Moody's Mega Math Challenge Team 218 - Moody's Math Challenge

page 1

State of the U.S. Multifamily Market

2015 Review and Forecast

page 2

• Economic Overview

• Apartment Leasing Fundamentals

• Apartment Rent Trends

• Capital Markets

Agenda

page 3

Economic Backdrop

page 4

Contributions To GDP Growth

3/31/2007

6/30/2007

9/30/2007

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

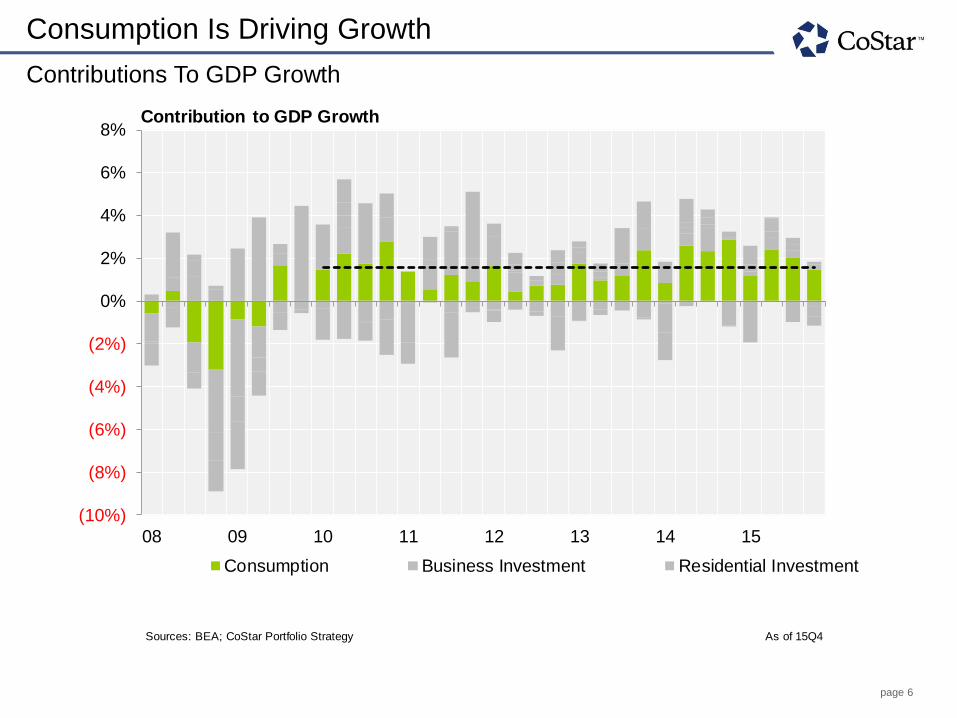

Sources: BEA; CoStar Portfolio Strategy As of 15Q4

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

08 09 10 11 12 13 14 15

Consumption Business Investment Residential Investment

Government Net Exports Change in Inventories

Total GDP

Contribution to GDP Growth

page 5

Consumption Is Driving Growth

Contributions To GDP Growth

3/31/2007

6/30/2007

9/30/2007

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

Sources: BEA; CoStar Portfolio Strategy As of 15Q4

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

08 09 10 11 12 13 14 15

Consumption Business Investment Residential Investment

Government Net Exports Change in Inventories

Contribution to GDP Growth

page 6

Consumption Is Driving Growth

Contributions To GDP Growth

3/31/2007

6/30/2007

9/30/2007

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

Sources: BEA; CoStar Portfolio Strategy As of 15Q4

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

08 09 10 11 12 13 14 15

Consumption Business Investment Residential Investment

Contribution to GDP Growth

page 7

Weak Global Economy and Strong Dollar Hurt Exports

3/31/2007

6/30/2007

9/30/2007

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

Sources: BEA; CoStar Portfolio Strategy As of 15Q4

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

08 09 10 11 12 13 14 15

Consumption Business Investment Residential Investment

Government Net Exports Change in Inventories

Contribution to GDP Growth

page 8

Global Capital Flows Have Favored U.S.

Net Change in U.S. International Investment Position

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

Source: Bureau of Economic Analysis As of 15Q3

($1.0T)

$0.0T

$1.0T

$2.0T

$3.0T

$4.0T

$5.0T

10 11 12 13 14 15

Cumulative Net Capital Flows to US since 2009Q4

page 9

Residential Investment Steady If Unspectacular

3/31/2007

6/30/2007

9/30/2007

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

Sources: BEA; CoStar Portfolio Strategy As of 15Q4

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

08 09 10 11 12 13 14 15

Consumption Business Investment Residential Investment

Government Net Exports Change in Inventories

Contribution to GDP Growth

page 10

Volatile Quarterly Growth = Steady Annual Growth

3/31/2007

6/30/2007

9/30/2007

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

Sources: BEA; CoStar Portfolio Strategy As of 15Q4

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

08 09 10 11 12 13 14 15

Consumption Business Investment Residential Investment

Government Net Exports Change in Inventories

Total GDP

Contribution to GDP Growth

page 11

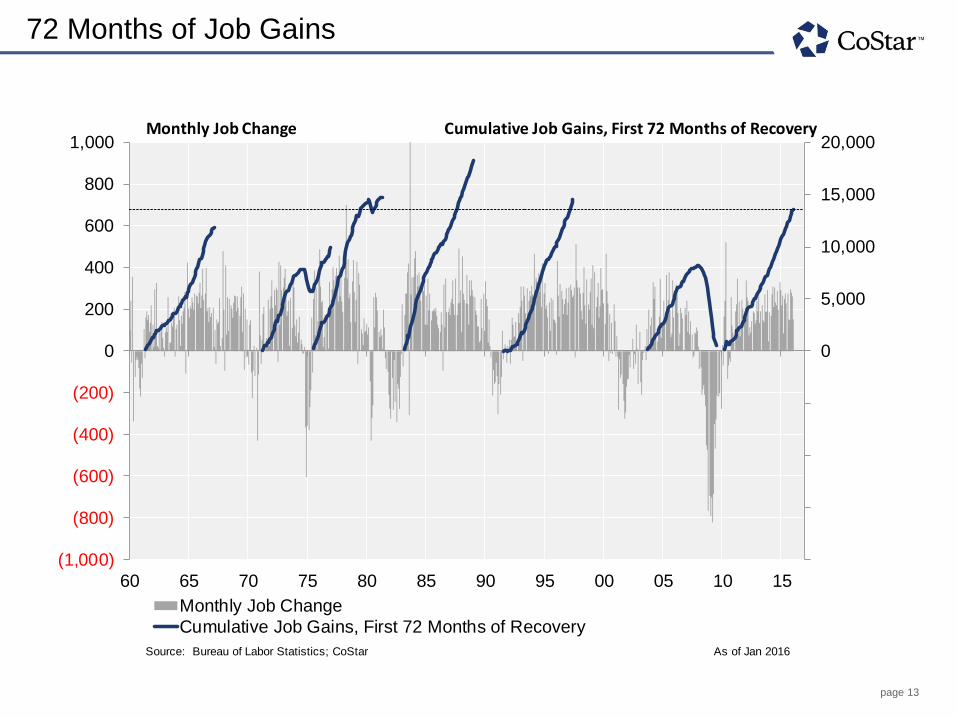

72 Months of Job Gains

31-Jan-39

28-Feb-39

31-Mar-39

30-Apr-39

########

30-Jun-39

31-Jul-39

31-Aug-39

30-Sep-39

31-Oct-39

30-Nov-39

31-Dec-39

31-Jan-40

29-Feb-40

31-Mar-40

30-Apr-40

########

30-Jun-40

31-Jul-40

31-Aug-40

30-Sep-40

31-Oct-40

30-Nov-40

31-Dec-40

31-Jan-41

28-Feb-41

31-Mar-41

Source: Bureau of Labor Statistics; CoStar As of Jan 2016

(1,000)

(800)

(600)

(400)

(200)

0

200

400

600

800

1,000

60 65 70 75 80 85 90 95 00 05 10 15

Monthly Job Change

Monthly Job Change

page 12

72 Months of Job Gains

31-Jan-39

28-Feb-39

31-Mar-39

30-Apr-39

########

30-Jun-39

31-Jul-39

31-Aug-39

30-Sep-39

31-Oct-39

30-Nov-39

31-Dec-39

31-Jan-40

29-Feb-40

31-Mar-40

30-Apr-40

########

30-Jun-40

31-Jul-40

31-Aug-40

30-Sep-40

31-Oct-40

30-Nov-40

31-Dec-40

31-Jan-41

28-Feb-41

31-Mar-41

Source: Bureau of Labor Statistics; CoStar As of Jan 2016

0

5,000

10,000

15,000

20,000

(1,000)

