State!of!Kansas!! eSolutions!Benchmarking!Report!...

81

State of Kansas eSolutions Benchmarking Report 2015 Strategic Networks Group. Inc. 2015 www.sngroup.com Page 1 of 48 State of Kansas eSolutions Benchmarking Report January 2015 Prepared for:

Transcript of State!of!Kansas!! eSolutions!Benchmarking!Report!...

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group. Inc. 2015 www.sngroup.com Page 1 of 48

State of Kansas

eSolutions Benchmarking Report

January 2015

Prepared for:

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group. Inc. 2015 www.sngroup.com Page 2 of 48

Table of Contents

Executive Summary .................................................................................................................. 4

1 Kansas Businesses ............................................................................................................. 8 1.1 Respondent Profile ........................................................................................................... 8 1.2 Business Connectivity Characteristics ............................................................................ 10 1.2.1 Internet Speeds ....................................................................................................... 10 1.2.2 Cost ......................................................................................................................... 14 1.2.3 Satisfaction .............................................................................................................. 14

1.3 Broadband Utilization and Benefits ............................................................................... 15 1.3.1 Utilization Patterns ................................................................................................. 15 1.3.2 Broadband and Deciding Where to Locate ............................................................. 19 1.3.3 Broadband Benefits and Impacts ............................................................................ 19

1.4 Barriers and Adoption Issues .......................................................................................... 20 1.4.1 Barriers to Adoption ................................................................................................ 20 1.4.2 Expertise and Knowledge Issues ............................................................................. 20 1.4.3 Skills Acquisition ...................................................................................................... 21

1.5 Financial and Employment Impacts from Internet Use .................................................. 23

2 Kansas Households ......................................................................................................... 25 2.1 Household Profiles and Connectivity ............................................................................. 25 2.1.1 Respondent Characteristics .................................................................................... 25 2.1.2 Connectivity Characteristics .................................................................................... 26

2.2 Broadband Utilization and Benefits ............................................................................... 29 2.2.1 Broadband Utilization ............................................................................................. 29 2.2.2 Mobile Uses ............................................................................................................ 31 2.2.3 Household Benefits ................................................................................................. 33

2.3 Barriers and Adoption Issues .......................................................................................... 34

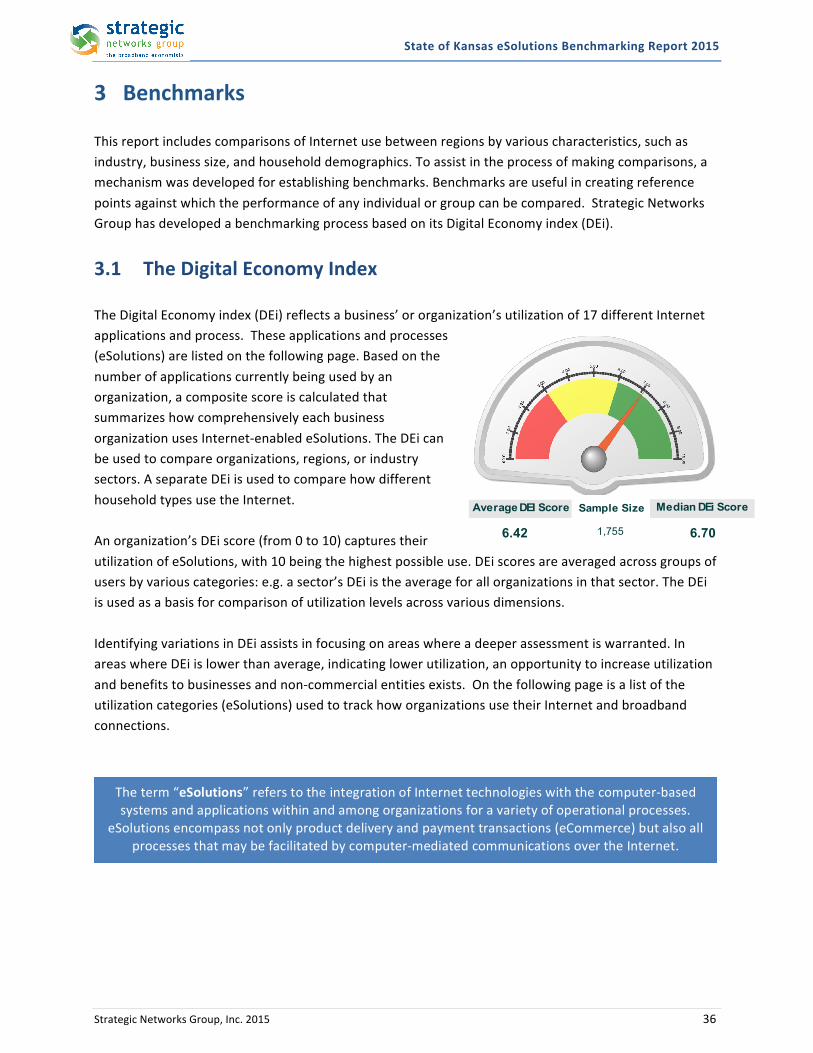

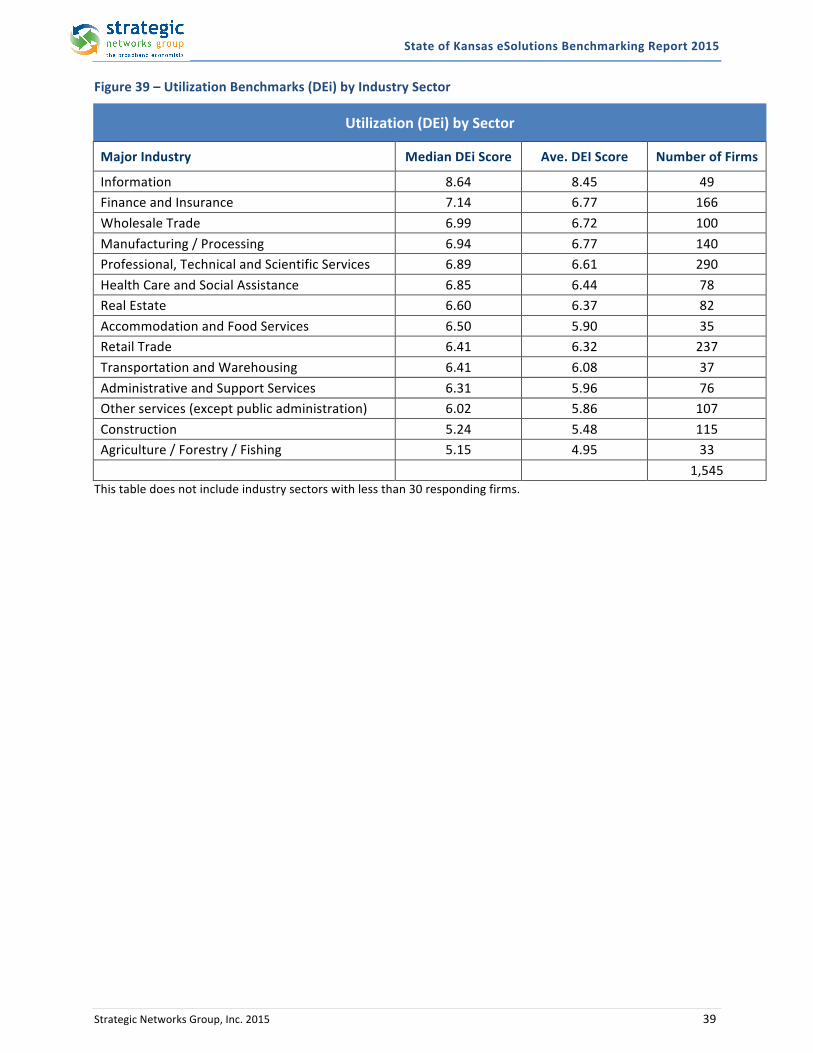

3 Benchmarks .................................................................................................................... 36 3.1 The Digital Economy Index ............................................................................................. 36 3.2 Business Benchmarks ..................................................................................................... 37

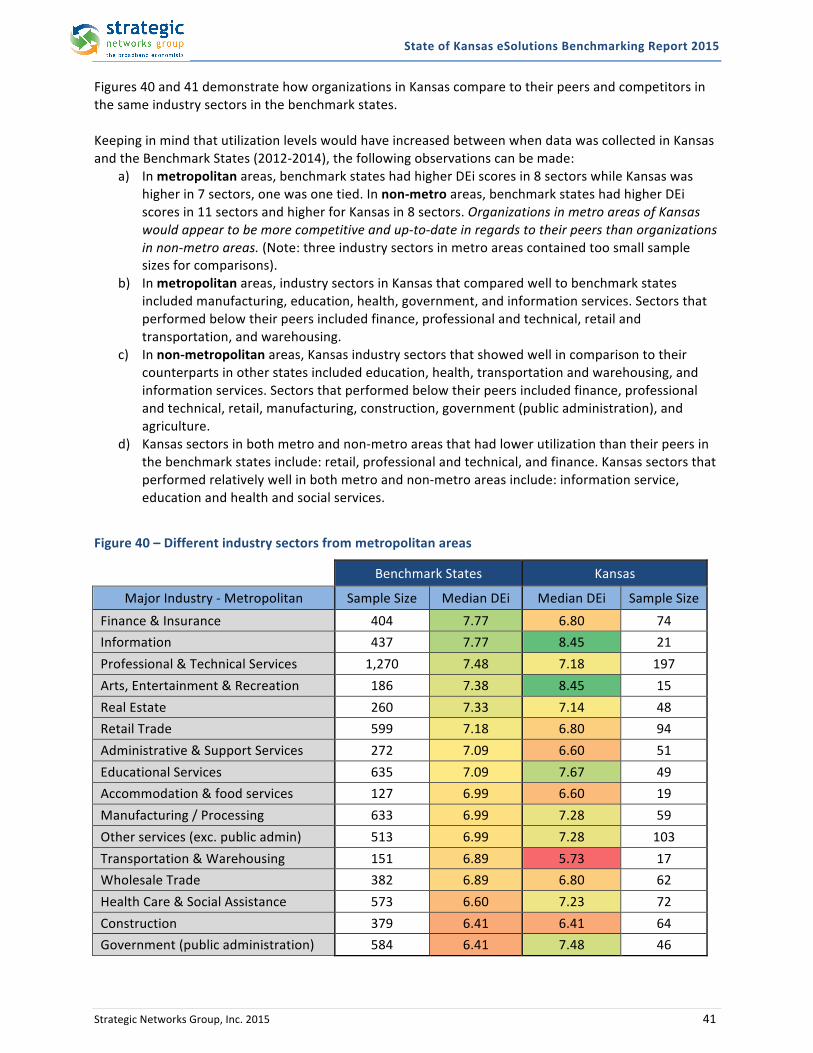

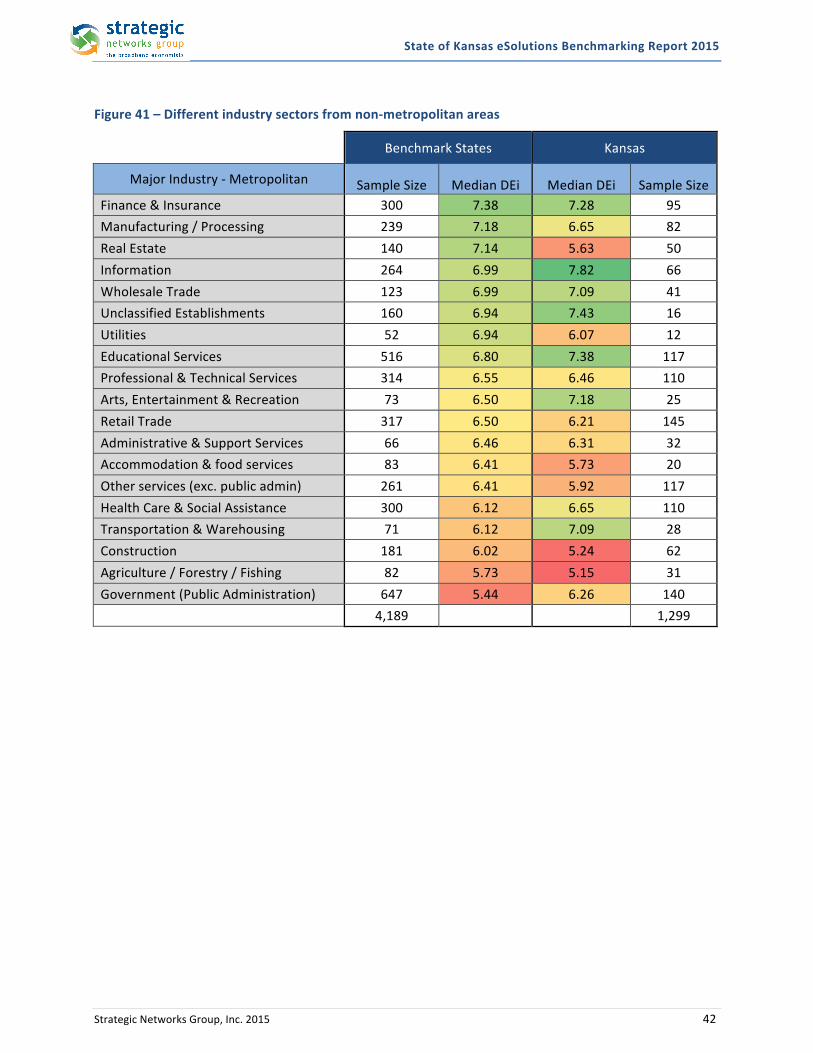

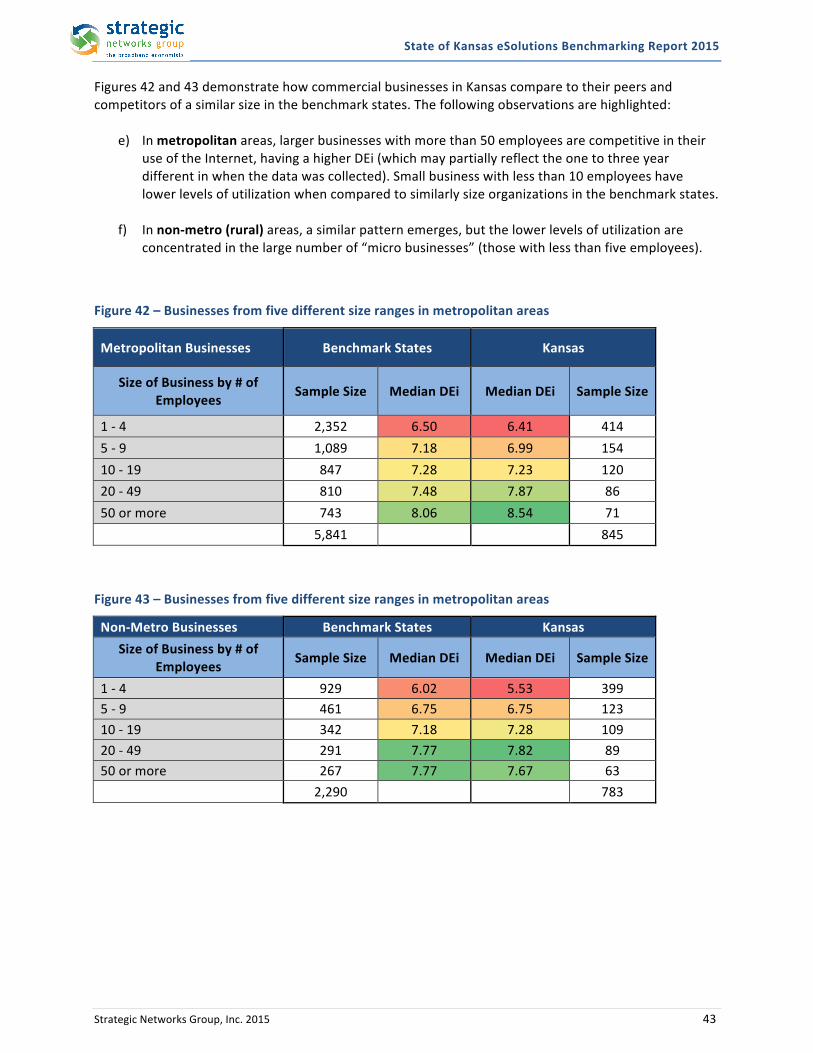

4 Comparative Analysis ...................................................................................................... 40

