Stock Code: BSE NSE Reuters ABRL BO / ABRL NS / … Meet/100303_20131113.pdf · Among the largest...

55

Stock Code: BSE : 500303 NSE : ABIRLANUVO Reuters : ABRL.BO / ABRL.NS / IRYN.LU Bloomberg : ABNL IN / IRIG LX

-

Upload

trannguyet -

Category

Documents

-

view

212 -

download

0

Transcript of Stock Code: BSE NSE Reuters ABRL BO / ABRL NS / … Meet/100303_20131113.pdf · Among the largest...

Stock Code: BSE : 500303 NSE : ABIRLANUVO Reuters : ABRL.BO / ABRL.NS / IRYN.LU Bloomberg : ABNL IN / IRIG LX

2

Aditya Birla Nuvo – A Snapshot 3 – 15

Our businesses :

Financial Services 17

Fashion & Lifestyle 27

Telecom 33

IT-ITeS 36

Manufacturing 38

Annexure 43 – 55

Contents

3

Part of the Aditya Birla Group

The Aditya Birla Group is in league of fortune 500

A USD 42 billion Corporation by revenue size and USD 29 billion Group by Market Cap

Operating in 36 countries in 6 continents with over 50% of revenue flowing from overseas operations

Among the largest and the most reputed business houses in India

Flagship listed companies: Aditya Birla Nuvo (Conglomerate), Grasim & Ultratech (VSF & Cement), Hindalco

- Incl. Novelis (Aluminium & Copper), Idea Cellular (Telecom)

Ranked 4th in global top companies for leaders & 1st in Asia Pacific (Source: Aon Hewitt, Fortune Magazine & RBL -2011)

Anchored by over 136,000 employees belonging to 42 nationalities

Trusted by ~ 1.5 million shareholders and over 125 million customers

In India

Leadership Aluminium, Cement, Carbon Black, VSF, VFY,

Position Branded Apparels, Copper, Chlor-alkali,

Insulators (in terms of production / sales)

Top 3 Telecom (in terms of wireless revenue market share)

Top 5 Life Insurance (in terms of new business premium)

Asset Management (in terms of average AUM)

Global positioning

Aluminium World’s largest aluminium rolling unit

VSF World’s largest manufacturer

Carbon Black World’s largest in terms of capacity

Cement Among top 10 manufacturers in the world

Our Values – Integrity, Commitment, Passion, Seamlessness, Speed

4

Aditya Birla Nuvo : Vision & Mission

Kumar Mangalam Birla

Chairman

Vision

“To be a premium conglomerate building leadership in businesses

and creating value for all the stakeholders”

Mission

• Investing in the promising sectors

• Building leadership in businesses

• A platform to drive synergy of resources

• Delivering best value to all the stakeholders

• To be a responsible corporate citizen

5

Savings led Consumption ledInfrastructure &

Agriculture ledOutsourcing led

Growth Drivers

High rate of savings Rising income levelsHigh rate of

capital formationRising outsourcing trend

Lower penetration of

financial servicesA large young population

Steady economic

reform regime

Highly skilled

human capital

Growing awareness

for financial planningBurgeoning middle class

Investor friendly policies

Increasing FII & FDI flowLow cost destination

Key sectors to

benefitFinancial Services

Telecom, Fashion &

Lifestyle, Textiles,

Automobiles,

Power, Roads,

AgricultureIT-ITeS

ABNL : Well positioned to tap growth opportunities

Aditya Birla Nuvo :

A large eco-system

1995 2013

Revenue 0.2 4.75

Businesses 5

De-risking through portfolio of 15

businesses representing varied sectors

of Indian Economy

Brands ~ 6 ~30

Customers < 1 million Touching lives of 125 million Indians

Employees ~ 13,500Anchored by strong management teams

& about 69,000 employees

6Invested ~ USD 1.5 billion over these years to support growth

Transformation from a Manufacturing Company ..

2000: Foray in Fashion & Lifestyle biz. through acquisition of international brands

2006 : Became largest shareholder in Idea

2005 : Merger of Agri and other Financial Services in ABNL

2001 : Foray in Life Insurance business through JV with Sun Life Canada

2013 : Acquisition of Pantaloons

Divestment of Carbon Black business

7

… to a USD 4.75 billion conglomerate

Manufacturing

Rayon*

Agri*

IT-ITeS^

(99.85%)

Fashion &

Lifestyle

Financial

ServicesTelecom $ #

(25.25%)

Asset Management^

(51%) @

Life Insurance^

(74%) @

Private Equity^

Broking (75%)^

Wealth management^

General Insurance Advisory (50.01%)^

Insulators*

Represent Joint VenturesRepresent Subsidiaries @ JV with Sun Life Financial, CanadaRepresent Divisions # Listed, Aditya Birla Group holds 45.85%* ^ $

Leadership position in India

Leader Top 3 Top 5

Pantaloons^(67.95%)

Madura*

Textiles *

Note : Percentage figures indicated above represent ABNL’s shareholding in its subsidiaries /JV’s

NBFC^

8

Sector Market Position Brand

Financial Services Among top 5 fund managers (excl. LIC)

Fashion & Lifestyle

Largest premium branded apparel player

Largest linen manufacturer

TelecomAmong top 3 cellular operators by revenue

market share

Agri Business

Rayon

Insulators

2nd best energy efficient urea plant

2nd largest manufacturer of VFY

Largest insulators manufacturer

IT-ITeSRanks among top 10 Indian BPO companies by

revenue size

Leadership position across businesses in India

9

Strongly placed in its businesses

Size : Large sizeable player across the businesses

Competitive edge : Well positioned vis-à-vis competition

Operating Performance : Marching on profitable growth

Future Prospects : Capturing opportunities across the businesses to achieve next level of growth

Financial position : Strong standalone balance sheet supporting growth

Return on investment : Earning strong return on investments in most of the businesses

10

Financial snapshot : Consolidated

Earnings growing at robust CAGR

All the businesses are contributing to the

profitable growth

With Idea and Birla Sun Life insurance declaring

dividend, ABNL has started generating return on

its long term investments

Net Profit (` Cr.)

151

(436)

155

822 890

1,059

FY08 FY09 FY10 FY11 FY12 FY13

Revenue (` Cr.)

11,375 14,331 15,523

18,188

21,840

25,490

FY08 FY09 FY10 FY11 FY12 FY13

1,153 867

1,686

2,685

3,259

4,142

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA (` Cr.)

11

Consolidated Mix – FY13

Financial Services

27%

Telecom24%

Fashion & Lifestyle

21%

IT-ITeS10%

Manufacturing 18%

Financial Services

32%

Telecom29%

Fashion & Lifestyle

14%

IT-ITeS8%

Manufacturing 17%

Revenue1EBIT1

Note 1 : Revenue and EBIT Mix is without Carbon Black business. Having received shareholders’ approval, ABNL has accounted for slump sale of the Carbon Black business w.e.f. 1st Apr’13

12

Achieved revenue growth across the businesses

Note 1 : Including full figures of Asset Management business. As per AS27, Asset Management business has been proportionately consolidated @ 50% in ABNL’s financials, being a 50:50 Joint Venture till 9th Oct’12.

Thereafter it is consolidated as subsidiary since ABFS holds 51% w.e.f. 10th Oct’12.

Note 2 : Full financial numbers of Idea Cellular. Being a JV, Idea Cellular has been consolidated at 31.78% from 10th March 2007 upto 12th August 2008, at 27.02% upto 1st March 2010 and

at ~ 25.3% thereafter as per AS 27.

