Strands: How to Win the FinTech Race

25

© Strands Inc. 201 HOW TO WIN THE FINTECH RACE? 21st of May 2015, Brussels Transform threats into opportunities in the competitive digital banking landscape Dario Lombardi, General Manager

-

Upload

strands-finance -

Category

Technology

-

view

581 -

download

1

Transcript of Strands: How to Win the FinTech Race

© Strands Inc. 201

HOW TO WIN THE FINTECH RACE?

21st of May 2015, Brussels

Transform threats into opportunities in the competitive digital banking landscape

Dario Lombardi, General Manager

© Strands Inc. 2015

LEADER’S VIEW

2

“They all want to eat our lunch.”– Jamie Dimon, JP Morgan Chase CEO

© Strands Inc. 2015

LEADER’S VIEW

3© Strands Inc. 2014

“We are on the leading edge of a technology revolution in financial services.”– Anthony Jenkins, Barclays CEO

© Strands Inc. 2015

LEADER’S VIEW

4

“Banks are losing their monopoly on banking.”

“In the future, BBVA will be a software company!– Francisco González, BBVA CEO

© Strands Inc. 2015 5

COMPETITIVE LANDSCAPE

Source: The Economist Intelligence Unit 2015, “The 3Rs of retail banking”

36%

21%

13%

Technology & e-commerce (ie Amazon, Apple)

11% in 2011

Non-financial service firms (ie traditional retailers, telecom firms)

New banks (branch, online, telephones, etc)

© Strands Inc. 2015 6

TOP TRENDS UP TO 2020

0

0,11

5

0,23

0,34

5

0,46

35%

46%

46%The impact of regulation

Changing customer behaviour and demands

New entrants/competitors

Source: The Economist Intelligence Unit 2015, “The 3Rs of retail banking”

© Strands Inc. 2015 7

MILLENNIALS ARE THE LESS LOYAL

Source: Viacom Media Networks (2013)

