State Liaison Roster, Reports and Updates · 2007-11-28 · Report Report LIAISONS Page LIAISONS...

186

Committee on State Regulation of Securities Page 1 Subcommittee on Liaisons to the States and NASD ABA Business Law Section Committee on State Regulation of Securities Subcommittee of Liaisons to the States and NASD State Liaison Roster, Reports and Updates as of September 21, 2007 Co-Chair: Mr. Donald A. Rett Law Office of Donald Rett 1660 Metropolitan Circle Tallahassee, Florida 32308 E-Mail – [email protected] (850) 298-4454 (Work) Co-Chair: Mr. Shane B. Hansen Warner Norcross & Judd LLP 111 Lyon Street, N.W. Grand Rapids, Michigan 49503 E-mail – [email protected] (616) 752-2145 (Work) Report Report LIAISONS Page LIAISONS Page AL Ms. Carolyn L. Duncan 7 Cabaniss Johnston, et al. Ste. 700, 2100 Park Pl N Birmingham, Alabama 35203-2744 E-Mail – [email protected] (205) 716-5200 (Work) (205) 716-5389 (Fax) AK Mr. Julius J. Brecht 10 Wohlforth, Johnson, Brecht, Cartledge & Brooking Suite 600, 900 West 5th Avenue, Anchorage, Alaska 99501-2044 Direct E-Mail – [email protected] (907) 276-6401 (Work) (907) 276-5093 (Fax) AZ Mr. Dee Riddell Harris Arizona Angels Venture Group, Inc. 2415 E. Camelback Rd., Suite 700 Phoenix, Arizona 85016 E-Mail – [email protected] (602) 508-6055 (Work) (602) 840-4078 (Home) (602) 508-6099 (Fax) (602) 840-6824 (Home Fax) AR Mr. John S. Selig 12 Mitchell, Williams, Selig, Gates & Woodyard, P.L.L.C. 425 West Capitol Avenue, Suite 1800 Little Rock, Arkansas 72201-3525 E-Mail – [email protected] (501) 688-8804 (Work) (501) 821-1540 (Home) (501) 688-8807 (Fax) CA Mr. Keith Paul Bishop 13 Buchalter Nemer Fields & Younger 184 Von Karman Avenue, #800 Irvine, California 92612 E-Mail – [email protected] (949) 224-6293 (Work) (949) 224-6228 (Fax) CO/MT/WY Mr. Robert J. Ahrenholz 20 Kutak Rock LLP 1801 California Street, Suite 3100 Denver, Colorado 80202 E-Mail – [email protected] (303) 297-2400 (Work) (303) 292-7799 (Fax)

Transcript of State Liaison Roster, Reports and Updates · 2007-11-28 · Report Report LIAISONS Page LIAISONS...

Committee on State Regulation of Securities Page 1 Subcommittee on Liaisons to the States and NASD

ABA Business Law Section Committee on State Regulation of Securities

Subcommittee of Liaisons to the States and NASD

State Liaison Roster, Reports and Updates as of September 21, 2007

Co-Chair: Mr. Donald A. Rett Law Office of Donald Rett 1660 Metropolitan Circle Tallahassee, Florida 32308 E-Mail – [email protected] (850) 298-4454 (Work)

Co-Chair: Mr. Shane B. Hansen Warner Norcross & Judd LLP 111 Lyon Street, N.W. Grand Rapids, Michigan 49503 E-mail – [email protected] (616) 752-2145 (Work)

Report Report LIAISONS Page LIAISONS Page AL Ms. Carolyn L. Duncan 7 Cabaniss Johnston, et al. Ste. 700, 2100 Park Pl N Birmingham, Alabama 35203-2744 E-Mail – [email protected] (205) 716-5200 (Work) (205) 716-5389 (Fax) AK Mr. Julius J. Brecht 10 Wohlforth, Johnson, Brecht, Cartledge & Brooking Suite 600, 900 West 5th Avenue, Anchorage, Alaska 99501-2044 Direct E-Mail – [email protected] (907) 276-6401 (Work) (907) 276-5093 (Fax) AZ Mr. Dee Riddell Harris Arizona Angels Venture Group, Inc. 2415 E. Camelback Rd., Suite 700 Phoenix, Arizona 85016 E-Mail – [email protected] (602) 508-6055 (Work) (602) 840-4078 (Home) (602) 508-6099 (Fax) (602) 840-6824 (Home Fax)

AR Mr. John S. Selig 12 Mitchell, Williams, Selig, Gates & Woodyard, P.L.L.C. 425 West Capitol Avenue, Suite 1800 Little Rock, Arkansas 72201-3525 E-Mail – [email protected] (501) 688-8804 (Work) (501) 821-1540 (Home) (501) 688-8807 (Fax) CA Mr. Keith Paul Bishop 13 Buchalter Nemer Fields & Younger 184 Von Karman Avenue, #800 Irvine, California 92612 E-Mail – [email protected] (949) 224-6293 (Work) (949) 224-6228 (Fax) CO/MT/WY Mr. Robert J. Ahrenholz 20 Kutak Rock LLP 1801 California Street, Suite 3100 Denver, Colorado 80202 E-Mail – [email protected] (303) 297-2400 (Work) (303) 292-7799 (Fax)

Report Report LIAISONS Page LIAISONS Page

Committee on State Regulation of Securities Page 2 Subcommittee on Liaisons to the States and NASD

CT Mr. Richard Slavin 44 Cohen and Wolf, P.C. 1115 Broad Street Bridgeport, CT 06604-4247 E-Mail – [email protected] (203) 337-4103 (Work) (203) 394-9901 (Fax) DE Mr. Andrew M. Johnston Morris Nichols, et al. Wilmington, Delaware 19899-1347 E-Mail – [email protected] (302) 351-9202 (Work) (302) 658-3989 (Fax) DC Ms. Michele A. Kulerman 48 Hogan & Hartson L.L.P. Columbia Square 555 Thirteenth St., N.W. Washington, D.C. 20004-1109 E-Mail – [email protected] (202) 637-5743 (Work) (301) 279-6772 (Home) (202) 637-5910 (Fax) FL Mr. Donald A. Rett 52 Law Office of Donald Rett 1660 Metropolitan Circle Tallahassee, Florida 32308 E-Mail – [email protected] (850) 298-4454 (Work) (904) 894-0700 (Home) (850) 298-4494 (Fax) GA J. Steven Parker 54 Page Perry, LLC 1040 Crown Pointe Parkway Suite 1050 Atlanta, Georgia 30338 E-Mail – [email protected] (770) 673-0047 (Work) (770) 673-0120 (Fax)

HA Mr. David J. Reber 57 Goodsill Anderson Quinn & Stifel 1099 Alakea Street, Suite 1800 Honolulu, Hawaii 96813 E-Mail – [email protected] (808) 547-5611 (Work) (808) 395-7994 (Home) (808) 547-5880 (Fax) ID Mr. Jeffrey W. Pusch Batt & Fisher, LLP 101 South Capitol Boulevard, 5th Fl. P.O. Box 1308 Boise, Idaho 83701 E-Mail – [email protected] (208) 331-1000 (Work) (208) 331-2400 (Fax) IL [IL liaison changing) 62 IN Mr. Stephen W. Sutherlin 64 Stewart & Irwin 251 East Ohio Street Suite 1100 Indianapolis, Indiana 46204 E-Mail – [email protected] (317) 639-5454 (Work) (317) 396-9541 (Direct Dial) (317) 733-8084 (Home) (317) 632-1319 (Fax) (317) 696-2254 (Cell) IA Ms. Katherine G. Manghillis 73 Schottenstein Zox & Dunn Co., LPA Arena District 250 West Street Columbus, OH 43215-2538 E-Mail –[email protected] (614) 462-1087 (Work) (614) 462-5135 (Fax)

Report Report LIAISONS Page LIAISONS Page

Committee on State Regulation of Securities Page 3 Subcommittee on Liaisons to the States and NASD

KS/MO Mr. William M. Schutte Polsinelli Law Firm 6201 College Blvd., Suite 500 Overland, KS 66211 E-Mail – [email protected] (913) 234-7414 (Work) (913) 451-6205 (Fax) (913) 345-0054 (Home) KY Mr. Manning G. Warren III University of Louisville Louis D. Brandeis School of Law 2301 South Third Street Louisville, Kentucky 40292 E-Mail – [email protected] (502) 852-7265 (Work) (502) 852-0862 (Fax) LA Mr. Carl C. Hanemann 78 Jones, Walker, Waechter, Poitevent, Carrere & Denegre, L.L.P. Place St. Charles 201 St. Charles Avenue, 51st Floor New Orleans, Louisiana 70170-5100 E-Mail – [email protected] (504) 582-8156 (Work) (504) 861-3992 (Home) (504) 582-8012 (Fax) ME Mr. Wayne E. Tumlin 83 Bernstein, Shur, Sawyer & Nelson, P.A. 100 Middle Street – W. Tower P.O. Box 9729 Portland, ME 04104-5029 E-Mail – [email protected] [email protected] (207) 774-1200 (Work) (207) 774-1127 (Fax) MD Mr. Wm. David Chalk Piper Marbury Rudnick & Wolfe LLP 6225 Smith Avenue Baltimore, MD 21209-3600 E-Mail – [email protected] (410) 580-4120 (Work) (410) 580-3001 (Fax)

