Strategic analysis

40

Vincent Boiteau FIP HEC Executive MBA modular 2012 Painting Services Marketplace A startup business plan

-

Upload

vincent-boiteau -

Category

Investor Relations

-

view

745 -

download

1

description

Transcript of Strategic analysis

Vincent Boiteau FIP HEC Executive MBA modular 2012

Painting Services Marketplace A startup business plan

Vincent Boiteau, HEC EMBA, April 2012 Page 2

About the Author A2012 Executive MBA candidate of HEC, I am an engineer by trade. Born and raised in France, I moved to Canada when I was 17 and experienced my schooling and early career there. I quickly became fond of new experiences, enjoying the opportunity to arbitrage best practices. This transpired directly into my career. I have worked for many companies, of many sizes, in many countries and in many functions. At 40, my professional experience is eclectic to say the least. Nonetheless, a few years ago, my strategy changed to focusing on energy as an industry and business development as a function.

Innovation is the only viable path to value creation and therefore, personal career development. As a business developer, novelty is at the heart of my job. Innovating means exploring unknown sources of value. The search and discovery of profit is an exercise I enjoyed. As a result, I chose to explore the feasibility of a business model in a field and a function almost unbeknownst to me: internet marketplaces.

Special Thanks I wish to take this opportunity to thank Mr. Gerard Maupeou, my FIP advisor who provided me with fantastic guidance and responsiveness. Gerard was kind enough to bring me is support at the last minute as I was late in beginning this strategic analysis.

Special thanks also to Isabelle Rainaud for relentless care of each and every member of our promotion;

Thank you also to the institution of HEC that has given me powerful management tools that will allow me to dare new challenges.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publisher, Vincent Boiteau. The facts of this document are believed to be correct at the time of publication but cannot be guaranteed. Please note that the findings, conclusions and recommendations that Vincent Boiteau delivers are be based on information gathered in good faith from both primary and secondary sources, whose accuracy we are not always in a position to guarantee. As such Vincent Boiteau can accept no liability whatever for actions taken based on any information that may subsequently prove to be incorrect.

Vincent Boiteau, HEC EMBA, April 2012 Page 3

Executive summary

Mister Jones is a busy man. Weekends are the times he cherishes. That’s when he can finally spend some quality time with his wife, Jenny and his newborn son, Jim. They often talk about refreshing the apartment. Today, it’s decided, the baby’s room will get a new flashy coat of paint and the kitchen will finally lose its old faded tint. Jenny grabs the tablet and visits XXX.com. They answer a few questions online about the work that has to be done and she posts the project on the website. After the coffee, they notice some painters have already bided on their work, and it’s cheaper than they thought! A couple of days later, Jenny’s friends are visiting. Checking the website, they settle for Bill, a painter with lots of recommendations and a specialty in flashy colors, he even sent her a mail suggesting that new paint that changes tint with seasons! Bill is happy because he didn’t have to drive over to Jenny’s to see the apartment; she described it just right online. Bill can also manage all his jobs the same way right inside XXX.com, he can buy more of that color changing paint mothers love and find the help he needs on the website. He can even lower his cost because he can group his jobs. He’s currently bidding for jobs in Jenny’s neighborhood and he’ll offer to do them all next week for a small discount.

Today, things are not quite that easy. Accessing the market is complicated and results are uncertain. We at XXX.com believe there is an opportunity in the extreme fragmentation of the market and the absence of efficient intermediation. Internet, social networks, e-tailers and cloud computing have changed the way we shop. Powerful application modules can be developed more cheaply than ever (its cost is spread over a large clientele) and traffic can be efficiently attracted to a website.

Our concept aims at creating a marketplace where buyers and painters will easily be able to post and bid for projects for free. A portion of the painters (paying members) will be offered to access simple and powerful productivity tools that will help them run their business more efficiently. Peer review system will be widely deployed to further the community atmosphere.

The implementation plan of this company is 4-phased:

1. Refine value proposition (which functionality to offer) and plan organisation

2. Develop modules and forge partnerships

3. Launch online marketplace regionally

4. Launch online marketplace nationally

Each stage has an exit strategy to minimize value-at-risk. For instance, value after 4 years of plan implementation, enterprise value ranges from €5M to €10M. Free cash flow is positive 6 months into stage 4 and EBITDA is projected to reach €2M in that stage. Member count at the end of year 4 is to reach 1 million.

Phase one and two (pre online launch) represent an investment of €175k. Launch phase (regional then national) represent a funding need of €900k. Stage 1 is financed by the entrepreneur and XXX.com seeks investors for the subsequent stages.

Vincent Boiteau, HEC EMBA, April 2012 Page 4

Contents

Business idea .............................................................................................................................................. 5

External Analysis ........................................................................................................................................ 6

Macro-economic forces .......................................................................................................................................... 6

Industry ................................................................................................................................................................... 7

Seller typology .................................................................................................................................................... 7

Evaluating the black market and the DIY market: ................................................................................................ 9

A distributed and atomized market .................................................................................................................... 11

Typical P&L ....................................................................................................................................................... 11

Industry Value curve .............................................................................................................................................. 12

Current Value proposition (internet search) ............................................................................................................ 13

The industry of internet marketplaces ...................................................................................................... 14

Macro forces ......................................................................................................................................................... 14

Industry ................................................................................................................................................................. 15

Competitive forces ................................................................................................................................................ 15

Key success factors online marketplace ................................................................................................................ 16

Strategic options ....................................................................................................................................... 17

Designing a new value proposition for the end-customer ...................................................................................... 17

A new value curve ................................................................................................................................................. 18

Designing a new value proposition for the supplier ................................................................................................ 18

Tentative overall objectives ...................................................................................................................... 20

Vision .................................................................................................................................................................... 20

Mission statement ................................................................................................................................................. 20

The strategy .......................................................................................................................................................... 21

The value chain ..................................................................................................................................................... 21

The proposed business model ............................................................................................................................... 22

The implementation plan .......................................................................................................................... 24

The financials ............................................................................................................................................ 28

Provisional P&L ..................................................................................................................................................... 28

Financial upsides .................................................................................................................................................. 30

Funding ................................................................................................................................................................. 30

Exit strategies ....................................................................................................................................................... 30

Sensitivity analysis ................................................................................................................................................ 31

The conclusion .......................................................................................................................................... 32

Appendix A Concentration ......................................................................................................................... 33

Appendix B Real estate market ................................................................................................................. 35

Appendix C The renovation market ........................................................................................................... 37

Appendix D Prototype ............................................................................................................................... 38

Appendix E P&L ......................................................................................................................................... 40

Vincent Boiteau, HEC EMBA, April 2012 Page 5

Business idea

XXX.com is the first platform to offer an online, inexpensive and simple industrial-grade ERP system for self-employed painters. Integrating these productivity modules directly into a marketplace will allow real-time functionality to be deployed. Indeed, XXX.com will also feature a free auction-type marketplace where painters bid on project posted by buyers.

The value proposition to the buyer is compelling: post your project and select painters based on their bids and their reputation (peer-review system)

The value proposition to the painter is also undeniable: bid on projects for free and pay-as-you go to use cloud-based advanced functionality such as:

Scheduling of projects

Grouping of purchasing activity

Sourcing of labor

Business Intelligence

Managing reputation

Logistics

CRM

…etc

Current intermediation platforms, both off and online, stop short of the above business idea. They simply create a marketplace and sell advertising space based on traffic density. The value of this venture does not lie in the aggregation of supply and demand. Rather, it is in the value added by simple and powerful functionality that creates the revenue flow. This strategic choice creates a sustainable business models as it essentially increases the barriers to entry and secures recurring EBITDA. New competitors will come but they will all need to develop the functionality and brand which XXX.com will already possess.