71%

would rather go to the dentist than listen to

what banks are saying

33%

are open to switching banks in the next

90 days

73%

would be more excited about a new offering in financial services from

Google, Amazon, Apple, Paypal, or Square

70%

in 5 years, the way we pay for things will be

totally different

© Strands Inc. 2015

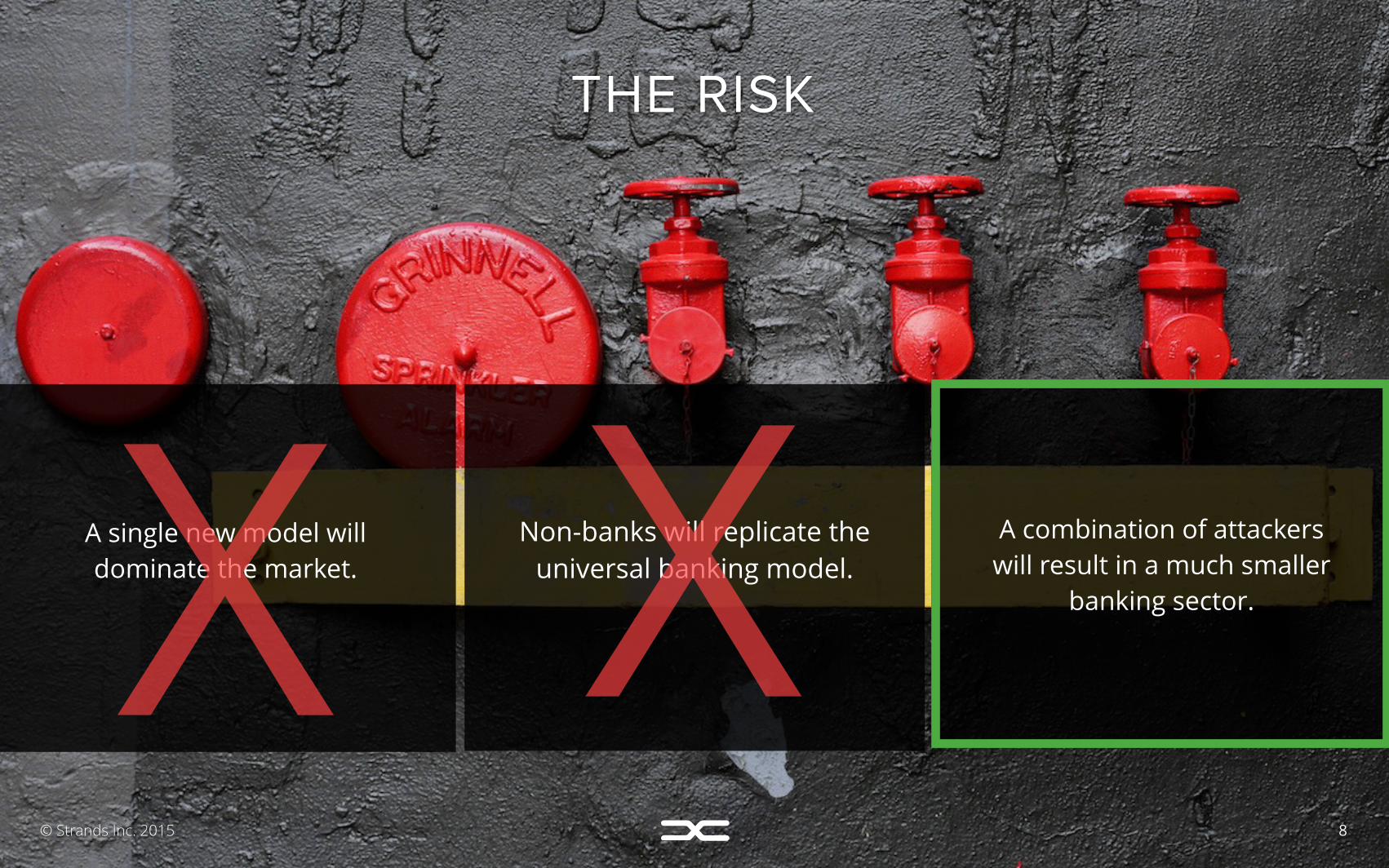

THE RISK

8

Non-banks will replicate the universal banking model.

A single new model will dominate the market. X X A combination of attackers

will result in a much smaller banking sector.

© Strands Inc. 2015

THE OPPORTUNITY

9

“(…) the good news is that we still have one significant advantage, which is the vast array of financial and non-financial DATA that we accumulate.”

