State of the U.S. Multifamily...

54

State of the U.S. Multifamily Market Q1 2015 Review and Forecast

-

Upload

phungthuan -

Category

Documents

-

view

218 -

download

1

Transcript of State of the U.S. Multifamily...

State of the U.S. Multifamily Market

Q1 2015 Review and Forecast

• Economy

• Leasing Fundamentals

• Rent and NOI Trends

• Single-Family Market

• Capital Markets

Agenda

page 3

Economy

page 4

GDP Growth

Contributions To GDP Growth

08

08

08

08

09

09

09

09

Sources: Moody's Analytics; BEA; CoStar Portfolio Strategy As of 15Q1

(15%)

(10%)

(5%)

0%

5%

10%

08 09 10 11 12 13 14 15

Consumption Business Investment Residential Investment

Change in Inventories Exports Imports

Government Total GDP

Contribution to GDP Growth

page 5

Employment Growth

Total Nonfarm Employment

Sources: Moody's Analytics; BLS; CoStar Portfolio Strategy As of May 2015

(6%)

(5%)

(4%)

(3%)

(2%)

(1%)

0%

1%

2%

3%

4%

(900)

(750)

(600)

(450)

(300)

(150)

0

150

300

450

600

05 06 07 08 09 10 11 12 13 14 15

Jobs Gained/Lost Growth (Y/Y)

Monthly Jobs Gained / Lost 3-Month Moving Average Growth (Y/Y)

page 6

Employment For Prime Renters

Labor Force Participation Rate And Unemployment Rate Of Young

People Year

99

99

99

99

00

00

00

00

01

0101

01

02

02

02

02

03

03

03

03

04

04

04

04

05

05

05

05

06

06

06

Sources: Census Bureau; BLS; CoStar Portfolio Strategy As of 15Q1

62%

63%

64%

65%

66%

67%

68%

0%

2%

4%

6%

8%

10%

12%

14%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Labor Force Participation Rate 20-34 Years Old Unemployment Rate

20 Years And Over Unemployment Rate

Unemployment Rate Labor Force Participation Rate

page 7

Employment To Population Ratio And Labor Force Participation Rate

Of 25-34 Year Olds

04

04

04

04

04

04

04

04

04

04

04

04

05

05

05

05

05

05

05

05

05

05

05

05

06

06

06

06

06

06

Sources: Bureau of Labor Statistics; U.S. Census Bureau As of 15Q1

70%

72%

74%

76%

78%

80%

82%

84%

86%

04 05 06 07 08 09 10 11 12 13 14 15

Employment To Population Ratio Labor Force Participation Rate

Employment To Population Ratio & Labor Force Participation Rate

Labor Participation and Employment-Population Trends

page 8

Labor Participation and Employment-Population Trends

Employment To Population Ratio And Labor Force Participation Rate

Of 20-24 Year Olds

04

04

04

04

04

04

04

04

04

04

04

04

05

05

05

05

05

05

05

05

05

05

05

05

06

06

06

06

06

06

Sources: Bureau of Labor Statistics; U.S. Census Bureau As of 15Q1

58%

60%

62%

64%

66%

68%

70%

72%

74%

76%

78%

04 05 06 07 08 09 10 11 12 13 14 15

Employment To Population Ratio Labor Force Participation Rate

Employment To Population Ratio & Labor Force Participation Rate

page 9

Part-Time Employment

20-24 Year Old Full-Time Vs. Part-Time Employment

Year

00

00

00

00

01

01

01

01

02

0202

02

03

03

03

Sources: Census Bureau; BLS; CoStar Portfolio Strategy As of 15Q1

*Four-quarter average

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

2,000

4,000

6,000

8,000

10,000

12,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

20-24 Years Old Full-Time Workers 20-24 Years Old Part-Time Workers

20-24 % Part-Time

Number of Workers* (000s) % of Workers Part-Time

page 10

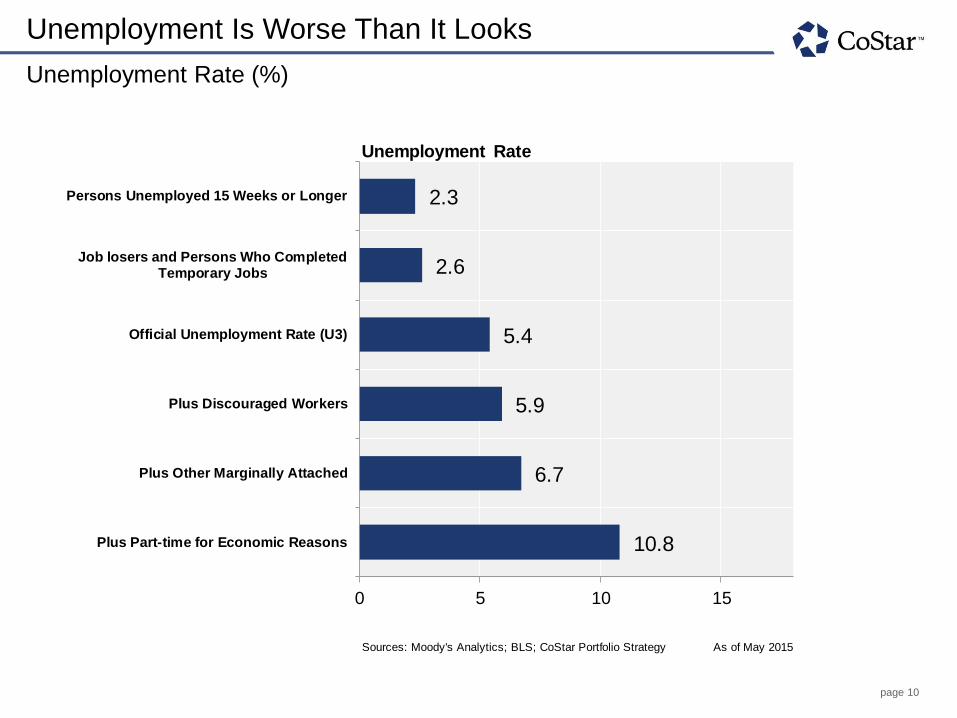

Unemployment Is Worse Than It Looks

Unemployment Rate (%)