(800)

(600)

(400)

(200)

0

200

400

600

800

1,000

60 65 70 75 80 85 90 95 00 05 10 15Monthly Job Change

Cumulative Job Gains, First 72 Months of Recovery

Monthly Job Change Cumulative Job Gains, First 72 Months of Recovery

page 13

72 Months of Job Gains

31-Jan-39

28-Feb-39

31-Mar-39

30-Apr-39

########

30-Jun-39

31-Jul-39

31-Aug-39

30-Sep-39

31-Oct-39

30-Nov-39

31-Dec-39

31-Jan-40

29-Feb-40

31-Mar-40

30-Apr-40

########

30-Jun-40

31-Jul-40

31-Aug-40

30-Sep-40

31-Oct-40

30-Nov-40

31-Dec-40

31-Jan-41

28-Feb-41

31-Mar-41

Source: Bureau of Labor Statistics; CoStar As of Jan 2016

0

5,000

10,000

15,000

20,000

(1,000)

(800)

(600)

(400)

(200)

0

200

400

600

800

1,000

60 65 70 75 80 85 90 95 00 05 10 15

Monthly Job Change

Cumulative Job Gains, First 72 Months of Recovery

Monthly Job Change Cumulative Job Gains, First 72 Months of Recovery

page 14

West And South Are Fastest Growing

Projected Household Growth

Live Data

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Pasted Data

1

2

3

4

Sources: Moody's Analytics; CoStar Portfolio Strategy As of 15Q4

0

50

100

150

200

250

300

350

400

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%O

rlando

Ra

leig

h

Palm

Be

ach

Pho

enix

Austin

Las V

egas

Ch

arlotte

Atlan

ta

Da

llas -

FW

Jacksonvill

e

Ho

usto

n

Fort

Laud

erd

ale

Tam

pa

Inla

nd E

mpire

San

An

tonio

De

nve

r

Mia

mi

Port

land,

OR

Sea

ttle

Na

shvill

e

Metro Average (15Q4-20Q4) National Index (15Q4-20Q4) Cumulative Growth

New Households (000s)

South East Midwest West

Average Annual Household Growth (15Q4-20Q4)

page 15

South And West Enjoying Strong Growth

Metro Wage And Salary Growth

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Rank

1

2

3

4

5

Sources: Moody's Analytics; CoStar Portfolio Strategy As of 15Q4

20%

25%

30%

35%

40%

45%

50%

55%O

rlando

Jacksonvill

e

Palm

Be

ach

Tam

pa

San

Fra

ncis

co

India

na

polis

Sea

ttle

Fort

Laud

erd

ale

Pho

enix

Port

land

Austin

Da

llas -

FW

Sta

mfo

rd

Ra

leig

h

San

Jose

Mia

mi

Ch

arlotte

Salt L

ake C

ity

Na

shvill

e

De

troit

Metro Wage and Salary Growth (15Q4-20Q4)

National Index Wage and Salary Growth (15Q4-20Q4)

Wage and Salary Growth (15Q4-20Q4)

South East Midwest West

page 16

Where the High-Earners Go

Relative Share and Gains of High-Income/High-Growth Jobs, 2010-

2014

New YorkLos AngelesChicagoHoustonAtlantaWashingtonDallasPhiladelphiaPhoenixMinneapolisBostonSeattleOrange CountyDenverSan DiegoSt. LouisBaltimoreInland EmpireTampaPittsburghSan FranciscoOrlandoPortlandMiamiOaklandClevelandCincinnatiKansas CityEdisonSan Jose

Source: Bureau of Labor Statistics Occupational Employment Statistics As of 2014Note: Bubble size denotes total employment. Color coding denotes average income as of 2014; blue is higher and red is lower.Note: "High Income/High Growth" jobs refer to occupations with incomes and growth rates in the top third.

New York

Los AngelesChicago

Houston

Washington

Philadelphia

Minneapolis

BostonSeattle

Denver

San Diego

Inland Empire

Pittsburgh

San Francisco

Orlando

Miami

Oakland

Cincinnati

Edison

San Jose

San Antonio

Las Vegas

Fort LauderdaleNorfolk

(60%)

(40%)

(20%)

0%

20%

40%

60%

80%

100%

(80%) (60%) (40%) (20%) 0% 20% 40% 60% 80% 100% 120%

Relative Share of High Income/High Growth Jobs, 2010

Relative Gain in High Income/High Growth Jobs, 2010-2014

More than fair share of high income / high growth jobs, and gaining share

Less than fair share of high income / high growth jobs, but gaining share

Less than fair share of high income / high growth jobs, and losing share

More than fair share of high income / high growth jobs, but losing share

page 17

Demographic Tailwinds Remain

U.S. Population By Age

Year

1910

1911

1912

1913

1914

1915

1916

1917

1918

1919

1920

1921

1922

1923

1924

1925

1926

1927

1928

1929

1930

1931

1932

1933

1934

1935

1936

1937

1938

1939

1940

Sources: Center for Health Statistics; Moody's Analytics; CoStar Portfolio Strategy As of 13Q4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

98 93 88 83 78 73 68 63 58 53 48 43 38 33 28 23 18 13 8 3

Current AgeRenters Owners

MillenialsBaby Boom Generation X

U.S. Population (Millions)

Generation Z

page 18

Leasing Fundamentals

page 19

Who Are Today’s Renters?

page 20

Two Quarters Do Not Make A Trend, But…….

Homeownership Rate And Renter Occupied Households

65

65

65

66

66

66

66

67

67

67

67

68

68

68

68

69

69

69

69

70

70

70

70

71

71

Sources: Moody's Analytics; U.S. Census Bureau; CoStar Portfolio Strategy As of 15Q4

30

32

34

36

38

40

42

44

60

61

62

63

64

65

66

67

68

69

70

94 96 98 00 02 04 06 08 10 12 14

Renter Households U.S. HO Rate

Homeownership Rate (%) Renter Occupied Households (Millions)

page 21

Drop In Homeownership = More Renter Households

Homeownership Rate And Renter Household Growth By Age Cohort

12/31/2014

3/31/2006

8.76

330.78

(2,520.24)

Households

Sources: U.S. Census Bureau; Moody's Analytics; JCHS; CoStar Portfolio Strategy As of 15Q4

55%

60%

65%

70%

75%

80%

85%

35-44 Years 45-54 Years 55-64 Years 65 Years AndOlder

Average HO Rate (1982-06) 2006Q1 Current HO Rate

0

500

1,000

1,500

2,000

2,500

Less Than 35Years

35-44 Years 45-54 Years 55-64 Years 65 Years AndOlder

Renter Household Growth (2006-14)

Homeownership Rate

Renter Household Growth (000s)

30%

32%

34%

36%

38%

40%

42%

44%

Less Than 35 Years

page 22

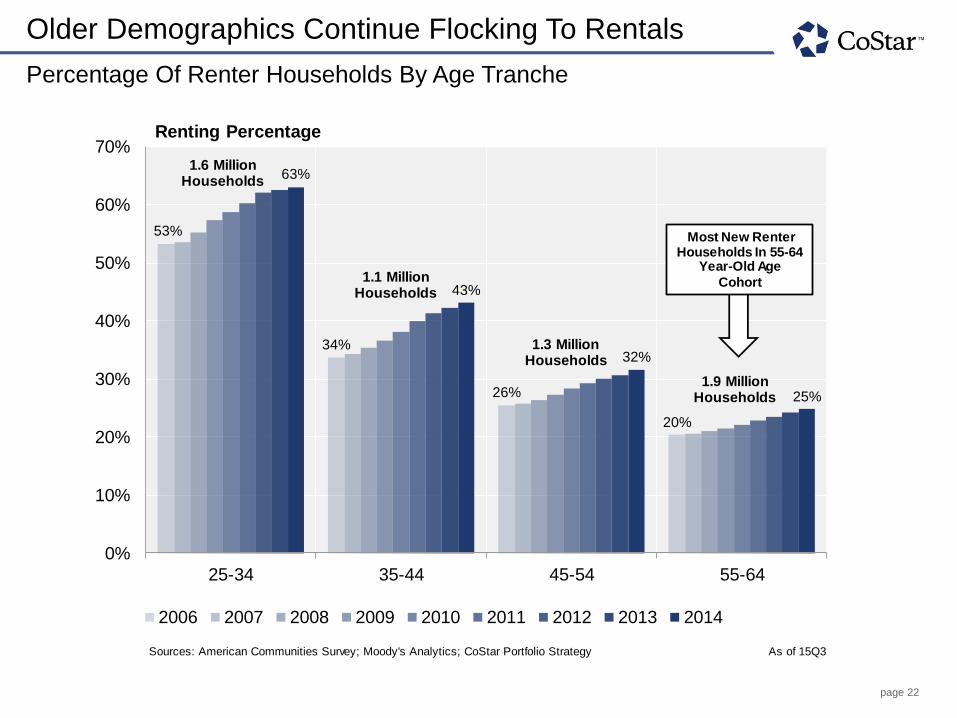

Older Demographics Continue Flocking To Rentals

Percentage Of Renter Households By Age Tranche

2006

2007

2008

2009

2010

2011

2012

2013

2014

Sources: American Communities Survey; Moody's Analytics; CoStar Portfolio Strategy As of 15Q3

