St. John the Baptist Parish Council on Aging, Inc. · The Council has presented the General Fund,...

59

n:i1 ST, JOHN PARISH COUNCIL ON AGING, INC Reserve, Louisiana Annual Financial Statements As of and For the Year Ended June 30, 2009 Under provisions of state law, this report is a public document. Acopy ofthe report has been submitted to the entity and otherappropriate public officials. The report is available for public inspection at the Baton Rouge office ofthe LegislativeAuditor and, where appropriate, at the office of the parish clerk of court. Release Date DONALD C. De VILLE Certified Public Accountant 7829 Bluebonnet Boulevard Baton Rouge, Louisiana 70810

Transcript of St. John the Baptist Parish Council on Aging, Inc. · The Council has presented the General Fund,...

n:i1

ST, JOHN PARISH COUNCIL ON AGING, INC Reserve, Louisiana

Annual Financial Statements As of and For the Year Ended June 30, 2009

Under provisions of state law, this report is a public document. Acopy ofthe report has been submitted to the entity and otherappropriate public officials. The report is available for public inspection at the Baton Rouge office ofthe LegislativeAuditor and, where appropriate, at the office of the parish clerk of court.

Release Date

DONALD C. De VILLE Certified Public Accountant 7829 Bluebonnet Boulevard

Baton Rouge, Louisiana 70810

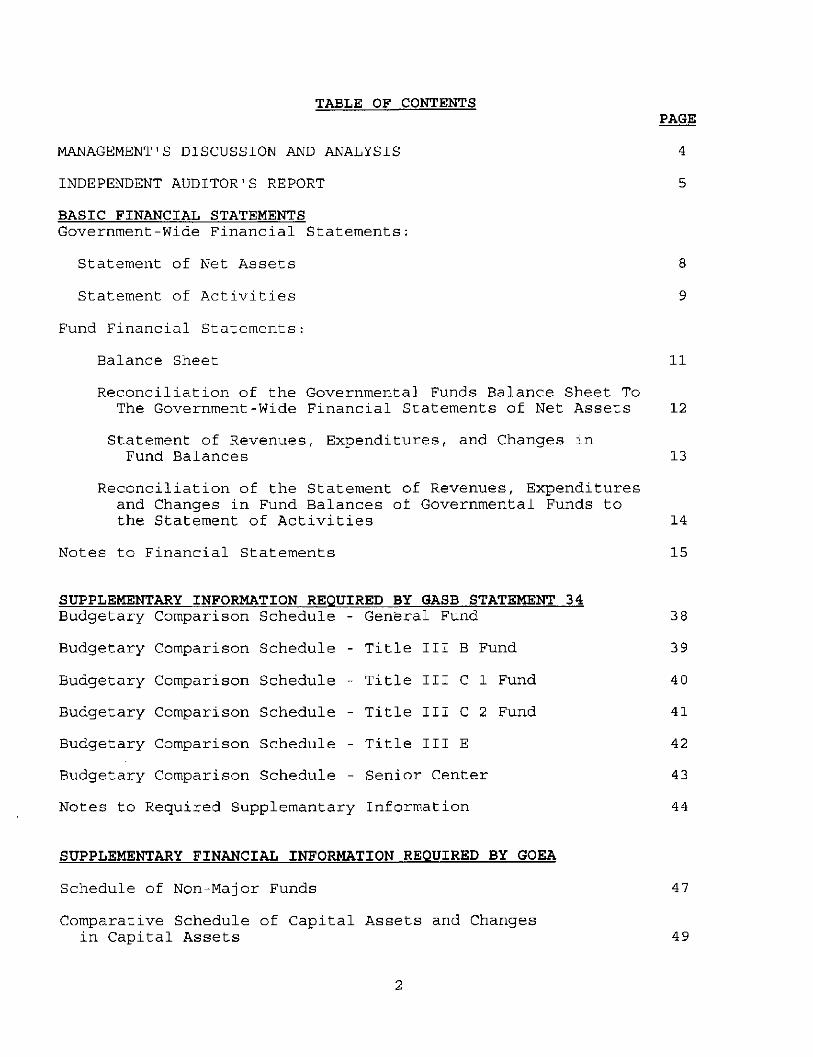

TABLE OF CONTENTS PAGE

MANAGEMENT'S DISCUSSION AND ANALYSIS 4

INDEPENDENT AUDITOR'S REPORT 5

BASIC FINANCIAL STATEMENTS

Government-Wide Financial Statements:

Statement of Net Assets 8

Statement of Activities 9

Fund Financial Statements:

Balance Sheet 11

Reconciliation of the Governmental Funds Balance Sheet To The Government-Wide Financial Statements of Net Assets 12 Statement of Revenues, Expenditures, and Changes in Fund Balances 13

Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances of Governmental Funds to the Statement of Activities 14

