StartUp Health Insights Funding Report 2016 Year End

33

© 2017 StartUp Health, LLC A StartUp Health Insights Report 2016 Digital Health Funding Rankings Data from January 1, 2016 through December 31, 2016 Report is inclusive of seed, venture, corporate venture and private equity funding Sign up to receive weekly funding insights at startuphealth.com INCLUDING CAREGIVING FUNDING SPONSORED BY INCLUDING TOP MARKET FUNDING SPONSORED BY 2016: THE HEALTH MOONSHOT MOVEMENT TM

-

Upload

startup-health -

Category

Healthcare

-

view

6.844 -

download

0

Transcript of StartUp Health Insights Funding Report 2016 Year End

© 2017 StartUp Health, LLC

A StartUp Health Insights Report 2016 Digital Health Funding Rankings

Data from January 1, 2016 through December 31, 2016 Report is inclusive of seed, venture, corporate venture and private equity funding Sign up to receive weekly funding insights at startuphealth.com

INCLUDING CAREGIVING FUNDING SPONSORED BY

INCLUDING TOP MARKET FUNDING SPONSORED BY

2016: THE HEALTH MOONSHOT MOVEMENT

TM

startuphealth.com/reports

ABOUT STARTUP HEALTH

Pages Topic

2-3 ………………………………………….…………… About StartUp Health

4 ………………………………………….…………… Year End Summary

5-18 ………………………………………….…………… Deals and Funding

19-20 ………………………………………….…………… Geography

21-23 ………………………………………….…………… Investors

24-25 ………………………………………….…………… Outlook

26-30 ………………………………………….…………… Caregiving

26 ………………………………………….…………… Methodology

In 2011, StartUp Health introduced a new model for transforming health by organizing and supporting a global army of entrepreneurs called Health Transformers. With the world’s largest digital health portfolio (more than 180 companies spanning 5 continents, 16 countries and 60+ cities), StartUp Health is mobilizing this rapidly growing army along with the world’s ‘batteries included’ leaders, innovators and investors, to achieve 10 Health Moonshots, with a 25 year mission to improve the health and wellbeing of everyone in the world.

Learn more about how you can join this movement and support Health Transformers at www.startuphealth.com.

Jennifer Hankin

Polina Hanin

Troy Bannister

Mark Liber

Anne Dordai

Nicole Kinsey

Tara Salamone

StartUp Health InsightsTM Contributors

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

Ali McDonough

Niharika Gupta

Rami Tal

2

startuphealth.com/reports

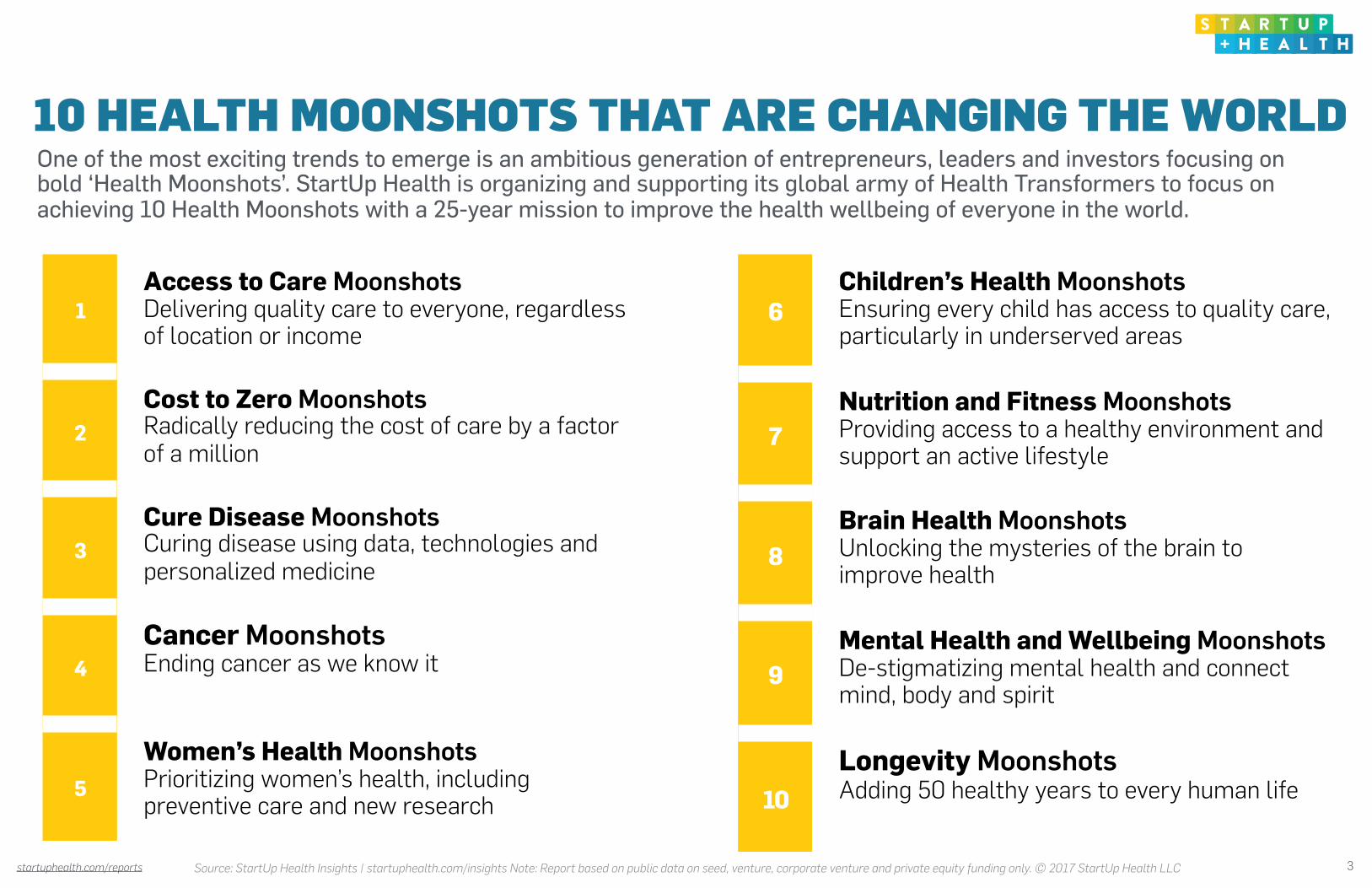

1Access to Care Moonshots Delivering quality care to everyone, regardless of location or income

2Cost to Zero Moonshots Radically reducing the cost of care by a factor of a million

3Cure Disease Moonshots Curing disease using data, technologies and personalized medicine

4Cancer Moonshots Ending cancer as we know it

5

Women’s Health Moonshots Prioritizing women’s health, including preventive care and new research

6Children’s Health Moonshots Ensuring every child has access to quality care, particularly in underserved areas

7Nutrition and Fitness Moonshots Providing access to a healthy environment and support an active lifestyle

8Brain Health Moonshots Unlocking the mysteries of the brain to improve health

9Mental Health and Wellbeing Moonshots De-stigmatizing mental health and connect mind, body and spirit

10Longevity Moonshots Adding 50 healthy years to every human life

10 HEALTH MOONSHOTS THAT ARE CHANGING THE WORLDOne of the most exciting trends to emerge is an ambitious generation of entrepreneurs, leaders and investors focusing on bold ‘Health Moonshots’. StartUp Health is organizing and supporting its global army of Health Transformers to focus on achieving 10 Health Moonshots with a 25-year mission to improve the health wellbeing of everyone in the world.

3Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING GEOGRAPHY INVESTORS OUTLOOK

“The urgency is now, it’s

about changing the culture, it’s about coming up with a new

strategy.”

-Vice President Joe Biden, at StartUp Health’s Showcase at The Cleveland Clinic Medical

Innovation Summit 2016

2016 YEAR END SUMMARY2016 was the beginning of the health sector’s ‘Moonshot Movement’. Thousands of entrepreneurs, industry leaders and investors, coupled with a generation of new industry entrants started to rethink the future of health. From Vice President Joe Biden’s Cancer Moonshot to speed up the progress in ending cancer as we know it, to The Chan Zuckerberg Initiative to cure all disease within 100 years, billions of dollars are being committed to health innovation - a mindset that exponential progress is possible.

4

Over $8 Billion were invested in over 500 digital health companies alone. This staggering figure has fueled innovation across the board in medicine, infrastructure and consumer-driven health.

Record-Breaking Digital Health Funding:

1

New Investors Pour In:More than 200 new investors entered the funding ecosystem in 2016, putting the total unique investors at almost 900. These investors come from a variety of institutions and geographies, beyond the traditional VC and angel investor, ranging from Fortune 500 to Private Equity.

2

Investors continue to support early-stage startups with hundreds of Seed and Series A Rounds this year.

Investors Support Early Stage Innovation: 3

Big deals dominated 2016 with almost 25% of all funding invested into five deals. It’s no coincidence that companies receiving large amounts of capital like Onduo or Human Longevity Inc. are examples of companies with bold visions, setting out to achieve Moonshots.

A Year of Mega Deals:

4

Almost 160 patient/consumer experience focused companies received funding in 2016 - between 2-3x as many as other subsectors. Patient engagement and behavior change remain largely unsolved problems and while these early stage companies continue to experiment, we look forward to new models and strategies emerging that incorporate lessons learned.

Delivering Care & Content Receives Most Funding:

5

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

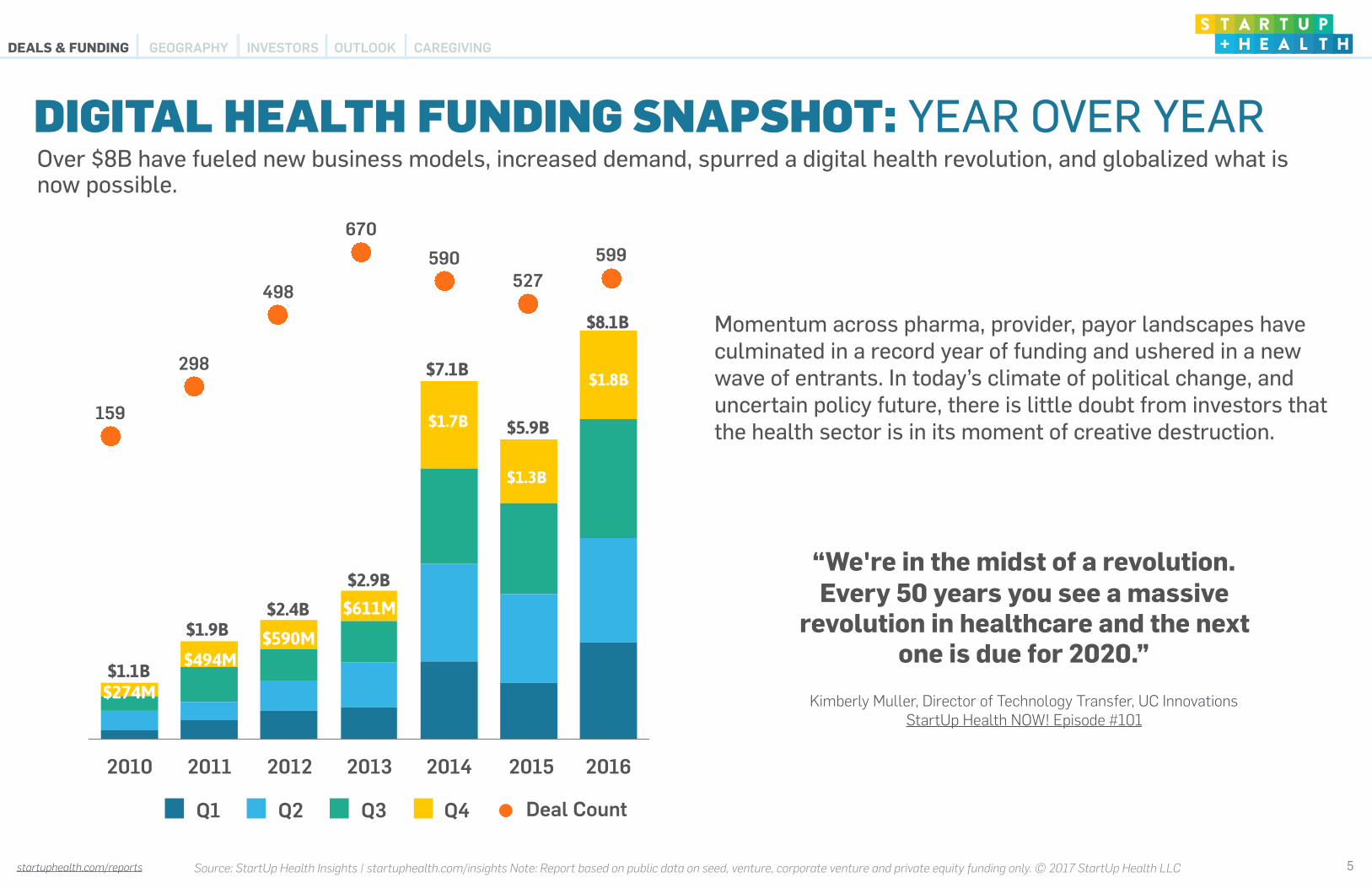

2010 2011 2012 2013 2014 2015 2016

Q1 Q2 Q3 Q4

DEALS & FUNDING GEOGRAPHY INVESTORS OUTLOOK

159

298

498

670

590527

599

Deal Count

$1.3B

$1.8B

$1.7B

$611M

$590M$494M

$274M

$8.1B

$5.9B

$7.1B

$2.9B

$2.4B$1.9B

$1.1B

Momentum across pharma, provider, payor landscapes have culminated in a record year of funding and ushered in a new wave of entrants. In today’s climate of political change, and uncertain policy future, there is little doubt from investors that the health sector is in its moment of creative destruction.

DIGITAL HEALTH FUNDING SNAPSHOT: YEAR OVER YEAR

5

“We're in the midst of a revolution. Every 50 years you see a massive

revolution in healthcare and the next one is due for 2020.”

Kimberly Muller, Director of Technology Transfer, UC Innovations StartUp Health NOW! Episode #101

Over $8B have fueled new business models, increased demand, spurred a digital health revolution, and globalized what is now possible.

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

$0B

$0.2B

$0.4B

$0.6B

$0.8B

$1B

$1.2B

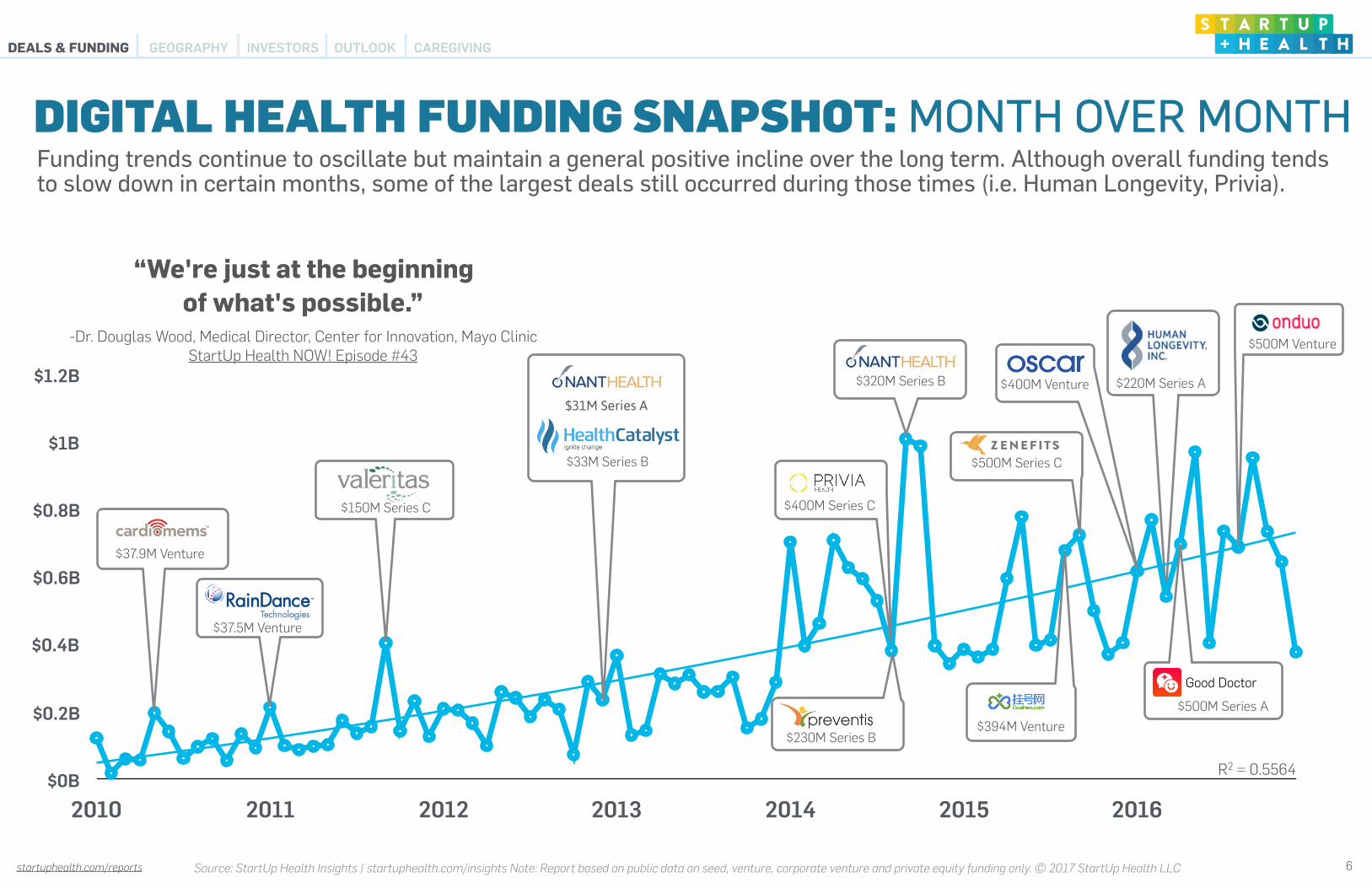

2010 2011 2012 2013 2014 2015 2016

$320M Series B

$150M Series C

$37.5M Venture

$37.9M Venture

$394M Venture

$33M Series B

$31M Series A

$400M Series C

$230M Series B

$500M Series C

R2 = 0.5564

$400M Venture $220M Series A

Good Doctor

$500M Venture

DIGITAL HEALTH FUNDING SNAPSHOT: MONTH OVER MONTH

GEOGRAPHY INVESTORS

6

Funding trends continue to oscillate but maintain a general positive incline over the long term. Although overall funding tends to slow down in certain months, some of the largest deals still occurred during those times (i.e. Human Longevity, Privia).

$500M Series A

“We're just at the beginning of what's possible.”

-Dr. Douglas Wood, Medical Director, Center for Innovation, Mayo Clinic StartUp Health NOW! Episode #43

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

$0B

$0.2B

$0.4B

$0.6B

$0.8B

$1B

$1.2B

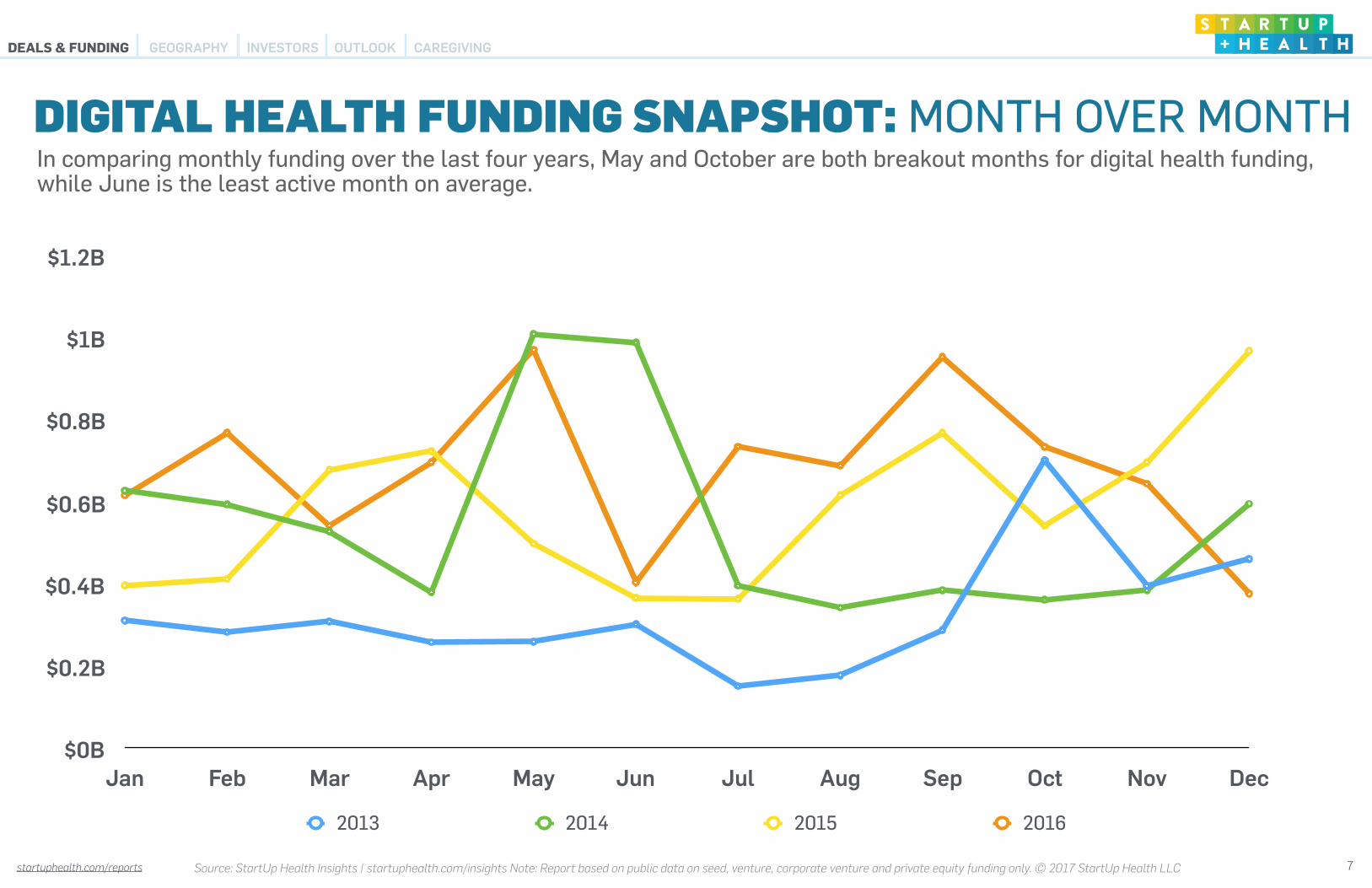

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014 2015 2016

In comparing monthly funding over the last four years, May and October are both breakout months for digital health funding, while June is the least active month on average.