53%

34%

26%

20%

63%

43%

32%

25%

0%

10%

20%

30%

40%

50%

60%

70%

25-34 35-44 45-54 55-64

2006 2007 2008 2009 2010 2011 2012 2013 2014

Renting Percentage

1.6 Million Households

1.1 Million Households

1.3 Million Households

1.9 Million Households

Most New RenterHouseholds In 55-64

Year-Old Age

Cohort

page 23

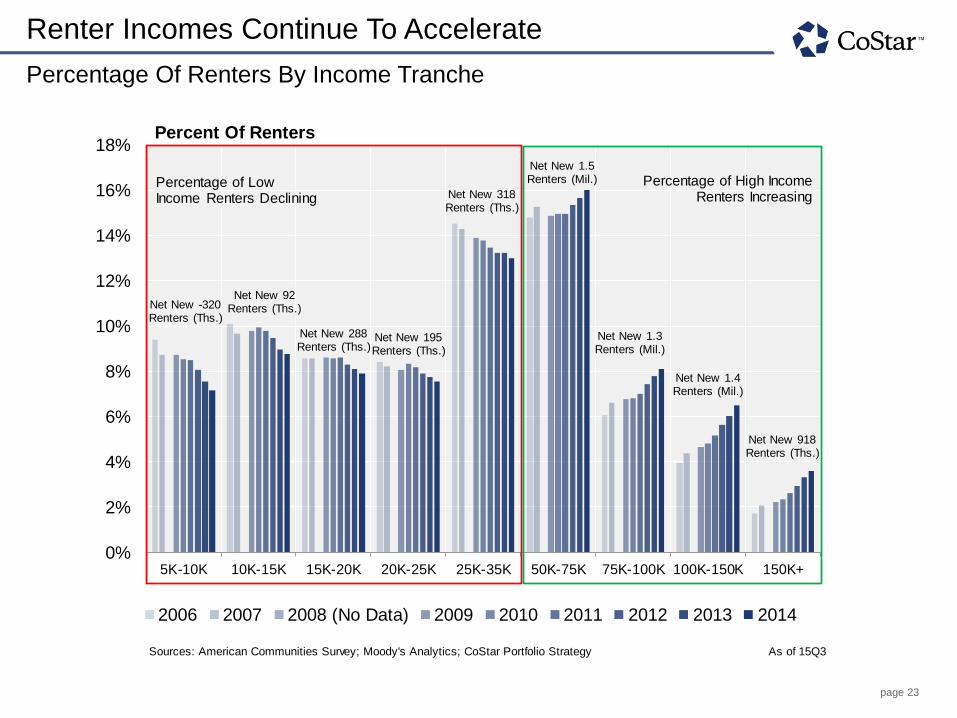

Renter Incomes Continue To Accelerate

Percentage Of Renters By Income Tranche

From: file:///\\ppr3\common\Work%20in%20Progress\Tom%20Conville\Sam\Income%20Demographics\Income%20by%20Owner%20and%20Renter.xlsxOwner Income

0-5000

150000+

Renter Income

5K-10K10K-15K15K-20K20K-25K25K-35K50K-75K

150K+

2006-2014

Sources: American Communities Survey; Moody's Analytics; CoStar Portfolio Strategy As of 15Q3

Net New -320 Renters (Ths.)

Net New 92 Renters (Ths.)

Net New 288 Renters (Ths.)

Net New 195 Renters (Ths.)

Net New 318 Renters (Ths.)

Net New 1.5 Renters (Mil.)

Net New 1.3 Renters (Mil.)

Net New 1.4 Renters (Mil.)

Net New 918 Renters (Ths.)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

5K-10K 10K-15K 15K-20K 20K-25K 25K-35K 50K-75K 75K-100K 100K-150K 150K+

2006 2007 2008 (No Data) 2009 2010 2011 2012 2013 2014

Percentage of Low Income Renters Declining

Percentage of High Income Renters Increasing

Percent Of Renters

page 24

Folks Are Getting Married Later In Life

Median Age At First Marriage, United States

Table MS-2. Estimated Median Age at First Marriage: 1890 to present

20142013201220112010

20092008200720062005200420032002200120001999199819971996199519941993199219911990198919881987

Sources: U.S. Census Bureau; CoStar Portfolio Strategy As of 15Q3

20

22

24

26

28

30

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

Men Women

Median Age At First Marriage

page 25

More People Are Living Alone

Single Person Households, United States

r

r

Sources: U.S. Census Bureau; Current Population Survey, Annual Social and Economic Supplement; As of 15Q3

CoStar Portfolio Strategy

10%

15%

20%

25%

30%

0

5

10

15

20

25

30

35

40

60 64 68 72 76 80 84 88 92 96 00 04 08 12

Single Person Households Single Person Households as % of Total Households

Single Person Households (Millions) % Single Person Households

page 26

Living With Friends/Partners Helps Pay The Rent

2005200620072008200920102011201220132014

Sources: U.S. Census, CoStar Portfolio Strategy As of 15Q3

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

05 06 07 08 09 10 11 12 13 14

Non Family Households With Annual Earnings Over 150K Total U.S. Households

Cumulative Growth Since 2005

# of Non Family Households With

Earnings Over 150K

2005: 800,000 2014: 1.5 Million

Growth In High Earning Non-Family Households

page 27

Good Luck Getting A Mortgage If You're Young

Mortgage Origination By Riskscore And Average Credit Rating By Age

Sources: New York Fed Consumer Credit Panel/Equifax; Credit Karma; CoStar Portfolio Strategy As of 15Q2

$0

$200

$400

$600

$800

$1,000

$1,200

03 04 05 06 07 08 09 10 11 12 13 14 15

<620 620-659 660-719 720-779 780+

Mortgage Origination By Riskscore (Billions)

630 628 630647

697

580

600

620

640

660

680

700

720

18-24 25-34 35-44 45-54 55+

Average Credit Rating

Credit Score 2007 2015

<659 19% 8%

780+ 32% 50%

page 28

Apartment Market Fundamentals

page 29

Some Of The Heaviest Supply Levels For The Cycle

National Apartment Supply, Demand, and Vacancy

90

90

90

90

91

91

91

91

92

92

92

92

93

93

93

93

94

94

94

94

95

95

95

95

96

96

96

96

Source: CoStar Portfolio Strategy As of 15Q4

3%

4%

5%

6%

7%

8%

(20)

(10)

0

10

20

30

40

50

60

70

80

90

100

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Demand Change (Q/Q) Supply Change (Q/Q)

Vacancy Historical Avg Vacancy (2000-2014)

Demand & Supply (000s Units) Vacancy

page 30

Developers Building Smaller Units

Single Person Households And Small Unit Construction

s

r

r

Sources: U.S. Census Bureau; Current Population Survey, Annual Social and Economic Supplement; As of 15Q4

CoStar Portfolio Strategy

35%

40%

45%

50%

55%

60%

65%

10%

15%

20%

25%

30%

70 75 80 85 90 95 00 05 10 15

Single Person Households as % of Total Households

Studios or 1 BRs as % of New Construction

% Single Person Households Studios or 1 BRs as % of New Construction

page 31

Developers Focused On CBDS

Units Under Construction As A % Of Inventory In Top U.S. Markets

2012

2012

2012

2012

2013

2013

2013

2013

2014

2014

2014

2014

2015

2015

2015

2015

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

50

100

150

200

250

2012 2013 2014 2015

CBD % Inventory Underway Premier Suburban % Inventory Underway

Suburban % Inventory Underway CBD Units Underway

Premier Suburban Units Underway Suburban Units Underway

Units Under Construction (000s) Under Construction As A % Of Inventory

page 32

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2016 (14Q4-16Q4)