MA Mr. Michael M. Jurasic 87 Ropes & Gray One International Place Boston, MA 02110-2624 (617) 951-7754 (Work) (617) 235-0698 (Fax) E-mail – [email protected] MI Mr. Shane B. Hansen 90 Warner Norcross & Judd LLP 111 Lyon Street, N.W., Suite 900 Grand Rapids, Michigan 49503-2487 E-mail – [email protected] (616) 752-2145 (Work) (616) 942-7063 (Home) (616) 752-2500 (Fax) MN (See IOWA) 96 MS Mr. Daniel G. Hise 99 Butler, Snow, O’Mara, Stevens & Cannada, PLLC P.O. Box 22567 Jackson, MS 39225-2567 E-Mail – [email protected] (601) 985-5711 (Work) (601) 355-1742 (Home) (601) 985-4500 (Fax) MO (SEE KANSAS) MT (SEE COLORADO) 101 NE Mr. David R. Tarvin, Jr. [New Street Address] Omaha, Nebraska 68102 E-Mail – david.tarvin@[email protected] (402) 960-1332 (Cell) NV Mr. Ken Creighton 9295 Prototype Drive Reno, NV 89511 E-Mail – [email protected] (775) 448-0119 (Work) (775) 825-1844 (Home) (775) 448-0120 (Fax)

Report Report LIAISONS Page LIAISONS Page

Committee on State Regulation of Securities Page 4 Subcommittee on Liaisons to the States and NASD

NH Mr. Richard A. Samuels 117 McLane, Graf, Raulerson & Middleton P.A. 900 Elm Street P.O. Box 326 Manchester, NH 03105-0326 E-Mail – [email protected] (603) 628-1470 (Work) (603) 228-8636 (Home) (603) 625-5650 (Fax)

NJ Mr. Peter D. Hutcheon 119

Norris, McLaughlin & Marcus, P.A. 721 Route 202-206 P. O. Box 1018 Somerville, New Jersey 08876-1018 E-Mail – [email protected] (856) 881-6621 (Work) (908) 356-4766 (Home) (908) 722-0755 (Fax) NM Mr. Robert G. Heyman Sutin Thayer & Browne 100 North Guadalupe, Suite 202 Santa Fe, NM 87501 Mailing Address: P.O. Box 2187 Santa Fe, NM 87504 E-Mail – [email protected] (505) 986-5493 (Work) (505) 982-5297 (Fax) NY Mr. F. Lee Liebolt, Jr. 129 Suite 2620 420 Lexington Avenue New York, New York 10170 E-Mail – [email protected] (212) 286-1384 (Work) (212) 369-8067 (Home) (212) 286-1389 (Fax) NC Mr. David N. Jonson 132 Kennedy Covington Lobdell & Hickman, L.L.P. 4350 Lassiter at North Hills Avenue Suite 300 (27609) Post Office Box 17047 Raleigh, North Carolina 27619-7047 E-Mail – [email protected] (919) 743-7308 (Work) (919) 639-0598 (Home) (919) 516-2008 (Fax)

ND Mr. Craig A. Boeckel Tschider & Boeckel Provident Life Building 316 N. 5th Street P. O. Box 668 Bismarck, North Dakota 58502-0668 E-Mail – [email protected] (701) 258-2400 (Work) (701) 258-9269 (Fax) OH Mr. Edward D. McDevitt 135 Bowles Rice McDavid Graff & Love LLP 60 Quarrier Street Charleston, WV 25301 P.O. Box 1386 Charleston, WV 25325-1386 E-Mail – [email protected] (304) 347-1711 (Work) (304) 343-3058 (Fax) OK Mr. C. Raymond Patton, Jr. Conner & Winters A Professional Corporation 3700 First Plaza Tower 15 East Fifth Street Tulsa, OK 74103 E-Mail – [email protected] (918) 586-8523 (Work) (918) 299-5838 (Home) (918) 586-8548 (Fax) OR Mr. Richard M. Layne Layne & Lewis 111 SW Columbia Street, Suite 1000 Portland, OR 97201 E-Mail – [email protected] (503) 295-1882 (Work) (503) 246-1441 (Home) (503) 295-2057 (Fax) PA Mr. Michael Pollack Reed, Smith, Shaw & McClay LLP One Liberty Place, Suite 2500 1650 Market Street Philadelphia, PA 19103-7301 E-Mail – [email protected] (215) 851-8182 (Work) (215) 628-9904 (Home) (215) 851-1420 (Fax)

Report Report LIAISONS Page LIAISONS Page

Committee on State Regulation of Securities Page 5 Subcommittee on Liaisons to the States and NASD

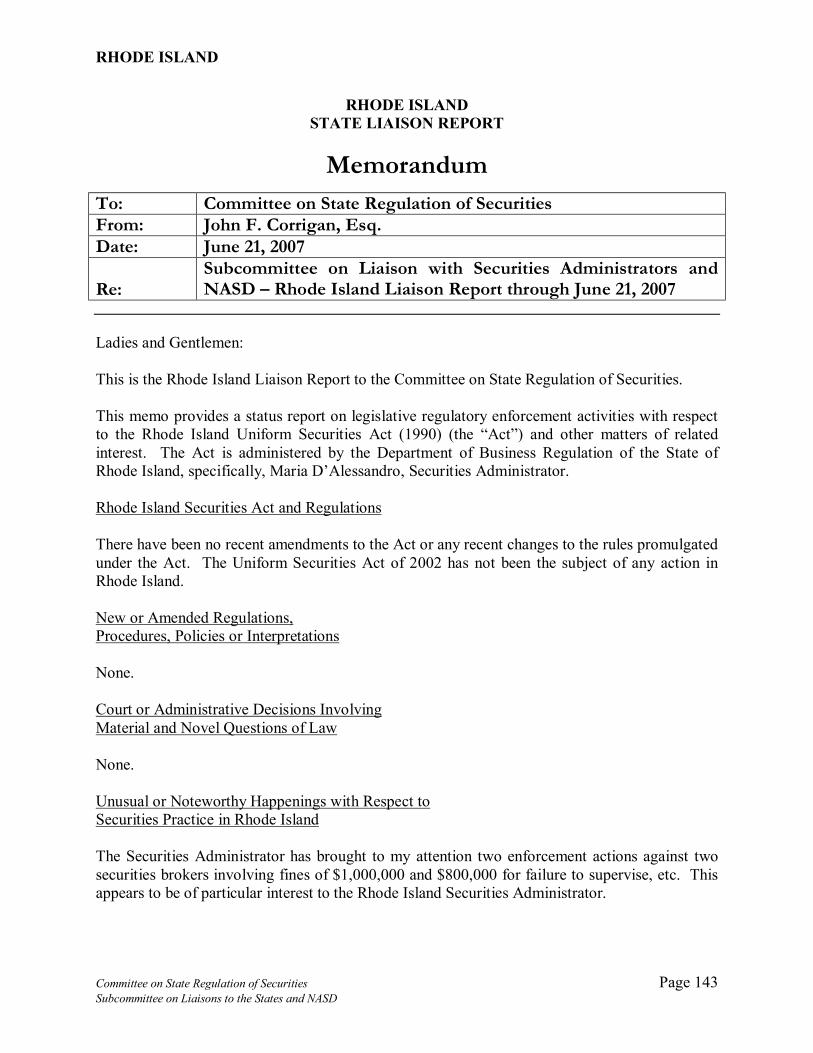

PR [VACANT] RI Mr. John F. Corrigan 143 Adler Pollock & Sheehan PC 1 Citizens Plz. Ste. 800 Providence, Rhode Island 02903-1345 E-Mail – [email protected] (401) 274-7200 (Work) (401) 885-1025 (Home) (401) 751-0604 (Fax) or 351-4607 SC Mr. F. Daniel Bell III 145 Kennedy Covington Lobdell & Hickman L.L.A. 434 Fayetteville Street Mall, 19th Fl. Raleigh, NC 27602-1070 E-Mail – [email protected] (919) 743-7335 (Work) (919) 872-7886 (Home) (919) 516-2035 (Fax) SD Mr. Charles D. Gullickson 146 Davenport, Evans, Hurwitz & Smith, L.L.P. 206 West 14th Street P. O. Box 1030 Sioux Falls, South Dakota 57101-1030 E-Mail – [email protected] (605) 357-1270 (Work) (605) 331-3880 (Home) (605) 335-3639 (Fax) TN Ms. E. Marlee Mitchell Waller Lansden Dortch & Davis, PLLC Nashville City Center Suite 2100, 511 Union Street Nashville, Tennessee 37219-1760 E-Mail – [email protected] (615) 244-6380 (Work) (615) 298-2514 (Home) (615) 244-6804 (Fax)