– Francisco González, BBVA CEO

© Strands Inc. 2015 10

BIG DATA AND DIGITAL RELATIONS

© Strands Inc. 2014 11

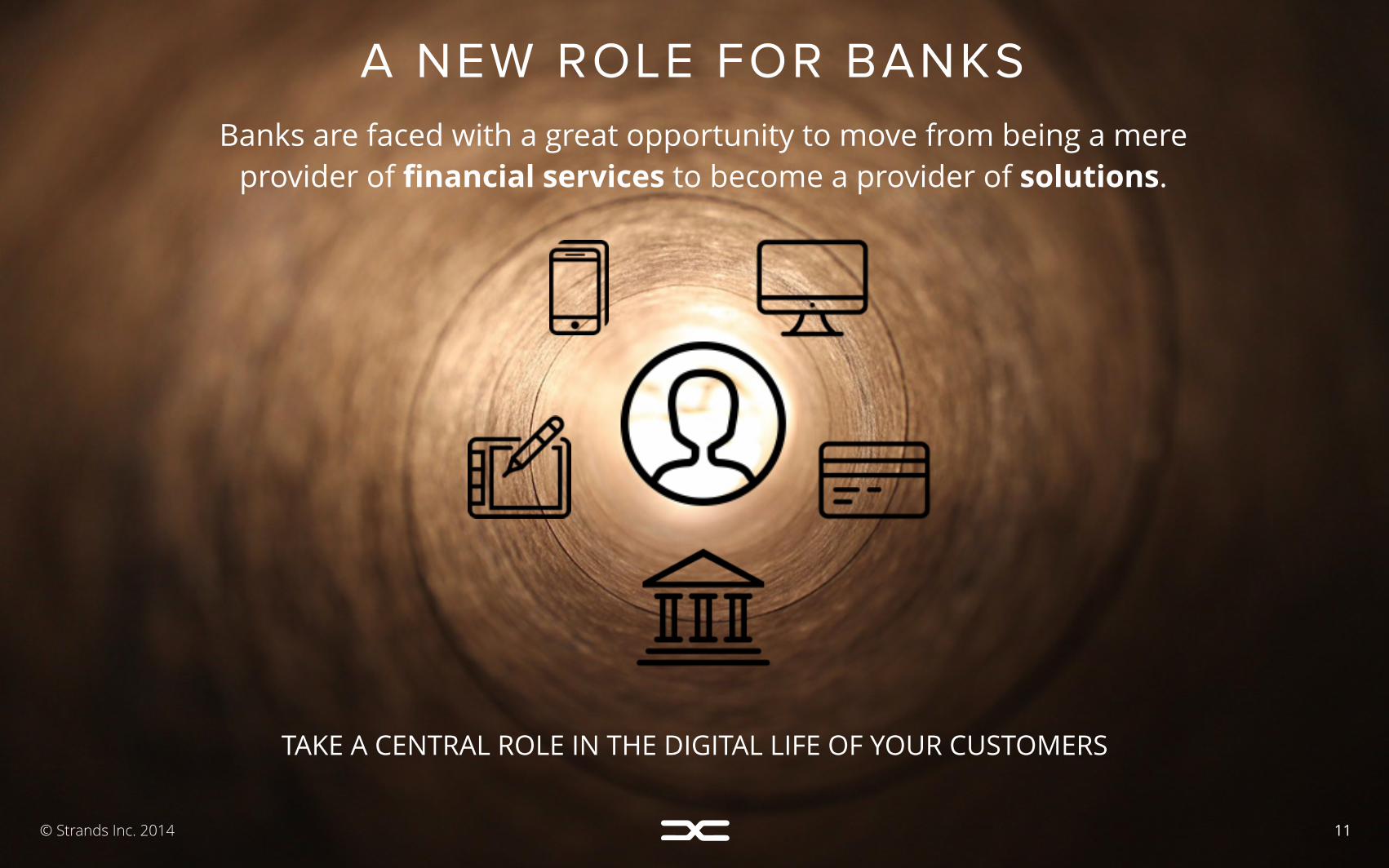

A NEW ROLE FOR BANKS

Banks are faced with a great opportunity to move from being a mere provider of financial services to become a provider of solutions.

