WMQRS IoM Cancer & Surgical Specialities Report V1.1 20150305 1426607835

Upload

maryjanetbibinCategory

view

217download

0

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 1/35

State of the Region Report 2009

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 2/35

The State of the Region Report 2009

is sponsored by Newman University College

Newman University College has been serving the West

Midlands through the provision o high quality education

or over 40 years.

Based on Catholic values o inclusion, tolerance, respectand social justice, Newman provides opportunities or all

who have the ability to benet, regardless o background,

at undergraduate and postgraduate level.

Newman makes a valuable contribution to the local

economy, as most students are rom the region and work

here ater graduation. Newman graduates develop the

critical analysis, empathy, problem solving abilities and

proessionalism required by graduate employers. Newman

is also a leading provider o work-based continuingproessional development, and has one o the best

graduate employment rates o UK universities.

From short training courses, knowledge transer and

research and consultancy, Newman also ofers a range o

services and resources to enhance innovation and

perormance in organisations across the private, public and

third sectors.

www.newman.ac.uk

Newman University College – Expect to Achieve

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 3/35

2Foreword by Rosie Paskins

4The State of the Region

25Looking to the Future

27Appendix 1: The State of the Region Process

29Appendix 2: Contents of the Memory Stick

30Endnotes

State of the Region Annual Synthesis Report 2009

Contents

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 4/35

Foreword by Rosie Paskins

Welcome to the second annual synthesis report for the new Stateof the Region process. The process, introduced in last year’sreport, brings together those responsible for preparing the region’sevidence base with those who use it to develop policies andstrategies for the region and its constituent parts. The aim is toensure that the evidence being provided by researchers, includingthe Observatory, better meets the needs of policy-makers, andthat it is used effectively to improve regional policies andstrategies.

This report brings together some of the key evidence from the State of the Region dialogues witha range of other information about the major issues facing the West Midlands.

The year since the publication of the last State of the Region report has been a difficult one forthe West Midlands. The economic recession is a global one, but it has hit our region harder thanmost. Businesses are reporting that economic output is falling faster than in any other part of thecountry, particularly amongst our manufacturing base. We have also seen unemployment risingfaster than elsewhere, with young people particularly badly affected.

The impact of the recession has been felt not just in those places, and amongst those groups, whichhave historically suffered from deprivation, but has also affected some additional areas and groups.This means that, in the short term, the focus of regional attention has shifted. Good quality, timelyevidence has been vital to ensure the regional response to the recession has been appropriate andtargeted.

Although the effects of the recession will last for some time, the region needs to prepare for thefuture now, and the evidence base must help to point it in the right direction. The new Strategyfor the West Midlands will bring together a number of key policies, notably around the economy,communities and the environment. To inform the strategy we will need to integrate the evidenceacross all of these areas. The State of the Region process, and reports such as the Observatory’srecent West Midlands: Fit for the Future are part of that integration.

Regardless of the recession, the long-term structural challenges facing the region remain, and manyhave been brought into even sharper focus by the recession. Within this report you will find thelatest evidence about some of these key challenges.

The West Midlands economy is still less productive than the national average, and the gap is growing

- latest estimates suggest that the region's output gap has grown to around £15 billion. The numberof people who are not working, and hence not contributing to the region’s economy, was increasingeven before the recession and has now reached about 30% of the region's working age population.Worklessness is higher still amongst young people (around one in ten of whom are now claimingJobseekers' Allowance), people with disabilities or health problems (particularly those with mentalhealth problems), members of some minority ethnic groups and people with no formal qualifications.Although overall skill levels are improving, we still lag behind most regions and have more peoplewithout qualifications than any other region, impacting on their productivity and their ability tofind work. Having people with the right skills will be crucial in fostering the innovative approachesneeded for the region to meet the challenges it faces and for its businesses to prosper in the futureeconomy.

But the challenges aren’t just economic. Climate change will have a big impact on the region,

through stretching targets for reduction of carbon emissions and the need to adapt to changingenvironmental conditions. The region’s population is also changing, with growing ethnic diversity

State of the Region Annual Synthesis Report 20092

Foreword by Rosie Paskins

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 5/35

and an increase in the number of people in older age groups - those aged 85 and over are expected

to double in the next 20 years. Whilst these changes present challenges they also provideopportunities, particularly if the region embraces new ideas and ways of working.

A growing and ageing population, along with lifestyle changes, will mean a demand for more houses.This will increase pressure on the region’s environment and its transport system. Both are potentialassets for the region, but the natural environment is already particularly fragmented and parts ofthe transport network suffer from high levels of congestion. Enhancing both is important becauseof the key role they play in improving the image of the region, vital to encouraging more peopleand businesses to locate here. Equally important to the regional image are quality of life issuessuch as health, anti-social behaviour and the quality of local services. The cultural sector, too, isincreasingly important, economically as well as socially, particularly as some parts of the sectorhave fared better during the recession than most other industries.

These challenges are inter-connected, and the region will need to address them all if it is to besuccessful. To do this, we will need evidence that makes those connections and helps us tounderstand what addressing one challenge will mean for the others. This will be increasinglyimportant as the main regional strategies come together into the new Strategy for the West Midlands,work on which will begin soon.

Of course, the region covers a large area, with a diverse mix of places within it. The challengesfacing different places aren’t the same: economic output per employee is £10,000 higher in Solihullthan in Stoke; over 40% of Birmingham's working age population are not employed, roughly doublethe rate in Warwickshire; a quarter of Herefordshire's population is above state pension age,compared to around one in six of Birmingham's; levels of physical activity in Walsall are half thosein Worcestershire and Shropshire. This means that the evidence we produce needs to include anunderstanding of these differences; this will demand better links between regional and localevidence and more sophisticated use of information about places and the connections betweenthem.

Meeting the challenges facing the region will also require an evidence base that helps us to findsolutions. Much of the evidence we have produced so far has been about understanding the challengeswe face. It has been backward looking, identifying the current “State of the Region”. We also needto look forward, finding more evidence for how we can change the future “State of the Region”.This doesn’t mean we should stop monitoring the progress that we are making, but it does meanthat the evidence base for policy must evolve, so that it focuses even more on developing betterpolicies for the future. That is what the State of the Region process is all about.

Whilst this report and the State of the Region process which underpins it provide a range of important

information for regional policy-makers, their success will depend on how that information is used.The messages emerging from the State of the Region process deserve to be heard by a wideraudience. This annual report provides an opportunity for this to happen. I hope that you will wishto get involved in the process over the coming year. Together we can ensure that better evidenceleads to better policy.