TX Mr. Daniel R. Waller 151 Secore & Waller LLP Suite 1100 12221 Merit Dr. Dallas, TX 75251-2227 E-Mail – [email protected] (972) 776-0200 (Work) (972) 392-2452 (Home) (972) 776-0240 (Fax) USVI Mr. Tom Bolt Tom Bolt & Associates PC Corporate Place 5600 Royal Dane Mall St. Thomas, VI 00802-6410 E-Mail – [email protected] (340) 774-2944 (Work) (340) 776-1639 (Fax) UT Mr. Arthur B. Ralph 157 Van Cott, Bagley, Cornwall & McCarthy, P.C. 50 South Main Street, Suite 1600 Salt Lake City, Utah 84144-0450 E-Mail – [email protected] (801) 532-3333 (Work) (801) 272-5027 (Home) (801) 534-0058 (Fax) VT Mr. William (Chip) A. Mason 169 Gravel and Shea 76 St. Paul Street, 7th Floor P.O. Box 369 Burlington, VT 05402-0369 E-Mail – [email protected] 802.658.0220 (Work) 802.658.1456 (Fax) VA Mr. Thomas G. Voekler 171 Hirschler Fleischer The Edgeworth Building 2100 E. Cary Street Richmond, Virginia 23223-7078 Post Office Box 500 Richmond, Virginia 23218-0500 E-mail – [email protected] (804) 771-9599 (Work) (804) 241-3529 (Cell) (804) 644-0957 (Fax)

Report Report LIAISONS Page LIAISONS Page

Committee on State Regulation of Securities Page 6 Subcommittee on Liaisons to the States and NASD

WA Mr. John L. Mericle 172 Harris, Mericle & Wakayama 999 Third Avenue, Suite 3210 Seattle, Washington 98104 E-Mail – [email protected] (206) 621-1818 (Work) (206) 624-8560 (Fax) WV Mr. Edward D. McDevitt 175 Bowles Rice McDavid Graff & Love, PLLC 600 Quarrier Street Charleston, West Virginia 25314 E-Mail – [email protected] (304) 347-1711 (Work) (304) 345-4188 (Home) (304) 343-3058 (Fax) WI Mr. Terry Nelson 176 Foley & Lardner 150 East Gilman P.O. Box 1497 Madison, WI 53701 E-Mail – [email protected] (608) 258-4232 (Work) (608) 836-8855 (Home) (608) 258-4258 (Fax) WY SEE COLORADO 178 CAN Mr. Paul G. Findlay 184 Borden Ladner Gervais LLP Scotia Plaza, Suite 4400 40 King Street West Toronto, Ontario M5H 3Y4 Canada E-Mail – [email protected] (416) 367-6191 (Work) (416) 484-9862 (Home) (416) 361-7083 (Fax) NASD Mr. Peter W. LaVigne Sullivan & Cromwell LLP 125 Broad Street New York, NY 10004 E-Mail – [email protected] (212) 558-7402 (Work) (212) 558-3588 (Fax)

ALABAMA

Committee on State Regulation of Securities Page 7 Subcommittee on Liaisons to the States and NASD

ALABAMA STATE LIAISON REPORT

TO THE ABA STATE REGULATION OF SECURITIES COMMITTEE

This report summarizes significant development in the securities laws of Alabama during the past year, and updates matters previously reported to the Committee. Proposed Statutory Changes

Following unsuccessful attempts in 2004, 2005 and 2006 to adopt the 2002 Uniform Securities Act, the Alabama Securities Commission this year sought piecemeal legislation to increase filing fees, criminal penalties and civil fines, plus a few changes intended to conform the Alabama statutes to NSMIA. This year’s legislative attempt also failed, but only as a result of an overall political deadlock in the Alabama Senate and not as a consequence of any known opposition to the proposal. The bill is expected to be reintroduced in the next legislative session.

Alabama’s version of the 2002 Uniform Securities Act, a project of the Alabama Law Institute

and unanimously supported by the Law Institute’s Securities Act Committee, was repeatedly blocked by the life insurance industry over the issue of variable annuities. The proposed act would have included variable annuities within the definition of security, but exempt them from securities registration, thus giving the Securities Commission enforcement authority to address sales practice abuses. While variable annuities have been the subject of regulatory turf battles in some states, that is not the case here; in the last effort to pass the bill in 2006, the Commissioner of Insurance also supported the Securities Commission and the Law Institute.

The changes proposed for adoption this year, and expected to be reintroduced in the next

legislative session (beginning in February, 2008, or possibly later this year if a special session is called) are as follows:

Fee Increases

• Broker-dealer and investment adviser registration and annual fees will increase from

$200 to $250, and fees for agents/associated persons of broker-dealers and investment advisers will increase from $50 to $60 annually.

• Notice filing fees for mutual funds that are covered securities will increase slightly, from

$1040 initial filing and $1000 annually, to a graduated annual filing fee ranging from $350 for up to $25 million in net assets, to $1200 for over $100 million in net assets.

• Notice filing fees and fees for all other securities registrations will remain at one-tenth of

one percent, but the minimum and maximum fee amounts will increase from $40 and $1000 to $100 and $1500.

• Notice filing fees for Rule 506 offerings and fees for other exemptions requiring filing

fees, including requests for waivers, will increase from $250 to $300.

ALABAMA

Committee on State Regulation of Securities Page 8 Subcommittee on Liaisons to the States and NASD

Criminal Penalty Increases

• Criminal penalties will be increased from Class C felonies to Class B felonies (two to twenty year prison terms and fines up to $10,000 plus twice the amount of any criminal gain) for:

o Willful violations of the strict liability provisions of Code of Alabama 1975, as

amended (the Code), § 8-6-3 (registration requirements for broker-dealers, agents, investment advisers and investment adviser representatives), and Code § 8-6-4 (securities registration requirements); and

o Violations of the anti-fraud statute, Code § 8-6-17 (a), (b) or (c).

NSMIA Conforming Changes

• A new Code section 8-6-5 would replace the existing provision for registration by notification, no longer of any use, with the equivalent of section 302 of the 2002 Uniform Act. This will not resolve all the statutory inconsistencies occasioned by NSMIA, but will at least clarify the filing requirements for covered securities of registered investment companies under 18(b)(2) and Rule 506 offerings under 18(b)(4)(D) of the Securities Act of 1933 (15 U.S.C. Section 77r(b)(4)(D).

The foregoing is a synopsis of House Bill 797, as introduced in the 2007 Regular Session of the Alabama Legislature, the full text of which is available from the Alabama Legislative Information System at

http://alisdb.legislature.state.al.us/acas/ACASLogin.asp. I will also be happy to send a copy to anyone who wishes. Regulatory Changes to be Considered

For several years now, the Commission has delayed a long-needed comprehensive review of its regulations in anticipation of the eventual adoption of the new Uniform Act. Given the unlikelihood of a new act in the foreseeable future, that review is expected to be undertaken in the next year. Commission Director Joe Borg requests that anyone who is aware of specific problem areas or otherwise has suggestions or comments please convey those, either directly to the Commission staff (contact Associate Counsel Ed Reed or Registration Manager Lisa Tolar), or to me. As the project gets underway, I will stay in close touch with the Commission and will be seeking input from the securities bar. Proposed new regulations will be published for comment prior to adoption, and I will also be happy to provide copies to anyone interested or otherwise facilitate bar involvement. Case Law: Immateriality as a Matter of Law A decision last fall by the Alabama Supreme Court has added another case to the relative few holding that alleged misrepresentations and omissions of fact were not material, as a matter of law. Blackmon v. Nexity Financial Corporation, 953 So.2d 1180 (Ala. 2006), explicitly relying on federal interpretations of materiality, held that materiality is not necessarily a factual question for a jury when the alleged misrepresentations and omissions

ALABAMA

Committee on State Regulation of Securities Page 9 Subcommittee on Liaisons to the States and NASD

“1) are of such common knowledge that a reasonable investor can be presumed to understand them; 2) present or conceal such insignificant data that, in the total mix of information, it simply would not matter; 3) are so vague and of such obvious hyperbole that no reasonable investor would rely upon them; or 4) are accompanied by sufficient cautionary statements.” Blackmon, 953 So.2d at 1192, quoting In re Amdocs Ltd. Sec. Litig., 390 F.3d 542, 548 (8th Cir. 2004).

In this instance, the private offering memorandum contained numerous specific cautionary statements relating directly to the alleged misrepresentations and omissions, sufficient to invoke the “bespeaks caution” doctrine. The Court also found that the that written cautionary statements took precedence over alleged contradictory oral representations and rendered the oral representations immaterial as a matter of law.