Data Collection Methods and Results ................................................................ 46 Appendix A -‐

Glossary ............................................................................................................ 48 Appendix B -‐

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group. Inc. 2015 www.sngroup.com Page 3 of 48

Table of Figures

Figure 1 – Survey Responses by Employment Size of Business (Number of Employees) .............................. 8 Figure 2 – Survey Responses by Industry Sector ........................................................................................... 9 Figure 3 – How Kansas Businesses Connect to the Internet ....................................................................... 10 Figure 4 – Speed-‐Test Results for Average Upload Speeds ......................................................................... 11 Figure 5 – Speed-‐Test Results for Average Download Speeds .................................................................... 11 Figure 6 – Speed-‐Test Results by Type of Connectivity ............................................................................... 12 Figure 7 – Speed-‐Test Download Speeds (mbps) by Connection and Level of Urbanization ...................... 13 Figure 8 – Speed-‐Test Upload Speeds (mbps) by Connection and Level of Urbanization ........................... 13 Figure 9 – Internet Costs by Type of Connection ........................................................................................ 14 Figure 10 – eCommerce Uses of Broadband ............................................................................................... 15 Figure 11 – eProcess Uses of Broadband .................................................................................................... 15 Figure 12 – Utilization of Mobile Internet ................................................................................................... 16 Figure 13 – Use of Web-‐enabled Mobile Devices ....................................................................................... 17 Figure 14 – Percentage of Businesses Using Cloud Based Services ............................................................ 17 Figure 15 – Motivating Drivers of Adoption of Cloud Services ................................................................... 18 Figure 16 – Mobile applications used by businesses .................................................................................. 18 Figure 17 – Importance of Broadband Benefits for Businesses .................................................................. 20 Figure 18 – Barriers to Increase Business Internet Utilization .................................................................... 21 Figure 19 – Preferred Methods for Acquiring Internal Knowledge ............................................................. 22 Figure 20 – Annual Revenues and Cost Savings from Internet Utilization .................................................. 23 Figure 21 – Summary of Employment Impacts of Business Responses ...................................................... 24 Figure 22 – Summary of Employment Impacts Specific to Internet Use ..................................................... 24 Figure 23 – Distribution of Respondents by Urban / Rural ......................................................................... 25 Figure 24 – Computer Skills by Age Group .................................................................................................. 26 Figure 25 – How Households Connect to the Internet ................................................................................ 26 Figure 26 – Speed-‐Test Upload Results for Households ............................................................................. 27 Figure 27 – Speed-‐Test Download Results for Households ......................................................................... 27 Figure 28 – Speed (Megabits per second) by Connection Type .................................................................. 28 Figure 29 – Broadband Productivity Uses by Community Population Density ........................................... 30 Figure 30 – Types of Mobile Applications use by Households .................................................................... 31 Figure 31 – Home-‐based Business Uses of the Internet ............................................................................ 32 Figure 32 – Distance to Telework Employer ............................................................................................... 33 Figure 33 – Significance of Broadband for Household Benefits .................................................................. 34 Figure 34 – Barriers to Enhanced Use of the Internet ................................................................................. 35 Figure 35 – Preferred Means for Increasing Broadband Skills .................................................................... 35 Figure 36 – Utilization Benchmarks (DEi) for Businesses by Level of Urbanization .................................... 37 Figure 37 – Utilization Benchmarks (DEi) for Businesses by Region ........................................................... 38 Figure 38 – Utilization Benchmarks (DEi) for Businesses by Size of Firm .................................................... 38 Figure 39 – Utilization Benchmarks (DEi) by Industry Sector ...................................................................... 39 Figure 40 – Different industry sectors from metropolitan areas ................................................................ 41 Figure 41 – Different industry sectors from non-‐metropolitan areas ......................................................... 42 Figure 42 – Businesses from five different size ranges in metropolitan areas ............................................ 43 Figure 43 – Businesses from five different size ranges in metropolitan areas ............................................ 43 Figure 44 – Households by age ................................................................................................................... 44 Figure 45 – Households by level of urbanization ........................................................................................ 44

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 4

Executive Summary This eSolutions Benchmarking (eSB) Report is a documentation of data collected in Kansas during December 2014 and January 2015. This summary provides an understanding of current broadband access, adoption and utilization patterns around the state.

Response Levels: A total of 2,532 organizations and 1,449 households contributed to the broadband benchmarking effort. The organizations consisted of 1,755 commercial businesses, 409 government entities and 368 non-‐for profits. Businesses and Organizations Connectivity: While connectivity speeds failed to meet the original FCC definition of broadband (768 kbps or more in at least one direction) for only 1.6% of respondents, 19.8% of those taking the speed test had upload speeds of less than 768 kbps. With the FCC poised to redefine broadband as 25 down, 3 up, only 19% of respondents meet the download while 37% meet the upload requirements of the anticipated redefining of broadband. Section 1.2 outlines the types of connectivity of respondents, as well as their levels of satisfaction. In recent years, wireless networks and mobile devices have increasingly become a factor in how people communicate, and how businesses and organizations bring efficiency to their operations. Over 80% of business respondents use a smart phone and 74.8% use a web-‐enabled laptop computer. Looking to capitalize on these newer channels of communications, 42.3% of businesses have recognized the importance of mobiles apps and have tailored their existing websites to mobile devices. Further, 29.7% of businesses are planning to optimize their websites for mobile browsers. Interestingly, over 70% of mobile users have made an online purchase with their mobile device. Additionally, over 43% of households with mobile device say they used their mobile device to purchase from a business for the first time. This is a remarkable indicator of the ability and importance of mobile communications to help businesses reach new markets and customers in non-‐traditional locations. Internet Utilization Patterns: Over 79% of businesses use the Internet to purchase goods and services online. In contrast, only 52.6% of organizations sell goods and services online. Section 1.3 looks at the level of adoption of different types of Internet applications, as well as cloud solutions, use of mobile services, and which impacts of Internet use are most valued by their users. Barriers: Security and privacy concerns are the two barriers to Internet utilization that rate the highest in importance, with almost 40% and 29% of businesses, respectively, rating them as very important. Financial and Employment Impacts of Internet Use: While reporting businesses created 1,852 new positions in the preceding 12 months, the same businesses experienced job reductions, resulting in a net job increase of 1,032 positions. The net job increase attributed to using the Internet was 628 positions. Respondents report that use of the Internet facilitated the creation of 37.6% of all new jobs created and

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 5

constituted 60.8% of net jobs created. Section 1.5 outlines employment impacts, as well as reported impacts on revenues and costs in responding organizations.

Households Connectivity: of the 556 households that took the speed test, 29% of recorded less than 768kbps on the upload speed test, 4.8% failed to record 768kbps or higher on the download speed test. Section 2.1. outlines the connectivity characteristics of respondents, including costs. Utilization: Broadband households using the Internet for a home-‐based business or for teleworking were a significant group at just over 18.7% and 18% respectively of all responding households. Section 2.2 explores how household use the Internet to increase their economic well being, with particular attention to home-‐based businesses and teleworking. Barriers: 58.1% of households expressed a desire to increase or improve their use of the Internet. The two main barriers are concerns over privacy and security (50.5% say this is a very important barrier), followed by an inadequate Internet connection (48%). See Section 2.3 for a more detailed review of this issue, including the methods that household prefer to acquire additional skills. For example, online information, webinars, and training courses are favored by over 80% of households. Classroom courses are the least preferred learning method, with 38% of respondents saying they would never take classroom courses to acquire Internet skills. Home-‐based business:

! 37.4% of home businesses (narrowly defined, see page 33) strongly agree that they would not be in business without the Internet

! 23.6% would need to relocate to get broadband if it was not available ! 88.5% of home-‐based businesses agree broadband is essential for their business to function.

Telework:

! Almost half (44.8%) of teleworkers are employed by organizations more than 30 miles (one-‐way) from their residence

! 19% would need to travel over 100 miles to their workplace if they were unable to telework ! The most important motivation factors cited for teleworking households are:

a. More family time (67%) b. Life-‐work balance (60.7%) c. Reducing commute time to their work location (59.8%) and d. Increased productivity (59.8%).

! The largest industry category for teleworking is “Professional and Technical Services” at 24%, followed by “Health Care” at 15.2%. However, teleworkers are found in a broad range of other industries.

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 6

Benchmarks for Organizations and Household: Section 3 provides statewide benchmarking to compare how different regions, industry sectors and types of households utilize the Internet. Key conclusions are that size of business and geographic location are key factors in the level of Internet utilization. Larger and more metropolitan businesses utilize the Internet more than smaller and more rural businesses. In essence, there is a digital divide or utilization gap, between small and large businesses.

Introduction This eSolutions Benchmarking (eSB) Report is a summary report that provides insights into current Internet access, adoption and utilization patterns across the state. On behalf of the State of Kansas Department of Commerce, SNG reached out to households, community institutions, and small-‐to-‐medium sized businesses across the state to encourage participation in the online assessment. Households, organizations, and businesses were asked to complete a self-‐assessment in the form of an online survey that collected information on the availability of broadband (high-‐speed Internet access), how broadband is being used in the business or the home, along with questions that would help identify benefits, drivers and barriers to adoption and utilization. While it is not possible to include every question and response from the assessment here, this eSB report provides insights into key findings that will point to gaps and opportunities for increasing broadband utilization. In addition to the information presented in this report, all the data collected through this initiative is available through an online platform called the Digital Economy Analytics Platform (DEAP), which the staff of the Department of Commerce can access. The broad insights contained within this eSB report should be used as a guide for developing an overall broadband utilization strategy. The report is organized into the following sections:

• Introduction and Methodology Overview – A brief description of the benchmarking initiative, an overview of the key methods used, and scope of research and analysis.

• Key Findings for Businesses – Summary and highlights from data provided by businesses.

• Key Findings for Households – Summary of highlights from data provided by households.

• Benchmarks for Analysis of Internet Utilization – As a benchmarking process, SNG has created

the Digital Economy Index (DEi) to compare Internet use between groups by various characteristics, such as industry, business size, and geographic location. Benchmarks create reference points against which the performance of any establishment or group can be compared.

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 7

Methodology Overview – The core methodology is founded on primary research consisting of data collection through an online self-‐assessment of businesses, organizations and households. Due to the distinct nature of the uses and benefits of different categories of Internet users, separate and distinct surveys were used for businesses and organizations and for households. Information was collected directly from Internet users in the following categories: user profile, Internet utilization, Internet benefits and barriers to Internet use. The business assessments were made available for online access through one of two means:

• Individual businesses, non-‐commercial organizations, and households were invited to participate via direct email invitations sent from a large, statewide contact list.

• Businesses and other organizations were encouraged through a variety of communications channels to access a web link to the survey.

Email invitations were sent directly to roughly 51,000 businesses and organizations across Kansas. Surveys were deployed using direct email invitation to households and organizations providing access to online surveys. The initial email invitation was sent on December 10, 2014 and reminder emails were sent roughly every seven days with the last email reminder sent on January 8th, 2015. For households, over 80,000 invitations were sent out, starting on December 15th and closing January 13th, with four reminders in between. A total of 2,532 organizations and 1,449 households contributed to the broadband benchmarking effort. The organizations consisted of 1,755 commercial businesses, 409 government entities and 368 non-‐for profits. This eSolutions Benchmarking Report provides an overview of the Internet connectivity and utilization characteristics of businesses and households. Additional data is provided through the Kansas DEAP website. The majority of respondents fully completed the surveys. However, partially completed surveys are included in the analysis on the basis that the responses provided are valid and useful even if the respondent chose not to complete the entire survey. Therefore, every data chart in this report indicates the N= value that provides the number of data points included to generate each particular figure. Further details on methodology is provided in Appendix A with a brief Glossary of report terminology in Appendix B.

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 8

1 Kansas Businesses Access to and effective use of the Internet has become an essential element in the survival and success of businesses in today’s economy. This section identifies key findings related to how businesses use the Internet, what types of benefits they value most, and which barriers prevent more effective use. The findings are broken down by key respondent characteristics such as industry sector, employment size and connectivity type.

1.1 Respondent Profile The sample set outlined in this section includes data from businesses across the state. The sample includes survey responses from businesses across all 20 industries classified by NAICS.1 Unless otherwise noted, Section 1 only includes data from respondents that identified themselves as commercial businesses. Previous studies conducted by SNG have shown that that the size of a business is correlated to how business access and use the Internet. Figure 1 shows the breakdown of survey responses by size of establishment, as measured by number of employees. The chart provides a comparison to the state profile of establishments. The survey sample is very similar to the state profile as reported by the Census Bureau, with a very slight under-‐representation of micro businesses (those with less than 10 employees).

Figure 1 -‐ Survey Responses by Employment Size of Business (Number of Employees)

1 North American Industry Classification System. Industry breakdowns are at the 2-‐digit NAICS code level. Some survey responses did not have an industry classification.