TAKE A CENTRAL ROLE IN THE DIGITAL LIFE OF YOUR CUSTOMERS

© Strands Inc. 2015 12

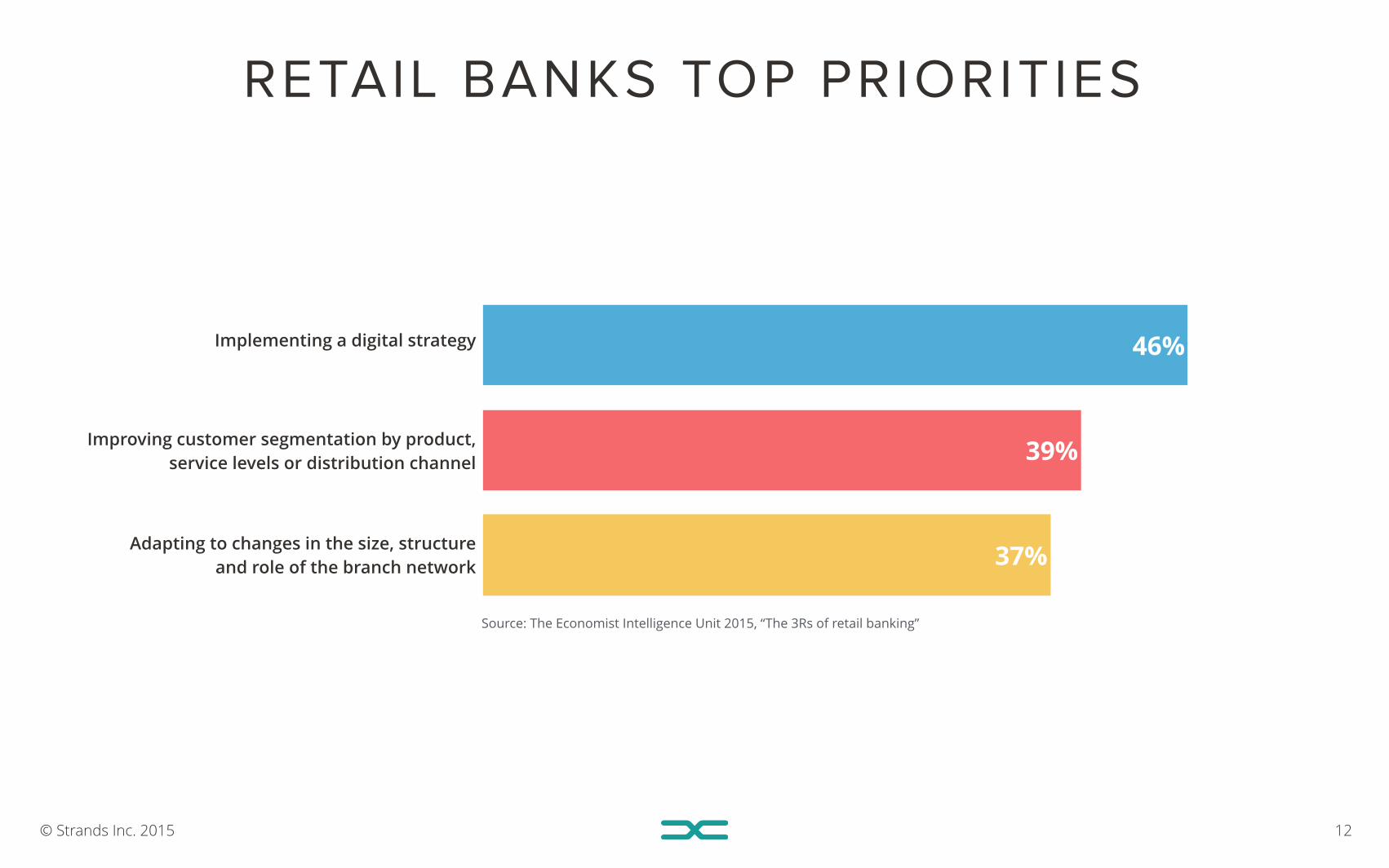

RETAIL BANKS TOP PRIORITIES

0

0,11

5

0,23

0,34

5

0,46

37%

39%

46%Implementing a digital strategy

Improving customer segmentation by product, service levels or distribution channel

Adapting to changes in the size, structure and role of the branch network

Source: The Economist Intelligence Unit 2015, “The 3Rs of retail banking”

© Strands Inc. 2015 13

DIGITAL INVESTMENT DRIVERS

0

0,1

0,2

0,3

0,4

12%

28%

40%Cross- and up-selling

New customer acquisition

Pricing optimisation

Source: The Economist Intelligence Unit 2015, “The 3Rs of retail banking”

© Strands Inc. 2015

CARD LINKED OFFERS

14

HELP

CLO

How do I find the

most relevant

offers?

How can I attract

new customers?

IsHow well do I know

my customers?