June 21, 2007 Carolyn L. Duncan Cabaniss, Johnston, Gardner, Dumas & O’Neal LLP Suite 700 2001 Park Place North Birmingham, Alabama 35203 Telephone (205) 716-5200 Fax (205) 716-5389 Email: [email protected]

ALASKA

Committee on State Regulation of Securities Page 10 Subcommittee on Liaisons to the States and NASD

ALASKA STATE LIAISON REPORT

-----Original Message----- From: Julius Brecht [mailto:[email protected]] Sent: Friday, June 15, 2007 7:10 PM To: Lieberman, Ellen Subject: ABA Committee State Securities 6/07 Report As requested, the report from Alaska on activities of the Alaska Division of Banking and Securities since my last report dated 1/13/07 is as follows: (1) The Alaska Division of Banking and Securities continues its interest and efforts to seek support for the repeal and reenactment of the Alaska Securities Act to follow the provisions of USA 2002. In 1959, Alaska was the first state to adopt the then Uniform Securities Act. In January 2007, the Alaska legislature convened the first session of a two session legislature. A committee was formed to work on the content of the bill submitted to the legislature, and I am on that committee. However, the bill remains in its first legislative committee of referral. I have spoken with the Alaska Administrator about the effort to be launched for the next session of the legislature in 2008. If the bill does not pass at that session it dies, and any further effort on change to ASA would have to be through a new bill submitted at the earliest to the new legislature to convene in 2009. (2) Under the current ASA, in addition to the "uniform" provisions of ASA having close correspondence with the uniform act, the Alaska Administrator of Securities has the unique responsibility to respond to complaints filed by shareholders of Native corporations as to the fair disclosure of information in proxy statements used in special and annual meetings of shareholders of the corporations. These Native corporations are ones formed pursuant to the Alaska Native Claims Settlement Act of 1991, as amended, and under the provisions of the Alaska corporate. Under ASA, the administrator adopted regulations in the early 1980s setting forth required content of proxy materials and allowable means of proxy solicitation. These regulations are based upon SEC regulations in place at that time and applying to corporations throughout the country and of a comparable size. Under this law, the division receives numerous proxy filings. During 2007, the division responded to numerous complaints. The complaints are processed through an independent hearing process administered through the division with an independent hearing officer making findings of fact and conclusions of law and recommendations for action to the administrator. (3) Changes to the Native proxy regulations proposed prior to 2006 have not been acted upon by the division. The state has a new governor as a result of an election late last year. Remains uncertain at this point as to what action if any might be taken with respect to the proposed regulations.

ALASKA

Committee on State Regulation of Securities Page 11 Subcommittee on Liaisons to the States and NASD

(4) While the division had ongoing investigations during this period, there were no other administrative actions or enforcement actions of note finalized during the period. (5) The division's senior securities examiner retired earlier this year. His replacement is Angela Otis. (6) The division's senior bank and financial institutions examiner will retire next month. No replacement had been announced as of the date of this report. The banking section and the securities section within the division work closely on investigations and other things of mutual interest regarding the areas regulated through the division. As in the past, please send me a copy of the full report to the committee in which the outline is placed. Thanks. 1967-2007: Celebrating 40 Years of Service in Alaska Julius J. Brecht Wohlforth, Johnson, Brecht, Cartledge & Brooking [email protected] www.akatty.com Phone: 907.276.6401 Fax: 907.276.5093

ARKANSAS

Committee on State Regulation of Securities Page 12 Subcommittee on Liaisons to the States and NASD

ARKANSAS STATE LIAISON REPORT

MEMORANDUM TO: Committee on State Regulation of Securities

FROM: John S. Selig

DATE: June 21, 2007

RE: Subcommittee on Liaison with Securities Administrators and NASD Arkansas Liaison Report and Enforcement Actions Through May 31, 2007

Ladies and Gentlemen:

This is the Arkansas Liaison Report as of May 31, 2007, to the Committee on State Regulation of Securities. This letter provides a status report since January 1, 2006, on legislative, regulatory, and enforcement activities with respect to Arkansas Uniform Securities Act, as amended (“Arkansas Securities Act”), and other matters of related interest.

The Arkansas Securities Act is administered by Arkansas Securities Commissioner (the “Commissioner”).

Arkansas Securities Act and Regulations

There have been no amendments to the Arkansas Securities Act nor any changes to the rules promulgated under the Act since January 1, 2006. The Uniform Securities Act of 2002 has not been adopted in Arkansas.

Change in Governor

Governor Mike Beebe, a Democrat, took office in January 2007 from Mike Huckabee, a Republican. The Commissioner serves at the pleasure of the Governor. The current Commissioner, Michael Johnson, was appointed by Governor Huckabee. No announcement has yet been made about whether Commissioner Johnson will stay or be replaced.

Please let me know if you have any questions.

John S. Selig

CALIFORNIA

Committee on State Regulation of Securities Page 13 Subcommittee on Liaisons to the States and NASD

CALIFORNIA STATE LIAISON REPORT

MEMORANDUM To: Ellen Lieberman, Chair

The State Regulation of Securities Committee of the Section of Business Law of the American Bar Association

File No.: 77706-0010

From: Keith Paul Bishop

Date: January 22, 2007

Subject: California Liaison Report

The following are the principal developments with respect to the California Department of Corporations and the California Corporate Securities Law of 1968: APPOINTMENT OF NEW COMMISSIONER On June 2, 2006, Governor Schwarzenegger appointed Preston DuFauchard as Commissioner of Corporations. Mr. DuFauchard previously acted as assistant general counsel for Bank of America. In that capacity, he supervised securities litigation related to mergers, investment banking, and broker-dealer operations. Before then, he was a partner in the law firm of Landels, Ripley and Diamond. He received his law degree from Boalt Hall School of Law at the University of California, Berkeley and his undergraduate degree from Stanford University. The appointment is subject to confirmation by the California Senate. MINOR LEGISLATIVE CHANGES During 2006, the California legislature enacted only minor changes to the Corporate Securities Law of 1968. Section 25005.1 was amended to include references to the newly enacted Uniform Partnership Act of 2008, which will become operative on January 1, 2008. (A.B. 339 §32, Chapter 495, Statutes of 2006). The legislature also made some non-substantive changes to Section 25100.1 (SB 1852, §83, Chapter 538, Statutes of 2006). PROPOSED AMENDMENTS TO COMPENSATORY BENEFIT PLAN RULES The Department of Corporations has proposed various amendments to its compensatory benefit plan regulations under the Corporate Securities Law of 1968. Specifically, the Department has proposed amending Sections 260.140.8, 260.140.41, 260.140.42, 260.140.45, and 260.140.46 of Title 10, California Code of Regulations. The proposed amendments relate to

CALIFORNIA

Committee on State Regulation of Securities Page 14 Subcommittee on Liaisons to the States and NASD

the standards governing exercise and purchase prices, vesting periods and approval procedures for compensatory option arrangements, The amendments would also make other clarifying and conforming changes. The comment period for these proposed amendments ended on December 18, 2006. The notice, a revised notice, proposed text of amendments, and initial statement of reasons are posted on the Department’s website, www.cal.ca.gov. PROPOSED AMENDMENTS REGARDING THE MANDATORY USE OF THE INVESTMENT ADVISOR REGISTRATION DEPOSITORY (IARD) The Department of Corporations has proposed to amend Sections 260.230, 260.231, 260.236.1, 260.241.4 and 260.242, and repeal Sections 260.231.2 and 260.236.2, of Title 10, California Code of Regulations. Legislation that took effect on January 1, 2005 (Chapter 461, Statutes of 2004) requires all investment adviser and investment adviser representative applications and other specified documents to be filed electronically with and transmitted to the web-based IARD, which is operated by the National Association of Securities Dealers. The proposed amendments would make conforming changes to the rules regarding the filing of applications and amendments. In 2003, the California legislature added Section 25612.3 to the California Corporations Code (Chapter 473, Statutes of 2003) to require the Commissioner of Corporations to use certain forms in connection with the licensing of broker-dealers and investment advisers. Because the forms are now required by statute, all existing versions of these forms are being redacted in this rulemaking proposal. Finally, this rulemaking action eliminates the reference to the appeal process pursuant to the Permit Reform Act. That law was repealed in 2003 (Chapter 229, Statutes of 2003). The comment period for this proposal ended on September 18, 2006. The notice, proposed text of amendments, and initial statement of reasons are posted on the Department’s website, www.cal.ca.gov. INVITATION FOR COMMENTS ON REGULATION OF FINDERS IN SECURITIES OFFERINGS The Department of Corporations has invited comments on the question of whether the Department should adopt an exemption and/or limited registration system for finders and private placement broker-dealers. The comment period ended on December 28, 2006. The invitation for comment is posted on the Department’s website, www.cal.ca.gov.

CALIFORNIA

Committee on State Regulation of Securities Page 15 Subcommittee on Liaisons to the States and NASD

CALIFORNIA SUPREME COURT CLARIFIES WHETHER GUILTY KNOWLEDGE IS AN ELEMENT OF THE CRIME OF SELLING UNQUALIFIED SECURITIES In People v. Salas, 37 Cal.4th 967, 127 P.3d 40, 38 Cal.Rptr.3d 624 (2006), the California Supreme Court addressed whether a defendant’s good faith belief that the offer and sale of securities was exempt from qualification was relevant to the defendant’s criminal culpability. The court held that “a seller who believes reasonably and in good faith that a security is exempt is not guilty of the crime of unlawful sale of an unregistered security.” However, the court explained that guilty knowledge is not an element of the crime but an affirmative defense. This case follows the Supreme Court’s prior decision in People v. Simon, 9 Cal.4th 493, 37 Cal.Rptr.2d 278, 886 P.2d 1271 (1995). Simon involved a criminal conviction under California Corporations Code Section 25401 which prohibits the offer and sale of securities "by means of any written or oral communication which includes an untrue statement of a material fact or omits to state a material fact necessary in order to make the statements made . . . not misleading." The court in Simon held that "knowledge of the falsity or misleading nature of a statement or of the materiality of an omission, or criminal negligence in failing to investigate and discover them, are elements of the criminal offense described in section 25401."