49.9%

17.0%

14.1%

10.7%

4.4%

2.5%

.6%

.8%

53.3%

19.5%

13.2%

8.8%

2.9%

1.6%

.4%

.2%

0% 10% 20% 30% 40% 50% 60%

1 -‐ 4

5 -‐ 9

10 -‐ 19

20 -‐ 49

50 -‐ 99

100 -‐ 249

250 -‐ 499

500 or more

State Profile Survey Sample N = 1,629

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 9

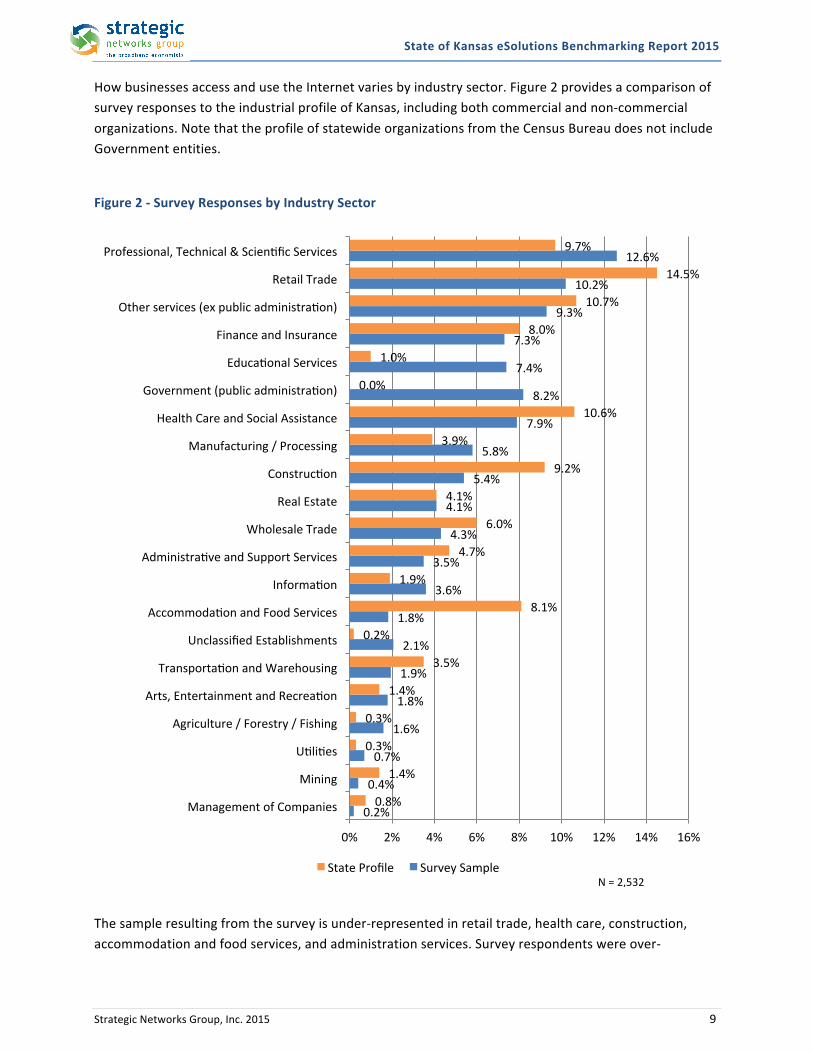

How businesses access and use the Internet varies by industry sector. Figure 2 provides a comparison of survey responses to the industrial profile of Kansas, including both commercial and non-‐commercial organizations. Note that the profile of statewide organizations from the Census Bureau does not include Government entities.

Figure 2 -‐ Survey Responses by Industry Sector

The sample resulting from the survey is under-‐represented in retail trade, health care, construction, accommodation and food services, and administration services. Survey respondents were over-‐

0.2%

0.4%

0.7%

1.6%

1.8%

1.9%

2.1%

1.8%

3.6%

3.5%

4.3%

4.1%

5.4%

5.8%

7.9%

8.2%

7.4%

7.3%

9.3%

10.2%

12.6%

0.8%

1.4%

0.3%

0.3%

1.4%

3.5%

0.2%

8.1%

1.9%

4.7%

6.0%

4.1%

9.2%

3.9%

10.6%

0.0%

1.0%

8.0%

10.7%

14.5%

9.7%

0% 2% 4% 6% 8% 10% 12% 14% 16%

Management of Companies

Mining

Uiliies

Agriculture / Forestry / Fishing

Arts, Entertainment and Recreaion

Transportaion and Warehousing

Unclassified Establishments

Accommodaion and Food Services

Informaion

Administraive and Support Services

Wholesale Trade

Real Estate

Construcion

Manufacturing / Processing

Health Care and Social Assistance

Government (public administraion)

Educaional Services

Finance and Insurance

Other services (ex public administraion)

Retail Trade

Professional, Technical & Scienific Services

State Profile Survey Sample N = 2,532

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 10

represented in Information, Educational Services, Professional and Technical, and Manufacturing. State profile data does not include data on Public Administration.2

1.2 Business Connectivity Characteristics The speed and quality of business Internet connections strongly impact many uses of the Internet, such as video conferencing and real time collaboration. As seen in Figure 3, the survey includes responses from users of a mix of Internet connectivity technologies. The use of broadband is very high across all types and locations of businesses. While over 98% of responding businesses have connectivity other than dial-‐up or satellite, many still lack broadband level connections in at least one direction. As of 2010, broadband speeds are defined by the U.S. Federal Government as being 4 megabits per second (4Mb/s) for downloads, and at least 1 megabit per second (1Mb/s) for uploads. A raise in these minimums is anticipated in 2015 to 25 and 3 megabits respectively. As seen in Figure 3 below, cable, DSL, and fiber are the predominant technologies for connectivity. A small percentage of businesses use dial-‐up (0.7%) and satellite (2.1%) connections as their primary connection. These are predominantly very small businesses. Businesses with less than 50 employees are more likely than larger businesses to use cable, DSL and fixed wireless. Larger businesses are far more likely to have a T1 connection. Fiber connections are spread across all sizes of businesses.

Figure 3 – How Kansas Businesses Connect to the Internet

1.2.1 Internet Speeds The survey included an opportunity for respondents to take a live speed test that assessed their actual upload and download speeds. The survey responses, indicated by N in each chart, vary because

2 State data source: US Census Bureau County Business Patterns 2011 – Number of establishments shown for sample do not include Public Administration in the totals for comparative purposes.

.6%

.7% 2.1% 2.6% 3.2% 4.1%

7.6% 8.1%

13.9% 23.1%

34.0%

0% 5% 10% 15% 20% 25% 30% 35% 40%

No Internet Dial-‐up Satellite

Mobile Wireless Other High-‐speed Internet

Not Sure Fixed Wireless

T1 Fiber DSL

Cable

Pct. Establishments N = 1,775 N =

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 11

completion of the speed test portion was optional. Figures 4 through 6 summarize the results of the speed test portion of the business survey. While connectivity speeds failed to meet the original FCC definition of broadband (768 kbps or more in at least one direction) for only 1.6% of respondents merely reporting their speed of service, 19.8% of those taking the speed test had upload speeds of less than 768 kbps. Important to note is that SNG’s internal analysis shows a stronger correlation with Internet utilization and upload speeds than with download speeds. Thus, for businesses to get the most out of broadband, upload speed is proving to be the critical direction.

Figure 4 – Speed-‐Test Results for Average Upload Speeds

Figure 5 – Speed-‐Test Results for Average Download Speeds

.8%

19.0%

26.0%

17.0%

17.8%

7.9%

6.9%

2.2%

1.7%

.7%

0% 5% 10% 15% 20% 25% 30%

Less than 200 kbps

200 kbps up to 768

768 kbps up to 1.5

1.5 mbps up to 3

3 mbps up to 6 mbps

6 mbps up to 10 mbps

10 mbps up to 25

25 mbps up to 50

50 mbps up to 100

100 mbps or more

Pct. of Users N = 872

1.6%

6.1%

7.6%

20.5%

15.1%

30.5%

10.6%

7.0%

1.0%

0% 5% 10% 15% 20% 25% 30% 35%

Less than 768 kbps

768 kbps up to 1.5 mbps

1.5 mbps up to 3 mbps

3 mbps up to 6 mbps

6 mbps up to 10 mbps

10 mbps up to 25 mbps

25 mbps up to 50 mbps

50 mbps up to 100 mbps

100 mbps up to 1 gbps

Pct. of Users N = 876

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 12

As seen in Figure 6, the speed test results varied significantly between different technologies, with fiber leading by a wide margin. Cable and fixed wireless formed the second fastest tier of service, while T1, DSL, mobile wireless and satellite recorded the slowest speeds. However, it is worth noting that based on SNG data collected since 2010, speeds are increasing rapidly for fiber, cable, and both fixed and mobile wireless. Figure 6 – Speed-‐Test Results by Type of Connectivity

7.8

8.8

10.2

10.7

13.5

20.6

37.2

2.0

1.7

4.4

3.9

6.5

4.8

27.7

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0

Satellite

DSL

Mobile Wireless

Fixed Wireless

T1

Cable

Fiber

Megabits per second

Ave. Upload Speed (Mbps) Ave. Download Speed (Mbps) N = 872

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 13

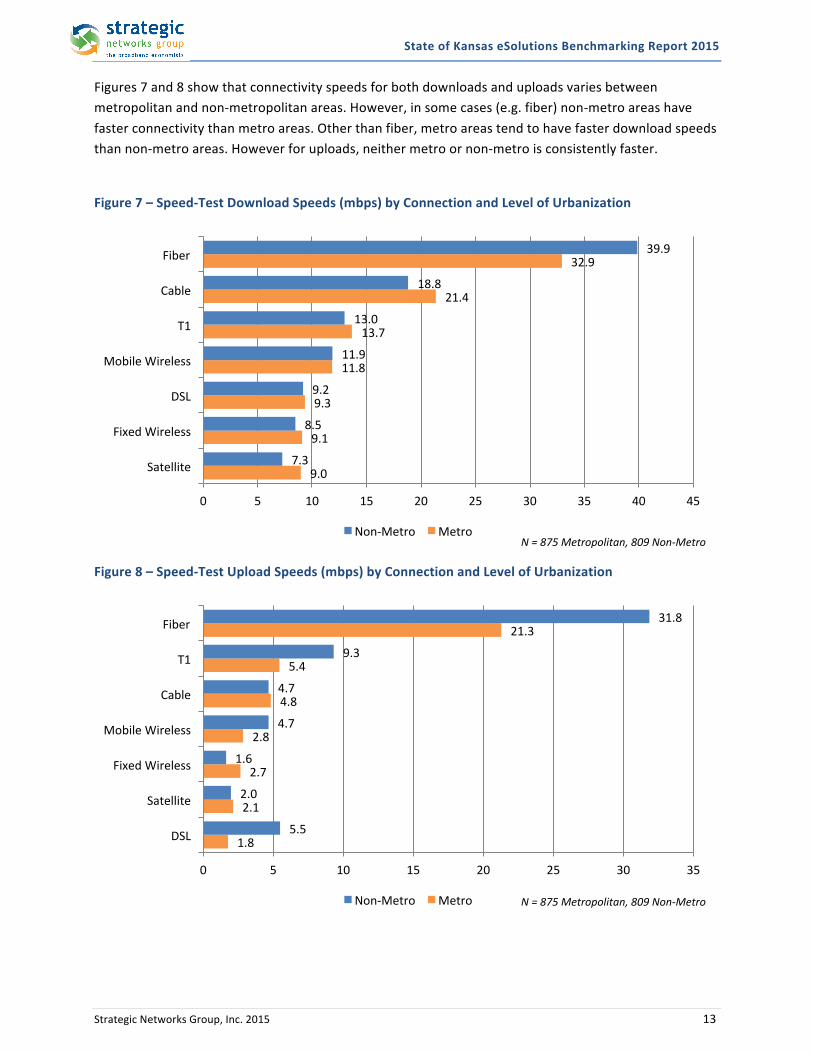

Figures 7 and 8 show that connectivity speeds for both downloads and uploads varies between metropolitan and non-‐metropolitan areas. However, in some cases (e.g. fiber) non-‐metro areas have faster connectivity than metro areas. Other than fiber, metro areas tend to have faster download speeds than non-‐metro areas. However for uploads, neither metro or non-‐metro is consistently faster.

Figure 7 – Speed-‐Test Download Speeds (mbps) by Connection and Level of Urbanization

Figure 8 – Speed-‐Test Upload Speeds (mbps) by Connection and Level of Urbanization

9.0

9.1

9.3

11.8

13.7

21.4

32.9

7.3

8.5

9.2

11.9

13.0

18.8

39.9

0 5 10 15 20 25 30 35 40 45

Satellite

Fixed Wireless

DSL

Mobile Wireless

T1

Cable

Fiber

Non-‐Metro Metro N = 875 Metropolitan, 809 Non-‐Metro

1.8

2.1

2.7

2.8

4.8

5.4

21.3

5.5

2.0

1.6

4.7

4.7

9.3

31.8

0 5 10 15 20 25 30 35

DSL

Satellite

Fixed Wireless

Mobile Wireless

Cable

T1

Fiber

Non-‐Metro Metro N = 875 Metropolitan, 809 Non-‐Metro

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 14

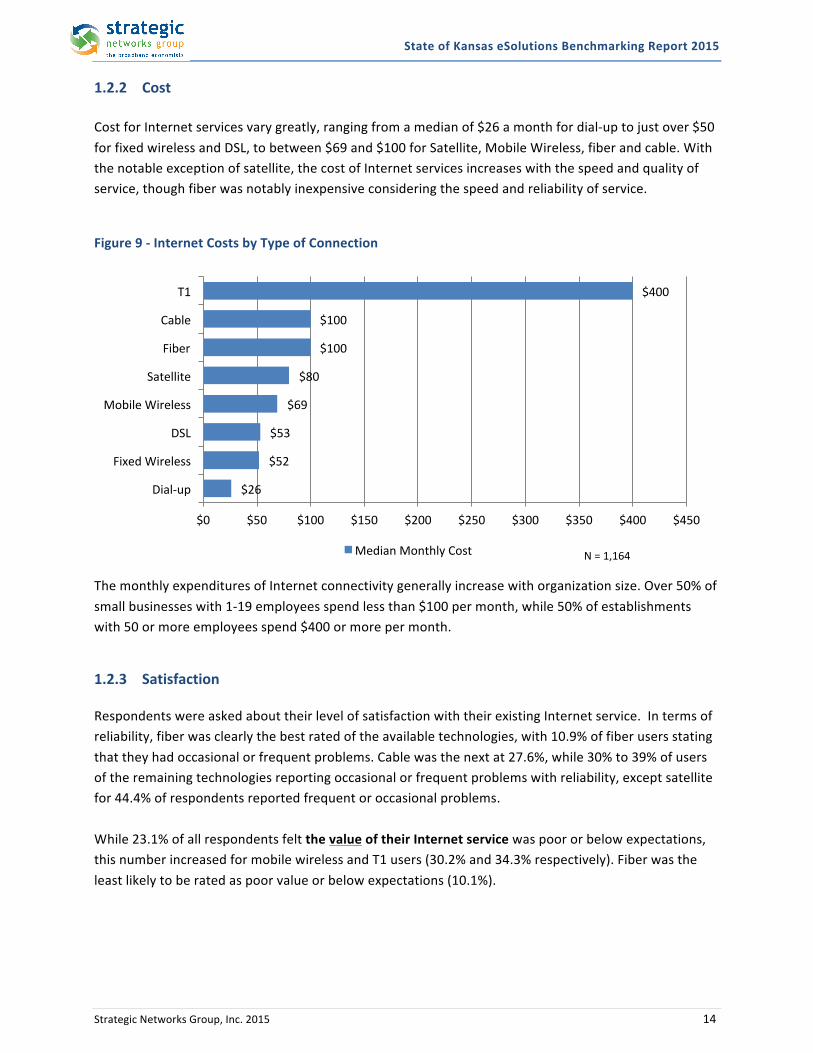

1.2.2 Cost Cost for Internet services vary greatly, ranging from a median of $26 a month for dial-‐up to just over $50 for fixed wireless and DSL, to between $69 and $100 for Satellite, Mobile Wireless, fiber and cable. With the notable exception of satellite, the cost of Internet services increases with the speed and quality of service, though fiber was notably inexpensive considering the speed and reliability of service.

