State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

86

-

Upload

cbcpolitics -

Category

Documents

-

view

221 -

download

0

Transcript of State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 1/86

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 2/86

Permission to Reproduce

Except as otherwise specically noted, the inormation in this publication may be reproduced, in part or in wholeand by any means, without charge or urther permission rom the Science, Technology and Innovation Council,provided that due diligence is exercised in ensuring the accuracy o the inormation reproduced, that the Science,Technology and Innovation Council (STIC) is identied as the source institution, and that the reproduction is notrepresented as an ocial version o the inormation reproduced, nor as having been made in aliation with, orwith the endorsement o, STIC.

© 2011, Government o Canada (Science, Technology and Innovation Council).

State o the Nation 2010 — Canada’s Science, Technology and Innovation System:

Imagination to Innovation — Building Canadian Paths to Prosperity

All rights reserved.

Aussi oert en rançais sous le titre L’état des lieux en 2010 — Le système des sciences, de la technologie et de

l’innovation au Canada : De l’imagination à l’innovation — Le parcours du Canada vers la prospérité

This publication is also available online at www.stic-csti.ca.

This publication is available upon request in accessible ormats. Contact the Science, Technology and InnovationCouncil Secretariat at the number listed below.

For additional copies o this publication, please contact:

Science, Technology and Innovation Council Secretariat235 Queen Street9th FloorOttawa ON K1A 0H5

Telephone: 613-952-0998Fax: 613-952-0459Website: www.stic-csti.ca Email: [email protected]

Cat. No. Iu4-142/2010EISBN 978-1-100-17972-860872

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 3/86

Imagination to InnovationBuilding Canadian Paths to Prosperity

State o the Nation 2010Canada’s Science, Technologyand Innovation System

Science, Technologyand Innovation Council

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 4/86

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 5/86

ContentsExecutive Summary ........................................................................................................... 1

1 Introduction .................................................................................................................. 3

2 Tracking Progress in Canada’s Innovative Perormance — 2010 vs. 2008 .................. 4

3 Going Forward — A Core Set of Indicators to Measure Innovation ....................................... 8

4 Recent Developments in Measuring Innovation ..................................................... 10

5 Resources or Research and Development ............................................................. 12

6 Digest o Indicators ................................................................................................... 19

7 Conclusion ................................................................................................................... 74

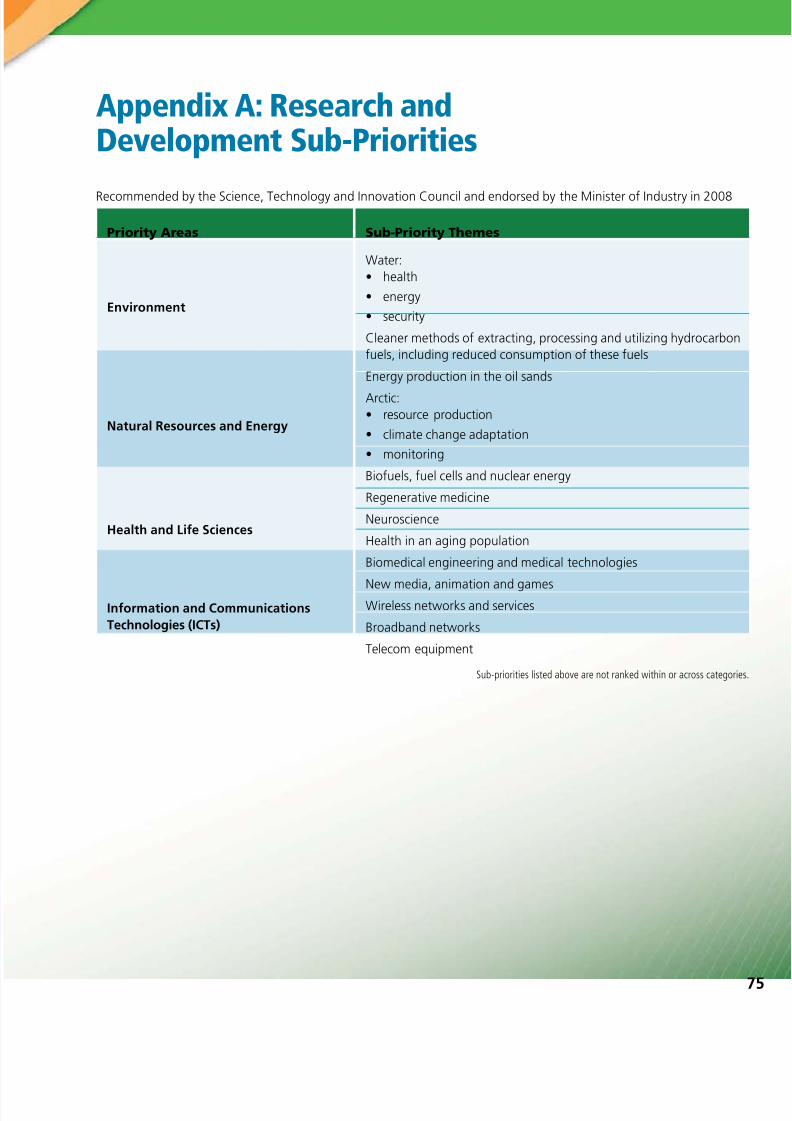

Appendix A: Research and Development Sub-Priorities .............................................. 75

Appendix B: State of the Nation 2008 Areas or Attention ......................................... 76

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 6/86

State of the nation 2010

ii

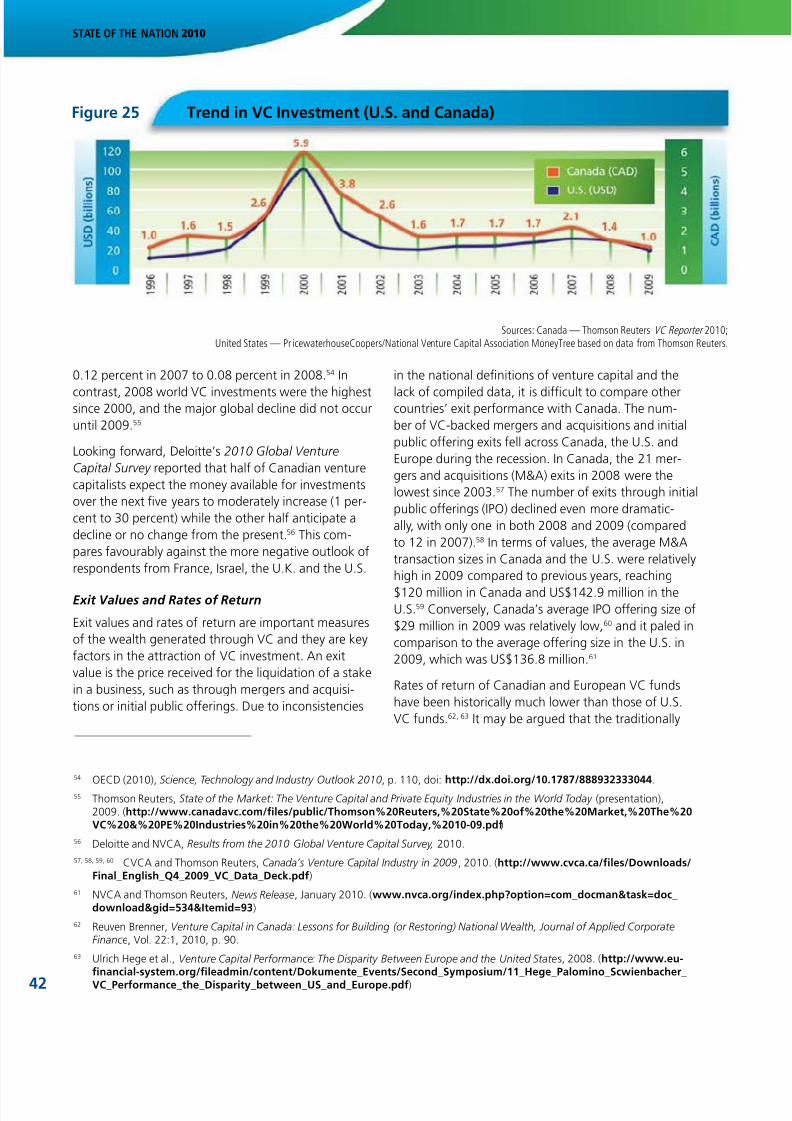

Digest o Indicators (Section 6)

6.1 Busss iv idcrs ........................................................................................19

6.1.1 Going Beyond R&D Indicators to Measure Innovation ............................................................. 19

6.1.2 Productivity Growth or Improved Standards o Living ............................................................ 19

6.1.3 Innovation Focus in Business Strategy ...................................................................................... 236.1.4 Innovation through Research and Development ....................................................................... 27

6.1.5 Innovation through Investments in Machinery and Equipment .............................................. 33

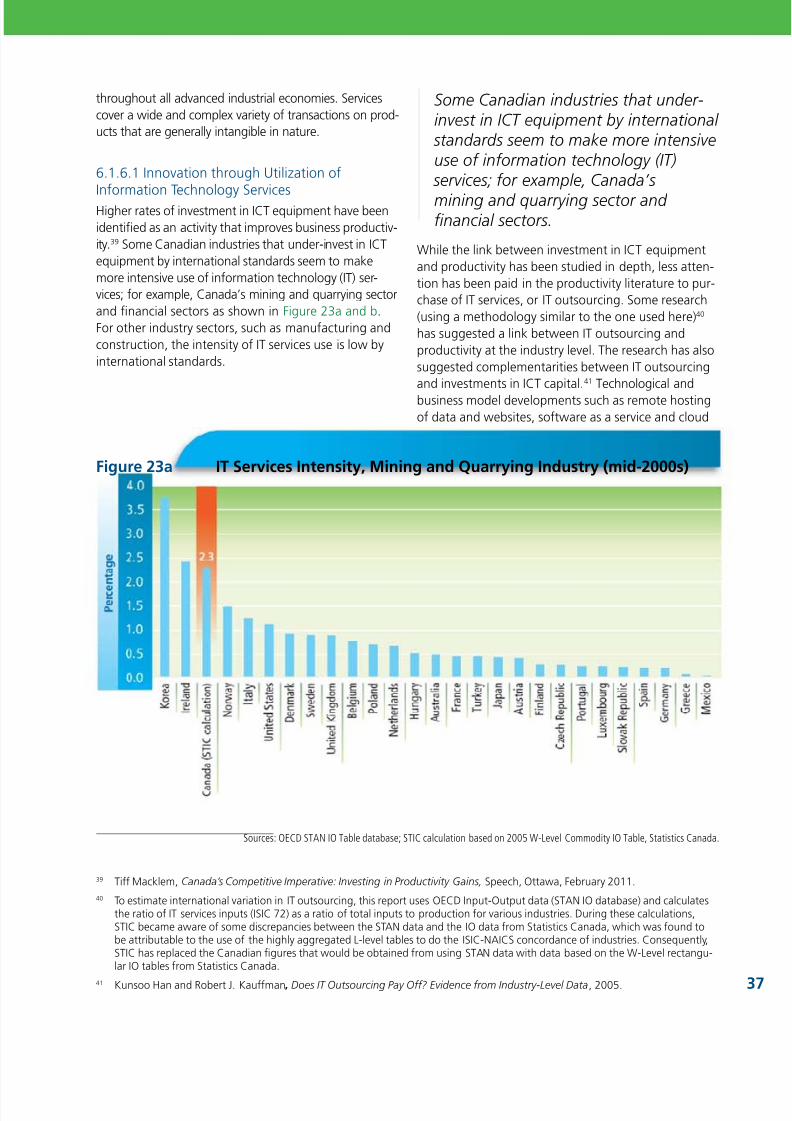

6.1.6 Innovation and the Rise o Service Industries .......................................................................... 36

