Store of the Future 2017 - lp.planetretail.net Final 11 10... · 3 | Store of the Future 2017...

65

1 | Store of the Future 2017 Store of the Future WINNING STRATEGY

-

Upload

vuongkhanh -

Category

Documents

-

view

214 -

download

0

Transcript of Store of the Future 2017 - lp.planetretail.net Final 11 10... · 3 | Store of the Future 2017...

1 | Store of the Future 2017

Store of theFuture

WINNING STRATEGY

2 | Store of the Future 2017

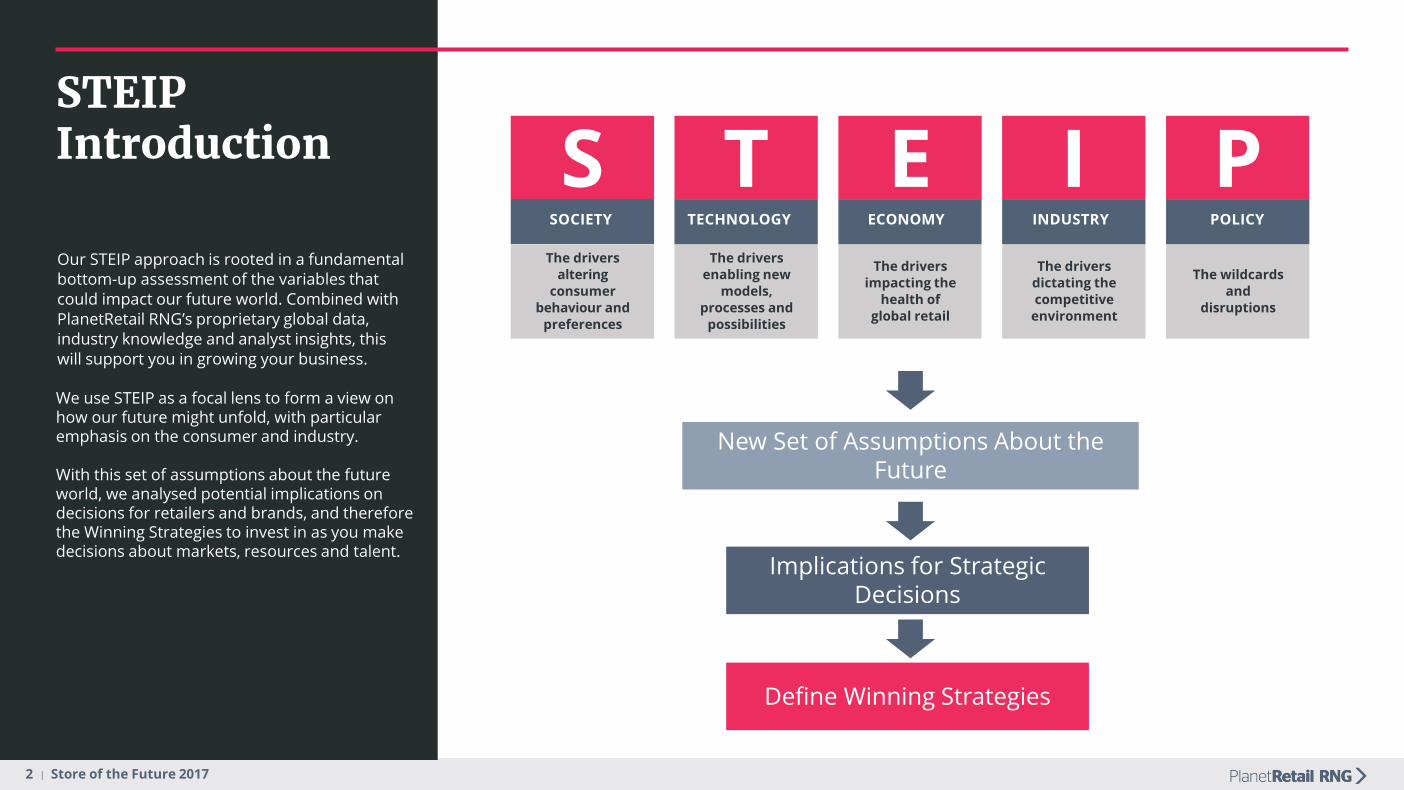

STEIPIntroduction

New Set of Assumptions About the Future

Implications for Strategic Decisions

SSOCIETY

The driversaltering

consumerbehaviour and

preferences

TECHNOLOGY

The driversenabling new

models,processes and

possibilities

ECONOMY

The driversimpacting the

health of global retail

INDUSTRY

The driversdictating thecompetitive

environment

POLICY

T E I PThe wildcards

and disruptions

Our STEIP approach is rooted in a fundamental bottom-up assessment of the variables that could impact our future world. Combined with PlanetRetail RNG’s proprietary global data, industry knowledge and analyst insights, this will support you in growing your business.

We use STEIP as a focal lens to form a view on how our future might unfold, with particular emphasis on the consumer and industry.

With this set of assumptions about the future world, we analysed potential implications on decisions for retailers and brands, and therefore the Winning Strategies to invest in as you make decisions about markets, resources and talent.

Define Winning Strategies

3 | Store of the Future 2017

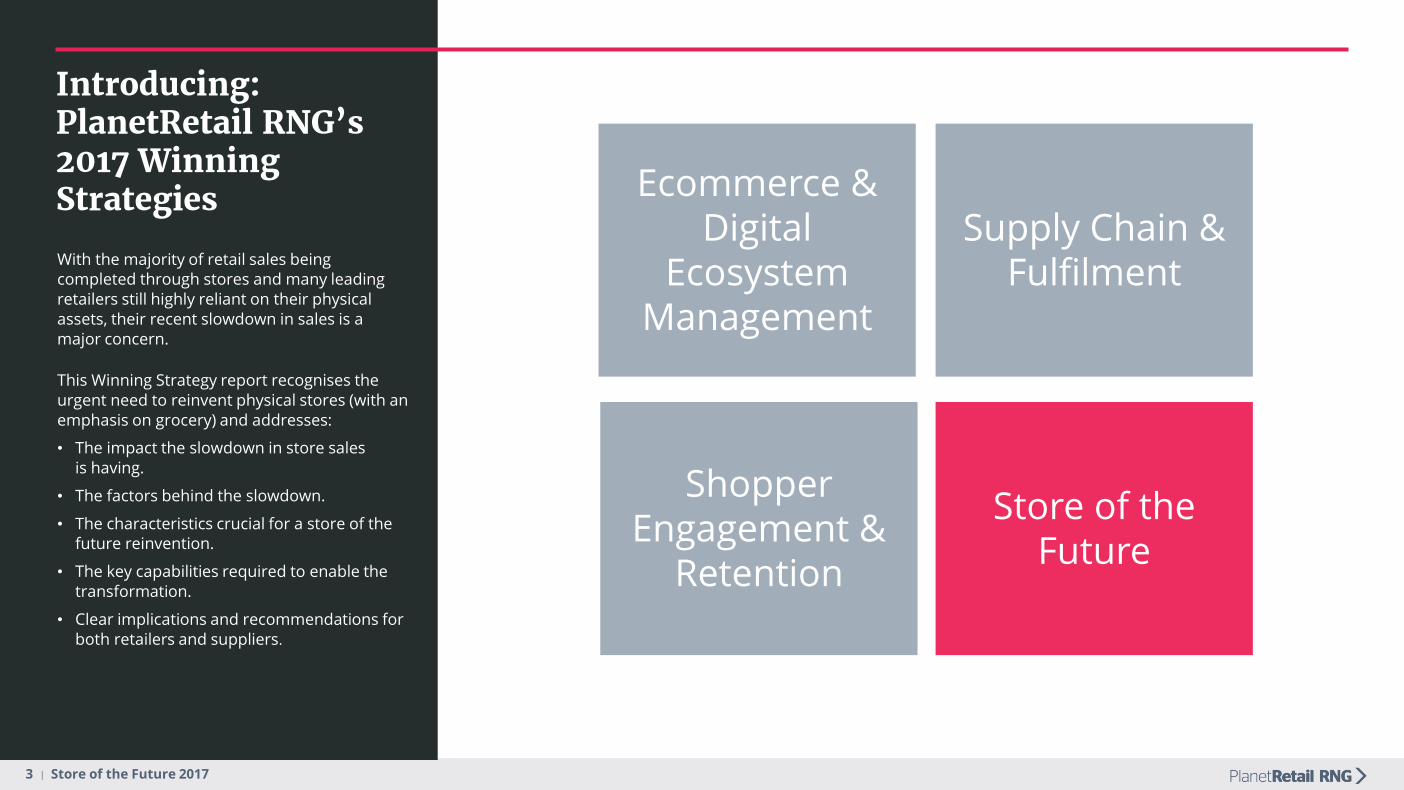

Introducing: PlanetRetail RNG’s 2017 Winning Strategies

With the majority of retail sales being completed through stores and many leading retailers still highly reliant on their physical assets, their recent slowdown in sales is a major concern.

This Winning Strategy report recognises the urgent need to reinvent physical stores (with an emphasis on grocery) and addresses:

• The impact the slowdown in store sales is having.

• The factors behind the slowdown.

• The characteristics crucial for a store of the future reinvention.

• The key capabilities required to enable the transformation.

• Clear implications and recommendations for both retailers and suppliers.

Ecommerce & Digital

Ecosystem Management

Supply Chain & Fulfilment

Shopper Engagement &

Retention

Store of the Future

4 | Store of the Future 2017

Contents1. Situational Analysis 2. STEIP Drivers of Change3. Store of the Future Explained4. Key Capabilities5. The Future World6. Implications for Retailers

and Suppliers

Research for this report included interviews with leading retailers currently pursuing their own Store of the Future initiatives.

5 | Store of the Future 2017

Situational Analysis

6 | Store of the Future 2017

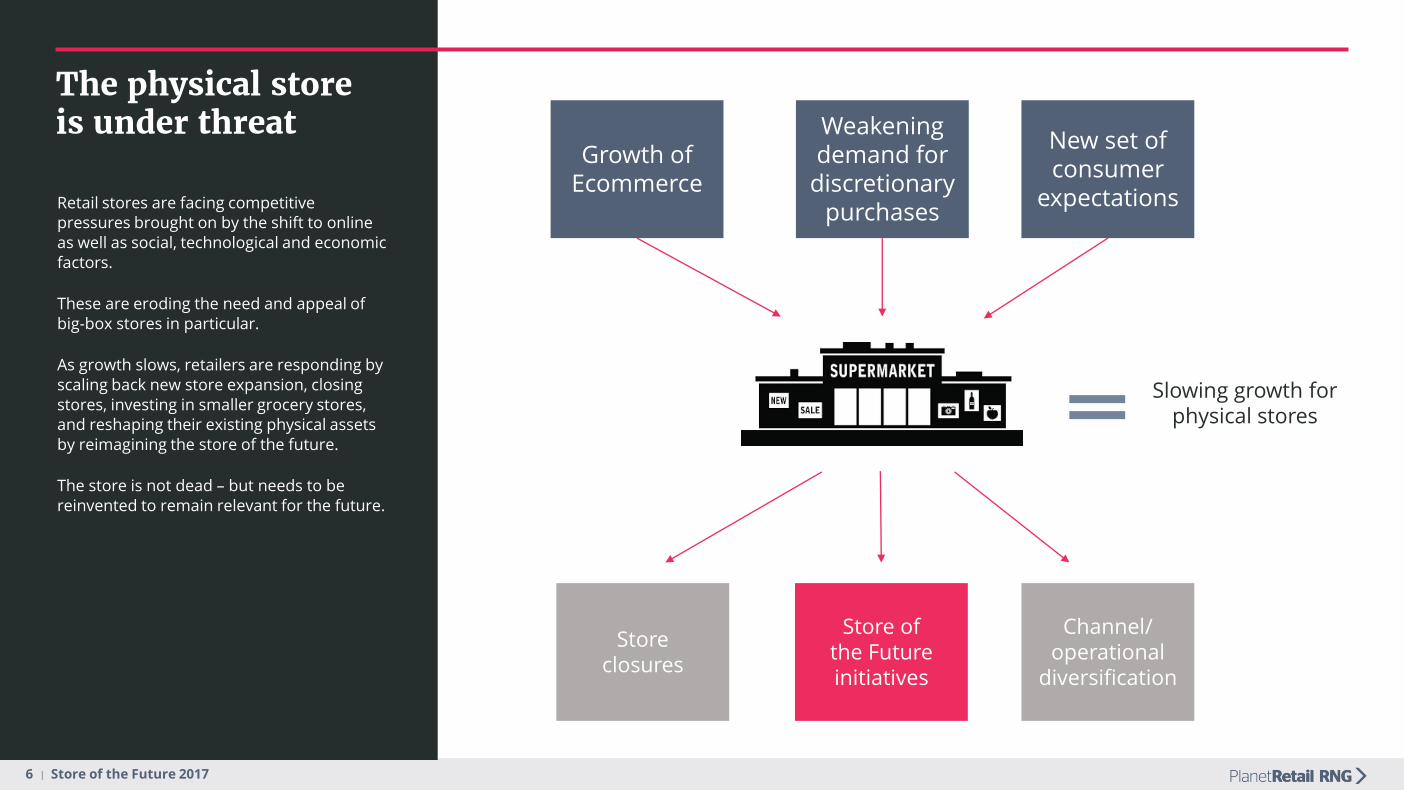

The physical store is under threat

Retail stores are facing competitive pressures brought on by the shift to online as well as social, technological and economic factors.

These are eroding the need and appeal of big-box stores in particular.

As growth slows, retailers are responding by scaling back new store expansion, closing stores, investing in smaller grocery stores, and reshaping their existing physical assets by reimagining the store of the future.

The store is not dead – but needs to be reinvented to remain relevant for the future.

Growth ofEcommerce

Weakening demand for

discretionary purchases

New set of consumer

expectations

Slowing growth for physical stores

Storeclosures

Store ofthe Future initiatives

Channel/ operational

diversification

7 | Store of the Future 2017

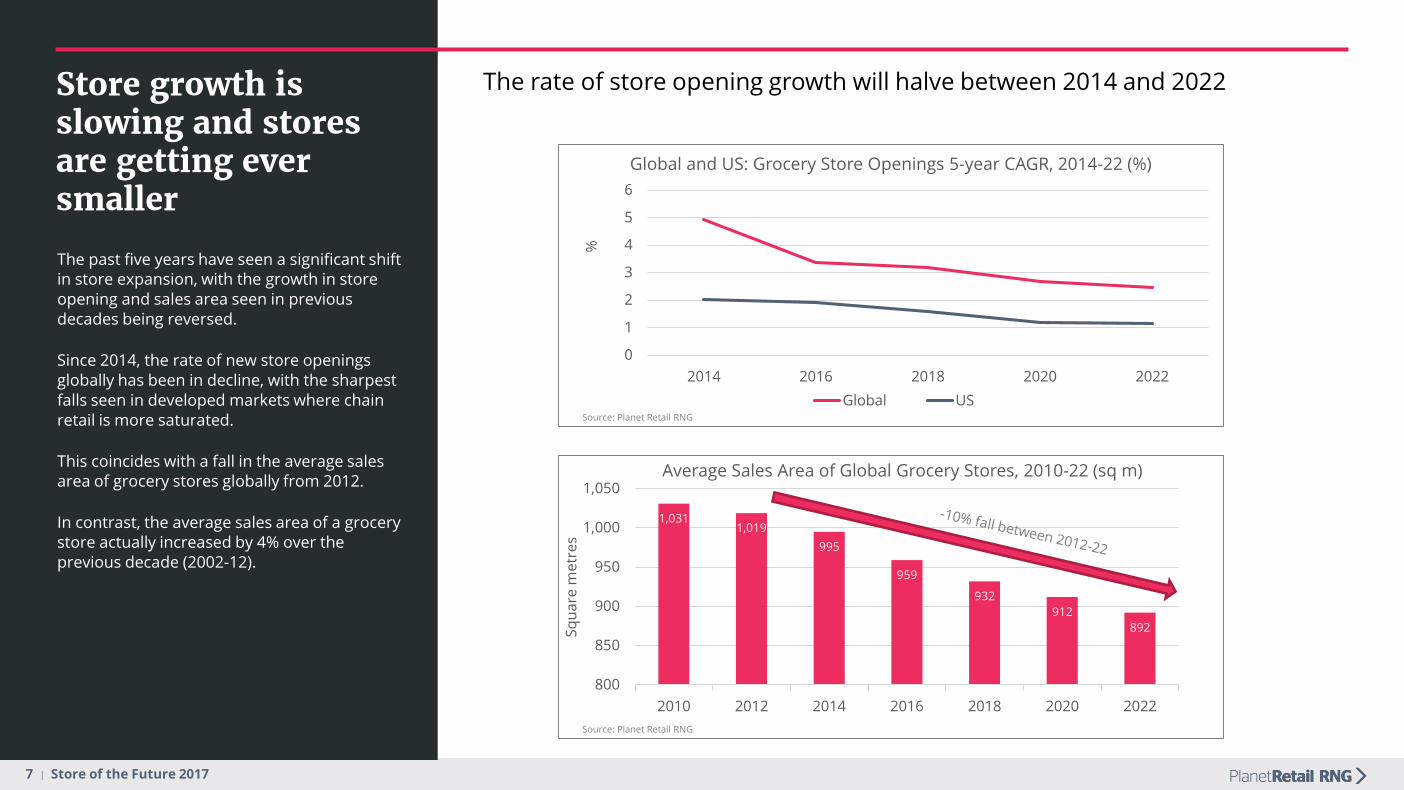

Store growth is slowing and stores are getting ever smaller

The past five years have seen a significant shift in store expansion, with the growth in store opening and sales area seen in previous decades being reversed.

Since 2014, the rate of new store openings globally has been in decline, with the sharpest falls seen in developed markets where chain retail is more saturated.

This coincides with a fall in the average sales area of grocery stores globally from 2012.

In contrast, the average sales area of a grocery store actually increased by 4% over the previous decade (2002-12).

1,0311,019

995

959

932

912

892

800

850

900

950

1,000

1,050

2010 2012 2014 2016 2018 2020 2022

Sq

ua

re m

etr

es

Average Sales Area of Global Grocery Stores, 2010-22 (sq m)

0

1

2

3

4

5

6

2014 2016 2018 2020 2022

%

Global and US: Grocery Store Openings 5-year CAGR, 2014-22 (%)

Global USSource: Planet Retail RNG

Source: Planet Retail RNG

The rate of store opening growth will halve between 2014 and 2022

8 | Store of the Future 2017

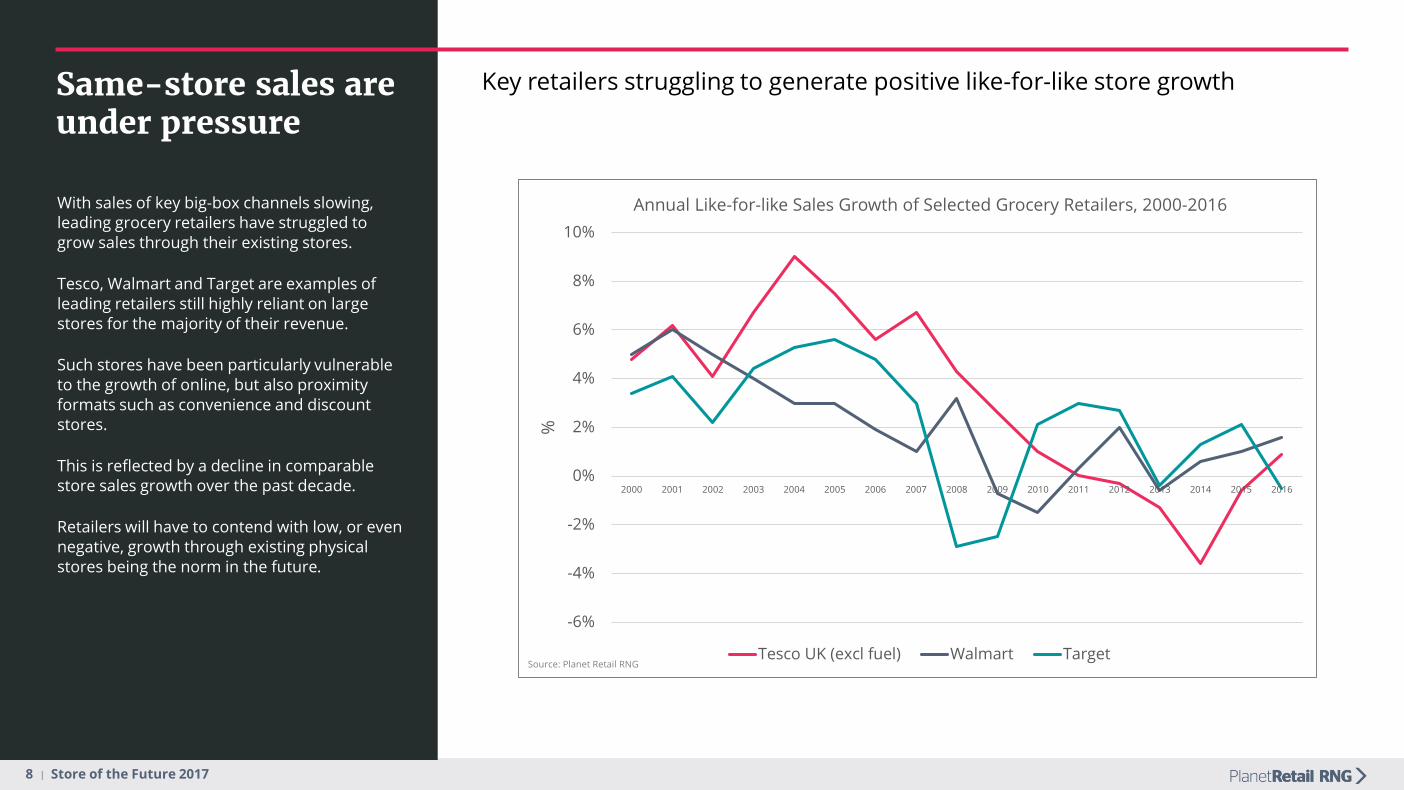

Same-store sales are under pressure

With sales of key big-box channels slowing, leading grocery retailers have struggled to grow sales through their existing stores.

Tesco, Walmart and Target are examples of leading retailers still highly reliant on large stores for the majority of their revenue.

Such stores have been particularly vulnerable to the growth of online, but also proximity formats such as convenience and discount stores.

This is reflected by a decline in comparable store sales growth over the past decade.

Retailers will have to contend with low, or even negative, growth through existing physical stores being the norm in the future.

Key retailers struggling to generate positive like-for-like store growth

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

%

Annual Like-for-like Sales Growth of Selected Grocery Retailers, 2000-2016

Tesco UK (excl fuel) Walmart TargetSource: Planet Retail RNG

9 | Store of the Future 2017

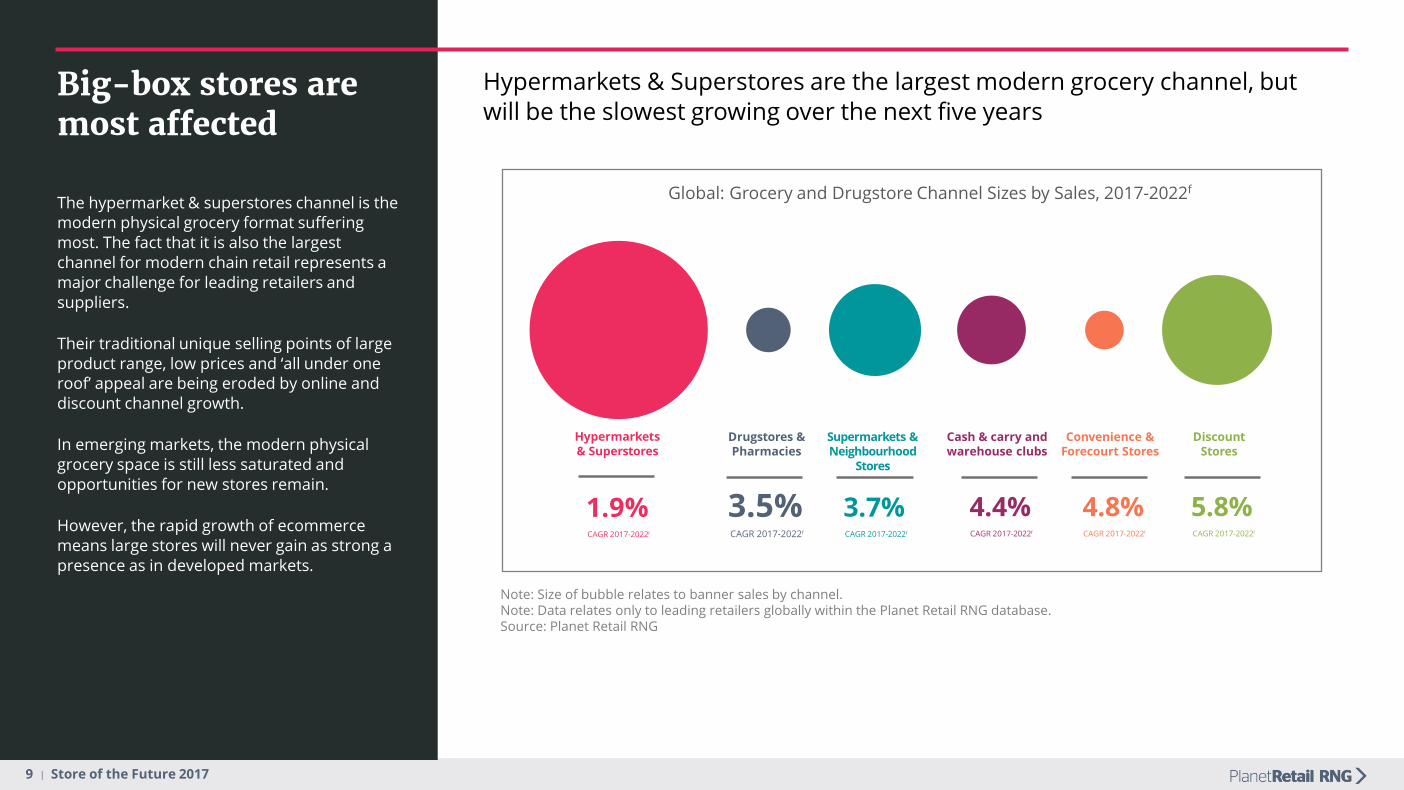

Big-box stores are most affected

The hypermarket & superstores channel is the modern physical grocery format suffering most. The fact that it is also the largest channel for modern chain retail represents a major challenge for leading retailers and suppliers.

Their traditional unique selling points of large product range, low prices and ‘all under one roof’ appeal are being eroded by online and discount channel growth.

In emerging markets, the modern physical grocery space is still less saturated and opportunities for new stores remain.

However, the rapid growth of ecommerce means large stores will never gain as strong a presence as in developed markets.

Note: Size of bubble relates to banner sales by channel.Note: Data relates only to leading retailers globally within the Planet Retail RNG database.Source: Planet Retail RNG

Hypermarkets & Superstores are the largest modern grocery channel, but will be the slowest growing over the next five years

Global: Grocery and Drugstore Channel Sizes by Sales, 2017-2022f

Hypermarkets& Superstores

1.9%CAGR 2017-2022f

Drugstores &Pharmacies

3.5%CAGR 2017-2022f

Supermarkets & Neighbourhood

Stores

3.7%CAGR 2017-2022f

Convenience & Forecourt Stores

4.8%CAGR 2017-2022f

Discount Stores

5.8%CAGR 2017-2022f

Cash & carry and warehouse clubs

4.4%CAGR 2017-2022f

10 | Store of the Future 2017

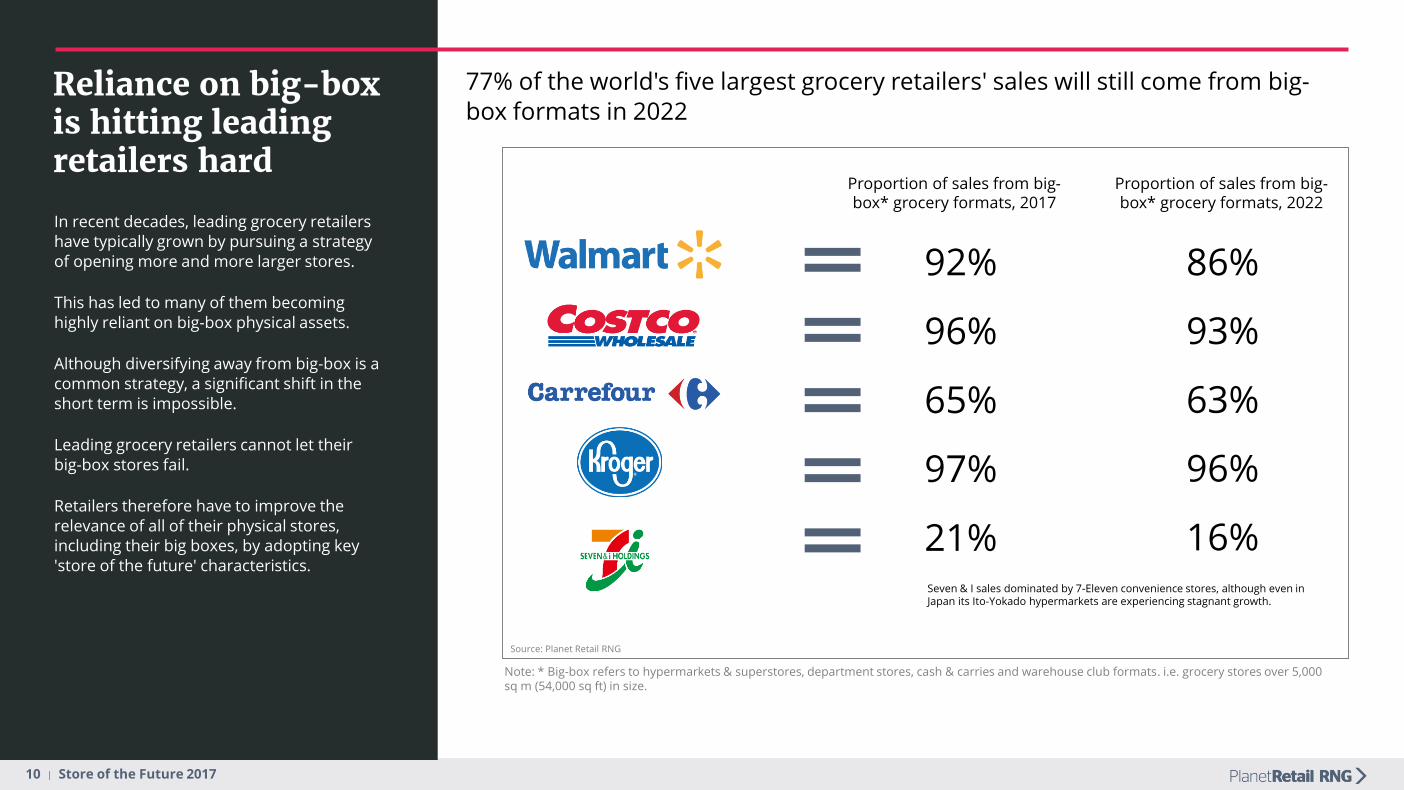

Reliance on big-box is hitting leading retailers hard

In recent decades, leading grocery retailers have typically grown by pursuing a strategy of opening more and more larger stores.