DIGITAL HEALTH FUNDING SNAPSHOT: MONTH OVER MONTH

GEOGRAPHY INVESTORS

7

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

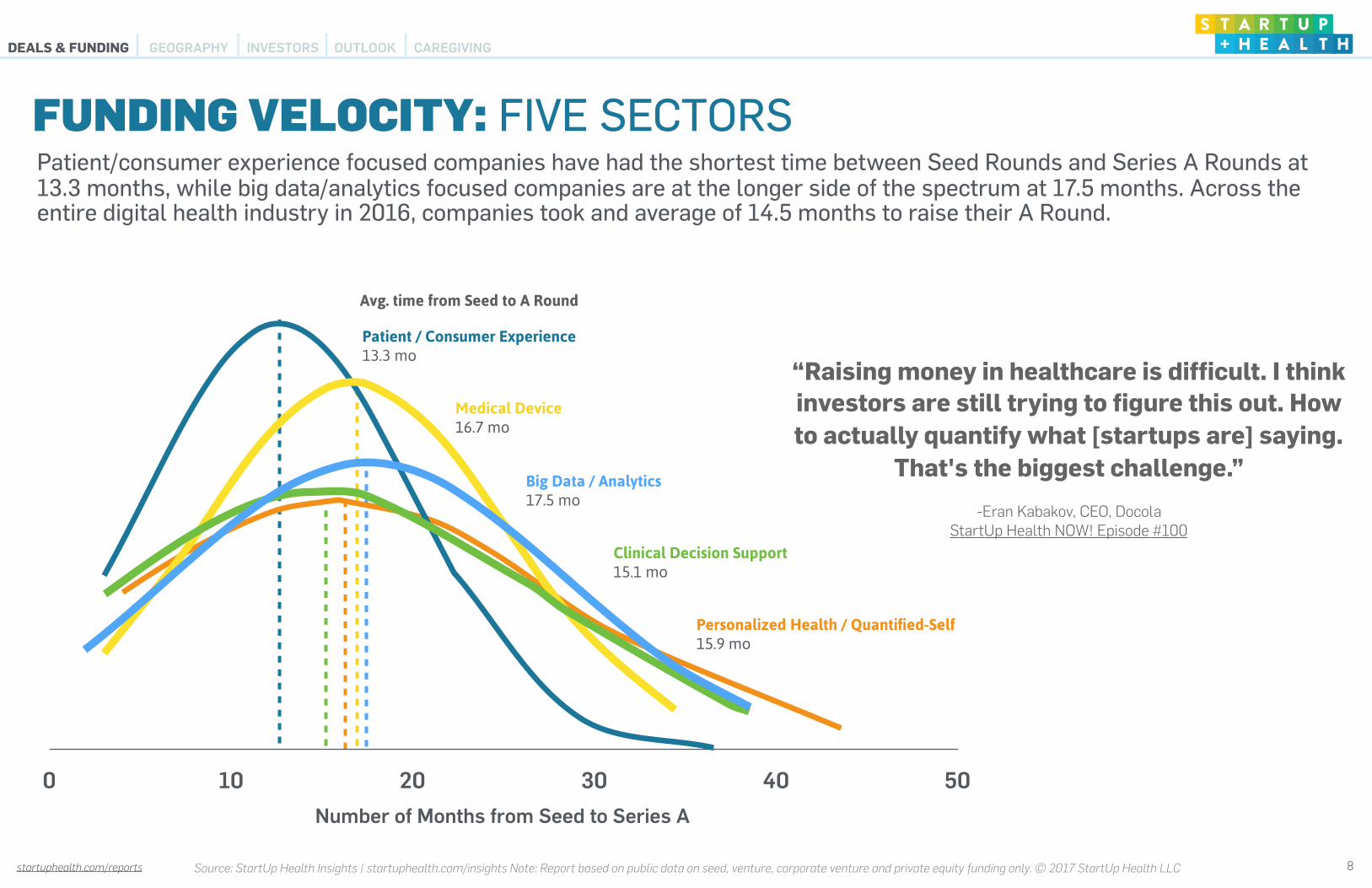

Patient/consumer experience focused companies have had the shortest time between Seed Rounds and Series A Rounds at 13.3 months, while big data/analytics focused companies are at the longer side of the spectrum at 17.5 months. Across the entire digital health industry in 2016, companies took and average of 14.5 months to raise their A Round.

Number of Months from Seed to Series A

Big Data / Analytics 17.5 mo

Medical Device 16.7 mo

Clinical Decision Support 15.1 mo

Avg. time from Seed to A Round

Patient / Consumer Experience 13.3 mo

Personalized Health / Quantified-Self 15.9 mo

FUNDING VELOCITY: FIVE SECTORS

GEOGRAPHY INVESTORS

“Raising money in healthcare is difficult. I think investors are still trying to figure this out. How to actually quantify what [startups are] saying.

That's the biggest challenge.”

-Eran Kabakov, CEO, Docola StartUp Health NOW! Episode #100

8

0 10 20 30 40 50

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

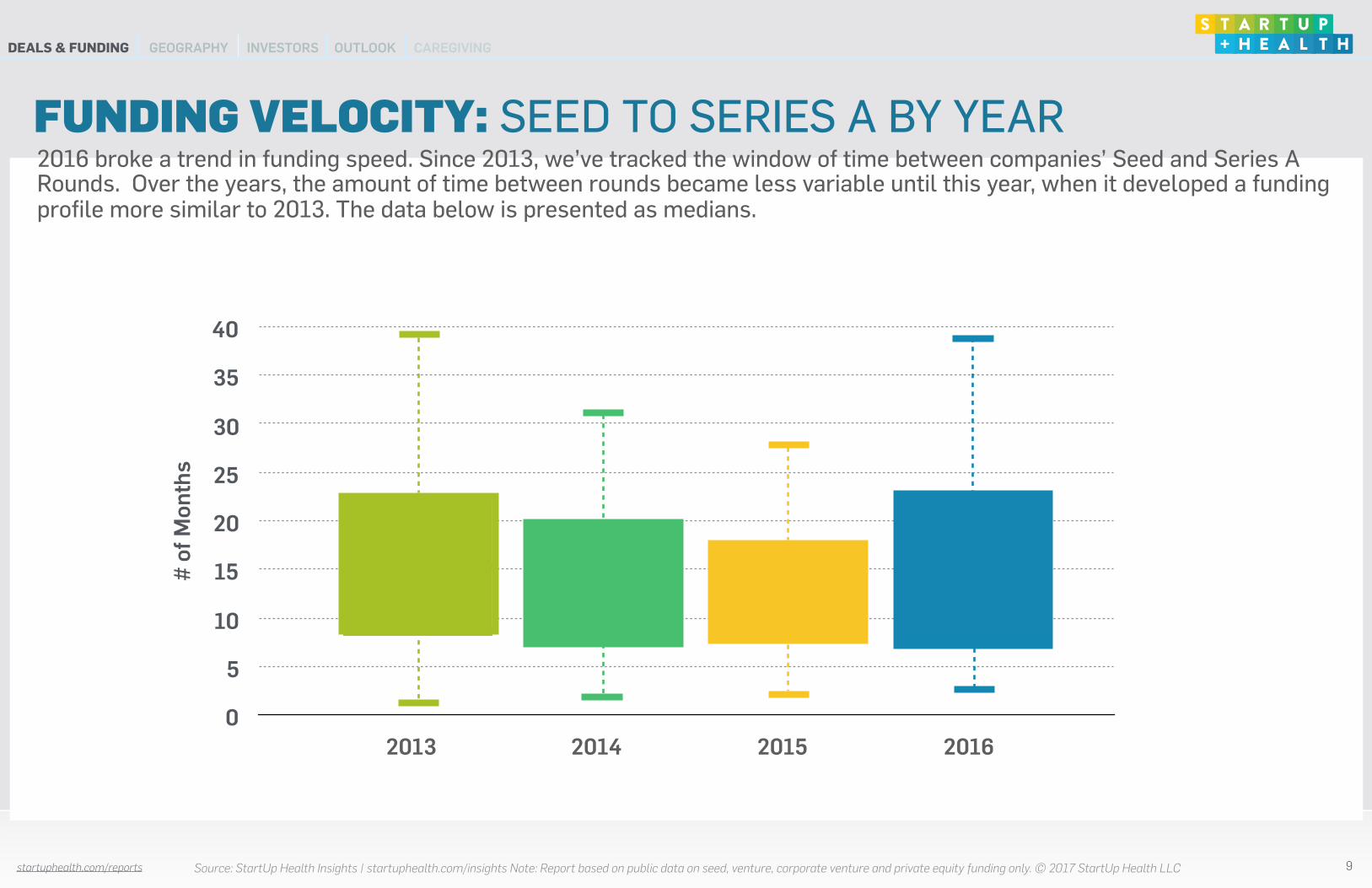

2016 broke a trend in funding speed. Since 2013, we’ve tracked the window of time between companies’ Seed and Series A Rounds. Over the years, the amount of time between rounds became less variable until this year, when it developed a funding profile more similar to 2013. The data below is presented as medians.

# of

Mon

ths

0

5

10

15

20

25

30

35

40

2013 2014 2015 2016

FUNDING VELOCITY: SEED TO SERIES A BY YEAR

GEOGRAPHY INVESTORS

9

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

Company $ Invested Subsector Notable Investor

1 $500M Patient/Consumer Experience

1 $500M Patient/Consumer Experience Undisclosed

3 $448M Patient/Consumer Experience

4 $400M Wellness

5 $220M Personalized Health

6 $160M Wellness

7 $151M Patient/Consumer Experience

8 $145M Big Data/Analytics

9 $120M Patient/Consumer Experience

10 $100M Medical Device Undisclosed

10 $100M Medical Device

10 $100M Personalized Health

DEALS & FUNDING OUTLOOK

THE TOP 10 LARGEST DEALS OF 2016

GEOGRAPHY INVESTORS

10

Three of the top five deals in record were signed this year, demonstrating international commitment to supporting paradigm shifting ideas in digital health.

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

Company Location Subsector Notable Investor

Palo Alto, CA Patient/Consumer Experience

Dallas, TX Population Health

Agoura Hills, CA Patient/Consumer Experience

Palo Alto, CA Research

Stockholm, Sweden Wellness

San Mateo, CA Big Data/Analytics

Sacramento, CA Big Data/Analytics

Toronto, ON Wellness

Montreal, QC Personalized Health/Quantified-Self

New York, NY Big Data/Analytics

Hong Kong Personalized Health/Quantified-Self

Chicago, IL Workflow

Boston, MA Patient/Consumer Experience

Chicago, IL Workflow

New York, NY Wellness

CROSS SECTION: $10M DEALS

GEOGRAPHY INVESTORS

11

Taking a look at a group of $10M deals, we can see a variety of companies that have managed to attract mid-level investments over the course of the last year.

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

Company Location Subsector Notable Investor

Singapore Population Health

Denver, CO Patient/Consumer Experience

Dallas, TX Patient/Consumer Experience

Tel Aviv, Israel Big Data/Analytics

Chicago, IL Education/Training

Flo Wilmington, DE Personalized Health/Quantified Self

Los Angeles, CA Wellness

Seattle, WA Research

Helsinki, Finland Patient/Consumer Experience

Akron, OH Medical Device

New York, NY Medical Device Undisclosed

Baltimore, MD Big Data/Analytics

Irvine, CA Workflow

Nashville, TN Patient/Consumer Experience

Denver, CO Workflow

CROSS SECTION: $1M DEALS

GEOGRAPHY INVESTORS

12

An early-stage investment cross-section offers insight across an industry experimenting with maturing ideas. It’s interesting to take note of the varied investors, from population health to workflow supporting these young businesses.

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

Company Amount Subsector Notable Investor

$220M Personalized Health / Quantified-Self

$22.0M Wellness

$13.7M Patient/Consumer Experience

$10.0M Wellness

$7.8M Medical Device

$3.0M Clinical Decision Support

$2.4M Research

$2.1M Medical Device

$2.0M Personalized Health / Quantified-Self

$1.4M Medical Device

StartUp Health Portfolio: Top 10 Deals

GEOGRAPHY INVESTORS

13

The StartUp Health portfolio of 178 companies has raised over $300M in 2016.

