Stock market special report by epic research 16th july 2014

8

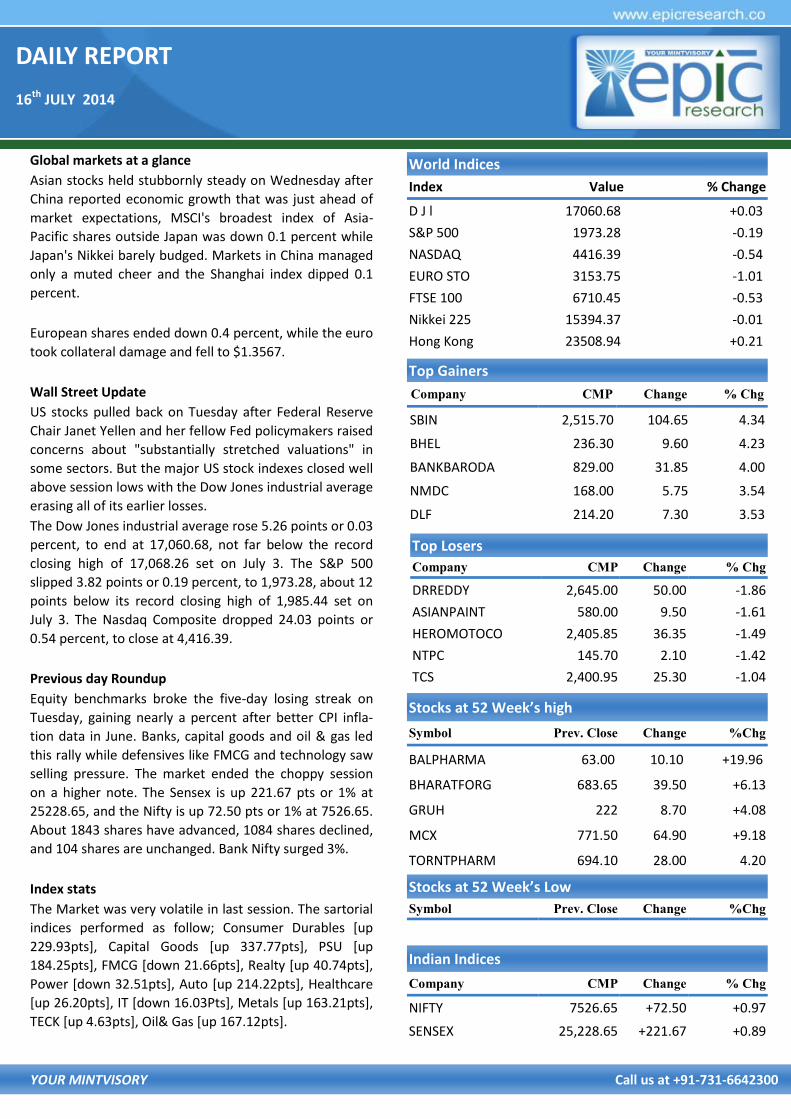

DAILY REPORT 16 th JULY 2014 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance Asian stocks held stubbornly steady on Wednesday after China reported economic growth that was just ahead of market expectations, MSCI's broadest index of Asia- Pacific shares outside Japan was down 0.1 percent while Japan's Nikkei barely budged. Markets in China managed only a muted cheer and the Shanghai index dipped 0.1 percent. European shares ended down 0.4 percent, while the euro took collateral damage and fell to $1.3567. Wall Street Update US stocks pulled back on Tuesday after Federal Reserve Chair Janet Yellen and her fellow Fed policymakers raised concerns about "substantially stretched valuations" in some sectors. But the major US stock indexes closed well above session lows with the Dow Jones industrial average erasing all of its earlier losses. The Dow Jones industrial average rose 5.26 points or 0.03 percent, to end at 17,060.68, not far below the record closing high of 17,068.26 set on July 3. The S&P 500 slipped 3.82 points or 0.19 percent, to 1,973.28, about 12 points below its record closing high of 1,985.44 set on July 3. The Nasdaq Composite dropped 24.03 points or 0.54 percent, to close at 4,416.39. Previous day Roundup Equity benchmarks broke the five-day losing streak on Tuesday, gaining nearly a percent after better CPI infla- tion data in June. Banks, capital goods and oil & gas led this rally while defensives like FMCG and technology saw selling pressure. The market ended the choppy session on a higher note. The Sensex is up 221.67 pts or 1% at 25228.65, and the Nifty is up 72.50 pts or 1% at 7526.65. About 1843 shares have advanced, 1084 shares declined, and 104 shares are unchanged. Bank Nifty surged 3%. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 229.93pts], Capital Goods [up 337.77pts], PSU [up 184.25pts], FMCG [down 21.66pts], Realty [up 40.74pts], Power [down 32.51pts], Auto [up 214.22pts], Healthcare [up 26.20pts], IT [down 16.03Pts], Metals [up 163.21pts], TECK [up 4.63pts], Oil& Gas [up 167.12pts]. World Indices Index Value % Change D J l 17060.68 +0.03 S&P 500 1973.28 -0.19 NASDAQ 4416.39 -0.54 EURO STO 3153.75 -1.01 FTSE 100 6710.45 -0.53 Nikkei 225 15394.37 -0.01 Hong Kong 23508.94 +0.21 Top Gainers Company CMP Change % Chg SBIN 2,515.70 104.65 4.34 BHEL 236.30 9.60 4.23 BANKBARODA 829.00 31.85 4.00 NMDC 168.00 5.75 3.54 DLF 214.20 7.30 3.53 Top Losers Company CMP Change % Chg DRREDDY 2,645.00 50.00 -1.86 ASIANPAINT 580.00 9.50 -1.61 HEROMOTOCO 2,405.85 36.35 -1.49 NTPC 145.70 2.10 -1.42 TCS 2,400.95 25.30 -1.04 Stocks at 52 Week’s high Symbol Prev. Close Change %Chg BALPHARMA 63.00 10.10 +19.96 BHARATFORG 683.65 39.50 +6.13 GRUH 222 8.70 +4.08 MCX 771.50 64.90 +9.18 TORNTPHARM 694.10 28.00 4.20 Indian Indices Company CMP Change % Chg NIFTY 7526.65 +72.50 +0.97 SENSEX 25,228.65 +221.67 +0.89 Stocks at 52 Week’s Low Symbol Prev. Close Change %Chg

-

Upload

epic-research-private-limited -

Category

Economy & Finance

-

view

133 -

download

2

description

Epic Research is a leading financial advisory firm, we are well known stock advisory, commodity advisory, equity advisory, share advisory, forex advisory, MCX advisory, NCDEX advisory firm in india. Call- 07316642300

Transcript of Stock market special report by epic research 16th july 2014

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

Asian stocks held stubbornly steady on Wednesday after

China reported economic growth that was just ahead of

market expectations, MSCI's broadest index of Asia-

Pacific shares outside Japan was down 0.1 percent while

Japan's Nikkei barely budged. Markets in China managed

only a muted cheer and the Shanghai index dipped 0.1

percent.

European shares ended down 0.4 percent, while the euro

took collateral damage and fell to $1.3567.

Wall Street Update

US stocks pulled back on Tuesday after Federal Reserve

Chair Janet Yellen and her fellow Fed policymakers raised

concerns about "substantially stretched valuations" in

some sectors. But the major US stock indexes closed well

above session lows with the Dow Jones industrial average

erasing all of its earlier losses.

The Dow Jones industrial average rose 5.26 points or 0.03

percent, to end at 17,060.68, not far below the record

closing high of 17,068.26 set on July 3. The S&P 500

slipped 3.82 points or 0.19 percent, to 1,973.28, about 12

points below its record closing high of 1,985.44 set on

July 3. The Nasdaq Composite dropped 24.03 points or

0.54 percent, to close at 4,416.39.