In the last 10 years, the internet sector has been one of the most active and successful sectors of the global economy. The ecosystem is in place and company transmission mechanisms are mature.

Vincent Boiteau, HEC EMBA, April 2012 Page 6

External Analysis

First analysing the home painting industry will help size the market, target the right participants and develop a financial plan.

In France, painting professionals are specialized in interior and exterior painting of buildings or civil works. They mainly have home-owners as clients during the renovation or maintenance phase.

The industry is very atomized and employs 110,000 people and features almost 20,000 entities. Most are very small family businesses, turnover is high as barriers to entry are low, and especially since the “auto-entrepreneur” status (2007) has allowed simply self-employment in France.

Overview of the market we will study:

Local: France

NAF code (rev. 2, 2008): 43.34Z

Main data source is XERFI market study 1BAT04/X07 of April 2011

Macro-economic forces

Political:

France sets itself apart by demanding a high level of state intervention. The professional painting services sector is no exception. It is therefore regulated. For example, interior renovation is subject to the reduced VAT, 7% rather than 21% in order to fight the black market tendency of this industry.

Economic:

The housing sector in France is structurally under capacity, there are more seekers of housing than offers. This sustains high prices as French people traditionally invest in real-estate for savings. VAT and other fiscal incentives are helping ensure the value of real-estate remains high as it facilitates frequent maintenance works.

Sociocultural:

Demographics have a strong influence on this industry simply because nativity and age distribution impacts the construction sector and future renovation potential. Demand has a strong geographical component. Migration and population growth in southern France will increase population as density in the north increases difficulty of access to housing.

Technological:

Painting is not a particularly influenced by technological advances. Some developments have allowed creative results via application methods enhancements but they represent more of an evolution rather than game-changing innovations. The core value adding process of paint application remains largely based on the paint roller and masking tape.

Environmental:

Environmental and health concerns are increasingly important in this industry. They are largely handled by the upstream players, namely the coating industry rather than its application professionals. Painter, however, is responsible for the knowledge of the regulations.

Legal:

Labor and fiscal laws strongly affect this market as “under the table” activities are rampant. A stronger application of the current laws could have a large effect on this industry. The new legal status of “auto-entrepreneur” has also made it much easier to start and run a self-employed business (reduced taxes, favorable tax payment schedule…). Maintaining housing is well engrained in French mentalities.

Reduced VAT rate for renovation works of dwellings

Income tax reduction via the “aide à la personne” mechanism

Vincent Boiteau, HEC EMBA, April 2012 Page 7

Industry

Seller typology

The professional painting services market is mature. Altogether, it represents a turnover of €11B and counts about 46,000 companies. It can be divided by client type:

1

2

1 Market study XERFI 1BAT04 – Apr. 2011 2 Market study XERFI 1BAT04 – Apr. 2011

Residential renovation has traditionally been favored by the governmentNew and simplified status increases entrantsBusiness is correlated to economic cyclesRECAP

home owner-50%

public housing-19%

Public companies-31%

Turnover by client type

less than 9 employees; 50% 10-19 employees;

16%

20-49 employees; 20%

more than 50 employees; 14%

Mix by turnover

Vincent Boiteau, HEC EMBA, April 2012 Page 8

3

So, we can divide the market in 2 distinct types of businesses:

We will focus on the B2C segment, the home-owner segment, typically:

more receptive to innovation

more buoyant yet more illiquid

faster to adopt improvements

In that segment, demand is increasing (fiscal incentives, demographics, economic growth) and barrier to entries are low, so there is a steady increase in both suppliers of painting services and demand

In light of the business idea of a marketplace, the market can be further segmented through the following statistics:

3 Market study XERFI 1BAT04 – Apr. 2011

1 employee: 50%

2-4 employees: 30%

5-9 employees: 13%

10-19 employees: 4%

20-49 employees: 3%

more than 50 employees: 2%

Mix by Size

Total Market

46,000 companies€11B turnover

B2C

less than 10 empoyees

41,000 companies

€5B turnover

B2B

more than 10 employees

5,000 companies

€6B turnover

Vincent Boiteau, HEC EMBA, April 2012 Page 9

4

5

Combining these 2 statistics, we can again refine the market. Younger companies will have a different size, strategy and therefore needs than established ones.

This leads to the existence of 2 strategically distinct groups within the industry each with different goals:

Evaluating the black market and the DIY market:

Let us begin by evaluating the home renovation interior painting for the entire territory.

4 Market study XERFI 1BAT04 – Apr. 2011 5 Market study XERFI 1BAT04 – Apr. 2011

less than 5 years; 55.4%

more than 5 years; 44.6%

Age of Company

18-25; 0.9%25-29; 4.1%

30-34; 8.4%

35-39; 15.7%

40-44; 16.4%

45-49; 15.5%50-54; 16.6%

55-59; 15.9%

60-64; 4.1%

65+; 2.4%

Average age of manager

B2C Market41,000 companies

€5 B turnover

Less than 5-years old55.4%/22,700 companies

Average manager age: 35 y.o.

Focus on market sharebest use of limited resources

Growth strategy

€1.5B turnover - €60k/companySelf-employed

More than 5-years old44.6%/18,300 companies

average manager age: 48 y.o.

Consolidate market shareFocus on repeat business

Cost strategy

€3.5B turnover - €190k/company Family business (3-5 persons)

Vincent Boiteau, HEC EMBA, April 2012 Page 10

There are 41,000 interior painting professionals and 27,300,000 dwellings with and average size of 88m2 and 141m2 of “paintable” interior surface. Knowing that the average painting company turns over €120k per year, we reach an average age of renovation of 14 year. Now, clearly this mean that a measurable quantity of the home renovation are done outside of the professional painters, either under the table or DIY. Let us assume the average time between repaint is closer to 8 years which is rather conservative. This suggests that there is another €3B worth of painting services equivalent that is being performed outside of the official channels either under the table or by do it yourselfers.

Number of appartments 27.3 million population per dwelling 2.3 persons Average floor size 88 m2 Average wall painting 141 m2 Interior painting global turnover 5 €B Number of companies 41000 companies Cost of painting 18 €/m2 Cost of painting per dwelling 2534 € Number of transactions per year 2.0 Million Population of France 62.5 Million Average turnover per company 122 €k Number of jobs per year 48.1 jobs Average number of work days 217 d/y Average length of works 3.0 days Average lifetime of paint 14 years

DIY and unofficial transactions represent an €3B market.

Overall painting services market turns over €11B (B2C: €5B and B2B: €6B)55% of B2C companies ( 22700 companies) are recent self-employed.There are 3-4 million individual projects each year, 2 million are official.RECAP

Houses-44%

appartment-29%

Commercial-27%

Turnover by type of work

Vincent Boiteau, HEC EMBA, April 2012 Page 11

6

7

A distributed and atomized market

This industry is quite atomized; it has about 41,000 distinct companies for a total employment of 101,000 persons leading to an average size of 4 people per company. Indeed, 91% of companies are registered under the less-than-10-employee status. The new “auto-entrepreneur” status has further increased the number of players in this field and reduced the average company size. The number of entrants is growing. See appendix A

Typical P&L

Turnover 100% Gross Margin 80% EBITDA Margin 6% Working Capital 20 days of turnover Personnel Costs 49% Material Costs 31%

6 Market study XERFI 1BAT04 – Apr. 2011 7 Market study XERFI 1BAT04 – Apr. 2011

interior-69%

Exterior-26%

Other-5%

Home-owner market by turnover by type

renovation-69%

new works-31%

Turnover by type of work

Vincent Boiteau, HEC EMBA, April 2012 Page 12

Industry Value curve

Currently the intermediation in the home painting industry is done by either:

Yellow Pages type of services

Peers

Past use of painter

B2C market is mostly renovations of dwellings.Market is highly fragmented and distributed by demographics.Market with low barriers to entry, is active and growing.RECAP

Painter Performs coa-

ting

Intermediary Yellow Pages

Internet search

Client Seeks quality,

timing and cost

Storage Allows scale

purchase Improves lo-

gistics

HW store Incites DIY

Govt Health regula-tion and VAT

Schools Trains neces-

sary labor

Chamber of commerce

Provides sup-port/BI

Media Create urge

Paint mfg Provides quali-

ty + com-pliance

Labor Provides

help/ability to grow

Friends Influences

client

Banks Facilitate fi-

nancing

Vincent Boiteau, HEC EMBA, April 2012 Page 13

Today, home owners face difficulties in accessing bidders to do their painting works. The tools are few and far between. They often are found by word of mouth or yellow pages. At that stage, quotations are needed and that can take up to several weeks with the constant fear that the job will not be done properly or honestly. A certain portion of end-user therefore prefers to undertake the task themselves with the certainty that the extra time and cost of using a professional is not warranted despite a lower end-result quality. The reasons for this inefficient pre-transaction process are defined in the curve below.

Current Value proposition (internet search)

The difficulties faced by people who have made the decision to paint are

Finding trustworthy painter that will Respect delays/timing

Acceptable price

Quality and timely result

I need a painting professio

nal

Locate professi

onal

Internet SearchRepeat business

Ask friend

decide DYI or painter

1

2

3

4

5

Internet search

Repeat business

Peers

Price:Free

Risk:no quality assurance

Effort/time:lots of work to activate

competition

Justification:Serious publication

Rcognize brand

Difference:Free

impartial

Promise:Contact Information

Vincent Boiteau, HEC EMBA, April 2012 Page 14

For some, cost is so paramount that DIY is the only options no matter how other factors are fulfilled by the supplier. However, for those that choose to search or activate word-of-mouth, price is but a factor amongst others. They are usually aware of pricing and are more likely to rank quality and timeliness as the top choice factors.

The case of do-it-yourselfers:

A particular point of interest is the person that has gone through the quoting process but has decided to do the work himself. In that category, the price issue is likely the hurdle. There exists, therefore, an opportunity to transform DIY that did choose the professional route into a consumer if an adequate system allows lower prices.

The people that choose the professional route do so because they wish to save time and increase quality (vs. DIY) in exchange for a larger payment. The process up to the decision point is long, perhaps weeks and is a sunk cost for the buyer and the seller. People that will attach most value to reducing this time will probably be busy people, in the middle of their career, with children, living in a large city (prices are higher there and so, the work time needed to acquire a dwelling is higher than in smaller cities). Painting as a home-improvement probably involves the decision maker more that simple maintenance painting so first-time owners will value more quality and speed as their busy schedule and emotional attachment to their home is increased. Also new constructions are much less promising as second-hand homes lend themselves to renovations immediately after the acquisition. The use of the internet, especially social networks must be proven.

• Current intermediation players are inefficient (internet, yellow pages, friends)

• Clients face difficulty in accessing services

Buyer Profile, see appendix B for details

For our market place concept, we can therefore assess the end-user target group:

30-45 years old

Has children

Belongs to the 3rd and 4th quartile of the population

Buys second hand homes rather than new construction

Live in 100 000+ population cities where demographics show growth

Young mothers as the decision making target, less active than the male

Fondness for renovation

Busy schedule

Internet versed

The industry of internet marketplaces

Macro forces

Political:

Internet, in general, is not very influenced by political developments. However, unification of rules and regulation (globalization) will affect positively the growth of internet marketplaces.

Current intermediation players are inefficient (internet, yellow pages, friends)Cients face difficulty in accessing services of their choice,Painters would also increase their turnoverRECAP

Vincent Boiteau, HEC EMBA, April 2012 Page 15

Current crisis dictates more emphasis is placed on growth and tech companies may benefit from special government support and subsidies as it is clearly a high value added activity.

As margins are usually high, increased fiscal pressure may come upon this industry if crisis deepens dramatically.

Economic: Economic climate have a direct impact on marketplace performance as it deals with portion of purse issues. Social: Further integration of the Internet in the daily life will be a major issue in the next years. This is a great opportunity for ecommerce platforms and will affect them very positively.

Online shopping is becoming main stream and affects positively internet based marketplaces but a strong brand will become more and more important as customer will be bombarded by a myriad of choices.

Demographic changes are to be taken into account, mostly as OECD countries will experience an aging population and so, user friendliness will become more and more critical.

Intra-country migration, notably urban exodus will affect regional transaction flux as masses move around the territory

Technological: Social networking will allow trust to be built online as face-to-face transaction will decrease. Group and social buying is the next development for both sales and marketing as individual information now allows mass one-to-one marketing.

Environmental:

Not applicable

Legal:

Regulations could be passed making sites ensure a certain level of security in online shopping, increasing customer security but also costs for online businesses.

As barriers to entry are low, patent securitization will become an incumbent best weapon to defend its position.

Industry

Marketplaces are now common on the internet. Most have been focusing on product ecommerce and have become very large multinationals like eBay or amazon. Some have ventured into services, much more difficult to specify, therefore exchange. Match.com is a good example as it is, in essence, a marketplace where desires are exchanged. Online shopping, from buying dog food to renting a car, is becoming more and more mainstream and expanding towards the 50+ age groups. Social network’s spectacular growth allows more trust to be built into those marketplaces as buyers ranks the sellers.

Forces that influence this industry, notably:

Rapidly evolving technologies mean it must be a key competency/activity

Social networking is influencing ways to shop

Globalisation means size of market is growing

Size matters as it lowers cost and give competitive advantage

Industry specific

Low CAPEX means low barrier to entry

Regulations are uncertain as sector evolves

Customers get used to using internet

Competitive forces

In France, there is no full-featured marketplace for painting services as there are for retail for example (eBay, Groupon). There exists, however, website that try create a free marketplace for such services but they are based on the Advertising revenue generating business model. They do not provide the added services to the professional

Vincent Boiteau, HEC EMBA, April 2012 Page 16

painters as does our value proposition. The closest competition is www.quipeutlefaire.com it consists of a buyer posting a project and painters bidding for those projects. It’s main weaknesses are

1. It is very complicated to go through the steps.

2. The bidding mechanism is weak because painters accept or refuse the estimate of the buyer.

3. The site is national and makes it difficult to physically create a marketplace of geographically close buyers and sellers. Our staged launch has an initial local launch phase to mitigate that risk.

4. No recognized partners seem to be involved with this website. Our deployment includes an important step to strike deals with partners that will give us the initial authenticity.

5. There is no functionality provided to the painter. At the heart of our business model is the creation of simple, powerful and inexpensive of online tools that will improve the painter’s bottom line and growth.

6. The advertising budget needs to be much higher to create top-of-mind awareness of the brand. Our proposal includes a large traffic-generating advertising account allowing us to quickly capture audience.