Note 3 : Represents Branded apparels & Accessories (Madura & Pantaloons) and Textiles. In FY13, nine months financials for Pantaloons are included pursuant to its acquisition w.e.f. appointed date 1st July 2012

Note 4 : Represents Agri, Rayon and Insulators. Having received shareholders’ approval, ABNL has accounted for slump sale of the Carbon Black business w.e.f. 1st Apr’13

Revenue

3500

4778

58716313 6550 6390

FY08 FY09 FY10 FY11 FY12 FY13

Financial Services1

1622 1688 18262576

3281

4930

FY08 FY09 FY10 FY11 FY12 FY13

Fashion & Lifestyle3

1677 17771530

1692

2082

2466

FY08 FY09 FY10 FY11 FY12 FY13

IT-ITeS

1662

22121988

2327

3255

4155

FY08 FY09 FY10 FY11 FY12 FY13

Manufacturing4

( ` Crore)

6720

1013112398

15438

1948922407

FY08 FY09 FY10 FY11 FY12 FY13

Telecom2

13

Augmented profitability across the businesses

-351-586

-231

544661

819

FY08 FY09 FY10 FY11 FY12 FY13

Financial Services 1

107

-10466

235339

466

FY08 FY09 FY10 FY11 FY12 FY13

Fashion & Lifestyle3

454

105

193 189

251

FY08 FY09 FY10 FY11 FY12 FY13

IT-ITeS

363

474426 420 406

446

FY08 FY09 FY10 FY11 FY12 FY13

Manufacturing4

EBITDA ( ` Crore)

23763051

3621 3903

5135

6091

FY08 FY09 FY10 FY11 FY12 FY13

Telecom 2

Note 1 : Including full figures of Asset Management business. As per AS27, Asset Management business has been proportionately consolidated @ 50% in ABNL’s financials, being a 50:50 Joint Venture till 9th Oct’12.

Thereafter it is consolidated as subsidiary since ABFS holds 51% w.e.f. 10th Oct’12. Interest cost of NBFC biz., being operating expense as per AS17, is deducted from segmental EBITDA.

Note 2 : Full financial numbers of Idea Cellular. Being a JV, Idea Cellular has been consolidated at 31.78% from 10th March 2007 upto 12th August 2008, at 27.02% upto 1st March 2010 and

at ~ 25.3% thereafter as per AS 27.

Note 3 : Represents Branded apparels & Accessories (Madura & Pantaloons) and Textiles. . In FY13, nine months financials for Pantaloons are included pursuant to its acquisition w.e.f. appointed date 1st July 2012

Note 4 : Represents Agri, Rayon and Insulators. Having received shareholders’ approval, ABNL has accounted for slump sale of the Carbon Black business w.e.f. 1st Apr’13

14

Growth supported by strong Standalone Balance Sheet

Standalone Capital Employed

(` Cr.)

Strong balance sheet : Net Debt to EBITDA @ 2.1x and Net Debt to Equity @ 0.41x as on 30th Sep‟13

Despite more than 70% of standalone capital employed being deployed in long term investments

Led by reduction in debt on account of slump sale of Carbon Black business w.e.f. 1st Apr’13

Dividend / buyback proceeds of ` 294 Cr. from BSLI & realisation of subsidy in Agri business also contributed

Strengthening of the balance sheet will support ABNL‟s investment and capex plans

Equity infusion of ` 671 Cr. by promoters in Nov’13 on conversion of remaining 9.82 million warrants

Investment plan includes funding growth capital requirement of NBFC business

4,982 5,4365,424

5,598 5,857

7,616

3,7673,044

3,4374,696

5,157 2,915

Mar'09 Mar'10 Mar'11 Mar'12 Mar'13 Sep'13

Long Term

Investments

Fixed Assets &

Working Capital

5.8

4.1

3.3 3.6 3.3

2.1

0.87

0.74

0.580.66

0.53

0.41

Mar'09 Mar'10 Mar'11 Mar'12 Mar'13 Sep'13

Net Debt / EBITDA Net Debt / Equity

Standalone Ratios

15

Anchored by a strong Management Team

Business Head/Director Business

Dr. Rakesh Jain Sector Head - Agri,

Insulators, Chemicals

IT-ITeS

Mr. Ajay Srinivasan Financial Services

Mr. Pranab Barua Fashion & Lifestyle

(Madura & Pantaloons)

Mr. Thomas Varghese Textiles

Mr. Lalit Naik VFY , Chemicals, Agri,

Insulators

Mr. Himanshu Kapania Telecom

Whole Time Director & Chief Financial Officer

Mr. Sushil Agarwal

Board of Directors

The Company has a balanced Board, comprising of 3

Executive, 3 Non-Executive and 6 Independent

Directors.

• Each business is run as an independent SBU under the

leadership of a business head

• Chief Financial Officer heads the finance function which

is the life blood for a business

• Business heads and the Chief Financial Officer have

wide-ranging experience in the areas of business

development, strategy formulation, restructuring,

acquisitions, technology management etc.

• Some of the senior management team members, prior

to joining Aditya Birla Group, have also played key roles

in the globally renowned organisations viz., GE,

Prudential Corporation Asia, Hindustan Unilever, Reckitt

Benckiser etc.

• Independent directors have rich experience in their

respective fields and incl. ex-secretary to the President

of India and former top executives from the esteemed

organisations viz., Exim Bank, LIC, IDBI, UTI etc.

16

17

Aditya Birla Financial Services

18

Ranks among top 5 fund managers in India (excl. LIC)

Funds under management @ ~USD 20 billion

Revenue of ~USD 1.2 billion

Anchored by ~14,750 employees & trusted by ~5 mn customers

Nation wide presence through ~1,550 branches / touch points and

~160,000 agents / channel partners

Strong growth in profitability

Generated return on average capital employed of 31% in FY13

Aditya Birla Financial Services (ABFS)

Note 1 : Includes AUM of Life Insurance, Private Equity and quarterly AAUM of Asset Management business

Note 2 : Including full figures of Asset Management business. As per AS27, Asset Management business has been proportionately consolidated @ 50% in ABNL’s financials, being a 50:50 Joint Venture till 9th

Oct’12. Thereafter it is consolidated as subsidiary since ABFS holds 51% w.e.f. 10th Oct’12. Interest cost of NBFC biz., being operating expense as per AS17, is deducted from segmental EBITDA.

-351-586

-231

544661

819

FY08 FY09 FY10 FY11 FY12 FY13

2EBITDA

3500

4778

58716313 6550 6390

FY08 FY09 FY10 FY11 FY12 FY13

2Revenue

5144557825

8347288309 88393

107560

Mar'08 Mar'09 Mar'10 Mar'11 Mar'12 Mar'13

1Funds under Management

19

Aditya Birla Financial Services (ABFS)

Gained market share across the businesses

Strong growth in lending book and assets under management

Business Parameter FY12 FY13

Life Insurance Private sector’s new business premium 7.8% 8.0%

Asset Management Domestic avg. AUM 9.2% 9.4%

Non-life Insurance Advisory Non-life industry premium ~0.5% ~0.9%

Broking Retail cash equity broking 1.16% 1.50%

Business Parameter FY12 FY13

Life Insurance AUM (Y-o-Y growth%) 21,110 22,929 (+9%)

NBFC Book Size (Y-o-Y growth%) 3,425 8,000 (+135%)

Asset Management Avg. AUM - Q4 (Y-o-Y growth%) 66,082 83,451 (+26%)

Wealth Management Avg. assets under advisory 14,000 16,500 (+18%)

Non-life Insurance Advisory Premium placed (Y-o-Y growth%) 304 634 (+108%)

(` Crore) (` Crore / y-o-y growth)

20

Sound fund performance in Asset Management

and Life Insurance businesses

Capital Infusion to support growth in NBFC

Lending book grew from ` 900 Cr. in Mar’10 to

reach ` 8,300 Cr. in Sep’13

A sum of ` 875 Cr. was invested during this period

years to support growth

Returning surplus funds to the shareholders by

Birla Sun Life Insurance (BSLI)

Birla Sun Life Insurance turned profitable in FY11

Distributed interim dividend of ` 98 Cr. in FY12

and ` 197 Cr. in FY13

Distributed final dividend of ` 118 Cr. in Jul’13 and

` 280 Cr. through buyback of shares in Q1FY14

This will support ABNL’s capital commitments

towards the Financial Services business

Aditya Birla Financial Services (ABFS)

2012-13 2011-12

Revenue

Birla Sun Life Insurance 5,037 5,691

Birla Sun Life Asset Management 405 315

Aditya Birla Finance 713 348

Aditya Birla Money 84 88

Aditya Birla Money Mart 76 60

Aditya Birla Insurance Brokers 57 32

Aditya Birla Capital Advisors (PE) 24 21

Elimination (6) (5)

Revenue 6,390 6,550

Earnings before tax 761 600

Net Profit 672 539

` Crore Full Year

Note : Including full figures of Asset Management business. As per AS27, Asset

Management business has been proportionately consolidated @ 50% in ABNL’s

financials, being a 50:50 Joint Venture till 9th Oct’12. Thereafter, it is consolidated as

subsidiary since ABFS holds 51% w.e.f. 10th Oct’12.