Notes to Financial Statements 15

SUPPLEMENTARY INFORMATION REQUIRED BY GASB STATEMENT 34

Budgetary Comparison Schedule - General Fund 38

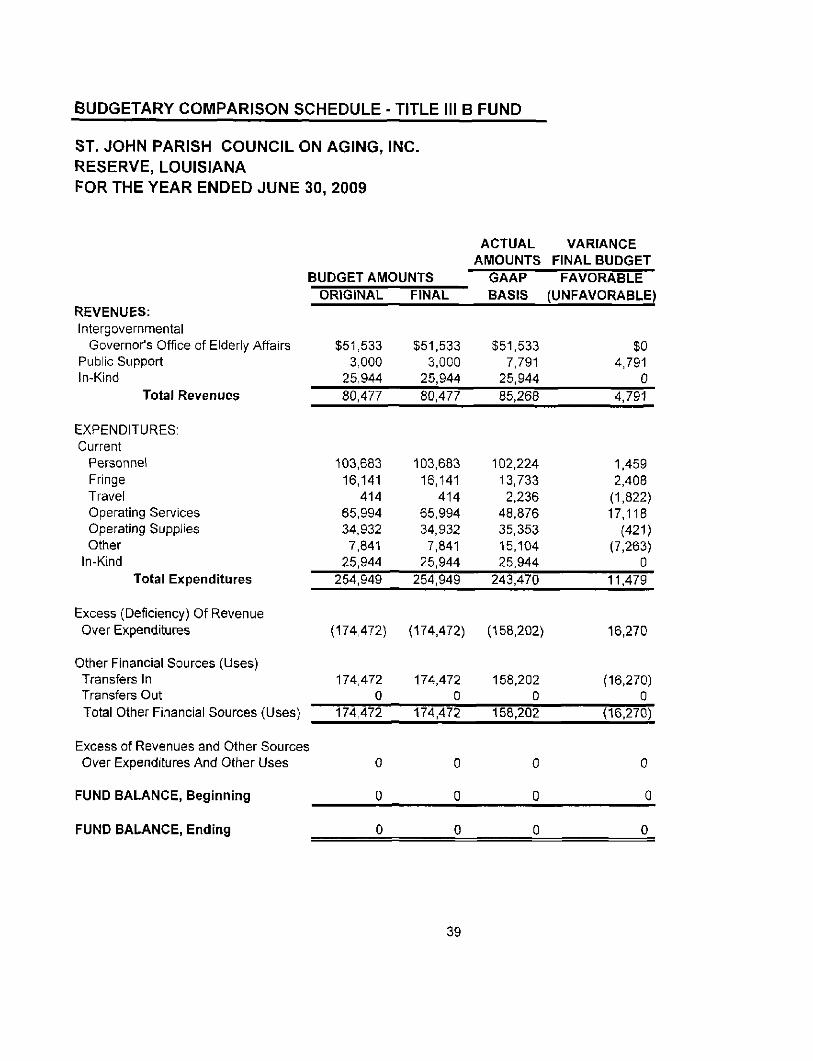

Budgetary Comparison Schedule - Title III B Fund 39

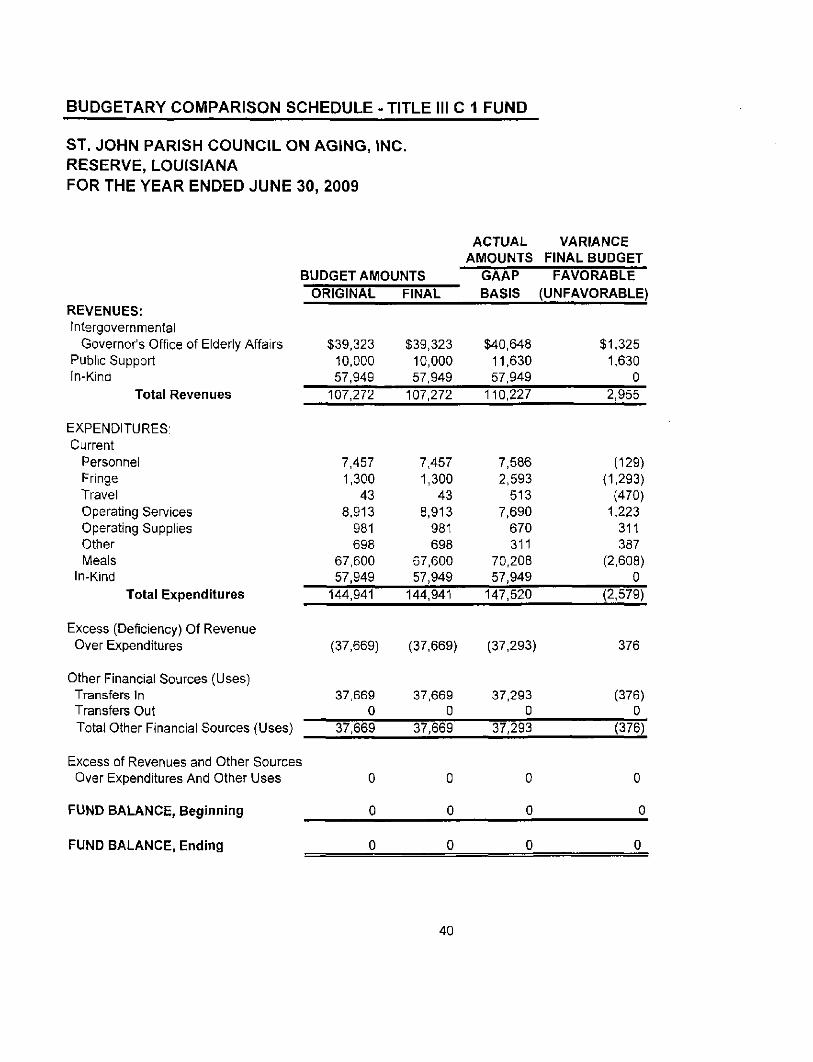

Budgetary Comparison Schedule - Title III C 1 Fund 40

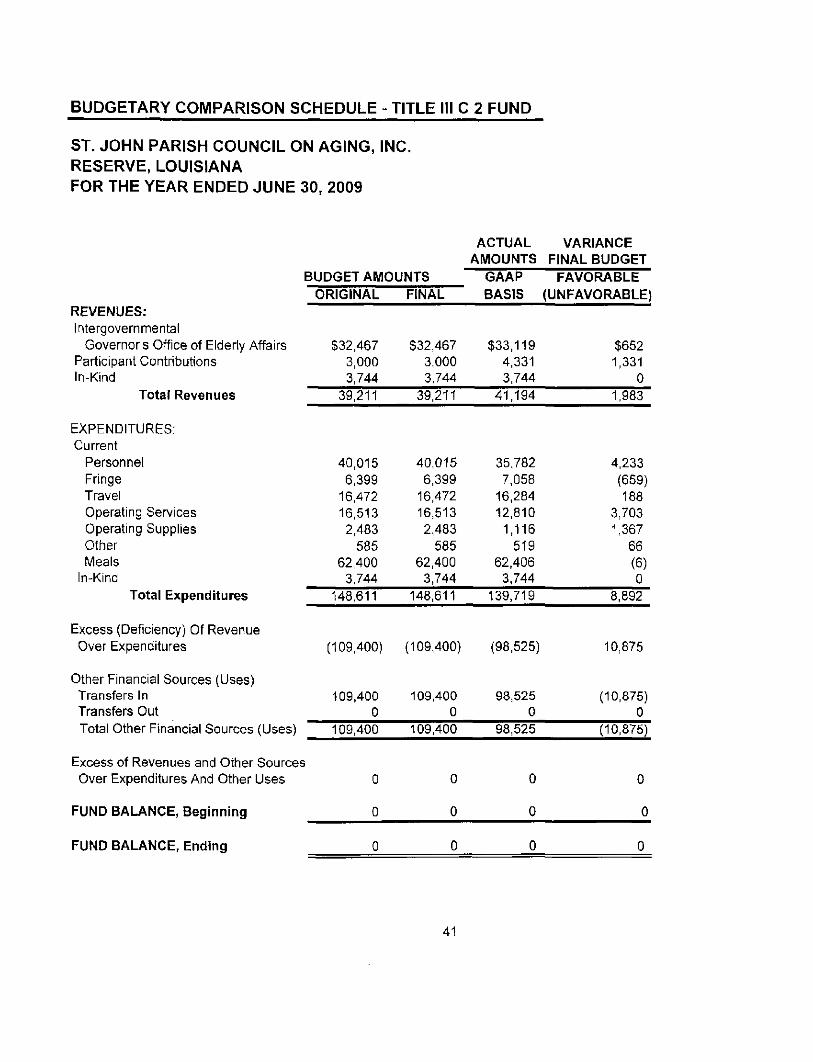

Budgetary Comparison Schedule - Title III C 2 Fund 41

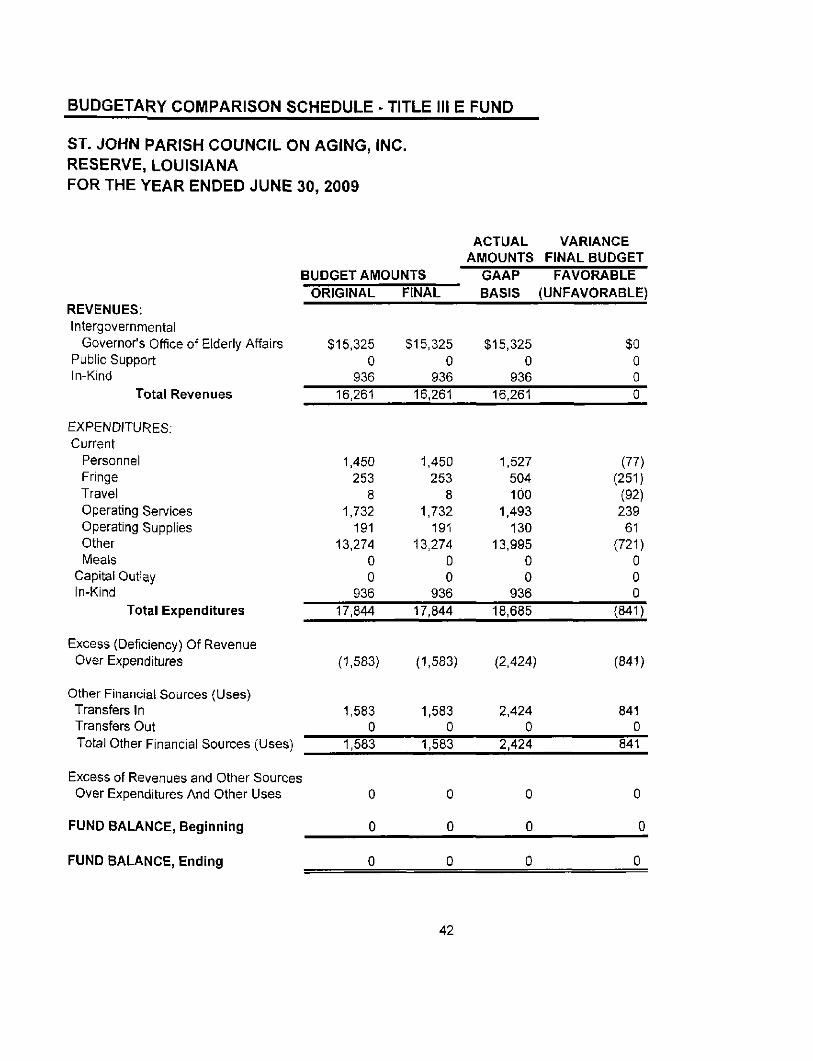

Budgetary Comparison Schedule - Title III E 42

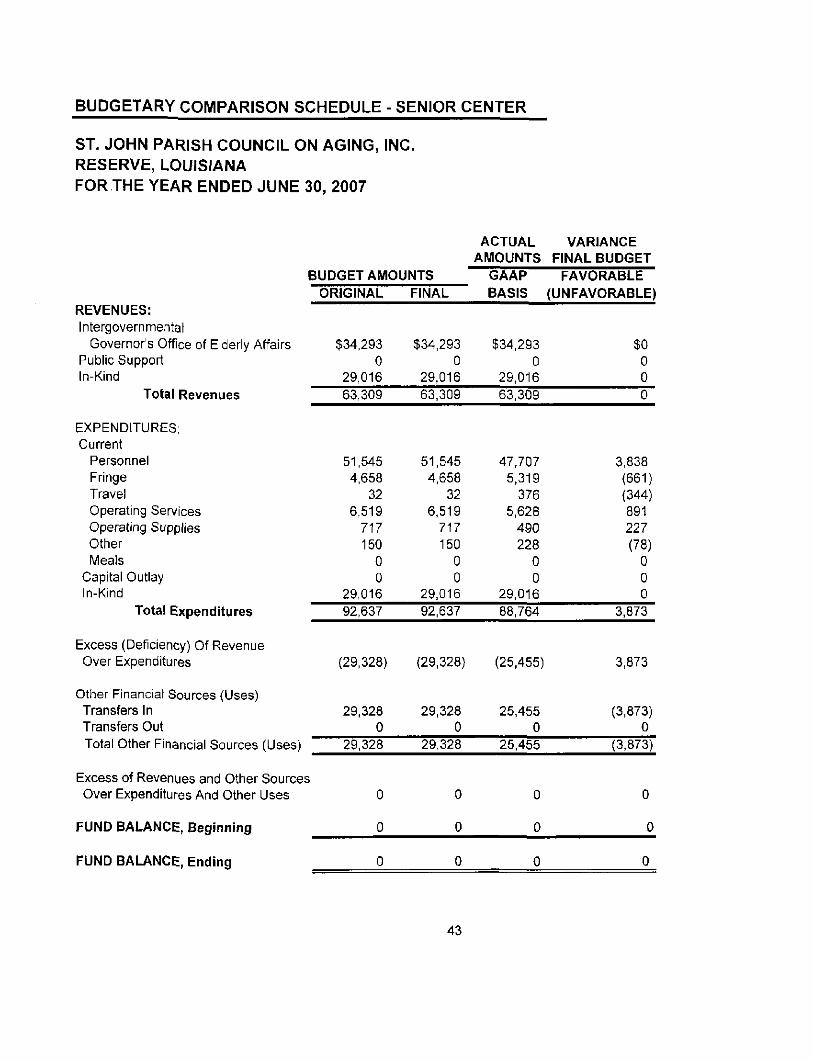

Budgetary Comparison Schedule - Senior Center 43

Notes to Required Supplemantary Information 44

SUPPLEMENTARY FINANCIAL INFORMATION REQUIRED BY GOEA

Schedule of Non-Major Funds 47

Comparative Schedule of Capital Assets and Changes in Capital Assets 49

TABLE OF CONTENTS - (CONTINUED;

OTHER REPORTS REQUIRED BY GOVERNMENTAL AUDITING STANDARDS

Report on Compliance and on Internal Control over Financial Reporting Based on an Audit of Financial Statements Performed In Accordance with Government Auditing Standards 50

Schedule of Prior Years Findings 52

Schedule of Findings and Questioned Cost 53

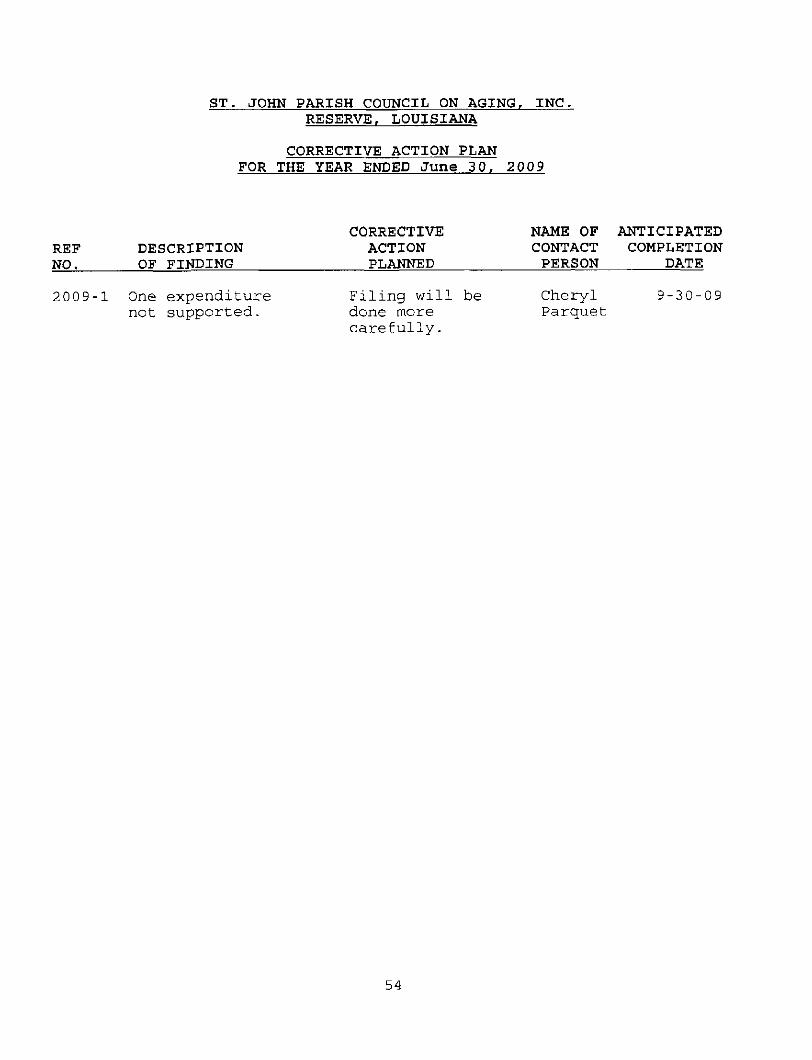

Corrective Action Plan 54

MANAGEMENTS DISCUSSION AND ANALYSIS

St. John Parish Council on Aging

The " Management's Discussion and Analysis" of the St. John Parish Council On Aging, Inc.'s (the Council) financial performance presents a narrative overview and analysis ofthe Council's fmancial activities for the year ended June 30, 2009. This report highlights the current year's activities, resulting changes, and relevant facts. Please read this report in conjunction with basic fmancial statements, which follow this section.

FINANCIAL HIGHLIGHTS (see statements on 8 and 9)

The Council's assets exceeded its liabilities at the close of fiscal year 2009 by $332,651 (net assets), which represents 3% increase from last year.

Cash was $291,856 at June 30, 2009 compared to $235,194 at June 30, 2008. This is an increase of $56,662 due to an increase in local property taxes and increased funding from the Govemor's Office ofElderly Affairs.

The Council's revenue decreased by $807 or . 1 % primarily due to an increased in expenses.

The Council's expenses increased by $12,690 or 2% due to an increase in congregate and home delivered meals.

Capital assets increased by $5,790 due to the purchase of a vehicle.

The Council did not have any funds with deficit fund balances.

Fund balance at the year-end for the Council was $254,258. (Page 13)

4i

OVERVIEW OF THE FINANCIAL STATEMENTS

This discussion and analysis is intended to serve as an overview to the Council's basic financial statements. The Council's annual report consists of five parts; (1) management's discussion and analysis (this section) (2) basic financial statements (3) required supplementary information, and (4) the optional section that presents combining statements for non-major govemmental funds and other schedules by certified public accounts and managements.