Previous day Roundup

Equity benchmarks broke the five-day losing streak on

Tuesday, gaining nearly a percent after better CPI infla-

tion data in June. Banks, capital goods and oil & gas led

this rally while defensives like FMCG and technology saw

selling pressure. The market ended the choppy session

on a higher note. The Sensex is up 221.67 pts or 1% at

25228.65, and the Nifty is up 72.50 pts or 1% at 7526.65.

About 1843 shares have advanced, 1084 shares declined,

and 104 shares are unchanged. Bank Nifty surged 3%.

Index stats

The Market was very volatile in last session. The sartorial

indices performed as follow; Consumer Durables [up

229.93pts], Capital Goods [up 337.77pts], PSU [up

184.25pts], FMCG [down 21.66pts], Realty [up 40.74pts],

Power [down 32.51pts], Auto [up 214.22pts], Healthcare

[up 26.20pts], IT [down 16.03Pts], Metals [up 163.21pts],

TECK [up 4.63pts], Oil& Gas [up 167.12pts].

World Indices

Index Value % Change

D J l 17060.68 +0.03

S&P 500 1973.28 -0.19

NASDAQ 4416.39 -0.54

EURO STO 3153.75 -1.01

FTSE 100 6710.45 -0.53

Nikkei 225 15394.37 -0.01

Hong Kong 23508.94 +0.21

Top Gainers

Company CMP Change % Chg

SBIN 2,515.70 104.65 4.34

BHEL 236.30 9.60 4.23

BANKBARODA 829.00 31.85 4.00

NMDC 168.00 5.75 3.54

DLF 214.20 7.30 3.53

Top Losers

Company CMP Change % Chg

DRREDDY 2,645.00 50.00 -1.86

ASIANPAINT 580.00 9.50 -1.61

HEROMOTOCO 2,405.85 36.35 -1.49

NTPC 145.70 2.10 -1.42

TCS 2,400.95 25.30 -1.04

Stocks at 52 Week’s high

Symbol Prev. Close Change %Chg

BALPHARMA 63.00 10.10 +19.96

BHARATFORG 683.65 39.50 +6.13

GRUH 222 8.70 +4.08

MCX 771.50 64.90 +9.18

TORNTPHARM 694.10 28.00 4.20

Indian Indices

Company CMP Change % Chg

NIFTY 7526.65 +72.50 +0.97

SENSEX 25,228.65 +221.67 +0.89

Stocks at 52 Week’s Low

Symbol Prev. Close Change %Chg

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATIONS [FUTURE]

1. REKLIANCE INFRA FUTURE

REL INFRA FUTURE is looking strong on charts, long build up

has been seen, we may see more upside, if it sustains above

760 levels. We advise buying around 760-770 levels with

strict stop loss of 745 for the targets of 785 – 800 levels.

2. AUROBINDO PHARMA FUTURE

AUROPHARMA FUTURE looking strong on charts, long build

up has been seen, we may see more upside, if it sustains

above 720 levels. We advise buying around 715-720 levels

with strict stop loss of 705 for the targets of 735-750 levels.

EQUITY CASH & FUTURE

STOCK RECOMMENDATION [CASH]

1. DISHMAN PHARMA

DISHMAN PHARMA rising wedge on daily chart. We advise

selling around 130 level with strict stop loss 131.50 for the

targets of 128.50 -127

MACRO NEWS

Interest rate on fixed deposits between 7-179 days has

been reduced to 7 per cent from 7.5 per cent by SBI and

SBI also sold NPA worth Rs 3,590 crore to ARCs last fiscal.

Aditya Birla Group to merge all retail businesses.

Maruti Suzuki India, Muthoot Vehicle and Asset Finance

sign MOU to help customers avail 100 per cent finance.

United Spirits to buy JP Impex Incorp's Karnataka-based

assets.

Reserve Bank signals cheaper housing, infra loans

The Indian Govt will decide next month on whether to sell

a 5 pct stake in Oil and Natural Gas Corp. The stake would

be worth around US$3bn, based on the current market

cap and would be a firm statement of the government's

intent to pursue its divestment programme.

