strategic industry plan

74

JANUARY 2013 REPRINTED JULY 2014 strategic industry plan

Transcript of strategic industry plan

J A N U A R Y 2 0 1 3R E P R I N T E D J U LY 2 0 1 4

strategic industry plan

3executive summary

7industry visionindustry objectivecurrent state of industry

13critical success factors

design and innovation regulatory and compliance regime labour skills and training supply chain

34strategic directions for the industry

strategies to enhance industry development and business competitiveness

industry leadership – actions to be pursued at the association level

role for government

51conclusion- summary of issues & recommended actions

design and innovation

regulatory and compliance regime

labour skills and training

supply chain

The Strategic Plan has been prepared by the Kreitals Consulting Group. http://www.kreitals.com.au/

3

executive summaryThe Australian Furniture Cabinets and Joinery (FCJ) industry is a significant sector of Australian manufacturing, employing more than 130,000 persons across the country and contributing almost

$33 billion per annum to the domestic economy.

x

However, similar to Australian manufacturing generally, the local FCJ industry is an economically fr agmented sector characterised

by a preponderance of small, family-owned businesses. Less than one per cent of businesses in the sector employ more than 200

employees with the majority employing less than 20 workers. Over 80 per cent of businesses are based on the Eastern Seaboard with

58 per cent located in the traditional manufacturing states of Victoria and New South Wales and hence away from the growth states of

Western Australia, Queensland and the Northern Territory.

Activities within the sector comprise domestic and commercial, free standing and built in furniture; wooden doors; roof trusses and wall

frames; aluminium, timber and uPVC framed glazed windows and doors; other wooden builders’ joinery and carpentry, parquetry strips;

wooden industrial products and on-site installation.

The industry is currently under considerable restructuring pressure, competing against low cost imports in a high cost environment. This

is further compounded by the high Australian Dollar coupled with contracting market demand as both, new house starts and renovation

activity (traditionally key drivers for the industry), continue to decline.

Over 2011/12, total FCJ manufacturing revenue continued to decline (by a further 1.5 per cent), bringing the annual revenue level down

by almost 8 per cent to that prevailing pre-GFC. Moreover, industry productivity, as measured by value added per employee has also

fallen by a significant 10 per cent over this same period, despite the employment levels and total industry wages and salaries remaining

relatively stable over recent years.

Thus, recognising the critical turning point now confronting the industry, the 7 core industry associations representing the key sub-

sectors of the industry across Australia, have formed the FCJ Alliance (FCJA).

Currently, the FCJ industry can be characterised as being:

At a mature lifestyle stage; With negligible industry assistance; Subject to medium to low barriers to entry;

In a highly globalised industry confronting significant low cost import competition; and

Susceptible to revenue volatility.

However, the FCJA’s vision is to turn the Australian Furniture Cabinets and Joinery industry into one that is globally recognised as a vibrant,

design focussed industry sector, with world-class management, attracting the best workforce producing high value add, professionally

crafted, highly innovative furniture, cabinet and joinery products.

To help achieve this vision the FCJA has identified the following strategic objectives to underscore the industry’s ongoing development:

Embrace design and innovation as a core characteristic for future growth

Maximise its share of the domestic market

Develop an Export Culture and progressively grow export markets

Capitalise on and adopt latest technological developments

Attract more highly skilled, highly trained workers

Embody the latest management practices, reflecting world’s best practice in business management

Be an integral player in the global FCJ supply chain.

1

2

3

4

5

4

This Strategic Industry Plan has been developed by the FCJA to help

determine the most appropriate strategies that should be pursued to help

realise the above objectives. While the prime intention of the Plan is to

identify strategies and actions that the industry, and its representative

associations, should focus upon, it is clearly evident that there is a real role

for Government to play – both in ensuring that there are no unnecessary

impediments to the industry’s growth path and in supporting/encouraging

the priority development activities for the industry.

While many of the issues confronting the FCJ sector are ones that impact

on all manufacturing businesses, there are also many unique challenges

that must be addressed by the industry that require special attention, and

these are highlighted below. Nonetheless, much of the commentary on

manufacturing to date, and the focus of Government policy and policy

measures, seems to be driven by “big” manufacturing business. But there are

very few big businesses remaining in manufacturing in Australia, and those

that are can successfully straddle between local and offshore manufacture.

As far as the FCJ sector is concerned, it is predominantly epitomised by

small business, albeit it is a sector that collectively represents the major

employment base in Australian manufacturing.

Consequently, there needs to be a significant rethink to determine what

strategies are necessary for such a sector of industry. In developing this

Strategic Industry Plan it was soon evident that there are four Critical Areas

of Success for the Australian FCJ sector, and that strategies and Action

Plans would need to be developed for each of these – being Design and

Innovation, Regulation and Compliance, Skills Development and Training and

finally Supply Chain.

However, while priority action plans have been developed to address the

industry’s needs in each Critical Success Area, it is vital to recognise enhanced

development in all 4 critical areas must be progressed concurrently, and that

no recommended action should be considered in isolation from the others.

It is crucial to pursue all strategies as a collective whole, and only in that way

can the industry’s future viability be truly ensured.

The reality is that in the high cost environment now faced by Australian

FCJ producers, competing on price is no longer a sustainable model. For

Australian businesses to be sustainable long-term they need to be actively

seeking to enhance their operational efficiencies through enhanced capital

productivity (which means adopting the latest technologies) and labour

productivity (by upgrading skills at both management and operational

level), and they need to differentiate their product as a premium offering

based on superior quality, design and innovation.

The first and foremost critical success factor for the industry must

therefore be the development of a widespread and deeply ingrained design

/ innovation culture within the industry. Numerous companies in Australia

but predominantly overseas have successfully grown their markets

through incorporation of technologies and functionality (Herman Miller),

quality ground breaking design (Carl Hansen & Son) and customer tailored

design and development for both commercial and residential customers

(Schiavello, Sealy). Very often this has been done in conjunction with

recognised designers as a means of providing a unique, valued and sought

after product.

Of course, a design and innovation focus is more than just enhanced

product design, and embraces the whole operational process, from

production through packaging to ultimate marketing and customer service,

and even encompasses the overall business model. It is crucial that the FCJ

EXECUTIVE SUMMARY

5

industry of tomorrow has an inherent Design Culture which encompasses

design and innovation in all these facets.

Underscoring this Design focus is a need to enhance productivity within the

industry. Research conducted by the FCJA, Manufacturing Skills Australia

and numerous Government departments shows that the FCJ sector suffers

from a profound shortage of skilled workers across all disciplines necessary

for its operation. Since 2007 the number of apprenticeship commencements

has fallen each year. This lack of new entrants is compounded by an aging

workforce meaning that approximately an additional 15,000 workers will be

needed in the next five years to just maintain business as usual.

A core focus identified by the FCJA will be to work with governments,

tertiary education providers and individual enterprises to develop strategies

which maximise entrants to the workforce from non-traditional pathways

such as up-skilling of staff, greater engagement with secondary school

leavers and ways of increasing the participation of women into the sector.

Compounding the issue of a skills shortage is also the lack of structured

training at management and owner levels in the FCJ organisations. Further

training in the areas of finance, marketing, competitive manufacturing,

employee/subcontractor management and project management have been

particularly identified as needing to be addressed. Without development

and training in these areas business owners or managers will not have the

necessary skills to fully capitalise on emerging growth opportunities.

Greater focus will also be required in engaging in high end technical skills

related to computer aided manufacturing and design, production scheduling

and costing and pricing. Greater understanding on the potential of the

internet and other approaches direct to customers is also required.

To help achieve this, the FCJA will need to be more actively engaged in

the identification and development of training needs than it has in the past.

Currently the nature and delivery mode of training is simply not delivering

what the industry needs and the industry is united in its views that the

training package must be developed through the Forestworks Skills Council.

Another critical success factor identified by the FCJA is that of regulation

and compliance. In many ways this factor above all others has the greatest

potential to stifle the development of a sustainable, world class design

and innovation focused FCJ sector in Australia. While it is understood that

governments must make regulations to address market deficiencies or

achieve a common goal very often there are unintended consequences of

these actions.

However, the FCJA accepts that many regulations and standards are

necessary, to ensure the appropriate quality and performance requirements

are being fully met, and to safeguard consumers through the various product

safety standards. The FCJA supports the implementation of such standards

where they are clearly necessary, but is dismayed at the extent to which

imported product is able to breach such standards and regulations. It is

vital that where such legislative requirements exist, all imported products

must be monitored to the same extent as domestic product to ensure

compliance, and where it is non-compliant then necessary corrective action

must be taken, including strict enforcement of meaningful penalties.

The FCJA will seek to work with Governments to ensure that the industry’s

uniqueness is considered in the development of new legislation and

guidelines while also working through an identified list of regulations that

are either inhibiting growth, or are being applied

EXECUTIVE SUMMARY

6

inequitably with compliance only enforced upon local

manufacturers. The FCJA has undertaken a comprehensive review

of all legislation that impacts the sector (included as an Appendix

to the Strategic Plan) and believes that a pro-active cooperative

approach with governments is required to ensure the industry

can achieve its aims, and is not being treated in a discriminatory

fashion.