6.1.7 Financing Innovation through Venture Capital ......................................................................... 41

6.2 Kwldg Dvlpm d trsr idcrs .........................................................45

6.2.1 Advancing the Frontiers o Knowledge through Science and Technology ............................. 45

6.2.2 Transerring Knowledge into Innovation ................................................................................... 50

6.3 tl idcrs ...............................................................................................................56

6.3.1 Science, Math, Reading Skills o 15 Year-Olds ........................................................................... 566.3.2 Pursuing Formal Education (15 to 19 Year-Olds) ........................................................................ 58

6.3.3 Share o the Population with Post-Secondary Education ......................................................... 58

6.3.4 College and University Graduation Rates .................................................................................. 59

6.3.5 Science and Engineering Education or Growth and Prosperity .............................................. 59

6.3.6 Inormation and Communication Technology Skills; Access and Use o ICT............................ 59

6.3.7 Education or Entrepreneurial Success ....................................................................................... 62

6.3.8 PhDs — Country Comparisons .................................................................................................... 62

6.3.9 Enrolment and Graduation in Science-Based Doctoral Programs by Canadian Students ....... 64

6.3.10 Unemployment Rates o Doctorate Holders .............................................................................. 646.3.11 Internships and Co-ops or Enhanced Opportunities ................................................................ 64

6.3.12 Returns on Obtaining Post-Secondary Education ...................................................................... 65

6.3.13 Attracting Great Talent to Canada .............................................................................................. 65

6.3.14 Education: A Lielong Pursuit ..................................................................................................... 69

6.3.15 Human Resources in Science and Technology ........................................................................... 69

6.3.16 Business Researchers.................................................................................................................... 70

6.3.17 Making Use o Highly Skilled People to Improve Productivity Growth ................................... 70

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 7/86

Role o the Report

The Science, Technology and Innovation Council’s State o the Nation 2008 report on Canada’s science, technologyand innovation system set out a baseline rom which Canada’s innovation perormance could be measured. This2010 report allows us to track progress and continue eorts to understand how innovation happens in Canada.

Benchmarking builds an evidence base or action, puncturing complacency and prompting greater refection. TheState o the Nation 2010 report puts a greater ocus on business innovation and the ways in which other par-ticipants in the innovation system work in partnership with companies. The report delves deeper to benchmarkindustry sector research and development on an international basis. It looks at product, process, and organiza-tional innovation as well as investments in inormation and communications technologies goods and services.Canadians ace choices in innovation that will create wealth in our country and improve the quality o lie or indi-viduals. Where should we ocus to make innovation gains? How can Canada’s science, technology and innovationsystem support these eorts? How can individual actions be leveraged to strengthen our ability to innovate andcompete? This report aims to inorm these considerations and decisions.

2010 STIC CouncilDr. hwrd alpr Chair, Science, Technology and Innovation Council

Dr. frcsc Bll Chairman, Picchio International Inc.

Mr. erc Brgr President and CEO, Optosecurity Inc.

Mr. Rcrd Dcr Deputy Minister, Industry Canada

Mr. Dvd fssl President and CEO, ASL Environmental Sciences Inc.

Dr. Pr McK President and Vice-Chancellor, University o Saskatchewan

Dr. trc Mws Chair, Mitel / Chair, Wesley Clover Corporation

Dr. hr Mur-Blum Principal and Vice-Chancellor, McGill University

Mr. Dvd o’Br Chair, Encana Corporation and Chair, Royal Bank o Canada

Mr. J. Rbr S. Prcrd Vice Chair, Science, Technology and Innovation Council; Chair, Torys LLP andChair, Board o Directors, Metrolinx

Dr. Guy Rulu MD, PhD; Canada Research Chair in Genetics o the Nervous System andProessor, Department o Medicine, Université de Montréal; Director, ResearchCentre, Sainte-Justine University Hospital Centre

Dr. W.a. (Sm) Sw President and CEO, Northern Alberta Institute o Technology (to October 2010)

Dr. Mlly Sc Canada Research Chair in Tissue Engineering and Proessor, Universityo Toronto

Dr. Ml Ulru Canada Research Chair, Adaptive Inormation Inrastructures or the eSociety;Director, Adaptive Risk Management Lab and Proessor, Faculty o ComputerScience, University o New Brunswick

Dr. hrvy P. Wgr President and CEO, Higher Education Quality Council o Ontario;President Emeritus, University o Calgary

Mr. Rb Wldbr Executive Chairman, Martinrea International Inc.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 8/86

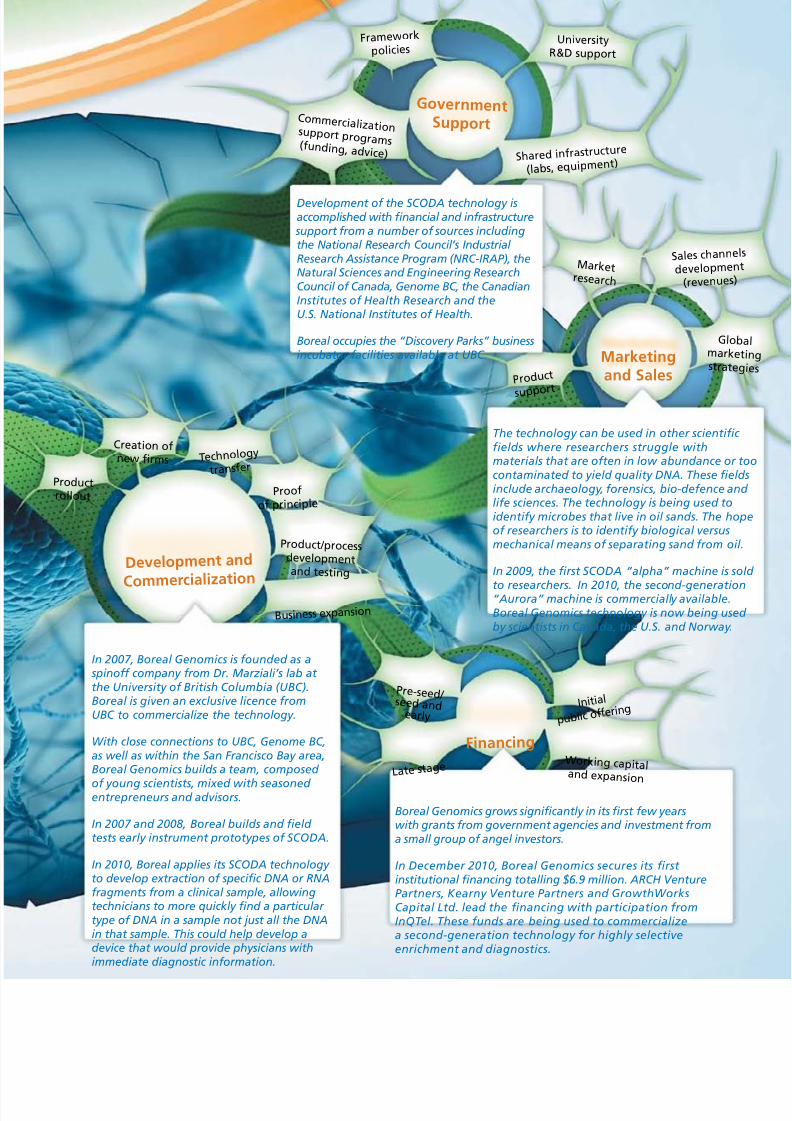

Research ( discoveries and inventions)Basic and

applied research

Dr. Andre Marziali and Dr. Lorne Whitehead o theUniversity o British Columbia (UBC) discover a new way to extract DNA molecules rom small or heavily contaminated samples by exploiting a unique property o DNA molecules. They develop a technology called SCODA or Synchronous Coefcient o Drag Alteration.

Go vernmen t

labora tories

S tuden tsResea

r cher s

En trepreneurs

Talent(science and

business)

Universities

Business

Colleges

Innovation PathwaysBasic research and value creation

Where people, knowledge and

entrepreneurship connect,innovation happens.Like synapses between nerve cells in the brain,connections are complex, not linear.

