Strategic Managmnt.

30

-

Upload

hina-afshin -

Category

Documents

-

view

218 -

download

0

Transcript of Strategic Managmnt.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 1/30

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 2/30

We change the world not byWhat we say or do

But as a consequences

of what we have become.

I thank, first and foremost, Allah for having enabled me to

complete such a project that would not have been possible for

me to complete without His help in all stages of its preparation.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 3/30

I would like to say specious word “thanks” to my most Respected

Sir IMRAN who helps me to do and understand different things

in different way.

I am also very thankful to my parents and all other teachers

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 4/30

“I want to dedicate all my jeopardized efforts to my

beloved parents, no doubt a role model for me in every

facet of my life, an ocean of ethics and a light house that

guides me in every next step of my life.”

Strategic management:

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 5/30

“It can be defined as an art and science of formulating,

implementing, and evaluating cross functional decisionsthat enable an organization to achieve its objectives.”

Stages of strategic decision process:

There are three stages o this process:

•

Strategy formulation

• strategy implementation

• And strategy evaluation

Strategy formulation

It Includes development of vision and mission statements,

identifying an organization external opportunities threats

and determining internal strengths and weaknesses.

Strategy implementation

It requires a firm to establish annual objectives. Devisepolicies, motivate employees and allocate resources so hat

formulated strategies can be executed.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 6/30

Strategy evaluation

Is the final stage in strategic management? Managers

desperately need to know when particular stages are not

working well;’ strategy evaluation is a primary mean for

obtaining this information.

Example of a strategy decision:

In most businesses, a few decisions make the difference

between superior performance and ordinary results. But

strategic decisions are seldom easy. They call for high

quality analysis and strategic thinking, in order to select

the right decision from amongst the many possible options.

They also depend on skills in managing the decision

process, including sequencing activities, defining roles,

effective teamwork and handling the people side. This

practical and highly interactive program will help you

improve the quality of your strategic decision making,

providing practical tools for addressing both the analytic

and process management challenges.

What will we learn?

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 7/30

• The difference between strategic and operational

thinking.

• Practical tools for developing strategy.

• Techniques for managing the decision making

process.

• Tips and pitfalls in making strategic decisions, based

on the tutors' 40+ years of combined experience

working in large organizations.

Who’s it for?

Senior managers involved in making strategic decisions,

either in a general management position or a functional

role, who want to understand both the theory and the

practice of making good decisions,. You may be in

transition from the operational to a more strategic role,

needing to have a better understanding of strategies you

have to implement or actually shaping strategic direction.

How will my company or organization benefit?

In order to succeed an organization needs strategic

thinkers. Your increased understanding will raise the

quality of your strategic thought process. This will be

reflected in the outcome of your future decisions.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 8/30

What makes this programme different?

• The combination of tools for developing strategy and

managing the decision making process.

• The emphasis on experiential learning - the final role-

play, based on a real business decision, pulls all the

elements together in a situation reflecting the

complexities and uncertainties of real life.

• The caliber of the participants.

• The ability to take the course either in a one five day

session in May or November, or in two modules, of two

and three days. See the sidebar on the right of this

webpage for further details.

• The opportunity to stay in touch with the tutors and

other participants through the use of our post-course

website forum.

Question # 02

Strategy - the strategic audit

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 9/30

In our introduction to business strategy, we emphasized

the role of the "business environment" in shaping strategic

thinking and decision-making.

The external environment in which a business operates can

create opportunities which a business can exploit, as well

as threats which could damage a business. However, to be

in a position to exploit opportunities or respond to threats,

a business needs to have the right resources and

capabilities in place.

An important part of business strategy is concerned with

ensuring that these resources and competencies are

understood and evaluated - a process that is often known

as a "Strategic Audit".