For this reason, the FCJA is strongly of the view that a single

body should be tasked specifically with monitoring compliance

by all products with existing standards and regulations, and

enforcing strict penalties where non-compliance is clearly evident.

Indeed, the reverse discrimination that appears to be applied

by Government agencies against Australian produced product

is also evident in the areas of import scrutiny and government

procurement. In particular, the FCJA contends that anti-dumping

provisions should be strengthened to transfer the onus of proof

to the importer rather than the local manufacturer, and Australian

Customs (or another appropriate Government agency) should

be properly resourced to ensure that product entering Australia

is properly classified to ensure it is subject to the requisite

tariff duties (too much product is being imported either falsely

classified to avoid duty or undervalued to minimise duty).

Moreover, government procurement officers, in assessing tenders

need to take account of the full impact of overall Government

Policy, as well as “whole of life” value assessment of the goods,

in the decision-making process. It is entirely appropriate that a

country with a high standard of living such as Australia should have

EXECUTIVE SUMMARY

demanding social, workplace, safety and environmental policies

in place. However, implementation of these policies imposes

significant costs on local industry and it is therefore inappropriate

for Government agencies to then purchase product from offshore

when it is simply cheaper because the same expectations have not

been placed on the offshore suppliers.

Finally, due to the fragmented nature of the industry and the

relative small size of the individual enterprises, effective Supply

Chain management is also a critical issue for the industry. To

help overcome the vulnerability induced by these industry

characteristics, strategies are necessary to encourage the industry

to collaborate more effectively together to improve the supply

chain relationships and to help enhance the industry’s profile and

sales on the global market.

To help implement the strategies identified in this Industry Plan,

to ultimately achieve the previously stated objectives, the FCJA

has determined a range of specific recommendations for both

the industry and government to pursue under each of the critical

success factors

and these are outlined in the FCJA Future Strategic Action

Steps at the conclusion of this document (Section 6). However,

it is important to recognise that this is an integrated set of

Recommendations and they should not be considered in isolation

of each other but should be implemented as a whole over time (of

course some are of more immediate need but the intention would

be for all the proposed Actions to be implemented within the next

two years).

x

7

1. industry vision

2. industry objectives

The Australian Furniture Cabinets and Joinery industry will be globally recognised as a vibrant, design

focussed industry sector, with world-class management, attracting the best workforce producing high

value add, professionally crafted, innovative furniture cabinet joinery products.

The Vision for the Industry is that within the next 10 years:

The prime objectives for the industry over the next 10 plus years are to:

Embrace Design and Innovation as a core characteristic for future growth

Maximise its share of the domestic market

Develop an Export Culture and progressively grow export markets

Capitalise on and adopt latest technological developments

Attract more highly skilled, highly trained workers

Embody the latest management practices, reflecting world’s best practice in business management

Be an integral player in the global FCJ supply chain

3. current state of the industry

The gross value of the Furniture and other Cabinet Making & Joinery (FCJ) industry in Australia is estimated at $32.8 billion in current prices. The furniture and furnishings component is estimated at around $25 billion or 76% of the total with Other Cabinet Making & Joinery accounting for the $7.8 billion balance. Furthermore, the door and window manufacturing industry is in itself a significant component of the FCJ sector, with an annual turnover of around $5.5 billion.

The ‘Furniture’ industry comprises all domestic and commercial free standing and built-in furniture.‘Other cabinet making & joinery’ includes wooden doors, roof trusses, wall and window frames, other wooden builders’ joinery and

carpentry, parquetry strips, other wooden industrial products and on-site installation.

The ‘door and window’ industry consists of firms that manufacture the following for the housing, residential and commercial sectors:

timber products such as framed window and doors, uPVC framed windows and doors

Imports declined by 7.6 per cent to $3.7 billion over 2011/12 while exports fell by 17 per cent to 0.2 billion

38 per cent of total imports were from China, with the next most significant sources being Malaysia (4 per cent), and then Vietnam, USA and Italy (3 per cent each). NB China accounts for 59 per cent of all Furniture imports into Australia and the estimated import share of total retail furniture turnover is 45 per cent, having increased from 36 per cent just 5 years ago

Of total FCJ exports around 13 per cent is exported to New Zealand, 5 per cent to USA, 3 per cent to Singapore and the rest being then spread across a wide range of countries.

architectural aluminium products such as doors, railings, partitions, window frames, aluminium framed windows, doors and shower screens,

Manufacturing revenue declined by 1.5 per cent over 2011/12 to $24.5 billion (in 2007/08 constant dollars, ie when adjusted for inflation) with the only growth sector of the industry being aluminium windows and doors manufacturing (indeed, the FCJ sector as a whole is still some 7.6 per cent below pre GFC levels)

Industry value added fell by 4 per cent over 2011/12 to $7.7 billion

Employment declined slightly (-0.4 per cent) over the year, to be just over 130,000 persons, while wages and salaries costs also declined marginally (by 0.6 per cent)

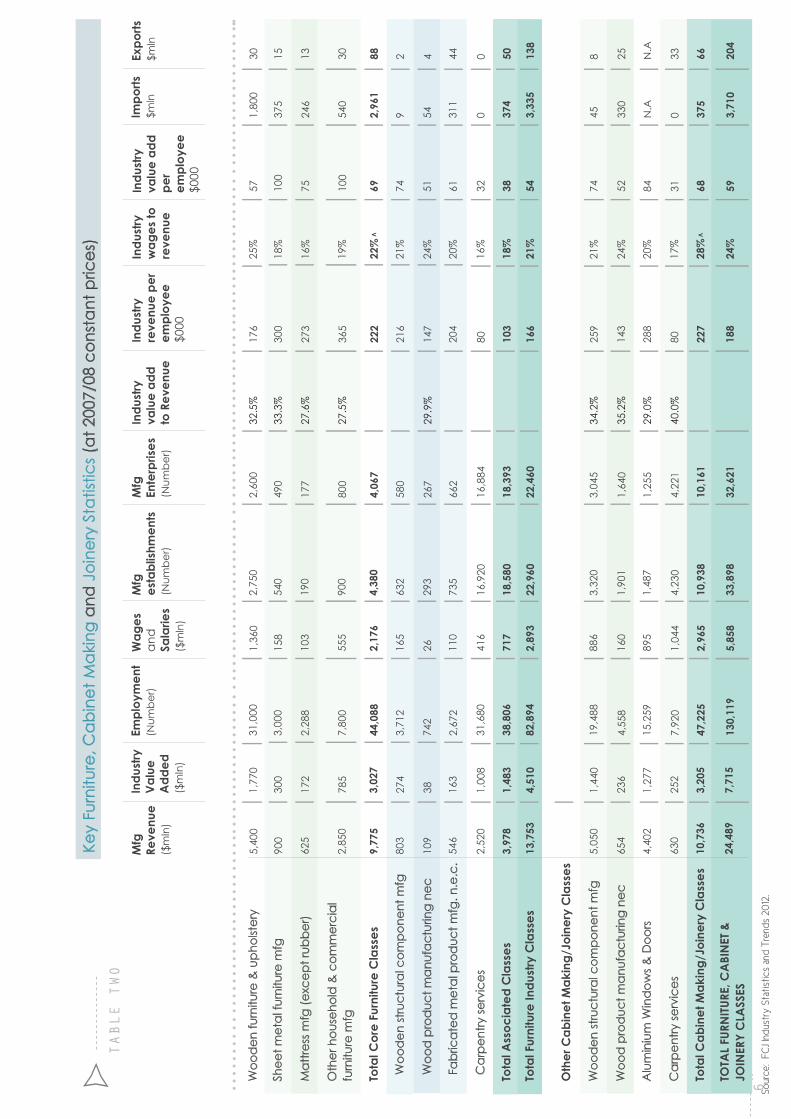

In addition a group of associated classes are also identified relating to soft furnishings such as carpets, cushions, curtains and drapes however these are separated from the other two sectors above and are not included in the coverage of this strategy document. The table on the following page provides a detailed break-up of the sector across a variety of indicators for 2011/12 with the main points being:

8

As a measure of productivity, industry value added per employee has fallen by 9.5 per cent over the five years to 2011/12, indicative of an industry that is struggling to gain productivity improvements

The number of manufacturing establishments grew marginally over 2011/12 (by 0.2 per cent), but it is still 3 per cent lower than 5 years earlier