Figure 9 -‐ Internet Costs by Type of Connection

The monthly expenditures of Internet connectivity generally increase with organization size. Over 50% of small businesses with 1-‐19 employees spend less than $100 per month, while 50% of establishments with 50 or more employees spend $400 or more per month.

1.2.3 Satisfaction Respondents were asked about their level of satisfaction with their existing Internet service. In terms of reliability, fiber was clearly the best rated of the available technologies, with 10.9% of fiber users stating that they had occasional or frequent problems. Cable was the next at 27.6%, while 30% to 39% of users of the remaining technologies reporting occasional or frequent problems with reliability, except satellite for 44.4% of respondents reported frequent or occasional problems. While 23.1% of all respondents felt the value of their Internet service was poor or below expectations, this number increased for mobile wireless and T1 users (30.2% and 34.3% respectively). Fiber was the least likely to be rated as poor value or below expectations (10.1%).

$26

$52

$53

$69

$80

$100

$100

$400

$0 $50 $100 $150 $200 $250 $300 $350 $400 $450

Dial-‐up

Fixed Wireless

DSL

Mobile Wireless

Satellite

Fiber

Cable

T1

Median Monthly Cost N = 1,164

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 15

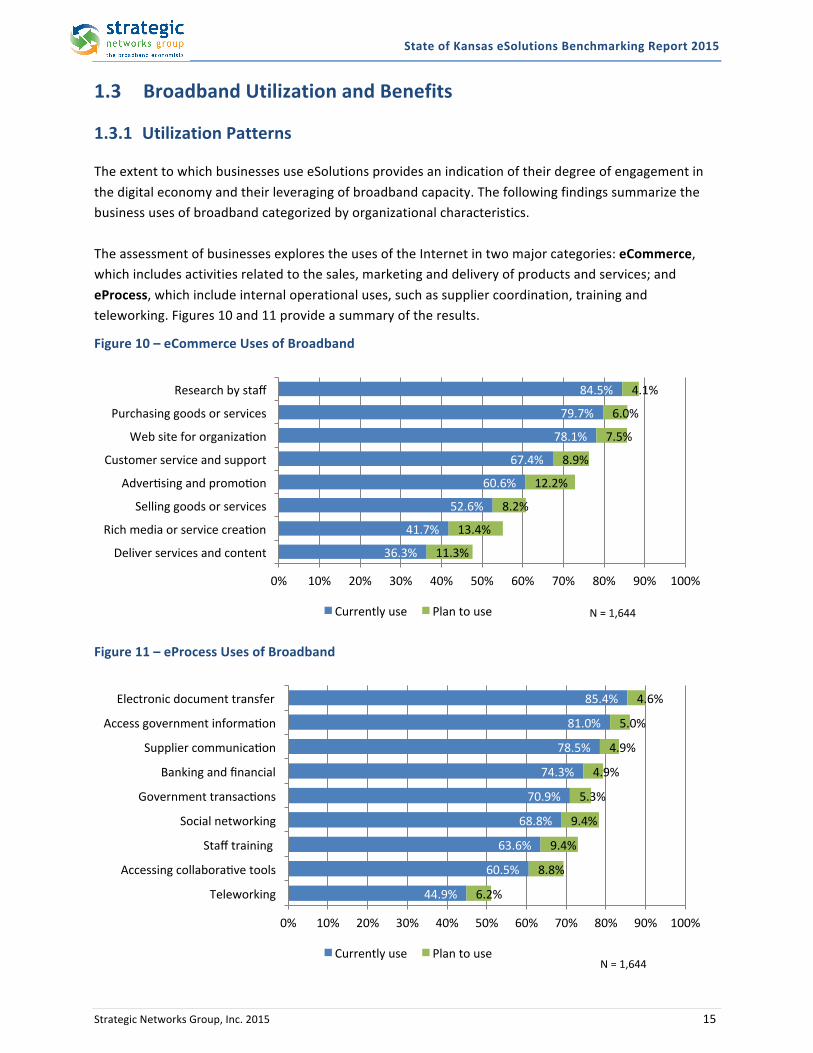

1.3 Broadband Utilization and Benefits 1.3.1 Utilization Patterns The extent to which businesses use eSolutions provides an indication of their degree of engagement in the digital economy and their leveraging of broadband capacity. The following findings summarize the business uses of broadband categorized by organizational characteristics. The assessment of businesses explores the uses of the Internet in two major categories: eCommerce, which includes activities related to the sales, marketing and delivery of products and services; and eProcess, which include internal operational uses, such as supplier coordination, training and teleworking. Figures 10 and 11 provide a summary of the results.

Figure 10 – eCommerce Uses of Broadband

Figure 11 – eProcess Uses of Broadband

36.3%

41.7%

52.6%

60.6%

67.4%

78.1%

79.7%

84.5%

11.3%

13.4%

8.2%

12.2%

8.9%

7.5%

6.0%

4.1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Deliver services and content

Rich media or service creaion

Selling goods or services

Adverising and promoion

Customer service and support

Web site for organizaion

Purchasing goods or services

Research by staff

Currently use Plan to use N = 1,644

44.9%

60.5%

63.6%

68.8%

70.9%

74.3%

78.5%

81.0%

85.4%

6.2%

8.8%

9.4%

9.4%

5.3%

4.9%

4.9%

5.0%

4.6%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Teleworking

Accessing collaboraive tools

Staff training

Social networking

Government transacions

Banking and financial

Supplier communicaion

Access government informaion

Electronic document transfer

Currently use Plan to use N = 1,644

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 16

Utilization of Internet-‐enabled applications and operations is still evolving. Simpler processes that have long been available, such as email, are heavily accessed by all user types. Differentiation emerges in utilization patterns as more complex business and transactional processes come “online,” and more current technologies spawn enhanced or new capabilities. The two most significant factors in broadband utilization levels are size of organization and industrial classification to which an organization belongs. Broadband offers uses that can transform the way businesses conduct their operations. Over 79% of businesses use broadband for coordination with suppliers, while over 62% use broadband for employee training and another 66% for improving customer service. Likewise, 78.6% of businesses use the Internet to purchase goods and services online. In contrast, only 52.8% of organizations sell goods and services online and just over 36.8% deliver services and content online.

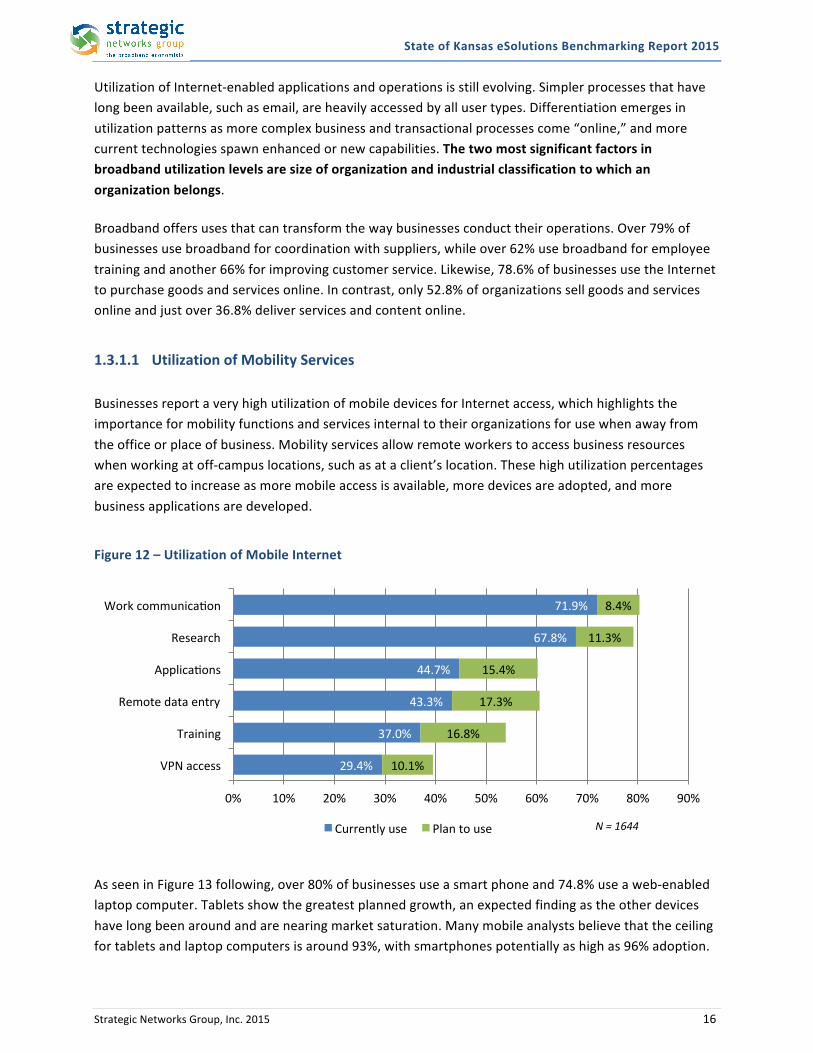

1.3.1.1 Utilization of Mobility Services Businesses report a very high utilization of mobile devices for Internet access, which highlights the importance for mobility functions and services internal to their organizations for use when away from the office or place of business. Mobility services allow remote workers to access business resources when working at off-‐campus locations, such as at a client’s location. These high utilization percentages are expected to increase as more mobile access is available, more devices are adopted, and more business applications are developed.

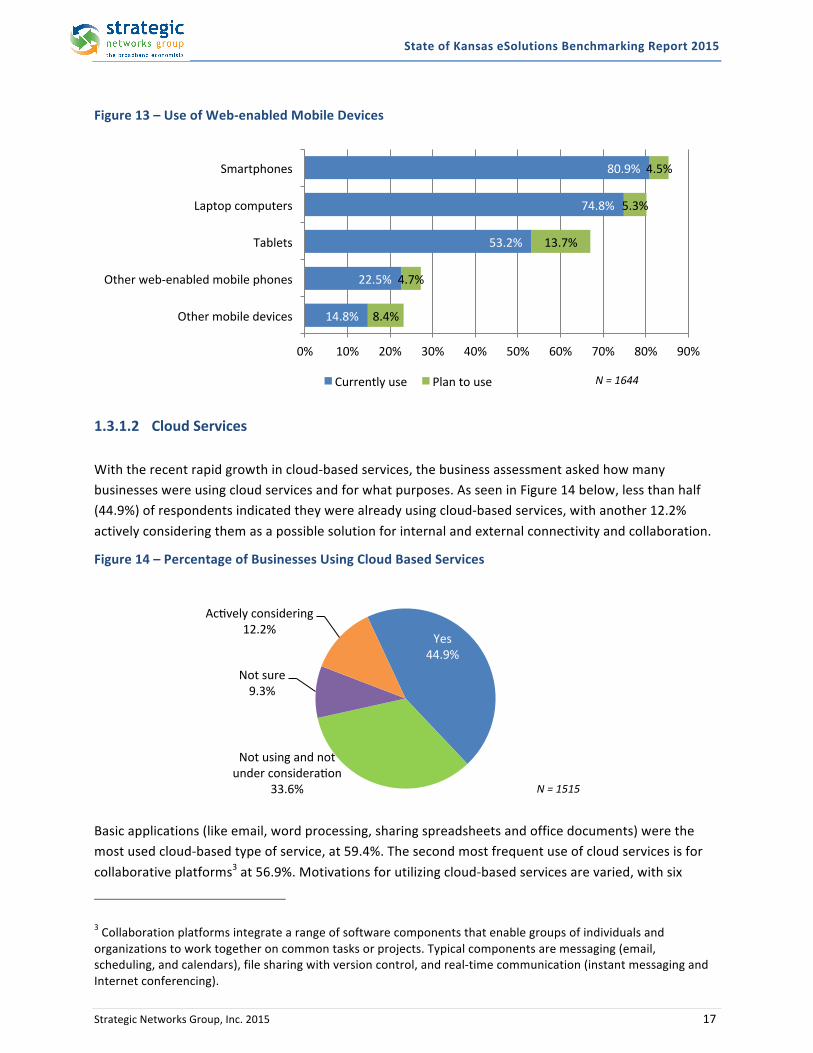

Figure 12 – Utilization of Mobile Internet

As seen in Figure 13 following, over 80% of businesses use a smart phone and 74.8% use a web-‐enabled laptop computer. Tablets show the greatest planned growth, an expected finding as the other devices have long been around and are nearing market saturation. Many mobile analysts believe that the ceiling for tablets and laptop computers is around 93%, with smartphones potentially as high as 96% adoption.

29.4%

37.0%

43.3%

44.7%

67.8%

71.9%

10.1%

16.8%

17.3%

15.4%

11.3%

8.4%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

VPN access

Training

Remote data entry

Applicaions

Research

Work communicaion

Currently use Plan to use N = 1644

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 17

Figure 13 – Use of Web-‐enabled Mobile Devices

1.3.1.2 Cloud Services With the recent rapid growth in cloud-‐based services, the business assessment asked how many businesses were using cloud services and for what purposes. As seen in Figure 14 below, less than half (44.9%) of respondents indicated they were already using cloud-‐based services, with another 12.2% actively considering them as a possible solution for internal and external connectivity and collaboration.

