Strategic Partnerships in Offshore Project Installations ... · Greater Gabbard was an ‘expensive...

14

1 Strategic Partnerships in Offshore Project Installations and Wind Farm Operation Track: Policy, Industry, Markets & Regulation Presentation Document EWEA Annual Event, Brussels, March 14, 2011 Speaker: Thomas Karst, MAKE Consulting

Transcript of Strategic Partnerships in Offshore Project Installations ... · Greater Gabbard was an ‘expensive...

1

Strategic Partnerships in Offshore ProjectInstallations and Wind Farm Operation

Track: Policy, Industry, Markets & Regulation

Presentation Document

EWEA Annual Event, Brussels, March 14, 2011Speaker: Thomas Karst, MAKE Consulting

MAKE Consulting A/S

2

MAKE Consulting is an advisory company specialized in the renewable energy market with particular focus on intelligence and strategy for the wind energy market.

MAKE Consulting employs a team of professional and independent advisors with documented experience from the international wind energy industry providing an in-house detailed market intelligence which we make every effort to translate into a product that provides the players with a competitive advantage.

MAKE Consulting has offices in Aarhus, Denmark and in Chicago and Boston, USA and Tianjin, P. R. China.

MAKE Consulting A/S, www.make-consulting.com

Speaker:Thomas Karst.Masters in Chemical Engineering12 years experience in wind energy from NEG Micon, Vestas and MAKE Consulting.

3

Contents

1. The Offshore Opportunity

3. Some of the Key Risks in Offshore Projects

2. Owners and Suppliers

4. Historical Changes to Contracting Structure

5. Why move to Strategic Partnerships?

7. Advantages in Strategic Partnerships

6. Different Cases of Recent Partnerships

8. Qualifying the Risk Reduction

4

Suppliers of WTGs, Foundations, Vessels, and Cables are most important players

Historical Offshore Cost Split

The Offshore Opportunity

Offshore Market Outlook

WTG44%

Installation vessels

15%

Foundation22%

Electrical grid7%

Substation7%

CAR insurance

2%

Man.2%

Eng.1%

WTG Installation vesselsFoundation Electrical gridSubstation CAR insuranceManagement Engineering

5

Diversification among Owners – but relatively few WTG OEMs

Owners and Suppliers

Owner Market Shares (2013) WTG OEM Market Shares (2013)

6

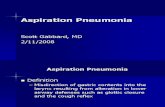

Some of the Key Risks in Offshore Projects

FinancingGround/soilCablesAccessibilityInstallation vesselsWTG ReliabilityNew WTG technologySubstationDamage to equipmentDelaysInterface problems

Development & Contracting

Survey & Planning Installation Testing &

Commissioning O&M

Qualification of partner

Planning in unisonRisk definition Specification of

common contingencies

Minimization of fiscal warranties

Adequate time allocation

Partner steering committee

Performance driven execution

Risk management and mitigation process

Common communication route

Litigation management process

“Common lessons learned“

Strategic Partnerships draws on combined “Lessons Learned” to minimize risks

Partnerships establishment Partnerships execution

“Controlled execution at less cost”