CALIFORNIA

Committee on State Regulation of Securities Page 16 Subcommittee on Liaisons to the States and NASD

MEMORANDUM To: Committee on State Regulation of Securities File No.: 77706-0010

From: Keith Paul Bishop

Date: June 12, 2007

Subject: California Liaison Report

1. Confirmation of Commissioner DuFauchard.

The California Senate has confirmed the appointment of Commissioner Preston DuFauchard by a vote of 36-0. Governor Schwarzenegger appointed Commissioner DuFauchard in June of last year. In California, a gubernatorial appointee may serve in office prior to confirmation. However, the office becomes vacant if the Senate fails or refuses to confirm within 365 days after the day the appointee first began performing the duties of the office. Cal. Gov. Code § 1774(c). Commissioner DuFauchard serves at the pleasure of the governor. Cal. Corp. Code § 25600. The Department of Corporations is part of the much larger California Business, Transportation & Housing Agency and the Commissioner of Corporations is subject to the general supervision of the Secretary of that agency. Cal. Gov. Code § 13978.

Mr. DuFauchard previously acted as assistant general counsel for Bank of America. In that capacity, he supervised securities litigation related to mergers, investment banking and broker-dealer operations. Before then he was a partner in the law firm of Landels, Ripley and Diamond. He received his law degree from Boalt Hall School of Law at the University of California, Berkeley and his undergraduate degree from Stanford University.

2. Commissioner Adopts Changes to Investment Adviser Regulations.

The Commissioner of Corporations has adopted regulations to clarify that all applications, reports and other documents must be filed electronically through the Investment Adviser Registration Depository in accordance with California Corporations Code Section 25231. The amendments also eliminate references to the California Permit Reform Act which was repealed in 2003. 2003 Stats. Ch. 229 (AB 1757). The sections amended are: 10 CCR §§ 260.230, 260.231, 260.236.1, 260.241.4, and 260.242. In addition, the following sections were repealed: 10 CCR §§ 260.231.2 and 260.236.2. The regulations were filed with the Secretary of State on March 6, 2007 and became effective on April 5, 2007.

3. Commissioner Finalizes Changes to Compensatory Benefit Plan Regulations.

The Commissioner of Corporations has completed the notice and comment process for proposed changes in the compensatory benefit plan regulations. This culminates many years of on and off again proposals to amend these regulations. The Department of Corporations first proposed amendments to these regulations in 1999 but the proposal was dropped. A few years later, the Department of Corporations adopted amendments to the regulations to account for options

CALIFORNIA

Committee on State Regulation of Securities Page 17 Subcommittee on Liaisons to the States and NASD

granted by limited liability companies. Although encouraged to do so, the Department declined to extend the rulemaking to the changes that it had proposed in 1999. In 2002, the Department issued an invitation for comment on amending the regulations. However, the Department again declined to take action. In November 2006, Commissioner DuFauchard proposed changes. This time the Department has completed the rulemaking process. The amendments affect the following sections: 10 CCR §§ 260.1 40.8 (restrictions on transfer); 260.140.41 (employee, director and consultant options); 260.140.42 (employee, director, manager and consultant purchases); 260.140.45 (limitation on the number of shares) and 260.140.46 (information to security holders). In accordance with California’s Administrative Procedure Act, the regulations have been filed with the Office of Administrative Law. That office reviews regulations for compliance with the rulemaking provisions of California law. If approved, the regulations are filed with the Secretary of State. Generally, regulations become effective 30 days after filing with the Secretary of State. Cal. Gov. Code Section 11343.4. However, I understand that the Commissioner has requested that the regulations become effective upon filing with the Secretary of State.

4. Covered Securities Filing Release.

On February 5, 2007, Commissioner DuFauchard issued a revision to Release 109-C. This revision updates the requirements with respect to filings under the National Securities Markets Improvement Act of 1996.

CALIFORNIA

Committee on State Regulation of Securities Page 18 Subcommittee on Liaisons to the States and NASD

MEMORANDUM To: Committee on State Regulation of Securities File No.: 77706-0010

From: Keith Paul Bishop Buchalter Nemer

Date: September 7, 2007

Subject: California Liaison Report - Update

1. Investment Adviser Omnibus Rulemaking. The Commissioner has proposed to adopt, repeal, and amend rules under the Corporate Securities Law of 1968 relating to the regulation of investment advisers. Specifically, the Commissioner proposes to effect the following changes to Title 10 of the California Code of Regulations:

• amend Sections 260.231, 260.235, 260.237, 260.237.2, 260.238, and 260.241.3;

• repeal Section 260.237.1; and

• adopt Sections 260.235.5, 260.238.1, 260.238.2, 260.238.3, and 260.238.4.

Comments on the Commissioner’s proposal may be submitted to Karen Fong, Office of Legislation and Policy, Department of Corporations, 1515 K Street, Suite 200, Sacramento, California, 95814-4052. Comments are due no later than 5:00 p.m., October 30, 2007.

2. Certifications of the NASDAQ Global Market. On August 9, 2007, the Commissioner of Corporations issued Revised Release Nos. 87-C and 88-C. Release No. 87-C provides certification of the NASDAQ Global Market of the NASDAQ Stock Market LLC, pursuant to subdivision (o) of California Corporations Code Section 25100. Section 25100(o) provides an exemption for securities listed on a national securities exchange, as certified by the Commissioner, from the qualification provisions of Sections 25110, 25120, and 25130. Release 88-C provides certification of the NASDAQ Global Market of the NASDAQ Stock Market LLC, pursuant to subdivision (a) of Corporations Code Section 25101. Section 25101(a) provides an exemption for securities of issuers whose securities are listed on certain national exchanges, in particular those exchanges certified by the California Corporations Commissioner, from the qualification provisions of Section 25130. 3. California Appellate Court Finds No NSMIA Preemption for State Attorney General Action. In People v. Jones (Aug. 24, 2007), the California Attorney General brought an action against a brokerage firm for failing to disclose adequately to investors and potential investors certain shelf-space” agreements under which the broker received additional compensation for selling certain preferred mutual funds. The Court of Appeal found that the action is not preempted by the National Securities Markets Improvement Act of 1966 because it is a type of action expressly permitted by that statute. The Court also concluded that the action is

CALIFORNIA

Committee on State Regulation of Securities Page 19 Subcommittee on Liaisons to the States and NASD

not preempted by the United States Securities and Exchange Commission Rule 10b-10 because the action does not conflict with that rule. 4. California Appellate Court Holds that Department of Corporations is not Liable for Investor Losses. In Dept. of Corp. v. Superior Court, 153 Cal. App. 4th 916 (2007), the Court of Appeal found that the Department of Corporations was not liable for investment losses suffered by investors who purchased fraudulent securities from brokers subject to "desist and refrain orders" after those orders were rescinded by the Department.

COLORADO

Committee on State Regulation of Securities Page 20 Subcommittee on Liaisons to the States and NASD

COLORADO STATE LIAISON REPORT

January 2007 Update

COLORADO The Colorado Division of Securities is a unit of the Colorado Department of Regulatory Agencies. Its mission is to protect investors and maintain public confidence in the securities markets while avoiding unreasonable burdens on participants in the capital markets. In this capacity, the Colorado Division of Securities is responsible for the administration and enforcement of the Colorado Securities Act (the “CSA”), the Colorado Commodity Code, the Colorado Municipal Bond Supervision Act, the Local Government Investment Pool Trust Fund Administration and Enforcement Act and the rules and regulations promulgated thereunder. The Colorado Division of Securities licenses and regulates stockbrokers and investment advisers and the securities they offer, sell and advise about in the State of Colorado. For additional information, visit the Colorado Division of Securities’ Web site at: www.dora.state.co.us.1

I. New Statutory Amendments, New or Amended Regulations or Administrative Procedures in Securities Regulation: The Second Regular Session of the Sixty-Fifth General Assembly convened on January 11, 2006 and adjourned on May 10, 2006 and the First Extraordinary Session convened on July 6, 2006 and adjourned on July 10, 2006. Since the June 2006 Update, the following bill relating to Colorado securities and securities regulation law was passed by the Colorado General Assembly:

a. House Bill No.06-1356: Concerning the exemption of certain licensed professionals from the requirement to obtain a supervised lender license in order to take assignment of supervised loans in default and, in connection therewith, specifically exempting Colorado-licensed collection agencies and attorneys from supervised lender licensing when taking assignment of supervised loans in default. This bill exempts licensed collection agencies and collection attorneys licensed to practice law in the State of Colorado from also having to be licensed as supervised lenders when taking assignment of supervised loans only after such loans are in default. Effective April 18, 2006.

II. Court or Administrative Decisions Addressing Novel Questions of Law or Changing Prior Interpretations of Law in Significant Ways: Since the June 2006 Update, although there have not been any court decisions addressing novel questions of law the following summaries of Court of Appeals decisions:

a. No. 01CA2020. People v. Pahl. Securities Fraud—Theft—At-Risk Adult—Computer Crime—Farmout Agreement—Oil and Gas Lease—Investors—Motion to Suppress—Evidence—Search Warrant—Warrantless Search—Indictment—Simple Variance—Testimony—Jury Instructions. Defendant appeals the judgment of conviction entered on jury

1 The information contained in the foregoing paragraph was obtained on 01/22/07 at http://www.dora.state.co.us/Securities/ (last updated 01/22/07).

COLORADO

Committee on State Regulation of Securities Page 21 Subcommittee on Liaisons to the States and NASD

verdicts finding him guilty of six counts of securities fraud, two counts of theft from an at-risk adult, and one count of computer crime.