The basic financial statements included two kinds of statements that present different views ofthe Council:

Government-wide Financial Statements

The Govemment-wide fmancial statements (see pages 8 and 9) are designed to provide readers with a broad overview of the Council's finances, in a manner similar to a private sector business. The statement of net assets presents information on all ofthe Council's assets and liabilities, with the difference between the two reports as net assets. Over time, increases or decreases in net assets may serve as a useful indicator of whether the financial position ofthe Council is improving or deteriorating. The statement of activities presents information showing how the Council's net assets change during each fiscal year (revenues less expenditures). All changes in net assets are reported as soon as the financial transaction occurs regardless ofthe timing ofthe related cash flows. Thus, revenue and expenditures are reported in this statement this fiscal year even though the resulting cash flow is in future fiscal years. The govemmental activity of the Council is health and welfare, which is comprised of various programs that include supportive services, nutritional services, utility assistance, disease prevention and caregiver support.

Fund Financial Statements

A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. All ofthe funds ofthe Council are govemmental funds.

4ii

Governmental Funds

Govemmental funds are used to account for essentially the same functions reported as govemmental activities in the govemment-wide financial statements. However, unlike the govemment-wide financial statements, govemmental fund financial statements focus on current year inflows and outflows of cash, as well as on balances of spendable resources available at the end of the fiscal year. Both the govemmental fund balance sheet and the govemmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to help with comparisons between govemmental funds and govemmental activities. (Pages 12 and 14)

The Council has presented the General Fund, Title III-B, Title III C-l, Title III C-2, Title III E, and Senior Center as major funds. All non-major govemmental funds are presented in one column, titled "Total Non-Major Funds". Combining financial statements of the non-major funds can be found in the Combining Fund Statements that follow the basic financial statements. (Page 47)

Notes to the Financial Statements

The notes provide additional information that is essential to a full understanding of the data provided in the govemment-wide and fund financial statements. The notes ofthe financial statements can be found on Page 15-36 of this report.

Other Information

In addition to the basic financial statements and accompanying notes, this report also represents certain required supplementary information that further explains and supports the information in the financial statements. The Govemmental Accounting Standards Board (GASB) Statement No. 34 requires budgetary comparison schedules for the General Fund and each major Special Revenue Fund that has a legally adopted budget. (Pages 38-43).

4iii

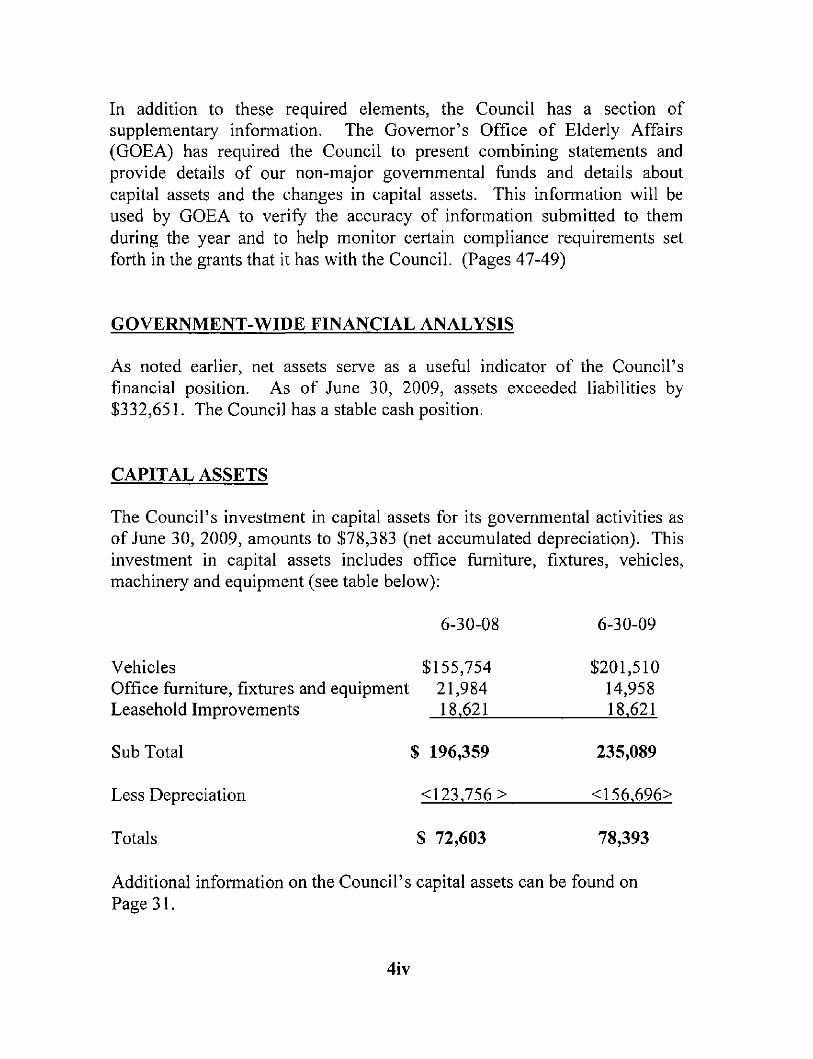

In addition to these required elements, the Council has a section of supplementary information. The Govemor's Office of Elderly Affairs (GOEA) has required the Council to present combining statements and provide details of our non-major govemmental funds and details about capital assets and the changes in capital assets. This information will be used by GOEA to verify the accuracy of information submitted to them during the year and to help monitor certain compliance requirements set forth in the grants that it has with the Council. (Pages 47-49)

GOVERNMENT-WIDE FINANCIAL ANALYSIS

As noted earlier, net assets serve as a useful indicator of the Council's fmancial position. As of June 30, 2009, assets exceeded liabilities by $332,651. The Council has a stable cash position.

CAPITAL ASSETS

The Council's investment in capital assets for its govemmental activities as of June 30, 2009, amounts to $78,383 (net accumulated depreciation). This investment in capital assets includes office fumiture, fixtures, vehicles, machinery and equipment (see table below):

6-30-08 6-30-09

Vehicles $155,754 $201,510 Office fumiture, fixtures and equipment 21,984 14,958 Leasehold Improvements 18.621 18.621

Sub Total $ 196,359 235,089

Less Depreciation <123.756> <156.696>

Totals $ 72,603 78,393

Additional information on the Council's capital assets can be found on Page 31.

4iv

ECONOMIC FACTORS AND NEXT YEARNS BUDGET AND RATES

The Council receives most of its funding from federal and state agencies and local taxes. Because of this, the source of income for the Council is consistent. However, some of the Council's grants and contracts are contingent upon the level of service provided by the Council, and therefore, those revenues are not fixed. There have been no significant changes to the funding levels or terms ofthe grants and contracts. The Govemor's Office ofElderly Affairs (GOEA) has approved the Council's budget for the fiscal year 2009-2010. There are no plans to add any significant programs for next fiscal year.

The Executive Director and Board of Directors consider the following factors and indicators when setting next year's budget, rates and fees. These factors and indicators include:

• Actual expenditures from previous fiscal years in relation to expected needs in the current year.

• Consideration of funding to be received from GOEA.

• Interest revenues have been budgeted with no anticipation of an increase in interest rates.

• Salaries and benefits are based on the number of employees needed to perform necessary services and the related benefits.

• Travel rates in accordance with state travel regulations.

• Services the Council will provide along with estimated service cost.

• Estimate operating supplies needed to perform necessary services.

• Detail plan of equipment needed to be purchased,

• Vehicle insurance based on quotes and contracts.

4v

REOUESTS FOR INFORMATION

This financial report is designed to provide a general overview of the Council's finances for all concemed.

Questions concerning any of the information provided in this report or request for additional information should be addressed to:

Board of Directors St. John Council on Aging, Inc. P.O. Drawer 512 Reserve, Louisiana - 70084 Phone: (985)479-0272 Cheryl A Parquet, Executive Director

4vi

VomU C. VeVtte % <

American insitute CPAs J^OtlUlO W* J ^ € ylllC Louisiana Society CPAs

7829 BLUEBONNET BLVD. BATON ROUGE, LA 70810

(225) 767-7829

INDEPENDENT AUDITOR'S REPORT

September 16, 2009

To the Board of Directors St. John Parish Council on Aging, Inc. Reserve, Louisiana

I have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of the St. John Parish Council on Aging, Inc. as of and for the year ended June 30, 2009, which collectively comprises the Council's basic financial statements as listed in the table of contents. These financial statements are the responsibility of the Council's management. My responsibility is to express an opinion of these basic financial statements based on my audit.

I conducted my audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that I plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. I believe that my audit provided a reasonable basis for my opinion.

In my opinion, the basic financial statements referred to above present fairly, in all material respects, the financial position of the governmental activities, each major fund, and the aggregate remaining fund information of the St. John Parish Council on Aging as of June 30, 2009, and the respective changes in financial position for the year then ended in conformity with accounting principles generally accepted in the United States of America.

The Management's discussion and analysis, page 4, and budgetary comparison information on pages 38 through 43, are not a required part of the basis financial statements but are supplementary information required by accounting principles generally accepted in the United States of America. I have applied certain limited procedures, which consisted principally of inquires of management regarding the methods of measurement and presentation of the supplementary information. However, I did not audit the information and express no opinion on it.

My audit was conducted for the purpose of forming an opinions on the financial statements that collectively comprise the St. John Parish Council On Aging, Inc. basic financial statements. The combining and individual nonmajor fund financial statements are presented for purposes of additional analysis and are not a required part of the basic financial statements. The combining and individual nonmajor fund financial statements have been subjected to the auditing procedures applied in the audit of the basic financial statements and, in my opinion, are fairly stated in all material respects in relation to the financial statements taken as a whole.

In accordance with Government Auditing Standards, I have also issued a report dated Septeber 16, 2009, on our consideration of St. John Parish Council on Aging, Inc.'s internal control over financial reporting and our tests of its compliance with laws, regulations, contracts and grants. That report is an integral part of an audit performed in accordance with Governmental Auditing Standards and should be read in conjunction with this report in considering the results of my audit.

^ J t . /kJd^

GOVERNMENT WIDE FINANCIAL STATEMENTS

GOVERNMENT WIDE STATEMENT OF NET ASSETS

ST. JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUSIANA

JUNE 30, 2009

GOVERNMETAL ACTIVITIES

ASSETS: Cash $291,856 Prepaid Expense

Insurance 2,486 Cruise Expense 7,612

Capital assets, net of accumulated depreciation 78,393 Total Assets 380,347

The accompanying notes are an integral part of this statement.