This has led to many of them becoming highly reliant on big-box physical assets.

Although diversifying away from big-box is a common strategy, a significant shift in the short term is impossible.

Leading grocery retailers cannot let their big-box stores fail.

Retailers therefore have to improve the relevance of all of their physical stores, including their big boxes, by adopting key 'store of the future' characteristics.

Note: * Big-box refers to hypermarkets & superstores, department stores, cash & carries and warehouse club formats. i.e. grocery stores over 5,000 sq m (54,000 sq ft) in size.

92%

96%

65%

97%

21%

Proportion of sales from big-box* grocery formats, 2017

77% of the world's five largest grocery retailers' sales will still come from big-box formats in 2022

Seven & I sales dominated by 7-Eleven convenience stores, although even in Japan its Ito-Yokado hypermarkets are experiencing stagnant growth.

Proportion of sales from big-box* grocery formats, 2022

86%

93%

63%

96%

16%

Source: Planet Retail RNG

11 | Store of the Future 2017

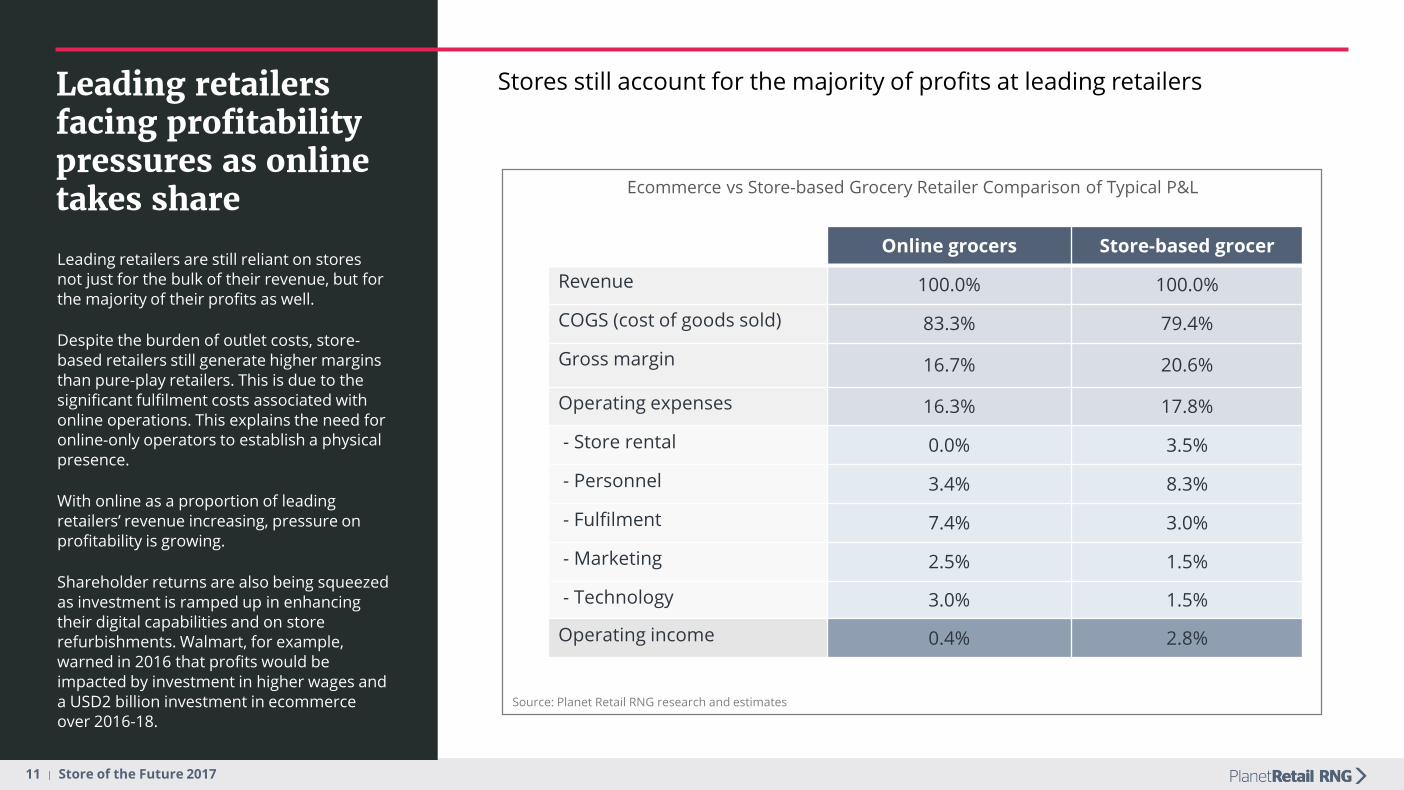

Leading retailers facing profitability pressures as online takes share

Leading retailers are still reliant on stores not just for the bulk of their revenue, but for the majority of their profits as well.

Despite the burden of outlet costs, store-based retailers still generate higher margins than pure-play retailers. This is due to the significant fulfilment costs associated with online operations. This explains the need for online-only operators to establish a physical presence.

With online as a proportion of leading retailers’ revenue increasing, pressure on profitability is growing.

Shareholder returns are also being squeezed as investment is ramped up in enhancing their digital capabilities and on store refurbishments. Walmart, for example, warned in 2016 that profits would be impacted by investment in higher wages and a USD2 billion investment in ecommerce over 2016-18.

Stores still account for the majority of profits at leading retailers

Online grocers Store-based grocer

Revenue 100.0% 100.0%

COGS (cost of goods sold) 83.3% 79.4%

Gross margin 16.7% 20.6%

Operating expenses 16.3% 17.8%

- Store rental 0.0% 3.5%

- Personnel 3.4% 8.3%

- Fulfilment 7.4% 3.0%

- Marketing 2.5% 1.5%

- Technology 3.0% 1.5%

Operating income 0.4% 2.8%

Ecommerce vs Store-based Grocery Retailer Comparison of Typical P&L

Source: Planet Retail RNG research and estimates

12 | Store of the Future 2017

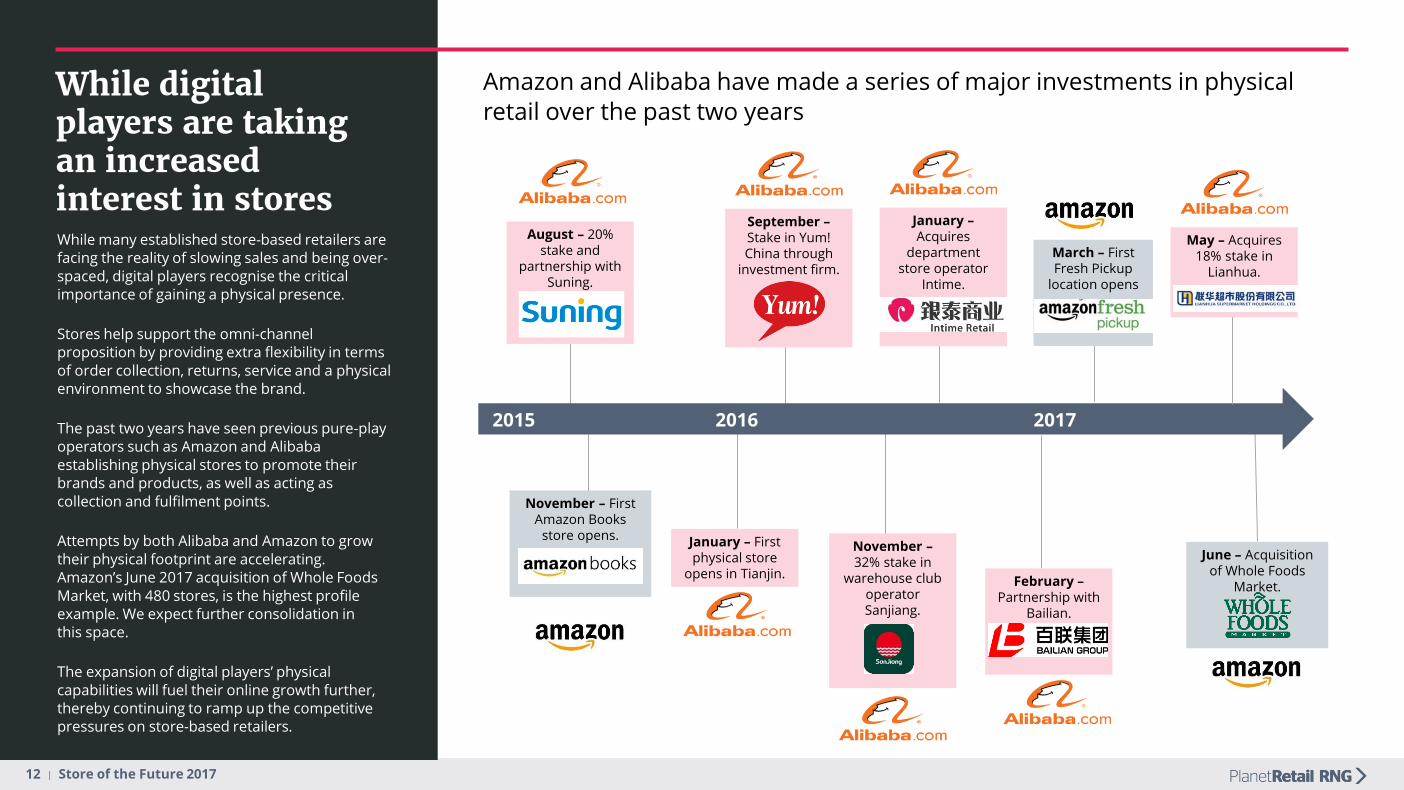

While digital players are taking an increased interest in storesWhile many established store-based retailers are facing the reality of slowing sales and being over-spaced, digital players recognise the critical importance of gaining a physical presence.

Stores help support the omni-channel proposition by providing extra flexibility in terms of order collection, returns, service and a physical environment to showcase the brand.

The past two years have seen previous pure-play operators such as Amazon and Alibaba establishing physical stores to promote their brands and products, as well as acting as collection and fulfilment points.

Attempts by both Alibaba and Amazon to grow their physical footprint are accelerating. Amazon’s June 2017 acquisition of Whole Foods Market, with 480 stores, is the highest profile example. We expect further consolidation in this space.

The expansion of digital players’ physical capabilities will fuel their online growth further, thereby continuing to ramp up the competitive pressures on store-based retailers.

2016 2017

November – First Amazon Books

store opens.

August – 20% stake and

partnership with Suning.

2015

January – First physical store

opens in Tianjin.

September –Stake in Yum! China through

investment firm.

June – Acquisition of Whole Foods

Market.

November –32% stake in

warehouse club operator Sanjiang.

January –Acquires

department store operator

Intime.

February –Partnership with

Bailian.

May – Acquires 18% stake in

Lianhua.

March – First Fresh Pickup

location opens

Amazon and Alibaba have made a series of major investments in physical retail over the past two years

13 | Store of the Future 2017

STEIP Drivers of Change

14 | Store of the Future 2017

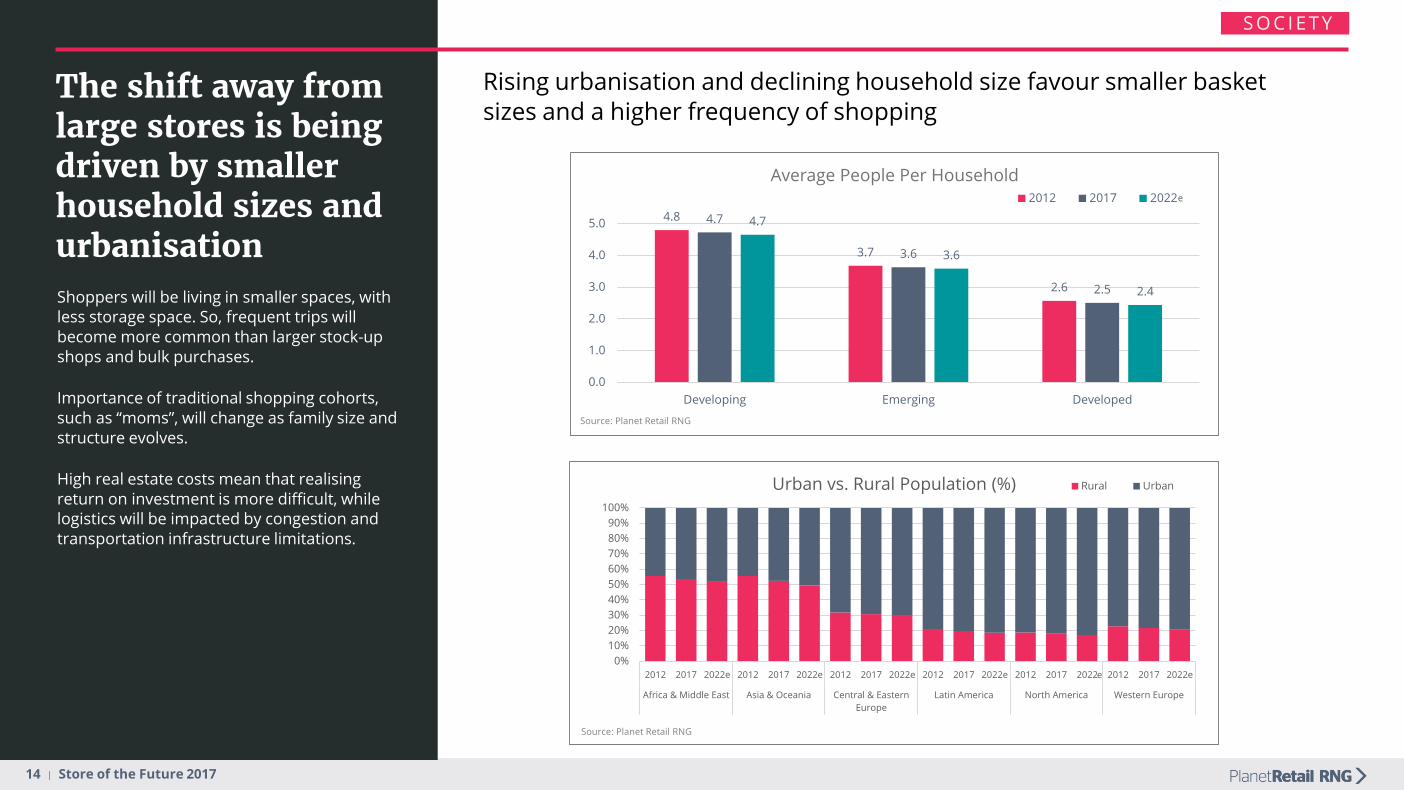

The shift away from large stores is being driven by smaller household sizes and urbanisationShoppers will be living in smaller spaces, with less storage space. So, frequent trips will become more common than larger stock-up shops and bulk purchases.

Importance of traditional shopping cohorts, such as “moms”, will change as family size and structure evolves.

High real estate costs mean that realising return on investment is more difficult, while logistics will be impacted by congestion and transportation infrastructure limitations.

S O C I E T Y

4.8

3.7

2.6

4.7

3.6

2.5

4.7

3.6

2.4

0.0

1.0

2.0

3.0

4.0

5.0

Developing Emerging Developed

Average People Per Household2012 2017 2022

Source: Planet Retail RNG

Source: Planet Retail RNG

Rising urbanisation and declining household size favour smaller basket sizes and a higher frequency of shopping

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2017 2022e 2012 2017 2022e 2012 2017 2022e 2012 2017 2022e 2012 2017 2022 2012 2017 2022e

Africa & Middle East Asia & Oceania Central & Eastern

Europe

Latin America North America Western Europe

Urban vs. Rural Population (%) Rural Urban

e

e

15 | Store of the Future 2017

Shoppers increasingly value experiences

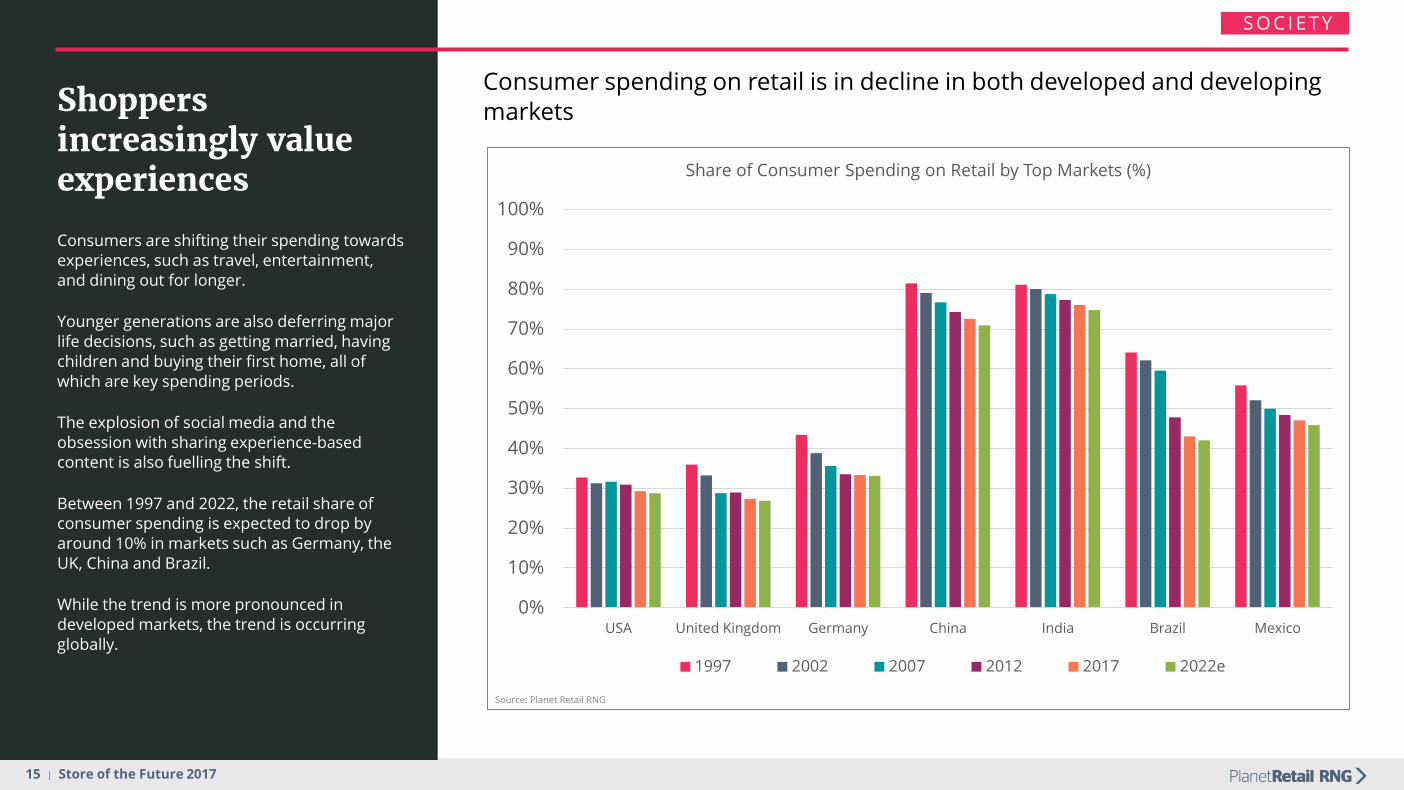

Consumers are shifting their spending towards experiences, such as travel, entertainment, and dining out for longer.

Younger generations are also deferring major life decisions, such as getting married, having children and buying their first home, all of which are key spending periods.

The explosion of social media and the obsession with sharing experience-based content is also fuelling the shift.

Between 1997 and 2022, the retail share of consumer spending is expected to drop by around 10% in markets such as Germany, the UK, China and Brazil.

While the trend is more pronounced in developed markets, the trend is occurring globally.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

USA United Kingdom Germany China India Brazil Mexico

Share of Consumer Spending on Retail by Top Markets (%)

1997 2002 2007 2012 2017 2022e

Source: Planet Retail RNG

S O C I E T Y

Consumer spending on retail is in decline in both developed and developing markets

16 | Store of the Future 2017

DemandsConvenience &

Flexibility

Hyper-Personalisation

Expectations

Seamless & Frictionless Experience

Demands ExperientialEnvironments

ImmediacyCritical – Instant

Gratification

Accountability Transparency &

Traceability

Asset-LightLifestyles

Consumer Empowerment

On-Demand Consumer

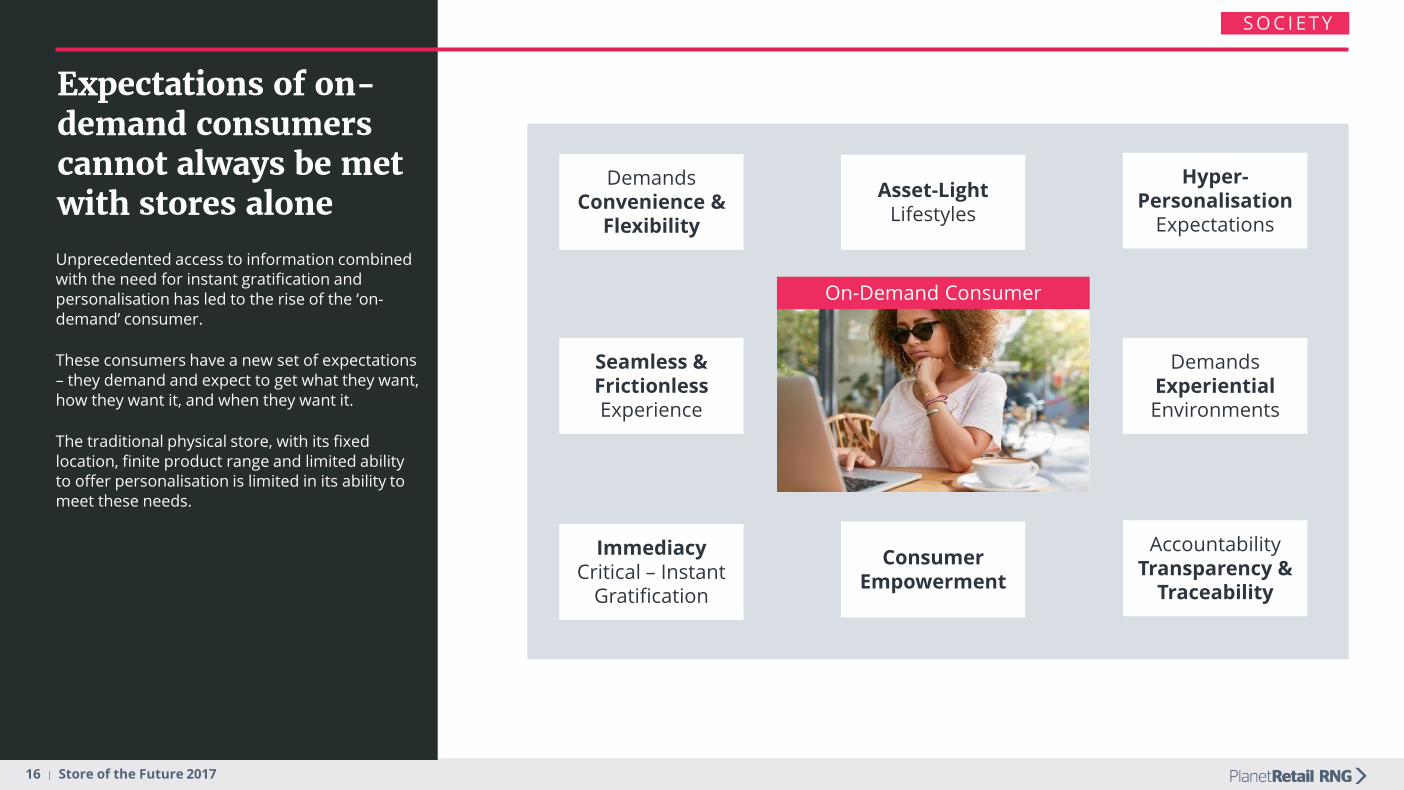

Expectations of on-demand consumers cannot always be met with stores aloneUnprecedented access to information combined with the need for instant gratification and personalisation has led to the rise of the ‘on-demand’ consumer.

These consumers have a new set of expectations – they demand and expect to get what they want, how they want it, and when they want it.

The traditional physical store, with its fixed location, finite product range and limited ability to offer personalisation is limited in its ability to meet these needs.

S O C I E T Y

17 | Store of the Future 2017

Digital access is opening up access to new consumers

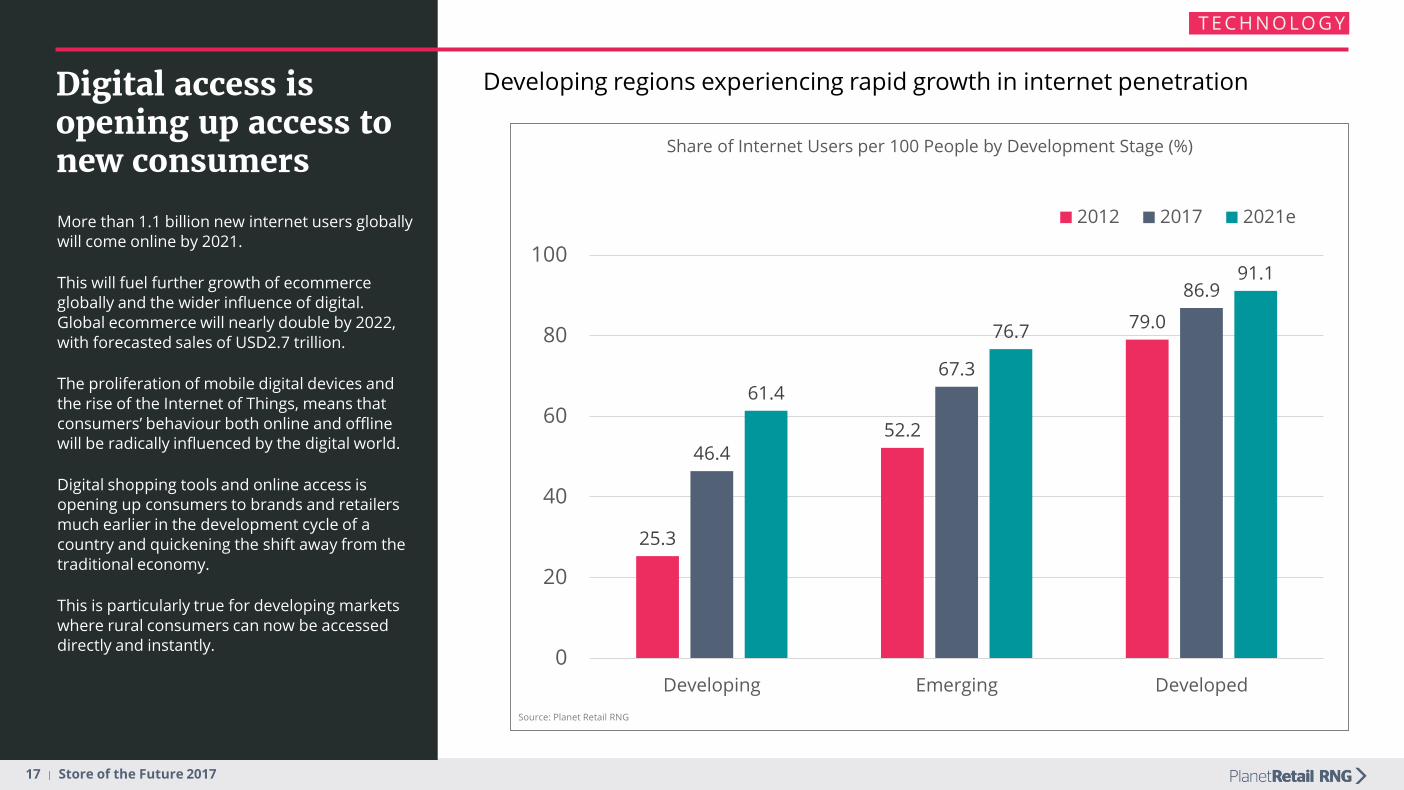

More than 1.1 billion new internet users globally will come online by 2021.

This will fuel further growth of ecommerce globally and the wider influence of digital. Global ecommerce will nearly double by 2022, with forecasted sales of USD2.7 trillion.

The proliferation of mobile digital devices and the rise of the Internet of Things, means that consumers’ behaviour both online and offline will be radically influenced by the digital world.

Digital shopping tools and online access is opening up consumers to brands and retailers much earlier in the development cycle of a country and quickening the shift away from the traditional economy.

This is particularly true for developing markets where rural consumers can now be accessed directly and instantly.

