All shows start at 7:00 pm • Bring a chair or blanket For ...

S corporations

Start time is 1:00 PM

Topics

- Corporations – General

- S Corporations

- S Corporate Liquidations

S Corporations

Difficulties for tax preparers

- IRS audit issues

- Information lacking

- Complicated tax rules

Page 1

Corporate Formalities

- Articles of incorporation;

- Issue stock;

- Pay corporate debt only from corporate checking;

- Have annual meetings.

Page 1

Note:

Piercing the corporate veil

- Corporate entity is not recognized.

- From either an income tax perspective or from a liability perspective.

Page 2

Insulating the Owners

From liabilities & debts

Only assets of corporation are at risk

Personal signature guarantee

Page 2

Professional negligence

Acts by shareholder who did not act prudently regarding

business operations.

Page 2

What Clients Think …

In one case SP incorporated and dropped all vehicle

insurance.

Page 2

What Clients Think …

He thought the corporate liability shield would

eliminate the need for insurance.

Page 2

What Clients Think …

Under these conditions, the business owner was held

personally liable.

Page 2

Personal Signature

Guarantees

- Many Vendors

- All Banks

Require a personal signature guarantee

Page 2

Incomplete Incorporations

- Reporting the 351 transfer

- Transferring title of assets

- Capitalizing & issuing stock

- Establishing minutes

Page 2

Incomplete Incorporations

- Establishing corporation bank accounts

- Establishing corporate licensing

- Transferring insurance coverage

Page 2

Types of Corporations

S Corporation

Generally, not taxed at Corp Level

Flow-through, taxed at shareholder level

Page 2

Types of Corporations

C Corporation

Separate Taxable Entity

Corporation pays taxes

Distributions taxed again at the shareholder level

Page 2

The LLC C Corporation

- Check the box regulations

- File Form 8832

- No further effort – Entity is taxed as C Corporation

Page 3

The SMLLC S Election

Two-prong procedure WAS required

1. Filing Form 8832 and

2. Filing Form 2553

Page 3

Both forms

no longer necessary

- Filing Form 2553 functions as “deemed” entity classification.

Page 3

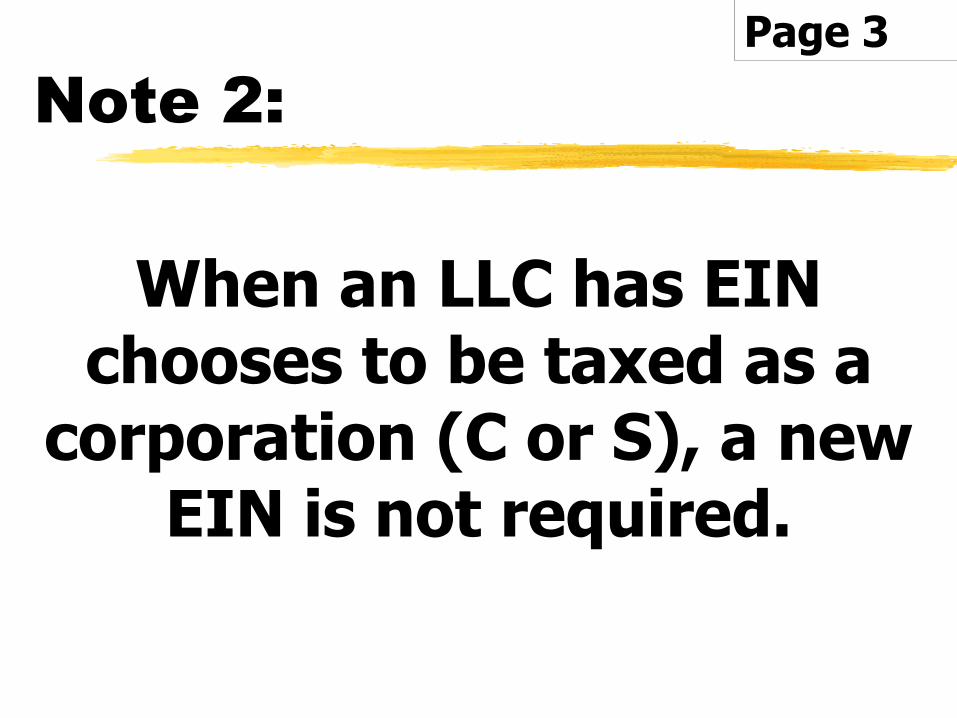

Note 2:

When an LLC has EIN chooses to be taxed as a

corporation (C or S), a new EIN is not required.

Page 3

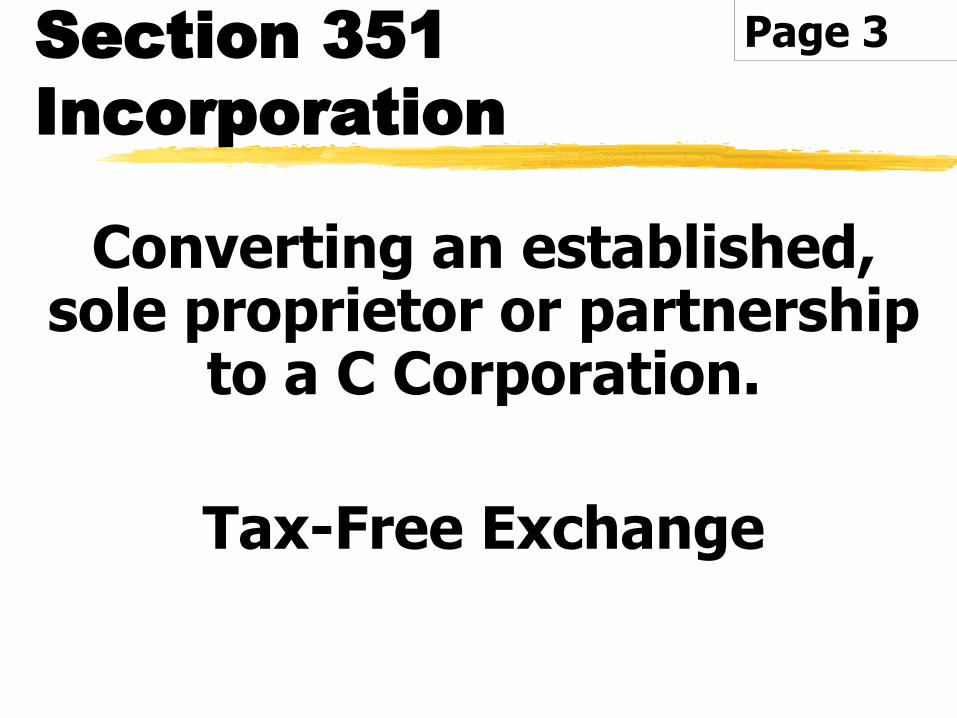

Section 351

Incorporation

Converting an established, sole proprietor or partnership

to a C Corporation.

Tax-Free Exchange

Page 3

§351 Transfer

- Transfer assets and liabilities in exchange for stock

- Receive only stock

Page 3

After the Exchange

In control of corporation

Must own at least 80% total voting power and 80% of all other classes of stock.

Page 3

§351 Transfer

Stock must be only asset received

Anything else is boot.

Gain is recognized to the extent of any boot received.

Page 3

Don’t …

Withdraw significant amounts of cash prior to incorporation.

If it’s working capital.

Working capital should be part of transfer.

Page 3

§351 Transfer

Cannot relieve the owner of debt that exceeds the basis of

the assets which are transferred to the corporation.

Page 4

Example 1:

Basis of AssetsTransferred $15,000Less: Debt Assumed (10,000)

Basis in Stock $ 5,000

Page 4

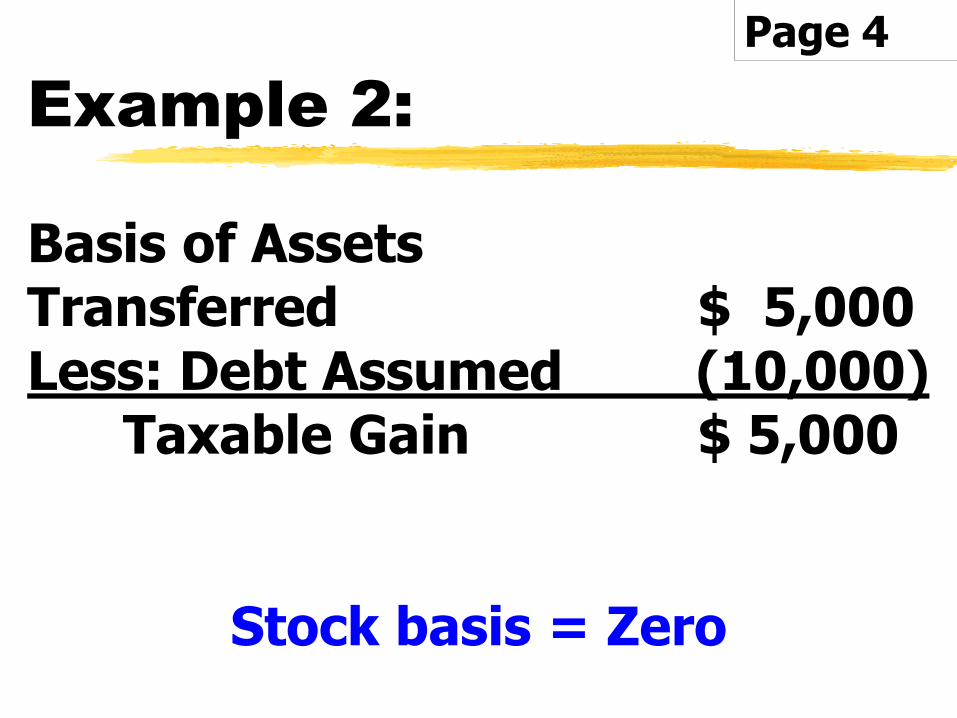

Example 2:

Basis of AssetsTransferred $ 5,000Less: Debt Assumed (10,000)

Taxable Gain $ 5,000

Stock basis = Zero

Page 4

§351 Incorporation

Balance Sheet

Assets Liabilities & Equity

Checking Account $ 5,000 Debt $105,000

Equipment 200,000 Equity 100,000

$205,000 $205,000

Equipment's FMV is $300,000.The taxpayer received only stock in the transaction. The stock received has a basis of $100,000.

Page 5

Change the facts …

Balance Sheet

Assets Liabilities & Equity

Checking Account $ 5,000 Debt $155,000

Equipment 250,000 Equity 100,000

$255,000 $255,000

The taxpayer also received a note receivable for $50,000.

Page 5

Change the facts - again

Balance Sheet

Assets Liabilities & Equity

Checking Account $ 5,000 Debt $155,000

Equipment 205,000 Equity 55,000

$210,000 $210,000

The taxpayer received a note receivable for $50,000.

Equipment's FMV is $250,000.

Page 5

Change the facts - again

In this last situation, even though the taxpayer received a note receivable for $50,000, only $5,000 is taxable.

Page 5

Page 6

Section 351 Transfer Statement

1. Assets transferred

2. Liabilities assumed

3. Stock received

FMV Basis

4. Notes received

5. Money received

6. Other property received

Sample §351 Statement

Attached to both the:

- Corporate tax return, and

- Individual tax return

Page 6

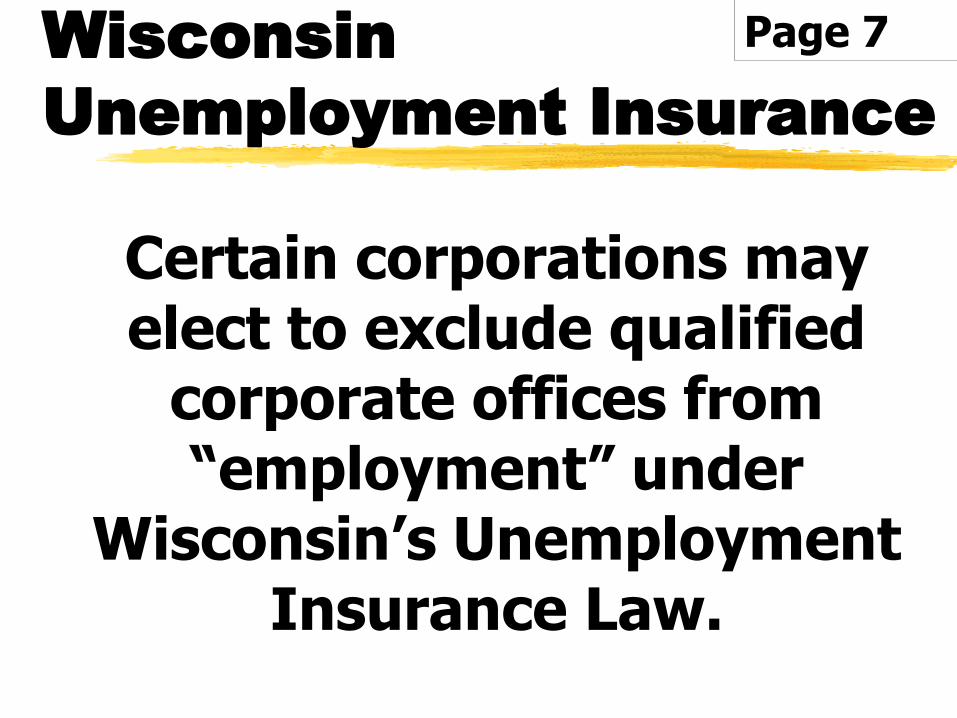

Wisconsin

Unemployment Insurance

Certain corporations may elect to exclude qualified

corporate offices from “employment” under

Wisconsin’s Unemployment Insurance Law.

Page 7

Wisconsin

Unemployment Insurance

If elected, the officer’s wages are not subject to state Unemployment Insurance taxes.

Remember to check with your specific state.

Page 7

Eligible for the Exclusion

Four conditions:

1. UI taxable payroll is less than $500,000.

2. Election made by March 31

Page 7

Eligible for the Exclusion

3. Election all officers who hold 25% or more interest.

4. The corporation has not previously elected the exclusion.

Page 7

Example 1:

An insurance agent started his S-Corp business in 2021 and

currently is the only employee with a salary of $30,000.

Page 7

Example 1:

His unemployment rate as a new business is 3.05%.

Without officer exclusion:

FUTA $ 42

SUTA 427

Total $469

Page 7

Example 1:

If he elected to exclude from SUTA, his FUTA would be $420.

Question: Is a savings of $49 enough to make the election?

Page 7

Example 2:

Same facts as example 1, except he has been in

business for several years and his SUTA rate is now 2.1%.

Without the exclusion, his

Page 7

Example 2:

His unemployment rate as a new business is 3.05%.

Without officer exclusion:

FUTA $ 42

SUTA 294

Total $336

Page 7

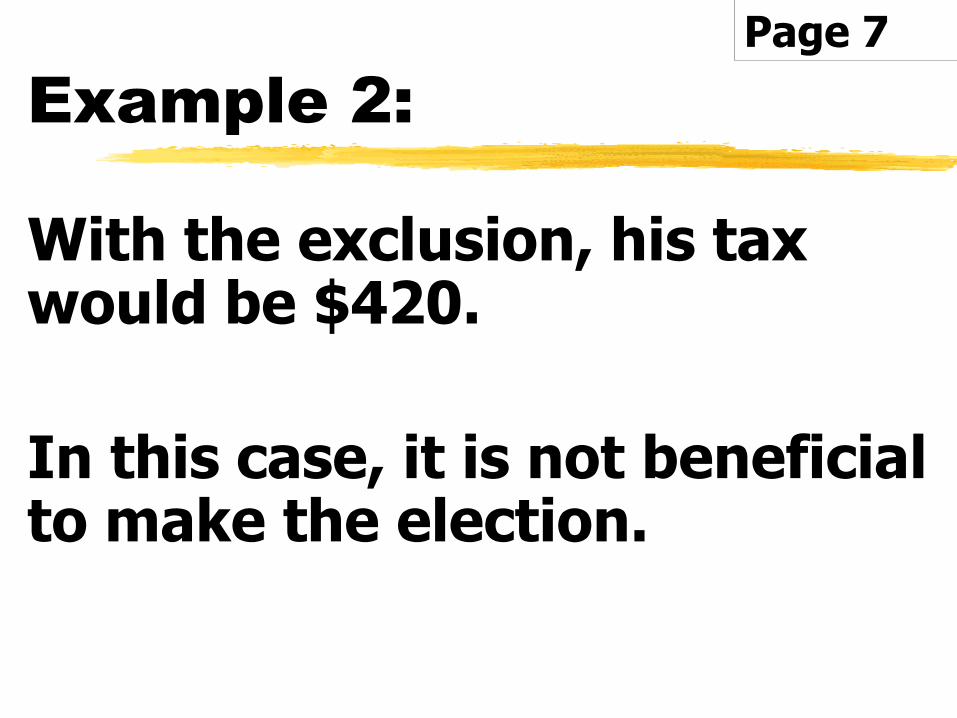

Example 2:

With the exclusion, his tax would be $420.

In this case, it is not beneficial to make the election.