8

LIABILITIES AND FUND BALANCES:

LIABILITIES: Accounts Payable $35,345 Payroll Taxes Payable 4,236 Deferred Revenue 8,115

Total Liabilities 47,696

NET ASSETS: Invested in Capital Assets, net of debt $78,393 Restricted for:

Utilities 1.912 Unreserved-Undesignated 252,346

Total Net Assets 332,651

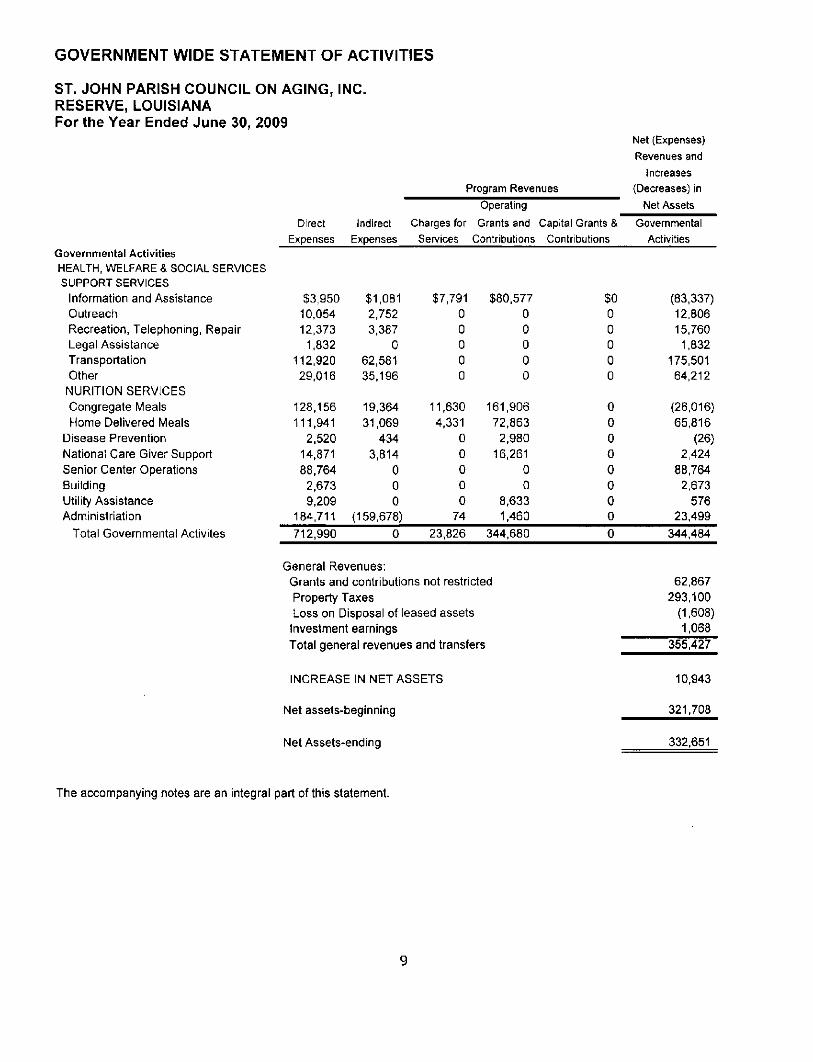

GOVERNMENT WIDE STATEMENT OF ACTIVITIES

ST. JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA For the Year Ended June 30, 2009

Governmental Activities HEALTH, WELFARE & SOCIAL SERVICES SUPPORT SERVICES

Information and Assistance Outreach Recreation, Telephoning, Repair Legal Assistance Transportation Other NURITION SERVICES Congregate Meals Home Delivered Meals

Disease Prevention National Care Giver Support Senior Center Operations Building Utility Assistance Administriation

Total Governmental Activites

Program Revenues

Direct Expenses

Indirect Expenses

Operating Charges for Grants and Capital Grants &

Sen/ices Contributions Contributions

Net (Expenses) Revenues and

Increases (Decreases) in

Net Assets

Governmental Activities

$3,950 10,054 12,373

1,832 112,920 29.016

128,156 111.941

2,520 14,871 88,764

2,673 9,209

184.711

$1,081 2.752 3,387

0 62,581 35,196

19,364 31,069

434 3,814

0 0 0

(159.678)

$7,791 0 0 0 0 0

11,630 4,331

0 0 0 0 0

74

$80,577 0 0 0 0 0

161.906 72,863 2,980

16.261 0 0

8,633 1,460

712,990 23,826 344,680

General Revenues: Grants and contributions not restricted Property Taxes Loss on Disposal of leased assets Investment earnings Total general revenues and transfers

$0 0 0 0 0 0

0 0 0 0 0 0 0 0

(83,337) 12,806 15.760 1.832

175.501 64.212

(26.016) 65.816

(26) 2,424

88.764 2,673

576 23.499

344,484

62.867 293.100

(1.608) 1,068

355.427

INCREASE IN NET ASSETS

Net assets-beginning

Net Assets-ending

10,943

321.708

332.651

The accompanying notes are an integral part of this statement.

FUND FINANCIAL STATEMENTS

10

BALANCE SHEET GOVERNMENTAL FUNDS

ST. JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA

JUNE 30, 2009

GENERAL TITLE

FUND III B

TITLE

II IC1

TITLE

I I IC2

TITLE

IIIE

NON

MAJOR

FUNDS

LIABILITIES AND FUND BALANCES:

TOTAL

ASSETS:

Cash

Grants Receivable

Due From Other Funds

Prepaid Expenditures:

Insurance

Insurance

Total Assets

$289,944

0

0

2,486

.7,612

300.042

$0

0

3,525

0

0

3.525

$0

0

5,995

0

0

5,995

$0

0

7,921

0

0

7,921

$0

0

8,274

0

0

8,274

$1,912

0

130

0

0

2,042

$291,856

0

25,845

2,486

7,612

327,799

LIABILITIES; Accounts Payable

Payroll Taxes Payable

Due to Other Funds

Deferred Cruise Revenue

Total Liabilities

FUND BALANCES:

Reserved For:

Utilities

Unreserved-Undesignated

Total Fund Balance

Total Liabilities and Fund Balances

$9,500

4,236

25.845

8,115

47,696

0

252,346

252.346

300,042

$3,525

0

0

0

3,525

0

0

0

3,525

$5,995

0

0

0

5,995

0

0

0

5,995

$7,921

0

0

0

7,921

0

0

0

7,921

$8,274

0

0

0

8.274

0

0

0

8,274

$130

0

0

0

130

1,912

0

1,912

2.042

$35,345

4,236

25,845

8,115

73,541

1.912

252,346

254.258

327.799

The accompanying notes are an integral part of this statement.

11

RECONCILIATION OF TOTAL GOVERNMENTAL FTJND BALANCE TO THE GOVERNMENT-WIDE FINANCIAL STATEMENT OF NET ASSETS

ST, JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA

JUNE 30, 2009

Amounts reported for governmental activities in the Statement of Net Assets are different because:

Total Governmental Fund Balance $254,258

Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds 78,393

Capital leases obligations are not due and payable in the current period and therefore are not reported as liabilities in governmental funds -0-

Net Assets of Governmental Activities 332,651

THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THIS STATEMENT

12

009 GENERAL

FUND

; $37,500

0

305,178

0

74

1,068

4,954

0

TITLE

IIIB

$51,533

0

0

4,022

3,769

0

0

25,944

TITLE

I I I C l

$40,648

0

0

11,630

0

0

0

57,949

TITLE

NIC 2

$33,119

0

0

4,331

0

0

0

3,744

TITLE

IIIE

$15,325

0

0

0

0

0

0

936

SENIOR

CENTER

$34,293

0

0

0

0

0

0

29,016

NON-

MAJOR

FUNDS

$45,529

8,633

0

0

10,000

0

0

8,424

TOTAL

$257,947

8,633

305,178

19,983

13,843

1,068

4,954

126,013

348,774 85,268 110,227 41,194 16,261 63,309 72,586 737,619

ST JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA STATEMENT OF REVENUE AND EXPENDITURES AND CHANGES IN FUND BALANCES GOVERNMENTAL FUNDS FOR THE YEAR ENDED JUNE 30, 2009

REVENUE: INTERGOVERMENTAL:

GOVERNOR OFFICE OF ELDERLY AFFAIRS

East Baton Rouge Council on Aging

AD VALOREM TAXES

PUBLIC SUPPORT:

PARTICIPANT CONTRIBUTIONS

OTHER SUPPORT

INTEREST INCOME

MISCELLANEOUS INCOME

INKIND CONTRIBUTIONS

Total Revenue

EXPENDITURES: HEALTH & WELFARE & SOCIAL SERVICES

CURRENT

SALARIES

FRINGE

TRAVEL

OPERATING SERVICES

OPERATING SUPPLIES

OTHER

MEALS

CAPITAL OUTLAY

UTILITIY ASSISTANCE

DEBT SERVICE:

PRINCIPAL RETIREMENT

INTEREST EXPENSE

INTERGOVERMENTAL:

IN-KIND EXPENDITURES

Total Expenditures

EXCESS OF REVENUE OVER

(UNDER) EXPENDITURES

OTHER FINANCIAL SOURCES (USES):

TRANSFERS IN

TRANSFER OUT

Net Changes in Fund Balances

Fund Balances - Beginning

Adjustments to increase beginning

Fund Balances

Fund Balances - Beginning, as restated

0

0

0

0

0

12,374

0

45,756

0

1,406

186

0

0

102,224

13.733

2,236

48,876

35.353

15,104

0

0

0

0

0

0

25,944

7,586

2,593

513

7,690

670

311

70,208

0

0

0

0

0

57.949

35,782

7,058

16,284

12,810

1,116

519

62,406

0

0

0

0

0

3,744

1,527

504

100

1,493

130

13,995

0

0

0

0

0

0

936

47,707

5,319

376

5,628

490

228

0

0

0

0

0

0

29,016

5.004

1,840

364

8,360

1,457

7.772

0

2,673

9.209

0

0

0

8.424

199.830

31.047

19,873

84.857

39,216

50,303

132,614

48,429

9,209

1.406

186

0

126,013

59.722

289,052

0

(293,840)

(293,840)

243.470

(158,202)

158,202

0

158,202

147.520

(37,293)

37,293

0

37.293

139,719

(98,525)

98.525

0

98,525

18,685

(2,424)

2,424

0

2,424

88,764

(25.455)

25,455

0

25.455

45,103

27,483

7,776

(35.835)

(28,059)

742,983

(5,364)

329,675

(329.675)

0

(4.788)

211,378

0

0

0

0

0

0

0

0

0

0

(576)

2.488

(5,364)

213,866

Fund Balances - Ending

45,756

257,134

252.346

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

2,488

1,912

45,756

259,622

254,258

The accompanying notes are an integral part of this statement. 13

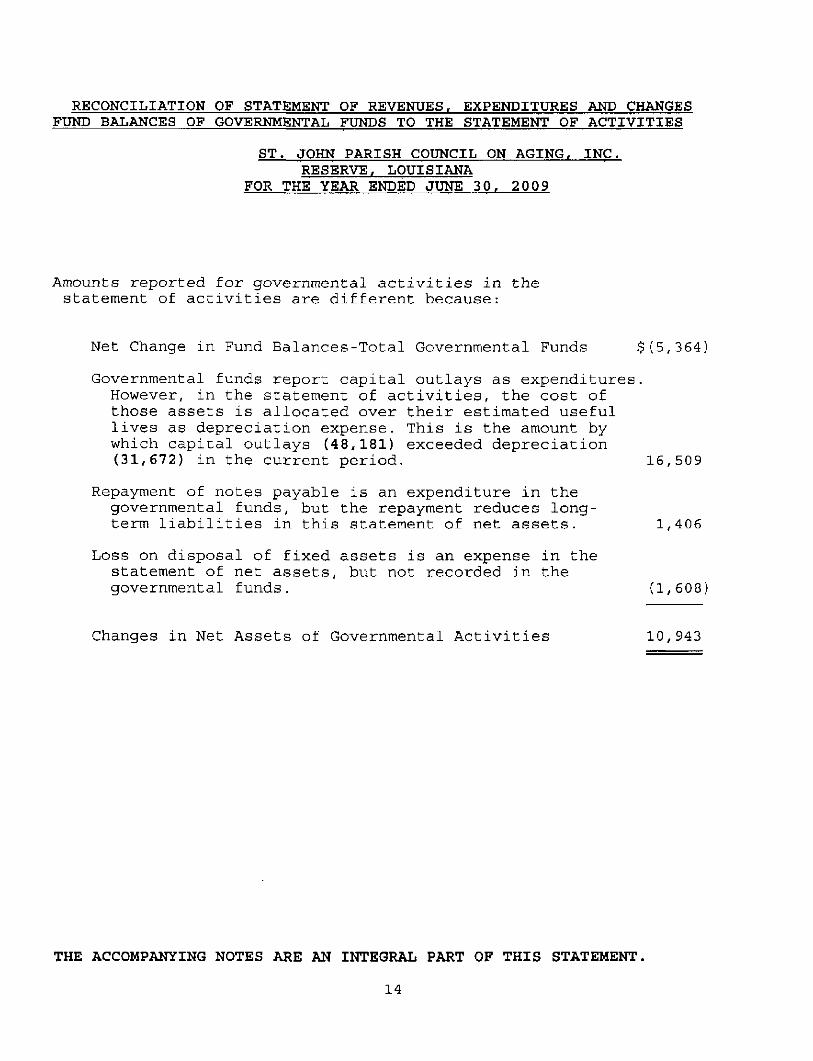

RECONCILIATION OF STATEMENT OF REVENUES, EXPENDITURES AND CHANGES FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES

ST. JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA

FOR THE YEAR ENDED JUNE 30, 2009

Amounts reported for governmental activities in the statement of activities are different because:

Net Change in Fund Balances-Total Governmental Funds $(5,364)

