16-1 Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin.

Upload

arnold-gainesCategory

view

215download

0

Strategic Control and Corporate Governance

Chapter Nine

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Learning Objectives

After reading this chapter, you should have a good understanding of:

LO1 The value of effective strategic control systems in strategy implementation.

LO2 The key difference between “traditional” and “contemporary” control systems.

LO3 The imperative for “contemporary” control systems in today’s complex and rapidly changing competitive and general environments.

9-2

Learning Objectives (cont.)

LO4 The benefits of having the proper balance among the three levers of behavioral control: culture, rewards and incentives, and boundaries.

LO5 The three key participants in corporate governance: shareholders, management (led by the CEO), and the board of directors.

LO6 The role of corporate governance mechanisms in ensuring that the interests of managers are aligned with those of shareholders from both the United States and international perspectives.

9-3

Strategic Control

• Strategic control the process of monitoring and correcting a

firm’s strategy and performance Informational, behavioral

9-4

Ensuring Informational Control

• Traditional control system1. strategies are formulated and top

management sets goals

2. strategies are implemented

3. performance is measured against the predetermined goal set

9-5

Traditional Approach to Strategic Control

9-6

Traditional Approach to Strategic Control

• Most appropriate when Environment is stable and relatively simple Goals and objectives can be measured with

certainty Little need for complex measures of

performance

9-7

Contemporary Approach to Strategic Control

• Contemporary control system Continually monitoring the environments

(internal and external) Identifying trends and events that signal the

need to revise strategies, goals and objectives

9-8

Contemporary Approach to Strategic Control

9-9

Contemporary Approach to Strategic Control

• Informational control Concerned with

whether or not the organization is “doing the right things”

• Behavioral control Concerned with

whether or not the organization is “doing things right” in the implementation of its strategy

9-10

Question

Top managers at USA Today meet every Friday to review daily operational reports and year-to-date data. This is an example of A. Behavioral controlB. Informational controlC. Strategy formulationD. Strategy implementation

9-11

Informational Control

• Deals with internal environment and external strategic context

• Key question “Do the organization’s goals and strategies

still ‘fit’ within the context of the current strategic environment?”