It does show positive keys points:

1. Peer review is present

2. Value proposition is clearly state “publish a project””compare offers” choose

3. It attempts at having the project definition done by the buyer rather than the painter

Key success factors online marketplace

Technology expertise

Strong algorithm

Simple interface

Local content

Relevant information

Innovation

Instill curiousness

Create compelling set of services/functionality

Brand name

Top of mind

legitimacy

Speedy traffic acquisition:

Motivation for visiting

Motivation for joining

Conversion to member

Motivation for staying

Guarantees

Peer review

Sales & Advertising

Cost of user acquisition

Customer service

Offline support

Strong first-mover advantage

Build defensive position quickly

Vincent Boiteau, HEC EMBA, April 2012 Page 17

Strategic options

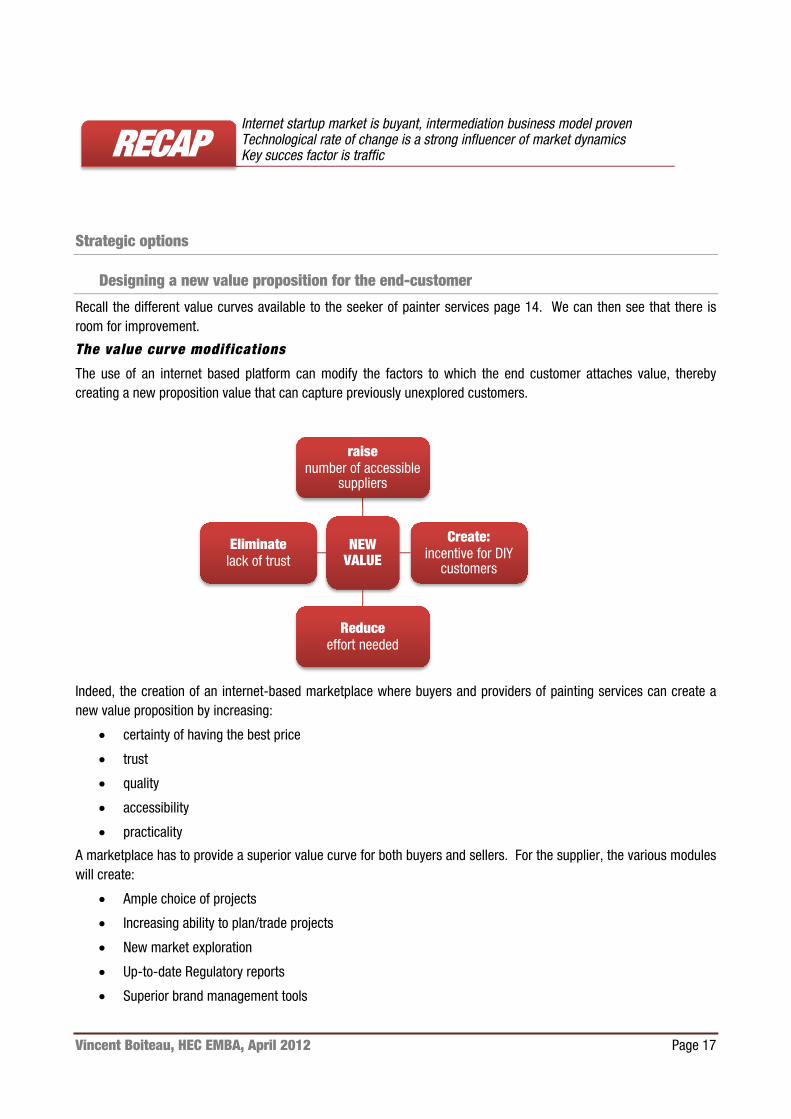

Designing a new value proposition for the end-customer

Recall the different value curves available to the seeker of painter services page 14. We can then see that there is room for improvement.

The value curve modifications

The use of an internet based platform can modify the factors to which the end customer attaches value, thereby creating a new proposition value that can capture previously unexplored customers.

Indeed, the creation of an internet-based marketplace where buyers and providers of painting services can create a new value proposition by increasing:

certainty of having the best price

trust

quality

accessibility

practicality

A marketplace has to provide a superior value curve for both buyers and sellers. For the supplier, the various modules will create:

Ample choice of projects

Increasing ability to plan/trade projects

New market exploration

Up-to-date Regulatory reports

Superior brand management tools

Internet startup market is buyant, intermediation business model proven Technological rate of change is a strong influencer of market dynamics Key succes factor is trafficRECAP

NEW VALUE

raisenumber of accessible

suppliers

Create:incentive for DIY

customers

Reduceeffort needed

Eliminatelack of trust

Vincent Boiteau, HEC EMBA, April 2012 Page 18

A new value curve

This leads to a new buyer value proposition

Designing a new value proposition for the supplier

The key to a new proposition to the supplier does not lie, as with the end-user, in the value curve but rather in the sequence of processes in the painter’s value chain:

1

2

3

4

5

Internet search

Repeat business

Peers

Market

Price:Lots of sellerscompetition

no fee!

Risk:insurance possible

Seller ranked by Social network

Effort/time:easy, 3 clickschoose timing

Justification:Internet based

Seller ranked by Social networkPhysical support

Difference:new concept

constantly updated

Promise:simple high quality painting jobs done

quickly

Technological rate of change is a strong influencer of market dynamics It is possible to produce a superior value proposition to the current productThere is no similar offer on the marketRECAP

Vincent Boiteau, HEC EMBA, April 2012 Page 19

Some key facts to remember (customers are directly inside the marketplace):

Marketing (customer-facing process):

Reaching potential customers is difficult as the options are few:

Use yellow pages

Word of mouth

Mass mailings, flyers, internet bulletin board/classifieds

Scheduling (internal process):

Scheduling is also a tricky task to accomplish efficiently as several projects need to be undertaken concurrently to ensure employment in the months ahead:

Difficulty to commit to start/end dates leads to customer dissatisfaction

Inexperienced painters are at a disadvantage

Quoting (customer-facing process):

Quoting process is a necessary evil:

Sunk cost for the painter as he/she is not sure whether client will accept bid or not

Possibility to discover job is not attractive post-ante

Resource planning (value-chain upstream facing):

Yet another difficult process to handle efficiently because:

Labor can only be contracted after bid has been accepted with limited amount of negotiation time

Need to accept more jobs than possible to handle to cover against risk of loss of project or start/end delays

Operations (customer facing):

Key value adding process

Service (customer facing):

With limited resources and visibility, this process can be difficult to deploy correctly for the painter:

The cost of CRM is sunk without adequate certainty return in terms of income and timing.

Tools are limited and most rely on making a good impression with the customer

after salecustomer loyaltyCRM for continuous improvement (TQM)

Service

Move furnituremask prepare supportcoatfinish

Operations

seek workersbuy supplies

resource planning

Use experience + market to price and time project

Quoting

use current order book and labor resources to determine timing

Scheduling

Reach clients via:- word of mouth- repeat business- advertizing

Marketing

Vincent Boiteau, HEC EMBA, April 2012 Page 20

Hence a value proposition to the suppliers may be:

Since the customer values timeliness, quality and price, the value adding processes that painters must focus on are Resource planning and Operations.

For our market place concept, we can therefore assess the supplier target group:

30-40 years old

Business educated (BTS…etc)

Upper end quality segmented

Interested in improvement of his processes

Recently formed company (5 year or less)

Live in 100 000+ population cities where demographics show growth

Internet versed

Tentative overall objectives

Vision

“To be your local home painting community”

Mission statement

“XXX allows individuals to easily create standardized offers online and request quotes online. Painters are able to bid on the projects of their choice, acquire the necessary labor and manage their workflow all in one place. XXX provides an enhanced ecosystem with peer-reviews and transactions”

Price:Free

€39.99/pay-as-you-go per month for premium seller

Risk:Reputation is

dematerializedTransparency

Effort/time:easy, 3 clicks

Linked to FB/linked profile

Justification:Custom designed application

Large network of buyersPhysical support

Difference:new concept

Promise:Lower costs

Increased revenuesenhanced processes

The painter must undertake processes that add no value.Painters also be made a superior value proposition Target is urban, 100,000h+ selfmployed 30 year old painterRECAP

Vincent Boiteau, HEC EMBA, April 2012 Page 21

The strategy

Build a unique position through superior functionality, service, transparency and ease of use.