Page 7

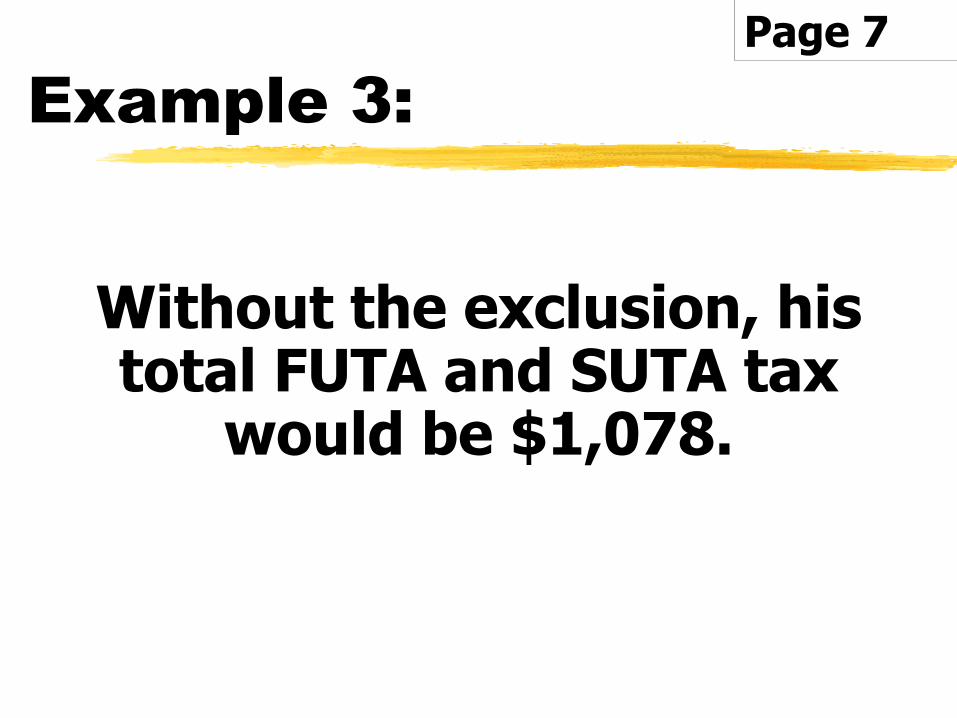

Example 3:

A home builder who has been in business for several years

operating as an S Corporation with a SUTA rate of 7.4%.

Page 7

Example 3:

Without the exclusion, his total FUTA and SUTA tax

would be $1,078.

Page 7

Example 3:

With the exclusion, his total FUTA tax would be $420.

A savings of $658 is worth the election.

Page 7

Workman’s

Compensation

Rules vary state to state

In this case, we are discussing Wisconsin only.

Page 8

Page 8

Wisconsin Only

Corporate Officers

If the corp. has no more than 2 corporate officers and no other employees, Worker’s Comp. policy is not required if both officers elect out.

Page 9

Wage for Officers

Workman’s Compensation

Normally based on amount of gross compensation.

For business owner’s it is based on amount of “deemed wages”

Page 9

Wage for Officers

Workman’s Compensation

Regardless of the amount of actual wages paid, the deemed:

Minimum wage = $290/week and

Max. wage = $1,641/week.

Page 9

Health Insurance

Workman’s compensation

If you elected out of workman’s compensation you may not be covered under your health insurance plan.

Check with your insurance agent.

Page 9

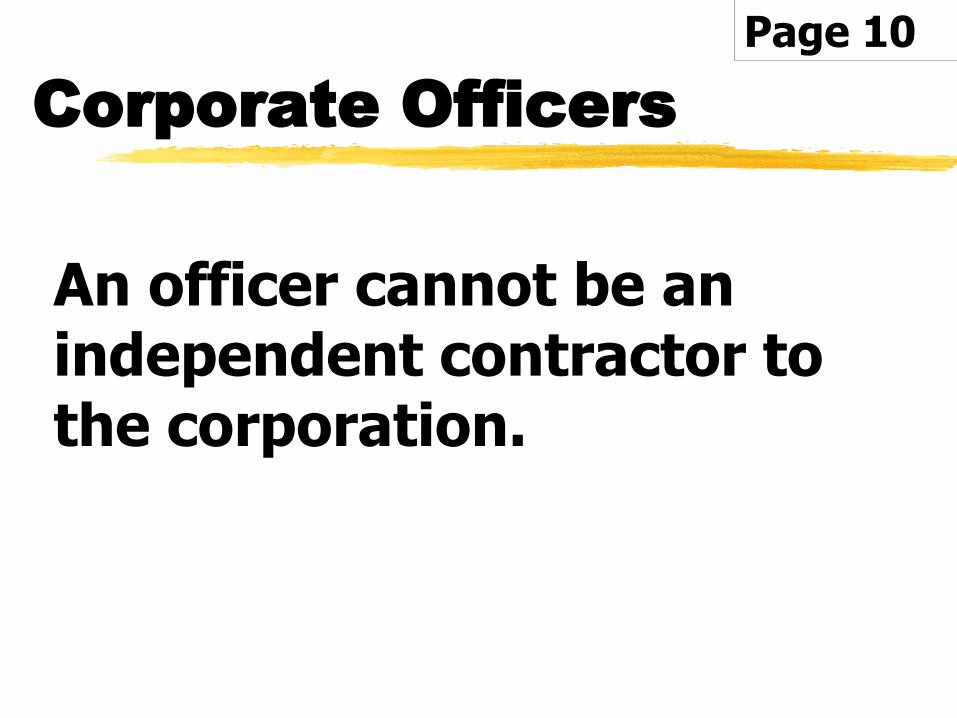

Corporate Officers

An officer cannot be an independent contractor to the corporation.

Page 10

Directors’ Fees

Deductible if it’s reasonable for the services rendered.

Other deduction on 1120

1099-NEC if over $600

Page 10

Social Security

Eligibility

Many business owners “reduce” their wages to stay under wage limits for early retirement.

If full retirement age no income limitations.

Page 10

When you work for

someone else

- Easy to determine if you’re retired

- If you own your business, it’s not so easy to determine.

Page 10

Areas of Concern

S Corporation Distributions

SSA may reclassify as earned income

Rent paid to Shareholders

SSA may reclassify as earned income

Distributions to other family members

Payroll to spouse

Page 10

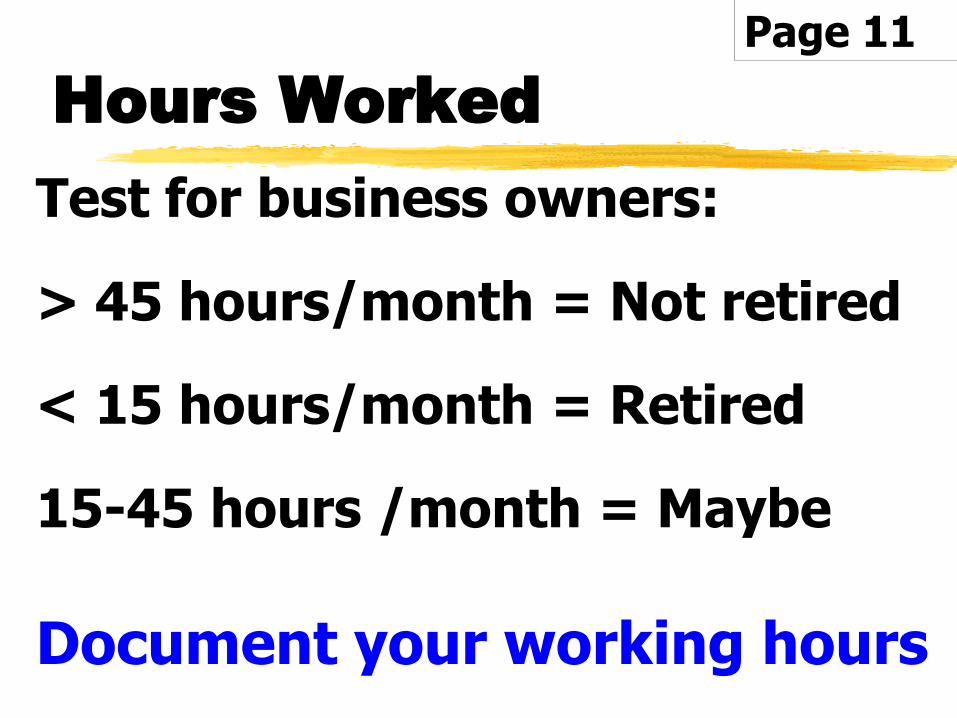

Hours Worked

Test for business owners:

> 45 hours/month = Not retired

< 15 hours/month = Retired

15-45 hours /month = Maybe

Document your working hours

Page 11

Recommendation

If your client is thinking of early retirement and owns a business have them go to:

www.socialsecurity.gov and print

Form SSA-4184 and review.

Page 11

Leasing Property

to Corporation

Lease payment deductible to Corporation.

Shareholder pays taxes on lease payments.

Rent in excess of FMV could be treated as a dividend.

Page 11

Duplicating Supply Co

Tax court found rent charged was excessive.

- Constructive dividend, plusnegligence penalties.

- Taxpayer made no attempt to determine FMV rent.

Page 11

Note:

Get a letter from local realtor to determine FMV for rental.

Draft a rental agreement

Payments should be made timely

Recorded in corporate minutes

Page 12

Caution:

Rental of personal property

Income is subject to:

Social Security Taxes AND

Sales Taxes

Page 12

Net Investment

Income Surtax (3.8%)

Generally applicable to Rental Income

$250,000 MFJ

$125,000 MFS

$200,000 S, HOH

Page 12

Self-Rental

Property that you rent to a trade or business in which you materially participate.

Page 12

Self-Rental

Deductible to Corporation

Taxable to Shareholder

Also subject to the NIIT if the shareholder does not materially participate.

Page 12

Example:

Tom works for ABC Inc.

He has no ownership in ABC.

Tom purchased RE to rent to ABC Inc.

Page 13

Example:

Tom materially participates in ABC Inc.

The rental property it self-rental – so it’s not subject to the NIIT.

Page 13

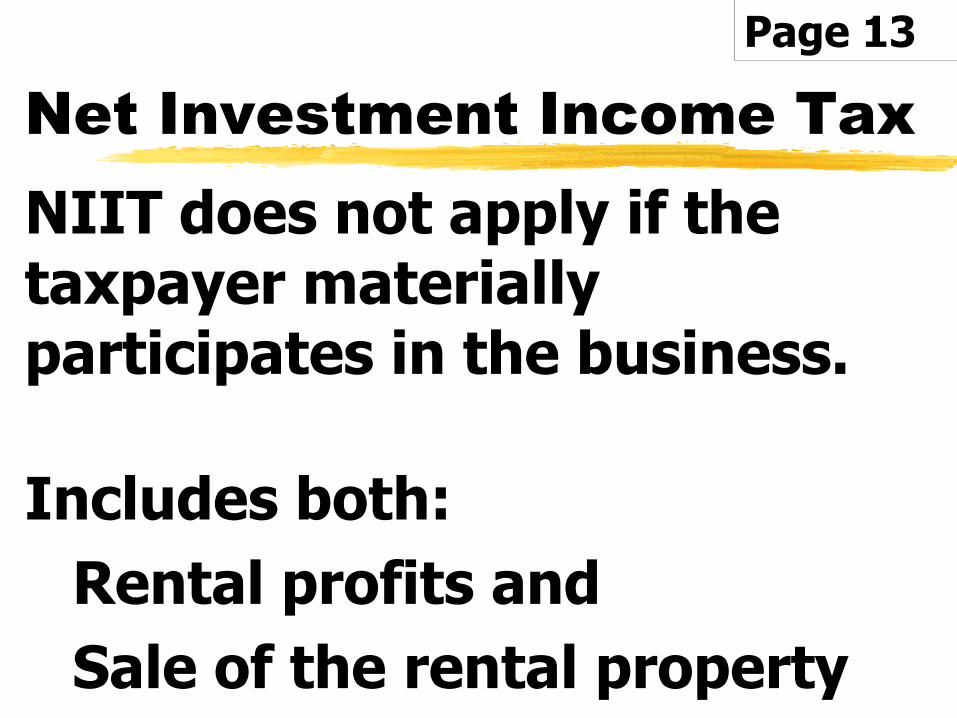

Net Investment Income Tax

NIIT does not apply if the taxpayer materially participates in the business.

Includes both:

Rental profits and

Sale of the rental property

Page 13

Renting your Home

For less than 15 days

- Do not report any income

- Do not take any deductions

Page 13

Note:

Some suggest:

- Hold meetings monthly in the shareholder’s home.

- Charge $1,000 per meeting

- Corp takes deduction

- Shareholder does not report

Page 13

Note:

A few basics:

- Must be bona fide meeting

- Rent must be reasonable.

We do not subscribe to this concept.

Page 13

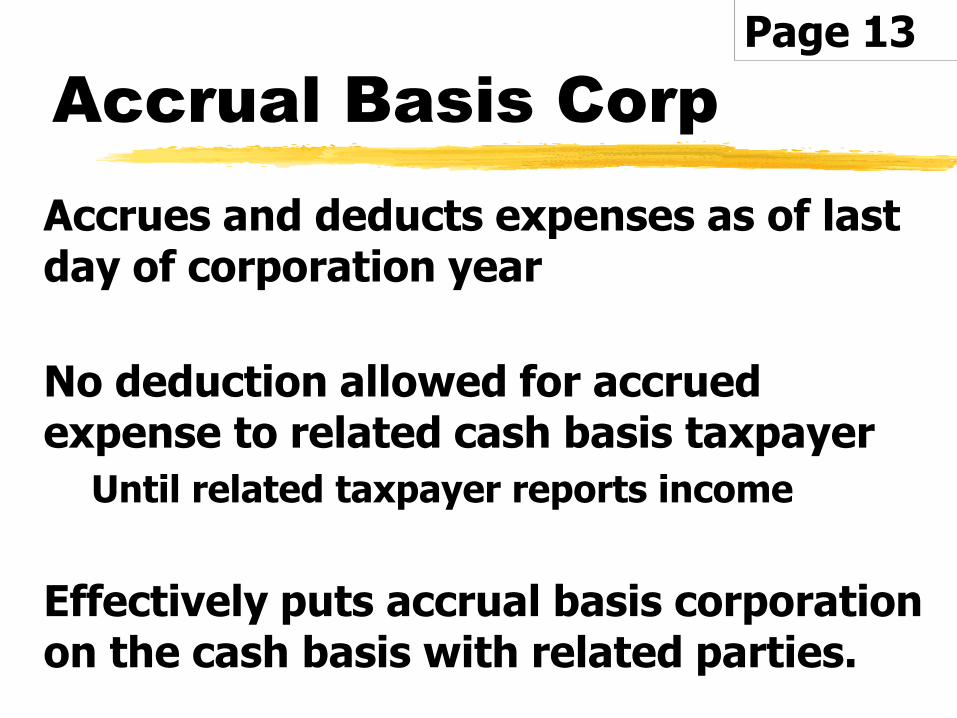

Accrual Basis Corp

Accrues and deducts expenses as of last day of corporation year

No deduction allowed for accrued expense to related cash basis taxpayer

Until related taxpayer reports income

Effectively puts accrual basis corporation on the cash basis with related parties.