3State of the Region Annual Synthesis Report 2009

Foreword by Rosie Paskins

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 6/35

The State of the Region

Impacts of the recession

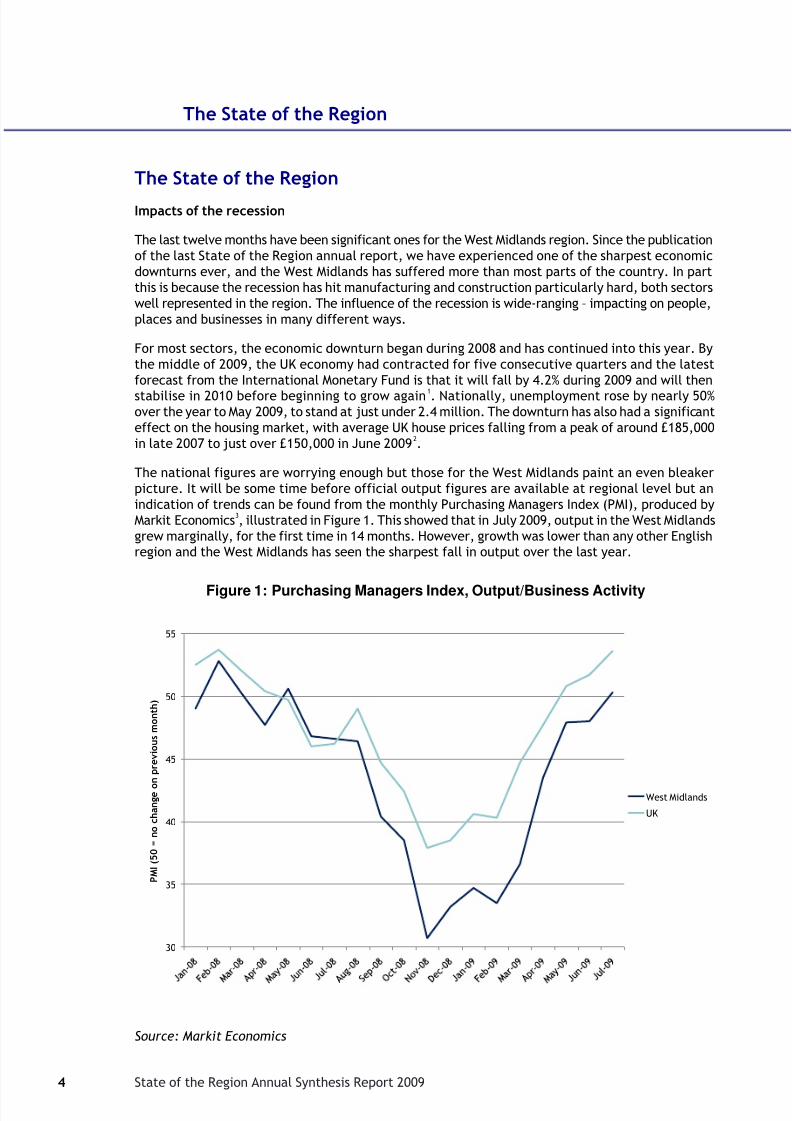

The last twelve months have been significant ones for the West Midlands region. Since the publicationof the last State of the Region annual report, we have experienced one of the sharpest economicdownturns ever, and the West Midlands has suffered more than most parts of the country. In partthis is because the recession has hit manufacturing and construction particularly hard, both sectorswell represented in the region. The influence of the recession is wide-ranging – impacting on people,places and businesses in many different ways.

For most sectors, the economic downturn began during 2008 and has continued into this year. Bythe middle of 2009, the UK economy had contracted for five consecutive quarters and the latestforecast from the International Monetary Fund is that it will fall by 4.2% during 2009 and will then

stabilise in 2010 before beginning to grow again1. Nationally, unemployment rose by nearly 50%over the year to May 2009, to stand at just under 2.4 million. The downturn has also had a significanteffect on the housing market, with average UK house prices falling from a peak of around £185,000in late 2007 to just over £150,000 in June 2009

2.

The national figures are worrying enough but those for the West Midlands paint an even bleakerpicture. It will be some time before official output figures are available at regional level but anindication of trends can be found from the monthly Purchasing Managers Index (PMI), produced byMarkit Economics

3, illustrated in Figure 1. This showed that in July 2009, output in the West Midlands

grew marginally, for the first time in 14 months. However, growth was lower than any other Englishregion and the West Midlands has seen the sharpest fall in output over the last year.

30

35

40

45

50

55

P M I ( 5 0 = n o c h a n g e o

n p r e v i o u s m o n t h )

Figure 1: Purchasing Managers Index, Output/Business Activity

West Midlands

UK

Source: Markit Economics

State of the Region Annual Synthesis Report 20094

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 7/35

Although output has fallen quickly overall, some economic sectors have fared worse than others.

Work undertaken for the West Midlands Taskforce

4

identified a number of sectors which wereparticularly vulnerable: automotive manufacturing, ceramics, manufacture of basic metal products,construction, property services, transportation, financial services, independent retailers &wholesalers, manufacture and sale of luxury goods, local government and pubs, bars & restaurants

5.

Some sectors are doing better, however. For example, an Observatory survey has found that theenvironmental technologies sector is doing relatively well, with many firms still actively diversifyingand recruitment continuing, particularly of individuals with specific skills

6. Some cultural

organisations have seen an increase in business and visits to attractions in the region are holdingup well, with numbers down by only 3% compared to 5% across the whole of England. Free attractionsare faring particularly well, for example visits to English Heritage properties were up by nearly 50%in June 2009 compared to a year earlier

7. Other sectors which have been affected less include

public services (other than local authorities), land-based industries and personal services8.

The West Midlands has also seen a sharp rise in numbers of people out of work as a result of theeconomic downturn. Whilst the national unemployment rate rose from 5.2% to 7.6% over the yearto May 2009, the figure for the region rose from 6.2% to 10.3%, significantly increasing the gapbetween the regional and national figures. This amounted to an extra 111,000 unemployed peopleout of a total of 276,000 in the region

2. This was driven by an increasing number of people becoming

unemployed in the region, with little change in the rate at which people were able to find work.

This increase in unemployment has not been evenly distributed between different groups of people.Young people (those aged under 25) have been particularly badly affected. They already had amuch higher unemployment rate than average but have seen that rate increase by 8 percentagepoints in the year to March 2009, up to 23.4%. This compares with an increase of 3 percentagepoints for those between 25 and 49, and just over 1 percentage point for those between 50 andretirement age9.

Another group which has suffered increased unemployment is that of people with no qualifications,whose unemployment rate has increased by nearly 6 percentage points, roughly twice the increaseamongst those with qualifications. Having said that, the recession has also hit those with higherlevel qualifications; the numbers involved are smaller but they are sufficient to increase the shareof unemployed people with higher qualifications from 8.2% to 11.2%.

Some groups that have traditionally suffered from high levels of economic exclusion do not seemto have been hit as hard by the recession. For example, the increase in the unemployment rate forthose with a disability has been smaller than average. The same is true for some minority ethnicgroups, particularly those of Asian origin. Nevertheless, these groups still have higher unemployment

rates than average, although the gap between their rate and that for the rest of the populationhas decreased slightly9.

5State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 8/35

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

O v e r a l l

A g e d 1 8 - 2 4

A g e d 2 5 - 4 9

A g e d 5 0 +

W h i t e - B r i t i s h

O t h e r W h i t e

M i x e d

I n d i a n

P a k

i s t a n i / B a n g l a d

e s h i

B l a c k o r B l a c k

B r i t i s h

C h

i n e s e o r O t h e r

Figure 2: Change in West Midlands claimant unemployment rate

by age and gender, June 2008 to June 2009

Jun-08

Jun-09

Source: Department of Work and Pensions, JSA Claimant Count

Alongside the increase in worklessness, the region has seen a corresponding fall of 88,000 peoplein employment, equivalent to 3% of the workforce. However, that fall has been concentratedamongst those in full-time, permanent employment. The number of part-time workers has fallenby just 3,000, whilst numbers in temporary employment have increased by 6,000. Evidence suggeststhat many more people are working part-time or in temporary jobs due to a lack of alternativeoptions. Around 13% of part-time workers and 30% of temporary workers would prefer to be workingfull-time and in permanent roles, both figures much higher than a year ago. This suggests that thetrue employment effect of the recession may be greater than implied by the headline figures

9.

Despite this picture, many firms have continued to recruit during the recession, particularly toensure that they have the right skill base to survive and prepare for the upturn. Around a third offirms who were attempting to recruit were still struggling to find people with the skills, experienceand qualifications they required. As a result, employer investment in workforce training has heldup relatively well during the recession

8.

The fall in house prices in the West Midlands has been lower than across the whole of England andWales. Over the year to June 2009, the average price of a house in the region fell by around 12%to £130,810

10, compared to a fall of 14% nationally. The fall in the region over that period was the

lowest of any of the English regions (or Wales).