The judgment is affirmed in part and reversed in part, and the case is remanded with directions. The evidence in this case established that defendant, in his capacity as president of Rautena Exploration Company (“Rautena”), entered into a “farmout” agreement with Samson Oil Co. (“Samson”) and Murfin Drilling Company (“Murfin”). Under the terms of the farmout, Samson and Murfin transferred their oil and gas lease rights to Rautena. Defendant then solicited investments from several people to drill a test well. Thereafter, defendant failed to drill the well, used the money for his personal expenses, and failed to disclose certain material facts to the investors before they decided to invest. This appeal follows defendant’s conviction for securities fraud, theft, and computer crime. Defendant contends the trial court erred in denying his motion to suppress evidence seized as a result of a search of his home conducted pursuant to a warrant. Where an affidavit includes information obtained unlawfully from a previous warrantless search, as well as information from lawful origins, evidence discovered by execution of the search warrant is admissible if the search pursuant to the warrant was supported by information from sources independent of the unlawfully procured information. After redacting the evidence obtained pursuant to the illegal search from the affidavit, the trial court concluded it was “eminently reasonable that a search of this apartment would have occurred and these items discovered.” Thus, the record supports the trial court’s conclusion that the later search and seizure were independent of the initial illegal entry. Defendant contends that the definitional instruction for a security impermissibly expanded the securities fraud charges alleged in the indictment. A simple variance occurs when the charged elements are unchanged, but the evidence presented at trial proves facts materially different from those alleged in the indictment. By adding other components of the statutory definition of “security” to the one listed in the indictment, the instruction did not change the elements of the offense, as the prosecution still had to prove defendant engaged in specified conduct in connection with a security. Thus, the difference between the indictment and the jury instructions was a simple variance, which did not prejudice defendant’s substantial rights. Defendant contends the evidence was insufficient to sustain his convictions for securities fraud. This was a question of fact for the jury, and reasonable jurors could find the agreement between defendant and the investors was a security. Defendant contends the trial court erroneously instructed the jury on the meaning of a security. The jury was given a definition of an investment contract, and was instructed to consider the totality of the circumstances in determining whether the venture was a security. This instruction was an adequate explanation of the law. Defendant contends the trial court erred in requiring the jury to find he acted willfully, instead of with specific intent. “Willfully” is the proper mental state for securities fraud. Defendant contends there was insufficient evidence to sustain his convictions for theft from an at-risk adult. As relevant here, an at-risk adult is any person who is 60 years of age or older. While the evidence was sufficient to support a reasonable inference that the trust and the corporation were victims of theft, it only shows these individuals served as conduits for the money between the corporation and trust and defendant. The judgment is reversed as to the two convictions of theft from an at-risk adult and the judgment is affirmed in all other respects. The case is remanded to the trial court to enter an order vacating the convictions and sentences for the two counts of theft from an at-risk adult.

COLORADO

Committee on State Regulation of Securities Page 22 Subcommittee on Liaisons to the States and NASD

b. No. 04CA2347. Salazar v. Clancy Systems International, Inc. Stock Certificates—Restrictive Legends—Tort Claims—Uniform Commercial Code—CRS § 4-8-401. Plaintiff appeals from the trial court’s summary judgment in favor of defendant Clancy Systems International, Inc. The judgment determined that plaintiff’s tort claims relating to restrictive legends on stock certificates were preempted by state statute. The judgment is reversed and the case is remanded for further proceedings.

Plaintiff alleged in his complaint that the value of his stock had depreciated by approximately $2 million between the time of his initial request for a stock certificate and the date the certificate was reissued without the restrictive legend. He asserted, as relevant here, tort claims of trespass to chattel and intentional interference with prospective advantage, alleging that defendant’s inclusion of the restrictive legend was wrongful and malicious and deprived him of his legal right to sell the stock. Defendant moved for summary judgment, asserting that plaintiff’s common law tort claims were preempted by the Uniform Commercial Code (“UCC”), specifically CRS § 4-8-401. The trial court granted summary judgment in favor of defendant. Plaintiff contends that the trial court erred in granting defendant’s motion for summary judgment and in concluding that plaintiff’s common law tort claims were preempted by the UCC, specifically CRS § 4-8-401. Common law tort remedies remain available unless a provision of the UCC clearly states otherwise.

Although CRS § 4-8-401(b) affords a remedy for a failure or refusal to register a transfer, this provision does not evince a clear intent by the General Assembly to occupy the entire field regarding the transfer of securities, particularly with respect to the placement or removal of restrictive legends. Thus, co-extensive remedies under this provision and under the common law may exist and CRS § 4-8-401 does not preempt common law claims or remedies relating to the placement and removal of restrictive legends. The summary judgment is reversed, and the case is remanded for further proceedings consistent with this opinion.

c. No. 04CA1794. People v. Hoover. Securities Fraud—Theft—Colorado Organized Crime Control Act (COCCA)—Evidence—Testimony—Hearsay—Relevance—Jury Instructions—Prosecutorial Misconduct—Lesser-Included Offenses—Sentence. Defendant Hoover appeals the judgment of conviction entered on jury verdicts finding him guilty of securities fraud, theft, and violating the Colorado Organized Crime Control Act (“COCCA”). He also appeals the sentences imposed. The judgment and sentence are affirmed. The evidence at trial showed that, over a period of several years, defendant defrauded dozens of investors and converted more than $15 million from them. After a two-week trial, a jury convicted defendant of 22 counts of securities fraud, 21 counts of theft, and one count of organized crime under COCCA. Defendant contends that his convictions for securities fraud must be reversed, because the trial court erred in prohibiting him from testifying about his attorney’s advice on hearsay grounds. However, defendant’s belief that the Bird Ventures debentures were not a security and his reasons as to why he filed for bankruptcy protection were irrelevant to the securities fraud prosecution. Additionally, defendant’s counsel did not make an offer of proof on the remaining objections and, therefore, failed to preserve the remaining issues for appeal. Defendant next contends that his securities fraud convictions should be reversed on the grounds that there was insufficient evidence to establish that the Agency Account was a security. Defendant did not object to the jury instructions, and there was sufficient evidence to support the jury’s finding that the Agency Account was a security. Defendant also contends that

COLORADO

Committee on State Regulation of Securities Page 23 Subcommittee on Liaisons to the States and NASD

his securities fraud convictions should be reversed because the prosecution committed misconduct during closing argument.

The record shows that the prosecution’s theory throughout the trial was that the Agency Account itself was a security, and this theory was consistent with the indictment and with those portions of defendant’s testimony used by the prosecution in closing argument. The prosecution’s comments were not an unfair characterization of defendant’s testimony and the legal inferences drawn by the prosecution were proper. Defendant contends that the trial court incorrectly answered a jury question and that his theft convictions therefore should be reversed. However, because defendant actively participated in preparing the response to the jury’s question and expressly agreed to it, defendant cannot now complain that the response was improper. Defendant contends that securities fraud and theft are lesser-included offenses of COCCA and that he should not have been convicted for both.

However, the General Assembly clearly authorized separate punishments for COCCA and the underlying predicate offenses of theft and securities fraud. Defendant contends that the trial court abused its sentencing discretion by imposing a total prison sentence of 100 years. A review of the record shows that the sentencing court engaged in a careful analysis of the pertinent factors, arrived at a sentence that was consistent with the purposes of the Criminal Code with respect to sentencing, and articulated on the record its basic reasons for imposing the sentence. Therefore, there was no abuse of discretion in the sentences imposed by the trial court.

III. Developments Relating to NSMIA: On April 30, 1998, Governor Romer signed into law House Bill 98-1244, a bill for the regulation of investment advisory activities. Under the law, the Colorado Securities Commissioner and Securities Division license and regulate state-based investment advisers and investment adviser representatives who work in Colorado, effective January 1, 1999.

The “Colorado Investment Adviser” law was enacted in the context of NSMIA, under which Congress split regulatory responsibility for investment advisers between the Securities and Exchange Commission and state securities regulators. Investment Advisor firms with more than $25 million in assets under management are regulated exclusively by the SEC. Colorado regulates Investment Adviser firms located in Colorado with assets under that threshold. Investment adviser representatives, individuals with a place of business in Colorado who work for Federal Covered Advisors or state Investment Adviser Firms in providing investment advice to customers, need a Colorado Investment Adviser Representative license.

To be licensed in Colorado, the filing of Investment Adviser and Investment Adviser Representative license applications and fees is required. Colorado Investment Adviser Representative license applicants are required to take and pass a minimum competency examination or provide proof of alternate qualifications. Annual fees will be required each year. Licensees are subject to inspection, dishonest and unethical business practice rules, customer disclosure requirements and anti-fraud provisions.

A Federal Covered Advisor with a place of business in Colorado, or who employs or otherwise engages an individual with a place of business in this state to act as an Investment Adviser Representative, is required to make a notice filing.