RBI said it set a cut-off rate of 8.15% at 3-day term repo

auction. The weighted average rate was at 8.18 pct. In-

dian banks' refinancing with RBI rises to 311.72 bln ru-

pees. Indian banks' cash balances with RBI rises to 3.22

trln rupees.

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts

)

Open

Interest

NIFTY PE 7,500 71 3,59,294 48,67,300

NIFTY PE 7,400 37.9 3,18,851 45,78,100

BANKNIFTY PE 7,300 18 2,54,736 45,29,300

BANKNIFTY PE 14,000 43.5 31,966 3,43,400

SBIN PE 2,400 18 4,008 1,76,875

RELIANCE PE 960 13.1 1,923 3,42,750

MCDOWELL-N PE 2,300 21 1,422 2,13,000

INFY PE 3,200 47.65 1,393 2,57,125

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 7,600 54.35 5,45,471 52,37,500

NIFTY CE 7,500 102.05 3,84,600 34,98,200

NIFTY CE 7,700 25.15 3,76,788 50,11,300

BANKNIFTY CE 15,500 90 46,586 5,56,875

SBIN CE 2,500 72.15 8,251 2,25,375

RELIANCE CE 1,000 13.25 3,578 9,54,000

ICICIBANK CE 1,400 28 2,718 3,83,750

IDFC CE 150 4.55 2,373 31,82,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 37793 1415.59 35999 1348.30 306466 11530.88 67.30

INDEX OPTIONS 322944 12118.10 301690 11309.64 1605859 60382.96 808.46

STOCK FUTURES 74796 2755.63 68122 2443.59 1548910 55078.33 312.04

STOCK OPTIONS 56356 2089.96 56338 2093.05 114731 4218.43 -3.09

TOTAL 1184.69

INDICES R2 R1 PIVOT S1 S2

NIFTY 7,582.65 7,554.65 7,506.90 7,478.90 7,431.15

BANK NIFTY 15,122.13 15,007.02 14,804.43 14,689.32 14,486.73

STOCKS IN NEWS

Results: Kotak Bank, Bajaj Finance, BajajFinserv, Feder-alBank, LakshmiVilasBank, SouthIndianBank, Zee Learn.

DLF on mega fundraising drive; eyes Rs 3000-3500cr.

Govt considers selling 5% stake in ONGC.

Tech Mahindra eyes HP's 60.49% stake in Mphasis.

Alstom, NASL to renovate & modernise NTPC's Odisha plant

SAIL to soon boost coking coal imports by over 60% on expansion

Glenmark gets final nod from USFDA for skin infection cream

NIFTY FUTURE

Nifty Future closed in the green in the last trading ses-sion. We advise buying around 7550 level with strict stop loss of 7500 for the targets of 7600-7650