Although all parts of the region have suffered during the recession, some local areas have been hit

harder than others. For example, the proportion of people claiming Jobseekers’ Allowance hasrisen everywhere in the region, from 3.6% in June 2008 to 6.4% a year later. However, the largestrises have been seen in a mix of traditional hot-spots like the Black Country (Walsall has seen thelargest rise in the region, up from 3.8% to 7.2%) but also in areas such as Redditch (up from 2.2%

State of the Region Annual Synthesis Report 20096

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 9/35

to 5.5%), Cannock Chase (up from 2.1% to 5.2%) and Tamworth (up from 1.8% to 4.9%). These places

have also seen some of the largest percentage increases in claimants, along with places likeBridgnorth, Staffordshire Moorlands, North Warwickshire and much of Worcestershire. Althoughthese areas still have relatively low levels of unemployment, rates are now more than 2½ timeshigher than a year ago

2.

Preparing for the recovery

But it’s not all doom and gloom. Although no-one can be sure how long the recession will last, orhow deep it will be, we do know that it will end. Some of its effects will be felt for years to come,with employment unlikely to return to its previous levels until well into the next decade

11.

Nevertheless, the region’s future prosperity depends on positioning ourselves so that we are ableto take maximum benefit from the upturn. There are no simple answers to this but the State ofthe Region process provides some important evidence.

The publication of West Midlands: Fit for the Future marks an important point in the debate. Thebook, published by the Observatory in July, comprises ten chapters written by different authorsgiving their perspective on how the region should position itself for the future. The authors rangefrom politicians to academics, bankers to environmentalists, trade unionists to business leaders.Not surprisingly, there were some differences of opinion. However, there was a consensus that thisis the right time to have the debate, and optimism that it can lead to an improvement in the region’ssituation – whether that is measured economically, socially or environmentally (or all three).

The debate will continue, particularly at the Observatory’s annual conference. However, the bookitself, along with reports from the other State of the Region dialogues, provides evidence whichcan contribute to that debate, and help to inform the new Strategy for the West Midlands.

One common theme which emerges from views on surviving the recession, including several chaptersof West Midlands: Fit for the Future, is the importance of innovation. The region has a long historyof innovation – after all Ironbridge is known as the birthplace of the industrial revolution. However,over time the region’s relative innovation performance has weakened, as the economic structureof the region has shifted. Reversing that trend will be important. Whilst product innovation willcontinue to be important, given the size of the region’s manufacturing base, we will need to thinkwider than this.

The State of the Region thematic report on Innovation in a Changing Economy highlights howinnovation is changing. Increasingly, effective innovation involves breaking down barriers – betweenservices and products, between the public, private and education sectors, between individual firmsand between companies and their customers. Thinking needs to be long-term and we need to beprepared to take some risks, as did the industrial pioneers who were so important to the region’spast prosperity.

Of course, effective innovation also relies on having people with the right skills, to come up withnew ideas, to spot which ones will be winners and to turn them into reality. Businesses will needto recognise that the best ideas won’t just come from within and that they will get benefits fromworking with others. This will happen most effectively in places where there are concentrationsof people with the skills needed to generate and exploit new ideas, as highlighted within thethematic reports on Innovation in a Changing Economy and The West Midlands Knowledge Economy .

The region’s performance on skills has improved over recent years but there is still much more todo. The report on The West Midlands Knowledge Economy highlights the importance of attractingand retaining graduates. We have a number of leading universities in the region but this hasn’t

translated into a thriving knowledge economy, as in some other parts of the country. There are avariety of reasons for this, including the image of the region and the quality of life it can offer.

7State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 10/35

However, attracting and retaining people with the right skills won’t be enough on its own. Equally

important will be how those skills are deployed within the regional economy. The region currentlyhas particularly low levels of graduates employed within its private sector businesses, where theymade up just 23% of the workforce in 2008, compared to 28% across the whole of England

12. This

impairs their ability to innovate and, ultimately, leads to lower productivity and greater vulnerabilityto economic downturns. Addressing this will require change in the leadership and managementculture in the region’s businesses, as highlighted in The West Midlands Knowledge Economy .

Of course, the recession doesn’t only affect businesses. As highlighted above, there are significantimpacts on communities too. This is particularly true of those communities which were alreadysuffering or those which rely heavily on a single, vulnerable industry, or even a single employer.This highlights some of the issues raised by the thematic report, What Makes a Community

Sustainable? This report highlights that the most sustainable communities are those which have anappropriate balance of economic, social and environmental conditions. They will also be diverse

in each of those elements, whilst still being united by a common interest. Ensuring our communitiesare sustainable will be important for the future development of the region.

Increasingly, the communities that matter to people are wider than just those which aregeographically based. Many people now associate more closely with communities based aroundtheir workplaces or their leisure pursuits, some of which are “virtual”. This trend has importantimplications for people affected by the recession, who may lose their support networks along withtheir jobs. It also has implications for deciding the best approach to providing support in theshort-term and for developing policies for the longer-term.

Despite this change, one potential impact of the recession will be a renewal of local communitiesin some important respects. The slowdown in the housing market may reduce, or even reverse, thehistoric trend of migration from the urban parts of the region to the surrounding rural areas, ashighlighted in the thematic report The West Midlands’ Changing Population. This could provide anopportunity to improve the sustainability of communities in both urban and rural areas, by balancingthe mix of people living and working in each.

Another possible consequence of the recession is that there may be an increasing desire to sourcemore products locally rather than risk exposure to problems in the global economy. This could alsoinvolve greater reuse of goods or waste locally, reducing both the use of natural resources andemissions associated with transport. Decentralised energy generation is another way in whichincreased localism could help reduce carbon emissions, as well as providing improved energysecurity. These potential changes could aid the development of more sustainable communities,meeting more of their own needs now and into the future. They could also have significant benefitsfor the regional economy which is currently a significant net-importer of energy, goods and services.

Increased local production also has potential environmental benefits, with reduced needs fortransportation leading to reduced carbon emissions, mitigating against climate change. This is oneof the issues explored in the thematic report, Challenge or Opportunity? How to Plan for Climate

Change. The short-term reduction in economic activity resulting from the recession obviously hasan impact on levels of emissions, although not for the right reasons. However, the recession mayalso act as a driver for firms to reduce costs by increasing their energy and resource efficiency,providing long-term benefits.

Facing up to the challenges

The advent of the recession means that the West Midlands faces a number of new challenges,particularly in the short term. However, that doesn’t mean that the challenges it already faced

have gone away. Indeed, some may have been reinforced by the recession. Last year’s State of theRegion Annual Report identified 12 challenges, drawn from different policy areas. All have beencovered during the year by the State of the Region process or other regional research.

State of the Region Annual Synthesis Report 20098

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 11/35

Closing the £10 billion output gap by improving productivity and economic inclusion

Most fundamental of all the challenges facing the West Midlands is the underperformance of theregion’s economy. Available data predates the recession but shows that, even then, the region’soutput gap had continued to grow. In 2007, the region’s output per person was £17,161, around£2,800 lower than the UK average. When scaled across the region’s population that amounts tonearly £15 billion. The increase is partly down to changes in the way that regional output (GVA) iscalculated but, even after that has been taken into account, the gap has increased by around £2billion over the last two years

13. It is too early to say how the recession will impact on the output

gap, but indications are that the region has fared worse than average and that the gap may havegrown still further.

0

2

4

6

8

10

12

14

16

1 98 9 19 90 1 991 1 99 2 1 99 3 19 94 1 995 1 99 6 1 99 7 1 99 8 1 999 2 00 0 2 00 1 2 002 2 00 3 2 00 4 20 05 2 006 2 00 7

O u t p u t

G a p

( £ b i l l i o n )

Figure 3: Growth of the West Midlands Output Gap 1989-2007

Source: Office for National Statistics, Regional GVA

The Observatory is currently undertaking research across a number of key areas, aiming to understandwhat causes the output gap. Two of these areas are innovation and enterprise.

On innovation, across a range of measures, the region underperforms the UK, although it doesbetter than the EU average. The West Midlands matches the UK in terms of applications of innovation,covering aspects such as sales of new products and employment in high-technology businesses, yetit lags behind in other important respects such as investment levels, collaboration and humancapital. Nevertheless, things are improving, with regional businesses becoming more active in termsof innovation and generating a greater share of their turnover from innovative activities

14.