COLORADO

Committee on State Regulation of Securities Page 24 Subcommittee on Liaisons to the States and NASD

IV. Significant Development in the Division’s Enforcement of Regulation Activities: Since the June 2006 Update, there have been 5 press releases dealing with the Division’s enforcement activities: a. Press Release: Aurora Man Sentenced in Stock Scam. In a press release dated July 13, 2006, Arapahoe County District Attorney Carol Chambers and Colorado Securities Commissioner Fred J. Joseph, announced that Aurora resident Elvin Vern Jones, 73 years old, was sentenced in Arapahoe District Court for defrauding a Colorado investor of $114,000. Following Jones’ entry of a plea of guilty to the crimes of attempted securities fraud and theft, Arapahoe County District Court Judge Angela Arkin sentenced Jones to 10 years of probation and, citing Jones’ lack of remorse, imposed a 40-day jail sentence. Judge Arkin also ordered Jones, despite his age, to obtain employment in order to pay back the $114,000 that he admitted to taking as part of his investment scam. Following a joint investigation by the Aurora Police Department and the Colorado Division of Securities, Jones was charged with two counts of securities fraud, both class three felonies, and two counts of theft, class four felonies, in connection with the sale of securities. Jones met prospective investors at a local church and induced at least one investor to invest in his non-existent company, Optimum International, Inc. Jones promised that, in seven days, he would triple the amount of any investment in an international investment program. Jones diverted significant portions of the funds for his own personal use. This case was prosecuted jointly by the Arapahoe County District Attorney’s Office and the Colorado Attorney General’s Office. Commissioner Joseph said, “This conviction was the result of different Colorado agencies working together to obtain a result that will enhance investor protection here in Colorado. We especially want to thank the Aurora Police Department, the Arapahoe County District Attorney’s office, and the Colorado Attorney General’s Office, whose contributions to this case all made this conviction happen.”

b. Press Release: Colorado Man Indicted and Arrested for Stock Scam. In a press release dated September 11, 2006, Colorado Attorney General John W. Suthers and Colorado Securities Commissioner Fred J. Joseph, announced the arrest of Mark Steven Blakemore of Erie, Colorado (DOB: 11/20/56), for his alleged participation in a securities scam in the Boulder-Denver area. Blakemore was arrested on a warrant issued by the Denver District Court following the return of an indictment by the Colorado State Grand Jury on September 8, 2006. Blakemore was indicted on 17 counts of securities fraud and six counts of theft in connection with the sale of securities in Colorado, all class three felonies.

It is alleged that Blakemore sold phony investments, through his company, Great Plains Financial, LLC, to at least 38 investors totaling over $3.2 million. It is alleged that Blakemore represented to investors that his company, Great Plains Financial, sold “short-term corporate debentures” which paid investors an exceedingly high rate of return. Blakemore allegedly represented to investors that he had a confidential trading relationship with a major bank ranked in the top 25 worldwide which generated substantial profits when no such relationship existed. It is further alleged that Blakemore either sent the investors moneys to Michael W. Conley of Shawnee, Kansas, and his company, Konza Financial, who paid Blakemore significant commissions, or was kept for Blakemore’s own personal use. In March 2006, Michael W. Conley entered a plea agreement with the U.S. Attorney for the Eastern District of Virginia for his role in a scheme to defraud investors through his company, Konza Financial. Conley, in his plea agreement, waived being indicted in exchange for a plea of guilty to one count of mail fraud. Conley was sentenced to seven years in federal prison on his plea of guilty. Blakemore

COLORADO

Committee on State Regulation of Securities Page 25 Subcommittee on Liaisons to the States and NASD

was arrested on September 8, 2006, and posted bond in the amount of $50,000. “Mr. Blakemore is accused of targeting teachers, convincing them to turn over their hard-earned money to a non-existent investment scheme,” said Attorney General Suthers. “This case is just another example of the successful partnership between our office and the Division of Securities.” Commissioner Joseph said, “The investment scheme promoted by Mr. Blakemore appears to be a variation of the ‘prime bank note’ schemes that have been circulating for years. This type of scheme continues to make regulator’s top ten list of investor’s traps.” Commissioner Joseph cautions investors to check out any investment opportunity, especially those promising high rates of return. (Note: Any indictment is merely an accusation and any defendant is presumed innocent until and unless proven guilty in a court of law.)

c. Press Release: Denver Man Sentenced to 48 Years for Financial Fraud. In a press release dated October 19, 2006, Attorney General John Suthers and Securities Commissioner Fred Joseph announced today that Raymond Paul Morris, 49, of Castle Rock, Colorado, was sentenced in Douglas County District Court yesterday to 48 years in the Department of Corrections after pleading guilty to four counts of securities fraud and one count of theft, all Class three felonies. Morris was also ordered to pay $2 million in restitution to his victims. Morris was indicted by the Colorado State Grand Jury in November 2005. “This case should be a lesson for both criminals and investors,” said Suthers. “Criminals are on notice that we take these crimes very seriously and will seek long jail sentences for such scams. Potential investors are cautioned that they must do their homework before investing.” Suthers further added, “I want to commend the Douglas County Sheriff’s Office for their diligent work on this case over the past several years.” Commissioner Joseph said, “The judge’s sentence in this case sends a clear message to all would-be con-artists. Colorado is a bad place to cheat investors. Don’t do it here because you will be caught, prosecuted and sent to jail for a long time.” According to the indictment, Morris employed several schemes to defraud his investors. Among those schemes, Morris promised lots in a parcel of land he did not yet own in an area he claimed to be developing for residential use, known as “Cherry Valley Land Development.” Morris failed to develop the land and investors never received title to the property for which they paid. Another alleged scheme Morris used to defraud investors was convincing them to lend money to third parties, offering promissory notes secured with forged deeds of trust to the third parties’ homes. However, the third parties were never involved in the transaction and never received any of the money. Morris also solicited and accepted investor money to trade in the foreign currency market promising substantial returns, but failed to disclose poor performance on prior returns. Morris further failed to inform the investors that some of the money would be used for personal purposes.

d. Press Release: 20 Year Prison Sentence for Defrauding Seniors. In a press release dated October 19, 2006, District Attorney Scott Storey and Securities Commissioner Fred Joseph announced that Andrew Paul Weis (DOB: 10/27/50), of Lakewood, was sentenced to 20 years in prison, plus five years mandatory parole, for securities fraud. He defrauded at least 25 people, most being older adults, out of almost $600,000. Weis operated under the business names of Total Financial Management, Total Financial Group, Total Financial Fund and Total Financial in Lakewood, Colorado. Between 1999 and December 2002, Weis held himself and his business out to the public as a safe way for people to invest their retirement savings. He solicited money,

COLORADO

Committee on State Regulation of Securities Page 26 Subcommittee on Liaisons to the States and NASD

primarily in Colorado and New Mexico, and often through presentations at retirement and senior centers. Mr. Weis failed to invest this money as he indicated he would and, instead, used the money to pay his personal living expenses, supporting his $200,000 a year lifestyle. In a Ponzi-like fashion, some money was used to pay other investors a dividend so that they would think that their money was actually invested. Mr. Weis failed to tell investors that he was not licensed or authorized to transact business as a securities broker-dealer or sales representative. Many of the victims were “at risk” adults and two of the victims passed away during the course of the case.

District Attorney Storey was pleased with the sentence, saying, “As strong a message as this sentence will send to criminals, it also reinforces my commitment to continuing to educate our senior citizens about fraud and their finances through our Communities Against Senior Exploitation (“CASE”) program. Seniors need to be very cautious and seek second or third opinions before moving their retirement savings and consult with friends or family about these decisions.” At sentencing, Weis proposed a payment plan to the court that would include him being on probation, finding a job and paying $2000 a month to victims. Chief Judge Brooke Jackson found the proposed plan to be unacceptable given the amount of money stolen, the length of time it would take to pay victims in full at this rate, the speculative nature of the job prospect, and the nature of the defendant’s conduct and harm he had caused. Weis pled guilty on August 17 to two counts of Securities Fraud and one count of Theft of an At-Risk Adult, all class three felonies. Commissioner Joseph said, “Weis used ‘free lunch’ seminars to dupe investors, mainly seniors, into turning over their retirement savings to him.” Commissioner Joseph cautioned investors to do their homework before investing. “The length of the judge’s sentence puts con-artists on notice that ripping off investors, particularly seniors, carries severe consequences,” added Joseph.

e: Press Release. Klytie’s Developments, Hidai Friedman, Efrat Friedman, and Jason Sharkey Enjoined on Charges of Securities Law Violations—Canadian Company and Three Principals Alleged To Have Violated Law by Colorado Securities Commissioner. In a press release dated October 24, 2006, Colorado Securities Commissioner Fred J. Joseph announced that he has filed a complaint in Denver District Court and obtained a temporary restraining order against two entities and three individuals alleging that they are violating the anti-fraud provisions and securities registration provisions of the Colorado Securities Act (“the Act”). Named in the complaint, which was filed on October 23, 2006, and subject of the temporary restraining order, are Klytie’s Developments, Inc., Hidai Friedman, and Efrat Friedman, all of Calgary, Alberta, and Klytie’s Developments, LLC, and Jason Sharkey, all of Colorado. In the complaint, the Commissioner has alleged that since at least March 2005, the Defendants have offered and sold investments in the so-called “Global Real Estate Fund.”