© Strands Inc. 2015 15

UNLEASH THE VALUE OF CUSTOMER DATA

Strands CLO is a marketing tool that enables retailers to target highly relevant

deals to card-holders through digital banking channels

© Strands Inc. 2015 16

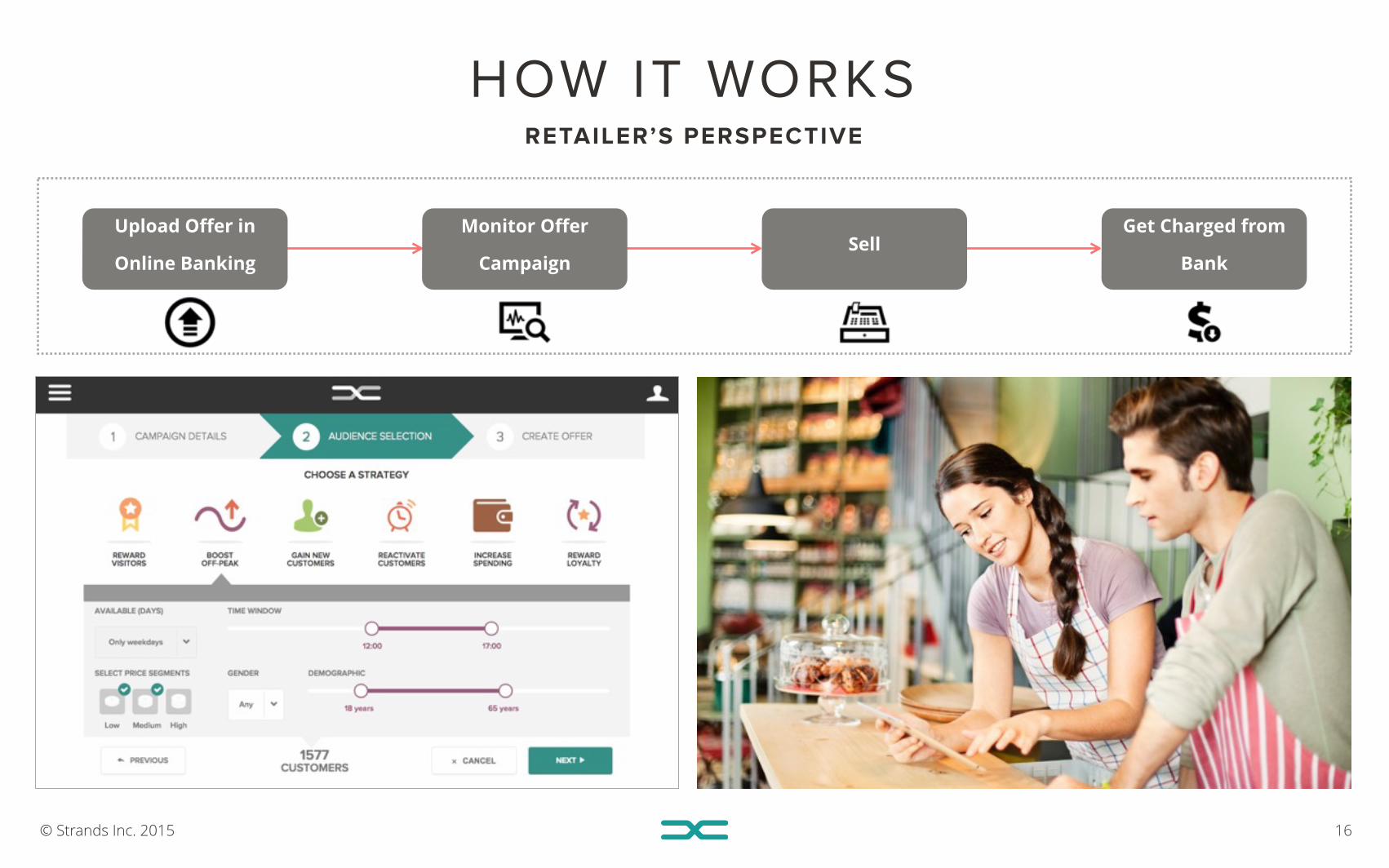

HOW IT WORKSRETAILER’S PERSPECTIVE

Get Charged from

Bank

Upload Offer in

Online Banking

Monitor Offer

CampaignSell

© Strands Inc. 2015 17

HOW IT WORKSCARD-HOLDER’S PERSPECTIVE

Accept Offer in

Digital BankingBuy at Merchant Pay with Bank Card

Get Cash Back in

Your Account

© Strands Inc. 2015 18

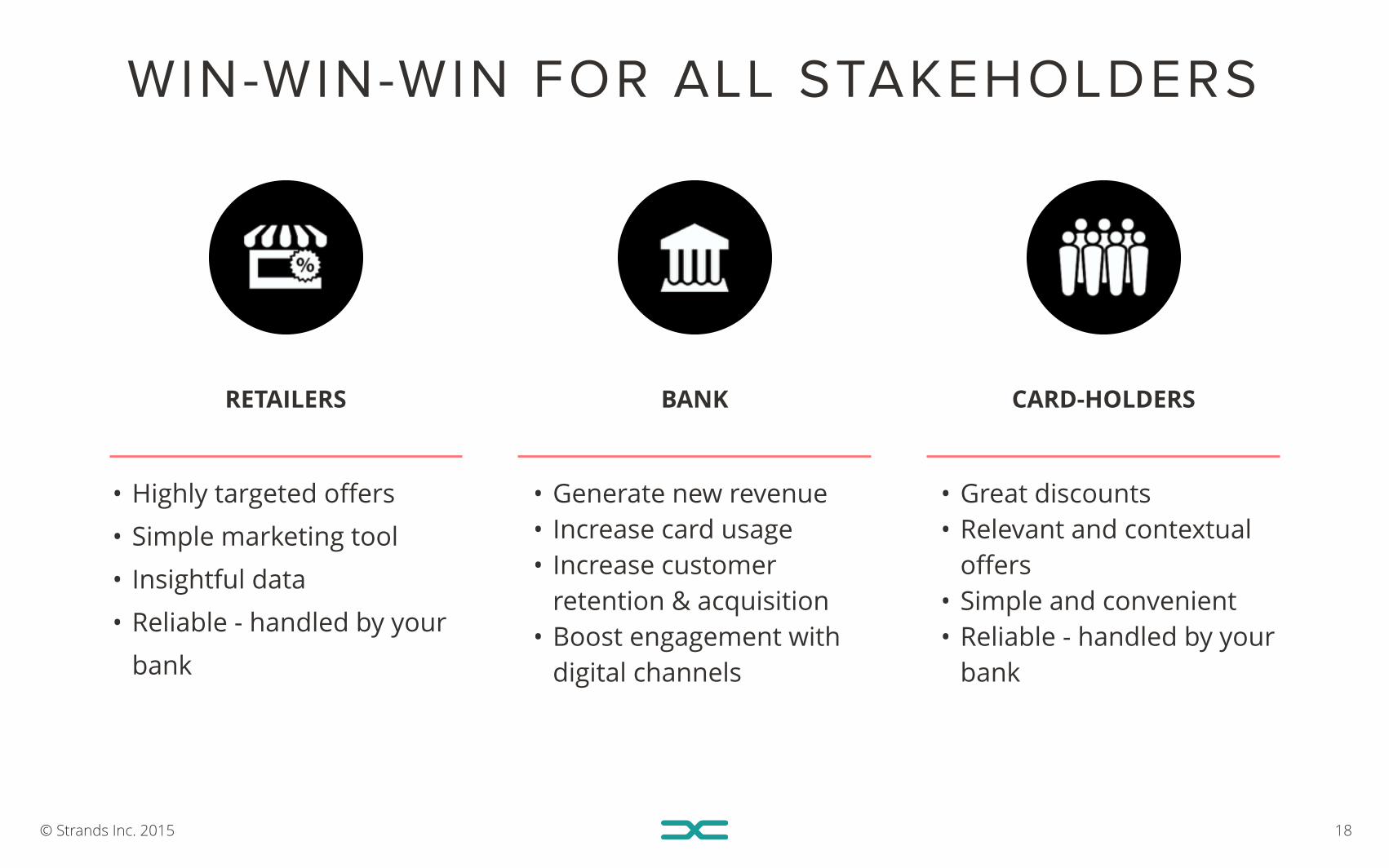

WIN-WIN-WIN FOR ALL STAKEHOLDERS

RETAILERS

• Highly targeted offers

• Simple marketing tool

• Insightful data

• Reliable - handled by your

bank

BANK

• Generate new revenue • Increase card usage • Increase customer

retention & acquisition • Boost engagement with

digital channels

CARD-HOLDERS

• Great discounts • Relevant and contextual

offers • Simple and convenient • Reliable - handled by your

bank

© Strands Inc. 2015 19

Hi, my name is Mario and I like wearing trendy clothes

Hi, my name is Sarah and have a shop selling trendy shoes

© Strands Inc. 2015 20

Engage Target Retain & Grow+ =

STRANDS’ VISION

ACCELERATE PRODUCT INNOVATION: DON’T DO IT INTERNALLY > PARTNER WITH A FINTECH PROVIDER

© Strands Inc. 2015