Rank

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000H

ousto

n

Ne

w Y

ork

Da

llas

Washin

gto

n, D

C

Sea

ttle

Los A

ngele

s

Austin

Atlan

ta

De

nver

Bosto

n

Pho

enix

Ch

icago

Na

sh

vill

e

San

An

tonio

Ch

arlotte

Orlando

Mia

mi

San

Jose

Port

land,

OR

Phila

delp

hia

Kan

sa

s C

ity

Ora

ng

e C

ounty

San

Fra

ncis

co

Min

nea

polis

San

Die

go

Completions As A % Of InventorySouth East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 33

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2016 (14Q4-16Q4)

Rank

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000H

ousto

n

Ne

w Y

ork

Da

llas

Wash

ingto

n, D

C

Sea

ttle

Los A

ngele

s

Austin

Atlan

ta

De

nver

Bosto

n

Pho

enix

Ch

ica

go

Na

shvill

e

San

An

tonio

Ch

arlotte

Orlando

Mia

mi

San

Jose

Port

land,

OR

Phila

delp

hia

Kan

sas C

ity

Ora

ng

e C

ounty

San

Fra

ncis

co

Min

nea

polis

San

Die

go

South East Midwest West

New Supply (As % of Inventory)New Supply (Units)

2015 Deliveries 2016 Deliveries

page 34

And Supply Hits Unevenly Within Markets

Denver Submarkets Y/Y Supply Growth As A Percentage Of Metro Y/Y Supply Growth

1234567

Other 8 Submarkets

47

121515151515151311

310

21515

Source: CoStar Portfolio Strategy As of 15Q4

36.3%

14.7%

8.6%

8.2%

6.4%

5.3%4.3%

16.1% Downtown/Cherry Creek

West Denver

Southeast Corridor

Highlands Ranch/LoneTree

Aurora

DTC/Hampden

Lakewood/West Corridor

Other 8 Submarkets

% Submarket Stock Growth Of Metro Stock Growth

page 35

Starts Continue To Climb

U.S. Multifamily Starts And Permits

Sources: U.S. Census; Moody's Analytics; CoStar Portfolio Strategy As of 15Q4

0

50

100

150

200

250

83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15

Multifamily StartsMultifamily PermitsMultifamily Starts Historical Average (83-Present)

Starts and Permits (000s)

page 36

Breaking Ground: Construction Starts By Submarket

Construction Starts In 2015

151413121110

987654321

Source: CoStar Portfolio Strategy As of 15Q4

2,080

2,093

2,138

2,143

2,328

2,374

2,390

2,449

2,519

2,580

2,814

2,903

3,099

3,214

8,871

1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

NEWY -Midtown West

MIAM -Brickell/Downtown Miami

DALL - Oak lawn/Park Cities

NEWY -Williamsburg/Greenpoint/Navy…

DALL - Allen/McKinney

CHAR -Uptown

CHIC -North Lakefront

HOUS -Neartown/River Oaks

ATLA -Downtown/Midtown

DALL - Frisco/Prosper

LOSA -Downtown Los Angeles

NASH -West End/CBD

CHIC -Downtown Chicago

DENV -Downtown/Cherry Creek

NEWY -Long Island City/Hunters Point

Units

Highest Construction Starts In 2015

page 37

New Construction Lease Up A Bit Slower in ‘15

Quarterly Deliveries And Lease Up Trend By Year Of Delivery

Vacant Units

3/31/2013

6/30/2013

9/30/2013

3/31/2014

6/30/2014

9/30/2014

3/31/2015

6/30/2015

9/30/2015

Total Units

3/31/2013

6/30/2013

9/30/2013

3/31/2014

6/30/2014

9/30/2014

3/31/2015

6/30/2015

9/30/2015

Source: CoStar Portfolio Strategy As of 15Q4

0

10

20

30

40

50

60

70

0%

10%

20%

30%

40%

50%

60%

13Q1 13Q2 13Q3 13Q4 14Q1 14Q2 14Q3 14Q4 15Q1 15Q2 15Q3 15Q4 16Q1 16Q2

Quarterly Deliveries 2013 Vintage 2014 Vintage 2015 Vintage

Vacancy Rate Units Delivered (000s)

page 38

Apartment New Construction Leasing Is Slowing

2015 Delivery Lease Up Trends By Region

Vacant Units

East

3/31/2015

6/30/2015

9/30/2015

South

3/31/2015

6/30/2015

9/30/2015

Midwest

3/31/2015

6/30/2015

9/30/2015

West

3/31/2015

6/30/2015

9/30/2015

15Q1

15Q2

Source: CoStar Portfolio Strategy As of 15Q4

20%

25%

30%

35%

40%

45%

50%

55%

60%

15Q1 15Q2 15Q3 15Q4

East South Midwest West

Vacancy Rate

page 39

Vacancies Show The Effect Of Construction

Unstabilized Vacancies By Star Rating Since 2007

4 & 5 Star3 StarSpread

9/30/200212/31/2002

3/31/20036/30/20039/30/2003

12/31/20033/31/20046/30/20049/30/2004

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/2006

Source: CoStar Portfolio Strategy As of 15Q4

3%

4%

5%

6%

7%

8%

9%

10%

07 08 09 10 11 12 13 14 15

4 & 5 Star Vacancy 3 Star Vacancy 1 & 2 Star Vacancy

Vacancy Rate

page 40

Higher Vacancies In The Core

Vacancy By Submarket District Type

Stock

Vacancy

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

ATLA

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

14%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

CBD SecondaryCore

Urban PrimeSuburban

Suburban Rural

Vacancy % % UC of Inventory

Vacancy % UC of Inventory

page 41

Late Recovery Markets Showed Improved Fundamentals

Vacancy Change Past 12 Months

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

Source: CoStar Portfolio Strategy As of 15Q4

(150)

(100)

(50)

0

50

100

150T

am

pa

Las V

egas

Ho

nolu

luN

orf

olk

India

na

polis

Washin

gto

n, D

CS

an

An

tonio

Jacksonvill

eC

incin

nati

Austin

Sain

t Louis

Pho

enix

Ra

leig

hR

ich

mond

Mem

phis

De

troit

Inla

nd E

mpire

Da

llas -

FW

Atlan

taS

tam

ford

Sacra

mento

Ch

icago

Phila

delp

hia

Ch

arlotte

Cle

ve

land

Fort

Laud

erd

ale

Co

lum

bus O

HN

ort

hern

NJ

Baltim

ore

Los A

ngele

sS

an

Die

go

Ora

ng

e C

ounty

Sea

ttle

Orlando

San

Fra

ncis

co

Ne

w O

rlean

sP

ort

land,

OR

Ho

usto

nE

ast

Bay

Min

nea

polis

Okla

hom

a C

ity

Long I

sla

nd

Pitts

burg

hS

alt L

ake C

ity

Ne

w Y

ork

Kan

sas C

ity

Na

sh

vill

eD

enver

Milw

aukee

San

Jose

Mia

mi

Bosto

nH

art

ford

Palm

Be

ach

South East Midwest West

One Year Vacancy Change (BPS)