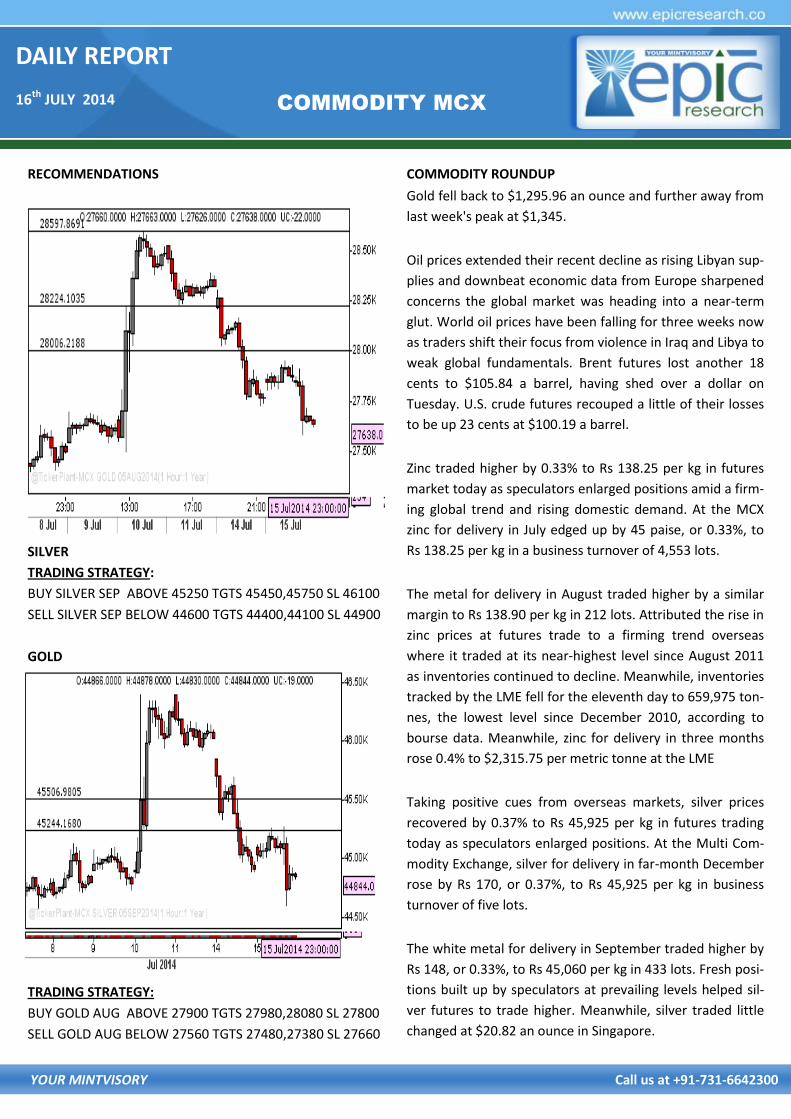

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

COMMODITY MCX

RECOMMENDATIONS

SILVER

TRADING STRATEGY:

BUY SILVER SEP ABOVE 45250 TGTS 45450,45750 SL 46100

SELL SILVER SEP BELOW 44600 TGTS 44400,44100 SL 44900

GOLD

TRADING STRATEGY:

BUY GOLD AUG ABOVE 27900 TGTS 27980,28080 SL 27800

SELL GOLD AUG BELOW 27560 TGTS 27480,27380 SL 27660

COMMODITY ROUNDUP

Gold fell back to $1,295.96 an ounce and further away from

last week's peak at $1,345.

Oil prices extended their recent decline as rising Libyan sup-

plies and downbeat economic data from Europe sharpened

concerns the global market was heading into a near-term

glut. World oil prices have been falling for three weeks now

as traders shift their focus from violence in Iraq and Libya to

weak global fundamentals. Brent futures lost another 18

cents to $105.84 a barrel, having shed over a dollar on

Tuesday. U.S. crude futures recouped a little of their losses

to be up 23 cents at $100.19 a barrel.

Zinc traded higher by 0.33% to Rs 138.25 per kg in futures

market today as speculators enlarged positions amid a firm-

ing global trend and rising domestic demand. At the MCX

zinc for delivery in July edged up by 45 paise, or 0.33%, to

Rs 138.25 per kg in a business turnover of 4,553 lots.

The metal for delivery in August traded higher by a similar

margin to Rs 138.90 per kg in 212 lots. Attributed the rise in

zinc prices at futures trade to a firming trend overseas

where it traded at its near-highest level since August 2011

as inventories continued to decline. Meanwhile, inventories

tracked by the LME fell for the eleventh day to 659,975 ton-

nes, the lowest level since December 2010, according to

bourse data. Meanwhile, zinc for delivery in three months

rose 0.4% to $2,315.75 per metric tonne at the LME

Taking positive cues from overseas markets, silver prices

recovered by 0.37% to Rs 45,925 per kg in futures trading

today as speculators enlarged positions. At the Multi Com-

modity Exchange, silver for delivery in far-month December

rose by Rs 170, or 0.37%, to Rs 45,925 per kg in business

turnover of five lots.

The white metal for delivery in September traded higher by

Rs 148, or 0.33%, to Rs 45,060 per kg in 433 lots. Fresh posi-

tions built up by speculators at prevailing levels helped sil-

ver futures to trade higher. Meanwhile, silver traded little

changed at $20.82 an ounce in Singapore.