Figure 14 – Percentage of Businesses Using Cloud Based Services

Basic applications (like email, word processing, sharing spreadsheets and office documents) were the most used cloud-‐based type of service, at 59.4%. The second most frequent use of cloud services is for collaborative platforms3 at 56.9%. Motivations for utilizing cloud-‐based services are varied, with six

3 Collaboration platforms integrate a range of software components that enable groups of individuals and organizations to work together on common tasks or projects. Typical components are messaging (email, scheduling, and calendars), file sharing with version control, and real-‐time communication (instant messaging and Internet conferencing).

14.8%

22.5%

53.2%

74.8%

80.9%

8.4%

4.7%

13.7%

5.3%

4.5%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Other mobile devices

Other web-‐enabled mobile phones

Tablets

Laptop computers

Smartphones

Currently use Plan to use N = 1644

Yes 44.9%

Not using and not under consideraion

33.6%

Not sure 9.3%

Acively considering 12.2%

N = 1515

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 18

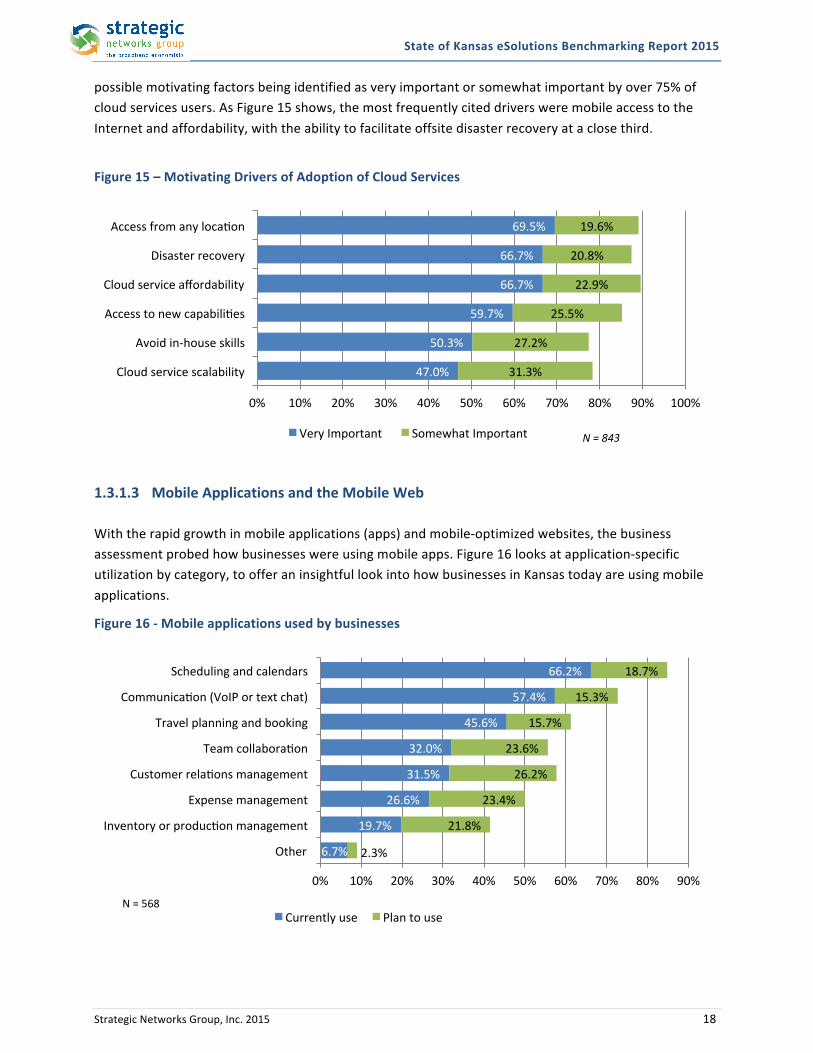

possible motivating factors being identified as very important or somewhat important by over 75% of cloud services users. As Figure 15 shows, the most frequently cited drivers were mobile access to the Internet and affordability, with the ability to facilitate offsite disaster recovery at a close third.

Figure 15 – Motivating Drivers of Adoption of Cloud Services

1.3.1.3 Mobile Applications and the Mobile Web With the rapid growth in mobile applications (apps) and mobile-‐optimized websites, the business assessment probed how businesses were using mobile apps. Figure 16 looks at application-‐specific utilization by category, to offer an insightful look into how businesses in Kansas today are using mobile applications.

Figure 16 -‐ Mobile applications used by businesses

47.0%

50.3%

59.7%

66.7%

66.7%

69.5%

31.3%

27.2%

25.5%

22.9%

20.8%

19.6%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Cloud service scalability

Avoid in-‐house skills

Access to new capabiliies

Cloud service affordability

Disaster recovery

Access from any locaion

Very Important Somewhat Important N = 843

6.7%

19.7%

26.6%

31.5%

32.0%

45.6%

57.4%

66.2%

2.3%

21.8%

23.4%

26.2%

23.6%

15.7%

15.3%

18.7%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Other

Inventory or producion management

Expense management

Customer relaions management

Team collaboraion

Travel planning and booking

Communicaion (VoIP or text chat)

Scheduling and calendars

Currently use Plan to use N = 568

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 19

If a business did not have a stand-‐alone app for their business, 42.3% of businesses have nonetheless recognized the importance of mobiles apps and have tailored their existing websites to mobile devices. Further, 29.7% percent of businesses are planning to optimize their websites for mobile browsers. Typically, a mobile-‐optimized website will contain most of the same content and information that a traditional browser-‐based website has, only organized and presented in a format suitable for smaller screens, touch controls, and intuitive navigation. An app would also integrate interactive map functionality for mobile customers to drive directly to the business location, and click to call function for quicker means of communication, as opposed to a traditional website that would perhaps offer a static map graphic with links to email the business. 1.3.2 Broadband and Deciding Where to Locate To better determine the impact of broadband on physical business locations, businesses were asked about the importance of broadband for both selecting their location and for remaining in their current location. Responses to the survey clearly indicate that availability and suitability of broadband play an important role in corporate decisions to remain in a community, and if a business is moving, which areas it is willing to consider. Over 33% of businesses say that broadband service was “essential” in selecting their business location, and over 53% say broadband is “essential” for remaining in their current location.

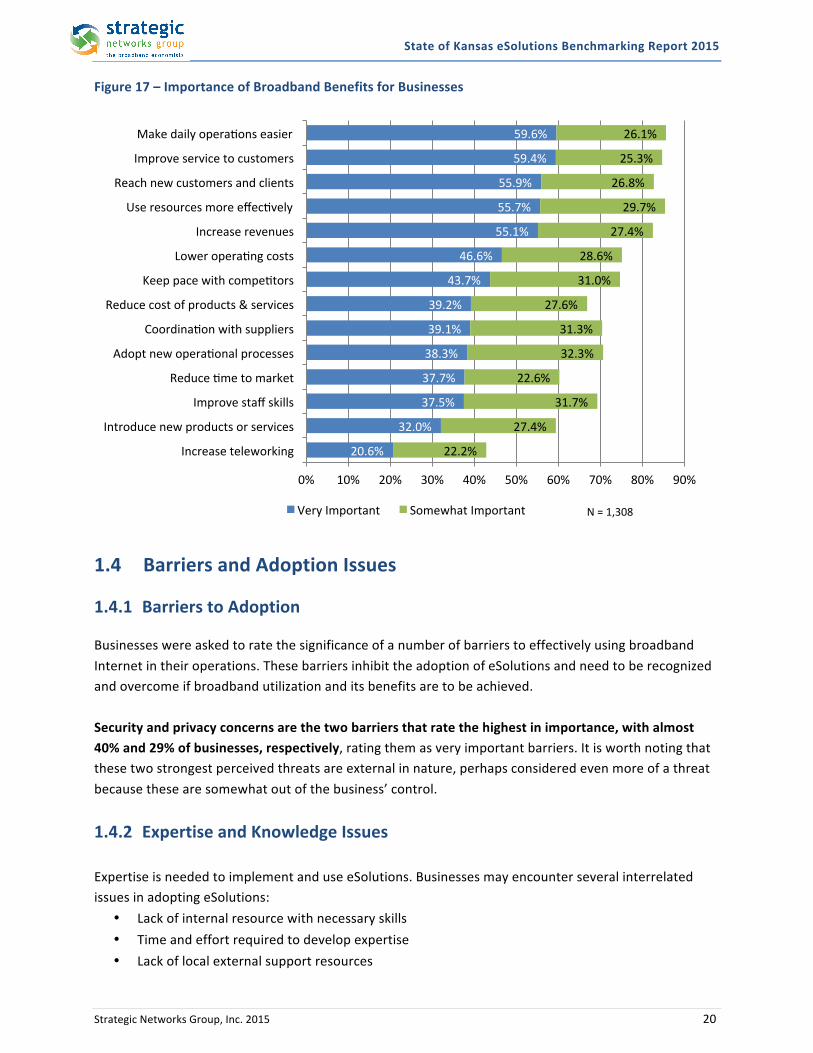

1.3.3 Broadband Benefits and Impacts Overall, the majority of businesses recognize broadband as important across all benefits dimensions. The most generally recognized benefits are related to improved efficiency and productivity, as well as improving service to customers. Productivity-‐related benefits are slightly more valued by businesses than the revenue-‐related benefits, such as market reach, competitiveness, increasing revenues, and introducing new products. The net effect of these benefits is to increase competitiveness, productivity and revenues, while reducing costs and improving profitability. Understanding broadband’s importance in contributing specific benefits allows for a more complete understand of broadband’s impact.

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 20

Figure 17 – Importance of Broadband Benefits for Businesses

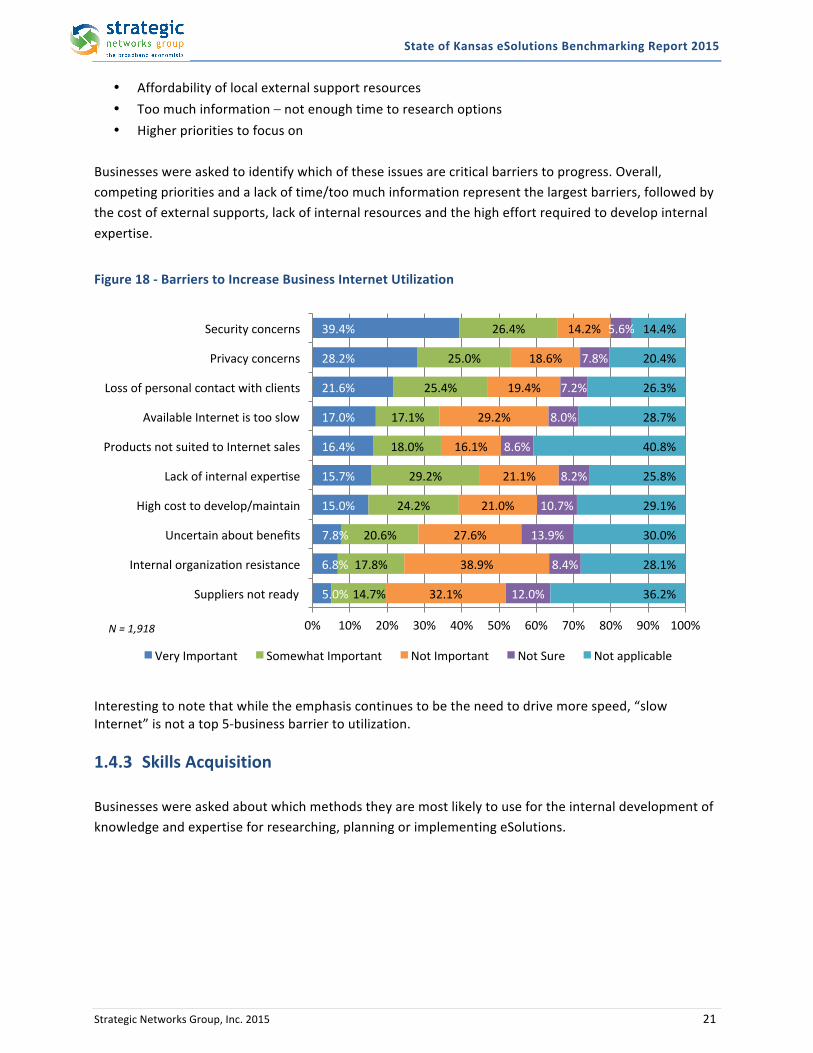

1.4 Barriers and Adoption Issues 1.4.1 Barriers to Adoption Businesses were asked to rate the significance of a number of barriers to effectively using broadband Internet in their operations. These barriers inhibit the adoption of eSolutions and need to be recognized and overcome if broadband utilization and its benefits are to be achieved. Security and privacy concerns are the two barriers that rate the highest in importance, with almost 40% and 29% of businesses, respectively, rating them as very important barriers. It is worth noting that these two strongest perceived threats are external in nature, perhaps considered even more of a threat because these are somewhat out of the business’ control.

1.4.2 Expertise and Knowledge Issues Expertise is needed to implement and use eSolutions. Businesses may encounter several interrelated issues in adopting eSolutions:

• Lack of internal resource with necessary skills • Time and effort required to develop expertise • Lack of local external support resources

20.6%

32.0%

37.5%

37.7%

38.3%

39.1%

39.2%

43.7%

46.6%

55.1%

55.7%

55.9%

59.4%

59.6%

22.2%

27.4%

31.7%

22.6%

32.3%

31.3%

27.6%

31.0%

28.6%

27.4%

29.7%

26.8%

25.3%

26.1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Increase teleworking

Introduce new products or services

Improve staff skills

Reduce ime to market

Adopt new operaional processes

Coordinaion with suppliers

Reduce cost of products & services

Keep pace with compeitors

Lower operaing costs

Increase revenues

Use resources more effecively

Reach new customers and clients

Improve service to customers

Make daily operaions easier

Very Important Somewhat Important N = 1,308

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 21

• Affordability of local external support resources • Too much information – not enough time to research options • Higher priorities to focus on

Businesses were asked to identify which of these issues are critical barriers to progress. Overall, competing priorities and a lack of time/too much information represent the largest barriers, followed by the cost of external supports, lack of internal resources and the high effort required to develop internal expertise.