Sources: Moody's Analytics; BLS; CoStar Portfolio Strategy As of May 2015

10.8

6.7

5.9

5.4

2.6

2.3

0 5 10 15

Plus Part-time for Economic Reasons

Plus Other Marginally Attached

Plus Discouraged Workers

Official Unemployment Rate (U3)

Job losers and Persons Who CompletedTemporary Jobs

Persons Unemployed 15 Weeks or Longer

Unemployment Rate

page 11

Leasing Fundamentals

page 12

Entering The Late Stages Of the Apartment Cycle

Real Estate Cycle Placement In 54 National Index Markets By Property Type

OCC

RENT

OCC

RENT

OCC

RENT

OCC

RENT

Source: CoStar Portfolio Strategy As of 15Q1

Recovery Early Expansion Late Expansion Contraction

Occupancy

Rent

Retail 52 2

Light Industrial 53 1

Logistics 40 13 1

Office 1 47 6

Apartment 7 47

page 13

Supply Coming But Vacancies Are Tight

National Apartment Supply, Demand, and Vacancy

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

13

14

15

16

17

Source: CoStar Portfolio Strategy As of 15Q1

3%

4%

5%

6%

7%

8%

0

50

100

150

200

250

300

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Demand Change (Y/Y) Supply Change (Y/Y) Vacancy

Demand & Supply (000s Units) Vacancy

page 14

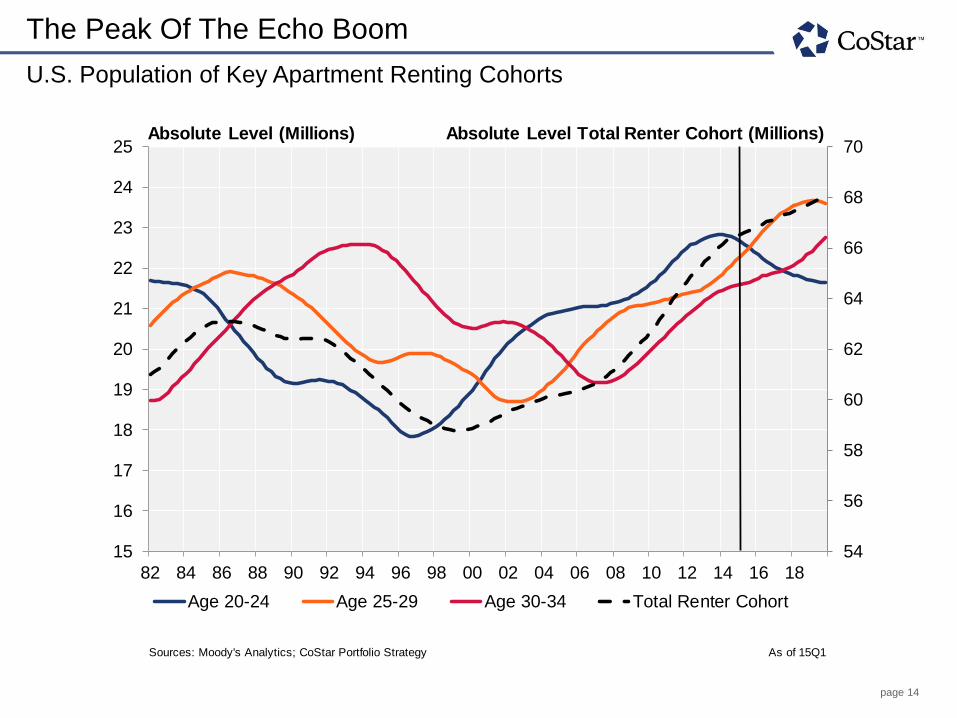

The Peak Of The Echo Boom

U.S. Population of Key Apartment Renting Cohorts

82

82

82

82

83

83

83

83

84

84

84

84

85

85

85

85

86

86

86

86

87

87

87

87

88

88

88

Sources: Moody's Analytics; CoStar Portfolio Strategy As of 15Q1

54

56

58

60

62

64

66

68

70

15

16

17

18

19

20

21

22

23

24

25

82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

Age 20-24 Age 25-29 Age 30-34 Total Renter Cohort

Absolute Level (Millions) Absolute Level Total Renter Cohort (Millions)

page 15

If You’re Under 40, Good Luck Getting A Loan…

Loans Serviced By Credit Score And Average Credit Scores By Age

Sources: U.S. Federal Housing Finance Agency (FHFA); FreeScore.com; Costar Group, Inc. As of 15Q1