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

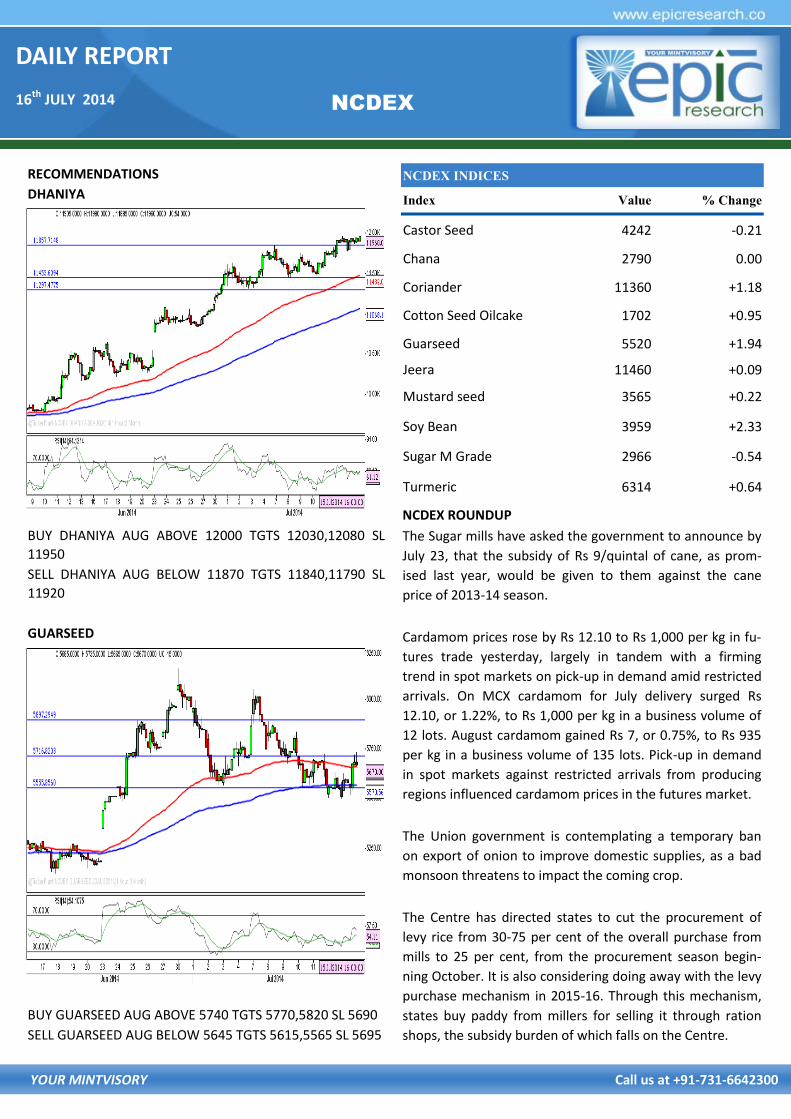

RECOMMENDATIONS

DHANIYA

BUY DHANIYA AUG ABOVE 12000 TGTS 12030,12080 SL

11950

SELL DHANIYA AUG BELOW 11870 TGTS 11840,11790 SL

11920

GUARSEED

BUY GUARSEED AUG ABOVE 5740 TGTS 5770,5820 SL 5690

SELL GUARSEED AUG BELOW 5645 TGTS 5615,5565 SL 5695

NCDEX

NCDEX INDICES

Index Value % Change

Castor Seed 4242 -0.21

Chana 2790 0.00

Coriander 11360 +1.18

Cotton Seed Oilcake 1702 +0.95

Guarseed 5520 +1.94

Jeera 11460 +0.09

Mustard seed 3565 +0.22

Soy Bean 3959 +2.33

Sugar M Grade 2966 -0.54

Turmeric 6314 +0.64

NCDEX ROUNDUP

The Sugar mills have asked the government to announce by

July 23, that the subsidy of Rs 9/quintal of cane, as prom-

ised last year, would be given to them against the cane

price of 2013-14 season.