Figure 18 -‐ Barriers to Increase Business Internet Utilization

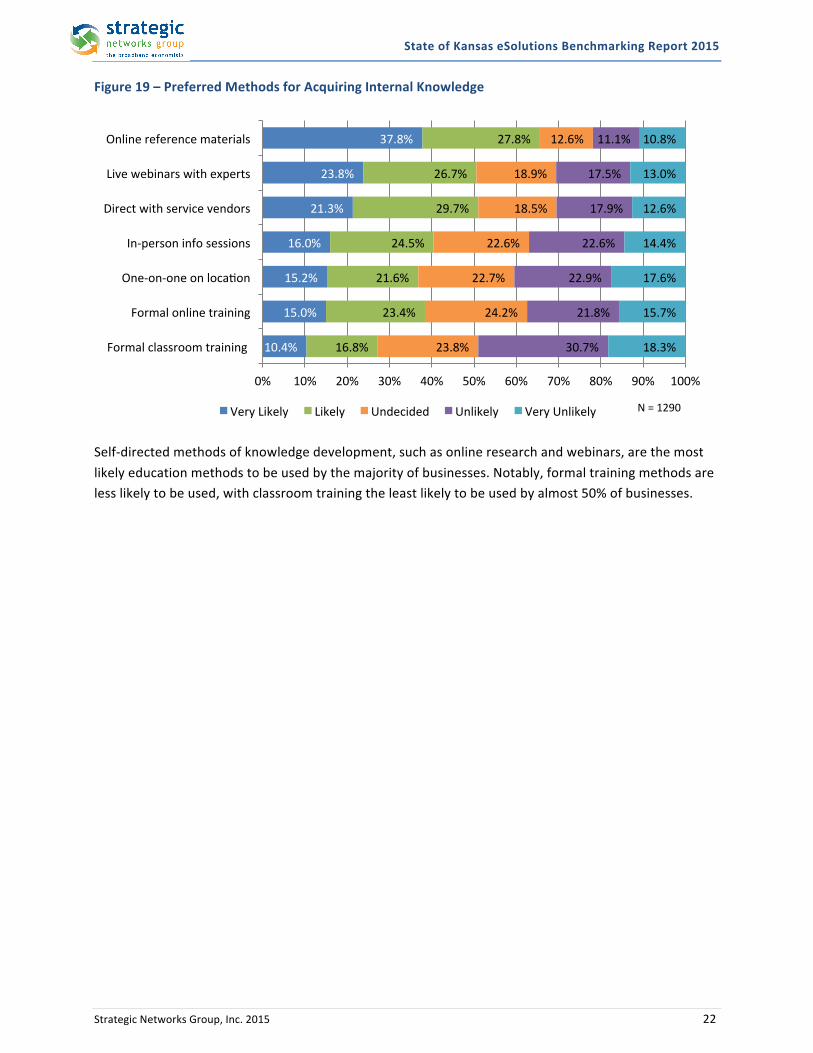

Interesting to note that while the emphasis continues to be the need to drive more speed, “slow Internet” is not a top 5-‐business barrier to utilization. 1.4.3 Skills Acquisition Businesses were asked about which methods they are most likely to use for the internal development of knowledge and expertise for researching, planning or implementing eSolutions.

5.0%

6.8%

7.8%

15.0%

15.7%

16.4%

17.0%

21.6%

28.2%

39.4%

14.7%

17.8%

20.6%

24.2%

29.2%

18.0%

17.1%

25.4%

25.0%

26.4%

32.1%

38.9%

27.6%

21.0%

21.1%

16.1%

29.2%

19.4%

18.6%

14.2%

12.0%

8.4%

13.9%

10.7%

8.2%

8.6%

8.0%

7.2%

7.8%

5.6%

36.2%

28.1%

30.0%

29.1%

25.8%

40.8%

28.7%

26.3%

20.4%

14.4%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Suppliers not ready

Internal organizaion resistance

Uncertain about benefits

High cost to develop/maintain

Lack of internal experise

Products not suited to Internet sales

Available Internet is too slow

Loss of personal contact with clients

Privacy concerns

Security concerns

Very Important Somewhat Important Not Important Not Sure Not applicable

N = 1,918

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 22

Figure 19 – Preferred Methods for Acquiring Internal Knowledge

Self-‐directed methods of knowledge development, such as online research and webinars, are the most likely education methods to be used by the majority of businesses. Notably, formal training methods are less likely to be used, with classroom training the least likely to be used by almost 50% of businesses.

10.4%

15.0%

15.2%

16.0%

21.3%

23.8%

37.8%

16.8%

23.4%

21.6%

24.5%

29.7%

26.7%

27.8%

23.8%

24.2%

22.7%

22.6%

18.5%

18.9%

12.6%

30.7%

21.8%

22.9%

22.6%

17.9%

17.5%

11.1%

18.3%

15.7%

17.6%

14.4%

12.6%

13.0%

10.8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Formal classroom training

Formal online training

One-‐on-‐one on locaion

In-‐person info sessions

Direct with service vendors

Live webinars with experts

Online reference materials

Very Likely Likely Undecided Unlikely Very Unlikely N = 1290

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 23

1.5 Financial and Employment Impacts from Internet Use To gauge the impacts of Internet use on the operations, businesses were asked to quantify how using the Internet has affected revenue generation, operating cost savings and employment. Due to the proprietary and sensitive nature of this information, these questions were optional for survey respondents. As a result, the sample sizes for usable data in these areas is significantly less than for the total survey response set. The business assessment reached approximately 1,892 commercial establishments, but the largest amount of data collected was in relation to employment and the impacts of the Internet, on which 585 establishments reported data. For other metrics, 345 and 167 businesses reported data for revenues and operating cost savings related to the Internet, respectively. Businesses were asked to provide their total annual4 revenues, operating costs, and current employment to provide a baseline for assessment of impacts. They were also asked to provide the changes as a result of using the Internet, specifically:

• Number of new jobs created in the past 12-‐month period and the number of new jobs created that can be attributed to using the Internet. Example: Consider the difference to job creation if your organization did not use the Internet.

• Total Annual Revenue from the Internet over the past 12-‐month period. Example: This may include direct Internet (online) and income enabled by using the Internet to interact with customers.

• Total Annual Cost Savings from using the Internet over the same period. Example: This may include direct labor costs and other operating cost savings through efficiencies in purchasing and new operating processes.

In terms of the impact of the Internet on generating both revenues and cost savings, 233 Kansas businesses reported 63.3% of 12-‐month revenues generated through the Internet, and 136 businesses in the state reported a 12-‐month operating cost savings of 3.8% due to their use of the Internet.

Figure 20 – Annual Revenues and Cost Savings from Internet Utilization

Annual Revenue Impacts Number of

Establishments Total Annual Revenue

($M) Annual Revenue from

Internet ($M) Percent Internet

Revenue

233 $1,696 $1,073 63.3%

Annual Operating Cost Impacts

Number of Establishments

Total Annual Operating Cost ($M)

Cost Saving from Internet ($M) Percent Cost Saving

136 $232 $9.3 3.8%

4 Annual figures were requested for the past 12 month reporting period.

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 24

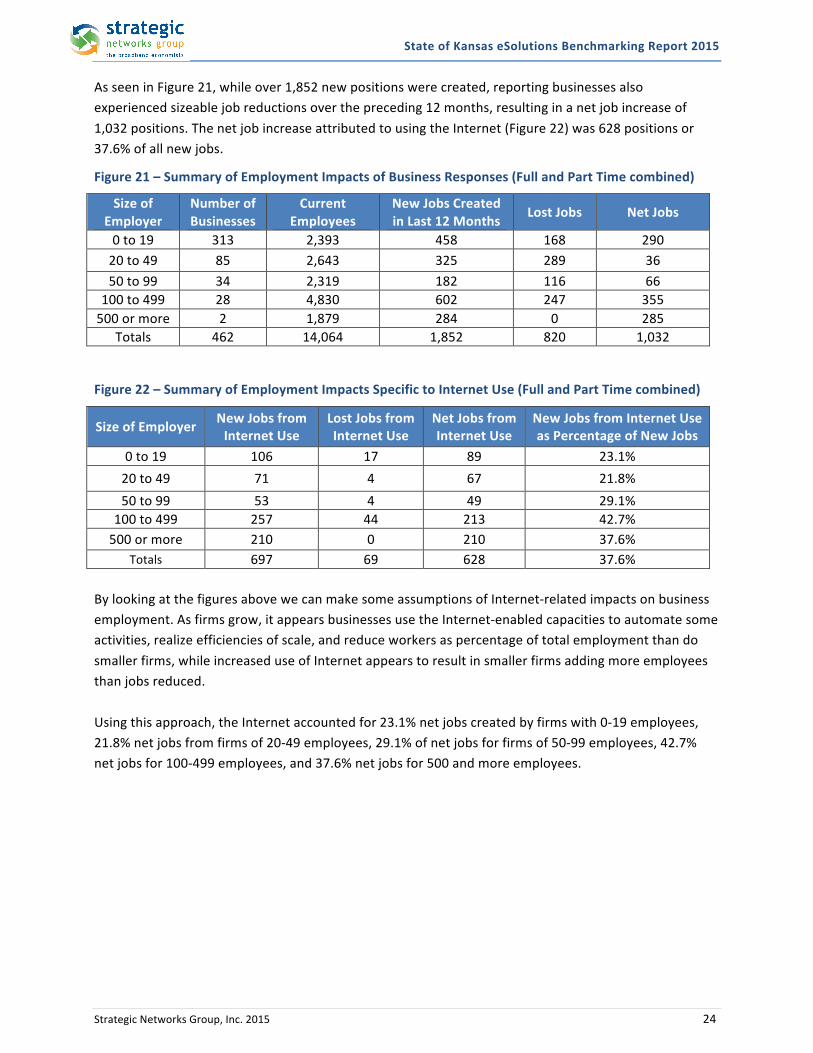

As seen in Figure 21, while over 1,852 new positions were created, reporting businesses also experienced sizeable job reductions over the preceding 12 months, resulting in a net job increase of 1,032 positions. The net job increase attributed to using the Internet (Figure 22) was 628 positions or 37.6% of all new jobs.

Figure 21 – Summary of Employment Impacts of Business Responses (Full and Part Time combined)

Size of Employer

Number of Businesses

Current Employees

New Jobs Created in Last 12 Months Lost Jobs Net Jobs

0 to 19 313 2,393 458 168 290 20 to 49 85 2,643 325 289 36 50 to 99 34 2,319 182 116 66

100 to 499 28 4,830 602 247 355 500 or more 2 1,879 284 0 285

Totals 462 14,064 1,852 820 1,032

Figure 22 – Summary of Employment Impacts Specific to Internet Use (Full and Part Time combined)

Size of Employer New Jobs from Internet Use

Lost Jobs from Internet Use

Net Jobs from Internet Use

New Jobs from Internet Use as Percentage of New Jobs

0 to 19 106 17 89 23.1% 20 to 49 71 4 67 21.8% 50 to 99 53 4 49 29.1%

100 to 499 257 44 213 42.7% 500 or more 210 0 210 37.6%

Totals 697 69 628 37.6% By looking at the figures above we can make some assumptions of Internet-‐related impacts on business employment. As firms grow, it appears businesses use the Internet-‐enabled capacities to automate some activities, realize efficiencies of scale, and reduce workers as percentage of total employment than do smaller firms, while increased use of Internet appears to result in smaller firms adding more employees than jobs reduced. Using this approach, the Internet accounted for 23.1% net jobs created by firms with 0-‐19 employees, 21.8% net jobs from firms of 20-‐49 employees, 29.1% of net jobs for firms of 50-‐99 employees, 42.7% net jobs for 100-‐499 employees, and 37.6% net jobs for 500 and more employees.

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 25

2 Kansas Households

The following analysis is based on assessment responses from 1,449 households from across Kansas. The assessment results presented in this chapter focus on key findings related to Internet usage, benefits and barriers, with selected results broken down by key respondent characteristics, such as household income, Internet connectivity type, and rural versus non-‐rural regions.

2.1 Household Profiles and Connectivity

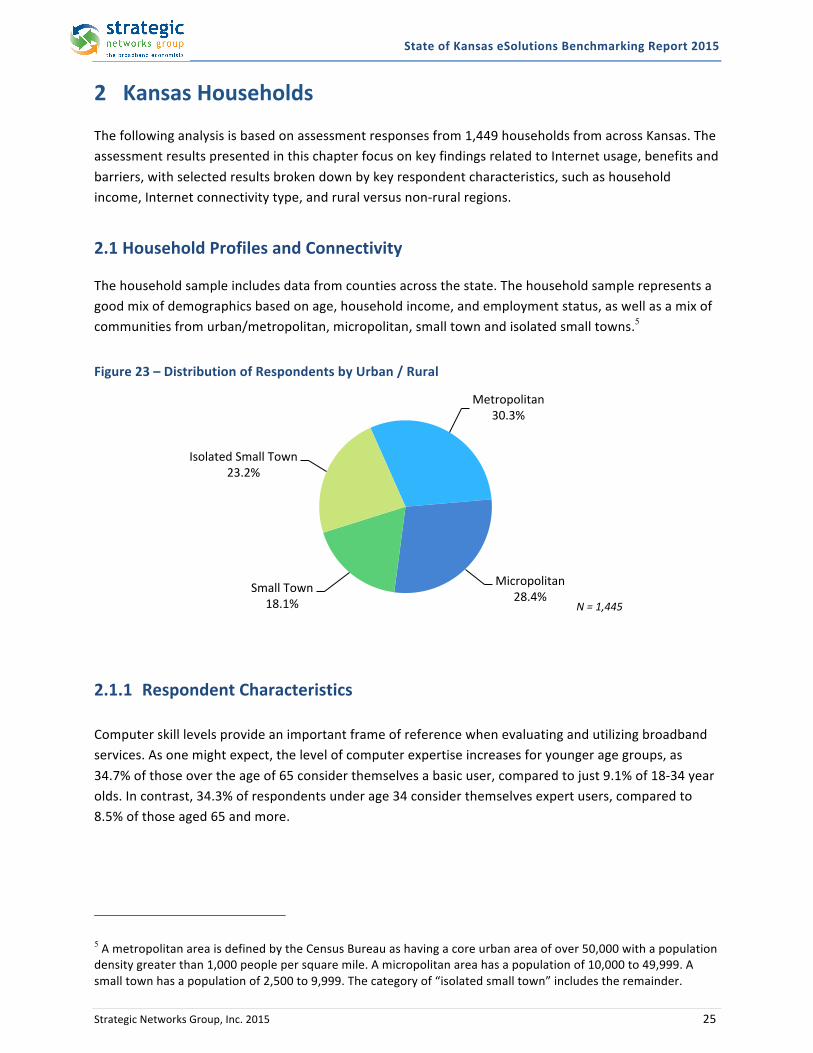

The household sample includes data from counties across the state. The household sample represents a good mix of demographics based on age, household income, and employment status, as well as a mix of communities from urban/metropolitan, micropolitan, small town and isolated small towns.5