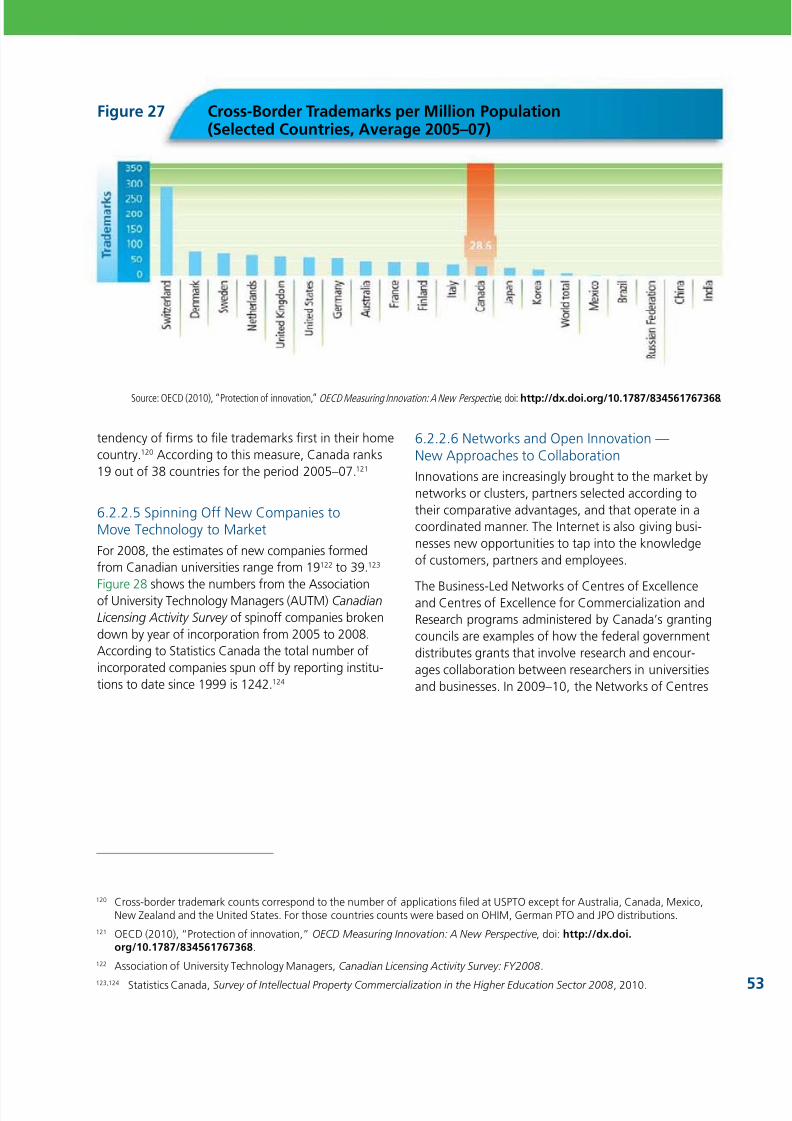

This image shows how Boreal Genomics made connections totake research to the market.

Boreal Genomics, based in Vancouver, B.C., is a small growing company that develops and commercializes methods and instruments or DNA molecule purifcation, enrichment

and detection.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 9/86

Financing

Marketingand Sales

The technology can be used in other scientifcields where researchers struggle withmaterials that are oten in low abundance or tcontaminated to yield quality DNA. These feldinclude archaeology, orensics, bio-deence anlie sciences. The technology is being used toidentiy microbes that live in oil sands. The hoo researchers is to identiy biological versusmechanical means o separating sand rom oil

In 2009, the frst SCODA “alpha” machine is so

to researchers. In 2010, the second-generation“Aurora” machine is commercially available.Boreal Genomics technology is now being useby scientists in Canada, the U.S. and Norway.

Boreal Genomics grows signifcantly in its frst ew yearswith grants rom government agencies and investment roma small group o angel investors.

In December 2010, Boreal Genomics secures its frst institutional fnancing totalling $6.9 million. ARCH VenturePartners, Kearny Venture Partners and GrowthWorksCapital Ltd. lead the fnancing with participation romInQTel. These unds are being used to commercializea second-generation technology or highly selectiveenrichment and diagnostics.

Government Support

Frame work

policiesUniversity

R&D support

C ommer c ializat ion suppor t pr ogr ams ( f unding, adv ic e) Shared in fras truc ture

(labs, equipmen t )

De velopment and

Commercialization

In 2007, Boreal Genomics is ounded as a spino company rom Dr. Marziali’s lab at the University o British Columbia (UBC).Boreal is given an exclusive licence romUBC to commercialize the technology.

With close connections to UBC, Genome BC,as well as within the San Francisco Bay area,Boreal Genomics builds a team, composed

o young scientists, mixed with seasoned entrepreneurs and advisors.

In 2007 and 2008, Boreal builds and feld tests early instrument prototypes o SCODA.

In 2010, Boreal applies its SCODA technology to develop extraction o specifc DNA or RNAragments rom a clinical sample, allowingtechnicians to more quickly fnd a particular type o DNA in a sample not just all the DNAin that sample. This could help develop adevice that would provide physicians withimmediate diagnostic inormation.

Technolog y

trans fer

Creation o new frms

Proof

of principle

Product / process development and testing

Product rollout

Business expansion

Mar ket r esear c h

Produc t

suppor t

Globmarkestrateg

Sales channel

de velopmen t

(re venues )

P r e-seed / seed and ear ly

La te s tage

I n i t ia l

p u b l i c o f fe r i ng

W or king capital and expansion

Development o the SCODA technology isaccomplished with fnancial and inrastructure

support rom a number o sources includingthe National Research Council’s Industrial Research Assistance Program (NRC-IRAP), theNatural Sciences and Engineering ResearchCouncil o Canada, Genome BC, the CanadianInstitutes o Health Research and theU.S. National Institutes o Health.

Boreal occupies the “Discovery Parks” businessincubator acilities available at UBC.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 10/86

State of the nation 2010

Defnitions:Research and DevelopmentInnovation

The Frascati Manual (2002) is the basis or the Organisation or Economic Co-operation andDevelopment (OECD) defnition o research and development, which is said to encompassthree activities: “‘Basic research’ is experimental or theoretical work undertaken primarily toacquire new knowledge o the underlying oundation o phenomena and observable acts,without any particular application or use in view. ‘Applied research’ is also original investiga-tion undertaken in order to acquire new knowledge. It is, however, directed primarily towardsa specifc practical aim or objective. ‘Experimental development’ is systematic work, drawingon existing knowledge gained rom research and/or practical experience, which is directedto producing new materials, products or devices, to installing new processes, systems andservices, or to improving substantially those already produced or installed.”

The Oslo Manual (2005) is the basis or the OECD defnition o innovation: “the implementa-tion o a new or signifcantly improved product (good or service), or process, a new market-ing method, or a new organizational method in business practices, workplace organizationor external relations.”

The Science, Technology and Innovation Council defned innovation in the State o the

Nation 2008 report as “the process by which individuals, companies and organizationsdevelop, master and use new products, designs, processes and business methods. Thesecan be new to them, i not to their sector, their nation or to the world. The components oinnovation include research and development, invention, capital investment and training

and development.”

vi

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 11/86

Executive Summary

Canada aims to be among the world’s innovation leaders. To do so we must understand the components andconnections in the science, technology and innovation (STI) system. A well-unctioning STI system is built on theoundation o a strong talent pool, excellent research, public and private sector institutions that create value romresearch and development, strong systemic mechanisms or knowledge transer and application, and successulcommercialization o innovation within the private sector. It takes a well-unctioning integrated system to moveideas rom imagination to innovation to markets.

Innovation is more than research and development (R&D) — it is transorming knowledge into products andservices that Canadians and others in today’s global marketplace need, want and will pay or. To leverage know-ledge into robust outcomes o better health, and strong and sustainable growth and jobs, we need to build andreinorce the paths to prosperity.

How good is Canada’s science, technology and innovation system at delivering the outcomes we want?

Our talent pool is holding its own and the number o Canadian university graduates is rising, with especiallyrapid growth in doctoral degrees in science. Graduation rates in master’s and doctoral science and engineering

degree programs have risen substantially more than in other advanced economies and aster than the growtho advanced degrees in all elds o study. Fiteen-year-old Canadians continue to outperorm most countries inreading, math and science. Canada remains in rst place in the G7 in the proportion o citizens with an educationbeyond high school.

Broader outcome-based indicators o excellence in universities and colleges have yet to be dened and applied onan international basis. Canadian business has markedly increased the R&D it unds in universities, although this isstill small — less than one tenth o overall R&D spending by business. Transerring knowledge rom research insti-tutions in universities and government to the marketplace and building a culture o innovation in business remainpaths requiring attention. Generating wealth rom commercialization is a valuable outcome o our commitment toscience, technology and innovation (STI) — an outcome that benets society both in economic and social terms.I we are underperorming in delivering the ull value o our STI progress, we must seek to understand why and

address these shortcomings.

Research and development perormed by business in Canada is low by international standards. In addition, rom2007 to 2009 Canadian industry R&D declined urther in both current and real dollar terms. Examinations oR&D intensity by industry, and in comparison with the same industries in other countries, indicate that in 2005,8 out o 16 industries examined had lower R&D intensity than the OECD average. There were, however, somenotable exceptions to Canadian levels o R&D perormance. Business R&D intensity higher than the Organisationor Economic Co-operation and Development (OECD) average was perormed in the paper, lumber and relatedindustry; inormation and communications technologies (ICT) manuacturing industry; wholesale and retail tradeas well as nance and communications service industries; transportation and storage industries; utilities; realestate and business services (including R&D and inormation technology (IT) services) industry.

Broadening the measure o innovation to include two important drivers o productivity growth — investments inmachinery and equipment (M&E), and investments in inormation and communications technologies — revealedmore challenging themes. In comparison with the United States (U.S.), over the period 2000 to 2007, M&E invest-ment intensity in Canada has been less than three quarters o U.S. levels and ICT investment intensity was lessthan hal o U.S. levels. However, the Canadian oil and gas extraction industry and nance, insurance, real estateand management o companies industry have registered higher M&E intensities than their U.S. counterparts. Datapresented in State o the Nation 2010: Imagination to Innovation also suggest that it is worth considering trendsin Canadian expenditures on IT services rather than only IT purchases, given their potential contribution to improv-ing innovation and productivity.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 12/862

State of the nation 2010

Not all innovation is the result o R&D. Process innovation and incremental innovation can be strong contributorsto productivity. Innovation success ultimately results rom the ambition and attention o management teams.

Beyond benchmarking, what principles should guide eorts to strengthen Canada’sinnovation perormance?

We must guard against complacency and continue to nurture talent at all levels. While 15-year-old Canadians’

scores remained airly stable, they ell in terms o rank in reading, science and math because others are improvingaster. We must work to support students to better learn and apply their knowledge.

Research and development sub-priorities identied by the Science, Technology and Innovation Council (STIC) in2008 can assist all innovation sectors to play rom Canada’s research and economic strengths. Even i one thirdo our resources are ocused in these areas, it will help to reinorce Canadian excellence on a global scale.