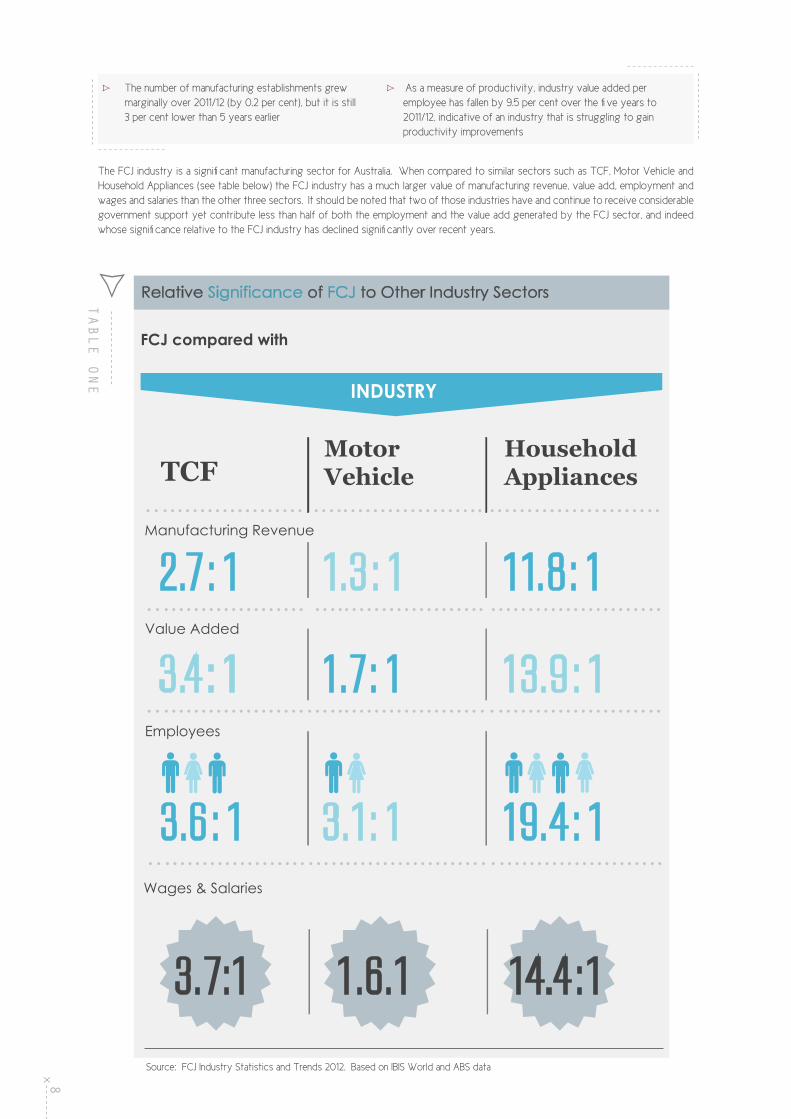

The FCJ industry is a significant manufacturing sector for Australia. When compared to similar sectors such as TCF, Motor Vehicle and Household Appliances (see table below) the FCJ industry has a much larger value of manufacturing revenue, value add, employment and wages and salaries than the other three sectors. It should be noted that two of those industries have and continue to receive considerable government support yet contribute less than half of both the employment and the value add generated by the FCJ sector, and indeed whose significance relative to the FCJ industry has declined significantly over recent years.

Relative Significance of FCJ to Other Industry Sectors

TCF Motor Vehicle

Household Appliances

FCJ compared with

Manufacturing Revenue

Value Added

Employees

Wages & Salaries

2.7 : 1 1.3 : 1 11.8 : 1

3.4 : 1 1.7: 1 13.9: 1

3.6 : 1 3.1: 1 19.4: 1

3.7:1 1.6.1 14.4:1

INDUSTRY

TABLE ONE

Source: FCJ Industry Statistics and Trends 2012. Based on IBIS World and ABS data

9

Mfg

Re

venu

e ($

mln

)

Indu

stry

Va

lue

Add

ed

($m

ln)

Empl

oym

ent

(Num

ber)

Wag

es

and

Sala

ries

($m

ln)

Mfg

es

tabl

ishm

ents

(Num

ber)

Mfg

En

terp

rises

(Num

ber)

Indu

stry

va

lue

add

to R

even

ue

Indu

stry

re

venu

e pe

r em

ploy

ee

$000

Indu

stry

w

ages

to

reve

nue

Indu

stry

va

lue

add

per

empl

oyee

$0

00

Impo

rts

$mln

Expo

rts

$mln

Woo

den

furn

iture

& u

phol

ster

y

Shee

t met

al fu

rnitu

re m

fg

Mat

tress

mfg

(exc

ept r

ubbe

r)

Oth

er h

ouse

hold

& c

omm

erci

al

furn

iture

mfg

Tota

l Cor

e Fu

rnitu

re C

lass

es

Woo

den

stru

ctur

al c

ompo

nent

mfg

Woo

d p

rod

uct m

anuf

actu

ring

nec

Fab

ricat

ed m

etal

pro

duc

t mfg

. n.e

.c.

Car

pent

ry se

rvic

es

Tota

l Ass

ocia

ted

Cla

sses

Tota

l Fur

nitu

re In

dust

ry C

lass

es

Oth

er C

abin

et M

akin

g/Jo

iner

y C

lass

es

Woo

den

stru

ctur

al c

ompo

nent

mfg

Woo

d p

rod

uct m

anuf

actu

ring

nec

Alu

min

ium

Win

dow

s & D

oors

Car

pent

ry se

rvic

es

Tota

l Cab

inet

Mak

ing/

Join

ery

Cla

sses

TOTA

L FU

RNITU

RE, C

ABI

NET

&

JOIN

ERY

CLA

SSES

5,40

0

900

625

2,85

0

9,77

5

803

109

546

2,52

0

3,97

8

13,7

53

5,05

0

654

4,40

2

630

10,7

36

24,4

89

1,77

0

300

172

785

3,02

7

274

38 163

1,00

8

1,48

3

4,51

0

1,44

0

236

1,27

7

252

3,20

5

7,71

5

31,0

00

3,00

0

2,28

8

7,80

0

44,0

88

3,71

2

742

2,67

2

31,6

80

38,8

06

82,8

94

19,4

88

4,55

8

15,2

59

7,92

0

47,2

25

130,

119

2,75

0

540

190

900

4,38

0

632

293

735

16,9

20

18,5

80

22,9

60

3,32

0

1,90

1

1,48

7

4,23

0

10,9

38

33,8

98

1,36

0

158

103

555

2,17

6

165

26 110

416

717

2,89

3

886

160

895

1,04

4

2,96

5

5,85

8

2,60

0

490

177

800

4,06

7

580

267

662

16,8

84

18,3

93

22,4

60

3,04

5

1,64

0

1,25

5

4,22

1

10,1

61

32,6

21

32.5

%

33.3

%

27.6

%

27.5

%

29.9

%

34.2

%

35.2

%

29.0

%

40.0

%

176

300

273

365

222

216

147

204

80 103

166

259

143

288

80 227

188

57 100

75 100

69 74 51 61 32 38 54 74 52 84 31 68 59

1,80

0

375

246

540

2,96

1

9 54 311

0 374

3,33

5

45 330

N.A

0 375

3,71

0

30 15 13 30 88 2 4 44 0 50 138

8 25 N.A

33 66 204

25%

18%

16%

19%

22%

^

21%

24%

20%

16%

18%

21%

21%

24%

20%

17%

28%

^

24%

Key

Furn

iture

, Ca

bin

et M

aki

ng a

nd J

oine

ry S

tatis

tics

(at 2

007/

08 c

onst

ant

pric

es)

TABLE TWO

Sour

ce:

FCJ

Ind

ustr

y S

tatis

tics

and

Tre

nds

2012

.

10

There are some businesses with genuine scale, as well as a substantial number with of a medium size featuring a high level of entrepreneurial

spirit and capacity to grow. However, the bulk of the sector is characterised by small businesses of the type that are the backbone of the

Australian economy and which collectively employ a significant number of people. Less than 1 per cent of FCJ businesses employ more

than 200 persons but the bulk of the industry employs less than 20 workers or no workers at all (sole proprietors). Such a large number

of sole proprietors and small businesses present both a challenge and opportunity for the FCJ sector.

On a geographical basis Chart 1 shows the distribution of FCJ manufacturing companies in Australia. Almost 80 per cent of establishments

are located on the Eastern Seaboard of Australia with some 60 per cent in the traditional manufacturing states of New South Wales and

Victoria. Western Australia accounts for 10 per cent and South Australia 7.3 per cent of all FCJ establishments. Both the ACT and NT

account for less than 3 per cent of total FCJ establishments in Australia.

