Russia, the Eurasian Customs Union and the EU—Cooperation, Stagnation or Rivalry

29 October 2013

Danske Bank Markets Analyst: Sanna Kurronen +358 10 546 8369

Stagnation is starting to look like a policy goal in Russia

Important disclosures and certifications are contained from page 16 of this report.

2

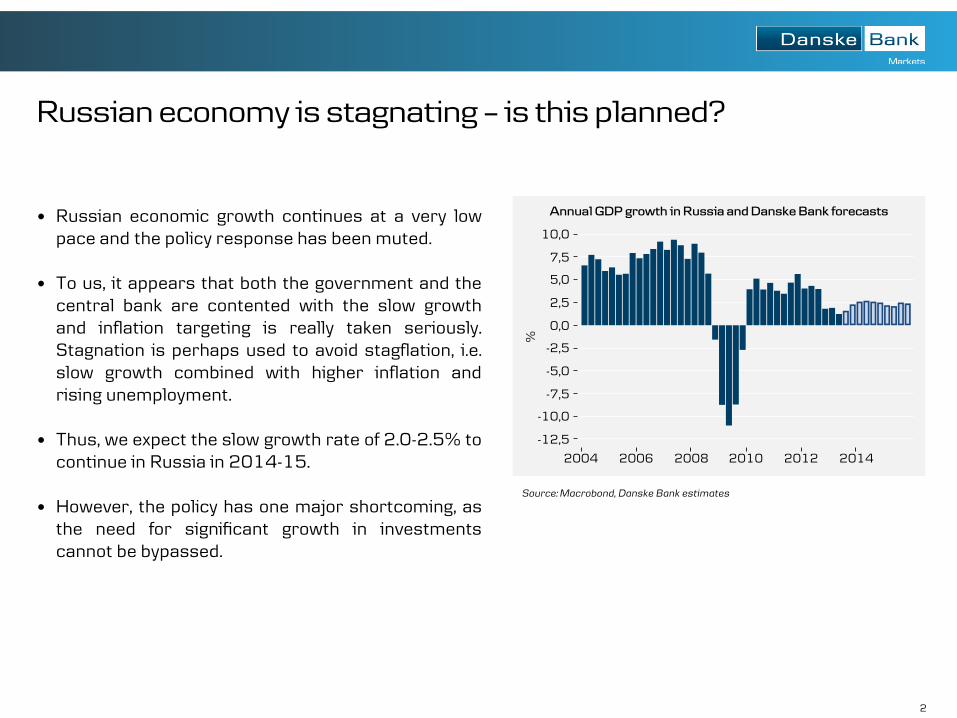

Russian economy is stagnating – is this planned?

Russian economic growth continues at a very low pace and the policy response has been muted.

To us, it appears that both the government and the central bank are contented with the slow growth and inflation targeting is really taken seriously. Stagnation is perhaps used to avoid stagflation, i.e. slow growth combined with higher inflation and rising unemployment.

Thus, we expect the slow growth rate of 2.0-2.5% to continue in Russia in 2014-15.

However, the policy has one major shortcoming, as

the need for significant growth in investments cannot be bypassed.

Source: Macrobond, Danske Bank estimates

3

Stagnation is used in Russia to buy time

Given several major bottlenecks in the Russian economy (labour force, logistics, production capacity, etc.), we believe Russian politicians are trying to buy time with stagnation to improve the investment environment in the economy.

Without significant investment, rapid growth is

likely to lead to higher inflation. However, as the investment environment

remains poor in Russia, time is needed to improve the environment to enhance investments.

Source: Macrobond, Danske Bank Markets

4

What is dragging investments in Russia?

Slowdown in fixed investments this year is due mostly to public investments and investments of state-owned companies.

Lower energy price expectations deter

investments in mineral extraction sector. The change of mayor in Moscow and St

Petersburg has caused significant delays in some of the investments in these areas.

Access to finance can be an obstacle as well

for private companies.

However, the most important obstacle for investments remains the poor overall investment environment.