The process of conducting a strategic audit can be

summarised into the following stages:

(1) Resource Audit:

The resource audit identifies the resources available to a

business. Some of these can be owned (e.g. plant and

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 10/30

machinery, trademarks, retail outlets) whereas other

resources can be obtained through partnerships, joint

ventures or simply supplier arrangements with other

businesses.

(2) Value Chain Analysis:

Value Chain Analysis describes the activities that take

place in a business and relates them to an analysis of the

competitive strength of the business. Influential work by

Michael Porter suggested that the activities of a business

could be grouped under two headings:

(1) Primary Activities - those that are directly concerned

with creating and delivering a product (e.g. component

assembly);

(2) Support Activities, which whilst they are not directly

involved in production, may increase effectiveness or

efficiency (e.g. human resource management).

It is rare for a business to undertake all primary

and support activities. Value Chain Analysis is one way of

identifying which activities are best undertaken by a

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 11/30

business and which are best provided by others

("outsourced").

(3) Core Competence Analysis:

Core competencies are those capabilities that are critical to

a business achieving competitive advantage. The starting

point for analysing core competencies is recognising that

competition between businesses is as much a race for

competence mastery as it is for market position and

market power. Senior management cannot focus on all

activities of a business and the competencies required to

undertake them. So the goal is for management to focus

attention on competencies that really affect competitive

advantage

(4) Performance Analysis

The resource audit, value chain analysis and core

competence analysis help to define the strategiccapabilities of a business. After completing such analysis,

questions that can be asked that evaluate the overall

performance of the business. These questions include:

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 12/30

- How have the resources deployed in the business

changed over time; this is "historical analysis"

- How do the resources and capabilities of the business

compare with others in the industry - "industry norm

analysis"

- How do the resources and capabilities of the business

compare with "best-in-class" - wherever that is to be found-

"benchmarking"

- How has the financial performance of the business

changed over time and how does it compare with key

competitors and the industry as a whole? - "ratio analysis"

(5) Portfolio Analysis:

Portfolio Analysis analyses the overall balance of the

strategic business units of a business. Most large

businesses have operations in more than one market

segment, and often in different geographical markets.

Larger, diversified groups often have several divisions

(each containing many business units) operating in quite

distinct industries.

An important objective of a strategic audit is to ensure that

the business portfolio is strong and that business units

requiring investment and management attention are

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 13/30

highlighted. This is important - a business should always

consider which markets are most attractive and which

business units have the potential to achieve advantage in

the most attractive markets.

Traditionally, two analytical models have been widely used

to undertake portfolio analysis:

- The Boston Consulting Group Portfolio Matrix (the

"Boston Box");

- The McKinsey/General Electric Growth Share Matrix

(6) SWOT Analysis:

SWOT is an abbreviation for Strengths, Weaknesses,

Opportunities and Threats. SWOT analysis is an importanttool for auditing the overall strategic position of a business

and its environment.

Question # 03:

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 14/30

If we conduct a Resourcse audit we will be helped by

the following model.

New Paradigm: Resource-Based Theory

The currently dominant view of business strategy –

resource-based theory or resource-based view (RBV) of

firms – is based on the concept of economic rent and the

view of the company as a collection of capabilities. This

view of strategy has a coherence and integrative role that

places it well ahead of other mechanisms of strategic

decision making.