Figure 23 – Distribution of Respondents by Urban / Rural

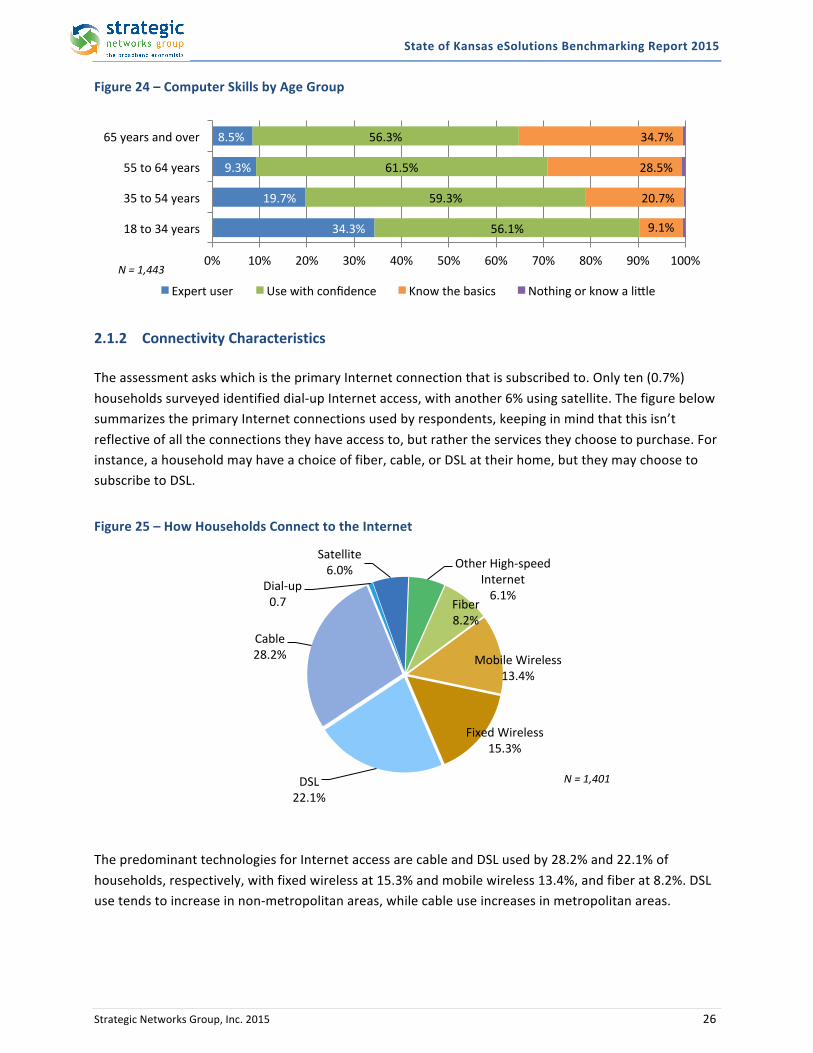

2.1.1 Respondent Characteristics Computer skill levels provide an important frame of reference when evaluating and utilizing broadband services. As one might expect, the level of computer expertise increases for younger age groups, as 34.7% of those over the age of 65 consider themselves a basic user, compared to just 9.1% of 18-‐34 year olds. In contrast, 34.3% of respondents under age 34 consider themselves expert users, compared to 8.5% of those aged 65 and more.

5 A metropolitan area is defined by the Census Bureau as having a core urban area of over 50,000 with a population density greater than 1,000 people per square mile. A micropolitan area has a population of 10,000 to 49,999. A small town has a population of 2,500 to 9,999. The category of “isolated small town” includes the remainder.

Metropolitan 30.3%

Micropolitan 28.4%

Small Town 18.1%

Isolated Small Town 23.2%

N = 1,445

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 26

Figure 24 – Computer Skills by Age Group

2.1.2 Connectivity Characteristics The assessment asks which is the primary Internet connection that is subscribed to. Only ten (0.7%) households surveyed identified dial-‐up Internet access, with another 6% using satellite. The figure below summarizes the primary Internet connections used by respondents, keeping in mind that this isn’t reflective of all the connections they have access to, but rather the services they choose to purchase. For instance, a household may have a choice of fiber, cable, or DSL at their home, but they may choose to subscribe to DSL.

Figure 25 – How Households Connect to the Internet

The predominant technologies for Internet access are cable and DSL used by 28.2% and 22.1% of households, respectively, with fixed wireless at 15.3% and mobile wireless 13.4%, and fiber at 8.2%. DSL use tends to increase in non-‐metropolitan areas, while cable use increases in metropolitan areas.

34.3%

19.7%

9.3%

8.5%

56.1%

59.3%

61.5%

56.3%

9.1%

20.7%

28.5%

34.7%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

18 to 34 years

35 to 54 years

55 to 64 years

65 years and over

Expert user Use with confidence Know the basics Nothing or know a liple

N = 1,443

Dial-‐up 0.7%

Satellite 6.0% Other High-‐speed

Internet 6.1%

Fiber 8.2%

Mobile Wireless 13.4%

Fixed Wireless 15.3%

DSL 22.1%

Cable 28.2%

N = 1,401

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 27

Internet Access Speeds6 Households were provided the option to perform a speed test to measure the upload and download speeds of their connections. While only 4.8% (five households) recorded less than 768kbps on the download speed test, 29% of households recorded less than 768kbps on the upload speed test. The following charts provide a summary of the speed test results for download and upload speed ranges and average download and upload speed by connectivity type. The findings are also consistent with data reported on the NTIA Broadband Map site, which reports a median upload speed for households of 0.7 mbps and download speed of 4.4mbps http://www.broadbandmap.gov/summarize/state/kansas.

Figure 26 – Speed-‐Test Upload Results for Households

Figure 27 – Speed-‐Test Download Results for Households

6 Speed test results should be used with great care. Different broadband mapping exercises have produced markedly different results, largely because they measure different outputs. Key points to keep in mind in using speed test data from this assessment include the measured actual upload and download speeds at the time the test was taken. Most broadband mapping exercises report speeds available in these same areas. Many consumers purchase Internet service with less than the maximum available speed, usually due to cost. Moreover, reported available speeds often reflect the maximum speed in a larger geographic area, not necessarily the speed available at that specific location.

2.8%

26.2%

23.6%

13.0%

15.8%

10.6%

7.1%

0.5%

0.4%

Less than 200 kbps

200 kbps up to 768 kbps

768 kbps up to 1.5 mbps

1.5 mbps up to 3 mbps

3 mbps up to 6 mbps

6 mbps up to 10 mbps

10 mbps up to 25 mbps

25 mbps up to 50 mbps

50 mbps or more

0% 5% 10% 15% 20% 25% 30% N = 576

4.8% 7.5%

11.7% 19.7%

14.6% 26.5%

7.8% 6.8%

0.7%

Less than 768 kbps 768 kbps up to 1.5 mbps 1.5 mbps up to 3 mbps 3 mbps up to 6 mbps

6 mbps up to 10 mbps 10 mbps up to 25 mbps 25 mbps up to 50 mbps 50 mbps up to 100 mbps 100 mbps up to 1 gbps

0% 5% 10% 15% 20% 25% 30% N = 589

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 28

For residential service, cable connectivity provides the fastest access, followed by fiber and mobile wireless. No dial-‐up respondents took the speed test, but dial-‐up is logically the slowest access choice, followed by satellite.

Figure 28 -‐ Speed (Megabits per second) by Connection Type

Internet Costs The median cost for household Internet access fell into the $50-‐$60 range. The median DSL and Fixed Wireless cost fell into the $40 to $50 range, while satellite fell in to the $60 to $70 range. The monthly costs for Internet service tends to be similar in rural versus non-‐rural areas. Internet Reliability and Satisfaction Levels Households were asked to rate how well their current Internet service meets their needs in terms of speed, reliability and value. Fiber has by far the best reliability of the broadband connection options. Cable, DSL and fixed wireless are comparable in terms of meeting household needs and expectations for speed, reliability and value. Reliability is generally poor for both dial-‐up and satellite Internet, with each contributing to poor ratings on price/value expectations. Satellite service shows occasional or frequent problems by 57.3% of households that subscribe to satellite, while dial-‐up also proves to be the most problematic with occasional or frequent problems cited by 62.5% of the 8 dial-‐up households, with none describing reliability as “always excellent.”

5.5

8.0

9.6

9.7

11.4

25.0

0.9

2.0

4.5

2.4

4.9

5.4

0 5 10 15 20 25 30

Satellite

DSL

Mobile Wireless

Fixed Wireless

Fiber

Cable

Ave. Upload (mbps) Ave. Download (mbps) N = 542

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 29

2.2 Broadband Utilization and Benefits

2.2.1 Broadband Utilization Households were asked about their current uses of the Internet as well as their planned use over the next 12 months. This report focuses primarily on household utilization in the productivity category7. Households were asked about how they use the Internet for personal productivity for:

• Educational or training courses (remote learning or supplemental courses from home) • Accessing workplace from home (occasional use) • Teleworking (formal workplace all or part of normal work hours) • Home-‐based business (full-‐time or part-‐time)

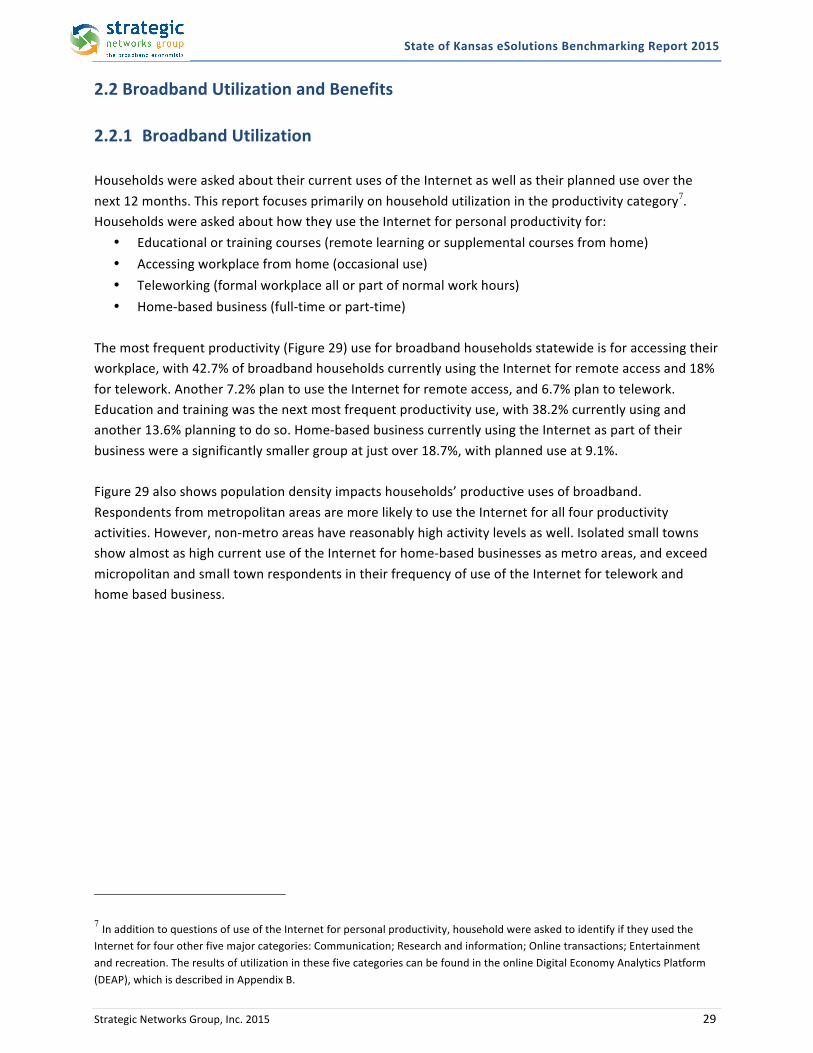

The most frequent productivity (Figure 29) use for broadband households statewide is for accessing their workplace, with 42.7% of broadband households currently using the Internet for remote access and 18% for telework. Another 7.2% plan to use the Internet for remote access, and 6.7% plan to telework. Education and training was the next most frequent productivity use, with 38.2% currently using and another 13.6% planning to do so. Home-‐based business currently using the Internet as part of their business were a significantly smaller group at just over 18.7%, with planned use at 9.1%. Figure 29 also shows population density impacts households’ productive uses of broadband. Respondents from metropolitan areas are more likely to use the Internet for all four productivity activities. However, non-‐metro areas have reasonably high activity levels as well. Isolated small towns show almost as high current use of the Internet for home-‐based businesses as metro areas, and exceed micropolitan and small town respondents in their frequency of use of the Internet for telework and home based business.

7 In addition to questions of use of the Internet for personal productivity, household were asked to identify if they used the Internet for four other five major categories: Communication; Research and information; Online transactions; Entertainment and recreation. The results of utilization in these five categories can be found in the online Digital Economy Analytics Platform (DEAP), which is described in Appendix B.

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 30

Figure 29 – Broadband Productivity Uses by Community Population Density

Higher population density linked to the use of the Internet to telecommute and access the workplace, speaks to the power of broadband being an equalizer of opportunity. Unfortunately, households in rural areas are more likely to be limited to dial-‐up connectivity and some productivity activities simply cannot be realized with dial-‐up. SNG data collected from multiple states over the last four years shows that there is a very significant difference in utilization between dial-‐up and broadband users. For these users, the lack of broadband becomes a meaningful impediment to practical Internet benefits to personal and household efficiencies and productivity. Lower quality dial-‐up connectivity has a major negative impact on a household’s productive use of the Internet. In all instances, significant percentages of broadband households are more productive in specific areas over their dial-‐up counterparts. SNG multi-‐state data indicate that many dial-‐up customers would plan to use more productive activities if they had broadband available for use. This indicates a level of awareness and latent demand for personal productivity uses through broadband.

25.4%

16.5%

9.4%

16.3%

21.5%

16.5%

16.3%

19.5%

54.1%

40.1%

36.9%

34.9%

42.2%

38.5%

36.5%

34.2%

7.9%

5.4%

6.4%

6.8%

8.1%

8.0%

8.2%

12.4%

6.4%

4.7%

8.2%

10.7%

13.1%

13.2%

17.6%

12.1%

0% 10% 20% 30% 40% 50% 60% 70%

Metropolitan

Micropolitan

Small Town

Isolated Small Town

Metropolitan

Micropolitan

Small Town

Isolated Small Town

Metropolitan

Micropolitan

Small Town

Isolated Small Town

Metropolitan

Micropolitan

Small Town

Isolated Small Town

Teleworking

Home bu

siness

Accessing workplace E

ducaio

n/training

Percent of Households

Currently use Plan to use N = 1,332

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 31

2.2.2 Mobile Uses As with businesses and other organizations, the impact of mobile Internet on households is important to recognize. During the online assessment, households were asked to respond to questions to think about the services and applications used most with their mobile devices. The results are in Figure 30 below.