Cardamom prices rose by Rs 12.10 to Rs 1,000 per kg in fu-

tures trade yesterday, largely in tandem with a firming

trend in spot markets on pick-up in demand amid restricted

arrivals. On MCX cardamom for July delivery surged Rs

12.10, or 1.22%, to Rs 1,000 per kg in a business volume of

12 lots. August cardamom gained Rs 7, or 0.75%, to Rs 935

per kg in a business volume of 135 lots. Pick-up in demand

in spot markets against restricted arrivals from producing

regions influenced cardamom prices in the futures market.

The Union government is contemplating a temporary ban

on export of onion to improve domestic supplies, as a bad

monsoon threatens to impact the coming crop.

The Centre has directed states to cut the procurement of

levy rice from 30-75 per cent of the overall purchase from

mills to 25 per cent, from the procurement season begin-

ning October. It is also considering doing away with the levy

purchase mechanism in 2015-16. Through this mechanism,

states buy paddy from millers for selling it through ration

shops, the subsidy burden of which falls on the Centre.

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

JPY/INR

BUY JPY/INR ABOVE 59.48 TGTS 59.63, 59.78 SL 59.28.

SELL JPY/INR BELOW 59.03 TGTS 58.88, 58.73 SL 59.23.

GBP/INR

BUY GBP/INR ABOVE 103.44 TGTS 103.59, 103.74 SL 103.24.

SELL GBP/INR BELOW 103.01 TGTS 102.86, 102.71 SL 103.21.

CURRENCY ROUNDUP

The rupee rose from a session low of 60.2450 to trade at

60.09/60.10, as gains in shares helped offset dollar demand

from state-run banks. It closed at 60.07/60.08 on Monday.

State-run banks have been mopping up dollars for oil- and

defence-related payments in the recent sessions, aiding the

Some of this demand could be for the government's effort

to pay Iran a part of its oil dues. The Indian rupee fell for a

second session in a row as dollar demand from state-run

banks for oil-and defence-related payments offset a recov-

ery in shares after a five-day losing streak. The partially con-

vertible rupee ended at 60.12/13 per dollar compared with

60.07/08 on Monday.

The single currency Euro took a mauling from the pound,

which jumped when UK inflation surprised with a high read-

ing, stoking speculation for interest rates to rise this year.

The euro sank to a two-year trough at 79.08 pence, while

sterling made a six-year peak on the dollar at $1.7191. The

U.S. currency still managed to gain elsewhere and its index

edged up to a three-week high at 80.416. An early mover in

Asia was the New Zealand dollar, which slid to $0.8714 after

the country reported softer-than-expected inflation.

The dollar clung to modest gains early on Wednesday after

bulls latched onto a comment by the head of the Federal

Reserve that rates could rise sooner if employment contin-

ued to improve, while strong inflation sent sterling to a six-

year high.

Oil prices dropped by as much as $2 on Tuesday, deepening

their biggest slide this year as rising Libyan supplies and

downbeat economic data sharpened concerns the global

market was heading into a near-term glut.

The bond market traded in a narrow range on Tuesday, ab-

sorbing Federal Reserve Chair Janet Yellen's message that

the U.S. economic recovery remains incomplete and early

signs of a pick-up in inflation are not enough to accelerate

anticipated interest rate increases.