9-12

Informational Control

• Two key issues Scan and monitor external environment

(general and industry) Continuously monitor the internal

environment

9-13

Effectiveness of Contemporary Control Systems

1. Focus on constantly changing information that has potential strategic importance.

2. The information is important enough to demand frequent and regular attention from all levels of the organization.

3. The data and information generated are best interpreted and discussed in face-to-face meetings.

4. The control system is a key catalyst for an ongoing debate about underlying data, assumptions, and action plans.

9-14

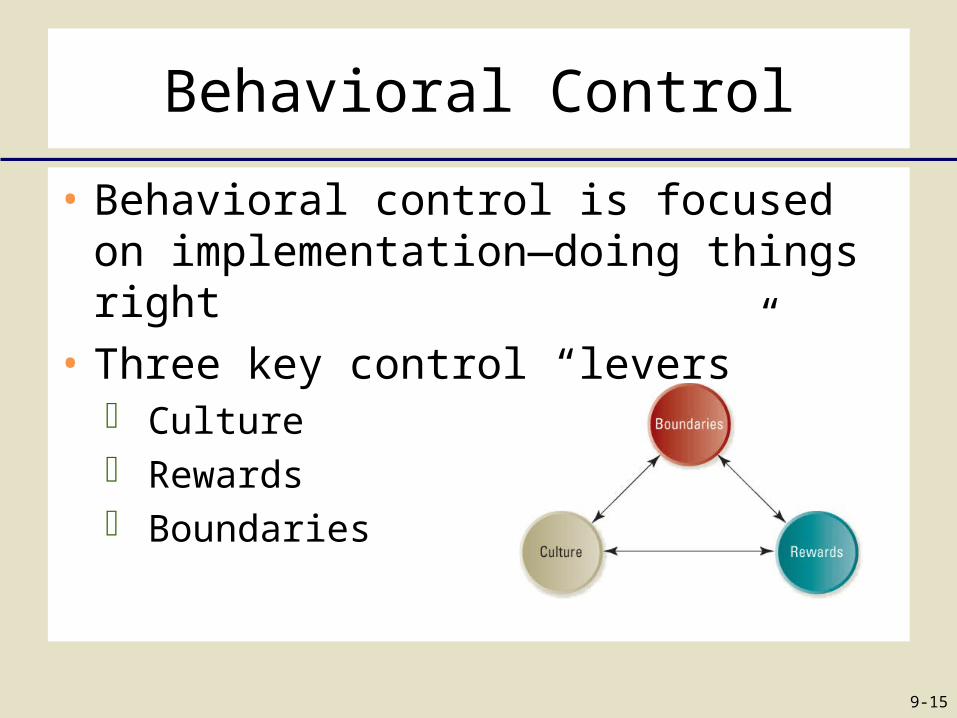

Behavioral Control

• Behavioral control is focused on implementation—doing things right

• Three key control “levers” Culture Rewards Boundaries

9-15

Reasons for an increased emphasis on culture and rewards

1. The competitive environment is increasingly complex and unpredictable, demanding both flexibility and quick response to its challenges.

2. The implicit long-term contract between the organization and its key employees has been eroded.

9-16

Building a Strong and Effective Culture

• Organizational culture a system of shared values and beliefs that

shape a company’s people, organizational structures, and control systems to produce behavioral norms.

9-17

Building a Strong and Effective Culture

• Culture sets implicit boundaries (unwritten standards of acceptable behavior) Dress Ethical matters The way an organization conducts its

business

9-18

Example: Wal-Mart

• A lot of Wal-Mart's success was attributed to the strong and pervasive culture at the company, which was developed and nurtured by founder Sam Walton.

• In over four decades of operation, Wal-Mart managed to retain most of the elements of culture it had when it first started out, as well as the entrepreneurial spirit which often drives startup companies to success.

9-19

Sustaining an Effective Culture

• Effective culture must be Cultivated Encouraged Fertilized

• Maintaining an effective culture Storytelling Rallies or pep

talks by top executives

9-20

Motivating with Rewards and Incentives

• Rewards and incentive systems Powerful means of influencing an

organization’s culture Focuses efforts on high-priority tasks Motivates individual and collective task

performance Can be an effective motivator and control

mechanism

9-21

Motivating with Rewards and Incentives

• Potential downside Subcultures may arise in different business

units with multiple reward systems May reflect differences among functional

areas, products, services and divisions

9-22

Characteristics of Effective Reward andEvaluation Systems

9-23

Setting Boundaries and Constraints

• Focus efforts on strategic priorities

• Providing short-term objectives and action plans Specific and measurable Specific time horizon for attainment Achievable, but challenging

9-24

Setting Boundaries and Constraints

• Improve operational efficiency and effectiveness

• Minimizing improper and unethical conduct

9-25

Question

Effective boundaries and constraints: A. Tend to inhibit efficiency and effectivenessB. Distract employees who are trying to focus on organizational prioritiesC. Minimize improper and unethical conductD. Tend to limit organizational growth

9-26

Organizational Control: Alternative Approaches

9-27

Evolving from Boundaries to Rewards and Culture

• System of rewards and incentives coupled with a strong culture Hire the right people Training plays a key role Managerial role models are vital Reward systems clearly aligned with

organizational goals and objectives

9-28

Role of Corporate Governance

• Corporate governance the relationship among various participants in

determining the direction and performance of corporations.

primary participants are the shareholders, the management, and the board of directors.”

9-29

The Modern Corporation

• Corporation A mechanism created to allow different

parties to contribute capital, expertise, and labor for the maximum benefit of each party.