Source: Rosstat Danske Bank Markets

0

10

20

30

40

50

60

70

80

90

2012

% o

f t

ota

l in

ve

st

me

nt

s

Fixed investments in Russia in most important

sectors of total fixed investments

Real estate

Transport and communication

Electricity, gas and water

Manufacturing

Mineral extraction

5

Putin’s 100 steps programme shows positive progress but it’s not enough We remain sceptical about Russia’s ability to

improve the investment environment. Putin’s 100 steps programme aims at

improving Russia’s rank in the Ease of doing business survey by 100 steps, ranking 20th as soon as 2018.

Progress has been apparent since the launch of the programme in 2012 and some red tape can still be removed relatively quickly (construction permits, trading across borders) but we are less convinced of improvements in investor protection and believe wide-ranging corruption will hamper progress towards the top ranks.

Source: World bank, Danske Bank Markets

0 50 100 150 200

Total rank

Starting a business

Dealing with construction permits

Getting electricity

Registering property

Getting credit

Protecting investors

Paying taxes

Trading across borders

Enforcing contracts

Resolving insolvency

Russia’s rank in Ease of doing business survey

2012 and 2014

2014 2012

6

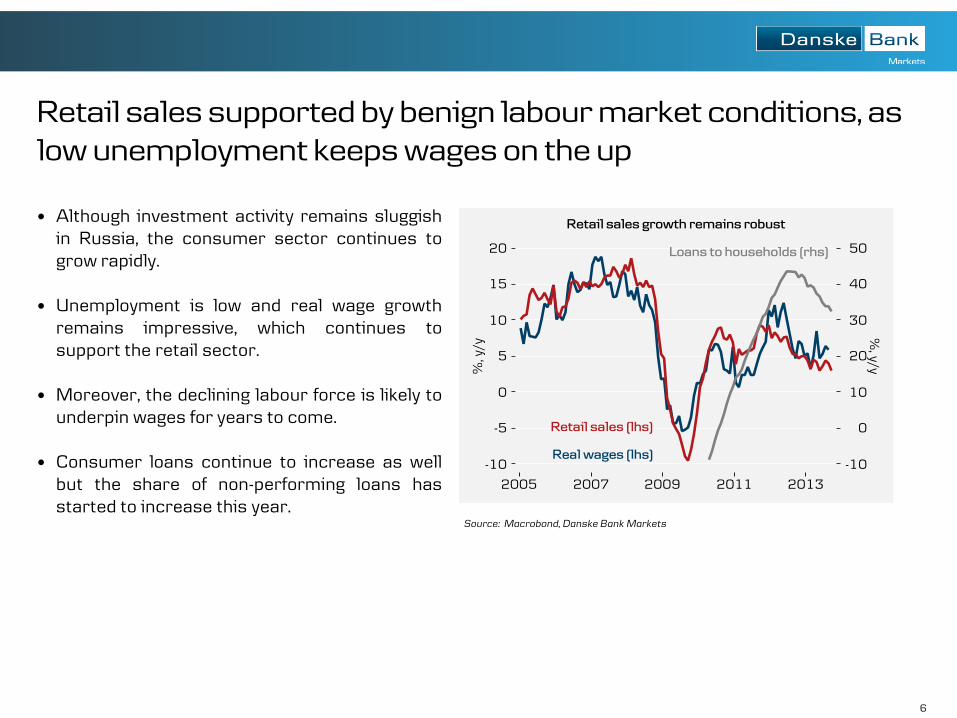

Retail sales supported by benign labour market conditions, as low unemployment keeps wages on the up

Source: Macrobond, Danske Bank Markets

Although investment activity remains sluggish in Russia, the consumer sector continues to grow rapidly.

Unemployment is low and real wage growth remains impressive, which continues to support the retail sector.

Moreover, the declining labour force is likely to underpin wages for years to come.

Consumer loans continue to increase as well but the share of non-performing loans has started to increase this year.

7

Is the consumer sector threatened by overheating or cooling?

The Russian central bank is trying to curb excessive growth in consumer loans through stricter regulation to prevent growth in non-performing loans.

However, excessive curbing of the overheating

might lead to declining consumer demand, if unemployment increases and wage pressures moderate simultaneously.

Thus, policy is about balancing between supporting consumer sector and eliminating the symptoms of overheating.

Source: CBR, Danske Bank Markets

0

1

2

3

4

5

6

7

8

%

Non-performing loan share of total loans at

the beginning of the year in Russia

All loans

Households

Mortgage

8

Inflation continues on its downward trend

Source: Macrobond, Danske Bank Markets

Russian inflation has started to ease since the summer and we expect the good harvest and slow economic growth to push inflation down further over the coming year.