25.3

52.2

79.0

46.4

67.3

86.9

61.4

76.7

91.1

0

20

40

60

80

100

Developing Emerging Developed

Share of Internet Users per 100 People by Development Stage (%)

2012 2017 2021e

Source: Planet Retail RNG

T E C H N O LO G Y

Developing regions experiencing rapid growth in internet penetration

18 | Store of the Future 2017

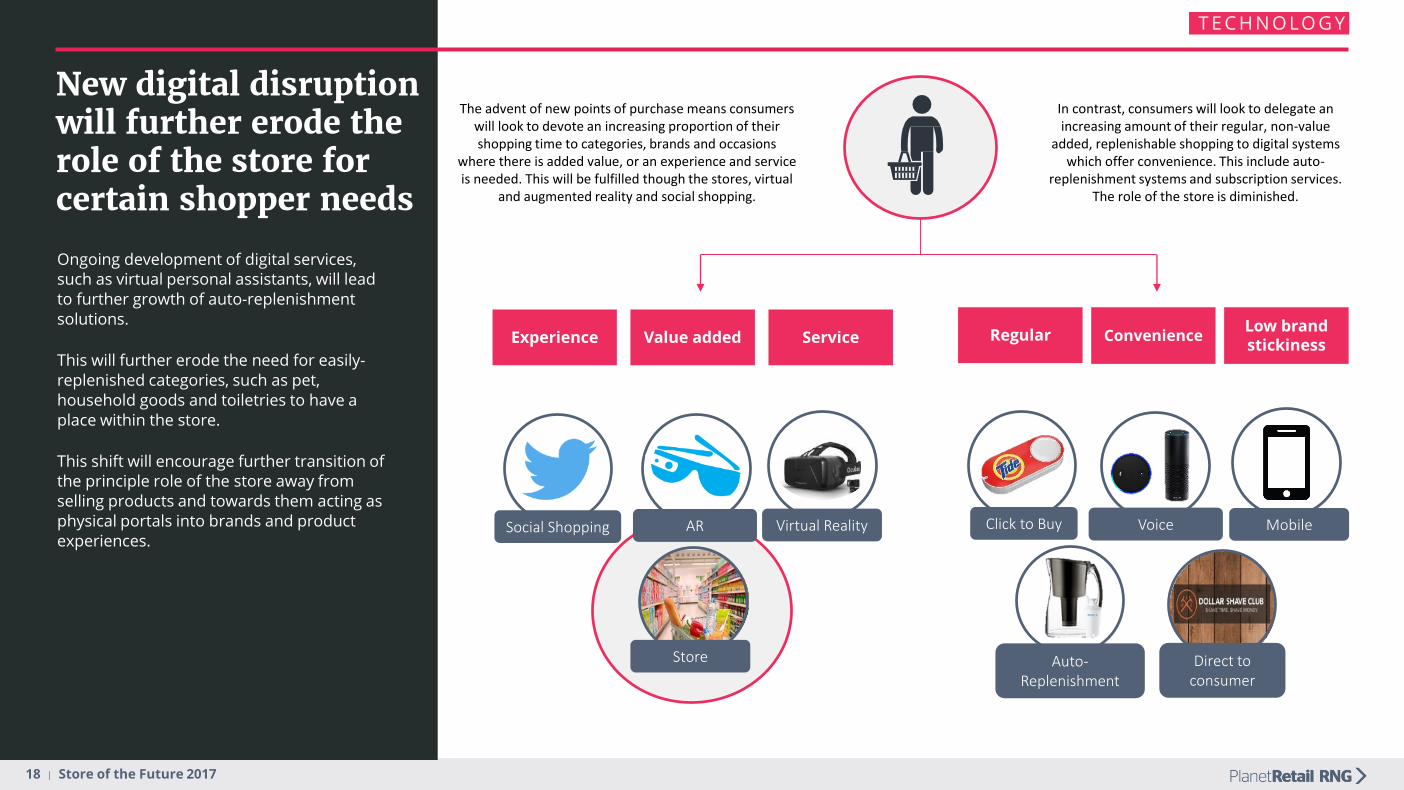

New digital disruption will further erode the role of the store for certain shopper needs

Ongoing development of digital services, such as virtual personal assistants, will lead to further growth of auto-replenishment solutions.

This will further erode the need for easily-replenished categories, such as pet, household goods and toiletries to have a place within the store.

This shift will encourage further transition of the principle role of the store away from selling products and towards them acting as physical portals into brands and product experiences.

Click to BuySocial Shopping Voice

Auto-Replenishment

Virtual RealityAR

Store

Mobile

Direct to consumer

Experience ConvenienceRegularValue added ServiceLow brand stickiness

The advent of new points of purchase means consumers will look to devote an increasing proportion of their shopping time to categories, brands and occasions

where there is added value, or an experience and service is needed. This will be fulfilled though the stores, virtual

and augmented reality and social shopping.

In contrast, consumers will look to delegate an increasing amount of their regular, non-value

added, replenishable shopping to digital systems which offer convenience. This include auto-

replenishment systems and subscription services. The role of the store is diminished.

T E C H N O LO G Y

19 | Store of the Future 2017

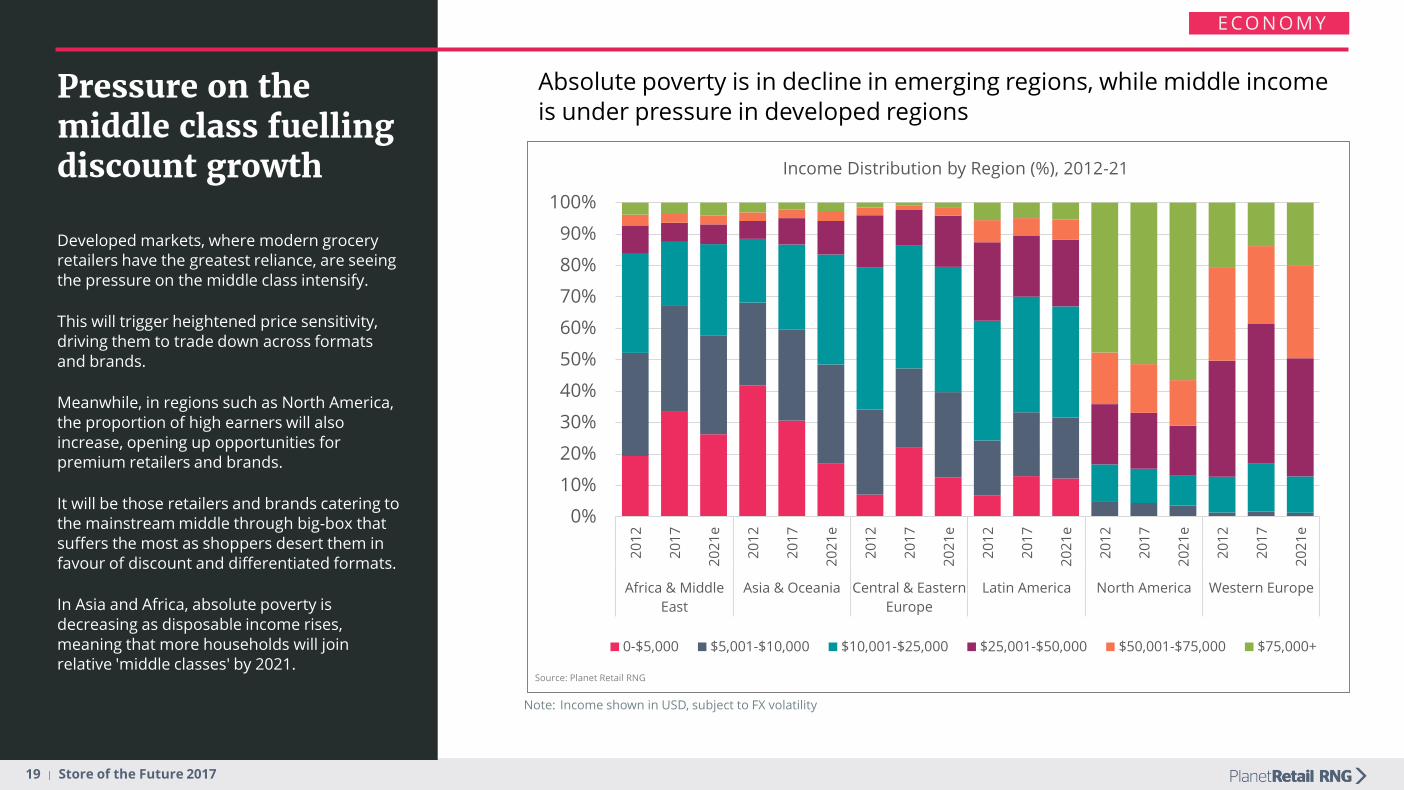

Pressure on the middle class fuelling discount growth

Developed markets, where modern grocery retailers have the greatest reliance, are seeing the pressure on the middle class intensify.

This will trigger heightened price sensitivity, driving them to trade down across formats and brands.

Meanwhile, in regions such as North America, the proportion of high earners will also increase, opening up opportunities for premium retailers and brands.

It will be those retailers and brands catering to the mainstream middle through big-box that suffers the most as shoppers desert them in favour of discount and differentiated formats.

In Asia and Africa, absolute poverty is decreasing as disposable income rises, meaning that more households will join relative 'middle classes' by 2021.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

12

20

17

20

21

e

20

12

20

17

20

21

e

20

12

20

17

20

21

e

20

12

20

17

20

21

e

20

12

20

17

20

21

e

20

12

20

17

20

21

e

Africa & Middle

East

Asia & Oceania Central & Eastern

Europe

Latin America North America Western Europe

Income Distribution by Region (%), 2012-21

0-$5,000 $5,001-$10,000 $10,001-$25,000 $25,001-$50,000 $50,001-$75,000 $75,000+

Note: Income shown in USD, subject to FX volatility

Source: Planet Retail RNG

E CO N O M Y

Absolute poverty is in decline in emerging regions, while middle income is under pressure in developed regions

20 | Store of the Future 2017

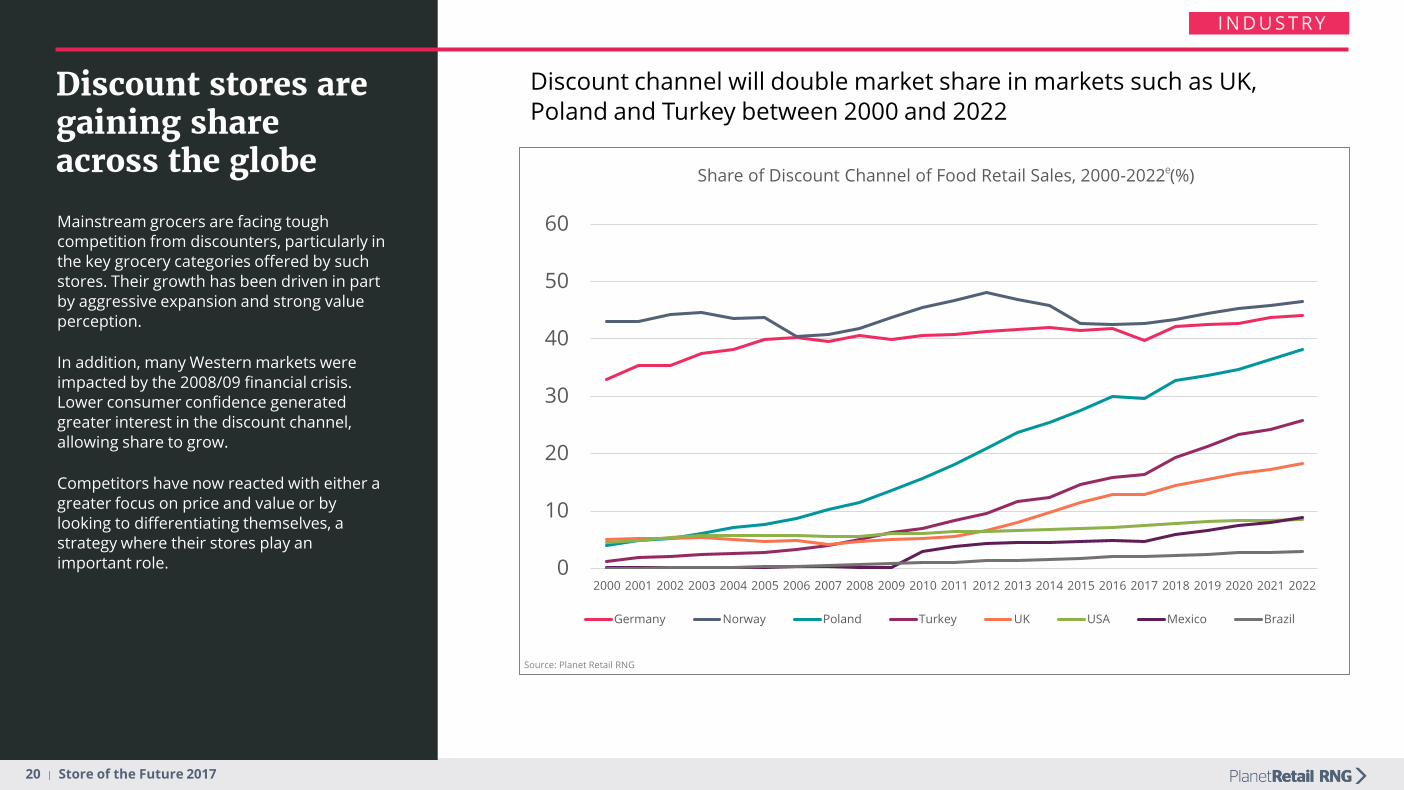

Discount stores are gaining share across the globe

Mainstream grocers are facing tough competition from discounters, particularly in the key grocery categories offered by such stores. Their growth has been driven in part by aggressive expansion and strong value perception.

In addition, many Western markets were impacted by the 2008/09 financial crisis. Lower consumer confidence generated greater interest in the discount channel, allowing share to grow.

Competitors have now reacted with either a greater focus on price and value or by looking to differentiating themselves, a strategy where their stores play an important role. 0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Share of Discount Channel of Food Retail Sales, 2000-2022 (%)

Germany Norway Poland Turkey UK USA Mexico Brazil

Source: Planet Retail RNG

I N D U S T R Y

Discount channel will double market share in markets such as UK, Poland and Turkey between 2000 and 2022

e

21 | Store of the Future 2017

Jun – Walgreens to acquire 2,186 Rite Aid stores

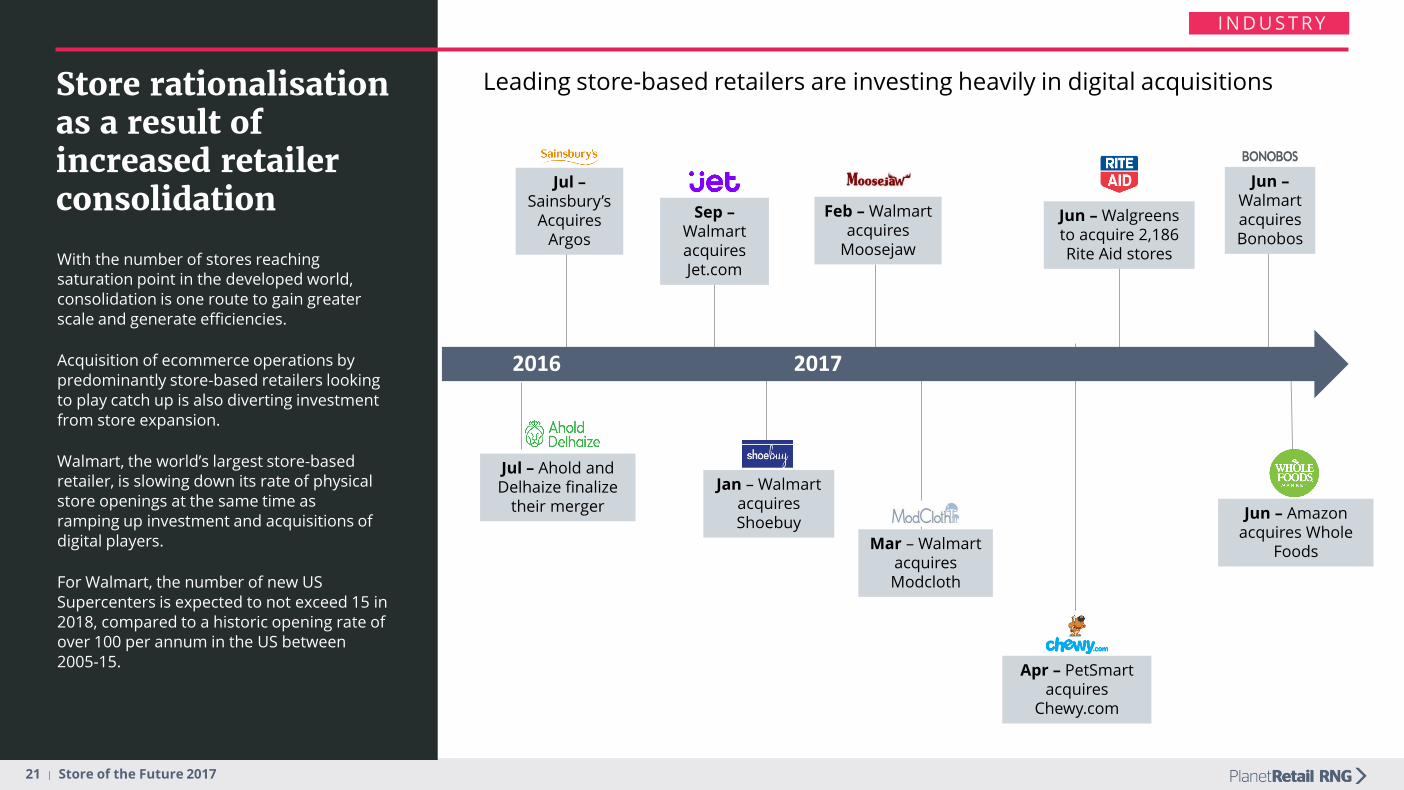

Store rationalisation as a result of increased retailer consolidation

With the number of stores reaching saturation point in the developed world, consolidation is one route to gain greater scale and generate efficiencies.

Acquisition of ecommerce operations by predominantly store-based retailers looking to play catch up is also diverting investment from store expansion.

Walmart, the world’s largest store-based retailer, is slowing down its rate of physical store openings at the same time as ramping up investment and acquisitions of digital players.

For Walmart, the number of new US Supercenters is expected to not exceed 15 in 2018, compared to a historic opening rate of over 100 per annum in the US between 2005-15.

Jan – Walmart acquires Shoebuy

Feb – Walmart acquires

Moosejaw

Mar – Walmart acquires Modcloth

Jun –Walmart acquires Bonobos

2016

Jun – Amazon acquires Whole

Foods

2017

Apr – PetSmart acquires

Chewy.com

Jul – Ahold and Delhaize finalize

their merger

Sep –Walmart acquires Jet.com

Jul –Sainsbury’s

Acquires Argos

I N D U S T R Y

Leading store-based retailers are investing heavily in digital acquisitions

22 | Store of the Future 2017

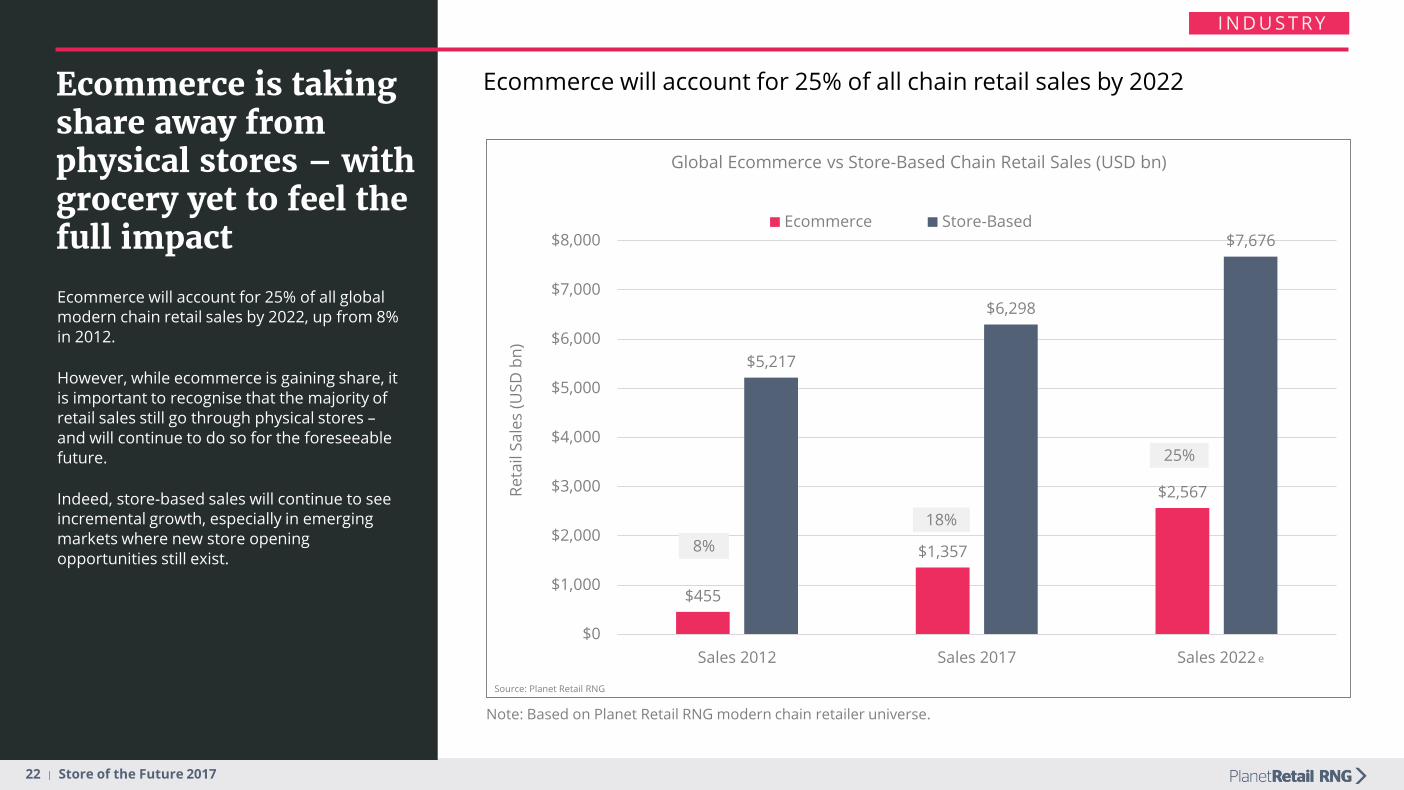

$455

$1,357

$2,567

$5,217

$6,298

$7,676

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Sales 2012 Sales 2017 Sales 2022

Re

tail

Sa

les

(US

D b

n)

Global Ecommerce vs Store-Based Chain Retail Sales (USD bn)

Ecommerce Store-Based

8%

18%

25%

Ecommerce is taking share away from physical stores – with grocery yet to feel the full impact

Note: Based on Planet Retail RNG modern chain retailer universe.

Ecommerce will account for 25% of all global modern chain retail sales by 2022, up from 8% in 2012.

However, while ecommerce is gaining share, it is important to recognise that the majority of retail sales still go through physical stores –and will continue to do so for the foreseeable future.

Indeed, store-based sales will continue to see incremental growth, especially in emerging markets where new store opening opportunities still exist.

Source: Planet Retail RNG

I N D U S T R Y

Ecommerce will account for 25% of all chain retail sales by 2022

e

23 | Store of the Future 2017

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Eco

mm

erc

e

Sto

re-B

ase

d

Eco

mm

erc

e

Sto

re-B

ase

d

Eco

mm

erc

e

Sto

re-B

ase

d

Eco

mm

erc

e

Sto

re-B

ase

d

Eco

mm

erc

e

Sto

re-B

ase

d

Asia/Pacific Europe Latin America Middle East & Africa North America

GM

V (

US

D b

n)

Ecommerce vs Store-Based GMV by Region (USD bn)

2012 2017 2022

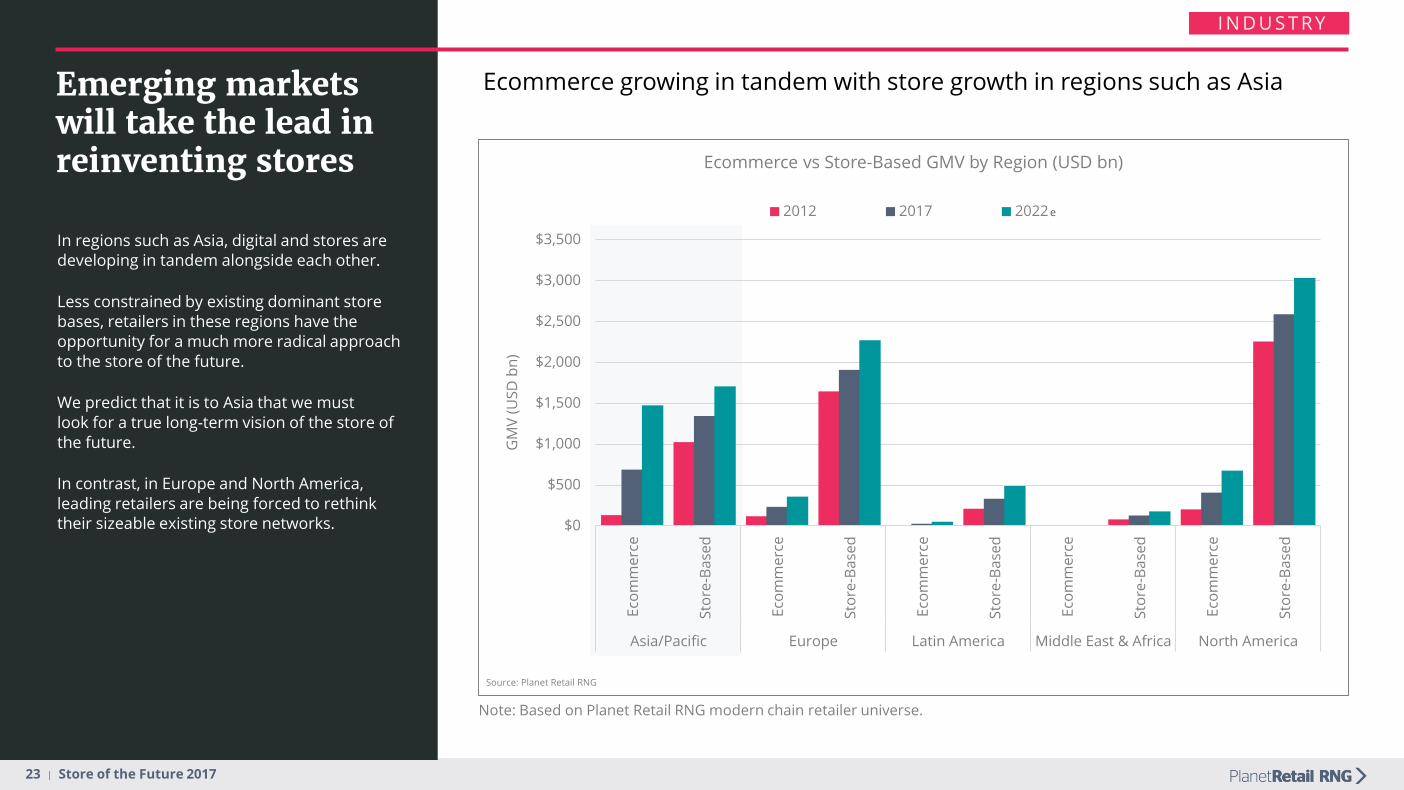

Emerging markets will take the lead in reinventing stores

In regions such as Asia, digital and stores are developing in tandem alongside each other.

Less constrained by existing dominant store bases, retailers in these regions have the opportunity for a much more radical approach to the store of the future.

We predict that it is to Asia that we must look for a true long-term vision of the store of the future.

In contrast, in Europe and North America, leading retailers are being forced to rethink their sizeable existing store networks.

Note: Based on Planet Retail RNG modern chain retailer universe.

Source: Planet Retail RNG

I N D U S T R Y

Ecommerce growing in tandem with store growth in regions such as Asia

e

24 | Store of the Future 2017

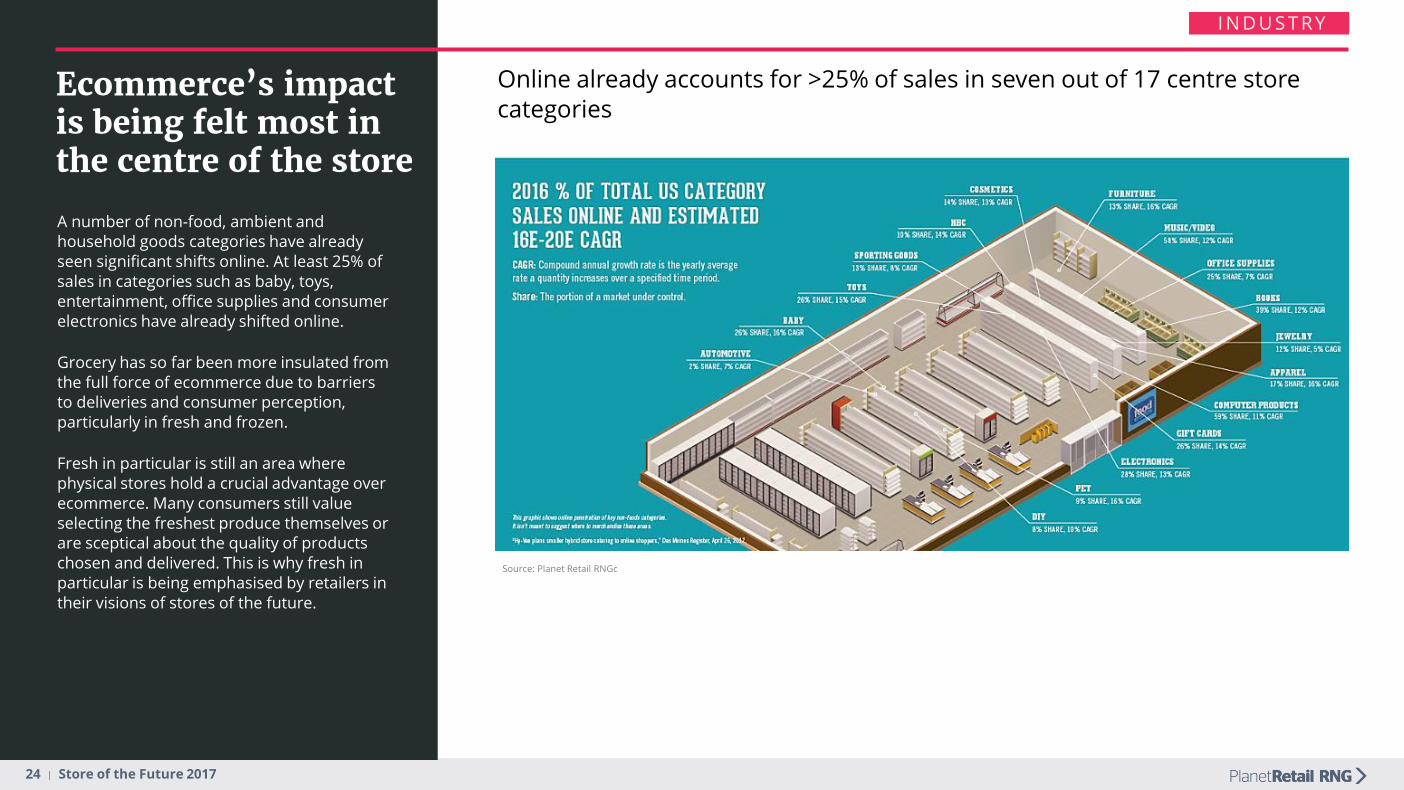

Ecommerce’s impact is being felt most in the centre of the store

A number of non-food, ambient and household goods categories have already seen significant shifts online. At least 25% of sales in categories such as baby, toys, entertainment, office supplies and consumer electronics have already shifted online.