7

Moving from EPC and Multi-contracting towards Strategic Partnerships

Historical Changes to Contracting Structure

1991-2004 2005 – Present Future

EPC/Turnkey Multi-contracting Strategic Partnerships

• Balanced Risk• Low

contingency• High influence

OWNER

• Balanced Risk• Low

contingency• High influence

Partners

• Lower Risk• Medium

contingency• Low influence

Non-Partners

• High risk• High

contingency• High influence

OWNER

• Lower risk• Medium

contingency• Medium

influence

Main suppliers

• Lower risk• Medium

contingency• Low influence

Sub suppliers

• Low risk• Low

contingency• Low influence

OWNER

• High risk• High

contingency• High influence

Contractor

• High risk• High

contingency• Low influence

Suppliers

8

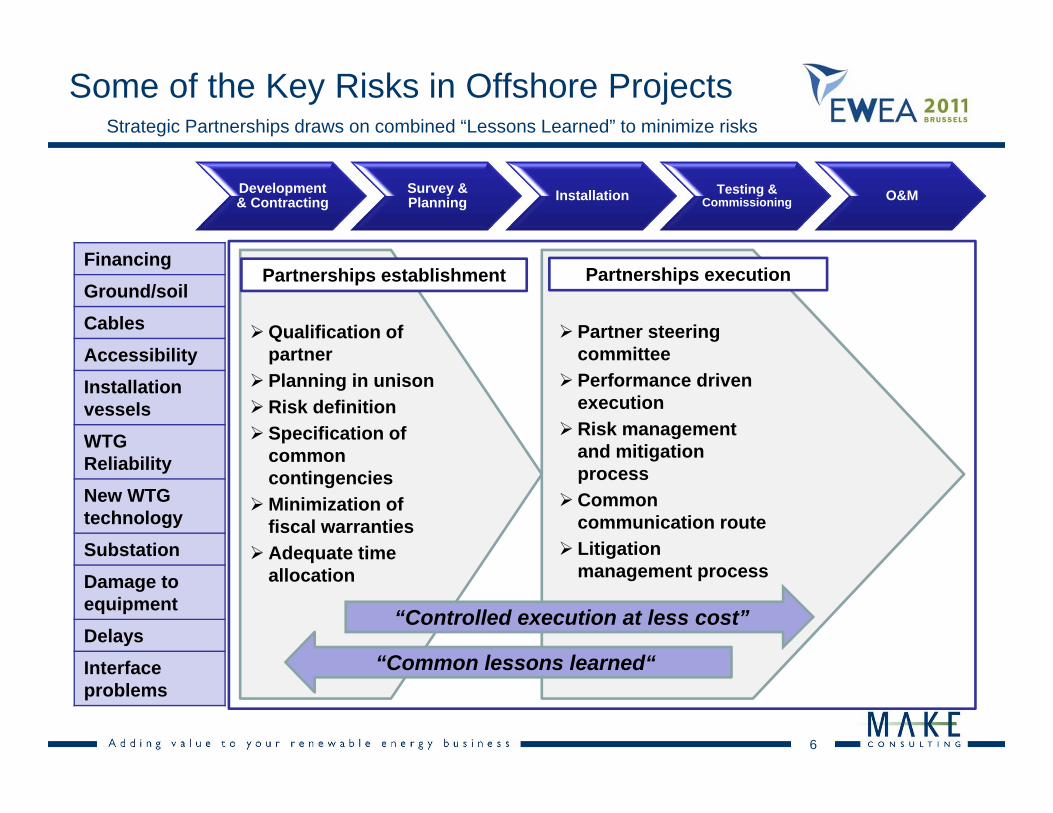

Two recent quotes from the offshore wind industry (February 2011)

• Project delay due to monopile welding defects• Subsea cable installation company Subocean

went bankrupt

• Flour reported total losses on the project ofo $ 163 million in Q3, 2010o $ 180 million in Q4, 2010

• “Seaton, who became CEO last month, said Greater Gabbard was an ‘expensive lesson’ and that Fluor would insist on controlling marine assets in future projects”. [Bloomberg]

Need for more control, risk reduction, and larger financial entities

• “There is a consensus that when Round 3 construction begins in 2015 there will be a significant shortage of HV cables”

• “Most [cable] suppliers have expansion plans in place but are currently unwilling to invest without a firm commitment”

• “The report calls for industry to work towards framework agreements.” [reNews]

Need for industry cooperation, better planning and greater transparency

Why move to Strategic Partnerships?

Fluor on Greater Gabbard Crown Estate on Cable supply

9

Complementing expertise and strong synergy effects

• Beluga Shipping GmbH is the world’s leading project and heavy goods shipper with a fleet of around 70 multipurpose heavy lift carriers.

• HOCHTIEF Construction AG is the fourth largest provider of construction-related services in the world with 68,000 employees.

• The joint venture Beluga Hochtief was formed in April 2009 in order to develop heavy-lift jack-up vessels for loading, transporting and installing huge offshore wind modules and undertake maintenance of offshore facilities

• Combining complementing expertise, the joint venture also provide access to technology, logistics, equipment and investment services

• A2SEA was established in 2000• Since then they have installed approximately

60% of all offshore wind turbines

• DONG and Siemens have a long history together with many offshore projects erected from 1991 and onwards

• With a purchase of A2SEA a strong trinity with several synergy effects could be created

• In July 2009 A2SEA was acquired 100% by Danish utility DONG Energy Power

• in November 2010 Siemens Wind Power entered as part-owner – buying 49% of A2SEA from DONG.

Different Cases of Recent Partnerships

Case 1: Beluga Hochtief Case 2: A2SEA/DONG/Siemens

10

Complementing expertise and strong synergy effects

• SMart Wind Ltd. is a joint venture betweenMainstream Renewable Power and Siemens Project Ventures GmbH put in place in order to deliver the 4GW Hornsea Zone by 2020

• Mainstream Renewable Power was formed in February 2008 a has a portfolio of 5.5GW offshore across Scotland, England and Germany, as well as over 3.5GW of onshore projects in Canada, Chile, S.A. and the US.

• Siemens Project Ventures brings in the Siemens Energy network, including Siemens Wind Power which is the leading supplier of offshore wind turbines, and Siemens Transmission and Distribution

• Also cooperating with Beluga Hochtief

Gamesa and Northrop Grumman Corporation• A large onshore WTG OEM setting up joint

R&D facilities with America’s largest shipbuilder and leading U.S. defence company

Different Cases of Recent Partnerships

Case 3: SMart Wind Ltd. Case 4,5,6, and 7

BARD Group• An alternative strategy with in-house WTG and

tri-pile foundation manufacturing - together with own installation jack-up and O&M vessel.

• Also offering financing and insurance.

Scottish and Southern Energy and Mitsubishi• Cooperating on “low carbon energy

development” including a range of new technologies for offshore wind farms, etc.