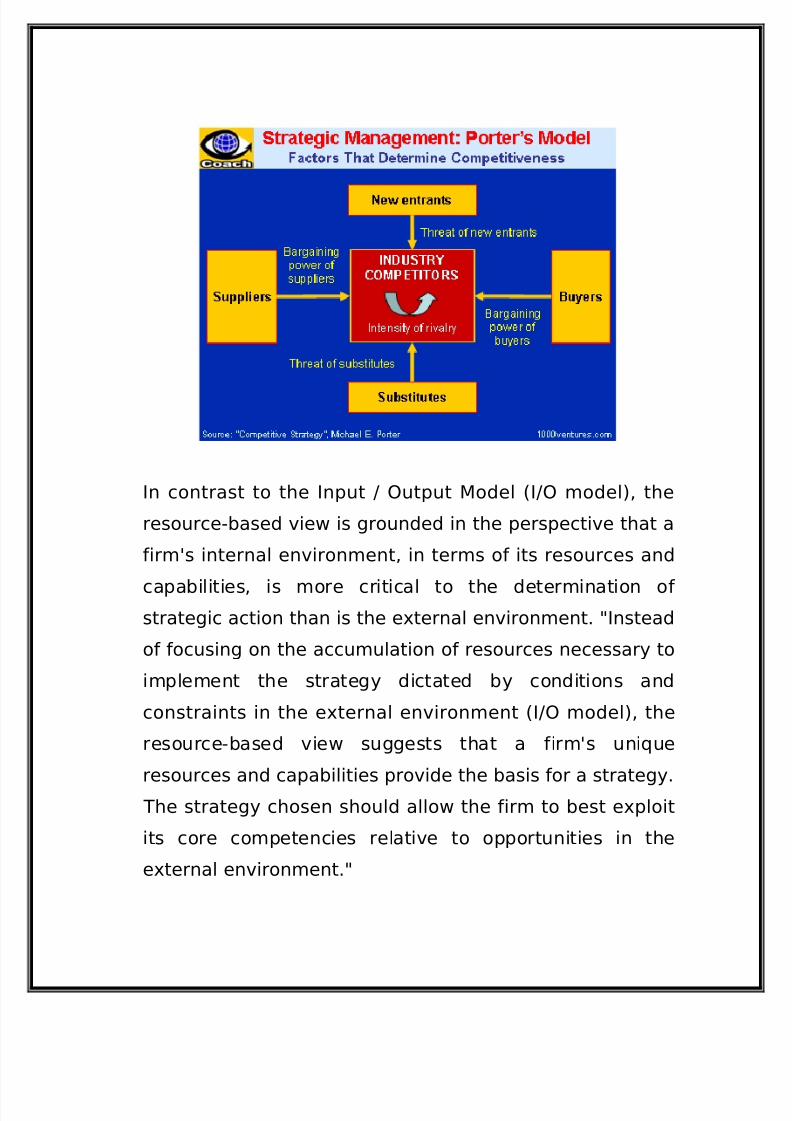

Traditional strategy models such as Michael

Porter's five forces model focus on the company's

external competitive environment. Most of them do not

attempt to look inside the company. In contrast, the

resource-based perspective highlights the need for a fit

between the external market context in which a company

operates and its internal capabilities.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 15/30

In contrast to the Input / Output Model (I/O model), the

resource-based view is grounded in the perspective that a

firm's internal environment, in terms of its resources and

capabilities, is more critical to the determination of strategic action than is the external environment. "Instead

of focusing on the accumulation of resources necessary to

implement the strategy dictated by conditions and

constraints in the external environment (I/O model), the

resource-based view suggests that a firm's unique

resources and capabilities provide the basis for a strategy.

The strategy chosen should allow the firm to best exploit

its core competencies relative to opportunities in the

external environment."

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 16/30

Sustainable Competitive Advantage

According to this view, a company's competitive

advantage derives from its ability to assemble and exploit

an appropriate combination of resources. Sustainable

competitive advantage is achieved by continuously

developing existing and creating new resources and

capabilities in response to rapidly changing market

conditions.

Creating Economic Rent

The resource based view of strategy emphasizes

economic rent creation through distinctive capabilities.

Economic rent, or Economic Value Added (EVA), is what

companies earn over and above the cost of the capital

employed in their business. It is the measure of the

competitive advantage, and competitive advantage is the

only means by which companies in competitive markets

can earn economic rent. The objective of a company is to

increase its economic rent, rather than its profit as such.

"A company which increases its profits but not its

economic rent - as through investments or acquisitions

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 17/30

which yield less than the cost of capital - destroys value."

The perspective of economic rent forces the question 'why

can't competitors do that?' into discussion.