page 42

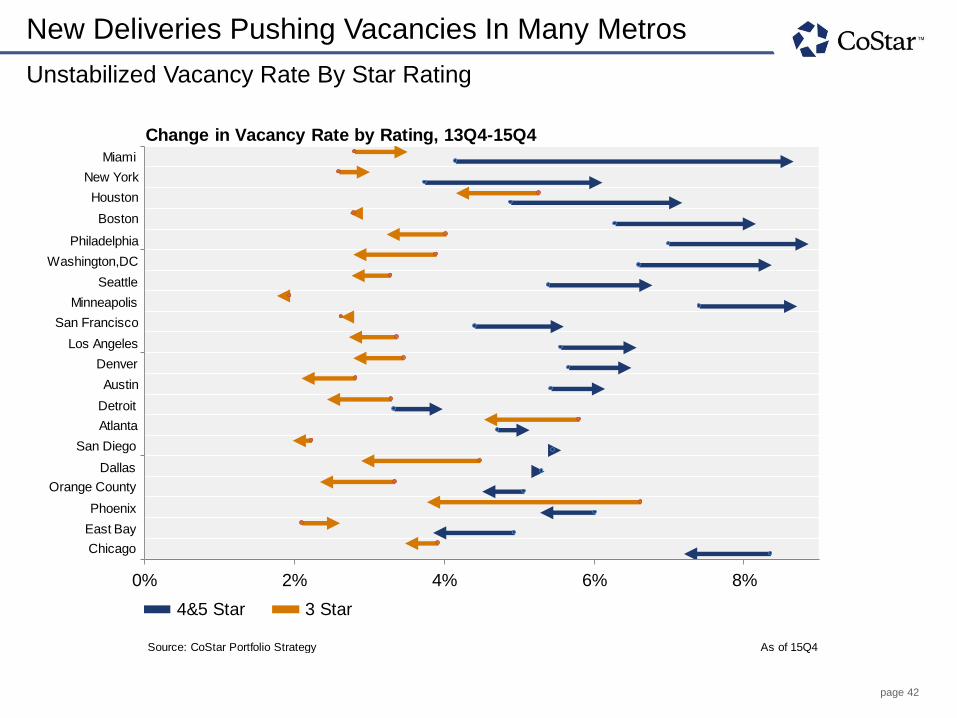

New Deliveries Pushing Vacancies In Many Metros

Unstabilized Vacancy Rate By Star Rating

14

15

16

17

18

19

20

Source: CoStar Portfolio Strategy As of 15Q4

0% 2% 4% 6% 8%

4&5 Star 3 Star

San Diego

Miami

East Bay

Chicago

Phoenix

Detroit

Orange County

Dallas

Change in Vacancy Rate by Rating, 13Q4-15Q4

New York

Houston

Boston

Philadelphia

Washington,DC

Seattle

Minneapolis

San Francisco

Los Angeles

Denver

Austin

Atlanta

page 43

Y/Y Vacancy Change Winners & Losers

Nominal Change In Vacancy By Submarket

151413121110

987654321

Source: CoStar Portfolio Strategy As of 15Q4

*Minimum 5,000 Units

3.0%

3.0%

3.0%

3.0%

3.3%

3.4%

3.7%

3.7%

3.7%

3.9%

4.2%

5.4%

5.5%

6.5%

9.1%

0% 2% 4% 6% 8% 10%

LASV -Enterprise/South Paradise

WASH - Capitol Heights/Largo

WASH - Downtown

WASH - Reston/Herndon Corridor

RICH -Chesterfield County

HOUS -Outlying Montgomery County

ATLA -Clayton County

INDI -Fishers/Noblesville

SANJ -Cupertino

NORT -Southeast Morris County

WASH - Old Town/Potomac Yards

WASH - Silver Spring

WASH - Southwest/Navy Yard

WASH - H Street/NoMa

WASH - Ballston

Change In Vacancy Y/Y

3.5%

3.6%

3.6%

3.8%

3.9%

4.0%

4.0%

4.1%

4.1%

4.1%

4.1%

4.9%

5.8%

8.0%

10.8%

0% 3% 6% 9% 12%15%

CHIC -Near North Suburban Cook

NEWY -Jersey City Waterfront

BOST -Fenway/Mission Hill

OKLA -Moore

HOUS -Cinco Ranch

MINN -Downtown Minneapolis

BALT -Harford County

SANF -Sunset/Lakeshore

HOUS -Heights

NASH -Williamson County

BOST -Everett/Malden/Medford/Melrose

PORT -Downtown Portland

BOST -Harvard/Central/Kendall/Cambridge

CHAR -South End

PHIL -University City

Best Vacancy Decrease Worst Vacancy Increase

page 44

Apartment Rent Trends

page 45

CoStar Apartment Rents in Buckhead

PropertyID

4803472

4803472

4803472

4803472

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

4803472

As of Jan 2016

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2011 2012 2013 2014 2015 2016

CoStar Reseach (n=3,768)

Asking Rent

page 46

CoStar Apartment Rents in Buckhead

PropertyID

4803472

4803472

4803472

4803472

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

4803472

As of Jan 2016

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2011 2012 2013 2014 2015 2016

CoStar Reseach (n=3,768) Community Caller (n=561)

Asking Rent

page 47

CoStar Apartment Rents in Buckhead

PropertyID

4803472

4803472

4803472

4803472

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

4803472

As of Jan 2016

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2011 2012 2013 2014 2015 2016

CoStar Reseach (n=3,768) Community Caller (n=561)

Automated Data Collection (n=7,542)

Asking Rent

page 48

CoStar Apartment Rents in Buckhead

PropertyID

4803472

4803472

4803472

4803472

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

9409478

9409478

9409478

4803472

4803472

4803472

9409478

9409478

9409478

4803472

As of Jan 2016

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2011 2012 2013 2014 2015 2016

CoStar Reseach (n=3,768) Community Caller (n=561)

Automated Data Collection (n=7,542) Apartments.com Feed (n=51,872)

Observed Asking Rent

page 49

7,375 1-BR Rent Observations for a Single Building

Asset in Greater Atlanta

PropertyID

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

8422582

Source: CoStar As of January 2016

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16

Asking Rent: 1-BR Units for Asset in Greater Atlanta

page 50

A Volatile Year for Apartment Rents

CoStar Same-Store Chain-Linked Apartment Rents

1/31/2011

2/28/2011

3/31/2011

4/30/2011

5/31/2011

6/30/2011

7/31/2011

8/31/2011

9/30/2011

10/31/2011

11/30/2011

12/31/2011

1/31/2012

2/29/2012

3/31/2012

4/30/2012

5/31/2012

6/30/2012

7/31/2012

8/31/2012

9/30/2012

10/31/2012

11/30/2012

12/31/2012

1/31/2013

2/28/2013

3/31/2013

4/30/2013

5/31/2013

6/30/2013

7/31/2013

Source: CoStar As of Jan. 2016

$0.95

$1.00

$1.05

$1.10

$1.15

$1.20

$1.25

(10%)

(5%)

0%

5%

10%

15%

2011 2012 2013 2014 2015 2016

Annualized Monthly Rent Change National 1-BR, 1-BA Rent Equivalent

Monthly Rent Change (Annualized) National 1-BR, 1-BA Equivalent Rent/SF

page 51

Strongest Rent Growth in 2015

Weighted

By Market

31

51

43

33

19

27

1

39

5

36

32

29

12

44

2

37

26

14

58

42

50

6

35

38

15

Source: CoStar As of Jan. 2016

15.1%

11.7%11.0% 10.6% 10.2% 9.9%

9.4% 9.3% 9.0% 8.8% 8.7% 8.6% 8.4% 8.4%7.6% 7.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%P

ort

land

East

Bay/O

akla

nd

Na

shvill

e

Sacra

mento

Long I

sla

nd (

New

York

)

Orlando

Atlan

ta

Tam

pa/S

t P

ete

rsburg

Ch

arlotte

Sea

ttle

/Puge

t S

ound

Ra

leig

h/D

urh

am

Pho

enix

De

nver

Las V

egas

Austin

Sou

th F

lorida

2015 Rent Growth

page 52

Strongest Rent Growth in 2015

Weighted

By Market

31

51

43

33

19

27

1

39

5

36

32

29

12

44

2

37

26

14

58

42

50

6

35

38

15

Source: CoStar As of Jan. 2016

15.1%

11.7%11.0% 10.6% 10.2% 9.9%

9.4% 9.3% 9.0% 8.8% 8.7% 8.6% 8.4% 8.4%7.6% 7.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%P

ort

land

East

Bay/O

akla

nd

Na

shvill

e

Sacra

mento

Long I

sla

nd (

New

York

)

Orlando

Atlan

ta

Tam

pa/S

t P

ete

rsburg

Ch

arlotte

Sea

ttle

/Puge

t S

ound

Ra

leig

h/D

urh

am

Pho

enix

De

nver

Las V

egas

Austin

Sou

th F

lorida

2015 Rent Growth

page 53

Strongest Rent Growth in 2015

Weighted

By Market

31

51

43

33

19

27

1

39

5

36

32

29

12

44

2

37

26

14

58

42

50

6

35

38

15

Source: CoStar As of Jan. 2016

15.1%

11.7%11.0% 10.6% 10.2% 9.9%

9.4% 9.3% 9.0% 8.8% 8.7% 8.6% 8.4% 8.4%7.6% 7.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%P

ort

land

East

Bay/O

akla

nd

Na

shvill

e

Sacra

mento

Long I

sla

nd (

New

York

)