The value chain

SWOT

Since this is a startup, the S and W will be part of the implementation chapter

O:

Markets that are local are still open

Buyer/seller meeting is inefficient

T:

Success mean more competitor will come quickly

XXX allows individuals to easily create standardized offers online in order to purchase painting service.

•Removes current time/effort barriers between buyers and sellers•Eliminates search/visit/process which adds no value

Painters are able to bid on the projects of their choice, acquire the necessary labor and manage their workflow all in one place

• Optimizes suppliers processes• Enhances scheduling• Increases growth and margins• ability to source labor, materials...etc

XXX provides a secure global ecosystem for peer-reviews and transactions

• Provides news and information• Creates confidence• Opens new markets

after sale QA process

CRM

Peer review

Key partnership

security/fraud

Payment

Functionality that help painter processes

compelling and stable functionality

Operations

Transparency of process

Bid/Ask process

Ergonomics of site

Key partnerships

communication of value proposition

Conversion

One-to-One marketing to create supplier base

On-to-many marketing to create buyer traffic (free)

Marketing

Vincent Boiteau, HEC EMBA, April 2012 Page 22

Fraud

The proposed business model

Idea is to create more than a marketplace: a local ecosystem. basic service is free, premium pay membershipMission, vision and strategy are clearly formulatedRECAP

Clientdefine and posts projects for free

visit xxx.com

register with FB

defines project

Posts project

Chooses offer

Ranks painter

Painterbids on projects for

free

visits xxx.com

Registers free

Seeks project

Bids

Accepts offer

Premium painterhas additional funcionality

visits xxx.com

Registers premium

clicks "my office"

Bids

Seeks labor

chooses offer

Manages schedule

optimizes logistic

trades projects

buys bulk

does accounting

...etc

Labor Bids on painter's

projects

visits xxx.com

Resters with FB

Seeks painters

bids

accepts offer

Premium membership

module 1labor support

Module 2advanced logistics

Module 3accounting

Module 4 project trading

Module X based on

painter needs

Basic bid/ask free

Vincent Boiteau, HEC EMBA, April 2012 Page 23

Business model options

Which revenue stream option?

The basic families of possible revenue streams and hence business models are:

In our practical case, the pros and cons are:

Transaction: this type of revenue scheme as it is a hurdle to an essential part of the concept: traffic.

Advertising: few complementary products would be of interest to either of the parties. Perhaps paint manufacturers, home renovation credit brokers or tooling manufacturers could be interested in such traffic. Nonetheless, some advertising can be done as the selected business model will generate a similar amount of traffic.

Freemium: this allows strong traffic generation because part of the value proposition is free. However, value proposition to the paying segment must be compelling.

Who are the key partners?

Our mission is more to create an enhanced marketplace, more of an ecosystem. Painting services are part of a value chain.

Chambers of Commerce: In France, each small business type has its national and regional Chambre des Métiers et de l’Artisanat (CMA) and Chambre Régionale des Métiers et de l’Artisanat (CRMA). Their mission is one of support to the painter, notably advisory services, training and general business intelligence. Some of the services to be offered by XXX would overlap with those missions and as a result, a partnership is possible as XXX would facilitate the work of the CMA/CRMA. In return, XXX could acquire some legitimacy (and hence brand value) by the support shown by CMA/CRMA. The CMA and XXX have a similar objective, caring for the development of the profession they are to manage: painters. Exclusive partnership will also further raise barriers to entry.

Facebook/main social networks: One of the KSF is efficient member acquisition. Member acquisition is the result of the following chain of events for each member:

Typically, the attrition rate through each step is of the order of 5% (simulation under Google Adwords). In addition, the ratio of join-to-visit is highly dependent on the simplicity. Nowadays, having a “use your Facebook/Google+/LinkedIn

Advertising

Revenues come from sale of advertising

space

Prosno functionality to create

ConsEasy to copy

need to create compelling content

Transaction

Revenues come from percentage of sale

ProsNo functionality to create

ConsEasy to copy

hard to keep transaction official

Freemium

Revenues come from portion of users that

pay membership

Prosvalue based on both traffic

and SW innovation

Conshigh investment needed to

develop functionality

Motivation to visit Motivation to join Motivation to pay

Vincent Boiteau, HEC EMBA, April 2012 Page 24

account to sign-in” very much helps converts visits to joins since the user doesn’t to fill out tedious information or manage its privacy settings. Therefore, partnerships must be made not only with the current heavyweights of the social network industry but also tomorrows players.

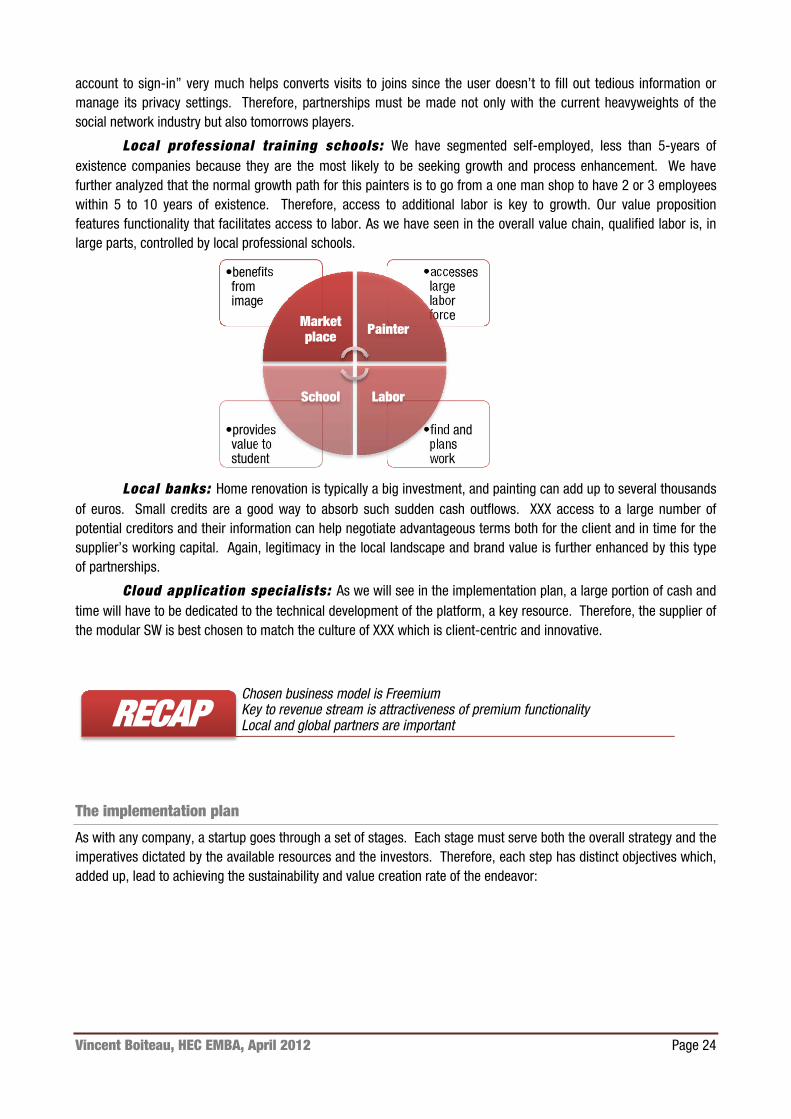

Local professional training schools: We have segmented self-employed, less than 5-years of existence companies because they are the most likely to be seeking growth and process enhancement. We have further analyzed that the normal growth path for this painters is to go from a one man shop to have 2 or 3 employees within 5 to 10 years of existence. Therefore, access to additional labor is key to growth. Our value proposition features functionality that facilitates access to labor. As we have seen in the overall value chain, qualified labor is, in large parts, controlled by local professional schools.