Resources and Capabilities

Each organization is a collection of unique resources and

capabilities that provides the basis for its strategy and the

primary source of its returns. In the 21st-century hyper-

competitive landscape, a firm is a collection of evolving

capabilities that is managed dynamically in pursuit of

above-average returns. Thus, differences in firm's

performances across time are driven primarily by their

unique resources and capabilities rather than by an

industry's structural characteristics.

Resources are inputs into a firm's production process,

such as capital, equipment, the skills of individual

employees, patents, finance, and talented managers.

Resources are either tangible or intangible in nature. With

increasing effectiveness, the set of resources available to

the firm tends to become larger. Individual resources may

not yield to a competitive advantage. It is through the

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 18/30

synergistic combination and integration of sets of

resources that competitive advantages are formed.

A capability is the capacity for a set of resources to

interactively perform a stretch task or an activity. Through

continued use, capabilities become stronger and more

difficult for competitors to understand and imitate. As a

source of competitive advantage, a capability "should be

neither so simple that it is highly imitable, nor so complex

that it defies internal steering and control."

7 Dimensions of Strategic Innovation

The Strategic Innovation framework weaves togetherseven dimensions to produce a range of outcomes that

drive growth.

Core Technologies and Competencies is the set of internal

capabilities, organizational competencies and assets that

could potentially be leveraged to deliver value to

customers, including technologies, intellectual property,brand equity and strategic relationships.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 19/30

The Growing Role of the Business Architect

In today's knowledge- and innovation-driven complex

economy, business architects are in growing demand.

They are cross-functionally excellent people who can tie

several silos of business development expertise together,

create synergies, design winning business model and a

balanced business system and then lead people who will

put their plans into action.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 20/30

Question # 04:

Part (a)

Question # 05

There are numerous questions concerning motives for any

merger that need to be asked and answered when

evaluating the new company. Among others, investors

need to know if a merger makes sense and what are the

chances of the new company making it in the tough world

of capital markets.

A few of the motives for mergers are discussed below.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 21/30

Synergy

The word synergy has been somewhat abused, but it still

conveys the message that two in one are worth more than

the sum of their respective parts. The idea is to combine

assets and liabilities, trim the fat, and thus either cut down

costs or boost up revenues.

Speaking of cutting down costs, this goal is typically

achieved through economies of scale, particularly when it

comes to sales and marketing, administrative, operating,

and/or research and development costs. As for revenue

synergies, these are achieved through product cross-

selling, higher prices due to less competition, or staking a

larger market share.

Growth

Increasing a company’s growth rate is perhaps the most

often cited motive for a merger. No surprises there,considering the pressure put on corporate managers today

to increase sales, earnings, profit margins, etc. Growth can

be achieved either internally by investing in capital

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 22/30

projects, or externally by buying assets of other

companies. Empirical studies confirm that faster growth

rates are achieved through external growth, which is why

mergers and acquisitions come in very handy.

Acquiring More Market Power

If a company operates within a concentrated market where

there are fewer competitors, merging via horizontal

integration could provide the company with even more

market power. Having more market power also means

having the ability to impact and/or control prices. If taken

to an extreme, horizontal mergers could create a

monopoly.

Note that horizontal mergers are not the only type of

mergers that can yield more market power. Vertical

mergers can enable a company to capture sources of

supplies, for example, that are of paramount importance to

its competitors. This is why industry regulators routinely

limit and even disallow horizontal and vertical mergers if

there is even a hint of too much market power

concentrating in the hands of only a few companies.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 23/30

Diversification

Diversification is another frequently cited reason for

mergers. Actually, it was THE reason during the

conglomerate merger wave. The idea was to circumvent

regulatory restrictions on horizontal and vertical mergers

by going outside a company’s industry into new markets

and to achieve growth there.