Page 13

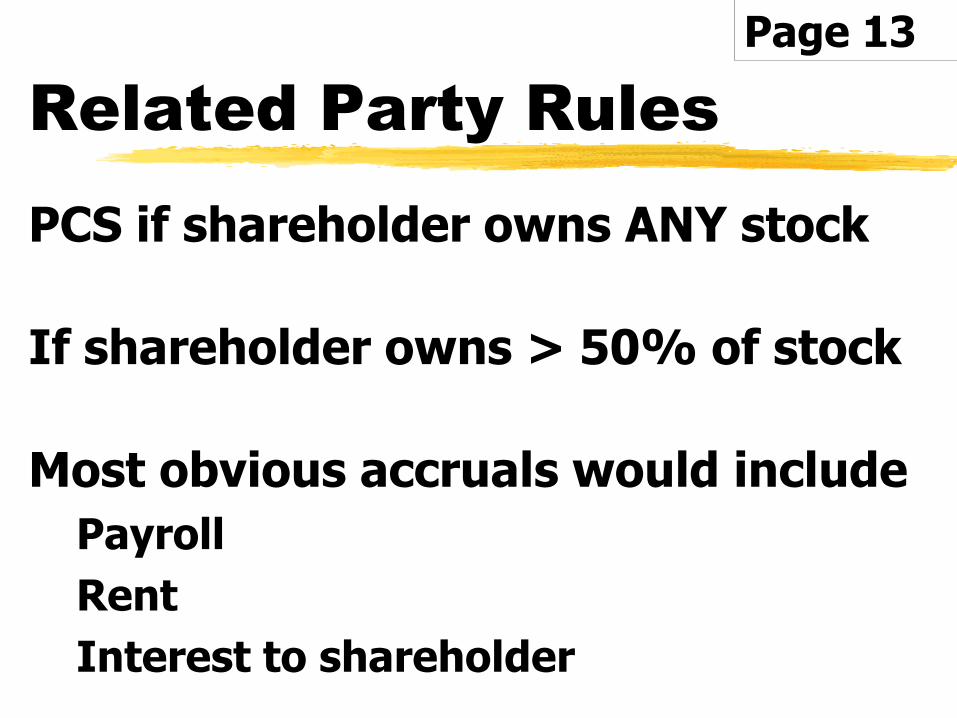

Related Party Rules

PCS if shareholder owns ANY stock

If shareholder owns > 50% of stock

Most obvious accruals would include

Payroll

Rent

Interest to shareholder

Page 13

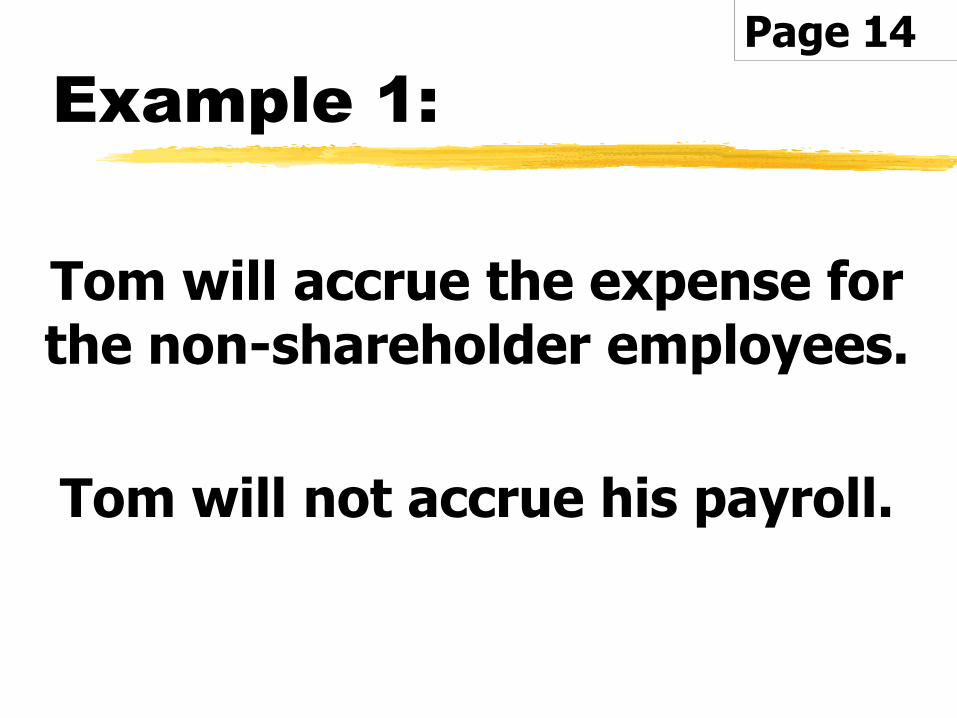

Example 1:

Tom owns 100% of ABC Inc.

Pays employees and himself every other week.

Year end pay period falls on the day after the Corporate year end.

Page 14

Example 1:

Tom will accrue the expense for the non-shareholder employees.

Tom will not accrue his payroll.

Page 14

Related Party Rules

Related parties are members of the same family.

Spouse, siblings, ancestors, and lineal descendants.

Page 14

Accrued Payment

Deadline

- Allowed if paid within 2-½ months of year end.

- For calendar year corporations - March 15.

Page 14

Accrued Payment

Deadline

Promissory notes, letters of credit and other evidence of

indebtedness are not considered payment.

Page 14

Office in Home

Corporation could:

Pay rent for the office space,

or

Reimburse the employee.

Page 15

Office in home

non-accountable plan

Taxable to shareholder

Deductible to corporation

Reported on Schedule E

No deductions allowed

Page 15

Office in home

Non-Accountable Plan

- Taxable to shareholder

- Deductible to corporation

Reported on Schedule E

No deductions allowed

Page 15

Example:

Sally is employee of ABC Inc

Operates an office in her home.

ABC Inc pays her $500 per month to rent that area in her home.

Page 15

Example:

Sally reports income on Schedule E.

However, she still may deduct qualified mortgage interest and RE taxes on her Schedule A.

Page 15

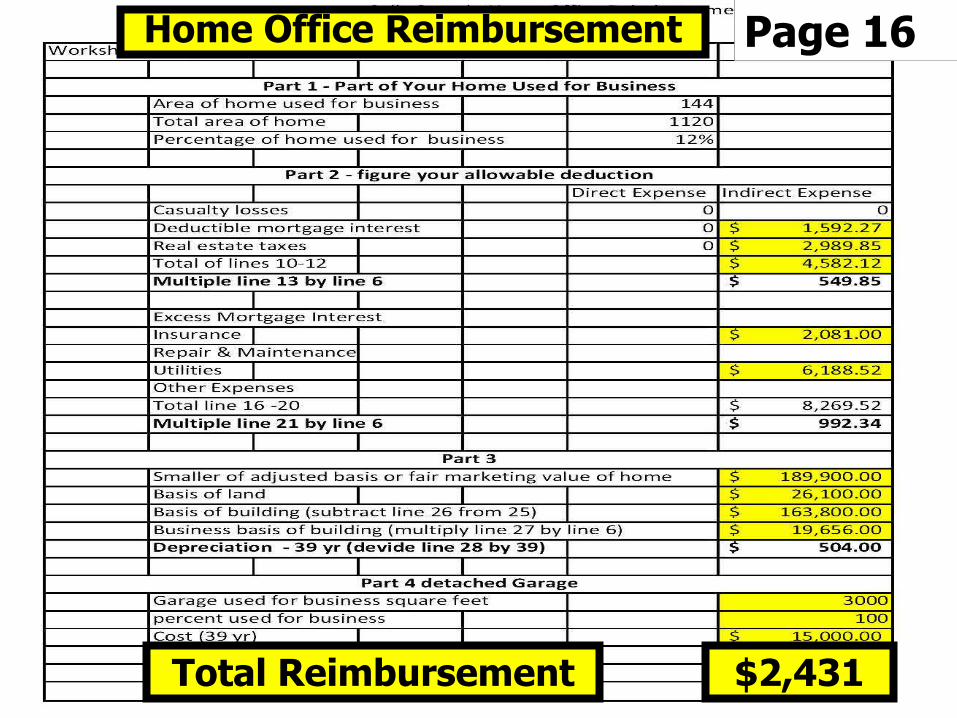

Office in home

Accountable Plan

Corporation could reimburse for a portion of the utilities, insurance,

repairs, mortgage interest, …

- Deductible by corporation

- Tax-free to taxpayer

Page 15

Page 16

Total Reimbursement

Home Office Reimbursement

$2,431

S Corporations

Page 17

S Corporation

Problem Areas

Net Income

Calculating basis

Shareholder compensation

Page 17

Note:

Basis calculations and shareholder compensation are obvious concerns for

preparer penalties.

Page 17

Filing Requirements

Required to file regardless of income.

If a corporation was an S corporation any time during the year – you must file Form 1120S

Due date is March 15th.

Page 17

Late Filing

For returns with no tax due

$210 per month for each shareholder during the year.

Page 17

Late Filing

For returns with tax due

Amount calculated above plus

5% of the unpaid tax for each month late up to 25%.

Page 17

Late Filing

The minimum penalty for a return that is > 60 days late is the smaller of tax due or $435.

Page 17

Note:

For a sole shareholder company filing a year late,

the penalty would be $2,520.

Page 17

Eligible S Shareholder

Individuals

Estate

Certain Trusts

(Example: Revocable Trust)

Page 17

Eligible S Shareholder

Not Allowed:

C Corporation

LLC

Partnership

Page 17

Grantor Trust

If the grantor dies the trust is allowed to continue for:

- 60 days, or

- Two years (if the assets of the trust are includable in the estate of the grantor).

Page 17

Testamentary Trust

If the stock is transferred by will.

The trust is allowed to continue for two years after the transfer.

Page 17

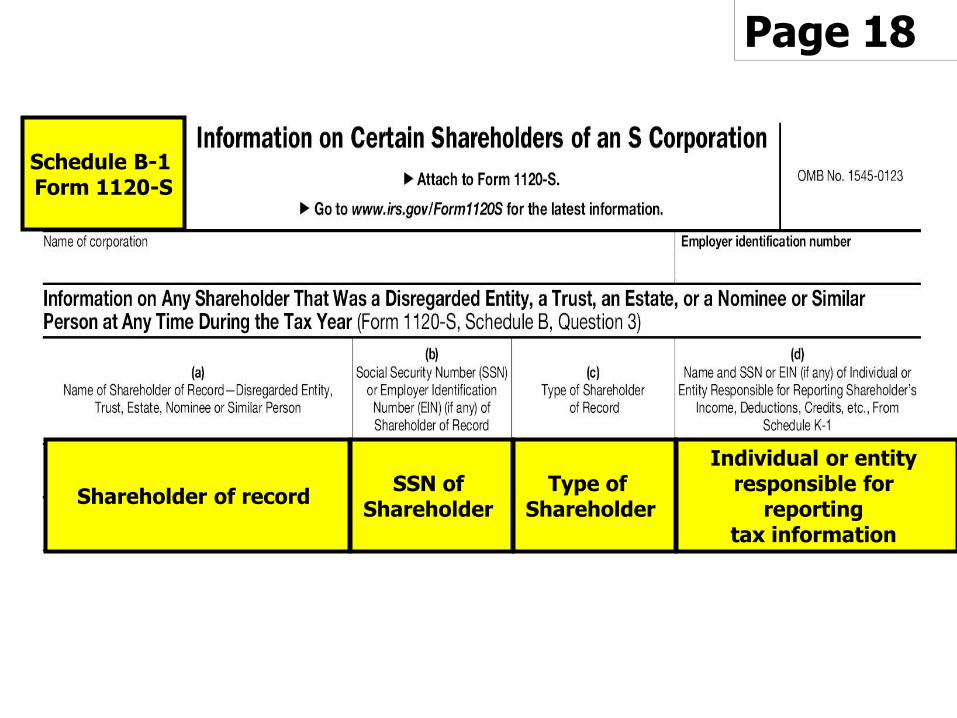

Schedule B-1

Must file for an S Corporation that has a disregarded entity,

trust, or an estate as a shareholder.

Page 18

Page 18

SSN of Shareholder

Type of Shareholder

Individual or entity responsible for

reporting tax information

Shareholder of record

Schedule B-1 Form 1120-S

Form 2553

Articles of Incorporation with Secretary of State

Form 2553

Filed within 2½ months

COORDINATE WITH THE ATTORNEY - WHO WILL FILE?

Page 18

Example 1:

ABC Inc began operations Jan. 6

2½ month period ends March 21.

No prior tax year, election cannot be made prior to January 6.

Page 18

Example 2:

ABC Inc has been filing Form 1120 for several years.

Form 2553 must be filed on or before March 15.

With prior tax year, election can be made any time in prior year.

Page 18

Note:

For a new S Corporate client

Request a copy of 2553 and/or acceptance letter.

Under audit, it will be one of the first items requested.

Page 18

Acceptance or

nonacceptance of Election

Acceptance letter will be sent from IRS within 60 days.

If you do not receive within two months call 1-800-829-4933.

Page 18

Note:

Consider sending Form 2553 certified mail.

IRS could require proof of filing.

Page 19

Caution:

Failure to be recognized as S Corporation problems arise.

Income/Loss is trapped in the

C Corporation.

Any distributions are treated as dividends creating double taxation.

Page 19

Waiver of Invalid S Election

IRS has authority to waive an invalid election and allow the S election to become effective if

certain conditions are met.

Page 19

Waiver of Invalid S Election

1. IRS determines circumstances resulting in the ineffective election were inadvertent.

2. Steps are taken within reasonable period to qualify as S corporation.

3. Corporation and all shareholders agree to IRS adjustments.

Page 19

Methods of

Obtaining Relief

1. Failure to obtain shareholder consents

S corporation can request extension to furnish shareholder consent

2. Relief under Rev Proc 2013-30

3. Request Letter Ruling

Fees do apply for letter rulings

Page 20

Rev. Proc. 2013-30

- Extends time to apply for relief to three years and 75 days.

- Relief is retroactive to intended date if IRS grants relief

- If denied, the taxpayer may still request a letter ruling.

Page 20

To qualify for relief

1. Intended to be classified an S corporation from the beginning.

2. Requests relief within three years and 75 days.

3. Failed to qualify solely for late

Form 2553.

4. Reasonable cause for its failure and acted timely to correct.

Page 20

Basis

Similar to a partnership

Income and/or losses flow through to shareholders

Shareholders pay income tax

Page 24

Unlike a Partnership

If S corporation incurs a loss, basis calculation does not include entity debt.

Loss deduction is more limited than a partnership.

Page 24

Basis Worksheet

Is required for a shareholder who:

- Reports a loss,

- Receives a distribution,

- Disposes of stock, or

- Receives a loan repayment from the S corporation.

Page 25

Page 25Form 1040 Schedule E

Page 2

(e) Check if basis computation

is required

Partnerships and S

Corps also differ

Substantial Economic Effect

Income allocation is:

- Available for a Partnership

- Not available for an S Corporation

Page 25

S Corporation Basis

Important for 3 reasons:

1. Deductible loss limitations

2. Gain/loss on sale of stock

3. Limits tax-free distributions

Page 25

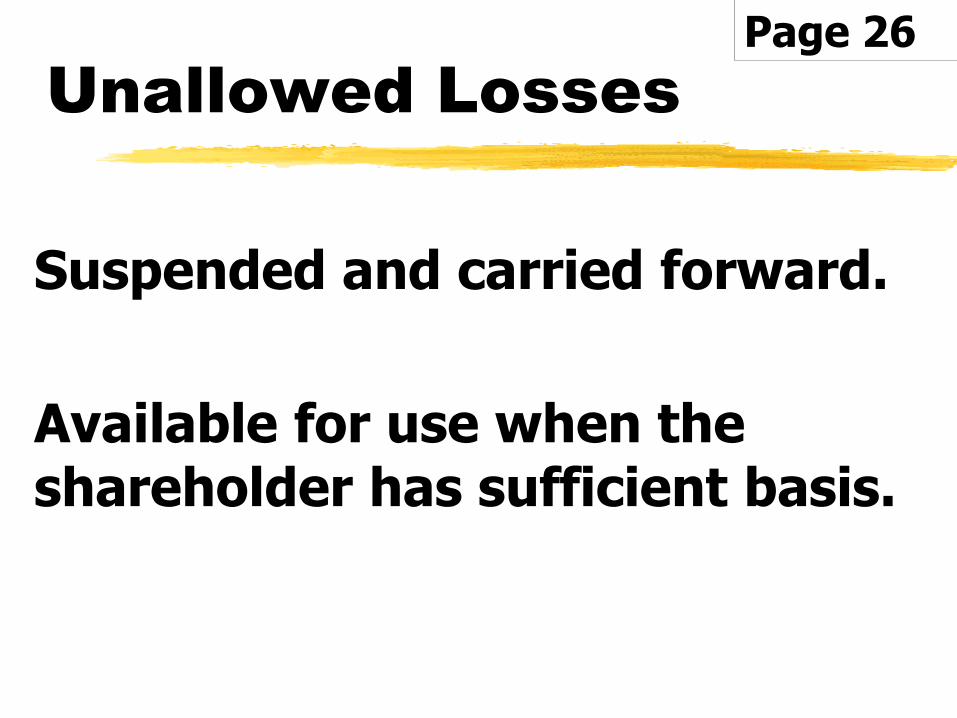

Unallowed Losses

Suspended and carried forward.

Available for use when the shareholder has sufficient basis.

Page 26

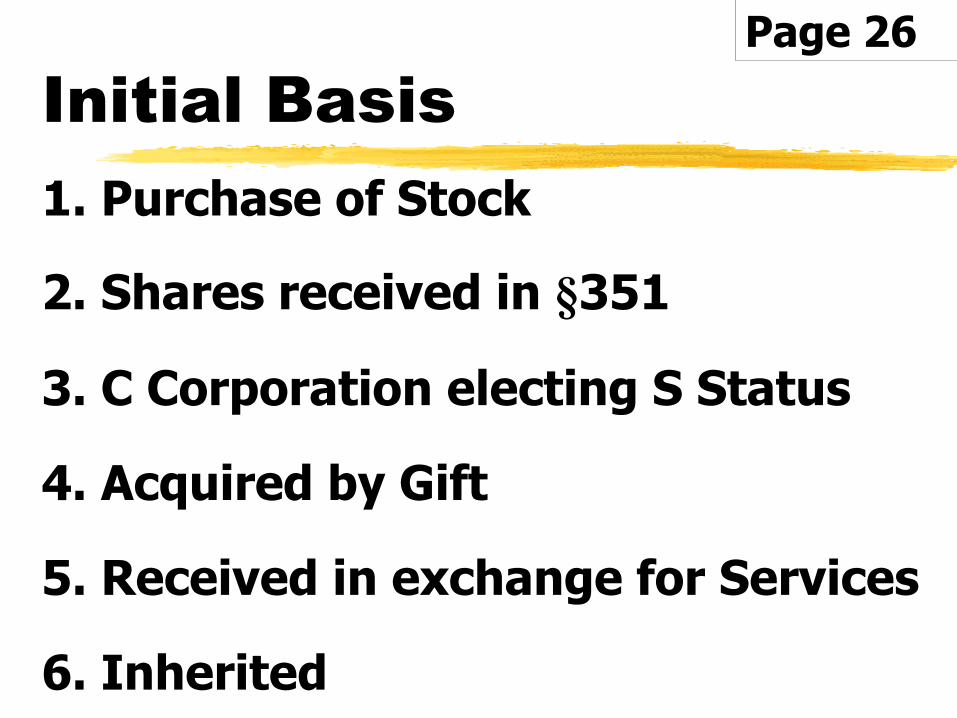

Initial Basis

1. Purchase of Stock

2. Shares received in §351

3. C Corporation electing S Status

4. Acquired by Gift

5. Received in exchange for Services

6. Inherited

Page 26

Basis Adjustments

Basis is:

1. Increased by share of income

2. Decreased by distributions and

3. Decreased by share of loss

Page 28

Example 1:

Tom & Jim each contribute $5,000 to form XYZ.