Local banks: Home renovation is typically a big investment, and painting can add up to several thousands

of euros. Small credits are a good way to absorb such sudden cash outflows. XXX access to a large number of potential creditors and their information can help negotiate advantageous terms both for the client and in time for the supplier’s working capital. Again, legitimacy in the local landscape and brand value is further enhanced by this type of partnerships.

Cloud application specialists: As we will see in the implementation plan, a large portion of cash and time will have to be dedicated to the technical development of the platform, a key resource. Therefore, the supplier of the modular SW is best chosen to match the culture of XXX which is client-centric and innovative.

The implementation plan

As with any company, a startup goes through a set of stages. Each stage must serve both the overall strategy and the imperatives dictated by the available resources and the investors. Therefore, each step has distinct objectives which, added up, lead to achieving the sustainability and value creation rate of the endeavor:

•find and plans work

•provides value to student

•accesses large labor force

•benefits from image

Market place Painter

LaborSchool

Chosen business model is FreemiumKey to revenue stream is attractiveness of premium functionalityLocal and global partners are important RECAP

Vincent Boiteau, HEC EMBA, April 2012 Page 25

Phase 1, objectives

Timeline 3 months Cash inflow €40k Cash burn €12k/mth Funding source: Friends & Family, love money Objective 1: Decide which modules to develop Objective 2: Decide which region to start in Objective 3: Refine Phase 2 budget Objective 4 Ink key partnerships with Social Network sites and CRMA

This subtask takes the basic recommendations and finding of the present document and determines the specifics. This is also important because of the cost of developing these offerings is rather substantial and so, response needs to be evaluated beforehand.

What to offer?

Is the free functionality, namely, ability to bid and offer, sufficient to attract strong traffic?

Which services is the paying category (premium) willing to pay for?

Ability to plan and acquire labor (pre and post quoting)

Free membership for assistants

Ability to source assistants

Increased reach

Collaborate with schools

Ability to save on supplies

Systems know when and where what supplies and needed, can allow grouped purchases

System can advertise alternatives

System can suggest storage location + pricing

Ability to receive Business Intelligence

Advanced local stats available

Ability to have information on clients

Ability to warn on location of growth areas

Phase 4

• National launch• KFS addressed• Sustainability• Economies of scale

Phase 3

• Local Launch• Proof of concept

• KFS addressed• Ability to create traffic

• Ability to generate revenue

Phase 2

• Platform setup• design simple & powerful platform

• Forge partnerships• KFS addressed• Technical superiority

Phase 1

• Detailed analysis• What services• What local market• What budget

• KFS addressed• Compelling value proposition

Vincent Boiteau, HEC EMBA, April 2012 Page 26

Advanced planning functionality

Trading of projects (time or geographical optimization)

Accounting services

CRM services

Possibility to choose services à la carte

Mobile platform

E-payments

Revenue forecasting, cost management, inventory control…etc

Where to start?

As we have seen in the previous sections, the market is highly dependent on client location and as such is basically a collection of local micro markets. The business model is therefore easily scalable as the micro markets are similar to each other.

The expansion should then be circular and outwards as to create a zone inside which a small but functional market exists. National launch is therefore not desirable as a starting point. In addition, most local partners are sized in the same way, CRMA, banks…etc and have strong regional content. W. Reinartz and W. Ulaga confirm this strategy in their 2008 HBR article: How to sell your services more profitably. They note that “Successful firms begin slowly, identifying and charging for simple services…”

Let us take advantage of this. A sensible option would be to select one small market to gain experience before full deployment. Beginning with a regional zone will both reduce cost and keep larger competitors away as they are not configured for local content.

The questions to be answered by the end of this phase would notably be:

Which regional chambers of commerce are interested by partnering?

What is the proper size of the pilot region?

Are extremely high density areas (Paris, Lyon) more desirable to moderately dense areas?

Phase 2, objectives

Timeline 6 months Cash inflow €125k Cash burn €21k/mth Funding source Business angels Objective 1: Develop platform & modules decided in phase 1 Objective 2: Implement regional launch plan (sales force, training…etc) Objective 3: Run test value proposition with small group of painters

This second stage is where the customer knowledge is implemented into:

A single web platform that features the various functionality decision above

o SW modules must be created and stabilized before launch

Hand pick 20 suppliers to beta test in exchange for free premium membership

In addition, preparation for phase 3 is necessary:

Decide which region to start:

o Strategically, one region should be chosen, one of the larger ones preferably.

o Begin near centre of region to block competitors starting in the same region

Recruit and train tech savvy sales forces both for buyer traffic acquisition and premium member base.

Vincent Boiteau, HEC EMBA, April 2012 Page 27

Develop sales tools

Phase 3, objectives and KPIs

Timeline 12 months Cash inflow €600k Cash burn €50k/mth Funding source VC Objective 1: Improve operational processes Objective 2: Build traffic Objective 3: Transition from product-centric to customer-centric organisation Objective 4: Create 2-3 new modules based on customer feedback Objective 5: Strengthen brand

Stabilize platform, this is version 0 of the software, bug will be present. New functionality needs to be added on top of the modules developed in phase 2

Reinforce customer-centric vision. Each function must now have a direct link to customer.

Increase online marketing budget + advertising to create buyer presence in same area.

Phase 4, objectives and KPIs

Timeline 24 months Cash inflow €300k Cash burn €50k/mth for the first 6 months Funding source VC/PE Objective 1: Implement TQM Objective 2: Deploy advertising revenue scheme Objective 3: Reduce costs (acquisition cost, service cost, fixed cost) Objective 4: Strengthen brand value as innovator by developing new functionality Objective 5: Formulate exit strategy

National lunch leveraging economies of scale

Focus on acquiring advertisers as traffic has been proven

Focus on process and cost control, no longer in startup phase so management needs to reflect new objectives, this is where managers will take over operations from entrepreneurs

Launch co-creation process of new functionality

o Key suppliers and customers can be accessed to feedback requirements to platform development team

Organisational structure

Customer centric organisation is paramount in today’s market. The key customers in our business model must be at the core of the value-creating processes. Priority, in the early stages, is focused on technical innovation and so,

Vincent Boiteau, HEC EMBA, April 2012 Page 28

organisation is product-centric in the beginning and turning into customer oriented as regional launch approaches

The financials

Provisional P&L

person 1Entrepreneur

Phase 1

Head of technology

Phase 2

Head of marketing

Phase 3

Head of operations

Phase 3

Head of investor relations

Phase4

Business Partner

Phase 2

First stage of deployment of startup is on a small regionInitial focus is on product quality to evolve to client focusThis will mean a complete realignment of the shared values in growth phaseRECAP

-100 €

-50 €

- €

50 €

100 €

150 €

200 €

déc.

-12

févr

.-13

avr.-

13

juin

-13

août

-13

oct.-

13

déc.

-13

févr

.-14

avr.-

14

juin

-14

août

-14

oct.-

14

déc.

-14

févr

.-15

avr.-

15

juin

-15

août

-15

oct.-

15

déc.

-15

févr

.-16

avr.-

16

juin

-16

août

-16

oct.-

16

déc.

-16

48-period monthly EBITDA (k€)see appendix E complete P&L

PHASE1

PHASE2

PHASE3

PHASE4

Vincent Boiteau, HEC EMBA, April 2012 Page 29

Phase 1 (purple bars in graphic above)

During phase 1(3 months), most of the activities will consist of fine-tuning this preliminary study. Cash outflow will result as travel, marketing focus groups, surveys and studies will need to be conducted.