1,750

1,950

2,150

2,350

2,550

2,750

2,950

3,150

3,350

08Q1 09Q1 10Q1 11Q1 12Q1 13Q1 14Q1

Fannie Mae - Total Loans Serviced With Original Credit Score < 660

Conforming Home Loans Serviced ('000s)

600

620

640660680

700

720740

18-29 30-39 40-49 50-59 60-69 70+

Avg Credit Score By Age (Years)

Credit Score

654

637

page 16

Young People Still Underemployed

Change In Population And Employment By Age Cohort (20-34-Year-Olds)

3/31/2000

6/30/2000

9/30/2000

12/31/2000

3/31/2001

6/30/2001

9/30/2001

12/31/2001

3/31/2002

6/30/2002

9/30/2002

12/31/2002

3/31/2003

6/30/2003

9/30/2003

12/31/2003

3/31/2004

6/30/2004

9/30/2004

12/31/2004

3/31/2005

6/30/2005

9/30/2005

12/31/2005

3/31/2006

6/30/2006

Sources: BLS; Moody's Analytics; CoStar Portfolio Strategy As of 14Q4

(4,000)

(3,000)

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

5,000

07 08 09 10 11 12 13 14

People Employed Employed at Normal Participation Rate

Cumulative Change in Population and Employed (000s)

If labor force participation rate (71.9%) returns to historical norm (75%), there is a potential increase of

2 million employed people in primary-renting demographic.

page 17

Starts Continue To Climb To Historical Levels

U.S. Multifamily Starts and Permits

Sources: U.S. Census; Moody's Analytics; CoStar Portfolio Strategy As of 15Q1

0

50

100

150

200

250

83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15

Multifamily StartsMultifamily PermitsMultifamily Starts Historical Average (83-Present)

Starts and Permits (000s)

page 18

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2016 (14Q4-16Q4)

Rank

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Source: CoStar Portfolio Strategy As of 15Q1

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000N

ew

York

Da

llas -

FW

Washin

gto

n, D

C

Sea

ttle

Atlan

ta

De

nver

Los A

ngele

s

Austin

Pho

enix

Bosto

n

San

An

tonio

Ch

arlotte

Ch

icago

Orlando

Port

land

Min

nea

polis

San

Jo

se

Na

sh

vill

e

Mia

mi

San

Fra

ncis

co

Phila

delp

hia

Ora

ng

e C

ounty

Tam

pa

Ra

leig

h

San

Die

go

Completions As A % Of Inventory

South East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 19

North Of The Line: Most Markets Forecast To Oversupply

Change in Near Term (15Q1-16Q1) Supply and Demand

Cleveland

Hartford

Chicago

Cincinnati

Memphis

Detroit

St. Louis

New York

San Diego

East Bay

Honolulu

Milwaukee

Richmond

Baltimore

Miami

Pittsburgh

Tampa

San Jose

Phoenix

Source: CoStar Portfolio Strategy As of 15Q1

Atlanta

Austin

Baltimore

Boston

Charlotte

ChicagoCincinnati

Cleveland

Dallas - Fort Worth

Denver

East Bay

Houston

Los Angeles

Miami

Milwaukee

Nashville

New York

Orange County

Orlando

Philadelphia Phoenix

Pittsburgh

Portland, OR

Raleigh

St. Louis

Salt Lake City

San Antonio

San Diego

San Francisco

San Jose

Seattle

Washington, DC

0%

1%

2%

3%

4%

5%

6%

0% 1% 2% 3% 4% 5%

Change in Supply

Change in Demand

South East Midwest West

page 20

Supply Putting Upward Pressure Most Places

Vacancy Changes In Coming 12 Months

54

53

52

51

50

49

48

47

46

45

44

43

42

41

40

39

38

37

36

35

34

33

32

31

30

29

28

Source: CoStar Portfolio Strategy As of 15Q1

(50)

0

50

100

150

200

250

300D

etr

oit

No

rfolk

Ne

w O

rlean

sO

rang

e C

ounty

Sacra

mento

Baltim

ore

San

Fra

ncis

co

Jacksonvill

eS

ain

t Louis

Ho

nolu

luE

ast

Bay

Mem

phis

India

na

polis

San

Die

go

Inla

nd E

mpire

Co

lum

bus O

HLas V

egas

Long I

sla

nd

Los A

ngele

sD

alla

s -

FW

Min

nea

polis

Ra

leig

hN

ort

hern

NJ

San

Jose

Ha

rtfo

rdP

hila

delp

hia

Ch

icago

Port

land

Cle

vela

nd

Pho

enix

Ne

w Y

ork

Tam

pa

Kan

sas C

ity

Bosto

nS

alt L

ake

City

Ric

hm

ond

Ch

arlotte

Palm

Be

ach C

ounty

Mia

mi

Na

shvill

eC

incin

nati

San

An

tonio

Atlan

taF

ort

Laud

erd

ale

Okla

hom

a C

ity

Sea

ttle

Pitts

burg

hA

ustin

Orlando

Milw

aukee

De

nve

rW

ashin

gto

n, D

CS

tam

ford

Ho

usto

n

One Year Vacancy Change (BPS)