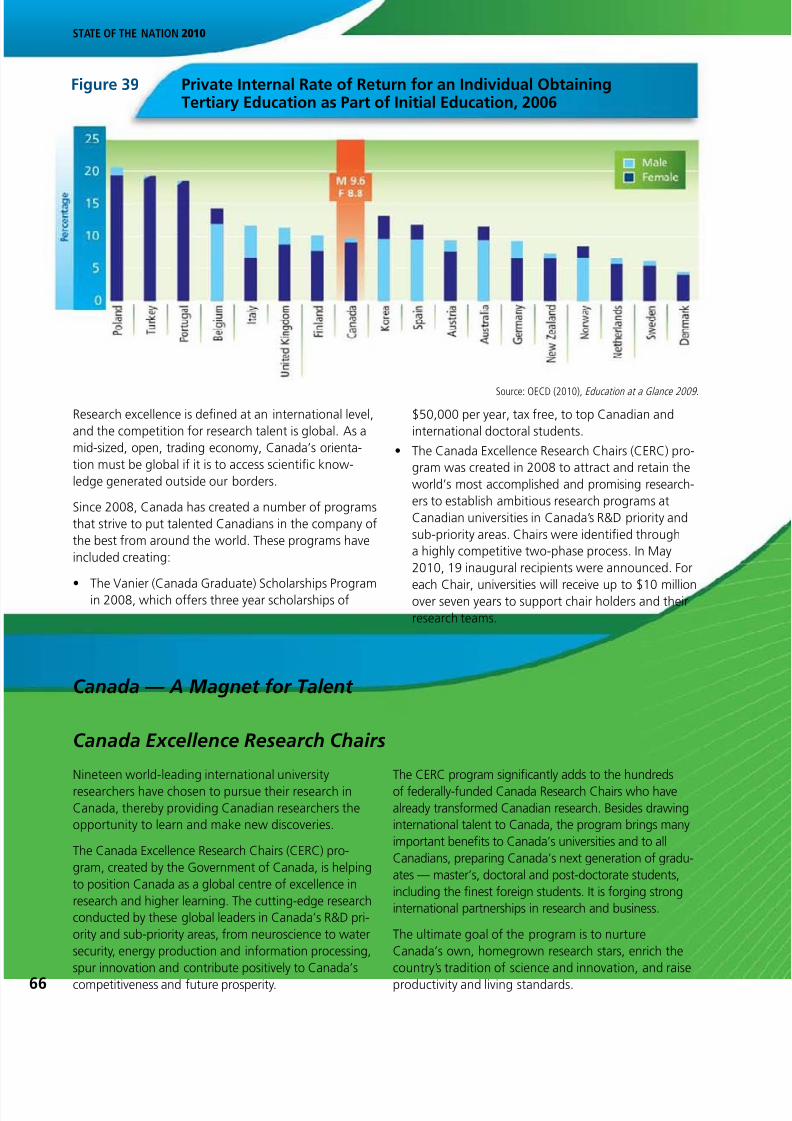

Competition and peer review have led to improved Canadian R&D at international levels o excellence. Themost recent example o this has been the quality and breadth o the Canada Excellence Research Chairs whoseresearch spans basic to more applied research. The competition demonstrated that not only large but also smallerCanadian universities can carve out niches o expertise and build alliances to establish a global reputation.

Collaboration should be considered in a clusters context, among universities and colleges, and small and large

companies. Support or clusters is one way to build critical mass in both short-term and long-term research areaso joint interest to companies and research organizations. Such collaborations also improve companies’ ability torecruit Canada’s highly qualied graduates. The participation o innovation intensive companies in such clustersand the active collaboration o the research and business communities will help ensure that Canada’s world-classresearch can be successully commercialized or the benet o this country.

The Research and Development Review Expert Panel, due to report in autumn 2011, will address how we canbetter leverage public unds to improve innovation commercialization outcomes in industry. Its recommendationswill be important or the uture o Canada’s STI system, and can reshape government programs to better incentprivate sector spending and to support entrepreneurship through simplied and better targeted assistance.

Between the 2008 and 2010 State o the Nation reports, Canadian industry has been bueted by a severe nan-cial crisis. As Canada emerges rom the crisis, opportunities remain to work together to achieve the innovationgoals we set or ourselves and to build paths to prosperity.

The State o the Nation 2010 report gets us closer to understanding how Canadian companies innovate. Datashow that some Canadian industries are global leaders. We are also ortunate to have a strong talent pool thatcould deliver on high ambitions. The challenge is to deploy talent well, invest in advanced technology, integrateinnovation into corporate and country strategies and leverage our eorts to deliver prosperity or all Canadians.This alignment will improve our lagging productivity growth. 2010 began with Canada’s athletes inspiring thenation with their resolve and high ambition. STIC’s State o the Nation reports are a starting point or bench-marking eorts in companies, universities and colleges, and governments across the country. Refecting onthe data in this report can help set ambitious goals that will put more Canadians and Canadian companieson global podiums.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 13/86

put orward two options. The rst option was a listo three indicators o innovation: patent applicationsweighted by Gross Domestic Product (GDP); percent-age o employment in knowledge intensive activities;and percentage o the value o medium- and high-techgoods as a share o both exports and imports. Thesecond option was the share o ast growing innovativerms in the economy.

The Science, Technology and Innovation Council’s(STIC) State o the Nation 2010 report opens withcommentary on progress since the State o the Nation

2008 report, and a summary o progress on key indi-cators noted in the report. Section 3 proposes a listo 20 indicators to measure innovation perormancegoing orward. These measures would serve to gaugeinnovation inputs including talent and research and

development (R&D), as well as proxies or innovationoutputs such as trademarks and licensing. Ideally theseindicators would also capture the degree o collabora-tion between dierent elements in the innovationsystem. An indicator or uture benchmarking couldbe based on components o Canada’s technologyintensive balance o payments. This would includeinternational transactions or the use o patents,licences, trademarks, designs, technical services andindustrial R&D carried out abroad. Together this shortlist o indicators could provide a common reerence

point or dierent parts o the innovation system.Section 4 reviews progress on measuring innova-tion and Section 5 shows the fow o unds betweensources and perormers o R&D. Section 6 providesmore detailed inormation on a longer list o indicatorso business innovation, knowledge developmentand transer, as well as talent.

Canada has come through the nancial crisis relativelywell. But beore breathing a sigh o relie, Canadiansmust prepare to tackle longer-term structural challengesto the economy. Our relatively strong Canadian dollarpresents challenges to exporters but reduces the cost orCanadian companies to import newer advanced capital.Productivity growth is essential or an aging and smallerworkorce to succeed in a highly integrated and com-petitive global economy. Innovation continues to matterbecause it can help meet these challenges.

Annual growth in Canada’s labour productivity (outputper hour worked) has been slowing and has been lessthan 1 percent or most o the last decade. In termso growth in labour productivity, the Institut européend’administration des aaires (INSEAD) ranked Canada95th o 132 countries. The International Institute orManagement Development (IMD) in Lausanne,Switzerland ranked Canada 45th o 58 countries. Parto Canada’s low international standings in productivity

growth is attributable to the act that developing coun-tries have a much greater potential or rapid productivitygrowth through technological convergence or catch-up rom low productivity levels. Among 33 advancedeconomies in the IMD standings, Canada’s productivitygrowth ranks 24th. As Canada’s productivity continuesto lag despite macro-economic reorms intended toimprove economic perormance, economists are increas-ingly ocusing on a lack o innovation in Canada as acontributor to poor productivity perormance.

Countries have made progress in eorts to understand

how innovation occurs. In Canada, analysis is currentlyunder way on the ndings o its pilot 2009 Survey o

Innovation and Business Strategy , some o the resultso which are published in this report. The rst com-prehensive United States (U.S.) ocial statistics oninnovation appeared in late 2010. The High-Level Panelon the Measurement o Innovation convened by theEuropean Commissioner or Research, Innovation andScience issued a report in September 2010. The panel

Introduction1

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 14/864

There have been some signicant developments in keyareas noted in the Science, Technology and InnovationCouncil’s State o the Nation 2008 report,which include:

Talent — developing a highly qualifed workorce

attuned to innovation opportunities

Young Canadians continue to perorm well in inter-national rankings o reading, math and science skills.The latest results rom the Organisation or EconomicCo-operation and Development’s (OECD) Programme

or International Student Assessment (PISA) showeither sustaining or slightly declining raw scores,but Canada remains in the top tier o perormers(Section 6.3.1). More Canadian students are enrol-ling in undergraduate science, engineering and

The State o the Nation 2008 report underlined that all participants in the innovation system have a role to play in strengthening the system. In the last two years the pro-

le o productivity and innovation issues has risen signicantly in public discourse. Themedia have given innovation issues sustained attention. Major industry organizationslike the Canadian Chamber o Commerce,1 the Canadian Manuacturers & Exporters,2 and the Canadian Council o Chie Executives and initiatives such as the Coalition or

Action on Innovation in Canada3 have deepened consideration o innovation by busi-ness. Organizations such as the Public Policy Forum, the Conerence Board o Canada,the Canadian Science Policy Centre, the Institute or Competitiveness and Prosperity, and the Federal Partners in Technology Transer have engaged other players in the innovation

system. Participants in the innovation system are mobilizing, building new paths toinnovation and prosperity.

1 Canadian Chamber o Commerce, Canadian Businesses Go Global or Growth, August 2010.

2 Canadian Manuacturers & Exporters, Invest to Grow: Technology, Innovation and Canada’s Productivity Challenge, October 2010.

3 Coalition or Action on Innovation in Canada, An Action Plan or Prosperity , October 2010.

mathematics programs (Section 6.3.5). More Canadiansare enrolling and graduating rom science-based doc-toral programs, but other countries remain higher interms o doctoral-level graduates per million population(Section 6.3.8). Canada also has higher unemploymentlevels or science-based doctoral-level graduates thanother OECD countries. (Section 6.3.10).

Knowledge Development and Transer

Since 2008, more was done to ocus on researchpriorities and conduct research at international levels

o excellence. The rst recipients o the CanadaExcellence Research Chairs were announced. The chairsrefect the STIC research and development sub-priority

Tracking Progress in Canada’sInnovative Perormance —

2010 vs. 2008

2

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 15/86

Measuring Innovation Perormance

Canada’s 2009 Survey o Innovation and Business

Strategy (SIBS) was released in November 2010. Careneeds to be taken in the uture to ensure that questionsin this survey align with international data on businesscollaboration with universities and companies obtainedthrough the U.S. and European Union (EU) surveys.