However, big challenges remain. The State of the Region thematic report, Innovation in a Changing

Economy , looks at what innovation means in today’s economy with its increasing focus onknowledge-based industries and the long-term shift from production to services, as well as anincreasing blurring of the boundary between the two. Closing the output gap will mean not just

9State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 12/35

innovating more, but also utilising new forms of innovation such as more collaboration between

organisations, increasing emphasis on design aspects and greater involvement of users in thedevelopment of products and services.

Enterprise influences the output gap in many ways. The region has too few businesses and they arenot as productive as those in some other regions. In particular, we have a low share of some of themost productive sectors. Most notable in this respect are financial and business services, whichbetween them account for around 70% of the output gap

14.

The financial services sector is dominated by London, the most productive region, and the WestMidlands is unlikely to be able to compete with the capital’s global pre-eminence in this sector

15.

London also performs strongly in business services but here the region may be better able tocompete. However, at the moment the sector is insufficiently productive in the West Midlands,partly because of the low share of employment in managerial and professional occupations, the

jobs which generate the most value16

.

Improving the reliability of the Region’s transport network allowing it to take advantage of its central location

A comprehensive, reliable and sustainable transport network is important to the region in manyways: it provides access to markets, and to a suitable workforce, for the region’s businesses; itallows individuals to access employment opportunities, services and leisure activities; and it doesso in a way which is safe and enhances or avoids damage to the environment.

Transport improvements can bring economic benefits through reducing costs associated with journeytimes or unreliability, bringing businesses closer together, improving accessibility of markets andimproving individuals’ access to work. In addition, schemes can provide a range of welfare benefits,

such as commuting and leisure journey time savings, environmental and safety benefits.

During the year, the Observatory has analysed the economic case for the transport schemes whichhave been identified as regional priorities. This found that the schemes which yielded the mosteconomic benefits were those which:

Were located on strategically important routes, with high volumes of business and freighttrips; or

Were located in areas suffering from high levels of congestion, in both peak and off-peakperiods; or

Involved a significant development or regeneration element; or

Use existing infrastructure better, through improved management of traffic, for example

through improved intelligent signalling systems or variable message signs.Work undertaken to inform the region’s contribution to DfT’s Developing a Sustainable TransportSystem programme has identified other ways in which transport can contribute to regional goals.As well as the economic benefits, transport improvements can contribute to reducing carbonemissions, improving safety, security and health, enabling equality of opportunity and enhancingquality of life

17.

Transport networks also have an important role to play in the response to climate change, ashighlighted within the thematic report Challenge or Opportunity? How to Plan for Climate Change.

This identifies how future transport systems could reduce the need to travel, for example by locatingemployment sites closer to the homes of their workers, and encourage modal shift by providing agreater variety of options for the use of public transport, walking and cycling.

State of the Region Annual Synthesis Report 200910

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 13/35

Reducing worklessness so that more of the population are able to contribute to economic

prosperity

Whilst the region’s economic performance is closely linked to the productivity of its businesses,another key factor is the extent to which everyone in the region is able to make an economiccontribution. High levels of worklessness prevent this from happening.

The effect of worklessness on some key groups – notably minority ethnic groups and those with adisability or health problem - is highlighted later in this report. However, worklessness problemsare more widespread than this. In May 2009, about 30% of the region’s working age population werenot in employment, an increase of 2.7% compared with a year earlier. This amounted to nearly100,000 more people who were not in work. The region was already performing poorly but the gapwith the national average has widened

9.

Research undertaken for the Economic Inclusion Panel has identified that people with noqualifications and those aged under 25 are particularly likely to be workless, along with those withdisability or health problems and those from certain minority ethnic groups. Around one in threeclaimants of Jobseekers’ Allowance are aged between 18 and 25 and this age group has beenparticularly hard hit by the recession. Older people, those aged over 50, are also less likely to bein work than those aged between 25 and 49

19.

As well as understanding which groups are most likely to be workless, the research also looked atthe barriers which people face to entering, or retaining, work. Amongst the most important factorsidentified are:

Disability or poor health

Low skill levels, particularly language, numeracy and literacy problems

Lack of relevant work experience or a poor work historyEmployer attitudes or discrimination

Low confidence

Caring responsibilities

Financial considerations, such as loss of benefits and low pay

Lack of personal transport and poor public transport

Many of these factors are inter-related and some individuals will be affected by more than one ofthem. Those people facing multiple disadvantages will be particularly hard to reach and will sufferthe greatest difficulty in accessing work

18.

Raising qualification levels and reducing the number of people without qualifications

Another key influence on the output gap is the level of skills amongst the region’s workforce. Theimpact is felt in many ways, amongst them the ability of individuals to find work, their productivitywithin their jobs and the region’s ability to attract the kind of knowledge-intensive businesses itwill need for the future.

Historically, the region’s performance on skills has been poor. More recently, however, theObservatory’s Skills Performance Index has shown that things are improving. In 2003, when theindex was first introduced, the region was below all other English regions and was 6 points belowaverage. By 2008, the gap had closed to 1 point and the region was ranked fifth out of nine regions.This improvement has been driven by increasing commitment to skills development, both byemployers and individuals. For example, more employers were involved in the Train to Gainprogramme than anywhere else in England, Apprenticeships had the highest success rates in the

country and the number of young people remaining in education now matches the national average12.

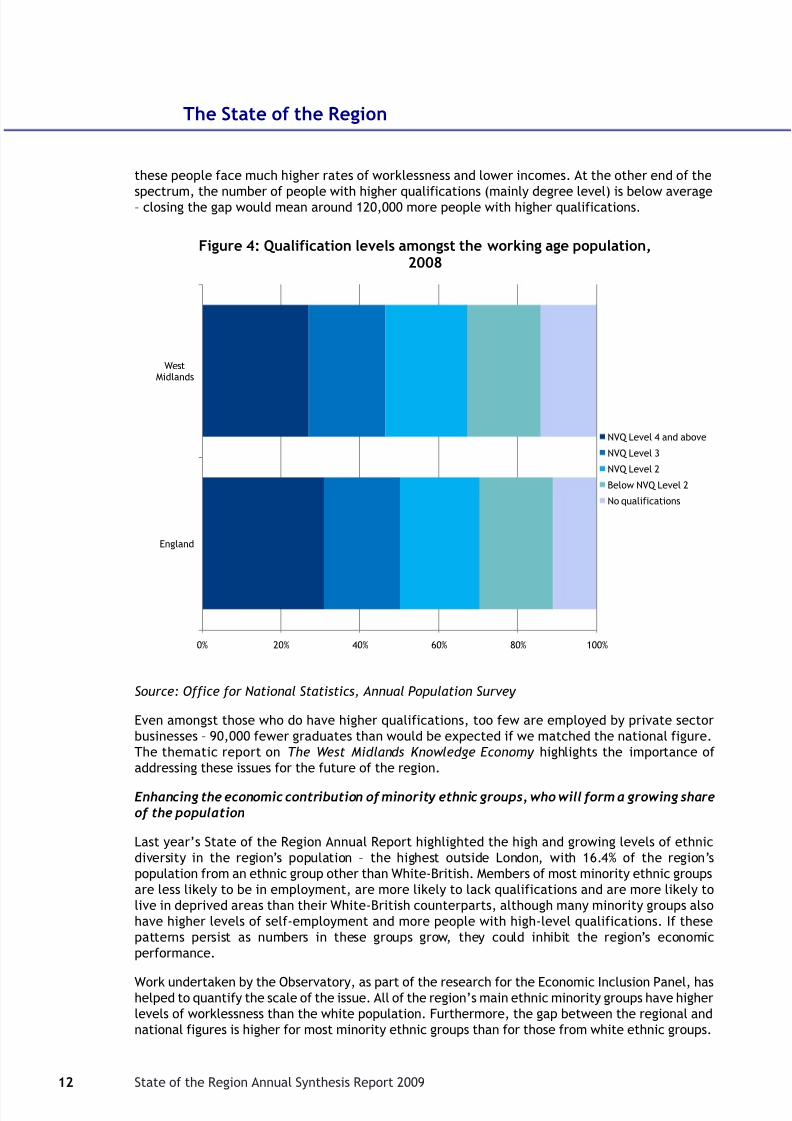

Nevertheless, some important skills challenges remain. There are still too many people with noqualifications, at 14% the highest figure in the country – nearly 100,000 people would need to gaina qualification for the first time to close the gap with the national average. As discussed earlier,

11State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 14/35

these people face much higher rates of worklessness and lower incomes. At the other end of the

spectrum, the number of people with higher qualifications (mainly degree level) is below average– closing the gap would mean around 120,000 more people with higher qualifications.