21

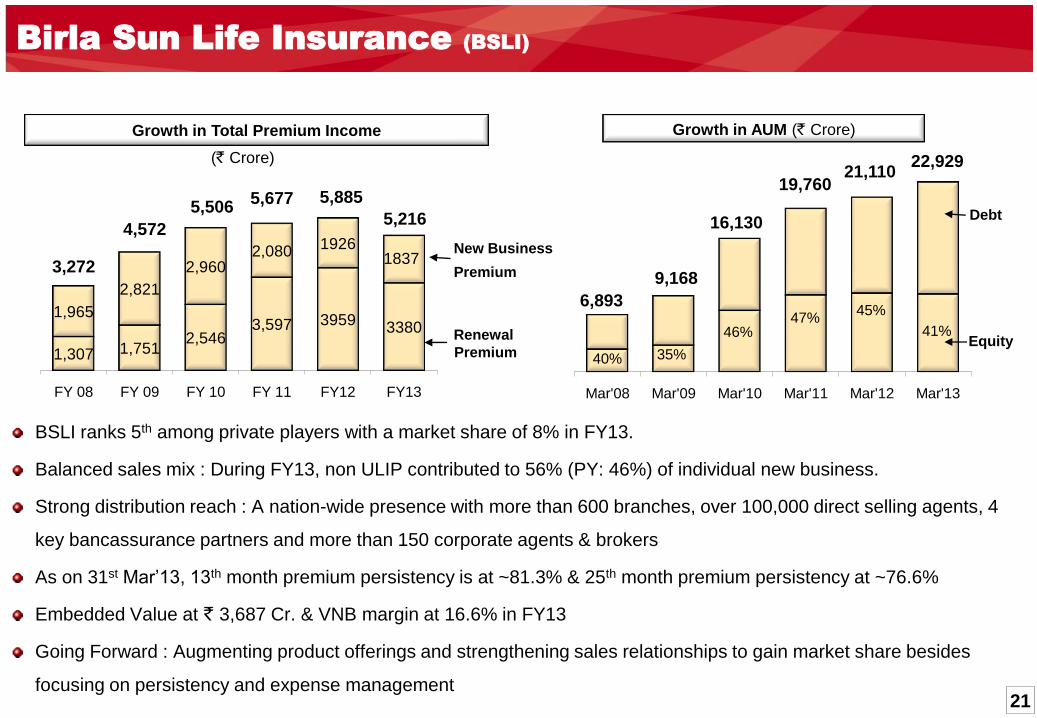

Birla Sun Life Insurance (BSLI)

Growth in Total Premium Income Growth in AUM (` Crore)

BSLI ranks 5th among private players with a market share of 8% in FY13.

Balanced sales mix : During FY13, non ULIP contributed to 56% (PY: 46%) of individual new business.

Strong distribution reach : A nation-wide presence with more than 600 branches, over 100,000 direct selling agents, 4

key bancassurance partners and more than 150 corporate agents & brokers

As on 31st Mar’13, 13th month premium persistency is at ~81.3% & 25th month premium persistency at ~76.6%

Embedded Value at ` 3,687 Cr. & VNB margin at 16.6% in FY13

Going Forward : Augmenting product offerings and strengthening sales relationships to gain market share besides

focusing on persistency and expense management

(` Crore)

1,307 1,7512,546

3,597 39593380

1,965

2,821

2,9602,080 1926

1837

FY 08 FY 09 FY 10 FY 11 FY12 FY13

3,272

4,572

5,506

52%

New Business

Premium

Renewal

Premium

5,677 5,885

5,216

19,760

Mar'08 Mar'09 Mar'10 Mar'11 Mar'12 Mar'13

6,893

9,168

16,130

40% 35%

47%

Debt

Equity46%

21,110

45%

22,929

41%

22

1,6261,037

+447+195

- 401- 139 - 63

-367

1,259

•Movement of Embedded Value – FY2012-13

2012-13

EV

3,687

2,428

Dividend

& DDT

Operating

Variance -

Experience

Operating

Variance -

Assumptions

Expense

OverrunVNB*Economic

Variance incl.

Unwinding

2011-12

EV

4,015

2,978 In-force Business Value

Adjusted Net worth

* Value of New Business margin, as % of Individual APE (Annual Premium Equivalent) is 16.6% for 2012-13

4,054

2012-13

EV (before dividend

distribution)

2,428

23

Birla Sun Life Asset Management (BSAMC)

Growth in AUM (` Crore)

17 years + journey of continued wealth creation

Ranked 4th in India with market share of 9.4% in Q4FY13

Registered 2nd highest y-o-y growth rate among top 5 players

Building alternate assets : Maiden Real Estate Onshore Fund of ` 1,060 Cr.

Expanding International Presence : Set up offices in Dubai & Singapore

Offshore AUM grew to ~USD 900 million

Posted revenue at ` 405 Cr. & Net profit at ` 73 Cr. in FY13

Going forward : Growing profitable assets with a thrust on improving distribution efficiency and fund performance

1Equity AUM (Domestic & Offshore) + PMS + Real Estate Onshore Fund

28,38142,489

52,902 52,383 50,543 66,284 69,336 16,171

6,168

13559 15,285 15,539

17,167 17,512

Mar'08 Mar'09 Q4FY10 Q4FY11 Q4FY12 Q4FY13 Q1FY14

44,552

66,461

48,657

Equity & Alternate Assets1

Debt & Liquid

67,66866,082

83,45186,849

24

Financials

•Birla Sun Life Asset Management

` Crore 2012-13 2011-12

New Business Premium

Individual Business 1,048 1,250

Group Business 788 676

New Business Premium (Gross) 1,837 1,926

Renewal Premium (Gross) 3,380 3,959

Premium Income (Gross) 5,216 5,885

Less : Reinsurance ceded & Service tax (313) (261)

Premium Income (Net) 4,903 5,624

Other Operating Income 134 67

Revenue 5,037 5,691

Earnings before tax 542 461

Net Profit 542 461

Capital 2,450 2,450

Assets under management 22,929 21,110

Q4FY13 Q4FY12

Equity 10,860 10,631

Debt & Liquid 66,284 50,543

Domestic AUM 77,144 61,174

Off shore 4,600 3,368

PMS 643 461

Real Estate Fund 1,063 1,078

Total AUM 83,451 66,082

2012-13 2011-12

Revenue (Fee Income) 405 315

Earnings before tax 107 89

Net Profit 73 59

Average AUM ` Crore

` Crore

Revenues

Birla Sun Life Insurance Birla Sun Life Asset Management

25

Aditya Birla Finance (NBFC)

Closing book as on 30th Sep’13 grew by 61% y-o-y to reach ~ ` 8,300 Cr.

All the segments are contributing to the growth

Net worth as on 30th Sep’13 is ` 1,381 Cr. (Mar’12: ` 628 Cr.)

Share Capital of ` 575 Cr. was infused in past 18 months to

support growth.