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

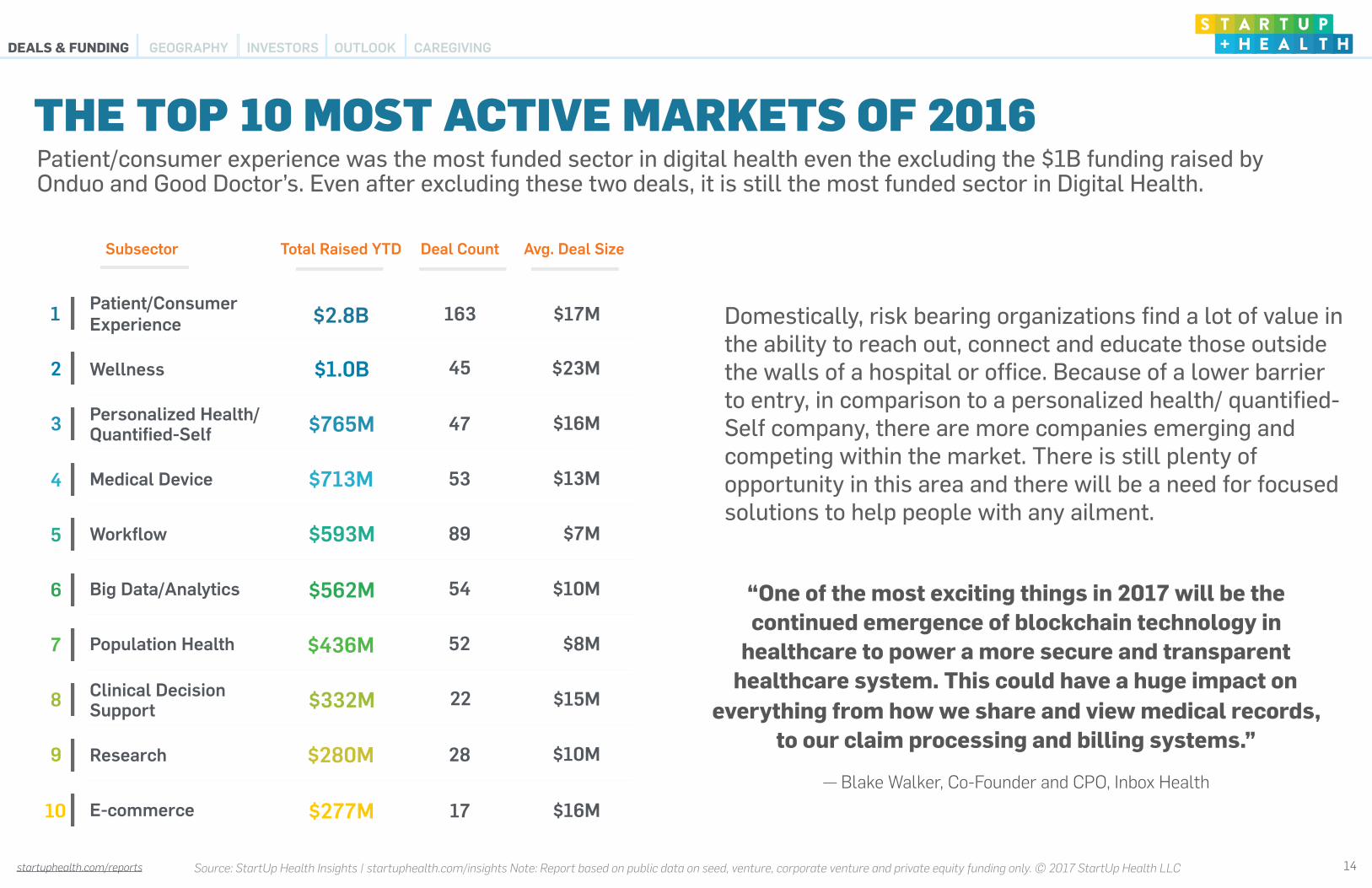

Patient/consumer experience was the most funded sector in digital health even the excluding the $1B funding raised by Onduo and Good Doctor’s. Even after excluding these two deals, it is still the most funded sector in Digital Health.

DEALS & FUNDING OUTLOOK

Subsector Total Raised YTD Deal Count Avg. Deal Size

1 Patient/Consumer Experience $2.8B 163 $17M

2 Wellness $1.0B 45 $23M

3 Personalized Health/ Quantified-Self $765M 47 $16M

4 Medical Device $713M 53 $13M

5 Workflow $593M 89 $7M

6 Big Data/Analytics $562M 54 $10M

7 Population Health $436M 52 $8M

8 Clinical Decision Support $332M 22 $15M

9 Research $280M 28 $10M

10 E-commerce $277M 17 $16M

Domestically, risk bearing organizations find a lot of value in the ability to reach out, connect and educate those outside the walls of a hospital or office. Because of a lower barrier to entry, in comparison to a personalized health/ quantified-Self company, there are more companies emerging and competing within the market. There is still plenty of opportunity in this area and there will be a need for focused solutions to help people with any ailment.

“One of the most exciting things in 2017 will be the continued emergence of blockchain technology in

healthcare to power a more secure and transparent healthcare system. This could have a huge impact on

everything from how we share and view medical records, to our claim processing and billing systems.”

— Blake Walker, Co-Founder and CPO, Inbox Health

THE TOP 10 MOST ACTIVE MARKETS OF 2016

GEOGRAPHY INVESTORS

14

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

2010

2011

2012

2013

2014

2015

2016

0% 25% 50% 75% 100%

Seed Series A Series B Series C Series D Series E Series F + G + H

31% 33% 7%22% 3%

*Deal count only includes Seed though Series G rounds. Does not include venture rounds or growth equity.

Deal Count*

124

237

304

450

391

300

344

2013 remains the year with the most early-stage investments at 74% or 331 deals. The last three years have remained strong with 2/3 of all deals being Seed or A Rounds. Steady Seed Round & Series A funding in 2016 was an encouraging sign that capital is still being distributed among early-stage digital health companies.

DEAL ACTIVITY BY STAGE

GEOGRAPHY INVESTORS

15

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

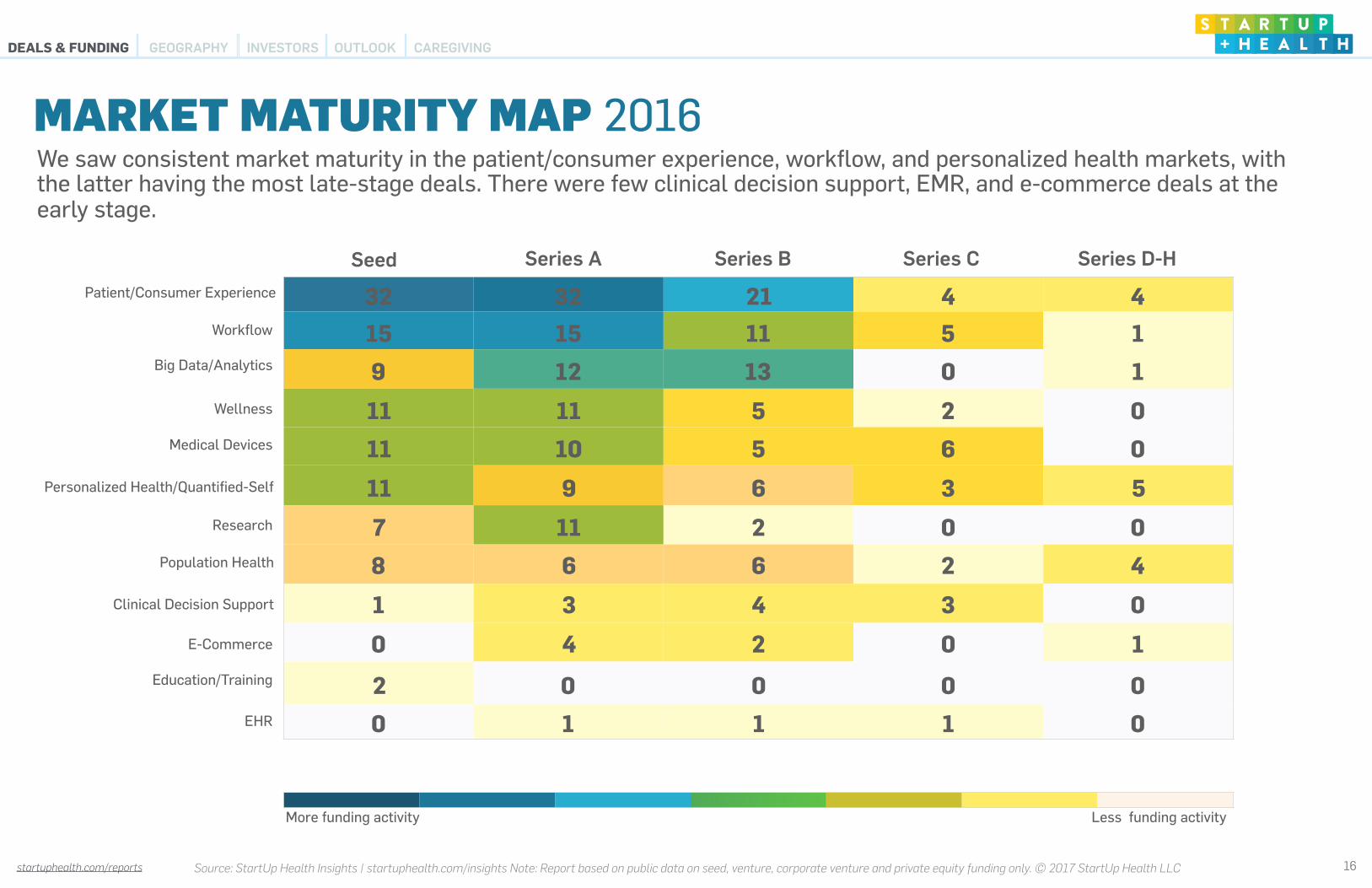

We saw consistent market maturity in the patient/consumer experience, workflow, and personalized health markets, with the latter having the most late-stage deals. There were few clinical decision support, EMR, and e-commerce deals at the early stage.