9-30

Agency Theory

• Deals with the relationship between Principals – who are owners of the firm

(stockholders), and the Agents – who are the people paid by

principals to perform a job on their behalf (management)

9-31

Agency Theory: Two Problems

1. The conflicting goals of principals and agents, along with the difficulty of principals to monitor the agents, and

2. The different attitudes and preferences towards risk of principals and agents.

9-32

Governance Mechanisms

• Board of directors a group that has a fiduciary duty to ensure

that the company is run consistently with the long-term interests of the owners, or shareholders, of a corporation and that acts as an intermediary between the shareholders and management.

9-33

The New Rules for Directors

9-34

Governance Mechanisms

• Shareholder activism actions by large shareholders, both

institutions and individuals, to protect their interests when they feel that managerial actions diverge from shareholder value maximization.

9-35

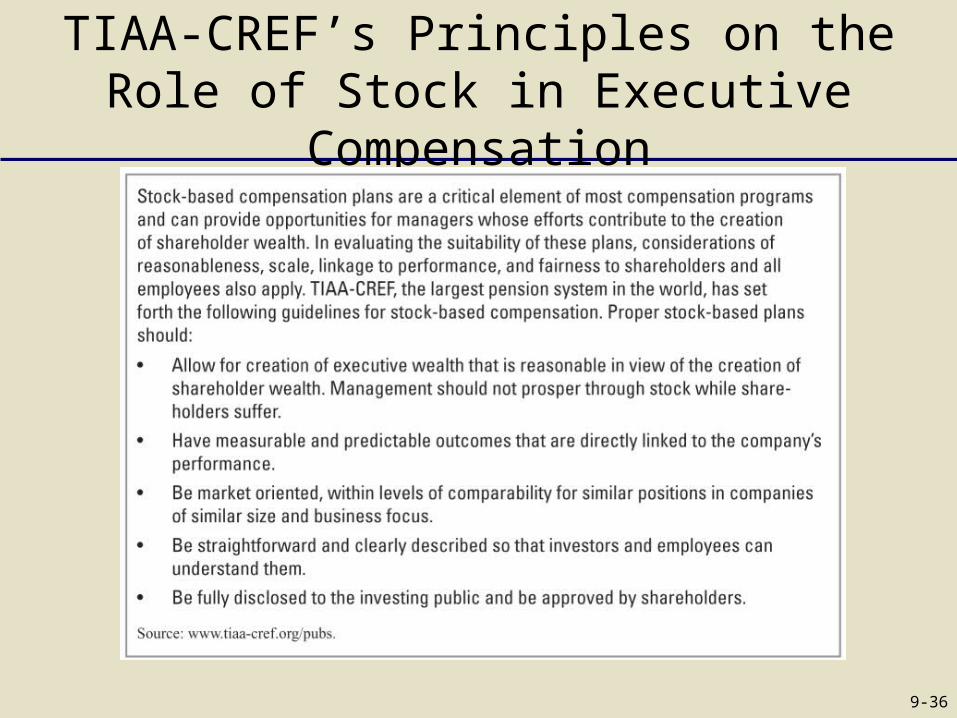

TIAA-CREF’s Principles on the Role of Stock in Executive Compensation

9-36

External Governance Control Mechanisms

• External governance control mechanisms methods that ensure that managerial actions

lead to shareholder value maximization and do not harm other stakeholder groups and that are outside the control of the corporate governance system.

9-37

External Governance Control Mechanisms

• Market for corporate control

• Auditors

• Banks and analysts

• Regulatory bodies

• Media and public activists

9-38

Sarbanes-Oxley Act

• Auditors Barred from certain types of non-audit work Not allowed to destroy records for five years Lead partners auditing a firm should be

changed at least every five years

9-39

Sarbanes-Oxley Act

• CEOs and CFOs Must fully reveal off-balance sheet finances Vouch for the accuracy of information

revealed

• Executives Must promptly reveal the sale of shares in

firms they manage Are not allowed to sell shares when other

employees cannot

9-40