The business is growing at a good pace and will require further

capital for future growth

Scaling up the book size while keeping risk under control

Posted revenue at ` 713 Cr. & Net profit at ` 100 Cr. in FY13

Capital Infusion (` Crore)

- - 225 75 350 225

600 9001,850

3,425

8,000 8,300

Mar'09 Mar'10 Mar'11 Mar'12 Mar'13 Sep'13

Growth in Lending book

(` Crore)~

~

~

~~ ~

Key business metrics

H1FY13

(PY)

H1FY14

(CY)

Net Interest Income (incl. fee income) (%) 5.8% 5.1%

Opex to NII Ratio (%) 44% 30%

Return on Avg. Net Worth (p.a.) (%) 12.7% 13.7%

Return on Avg. Assets (p.a.) (%) 2.0% 1.9%

Gross NPA (as % of total loans & advances) 1.6% 1.9%

Net NPA (as % of total loans & advances) 1.3% 1.3%

Revenue (` Crore) 286 550

Net Profit (` Crore) 40 78

Net Worth (` Crore) 769 1,381

Borrowings (` Crore) 4,547 7,068

Leverage (x) 5.92x 5.12x

Capital Market 29%

Infra Financing

27%

Mortgage*23%

Others2%

Corporate Finance

19%

Lending book as on 30th Sep‟13 : Break-up

* LAP / LRD & Construction Finance

26

Other Financial Services

Aditya Birla Private Equity : Of ` 1,179 Cr. corpus, ABPE has deployed / committed ~60% of the deployable surplus

ABPE Fund I (Size : ` 881 Cr.) has invested in Anupam Industries, Bombay Stock Exchange, Credit Analysis &

Research Ltd., GEI Industrial systems, Alphion India Pvt. Ltd., Trimax IT Infrastructure & Services and Ratnakar Bank

Sunrise Fund (Size : ` 299 Cr.) : Investment made in SMS Paryavaran Ltd., Olive Bar and Kitchen Ltd. and Tree

House Education & Accessories Ltd.

Aditya Birla Money : is a retail broking company with nationwide network of more than 900 touch points (including

franchisees) serving over 300,000 customers across more than 150 cities

Aditya Birla Money Mart : A large corporate mutual fund distributor in India having Assets under Advisory of about

` 100 billion (Sep’13) and a nationwide presence with 21 branches and ~16,000 channel partners

Aditya Birla Insurance Brokers : A leading non-life insurance broking company in India. The premium placement

more than doubled year on year to ` 634 Crore in FY13

2012-13 2011-12 2012-13 2011-12 2012-13 2011-12 2012-13 2011-12

Revenue 24 21 84 88 76 60 57 32

Earnings before tax 9 6 (15) (19) (2) (21) 16 9

Net Profit / (Loss) 6 4 (15) (18) (2) (21) 11 6

` Crore

Aditya Birla Capital

Advisors (Private Equity)

Aditya Birla Money Mart

(Wealth Management)

Aditya Birla Insurance

Brokers (General

Insurance Advisory)

Aditya Birla Money

(Broking)

27

Fashion & Lifestyle

28

The largest branded apparel player in India selling one apparel every

second

Largest manufacturer of linen fabric in India

Nationwide reach through a large controlled retail presence of 1,587

stores spanning across 4.1 million sq. ft. as on 30th Sep’13

Besides, reaching customers through more than 4,750 MBOs &

Department Stores.

Combined revenue (annualised)1 of ~USD 1 billion

Generated return on operating capital employed @ 25% in FY13

Fashion & Lifestyle

Business EBOs /

Stores

Retail

Space (million sq. ft.)

Madura 1,405 2.01

Pantaloons (incl.

Factory Outlets)97 1.96

Jayashree Textiles (Linen Club)

85 0.1

1,587 4.1

1FY13 includes nine months financials of Pantaloons Fashion business acquired w.e.f. the appointed date 1st July 2012

Madura51%

Pantaloons26%

Jayashree23%

Revenue mix1 (FY13)

(For 9 months

Jul’12-Mar’13)

1622 1688 18262576

3281

4930

FY08 FY09 FY10 FY11 FY12 FY13

Revenue1

107

-10466

235339

466

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA1

2

2FY13 EBITDA excludes interest income of ` 62 Cr. on current investments to make performance comparable

29

1,026 1,116

1,251

1,811 2,239

2,523

FY08 FY09 FY10 FY11 FY12 FY13

Madura Fashion & Lifestyle

Revenue (` Cr.)

39

(158)

(4)

136

196 245

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA (` Cr.)

Madura Fashion & Lifestyle is the largest branded apparel player in India

Strong Brands : Louis Philippe, Van Heusen, Allen Solly, Peter England,

Collective, Plant Fashion, People

Louis Philippe & Van Heusen are the best selling brands in India

EBITDA margin of brands enhanced to 11.5% in FY13 (PY:10.2%)

Revenue doubled in past 3 years to cross ` 2,500 Cr. mark – growing @

CAGR of 26% while capital employed is managed at similar levels –

leading to ROACE expansion from 11% in FY11 to 29% in FY13

Expanding retail channel to strengthen market leadership

Besides these EBOs, Madura is reaching customers through more than

1,750 MBOs & Department Stores

•Retail Channel

895 1,129

1,272 1,405

Mar'11 Mar'12 Mar'13 Sep'13

1.271.64

1.86 2.01

Retail Space (Million Sq Ft)

No. of EBOs

30

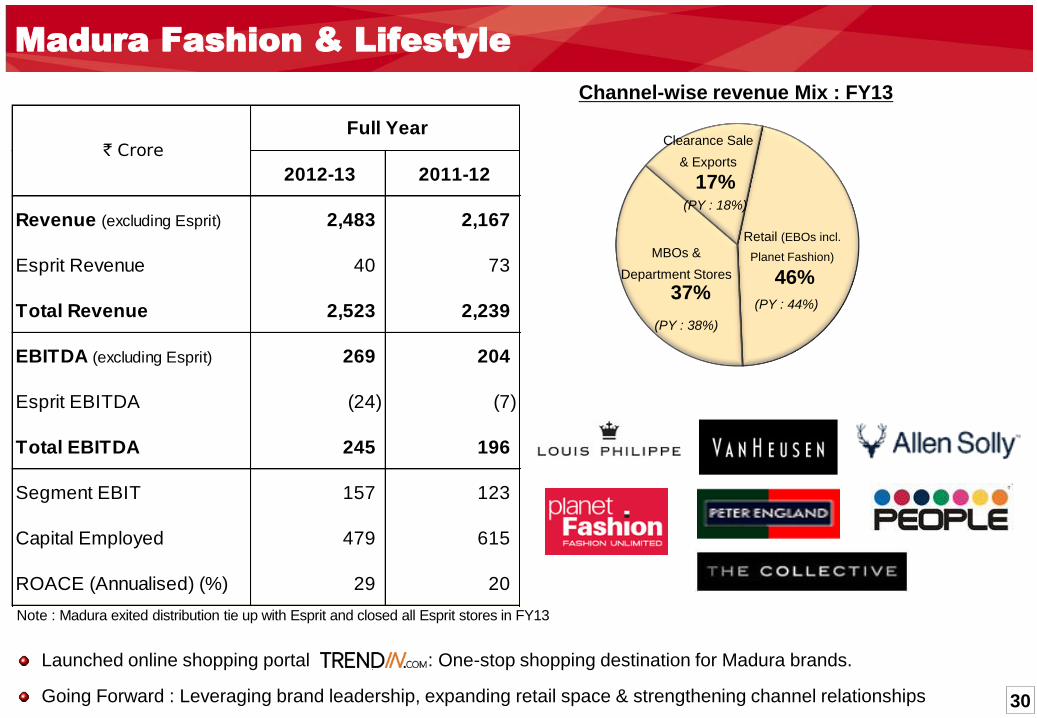

Madura Fashion & Lifestyle

46%37%

17%

Channel-wise revenue Mix : FY13

Clearance Sale

& Exports

Retail (EBOs incl.

Planet Fashion)MBOs &

Department Stores

(PY : 38%)

(PY : 44%)

(PY : 18%)

2012-13 2011-12

Revenue (excluding Esprit) 2,483 2,167

Esprit Revenue 40 73

Total Revenue 2,523 2,239

EBITDA (excluding Esprit) 269 204

Esprit EBITDA (24) (7)

Total EBITDA 245 196

Segment EBIT 157 123

Capital Employed 479 615

ROACE (Annualised) (%) 29 20

` Crore

Full Year

Launched online shopping portal : One-stop shopping destination for Madura brands.