QLD 22%

SA 6%

NSW 31%

WA 11%ACT 1%NT 1%

VIC 26%

TAS 2%

FCJ IndustriesEmployment by State

2

2%

6% 11% 31%

26%

Source: FCJ Industry statistics and trends 2012

CHART ONE

1

2

3

4

5

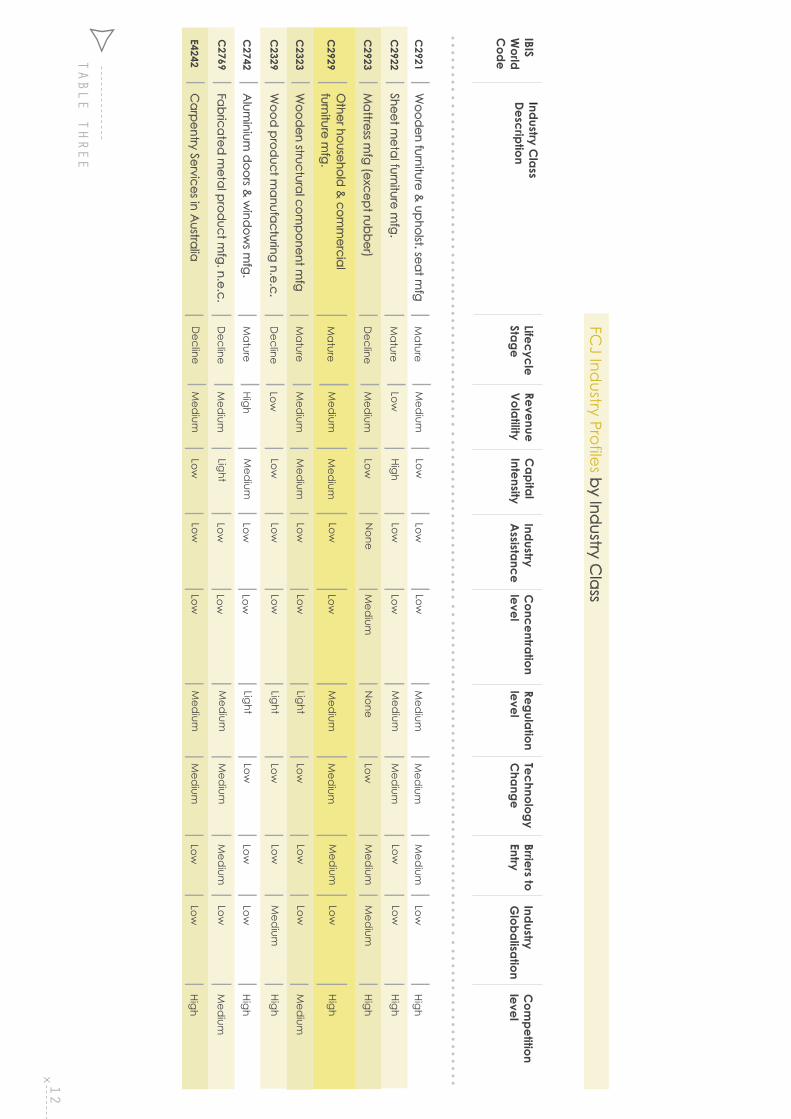

Like many Australian Industries the FCJ sector operates in an environment that is very different to that of many of the countries from

where imported product is sourced. Table 1 on the following page shows the profile of various FCJ industry sectors against a range of

measures highlighting that the industry:

Is a well-established, mature industry

Has low to no industry assistance

Encounters medium to low barriers to entry

Competes in a highly globalised industry confronted by significant low cost import competition

Is susceptible to revenue volatility.

Moreover, the key drivers for the bulk of FCJ product are highly vulnerable to changes in the overall economic environment. At the broad

level industry demand for products is a function of:

Consumer Sentiment and Confidence which are governed by

Household disposable income

Interest rates

Employment levels

Growth in the construction sector both residential and commercial

Commercial occupancy rates

Government expenditures (for those products related to common good services and sectors, hospitals, community centres etc.)

11

While these problems are largely faced by many industries, they are crucial factors for the FCJ industries and are an important consideration

in determining future strategic directions (and policies) for the sector.

The industry has been unstable over the past five years. Even prior to the onset of the global economic downturn, the industry had its

share of woes. Rising interest rates curtailed residential housing demand and domestic operators faced rapidly rising import competition

from low-cost producers such as China. Aggressive price discounting coupled with muted demand conditions saw industry profitability

decline considerably as domestic manufacturers could not compete with their overseas counterparts. The collapse of the housing market

and the start of the global financial crisis effectively crippled demand from construction markets, the door, window and joinery industry’s

primary sources of revenue. Revenue will recover as construction activity increases

According to the IBISWorld life cycle model, the industry is in a mature stage of its economic life cycle. Indicators of this phase include

slow growth in establishment numbers and domestic demand, and a slowdown in technological investments and product innovation. The

industry’s products, and associated technology used in production, are well established.

These are however factors that are not necessarily impossible to overcome, as evidenced by the situation in Germany and the performance

of its ‘Mittelstand’ during the Global Financial Crisis. Whereas the Australian economy was able to hold back the impacts of the GFC due

to its large endowment of natural resources the German economy also emerged in much better shape relative to the majority of European

countries.

Instead a core component of Germany’s success is placed at the feet of a group of enterprises known as the Mittelstand, which have the

following characteristics:

The success of the Mittelstand is their focus on international excellence in niche markets where they can maintain strong market positions.

Their value is obtained through offering superior value that cannot be readily or easily matched by low cost producers.

To do this they invest heavily in R&D and continuous improvement of both their products and processes. Their production networks are

closely linked to their R&D and they maintain close contact with their customers, suppliers and employees – the latter via a bottom-up

management style.

Furthermore, these Mittelstand enterprises account for 83 per cent of all apprenticeships in Germany.

When the Australian experience is examined it shows a much larger number of micro-businesses which employ very few, if any, staff and

thus the Australian Mittelstand accounts for only 3.7 per cent of all businesses in the economy. As a result Australia does not have the significant economic boost that a vibrant mid-sized business sector has nor does it allow the industry to capitalise on the R&D strengths in Australia. However, it is these characteristics that are the key to the ongoing development of manufacturing in Australia.

Thus the solution to developing a strong Australian FCJ sector, drawing on the observations of the German Mittelstand, include:

Typically employ between 10 and 250 workers

Have turnovers of between $2.6 million to $64.9 million

Account for 26 per cent of all manufacturing firms in Germany

Employ around 42 per cent of the workforce

Contribute around 35 per cent of value adding

Over 70% are family owned and located in smaller cities or regional towns

Adoption and development of management systems not typically suited to small businesses

Support by Governments for programs targeted at the < 100 employee sector in Australia rather than the large companies or micro-businesses

Consideration in broader policy development including taxation and environmental policy of the impacts to these currently micro to small sized businesses.

The strategies outlined in the remainder of this document are considered critical by the FCJ to the successful transition of the Furniture,

Cabinet Making and Joinery industry to a similar model of ongoing growth and success.

x

12

Lifecycle Stage

Revenue Volatility

Capital

IntensityIndustry A

ssistanceC

oncentration level

Regulation level

Technology C

hangeBrriers to Entry

Industry G

lobalisationC

ompetition

levelIBIS W

orld C

ode

Wood

en furniture & upholst. seat m

fg

Sheet metal furniture m

fg.

Mattress m

fg (except rubber)

Other household

& com

mercial

furniture mfg.

Wood

en structural component m

fg

Wood

product m

anufacturing n.e.c.

Alum

inium d

oors & w

indow

s mfg.

Fabricated m

etal product m

fg. n.e.c.

Carpentry Services in A

ustralia

Mature

Mature

Decline

Mature

Mature

Decline

Mature

Decline

Decline

Med

ium

Low

Med

ium

Med

ium

Med

ium

Low

High

Med

ium

Med

ium

Low

High

Low

Med

ium

Med

ium

Low

Med

ium

Light

Low

Low

Low

Med

ium

Low

Low

Low

Low

Low

Low

Low

Low

None

Low

Low

Low

Low

Low

Low

Med

ium

Med

ium

None

Med

ium

Light

Light

Light

Med

ium

Med

ium

Med

ium

Med

ium

Low

Med

ium

Low

Low

Low

Med

ium

Med

ium

Med

ium

Low

Med

ium

Med

ium

Low

Low

Low

Med

ium

Low

Low

Low

Med

ium

Low

Low

Med

ium

Low

Low

Low

High

High

High

High

Med

ium

High

High

Med

ium

High

C2921

C2922

C2923

C2929

C2323

C2329

C2742

C2769

E4242

FCJ Ind

ustry Profiles by Ind

ustry Cla

ss

Industry Class

Description

TABLE THREE

13

design and innovation

Given the relatively high cost of labour in Australia, quality design

has to be one of the differentiators that enable our industries to

compete with imports. The industry must develop a greater focus

on design and innovation, to the point where it becomes globally

recognised as epitomising an inherent design culture. In this way,

it can expand beyond the domestic market and build potential sales

and genuine value in targeting niche export markets.

Australia’s furnishing cabinet and joinery industries have some

outstanding designers, but they are not well known and the practice

of great design is not widely promoted within the industry. For

instance one Australian based designer has noted that he has not

worked with Australian manufacturers for over 15 years despite

being in constant demand by overseas manufacturers.

A core issue that the industry needs to overcome is the resistance

to adopting design and innovation as complementary terms.

Currently much of the industry sees innovation only in the sense of

inherent functionality and/or process improvement, with no role for

design. However as overseas FCJ industries and other Australian

manufacturing industries such as automotive and TCF have shown,

design needs to become integral to innovation, and of course

design transcends beyond just product design.