An S Corporation.

Initial basis is $5,000 each.

Page 29

Example 1: During 2020

Business profit of $100,000.

Each received distribution of $35,000.

Both have ending basis of $20,000.

[$5,000 + (50% of $100,000) – $35,000]

Page 29

Example 2:

Assume Instead

Beginning Basis of $5,000.

Business loss of $20,000.

Shareholder distribution of $10,000.

Corporation took a loan of $50,000.

Page 29

Example 2:

Tom’s Beg. Basis $5,000

Distribution of $10,000

Creates $5,000 of taxable income

Capital Gain

Page 29

Example 2:

$50,000 Corporate Loan

No effect on the shareholder’s basis.

Unlike a partnership.

Page 29

Example 2:

$50,000 Corporate Loan

Basis is only enhanced if the loan is directly between the corporation and the shareholder

Page 29

Example 2:

Tom’s share of the $20,000 loss.

Cannot be used until he has sufficient basis.

Loss will be carried forward.

Page 29

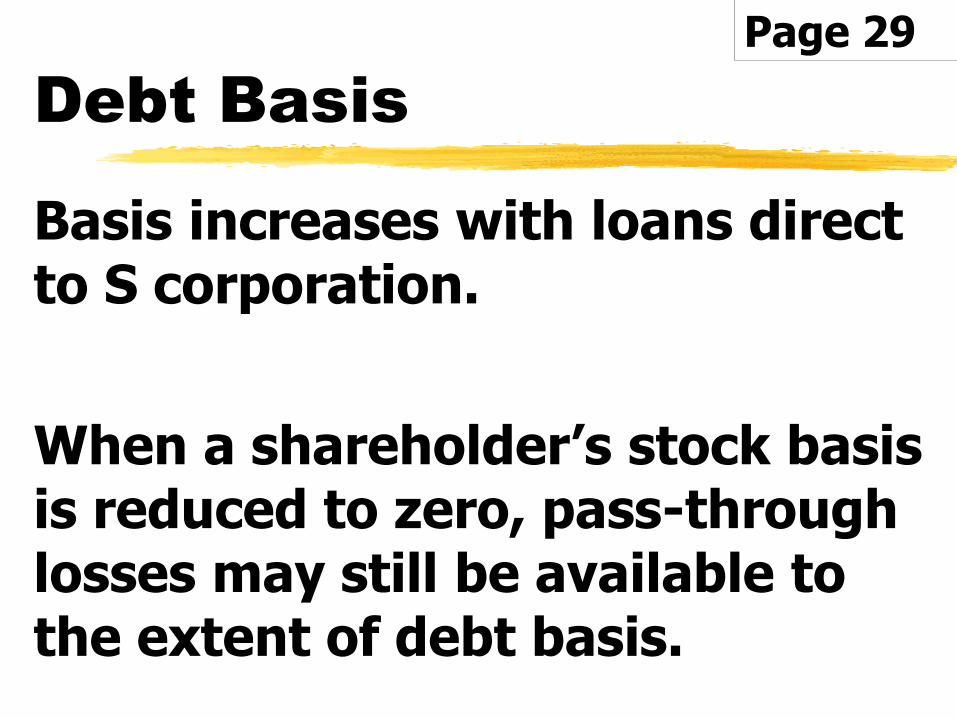

Debt Basis

Basis increases with loans direct to S corporation.

When a shareholder’s stock basis is reduced to zero, pass-through losses may still be available to the extent of debt basis.

Page 29

Example 1:

Tom contributes $5,000

Corp has loss of $10,000

Tom can deduct $5,000

The $5,000 loss is suspended until sufficient basis is restored.

Page 29

Example 2:

Assume the same facts as Example 1, except, Tom has a loan to the S Corp of $5,000.

His basis is increased by the debt.

He can now deduct the entire $10,000 loss.

Page 29

Shareholder loan

used to support loss

Repayment of loan can be taxable.

Will be taxed as:

LTCG if written note

Ordinary income if no written note

Page 30

Example:

Same as example 2 except

During 2020 XYZ

Had a loss of $5,000

Repaid the $5,000 loan to Tom

$5,000 loss is suspended for 2020.

Page 30

Example:

Loan repayment reduces

Tom has taxable income of $5,000.

Debt was not evidenced by written note, so he has $5,000 ordinary income for 2020.

Tom’s basis is now zero.

Page 30

Planning Tip 1:

If you anticipate a loss in the corporation.

You have limited basis, and

You anticipate large taxable income from other sources.

Consider lending money to corporation to increase basis & deduct loss.

Page 30

Planning Tip 2:

If you have suspended losses in corp

Anticipate large taxable income from other sources

Consider lending money to Corp

Suspended losses will be deductible

Page 30

S Corporation

Distributions

Distributions from earnings are generally not taxable.

Distribution that exceeds earnings

Return of Stock Basis, then

LTCG

Page 31

Example 1:

Beg. Stock Basis $30,000

Current year income 49,000

Distributions (45,000)

Basis before loss

And deduction items $34,000

Page 31

Example 1:

Basis before loss

and deduction items $34,000

LT Capital Loss Current (2,000)

Ending Basis $32,000

$45,000 distribution is not taxable.

Page 31

Example:

Beg. Stock Basis $30,000

Current year income 49,000

Distributions (90,000)

Basis before loss

And deduction items - 0 -

Page 32

Example:

Basis before loss

and deduction items $ - 0 -

LT Capital Loss Current ---------

Ending Basis $ - 0 -

Page 32

Example:

$90,000 distribution

- Not taxable to the extent of basis of $79,000.

- $11,000 is taxable LTCG.

$2,000 LT Capital Loss carries over.

Page 32

Page 32

ABC Inc. Distribution in excess of basis

Form 8949

Part II

11,000 11,000- 0 -

Disproportionate

Distributions

Distributions based on shares owned by each shareholder.

Disproportionate amounts create a second class of stock, terminating S corporation status.

Page 33

S Corporation

with C Corporation AE&P

Previous “C” Corporate Earnings

Distribution exceeds “S” earnings

What is the excess distribution?

Page 33

Previously a

C Corporation

1. Accum. Adjustments Account (AAA)

2. Dividends to the extent of E&P

3. Reduction of any remaining basis

4. Capital Gain

Page 33

Take Advantage

of lower tax brackets

Dividends are taxed as LTCG rates

(0% , 15%, or 20%)

Client Profile:

Shareholder in 12% bracket

Corporation has excess cash

Consider a dividend distribution

Page 33

Election to

Distribute AE&P First

Made with the consent of all shareholders.

A statement is made on a timely filed or AMENDED 1120S return.

Effective ONLY for year election made.

Page 34

Example:

XYZ Corp $20,000 AE & P

S Corporation

Has $20,000 AAA on books

Took a $10,000 distributions

In 12% marginal tax bracket

Page 34

Example:

He would get prior C Corporation earnings.

While paying no income taxes.

12% marginal = 0% Dividends

Page 34

Deemed Dividend

Distribution

Corporation has insufficient cash to distribute AE & P.

Corp may elect to make a deemed distribution.

Deemed to be made on the last day of the tax year.

Page 35

Example:

Same as above example except no distributions

Deemed electionReduces prior C earnings

No additional tax

Page 35

Page 35

Attach the election to a timely filed return.

Planning Tip:

Election can be made at tax preparation time for deemed distributions.

Page 35

Note:

1. Form 1099-DIV is required

2. Distributions of AE&P can help eliminate or reduce BIG tax or Net Investment Income Tax (NIIT).

Page 35

QBI Deduction

20% deduction for QBI, is potentially limited if the

business is a SSTB.

Page 36

RPE Reporting

A relevant pass-through entity (RPE) can include a:

Partnership,

S corporation,

Trust, or Estate.

Page 36

Schedule K-1 Reporting

RPEs are required to report:

- Whether the business is an SSTB.

- Whether there is more than one trade or business.

Page 37

Schedule K-1 Reporting

- QBI for each business.

- The W-2 wages and UB of qualified property.

- Any REIT dividends.

- Any PTP income.

Page 37

Note:

If the RPE fails to report the information on the

Schedule K-1, the amounts are presumed

to be zero.

Page 37

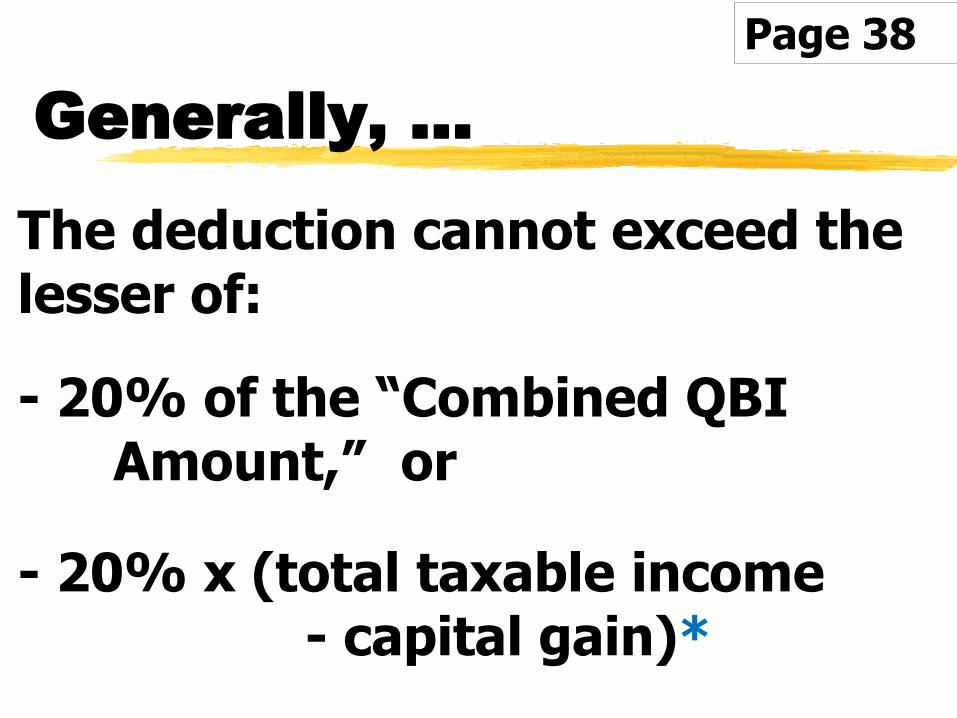

Generally, …

The deduction cannot exceed the lesser of:

- 20% of the “Combined QBI Amount,” or

- 20% x (total taxable income - capital gain)*

Page 38

Combined QBI amount

1. Is the sum of the deductible amounts for each qualified trade or business,

PLUS

2. REIT dividends and PTP income.

Page 38

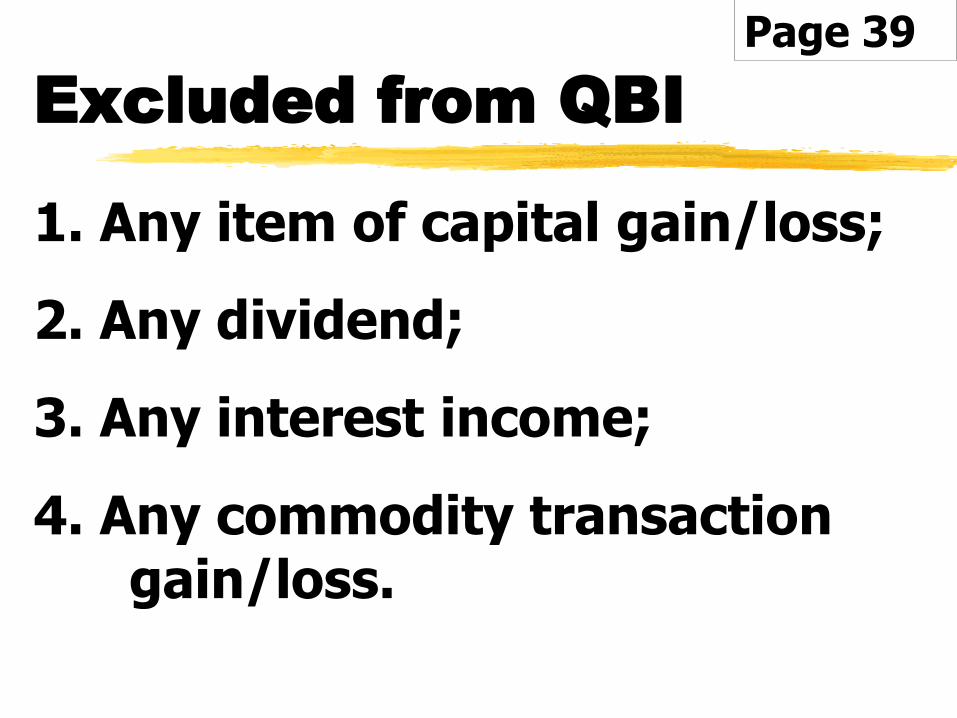

Excluded from QBI

1. Any item of capital gain/loss;

2. Any dividend;

3. Any interest income;

4. Any commodity transaction gain/loss.

Page 39

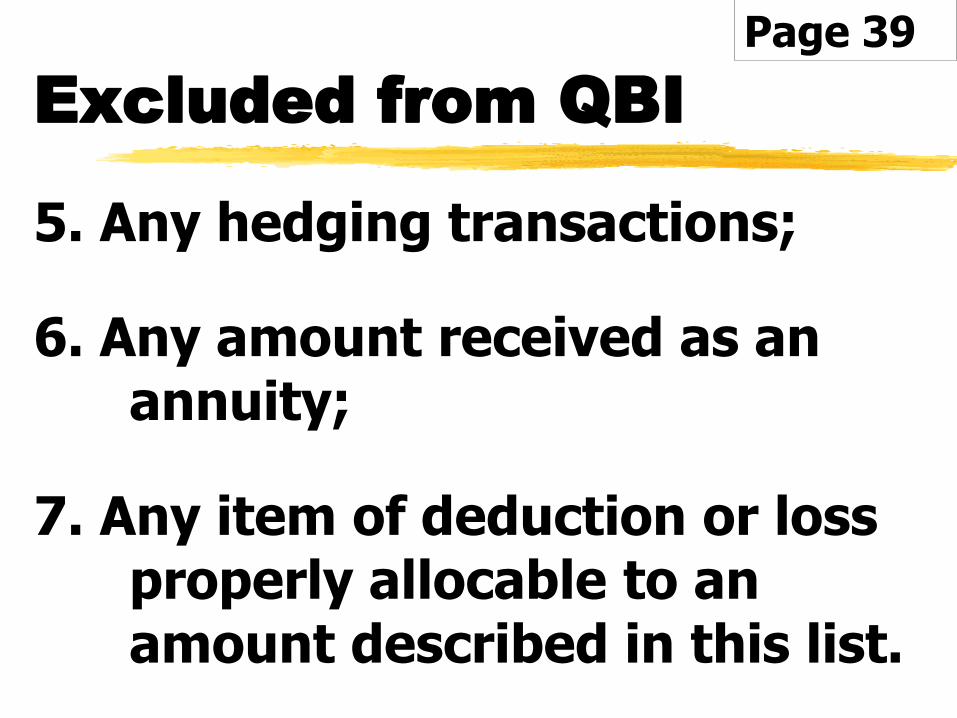

Excluded from QBI

5. Any hedging transactions;

6. Any amount received as an annuity;

7. Any item of deduction or loss properly allocable to an amount described in this list.

Page 39

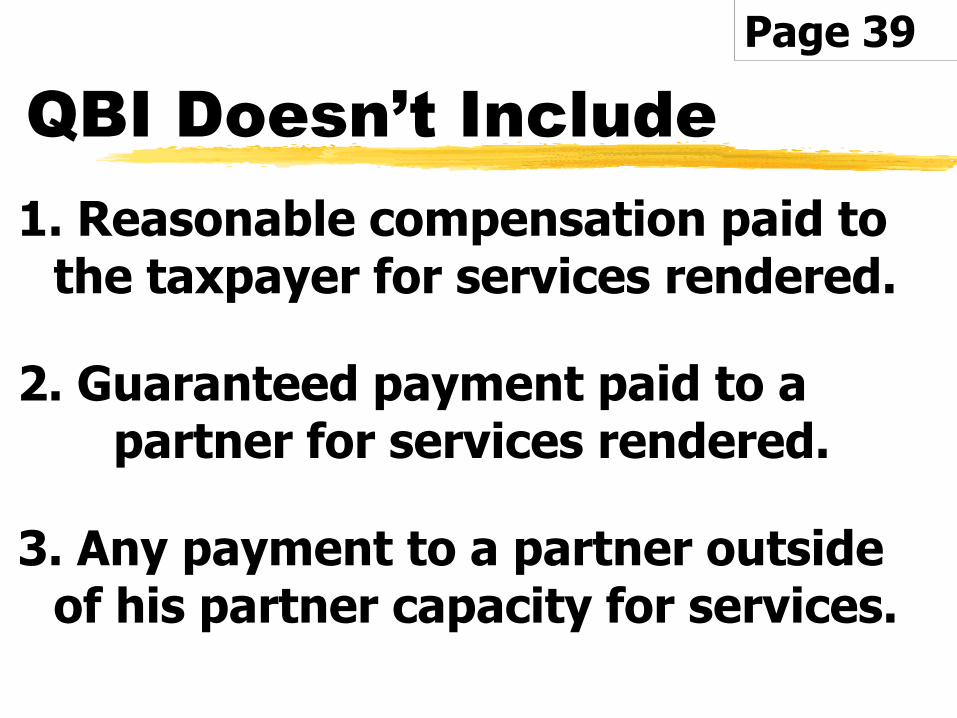

QBI Doesn’t Include

1. Reasonable compensation paid to the taxpayer for services rendered.

2. Guaranteed payment paid to a partner for services rendered.

3. Any payment to a partner outside of his partner capacity for services.

Page 39

Note:

IRS still expects reasonable compensation for the services

performed and work done.