AREVA/ALSTOM/GE• Conglomerates capable of handling every

aspect of an offshore project on their own• Know-how transition from other technologies

2. Risk Assessment

3. Plan Mitigations

4. Implement

Actions

5. Control and

Monitor

1. Identify Risks

11

Cooperation will bring down costs and create synergies using Risk Management

Advantages in Strategic Partnerships

WTG OEM Foundation Supplier

InstallationVessel

Provider

OffshoreCable

Supplier

Reduce accumulated

contingencies

Reduce fiscal warranties and

bonds

Reduce time slackand waiting cost in

planning

Reduce litigious environment

project cost and cash flow

Improved project cost and

cash flow

12

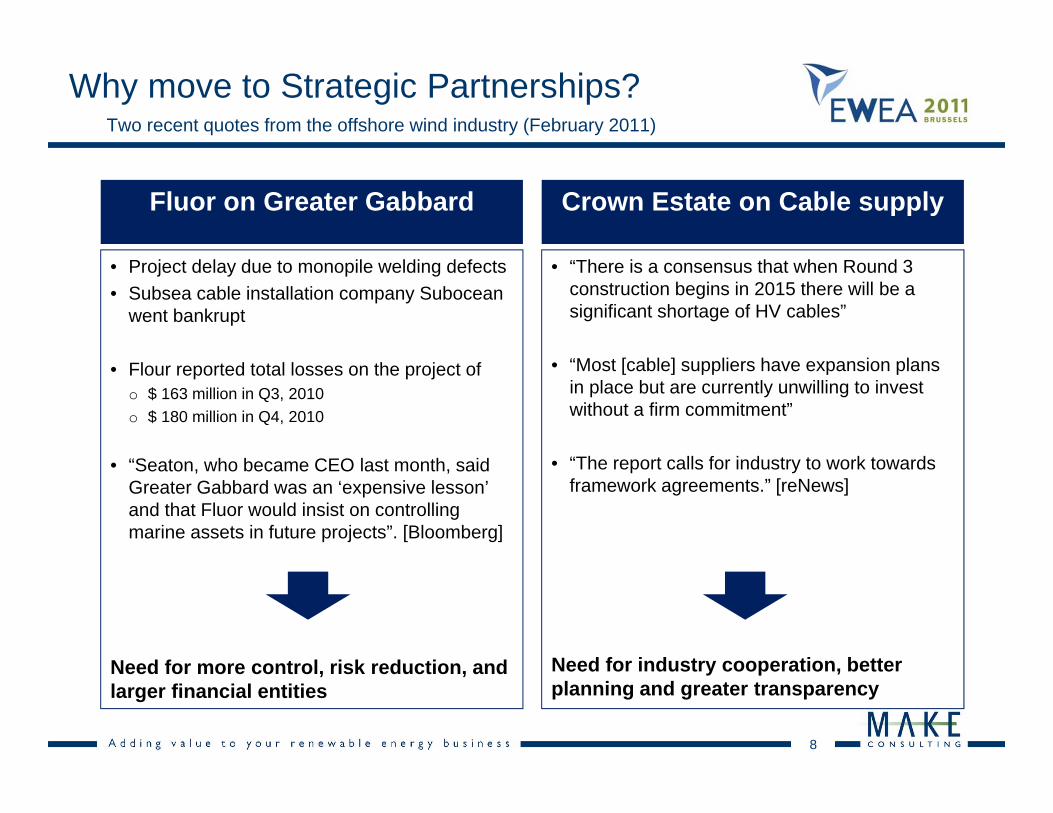

The effect of Strategic Partnerships

Qualifying the Risk Reduction

Combining complementary

expertise

Strengthening the supply chain by

adding new elements

Gaining volume and larger financial impact

Thereby covering interface problems

and creating synergy

Thereby increasing project robustness

and feasibility

Thereby increasing technological

know-how and skills

13

Thank you!

14

MAKE Consulting

Aarhus, Denmark (Head Office)Tianjin, P. R. ChinaChicago, USABoston, USA

Copyright © 2011 MAKE Consulting A/S. All rights reserved.Reproduction or distribution of this report in any form without prior written permission is strictly forbidden. Violation of the above restrictions will be subject to legal action under the Danish Arbitration Act. The information herein is taken from sources considered reliable, but its accuracy and completeness are not warranted, nor are the opinions, analyses and forecasts on which they are based. MAKE Consulting A/S cannot be held liable for any errors in this report, neither can MAKE Consulting A/S be liable for any financial loss or damage caused by the use of the information presented in this report.

Reports and notes recently compiledby MAKE Consulting:

• 2H 2010: Global wind turbine order activity at highest level in two years(research note, February 11, 2011)

• French offshore tender – too little, too late??(flash note, January 31, 2011

• Wind Turbine Trends 2010(market report, December 29, 2010)

• Goldwind marks major milestone with Mainstream(flash note, December 23, 2010)

• Wind power to receive support in China's 12th Five Year Plan(flash note, December 7, 2010)

• Competition intensifies in low wind speed WTG segment(flash note, November 30, 2010)

• Wind power blows into Eastern Europe(research note, November 22, 2010)

• Chinese onshore WTG pricing drops to all-time lows(flash note, November 19, 2010)

• U.S. tower manufacturers face dubious future(research note, November 18, 2010)