There are numerous examples within the furniture industry of

companies benefiting from a focus on design and innovation. It

is readily apparent that as customers become more educated and

demanding of good design and quality products that meet their

specific need, the FCJ industry must adapt accordingly.

To do this companies are employing a variety of techniques to

engage consumers. Herman Miller for instance is focusing on the

issues around what the home office should look like when iPads,

other tablets and notebooks have freed people to work anywhere

– ie. will people still seek to work at desks or will the couch, kitchen

critical success factorsThe problems faced by Australia in competing in a global FCJ market have been outlined above. As evidenced by the German Mittelstand experience, the current structure of the FCJ industry can become a strength for Australia through a focus

on design and innovation, skills and training and the supply chain.

table or balcony become the new office and what furniture will be

required? The company is focused on not just adding technology

on top of an existing product but building it in as a fundamental part

of the product.

Indeed, there are numerous examples where furniture has been

designed to incorporate new technologies, eg. the iCon Bed (Hollandia)

with docking stations for two iPads, speakers and amplifier or the

Fluer de Noyer chest of drawers (Think Fabricate) which features an

in-built charging station for electronic devices.

In many ways this process is not new and has been successfully

implemented time and time again by the electronics industry who

have utilised Bluetooth, wireless internet connections and complete

interactivity with the user to sell TV’s, cars, stereos and household

appliances. The furnishing industry is in a prime position to capitalise

on this convergence of technologies.

It is not unusual for overseas companies, particularly in Europe and

the United States to collaborate with a well-known designer on the

development of a product where the designers name and reputation

is core to the product being sold. The designer enables the company

to engage with the new more aware and savvy consumer seeking

products which meet their lifestyles.

The potential of this partnering is perhaps best illustrated by the

success of Danish furniture manufacturer Carl Hansen & Son. As

highlighted in the Case Study outlined below, after establishing a

reputation for high quality craftsmanship making bespoke furniture

the company engaged a designer Hans Wegner. Through this

collaboration over the 1950’s and 1960’s Wegner designed furniture

radically different to anything on the market including the ‘wishbone

chair’ which has been on the market since its inception. Incumbent in

the designs was a high level of complexity that required exceptional

craftsmanship which Carl Hansen & Son could provide.

4.1

4.

14

case study carl hansen & son denmark

Established in Odense on the island of Funen (located between Jutland and Zealand) in 1908.

Developed a reputation for high quality craftsmanship making bespoke furniture.

Gradually began to produce a small range of its most popular pieces.

These pieces along with fine craftsmanship became the company’s hallmark.

In the 1940s started to use a designer.

In the late 1940s a number of Danish furniture designers were gaining prominence.

From these designers they took a chance on Hans Wegner, a relatively unknown designer.

The company flourished on the back Wegner’s designs.

These designs were radically different to anything

on the market and were very complex and difficult

to manufacture – they demanded very high level

craftsmanship.

These designs included the ‘wishbone chair’ which has been on the market uninterrupted ever since.

The wishbone chair proved especially challenging – it back rail was steam bent and rear legs required turning by a contact turner.

Until that time chair seats were woven with reed, in the wishbone chair paper cord (developed during the war for use in grain binders in Sweden) was used.

Manufacturing furniture with such novel designs that were very difficult to make presented a big risk for the company. The furniture was not an immediate hit in the market place.

In 1951 Carl Hansen (and Wegner) and a number of other Danish furniture manufacturers formed a consortium called SALESCO, a sales and marketing company that promoted Wegner’s designs in Denmark and overseas and played a role in establishing Denmark’s distinct furniture design image.

In 2001 Knud Erik Hansen Carl Hansen’s grandson, took over as Managing Director.

Today the company continues to release ‘new’ Wegner designs.

This shows that the Danish furniture businesses have been extremely good at capitalising on, and selling products from the ‘golden age’ of Danish furniture, the 1950s.

While the company has developed new designs over its lifetime the most popular continue to be Wegner’s designs and the company

continues to produce them 40 to 50 years after their initial development. The level of complexity inherent in the design has also meant

that while copies have been created by low cost countries they cannot match the quality and standards of the original and it is the latter

inherent craftsmanship that consumers will pay a premium for.

Schiavello (see details in the following Case Study) is an excellent example of a company which has focused on developing leading edge

products and service which are both durable and functional and beautiful. They appeal to a consumer’s desire to have furnishings that

represent their particular lifestyle. To achieve this reputation and track record it has partnered with Australian and international designers

to create a large range of furniture.

case study schiavello market growth through design and innovation

Schiavello is an Australian based international company

founded in 1966 on the principles of innovation, quality and

service experience. Its aim is to be seen as an organisation

where intelligent design ranks as highly as the built quality of

our products.

Schiavello provides a fully integrated approach to dealing

with clients incorporating a broad product mix with design,

construction, fit out and specialty consulting service. It

employs over 1200 skilled employees and has sales offices

across the globe with manufacturing located in Australia.

With an accomplished team of industrial and furniture

designers, and mechanical engineers, working with advanced

software programs and Engineering/Stress Analysis

technology they design, prototype, test and build products.

Increasingly, the company works with Australian and

international designers to keep themselves at the leading-

edge of product and services design; to create products

that are not only strong and durable and functional, but

beautiful, too: products with high design values, that

you want to be around and have around, as much for the

pleasure they provide consumers as for their comfort and

practicality.

Another good example of triggering an emotive connection with the consumer is Pacific Green furniture, which has embraced a strong

environmental focus for the creation of its Palmwood as an ecologically sustainable timber alternative. Utilising new technology they

created a durable consumer orientated product suitable for a variety of climates and resistant to wood boring insects. The company’s

employment of indigenous designers and process workers delivers additional benefits to local communities in Fiji while its recycling

of palm trees provides it with a product attractive to those consumers concerned about logging and forestry processes including the

resultant impact on indigenous populations and other land users.

15

case study pacific green furniture design and innovation to produce environmental solutions

Development of hardwood substitutes: Palmwood was the

name Pacific Green gave to the finished ‘hardwood’ material

it developed. Process breakthroughs had created a durable

consumer-oriented product that was suitable in a variety of

climates and resilient to wood-boring insects. Palmwood is an

ecologically-sustainable timber alternative.

Indigenous design: Each piece is handcrafted by artisans using

traditional techniques and is designed to give a sense of its

global ethnic origins.

Socially-responsible manufacturing: Pacific Green pioneered

the creation of a socially-responsible industry for the Pacific

region. By recycling unproductive coconut palms, old plantation

land was returned to the local villages to replant with young

fruit-bearing palms and other cash crops. The factory was built

in consultation with the surrounding villages, and the land used

was leased from the villagers to respect local ownership. Pacific

Green Industries (Fiji) Limited is listed on the South Pacific Stock

Exchange and its majority owners are the Fijian people.

Manufacturing processes use no toxins or chemicals and by-

products are reused. In 2001, Pacific Green addressed the United

Nations Conference on Trade and Development (UNCTAD) on

the social responsibility of manufacturing companies. Pacific

Green also advised the United Nations Food and Agriculture

Organization on its study on Coconut Palm Stems[4]. From

the mid-1990s to early-2000s, actor Pierce Brosnan was the

company’s Environmental Spokesperson.

As a result, Pacific Green was invited to participate at the World

Expo 2010 within the Pacific Pavilion[5].

Pacific Green unveiled the Indigenous Masterpieces concept at

its debut in Milan’s Salone del Mobile in 2011.

While it is critical for the FCJ industry to invest in new design and innovation it must overcome its exceptionally low historical spend

in respect of R&D compared to other industries. The ABS reports that in 2009-10 the furniture and other manufacturing sector spent

$30.6 million on business R&D. This accounted for less than one per cent of total business R&D expenditure and was the lowest of the

15 ANZSIC subdivisions included in the table. On the positive side this expenditure was 31 per cent higher than business R&D spend in

2007-08.

The “furniture and other” manufacturing sector also appears to be one of the least likely sectors to adopt the latest technologies,

spending only an estimated $170 million ( viz. one per cent of total business capital expenditure) in 2009-10 representing a 55 per cent

reduction in its level of capital expenditure (although there is a significantly high standard error in the estimates).

16

regulatory and compliance

exchange rate

import standards

Clearly, government action (or inaction) can have significant impact on an industry and an economy overall. This section addresses the

issues identified by the FCJ sector in the areas where government regulation and consequent manner of enforcement can skew the relative

competitiveness of the local industry...

In many of the countries which compete with Australian FCJ products, manufacturers do not face the same levels of regulation, receive

greater industry assistance (directly or indirectly) including for many high tariff or other trade barriers to entry (even given the concessions

through many of Australia’s FTA’s – some of which are still several years away from parity).

These issues are compounded by:

A consistently high Australian dollar and the advantages

it provides to importers

Thus the industry’s ability to compete effectively against imports into the Australian market but also to secure market share in export

markets is severely limited. This is particularly the case when it is considered that on average across all sectors of FCJ over 75 per cent

of costs are related to raw material purchases and labour costs.