Grocery has so far been more insulated from the full force of ecommerce due to barriers to deliveries and consumer perception, particularly in fresh and frozen.

Fresh in particular is still an area where physical stores hold a crucial advantage over ecommerce. Many consumers still value selecting the freshest produce themselves or are sceptical about the quality of products chosen and delivered. This is why fresh in particular is being emphasised by retailers in their visions of stores of the future.

I N D U S T R Y

Online already accounts for >25% of sales in seven out of 17 centre store categories

Source: Planet Retail RNGc

25 | Store of the Future 2017

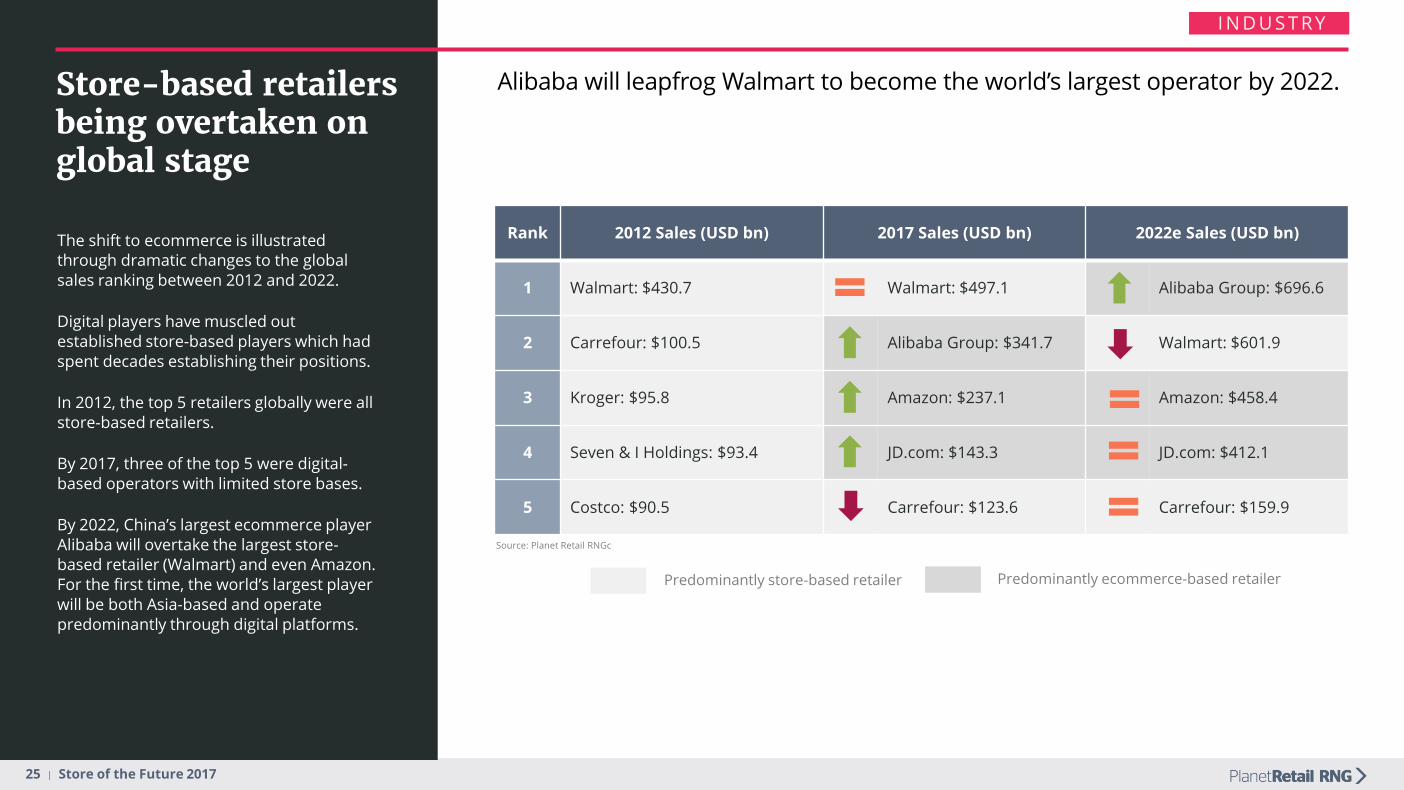

Store-based retailers being overtaken on global stage

The shift to ecommerce is illustrated through dramatic changes to the global sales ranking between 2012 and 2022.

Digital players have muscled out established store-based players which had spent decades establishing their positions.

In 2012, the top 5 retailers globally were all store-based retailers.

By 2017, three of the top 5 were digital-based operators with limited store bases.

By 2022, China’s largest ecommerce player Alibaba will overtake the largest store-based retailer (Walmart) and even Amazon. For the first time, the world’s largest player will be both Asia-based and operate predominantly through digital platforms.

Predominantly ecommerce-based retailerPredominantly store-based retailer

Rank 2012 Sales (USD bn) 2017 Sales (USD bn) 2022e Sales (USD bn)

1 Walmart: $430.7 Walmart: $497.1 Alibaba Group: $696.6

2 Carrefour: $100.5 Alibaba Group: $341.7 Walmart: $601.9

3 Kroger: $95.8 Amazon: $237.1 Amazon: $458.4

4 Seven & I Holdings: $93.4 JD.com: $143.3 JD.com: $412.1

5 Costco: $90.5 Carrefour: $123.6 Carrefour: $159.9

Source: Planet Retail RNGc

I N D U S T R Y

Alibaba will leapfrog Walmart to become the world’s largest operator by 2022.

26 | Store of the Future 2017

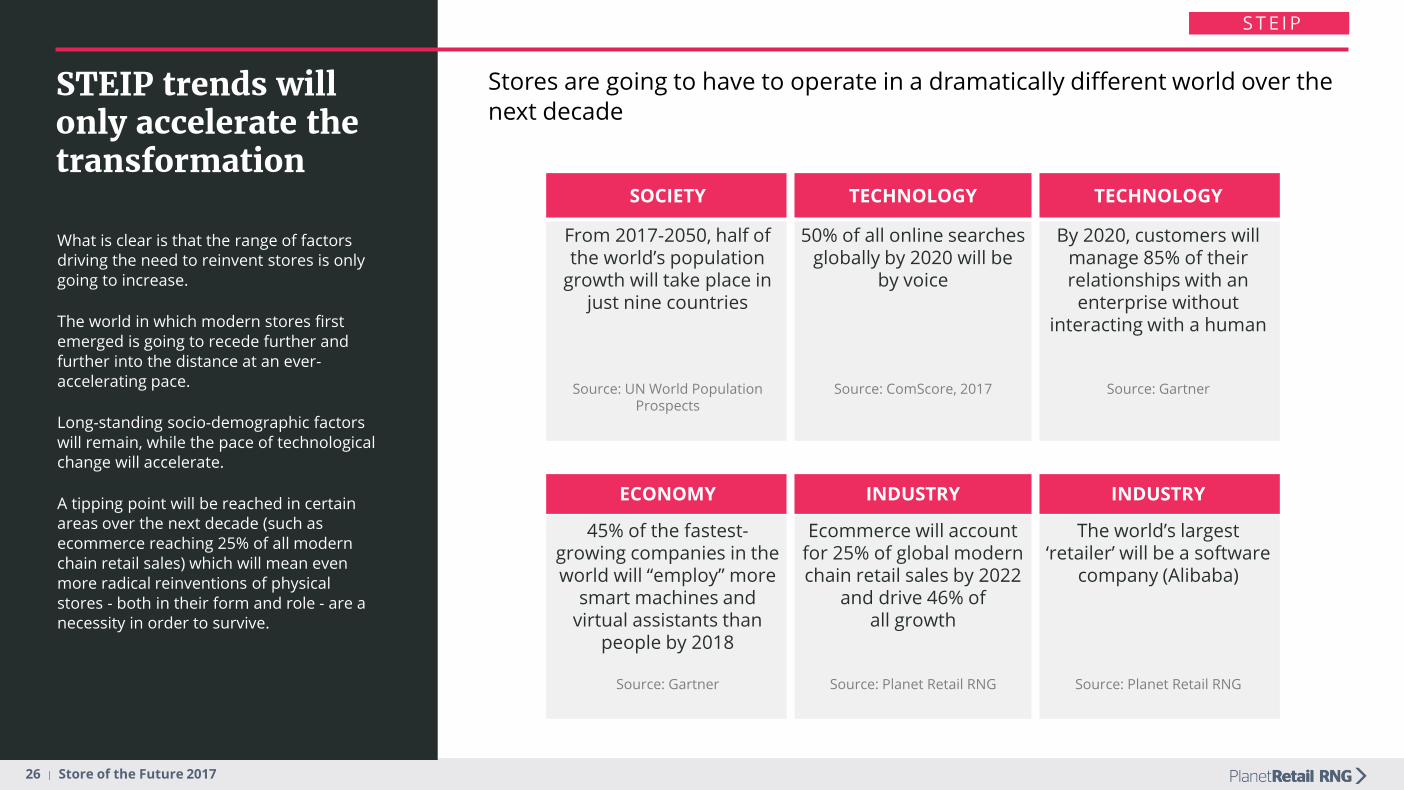

STEIP trends will only accelerate the transformation

What is clear is that the range of factors driving the need to reinvent stores is only going to increase.

The world in which modern stores first emerged is going to recede further and further into the distance at an ever-accelerating pace.

Long-standing socio-demographic factors will remain, while the pace of technological change will accelerate.

A tipping point will be reached in certain areas over the next decade (such as ecommerce reaching 25% of all modern chain retail sales) which will mean even more radical reinventions of physical stores - both in their form and role - are a necessity in order to survive.

Stores are going to have to operate in a dramatically different world over the next decade

SOCIETY TECHNOLOGY TECHNOLOGY

From 2017-2050, half of the world’s population

growth will take place in just nine countries

Source: UN World Population Prospects

50% of all online searches globally by 2020 will be

by voice

Source: ComScore, 2017

By 2020, customers will manage 85% of their relationships with an

enterprise without interacting with a human

Source: Gartner

ECONOMY INDUSTRY INDUSTRY

45% of the fastest-growing companies in the world will “employ” more

smart machines and virtual assistants than

people by 2018

Source: Gartner

Ecommerce will account for 25% of global modern chain retail sales by 2022

and drive 46% of all growth

Source: Planet Retail RNG

The world’s largest ‘retailer’ will be a software

company (Alibaba)

Source: Planet Retail RNG

S T E I P

27 | Store of the Future 2017

Store of the Future Explained

28 | Store of the Future 2017

Click & collect

Digital engagement

Fulfilled by store

Checkout-less stores

Events

Inspiration

Shop-in-shops

Education

Customer serviceand experience

Product curation

Exclusives

Focus on fresh

“Made in Store”

Community role

Social and meeting hub

Restaurants

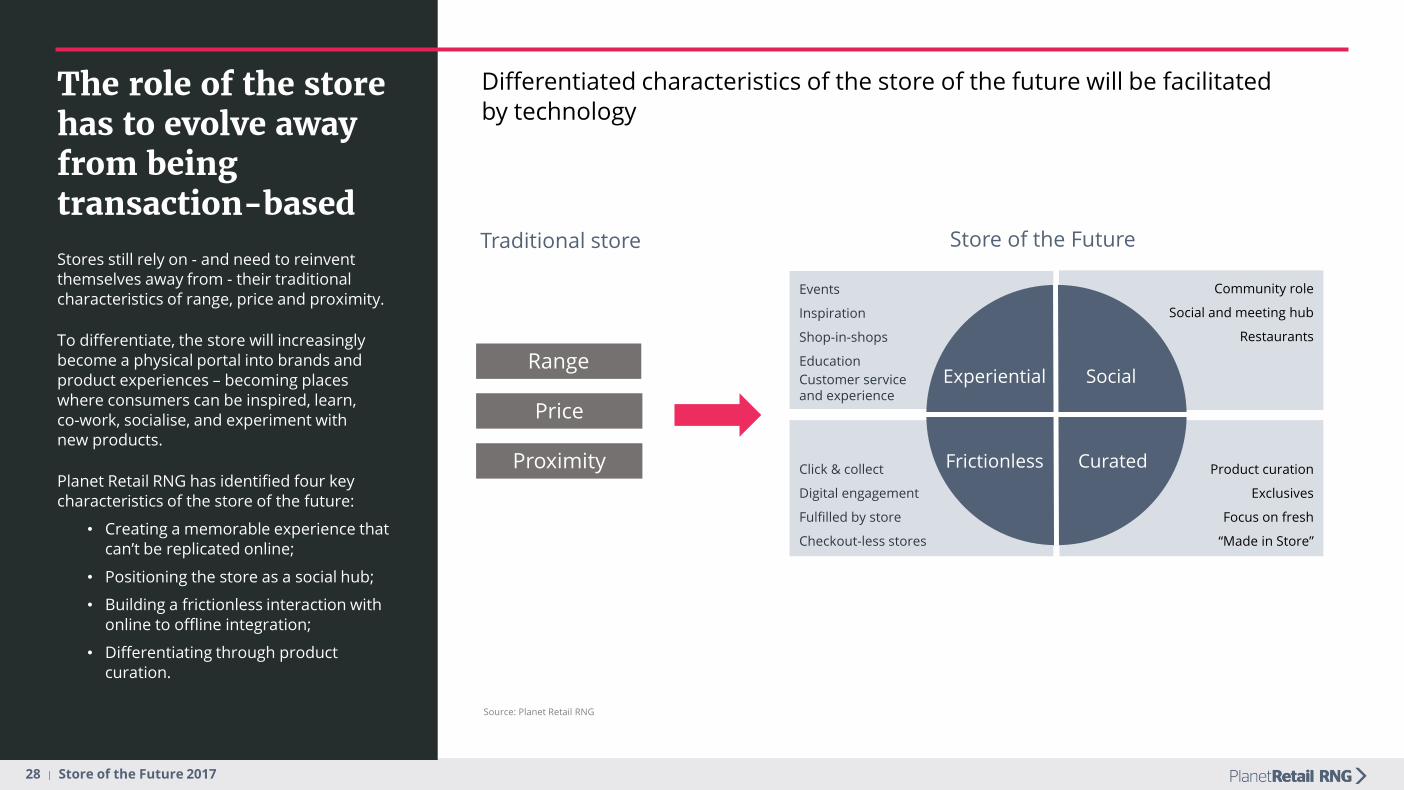

The role of the store has to evolve away from being transaction-basedStores still rely on - and need to reinvent themselves away from - their traditional characteristics of range, price and proximity.

To differentiate, the store will increasingly become a physical portal into brands and product experiences – becoming places where consumers can be inspired, learn, co-work, socialise, and experiment with new products.

Planet Retail RNG has identified four key characteristics of the store of the future:

• Creating a memorable experience that can’t be replicated online;

• Positioning the store as a social hub;

• Building a frictionless interaction with online to offline integration;

• Differentiating through product curation.

Range

Price

Proximity

Traditional store

Differentiated characteristics of the store of the future will be facilitated by technology

Source: Planet Retail RNG

Store of the Future

Experiential Social

Frictionless Curated

29 | Store of the Future 2017

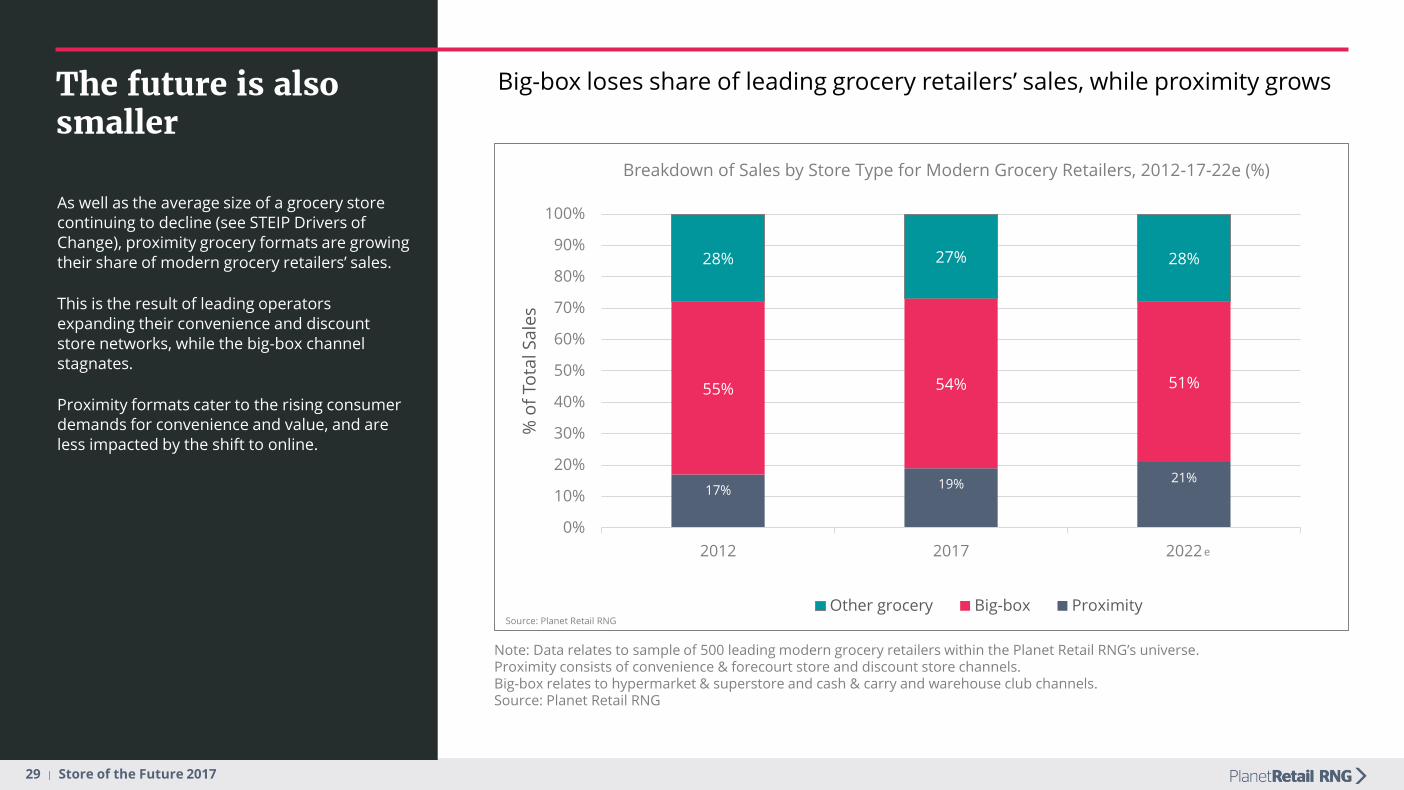

The future is also smaller

As well as the average size of a grocery store continuing to decline (see STEIP Drivers of Change), proximity grocery formats are growing their share of modern grocery retailers’ sales.

This is the result of leading operators expanding their convenience and discount store networks, while the big-box channel stagnates.

Proximity formats cater to the rising consumer demands for convenience and value, and are less impacted by the shift to online.

17% 19% 21%

55% 54% 51%

28% 27% 28%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2017 2022

% o

f To

tal S

ale

s

Breakdown of Sales by Store Type for Modern Grocery Retailers, 2012-17-22e (%)

Other grocery Big-box Proximity

Note: Data relates to sample of 500 leading modern grocery retailers within the Planet Retail RNG’s universe.Proximity consists of convenience & forecourt store and discount store channels.Big-box relates to hypermarket & superstore and cash & carry and warehouse club channels.Source: Planet Retail RNG

Source: Planet Retail RNG

Big-box loses share of leading grocery retailers’ sales, while proximity grows

e

30 | Store of the Future 2017

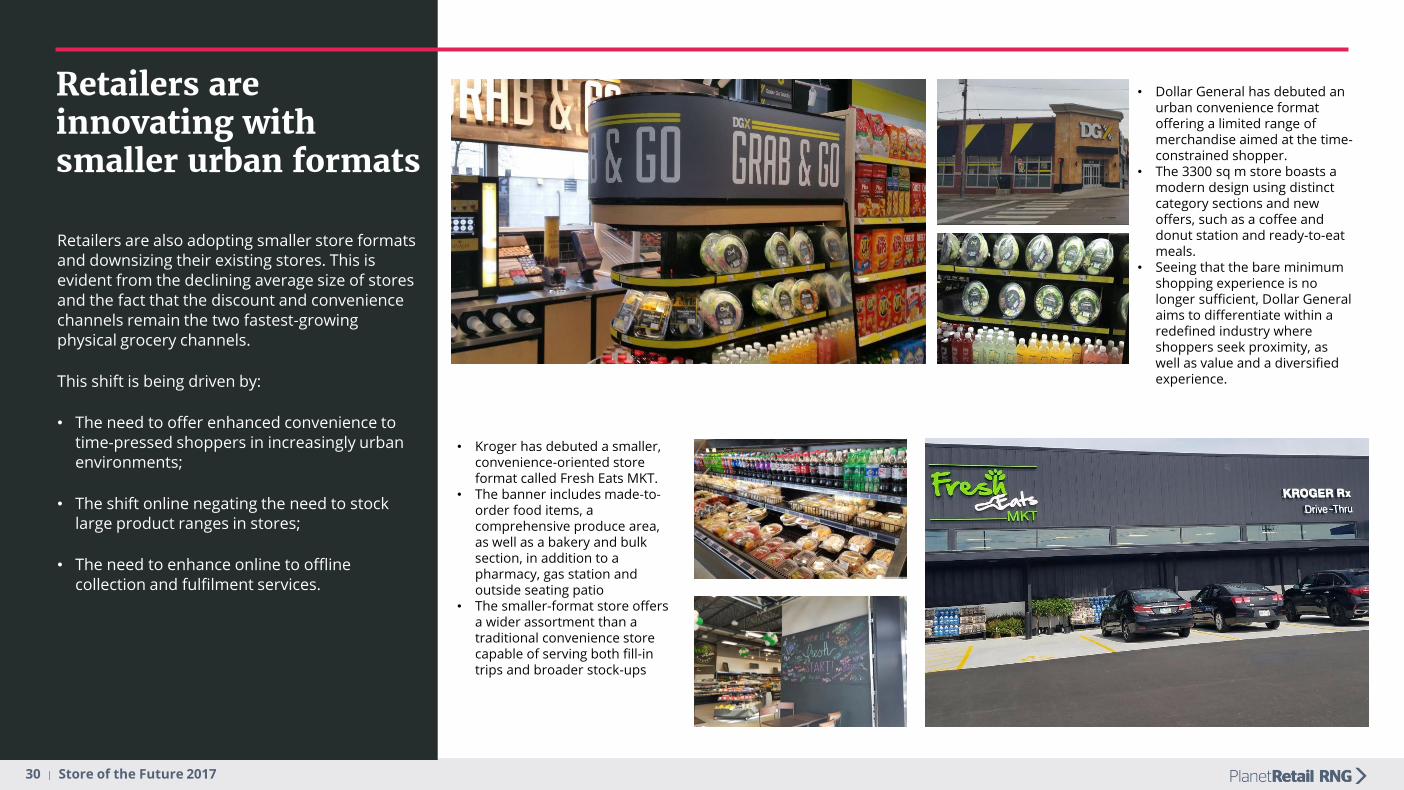

Retailers are innovating with smaller urban formats

Retailers are also adopting smaller store formats and downsizing their existing stores. This is evident from the declining average size of stores and the fact that the discount and convenience channels remain the two fastest-growing physical grocery channels.

This shift is being driven by:

• The need to offer enhanced convenience to time-pressed shoppers in increasingly urban environments;

• The shift online negating the need to stock large product ranges in stores;

• The need to enhance online to offline collection and fulfilment services.

• Dollar General has debuted an urban convenience format offering a limited range of merchandise aimed at the time-constrained shopper.

• The 3300 sq m store boasts a modern design using distinct category sections and new offers, such as a coffee and donut station and ready-to-eat meals.

• Seeing that the bare minimum shopping experience is no longer sufficient, Dollar General aims to differentiate within a redefined industry where shoppers seek proximity, as well as value and a diversified experience.

• Kroger has debuted a smaller, convenience-oriented store format called Fresh Eats MKT.

• The banner includes made-to-order food items, a comprehensive produce area, as well as a bakery and bulk section, in addition to a pharmacy, gas station and outside seating patio

• The smaller-format store offers a wider assortment than a traditional convenience store capable of serving both fill-in trips and broader stock-ups

31 | Store of the Future 2017

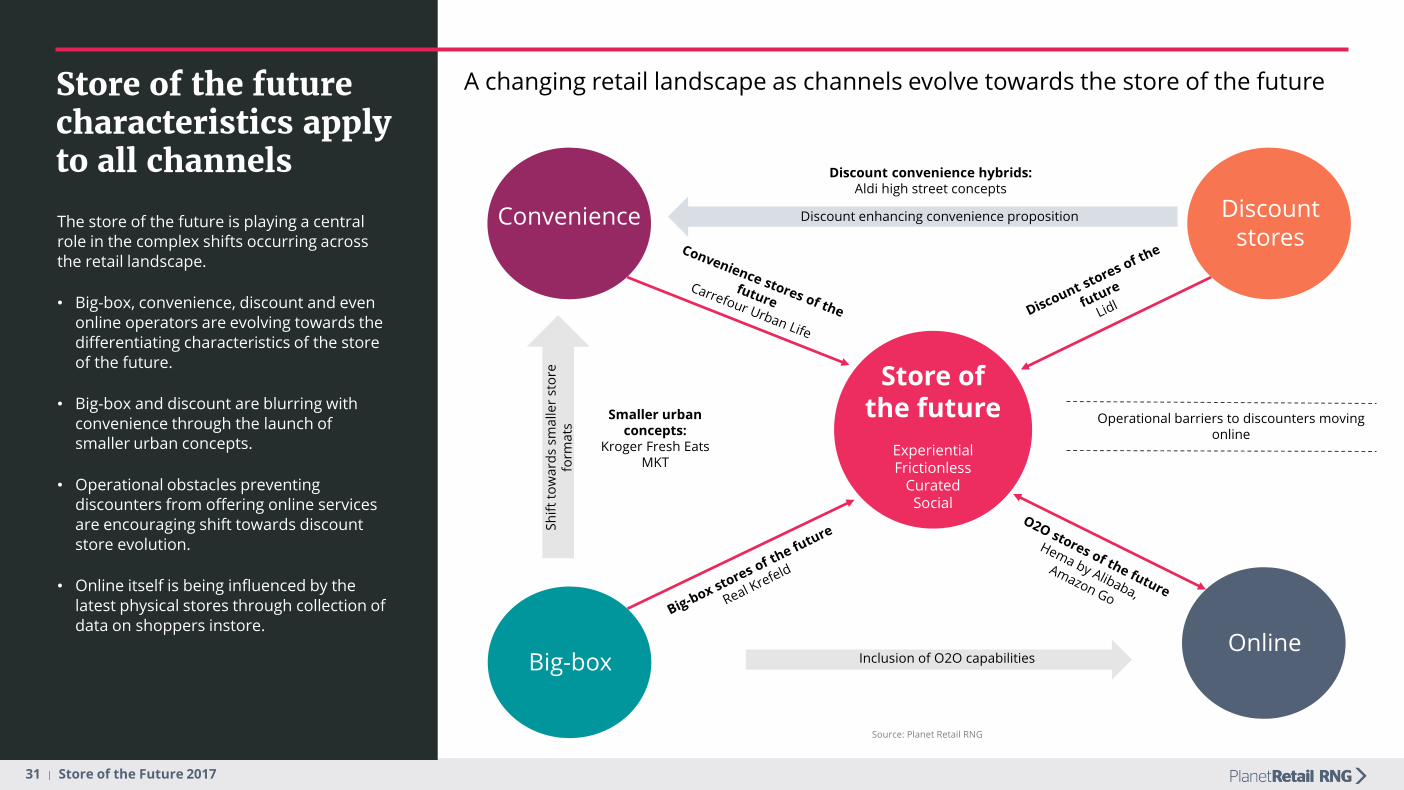

Store of the future characteristics apply to all channels

The store of the future is playing a central role in the complex shifts occurring across the retail landscape.

• Big-box, convenience, discount and even online operators are evolving towards the differentiating characteristics of the store of the future.