Governmental funds report capital outlays as expenditures. However, in the statement of activities, the cost of those assets is allocated over their estimated useful lives as depreciation expense. This is the amount by which capital outlays (48,181) exceeded depreciation (31,672) in the current period. 16,509

Repayment of notes payable is an expenditure in the governmental funds, but the repayment reduces long-term liabilities in this statement of net assets. 1,406

Loss on disposal of fixed assets is an expense in the statement of net assets, but not recorded in the governmental funds. (1,608)

Changes in Net Assets of Governmental Activities 10,943

THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THIS STATEMENT

14

NOTES TO FINANCIAL STATEMENTS

ST. JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA

JUNE 30, 2009

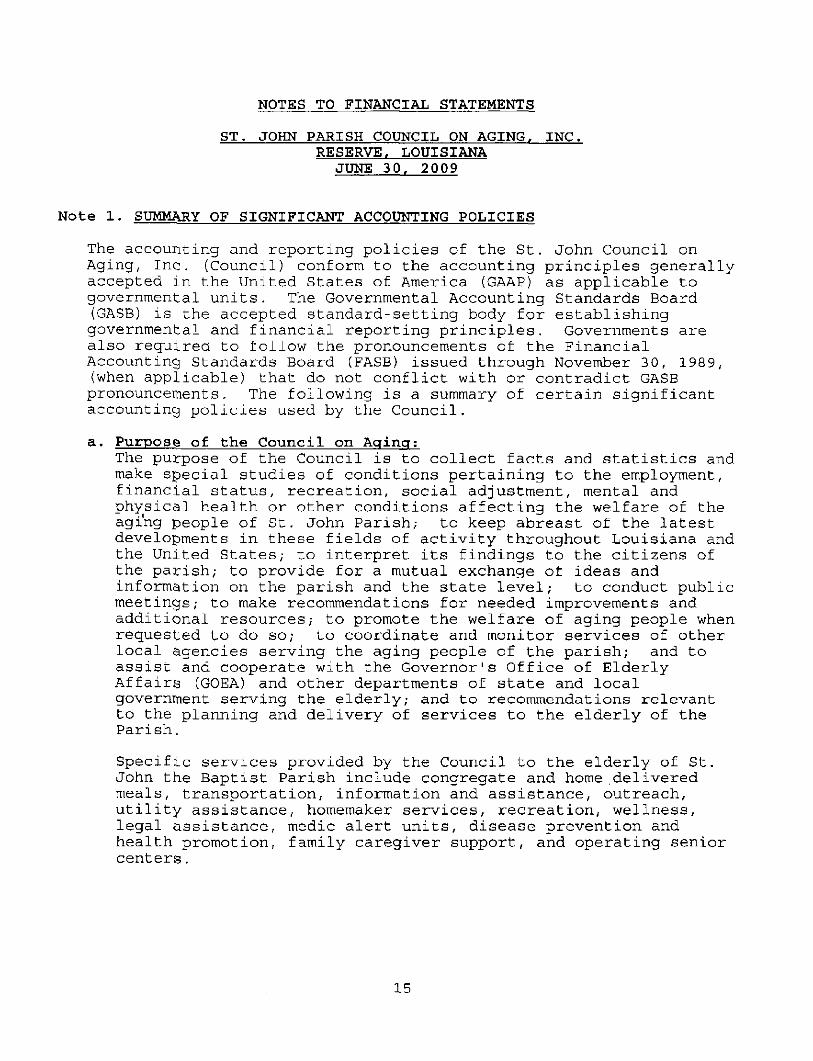

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accounting and reporting policies of the St. John Council on Aging, Inc. (Council) conform to the accounting principles generally accepted in the United States of America (GAAP) as applicable to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental and financial reporting principles. Governments are also required to follow the pronouncements of the Financial Accounting Standards Board (FASB) issued through November 30, 1989, (when applicable) that do not conflict with or contradict GASB pronouncements. The following is a summary of certain significant accounting policies used by the Council.

a. Purpose of the Council on Acrinq: The purpose of the Council is to collect facts and statistics and make special studies of conditions pertaining to the employment, financial status, recreation, social adjustment, mental and physical health or other conditions affecting the welfare of the aging people of St. John Parish; to keep abreast of the latest developments in these fields of activity throughout Louisiana and the United States; to interpret its findings to the citizens of the parish; to provide for a mutual exchange of ideas and information on the parish and the state level; to conduct public meetings; to make recommendations for needed improvements and additional resources; to promote the welfare of aging people when requested to do so; to coordinate and monitor services of other local agencies serving the aging people of the parish; and to assist and cooperate with the Governor's Office of Elderly Affairs (GOEA) and other departments of state and local government serving the elderly; and to recommendations relevant to the planning and delivery of services to the elderly of the Parish.

Specific services provided by the Council to the elderly of St. John the Baptist Parish include congregate and home delivered meals, transportation, information and assistance, outreach, utility assistance, homemaker services, recreation, wellness, legal assistance, medic alert units, disease prevention and health promotion, family caregiver support, and operating senior centers.

15

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

In 1964, the State of Louisiana passed Act 456 which authorized the charter of voluntary councils on aging for the welfare of the aging people in each parish of Louisiana. In 1979, the Louisiana Legislature created the Governor's Office of Elderly Affairs (GOEA.) (La R.S. 46:931) with the intention of GOEA administer and coordinate social services and programs for the elderly population of Louisiana through sixty-four parish voluntary councils on aging.

Before a council on aging can begin operations in a specific parish, its application for a charters must receive approval from the GOEA pursuant to LA R.S. 46:1602. Each council on aging in Louisiana must comply with the state laws apply to quasi-public agencies as well as the polices and regulations established by GOEA.

The St. John Parish Council on Aging ( the Council) is legally separate, non-profit, quasi-public corporation. It received its charter and began operations on March 28, 1973, and subsequently incorporated on May 15, 1973, under the provisions of Title 12, Chapter 2 of the Louisiana Revised Statutes.

A board of directors, consisting of fifteen voluntary members, who serve three-year terms, governs the Council. The board of directors is comprised of representatives of the Parish's general public who are interested in and have the time and desire to serve the needs of the elderly. Board members are elected by the general membership of the Council. Membership in the Council is open to the general public. Membership fees are not charged.

Based on the criteria set forth in GASB Statement 14, The Financial Reporting Entitv, the Council is not a component unit of another primary government nor does it have any component units which are related to it. In addition, based on criteria set forth in this statement, the Council has presented its financial statements as a special purpose, stand alone government; accordingly, it is applying the provisions of Statement 14 as if it were a primary government.

c. Basis of Presentation of the Basic Financial Statements;

The Council's basic financial statements consist of "government-wide" financial statements on all activities of the Council, which are designed to report the Council as a whole entity, and "fund" financial statements, which purpose are to report individual major governmental funds and combined nonmajor governmental funds.

Both the government-wide and fund financial statements categorize primary activities as either "governmental" or "business" type. The Council's functions and programs have been classified as governmental activities.

16

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

The Council does not have any business-type activities. Accordingly, the government-wide financial statements do not include any of these activities or funds.

Government-Wide Financial Statements: The government-wide financial statements include the Statement of Net Assets and the Statement of Activities for all activities of the Council. As a general rule, the effect of interfund activity has been eliminated from these statements. The government-wide presentation focuses primarily on the sustainabiHty of the Council as an entity and the change in its net assets (financial position) resulting from the activities of the current fiscal year. Governmental activities generally are supported by intergovermental and property tax revenue.

In the government-wide Statement of Net Assets only one column of numbers has been presented. The amounts are presented on a consolidated basis and represent only governmental type activities.

The Statement of Net Assets has been prepared on a full accrual, economic resource basis, which recognizes all long-term assets and receivables as well as long-term debt and obligations. The Council's net assets are reported in three parts - invested in capital assets, net of related debt; restricted net assets; and unrestricted net assets.

The government-wide Statement of Activities reports both the gross net cost of each of the Council's functions and significant programs. Many functions and programs are supported by general government revenues like intergovernmental revenues, and unrestricted investment income, particularly if the function or program has a net cost. The Statement of Activities begins by presenting gross direct and indirect expenses that include depreciation, and then reduces the expenses by related program revenues, such as operating and capital grants and contributions, to derive the net cost of each function or program. Program revenues must be directly associated with the function or program to be used directly offset its cost. Operating grants include operating-specific and discretionary (either operating or capital) grants, while the capital grants column reflects capital-specific grants.

Direct expenses reported in the Statement of Activities are those that are clearly identifiable with a specific function or program, whereas, the Council allocates its indirect expenses among various functions and programs in accordance with OMB Cicrular A-87. In addition, GOEA provided grant funds to help the Council pay for a portion of its indirect cost.

17

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

As a result, only the indirect costs in excess of the GOEA funds are allocated to the Council's other functions and programs.

In the Statement of Activities, charges for services represent program revenues obtained by the Council when it renders services that are provided by a specific function or program to people or other entities. Contributions, grants property taxes, interest income, and miscellaneous revenues that are not properly included among program revenues are reported instead as general revenues in this statement. Special items, if any, are significant transactions within the control of management that are either unusual in nature or infrequent in occurrence and are separately reported below general revenues.

Fund Financial Statements:

The fund financial statements present financial information that is very similar to that which was included in the general-purpose financial statements issued by governmental entities before Statement No. 34 required the format change.

The daily accounts and operations of the Council continue to be organized using funds and account groups. Fund accounting is designed to demonstrate legal compliance and to aid financial management by segregating transactions relating to certain governmental functions or activities. The operations of each fund are accounted for with a separate set of self-balancing accounts that comprise it assets, liabilities, equity, revenues and expenditures. Governmental Resources are allocated to and accounted for in individual funds based upon the purpose for which they are to be spent and the means by which spending activities are controlled. The various funds are reported by generic classification within the financial statements.

The Council uses governmental fund types. The focus of the governmental funds' measurement (in the fund statements) is on determination of financial position and changes in financial position (sources, uses, and balances of financial resources) rather than on net income. An additional emphasis is placed on major funds within the governmental fund types. A fund is considered major if it is the primary operating fund of the Council or if its total assets, liabilities, revenues or expenditures are at least 10% of the corresponding total for all funds of that category or type into a single column in the fund financial statements.

18

Note 1. SUMMARY OF SIGNIFICAl^ ACCOUNTING POLICIES - (Continued)

Governmental fund equity is called the fund balance. Fund balance is further classified as reserved and unreserved, with unreserved being further split into designated and undesignated. Reserved means that the fund balance is not available for expenditure because resources have already been expended (but not consumed), or a legally restriction has been placed on certain assets that makes them only available to meet future obligations. Designated fund balances result when management tentatively sets aside or earmarks certain resources to expend in a designated manner. In contrast to reserved fund balances, designated amounts can be changed at the discretion of management.

The following is a description of the governmental funds of the Council:

General Fund is the primary operating fund of the Council and it accounts for all financial resources except those required to be accounted for in another fund. The following are brief descriptions of the programs that comprise the Council's General Fund:

General

The Council receives revenues that are not required to be accounted for in a specific program or fund. Accordingly, revenues, such as: proceeds of a property tax, assessment, donation from the general public, allocations from the United Way, interest income earned on unrestricted fund balances, and net proceeds from the sale of fixed assets, are recorded in the local program of the General Fund. Most funds are unrestricted and may be used at the Council's discretion. Expenditures to acquire fixed assets, and expenditures for costs not allowed by another program due to the budget limitations or the nature of the expenditure, are generally charged to the local program.

Because of their unrestricted nature, local funds are often transferred to other programs to eliminate deficits in cases where the expenditures of the other programs exceeded their revenues.

Also in the General Fund are PCOA funds are appropriated for the Council by Louisiana Legislature and remitted to the Council via the Governor's Office of Elderly Affairs (GOEA). The Council may use these "Act 735" funds at its discretion provided the program is benefiting people who are at least 60 years old. In this fiscal year, the Council transferred all of its PCOA funds to the Title III B fund to pay for program expenditures exceeding the grant reimbursements from GOEA.