South East Midwest West

page 21

Vacancies Will Remain Tighter In West Coast Markets

Regional Vacancy Rates

Source: CoStar Portfolio Strategy As of 15Q1

2%

3%

4%

5%

6%

7%

8%

9%

10%

01 03 05 07 09 11 13 15

East South Midwest West National Index

Vacancy Rate

page 22

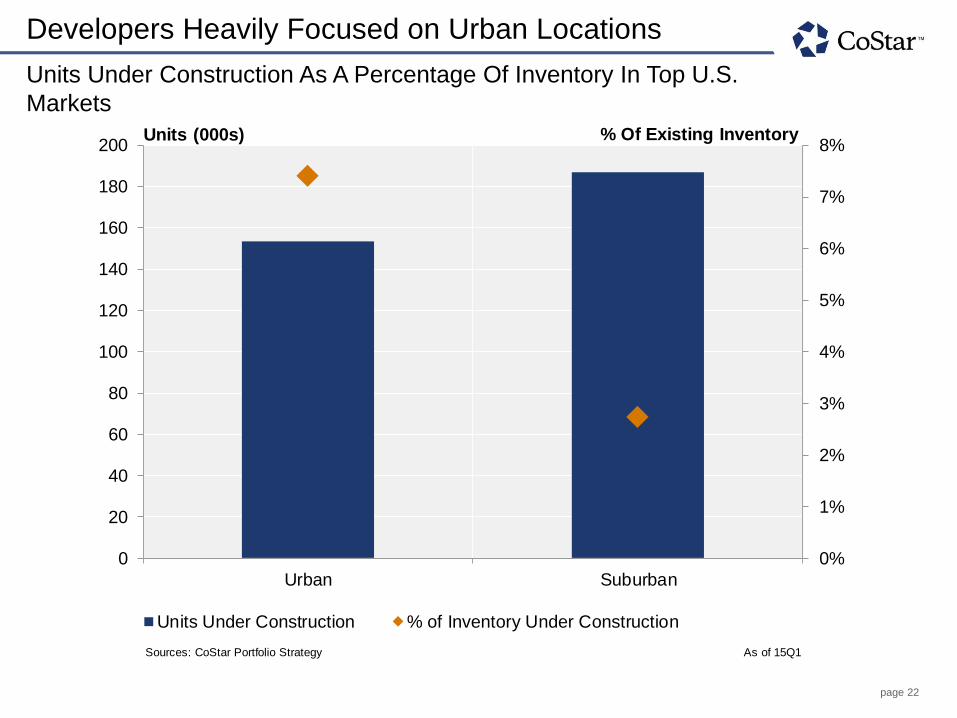

Developers Heavily Focused on Urban Locations

Units Under Construction As A Percentage Of Inventory In Top U.S.

Markets

Urban

Suburban

CBD

Suburban

Sources: CoStar Portfolio Strategy As of 15Q1

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

20

40

60

80

100

120

140

160

180

200

Urban Suburban

Units (000s)

Units Under Construction % of Inventory Under Construction

% Of Existing Inventory

page 23

Vacancies In 3 Star Properties Still Tightening

Change In Vacancy By Star Over Last 2 Years By Star Rating

Building Rating

Row Labels

3/31/2013

3/31/2015

Grand Total

0.071755414

Source: CoStar Portfolio Strategy As of 15Q1

(0.6%)

(0.4%)

(0.2%)

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

4 & 5 Star 3 Star 1 & 2 Star

Y/Y Change in Vacancy

Vacancy Change

page 24

New Deliveries Pushing Vacancies In Many Metros

Vacancy Rate By Star Rating

Source: CoStar Portfolio Strategy As of 15Q1

0% 2% 4% 6% 8%

4&5 Star 3 Star

Orange County

Minneapolis

Phoenix

Seattle

Atlanta

East Bay

Dallas - FW

Detroit

Change in Vacancy Rate by Rating, 13Q1-15Q1

Philadelphia

Washington DC

Boston

Houston

Austin

Denver

Chicago

Los Angeles

San Francisco

New York

San Diego

Miami

page 25

Rent and NOI Trends

page 26

Some Markets Are Now Very Expensive

Current Asking Rents As A % Of Prerecession Peak

Rank

1

2

3

4

9

10

11

12

13

15

16

18

19

21

22

24

25

29

34

35

36

38

39

41

45

46

47

50

52

53

54

Source: CoStar Portfolio Strategy As of 15Q1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

90%

95%

100%

105%

110%

115%

120%

125%

130%

135%S

an

Fra

ncis

co

San

Jose

De

nver

East

Bay

Sea

ttle

Mia

mi

Ho

usto

n

Los A

ngele

s

San

Die

go

Bosto

n

Okla

hom

a C

ity

Da

llas -

FW

Da

llas -

Fort

Wort

h

Baltim

ore

Min

nea

polis

Ora

ng

e C

ounty

Ch

icago

Fort

Laud

erd

ale

Cle

vela

nd

Washin

gto

n, D

C

Atlan

ta

Milw

aukee

Sacra

mento

Inla

nd E

mpire

Ne

w Y

ork

Orlando

Ric

hm

ond

Pho

enix

No

rthern

New

Jers

ey

Sta

mfo

rd

Las V

egas

Rent As A % Of Prerecession Peak Current Rent

Rent As A % Of Prerecession Peak

South East Midwest West

Asking Rent ($)

page 27

Rent Growth Slowing Across Market Tiers

Y/Y Effective Rent Growth By Tier (National Index)