0% 20% 40% 60% 80% 100%

WestMidlands

England

Figure 4: Qualification levels amongst the working age population,2008

NVQ Level 4 and above

NVQ Level 3

NVQ Level 2

Below NVQ Level 2

No qualifications

Source: Office for National Statistics, Annual Population Survey

Even amongst those who do have higher qualifications, too few are employed by private sectorbusinesses – 90,000 fewer graduates than would be expected if we matched the national figure.The thematic report on The West Midlands Knowledge Economy highlights the importance ofaddressing these issues for the future of the region.

Enhancing the economic contribution of minority ethnic groups, who will form a growing shareof the population

Last year’s State of the Region Annual Report highlighted the high and growing levels of ethnicdiversity in the region’s population – the highest outside London, with 16.4% of the region’spopulation from an ethnic group other than White-British. Members of most minority ethnic groupsare less likely to be in employment, are more likely to lack qualifications and are more likely tolive in deprived areas than their White-British counterparts, although many minority groups alsohave higher levels of self-employment and more people with high-level qualifications. If thesepatterns persist as numbers in these groups grow, they could inhibit the region’s economicperformance.

Work undertaken by the Observatory, as part of the research for the Economic Inclusion Panel, hashelped to quantify the scale of the issue. All of the region’s main ethnic minority groups have higherlevels of worklessness than the white population. Furthermore, the gap between the regional andnational figures is higher for most minority ethnic groups than for those from white ethnic groups.

State of the Region Annual Synthesis Report 200912

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 15/35

Nearly 75,000 more people from minority ethnic groups would need to enter employment to match

the employment rate amongst white people. This is made up of about 19,000 people from the Blackor Black British population, 11,000 people of Indian background and nearly 45,000 people fromPakistani or Bangladeshi communities. It is worth noting, however, that cultural attitudes amongstPakistani and Bangladeshi communities mean that relatively few women from those groups are inwork, inflating the last figure

19.

The figures quoted above pre-date the current economic slowdown. More recent data suggest thatsome minority ethnic groups are not being affected as badly by the recession as the population asa whole. This is despite the fact that two groups which are badly affected, young people and thosewith no qualifications, are more numerous amongst ethnic minorities. All ethnic groups have seena rise in claims for Jobseekers’ Allowance. However, the rise has been lower amongst those of Asianor Asian British origin and amongst non-British white ethnic groups. Rises have been highest amongstthose from Black or Black British groups, who already had the highest claimant rates

9.

In recent years, one of the key drivers of the region’s increasing diversity has been growinginternational migration, particularly from the new member states

20which joined the European

Union in 2004. Latest figures suggest that the number of incoming migrants has slowed, with around43,200 registering to work in the region during 2008, compared to 53,400 in 2007. Most of that fallwas due to a drop in the numbers from new EU member states, which dropped from 28,500 to20,900

21. At the same time, the number of non-UK nationals emigrating from the UK rose by 24%

and the number from the EU member states more than doubled, although regional figures are notavailable.

The State of the Region report on demographic change, The West Midlands’ Changing Population,

looks at some of the implications of the growing ethnic diversity of the region. For example, serviceproviders will need to become increasingly flexible, adapting to differing needs as a result oflanguage, regional and local identities or cultural values and practices. The forthcoming dialoguelooking at equality and diversity will develop this further and consider some of the factors influencingthe differences in labour market outcomes faced by different ethnic groups.

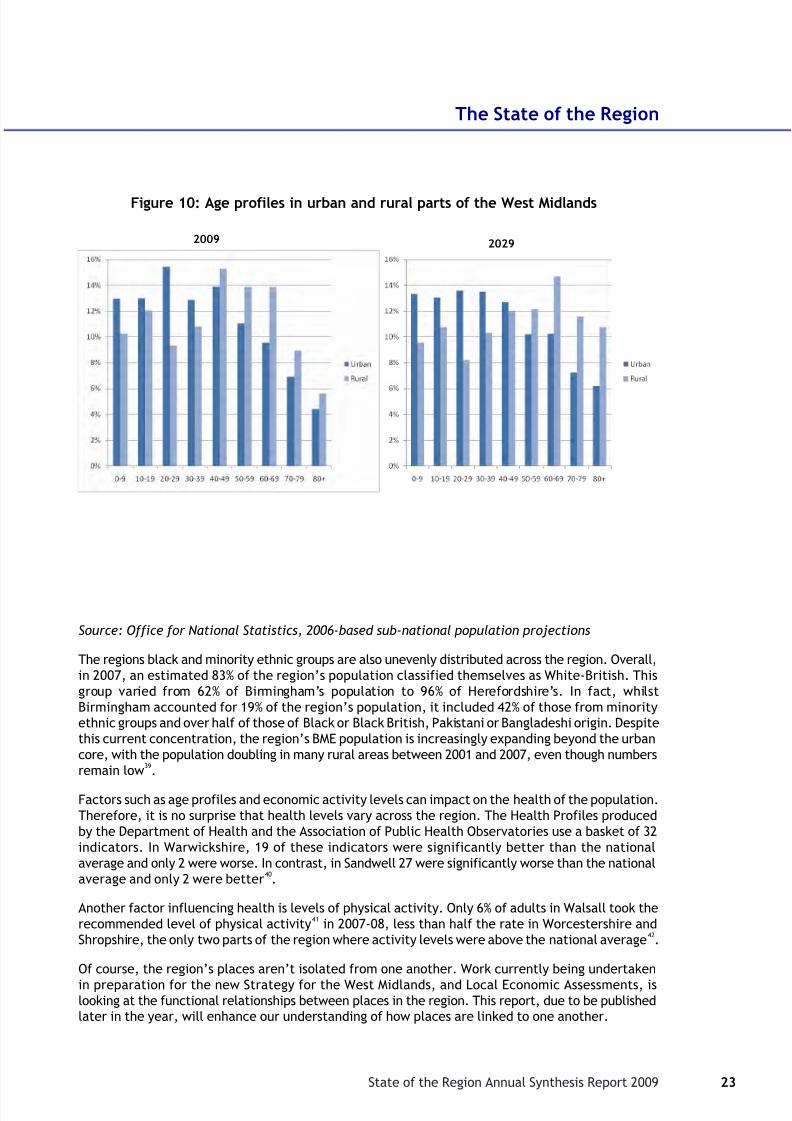

Addressing the needs of an ageing population and a growing gap in age profiles between urbanand rural areas

Another growing section of the population is people in older age groups. However, this growth isnot evenly distributed across the region. Latest population estimates show that the gap betweenthe age profiles of urban and rural parts of the region continues to grow. Projections show thatthis gap is likely to continue to grow with a significant rise in the elderly population in rural areas,compared with only modest growth in urban areas.

Over the next 20 years, the population of the region is projected to grow by around 11%, reachingalmost 6.1 million by 2029. However, over that time the number of people aged over 85 is expectedto double so that age group will rise from just over 2% of the region’s population to nearly 4%. Thepopulation aged 65 and over will rise from 17% to 22% of the total. This age group is projected to

13State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 16/35

overtake the numbers aged under 15 in around 2014, although this will differ across the region, for

example the proportion aged 65 and over in Herefordshire will be more than twice that inBirmingham, 32% in the former, 14% in the latter22

.