• Big-box and discount are blurring with convenience through the launch of smaller urban concepts.

• Operational obstacles preventing discounters from offering online services are encouraging shift towards discount store evolution.

• Online itself is being influenced by the latest physical stores through collection of data on shoppers instore.

Big-box

Convenience Discount stores

Online

Store ofthe future

ExperientialFrictionless

CuratedSocial

Smaller urban concepts:

Kroger Fresh Eats MKT

Operational barriers to discounters moving online

Sh

ift

tow

ard

s sm

alle

r st

ore

fo

rma

ts

Discount enhancing convenience proposition

Discount convenience hybrids:Aldi high street concepts

A changing retail landscape as channels evolve towards the store of the future

Inclusion of O2O capabilities

Source: Planet Retail RNG

32 | Store of the Future 2017

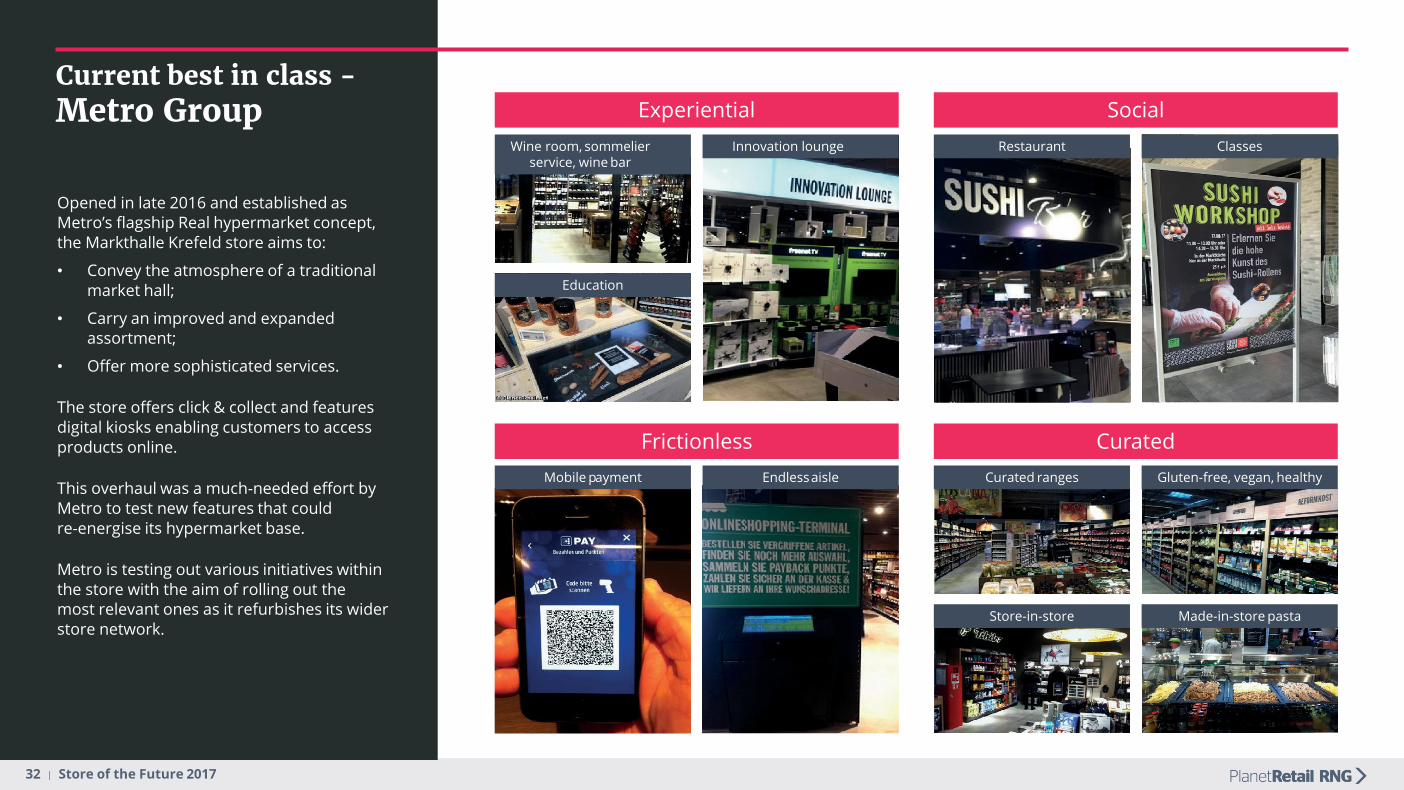

Current best in class -Metro Group

Opened in late 2016 and established as Metro’s flagship Real hypermarket concept, the Markthalle Krefeld store aims to:

• Convey the atmosphere of a traditional market hall;

• Carry an improved and expanded assortment;

• Offer more sophisticated services.

The store offers click & collect and features digital kiosks enabling customers to access products online.

This overhaul was a much-needed effort by Metro to test new features that could re-energise its hypermarket base.

Metro is testing out various initiatives within the store with the aim of rolling out the most relevant ones as it refurbishes its wider store network.

Wine room, sommelierservice, wine bar

Restaurant

Mobile payment Curated ranges

Store-in-store

Education

Innovation lounge Classes

Endlessaisle Gluten-free, vegan, healthy

Made-in-store pasta

Experiential Social

Frictionless Curated

33 | Store of the Future 2017

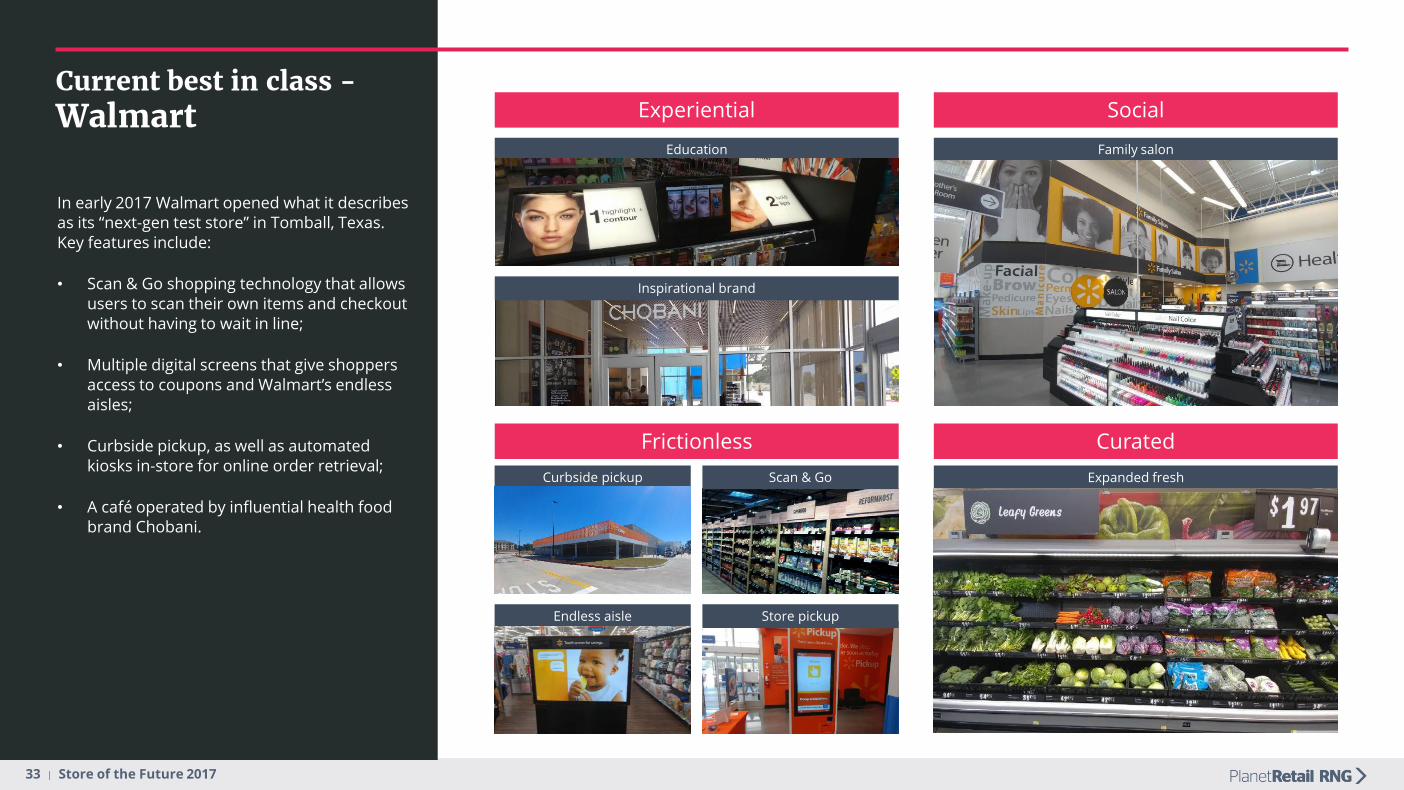

Current best in class -Walmart

In early 2017 Walmart opened what it describes as its “next-gen test store” in Tomball, Texas. Key features include:

• Scan & Go shopping technology that allows users to scan their own items and checkout without having to wait in line;

• Multiple digital screens that give shoppers access to coupons and Walmart’s endless aisles;

• Curbside pickup, as well as automated kiosks in-store for online order retrieval;

• A café operated by influential health food brand Chobani.

Family salon

Curbside pickup

Endless aisle

Scan & Go

Store pickup

Experiential Social

Frictionless Curated

Education

Inspirational brand

Expanded fresh

34 | Store of the Future 2017

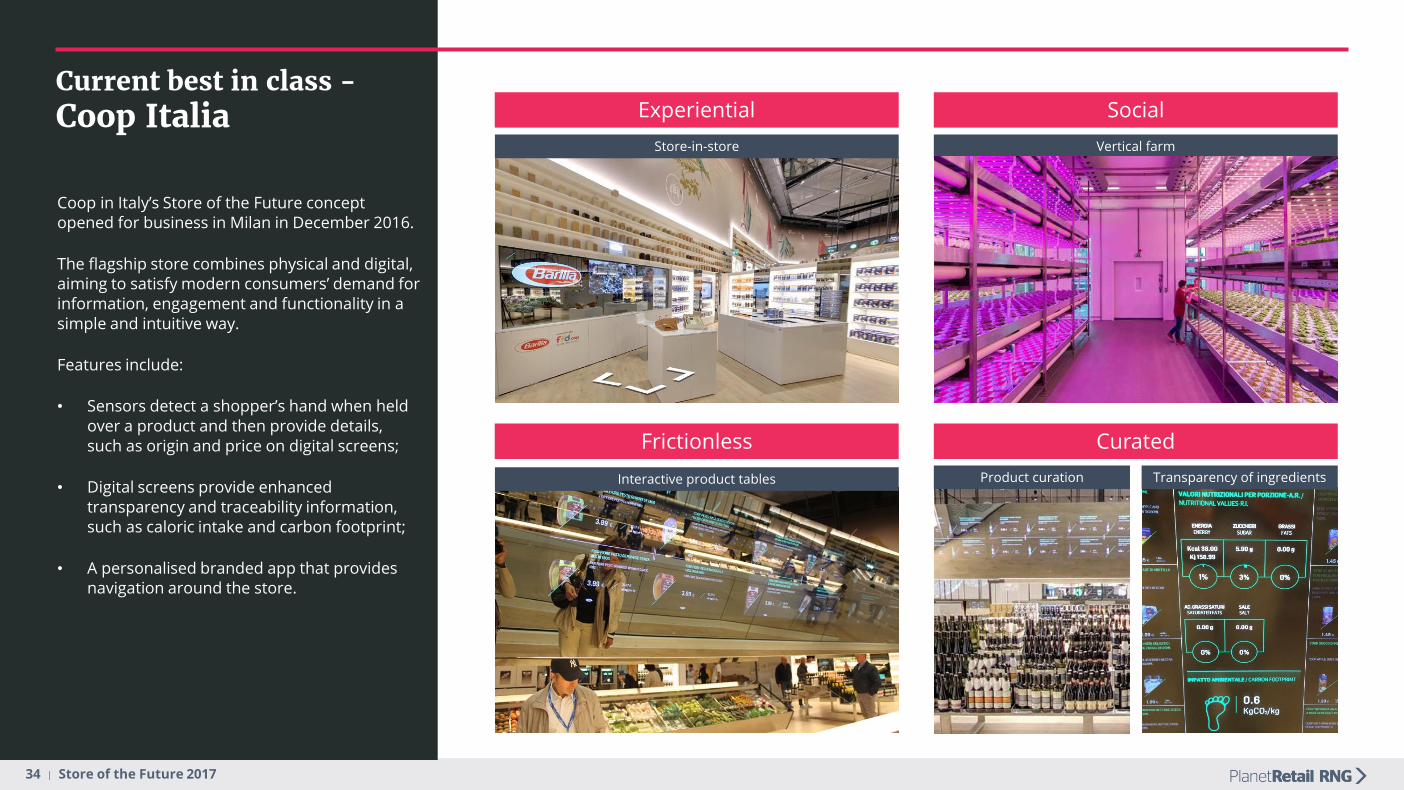

Current best in class -Coop Italia

Coop in Italy’s Store of the Future concept opened for business in Milan in December 2016.

The flagship store combines physical and digital, aiming to satisfy modern consumers’ demand for information, engagement and functionality in a simple and intuitive way.

Features include:

• Sensors detect a shopper’s hand when held over a product and then provide details, such as origin and price on digital screens;

• Digital screens provide enhanced transparency and traceability information, such as caloric intake and carbon footprint;

• A personalised branded app that provides navigation around the store.

Vertical farm

Experiential Social

Frictionless Curated

Store-in-store

Product curation Transparency of ingredientsInteractive product tables

35 | Store of the Future 2017

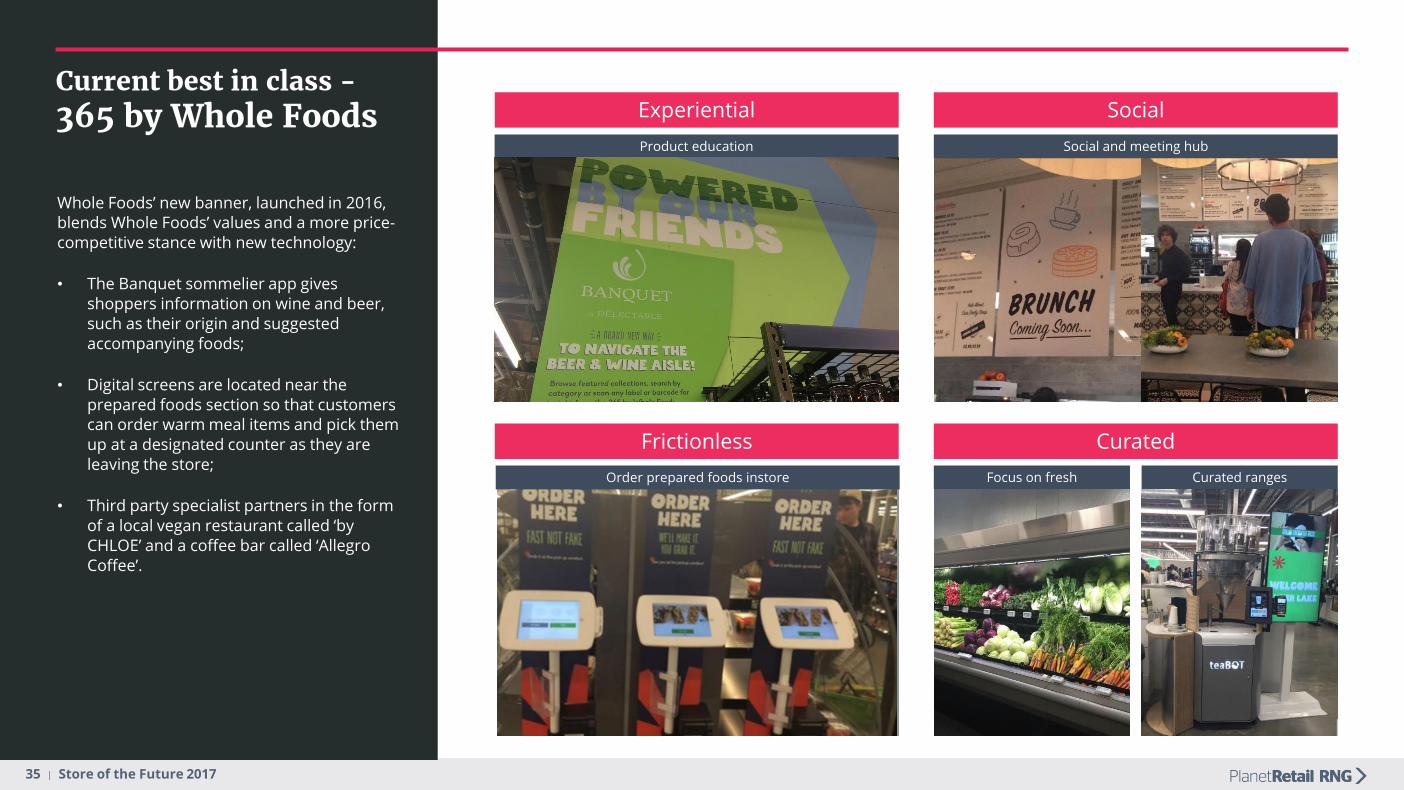

Current best in class -365 by Whole Foods

Whole Foods’ new banner, launched in 2016, blends Whole Foods’ values and a more price-competitive stance with new technology:

• The Banquet sommelier app gives shoppers information on wine and beer, such as their origin and suggested accompanying foods;

• Digital screens are located near the prepared foods section so that customers can order warm meal items and pick them up at a designated counter as they are leaving the store;

• Third party specialist partners in the form of a local vegan restaurant called ‘by CHLOE’ and a coffee bar called ‘Allegro Coffee’.

Experiential Social

Frictionless Curated

Product education Social and meeting hub

Order prepared foods instore Focus on fresh Curated ranges

36 | Store of the Future 2017

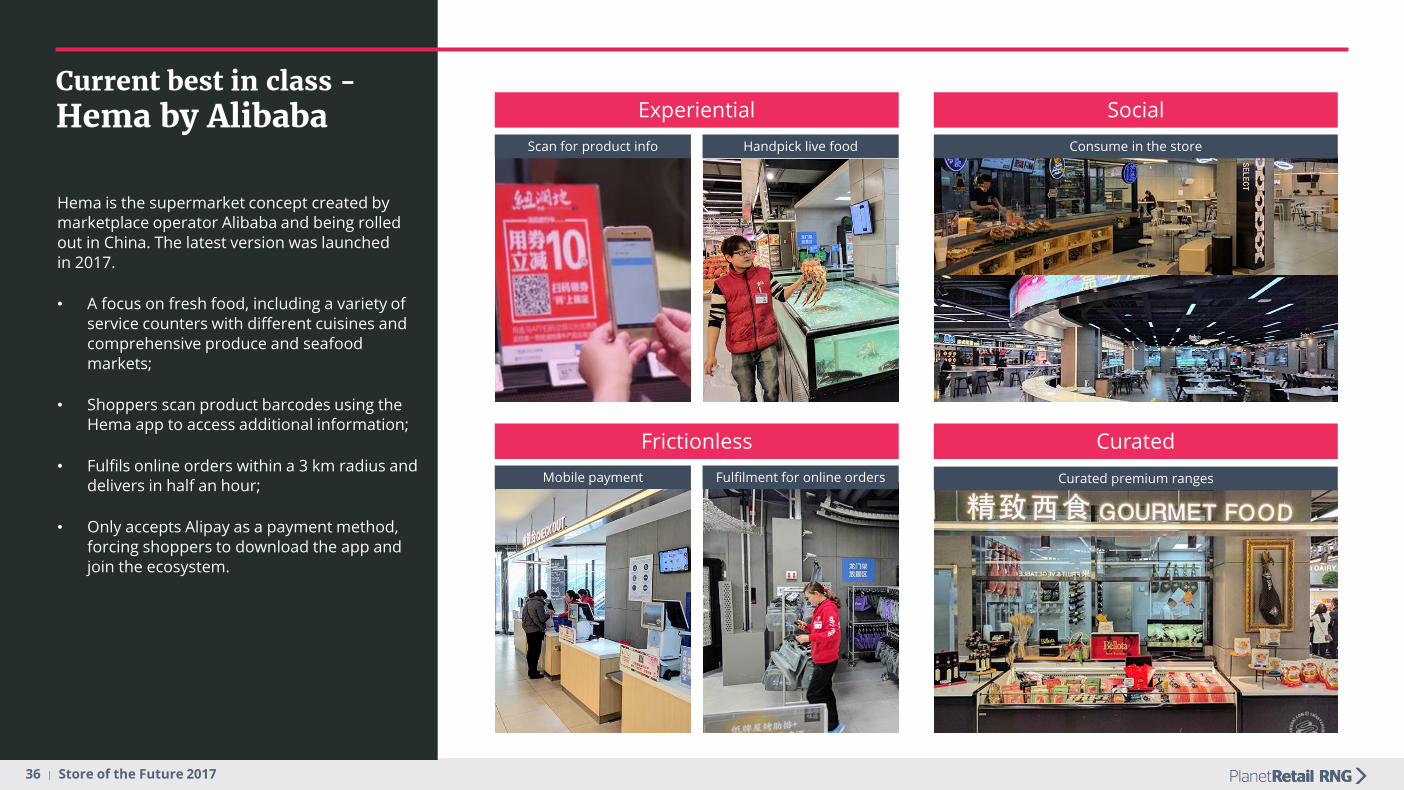

Current best in class -Hema by Alibaba

Hema is the supermarket concept created by marketplace operator Alibaba and being rolled out in China. The latest version was launched in 2017.

• A focus on fresh food, including a variety of service counters with different cuisines and comprehensive produce and seafood markets;

• Shoppers scan product barcodes using the Hema app to access additional information;

• Fulfils online orders within a 3 km radius and delivers in half an hour;

• Only accepts Alipay as a payment method, forcing shoppers to download the app and join the ecosystem.

Experiential Social

Frictionless Curated

Curated premium rangesMobile payment Fulfilment for online orders

Consume in the storeScan for product info Handpick live food

37 | Store of the Future 2017

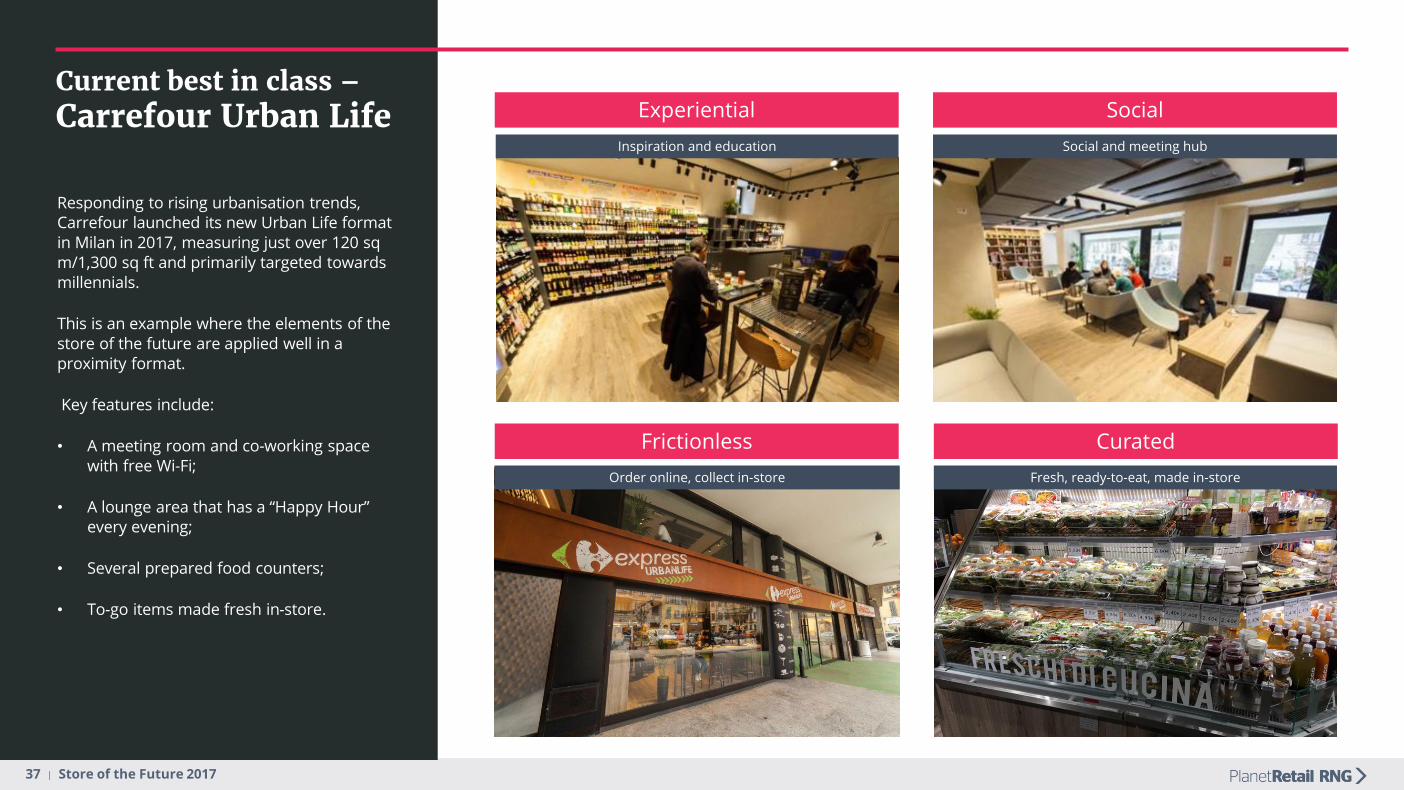

Current best in class –Carrefour Urban Life

Responding to rising urbanisation trends, Carrefour launched its new Urban Life format in Milan in 2017, measuring just over 120 sqm/1,300 sq ft and primarily targeted towards millennials.

This is an example where the elements of the store of the future are applied well in a proximity format.

Key features include:

• A meeting room and co-working space with free Wi-Fi;

• A lounge area that has a “Happy Hour” every evening;

• Several prepared food counters;

• To-go items made fresh in-store.

Experiential Social

Frictionless Curated

Inspiration and education Social and meeting hub

Order online, collect in-store Fresh, ready-to-eat, made in-store

38 | Store of the Future 2017

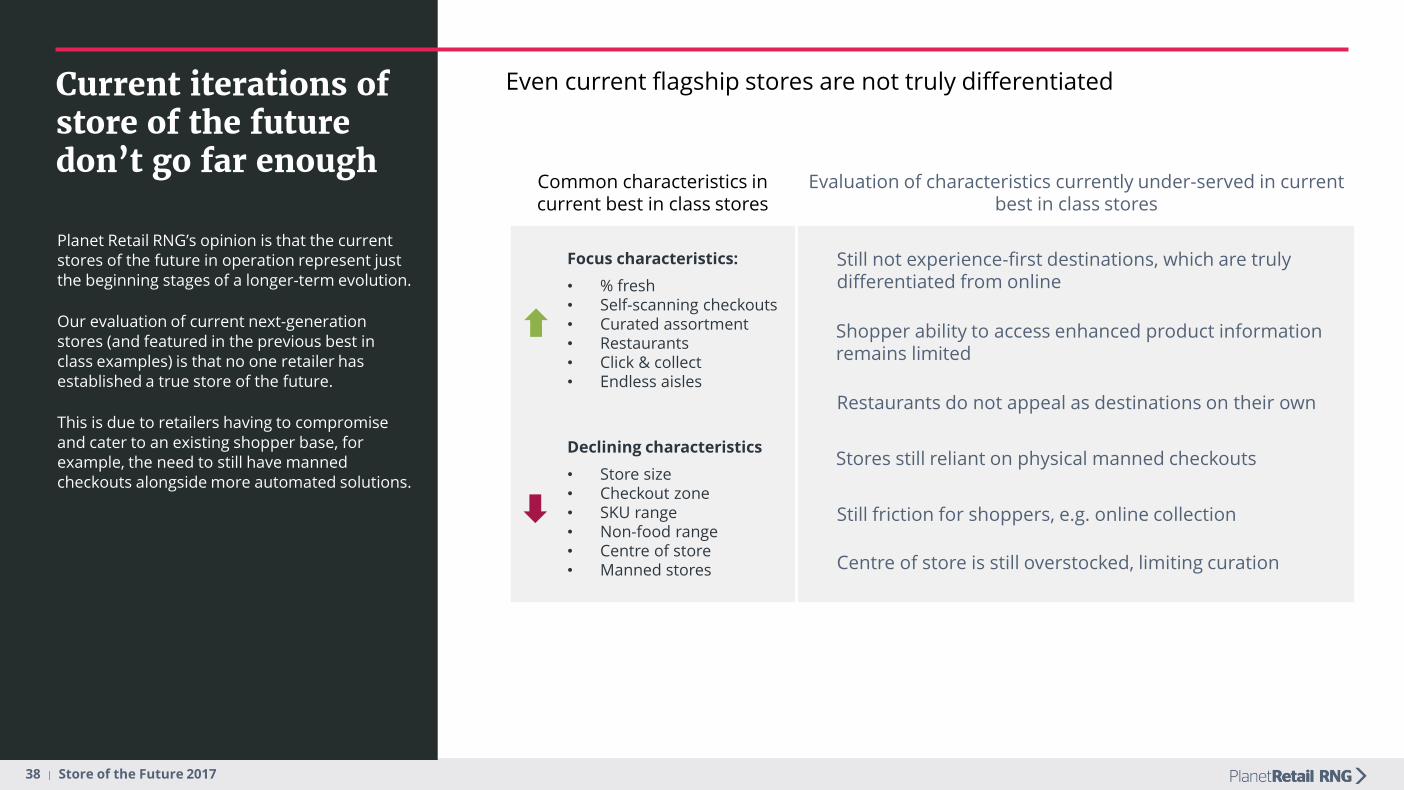

Current iterations of store of the future don’t go far enough

Planet Retail RNG’s opinion is that the current stores of the future in operation represent just the beginning stages of a longer-term evolution.