Page 40

Example:

David is the sole shareholder an S corporation that is a

qualified trade or business.

Page 40

Example:

The business has net income in 2018 of $150,000 after

deducting his $80,000 salary.

Page 40

Example:

David received $80,000 as wages and $150,000 as distributions.

Page 40

Example:

Assume that reasonable compensation for someone with

David’s experience and responsibilities is $120,000.

Page 40

Example:

David’s QBI from the S corp. should be $110,000.

(not $150,000 as reported)

Page 40

Example:

The $40,000 adjustment for payments treated as

reasonable compensation is not QBI.

Page 40

Qualified Trade or

Business

Any trade or business other than a SSTB, or the trade or

business of performing services as an employee.

Page 40

Specified Service

Trade or Business (SSTB)

1. Any trade or business under IRC §1202(e) other than

engineering or architecture.

Page 41

Examples:

Health

Law

Accounting

Actuarial science

Performing arts

Consulting, athletics

Financial / Brokerage services

Page 41

Specified Service

Trade or Business (SSTB)

2. Any trade or business which involves performance of services that consist of investing and investment management, trading, or dealing in securities.

Page 41

Specified Service

Trade or Business (SSTB)

3. And any business where the principal asset of such trade or business is the reputation or skill of one or more of its

employees.

Page 41

Reputation or skill

1. Endorsing products or services.

2. Receiving fees, for the use of an individual’s image, name, or trademark.

Page 41

Reputation or skill

3. Receiving fees, compensation, or other income for appearing at an event or on radio, television, or another media format.

Page 41

Qualified Trade or

Business

However, a SSTB is treated as a qualified trade or business if taxable income is under:

$329,800 MFJ

Page 42

Thresholds and

Exclusions

When taxable income is above the threshold, the

deduction begins to phase-out for a SSTB.

Page 42

Lower Thresholds Upper Thresholds

2018 2021 2018 2021

MFJ $315,000 $329,800 $415,000 $429,800

HOH $157,500 $164,900 $207,500 $214,900

SINGLE $157,500 $164,900 $207,500 $214,900

MFS $157,500 $164,925 $207,500 $214,925

2021 Taxable Income Thresholds

Page 42

Payroll or S Distribution

S income is not SE Income

Distributed or

Not Distributed

Can lead to abuse

Page 43

Reasonable Compensation

IRS has issued no guidance on

“Reasonable Compensation”

However, the IRS can reclassify distributions as wages.

Page 43

Reasonable Compensation

1. Employee Qualifications.

2. Nature, Extent and Scope of Work.

3. Industry Compensation Rates.

4. Size and Complexity of Business.

5. Compensation to non shareholder employees.

Page 43

Note:

Reasonable compensation vs. distribution analysis must look at multiple years.

Not just a single tax year.

Page 43

Potential Problems

- Payroll taxes issues including penalties and interest,

- Insufficient SS contributions

- Could reduce the §199A (QBI)

deduction

Page 43

Watson vs. US

February 2012

Took wages 2002 & 2003 of $24,000

Took distributions

2002 $203,981

2003 $175,470

Court ruled $91,044 was reasonable.

Page 45

Following Factors

1. Accountant with advance degrees

2. 35-40 Hours P/W – Primary earner

3. Earnings over $2 Million (per year)

4. $24,000 unreasonable low versus other accountants at firm

5. Financial position of the company

Page 45

Reasonable Compensation

Simple Solution

What would you pay someone else to do the same job?

Page 48

Industry Compensation

You could hire a consulting firm or go to:

www.salary.com

or

www.bls.gov

or

www.salaryexpert.com

Page 48

Family Members

If family members perform services and do not receive reasonable compensation.

IRS may also recharacterize S Distributions as wages.

Page 49

Items Other than

S Distributions

A loan to shareholder/employee from the corporation could also be an issue.

Re-characterization of the loan payments is possible.

Page 50

Items Other than

S Distributions

In one case an S Corporation entered into an agreement for no distributions and no payroll.

All payments were classified as loans.

Page 50

Items Other than

S Distributions

Based on the following:

- The loans were unsecured demand notes bearing no interest,

- They did not specify repayment terms,

- The shareholder regularly performed substantial services for the Corporation.

Page 50

Note:

Loans from an S Corporation to shareholder/employees should be

properly documented and a reasonable rate of interest paid.

Page 50

Corporate Minutes

We recommend reasonable compensation be reviewed

annually and addressed within the corporate minutes.

Page 51

S Corporation

Health Insurance

Premiums paid on behalf of more-than-2% shareholder-employees are reported as additional compensation.

Page 53

> 2% S shareholder -employees are reported as additional compensation.

Subject to FITW

But not FICA, and Medicare.

S Corporations

Nondiscriminatory

Page 53

Note: 2% Shareholder

Family attribution rules also apply for the spouse,

children, grandchildren, and/or parents.

Page 53

> 2% S shareholder -employees are reported as additional compensation.

Subject to FITW

and FICA, and Medicare.

S Corporation

Discrimination

Page 53

To claim the deduction, the health insurance plan must

be established under the taxpayer's business.

SE Health

Insurance Deduction

Page 54

If the taxpayer is:

A 2%-or-more S corporation shareholder, the policy can be either in the taxpayer's or the S corporation's name.

SE Health

Insurance Deduction

Page 54

To be deductible:

- The shareholder can pay the premiums directly and be reimbursed by the corporation, or

- The S corporation can pay the premiums.

Notice 2008-1 Page 54

Passive

Investment Rules

If a C Corporation switches to an S Corporation, it may

be subject to a tax on excess net passive income.

Page 55

Excess Net

Passive Income

1) C corporation AE & P,

AND

2) Passive investment income more than 25% of gross receipts.

Page 55

Calculated as follows:

“A” “B”

Excess of Net Income = Net Passive X Passive Investment Income

Passive Income Income in Excess of 25% of Gross Receipts

Passive Investment Income

“C”

Page 55

Example 1:

Wild Widget has S Corp status

Has prior “C” E& P

Gross Receipts $8,000

Gross passive income 4,000

Allowable deductions 1,000

Page 56

Example 1:

A = $4,000 - $1,000 = $3,000

B requires two steps

Find 25% of Gross Receipts $8,000 x 25% = $2,000

$4,000 - $2,000 (from above) = $2,000

C = $4,000

Page 56

Example 1:

A B

$3,000 X $2,000 = $1,500

$4,000

C

The excess net passive income tax would be $315 ($1,500 x 21%).

Page 56

Excess Net Passive

Income 3 Consecutive Yrs

S election will terminate if:

Have AE&P

AND

Gross passive investment income exceeds 25% of gross receipts in each of 3 consecutive years.

Page 56

Note:

An election to treat distributions as “C” dividends may avoid the

excess net passive income rules.

Page 56

Taxable Income

Limitation

No tax is imposed if the corporation's taxable income for the year is zero.

Page 57

Example 2:

Assume the same facts as in Example 1, except that Wild

Widget has business expenses of $7,500.

Page 57

Example 2:

Wild Widget's taxable income for the year is $500 ($8,000 - $7,500).

The excess net passive income for the current year is limited to $500.

Page 57

Example 2:

Thus, the excess net passive income tax would be $105.

($500 x 21%)

Page 57

Tax-Exempt

Interest Income

Is included in passive investment income for purposes of the tax on excess net passive income.

Page 57

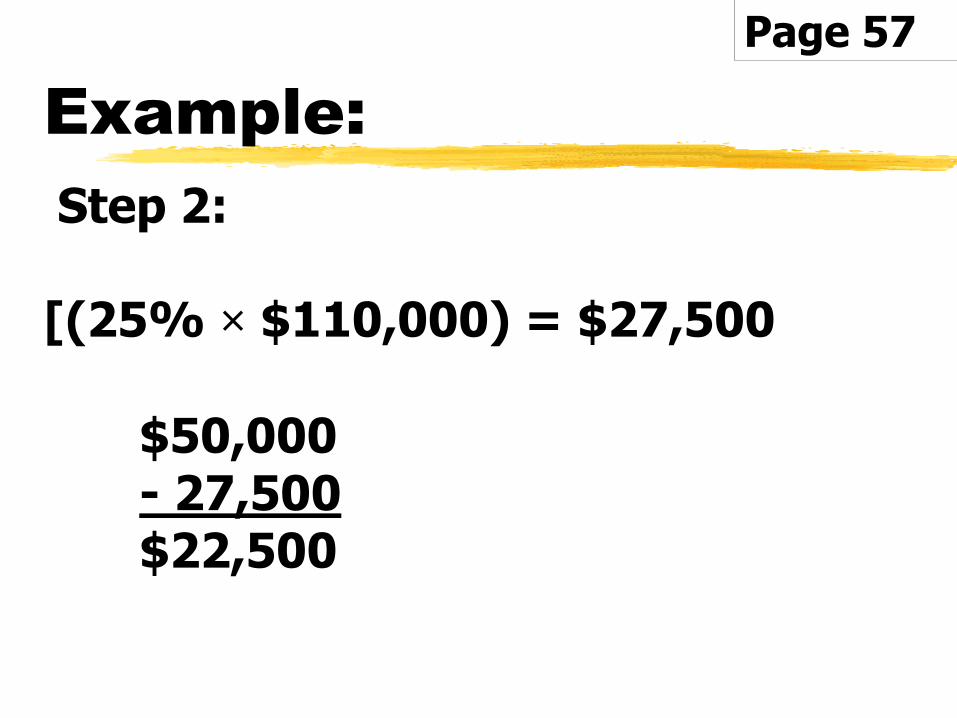

Example: S Corporation

Gross incomefrom operations $60,000

Operating expenses (20,000)

Tax-exempt interest 50,000

Page 57

Example:

ABC's gross receipts equal $110,000 ($60,000 + $50,000).

Passive investment income and net passive income are $50,000.

ABC's net income (computed as if it were a C corporation) is $40,000.

Page 57

Example:

Step 2:

[(25% × $110,000) = $27,500

$50,000- 27,500$22,500

Page 57

Example:

A B

$50,000 X $22,500 = $22,500

$50,000

C

The excess net passive income tax would be $4,725 ($22,500 x 21%).

Page 57

Built-in-Gains (BIG) Tax

Before electing S Status from C Corp

Consider potential of BIG Tax

Applies if:

1. Was a C Corporation and

2. Made election after 1986

Page 58

Recognition Period

S Corporations recognition period limited to 5 years.

Beginning with the date the S election becomes effective.

Page 58

Concept …

To prevent C Corporations from avoiding taxes.

Taxed at flat 21%

Gain applies to asset gain as if sold on date of S Election.

Page 58

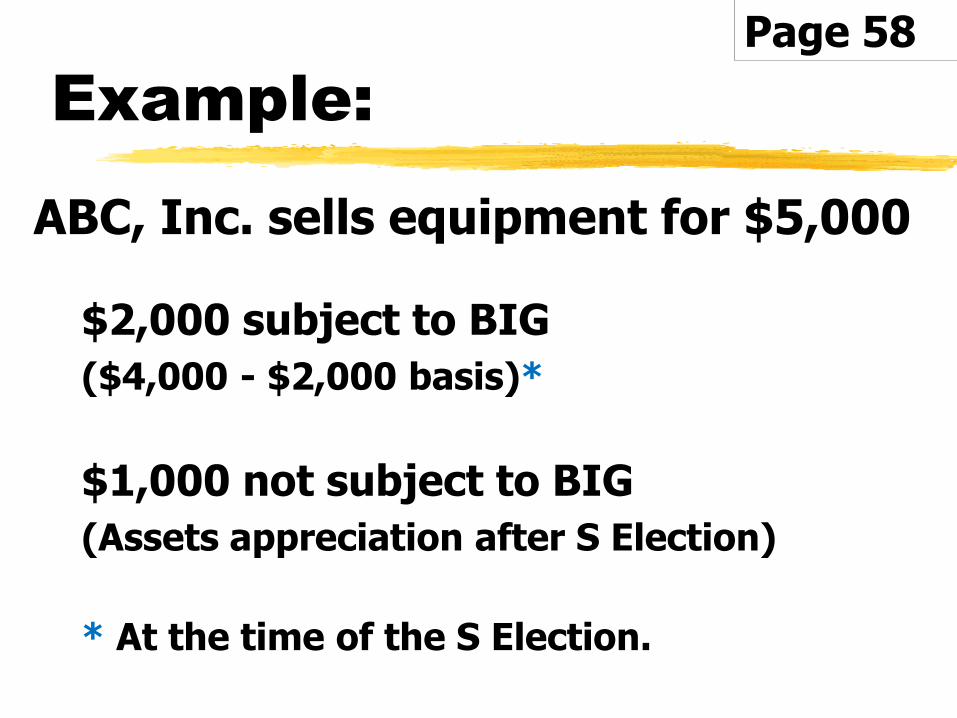

Example:

ABC, Inc. had equipment FMV $4,000 basis of $2,000 at time of the S Election.

If sold within 5 years – the gain is subject to BIG tax.

Page 58

Example:

ABC, Inc. sells equipment for $5,000

$2,000 subject to BIG

($4,000 - $2,000 basis)*

$1,000 not subject to BIG

(Assets appreciation after S Election)

* At the time of the S Election.

Page 58

Accounts Receivable

Cash Basis C Corporations

AR not taxed subject to BIG tax

AP allowed as deduction against AR

Page 58

Example 1:

ABC Inc has AR $50,000

ABC Inc has AP $40,000

BIG tax applicable on $10,000

Page 58

Planning Tip:

Collect as much accounts receivable as you can prior to making election.

Maybe offer discount for early payment

10% is less than 21% BIG tax

Page 59

Deduction for BIG tax

S Corporation pays income tax at 21% for any BIG income.

Income flows to shareholder and taxed at shareholder level.

Page 59

Deduction for BIG tax

However, the shareholder does receive a deduction for the amount of the BIG tax.

Page 59

Example:

ABC Inc sold equipment with gain of $10,000 subject to BIG tax

BIG tax $2,100 ($10,000 x 21%)

Page 59

Example:

Shareholder reports income from the gain in the amount of $7,900.

($10,000 gain – $2,100 BIG Tax)

Page 59

BIG Tax Overall Limit

Limited to gain on assets as if sold attime of S election

FMV *– basis = Potential BIG

*At the time of the S Election.

Page 59

Gain would be taxed in two stages:

1. Potential gain at the time of the

S corporation election, and

2. Gain from date of the S election to the date of the asset sale.

Assets likely to

appreciate in value

Page 59

1) Tax-deferred exchange does not trigger built- in gain in that asset.