Going Forward : Leveraging brand leadership, expanding retail space & strengthening channel relationships

Note : Madura exited distribution tie up with Esprit and closed all Esprit stores in FY13

31

Pantaloons Fashion & Retail Ltd.

Pantaloons : Posted revenue1 at ` 1,285 Cr. & EBITDA^ at ` 67 Cr. (incl. 9 months financials of the acquired Pantaloons business)

Gross margin was sustained, however, moderated sales growth and higher sellex impacted EBITDA

One time costs on account of change in accounting policy also lowered profitability

Customer reach stands expanded to 72 Pantaloons stores & 25 Factory Outlets across 1.96 million sq. ft.

Added 5 new Pantaloons stores during H1FY14

Refinancing of debt to optimize finance costs : Utilised current investments of ` 800 Cr. in Q1 and raised term loans

of ` 600 Cr. & NCDs of ` 300 Cr. to repay high cost debt

Menswear35%

Womenswear38%

Kidswear9%

Non-apparel18%

Revenue Mix (FY13)

2012-13

(Including nine

months financials

of Pantaloons)

Revenue 1,285

EBITDA^ 67

Finance Cost^ 82

Depreciation 54

Net Profit / (Loss) (69)

Net of interest income of ` 62 Cr. on current investments

` Crore

1

1FY13 includes nine months financials of Pantaloons Fashion business acquired w.e.f. the appointed date 1st July 2012

` Crore As on

31st Mar'13

Net Fixed Assets 488

Goodwill 1,168

Net Working Capital 44

Capital Employed 1,700

Net Worth 770

Net Debt# 931

# Net of current investments of ` 800 Cr.

32

Jaya Shree Textiles (JST) is the domestic market leader in Linen segment

Branding & promoting linen fabric under “Linen Club”

Focus on high margin linen fabric OTC segment

Contributes to 50% of total linen fabric sales

One of the largest player in Wool segment in India

Revenue crossed ` 1,100 Cr. mark

ROACE improved considerably: Earnings doubled in past 3 years while capital employed is managed at a lower level.

To capitalise on buoyant demand in the linen segment, JST has expanded linen yarn capacity from 2,300 TPA to 3,400

TPA in Q2FY14 & targets to expand linen fabric processing capacity from 7.3 million meters to 10.1 million meters by the

end of Q3FY14

Jaya Shree Textiles

600 573 577

774

1,0461,144

FY08 FY09 FY10 FY11 FY12 FY13

Revenue (` Cr.)

6854

69

99141

154

11.3%9.5%

12.0% 12.8%

13.4% 13.5%

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA (` Cr.) OPM(%)

359 345

281

198

88

179

15% 9%15%

32%

82%

97%

FY08 FY09 FY10 FY11 FY12 FY13

Capital Employed (` Cr.) ROACE (%)

33

Telecom

34

Idea Cellular (Telecom)

672010131

1239815438

1948922407

FY08 FY09 FY10 FY11 FY12 FY13

Revenue (` Cr.)

Having a market cap of ~USD 9 billion, Idea is the biggest revenue market share gainer in India since past four years

Ranks 3rd in terms of pan India revenue market share1 at 15.7% up from 15% a year ago.

Contributed to 22% of industry’s incremental mobile revenue1 in FY13

Ranks among top 10 players globally with total Minutes of voice usage of about 1.6 billion per day

Base of 127 mn subscribers provides a platform for upgrading pure voice customers to wireless data services in future

Winner of 3G spectrum in 11 service areas which contribute more than 75% of Idea’s existing 2G revenue

Idea holds 16% stake in the world’s largest Indus Towers

Strong balance sheet & cash profit to support growth :Standalone Net Debt/EBITDA 1.33 & Net Debt/Equity 0.61 (Sep’13)

Generated cash profit of ` 4,697 Cr. in FY13 attaining 30% y-o-y growth

Maiden dividend proposed @ 3% of share capital : Overall payout of ` 116 Cr. (incl. dividend distribution tax)

ROACE (annualised) improved y-o-y from 9% to 13% in H1FY14

11.7%12.6%

13.6%15.0%

15.7%

Q4FY09 Q4FY10 Q4FY11 Q4 FY12 Q4 FY13

Revenue Market Share1

23763051

3621 3903

5135

6091

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA (` Cr.)

1Based on gross revenue for UAS & Mobile licenses only, as released by TRAI

35

Idea Cellular (Telecom)

Currently, 30.9 million subscribers use mobile data services, contributing 7.2% of total service revenue in Q1FY14

As on 30th Apr’13, Idea has around 98.1% of reported subscribers as active subscribers, highest in the industry.

Going forward: Capitalising on brand !DEA, consolidating position in voice market & expanding in evolving wireless

broadband business

10.4 8.8 9.5 9.07.2

10.1

FY08 FY09 FY10 FY11 FY12 FY13

Mar'08 Mar'09 Mar'10 Mar'11 Mar '12 Mar '13

35

133 114

123131 143

65

89

79121

133140

Net Worth

Total Debt

Strong Balance Sheet (Figures in ` billion)

4,76310,114 24,793

49,86066,187 73,668

96,015 107,234

Mar'06 Mar'07 Mar'08 Mar'09 Mar'10 Mar'11 Mar '12 Mar '13

Subscribers (In Million)

Cell Sites: Capacity grew multifold

Robust growth in MOUs (billion minutes)

21 46 86 165 243363 453 532

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

7.4 14.0 24.043.0

63.889.5

112.7 121.6 127.2

Mar'06 Mar'07 Mar'08 Mar'09 Mar'10 Mar'11 Mar '12 Mar '13 Sep'13

Net Profit (` billion)

36

IT-ITeS

37

Aditya Birla Minacs (IT-ITeS)

Ranks among top 10 Indian BPO companies by revenue size (Source: NASSCOM)

A global solution provider serving > 100 clients through 36 centres in US, Canada, Europe, India & Philippines

Employees base of 20,500 (North America : ~8,000, APAC : 12,500) as on 31st Mar’13

Revenue reaches near to ` 2,500 Cr. mark in FY13 and EBITDA margin improved y-o-y from 9.1% to 10.2%

On constant currency2 basis, revenue grew y-o-y by 8% & EBITDA by 13% during FY13

Net profit surged by 80% from ` 70 Cr. to ` 125 Cr. in FY13

Generating steady cash profits to fund its capex and working capital requirements

Net Debt as on 31st Mar’13 at ` 977 Cr. stands reduced y-o-y by ` 129 Cr.

Operating at ROACE of 11.5% in FY13 at capital employed of ` 1,449 Cr. (PY : ` 1,399 Cr.)

Going Forward : Enhancing profitability with focus on operational efficiencies to improve margins.

1677 17771530

1692

2082

2466

FY08 FY09 FY10 FY11 FY12 FY13

Revenue (` Cr.)

454

105

193 189

251

FY08 FY09 FY10 FY11 FY12 FY13

1

EBITDA (` Cr.)

1Received employment incentive arrears of ` 25 Cr. in 2010-11

US77%

Canada14%

Asia Pacific

6%

Europe3%

Revenue Mix by Customer Location

2Normalising for CAD/INR translation impact due to forex movement

38

Manufacturing

39

Manufacturing Businesses

Revenue

FY12 FY13Business

EBITDA

FY12 FY13Remarks on profitability

2,107 2,924 Agri 211 197Lower urea sales volume and higher energy costs due to

planned maintenance shutdown

680 777 Rayon 128 189 Higher VFY & ECU realisation and growth in volumes

468 454 Insulators 67 61 Sales volume & margins were impacted due to cheaper imports

3,255 4,155 Total 406 446 Revenue grew by 28% and EBITDA by 10%

1,943 2,036 Carbon Black2 204 132Constrain on sales volume & margins due to cheaper imports

and lower off-take from tyre manufacturers

5,198 6,191 611 579

Revenue1 grew by 28% to ` 4,155 Cr. in FY13

EBITDA1 is up by 10% to ` 446 Cr.