Many industry-specic actors will have an impacton how industries in Canada innovate, and howwell this innovation is measured. Research on innova-tion, including research by the National Endowmentor Science, Technology and the Arts (NESTA) in theUnited Kingdom (U.K.), suggests that there is likely tobe substantial hidden innovation and that the extento hidden innovation may dier in dierent industries.Innovation, as dened by the OECD’s Oslo Manual

(2005), can be new to a company even i it is not new

to the industry or to the world. Some innovation isuser-driven and involves large scale eld testing thatis not dened or tracked as R&D. Other innovationinvolves copying best practices applied elsewhere.Until these investments are tracked separately they willremain unquantiable and accounted or on an anec-dotal basis. Data presented in this report enable betterbenchmarking by illuminating industry dierences.Data points are, however, only tools or improving ourunderstanding o innovation rather than the nal wordon Canadian industry practices.

I companies apply their own reality check to data presented and refect onthe relevant practices o countries and companies who are global leaders intheir sectors, Canada will move ahead.

Since 2008, both incremental and transormative actionshave taken place. These have yet to raise our perorm-ance on key indicators o R&D in Canada. The ollowingtable itemizes changes in a short list o indicatorstracked since the State o the Nation 2008 report.

areas disseminated in 2008. The rst Vanier (CanadaGraduate) Scholarships Program doctoral students werenamed and the new Banting Postdoctoral FellowshipsProgram was launched (Section 6.3.13). Canada’sgranting councils — Canadian Institutes o HealthResearch, Natural Sciences and Engineering Research

Council o Canada, Social Sciences and HumanitiesResearch Council o Canada — have used the sub-priorities to inorm a number o their own programs.Competitions or Networks o Centres o Excellencehave utilized the sub-priorities as a key requirement.

Knowledge transer to business was improvedsince 2008 by strengthening internship programs(Section 6.2.2.1). The launch o the Government oCanada’s Research and Development Review ExpertPanel in October 2010 marked a commitment to exam-ine knowledge transer issues in a more comprehensive

way. The panel is to report in autumn 2011.

Business Innovation

Total nancial resources or research and development(R&D) in Canada as a percentage o GDP decreasedrom 2006 to 2008. Most o the world’s innovatingnations increased resources or R&D. A more detailedlook at the perormers o R&D shows that expenditureson R&D by government and the higher education sec-tor increased rom 2006 to 2009. R&D expendituresby business have decreased over the same timeperiod (Section 5).

State o the Nation 2008 stated that low overall busi-ness R&D in Canada had been a constant eature or40 years. Canada’s business R&D intensity remainslower than the OECD average and is lower than thato China. R&D expenditure has diered by industrysectors over the years. The State o the Nation 2010

report provides a baseline or examining R&D on anindustry sector basis (Section 6.1.4.4).

Governments are pooling public unds with private undsto expand available venture capital. The Government

o Canada improved the ability o Canadian businessesto attract oreign venture capital by narrowing the de-inition o taxable Canadian property, thereby reeingmany oreign investors rom the tax reporting require-ments under section 116 o the Income Tax Act .

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 16/86

State o the Nation: Summary Comparison oSelected Indicators, 2008 and 2010 Reports

Section o Report / Indicator2008

Report

2010

Report

Change on Final Year

o Data rom 2008

to 2010*

Resources or Research and Development (R&D)

1. Gross domestic expenditure onR&D (GERD) as a percentage o GrossDomestic Product (GDP)

2006 1.97%

2008 1.84%

2006 to 2008

2. GERD by perorming sector(constant 2002 dollars)

2007 $0.28 billion$14.19 billion$8.53 billion

$2.21 billion

2008 $0.30 billion$13.22 billion$8.53 billion

$2.15 billion

2007 to 2008

by provincial governments

by business

by higher education

by ederal government

Business Innovation Indicators

3. Business expenditure on R&D (BERD)intensity, as a percentage o GDP

2006 1.10%15th place

20081.00%18th place

2006 to 2008

as a percentage o GDP

ranking in availableOECD countries

4. Direct and indirect government und-ing o business R&D, as a percentageo GDP

2005 0.21%0.023%

20080.22%0.022%

2005 to 2008

indirect governmentunding

direct governmentunding

5. Investment in machinery andequipment as a share o GDP

2004 6.2%

20076.3%

2004 to 2007

6. Venture capital relative to GDP 2007

0.12%

2008

0.08%

2007 to 2008

6

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 17/86

State o the Nation: Summary Comparison oSelected Indicators, 2008 and 2010 Reports

Section o Report / Indicator2008

Report

2010

Report

Change on Final Year

o Data rom 2008

to 2010*

Knowledge Development and Transer Indicators

7. Higher education perormance oR&D, as a percentage o GDP

2006 0.66%

20080.64%

2006 to 2008

8. Share o all business-nanced R&Dperormed by higher education sector

2006 5.7%

20096.3%

2006 to 2009

9. Intramural government R&D as ashare o GDP in Canada

2006 0.20%

20080.19%

2006 to 2008

Talent Indicators

10. Programme or International StudentAssessment (PISA): 15 year-olds

2006 Science: 5343rd place

Math: 5277th place

Reading: 5274th place

2009Science: 5298th place

Math: 52710th place

Reading: 5246th place

2006 to 2009

in science score

in science ranking

in math score

in math ranking

in reading score

in reading ranking

11. Percentage o population withtertiary education: top 10 Organisationor Economic Co-operation andDevelopment (OECD) countries

2006 47%1st place

200849%1st place

2006 to 2008

percentage opopulation withtertiary education

ranking in top 10

OECD countries

12. PhD graduates per millionpopulation: OECD countries

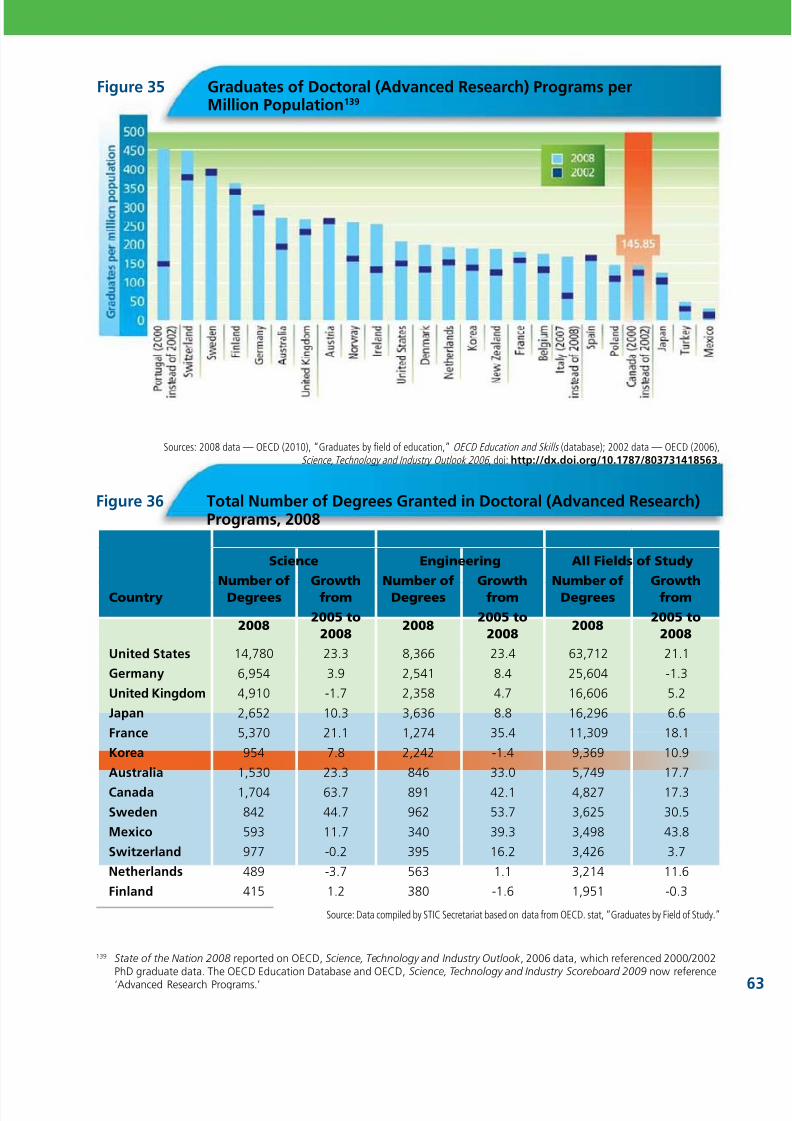

2002 129.620th place

2008 145.923rd place

2002 to 2008

in graduates permillion population

in ranking oOECD countries

(cont’d)

*Note: Direction o arrow indicates change rom years cite

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 18/868

between countries, oten do not provide the level odetail that helps countries compare or benchmark theinnovative perormance by industry or industry sector.

Research or the State o the Nation 2010 report,progress in developing metrics or innovation andconsultations with participants in the innovation sys-tem over the last three years, have led STIC to recom-mend a short list o indicators going orward. To betteraccount or innovation that is more than R&D andto enable better benchmarking by participants in theinnovation system, the ollowing set o indicators isidentied or ongoing monitoring.

Measuring innovation is a worldwide work in progress.It has evolved rom measures o research and develop-ment and talent to encompass measures o machineryand equipment, intangibles such as sotware and data-bases, and in-rm specic human and organizational

capital. Section 4 describes recent developments inmeasuring innovation. In Section 3 we propose a set oindicators that place a premium on allowing or inter-national comparison on a standardized basis. Someo the indicators are available or Canada only. Theindicators are useul because they are more recent, andoten provide signicant industry-level detail and allowor analysis across time. Other innovation measures arecompiled by international organizations such as theOECD, the World Economic Forum, INSEAD and others.International sources, while allowing or comparisons

Perormance Indicators or Canada’s Innovation System

IndicatorYearo

DataRationale

Talent

1. Organisation or EconomicCo-operation and Development’s(OECD) Programme orInternational Student Assessment(PISA): 15 year-olds

2009 Measures Canada against international sample, benchmarking talent atthe secondary school level. Assesses reading, mathematics and science.

2. Percentage o populationwith tertiary education 2008 Measures supply o advanced skills, which can contribute toproductivity gains.

3. Numbers o bachelor-degreegraduates in science andengineering-related disciplinesrom university

2008Measures graduates with a package o skills and knowledgethat is valued in the labour market and can contribute toeconomic growth.

4. Number o PhDs inscience, math andengineering (graduates)

2008 Measures talent pool at technology rontier.

5. Research and development(R&D) personnel in business 2007 Measures industry use o highly qualied researchers.

Going Forward —A Core Set of Indicators

to Measure Innovation

3

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 19/86

Perormance Indicators or Canada’s Innovation System

IndicatorYearo

DataRationale

Research and Development

6. Gross domestic expenditure

on R&D (GERD) as a share oGross Domestic Product (GDP) 2008Benchmarks Canadian resources allocated to R&D againstother countries.