01

01

01

01

02

02

02

02

03

03

03

03

04

04

04

04

05

05

05

05

06

06

06

06

Source: CoStar Portfolio Strategy As of 15Q1

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

10 11 12 13 14 15 16

Primary Secondary Tertiary

Effective Rent Growth (Y/Y)

page 28

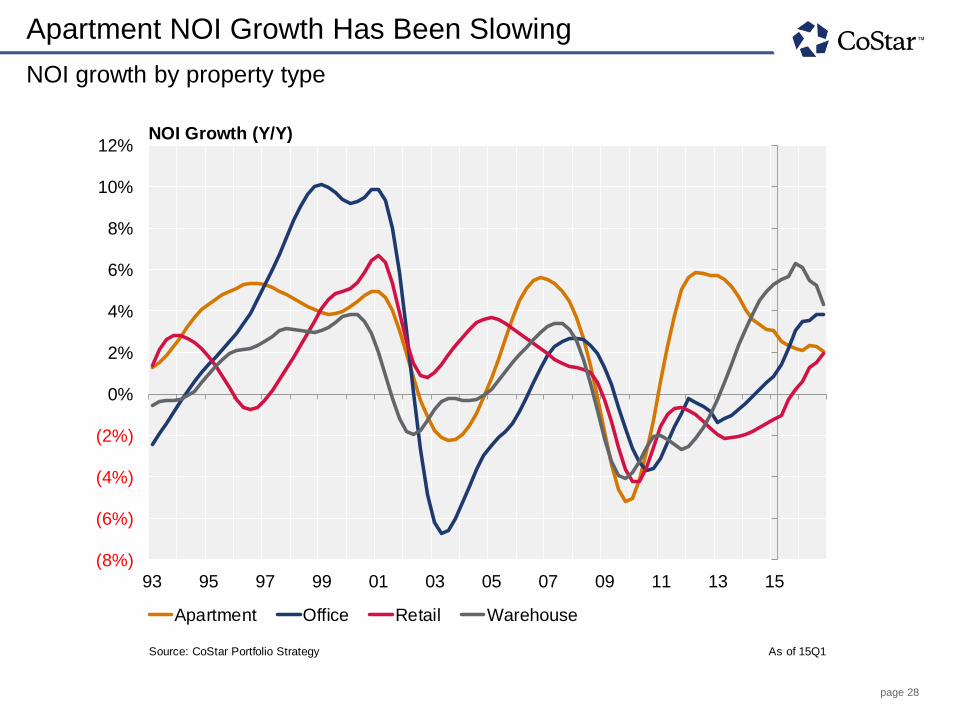

Apartment NOI Growth Has Been Slowing

NOI growth by property type

Metro Name

NOI Index YOY - Metro

Row Labels

3/31/1982

6/30/1982

9/30/1982

12/31/1982

3/31/1983

6/30/1983

9/30/1983

12/31/1983

3/31/1984

6/30/1984

9/30/1984

12/31/1984

3/31/1985

6/30/1985

9/30/1985

12/31/1985

3/31/1986

6/30/1986

9/30/1986

12/31/1986

3/31/1987

6/30/1987

9/30/1987

12/31/1987

3/31/1988

6/30/1988

9/30/1988

12/31/1988

Source: CoStar Portfolio Strategy As of 15Q1

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

10%

12%

93 95 97 99 01 03 05 07 09 11 13 15

Apartment Office Retail Warehouse

NOI Growth (Y/Y)

page 29

Single-Family Market

page 30

Housing In Recovery Mode

Home Price Indices

12/31/1999

3/31/2000

6/30/2000

9/30/2000

12/31/2000

3/31/2001

6/30/2001

9/30/2001

12/31/2001

3/31/2002

Sources: Moody's Analytics; NAR; FHFA; Case-Shiller; U.S. Census Bureau; PPR As of 15Q1

0

1000

2000

3000

4000

5000

6000

7000

8000

80

100

120

140

160

180

200

220

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Starts NAR FHFA (Purchase Only) Case-Shiller 20-City

Index (2000 = 100) Quarterly Housing Starts (Thousands)

page 31

Home Prices Rebounding Across The Country

But Housing Market Varies By Metro

21345867

1113

9121014161517182019212223

Sources: Moody's Analytics; BLS; CoStar Portfolio Strategy As of 15Q1

*Average Median Home Price From 2006-2007

(50%)

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

40%A

ustin

Ho

usto

n

De

nver

Da

llas

Pitts

burg

h

Sa

n J

ose

Ra

leig

h

Sa

n F

ran

cis

co

Bo

sto

n

Ph

iladelp

hia

Se

att

le

Ora

ng

e C

ou

nty

Ea

st

Bay

Atlan

ta

Ne

w Y

ork

Wash

ing

ton

, D

.C.

Sa

n D

ieg

o

Lo

s A

nge

les

Ph

oe

nix

Ch

ica

go

Mia

mi

La

s V

ega

s

De

tro

it

Home Price - Current Relative to 2006-07 Level*

Home Price - Current Relative to 2006-07 Level

page 32

Housing Affordability

But Housing Affordability Still High

3/31/1970

6/30/1970

9/30/1970

12/31/1970

3/31/1971

6/30/1971

9/30/1971

12/31/1971

3/31/1972

6/30/1972

9/30/1972

12/31/1972

3/31/1973

6/30/1973

9/30/1973

12/31/1973

3/31/1974

6/30/1974

9/30/1974

12/31/1974

3/31/1975

6/30/1975

9/30/1975

12/31/1975

3/31/1976

6/30/1976

Sources: Moody's Analytics; NRA; CoStar Portfolio Strategy As of 15Q1

0

20

40

60

80

100

120

140

160

180

200

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Composite Housing Affordability Index, (Index, SA)