Operating at an ROACE1 of 15.4%

2Having received shareholders approval, ABNL has accounted for slump sale of the Carbon Black business, w.e.f. 1st April 2013

1Agri, Rayon and Insulators

40

Acute deficit of urea in India – Approx. 25% of the demand is imported

Indo Gulf Fertilisers has 10-20% market share in the target markets

of Uttar Pradesh, Bihar, Jharkhand and West Bengal

Strong brand “ Birla Shaman” is preferred choice of farmers

Also offering value adding variety – Neem coated “Krishi Dev”

A complete agri-solutions provider – Fertilisers, Seeds, Pesticides

Capital employed in FY13 increased primarily due to higher outstanding subsidy owing to slower recovery, rise in natural

gas prices & increase in trading sales of imported P&K fertilisers. Trading in imported P&K fertilisers has been

discontinued in FY14.

Outstanding subsidy and receivables reduced q-o-q from ` 1,632 Cr. in Mar’13 to ` 828 Cr. in Sep’13.

Indo Gulf Fertilisers (Agri-business)

102

228

155176

211 19713%

18%

15% 14%

10%

7%

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA (` Cr.) OPM(%)

531 587

307496

984

1,854

18%

38%31%

39%

26%12%

FY08 FY09 FY10 FY11 FY12 FY13

Capital Employed (` Cr.) ROACE (%)

7871,250

1,0221,244

2,107

2,924

8701073 1106 1099

1152

1091

FY08 FY09 FY10 FY11 FY12 FY13

Revenue (` Cr.) Sales ('000 MT)

41

2nd largest producer of VFY in India with ~39% domestic production share and capacity of 19,800 tons p.a.

Largest Indian VFY exporter for consecutive 8th year

with ~48% share in VFY exports from India in FY13

Integrated facilities : Cost effective 34.5 MW captive power plant

VFY has a niche market globally

Premium is driven by quality and value added yarns

Expanded its presence in fine & superfine VFY segment using Spool Technology from Germany at a capex of ~ ` 270 Cr.

in Mar’13. New VFY plant has been commissioned and is targeting full capacity utilisation by the end of FY14. New

capacity will help in enhancing product quality and range, especially in superfine segment.

Increase in capital employed in FY13 is primarily on account of VFY capacity expansion. ROACE improved to 26%

Indian Rayon (VFY and Chemicals)

454437

430

440515

681

20%20%

28%

17%19%

26%

FY08 FY09 FY10 FY11 FY12 FY13

Capital Employed (` Cr.) ROACE (%)

476537 538 565

680 777

17923 16792 16616 1559216183 16806

FY08 FY09 FY10 FY11 FY12 FY13

Revenue (` Cr.) VFY Sales Volume (MT)

124 123155

110 128

189

26%23%

29%

19%19% 24%

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA (` Cr.) OPM(%)

42

Used in power generation, Transmission & distribution (T&D) and by Original Equipment Manufacturers (OEMs)

Aditya Birla Insulators is largest domestic producer & 4th largest globally with a capacity of 45,260 TPA at two plants

Power Grid corporation of India & State Electricity Boards , ABB, Areva, Siemens etc. are amongst major customers

Insulators industry’s domestic sales volume de-grew y-o-y by 15% during Apr’12-Feb’13 (Source : IEEMA)

Deferment of projects coupled with cheaper imports from China impacted sales and margins across the industry

Liquidity crunch in the power sector is also restricting dispatches

Aditya Birla Insulators contained de-growth in its volumes to 8% during the year

Finance Ministry has imposed safeguard duty of 35% on insulators imports from China from 20th Dec’12 to 19th Dec’13

and then 25% till 31stDec’13. Benefit of imposition of safeguard duty will not accrue immediately due to accelerated

imports of insulators in anticipation of duty.

Aditya Birla Insulators

136 123 116134

67 61

34%29% 27% 26%

14% 13%

FY08 FY09 FY10 FY11 FY12 FY13

EBITDA (` Cr.) OPM(%)

240 264294

362 375 395

58%43% 35% 34% 12% 10%

FY08 FY09 FY10 FY11 FY12 FY13

Capital Employed (` Cr.) ROACE (%)

399 425 428518

468 454

32304 3256137050

44281

39024 35889

FY08 FY09 FY10 FY11 FY12 FY13

Revenue (` Cr.) Sales Volumes (MT)

43

44

Segmental Revenue & EBIT - Consolidated( ` Crore)

Consolidated

2012-13 2011-12 2012-13 2011-12

6,295 6,392 Aditya Birla Financial Services 706 541

5,037 5,691 Life Insurance 542 461

1,258 702 Other Financial Services* 165 80

5,662 4,933 Telecom (Nuvo's share) @ 639 534

4930 3281 Apparels & Textiles 299 242

3,802 2,243 Branded Apparels & Accessories 170 125

1,144 1,046 Textiles 129 117

(16) (8) Inter-segment Elimination - -

2,466 2,082 IT-ITeS 164 111

4155 3255 Manufacturing 369 329

2,924 2,107 Agri-business 177 192

777 680 Rayon 153 92

454 468 Insulators 39 46

2,036 1,943 Carbon Black 93 164

(54) (46) Inter-segment Elimination - -

25,490 21,840 Segmental EBIT 2,270 1,921

Revenue EBIT

* Other Financial Services include Asset Management (proportionately consolidated at 50%, being a 50:50 JV till 9th Oct’12 and thereafter consolidated as subsidiary since ABFS holds

51% w.e.f. 10th Oct’12), NBFC, Private Equity, Broking, Wealth Management & General Insurance Advisory. Interest cost of NBFC business, being an operating expense as per AS

17, is deducted from Segmental EBIT

@ Idea is consolidated at ~25.3%

45

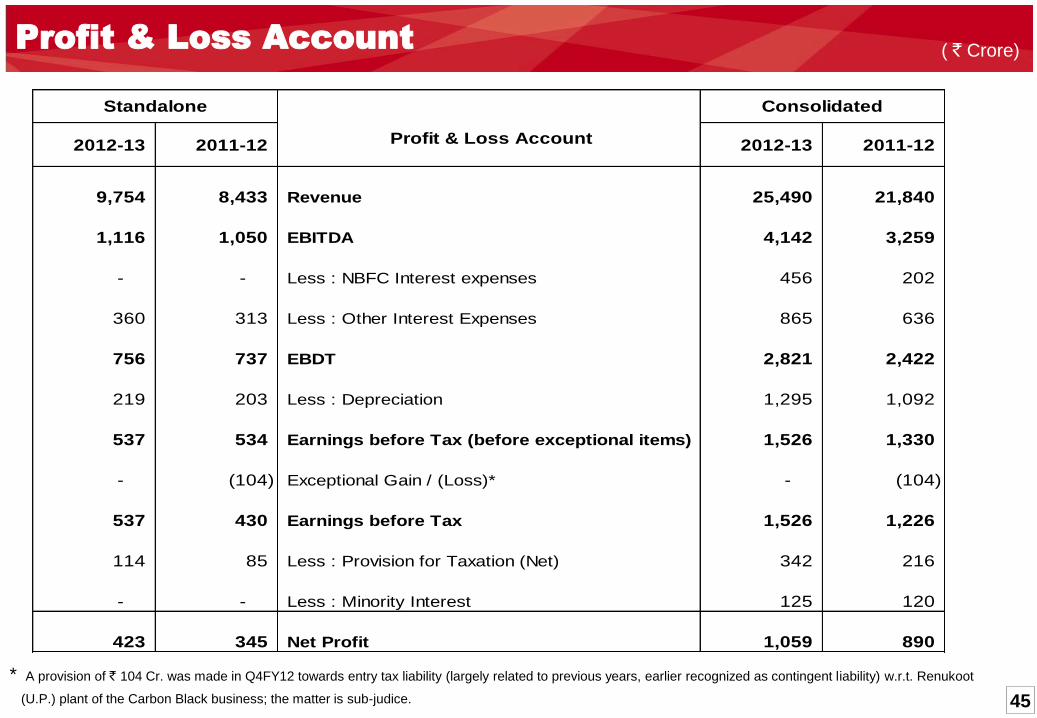

Profit & Loss Account ( ` Crore)

2012-13 2011-12 2012-13 2011-12

9,754 8,433 Revenue 25,490 21,840

1,116 1,050 EBITDA 4,142 3,259

- - Less : NBFC Interest expenses 456 202

360 313 Less : Other Interest Expenses 865 636

756 737 EBDT 2,821 2,422

219 203 Less : Depreciation 1,295 1,092

537 534 Earnings before Tax (before exceptional items) 1,526 1,330

- (104) Exceptional Gain / (Loss)* - (104)

537 430 Earnings before Tax 1,526 1,226

114 85 Less : Provision for Taxation (Net) 342 216

- - Less : Minority Interest 125 120

423 345 Net Profit 1,059 890

Standalone

Profit & Loss Account

Consolidated

* A provision of ` 104 Cr. was made in Q4FY12 towards entry tax liability (largely related to previous years, earlier recognized as contingent liability) w.r.t. Renukoot

(U.P.) plant of the Carbon Black business; the matter is sub-judice.