A complex and multiple taxation system across state and national governments

The Australian Dollar is being influenced by the strength of the domestic resources sector and this is seriously impacting on the international

competitiveness of other sectors of the Australian economy, including the furniture, cabinet and joinery industries.

While Australia has a deregulated currency, other countries still manipulate their currencies to certain extents. China has a deliberate policy

to hold down the value of the Renminbi (Yuan). The US also is prepared to “influence” its currency, and even Switzerland recently capped

the Swiss Franc to maintain its relativity with the Euro. The circumstances that led to the floating of the Australian Dollar have changed,

and there needs to be recognition of the adverse effect this is having on the traded goods sectors.

It is important to recognise that this is the prevailing market environment confronting the Australian industry. The FCJA is not necessarily

seeking any change to Australia’s exchange rate policy, simply highlighting that other countries who are a significant source of imports

do not operate a “free trade” currency.

This high and sustained level of the Australian dollar has exaggerated the deficiencies and problems of the FCJ industry bringing the

industry to the critical turning point it currently finds itself in. While the FCJ industry accepts that neither it nor governments can influence

the exchange rate, measures can be taken to help the industry restructure to help overcome resultant ramifications for the industry’s

overall international competitiveness.

A vital step is that every action possible be taken to ensure no unfair competition is imposed on the domestic industry. The remainder of

this Section addresses such issues which still need to be remedied.

Imported FCJ products are sold in the marketplace in competition with Australian made product in a deceptive manner, ie. not fit for

purpose, including for example:

cyclonic rated doors and windows which do not meet the

requisite quality or safety standards, non HMR kitchen,

bathroom and laundry cabinetry, etc.

in the Kitchens market, importers offer neither the length nor

comprehensive nature of the warranties enforced on

Australian made product.

The impact of products that are not up to Australian quality standards was clearly demonstrated in May 2012 with the collapse of St Hilliers,

a significant construction company in Australia (see CFMEU Report below). The collapse was bought on, amongst other things, through

the use of imported windows and doors which arrived on site but to wrong sizes and inferior specifications. This stalled development of

the Ararat prison site and prevented St Hilliers making payments to contractors and workers. This subsequently led to the company going

into receivership, contractors and labourers being put out of work and a stop to construction at the site.

Imports that do not comply with either standards or

the reasonable expectations of Australian consumers, eg

formaldehyde (a carcinogen) in board product, safety

glass that is dangerously below standard, etc

4.2

4.2

.14

.2.2

17

As reported by the CFMEU on Wednesday 17th May 2012.

imported windows behind ararat prison site closure

The crisis that has brought the Ararat prison site to a halt was

caused by faulty windows and doors imported from China.

Subcontractors withdrew their workers last week after learning

builder St Hilliers was unable to pay outstanding bills. The

company has now been placed in administration as a result of

losses arising on the job.

Hundreds of windows and doors manufactured in China arrived

on site cut to wrong sizes, making them useless. Some have

been sent back while others are lying around in packing cases on

the now idle site.

The folly of importing building components has again been

exposed and Victoria looks set to pay a heavy price. Local

manufacturing jobs have been sacrificed, building workers have

been tipped out of work and at some stage the state will have

to find the money to get the project going again.

The FCJ industry agrees with the CFMEU that the use of Australian made product, which must be tested to show it conforms to

BCA requirements, would have prevented this issue from arising in the first place. The use of fraudulent SAI Global stickers and direct

approaches by importers to building sites is a core regulatory issue that the industry and government must address.

Another related issue is that imported FCJ products are allowed to claim they are “Australia Made” or infer they are Australian by semantics,

suggesting that the country of origin laws need to be strengthened or better enforced by the ACCC and more broadly the industry. The

industry is speaking with the Australian Made campaign and groups such as Choice to work on opportunities to better raise awareness of

consumers to the differences between Australian made and imported products.

18

Much of the imported product that enters Australia, especially from

China is clearly dumped, often landing at prices for finished product

that is well below the world price for the core material inputs. This

puts unfair pressure on the local industry and measures need to

be implemented that enable the Australian industry to take more

effective action against dumping.

In addition to ensuring that Australia’s anti-dumping regime is

sufficient to protect the industry a greater focus is needed to

ensure that imported products are not circumventing duties both

through legitimate means and illegitimate means.

In respect to the former the industry seeks a review of the current

products allowed tariff free entry into Australia via policy-by-laws

and tariff concession orders. While many may be legitimate and

necessary, a whole of industry review will ensure that Australian

manufacturers are not being adversely affected particularly where

anti-dumping legislationand duting avoidance

excessive tax imposts on australian manufacturers

Australian manufacturers are subjected to a myriad of additional

taxes that add to their cost structure, while importers are not

subjected to this same degree of impost and thus have an

immediate advantage over the local industry.

This is evidenced by:

Various overseas tax comparison documents

proving Australia’s comparatively high overall tax structure

Payroll tax

Land Tax

Low depreciation allowances

The introduction of the Carbon Price policy is a further concern

for the industry through its potential to further erode the relative

competitiveness of the local industry, for questionable impact

on climate change. While there will be an impact on furniture

manufacturers through higher costs due to increasing energy

prices the bigger concern for the industry is the impact on wood

processors. The Engineered Wood Processors Product Association

of Australia released advice in May 2012 noting that many wood

processors had begun winding back production, mothballing

equipment and moving to three day weeks in order to cope with

the impact of the carbon price. One wood processor indicated

that their costs in energy alone would increase by $1 million before

any cost of emissions is taken into account.

If this was to occur the loss in supply of processed wood products

to other parts of the FCJ supply chain creates an environment

where Australian manufacturers are forced to source material off-

shore and potentially without the quality, fitness for purpose and

short supply times currently provided by local suppliers.

While the estimates of additional costs caused by the Carbon

Tax may seem low at a glance at around 1%, that 1% represents a

large proportion of the nett profit on sales currently experienced

by many businesses. Particularly in domestic furniture the nett

profits on sales is commonly below 5%, an unsustainable level

in manufacturing businesses. These businesses must have the

capacity to reinvest capital to buy more productive machinery to

survive in the longer term. For many business that 1% may be ½ to a

1/3 of their net profit, if indeed they are making money at all. Many

businesses have become unprofitable in the past six months with

sales falling precipitously as consumer confidence has plummeted

to GFC like levels.

The FCJ sector believes that the carbon tax is very likely to impact

the industry both in sales and increased cost due to:

The structure of the sector in Australia

Increasing import penetration into the market for FCJ products

An inability to fully pass through all cost rises

The exact impact is heavily dependent on a number of factors

external to the industry including:

The extent and availability of international permits

The actions of households and other sectors of the economy

to the carbon tax

The actions of other countries and the impact on their

domestic FCJ industries

Overall domestic and international conditions

The Clean Technology Investment Program (CTIP) and the push

from environmental groups such as Planet Arc to increase the

use of wood as a construction material given its carbon storage

benefits are unlikely to provide offset to the increased costs being

faced by more than a few business due to the current SME nature

of much of the industry (especially given the Government’s recent

action to “pause” grants under certain programs, including the CTP,

which further undermines investor confidence and creates further

uncertainty about the Government’s true commitment to industry

development in Australia).

advances or technological change in local production processes

and availability of raw materials may now make Australian

production feasible whereas in the past it may not have been

possible/economic..

There does remain however, clear evidence that a large number of

products are bypassing the 5 per cent tariff rate through deliberate

undervaluation and misclassification. While this is presumably

an issue for all industries, the FCJ sector advocates increased

funding to enable customs officers (or an appropriate alternative

government agency) to police and enforce with punitive penalties

those operators deliberately avoiding duty and competing unfairly

with Australian producers. The increased revenue generated by

ensuring importers actually pay the legislated rate of duty will more

than cover the increased resources needed to monitor and police

these provisions.

4.2

.44

.2.3

19

20

australia’s regulatory framework

Reflecting its developed nature, high standard of living, well developed labour market and high social awareness, Australia has in place a

range of regulations, codes and laws necessary to provide protection to employees, consumers and the general public. The FCJ industry

supports the need for these regulations and codes however asks that the Government acknowledge much of the competing product

entering Australia is made in countries which do not have the same levels of regulations and codes.

For example, commercial furniture manufacturers cannot compete with countries which have virtually no environment and safety regulation

and policies and thus companies operating in them need not invest in capital and processes to prevent this occurring. Likewise, less

stringent labour laws and employee protections – such as annual leave, superannuation etc. – place Australian producers at a competitive

disadvantage to these countries.

While the industry acknowledges that the Australian Government cannot actively change the rules and regulation of another sovereign

government it does have the power to implement policies which apply the same level of standards for imported product, to those

expected of Australian manufacturers. The most notable are through Australia’s custom legislation and processes, building codes,

standards and government procurement (the latter is covered in section 6 below while the first was covered above).

