst pursuant to the SEBI (Research Analysts) Regulations, 2014 ("Regulations").

This report does not take into account the particular investment objectives, financial situations, or needs of the recipients. It is not intended for

India│Strategy Note│May 2, 2017

27

and does not deal with prohibitions on investment due to law/jurisdiction issues etc. which may exist for certain persons/entities. Recipients should rely on their own investigations and take their own professional advice before investment.

The report is not a “prospectus” as defined under Indian Law, including the Companies Act, 2013, and is not, and shall not be, approved by, or filed or registered with, any Indian regulator, including any Registrar of Companies in India, SEBI, any Indian stock exchange, or the Reserve Bank of India. No offer, or invitation to offer, or solicitation of subscription with respect to any such securities listed or proposed to be listed in India is being made, or intended to be made, to the public, or to any member or section of the public in India, through or pursuant to this report.

The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from the other activities of CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CIMB India or its affiliates.

The analyst's, strategists' or economists' or his/her relative Research Analyst's, strategists' or economists' has not received any investment banking related compensation from the companies mentioned in the report in the past 12 months.

The analyst's, strategists' or economists' or his/her relative Research Analyst's, strategists' or economists' has not received any compensation from the companies mentioned in the report in the past 12 months.

None of the analyst, strategist, or economist has served as an officer, director or employee of the companies mentioned in the report.

The analyst(s) has(have) not had any serious disciplinary action taken against him/her(them).

The analyst, strategist, or economist does not have any material conflict of interest at the time of publication of this report.

CIMB Securities (India) Pte Ltd has not received any investment banking related compensation from the companies mentioned in the report in the past 12 months.

CIMB Securities (India) Pte Ltd has not received any compensation from the companies mentioned in the report in the past 12 months.