Orlando

Atlan

ta

Tam

pa/S

t P

ete

rsburg

Ch

arlotte

Sea

ttle

/Puge

t S

ound

Ra

leig

h/D

urh

am

Pho

enix

De

nver

Las V

egas

Austin

Sou

th F

lorida

2015 Rent Growth

page 54

Weakest Rent Growth in 2015

Weighted

By Market

31

51

43

33

19

27

1

39

5

36

32

29

12

44

2

37

26

14

58

42

50

6

35

38

15

Source: CoStar As of Jan. 2016

5.9% 5.9% 5.8% 5.7% 5.6% 5.4% 5.4% 5.4% 5.2% 5.2% 4.9% 4.5% 4.5% 4.0%3.3%

2.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%O

rang

e C

ounty

(C

alif

orn

ia)

Ho

usto

n

Salt L

ake C

ity

Mem

phis

San

An

tonio

Ch

icago

San

Fra

ncis

co

St. L

ouis

India

na

polis

Baltim

ore

Phila

delp

hia

Washin

gto

n, D

C

No

rthern

New

Jers

ey

Westc

heste

r/S

o C

onn

ecticut

Ha

rtfo

rd

Pitts

burg

h

2015 Rent Growth

page 55

Weakest Rent Growth in 2015

Weighted

By Market

31

51

43

33

19

27

1

39

5

36

32

29

12

44

2

37

26

14

58

42

50

6

35

38

15

Source: CoStar As of Jan. 2016

5.9% 5.9% 5.8% 5.7% 5.6% 5.4% 5.4% 5.4% 5.2% 5.2% 4.9% 4.5% 4.5% 4.0%3.3%

2.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%O

rang

e C

ounty

(C

alif

orn

ia)

Ho

usto

n

Salt L

ake C

ity

Mem

phis

San

An

tonio

Ch

icago

San

Fra

ncis

co

St. L

ouis

India

na

polis

Baltim

ore

Phila

delp

hia

Washin

gto

n, D

C

No

rthern

New

Jers

ey

Westc

heste

r/S

o C

onn

ecticut

Ha

rtfo

rd

Pitts

burg

h

2015 Rent Growth

page 56

Weakest Rent Growth in 2015

Weighted

By Market

31

51

43

33

19

27

1

39

5

36

32

29

12

44

2

37

26

14

58

42

50

6

35

38

15

Source: CoStar As of Jan. 2016

5.9% 5.9% 5.8% 5.7% 5.6% 5.4% 5.4% 5.4% 5.2% 5.2% 4.9% 4.5% 4.5% 4.0%3.3%

2.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%O

rang

e C

ounty

(C

alif

orn

ia)

Ho

usto

n

Salt L

ake C

ity

Mem

phis

San

An

tonio

Ch

icago

San

Fra

ncis

co

St. L

ouis

India

na

polis

Baltim

ore

Phila

delp

hia

Washin

gto

n, D

C

No

rthern

New

Jers

ey

Westc

heste

r/S

o C

onn

ecticut

Ha

rtfo

rd

Pitts

burg

h

2015 Rent Growth

page 57

Weakest Rent Growth in 2015

Weighted

By Market

31

51

43

33

19

27

1

39

5

36

32

29

12

44

2

37

26

14

58

42

50

6

35

38

15

Source: CoStar As of Jan. 2016

5.9% 5.9% 5.8% 5.7% 5.6% 5.4% 5.4% 5.4% 5.2% 5.2% 4.9% 4.5% 4.5% 4.0%3.3%

2.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%O

rang

e C

ounty

(C

alif

orn

ia)

Ho

usto

n

Salt L

ake C

ity

Mem

phis

San

An

tonio

Ch

icago

San

Fra

ncis

co

St. L

ouis

India

na

polis

Baltim

ore

Phila

delp

hia

Washin

gto

n, D

C

No

rthern

New

Jers

ey

Westc

heste

r/S

o C

onn

ecticut

Ha

rtfo

rd

Pitts

burg

h

2015 Rent Growth

page 58

Capital Markets

page 59

Property Sales Up 20%

Sales Volume By Property Type

1

21345

12345

Source: CoStar Portfolio Strategy As of 15Q4

18% 18%

7%

37%

45%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

$0

$20

$40

$60

$80

$100

$120

$140

$160

Multi-Family Office Retail Industrial Hospitality

2015 U.S. Sales Volume (Billions) 2015 vs 2014 %Change

page 60

Volume Remains High, But Will Rate Of Growth Moderate?

Top 210 Markets Annual Apartment Sales Volume

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Source: Costar Portfolio Strategy As of 15Q4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

$0

$20

$40

$60

$80

$100

$120

$140

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Sales Volume Annual Change In Volume

Total Sales (Billions) Y/Y Change In Volume

page 61

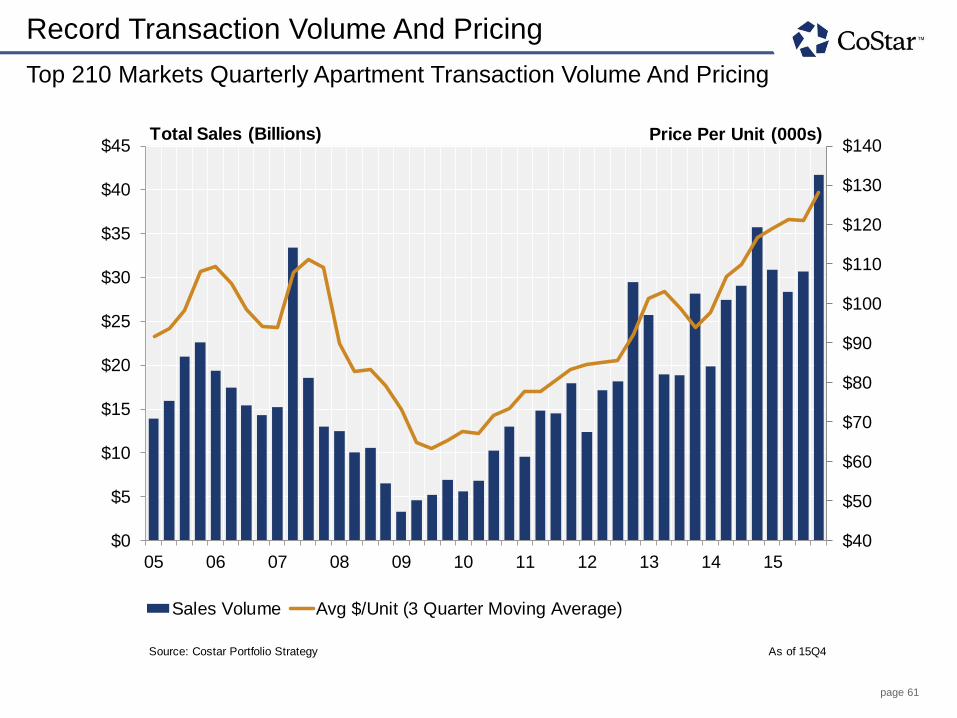

Record Transaction Volume And Pricing

Top 210 Markets Quarterly Apartment Transaction Volume And Pricing

04

04

04

05

05

05

05

06

06

06

06

07

07

07

07

08

08

08

08

09

09

09

09

10

10

10

10

11

Source: Costar Portfolio Strategy As of 15Q4

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

05 06 07 08 09 10 11 12 13 14 15

Sales Volume Avg $/Unit (3 Quarter Moving Average)