7. GERD by perorming sector inconstant dollars

2008 Illustrates the state o R&D spending by business, government and highereducation and highlights the trends in each.

8. Major fows o R&D undingin Canada 2009 Illustrates the links between sources o unding and R&D perormers.

9. Business expenditure on R&D(BERD) intensity by country 2008

Benchmarks R&D perormed in business in Canada vs. R&D perormed in busi-ness in other countries. Data can be presented on an industry sector basis.

10. Direct and indirect govern-ment support to businessor R&D

2008Tracks the type o mechanisms used by government to encourage privatesector investment in R&D. Benchmarking with other countries aids analy-sis on the ecacy o policy instruments.

11. Higher education perorm-

ance o R&D, as a share o GDP 2008

Benchmarks R&D perormed in universities in Canada vs. R&D perormed

in universities in other countries.12. Share o all business-nancedR&D perormed by higher educa-tion sector and others

2009 Illustrates trends in business strategies and propensity to perorm R&Din-house or through outsourcing.

13. Intramural government R&D:share o GDP in Canadaand the G7

2008Benchmarks R&D in government labs and institutes vs. R&D perormed ingovernment in other countries. Measures R&D important to achieving societalgoals that would not be conducted by other parts o the innovation system.

Innovation (other than R&D)

14. Investment in machinery andequipment, including inorma-tion and communications tech-nologies (ICT), as a share o GDP

2007Measures inputs to innovation other than R&D. New ideas are embedded inleading-edge technologies and enable workers to produce more and higher-quality goods and services through more ecient business processes.

15. Utilization o inormationtechnology (IT) services

2005Measures input to innovation other than R&D. Technological change isprompting changes in business processes, which result in inrastructure, intan-gibles such as sotware, and customer service being bundled as a service.

16. Venture capitalrelative to GDP 2008

Measures the pool o capital important or start-ups in the knowledgeintensive ICT and lie sciences industries. Tracks the capacity orundertaking high-risk investments.

17. Firms collaborating in innova-tive activities with public or privatepartners, government, and highereducation institutions by size

2002–2004,

noupdates

orCanada

Collaboration has become an important source o competitive advantage.Innovations are increasingly brought to the market by networks o busi-ness, academic and government partners. Regional associations can bepartners in tracking collaboration within geographic clusters.

18. Number o licences romuniversities to businesses

2008 Measures technology transer and potentially commercially-valuableknowledge transer to the private sector. Indicates leveraging o publicinvestments in higher education.

19. Trademarks 2008Trademarks can be applied to innovation in goods and services and encom-pass marketing innovation. The OECD has ound that trademark applicationsare highly correlated with other innovation indicators.

20. Technology intensivetrade fows (services and goods)

2010

Measures the ability o Canadian enterprises to export goods and servicesand trends in the use o goods and services by Canadian companies.Measures Canadian success on a global scale (i.e., global demand orCanadian ideas and expertise). Payments refect Canadian demand andawareness o global opportunities.

(cont’d)

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 20/8610

4.2 Ud Ss —

Busss R&D d iovo Survy

Ater years o absence rom the measurement o innov-ation, the U.S. National Science Foundation’s Divisiono Science Resources Statistics, in collaboration withthe Economic Directorate o the Bureau o the Census,has conducted a new Business R&D and Innovation

Survey (BRDIS). The stratied sample o 40,000 rms,with ve or more employees, includes a census olarge R&D perormers, the 50 largest rms, basedon payroll, in each state, and a sample o other rmsdrawn rom the U.S. Census Bureau’s Business Register.It went into the eld as a pilot survey in January 2009and R&D estimates were released in 2010.

The survey included the propensity or rms to innov-ate, and related variables, broken down by industry.It also reerred to the number o rms that do anddo not perorm R&D, providing an understanding othe place o R&D in the business strategies o small,medium and large companies. Results rom the newsurvey can be used to track the impact o new pro-grams on the industrial distribution o innovation.

Europe’s Community Innovation Survey (CIS) has beenrunning at regular intervals since 1992 and provided amodel or the 2005 innovation survey in Canada andor the innovation questions used in the U.S. BRDIS.CIS data are available rom Eurostat, the statisticaloce o the European Commission. Aggregate dataor the 27 European Union (EU) member states, andsome other countries, are presented in the EuropeanInnovation Scoreboard, which has recently beenrevised to become the Innovation Union Scoreboard.

This section highlights progressmade in the measurement o innovation that is not researchand development.

New surveys are in development and in the eld.A number o countries and international organiza-tions are also working on measuring innovation thatoccurs as a result o changes in business processes,organization or marketing or through investments inintangible assets. Canada’s 2009 Survey o Innovation

and Business Strategy (SIBS) and the United States’2009 Business R&D and Innovation Survey (BRDIS) arenew surveys that made data available or analysis in2010. Future analysis can draw on data to enable com-parisons with Europe’s Community Innovation Survey (CIS). The United Kingdom’s National Endowment or

Science, Technology and the Arts (NESTA) Innovation

Index and the Organisation or Economic Co-operationand Development’s (OECD) Measuring Innovation: A

New Perspective (2010) explore possible uture indica-tors. However, producing comparative analysis is sometime away, as protocols have yet to be developed orstandardization o data.

4.1 Cd — Survy of

iovo d Busss Srgy

The 2009 Survey o Innovation and Business Strategy (SIBS) sampled over 6,000 companies. Survey ques-tions address the motivation or innovation, spendingon innovation activities, collaboration and the resultsexpected rom innovation. This survey is discussed ingreater detail in Section 6.1.3.

Recent Developments inMeasuring Innovation

4

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 21/86

Using data rom 21 countries, the report concludedthat rms receiving public support or innovationinvested 40 percent to 70 percent more than thosewho did not. It is also suggested that higher levelso company investment in innovation lead toelevated sales o new-to-market products and

higher productivity.4

New work was undertaken to capture investments inintangible assets. The OECD divided these into com-

puterized inormation, which includes sotware anddatabases; innovative property , which includes scien-tic R&D, mineral exploration, copyright and licencecosts, and product development, design and research;and economic competencies, which include brandequity, rm-specic human capital and organizationalcapital. Work in this area does not yet include stan-dardized methods and denitions. It does show that

investments in intangibles are larger than investmentsin machinery and equipment in the U.S. and Sweden.Estimates o the contribution o intangible assets tolabour productivity growth show that these explaina good portion o multiactor productivity growth insome OECD countries.

Another highlight is the measure o “new-to-market”product innovators with and without R&D as a percent-age o innovators. This indicator shows that a largeshare o rms develop their innovation without per-orming any R&D.

New work was undertaken to captureinvestments in intangible assets:computerized inormation, innovative

property and economic competencies.

4.3 Ud Kgdm — Plnol edowm for Scc, tchology d

h ars iovo idx

The National Endowment or Science, Technology

and the Arts (NESTA) Innovation Index seeks to betterunderstand innovation at the rm level through captur-ing ‘hidden innovation’ and investigating the dierentways that innovation occurs in nine industries. NESTAdeveloped a rm-level innovation survey that wastailored to the dominant modes o innovation in eachindustry. Industries covered included energy production,accountancy services, specialist design, consultancy ser-vices, construction, architectural services, sotware andinormation technology (IT) services, legal services and

automotive. Results were published in November 2009.The survey asked rms about how they: obtained newideas rom elsewhere; turned ideas into products; andcommercialized innovation (i.e., used innovative goodsand services to make money).

The survey uncovered signicant levels o hiddeninnovation in several industries where levels o trad-itional R&D investment are low, and ound that hiddeninnovation was also important or high R&D industries.For every sector surveyed, except the energy produc-tion sector, where the eect was noted as small,

innovative rms showed higher sales growth thannon-innovators. This methodology is experimental andhas not been used in national data-gathering eorts.

4.4 orgs recmc C-pr dDvlpm — Msurg

iovo: a nw Prspcv

In its 2010 Measuring Innovation: A New Perspective report, the OECD presented new indicators along withnovel ways o looking at traditional ones. It includedmeasures o expenditure on “innovation” as opposedto “R&D” by rm size. Expenditure on innovationincludes: total expenditure by rms on R&D that theyperorm in-house or externally; acquisition o otherexternal knowledge (e.g., patents, licences and trade-marks); and acquisition o machinery, equipment andsotware. Canadian data or this indicator were 2005data and only or manuacturing.

4 OECD (2010), Measuring Innovation: A New Perspective, p. 78.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 22/8612

Resources or Researchand Development

5

As a share o GDP, R&D expenditures in Canada lagbehind the G7 average (Figure 1). From 2006 to 2008,GERD/GDP in Canada dropped rom 2.0 percent to justover 1.8 percent. This change was partly due to rapid

GDP growth; however, growth in Canadian GERD alsolagged that in the G7 over this period.

Gross domestic expenditure on research and develop-ment (GERD) is total expenditure on research anddevelopment perormed in the country during a givenperiod. Domestic perormers o research and develop-ment include government (ederal, provincial and prov-incial research organizations), business enterprise, privatenon-prot, and higher education. Funding or GERD

comes rom domestic and oreign sources.

The share o GERD relative to the size o a country’sGross Domestic Product (GDP) is a commonly used indi-cator o innovation perormance. This has been a useulinternational benchmark and guides many science, tech-nology and innovation strategies around the world.

Source: OECD, Main Science and Technology Indicators, 2010.

Figure 1 Gross Domestic Expenditure on R&D (GERD) as a Percentage Shareo GDP (2006 and 2008)

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 23/86

5 Federal Funding o Business R&D includes direct grants and contracts rom the ederal government or R&D perormed in the busi-ness enterprise sector in Canada. This gure does not include SR&ED tax credits, or repayable loans that may be made under certainederal programs. Foreign unding o R&D includes all unding o R&D perormed in Canada, which is unded by a oreign source,i the nancing o the R&D involves an international transer o unds rom a oreign country into Canada. This includes transers ounds between, or example, oreign parent companies and their Canadian aliates or R&D projects carried out in Canada.

6 OECD (2010), Main Science and Technology Indicators.

Figure 2 Gross Domestic Expenditure on R&D as a Percentage Share oGross Domestic Product, or Selected Countries, 1981–2008

Source: OECD, Main Science and Technology Indicators, 2

Figure 2 shows that among some o the top R&D-perorming countries, including Canada, total GERD/ GDP ratios over the past 10 years show mixed trends.Over this period, ratios substantially increased inJapan, China and South Korea. Canada showeda modest increase.