19

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

Special Revenue Foonds are used to account for the proceeds of specific revenue sources that are legally restricted to expenditures for specific purposes. The Council has established several special revenue funds. The following are brief descriptions of the purpose of each special revenue fund and their classification as either a major or nonmajor governmental fund:

MAJOR SPECIAL REVENUE FUNDS

The Title III B Fund accounts for funds that are used to provide various units of supportive social services to the elderly. GOEA has established the criteria for defining a qualifying unit of service for each of Title III program. Specific supportive social services, along with the numiber of units provided during the fiscal year, are as follows:

Transportation For People Age 60 17,039 Legal Assistance 3 5 Information and Assistance 382 Outreach 285

The Title III-C-1 Fund accounts for funds which are used to provide nutritional, congregate meals to people age 60 or older at senior centers in LaPlace and Edgard and at an additional meal site in Place DuBourg. During the fiscal year the Council served about 22,198 meals to people eligible to participate in this program. In addition to the meals serviced, the Council also provided 624 units of nutritional education to eligible participants under this program.

The Title III-C-2 Fund accounts for funds which provide nutritional meals to homebound people who are age 60 or older. During the fiscal year the Council provided 21,704 hone-delivered meals.

Title III-E Funds accounts for funds relating to the National Family Caregiver Support Program. The National Family Caregiver Support program is designed to provide multifaceted systems of support services for family caregivers and for grandparents or older individuals who are relative caregivers. This program targets older, low-income individuals. Specific types of services that can be provided by this program include: Adult Day Care, Adult Health Care, Material Aid, Case Management, Personal Care, Counseling, Support Groups, Respite Care, Sitter Service, and Information and Assistance,

20

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

Title III-E Funds accounts for funds relating to the National Family Caregiver Support Program. The National Family Caregiver Support program is designed to provide multifaceted systems of support services for family caregivers and for grandparents or older individuals who are relative caregivers. This program targets older, low-income individuals. Specific types of services that can be provided by this program include: Adult Day Care, Adult Health Care, Material Aid, Case Management, Personal Care, Counseling, Support Groups, Respite Care, Sitter Service, and Information and Assistance.

Eligible participants include (1) adult family members, another adult person, who provides uncompensated in-home and community care to an older person who needs supportive services or (2) grandparents, or a person 60 years of age or older, who is related to a child by blood or marriage and (1) lives with the child, (2) is the primary caregiver, and (3) has a legal relationship to the child or is raising the child informally. During the fiscal year, the Council provided 690 units of NFCSP In-Home Respite and 346 units of NFCSP Sitter Service and 54 units of NFCSP Public Education.

Senior Center Fund is used to account for the administration of Senior Center program funds appropriated by the Louisiana Legislature to the GOEA, which "passes through" the funds to the Council. This purpose of this program is to provide a community service center at which elderly people can receive supportive social services and participate in activities which foster their independence, enhance their dignity, and encourage their involvement in and with the community. The Council's senior centers are located in LaPlace and Edgard. Senior Center funds can be used at management's discretion to support any of the Council's programs that benefit the elderly. During the fiscal year, the Council used its Senior Center funds to pay for the costs of operating the senior citizens centers.

NON-MAJOR SPECIAL REVENUE FUNDS

The Title III-D Funds accounts for funds used for medication management and disease prevention and health promotion activities. During the fiscal year, the Council provided 1,637 units of wellness service and 957 medication management were provided to eligible participants in this program.

The Title III C Area Agency Administration Fund is used to account for a portion of the indirect costs of administering the Council's Programs. Each fiscal year GOEA provides the Council with funds to help pay for the costs of administering the Council's special programs for the aging. The amount of funding is not enough to pay for all the indirect cost. As a result, the Council will allocate its indirect cost to this fund first.

21

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

Once the GOEA funds are completely used, any indirect costs in excess of the funds provided by GOEA, are distributed to the Other funds and program using a formula based on the percentage each program's direct cost bears to direct costs for all programs. Indirect costs are not allocated to all funds because program restrictions may prohibit or limit the payment of administrative type costs.

The Supplemental Senior Center Fund was established to account for the funds that were appropriated by the Louisiana Legislature for the various councils on aging throughout Louisiana to supplement each Council's primary grant for senior center operations and activities. The Council was one of the parish councils to receive a supplemental grant of $3,100. GOEA provided these funds to the Council. The money received by this fund during the year was transferred to the Title III B Fund to pay for the costs of operating the centers.

The N.S.l.P Fund is used to account for the administration of Nutrition Services Incentive Program funds provided by the Administration on Aging, U.S.Department of Health and Human Services, To GOEA, which in turn "passes through" the funds to the Council. GOEA distributes NSIP funds to each parish council on aging in Louisiana based on how many meals each council on aging served in the previous year in relation to total meals served statewide by all councils. The primary purpose of the NSIP reimbursement is to provide money to buy food that will be used in the preparation of congregate and home-delivered meals under nutrition service programs. The food that is purchased for these purposes must be of United States origin or be commodities from the United State Department of Agriculture.

Audit Fund is used to account for funds received from the Governor's Office of Elderly Affairs that are restricted to use as a supplement to pay the cost of having an annual audit of the Council's financial statements. The cost of the audit was $6,563 whereas the supplement was $1,460. The additional audit expense was paid by a transfer of funds from the General Fund.

The Utility Assistance Fund is used to account for the administration of utility assistance programs that are sponsored by local utility companies. The companies collect contributions from service customers and remit the funds to the Parish Councils on the aging to provide assistance to the elderly for the payment of utility bills. The Council receives its Project Care donations directly from Capital Area Agency on Aging. During the year, the Council was able to provide 57 units of service with these funds. The maximum amount of assistance a person can receive in one year is usually limited to $200 from each program.

United Way Fund is used to account for the funds provided by United Way to be used for food for the elderly.

22

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

The Building Fund is used to account for the funds provided by insurance to cover the damage caused by Hurricane Katrina and the move to a new building.

d. Measurement Focus and Basis of Accounting

Measurement focus is a term used to describe "which" transactions are recorded within the various financial statements. Basis of accounting refers to "when" transactions are recorded regardless of the measurement focus applied.

Government-Wide Financial Statements - Accrual Basis The government-wide financial statements are prepared using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recognized when a liability is incurred, regardless of the timing of related cash flows.

Modified Accrual Basis - Fund Financial Statements (FFS) Governmental fund level financial statements are reported using a current financial resources measurement focus and the modified accrual basis of accounting. A current financial resources measurement focus means that only current assets and current liabilities are generally included on the fund balance sheet. The operating statements of these funds present increases (revenues and other financing sources) and decreases (expenditures and other uses) in net current assets. Under the modified accrual basis of accounting, revenues are recorded when susceptible to accrual (i.e. when they become both measurable and available), "Measurable" means the amount of the transaction can be determined and available means collectible within the current period or soon enough thereafter to pay liabilities of the current period. The Council considers all revenues "available" if they are collected within 60 days after year end. Expenditures are generally recorded under modified accrual basis of accounting when the related liability in incurred. The exceptions to this general rule are that (1) unmatured principal and interest on long-term debt, if any, are recorded when due, and (2) claims and judgements and compensated absences are recorded as expenditures when paid expendable available financial resource resources.

e. Interfund Activities

In the fund financial statements, interfund activity is reported as either loans or transfers. Loans between funds are reported as interfund receivables (due from) and payables (due from) as appropriate. Transfers represent a permanent re-allocation of resources between funds. In other words, they are not expected to be repaid.

23

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

Transfers between funds are netted against one another as part of the reconciliation of the change in fund balances in the fund financial statements to the change in net assets in the government-wide financial statements.

f. Cash

Cash includes not only currency on hand, but also demand deposits with banks or financial institutions. For purposes of the Statement of Net Assets restricted cash are amounts received or earned by the Council with an explicit understanding between the Council and the resource provider that the resource would be used for a specific purpose.

g. Receivables

The financial statements for the Council do not contain an allowance for uncollectible receivables because management believes all amounts will be collected. However, if management becomes aware of information that would change its assessment about the collectibility of any receivable, management would write off the receivable as a bad debt at that time.

h. Prepaid Expenses/Expenditures

Prepaid expenses include amounts paid for services in advance. These are shown as assets on the Government-Wide Statement of Net Assets. In the Fund Financial Statements, the Council has elected not to include amounts paid for future services as expenditures until those services are consumed to comply with the cost reimbursement terms of grant agreements. As a result, the prepaid expenditures are shown as an asset on the balance sheet of the Fund Financial Statements until they are consumed. In addition, a corresponding amount of the fund balance of the General Fund has been reserved to reflect the amount of fund balance not currently available for expenditure.

i. Capital Assets

The accounting and reporting treatment used for property, vehicles, and equipment (capital assets) depends on whether the capital assets are reported in the government-wide financial statements or the fund financial statements.

Government-Wide Financial Statements

Capital assets are long-lived assets that have been purchased or acquired with an original cost of at lease $1,000 and that have an estimated useful life of greater than one year. When purchased or acquired, these assets are recorded as capital assets in the government-wide Statement of Net Assets.

24

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

In contrast, in the Fund Financial Statements, capital assets are recorded as expenditures of the fund that provide the resources to acquire the assets. If the asset purchased, it is recorded in the books at it cost. If the asset was donated, when it is recorded at its estimated fair market value at the date of donation.

For capital assets recorded in the government-wide Financial Statements, depreciation is computed and recorded using the straight-line method for the asset's estimated useful life. The estimated useful lives of the various classes of despicable capital assets are as follows:

Equipment 6 to 10 Years Vehicles 5 Years Computers 5 Years Building Improvements 40 Years

When calculating depreciation, the State's guideline assumes that capital assets will not have any salvage value and that a full year's worth of depreciation will be taken in the year the capital assets are placed in service or disposed.

FUND FINANCIAL STATEMENTS

In the fund financial statements, capital assets used in the Council's operations are accounted for as capital outlay expenditures of the governmental fund that provided the resource to acquire the assets. Depreciation is not computed or recorded on capital assets for purposes of the fund financial statements.

j. Non-Current (Long-term) Liabilities

The accounting treatment of non-current liabilities depends on whether they are reported in the government-wide or fund financial statements. In government-wide financial statements, all non-current liabilities that will be repaid from governmental resources are reported as liabilities in the government-wide statements. In the fund financial statements, non-current liabilities for governmental funds are not reported as liabilities or presented anywhere else in these funds.

k. Unpaid Compensated Absences:

The Council's annual and sick leave policies require employes to consume any annual or sick leave they might earn within the Council's fiscal year. In other words, an employee must "use or lose" any earned leave on or before June 30th of every year. As a result the Council has not accrued a liability for any unused leave in the financial statements.

25

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

The Council's management has this policy to minimize the Council's exposure to a liability for which the Council may not have funds to pay.

1. Advances From Funding Agencies

Advances from funding agency represent unexpended balances of grant awarded to the Council that are required to be returned to the funding agency at the end of the grant period. Grant funds due back to the funding agency are recorded as a liability when the amount due becomes known, normally when a final accounting is submitted to the funding agency.

m. Deferred Revenue

The Council reports deferred grant revenue on both the Statement of Net Assets (government-wide) and Balance Sheet of the fund

Deferred property tax revenues arise when property taxes are expected to be received but not within 60 days after the end of the Council's fiscal year in which the taxes were levied. Deferred property tax revenues are reported on the Balance Sheet of the fund financial statements, but not the Statement of Net Assets, because the related revenues are recognized in the Statement of Activities using the full accrual basis of accounting. In subsequent periods when the deferred property tax revenues are collected, the deferral is removed from the Balance Sheet of the funds financial statements and the revenue is recognized.

n. Net Assets in the Government-wide Financial Statements

In the government-wide Statement of Net Assets, the Net Asset amount is classified and displayed in three components:

Invested in capital assets, net of related debt - This component consist of capital assets including restricted capital assets, net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes, capital lease obligations or other borrowings that are attributed to the acquisition, construction, or improvement of those capital assets. At year-end the Council had capital lease obligations that were related to capital assets.

26

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

Restricted net assets - This component consist of net assets with constraints placed on their use either by (1) external groups such as creditors, grantors, contributors, or laws or regulations of other governments; or (2) law through constitutional provisions.

Unrestricted net assets - This component consist of all other net assets that do not meet the definition of "restricted" or "invested in capital assets."