Although diversification sounds like a fine motive for a

merger, far too often it does not serve interests of a

conglomerate’s shareholders. Namely, conglomerate

mergers often cost serious money and may cause a

company to lose focus on an industry where it may have

competitive or comparative advantage. After all,

shareholders can diversify their own portfolios more easily

and certainly at a much lower cost.

“Bootstrapping Earnings”

When a company’s earnings increase as a result of the

merger transaction and not due to the allegedly created

economic benefit from the merger, this is called the

bootstrapping effect or bootstrapping earnings. It occurs

when the acquirer has higher price-to-earnings (P/E) ratio

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 24/30

than the target, and particularly if the acquirer’s P/E ratio

does not decrease after the merger is completed.

In an efficient market, when two companies merge, the

resulting P/E ratio should adjust to the weighted average

earnings of both entities. Typically, the market reacts

quickly to the merger activity and adjusts valuations

accordingly.

However, there were periods, particularly during the

conglomerate merger wave, when at least short-term

bootstrapping benefited managers, while investors

struggled to evaluate the newly formed entities. Similar

effects were observable during the tech bubble of the late

1990s, when numerous companies with high P/E ratios

achieved continuous and increased earnings through

mergers with lower P/E target companies.

Intelligent Business

BI, CPM and the intelligence of organizations

• Home

• Search

• Sitemap

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 25/30

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 26/30

Unique resources to compete with

One group of strategic scholars focused on looking for strategic advantages inside the

organisation (and not within circumstances surrounding the organisation): this wascalled the resource-based view (Black & Boal, 1994; Foss, 1997; Mata et al., 1995;Wernerfelt, 1984; Lippman & Rumelt, 1992; Teece, Pisano, & Shuen, 1997, Grimm et

al., 2006). For their explanation of the term ‘resources’ these last authors used the

paper of Barney (1986b): “all assets, capabilities, organizational processes, firmattributes, information, knowledge, etc. controlled by a firm that enable the firm to

conceive of and implement strategies that improve its efficiency and effectiveness.”

(Grimm et al., 2006, p. 70).

Since we concluded in the previous section, that resources today are much easier tocopy than they were before, we have to look for certain unique resources in the

organization. These resources need to be difficult to copy and therefore intangible, sothat the competition can be kept at a distance for some time. Rothberg & Erickson(2005) note that many companies forget their intangible resources when thinking about

strategic advantages, because intangible resources are more difficult to connect to

figures about profit or costs. “Less obvious is the analysis of the unique and rareresources that serve to support the activity, such as intangible skills and know-how of

employees, (…). Although this second category might be considered soft and

subjective, it can also be connected with important tangible costs and revenue (…).” (p.

76). As the authors state, it is lamentable that organizations don’t use see their intangible resources as of potential strategic value: “(…) people, their individual and

collective knowledge and ability to generate actionable intelligence, are the greatest

asset of the firm.” (p. 27).

Tacit knowledge as an unique resource in your organization

It can be concluded, that for example the knowledge of your employees that they have

built up by experience and cannot be put into documents (so-called tacit knowledge,

Polanyi 1967), can be a unique resource for your organization to compete with. Certainexperience can be very rare, difficult to copy or to replace: a very valuable resource in

times of strategic war! With a lot of experience in your organization, you can respond

quicker to a new development and take better and faster decisions (den Hamer, 2005;Rothberg & Erickson, 2005; Davenport & Prusak, 1998).

So, in these times of hypercompetition and strategic wars, you have to focus on those

resources that make your organization unique in the battle. Then why is it that during

the current economic crisis, the first things that happen are the lay-off of a lot of employees? The built up experience, the tacit knowledge of your people, the

knowledge that makes your organization unique: these unique resources deserve some

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 27/30

special consideration because they can save your organizations life during the strategic

battle yet to come.

Literature

• Barney, J. B. (1986b). Strategic Factor Markets: Expectations, Luck, andBusiness Strategy. Management Science, 32(10), 1231 - 1241.