Average per month Studies 6 000 € Employees 1 Cost per staff 3 000 € Other charges 3 200 €

Total 12 200 € Phase 2 (blue bars in graphic above)

Has the objective of:

creating bidding platform and a set of modules

Protecting developed SW via patents

Securing key partnerships

The basic assumptions are:

Average per month Development 8 000 € Employees 2 Cost per staff 4 000 € Other charges 5 200 €

Total 21 200 €

Phase 3 (green bars in graphic above)

The real life test of the project, where income begins to flow in. The formulas are:

%

% %

At this stage, the objective is to:

-1 500 000 €

-1 000 000 €

-500 000 €

- €

500 000 €

1 000 000 €

1 500 000 €

oct.-

12

mai

-13

nov.

-13

juin

-14

déc.

-14

juil.

-15

janv

.-16

août

-16

mar

s-17

Cumulative EBITDA

Vincent Boiteau, HEC EMBA, April 2012 Page 30

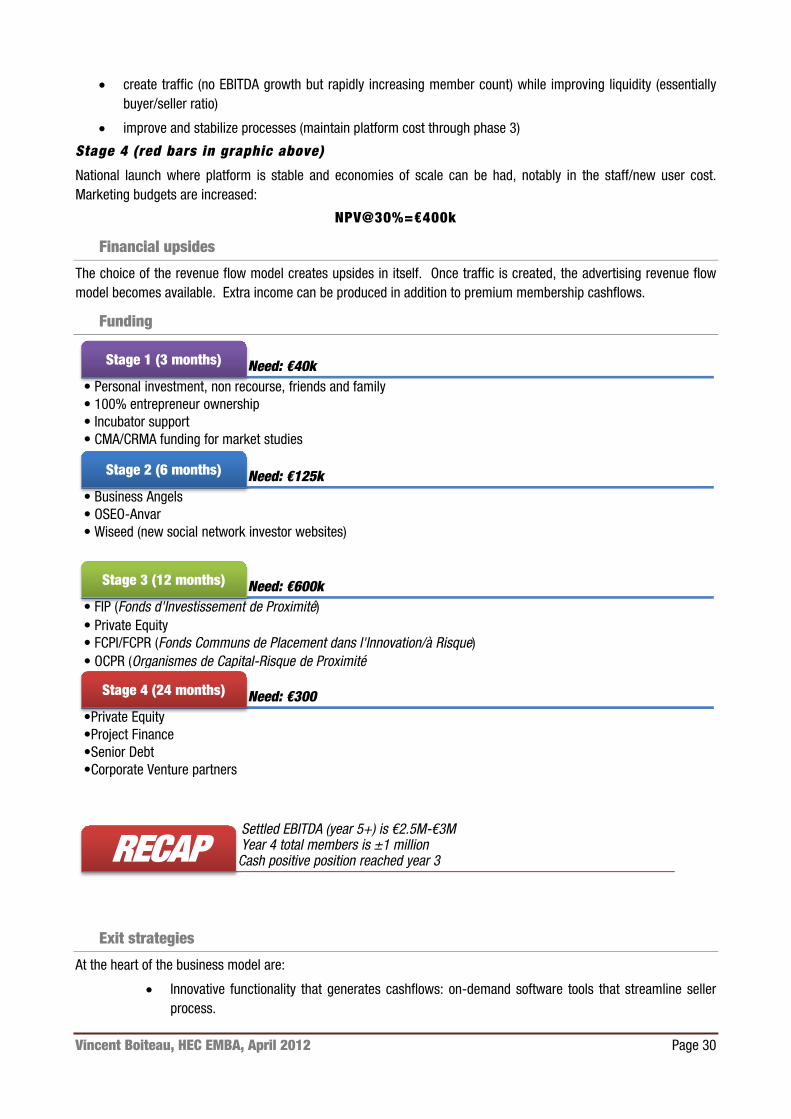

create traffic (no EBITDA growth but rapidly increasing member count) while improving liquidity (essentially buyer/seller ratio)

improve and stabilize processes (maintain platform cost through phase 3)

Stage 4 (red bars in graphic above)

National launch where platform is stable and economies of scale can be had, notably in the staff/new user cost. Marketing budgets are increased:

NPV@30%=€400k

Financial upsides

The choice of the revenue flow model creates upsides in itself. Once traffic is created, the advertising revenue flow model becomes available. Extra income can be produced in addition to premium membership cashflows.

Funding

Exit strategies

At the heart of the business model are:

Innovative functionality that generates cashflows: on-demand software tools that streamline seller process.

Need: €40kStage 1 (3 months)

• Personal investment, non recourse, friends and family• 100% entrepreneur ownership• Incubator support• CMA/CRMA funding for market studies

Need: €125kStage 2 (6 months)

• Business Angels• OSEO-Anvar• Wiseed (new social network investor websites)

Need: €600kStage 3 (12 months)

• FIP (Fonds d'Investissement de Proximité)• Private Equity• FCPI/FCPR (Fonds Communs de Placement dans l'Innovation/à Risque)• OCPR (Organismes de Capital-Risque de Proximité

Need: €300Stage 4 (24 months)

•Private Equity•Project Finance•Senior Debt•Corporate Venture partners

Settled EBITDA (year 5+) is €2.5M-€3MYear 4 total members is ±1 million

Cash positive position reached year 3RECAP

Vincent Boiteau, HEC EMBA, April 2012 Page 31

Robust activity generated by large member base

Once these two strategic objectives are demonstrated and sustainable (3-5 years) several exit strategies are available:

License software

o There also exists and opportunity to simply sell licenses of the SW on a stand-alone basis or pay-as-you-go cloud apps.

Sell to larger partner, better positioned to run mature business

o ERP specialists such SAP or Oracle can be interested in expanding into small business industry. Acquisition, in this case, is the best line of action for them. Multiple of EBITDA are then used

o EBay or Facebook may value the member base, in which case the value is proportional to the number of members and the information gathered. Facebook is valued at €80/user, Instagram at €40/user, Groupon is at €55/user. If we value each member at, say, €5/user, we reach an indicative year 4 value of €6M

Expand to other countries

o Once technique to create marketplace is proven and tools are available, geographical expansion is feasible

Expand to other related services

o SW is designed to optimize basic B2C small business processes in general and can therefore be of appeal to, say, plumbing industry, electrical works, carpentry…etc

Sensitivity analysis

The purpose of this analysis is to determine the key quantitative factors that have an effect on some of the key objectives. Naturally, margin-linked parameters such as EBITDA or RoE are included but some non-monetary factors may be interesting in terms of enterprise valuation, notably number of members or buyer to seller ratio which indicates the health of the marketplace function: creating liquidity. This large member base, in turn, creates the enterprise value.

As mentioned above, the keys objectives are platform development and member acquisition. Let’s examine the impact of their cost on the NPV (compounded at 20%)

Nominal per month

Total budget NPV project

Platform development €8k €94k €400k

Scenario 1/increase per month dev cost €20k/+250% €250k/+266% €250k/-38%

Scenario 2/same per month but double dev time

€8k/+0% €176k/+47% €350/-13%

The traffic generation cost is also to be examined

Buyers are acquired via targeted internet advertising such as Google adwords. As the advertisement is clicked, sending the person to the XXX.com website, a small fee is paid, typically ¢15-¢20. Once the user is on the XXX.com website and the fee has been paid, we need to convert this user to a member. The ratio used is the conversion factor, usually in the 5%-10% rate, which leads to a net member acquisition cost in the range of €2.