FHLMC: 30-Year Commitment Rate - Fixed Rate - National, (%, NSA)

FHLMC: 15-year fixed commitment rate, (%, NSA)

Interest Rates Housing Affordability Index

page 33

Signs Point To Continued Recovery

Housing Delinquencies, Foreclosures, And For-Sale Inventory

Delinquencies

6/30/1981

9/30/1981

12/31/1981

3/31/1982

6/30/1982

9/30/1982

12/31/1982

3/31/1983

6/30/1983

9/30/1983

12/31/1983

3/31/1984

6/30/1984

9/30/1984

12/31/1984

3/31/1985

Sources: BEA; Moody's Analytics; CoStar Portfolio Strategy As of May 2015

2

3

4

5

6

7

8

9

10

11

12

0%

2%

4%

6%

8%

10%

12%

84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

Months Supply of SF Homes DelinquenciesForeclosures Average SF Home Supply

Delinquencies and Foreclosures (% of Loans)Months Supply of Single-Family Homes

page 34

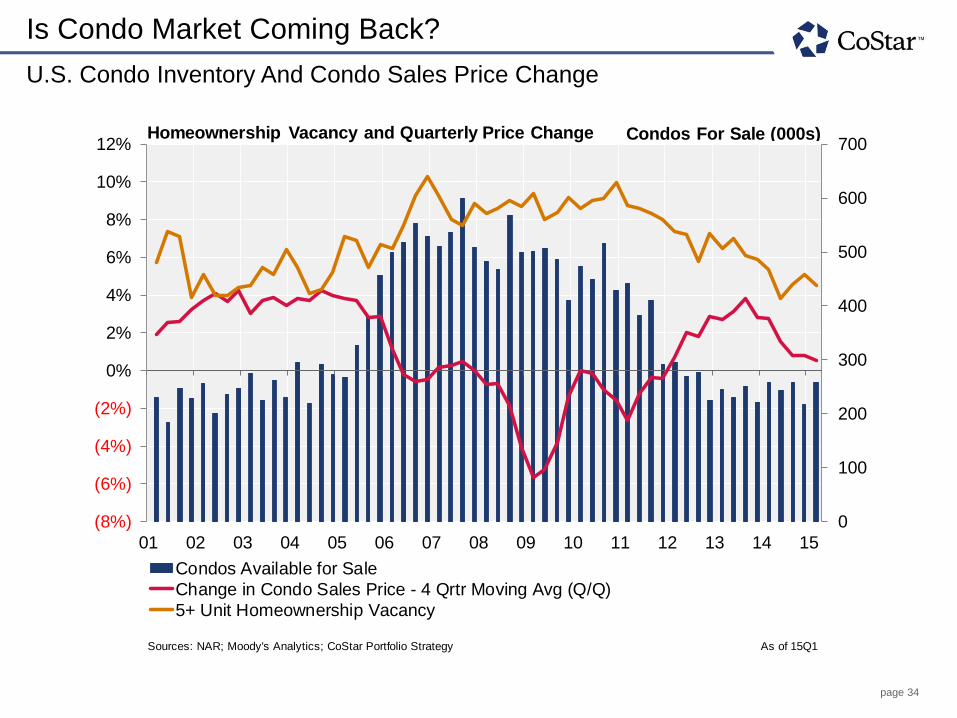

Is Condo Market Coming Back?

U.S. Condo Inventory And Condo Sales Price Change

Sources: NAR; Moody's Analytics; CoStar Portfolio Strategy As of 15Q1

0

100

200

300

400

500

600

700

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

10%

12%Homeownership Vacancy and Quarterly Price Change

Condos Available for Sale

Change in Condo Sales Price - 4 Qrtr Moving Avg (Q/Q)

5+ Unit Homeownership Vacancy

Condos For Sale (000s)

page 35

Homeownership Rate Continues To Decline

Homeownership Rate And Renter Occupied Households

65

65

66

66

66

66

67

67

67

67

68

68

68

68

69

69

69

69

70

70

70

70

71

71

71

Sources: Moody's Analytics; U.S. Census Bureau; CoStar Portfolio Strategy As of 15Q1

30

32

34

36

38

40

42

44

30

35

40

45

50

55

60

65

70

94 96 98 00 02 04 06 08 10 12 14

Renter Households Under 35 Years HO Rate U.S. HO Rate

Homeownership Rate (%) Renter Occupied Households (Millions)

page 36

Reasons Not To Own

FED Survey: Reason To Rent Or Own (Asked To Renters)

Other

Cheaper/More Convenient to Rent

Sources: Federal Reserve (2013 Survey of Consumer Finances); CoStar Portfolio Strategy As of 15Q1

0%

10%

20%

30%

40%

50%

60%

18-29 Years Old 30-44 Years Old 45-59 Years Old 60+ Years Old

Cheaper To Rent Than Own More Convenient To RentPlan On Moving In The Near Future Can't Qualify For A MortgageCan't Afford The Down Payment Simply Prefer To RentCurrently Looking To Buy

Percent of Respondents

page 37

Capital Markets

page 38

Volume Remains High

U.S. Quarterly Sales Volume

As Of 15Q1

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

12/31/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

5

10

15

20

25

30

35

40

05 06 07 08 09 10 11 12 13 14 15

Sales Volume Archstone Deal

Total Sales ($ Billions)

page 39

Volume Remains High; On Pace For Another Record Year

U.S. Quarterly Sales Volume

As Of 15Q1

12/31/200512/31/200612/31/200712/31/200812/31/200912/31/201012/31/201112/31/201212/31/201312/31/201412/31/2015

Source: CoStar Portfolio Strategy As Of 15Q1

$0

$20

$40

$60

$80

$100

$120

05 06 07 08 09 10 11 12 13 14 15

Sales Volume Year End 2015?