• Barney, J. B. (1991). Firm Resources and Sustained Competitive Advantage.

Journal of Management 17(1), 99 - 120.

• Davenport, T. H., & Prusak, L. (1998). Working Knowledge. Howorganizations manage what they know. Boston: Harvard Business School Press.

• den Hamer, P. (2005). De organisatie van business intelligence. Den Haag:

Academic Service.

• Foss, N. J. (1997). Resources, Firms and Strategies. Oxford: Oxford University

Press.• Grimm, C. M., Lee, H., & Smith, K. G. (2006). Strategy as action: competitive

dynamics and competitive advantage. . Oxford: Oxford University Press.

• Hislop, D. (2005). Knowledge management in organizations: a critical

introduction. Oxford: Oxford University Press.

• Kogut, B., & Zander, U. (1997). Knowledge of the Firm, Combinative

Capabilities, and the Replication of Technology. In N. J. Foss (Ed.), Resources,

Firms and Strategies (pp. 306 - 327). Oxford: Oxford University Press.

• Lippman, S. A., & Rumelt, R. P. (1992). Demand Uncertainty, CapitalSpecificity, and Industry Evolution. Industrial and Corporate Change, 1(1), 235

- 262.

•

Mata, F. J., Fuerst, W. L., & Barney, J. B. (1995). Information Technology andSustained Competitive Advantage: A Resource-Based Analysis. MIS Quarterly,

19(4), 487 - 505.

• Polanyi, M. (1967). The tacit dimension. London: Routledge & Kegan Paul.

• Porter, M. E. (1980). Competitive strategy: techniques for analyzing industries

and competitors. New York: Free Press.

• Prahalad, C. K., & Hamel, G. (1997). The Core Competence of the

Corporation. In N. J. Foss (Ed.), Resources, Firms and Strategies (pp. 235 -257). Oxford: Oxford University Press.

• Rothberg, H. N., & Erickson, G. S. (2005). From Knowledge to Intelligence.

Burlington, MA: Elsevier.

•

Teece, D. J., Pisano, G., & Shuen, A. (1997). Dynamic Capabilities andStrategic Management. In N. J. Foss (Ed.), Resources, Firms and Strategies (pp.

268 - 286).

• Wernerfelt, B. (1984). A Resource-Based View of the Firm. Strategic

Management Journal, 5(2), 171 - 180.

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 28/30

(No Ratings Yet)

Loading ...

Entry Filed under: Intelligence, Science

Related Posts:

The strategy as a guideline

Organisational Intelligence

What is Intelligence?

Corporate Performance Management

The FIT between BI-users and solutions

Leave a Comment

Name Required

Email Required, hidden

Url

Comment

Submit

Some HTML allowed:<a href="" title=""> <abbr title=""> <acronym title=""> <b> <blockquote cite="">

<cite> <code> <del datetime=""> <em> <i> <q cite=""> <strike> <strong>

Trackback this post | Subscribe to the comments via RSS Feed

þÿ

þÿ

þÿ

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 29/30

About...

Intelligent Business:

• Business Intelligence

• Corporate Performance M.

• Organizational Intelligence

Authors:

• Bas van Raaij

• Martijn van de Ridder

• Mariska Bulten

Search

Keywords

Blogroll

• BI Guru• BI Nerd

• Business Innovation• Dutch BI Blog

• KPI Portal

Categories

þÿ

8/8/2019 Strategic Managmnt.

http://slidepdf.com/reader/full/strategic-managmnt 30/30

• Business Intelligence

• Corporate Performance Management

o KPIs

•

General• Intelligence

• Science

• Website

Highest Rated

• Fifty years of Business Intelligence (5 out of 5)

• The strategy as a guideline (4.5 out of 5)

• The FIT between BI-users and solutions (4 out of 5)• KPI Portal has been born! (4 out of 5)

• What is Intelligence? (4 out of 5)

© Copyright Intelligent Business || All rights reserved || Contact

Log in