Our evaluation of current next-generation stores (and featured in the previous best in class examples) is that no one retailer has established a true store of the future.

This is due to retailers having to compromise and cater to an existing shopper base, for example, the need to still have manned checkouts alongside more automated solutions.

Focus characteristics:

• % fresh• Self-scanning checkouts• Curated assortment• Restaurants• Click & collect• Endless aisles

Declining characteristics

• Store size• Checkout zone• SKU range• Non-food range• Centre of store• Manned stores

Common characteristics in current best in class stores

Evaluation of characteristics currently under-served in current best in class stores

Still not experience-first destinations, which are truly differentiated from online

Stores still reliant on physical manned checkouts

Shopper ability to access enhanced product information remains limited

Still friction for shoppers, e.g. online collection

Centre of store is still overstocked, limiting curation

Restaurants do not appeal as destinations on their own

Even current flagship stores are not truly differentiated

39 | Store of the Future 2017

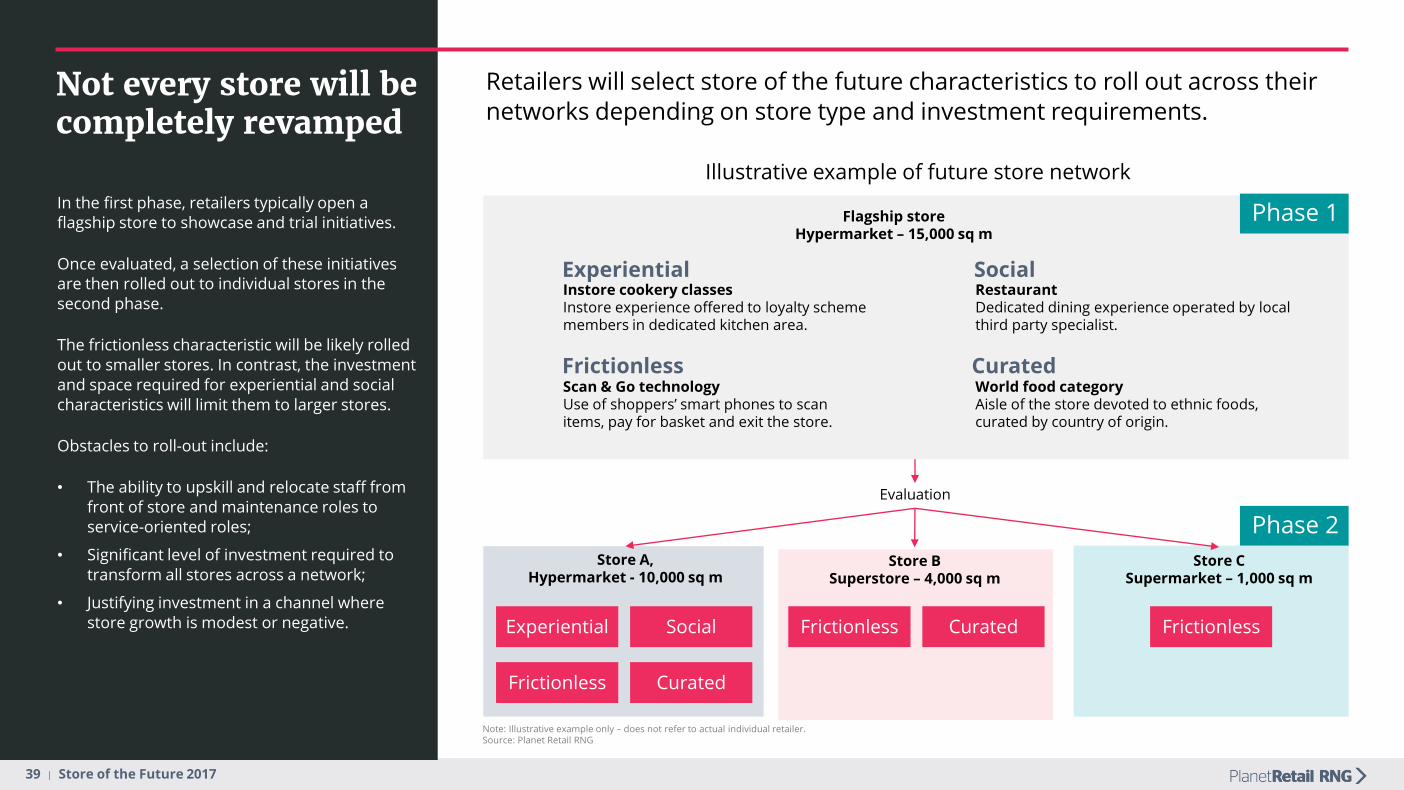

Not every store will be completely revamped

In the first phase, retailers typically open a flagship store to showcase and trial initiatives.

Once evaluated, a selection of these initiatives are then rolled out to individual stores in the second phase.

The frictionless characteristic will be likely rolled out to smaller stores. In contrast, the investment and space required for experiential and social characteristics will limit them to larger stores.

Obstacles to roll-out include:

• The ability to upskill and relocate staff from front of store and maintenance roles to service-oriented roles;

• Significant level of investment required to transform all stores across a network;

• Justifying investment in a channel where store growth is modest or negative.

Flagship storeHypermarket – 15,000 sq m

Evaluation

Store A, Hypermarket - 10,000 sq m

Store BSuperstore – 4,000 sq m

Store CSupermarket – 1,000 sq m

Experiential

RestaurantDedicated dining experience operated by local third party specialist.

Retailers will select store of the future characteristics to roll out across their networks depending on store type and investment requirements.

Note: Illustrative example only – does not refer to actual individual retailer.Source: Planet Retail RNG

World food categoryAisle of the store devoted to ethnic foods, curated by country of origin.

Scan & Go technologyUse of shoppers’ smart phones to scan items, pay for basket and exit the store.

Instore cookery classesInstore experience offered to loyalty scheme members in dedicated kitchen area.

Social

Frictionless Curated

Frictionless Curated Frictionless

Experiential Social

Frictionless Curated

Illustrative example of future store network

Phase 1

Phase 2

40 | Store of the Future 2017

By working together the industry can create the store of the futureThe reinvention of the store aligned to the four identified characteristics brings a number of opportunities for retailers and suppliers, as identified on the right.

These opportunities can only be fully realised if both parties can achieve a greater understanding of customers and their needs, demand and behaviour.

Suppliers with their own strong category expertise and shopper insight capabilities will therefore be seen as strong partners for retailers, especially those which have limited loyalty card or shopper data collection schemes themselves.

Recommendation for retailers• Recognition that experiences are not a ‘nice to have’, but

increasingly essential to differentiate.• Own and drive seasonal or weekend events throughout

the year.

Recommendation for suppliers• Align promotional activity with retailers’ events.• Exclusives and limited edition ranges.• Develop brand shop-in-shop concepts.• Develop own standalone flagship or pop-up shop concepts.• Look to provide educational content instore.

Recommendation for retailers• Partnerships with foodservice operators.• Devote areas of store to non-retailing space.• Reallocate and reskill employees to new tasks and away from

manual roles.

Recommendation for suppliers• Explore new impulse and cross-merchandising opportunities

instore aligned to expanded foodservice options.• Increase food-to-go offerings.

Recommendation for retailers• Investment in automation of front end solutions.• Ensure true digital integration – may require ramping up

investment in own tech capabilities (e.g. Walmart Pay).

Recommendation for suppliers• Partner with retailers to tap into the in-store tailored marketing

opportunities that digital enables.• Explore new impulse opportunities around online

collection points.• Ensuring just-in-time and in full deliveries to enable retailers to

fulfil effectively from the store.

Recommendation for retailers• Range rationalisation.• Increase focus on fresh category.• Partnerships with third party non-competitive retail authorities.• Private label innovation and expansion.• Focus on shopper missions and occasions.

Recommendation for suppliers• Diversify brands from mass-market to mass-premium and

extend sub-brands (see Store Positioning capability).• Private label opportunities.

Implications for retailers and suppliers across the four differentiated characteristics

Experiential Social

Frictionless Curated

41 | Store of the Future 2017

Key Capabilities

42 | Store of the Future 2017

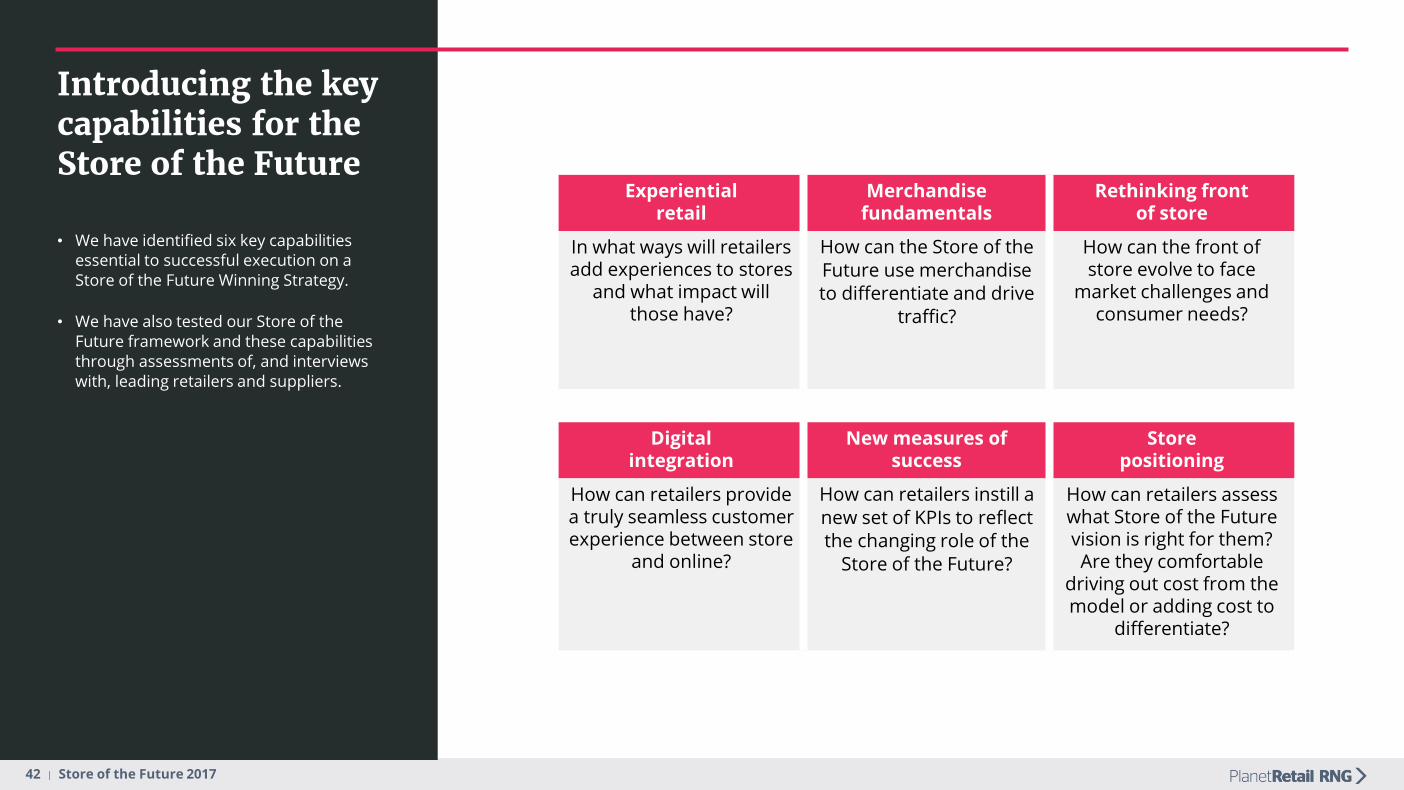

Introducing the key capabilities for the Store of the Future

• We have identified six key capabilities essential to successful execution on a Store of the Future Winning Strategy.

• We have also tested our Store of the Future framework and these capabilities through assessments of, and interviews with, leading retailers and suppliers.

Experientialretail

Merchandise fundamentals

Rethinking front of store

In what ways will retailers add experiences to stores

and what impact will those have?

How can the Store of the Future use merchandise to differentiate and drive

traffic?

How can the front of store evolve to face

market challenges and consumer needs?

Digitalintegration

New measures of success

Storepositioning

How can retailers provide a truly seamless customer experience between store

and online?

How can retailers instill a new set of KPIs to reflect the changing role of the

Store of the Future?

How can retailers assess what Store of the Future vision is right for them? Are they comfortable

driving out cost from the model or adding cost to

differentiate?

43 | Store of the Future 2017

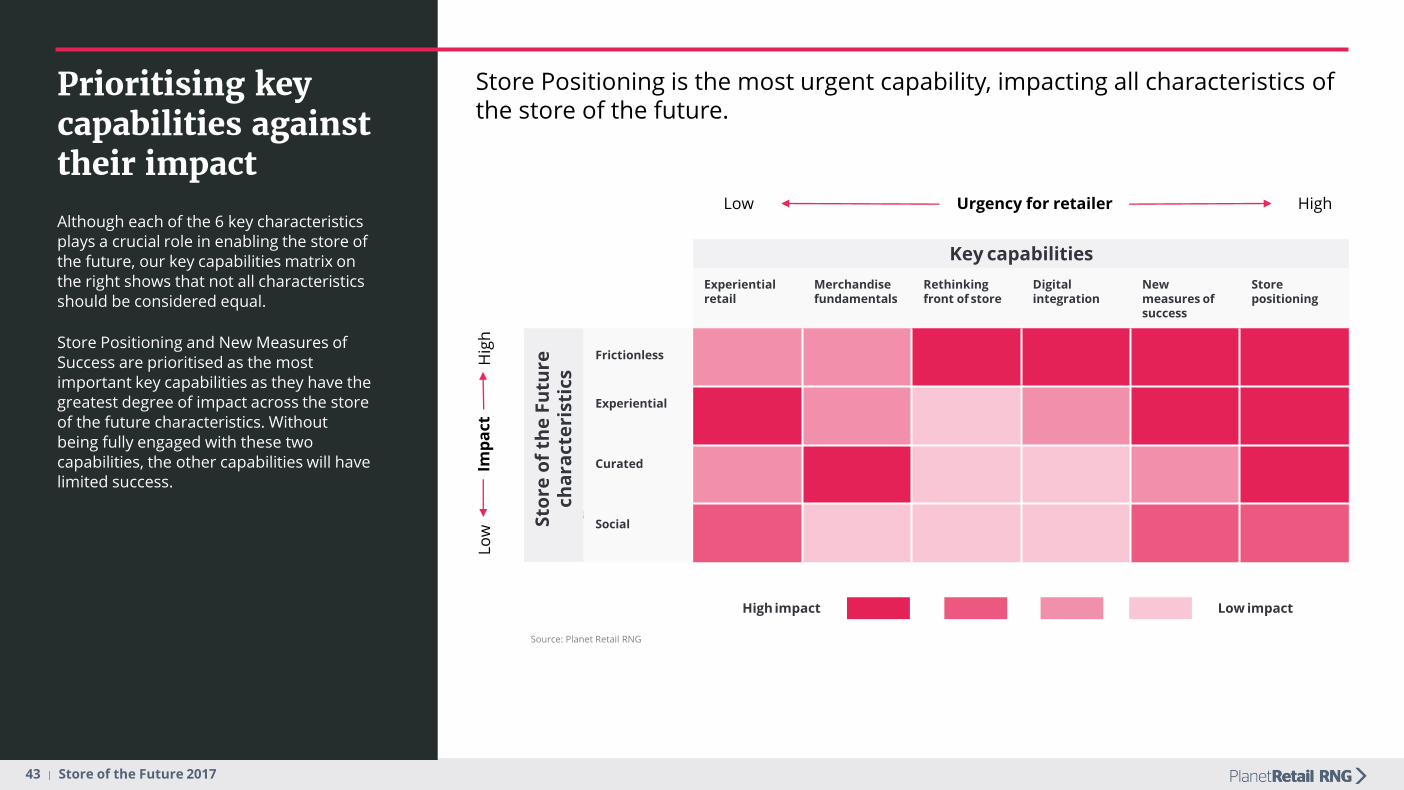

Prioritising key capabilities against their impact

Although each of the 6 key characteristics plays a crucial role in enabling the store of the future, our key capabilities matrix on the right shows that not all characteristics should be considered equal.

Store Positioning and New Measures of Success are prioritised as the most important key capabilities as they have the greatest degree of impact across the store of the future characteristics. Without being fully engaged with these two capabilities, the other capabilities will have limited success.

Imp

act

Urgency for retailer

Hig

hLo

w

Low High

Store Positioning is the most urgent capability, impacting all characteristics of the store of the future.

ch

ara

cte

rist

ics

Key capabilities

Experientialretail

Merchandisefundamentals

Rethinkingfront of store

Digitalintegration

Newmeasures ofsuccess

Storepositioning

Sto

re o

fth

e F

utu

rech

ara

cte

rist

ics

Frictionless

Experiential

Curated

Social

High impact Low impact

Source: Planet Retail RNG

44 | Store of the Future 2017

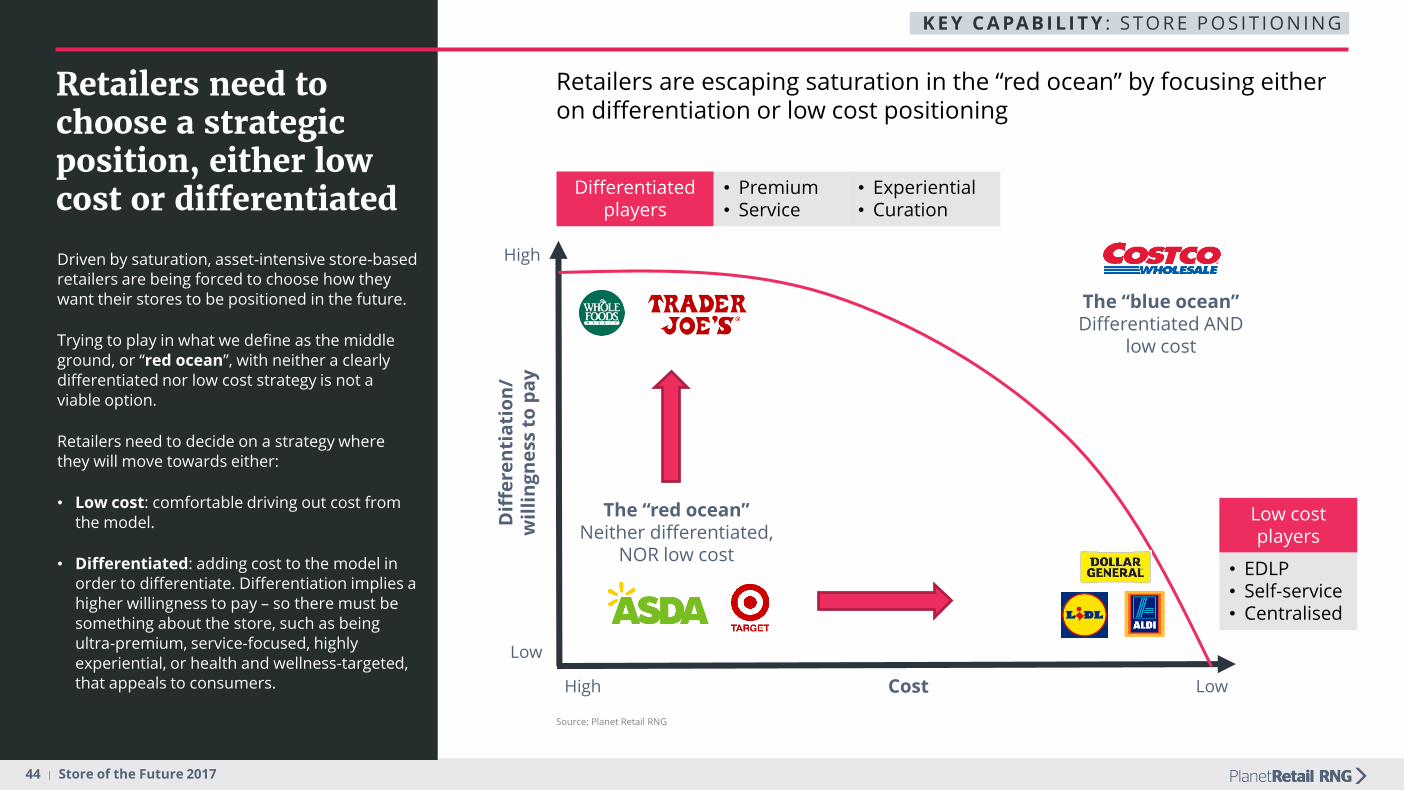

Retailers need to choose a strategic position, either low cost or differentiated

High

Low

CostHigh Low

Dif

fere

nti

ati

on

/ w

illi

ng

ne

ss t

o p

ay

Driven by saturation, asset-intensive store-based retailers are being forced to choose how they want their stores to be positioned in the future.

Trying to play in what we define as the middle ground, or “red ocean”, with neither a clearly differentiated nor low cost strategy is not a viable option.

Retailers need to decide on a strategy where they will move towards either:

• Low cost: comfortable driving out cost from the model.

• Differentiated: adding cost to the model in order to differentiate. Differentiation implies a higher willingness to pay – so there must be something about the store, such as being ultra-premium, service-focused, highly experiential, or health and wellness-targeted, that appeals to consumers.

Differentiated players

The “red ocean”Neither differentiated,

NOR low cost

Low cost players

Source: Planet Retail RNG

K E Y C A PA B I L I T Y : S TO R E P O S I T I O N I N G

Retailers are escaping saturation in the “red ocean” by focusing either on differentiation or low cost positioning

• EDLP• Self-service• Centralised

• Premium• Service

• Experiential• Curation

The “blue ocean”Differentiated AND

low cost

45 | Store of the Future 2017

Boundaries continue to be redefined

High

Low

CostHigh Low

Dif

fere

nti

ati

on

/ w

illi

ng

ne

ss t

o p

ay

The differentiated and low cost criteria continue to be redefined as leading operators constantly evolve and push the positional boundaries.

Retailers are attempting to enter the “blue ocean” by offering both differentiation and low cost.

Discounters realise that offering the bare minimum is no longer enough to retain and attract the evolving shopper.

Leading operators such as Lidl and Aldi are expanding their fresh and organic ranges, forging new partnerships and testing online collection services.

The need to attract new consumers and stay relevant means they are investing in different concepts that they would have simply viewed as adding complexity (and cost) in the past.

Differentiated players

The “red ocean”Neither

differentiated, NOR low cost

The “blue ocean”Differentiated AND

low cost

Low cost players

Source: Planet Retail RNG

K E Y C A PA B I L I T Y : S TO R E P O S I T I O N I N G

Leading players don’t stand still and are looking to offer both differentiation and low cost

In September 2017, Lidl launched an exclusive range of fashion items designed in collaboration with model Heidi Klum.

Lidl’s new-concept store, scheduled to open in late 2018/early 2019 in Sweden, will feature a ‘deli shop’ plus a restaurant and meeting areas.

Amazon slashed prices at Whole Foods in August 2017 as it looked to widen its appeal and shed its expensive image.

46 | Store of the Future 2017

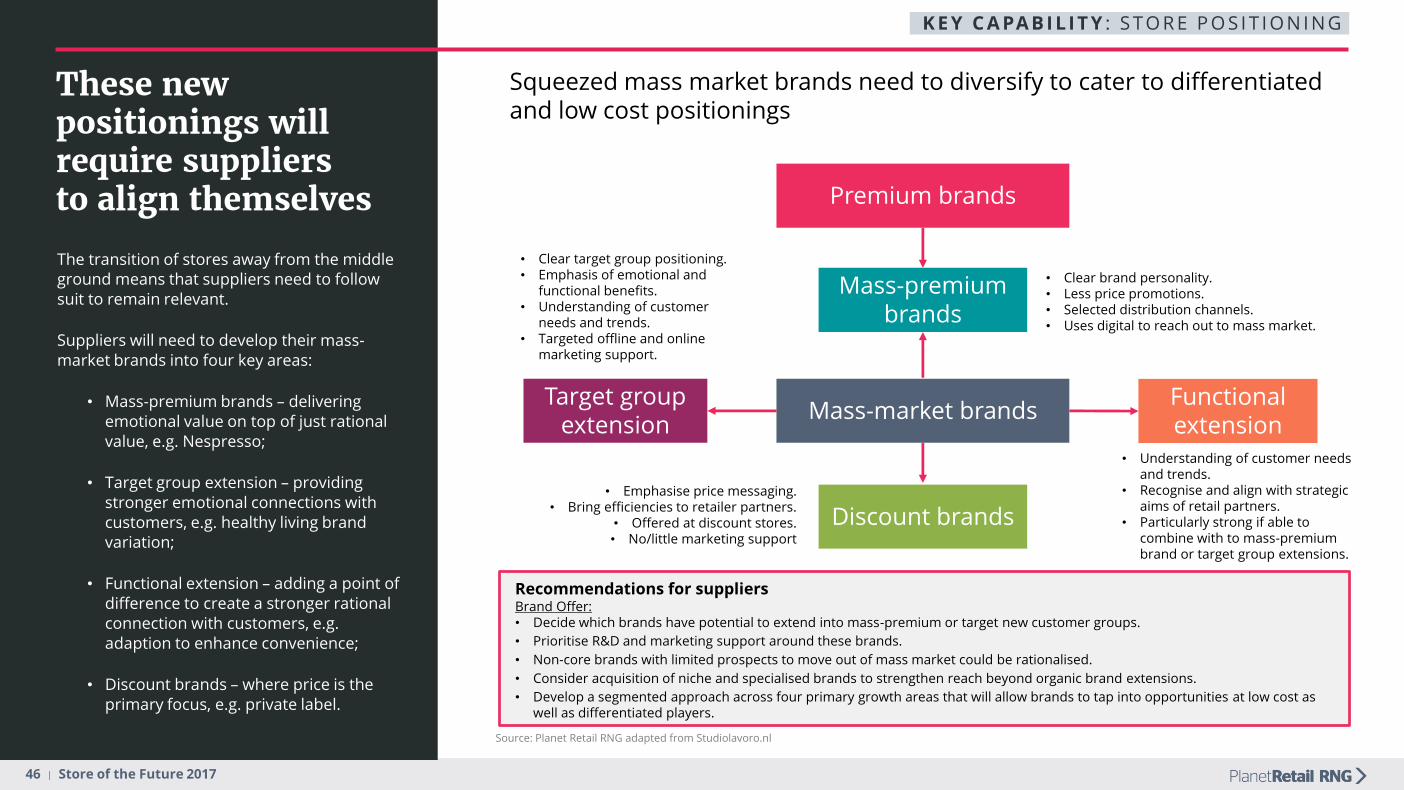

These new positionings will require suppliers to align themselves

Mass-market brands

Mass-premium brands

Discount brands

Functional extension

Target group extension

Premium brands

The transition of stores away from the middle ground means that suppliers need to follow suit to remain relevant.

Suppliers will need to develop their mass-market brands into four key areas:

• Mass-premium brands – delivering emotional value on top of just rational value, e.g. Nespresso;

• Target group extension – providing stronger emotional connections with customers, e.g. healthy living brand variation;

• Functional extension – adding a point of difference to create a stronger rational connection with customers, e.g. adaption to enhance convenience;

• Discount brands – where price is the primary focus, e.g. private label.

Source: Planet Retail RNG adapted from Studiolavoro.nl

K E Y C A PA B I L I T Y : S TO R E P O S I T I O N I N G

Squeezed mass market brands need to diversify to cater to differentiated and low cost positionings

Recommendations for suppliersBrand Offer: • Decide which brands have potential to extend into mass-premium or target new customer groups.

• Prioritise R&D and marketing support around these brands.

• Non-core brands with limited prospects to move out of mass market could be rationalised.

• Consider acquisition of niche and specialised brands to strengthen reach beyond organic brand extensions.

• Develop a segmented approach across four primary growth areas that will allow brands to tap into opportunities at low cost as well as differentiated players.

• Clear brand personality.• Less price promotions.• Selected distribution channels. • Uses digital to reach out to mass market.

• Clear target group positioning.• Emphasis of emotional and

functional benefits.• Understanding of customer

needs and trends.• Targeted offline and online

marketing support.

• Understanding of customer needs and trends.

• Recognise and align with strategic aims of retail partners.

• Particularly strong if able to combine with to mass-premium brand or target group extensions.

• Emphasise price messaging.• Bring efficiencies to retailer partners.

• Offered at discount stores.• No/little marketing support

47 | Store of the Future 2017

Stores creating a seamless experience with online

What is it?

Access to, and transparency of, relevant information at every step of the shopping journey. Digital and mobile technologies are driving consumer expectations of consistent pricing, convenience and service irrespective of channel.

Why is it important?

Urban shoppers are seeking instant gratification, combined with the availability of the endless aisle, and convenience of click & collect.

The pressure to reduce labour costs and improve efficiencies and customer service levels in-store through digital integration.

The need to engage with and target shoppers based on their personal information and online behaviour.

K E Y C A PA B I L I T Y : D I G I TA L I N T E G R AT I O N

Sainsbury’s - Argos (London, UK) –Digital Ordering/Pickup In-Store

Walmart (Arkansas, USA) –Automated Pickup Kiosk In-Store

O2

OD

igit

al e

xp

eri

en

ceTra

nsp

are

ncy

Walmart (Texas, USA) –Endless Aisle

IKEA (USA)Augmented Reality Shopping

Hema by Alibaba (China) –Scan for Product Info

Carrefour (Taoyuan, Taiwan) –3D Virtual Fitting Room

Walgreens Boots Alliance (UK) –Mobile Sales Assistant

Amazon Books (USA) – Price Parity with Online Website

Farfetch (London, UK) –RFID-Enabled Clothing Rack

48 | Store of the Future 2017

Digital can create a win-win for all

Supplier Case Study: Coca-Cola’s In-Store Digital Signage

• In 2017, Coca-Cola rolled out a new digital signage system attached to endcaps in the centre store of US grocery outlets to deliver branded video and e-coupons to customers.