CURRENCY

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 60.2195 Yen-100 59.2700

Euro 81.9510 GBP 102.7947

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

15/07/14 MCX GOLD AUG. BUY 27900 27980-28080 27800 NO PROFIT NO

LOSS

15/07/14 MCX GOLD AUG. SELL 27700 27620-27520 27800 BOOKED PROFIT

15/07/14 MCX SILVER SEP. BUY 45250 45450-45750 46100 NO PROFIT NO

LOSS

15/07/14 MCX SILVER SEP. SELL 44850 44650-44350 45150 BOOKED PROFIT

15/07/14 NCDEX GUARSEED AUG. BUY 5580 5610-5660 5530 BOOKED PROFIT

15/07/14 NCDEX GUARSEED AUG. SELL 5500 5470-5420 5550 NOT EXECUTED

15/07/14 NCDEX DHANIYA AUG. BUY 11865 11895-11945 11815 BOOKED FULL

PROFIT

15/07/14 NCDEX DHANIYA AUG. SELL 11780 11750-11700 11830 NOT EXECUTED

15/07/14 USD/INR JULY BUY 60.36 60.51-60.66 60.16 NO PROFIT NO

LOSS

15/07/14 USD/INR JULY SELL 60.06 59.91-59.76 60.26 NOT EXECUTED

15/07/14 EUR/INR JULY SELL 81.91 81.76-81.61 82.11 NO PROFIT NO

LOSS

15/07/14 EUR/INR JULY BUY 82.20 82.35-82.50 82.00 SL TRIGGERED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

15/07/14 NIFTY FUTURE SELL 7440 7390-7340 7510 NOT EXECUTED

15/07/14 ARVIND FUTURE BUY 210-212 215-218 205 BOOKED FULL

PROFIT

15/07/14 ORIENTAL BANK FUTURE BUY 282-285 288-292 279 BOOKED PROFIT

15/07/14 JUST DIAL CASH BUY 1600 1632-1664 1568 SL TRIGGERED

14/07/14 NIFTY FUTURE SELL 7480 7430-7380 7530 CALL OPEN

14/07/14 AXIS BANK FUTURE SELL 1840-1850 1810-1780 1880 SL TRIGGERED

11/07/14 NIFTY FUTURE SELL 7480 7430-7380 7530 CALL OPEN

DAILY REPORT

16th JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere efforts have been made to present the right investment perspective. The

information contained herein is based on analysis and up on sources that we consider reliable.

This material is for personal information and based upon it & takes no responsibility. The information given herein should be treated as only factor, while making invest-ment decision. The report does not provide individually tailor-made investment advice. Epic research recommends that investors independently evaluate particular invest-

ments and strategies, and encourages investors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the

information given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not necessarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without notice. Analyst or any person related to epic research might be

holding positions in the stocks recommended. It is understood that anyone who is browsing through the site has done so at his free will and does not read any views ex-

pressed as a recommendation for which either the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this disclaimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the completeness thereof. We

are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the recommendations above epic research does not purport to be

an invitation or an offer to buy or sell any financial instrument. Our Clients (Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Provided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME (ET) REPORT PERIOD ACTUAL CONSENSUS FORECAST PREVIOUS

MONDAY, JULY 14

NONE SCHEDULED

TUESDAY, JULY 15

8:30 AM RETAIL SALES JUNE 0.6% 0.3%

8:30 AM RETAIL SALES EX-AUTOS JUNE 0.6% 0.1%

8:30 AM IMPORT PRICE INDEX JUNE 0.4% 0.1%

8:30 AM EMPIRE STATE INDEX JULY 17.9 19.3

10 AM JANET YELLEN TESTIMONY

10 AM BUSINESS INVENTORIES MAY 0.6% 0.6%

WEDNESDAY, JULY 16

8:30 AM PRODUCER PRICE INDEX JUNE 0.2% -0.2%

9:15 AM INDUSTRIAL PRODUCTION JUNE 0.2% 0.6%

9:15 AM CAPACITY UTILIZATION JUNE 79.2% 79.1%

10 AM JANET YELLEN TESTIMONY

10 AM HOME BUILDERS' INDEX JULY 50 49

2 PM BEIGE BOOK

THURSDAY, JULY 17

8:30 AM WEEKLY JOBLESS CLAIMS 7-12 N/A 304,000

8:30 AM HOUSING STARTS JUNE 1.00 MLN 1.00 MLN

10 AM PHILLY FED JULY 16.5 17.8

FRIDAY, JULY 18

9:55 AM UMICH CONSUMER SENTIMENT JULY 82.7 82.5

10 AM LEADING INDICATORS JUNE -- 0.5%