Figure 30 -‐ Types of Mobile Applications use by Households

2.2.2.1 Online Transactions and Spending The survey reveals that:

• 63% of households spending more than $500 per year online • 92.5% of broadband households use the Internet to purchase goods and services online

o 68.7% of these households conducting more than 10 purchase transactions per year While on the topic of online purchases, mobile is becoming a growing segment of the digital economy. Households that own at least one mobile device were asked what percentage of online purchases they make through a mobile device. Interestingly, over 70% of mobile users have made an online purchase with their mobile device. Additionally, over 43% of households with mobile device say they used their mobile device to purchase from a business for the first time.

2.2.2.2 Home-‐based Business One somewhat surprising finding was the percentage of households that generated income over the Internet, particularly through a home-‐based business. Of particular interest is that 18.7% of broadband households stated that they currently operate a home-‐based business. These households were further asked if they operate a home-‐based business under the following definition:

43.6%

43.9%

49.2%

71.3%

71.3%

76.7%

11.1%

11.2%

12.3%

11.1%

9.9%

7.4%

45.3%

44.8%

38.5%

17.6%

18.8%

15.9%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Write review or share product opinions

Applicaions needed for work

Pay for goods or services on the spot

Compare prices or reviews while shopping

Order goods or services online

Find service close to locaion

Currently use Plan to use No plan to use N = 1,202

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 32

“A home-‐based business may be part-‐time or full-‐time activity by one or more household members that operate their business exclusively from home. This may include self-‐employed professionals and many other types of entrepreneurial business activities.”

Using this tighter definition, 13.1% of households surveyed operate a home-‐based business. Based on this more precise definition, 70% of the original 18.7% of respondents who initially stated that they ran a home-‐based business confirmed operating a home-‐based business using broadband. Taking this further, 37.4% of home businesses (narrowly defined) strongly agree that they would not be in business without the Internet, and 23.6% would need to relocate to get broadband if it was not available. A vast majority (88.5%) of home-‐based businesses agree broadband is essential for their business to function. The most frequent uses for home-‐based businesses are Online Banking and Research, which are each used by over 80% of home-‐based businesses. Over half (54.9%) of home businesses have a business website, while a majority of home businesses currently use the Internet as a tool for making day-‐to-‐day operations easier and making more effective use of their resources (productivity). Home-‐based businesses are more likely to sell online (61.7%) compared to all businesses (52.6%).

Figure 31 – Home-‐based Business Uses of the Internet

2.2.2.3 Teleworking In response to questions concerning use of the Internet for personal productivity 18% of households stated that teleworking is currently practiced. These households were further asked if one or more household member’s telework under the following definition:

54.9%

60.0%

60.0%

61.7%

63.4%

70.3%

70.3%

76.0%

83.4%

85.1%

11.4%

8.6%

7.4%

6.3%

11.4%

8.6%

6.9%

3.4%

2.9%

6.3%

8.0%

12.0%

8.6%

5.7%

8.0%

5.1%

6.9%

3.4%

4.6%

2.9%

25.7%

19.4%

24.0%

26.3%

17.1%

16.0%

16.0%

17.1%

9.1%

5.7%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Website

Adverising

Supplier Communicaion

Online Sales

Skills Development

Customer Service

Document Transfer

Online Purchasing

Research

Online Banking

Currently use Plan to use No plan to use Not applicable N = 1,190

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 33

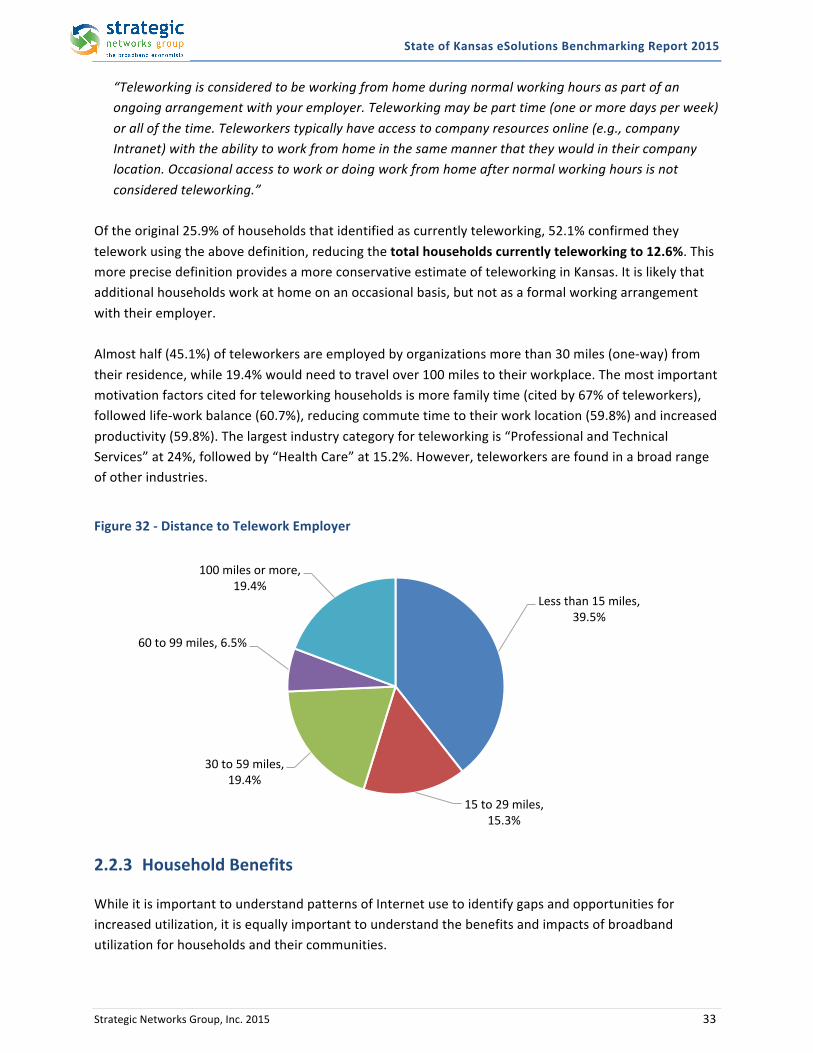

“Teleworking is considered to be working from home during normal working hours as part of an ongoing arrangement with your employer. Teleworking may be part time (one or more days per week) or all of the time. Teleworkers typically have access to company resources online (e.g., company Intranet) with the ability to work from home in the same manner that they would in their company location. Occasional access to work or doing work from home after normal working hours is not considered teleworking.”

Of the original 25.9% of households that identified as currently teleworking, 52.1% confirmed they telework using the above definition, reducing the total households currently teleworking to 12.6%. This more precise definition provides a more conservative estimate of teleworking in Kansas. It is likely that additional households work at home on an occasional basis, but not as a formal working arrangement with their employer. Almost half (45.1%) of teleworkers are employed by organizations more than 30 miles (one-‐way) from their residence, while 19.4% would need to travel over 100 miles to their workplace. The most important motivation factors cited for teleworking households is more family time (cited by 67% of teleworkers), followed life-‐work balance (60.7%), reducing commute time to their work location (59.8%) and increased productivity (59.8%). The largest industry category for teleworking is “Professional and Technical Services” at 24%, followed by “Health Care” at 15.2%. However, teleworkers are found in a broad range of other industries.

Figure 32 -‐ Distance to Telework Employer

2.2.3 Household Benefits

While it is important to understand patterns of Internet use to identify gaps and opportunities for increased utilization, it is equally important to understand the benefits and impacts of broadband utilization for households and their communities.

Less than 15 miles, 39.5%

15 to 29 miles, 15.3%

30 to 59 miles, 19.4%

60 to 99 miles, 6.5%

100 miles or more, 19.4%

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 34

To provide a perspective on the overall importance of broadband, households were asked, “Assuming you could never get broadband service, how likely is it that you would leave to relocate to a community that offers broadband?” Nearly one in three (30.9%) would relocate to another community if they needed access to broadband services. This breaks out as 13.5% of households saying they would definitely relocate with 17.4% saying relocation would be “very likely.” Households were also asked to rate the significance of the Internet for achieving the following household benefits:

• Improves knowledge and skills (through online education and/or research) • Enhances ability to earn additional income • Enhances school learning (through research and study) • Enhances awareness of what is happening in the community • Supports better balance of personal and work time • Supports choice of living location (e.g., for selecting or remaining in your community)

The following figure shows the perceived benefits of using the Internet for households.

Figure 33 – Significance of Broadband for Household Benefits

2.3 Barriers and Adoption Issues The data collected examines how households can get the most out of broadband by looking at their aspirations, barriers to achieving aspirations, and how they can acquire the skills to overcome those barriers. The first question is whether households are satisfied with their current level of Internet use, including the level of benefits they derive from using the Internet. 58.1% of household respondents want to increase their level of Internet use, while 40.2% feel their current level of use is about right, with only 1.7% desiring to reduce their use. With over half of all households wishing to increase or improve their use of the Internet, the next question is “what barriers do they see in striving to achieve that objective.” As seen in Figure 34, the two main barriers are concerns over privacy and security (50.5%) followed by an inadequate Internet

27.0%

32.4%

33.1%

38.4%

40.6%

56.4%

22.6%

31.5%

21.0%

41.3%

26.4%

30.6%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Addiional income

Life-‐work balance

Choice of locaion

Connecing with community

School learning

Knowledge and skills

Very Important Somewhat Important N = 1,280

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 35

connection (48% of households say this is a very important barrier). While speed is not a top barrier for utilization for businesses (number 7 barrier with 34% citing), it is clear that the “need for speed” is felt and recognized by households. Lack of skills or knowledge and awareness of online benefits is a far smaller group, with over two thirds of households reporting those are not important or applicable issues.

Figure 34 – Barriers to Enhanced Use of the Internet

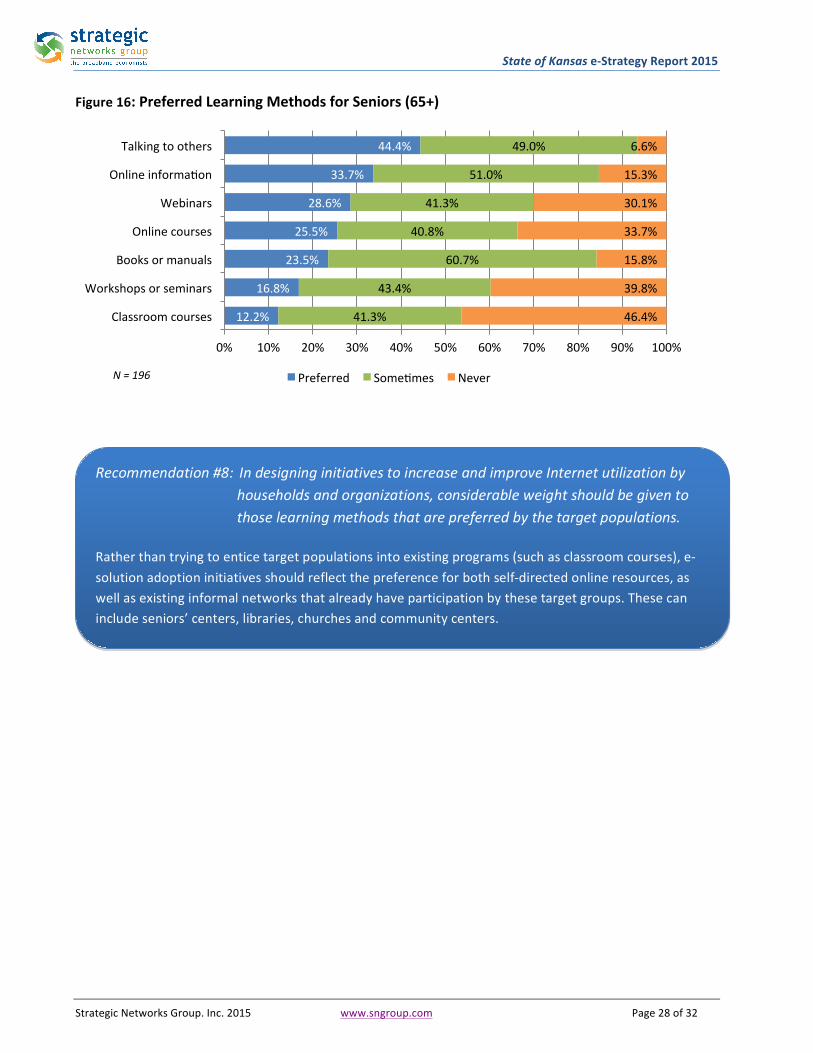

For those 30% of households interested in increasing their skill levels, the preferred learning methods, as seen in Figure 35, are self-‐directed, either by accessing online resources or talking with other people who have experience. The least favored methods are formal classroom activities. These statistics are important for initiatives designed to deliver training and support to households for increasing broadband utilization. In particular, providing access to online training would be favored by an overwhelming percentage of households, while also being a cost-‐effective method for delivering information and support for using broadband services.

Figure 35 – Preferred Means for Increasing Broadband Skills

10.1%

13.8%

22.2%

48.0%

50.5%

20.6%

27.4%

44.3%

29.5%

32.1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Lack of skills

Awareness of Internet benefits

Not enough ime

Connecion speed or reliability

Privacy and security concerns

Very Important Somewhat Important N = 733

19.2%

20.2%

24.5%

37.9%

41.0%

48.9%

49.9%

42.7%

43.5%

56.1%

39.4%

40.6%

43.0%

41.3%

38.1%

36.3%

19.3%

22.6%

18.4%

8.1%

8.8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Classroom courses

Workshops or seminars

Books or manuals

Online courses

Webinars

Talking to others

Online informaion

Preferred Someimes Never N = 1,263

State of Kansas eSolutions Benchmarking Report 2015

Strategic Networks Group, Inc. 2015 36

3 Benchmarks This report includes comparisons of Internet use between regions by various characteristics, such as industry, business size, and household demographics. To assist in the process of making comparisons, a mechanism was developed for establishing benchmarks. Benchmarks are useful in creating reference points against which the performance of any individual or group can be compared. Strategic Networks Group has developed a benchmarking process based on its Digital Economy index (DEi).