Figure 5: Age profile of West Midlands population, 2009 and 2029

-500 -400 -300 -200 -100 0 100 200 300 400 500

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80-84

85+

Population (thousands)

2009

2029

Source: Office for National Statistics, 2006-based sub-national population projections

Some of the implications of this are explored in the thematic report The West Midlands’ Changing

Population. For example, the older population will place increasing pressures on health and careservices. This suggests that innovative approaches will be needed to deliver a higher volume ofservices within budgetary constraints. In addition, as the population aged 65 and over rises, the

proportion of the region’s population who are of working age will fall. Unless productivity improves,or worklessness falls, amongst the working age population, this could lead to a decline in theregion’s output per head, reducing its prosperity overall.

Improving lifestyles to prevent future health problems developing

Another consequence of the ageing population is that there are likely to be more people sufferingfrom disabilities or long-term health problems. Many of these would like to work but struggle todo so. The Observatory’s work on economic inclusion has highlighted the close links between healthproblems and other forms of exclusion. People with a disability or long-term health problem aremore than twice as likely to be workless than the rest of the population. This amounts to a totalof 315,000 people, more than one in three of those who are not working

19.

This is reflected in figures in relation to benefit claimants illustrated in Figure 6. Over half of peopleclaiming out-of-work benefits in 2007 were on incapacity benefits. This number is more than doublethe numbers who were claiming Jobseekers’ Allowance at the time. Around four in five of claimants

State of the Region Annual Synthesis Report 200914

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 17/35

of incapacity benefits had been claiming for two years or more and three in five for over five years.

In fact, after 2 years claiming these benefits, a person is more likely to die or retire than to everwork again.

Figure 6: Out-of-work benefit claimants – West Midlands

Jobseekers’

Allowance

IncapacityBenefits

Loneparents

Otherbenefits

Source: Department of Work and Pensions, Benefit Claimant Data

Figure 6 also shows that around 40% of incapacity benefit claimants are suffering from mental andbehavioural disorders. Wider evidence suggests that this group is particularly unlikely to be working,even though the large majority have illnesses which would not prevent them from working ifappropriate support was in place for them

19.

Recent changes to the welfare and benefits systems, including the replacement of IncapacityBenefits with the new Employment Support Allowance are aimed at providing people with thesupport they need to prepare for and find work. Nevertheless, given the current economic downturn,these reforms face a particular challenge. It will be important to ensure that those people beingmade redundant don’t end up suffering from the sort of mental health problems which could leadto them finding it hard to return to work in the future.

Raising participation in cultural and sporting activities

One way of improving health and well-being is participation in sporting and cultural activities. Lastyear’s State of the Region report highlighted the relatively low levels of participation in culturaland sporting activities in the region. Latest data suggests that little has changed.

During the past year, the Regional Cultural Observatory, which is co-located with the RegionalObservatory, has produced two major evidence papers

23,24. The cultural sector forms an important

and growing part of the region’s economy, representing nearly a tenth of regional output according

15State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 18/35

to the latest figures23

. Productivity is also above average and the sector is not suffering as much as

some in the recession, as people see it as providing an opportunity to escape from the problemsthey are facing7.

But participation in cultural and sporting activities has much more than simply economic benefits.There are major health and well-being benefits, from obvious ones such as the reduction of obesityassociated with sporting activity to the less obvious such as improved mental health amongst thoseparticipating in arts-based activities. Cultural activities can also help engage people in learning,bring communities together and encourage those who are socially excluded to participate

24.

The region has a range of important cultural assets which can be used to encourage participation.Work published this year identified 16 internationally important cultural assets in the region, rangingfrom arts venues, through festivals and heritage assets to sporting venues

25. The work also identified

some gaps, notably the relative lack of cultural assets in the west and north of the region.

Complementing this work on the supply of cultural assets, this year has also seen the completionof a major study looking at the demand for cultural activities in the region. This highlighted twomain drivers of cultural participation – spending quality time with family & friends and enjoyingrespite or escapism from work or everyday life. The latter has grown in importance as economicconditions have worsened. However barriers such as cost, lack of awareness, accessibility and thelack of a “culture of culture” in many communities contribute to relatively low levels ofparticipation

26.

Improving the image of the Region to encourage people and businesses to locate here

The region’s cultural offer is one of the key elements influencing how people see the West Midlands.Whatever the true state of the region is, the decisions that people take will be influenced by their

perceived image of it. Those decisions will determine the future of the region, be they aboutwhether to live here or locate a company here, to invest in a property or a business, to come hereto study or to visit for leisure or for business. It is not enough simply to change the region – for itto succeed, we will need to change how people see the region.

Over the last two years, the Observatory has been developing the Regional Perceptions Indicator.This is one of the headline impact measures in the West Midlands Economic Strategy, emphasisingthe importance of image for the future of the region. The first results of the new indicator are dueto be published in November 2009 and they will, for the first time, allow us to compare people’sperceptions of the West Midlands against those of other parts of England.

The new State of the Region dialogue on Regional Image and Identity, which starts in the autumn,will build on the Regional Perceptions Indicator and a range of other evidence about how the regionis seen. It will help to establish what the main image problems that the region faces are and whatneeds to be done to improve them.

Protecting the natural environment whilst taking advantage of opportunities brought aboutby climate change

Another key influence on perceptions of the region is the state of the region’s environment, which,as a result, will be crucial to its future prosperity. The State of the Region report on The West

Midlands Knowledge Economy emphasises the importance of a quality environment to attract theright people and businesses to the region – and the natural environment is a key component of that.But the environment faces a number of inter-related threats – the handling of waste, limited waterresources, pressure on land use and, of course, climate change amongst them.

State of the Region Annual Synthesis Report 200916

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 19/35

The latest UK Climate Projections (UKCP09) were launched in June. Figure 7 illustrates some of

the main projected changes in the West Midlands climate

27

.

Figure 7: Projected Climate Change Scenarios for the West Midlands

Source: UK Climate Impact Programme, UK Climate Projections (UKCP09)

The changing climate will have many consequences, including changes to the natural environment,which will require us to adapt the way that we live our lives and run our businesses. Failure to doso could have serious consequences, such as health problems (including a rise in premature deaths),water shortages, increased flooding affecting homes and businesses and degradation of naturalhabitats which are already particularly fragmented in this region. We could also be affected by the

even greater impacts of climate change elsewhere in the world, for example through migration ofthose worst affected or through loss of food production. Some of these issues are explored in thethematic report, Challenge or Opportunity? How to Plan for Climate Change.

Even if carbon emissions fall to lower levels, climate change will still happen because of pastemissions. The results will be a little less dramatic but will still have significant consequences.Over the last year, the Observatory has begun a programme of work looking at how the region canmove to a low-carbon economy. One important aspect of that has been to look at what more weneed to do to reach targets for reducing carbon emissions. This shows that, even if all existingpolicies are implemented, there will still be a gap of 1.75 million tonnes of CO

2per annum to the

2020 target. This is 330kg per person, equivalent to one return flight from Birmingham to Rome ordriving 1,250 miles in a Ford Fiesta

28.

17State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 20/35

But climate change, and the culture changes that it will require, provide economic opportunities

for the region too. Previous work indicates that the region is well placed to take advantage. Noneof our most important business sectors will be amongst those which suffer the most from restrictionson carbon emissions

29. At the same time, we already have a strong environmental technologies

sector, part of a global industry expected to be worth US$1 trillion within the next three years.

The thematic report also looks at some of the opportunities which climate change will present.This builds on work to develop a low carbon vision for the region, which was discussed at the initialworkshop for the climate change dialogue. This sets out how the region could look in 2020, if itfully embraces a low-carbon future. It contains innovative ideas such as vertical urban farms andbio-digesters replacing old-style power plants, as well as the development of green infrastructureand sustainable transport networks

30. All these ideas are feasible, but will require improvements

in many policy areas, including innovation, skills and land-use. The thematic report explores someof these connections further.