The example of St Hilliers and the problems of using non-compliant and non-tested products in the Australian market is just one of

several examples, noted by the CFMEU and other industry stakeholders. These products are entering Australia by circumventing existing

standards and building codes due to poor enforcement and poor education of those making purchasing decisions. This is to the detriment

of local producers (and ultimately to the detriment of the Australian consumer).

Another well publicised example is the continuing issue with glass top tables exploding, seemingly spontaneously. Despite this problem

being identified since the late 2000’s products continue to be purchased in Australia which experience the same problem. Clearly this

points to a lack of enforcement or control on the standards of these products entering Australia.

While changes have been made to the Building Code of Australia to clause B 1.4(h)(iii) ‘Nickel Sulphide Clause’ requiring heat soak testing of

toughened and heat strengthened glass before it can be used, the FCJ is not aware of any changes to standards in regards to glass used

in furniture applications. As late as June 2011, tables are still exploding in Australia1 and overseas.

The local Australian manufacturer is subjected to significant additional costs in order to meet the numerous product standards and

building codes. Yet clearly there is a lack of enforcement of these standards in the end consumer markets as evidenced by the continuing

influx of inferior products into the Australian market.

The FCJ is seeking to work with the CFMEU, Industry aligned groups (HIA, MBA etc.), Consumer aligned groups (Choice, Planet Ark),

governments and opposition parties to ensure that those responsible for consumer safety are actively policing these codes and policies.

This includes building inspectors and surveyors and the ACCC where breaches of the Trade Practices Act occur.

1 ‘Exploding table shocks owners’, Fraser Coast Chronicle. http://www.frasercoastchronicle.com.au/story/2011/06/06/chemicals-cause-exploding-table-shocking-owners/ Last accessed 19 August 2012.

4.2

.5

21

government procurement practices

surety of supply of raw materials

Government procurement policies should recognise the full value of local manufacture to government. This is not a call for special

treatment but a commercial argument that all aspects, outside of mere invoice price, must be taken into consideration – and ideally written

into government policy - to ensure that Australian companies are being treated on a true “like-for-like” basis in government purchasing

decisions.

For example, Australian industry is making huge in-roads on environmental savings and sustainable development. This too should be a

factor taken into account in government procurement decisions. That is, Government Buyers should have an ethical purchasing policy – ie

everyone that Government purchases from, should comply with similar conditions to what is expected of Australian industry.

Moreover, it needs to be recognised, and publicly acknowledged, that there is an inherent strategic value in nurturing local capabilities.

Government Procurement can drive innovation and industry growth – but to do so, it must be prepared to reward the effort made

by industry, by giving preference to firms that can demonstrate that they are actively, and productively, pursuing all these areas of

desirable industry development in Australia. Otherwise Australia risks losing these capabilities from a domestic base, which in turn means

Government will be reliant on being suitably supplied through other suppliers – ie imports - through which it will have little control.

A proper assessment of true value must take into account the full economic impact, including an assessment of the “whole of life” value,

of local production in any ‘cost comparison’ with overseas purchased product. This should include an assessment of tax effects derived

through domestic business (GST, income tax collected from locally employed manufacturing staff, corporate tax, etc) and economic

multipliers, particularly for regional communities. A value must also be allocated (if not a requirement set) for firms abiding by Australian

standards with regards to workplace practices, environmental standards, community support, labelling (ie accuracy and adherence in

meeting stated country of origin, fibre content, care instructions statements), etc.

Significant product is imported into Australia containing timber product that has been illegally sourced, as evidenced by Federal

Government recognition in illegal logging proposals.

FCJ industries in Australia face challenges to guaranteed supply of raw timber material due to out-dated environmental concerns, water

allocations, and other issues. This has a significant bearing on effective resource allocation and the long term sustainability of the industry.

This challenge is compounded by the actions of groups such as “No Harvey No” campaign whose attack on Harvey Norman for selling

products using Australian Timber runs contrary to sustaining a viable Australian orientated furniture manufacturing industry. This and other

campaigns are based on a misrepresentation of “forest destruction” and often include gross distortions of the true facts. For example

Market for Change stated that 76% of Australia’s forest and wood lands could be logged when ABARES statistics show that only around

6% of Australian forests are used for logging, and that figure could not ever change upwards to a significant degree.

4.2

.64

.2.7

22

Campaigns like “No Harvey No” are most likely to drive consumers

to purchase products not made from Australian timber and thus

potentially made offshore and with less controls and less focus

on sustainable forestry practices. The FCJ industry welcomes the

warning by the Federal Government on the longer term impacts of

such a campaign to the broader furniture and construction supply

chain.

FCJA notes and applauds the action taken by Senator Kim Carr

in early 2012, whose intervention was crucial in persuading Get

Up to at least temporarily drop their support of the No Harvey

No campaign. This was an excellent demonstration of how a

government can be effective by simply and publically stating the

actual facts.

The FCJ welcomes the passage of the “Illegal Logging Prohibition Bill

2011” through Parliament and the regulations, penalties and tools it

will provide to identify and prosecute products from illegal logging.

However, there remains more work to ensure that the regulations

are not manipulated or abused. Consultation is also critical with

the FCJ industry on the development of both the prohibited and

regulated lists under the legislation.

Complementary to the need to punish the use of illegal logged

wood and wood products is the need for a focus on encouraging

and maintaining sustainable wood resources from both private and

public forests throughout Australia. Ensuring a domestic supply

of sustainable timber, which can be monitored, provides assurance

to consumers and NGO’s while also offering strong domestic

alternatives for producers of wood based products.

Strict monitoring of domestic wood sources in addition to

restrictions on illegally logged products will also assist in addressing

the miscommunication and misunderstanding of NGO’s and other

groups as to the real impact of the industry. While the FCJ sector

supports for the large part the role of NGO’s in identifying problems

and issues it does remain concerned at some of the ill-researched

and mis-guided statements that have been made in respect of the

furnishing industry such as that of the No Harvey No campaign. A

strong and transparent supply chain and domestic logging industry

will address this issue.

There are positive activities as well that the industry seeks to

foster and would seek government support. These include the

push by Planet Ark to encourage consumers to look at wood

based products as a store of carbon. Equally the focus by steel

manufacturers on environmental improvements and investment

in new materials and production processes also requires ongoing

encouragement.

As an example of these positive activities, the Case Study on

the opposite page shows the approach of Sealy to working with

its supply chain to produce high quality, durable products which

meet the performance needs of consumers. However, through a

pro-active approach to work with its suppliers it is also minimising

the environmental footprint of its products and delivering what

has become an increasingly important product characteristic for

consumers – environmental sustainability.

23

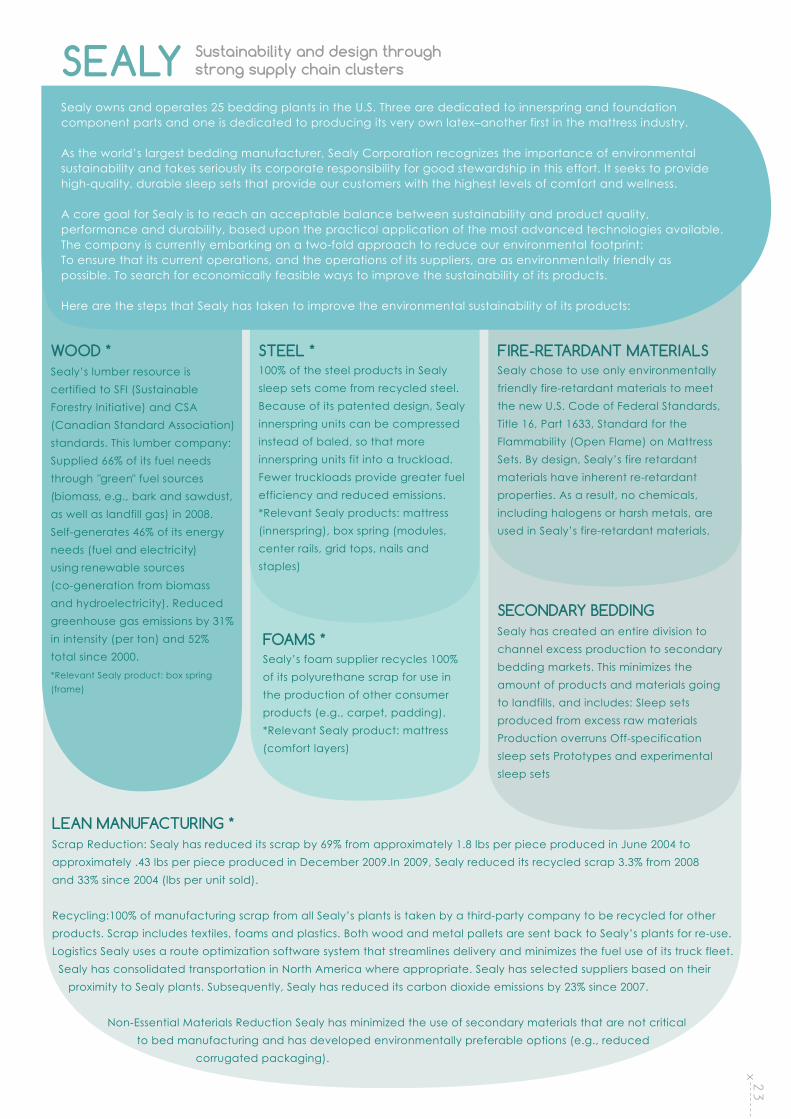

SEALY Sustainability and design through strong supply chain clusters

Sealy owns and operates 25 bedding plants in the U.S. Three are dedicated to innerspring and foundation component parts and one is dedicated to producing its very own latex–another first in the mattress industry.