46

6,854 5,679 Net Worth 9,384 7,517

- - Minority Interest 940 301

4,005 4,457 Debt 11,799 9,224

- - NBFC borrowings 6,903 2,973

155 158 Deferred Tax Liabilities (Net) 428 317

11,014 10,294 Capital Employed 29,455 20,331

- -

Policyholders' funds (Incl. funds

for future appropriation) 21,576 19,964

11,014 10,294 Total Liabilities 51,031 40,295

2,226 1,976 Net Block (Incl. Capital Advances) 10,710 9,385

- - Goodwill 4,793 3,146

- - NBFC Lending 8,000 3,425

2,577 2,012 Net Working Capital 1,837 1,177

5,857 5,598 Long Term Investments 354 319

- - Life Insurance Investments 22,929 21,110

- - Policyholders' Investments 21,559 20,095

- - Shareholders' Investments 1,371 1,015

353 707 Cash Surplus & Current Investments 2,409 1,733

570 500 Book Value (`) 781 662

3.3 3.6 Net Debt / EBITDA (x) 2.3 2.3

0.53 0.66 Net Debt / Equity (x) 1.00 1.00

11,727 10,723 Market Capitalisation - NSE

Mar-13

Consolidated

Mar-12Mar-12 Mar-13

Standalone

Balance Sheet

Balance Sheet ( ` Crore)

Excluding MTM gain of ` 22 Cr. as on 31st Mar’13 and MTM loss of ` 104 Cr. as on 31st Mar’12 w.r.t. fully hedged foreign currency working capital debt

47

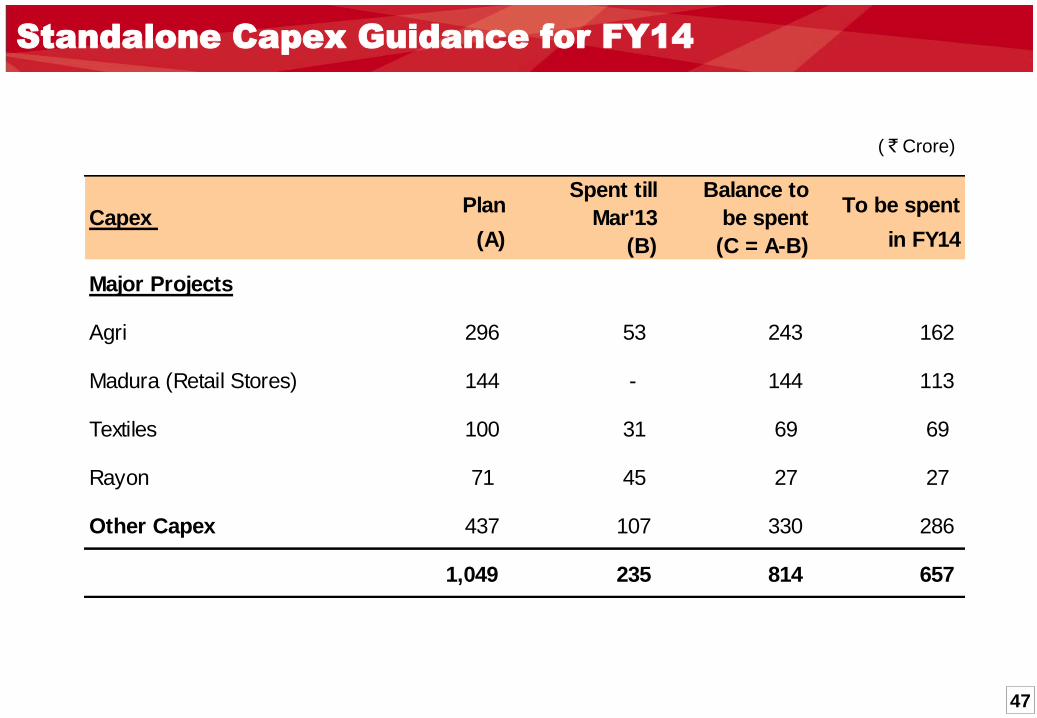

Standalone Capex Guidance for FY14

( ` Crore)

Plan To be spent

(A) in FY14

Major Projects

Agri 296 53 243 162

Madura (Retail Stores) 144 - 144 113

Textiles 100 31 69 69

Rayon 71 45 27 27

Other Capex 437 107 330 286

1,049 235 814 657

Capex

Balance to

be spent

(C = A-B)

Spent till

Mar'13

(B)

48

49

Consolidated Revenue

* Other Financial Services include Asset Management (proportionately consolidated at 50%, being a 50:50 JV till 9th Oct’12 and thereafter consolidated as subsidiary since ABFS holds 51% w.e.f.

10th Oct’12), NBFC, Private Equity, Broking, Wealth Management & General Insurance Advisory.

( ` Crore)

@ Idea is consolidated at ~25.3%

^ Accounted for slump sale of Carbon Black business w.e.f 1st April 2013

Quarter - 1 Revenue

2013-14 2012-13

(PY)

2013-14

(CY)

2012-13

(PY)

2013-14

(CY)

1,366 1,438 1,526 Aditya Birla Financial Services 2,755 2,892

895 1,177 1,083 Life Insurance 2,265 1,979

474 263 446 Other Financial Services* 493 920

(4) (2) (3) Elimination (4) (7)

1,651 1,343 1,596 Telecom (Nuvo's share) @ 2,736 3,247

1,294 1,376 1,613 Fashion & Lifestyle 2,204 2,907

982 1,090 1,303 Branded Apparels & Accessories 1,614 2,285

313 288 311 Textiles 592 624

(1) (1) (1) Elimination (2) (2)

658 628 774 IT-ITeS 1,227 1,431

786 1,165 994 Manufacturing 1,806 1,780

487 864 664 Agri-business 1,209 1,151

204 188 213 Rayon 374 418

95 112 116 Insulators 223 211

- 494 - Carbon Black^ 1,052 -

(11) (10) (10) Inter-segment Elimination (22) (21)

5,744 6,435 6,493 Consolidated Revenue 11,757 12,237

Half YearQuarter 2

50

Consolidated EBIT

* Other Financial Services include Asset Management (proportionately consolidated at 50%, being a 50:50 JV till 9th Oct’12 & thereafter consolidated as subsidiary since ABFS holds 51% w.e.f. 10th Oct’12),

NBFC, Private Equity, Broking, Wealth Management & General Insurance Advisory. Interest cost of NBFC business, being an operating expense as per AS 17, is deducted from Segmental EBIT

( ` Crore)

@ Idea is consolidated at ~25.3%

^ Accounted for slump sale of Carbon Black business w.e.f 1st April 2013

Quarter - 1 EBIT

2013-14 2012-13

(PY)

2013-14

(CY)

2012-13

(PY)

2013-14

(CY)