Building more houses in response to growing demand while protecting the environment

Whilst climate change is a potential threat to the environment, it isn’t the only one. Increasingpressure on land use has the potential to reduce and fragment the amount of natural greenspacein the region.

In its statutory capacity of Regional Planning Body, the West Midlands Regional Assembly has advisedthe Government that 365,600 dwellings should be built in the Region between 2006 and 2026 andhas recommended a distribution for these new dwellings across the Region

31. Overall this represents

a 40% increase over and above the housing proposals in the currently approved Regional SpatialStrategy (RSS). The proposed distribution carefully balances the requirement to meet housing needswhile supporting the continued regeneration of the Major Urban Areas and protecting the

environment. Following the recent Examination in Public on the Phase 2 RSS Revision, planninginspectors have recommended increasing this total to 398,000 new homes

32. A response from

Government is expected later in the year.

The current difficulties being experienced by the housing market as a result of the economicrecession are highlighted by a fall of average house prices in the region of 15% since 2007 and areduction of 51% in new housing starts. The full recovery of the housing construction sector is stillsome way off and the industry will struggle, at least in the short to medium term, to build sufficientnew houses and to fulfil its obligations with respect to the funding of infrastructure to open up newhousing sites, meeting zero carbon design standards and providing contributions towards affordablehousing.

A particularly pressing issue is around the provision of affordable (‘social’) housing to meet theneeds of households who cannot afford to purchase in the open market. It is estimated that up to40% of all the RSS new housing provision could be needed for affordable housing but, at this time,this is likely to be hard to implement

33. Opportunities for additional affordable housing will therefore

need to be sought through the existing housing stock.

Increasingly, the future volume and distribution of new housing will need to be linked to theeconomic development of the region. The availability of the right mix of housing is crucial to buildingsustainable communities and to attracting people and businesses to the region. These factors arehighlighted in the State of the Region thematic reports, What Makes a Community Sustainable?

and The West Midlands Knowledge Economy .

Addressing anti-social behaviour and improving access to services to raise quality of life

As highlighted in the State of the Region thematic report, The West Midlands Knowledge Economy ,quality of life issues are important to the region’s economy as well as to its people and communities.A variety of issues impact on quality of life, many of them covered elsewhere in this report.

State of the Region Annual Synthesis Report 200918

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 21/35

The importance of quality of life to the economic performance of the region is reflected in the

inclusion of the Regional Index of Sustainable Economic Well-being (R-ISEW) as one of the headlineimpact measures for the West Midlands Economic Strategy. The R-ISEW adjusts regional output totake account of various economic, social and environmental factors. The aim is to give a truerpicture of the economic well-being of regions

34.

Latest figures show that, whilst regional output grew steadily between the early nineties and 2006,economic welfare remained fairly static. As a result, the gap between the two measures increased,suggesting that the regional economy was becoming less and less sustainable, and that quality oflife wasn’t improving as much as it could have. The most significant reasons were the impact ofclimate change and resource depletion, the costs of income inequalities, the high level of importscompared to exports and costs associated with commuting and traffic accidents.

Figure 8: West Midlands R-ISEW and GVA per head1994-2006

Sources: Office for National Statistics Regional GVA,

New Economics Foundation Regional Index of Sustainable Economic Well-being

Another factor which has some impact on the R-ISEW is crime. Last year’s State of the Region AnnualReport highlighted the importance of crime in determining quality of life. It also highlighted thatcrime levels are relatively low in the region, particularly when compared with similar areas elsewherein the country. Since then, total recorded crime has fallen further, down by 6% in the region, slightlyhigher than the national fall.

Dealing with issues like crime and access to services, also highlighted in last year’s report, is

particularly important in establishing sustainable communities. They are amongst the issues exploredin the thematic report, What Makes a Community Sustainable? This report explores how quality oflife can be addressed as part of the wider drive to create sustainable communities.

19State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 22/35

Integrating the Evidence

The challenges which the region faces are inter-connected in a variety of complex ways. Dealingwith the challenges effectively will mean understanding how they influence one another. Helpingto achieve this understanding is an important role for the regional evidence base. The issue hasbeen highlighted in State of the Region reports right back to the very first one in 2004, which lookedat how these connections impacted on the lives of individuals in the region.

That is why several of this year’s State of the Region thematic reports focus particularly on howthe issues that they cover will impact across a wide variety of policy areas. Indeed, all of the reportshighlight broad implications requiring action from many different policy-makers and practitioners,not just those in the most immediately relevant areas.

Climate change is one policy area which has particularly wide-ranging impacts. This is recognised

in the thematic report on the subject, Challenge or Opportunity? How to Plan for Climate Change.Much of the evidence about the causes and impacts of climate change was set out in the State ofthe Region Update report in 2007. Rather than repeating that, this year’s report concentrates onwhat the evidence means for other policy areas. In some cases, impacts are mainly around reducingcarbon emissions, to meet government targets and to reduce the scale of climate change. In others,the issues are more to do with the need to adapt to the changes which will happen anyway.

For example, both housing and economic development will need new forms of building that can beadapted easily to cater for different uses during their lifetime. Buildings will be designed foreventual deconstruction and reuse. This could be combined with high levels of passive energydesign in layouts to, for example, maximise winter solar gain and minimise summer heating. Newrenewable energy infrastructure and distribution networks and use of waste for energy could alsobe part of a balanced approach.

Transport too has a clear relationship with climate change. Whilst this is well understood, historicallymost of us have failed to act on that information. Many common behaviours – including individuals’decisions to travel to work in a car, businesses’ decisions not to support Travel Wise or theGovernment’s decision to promote housing development in places that are hard to reach by publictransport – do not support the CO

2reductions required to meet national and regional targets.

Of course, climate change presents opportunities as well as threats. The region already has a strongenvironmental technologies sector which, coupled with its expertise in transport and buildingtechnologies, means that it is well placed to take advantage of a growing area, and one whichremains strong despite the recession.

To take advantage of these opportunities will require the region to encourage innovation. Thethematic report on Innovation in a Changing Economy highlights some of the approaches which willallow this to happen. Whilst much of the challenge is to the region’s businesses, not least to makethe investment needed, change will also be needed amongst public administrators and educationproviders. The latter, in particular, have a dual role – to provide the research and expertise whichare a catalyst for innovation, and to provide the highly-skilled individuals needed to make a realityof innovation. But if this is to be translated into economic benefits, our universities will need toget smarter at working with businesses, perhaps through intermediaries with experience of bothenvironments.

Individuals with high-level skills are also a necessity if the region’s knowledge economy is to thrive,as highlighted in the report The West Midlands Knowledge Economy . However, it won’t matter howmany graduates the region’s universities produce if we can’t retain them within the region, or

attract others from outside to move here. The report highlights the importance of providing theright “offer” to knowledge workers, and hence knowledge-intensive businesses.

State of the Region Annual Synthesis Report 200920

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 23/35

This is as much about providing an attractive environment and a range of successful communities

as it is about creating a vibrant economy; failure to address social and environmental challengeswill mean that it becomes impossible to maximise economic growth. Most policy areas contributeto this in one way or another and it is at the heart of the region’s strategy of Urban Renaissance.It also means improving the image of the region, so that recent improvements in the region arereflected in people’s perceptions of it. This issue will be addressed in the new thematic dialogueon Regional Image and Identity which is starting this autumn.

Of course, creating successful, and sustainable communities, is far from easy. The thematic reportWhat Makes a Community Sustainable highlights how sustainable communities require a balanceof economic, social and environmental factors. Addressing one of these without the others rarelyhas a positive long-term effect on communities. For example, providing new employment in adeprived area will not help local people if they don’t have the skills required for the jobs. Providingthem with the skills to get better jobs without improving the local environment or housing will

mean that they move away to be replaced by others with low skills and low incomes.