(§1031 is only eligible for real property)

2) Deferred if S Corporation has loss

(Deferred only until it has profit)

3) C Corporation NOL

Avoiding the BIG Tax

Page 60

S Corporation

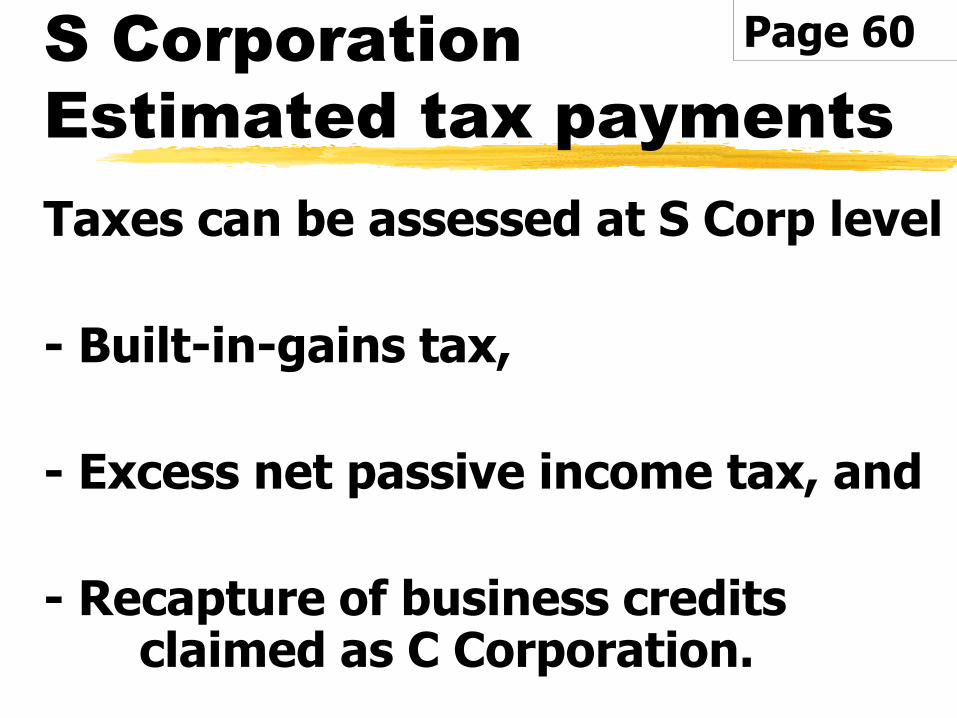

Estimated tax payments

Taxes can be assessed at S Corp level

- Built-in-gains tax,

- Excess net passive income tax, and

- Recapture of business credits claimed as C Corporation.

Page 60

S Corporation

Estimated tax payments

S Corporation required to make estimated tax payments if:

- The corporation subject to one or more of the taxes, and

- The total taxes for the year are more than $500.

Page 60

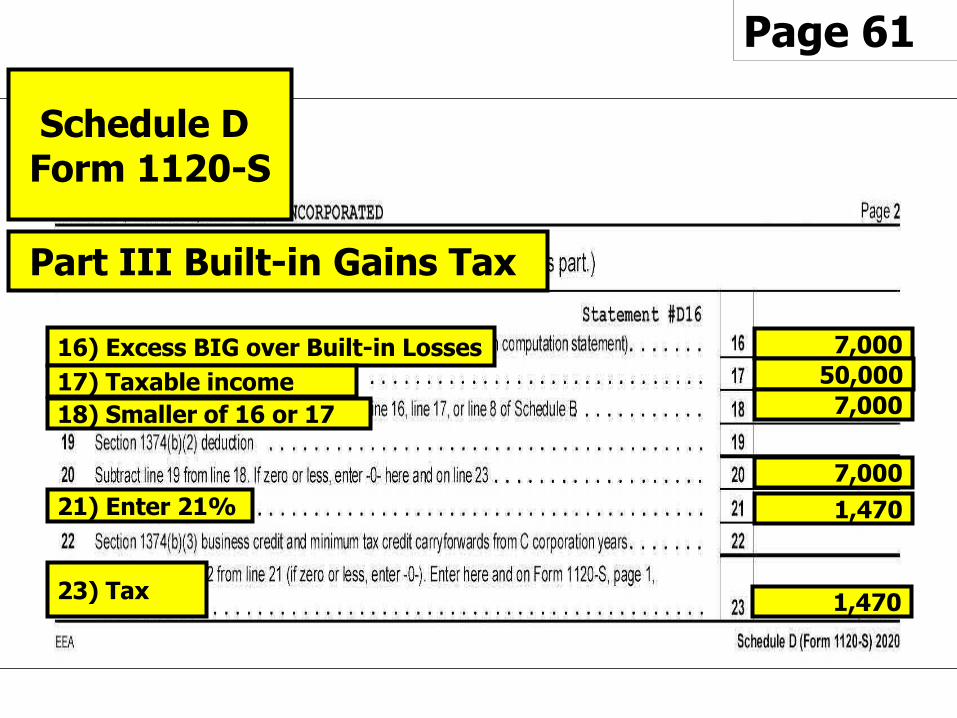

Example: BIG Tax

XYZ Purchased Equipment for $10,000

S Election on 1/16

Adj. Basis on 1/16 was zero.

Page 60

Example: BIG TAX

May 11, 2020

Sold Equipment for $7,000

BIG Tax = $1,470 ($7,000 x 21%)

Page 60

Page 61

Form 4797

Page 2

7,000

- 0 -

7,00024) Total gain

23) Adjusted basis

20) Gross sales price

Equipment

Page 61

7,000

50,000

7,000

7,000

1,470

1,47023) Tax

21) Enter 21%

Schedule D Form 1120-S

Part III Built-in Gains Tax

16) Excess BIG over Built-in Losses

17) Taxable income

18) Smaller of 16 or 17

Page 62

Form 1120-S

1,470

12) Taxes 1,470

22b) Tax from Sch. D

Page 63

1120S Income $50,000

BIG Tax - $1,470

1120S K-1= $48,530

1) 48,530

Schedule K-1 Form 1120-S

Page 64

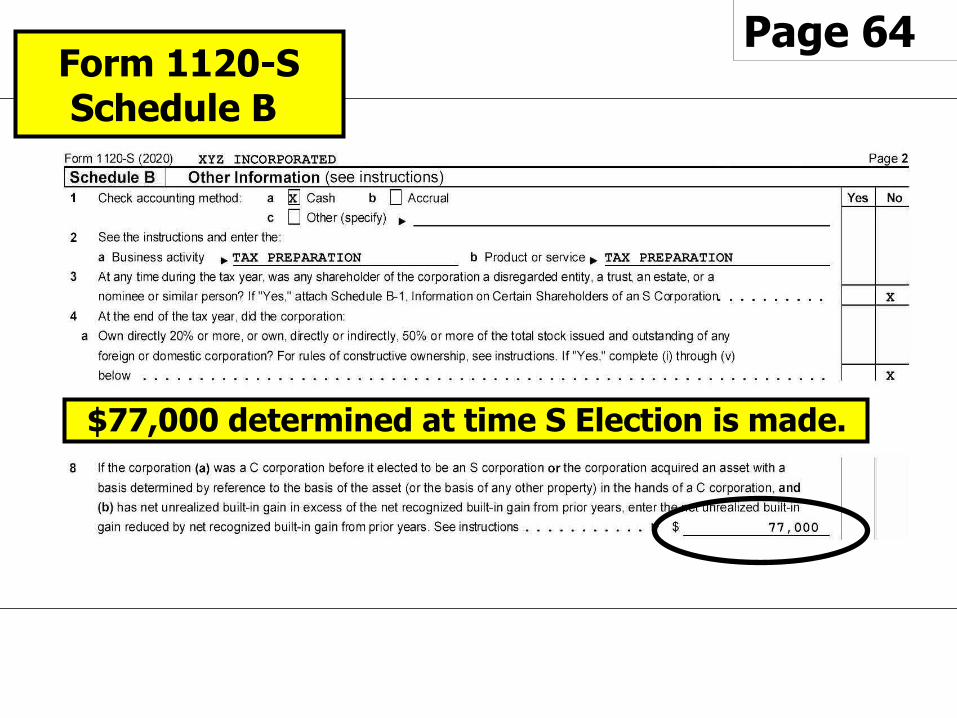

$77,000 determined at time S Election is made.

Form 1120-SSchedule B

Termination of S Status

S reverts to C status:

1. Violates Passive Income Rules

2. Fails to qualify as S Corp

3. Shareholders Revoke Election

Page 65

S Corp Election Revocation

Consent of more than 50%

Made on or before 15th day of 3rd

month of taxable year effective.

Page 65

Revocation

Made after the 15th day of 3rd month effective the following year.

Can be made with specific date.

No IRS form for revocation

Two statements requiredOne from Corporation

One from Shareholders

Page 65

Waiting Period

For S status to be reinstated

A 5-year period unless

they receive IRS consent

Page 66

S Corp. Liquidations

Page 67

S Corporation

Liquidations

Reasons to liquidate:

- Cease business activity

- Corporate Sale

Page 67

Cease Business Activity

File inactive return

Any distributions treated as dividends

Liquidate corporation

Distribute cash and/or assets

Treat as dividends

Page 67

Corporate Sale

Can occur as either

Stock sale or

Equipment/asset sale

Completely different results

Page 67

Stock Sale

Taxed on difference between sales price and stock basis.

Page 67

Stock Sale

Two Major Issues:

- Buyer also buys all current and potential liabilities.

- Assets receive no basis adjustment for depreciation purposes.

Page 67

§1202 Exclusion

Stock held for > 5 years

Stock acquired before 2/18/09

50% exclusion Remaining 50% @ 24% rate

Stock acquired after 2/18/09 and before 9/28/10

75% exclusion

Page 67

§1202 Exclusion

Stock held for > 5 years

Stock acquired after 9/27/2010 and before 1/1/2011

100% exclusion

AMT eliminated as preference item

The 2015 PATH Act

(permanent change)

Page 67

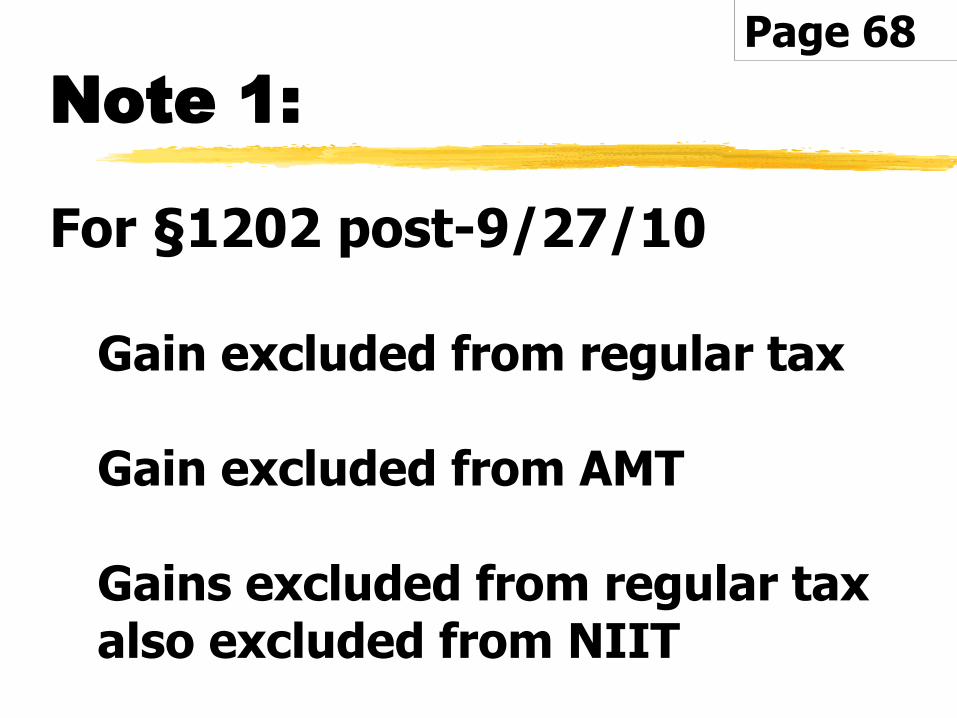

Note 1:

For §1202 post-9/27/10

Gain excluded from regular tax

Gain excluded from AMT

Gains excluded from regular tax also excluded from NIIT

Page 68

Note 2:

Gain eligible for exclusion cannot exceed the greater of:

1. $10 million reduced by taxpayer’s total prior year gains of same stock.

2. 10 times taxpayer’s basis in QSBS from corporation disposed during year.

Page 68

§1045 Rollover of Gain

- Stock must have been held more than 6 months.

- Proceeds from the sale must be used to purchase another qualified small business stock within 60 days of the sale.

Page 68

Example:

Oct. 1, 2019: Purch $300,000 of QSBS

Sept. 1, 2020: Sold for $500,000 ($200,000 Gain)

Sept. 1, 2020: Purch QSBS for $450,000

What’s the tax result?

Page 69

Example:

Proceeds from Sale: $500,000

Proceeds Applied (450,000)

Gain Recognized $50,000

Page 69

Purchase Price

New Stock $450,000

Deferred Gain ( 150,000)

Basis in New Stock $300,000

Page 69

Example:

Assets distributed

NOT Part of Liquidation

Not part of complete liquidation.

Tax treatment considerably different.

Page 71

S Corporation

Similar to a C Corporation, an asset distribution is a taxable event.

Unlike a C Corporation, gain flows through to shareholder.

Avoids one layer of tax

Page 71

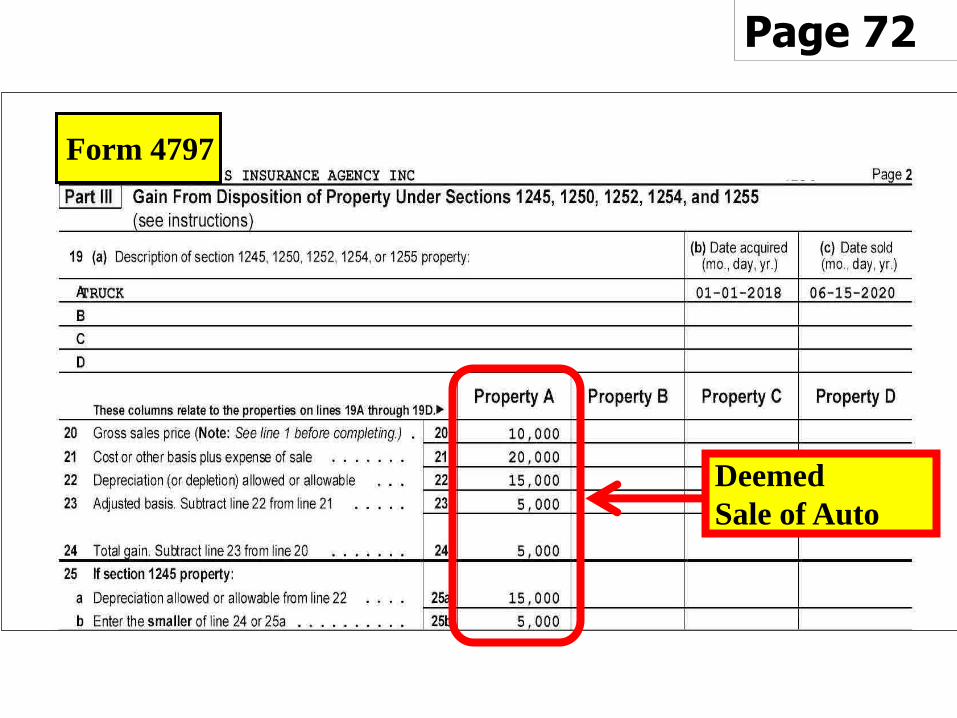

Example:

Sam distributes company auto to himself

Original Cost $20,000

Depreciation $15,000

FMV $10,000

Page 71

Example:

Corporation reports a gain of $5,000

Gain flows thru to shareholder

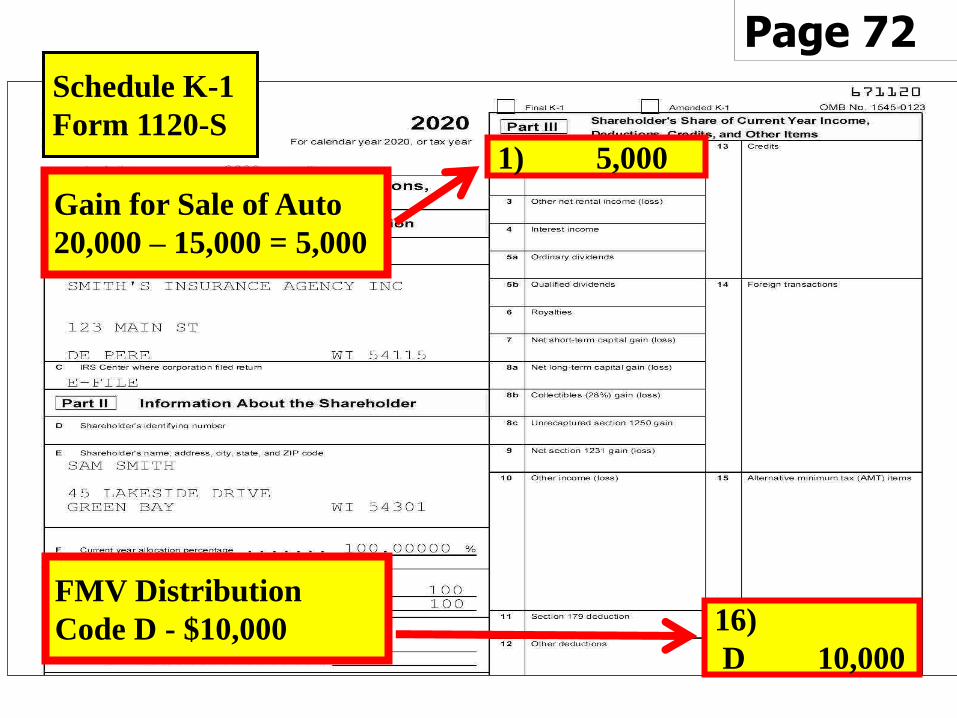

See Page 72

Page 2 – 4797 Gain on asset

Schedule K-1 Income - Line 1 $5,000

Schedule K-1 Distribution - Line 16 $10,000

Page 71

Page 72

Deemed

Sale of Auto

Form 4797

Page 72

FMV Distribution

Code D - $10,000

Gain for Sale of Auto

20,000 – 15,000 = 5,000

Schedule K-1

Form 1120-S 1) 5,000

16)

D 10,000

Assets distributed

NOT Part of Liquidation

If there is a loss:

- The loss is not allowed under the related party rules.