However, the weak rouble is adding some upside pressure to import prices.

The central bank’s inflation targets are 5.0% for 2014, 4.5% for 2015 and 4.0% for 2016.

All in all, the Russian central bank has shown commitment to its inflation target, which just might turn out to be a strategy worth sacrificing a couple of years growth for.

9

Rapid inflation impairs Russian competitiveness

Source: Macrobond, Danske Bank Markets

Despite the nominal weakening of the rouble, high inflation ensures real appreciation of the rouble as inflation in trade partner countries is lower on average.

Against a trade-weighted basket, the rouble has appreciated 50% in real terms over the past 10 years.

In practice, the real appreciation means that Russian companies lose their international competitiveness but Russian consumers are able to consume more and more foreign goods.

10

Oil price continues to be the main threat for the Russian economy The oil price still has a major effect on the

Russian economy: an oil price collapse would diminish the current account surplus, increase the budget deficit and reduce investments.

Such wide-ranging economic deterioration would spread to the whole economy.

We expect a moderate decline in the oil price in coming years, which should not have a dramatic effect on the Russian economy.

Source: Reuters EcoWin, Danske Bank Markets

Oil price and basket/RUB

09 10 11 12 13 14

32

33

34

35

36

37

38

39

40

60

80

100

120

140basket/RUB USD/barrel

<<Basket/RUB

Oil price and DB forecast >>

11

Russians are not concerned about rouble weakness anymore

Although the Russian central bank continues to limit rouble volatility, the rouble is almost free floating already. Thus, the current level of the rouble reflects its market valuation.

Moreover, the rouble will not be defended as strongly as it was in 2008-09 and, consequently, Russia will not drift to such a severe liquidity crisis in the case of a weakening rouble.

A weaker rouble is favourable for the government budget, as a big share of government income is USD-denominated from energy exports.

Source: Macrobond, Danske Bank Markets

12

Macroeconomic forecasts for Russia

Source: Danske Bank Markets, Macrobond, Rosstat

Russian macro forecasts -Danske Bank

5,6 5,22014 2,6 3,9 3,6 -2,0 3,7 6,3 2,7 2,8

Infla-

tion1

Russia

2012 3,4 6,6 6,7

Year Gdp1

Private.

Cons1

Fixed Inv1

Export1, 4

Import1, 4

3,5 2,6 5,3

Trade

Balance2, 4

Current

acc.2, 4

Industrial

prod.1

Unem-

ploym3

3,4 5,7 2,3

5,1

2013 1,8 4,4 -0,6 -1,8 3,8 7,2 3,1 0,3

3,5 6,0 9,5

2015 2,3 3,4 3,8 -1,5 3,0 5,8 4,8

5,5 6,4

1) Average % y/y 2) % of GDP 3) % of total work force 4) export and import prices

13

Disclosures

Lähde: Danske Bank Markets, Macrobond

This presentation has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’). The author of this presentation is Sanna Kurronen, Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in this research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’ rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

14

General disclaimer This presentation has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only and should be viewed solely in conjunction with the oral presentation provided by Danske Bank Markets and/or Danske Markets Inc. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The presentation has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this presentation.

The opinions expressed herein are the opinions of the research analysts responsible for the presentation and reflect their judgement as of the date hereof. These opinions are subject to change and Danske Bank does not undertake to notify any recipient of this presentation of any such change nor of any other changes related to the information provided in the presentation.

Danske Bank, its affiliates, subsidiaries and staff may perform services for or solicit business from any issuer mentioned herein and may hold long or short positions in, or otherwise be interested in, the financial instruments mentioned herein. The Equity and Corporate Bonds analysts of Danske Bank and undertakings with which the Equity and Corporate Bonds analysts have close links are, however, not permitted to invest in financial instruments that are covered by the relevant Equity or Corporate Bonds analyst or the research sector to which the analyst is linked.

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of our regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

This presentation is not intended for retail customers in the United Kingdom or the United States.

This presentation is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent.

Disclaimer related to presentations to U.S. customers

In the United States this presentation is presented by Danske Bank and/or Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank. In the United States, the presentation is intended solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this presentation are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this presentation who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.