Sustainable communities are also diverse ones – be that in terms of their population, their economyor the housing that they provide. Getting the balance wrong can store up problems for the future,particularly when times are hard as they are during the current recession. The renaissance of oururban areas relies on creating balanced, sustainable communities in places which have sufferedfrom historic declines. In rural areas, the opposite can be true, with a need to provide the rightopportunities for existing residents and workers alongside those choosing to move into what theyconsider to be more desirable places.

Getting the population mix wrong could cause isolation or conflict, ultimately leading to problemswith community cohesion and the breakdown of the social asepcts of the community. Getting theeconomic mix wrong could lead to high levels of worklessness, to increased commuting, placingpressure on the community’s infrastructure, or to an over-reliance on a single employer, leavingthe community vulnerable to economic shocks. Getting the housing mix wrong could lead to somelocal people being priced out of the area or could reduce the attractiveness to certain groups,again impacting on community cohesion.

Of course, the sustainability of communities into the future will depend on the population livingin them. The composition of the region’s population is changing – changes which are reflected inlocal communities too. As highlighted in the thematic report on The West Midlands’ Changing

Population these changes will have wide implications too. The ageing population, particularly inrural areas, will be increasingly demanding of service providers, who will need to adapt and providemore flexible and localised services. Increasing ethnic diversity will require more flexible servicestoo, taking account of language, cultural and identity differences. Businesses too will need to adapt

to an increasingly diverse labour force by moving further away from a stereotypical view of theiremployees.

The local dimension

Integration across policy areas is not the only way in which the evidence base needs to be broughttogether. Increasingly, regional organisations will need to work more closely with local andsub-regional ones to meet the challenges. To do this, we will need an increased understanding ofvariations across the region.

This process has already begun. Earlier in the report, we highlighted that the recession has hit someplaces harder than others. Understanding this has been crucial to ensuring that the regional responseis being targeted on the places which need it most. There is also an increasing amount of evidence

about the local situation in relation to other regional challenges.

Economic productivity varies dramatically across the region, with the average employee in Solihullgenerating nearly £10,000 more output than his or her counterpart in Stoke-on-Trent

35. This is driven

in part by the mix of businesses in the two areas; with Solihull having a far greater concentration

21State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 24/35

of private sector services, whilst Stoke has a knowledge economy more dominated by the public

sector, which generates less economic output

16

. Skill levels play a part too, with 32% of Solihull’sresidents having a higher qualification in 2008, compared to just 14% in Stoke36

.

Figure 9: GVA per employee by strategic local authority

Shropshire

Herefordshire

Telford

& Wrekin

Staffordshire

Stoke on Trent

WorcestershireWarwickshire

1 2

1 Wolverhampton

2 Walsall

3 Dudley

4 Sandwell

5 Birmingham

6 Solihull

7 Coventry34

5

6 7

Source: Office for National Statistics, Regional GVA and Annual Business Inquiry

As highlighted above, overall economic performance depends not just on productivity, but also onthe proportion of local people who are working. This too varies substantially across the region. In2008, nearly 40% of Birmingham’s working age population were not in employment, compared tojust over 20% in Warwickshire. This emphasises that the issues aren’t necessarily to do with location

– since Birmingham is the region’s largest employment centre, but are instead driven by issues suchas skills, health and cultural factors

19.

The make up of local populations also varies across the region. Over recent years, the gap betweenthe age profiles of urban and rural areas in the region has been growing. By 2008, around 16% ofBirmingham’s population was aged above state pension age, compared to 25% in Herefordshire

37.

Projections show this trend will continue, with older age groups growing rapidly in rural areas whilstremaining stable or even declining in many urban areas

38.

State of the Region Annual Synthesis Report 200922

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 25/35

Figure 10: Age profiles in urban and rural parts of the West Midlands

2009 2029

Source: Office for National Statistics, 2006-based sub-national population projections

The regions black and minority ethnic groups are also unevenly distributed across the region. Overall,in 2007, an estimated 83% of the region’s population classified themselves as White-British. Thisgroup varied from 62% of Birmingham’s population to 96% of Herefordshire’s. In fact, whilstBirmingham accounted for 19% of the region’s population, it included 42% of those from minorityethnic groups and over half of those of Black or Black British, Pakistani or Bangladeshi origin. Despitethis current concentration, the region’s BME population is increasingly expanding beyond the urbancore, with the population doubling in many rural areas between 2001 and 2007, even though numbersremain low

39.

Factors such as age profiles and economic activity levels can impact on the health of the population.Therefore, it is no surprise that health levels vary across the region. The Health Profiles producedby the Department of Health and the Association of Public Health Observatories use a basket of 32indicators. In Warwickshire, 19 of these indicators were significantly better than the nationalaverage and only 2 were worse. In contrast, in Sandwell 27 were significantly worse than the nationalaverage and only 2 were better

40.

Another factor influencing health is levels of physical activity. Only 6% of adults in Walsall took therecommended level of physical activity

41in 2007-08, less than half the rate in Worcestershire and

Shropshire, the only two parts of the region where activity levels were above the national average42

.

Of course, the region’s places aren’t isolated from one another. Work currently being undertaken

in preparation for the new Strategy for the West Midlands, and Local Economic Assessments, islooking at the functional relationships between places in the region. This report, due to be publishedlater in the year, will enhance our understanding of how places are linked to one another.

23State of the Region Annual Synthesis Report 2009

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 26/35

The links between places are also at the heart of the region’s Integrated Policy Model. This new

tool allows the impact of, and relationship between, policies in economic development, land useand the environment to be modelled. The model also allows the spatial relationships between thesefactors to be tested, across the region’s 34 local authority districts (prior to the unification ofShropshire earlier this year). The model is available for regional partners to test the impact of theirpolicy options.

Conclusion

The year since the last State of the Region Annual Report has been a significant one for the region.The changing economic circumstances have presented a series of new challenges to add to the onesthat we already faced. The region’s evidence base has had to adapt to these changing circumstances.

This has meant that the introduction of the new State of the Region process has been timely. As

demonstrated in this report, the process is yielding results which are relevant to the region’schallenges. However, the test of the process will be how those results are used to influence policydecisions. To be as influential as it can be, the process, and the rest of the regional evidence base,will need to change still further. The next section looks at the nature of these changes.

State of the Region Annual Synthesis Report 200924

The State of the Region

8/8/2019 State of the Region Synthesis Report v1.1 Report NW

http://slidepdf.com/reader/full/state-of-the-region-synthesis-report-v11-report-nw 27/35

Looking to the Future

If the West Midlands is to meet the challenges that it faces, and to prosper in the future, then itwill need to change. To support this, the evidence base which supports decisions about the directionwe take needs to change too. Until now, much of the regional evidence has been backward looking– not so much “Where are we now?” as “Where were we a couple of years ago?” This was neededto help us to identify the challenges we face and we will need to continue monitoring the currentsituation so that we know how we are progressing towards our goals.

However, to deal with the challenges, we need to look forward. Evidence must increasingly answerquestions such as “Where can we get to?” and “How should we get there?” This will meanunderstanding what drives change, now and in the future, and how we can influence those drivers.It will mean understanding what will happen if we do nothing, and the size of the challenge weface to get to where we want to be. It will mean understanding how changes in one policy areawill impact on others, and how different parts of the region influence, and are influenced by, otherplaces, both inside and outside the region.

This need to change our approach to evidence has been brought into even sharper focus by therecession. Much of the evidence behind existing regional strategies was based on a time wheneconomic growth was the norm and, as a result, the policies weren’t designed for an economicdownturn. In future, evidence will need to consider a range of possible future scenarios for theregion.

An approach to evidence which is forward-looking and based on scenarios will be particularlyimportant as the region moves towards a Strategy for the West Midlands over the next two or threeyears. The new strategy is one of the proposals within the Local Democracy, Economic Development

and Construction Bill, currently before parliament. The new strategy will be based on a vision ofthe future for its people, its places and its economy. This vision needs to be grounded in the realismthat evidence can bring. It will also need evidence about the actions that will be needed to makethe vision into a reality.