Total Sales (Billions) Price Per Unit (000s)

page 62

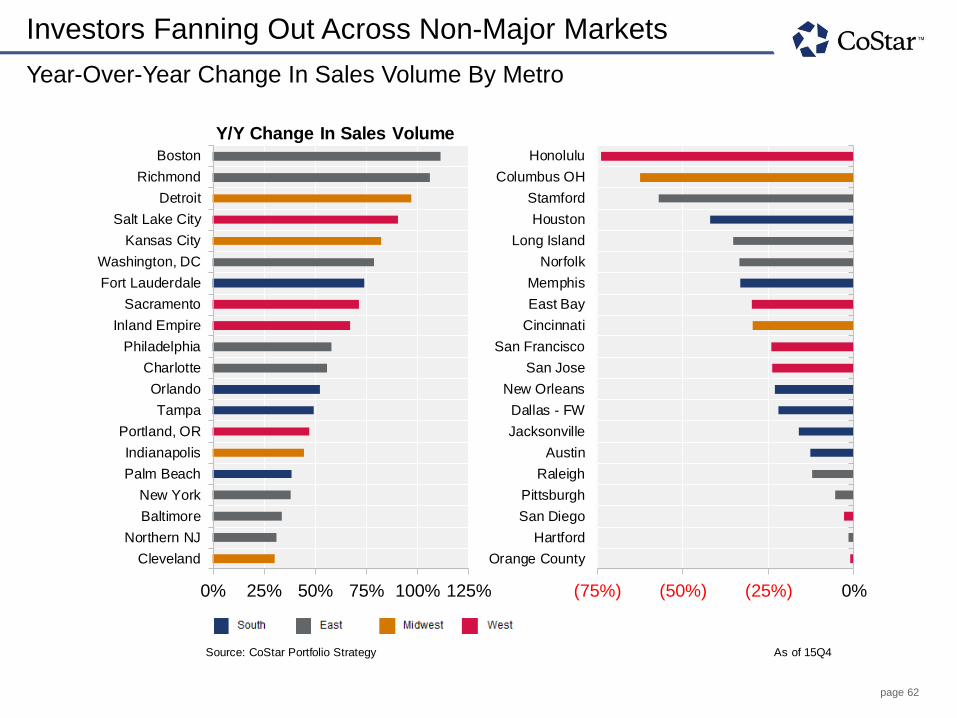

Investors Fanning Out Across Non-Major Markets

Year-Over-Year Change In Sales Volume By Metro

20

19

18

17

16

15

14

13

12

11

10

9

8

7

6

5

4

3

2

1

Source: CoStar Portfolio Strategy As of 15Q4

0% 25% 50% 75% 100% 125%

Cleveland

Northern NJ

Baltimore

New York

Palm Beach

Indianapolis

Portland, OR

Tampa

Orlando

Charlotte

Philadelphia

Inland Empire

Sacramento

Fort Lauderdale

Washington, DC

Kansas City

Salt Lake City

Detroit

Richmond

Boston

(75%) (50%) (25%) 0%

Orange County

Hartford

San Diego

Pittsburgh

Raleigh

Austin

Jacksonville

Dallas - FW

New Orleans

San Jose

San Francisco

Cincinnati

East Bay

Memphis

Norfolk

Long Island

Houston

Stamford

Columbus OH

Honolulu

Y/Y Change In Sales Volume

page 63

Cap Rates, After Jackson Pollack

Institutional Grade Transaction Cap Rates

36526.00

42369.00

Source: CoStar Portfolio Strategy. Cap rates are shaded by distance from trailing average to identify trend.

Includes 2+ star-rated apartment assets selling for at least $5 million.

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Transaction Cap Rate

Apartment Transaction Cap Rate

page 64

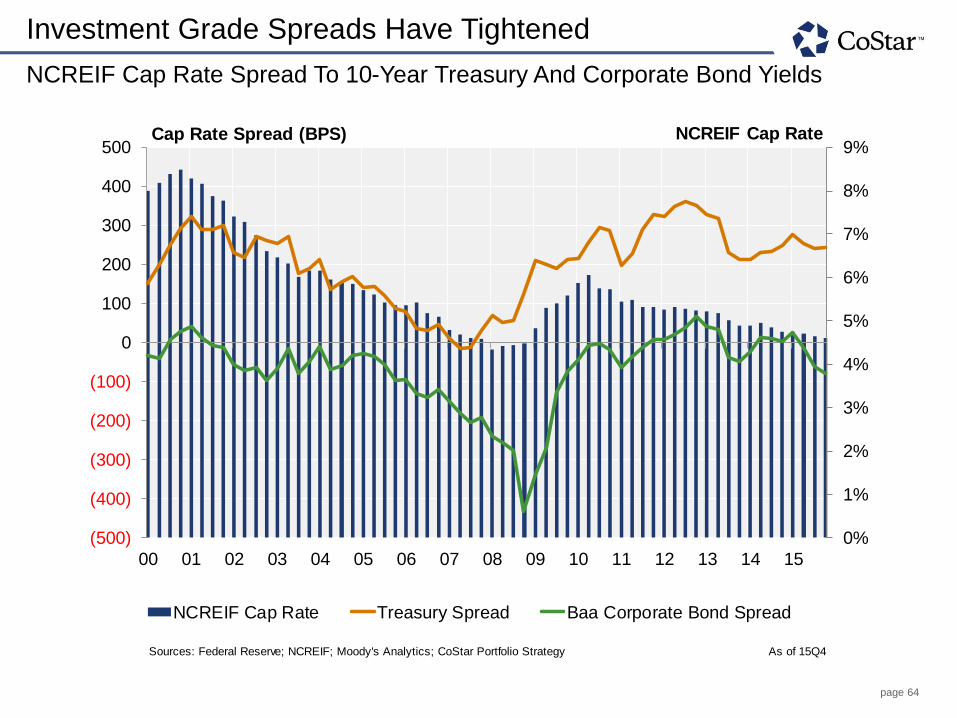

Investment Grade Spreads Have Tightened

NCREIF Cap Rate Spread To 10-Year Treasury And Corporate Bond Yields

Sources: Federal Reserve; NCREIF; Moody's Analytics; CoStar Portfolio Strategy As of 15Q4

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

(500)

(400)

(300)

(200)

(100)

0

100

200

300

400

500

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

NCREIF Cap Rate Treasury Spread Baa Corporate Bond Spread

Cap Rate Spread (BPS) NCREIF Cap Rate

page 65

California Cap Rates Among The Country’s Lowest

Average Cap Rates By Metro

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Source: CoStar Portfolio Strategy As of 15Q4