From 2006 to 2009, government,higher education, oreign sources and

private non-prot sectors all increased their unding or R&D.

Increasing Canada’s research intensity and osteringinnovation requires concerted and coordinated eortsby the three principal Canadian R&D-perorming sec-tors: the private sector, the higher education sector andgovernment. Figure 3 shows the R&D undingand perormance that are undertaken by these threeprincipal perorming sectors and other supportingagents such as private non-prot organizations.5

In the period rom 2006 to 2009, government, highereducation, oreign sources and private non-prot sectorsall increased their unding or R&D. Interestingly, the

private non-prot sector increased its overall undingo R&D by just over 16 percent (in current dollars), themost over the period o 2006 to 2009 compared tothe other sectors. During the same period, Canadianbusiness expenditure on R&D declined in infation-adjusted terms. The Government o Canada directly

unded just under $6 billion o R&D perormed inCanada in 2009 (in current dollars), an increase rom2006 o just under $500 million or 8.6 percent. Almosthal o this $6 billion was carried out in Government oCanada institutions and labs. The remainder o about$3 billion or R&D (in current dollars) was perormed bythe higher education, business and private non-protsectors. In-house government R&D as a share o GDPell slightly to 0.188 percent in 2008 rom 0.195 percentin 2006 (as reported in State o the Nation 2008) andthe gap between Canada and the G7 (minus Japan, orwhich data are not provided) continued to widen.6

Canadian business expenditureon R&D declined in infation-adjusted terms.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 24/86

State of the nation 2010

14

* Includes only ows and perormers > $100M.

Source: Statistics Canada, CANSIM Table 358-0001, August 2010.

Figure 3 Major Flows o R&D Funding in Canada, 2009*

Source: Statistics Canada, CANSIM Table 358-0001, July 15, 2010.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 25/86

Figure 6 shows that Canada is near the top o theOECD, and ranks number one in the G7, in terms ohigher education research and development (HERD) asa percentage o GDP. In 2008, higher education R&Dwas 0.644 percent o GDP, down slightly rom 0.664percent in 2006.7 HERD includes all research perormed

in higher education organizations such as universi-ties and aliated teaching hospitals. Canada’s leadincreased rom 1997 to 2001 because o its invest-ments in research inrastructure (such as laboratories),and rom 2001 to 2007 because o investments inresearch. The spending rate and the balance o und-ing between inrastructure and research have remainedstable over the last decade. Figure 7 shows that ederalHERD expenditure consistently increased rom 1997–98to 2008–09. The level o expenditure in inrastruc-ture increased rom 1997–98 to 2001–02, and thenremained relatively stable rom 2001–02 to 2008–09.Announced on January 27, 2009, as part o theGovernment o Canada’s Economic Action Plan, theKnowledge Inrastructure Program provided $2 billionto support enhancement at universities and collegesover two years.

Canada ranks number one in the G7, interms o higher education research and development (HERD) as a percentageo GDP.

Figure 4 shows the trend o R&D perormed by ederaland provincial governments, business and higher edu-cation sectors rom 1998 to 2008 in constant dollars.According to this gure, in Canada, growth in highereducation R&D perormance was responsible or justover hal o the growth in total R&D over the period o

1998 to 2008: higher education perormance o R&Dgrew rom just under $5 billion in 1998 to just over$8.5 billion in 2008 (infation-adjusted dollars).

Figure 5 shows that business-nanced R&D perormedby universities has grown substantially in Canada,especially since the early 1990s. In 2009, university-perormed R&D was 6.3 percent o total businessunded R&D (which includes R&D nanced and under-taken by businesses and R&D nanced by business butundertaken by other sectors). This share was down romthe peak o 6.6 percent in 1992, but was above the

more recent peak o 2000 (preceding the tech collapseo 2001). While the growth in the share has slowed inrecent years, the secular trend over the past two dec-ades is upwards.

Business-nanced R&D perormed by universities has grown substantially in Canada.

7 OECD (2010), Main Science and Technology Indicators .

Source: Statistics Canada, CANSIM Table 358-0001, September 2010.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 26/86

State of the nation 2010

16

Figure 7 Federal Expenditures onHigher Education R&D(Constant 2002 Dollars)8

Source: Industry Canada calculation based on data rom Statistics Canada(Catalogue 88-204) and the Granting Councils’ Funding Decision Databases.

8 Federal Expenditures on Higher Education R&D are dened as the three Granting Councils and the Canada Foundation orInnovation’s (CFI) expenditures on R&D in the Higher Education Sector. Inrastructure includes expenditures or all CFI programsexcept or the Inrastructure Operating Fund (IOF), and equipment and tools programs rom NSERC and CIHR. Research includesall other research grants rom the granting councils and the IOF portion o CFI.

9 OECD (2010), “Firms investing in R&D,” OECD Measuring Innovation: A New Perspective. (http://www.oecd.org/dataoecd/29/33/45188105.pd)

10 Johan Hauknes and Lennart Nordgren, Economic Rationales o Government Involvement in Innovation and the Supply o

Innovation-Related Services, The STEP Group, 1999.

Direct and Indirect Government Funding

o Business R&D

Governments use various tools to encourage privatesector investment in R&D. These tools can be classiedinto direct support and indirect support. Direct support

encompasses grants, loans and procurement. Indirectsupport includes R&D tax credits, R&D allowances andreductions in R&D workers’ wage taxes. The best bal-ance o tools to use varies rom country to country andis determined by the market or system ailure beingaddressed and the type o R&D that the governmentwants to stimulate.9 System ailure has been described asthe lack o coherence among institutions in an innova-tion system and in incentive structures.10

Source: OECD, Main Science and Technology Indicators , 2010.

Figure 6 Higher Education Perormance o R&D

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 27/86

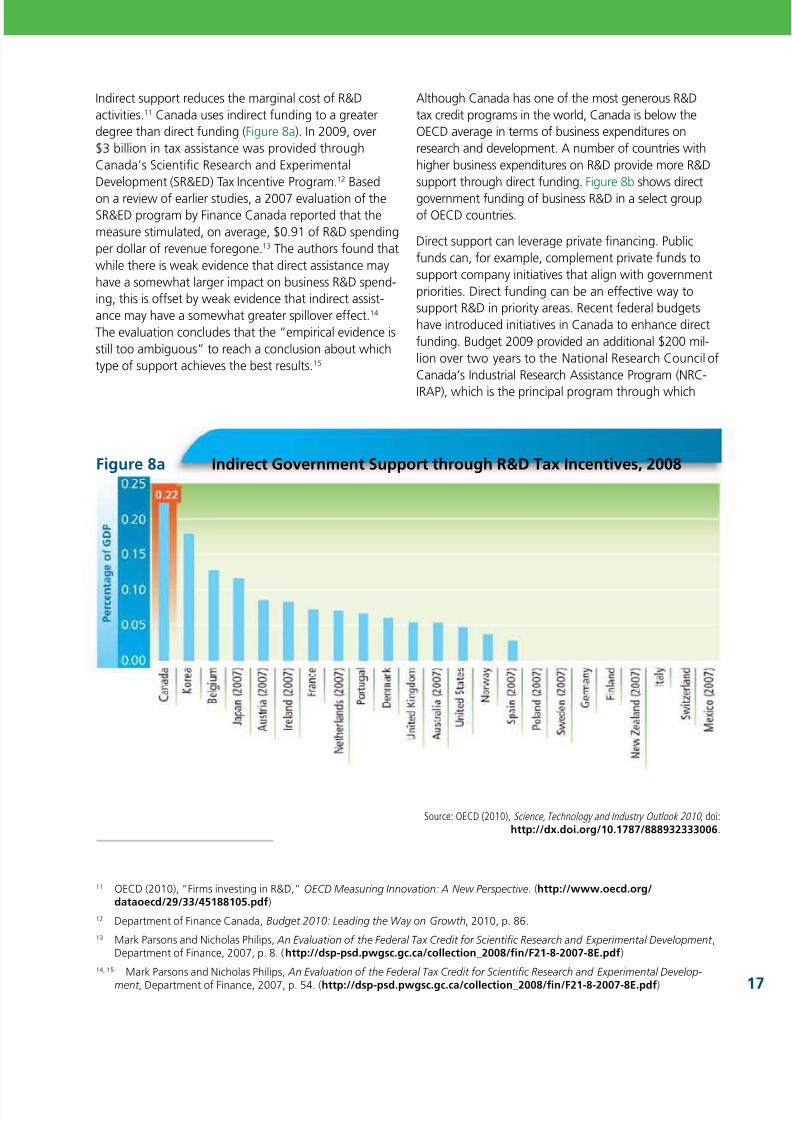

Indirect support reduces the marginal cost o R&Dactivities.11 Canada uses indirect unding to a greaterdegree than direct unding (Figure 8a). In 2009, over$3 billion in tax assistance was provided throughCanada’s Scientic Research and ExperimentalDevelopment (SR&ED) Tax Incentive Program.12 Based

on a review o earlier studies, a 2007 evaluation o theSR&ED program by Finance Canada reported that themeasure stimulated, on average, $0.91 o R&D spendingper dollar o revenue oregone.13 The authors ound thatwhile there is weak evidence that direct assistance mayhave a somewhat larger impact on business R&D spend-ing, this is oset by weak evidence that indirect assist-ance may have a somewhat greater spillover eect.14 The evaluation concludes that the “empirical evidence isstill too ambiguous” to reach a conclusion about whichtype o support achieves the best results.15

11 OECD (2010), “Firms investing in R&D,” OECD Measuring Innovation: A New Perspective. (http://www.oecd.org/dataoecd/29/33/45188105.pd)

12 Department o Finance Canada, Budget 2010: Leading the Way on Growth, 2010, p. 86.

13 Mark Parsons and Nicholas Philips, An Evaluation o the Federal Tax Credit or Scientic Research and Experimental Development ,Department o Finance, 2007, p. 8. (http://dsp-psd.pwgsc.gc.ca/collection_2008/fn/F21-8-2007-8E.pd )

14, 15 Mark Parsons and Nicholas Philips, An Evaluation o the Federal Tax Credit or Scientic Research and Experimental Develop-

ment , Department o Finance, 2007, p. 54. (http://dsp-psd.pwgsc.gc.ca/collection_2008/fn/F21-8-2007-8E.pd )

Figure 8a Indirect Government Support through R&D Tax Incentives, 2008

Source: OECD (2010), Science, Technology and Industry Outlook 2010 , doi:http://dx.doi.org/10.1787/888932333006.