47%

Patient/Consumer Experience

Wellness

Personalized Health/Quantified-Self

Big Data/Analytics

Medical Devices

Clinical Decision Support

E-Commerce

32 32 21 4 415 15 11 5 19 12 13 0 1

11 11 5 2 011 10 5 6 0

11 9 6 3 5

7 11 2 0 08 6 6 2 4

1 3 4 3 0

0 4 2 0 1

2 0 0 0 00 1 1 1 0

Workflow

Research

Population Health

EHR

Education/Training

Seed Series A Series B Series C Series D-H

DEALS & FUNDING OUTLOOK

MARKET MATURITY MAP 2016

GEOGRAPHY INVESTORS

More funding activity Less funding activity

16

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

47%

163 112 56 22 13108 113 60 25 11108 61 27 10 8

62 61 36 28 2154 73 48 16 13

50 45 32 18 15

45 50 27 9 5

44 43 36 30 25

37 37 16 6 621 31 14 5 5

15 10 8 5 818 9 4 4 4

DEALS & FUNDING OUTLOOK

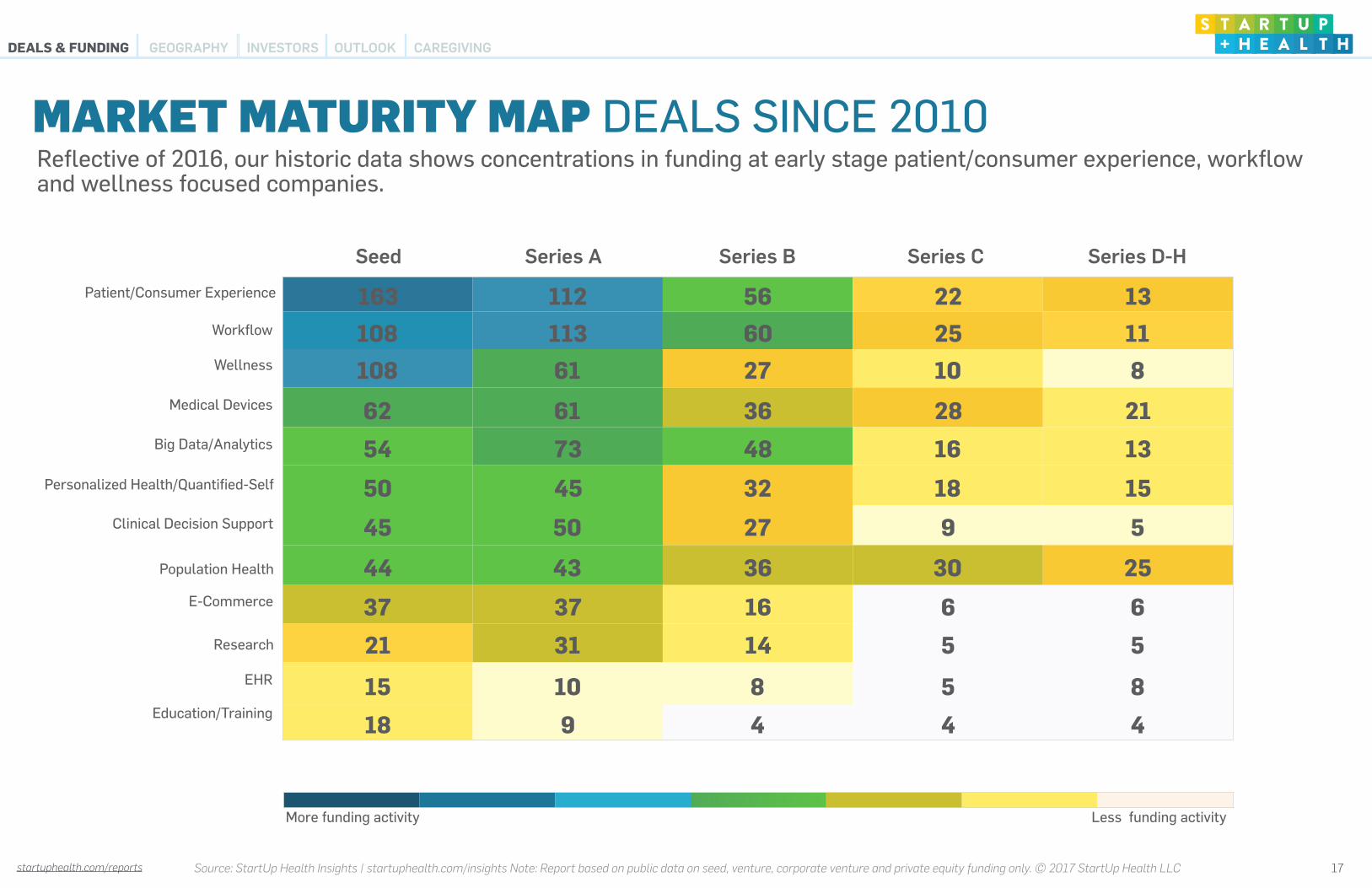

MARKET MATURITY MAP DEALS SINCE 2010

Seed Series A Series B Series C Series D-H

Medical Devices

Personalized Health/Quantified-Self

Big Data/Analytics

E-Commerce

Research

Clinical Decision Support

Population Health

Education/Training

EHR

GEOGRAPHY INVESTORS

Patient/Consumer Experience

Wellness

Workflow

17

More funding activity Less funding activity

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

Reflective of 2016, our historic data shows concentrations in funding at early stage patient/consumer experience, workflow and wellness focused companies.

startuphealth.com/reports

DEALS & FUNDING OUTLOOKFu

ndin

g ($

M)

$0M

$10M

$20M

$30M

$40M

2013 2014 2015 2016Avg. Deal Size Avg. Seed Avg. Series A Avg. Series B Avg. Series C

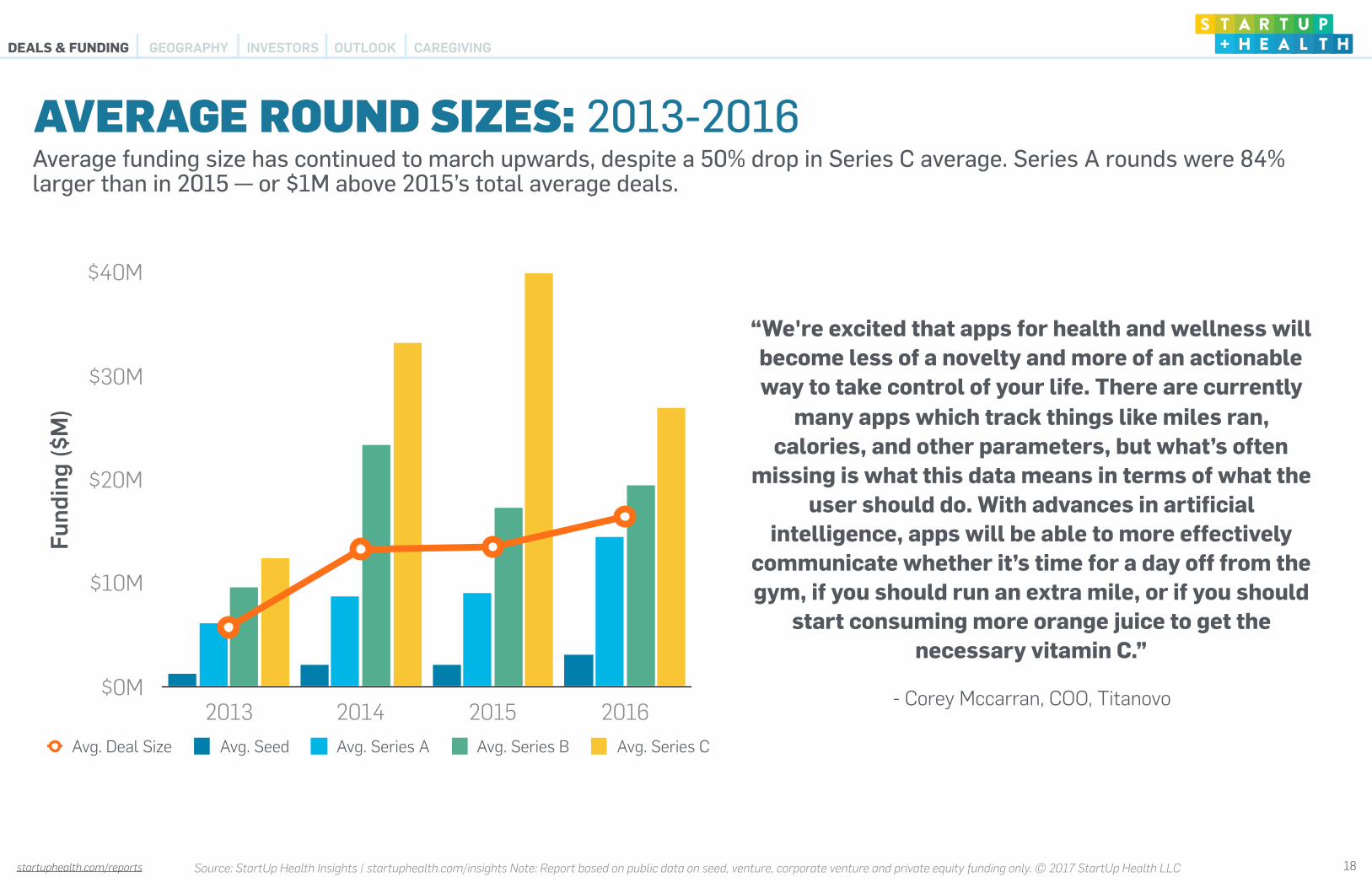

Average funding size has continued to march upwards, despite a 50% drop in Series C average. Series A rounds were 84% larger than in 2015 — or $1M above 2015’s total average deals.

AVERAGE ROUND SIZES: 2013-2016

GEOGRAPHY INVESTORS

18

“We're excited that apps for health and wellness will become less of a novelty and more of an actionable way to take control of your life. There are currently

many apps which track things like miles ran, calories, and other parameters, but what’s often

missing is what this data means in terms of what the user should do. With advances in artificial

intelligence, apps will be able to more effectively communicate whether it’s time for a day off from the gym, if you should run an extra mile, or if you should

start consuming more orange juice to get the necessary vitamin C.”

- Corey Mccarran, COO, Titanovo

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

Freq

uenc

y of

Dea

l Siz

e

0

50

100

150

200

$1M $5M $10M $25M $50M $100M $150M $200M $250M $300M $350M $400M $450M $500M

2014 2015 2016

DEALS & FUNDING OUTLOOK

$500M$400M

$448M

$394M

$500M

$400M

Good Doctor

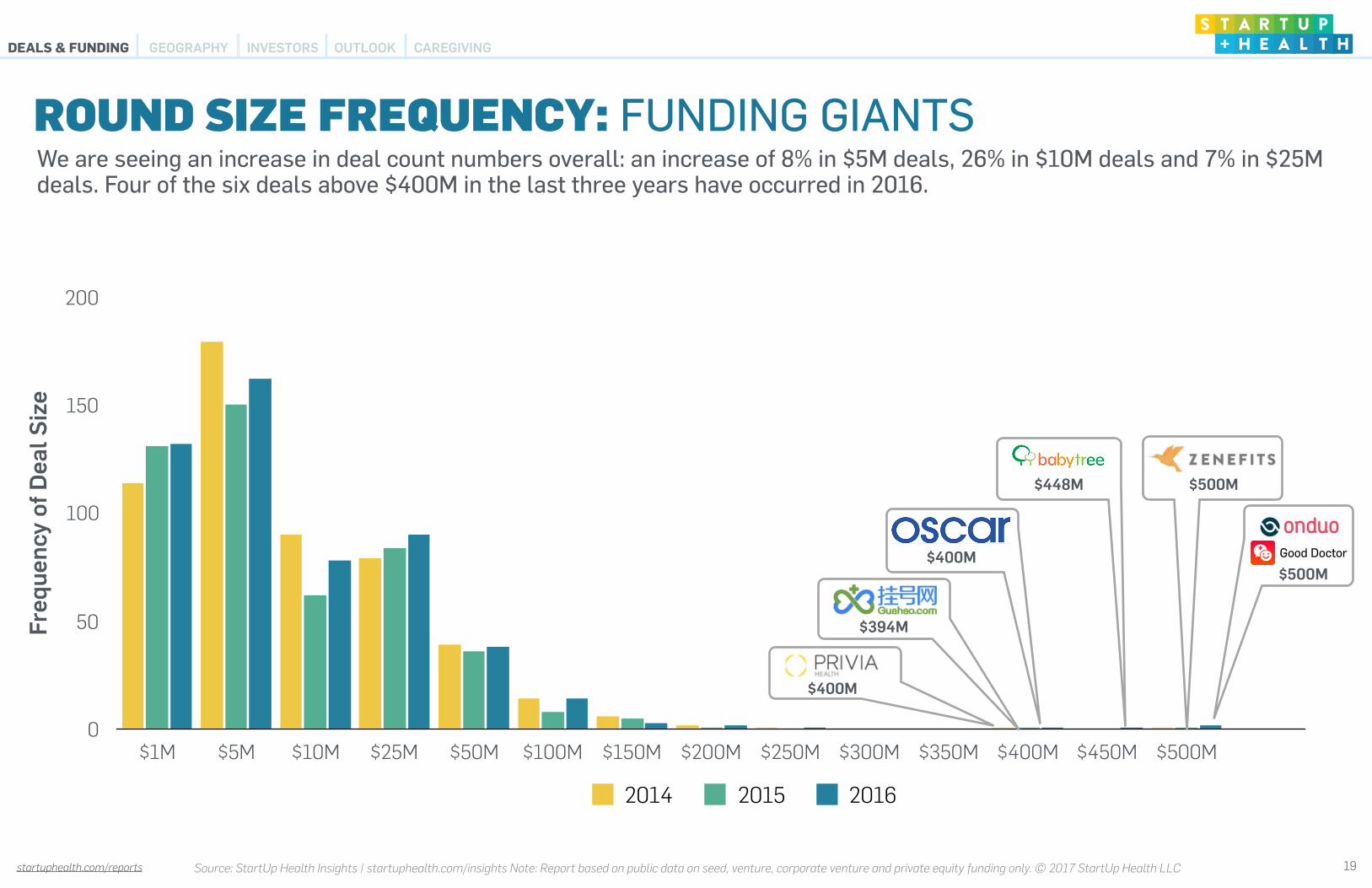

We are seeing an increase in deal count numbers overall: an increase of 8% in $5M deals, 26% in $10M deals and 7% in $25M deals. Four of the six deals above $400M in the last three years have occurred in 2016.