As the world’s largest bedding manufacturer, Sealy Corporation recognizes the importance of environmental sustainability and takes seriously its corporate responsibility for good stewardship in this effort. It seeks to provide high-quality, durable sleep sets that provide our customers with the highest levels of comfort and wellness.

A core goal for Sealy is to reach an acceptable balance between sustainability and product quality, performance and durability, based upon the practical application of the most advanced technologies available. The company is currently embarking on a two-fold approach to reduce our environmental footprint: To ensure that its current operations, and the operations of its suppliers, are as environmentally friendly as possible. To search for economically feasible ways to improve the sustainability of its products.

Here are the steps that Sealy has taken to improve the environmental sustainability of its products:

WOOD *Sealy’s lumber resource is certified to SFI (Sustainable Forestry Initiative) and CSA (Canadian Standard Association) standards. This lumber company: Supplied 66% of its fuel needs through "green" fuel sources (biomass, e.g., bark and sawdust, as well as landfill gas) in 2008. Self-generates 46% of its energy needs (fuel and electricity) using renewable sources (co-generation from biomass and hydroelectricity). Reduced greenhouse gas emissions by 31% in intensity (per ton) and 52% total since 2000.*Relevant Sealy product: box spring (frame)

STEEL *100% of the steel products in Sealy sleep sets come from recycled steel. Because of its patented design, Sealy innerspring units can be compressed instead of baled, so that more innerspring units fit into a truckload. Fewer truckloads provide greater fuel efficiency and reduced emissions.*Relevant Sealy products: mattress (innerspring), box spring (modules, center rails, grid tops, nails and staples)

FOAMS *Sealy’s foam supplier recycles 100% of its polyurethane scrap for use in the production of other consumer products (e.g., carpet, padding).*Relevant Sealy product: mattress (comfort layers)

LEAN MANUFACTURING *Scrap Reduction: Sealy has reduced its scrap by 69% from approximately 1.8 lbs per piece produced in June 2004 to approximately .43 lbs per piece produced in December 2009.In 2009, Sealy reduced its recycled scrap 3.3% from 2008 and 33% since 2004 (lbs per unit sold).

Recycling:100% of manufacturing scrap from all Sealy’s plants is taken by a third-party company to be recycled for other products. Scrap includes textiles, foams and plastics. Both wood and metal pallets are sent back to Sealy’s plants for re-use.Logistics Sealy uses a route optimization software system that streamlines delivery and minimizes the fuel use of its truck fleet. Sealy has consolidated transportation in North America where appropriate. Sealy has selected suppliers based on their proximity to Sealy plants. Subsequently, Sealy has reduced its carbon dioxide emissions by 23% since 2007.

Non-Essential Materials Reduction Sealy has minimized the use of secondary materials that are not critical to bed manufacturing and has developed environmentally preferable options (e.g., reduced corrugated packaging).

FIRE-RETARDANT MATERIALSSealy chose to use only environmentally friendly fire-retardant materials to meet the new U.S. Code of Federal Standards, Title 16, Part 1633, Standard for the Flammability (Open Flame) on Mattress Sets. By design, Sealy’s fire retardant materials have inherent re-retardant properties. As a result, no chemicals, including halogens or harsh metals, are used in Sealy’s fire-retardant materials.

SECONDARY BEDDINGSealy has created an entire division to channel excess production to secondary bedding markets. This minimizes the amount of products and materials going to landfills, and includes: Sleep sets produced from excess raw materials Production overruns Off-specification sleep sets Prototypes and experimental sleep sets

24

labour, skills and training 4.3

There is a profound shortage of skilled workers across all parts of the FCJ industry as identified in the following Table:

As Table 3 shows the range of occupations in the FCJ sector are for

the large part applicable across a range of manufacturing sectors

and the skill sets are very similar. As such the FCJ industry is not

just competing amongst itself for workers but also with other

manufacturing sectors and to some extent the booming resources

sector in Australia.

Manufacturing Skills Australia (MSA) confirms this trend across

manufacturing generally, noting in respect of skills shortages that

“Most attributed the attractiveness of other industries and salary

competition as the main reasons for their difficulty in recruiting the

skills they need. These were also blamed for difficulty in retaining

workers”.3 As noted below the booming resources and associated

construction sectors are proving a significant drain on workers to

the FCJ sector.

An approximation of the looming skills shortage (using Deloitte

Architectural glass designers and technicians

Supervisors

Kitchen and bathroom installers,manufacturers and designers

CNC operators and programmers

Upholsterers

Carpet/vinyl/timber floor layers

Glaziers

Project Managers

CAD specialists

Managers and management skills

Cabinet makers

Wood machinists

Window coverings makers & installers

Glass processing workers

Technical sales people

Industrial painters

Access Economics data on annual projected retirement rates)

would suggest an additional 15,000 workers will be needed over

the next five years just to maintain ‘business as usual’ for the

sector. This accounts for both new and replacement of retiring

workers from the industry.

While improvements in technology will drive productivity

improvements and greater efficiencies the skills shortage will be a

significant dampener on the potential growth and innovation in the

industry moving forward unless practical solutions are found.

The FCJ industry is also conscious of the potential workforce that

exists through non-traditional pathways, including up-skilling of

existing staff (from within FCJ or other parts of manufacturing),

greater encouragement for secondary students to consider FCJ as

a viable career option and increasing the participation of women in

the industry.

Skills Shortages, Furnishing2

2 Manufacturing Skills Australia, Environmental Scan 2012. February 2012. p 41 3 ibid. p 6

TABLE FOUR

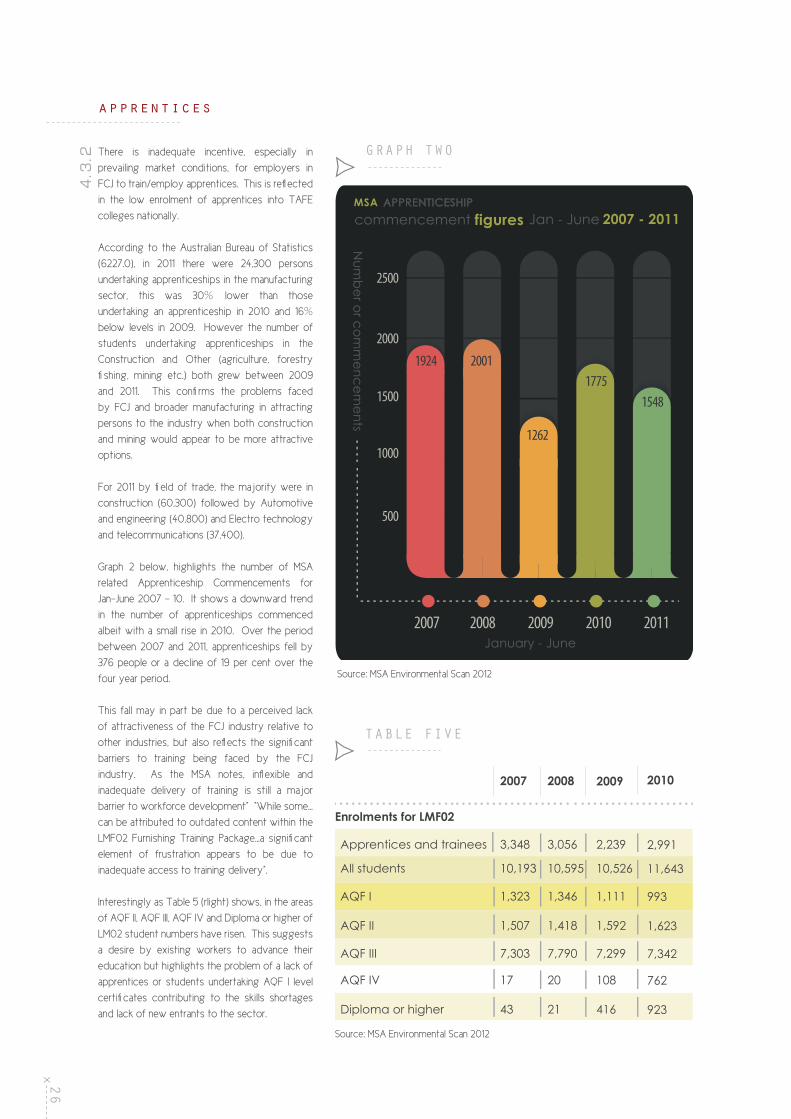

4.3

.1

25