Average Cap Rate

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%S

an

Fra

ncis

co

San

Jose

Ho

nolu

luO

rang

e C

ounty

Los A

ngele

sS

an

Die

go

East

Bay

Ne

w Y

ork

Sea

ttle

Ra

leig

hP

ort

land,

OR

Austin

Inla

nd E

mpire

Washin

gto

n, D

CLong I

sla

nd

De

nver

Sacra

mento

Mia

mi

Atlan

taJacksonvill

eN

ashvill

eC

harlotte

Orlando

Baltim

ore

Da

llas-

FW

San

An

tonio

Fort

Laud

erd

ale

Bosto

nS

alt L

ake C

ity

Pho

enix

Tam

pa

Palm

Be

ach

Phila

delp

hia

Las V

egas

Min

nea

polis

No

rthern

NJ\

Sta

mfo

rdM

ilwaukee

Co

lum

bus O

HN

orf

olk

Kan

sas C

ity

Ch

icago

Ho

usto

nR

ichm

ond

De

troit

Sain

t Louis

India

na

polis

Ha

rtfo

rdN

ew

Orlean

sO

kla

hom

a C

ity

Mem

phis

Pitts

burg

hC

incin

nati

Cle

vela

nd

Recession High Prerecession Low 2015 Average

page 66

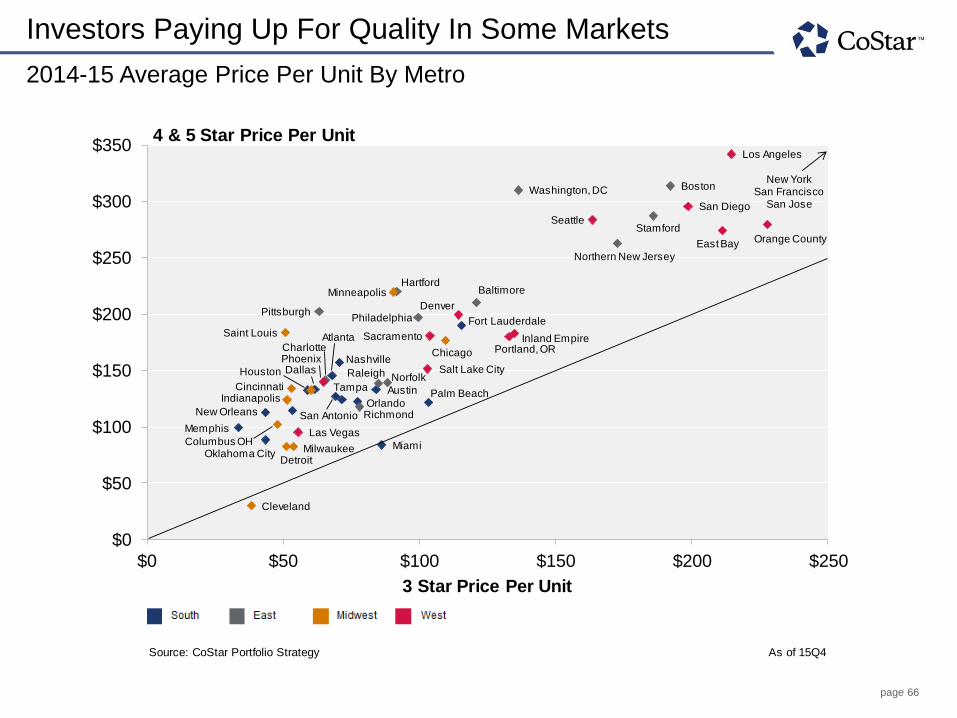

Investors Paying Up For Quality In Some Markets

2014-15 Average Price Per Unit By Metro

Atlanta

Austin

Baltimore

Boston

Charlotte

Chicago

Cincinnati

Cleveland

Denver

Detroit

East Bay

Hartford

Honolulu

Houston

Memphis

Miami

Milwaukee

Nashville

Source: CoStar Portfolio Strategy As of 15Q4

Atlanta

Austin

Baltimore

Boston

CharlotteChicago

Cincinnati

Cleveland

Columbus OH

Dallas

Denver

Detroit

East Bay

Fort Lauderdale

Hartford

Houston

Indianapolis

Inland Empire

Las Vegas

Los Angeles

Memphis

MiamiMilwaukee

Minneapolis

Nashville

New Orleans

Norfolk

Northern New Jersey

Oklahoma City

Orange County

OrlandoPalm Beach

Philadelphia

Phoenix

Pittsburgh

Portland, OR

Raleigh

Richmond

SacramentoSaint Louis

Salt Lake City

San Antonio

San Diego

SeattleStamford

Tampa

Washington, DC

$0

$50

$100

$150

$200

$250

$300

$350

$0 $50 $100 $150 $200 $250

3 Star Price Per Unit

4 & 5 Star Price Per Unit

New YorkSan Francisco

San Jose

page 67

Foreign Buyers Becoming More Active

Foreign Sales Volume As A Share Of Total, 2005-15

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Source: CoStar Portfolio Strategy As of 15Q4

0%

1%

2%

3%

4%

5%

6%

7%

$0

$20

$40

$60

$80

$100

$120

$140

$160

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Non Foreign Foreign Foreign Sales As A % Of Total

Sales Volume (Billions) Percent Foreign Sales Volume

page 68

Foreign Buyers Have An Empire State Of Mind

Foreign Sales Volume By Metro, 2014-15

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

14%

16%

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

Ne

w Y

ork

Washin

gto

n, D

C

Da

llas -

FW

Atlan

ta

San

Fra

ncis

co

Pho

enix

Ho

usto

n

Orlando

Sou

th F

lorida

Los A

ngele

s

Tam

pa

Bosto

n

Sea

ttle

De

nver

Austin

2014-15 Foreign Sales Volume Foreign Sales As A % Of Total

Sales Volume (Billions) Percent Foreign Sales Volume

page 69

Our Neighbors To The North Have Been Very Active

Foreign Investment By Region And Country, 2014-15

Region

South America

Oceania

Europe

Europe

Middle East

South America

North America

North America

North America

Asia

Europe

Europe

Europe

Europe

Asia

Asia

Asia

Europe

Middle East

Europe

Asia

Asia

Asia

Middle East

Europe

Asia

North America

Europe

Oceania

Europe

Asia

Source: CoStar As of 15Q4

Oceania (0.9%)

Middle East

(14.0%)

North America (54.3%)

Asia, (7.7%)

Europe (23.1%)

Canada (45.5%)

Israel (8.5%)

Switzerland (7.5%)

Germany (6.0%)

China (5.5%)

United Kingdom

(5.2%)

Sweden (5.2%)

Bahrain (4.7%)

Kuwait (3.3%)

France (2.3%)Other (6.3%)

By Region By Country

page 70

2015 Quarterly Volume Declines In High Supply Areas

Sales Volume And Price Per Unit In 25 Most Supply-Heavy Submarkets*

10

10

10

10

11

11

11

11

12

12

12

12

13

13

13

13

14

14

14

14

15

15

15

15

Source: CoStar Portfolio Strategy As of 15Q4

*Includes submarkets with the most units delivered (2012-15)

$0

$50

$100

$150

$200

$250

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

10 11 12 13 14 15

Sales Volume Price Per Unit

Sales Volume (Billions) Price Per Unit (000s)

page 71

Average Price Per Unit In 25 Submarkets Most Supply-Heavy Submarkets*

Source: CoStar Portfolio Strategy As of 15Q4

*Includes submarkets with the most units delivered (2012-15)

(60%)

(40%)

(20%)

0%

20%

40%

60%

80%

100%

120%

140%

$0

$100

$200

$300

$400

$500

$600

$700H

ou

sto

n -

Ne

art

ow

n/R

ive

r O

aks

Chic

ag

o -

Do

wn

tow

n C

hic

ag

o

Den

ve

r -

Dw

tn/C

he

rry C

ree

k

Sa

n J

ose

- N

ort

h S

an

Jo

se

Dallas -

Oa

k L

aw

n/P

ark

Citie

s

Ora

nge

Co

un

ty -

Irv

ine

Dallas -

Fa

rme

rs B

ranch

/Add

iso

n

Atla

nta

- B

uckh

ea

d

Hou

sto

n -

No

rth

west

Ho

usto

n

Sa

n A

nto

nio

- N

ort

hw

est

Sid

e

Au

stin -

So

uth

Atla

nta

- D

ow

nto

wn

/Mid

tow

n

Dallas -

Ea

st

Da

llas

Nash

vill

e -

We

st

En

d/C

BD

Lo

s A

ng

ele

s -

Do

wn

tow

n L

A

Se

att

le -

CB

D

New

Yo

rk -

LI

City/H

un

ters

Poin

t

Hou

sto

n -

Wo

od

lan

ds

Sa

n A

nto

nio

- F

ar

We

st

Se

att

le -

La

ke

Un

ion

Wa

sh

ing

ton

, D

C -

H S

t/N

oM

a

Sa

n A

nto

nio

- F

ar

No

rth

Ce

ntr

al

New

Yo

rk -

W'b

urg

/Gre

en

poin

t

Dallas -

Fri

sco

/Pro

spe

r

Ka

nsa

s C

ity -

Joh

nso

n C

nty

KS

2012-14 Average $/Unit 2015 Average $/Unit % Change In Pricing

Price Per Unit (000s) Change In Pricing

page 72

Not Enough Buyers To Go Around?

Buildings Aged Two Years Or Less, Price Per Unit And Total Volume

Source: CoStar Portfolio Strategy As of 15Q4

$0

$50

$100

$150

$200

$250

$0

$2

$4

$6

$8

$10

$12

$14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Sales Volume Average Price Per Unit

Total Sales ($ Billions) Price Per Unit (000s)

page 73

Select Top Multifamily Deals – 4Q 2015

Home Properties Merger with Lone Star Various States Home Properties Inc. sold the 116 community, 39,465 unit apartment portfolio to Lone Star Funds for $7.6 Billion or roughly $192K/unit. (price included all operations and debt assumption).

Peter Cooper Village/Stuyvesant Town New York, NY CW Capital LLC sold the 2 community, 11,243-unit portfolio to The Blackstone Group and Ivanhoe Cambridge for $$5.4 Billion or $485K/unit. This portfolio was sold at a 4% cap rate.

Greystar Portfolio Various States Greystar Investment Group, LLC sold this 32 community, 10,399 unit portfolio to The Blackstone Group LP for $2 Billion or $192K/unit. Greystar will continue to manage these properties.

350 Sharon Park Menlo Park, CA Essex Property Trust, Inc. sold this 296 unit complex for $245 million or $827K/Unit The cap was 5.2%.

Blackstone Portfolio FL, CA Phoenix Realty Group sold the 16 community 3800 unit portfolio to The Blackstone Group LP for $570 million or $150K/Unit. This was a recapitalization of a portfolio controlled mostly by Phoenix Realty Group.

Starwood Portfolio Tampa Bay, FL The Wilson Company sold 23 communities totaling 7,870 units to Starwood Capital Group for $351 million..

page 74

© Copyright 2016 CoStar Realty Information, Inc. No reproduction or distribution without permission. The following information includes projections and analyses that are based on various assumptions by CoStar

concerning future events and circumstances, as well as historical and current data maintained in CoStar’s database, obtained from public sources or provided by proprietary sources. Actual results may vary

materially from the projections presented. The information in this presentation speaks only as of the date(s) referenced and is provided ‘as is’. CoStar expressly disclaims any guarantees, representations or

warranties of any kind, including those of merchantability and fitness for a particular purpose. You should not construe any of the information herein as investment, tax, accounting or legal advice.