ROUND SIZE FREQUENCY: FUNDING GIANTS

GEOGRAPHY INVESTORS

19

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

INVESTORS OUTLOOK

Region

1 SF Bay Area

2 Boston Metro

3 New York Metro

4 San Diego

5 Los Angeles

6 Minneapolis/St. Paul

7 Philadelphia

8 Chicago

9 Salt Lake City

10 Washington, DC

$105M

$928M

$970M

$710M

$1.5B

San Francisco Bay Area Salt Lake City

San Diego Metro

New York City Metro

Boston Metro

$180MChicago Metro

$216M

Minneapolis / St. Paul Metro

$200M

Philadelphia Metro

(8 Deals)

(7 Deals)(116 Deals)

(15 Deals)

(15 Deals)

(17 Deals)(60 Deals)

(35 Deals)

Los Angeles Metro

$468M(29 Deals)

Washington, DC Metro

$97M

(9 Deals)

Funding continues to be significant in the Bay Area and in the Northeast. In 2016, the metro regions of Boston and New York City yielded 208 deals (47% of all deals) and approximately $3.4B in funding (54% of all funding).

DEALS & FUNDING GEOGRAPHY

THE MOST ACTIVE US METRO AREAS OF 2016

20

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

DEALS & FUNDING OUTLOOK

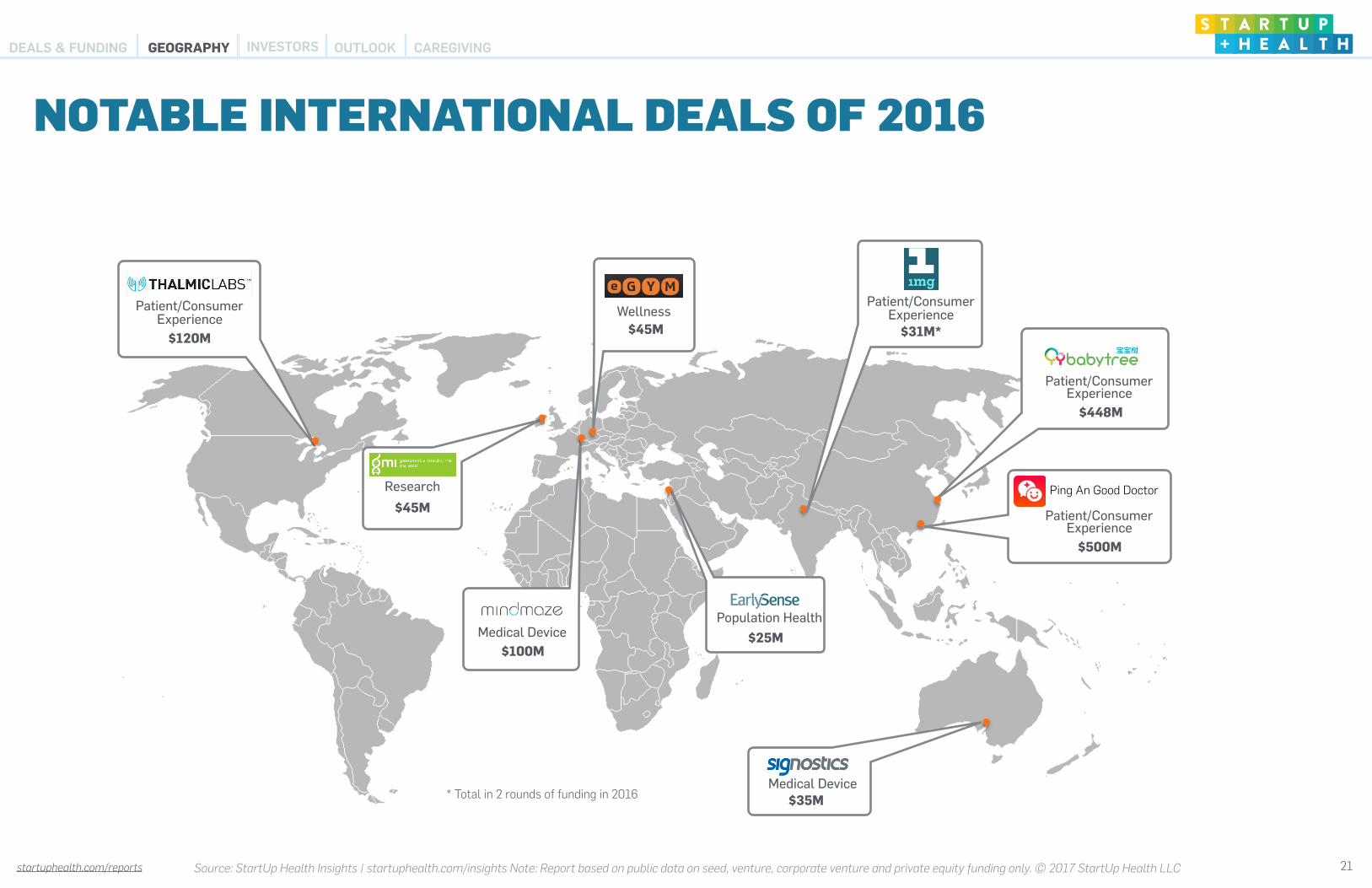

NOTABLE INTERNATIONAL DEALS OF 2016

China

$500M

Patient/Consumer Experience

Ping An Good Doctor

$448M

Patient/Consumer Experience

Patient/Consumer Experience

$120M

$100MMedical Device

$45MWellness

$45MResearch

Population Health$25M

Patient/Consumer Experience

$31M*

* Total in 2 rounds of funding in 2016 $35MMedical Device

INVESTORSGEOGRAPHY

21

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

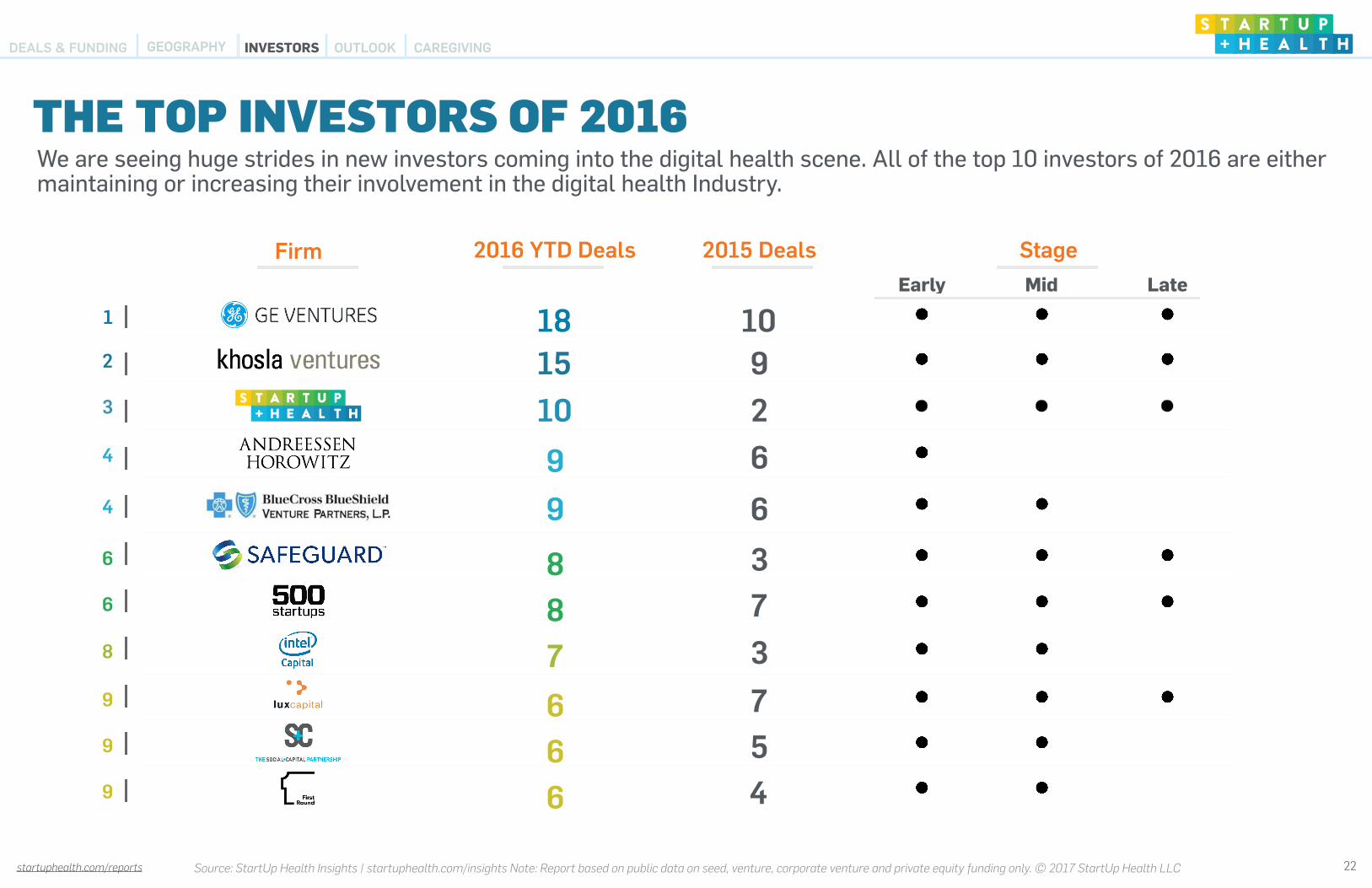

Firm 2016 YTD Deals 2015 Deals StageEarly Mid Late

1 18 102 15 93 10 24 9 64 9 66 8 36 8 78 7 39 6 79 6 59 6 4

DEALS & FUNDING OUTLOOK

THE TOP INVESTORS OF 2016

INVESTORSGEOGRAPHY

22

We are seeing huge strides in new investors coming into the digital health scene. All of the top 10 investors of 2016 are either maintaining or increasing their involvement in the digital health Industry.