Total Sales ($ Billions)

?

page 40

Sales Volume by Tier

As Of 15Q1

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

5

10

15

20

25

30

35

40

08 09 10 11 12 13 14 15

Primary Market Sales Volume Secondary Volume Tertiary Volume

Total Sales ($ Billions)

page 41

Sales Volume by Region

As Of 15Q1

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

5

10

15

20

25

30

35

40

08 09 10 11 12 13 14 15

Northeast Southeast Central West Coast

Total Sales ($ Billions)

page 42

Sales Volume By Star Rating

As Of 15Q1

Rating

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

5

10

15

20

25

30

35

40

08 09 10 11 12 13 14 15

5 Star 4 Star 3 Star 2 Star

Total Sales ($ Billions)

page 43

Volume By Star Rating For Primary Metros Only

As Of 15Q1

Rating

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

2

4

6

8

10

12

14

16

18

08 09 10 11 12 13 14 15

5 Star 4 Star 3 Star 2 Star

Total Sales ($ Billions)

page 44

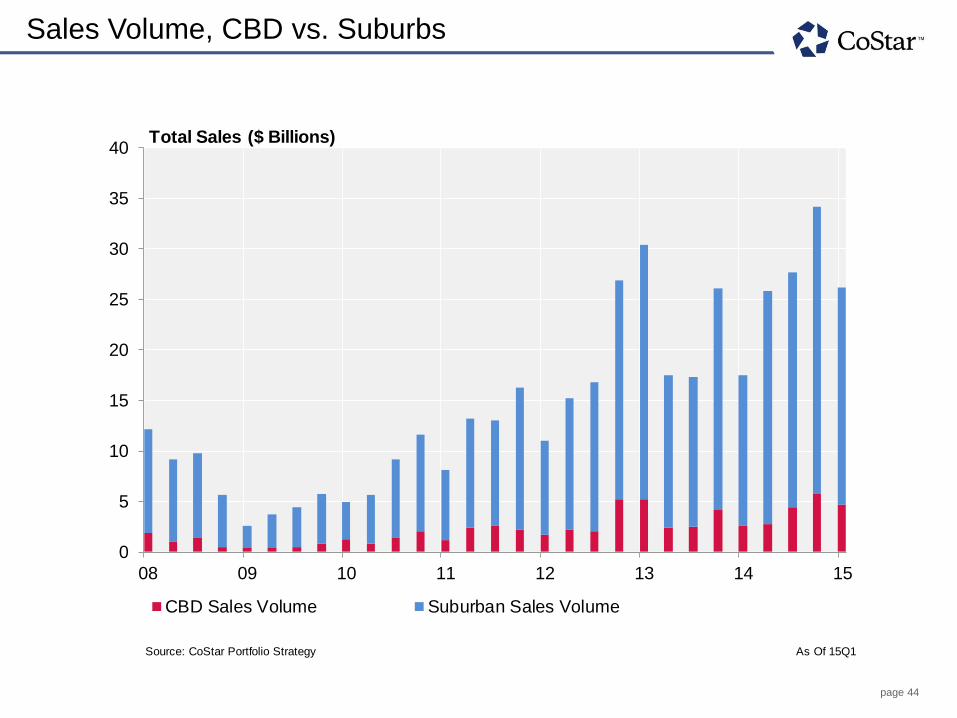

Sales Volume, CBD vs. Suburbs

As Of 15Q1Subtype:

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

5

10

15

20

25

30

35

40

08 09 10 11 12 13 14 15

CBD Sales Volume Suburban Sales Volume

Total Sales ($ Billions)