Nominal cost per member

per month (Q1)

Total budget (Q1-Q9)

NPV project

Platform development €45k €1.9M €400k

increase buyer acquisition: +25% €56k/+25% €2.3M/+21% €250k/-38%

Vincent Boiteau, HEC EMBA, April 2012 Page 32

A larger and more sales-relevant cost is the premium member acquisition cost. It is them that generate the revenues. Since it involves a physical sales force, cost is obviously higher but it is the safest way to sell what is essentially a B2B cloud computing offer. The sales force must be sized with the size of the market in mind. A market penetration (premium painters to total painter on the territory) target of 10% in phase 2 (regional) and 15% in phase 3 (national) is feasible. Below is the log chart of cost of new premium member against time.

It drops rapidly in phase 2 (regional launch) to settle to about €60 in the national launch phase.

If this cost increases 33%, from €60 to €80, the impact is destructive and the project is not feasible. Therefore, it becomes clearly and objective to determine the feasibility of acquiring paying member below €60 each.

The conclusion

The above analysis highlights an opportunity in the home-painting professional services industry. Leveraging unfulfilled needs in the market with an innovative internet platform is a promising venture. Powerful software modules, a Freemium revenue model, a carefully developed deployment plan will help ensure compelling exit strategies exist for you, the early investors.

1 944 €1250 875 648 455 313 216 167 135 113 91 82 63 63 63 63 63

1 €

10 €

100 €

1 000 €

10 000 €

oct.-

13

nov.

-13

déc.

-13

janv

.-14

févr

.-14

mar

s-14

avr.-

14

mai

-14

juin

-14

juil.

-14

août

-14

sept

.-14

oct.-

14

nov.

-14

déc.

-14

janv

.-15

févr

.-15

Cost per acq premium member (Log scale)

Several exit strategies exist because of choice of freemium modelPlatform development cost have limited impact of NPVPremium member acquisition cost is mission criticalRECAP

Vincent Boiteau, HEC EMBA, April 2012 Page 33

Appendix A Concentration

Pop. Pop. Companies Companies Turnover Dwellings x1000 % # % €M per comp.

Île-de-France 11 746 18.8% 8 487 20.7% 1 035 602 Rhône-Alpes 6 160 9.9% 4 797 11.7% 585 558 PACA 4 940 7.9% 3 813 9.3% 465 563 Nord-Pas-de-Calais 4 022 6.4% 1 394 3.4% 170 1 254 Pays de la Loire 3 538 5.7% 2 378 5.8% 290 647 Aquitaine 3 200 5.1% 2 501 6.1% 305 556 Bretagne 3 163 5.1% 2 173 5.3% 265 633 Midi-Pyrénées 2 865 4.6% 1 722 4.2% 210 723 Languedoc-Roussillon 2 616 4.2% 1 763 4.3% 215 645 Centre 2 544 4.1% 1 517 3.7% 185 729 Lorraine 2 342 3.7% 1 148 2.8% 140 887 Picardie 1 906 3.1% 779 1.9% 95 1 064 Alsace 1 847 3.0% 1 189 2.9% 145 675 Haute-Normandie 1 822 2.9% 943 2.3% 115 840 Poitou-Charentes 1 759 2.8% 1 189 2.9% 145 643 Bourgogne 1 637 2.6% 1 148 2.8% 140 620 Basse-Normandie 1 467 2.3% 943 2.3% 115 676

34000

36000

38000

40000

42000

44000

2003 2004 2005 2006 2007 2008 2009

Number of companiesprojected probable number of companies

0%

2%

4%

6%

8%

10%

12%

Turnover by top 4 comp. Turnover by top 10 comp. Turnover by top 50 comp.

Concentration

Vincent Boiteau, HEC EMBA, April 2012 Page 34

Auvergne 1 343 2.1% 984 2.4% 120 593 Champagne-Ardenne 1 336 2.1% 738 1.8% 90 787 Franche-Comté 1 168 1.9% 656 1.6% 80 774 Limousin 741 1.2% 492 1.2% 60 655 Corse 307 0.5% 246 0.6% 30 543

France 62469 100% 41 000 100% 5 000 712

Vincent Boiteau, HEC EMBA, April 2012 Page 35

Appendix B Real estate market

France Surface m2 Main residence 27 270 707 88 1 BR 1 581 313 40 2 BR 3 369 461 56 3 BR 5 726 812 73 4 BR 6 989 654 90 5 BR + 9 603 467 106 Second home 3 126 540Empty 2 182 219Total 32 579 466 Of which are houses 18 315 905 Of which are apartments 13 833 941

Dwelling size m2 Size of city 2002 2006 Rural or less than 5000h 98 106 5 000 to 50 000 h. 90 99 50 000 to 200 000 h. 86 91 more than 200 000 h. (excl. Paris) 83 87 Paris 70 73

Age group dwelling size m2 < 30 y.o. 6430-39 y.o. 6440-49 y.o. 6950-64 y.o. 97>65 y.o. 111

Types of inhabitants 1996 2006 Owner 56,0% 57,2% Renter 44,0% 42,8%

Dwelling yearly acquisition First home % tot 2002-2006 avg 2002-2006 avg

Total 608 890 100% 364 673 59.9%

By family type Single 75 502 12.4% 49 077 65.0% Couple w/o children 118 125 19.4% 72 292 61.2% Couple w/ children 378 121 62.1% 227 629 60.2% Single parent 28 618 4.7% 9 043 31.6% Other 8 524 1.4% 6 632 77.8%

Vincent Boiteau, HEC EMBA, April 2012 Page 36

Social status 1st quartile 38 360 6.3% 26 085 68.0% 2nd quartile 118 734 19.5% 72 546 61.1% 3rd quartile 203 978 33.5% 135 849 66.6% 4th quartile 247 818 40.7% 130 600 52.7%

Age less than 30 y.o. 122 996 20.2% 108 359 88.1% 30-39 y.o. 267 303 43.9% 172 410 64.5% 40-49 y.o. 142 480 23.4% 54 855 38.5% 50-64 y.o. 69 413 11.4% 21 032 30.3% 65 y.o. + 6 698 1.1% 1 112 16.6%

City Rural or less than 5000h 62 107 10.2% 39 873 64.2% suburbia 115 080 18.9% 71 925 62.5% Urban up to 100 000h 158 311 26.0% 92 612 58.5% Urban more than 100 000h 166 227 27.3% 96 245 57.9% Paris 107 165 17.6% 62 691 58.5%

Dwelling type New construction 196 063 32.2% 123 519 63.0% Second hand 412 827 67.8% 248 522 60.2%

Vincent Boiteau, HEC EMBA, April 2012 Page 37

Appendix C The renovation market

Renovation €103B

255,000 companies805,000 employees

Electrical, plumbing and other installation works

€47B

94,000 companies

351,000 employees

finishing works€44B

139,000 companies366,000 employees

Point of sale works€2.3B

2,100 companies9,500 employees

Carpentry and plastics works€11B

34,000 companies88,000 employees

Locksmith works€7.8B

13,000 companies54,000 employees

Floor and wall covering€5.8B

19,000 companies47,000 employees

Plaster works€5B

17,000 companies42,000 employees

Painting and window€11B

47,000 companies102,000 employees

other finishing works€1.1B

6,900 companies13,500 employees

Specialized works€11B

22,000 companies88,000 employees

Vincent Boiteau, HEC EMBA, April 2012 Page 38

Appendix D Prototype

Entry page

Project creation page

Vincent Boiteau, HEC EMBA, April 2012 Page 39

type de bien

•Maison•Appartement

Type

•Interieur•Exterieur

Combien de chambres•1•2•3

Type de salle

•Cuisine•Salle de bain•chambre à coucher...etc

Taille

•Grande,Moyenne,Petite?•je connais la taille

Combien de portes

•1•2,3...etc

Combien de fenetres

•1•2,3...etc

Description

•Moulures•Radiateurs...etc

Vincent Boiteau, HEC EMBA, April 2012 Page 40

Appendix E P&L