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

0

13

26

39

52

65

78

91

104

117

130

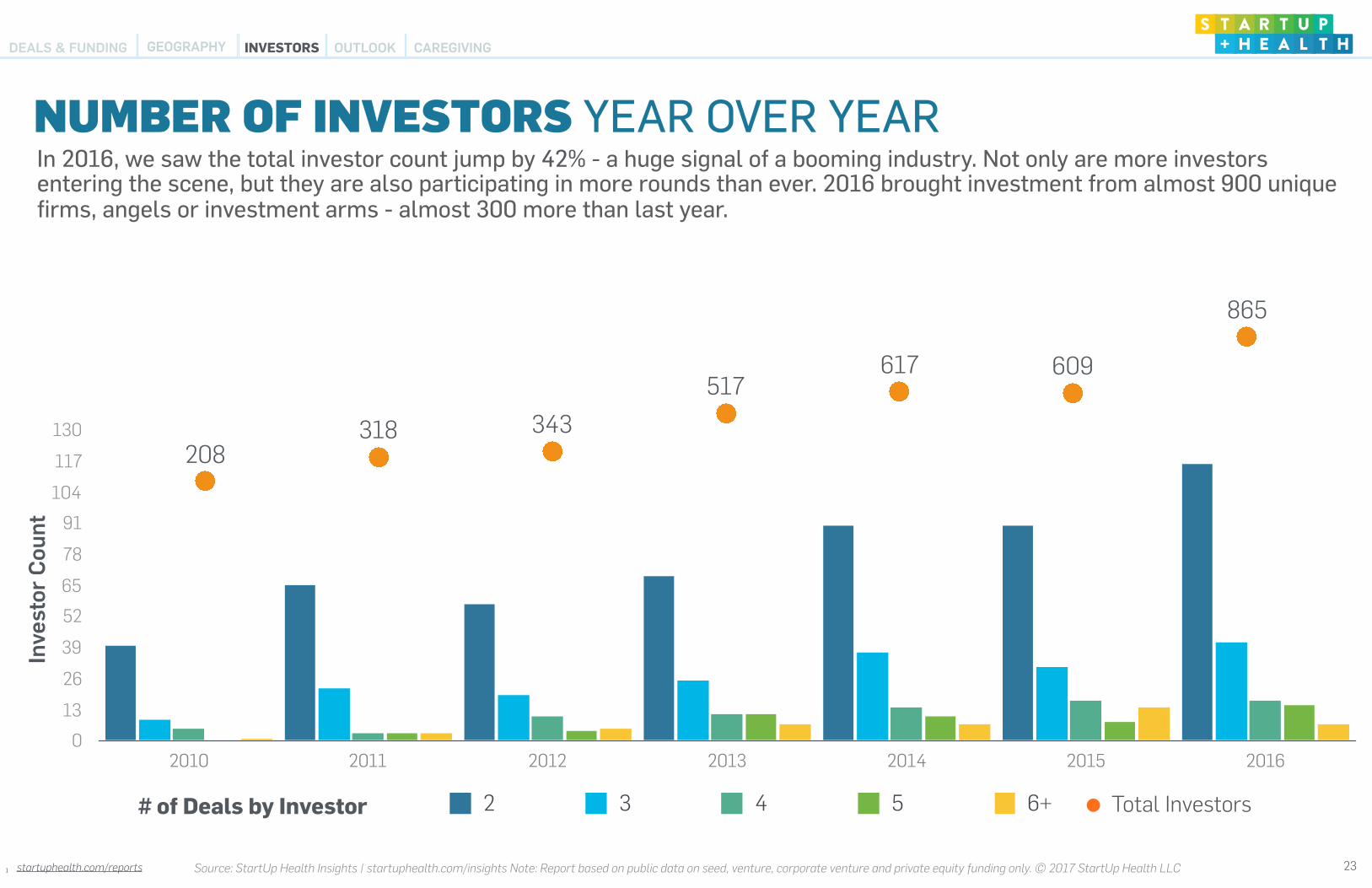

2010 2011 2012 2013 2014 2015 2016

2 3 4 5 6+

1

In 2016, we saw the total investor count jump by 42% - a huge signal of a booming industry. Not only are more investors entering the scene, but they are also participating in more rounds than ever. 2016 brought investment from almost 900 unique firms, angels or investment arms - almost 300 more than last year.

208318 343

517617 609

865

Inve

stor

Cou

nt

# of Deals by Investor

NUMBER OF INVESTORS YEAR OVER YEAR

Total Investors

23

DEALS & FUNDING OUTLOOKINVESTORSGEOGRAPHY CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports1

DEALS & FUNDING OUTLOOK

We surveyed Health Transformers from the StartUp Health Academy about their fundraising experiences in 2016 and their predictions for 2017.

15%

35% 35%

15%

<2 Months2-6 Months6 - 10 Months>10 Months

How long did Health Transformers most recent fundraising process last?

26%

16%

13%

26%

19%1 - 5 firms5 - 10 firms10-20 firms20-30 firms30+ firms

How many firms did Health Transformers pitch to while raising their last round?

INSIGHTS FROM HEALTH TRANSFORMERS

GEOGRAPHY INVESTORS

N = 37 N = 37

24

“Digital health reflects the incredible technological progress of the 21st century. It is another industry

revolution that we are lucky to witness and participate in.”

- -Leon Eisen, PhD, CEO, Oxitone Medical

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports1

DEALS & FUNDING OUTLOOK

1

“The change in access to care is going to be powerful and lead to happier and healthier people everywhere. I can't wait”

“I am excited that there is more interest in Mental Health than ever before and changes are coming in federal regulations to increase the attention in this area.

The gap between idea and implementation is a difficult one to bridge, which makes 2017 a truly exciting time to be an innovator in ‘aging-in-place’ technologies.”

“If we change ourselves, the realities of the world will change. I look forward to the day where all people, of all diversities, break the boundaries between healthcare provider and patient and celebrate the truth that we are all patients and we all have a responsibility in creating a better, sustainable world- especially in Health. I'm most excited about our world taking action towards the advancement of understanding, the destruction of ideologies and judgements, and the growth of consciousness. I know that health will play a central role in this growth of mankind.”

“I am thrilled to see that the healthcare ecosystem is being more receptive to AI and I am excited to see how our ecosystem really maximizes it to cut patient cost down and deliver better patient outcomes to all.”

“The recent developments in technology in 2016 now allow medical entrepreneurs to enter the world of digital health with a much lower technological threshold.”

“In 2017, we are most excited to see online healthcare increasingly become not only a tool to get quick online help from a doctor for a specific problem, but also a channel to deepen and extend your offline relationship with your preferred provider”

“Imagine a world though, where you can be in NYC, Springfield or Mali and have access to an identical level of care”

“2017 will be a year of big change and disruption. We will have to deal with some negative pressures but new opportunities can be born in such a high-pressure environment, and I believe that innovations by private companies and startups will fill the void created when the government steps back”

GEOGRAPHY INVESTORS

- Hunter Howard, Founder, President- Ansgar Bittermann, Founder, CEO

- Coley Parry, Founder, CEO

- Eric Price, Founder, CEO

- Teddy Hodges, Founder, CEO

- Beth Sanders, Founder, CEO- Jean Anne Booth, Founder, CEO- Maksim Tsvetovat, Founder, CTO

- Alex Guastella, Founder

INSIGHTS FROM HEALTH TRANSFORMERS

25

CAREGIVING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

A Spotlight on Caregiving sponsored by

Data sourced and provided by:

* Data in following section is separate from StartUp Health Insights data

*

26

DEALS & FUNDING OUTLOOKGEOGRAPHY INVESTORS CAREGIVING

startuphealth.com/reports Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

THE CAREGIVING INVESTMENT LANDSCAPEBy 2020, 117 million Americans are expected to need assistance of some kind, yet the overall number of unpaid caregivers is only expected to reach 45 million. Technology holds great promise for helping to reduce the complexities, stress, and sheer hard work of these caregivers. Companies from established multinationals to startups, mass-market firms to niche players, are recognizing this caregiving market opportunity that’s expected to reach $72 billion in 2020 alone.

27

DEALS & FUNDING OUTLOOKGEOGRAPHY INVESTORS CAREGIVING

startuphealth.com/reports Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

OUTLOOKGEOGRAPHY INVESTORS

28

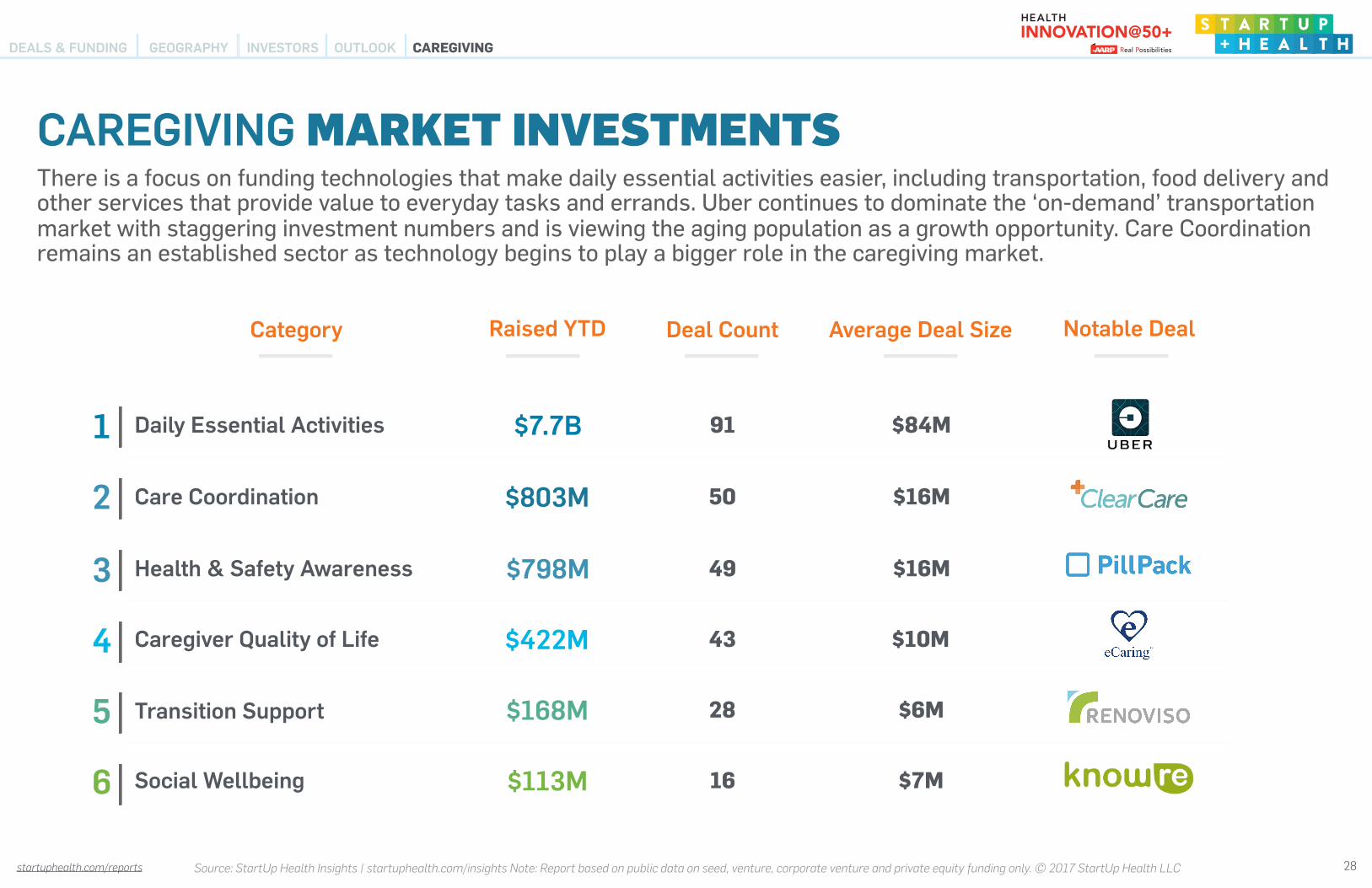

Category Raised YTD Deal Count Average Deal Size Notable Deal

1 Daily Essential Activities $7.7B 91 $84M

2 Care Coordination $803M 50 $16M

3 Health & Safety Awareness $798M 49 $16M

4 Caregiver Quality of Life $422M 43 $10M

5 Transition Support $168M 28 $6M

6 Social Wellbeing $113M 16 $7M

There is a focus on funding technologies that make daily essential activities easier, including transportation, food delivery and other services that provide value to everyday tasks and errands. Uber continues to dominate the ‘on-demand’ transportation market with staggering investment numbers and is viewing the aging population as a growth opportunity. Care Coordination remains an established sector as technology begins to play a bigger role in the caregiving market.

CAREGIVING MARKET INVESTMENTS

CAREGIVINGDEALS & FUNDING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

OUTLOOKGEOGRAPHY INVESTORS

29

CAREGIVING MARKET TOP DEALSWhile not counted in StartUp Health’s data as a digital health deal, Uber and several other top deals this year could have a significant healthcare impact on the aging community. There is a healthy mix of hedge funds, venture firms and other investor types interested in supporting the caregiving market.