- If the shareholder later recognizes a gain, cannot reduce gain.

Page 73

Example:

Sam distributes auto to himself

Original Cost $20,000

Depreciation $10,000

FMV $5,000

Page 73

Example:

No gain or loss to the corporation.

Within a year Sam sells for $10,000.

Sam will report STCG of $5,000.

He cannot reduce the gain by the previously disallowed loss.

Page 73

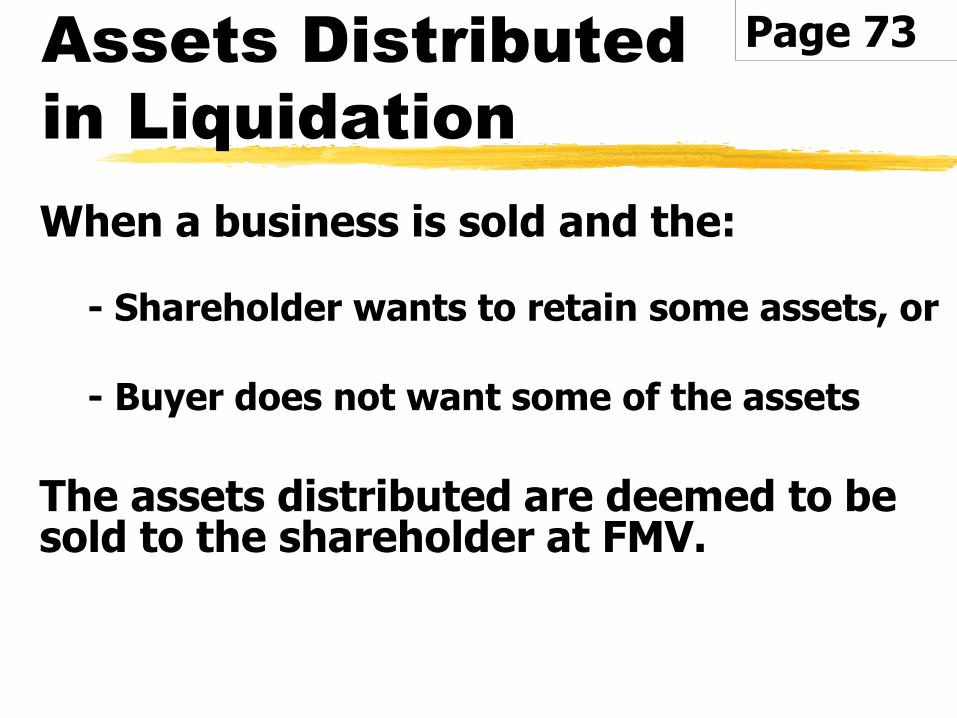

Assets Distributed

in Liquidation

When a business is sold and the:

- Shareholder wants to retain some assets, or

- Buyer does not want some of the assets

The assets distributed are deemed to be sold to the shareholder at FMV.

Page 73

Example:

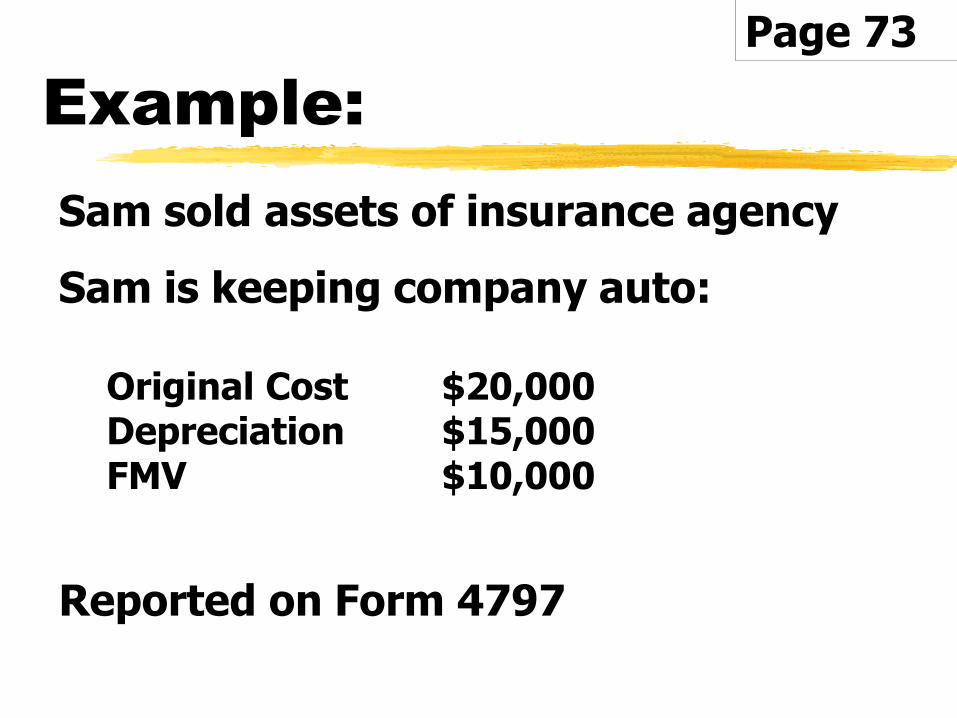

Sam sold assets of insurance agency

Sam is keeping company auto:

Original Cost $20,000Depreciation $15,000FMV $10,000

Reported on Form 4797

Page 73

Loss in an

Asset Distributed

Not a complete liquidation:

- Under the related party rules, the loss is not deductible.

Page 74

Loss in an

Asset Distributed

Under a complete liquidation:

The loss may be deductible if:

- The property distributions are prorata to all shareholders, and

- The property was not acquired in a §351 transaction or as a contribution of capital within the last five-years.

Page 74

Due Diligence Tip:

Have the owner get a statement regarding the FMV of the assets.

Page 74

Liability Exceeds

FMV of Distribution

If the liability exceeds the FMV of property distributed, the amount of the liability is the deemed FMV for selling price.

Page 74

Example:

Sam distributes auto from insurance agency to himself as part of complete liquidation.

Auto has basis of $5,000Auto has FMV of $10,000Auto has loan of $15,000

Deemed sales price = $15,000

Corporate recognizes gain $10,000($15,000 debt – $5,000 basis)

Page 74

Previously

Expensed Items

Part of distributions may include items that have been expensed

Tools & Supplies

Recognition of income at FMV

Page 75

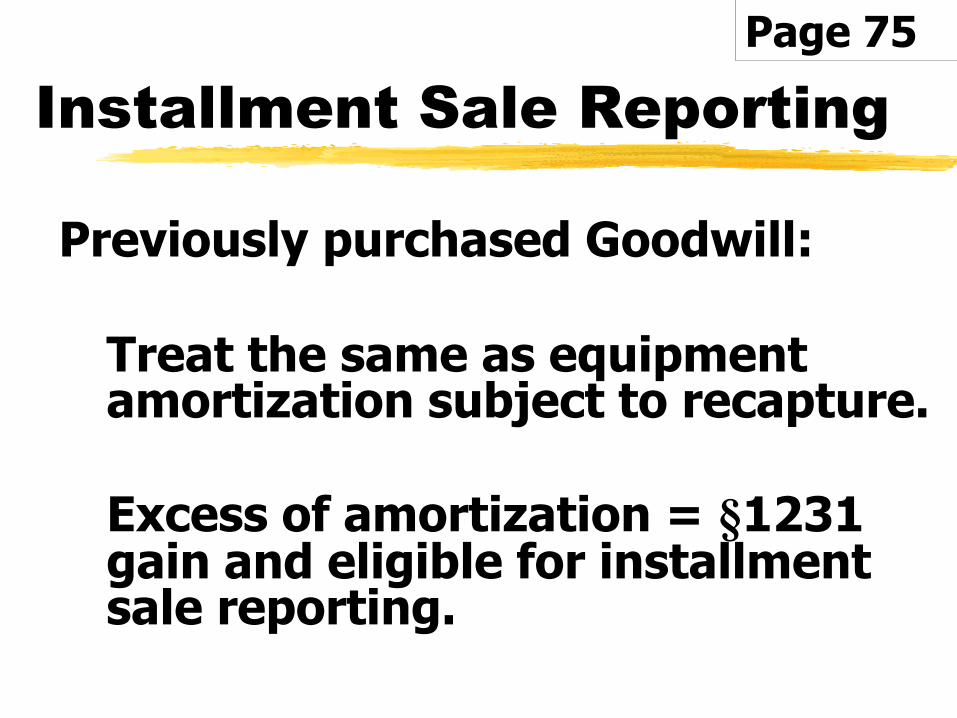

Installment Sale Reporting

Equipment:

Any depreciation is taxed as ordinary income and taxed at time of sale.

Any §1231 gain eligible for installment sale.

Page 75

Installment Sale Reporting

Building:

Entire sale qualifies for installment sale.

Depreciation unrecapture max 25% first then max 20% LTCG rate.

Page 75

Installment Sale Reporting

Land:

Entire sale qualifies for installment sale

Taxed as LTCG

Page 75

Installment Sale Reporting

Previously purchased Goodwill:

Treat the same as equipment amortization subject to recapture.

Excess of amortization = §1231 gain and eligible for installment sale reporting.

Page 75

Installment Sale Reporting

Previously purchased Covenant:

Treat the same as equipment amortization subject to recapture.

Excess of amortization = §1231 gain and eligible for installment sale reporting.

Page 75

Goodwill

Corporation Created

Sale of a capital asset

Eligible for installment sale

Page 76

Note:

Covenant not to compete:

Should be between shareholder and the buyer

If inadvertently tied to corporate sale taxed immediately upon distribution to the shareholder.

Page 76

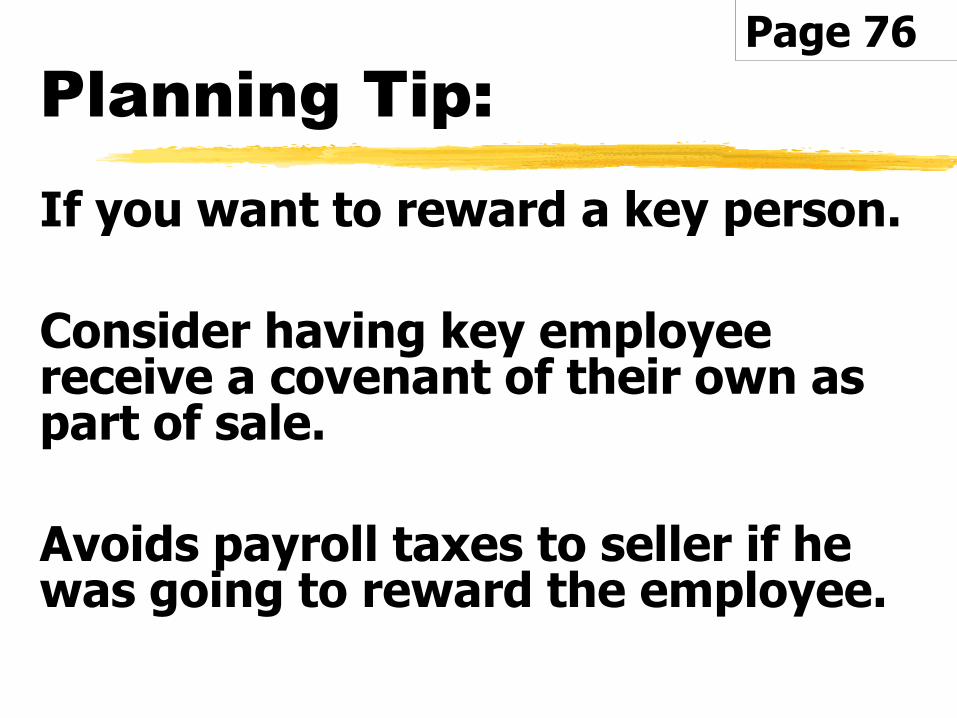

Planning Tip:

If you want to reward a key person.

Consider having key employee receive a covenant of their own as part of sale.

Avoids payroll taxes to seller if he was going to reward the employee.

Page 76

Special rule for

S Corporations

Installment obligations:

If distributed within 12 months of liquidation.

S Corp recognize gain only if BIG tax is involved.

Page 76

Example:

Smith’s Insurance Agency - Liquidation

Sold goodwill under installment sale for $150,000

Goodwill has no basis

Installment sale distributed to Sam within 12 months of liquidation

Page 77

Example:

Deferred gain is NOT recognized at corporate level

Sam will receive 1099-DIV that reflects $150,000 non-cash liquidating distribution

Sam will report sale on Form 1040, Form 6252 on his personal return as principal received

Page 77

Note 1:

Any previous installment sales prior to a plan of liquidation

Distributed to shareholder

Taxable upon distribution to shareholder!

Page 77

Note 2:

If the installment sale is distributed to shareholder NOT with liquidation

Taxes would be do immediately upon distribution to shareholder!

Page 77

Liquidation for

an S Corporation

Receives step up in basis in corporation for gain recognized by corporation

Distribution GENERALLY not taxed again

- Watch for built-in-gains tax

Page 77

Due Date of

Final return

S Corporation

15th day of 3rd month following end of the tax year.

Example:

Sam completes liquidation 6/30/21.

Final return due on or before 9/15/21.

Page 77

Sales Agreement

Make sure the sales agreement includes:

1. What was sold

2. Who was the seller (Corporation or the Shareholder – Covenant)

3. What portion of the sale does the down payment apply to

4. What components of sale are seller finance (if any).

Page 78

Valuation - Liquidation

If liquidation is in conjunction with business sale, assets (goodwill –covenant) have assignable value.

Also allocate the basis for each asset.

Focal point to determine gain/loss becomes FMV at time of liquidation.

Page 78

In many cases

May be wise to have appraisals.

Even if the business is sold to outside buyer and owner does not sell all the assets.

Page 78

Example:

Tom sells assets of corporation.

Tom retains company vehicle for his own personal use.

Tom should get estimate of FMV from a used car dealer.

Corporation must treat as a sale at FMV

Page 78

Taxation

Seller – S Corporation

Item Corporate Individual

Description Taxpayer Taxpayer

Equipment Sold by corp. Flows to sh

Previously

Purchased GW Sold by corp. Flows to sh

Goodwill Could be Could be = LTCG

Covenant Could be Could be = OI

Page 79

Note:

A covenant not to compete should be sold as separate

item between buyer and seller.

Page 79

Tax Considerations

for the Buyer

Asset Deducted

Equipment 7 years MCRS

Goodwill SL over 15 years

Covenant SL over 15 years

Page 79

Net Investment

Income Tax

3.8% tax

Applicable to interest

Generally applicable to Rental Income

$250,000 MFJ

$125,000 MFS

$200,000 S, HOH

Page 80

NIIT with

Material Participation

An item of income from an active trade or business of the taxpayer -i.e., one in which the taxpayer materially participates, isn't included in Net Investment Income.

Page 81

Liquidating Corporation

Retaining Building

Rental Income:

NIIT will be applied after the liquidation of the corporation.

Page 81

Liquidating Corporation

Retaining Building

Gain from sale:

If the shareholder has real estate that he sells, while materially participating in the business, the gain on the sale of the rental property is also exempt from NIIT.

Page 81

Liquidating corporation

retaining building, cont.

If you materially participated 5 of the last 10 years you maintain the NIIT exemption for both the:

Rental income, and

Sale of the building

Page 81

Administratively

Dissolved by State

Does not mean you are liquidated.

Voluntary dissolution is PART of, not the entire process.

Still required to follow federal rules for liquidation.

Page 81

Note:

Most states allow on-line verification for annual filing.

You may want to verify if your client is current each year, or at least when you start the liquidation process.

Page 81

As an S Corporation

If you are administratively dissolved, but have not completed corporate liquidation, any distributions are treated the same as if you withdrew as an operating S corporation.

Page 81

Plan of Dissolution

As part of the process:

The shareholders must formally elect a resolution or plan of dissolution or liquidation.

Page 82

Form 966 Reporting

Required to file with the IRS within 30 days after adopting a resolution or plan of dissolution or liquidation.

Page 82

Form 1099-DIV

A liquidating distribution is:

- Reported to the shareholders on Form 1099-DIV

(If in excess of $600)

Page 82

Example

S Corporation Sale

Sam Smith – sole stockholder, Incorporated January 1, 2008.