• The project was launched after Albertsons noticed fewer grocery shoppers were venturing down the beverage aisle and soda sales were slumping.

• The digital signage can tailor content messaging to approaching shoppers based on data from their smartphones.

• Targeted messaging can range from brand campaigns to store-specific promotional offers or even app-guided shopping lists.

• A 250-store pilot with Albertsons delivered a one-month return on investment.

• Albertsons also experienced a significant increase in overall category sales.

Implications:

Retailers that optimise their click & collect services to offer a frictionless in-store experience will stand out over retailers who have lagged behind in ecommerce fulfilment capabilities.

Incorporating emerging technologies into store trips differentiates the physical experience, while the fascination with new digital capabilities can be a significant driver of footfall.

Retailers and brands can leverage new technologies to collect impactful Big Data over time that will aid them in better serving customer needs.

Recommendations for suppliersDemand Chain Capabilities:• Brands should be open to aligning with non-traditional partners, including technology companies and data owners such as

Google. Does your brand have the right organisation and skills to support such partnerships?

• Suppliers that are able to demonstrate they are at the forefront of digital change will be able to position themselves as strongpartners with retailers. As such, suppliers may have to view investment in supporting digital initiatives in new ways – ensuring that ROI is seen as just one measure as part of developing a more holistic long-term relationship with retailers.

• Retailers’ mobile apps and their own in-store technology means they will increasingly be the gatekeepers between brands and shoppers in the store. Suppliers will need to ensure they have priority positioning across digital interfaces. Suppliers should therefore already be supporting retailers’ digital efforts through the provision of strong content and promotional initiatives.

• Suppliers should already be considering what proportion of their marketing and promotional spend should be diverted towards supporting such initiatives in the next five years.

K E Y C A PA B I L I T Y : D I G I TA L I N T E G R AT I O N

49 | Store of the Future 2017

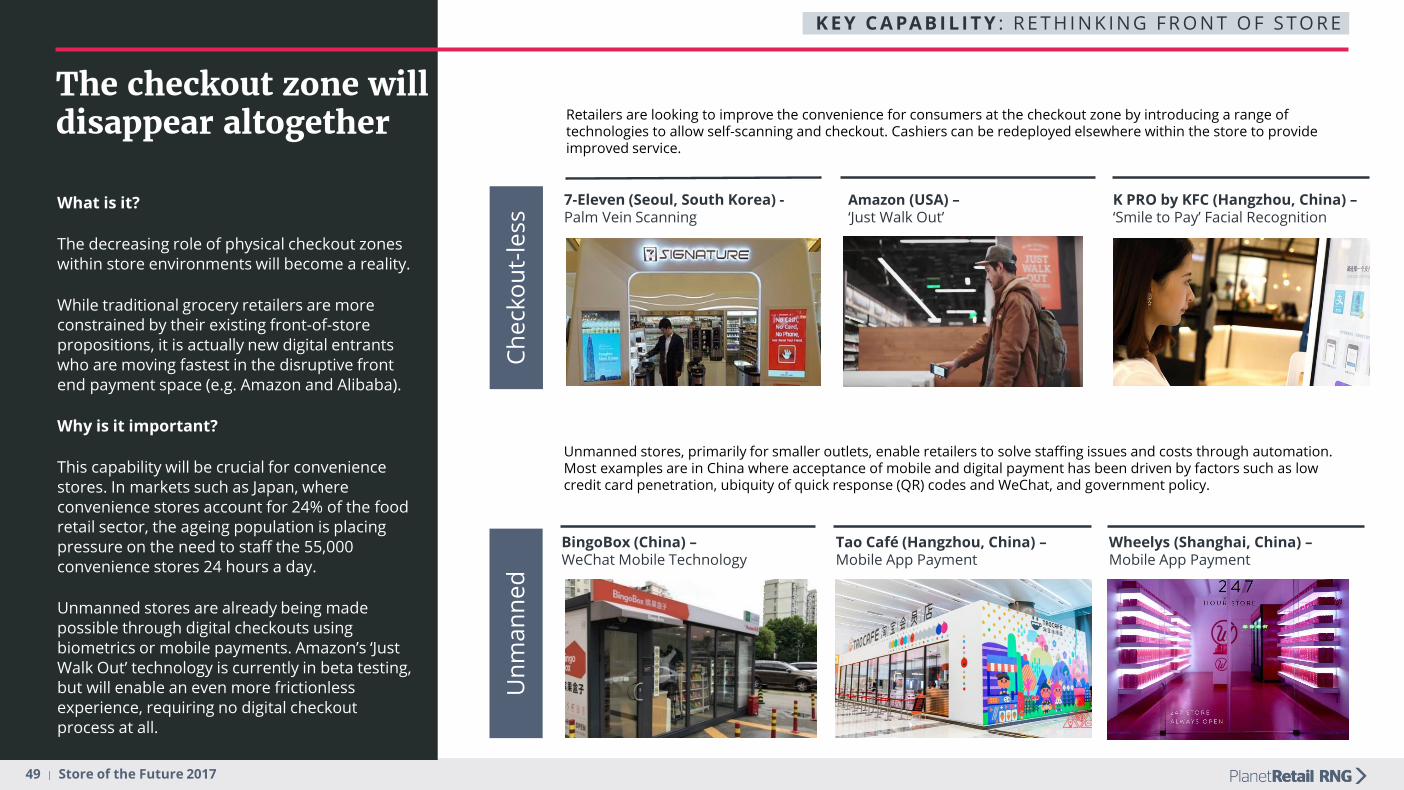

The checkout zone will disappear altogether

What is it?

The decreasing role of physical checkout zones within store environments will become a reality.

While traditional grocery retailers are more constrained by their existing front-of-store propositions, it is actually new digital entrants who are moving fastest in the disruptive front end payment space (e.g. Amazon and Alibaba).

Why is it important?

This capability will be crucial for convenience stores. In markets such as Japan, where convenience stores account for 24% of the food retail sector, the ageing population is placing pressure on the need to staff the 55,000 convenience stores 24 hours a day.

Unmanned stores are already being made possible through digital checkouts using biometrics or mobile payments. Amazon’s ‘Just Walk Out’ technology is currently in beta testing, but will enable an even more frictionless experience, requiring no digital checkout process at all.

K E Y C A PA B I L I T Y : R E T H I N K I N G F R O N T O F S TO R E

BingoBox (China) –WeChat Mobile Technology

7-Eleven (Seoul, South Korea) -Palm Vein Scanning

Amazon (USA) –‘Just Walk Out’

Ch

eck

ou

t-le

ssU

nm

an

ne

d

K PRO by KFC (Hangzhou, China) –‘Smile to Pay’ Facial Recognition

Tao Café (Hangzhou, China) –Mobile App Payment

Retailers are looking to improve the convenience for consumers at the checkout zone by introducing a range of technologies to allow self-scanning and checkout. Cashiers can be redeployed elsewhere within the store to provide improved service.

Wheelys (Shanghai, China) –Mobile App Payment

Unmanned stores, primarily for smaller outlets, enable retailers to solve staffing issues and costs through automation. Most examples are in China where acceptance of mobile and digital payment has been driven by factors such as low credit card penetration, ubiquity of quick response (QR) codes and WeChat, and government policy.

50 | Store of the Future 2017

Suppliers can exploit the new impulse opportunities New impulse siting opportunities

• Hershey is looking to tap into initiatives that are playing a greater role in stores of the future, such as vending machines located at curbside collection points.

• Meanwhile, the expansion of foodservice options and shopper mission-based ranges, such as food-to-go or “big night in”, provides new siting opportunities for snack, confectionery and beverage brands.

With physical checkouts having a decreased role in the store of the future, suppliers of impulse products need to identify and maximise new impulse opportunities.

Impulse will still exist, but is shifting to where the growth is occurring - towards online, discount and convenience.

The dunnhumby Global Trends study of shopping behaviour across 18 countries showed the average frequency of shopping trips increased by some 18% over the last five years as this shift occurred.

As a result, new product siting opportunities exist as retailers look to introduce more foodservice options and collection points, as well as any new digital integration that enables greater and more targeted engagement with shoppers.

© B

ell O

ne

Digital impulse

• The greater use of in-store digital technology to replace the front end provides opportunities for brands to generate impulse through targeted promotions.

• In 2015, Unilever used beacon technology in Tesco stores in the UK to send Magnum promotions to users of its app when either in-store or passing by.

• Meanwhile, augmented and virtual reality will allow brands to create a range of digital impulse opportunities as shoppers navigate the store.

K E Y C A PA B I L I T Y : R E T H I N K I N G F R O N T O F S TO R E

51 | Store of the Future 2017

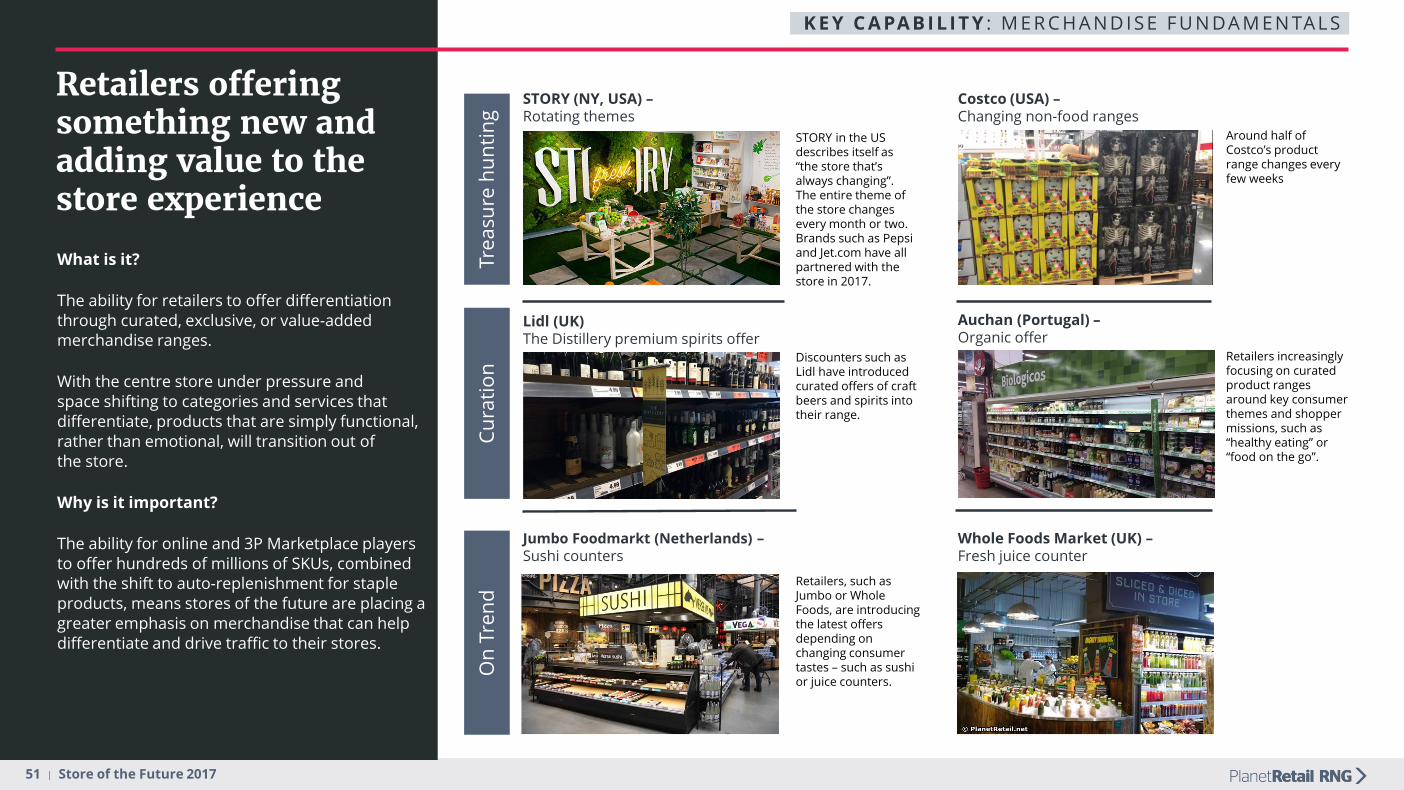

Retailers offering something new and adding value to the store experience

What is it?

The ability for retailers to offer differentiation through curated, exclusive, or value-added merchandise ranges.

With the centre store under pressure and space shifting to categories and services that differentiate, products that are simply functional, rather than emotional, will transition out of the store.

Why is it important?

The ability for online and 3P Marketplace players to offer hundreds of millions of SKUs, combined with the shift to auto-replenishment for staple products, means stores of the future are placing a greater emphasis on merchandise that can help differentiate and drive traffic to their stores.

K E Y C A PA B I L I T Y : M E R C H A N D I S E F U N DA M E N TA L S

STORY (NY, USA) –Rotating themes

Whole Foods Market (UK) –Fresh juice counter

Costco (USA) –Changing non-food ranges

Lidl (UK) The Distillery premium spirits offer

Jumbo Foodmarkt (Netherlands) –Sushi counters

Auchan (Portugal) –Organic offer

Tre

asu

re h

un

tin

gC

ura

tio

nO

n T

ren

d

STORY in the US describes itself as “the store that’s always changing”. The entire theme of the store changes every month or two. Brands such as Pepsi and Jet.com have all partnered with the store in 2017.

Retailers increasingly focusing on curated product ranges around key consumer themes and shopper missions, such as “healthy eating” or “food on the go”.

Retailers, such as Jumbo or Whole Foods, are introducing the latest offers depending on changing consumer tastes – such as sushi or juice counters.

Around half of Costco’s product range changes every few weeks

Discounters such as Lidl have introduced curated offers of craft beers and spirits into their range.

52 | Store of the Future 2017

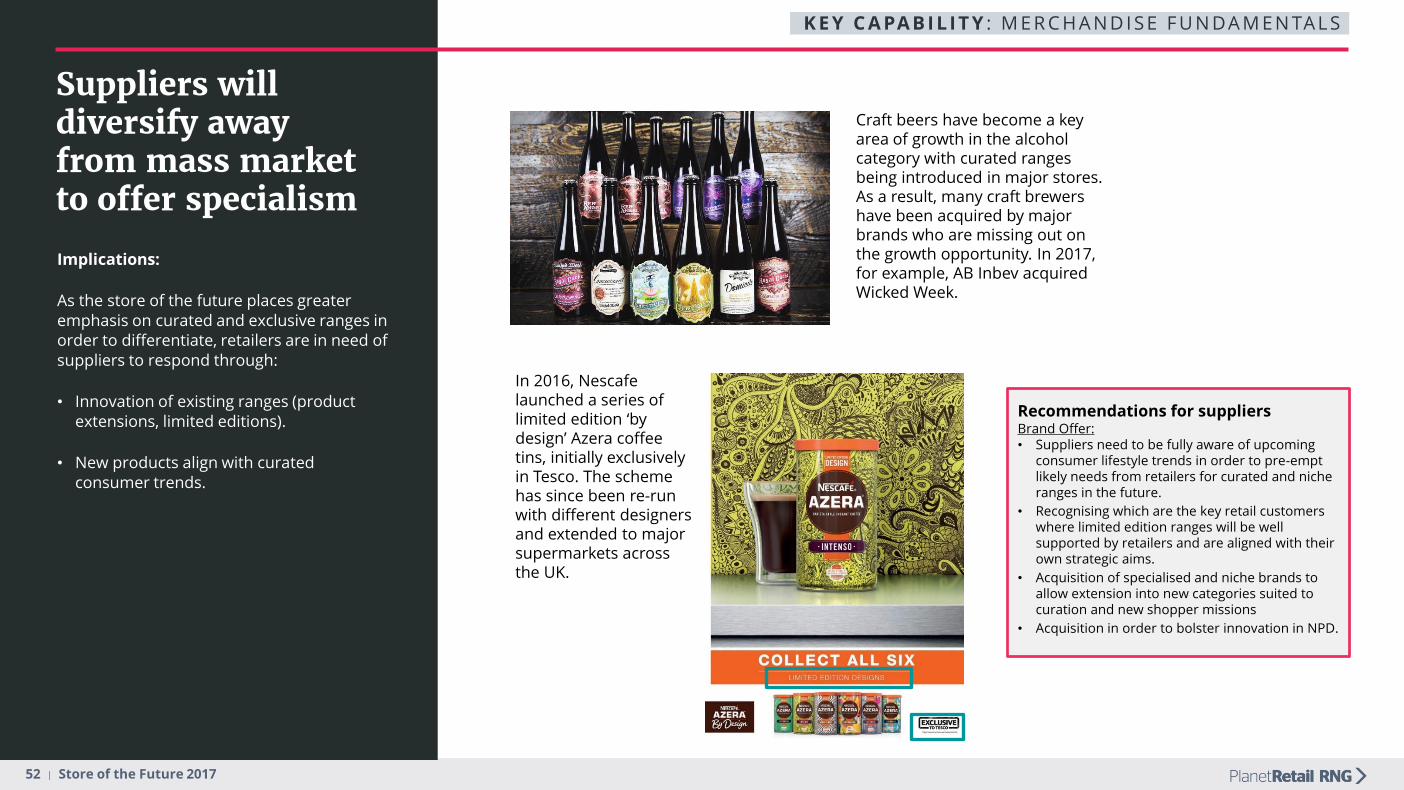

Suppliers will diversify away from mass marketto offer specialism

Implications:

As the store of the future places greater emphasis on curated and exclusive ranges in order to differentiate, retailers are in need of suppliers to respond through:

• Innovation of existing ranges (product extensions, limited editions).

• New products align with curated consumer trends.

In 2016, Nescafe launched a series of limited edition ‘by design’ Azera coffee tins, initially exclusively in Tesco. The scheme has since been re-run with different designers and extended to major supermarkets across the UK.

Craft beers have become a key area of growth in the alcohol category with curated ranges being introduced in major stores. As a result, many craft brewers have been acquired by major brands who are missing out on the growth opportunity. In 2017, for example, AB Inbev acquired Wicked Week.

Recommendations for suppliersBrand Offer:• Suppliers need to be fully aware of upcoming

consumer lifestyle trends in order to pre-empt likely needs from retailers for curated and niche ranges in the future.

• Recognising which are the key retail customers where limited edition ranges will be well supported by retailers and are aligned with their own strategic aims.

• Acquisition of specialised and niche brands to allow extension into new categories suited to curation and new shopper missions

• Acquisition in order to bolster innovation in NPD.

K E Y C A PA B I L I T Y : M E R C H A N D I S E F U N DA M E N TA L S

53 | Store of the Future 2017

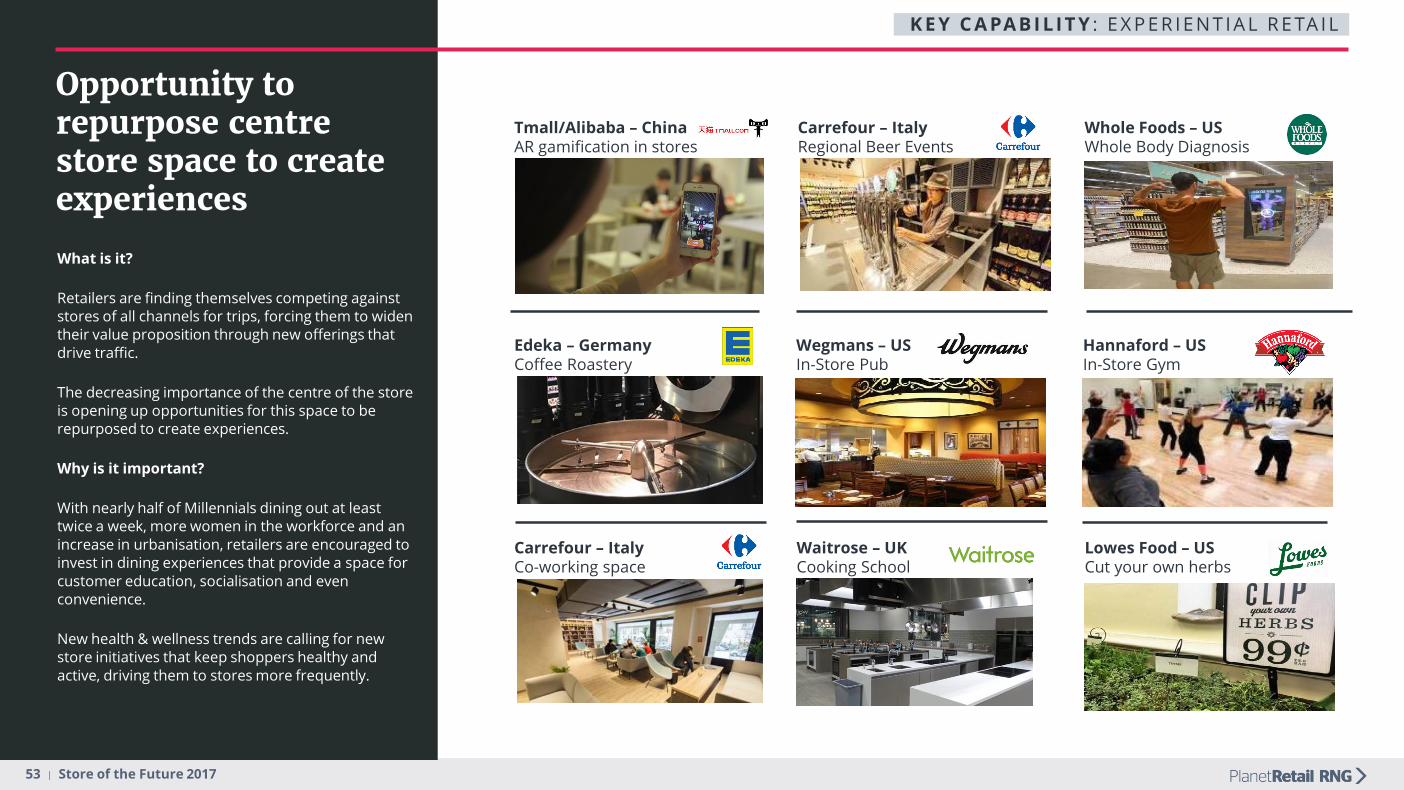

Opportunity to repurpose centrestore space to create experiences

What is it?

Retailers are finding themselves competing against stores of all channels for trips, forcing them to widen their value proposition through new offerings that drive traffic.

The decreasing importance of the centre of the store is opening up opportunities for this space to be repurposed to create experiences.

Why is it important?

With nearly half of Millennials dining out at least twice a week, more women in the workforce and an increase in urbanisation, retailers are encouraged to invest in dining experiences that provide a space for customer education, socialisation and even convenience.

New health & wellness trends are calling for new store initiatives that keep shoppers healthy and active, driving them to stores more frequently.

Tmall/Alibaba – China AR gamification in stores

Lowes Food – USCut your own herbs

Whole Foods – USWhole Body Diagnosis

Carrefour – ItalyRegional Beer Events

Edeka – GermanyCoffee Roastery

Waitrose – UKCooking School

Hannaford – US In-Store Gym

Wegmans – US In-Store Pub

Carrefour – ItalyCo-working space

K E Y C A PA B I L I T Y : E X P E R I E N T I A L R E TA I L

54 | Store of the Future 2017

Brands can partner with retailers to provide experiences Supplier Case Study - The “Candy Experience” by The

Hershey Company

• The “Candy Experience” by The Hershey Company is a 729 sq ft store-within-a-store placed in high traffic areas of the store away from the confectionery aisle –at the front of the store, for example.

• It features curved displays, bright graphics and easy-to-shop sections sorted by category, removing the clutter of traditional candy aisles.

• The initiative was based on Hershey research that showed that the candy category ranks last for ease of shopping, with 76% of shoppers unhappy with the clutter in the aisle.

• The initiative was first trialled in 2016 in the US.

• The result was a 25% increase in category retail sales with retailer investment payback achieved in less than two years.

Recommendations for suppliersBrand Offer:• Suppliers should partner with retailers to create shop-in-shop

experiences, brand implants, innovative promotions and in-store displays to help them enhance the experiential function of the store.

• Such brand touchpoints should also be considered in terms of the wider holistic benefits in terms of brand perception and online sales.

K E Y C A PA B I L I T Y : E X P E R I E N T I A L R E TA I L

Implications:

With retailers looking for new ways to provide experience to shoppers, suppliers have the opportunity to generate higher levels of brand engagement and in-store activation.

The declining role of the centre of store will open up additional space for experiences. In addition, brands will be looking to reduce their reliance on the centreof store and build a presence in new locations.

This will change the traditional, mainly transactional, relationship between retailers and suppliers towards a much more collaborative approach where both seek solutions.

55 | Store of the Future 2017

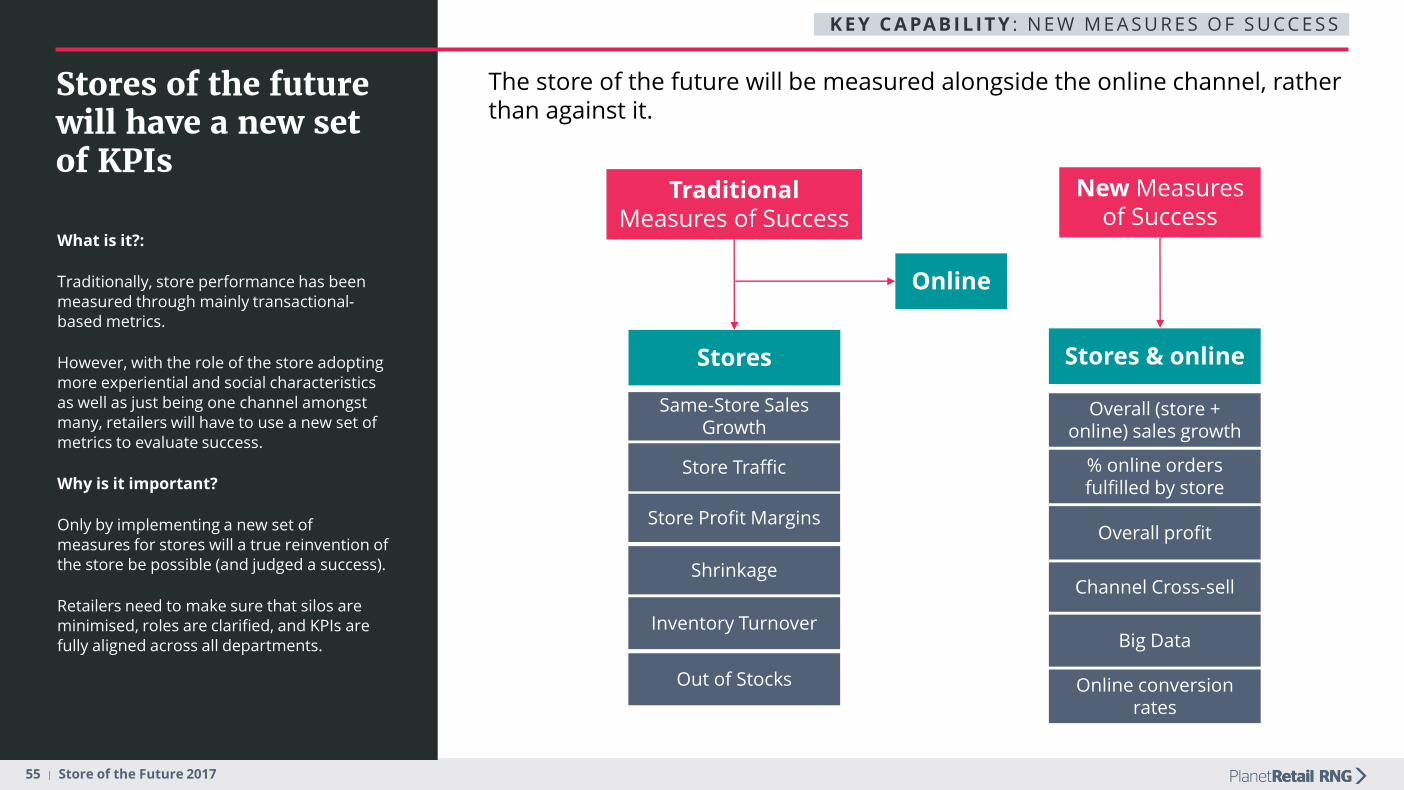

Stores of the future will have a new set of KPIs

What is it?:

Traditionally, store performance has been measured through mainly transactional-based metrics.

However, with the role of the store adopting more experiential and social characteristics as well as just being one channel amongst many, retailers will have to use a new set of metrics to evaluate success.

Why is it important?

Only by implementing a new set of measures for stores will a true reinvention of the store be possible (and judged a success).

Retailers need to make sure that silos are minimised, roles are clarified, and KPIs are fully aligned across all departments.

TraditionalMeasures of Success

New Measures of Success

Same-Store Sales Growth

Store Profit Margins

Store Traffic

Shrinkage

Overall (store + online) sales growth

Overall profit

Channel Cross-sell

% online orders fulfilled by store

Inventory TurnoverBig Data

Out of Stocks

Stores

Online

Stores & online

Online conversion rates

K E Y C A PA B I L I T Y : N E W M E A S U R E S O F S U CC E S S

The store of the future will be measured alongside the online channel, rather than against it.