Notable Deal Total Raised YTD Notable Investor Category

1 $5.9B Daily Essential Activities

2 $500M Daily Essential Activities

3 $189M Daily Essential Activities

4 $175M Care Coordination

5 $141M Daily Essential Activities

6 $127M Health & Safety Awareness

7 $126M Daily Essential Activities

7 $111M Daily Essential Activities

7 $100M Caregiver Quality of Life

7 $100M Caregiver Quality of Life

CAREGIVINGDEALS & FUNDING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

OUTLOOKGEOGRAPHY INVESTORS

30

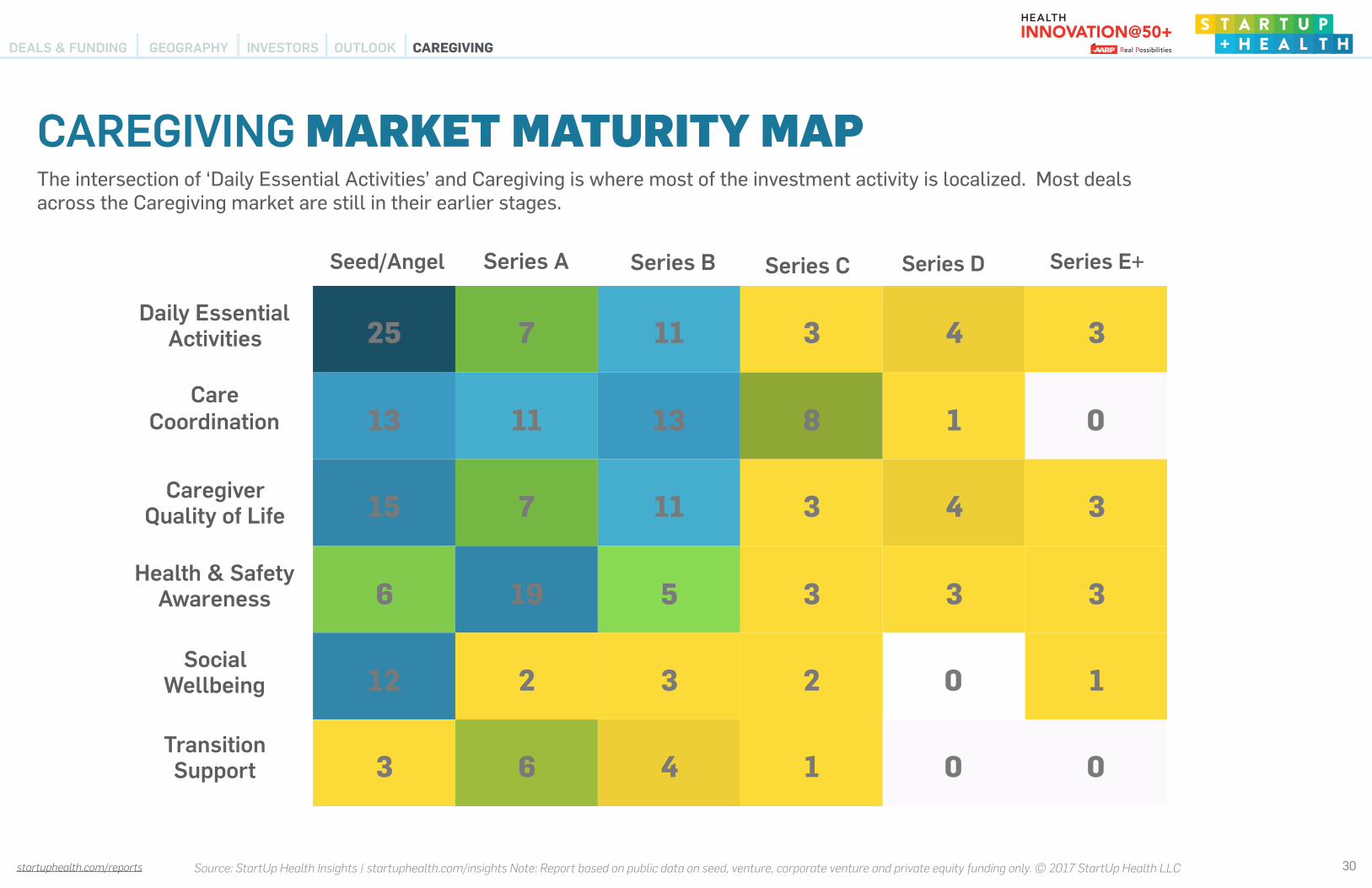

47%

45%

25 7 11 3 4 3

13 11 13 8 1 0

15 7 11 3 4 3

6 19 5 3 3 3

12 2 3 2 0 1

3 6 4 1 0 0

Seed/Angel Series A Series B Series C Series D

Care Coordination

Caregiver Quality of Life

Daily Essential Activities

Health & Safety Awareness

Social Wellbeing

Transition Support

The intersection of ‘Daily Essential Activities’ and Caregiving is where most of the investment activity is localized. Most deals across the Caregiving market are still in their earlier stages.

CAREGIVING MARKET MATURITY MAP

Series E+

CAREGIVINGDEALS & FUNDING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

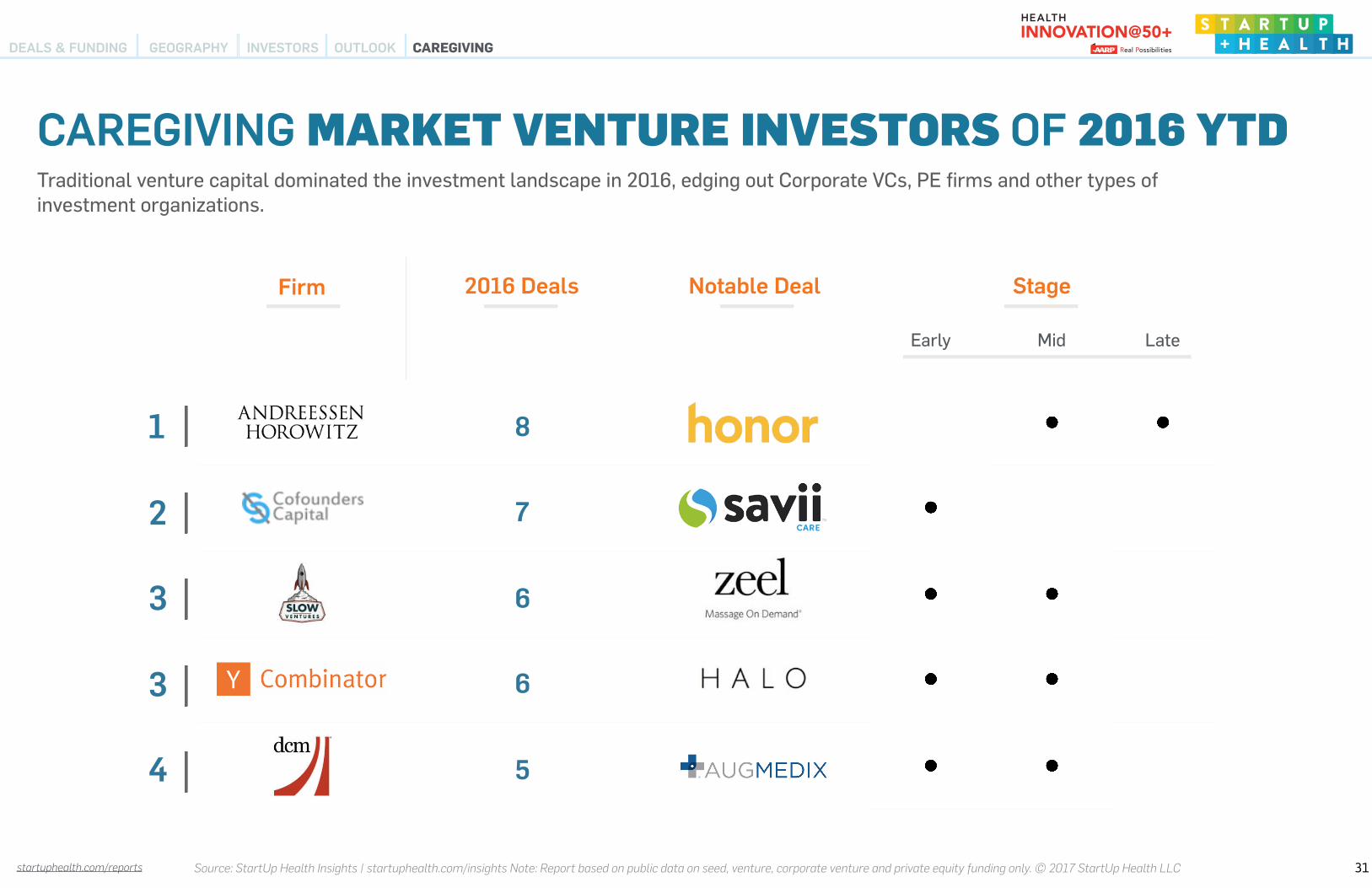

Traditional venture capital dominated the investment landscape in 2016, edging out Corporate VCs, PE firms and other types of investment organizations.

CAREGIVING MARKET VENTURE INVESTORS OF 2016 YTD

Firm 2016 Deals Notable Deal Stage

Early Mid Late

1 8

2 7

3 6

3 6

4 5

31startuphealth.com/reports

OUTLOOKGEOGRAPHY INVESTORS CAREGIVINGDEALS & FUNDING

Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports1

Sectors: • We have a broad view of digital health and believe that the current trend is a

cross-pollination of technology and data with all aspects of health and healthcare. StartUp Health InsightsTM tracks companies that enable health, wellness and the delivery of care through data / analytics, sensors, mobile, internet-of-things, 3D printing and genomics and personalized medicine.

• StartUp Health tracks companies based on their sectors, subsectors and specialties. Investments in subsectors and specialties are not mutually exclusive, as deals are tagged with multiple subsectors and specialties based on the company’s focus.

• Q2 of 2015 brought with it an extensive database quality assessment. A new system was implemented allowing StartUp Health to track innovation with enhanced granularity. Additionally, gaps in funding data were researched and added into our database enabling us to identify fundings previously unaccounted for in previous reports.

Stage of Funding: • StartUp Health InsightsTM records only publicly available data on cash for equity

investments as the cash is actually received by the company. StartUp Health InsightsTM is inclusive of accelerator, pre-seed, seed, venture, corporate venture and private equity funding.

• Early stage: The company has raised a Seed or Series A round • Mid stage: The company has raised a Series B or Series C round • Late stage: The company has raised a Series D or other growth equity round • StartUp Health also tracks incubator rounds and other financings into privately-

held entities (e.g. “unnamed” venture rounds, strategic investments, growth equity and private equity).

• In tabulating deal activity by stage we excluded rounds not clearly associated with a specific stage.

Sources: • Funding data is from StartUp Health InsightsTM, the most comprehensive

funding database for digital health, and managed by the StartUp Health team. Information, data and figures represent only publicly available data.

• Data for acquisitions slide was provided by a range of sources including StartUp Health InsightsTM, CrunchBase, AngelList and news reports.

• StartUp Health works to ensure that the information contained in the StartUp Health InsightsTM Report has been obtained from reliable sources. However, StartUp Health cannot warrant the ultimate validity of the data obtained in this manner. All data is subject to verification with the venture capital firms and/or the investee companies. Results are updated periodically. Therefore, all data is subject to change at any time.

• If you find an error please let us know so we can correct it.

This report is provided for informational purposes and was prepared in good faith on the basis of public information available at the time of publication without independent verification. StartUp Health does not guarantee or warrant the reliability or completeness of the data nor its usefulness in achieving any particular purposes. StartUp Health shall not be liable for any loss, damage, cost or expense incurred by reason of any persons use or reliance on this report. This report is a proprietary aggregation of publicly available data and shall not be forwarded or reproduced without the written consent of StartUp Health.

METHODOLOGIES

32Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC

startuphealth.com/reports

STARTUP HEALTH’S GROWING ARMY

33Source: StartUp Health Insights | startuphealth.com/insights Note: Report based on public data on seed, venture, corporate venture and private equity funding only. © 2017 StartUp Health LLC