220 177 156 Aditya Birla Financial Services 359 376

136 145 75 Life Insurance 292 210

84 32 81 Other Financial Services* 67 166

238 144 225 Telecom (Nuvo's share) @ 297 463

25 94 102 Fashion & Lifestyle 137 128

(7) 61 72 Branded Apparels & Accessories 65 65

32 33 30 Textiles 72 63

38 41 44 IT-ITeS 72 82

63 113 96 Manufacturing 186 159

15 61 40 Agri-business 86 55

41 37 43 Rayon 76 84

7 14 13 Insulators 24 21

- 15 - Carbon Black^ 57 -

584 584 624 Segmental EBIT 1,109 1,208

Half YearQuarter 2

51

Consolidated Profit & Loss ( ` Crore)

* Book gain of ` 24 Cr. and a net tax credit of ` 41 Cr. has been recognized in Q1FY14 w.r.t. the slump sale of Carbon Black business

Quarter - 1

2013-14 2012-13

(PY)

2013-14

(CY)

2012-13

(PY)

2013-14

(CY)

5,744 6,435 6,493 Revenue 11,757 12,237

1,174 1,039 1,203 EBITDA 1,955 2,377

166 95 176 Less : NBFC Interest expenses 176 342

211 234 181 Less : Other Interest Expenses 400 392

797 710 847 EBDT 1,379 1,643

388 321 384 Less : Depreciation 616 772

409 389 463 Earnings before Tax (before exceptional items) 763 872

24 - - Exceptional Gain / (Loss)* - 24

433 389 463 Earnings before Tax 763 896

77 73 155 Less : Provision for Taxation (Net)* 139 233

24 33 17 Less : Minority Interest 73 41

331 284 290 Net Profit 551 621

Quarter 2 Half Year Consolidated

Profit & Loss Account

52

7,335 6,854 Net Worth 10,211 9,384

- - Minority Interest 741 940

3,110 4,005 Debt 8,874 11,799

- - NBFC borrowings 7,068 6,903

86 155 Deferred Tax Liabilities (Net) 468 428

10,531 11,014 Capital Employed 27,362 29,455

- -

Policyholders' funds (Incl. funds

for future appropriation) 21,143 21,576

10,531 11,014 Total Liabilities 48,505 51,031

1,756 2,206 Net Block (Incl. Capital Advances) 10,306 10,677

20 20 Goodwill 5,096 4,825

- - NBFC Lending 8,300 8,000

1,000 2,577 Net Working Capital 474 1,837

7,616 5,857 Long Term Investments 365 354

- - Life Insurance Investments 22,381 22,929

- - Policyholders' Investments 21,217 21,559

- - Shareholders' Investments 1,164 1,371

139 353 Cash Surplus & Current Investments 1,584 2,409

610 570 Book Value (`) 849 781

2.1 3.3 Net Debt / EBITDA (x) 1.5 2.3

0.41 0.53 Net Debt / Equity (x) 0.71 1.00

14,939 11,727 Market Capitalisation - NSE

Sep-13

Consolidated

Mar-13Mar-13 Sep-13

Standalone

Balance Sheet

Balance Sheet ( ` Crore)

Excluding MTM gain of ` 22 Cr. as on 31st Mar’13 and MTM loss of ` 28 Cr. as on 30th Sep’13 w.r.t. fully hedged foreign currency working capital debt

Note : Standalone capex of ` 224 Cr. was incurred during H1FY14

53

Standalone Profit & Loss ( ` Crore)

* Book gain of ` 24 Cr. and a net tax credit of ` 41 Cr. has been recognized in Q1FY14 w.r.t. the slump sale of Carbon Black business

Quarter - 1 Standalone

Profit & Loss Account

2013-14 2012-13

(PY)

2013-14

(CY)

2012-13

(PY)

2013-14

(CY)

1,701 2,562 2,132 Revenue 4,599 3,833

315 271 392 EBITDA 485 707

64 96 66 Interest Expenses 182 129

251 175 326 EBDT 303 577

46 52 51 Depreciation 102 97

205 124 275 Earnings before Tax (before exceptional items) 201 480

24 - - Exceptional Gain / (Loss)* - 24

229 124 275 Earnings before Tax 201 504

(24) 28 57 Provision for Taxation (Net)* 47 32

253 96 218 Net Profit 154 472

Half YearQuarter 2

54

2,409

6,246

9,992

13,265

4,227

9,3369,244

10,72311,727

14,939402748

10711396

445906 814 945 976

1242

Mar'05 Mar'06 Mar'07 Mar'08 Mar'09 Mar'10 Mar'11 Mar'12 Mar'13 Sep'13

Market Cap (` Crores) Closing Share price (`)

Shareholding Pattern & Market Cap

Trusted by 140,363 shareholders

Over 97.5% of shares are in dematerialised form

Face value of ` 10 per share

For analysts coverage on ABNL visit :

Market Cap & Share Price

Source : NSE website

Stock Code – BSE : 500303 NSE : ABIRLANUVO Reuters : ABRL.BO / ABRL.NS / IRYN.LU Bloomberg : ABNL IN / IRIG LX

http://www.adityabirlanuvo.com/investors/downloads/third_party_analysts_coverage.aspx

Category

No. of No. of Shares Shareholding

Shareholders held (in million) (%)

Promoter & Promoter Group 21 64.62 53.74%

Foreign Institutional Investors 343 19.32 16.06%

Domestic Institutional Investors 179 16.36 13.60%

Non-Institutional Investors 139,816 16.78 13.95%

GDRs - Public 4 3.18 2.65%

Total 140,363 120.26 100.00%

As on 30th Sep'13

55

Disclaimer

Certain statements made in this presentation may not be based on historical information or facts and may be “forward looking statements” including,

but not limited to, those relating to general business plans & strategy of Aditya Birla Nuvo Limited ("ABNL"), its future outlook & growth prospects,

future developments in its businesses, its competitive & regulatory environment and management's current views & assumptions which may not

remain constant due to risks and uncertainties. Actual results may differ materially from these forward-looking statements due to a number of

factors, including future changes or developments in ABNL's business, its competitive environment, its ability to implement its strategies and

initiatives and respond to technological changes and political, economic, regulatory and social conditions in the countries in which ABNL conducts

business. Important factors that could make a difference to ABNL’s operations include global and Indian demand supply conditions, finished goods

prices, feed stock availability and prices, cyclical demand and pricing in ABNL’s principal markets, changes in Government regulations, tax regimes,

competitors actions, economic developments within India and the countries within which ABNL conducts business and other factors such as

litigation and labour negotiations.

This presentation does not constitute a prospectus, offering circular or offering memorandum or an offer to acquire any shares and should not be

considered as a recommendation that any investor should subscribe for or purchase any of ABNL's shares. Neither this presentation nor any other

documentation or information (or any part thereof) delivered or supplied under or in relation to the shares shall be deemed to constitute an offer of

or an invitation by or on behalf of ABNL.

ABNL, as such, makes no representation or warranty, express or implied, as to, and does not accept any responsibility or liability with respect to,

the fairness, accuracy, completeness or correctness of any information or opinions contained herein. The information contained in this presentation,

unless otherwise specified is only current as of the date of this presentation. ABNL assumes no responsibility to publicly amend, modify or revise

any forward looking statements on the basis of any subsequent developments, information or events or otherwise. Unless otherwise stated in this

document, the information contained herein is based on management information and estimates. The information contained herein is subject to

change without notice and past performance is not indicative of future results. ABNL may alter, modify or otherwise change in any manner the

content of this presentation, without obligation to notify any person of such revision or changes. This presentation may not be copied and

disseminated in any manner.

INFORMATION PRESENTED HERE IS NOT AN OFFER FOR SALE OF ANY EQUITY SHARES OR ANY OTHER SECURITY OF ABNL

This presentation is not for publication or distribution, directly or indirectly, in or into the United States, Canada or Japan. These

materials are not an offer of securities for sale in or into the United States, Canada or Japan.

Aditya Birla Nuvo Limited

Regd. Office: Indian Rayon Compound, Veraval – 362 266 (Gujarat)

Corporate Office: 4th Floor „A‟ Wing, Aditya Birla Center, S.K. Ahire Marg, Worli, Mumbai – 400 030

Website: www.adityabirlanuvo.com or www.adityabirla.com or Email: [email protected]