When both restricted and unrestricted resources are available for use in a specific program or for a specific purpose, the Council's policy is to use restricted resources first to finance its activities, except for nutrition services. When providing nutrition services, revenues earned by the Council under its NSIP contract with GOEA can only be used to pay for raw food component of each meal that is bought and served to person eligible to receive a meal under on of the nutrition programs. The Council's management has discretion as to how and when to use the NSIP revenue when paying for nutrition program costs. Quite often, unrestricted resources are available for use that must be consumed or they will have to be returned to the grantor agency. In such cases it is better for management to elect to apply and consume the unrestricted resources before using the restricted resources. As a result, in this case, the Council will depart from its usual policy of using resources first.

0. Fund Eguity - Fund Financial Statements

Governmental fund equity is classified as fund balance. Fund balance may be further classified as reserved and unreserved^ with unreserved further split into designated and undesignated. Reserve means that the Council has "reserved" portions of its fund balance that are not available for expenditure because resources have already been expended (but not consumed), or a legal restriction has been placed on certain assets which make them only available to meet future obligations.

Designated fund balances result when the Council's management intendeds to expend certain resources in designated manner. Designations of fund balances can be changed at the discretion of the Council's Board of Directors. There were no designated fund balances at year-end.

p. Management's Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect certain reported amounts and disclosures. Accordingly, actual results may differ from those estimates.

27

Note 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - (Continued)

q. Allocation of Indirect Expenses:

The Council reports all direct expenses by function and programs of functions in the Statement of Activities. Direct expenses are those that are clearly identifiable with a function or program. Indirect expenses are recorded as direct expenses of the Administration function. The net cost of the Administration functions is allocated using formula that is based on primarily on the relationship the direct cost a program bears to the direct cost of all programs. There are some programs that cannot absorb any direct cost allocation according to their grant or contract restrictions.

r, Elimination and Reclassifications

In the process of aggregating data for the Statement of Net Assets and Statement of Activities, some amounts reported as interfund activity and balances in the funds were eliminated or reclassified. Interfund receivables and payables were eliminated to minimize the "grossing up" effect on assets and liabilities within the governmental activities column.

NOTE 2 - REVENUE RECOGNITION

Revenues are recorded in the Government-Wide Statements when they are earned under the accrual basis of accounting.

Revenues are recorded in the Fund Financial Statements governmental using the modified accrual basis of accounting. In applying the susceptible to accrual concept using this basis of accounting, intergovernmental grant revenues, program service fees, and interest income are usually both measurable and available. However, the timing and amounts of the receipts of public support and miscellaneous revenues are often difficult to measure; therefore they are recorded as revenue in the period received.

Note 3. PROPERTY TAX

During the fiscal year 1995, the Council began receiving funds from a property tax which was adopted by the voters of St. John the Baptist Parish to provide money to finance the Council's operations. The Parish's Assessor began levying the property tax on November 15, 1994, and continued to do so each year through November 15, 2003. The voters renewed the property tax for an additional ten years in July 2004. The tax is based upon the assessed (appraised) value, less homestead exemptions, on all real and business personal property located within the Parish. The 1st of January preceding the annual levy date (November 15th) is used as the date to value the property subject to tax.

28

Note 3. PROPERTY TAX - (Continued)

The gross taxable value for the tax year 2008, of the certified tax roll was $296,733,636. After applying homestead exemptions of $83,574,781, the total value upon which the Council's property tax was computed was $380,308,417. The Council elected to assess property owners the legal maximum of one mill for the tax year 2008. Accordingly, management estimates the gross amount of property tax payable to the Council for the fiscal year to be approximately $3 05,17 8.

Property taxes are due on November 15 and are considered delinquent if not paid by December 31. Most of the property taxes are collected during the months of December, January and February. The St. John the Baptist Parish Sheriff acts as the collection agent for property taxes. The Sheriff will also have a "tax sale" in May or June of each year to try and collect as much of the taxes due as possible. Following the tax sale, the Sheriff will file tax liens to ensure collection of unpaid taxes at some future date.

Property taxes are recorded as receivables and deferred revenues at the time the tax levy is billed. As the Sheriff collects the taxes, they are forwarded to the St. John the Baptist Parish Council where they are deposited into a separate account maintained by the Parish Council for the benefit of the Council on Aging. However, the Council on Aging does not recognize revenue in the fund financial statement until the Parish Council remits the property taxes to it. Under the modified accrual basis of accounting the property taxes are not "available" to the Council until the Parish releases the funds.

Based on information available to management at the time these financial statement were prepared, management estimates $305,178 (approximately 100%) of the property taxes due from the tax year 2008 tax assessment will be collected.

The property tax revenues reported in the fund financial statements do not include any amounts ($-0-) that are due and remain uncollected by the sheriff. However, property tax revenue include amounts ($12,078) withheld by the Sheriff to make "on behalf payment for fringe benefits" which represent the Council's pro-rata share of retirement plan contributions for other governmental units. A corresponding intergovernmental expenditure of $12,078 has also been presented in that financial statement. For purposes of the government-wide Statement of Activities, property tax revenues of $305,178 were reduced by the $12,078 withheld by the Sheriff producing net property tax revenue of $293,100, which was a component of general revenues on that statement.

29

NOTE 4 - CASH

The Council maintains a consolidated bank account to deposit the money it collects and to pay its bills. The consolidated bank account is available for use by all funds. The purpose of this consolidated account is to reduce administration costs and facilitate cash management. The consolidated account also allows those funds with available cash balances to cover any negative cash balances in other funds at year end. At year end, the Council has cash and cash equivalent (book balances) totaling $291,856.

These deposits are stated at cost, which approximates market. Under state law, these deposits (or the resulting bank balances) must be secured by federal deposit insurance or the pledge of securities owned by the fiscal agent bank. The market value of the pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent.

These securities are held in the name of the pledging fiscal agent bank in a holding or custodial bank that is mutually acceptable to both parties.

Custodial Credit Risk-Deposits. At year-end the bank balance was $290,989. Of the bank balances, $250,000 was covered by federal depository insurance. $198,232 was collateralized with securities held by the pledging financial institution's trust department or agent but not in the Council's name (GASB Category 3).

GASB Statement 3 categorizes deposits into three categories of credit risk:

1. Insured by FDIC or collateralized with securities held by the Council or by its agent in the Council's name. (Category 1)

2. Uninsured but collateralized with securities held by the pledging financial institution trust department or agent in the Council's name. (Category 2)

3. Uninsured and uncollateralized; or collateralized with securities held by the pledging financial institution, or by its trust department or agent but not in the Council name; or collateralized with no written or approved collateral agreement. (Category 3)

Even though the pledged securities are considered uncollateralized (Category 3) under the provisions of GASB Statement 3, Louisiana R.S. 39:1229 imposes a statutory requirement on the custodial bank to advertise and sell the pledge securities within 10 days of being notified by the Council that the fiscal agent has failed to pay deposited funds upon demand.

Interest Rate-Deposits. The Council's policy does not address interest rate risk.

30

NOTE 4 - CASH (Continued)

Under state law, all bank deposits must be (1) secured by federal deposit insurance or by the pledge of securities owned by the fiscal agent bank, or (2) invested exclusively in instruments backed by the U.S. government. The fair value of the pledged securities plus the federal deposit insurance must always equal or exceed the amount on deposit with the fiscal agent.

NOTE 5 - GOVERNMENT GRANTS AND CONTRACTS RECEIVABLE

Government grants and contracts receivable represent amounts owed to the Council under a grant award or contract with a provider of federal, state, or local funds; such amounts being measurable and available as of year end. Government grants and contracts receivable at year end consist of reimbursements for expenses incurred under the following programs:

FUNDING PROGRAM FUND AGENCY AMOUNT

None

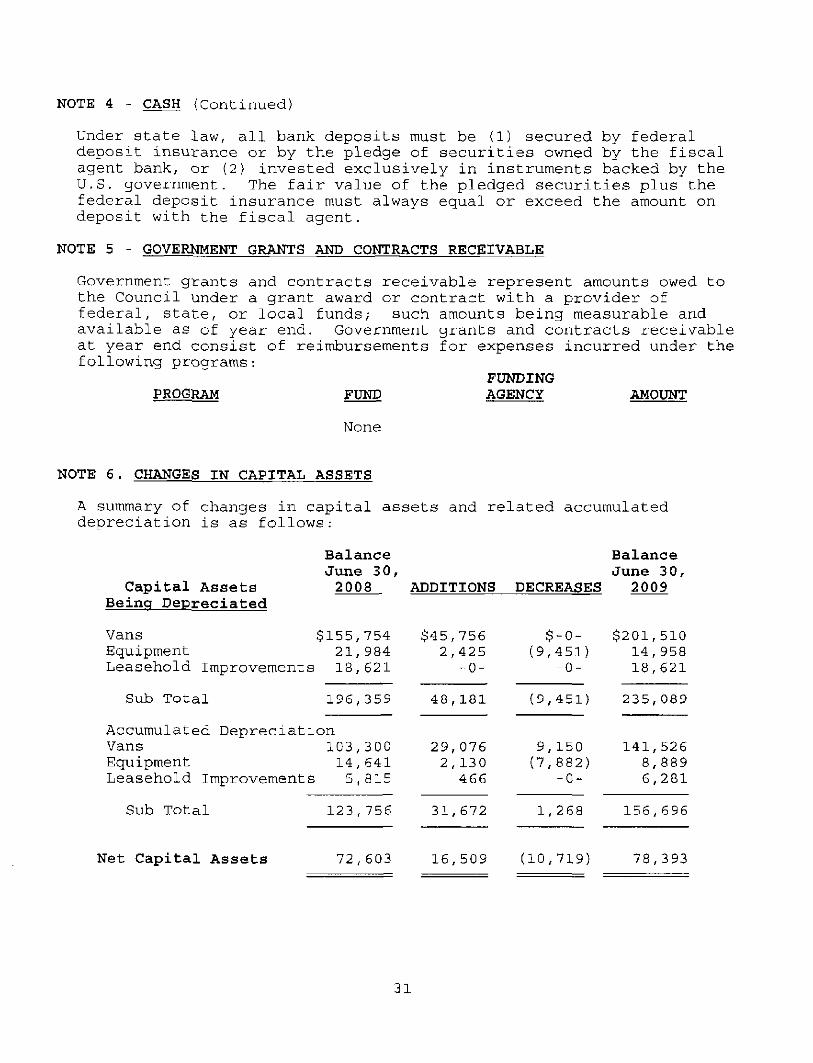

NOTE 6. CHANGES IN CAPITAL ASSETS

A summary of changes in capital assets and related accumulated depreciation is as follows:

Balance Balance June 3 0, June 3 0,

Capital Assets 2008 ADDITIONS DECREASES 2009 Being Depreciated

Vans $155,754 $45,756 $-0- $201,510 Equipment 21,984 2,42 5 (9,451) 14,958 Leasehold Improvements 18,621 -0- -0- 18,621

Sub Total 196,359 48,181 (9,451) 235,089

Accumulated Depreciation Vans 103,300 29,076 9,150 141,526 Equipment 14,641 2,130 (7,882) 8,889 Leasehold Improvements 5,815 466 -0- 6,281

Sub Total 123,756 31,672 1,268 156,696

Net Capital Assets 72,603 16,509 (10,719) 78,393

31

NOTE 6. CHANGES IN CAPITAL ASSETS (Continued)