Smith’s Insurance Agency adopted a plan to liquidate in early 2020.

Page 83

Example

S Corporation Sale

Sam agreed to sell equipment and client files for $700,000

At closing buyer pays $300,000

Seller takes note in the amount of $400,000

Sales agreement specifically states $100,000 cash at closing = equip. sale

Page 83

January 1

Balance Sheet

Assets

Cash $200,000Equipment 300,000Accum Depr. (300,000)

Total Assets $200,000

Page 83

January 1

Balance Sheet

Equity

Stock $50,000RE 150,000

Total Equity $200,000

Page 83

Prior to Liquidation

Corporation owns

Assets FMV Cost Basis

Equipment $200,000 $300,000 $ -0-Cash 300,000 N/A 300,000Client Files 500,000 N/A - 0 -

Totals $200,000 $300,000 $300,000

Page 83

Balance Sheet

After the Sale

Assets

Cash $600,000Installment Note 400,000

Total Assets $1,000,000

Page 84

Balance Sheet

After the Sale

Liabilities 6252 Deferred Gain $400,000

EquityStock $50,000Beginning RE 150,000Current Earnings 400,000

Total Equity 600,000

Total Liabilities & Equity $1,000,000

Page 84

Caution – not in text

If equipment is sold on the installment method the entire gain taxable in year of the sale.

Regardless of principal received

Depreciation recapture not eligible for installment reporting

Page 84

Individual Income

Information

Interest Income $ 5,000

Dividends Earned 5,000

Salary 100,000

Installment Sale

Received after 6252 trans 20,000

Interest received on 6252 10,000

Page 84

Page 85

This would be the same

whether S or C Corporation

Page 86

This would be the same

whether S or C

Corporation

Consent to the adoption of the dissolution

Page 86

The only difference in C or S Corporation

would be checking either 1120 or 1120S Box

Form 966

Note:

Wisconsin Forms

www.wdfi.org/corporations/forms

Arizona Forms

www.cc.state.az.us/corp

Not in Text

This would be the

same whether S or

C Corporation

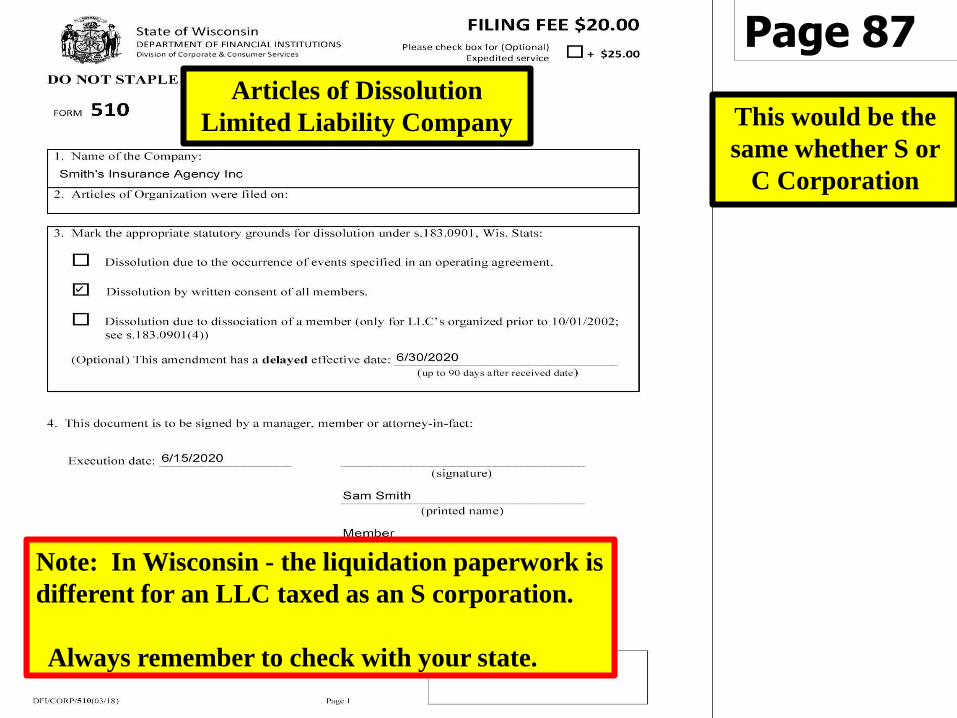

Note: In Wisconsin - the liquidation paperwork is

different for an LLC taxed as an S corporation.

Always remember to check with your state.

Page 87

Articles of Dissolution

Limited Liability Company

Page 88

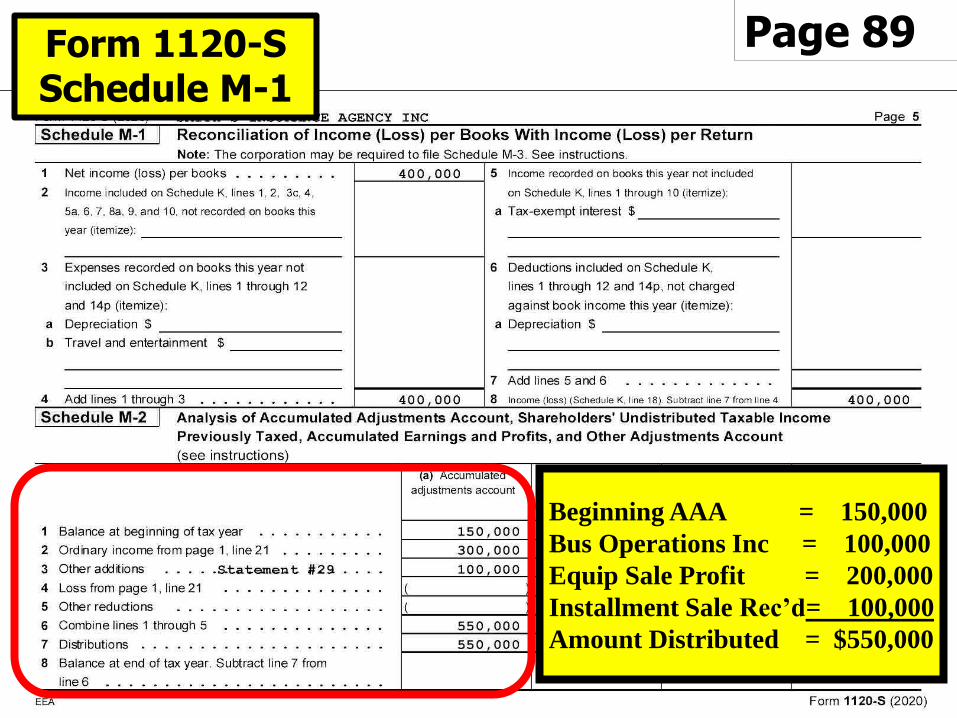

Installment sale notreported on 1120-S.

Reported on Form 6252direct to Schedule K-1.

Form 1120-S

Page 89

Beginning AAA = 150,000

Bus Operations Inc = 100,000

Equip Sale Profit = 200,000

Installment Sale Rec’d= 100,000

Amount Distributed = $550,000

Form 1120-SSchedule M-1

Page 89Schedule DForm 1120-S

11) LTCG from installment sale Form 6252

15) Net LTCG or (loss) 15) 100,000

11) 100,000

Page 90Schedule DForm 1120-S

1/1/20 RE Prev. Taxed $ 150,000

Stock Basis 50,000

2020 Earnings

Bus Operations 100,000

Equip Gain 200,000

Inst Sale rec 1120S 100,000

Def Inst Sale 400,000

Total Distribution $1,000,000

From 1120-S Form 6252

Received as S Corp $100,000

Ordinary Income = $100,000

1245 Depr. Rec. = $200,000

Line 1 = $300,000

Page 90

Ordinary Income

§1245 Depreciation Rec.

Equipment Sale

Form 4797

Page 91

Sales Price $500,000 Goodwill

Installment Payments Received

as an S Corporation $100,000

Form 6252

26) 100,000

7) 500,000

Page 91

1/1/20 RE Prev. Taxed $ 150,000

Stock Basis 50,000

2020 Earnings

Bus Operations 100,000

Equip Gain 200,000

Inst Sale rec 1120S 100,000

Def Inst Sale 400,000

Total Distribution $1,000,000

Checking Acct = $600,000

6252 Deferred Gain = $400,000

Form 1099-DIV

9) 600,000 10) 400,000

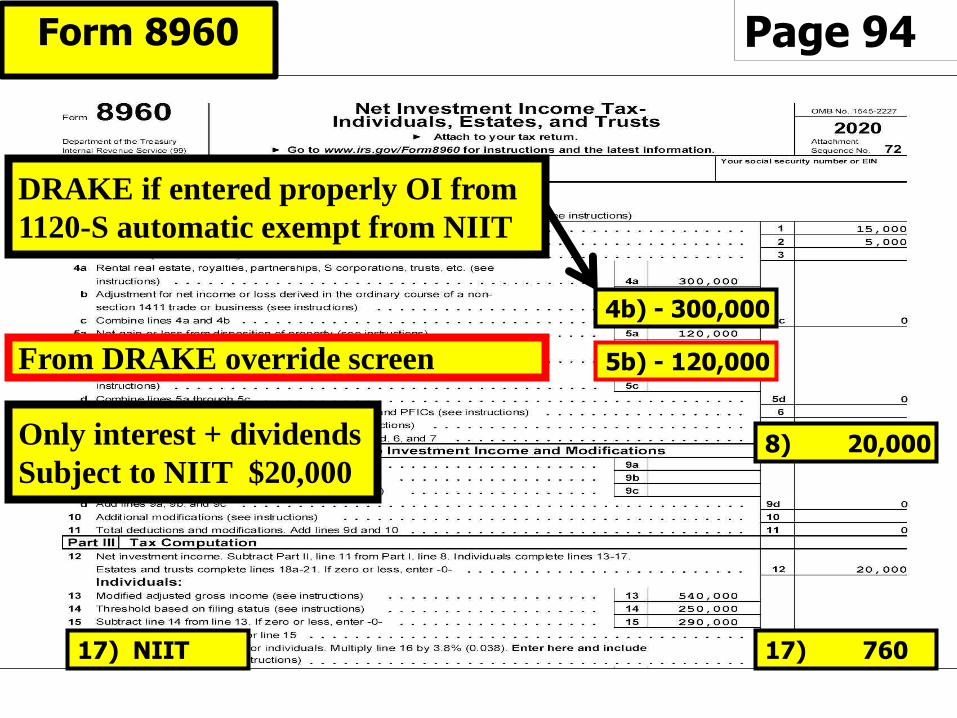

Page 94

DRAKE if entered properly OI from

1120-S automatic exempt from NIIT

Form 8960

4b) - 300,000

5b) - 120,000

Only interest + dividends

Subject to NIIT $20,0008) 20,000

From DRAKE override screen

17) 76017) NIIT

Page 94

5b) - 120,000

DRAKE Override screen

If you use DRAKE software

5b) Net gain from disposition of property not subject to NIIT

Exempt form NIIT with material participation in the business.

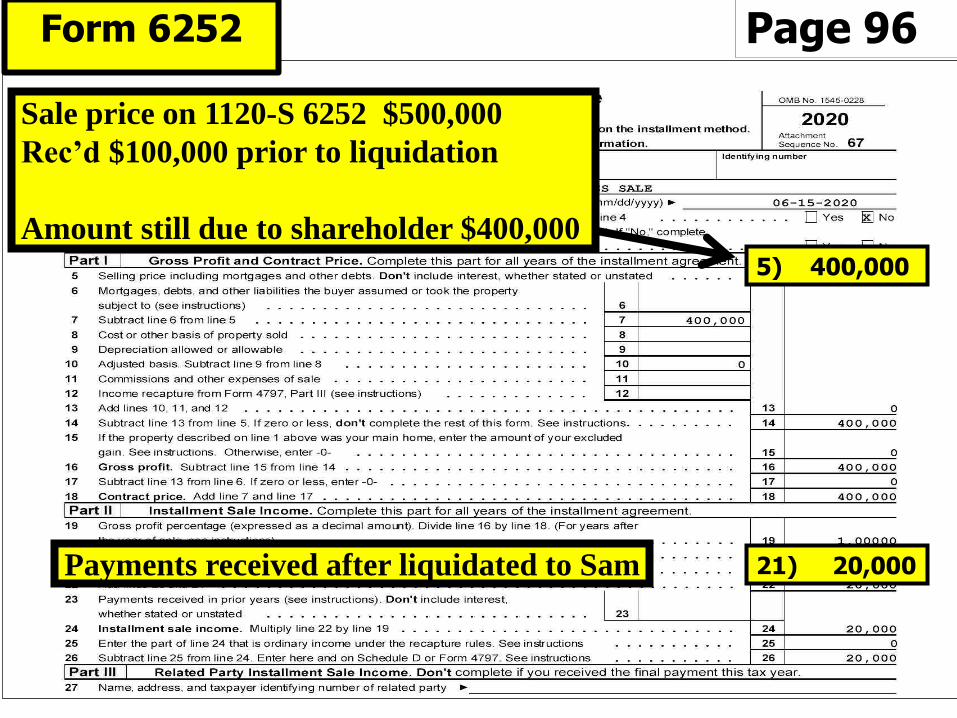

Page 96

Sale price on 1120-S 6252 $500,000

Rec’d $100,000 prior to liquidation

Amount still due to shareholder $400,000

Payments received after liquidated to Sam

Form 6252

21) 20,000

5) 400,000

Form 8594

Consistent reporting between buyer and seller

Congress developed §1060

Buyer and seller attach a copy to their income tax return

Page 96

Attorney who

Drafts the Contract

Should address this issue

Reduces the chance that the parties will have conflicting allocations later

Reduces the chance of audit

Page 96

Allocating

Purchase Price

Assets that constitute trade or business:

I. Cash

II. Traded Personal Property

III. Accts Receivable, mortgages, and credit card receivables

IV. Inventory

Page 97

Allocating

Purchase Price

Assets that constitute trade or business:

V. All assets not in I,II,III,VI or VIIEquipment & Building

VI. All 197 except GoodwillCovenant

VII. Goodwill

Page 97

Section 197 Considerations

Subject to amortization over 15 years

Includes:

Goodwill

Workforce in place

Books and records

Patent, copyright, formula process, etc.

Customer based intangible

Franchise, trademark, or trade name

Page 97

Page 96

Equipment = $200,000

Client Files = $500,000

Form 8594

6/15/20

Section 1244 Stock

Generally, a loss on the sale of stock is LTCL.

§1244 Stock losses can be treated as an ordinary loss.

Page 99

Example:

ABC liquidated

Shareholder receives cash $50,000

Shareholder assumed liability $150,000

Shareholder’s Stock Basis $5,000

Page 96

Example:

Cash received $ 50,000

Debt Assumed (150,000)

Net to Shareholder (100,000)

Stock Basis - 5,000

Stock Loss ($105,000)

1244 Stock Loss $5,000

LTCL $100,000

Page 99

§1244 Stock

Requirements

1. The stock must be issued for money or property.

(not securities or services)

2. Domestic small business

Capital contributions less than $1,000,000.

Page 99

§1244 Stock

Requirements

3. 5 most recent tax years before the loss > 50% gross receipts other than royalties, rents, dividends, interest, annuities, sale of stock,

4. Shareholder was originally issued stock from the corporation.

(Gift, inheritance, not eligible)

Page 99

§1244 Stock

Requirements

5. Issued before 7/19/84 must be common stock, after 7/18/84 can be common or preferred.

6. Shareholder cannot be a trust, or an estate, or corporation. However available to partner if the partner was member of partnership when acquired stock AND partnership sold the stock.

Page 99

§1244 Loss Limitation

Ordinary loss is limited to $100,000.

Any excess = LTCL

Page 100

Example:

Current year §1244 Loss of $110,000

Deduct $100,000 Ordinary loss

Remaining $10,000 = LTCL

No other LTCG deduct $3,000 this year

$7,000 LTCL carryover to next year

Page 100

Contributions to Capital

If basis of §1244 stock is increased through capital contributions or otherwise

It does not increase amount allocated to §1244 stock at time of sale.

Page 100

Example:

Tom received 100 Shares 1244 stock for $20,000 in Dec. 2002

Contribution of $5,000 in June 2006 increasing basis of stock to $25,000.

Page 100

Example:

Sold stock for $15,000 in April 2020 with Loss of $10,000.

$8,000 Ordinary loss

($10,000 x $20,000/$25,000)

Remaining $2,000 = LCTL

Page 100

S Corporation

§1244 Stock Loss

Applies to both C & S Corporations

Calculated differently

Previously reported losses may reduce original basis.

Page 100

Example:

Sam has original capital contribution of $100,000.

The S corporation had losses of $20,000 over the years.

Page 100

Example:

In liquidation Sam receives no asset and no liabilities.

Sam will be entitled to a §1244 loss of $80,000.

($100,000 - $20,000)

Page 100

Note:

Report §1244 loss on Form 4797

Any capital loss report on Sch D

Page 100

Back to Basics

Evaluations

CPE Certificates