56 | Store of the Future 2017

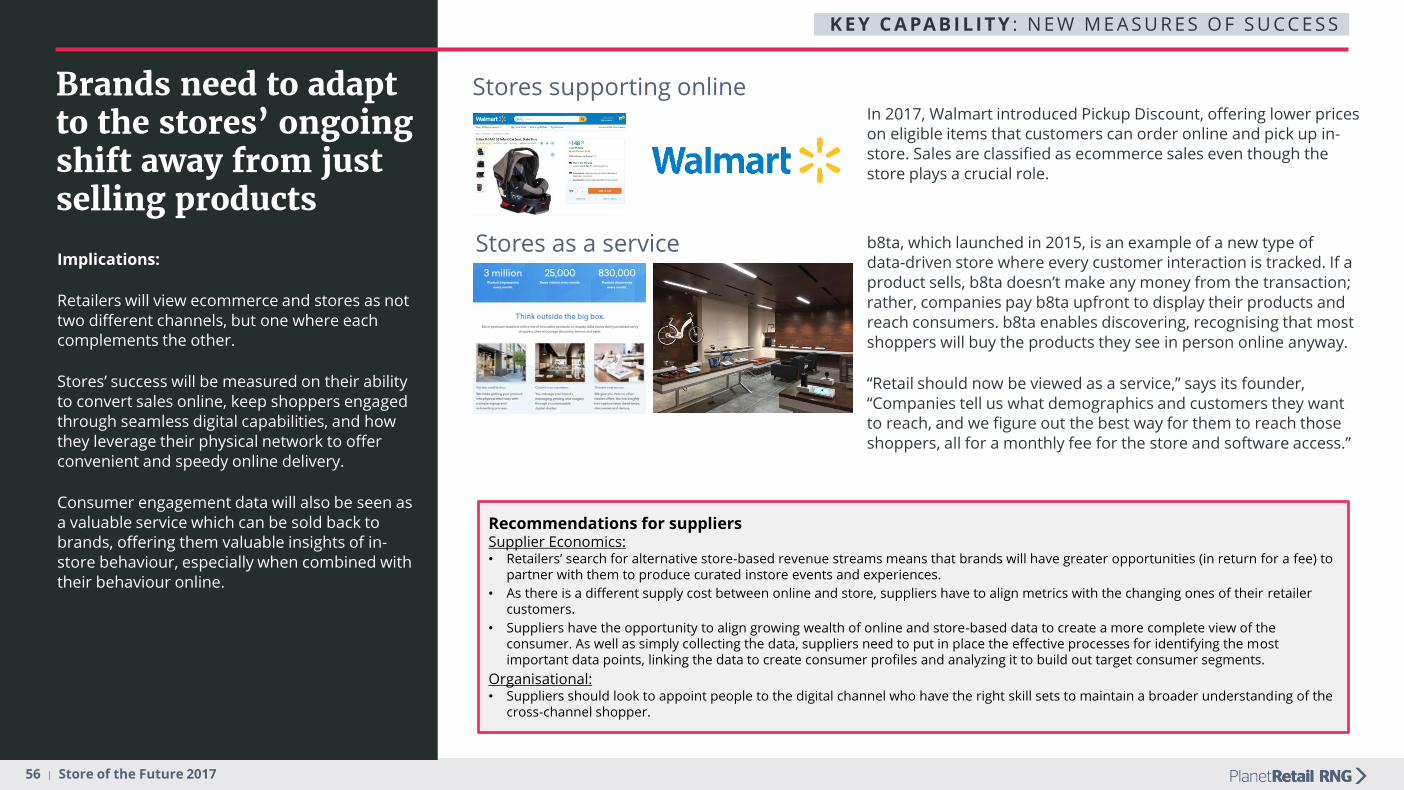

Brands need to adapt to the stores’ ongoing shift away from just selling products

Implications:

Retailers will view ecommerce and stores as not two different channels, but one where each complements the other.

Stores’ success will be measured on their ability to convert sales online, keep shoppers engaged through seamless digital capabilities, and how they leverage their physical network to offer convenient and speedy online delivery.

Consumer engagement data will also be seen as a valuable service which can be sold back to brands, offering them valuable insights of in-store behaviour, especially when combined with their behaviour online.

In 2017, Walmart introduced Pickup Discount, offering lower prices on eligible items that customers can order online and pick up in-store. Sales are classified as ecommerce sales even though the store plays a crucial role.

Stores supporting online

Stores as a service b8ta, which launched in 2015, is an example of a new type of data-driven store where every customer interaction is tracked. If a product sells, b8ta doesn’t make any money from the transaction; rather, companies pay b8ta upfront to display their products and reach consumers. b8ta enables discovering, recognising that most shoppers will buy the products they see in person online anyway.

“Retail should now be viewed as a service,” says its founder, “Companies tell us what demographics and customers they want to reach, and we figure out the best way for them to reach those shoppers, all for a monthly fee for the store and software access.”

Recommendations for suppliersSupplier Economics:• Retailers’ search for alternative store-based revenue streams means that brands will have greater opportunities (in return for a fee) to

partner with them to produce curated instore events and experiences.

• As there is a different supply cost between online and store, suppliers have to align metrics with the changing ones of their retailer customers.

• Suppliers have the opportunity to align growing wealth of online and store-based data to create a more complete view of the consumer. As well as simply collecting the data, suppliers need to put in place the effective processes for identifying the mostimportant data points, linking the data to create consumer profiles and analyzing it to build out target consumer segments.

Organisational:• Suppliers should look to appoint people to the digital channel who have the right skill sets to maintain a broader understanding of the

cross-channel shopper.

K E Y C A PA B I L I T Y : N E W M E A S U R E S O F S U CC E S S

57 | Store of the Future 2017

The future world

58 | Store of the Future 2017

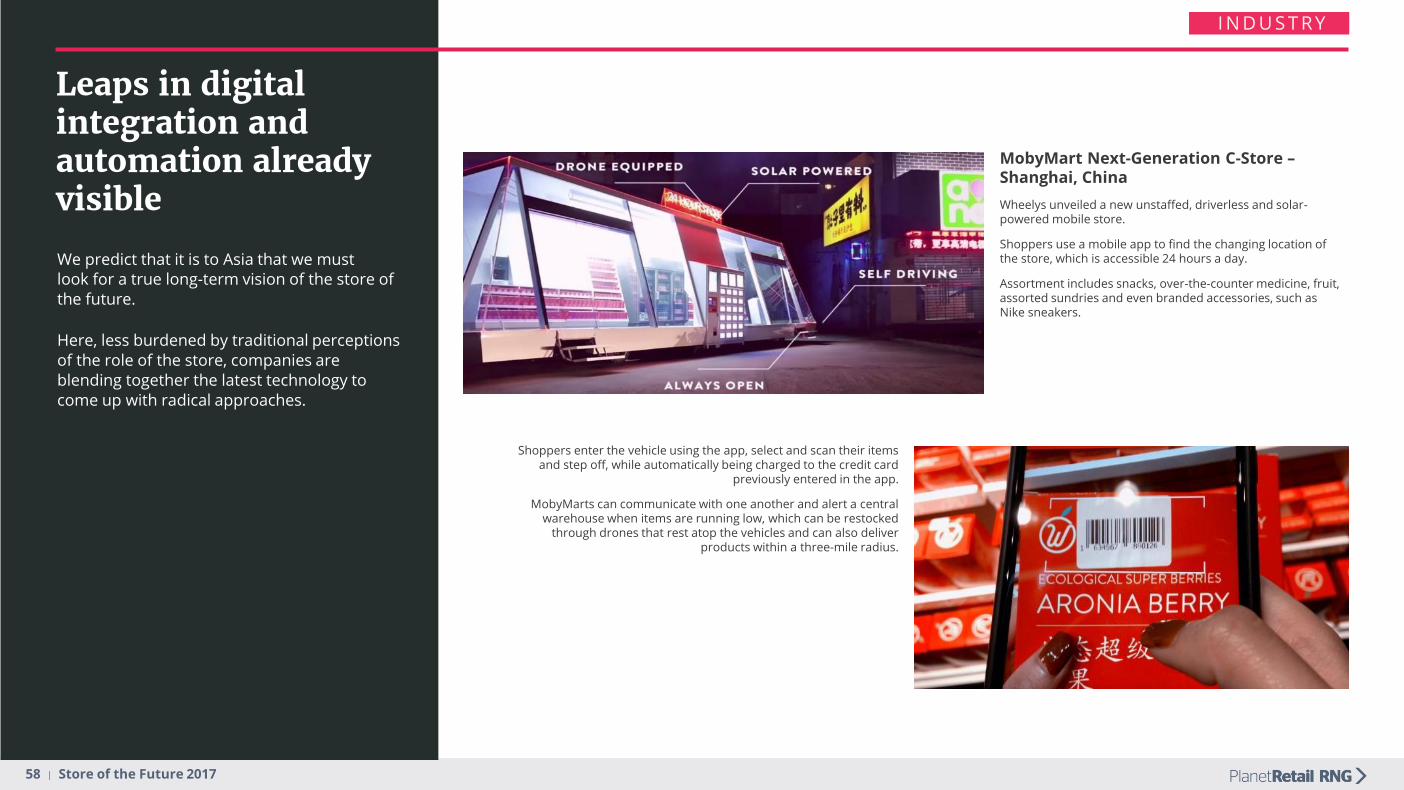

Shoppers enter the vehicle using the app, select and scan their items and step off, while automatically being charged to the credit card

previously entered in the app.

MobyMarts can communicate with one another and alert a central warehouse when items are running low, which can be restocked

through drones that rest atop the vehicles and can also deliver products within a three-mile radius.

Leaps in digital integration and automation already visible

We predict that it is to Asia that we must look for a true long-term vision of the store of the future.

Here, less burdened by traditional perceptions of the role of the store, companies are blending together the latest technology to come up with radical approaches.

I N D U S T R Y

MobyMart Next-Generation C-Store –Shanghai, China

Wheelys unveiled a new unstaffed, driverless and solar-powered mobile store.

Shoppers use a mobile app to find the changing location of the store, which is accessible 24 hours a day.

Assortment includes snacks, over-the-counter medicine, fruit, assorted sundries and even branded accessories, such as Nike sneakers.

59 | Store of the Future 2017

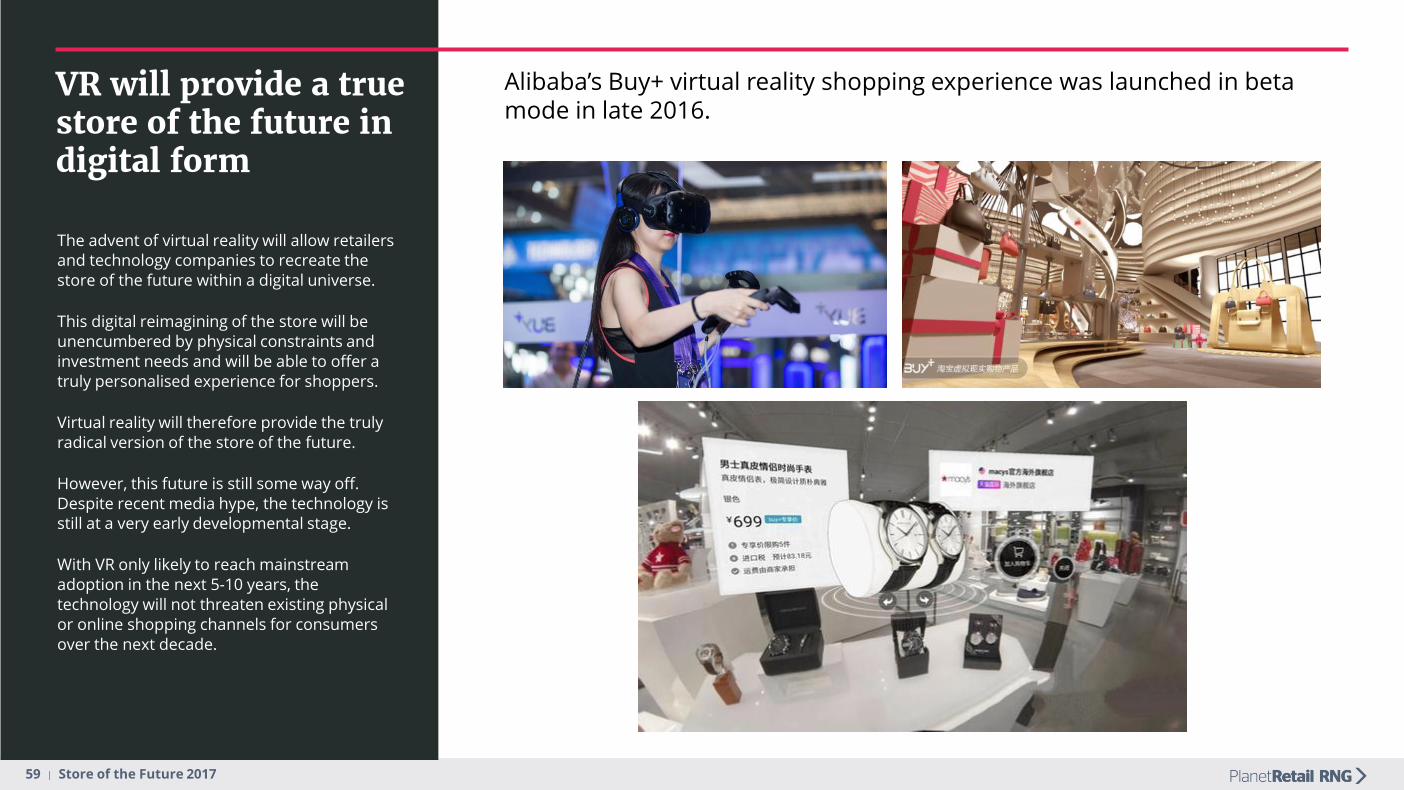

VR will provide a true store of the future in digital form

The advent of virtual reality will allow retailers and technology companies to recreate the store of the future within a digital universe.

This digital reimagining of the store will be unencumbered by physical constraints and investment needs and will be able to offer a truly personalised experience for shoppers.

Virtual reality will therefore provide the truly radical version of the store of the future.

However, this future is still some way off. Despite recent media hype, the technology is still at a very early developmental stage.

With VR only likely to reach mainstream adoption in the next 5-10 years, the technology will not threaten existing physical or online shopping channels for consumers over the next decade.

Alibaba’s Buy+ virtual reality shopping experience was launched in beta mode in late 2016.

60 | Store of the Future 2017

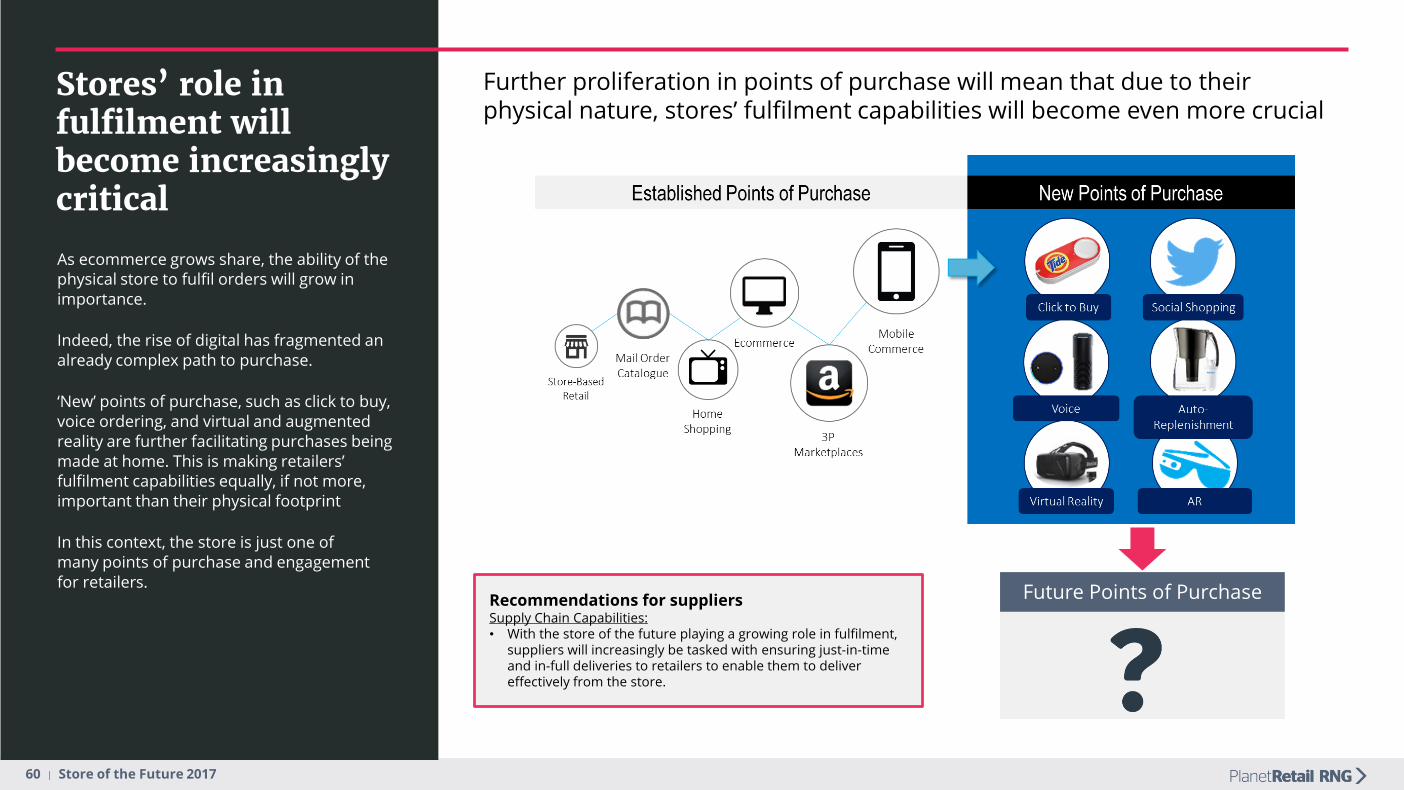

Stores’ role in fulfilment will become increasingly critical

As ecommerce grows share, the ability of the physical store to fulfil orders will grow in importance.

Indeed, the rise of digital has fragmented an already complex path to purchase.

‘New’ points of purchase, such as click to buy, voice ordering, and virtual and augmented reality are further facilitating purchases being made at home. This is making retailers’ fulfilment capabilities equally, if not more, important than their physical footprint

In this context, the store is just one of many points of purchase and engagement for retailers.

Future Points of Purchase Recommendations for suppliersSupply Chain Capabilities: • With the store of the future playing a growing role in fulfilment,

suppliers will increasingly be tasked with ensuring just-in-time and in-full deliveries to retailers to enable them to deliver effectively from the store.

Further proliferation in points of purchase will mean that due to their physical nature, stores’ fulfilment capabilities will become even more crucial

61 | Store of the Future 2017

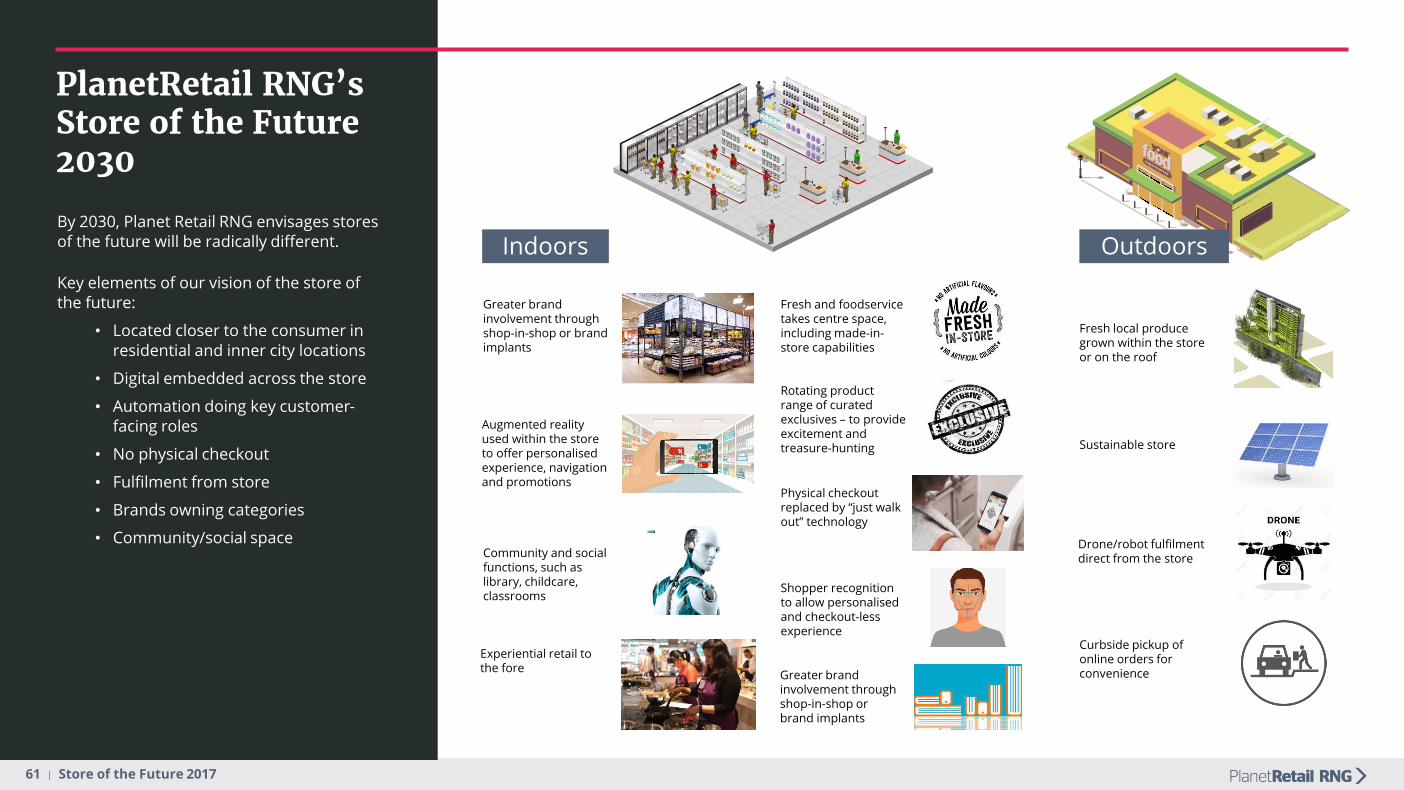

PlanetRetail RNG’s Store of the Future 2030

By 2030, Planet Retail RNG envisages stores of the future will be radically different.

Key elements of our vision of the store of the future:

• Located closer to the consumer in residential and inner city locations

• Digital embedded across the store

• Automation doing key customer-facing roles

• No physical checkout

• Fulfilment from store

• Brands owning categories

• Community/social space

Fresh local produce grown within the store or on the roof

Sustainable store

Drone/robot fulfilment direct from the store

Curbside pickup of online orders for convenience

Indoors Outdoors

Greater brand involvement through shop-in-shop or brand implants

Augmented reality used within the store to offer personalised experience, navigation and promotions

Community and social functions, such as library, childcare, classrooms

Experiential retail to the fore

Fresh and foodservice takes centre space, including made-in-store capabilities

Rotating product range of curated exclusives – to provide excitement and treasure-hunting

Physical checkout replaced by “just walk out” technology

Shopper recognition to allow personalised and checkout-less experience

Greater brand involvement through shop-in-shop or brand implants

62 | Store of the Future 2017

So Whats for Retailers and Suppliers

63 | Store of the Future 2017

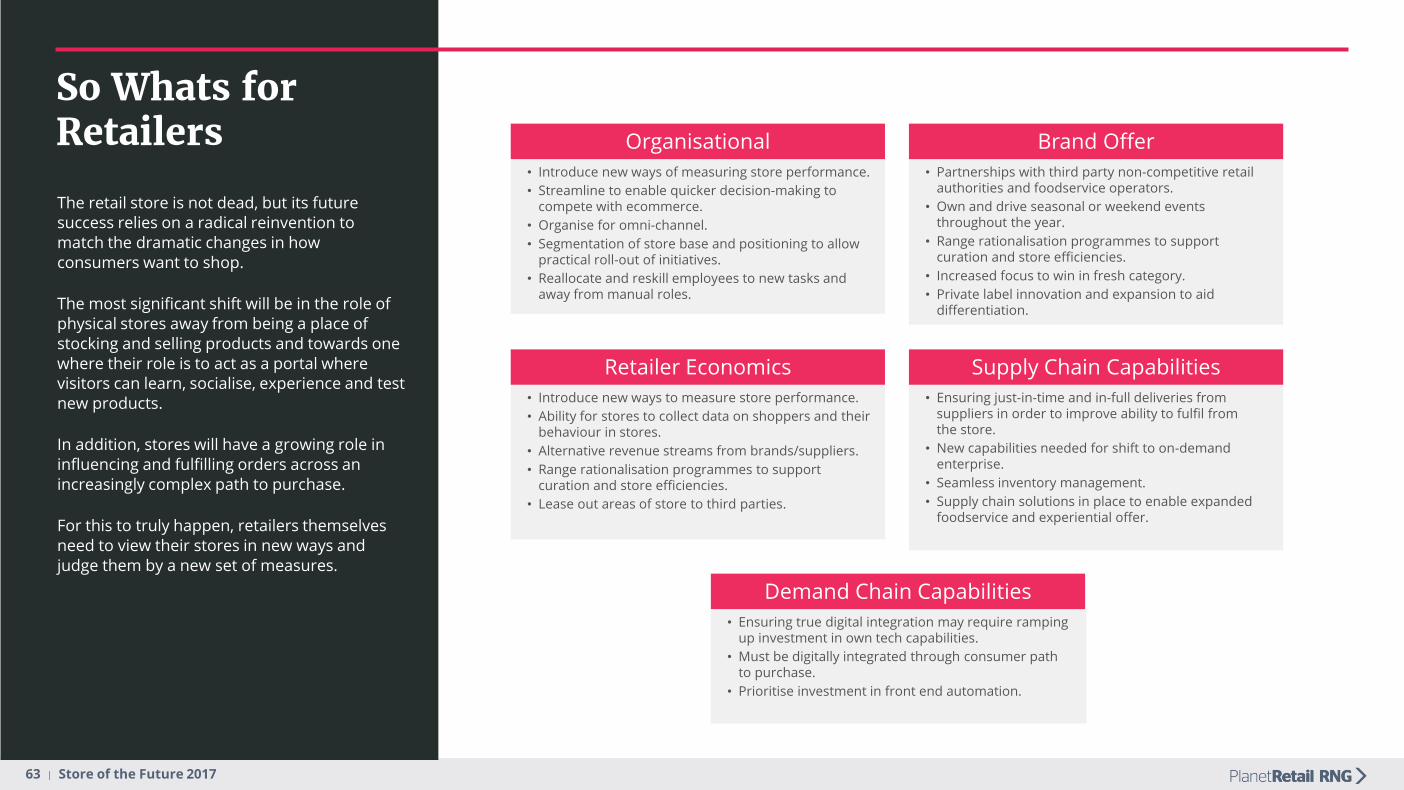

So Whats for Retailers

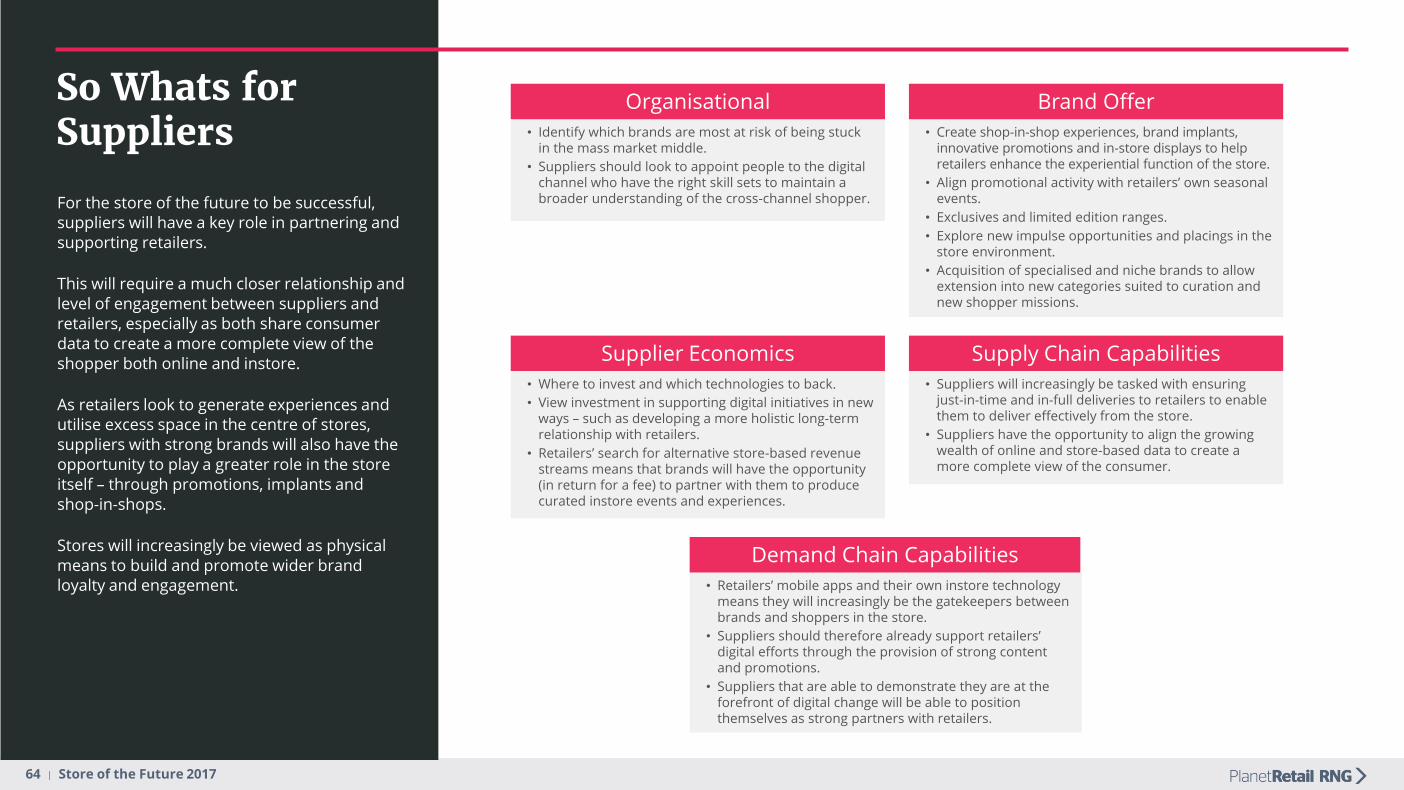

The retail store is not dead, but its future success relies on a radical reinvention to match the dramatic changes in how consumers want to shop.