page 45

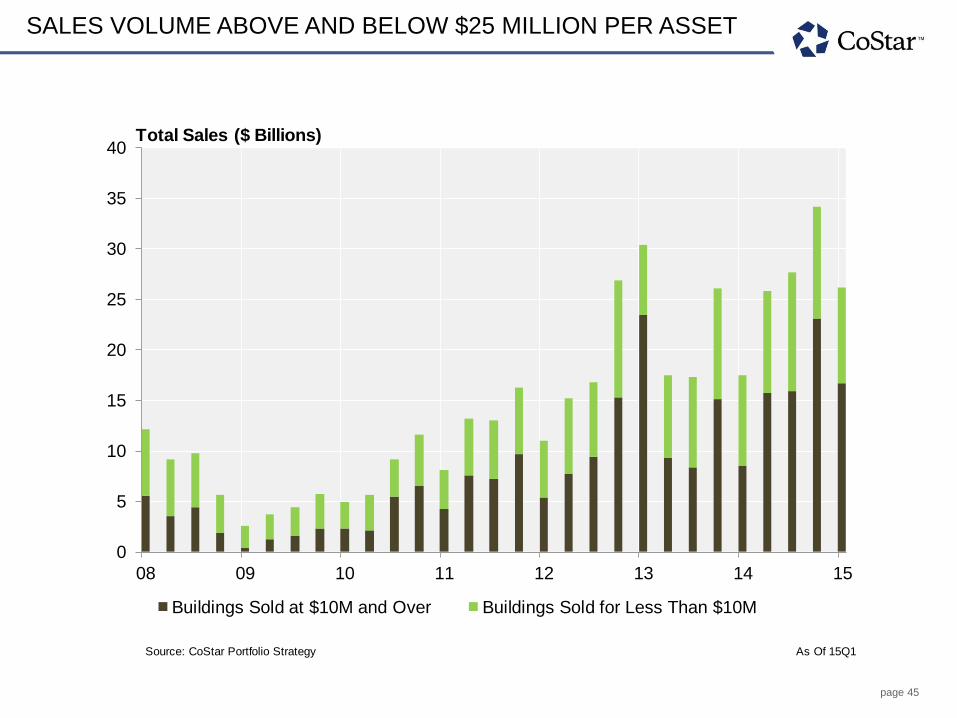

SALES VOLUME ABOVE AND BELOW $25 MILLION PER ASSET

As Of 15Q1Subtype:

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

5

10

15

20

25

30

35

40

08 09 10 11 12 13 14 15

Buildings Sold at $10M and Over Buildings Sold for Less Than $10M

Total Sales ($ Billions)

page 46

Price Per Unit Across Market Tiers

As Of 15Q1

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

$0

$50

$100

$150

$200

$250

$300

08 09 10 11 12 13 14 15

Primary Markets Secondary Markets Tertiary Markets

Price Per Unit

page 47

As Of 15Q1

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

$0

$50

$100

$150

$200

$250

$300

08 09 10 11 12 13 14 15

Primary Markets Secondary Markets Tertiary Markets

Price Per Unit

99%

54%

67%

Price Per Unit Across Market Tiers

page 48

PRICE/UNIT IN PRIMARY METROS, CBD vs. SUBURBAN

As Of 15Q1

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

0

100

200

300

400

500

600

08 09 10 11 12 13 14 15

Primary CBD Primary Suburban

Price Per Unit

page 49

Cap Rates By Region

As Of 15Q1

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

Source: CoStar Portfolio Strategy As Of 15Q1

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

04 05 06 07 08 09 10 11 12 13 14

Northeast Southeast Central West Coast

page 50

Cap Rates By Market Tier

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

04 05 06 07 08 09 10 11 12 13 14

Primary Secondary Tertiary

As Of 15Q1 Source: CoStar Portfolio Strategy

page 51

Cap Rates By Property Type

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

05 06 07 08 09 10 11 12 13 14 15

Apartment Office Warehouse Retail

Source: CoStar Portfolio Strategy As Of 15Q1

page 52

Too Early To Call A Trend, But % Of Ask Continues To Fall

Trends Of Properties Listed For Sale On CoStar

As Of 15Q1

12/31/200412/31/200512/31/200612/31/200712/31/200812/31/200912/31/201012/31/201112/31/201212/31/201312/31/201412/31/2015

Note: If there is a spike in 13Q4 it's due to deal ID 2925503 which was entered as 104 or 1,000 times the asking price. Need to delete it.

Source: CoStar Portfolio Strategy As Of 15Q1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

84%

86%

88%

90%

92%

94%

96%

98%

100%

102%

104%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Months To Close Percent of Ask

Months To ClosePercent Of Ask

page 53

Select Top Multifamily Deals – 1Q 2015

Praedium/Blackstone Multi-State Portfolio Praedium Group sold a 36-complex, 11,029 unit apartment portfolio to The Blackstone Group for $1.70 billion. Nationwide in scope, the Class A & B portfolio traded at $154,000 per unit.

MODE by Alta San Jose, CA Wood Partners sold the 111-unit luxury complex to Land & Houses, LLC for $73.63 million. Having delivered in late 2014, the 663,288 per unit complex has a pro-forma cap rate of 4.0%

OneEleven Chicago, IL The Related Companies to the 504-Unit “ultra-luxury” tower to Heitman, LLC for $328.23 million or $641,240 per unit. Conceived as a hotel, the seller re-developed the site since 2011 and it sold with an 80% occupancy.

8th & Hope Los Angeles, CA Wood Partners sold the 290-unit 8th & Hope to Essex Property Trust for 200.00 million. The building delivered in 4th Q 2014, transferred at 55% leased and is expected to stabilize by 3rd Q 2015 and a 3.75% cap rate.

Residences on the Avenue Washington, DC Boston Properties sold the 335 unit /50,000 sf retail building to the Kuwait-based WAFRA Investment Advisory Group for $196.00 million. With a 94% apartment occupancy and fully leased retail the property traded at a 4.1% cap..

4 Complex Student Housing Portfolio FL. GA, MO & TX A venture of JLL Income Property Trust sold Starwood Capital a four-complex portfolio for $123.81 million. Consisting of 1,212 units /3,480 beds it sold for 101,500 unit and at a 5.77% cap rate.

page 54

© Copyright 2015 CoStar Realty Information, Inc. No reproduction or distribution without permission. The following information includes projections and analyses that are based on various assumptions by CoStar

concerning future events and circumstances, as well as historical and current data maintained in CoStar’s database, obtained from public sources or provided by proprietary sources. Actual results may vary

materially from the projections presented. The information in this presentation speaks only as of the date(s) referenced and is provided ‘as is’. CoStar expressly disclaims any guarantees, representations or

warranties of any kind, including those of merchantability and fitness for a particular purpose. You should not construe any of the information herein as investment, tax, accounting or legal advice.