Although Canada has one o the most generous R&Dtax credit programs in the world, Canada is below theOECD average in terms o business expenditures onresearch and development. A number o countries withhigher business expenditures on R&D provide more R&Dsupport through direct unding. Figure 8b shows direct

government unding o business R&D in a select groupo OECD countries.

Direct support can leverage private nancing. Publicunds can, or example, complement private unds tosupport company initiatives that align with governmentpriorities. Direct unding can be an eective way tosupport R&D in priority areas. Recent ederal budgetshave introduced initiatives in Canada to enhance directunding. Budget 2009 provided an additional $200 mil-lion over two years to the National Research Council oCanada’s Industrial Research Assistance Program (NRC-

IRAP), which is the principal program through which

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 28/86

State of the nation 2010

18

State of the nation 2010

16 National Research Council o Canada’s Industrial Research Assistance Program (NRC-IRAP).

17 OECD (2010), Science, Technology and Industry Outlook 2010, p.103.

18 Anne Palkamo, Finland Plans Tax Incentives or Companies’ R&D Activities, Tekes, 2009. (http://www.tekes.f/en/community/

News/482/News/1344?name=Finland+plans+tax+incentives+or+companies+R%26D+activities)

Figure 8b Direct Government Funding o Business R&D, 2008

Source: OECD (2010), Science, Technology and Industry Outlook 2010 , doi:http://dx.doi.org/10.1787/888932333006.

direct support is delivered to small and medium-sizedenterprises (SMEs). For scal year 2009–10, IRAP’sbudget included about $187 million in direct supportto rms.16 The Canadian Innovation Commercialization

Program (CICP) or small and medium-sized enterpriseswas launched in September 2010. The CICP is a twoyear, $40 million pilot initiative that will support up to20 innovative demonstration projects.

Although Canada has one o the most generous R&D tax credit programs in theworld, Canada is below the OECD averagein terms o business expenditures onresearch and development.

Direct unding through grants, subsidies and loans isthe most common orm o support or business R&D inOECD countries.17 Finland recently reviewed its undingmodel, recognizing that tax incentives can complementa system traditionally dependent on direct supportalone.18 In conducting its review, Finland identiedNorway as a country with a well-unctioning modelthat employs both direct and indirect support. In 2008,the ratio o direct to indirect support in Norway wasapproximately two to one.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 29/86

growth in Canada by industry and by sector, and thencompares labour productivity levels, and their deter-minants, with the United States. The our determinants

examined include: multiactor productivity, investmentsin machinery and equipment (M&E), inormation andcommunications technologies (ICT) (equipmentand services), and research and development.

This report also includes new innovation survey nd-ings on how Canadian-based enterprises innovate,the place o innovation in their corporate strategies,and their expenditures on product and process innova-tions. The growth o technology intensive commercialservices trade is also described and analyzed. Finally,the report points out sectoral dierences in how muchlarge, medium and small companies are investing inR&D and developments in the availability o venturecapital or Canadian businesses.

6.1.2 Productivity Growth or ImprovedStandards o Living“There are, o course, other actors besides produc-

tivity growth that aect our standard o living, such

as changes in Canada’s terms o trade (the prices we

receive or what we sell abroad relative to the prices

we pay or imports) and changes in employment

rates (the proportion o the population that is actually employed). However, productivity growth is the major

source o improvement in our economic well-being in

the long run. Gains in productivity allow businesses to

pay higher real (infation-adjusted) wages and still keep

costs down and stay protable and competitive. So,

rising productivity is vital to sustained improvements in

real incomes and living standards over time.”– Bank o Canada19

6.1 Busssiv idcrs

Private sector innovation is an engine o wealth cre-ation. For individual rms, developing new or improvedproducts can help preserve and capture market share,

increasing revenues and prots. I these innovationsmerely shit market share rom one company to another,consumers may benet rom added choice but overallwealth creation has not occurred. However, i innova-tion prompts other rms to improve their products tocompete, the result can be an improvement in the qual-ity o goods available to consumers — an improvementin consumers’ net wealth. Firms may also introduceprocess innovation to reduce costs, which can have theeect o increasing prot margins, lowering prices orconsumers, or both.

6.1.1 Going Beyond R&D Indicators toMeasure InnovationThe State o the Nation 2008 report reerred to thelinks between innovation, productivity and our stan-dard o living. It noted that Canadian industries investless in R&D and machinery and equipment than com-parable industries around the world. R&D expendituresare only one indicator o innovation, but an importantindicator that is well correlated with other contribu-tions to innovation.

Highly aggregated, national data can provide a useulbenchmark or the innovative perormance o an econ-omy, but it can mask signicant dierences in industrialcomposition and the perormance o individual indus-tries and rms. Some industries are inherently moreR&D- or ICT-intensive than others, and the relationshipbetween these variables and productivity (as is the casewith any metric o innovation) also varies by industry.

STIC’s State o the Nation 2010 explores businessinnovation on an industry and sector basis. This sectionbegins by presenting data on productivity levels and

Digest o Indicators6

19 Bank o Canada, Backgrounder on Productivity , 2010. (http://www.bankocanada.ca/en/backgrounders/bg-p4.html)

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 30/8620

State of the nation 2010

R&D in Oil Sands and Heavy Oil

Dr. Josephine Hill, Zandmer/Canada Research Chair inHydrogen and Catalysis, at the University o Calgary,and recipient o the 2008 Minerva Mentoring Awardor encouraging women in engineering, scienceand inormation technology.

R&D Sub-Priority: Energy Production in the Oil Sands

Steam-assisted gravity drainage (SAGD) technology isan example o innovation in the oil and gas industrythat developed through extensive eld testing. Twohorizontal wells are drilled in oil sands ormations toproduce bitumen — which is a mixture o sand, clay,water, and a dense and viscous orm o petroleum.The upper well injects steam into the ormation, andthe lower well collects the heated crude oil or bitu-

men that fows out o the ormation, along with anywater rom the condensation o injected steam. The heatrom the steam reduces the viscosity o the heavy crude

oil or bitumen. This enhanced oil recovery technologyis considered twice as ecient as the older cyclicsteam stimulation process.

SAGD has gone through several transormations sinceit was rst conceived by Roger Butler in the late 1960s.Alberta Innovates Technology Futures (AITF) is sup-porting the development o alternative SAGD produced

water treatment technologies (e.g., ceramic mem-branes). Nexen’s Long Lake Project in the Athabascaoil sands is the rst to combine SAGD with an upgraderprocess that yields premium synthetic crude through acomparatively more ecient use o natural gas.

Research in Catalysis

Research and development sub-priorities span basic toapplied research. For example, research by JosephineHill, Zandmer/Canada Research Chair in Hydrogenand Catalysis, at the University o Calgary, examines andimproves eciencies in chemical and electrochemicalprocesses that can have application in energy produc-tion. The work in the catalysis eld has implicationsor: environmental impact; the development o uelcells; hydrotreating o heavy oil; and gasication.Implications also impact the conversion o solid wastematerials, such as petroleum coke and biomass intoactivated carbon, which can be used to clean up gasand liquid exhaust streams. The spent activated carboncan then be gasied to produce gaseous products,such as methane and syngas.

Productivity measures the total amount o goodsand services produced in a country or each input toproduction, such as labour, capital or land. The mostcommon measure o productivity is labour productiv-ity, which measures the amount o goods and servicesproduced by one hour o labour.

In Canada, labour productivity levels and their growthvary tremendously between industries. For example,Figure 9 reveals that private sector labour productivitylevels in service industries were only 89 percent o theaverage or the entire economy. The sectors o miningand oil and gas extraction and utilities were sectorswith at least three times the private sector labourproductivity levels o the overall economy. Productivity

in these sectors has been decreasing to an average o-4.5 percent and -1.7 percent respectively in the 2003to 2008 period. A decrease o -2.3 percent in labourproductivity was also registered in the constructionsector. In contrast, above average labour productivitygrowth was experienced in most service industries aswell as in the sector o agriculture, orestry, shing andhunting and the manuacturing sector over the 2003to 2008 period. Signicant labour productivity growthwas also experienced in the wholesale and retail tradesectors, both o which increased by 3.4 percent peryear in the 2003 to 2008 period.

8/6/2019 State of the Nation 2010: Imagination to Innovation, Building Canadian Paths to Prosperity

http://slidepdf.com/reader/full/state-of-the-nation-2010-imagination-to-innovation-building-canadian-paths 31/86

The sources o the strong labour productivity growth inthe U.S. service industries are attributable to high levelso ICT capital spending and rapid multiactor produc-tivity (MFP) growth. Multiactor productivity measures

joint infuences on economic growth, such as techno-logical change, eciency improvements, and returns

to scale.21

Economic research on the United States’ productiv-ity growth “miracle” suggests that service industries’labour productivity growth rate increased rom 1.0 per-cent per year beore 1995 to 2.3 percent per year insubsequent years.20 Much o the amed revival o U.S.productivity growth is attributable to services produc-

tivity. U.S. labour productivity growth is actually notmiraculous, but rather the result o corporate action.

20 Barry P. Bosworth and Jack E. Triplett, Is the 21 st Century Productivity Expansion Still in Services? And What Should Be Done About It?, Brookings Institution, Washington, D.C., January 2007.

21 Bank o Canada, The Virtue o Productivity in a Wicked World , remarks delivered by Mark Carney at the Ottawa Economics

Association, Ottawa, Ontario, March 24, 2010.

Figure 9 Private Sector Labour Productivity (2008) and Private Sector LabourProductivity Growth (2003–2008), by Industry

*Private sector labour productivity is calculated as real private sector Gross Domestic Product (in CAD) divided by total hours workedNote: Sectors are comprised o many industr ies

Source: Compilation by STIC Secretariat based on data rom Statistics Canada

SECTOR or IndustryLabour

Productivity,*2008

LabourProductivity

Growth(Average Annual

Growth (%)),2003–2008

GOODS SECTOR

AGRICULTURE, FORESTRY, FISHING AND HUNTING 35.2 4.7

MINING AND OIL AND GAS EXTRACTION 117.7 -4.5

UTILITIES 135.5 -1.7

CONSTRUCTION 28.7 -2.3

MANUFACTURING 48.7 0.8

AVERAGE FOR GOODS SECTOR 47.3 -0.6

SERVICES SECTOR