Defendants represented to investors that they would pool investor moneys to finance the purchase of real estate developments and holdings throughout the world. In turn, those real estate developments would form the assets of the Global Real Estate Fund and the investors would share in the profits and capital gains derived from the assets of the Fund. The Defendants guaranteed a minimum annual return of 10% to investors. In the complaint, the Commissioner has alleged that in connection with the offer and sale of interests in the Global Real Estate Fund, Defendants made misrepresentations to prospective investors which are materially false and misleading, including, but not limited to the following: (i) Defendants represented to investors that Klytie’s Developments owned the properties listed in

COLORADO

Committee on State Regulation of Securities Page 27 Subcommittee on Liaisons to the States and NASD

the Klytie’s Prospectus. In truth, some of the properties identified in the Prospectus do not even exist. (ii) Defendants represented to investors that investor’s funds would be pooled to purchase real estate. But investor funds were used for purposes other than the purchase of real estate, including the personal use by the Defendants. (iii) Defendants represented that the properties were held in trust by TD Canada Trust. But TD Canada Trust has no record of any trust documents filed with them by the Defendants.

The Division of Securities is currently aware of at least 50 investors who have invested over $2.25 million with Klytie’s Developments. Investments in Klytie’s may exceed $7 million. On October 23, 2006, at the request of the Commissioner, Denver District Court Judge Joseph Meyer issued a Temporary Restraining Order against the defendants in the matter. In the Order, Judge Meyer prohibited the defendants from offering or selling unregistered securities in Colorado and violating the anti-fraud provisions of the Colorado Securities Act. The Judge’s Order also froze various bank accounts maintained by the Defendants. In a related action, on October 4, 2006, the Alberta Securities Commission obtained an Interim Cease Trade Order against Klytie’s and the Friedman’s for violations of the Alberta securities laws. Both the U.S. Securities and Exchange Commission and the Alberta Securities Commission assisted in the investigation of this case. The Commissioner is represented in the action by attorneys from the office of State Attorney General John Suthers.

V. New Developments in Corporation, Partnership and Association Law: The Second Regular Session of the Sixty-Fifth General Assembly convened on January 11, 2006 and adjourned on May 10, 2006, and the First Extraordinary Session convened on July 6, 2006 and adjourned on July 10, 2006. Since the June 2006 Update, the following bills relating to Colorado general corporate law were passed by the Colorado General Assembly: a. Senate Bill No. 06-187: Concerning Title 7 of the Colorado Revised Statutes. This bill Standardizes rights of creditors, owners, and the entity with respect to dissolved business entities. The bill clarifies the rights of creditors of a corporation or nonprofit corporation and standardizes rules for unlawful distributions for a limited liability partnership, a limited liability limited partnership, and a limited liability company.

This bill amends the corporation and association laws by: (i) adding a definition of a “mutual ditch company” to the “Colorado Revised Nonprofit Corporation Act”, (ii) clarifying trade name laws as such laws pertain to delinquent or dissolved entities; (iii) modifying the definition, contents and operation of an operating agreement of a limited liability company; (iv) clarifying the duties that a party to an operating agreement has to a limited liability company or to another member, manager, or other person that is a party to the operating agreement; (v) clarifying the role of managers and members of a limited liability company, including agency authority; (vi) modifying the voting requirements with respect to mergers and conversions; (vii) clarifying the liabilities of directors and officers of a nonprofit corporation that dissolves but continues to operate without winding up; and (viii) clarifying when a delayed effective date shall not be used when a document is delivered to the Secretary of State for filing. This bill expands the authority of the Secretary of State to propound interrogatories to a domestic entity that has a constituent-filed document in the records of the Secretary of State, and a foreign entity that is authorized to transact business or conduct activities in Colorado. This bill sets deadlines by which an entity shall respond to the interrogatories and increases the penalties for failure to respond to interrogatories. This bill makes provisions relating to trade names effective

COLORADO

Committee on State Regulation of Securities Page 28 Subcommittee on Liaisons to the States and NASD

May 30, 2006. Portions of the bill became effective May 30, 2006 and portions effective July 1, 2006.

b. Senate Bill No.06-188: Concerning the Central Filing of an Effective Financing Statement. This bill clarifies the required elements to be included in an effective financing statement and clarifies the requirements for amending an effective financing statement. This bill requires that effective financing statements be on or in a medium as may be acceptable to the central filing officer and establishes filing requirements for effective financing statements. This bill allows the central filing officer to prepare, furnish and require the use of specific forms when filing an effective financing statement and to charge fees for filing and other services. This bill requires the central filing officer to publish and distribute a master list of effective financing statements electronically. This bill provides that the act is effective 90 days following certification in writing by the Secretary of State to the Revisor of Statutes that approval of changes to the central filing system enacted in the act has been obtained from the U.S. Department of Agriculture, and the Secretary of State has implemented the necessary computer system to publish and distribute the master list electronically and is able to do so. This bill became effective May 25, 2006.

c. House Bill No. 06-1042: Concerning the Repeal of Certain Provisions of the “Bank Electronic Funds Act.” This bill repeals certain provisions of the “Bank Electronic Funds Act,” except for provisions pertaining to consumer protection. This bill became effective August 7, 2006.

d. House Bill No.06-1119: Concerning Security Breaches Regarding Personal Identifying Information. This bill on and after September 1, 2006, requires an individual or a commercial entity that conducts business in Colorado and that owns or licenses computerized data that includes personal information about a resident of Colorado to, when it becomes aware of a breach of the security of the system, conduct in good faith a prompt investigation to determine the likelihood that the personal information has been or will be misused.

This bill requires the individual or the commercial entity to give notice as soon as possible to the affected Colorado resident, unless the investigation determines that the misuse of information about a Colorado resident has not occurred and is not reasonably likely to occur. This bill requires notice to be made in good faith, in the most expedient time possible and without unreasonable delay, consistent with the legitimate needs of law enforcement and with any measures necessary to determine the scope of the breach and to restore the reasonable integrity of the computerized data system. This bill requires the notification to be either written or electronic, unless the cost of the notice exceeds $250,000, the affected class exceeds 250,000 people, or there is insufficient contact information, in which case conspicuous Internet posting and notification to statewide media suffices.

This bill provides if an individual or commercial entity is required to notify more than 1,000 Colorado residents of a breach of the security of the system, requires the individual or commercial entity to also notify, without unreasonable delay, all consumer reporting agencies that compile and maintain files on consumers on a nationwide basis of the anticipated date of the notification to the residents and the approximate number of residents who are to be notified. The bill allows the attorney general to file suit to enforce the act and became effective September 1, 2006.

COLORADO

Committee on State Regulation of Securities Page 29 Subcommittee on Liaisons to the States and NASD

e. House Bill No.06-1140: Concerning the Registration of Trademarks. This bill repeals and reenacts the Colorado trademark laws. The bill establishes requirements and filing procedures for statements of trademark registration, as well as statements regarding the renewal, transfer or withdrawal of trademark registration.

The bill requires an individual or entity filing a statement of trademark registration to certify that such registrant believes the registrant has the right to use the trademark in connection with the goods and services identified in the filing; that the registrant is currently using the trademark; and that the registrant’s use of the trademark does not infringe the rights of any other person in that trademark. This bill requires that the filing be accompanied by a specimen demonstrating its use. This bill states that filing a statement of trademark registration does not confer substantive rights to the registrant or entitle the registrant to remedies not available at common law. This bill defines the period during which a statement of trademark registration is effective and the dates during which the Secretary of State may notify the registrant of an impending trademark expiration.

This bill establishes procedures for the cancellation of a statement of trademark registration and establishes procedures for service of process on a registrant. This bill makes an existing statement of trademark registration valid until its expiration under current law. This bill is effective May 29, 2007.

f. House Bill No.06-1156: Concerning Increased Consumer Rights Regarding the Use of Social Security Numbers. This bill prohibits any person or entity from: (i) publicly posting or displaying in any manner an individual’s social security number (“SSN”); (ii) printing an individual’s SSN on a card required for the individual to access products or services provided by the person or entity; (iii) requiring an individual to transmit his or her SSN over the Internet, unless the connection is secure or the SSN is encrypted; (iv) requiring an individual to use his or her SSN to access an Internet Web site, unless a password or unique personal identification number or other authentication device is also required to access the Internet Web site; and (v) printing an individual’s SSN on any materials that are mailed to the individual, unless state or federal law requires, permits or authorizes the SSN to be on the document to be mailed.

This bill lists exceptions, including uses required, permitted or authorized by state or federal law. This bill allows a preexisting nonconforming use of a SSN to continue if each of the following conditions is met: (A) the use of the SSN is continuous; and (B) the person or entity provides the individual with an annual disclosure that informs the individual that he or she has the right to stop the nonconforming use of his or her SSN. This bill requires the person or entity to implement a written request by an individual to stop the nonconforming use within 30 days after the receipt of the request. This bill prohibits the person or entity from denying services to an individual because the individual makes such a written request. This bill includes a SSN in financial data that may not be inspected as part of a public record, unless disclosure is required, permitted or authorized by state or federal law. This bill became effective January 1, 2007.

g. House Bill No.06-1247: Concerning the Adoption of Changes to the “Uniform Commercial Code” Proposed by the National Conference of Commissioners on Uniform State Laws and, in Connection Therewith, Repealing and Reenacting Articles 1 and 7 of the “Uniform Commercial Code.” This bill repeals and reenacts Articles 1, regarding general provisions, and 7, regarding documents of title, of the “Uniform Commercial Code” (“UCC”) as proposed by the

COLORADO

Committee on State Regulation of Securities Page 30 Subcommittee on Liaisons to the States and NASD