CLO CARD-LINKED

OFFERS

REC RECOMMENDER

BFM BUSINESS FINANCIAL

MANAGEMENT

PFM PERSONAL FINANCIAL

MANAGEMENT

21

STRANDS FINANCE SUITE

Engage

Target

Reta

in &

Gro

w

STRANDS LOOP

© Strands Inc. 2015 22

Deutsche Bank

OUR CLIENTS

© Strands Inc. 2015

CONCLUSIONS

23

FIND THE RIGHT TECHNOLOGY PARTNER & OCCUPY CENTRAL ROLE

IN CUSTOMERS LIVES

TECHNOLOGY IS DISRUPTING BANKS’

COMPETITIVE LANDSCAPE

BIG DATA AND DIGITAL RELATIONS ARE

BANKS’ MOST VALUABLE ASSETS

© Strands Inc. 2015

THANK YOU!

24

DARIO [email protected]

@dlombardiwin

WEB finance.strands.com

BLOG blog.strands.com

TWITTER @StrandsFinance

© Strands Inc. 2015 25

ABOUT STRANDSSTRANDS develops innovative software solutions that enable financial institutions & retailers to offer personalized customer experiences and create new revenue streams through digital channels.

The Strands Finance Suite includes white-label software solutions such as Personal Financial Management (PFM), Business Financial Management (BFM), and Card-Linked Offers (CLO), among others. In 2008, Strands revolutionized online banking by deploying the first PFM in Europe.

From our Barcelona HQ and offices in San Francisco, Miami, Madrid & Buenos Aires, we serve market leaders like Barclays, Deutsche Bank, BBVA, BNP Paribas, Bank of Montreal (BMO), Carrefour and Panasonic.