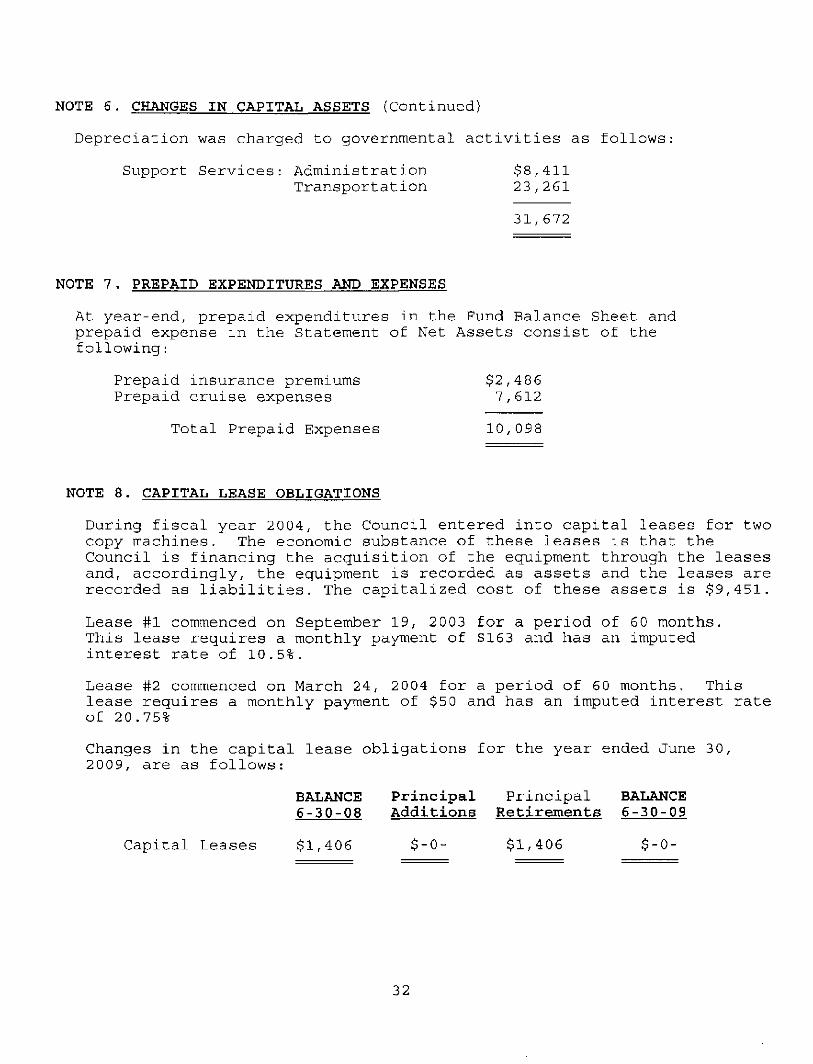

Depreciation was charged to governmental activities as follows

Support Services: Administration $8,411 Transportation 23,261

31,672

NOTE 7. PREPAID EXPENDITURES AND EXPENSES

At year-end, prepaid expenditures in the Fund Balance Sheet and prepaid expense in the Statement of Net Assets consist of the following:

Prepaid insurance premiums $2,486 Prepaid cruise expenses 7,612

Total Prepaid Expenses 10,098

NOTE 8. CAPITAL LEASE OBLIGATIONS

During fiscal year 2004, the Council entered into capital leases for two copy machines. The economic substance of these leases is that the Council is financing the acquisition of the equipment through the leases and, accordingly, the equipment is recorded as assets and the leases are recorded as liabilities. The capitalized cost of these assets is $9,451.

Lease #1 commenced on September 19, 2 003 for a period of 60 months. This lease requires a monthly payment of $163 and has an imputed interest rate of 10.5%.

Lease #2 commenced on March 24, 2004 for a period of 60 months. This lease requires a monthly payment of $50 and has an imputed interest rate of 20.75%

Changes in the capital lease obligations for the year ended June 30, 2009, are as follows:

BALANCE Principal Principal BALANCE 6-30-08 Additions Retirements 6-30-09

Capital Leases $1,406 $-0- $1,406 $-0-

32

NOTE 8. CAPITAL LEASE OBLIGATIONS (Continued)

There are no future minimum payments under capital leases as of June 30 2009.

NOTE 9. FUND BALANCES - FUND FINANCIAL STATEMENTS

At year-end, one special revenue fund had a remaining fund balance. Usually, the fund balances of the special revenue funds are cleared out a year-end to comply with the administration and accounting policies of the grantor agencies that have award the Council certain grants. However, there are exceptions to these policies.

The Council has $1,912 of utility assistance contributions that remain unspent as of year-end. The donors restrict these contributions for specific purposes. Accordingly, management separately accounts for them in a special revenue fund to ensure accountability.

Utility assistance fund balances are common amongst council on aging entities. Utility assistance is a supportive service rendered under the Council's Title III B program. Rather than commingle the accounting of the receipts and disbursements of the utility assistance within the Title III B Fund, GOEA prefers that councils on aging use a separate fund that can facilitate the monitoring of other Title III B activities separately for the utility assistance activities.

NOTE 10. PRIOR PERIOD ADJUSTMENTS

Fund balances at July 1, 2008, have been increased as follows in relation to the activities of prior years:

General Fund A $45,756 adjustment to properly correct the purchase of a van paid prior to June, 30, 2008, but was not received until after the June 30, 2008 year-end.

NOTE 11. BOARD OF DIRECTORS' COMPENSATION

The Board of Directors is a voluntary board; therefore, no compensation has been paid to any member. However, board members are reimbursed for out-of-town travel expenses incurred in accordance with the Council's reimbursement policy.

33

NOTE 12, IN-KIND DONATIONS

The Council received $126,013 in in-kind contributions during the year which have been valued at their estimated fair market value, and presented in this report as revenue. Related expenditures, equal to the in-kind revenues, have also been presented, thereby producing no effect on net income (loss) in the governmental fund types.

The primary in-kind contributions consist of free rent and utilities for a meal site.

A summary of the in-kind contributions and their respective assigned values is a follows:

Salaries $32,413 Buildings 93,600

Total In-Kind Contributions 126,013

NOTE 13. - INCOME TAX STATUS

The Council, a not-for-profit corporation, is exempt from federal income taxation under section 501, (C) (3) of the Internal Revenue Code of 1986 and as an organization that is not a private foundation as defined in Section 509 (a) of the Code. It is also exempt from Louisiana income

tax.

NOTE 14. JUDGEMENTS, CLAIMS AND SIMILAR CONTINGENCIES

There is no litigation pending against the Council as of year-end. The Council's management believes that any potential lawsuits would be adequately covered by insurance or resolved without any material impact upon the Council's financial statements.

No claims were paid-out or litigation costs incurred during the year ended June 30, 2 009.

34

NOTE 15. RISK MANAGEMENT

The Council is exposed to various risks of loss related to torts; thefts of, damage to, and destruction of assets; errors and omissions; injuries to employees; and natural disasters. The Council has purchased commercial insurance to cover or reduce the risk of loss that might arise should one of these incidents occur. There have been no significant reductions in coverage for the prior year. No settlements were made during the year that exceeded the Council's coverages.

The Council's management has not purchased commercial insurance or made provision to cover or reduce the risk of loss, as a result of business interruption and certain acts of God, like floods or earthquakes.

NOTE 16. CONTINGENCIES-GRANT PROGRAMS

The Council participates in a number of state and federal grant programs, which are governed by various rules and regulations. Cost charged to the respective grant programs are subject to audit by the grantor agencies; Therefore, to the extent that the Council has not complied with the rules and regulations governing the grants, refunds of any money received and the collectibility of any related receivable at year-end may be impaired. In management's opinion, there are no significant contingent liabilities relating to compliance with the rules and regulations governing state and federal grants; therefore, no provision has been recorded in the accompanying financial statements for such contingencies. Audits of prior years have not resulted in any significant disallowed costs or refunds. Any costs that would be disallowed would be recognized in the period agreed upon by the grantor agency and the Council.

NOTE 17. ECONOMIC DEPENDENCY

The Council receives the majority of its revenue from a property tax assessment and through grants administered by the Louisiana Governor's Office of Elderly Affairs (GOEA). The grant amounts are appropriated each year by the federal and state governments. If significant budget cuts are made at the federal and/or state level, the amount of funds the Council receives could be reduced significantly and have an adverse impact on its operations. Also, if the property in St. John the Baptist Parish were to be assessed at lower values due to natural disaster or another unpredictable event, the amount the Council receives annually from the property tax could be affected adversely. Management is not aware of any actions that will significantly affect the amount of funds the Council will receive in the next fiscal year relating to its property tax or grants.

35

NOTE 18. INTERFUND TRANSFERS

Interfund transfers to and from are listed by fund for the fiscal year

FUNDS TRANSFERRED IN

TRANSFERRED TITLE OUT GENERAL III B

General -0- 155,102 Title III D 26 -0-Sr Cnt Supp -0- 3,100 N.S.l.P. -0- -0-United Way -0- -0-

TITLE IIICl

37,293 -0--0--0--0-

TITLE IIIC2

65,816 -0--0-

26,000 6, 709

TITLE III E

2,424 -0--0--0--0-

SENIOR AUDIT CNT BLDG

5,103 25,455 2,673 -0- -0- -0--0- -0- -0--0- -0- -0--0- -0- -0-

TOTAL OUT

293,866 26

3,100 26,000 6,709

Total In 26 158,202 37,293 98,525 2,424 5,103 25,455 2,673 329,701

Transfers are used to (1) move revenue from the fund that statute or budget requires to collect them to the fund that statute or budget requires to expand them, and to (2) use unrestricted revenues collected in the General Fund to finance various programs accounted for in other funds in accordance with budgetary authorizations.

These transfers were eliminated as a part of the consolidated process in preparing the Government-Wide Financial Statements.

NOTE 19. RELATED PARTY TRANSACTIONS

There are no significant related party transactions during the year.

NOTE 20. ON-BEHALF PAYMENTS OF FRINGE BENEFITS

Because the Council is one of several governmental agencies receiving proceeds from a property tax assessment, state law requires the Council to bear a pro-rata share of the pension expense relating to the public employees of the St. John the Baptist Parish that participate in the Parochial Employees Retirement System. The Council's pro-rata share of the required contribution was $12,077 which was withheld by the Parish's sheriff to satisfy the Council's obligation. The amount withheld by the Sheriff has been included as an "intergovernmental" expenditure of the General Fund in these financial statements. As described in Note 3, the Council has also increased its property tax revenue by the same amount of the intergovernmental expenditure. None of the Council's employees participate in or benefit from any pension plan relating to this expenditure.

36

SUPPLEMENTARY INFORMATION REQUIRED BY GASB STATEMENT 34

37

BUDGETARY COMPARISON SCHEDULE - GENERAL FUND

ST. JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA FOR THE YEAR ENDED JUNE 30, 2009

REVENUES: Intergovernmental

Governor's Office of Elderly Affairs Department of Transportation

Ad Valorem Tax Public Support:

Other Interest Income Miscellaneous

Total Revenues

EXPENDITURES: Current

Other Capital Outlay Debt Service:

Principal Retirement Interest Expense

Intergovernmental Total Expenditures

BUDGET AMOUNTS ORiGINAL

$37,500 0

259,364

0 0 0

296,864

0 0

0 0 0 0

FINAL

$37,500 0

259,364

0 0 0

296,864

0 0

0 0 0 0

ACTUAL AMOUNTS

GAAP BASIS

$37,500 0

305,178

74 1,068 4,954

348,774

12,374 45,756

1,406 186

0 59,722

VARIANCE FINAL BUDGET

FAVORABLE (UNFAVORABLE)

$0 0

45.814

74 1,068 4.954

51,910

(12,374) (45,756)

(1,406) (186)

0 (59,722)

Excess (Deficiency) Of Revenue Over Expenditures 296,864 296,864 289,052 (7,812)

Other Financial Sources (Uses) Transfers In Transfers Out Total Other Financial Sources (Uses)

Excess of Revenues and Other Sources Over Expenditures And Other Uses

FUND BALANCE. Beginning Adjustments to increase beginning

Fund Balances Fund Balances-Beginning as restated

FUND BALANCE, Ending

0 (296,864) (296,864)

0

211,378

45,756 211,378

211.376

0 (296,864) (296.864)

0

211,378

45.756 257.134

257,134

26 (293,866) (293,840)

(4,788)

211.378

45,756 257,134

252,346

26 2,998 3,024

(4,788)

0

0 0

(4.788)

38

BUDGETARY COMPARISON SCHEDULE - TITLE III B FUND

ST. JOHN PARISH COUNCIL ON AGING, INC. RESERVE, LOUISIANA FOR THE YEAR ENDED JUNE 30, 2009

ACTUAL VARIANCE AMOUNTS FINAL BUDGET

REVENUES: Intergovernmental

Governor's Office of Elderly Affairs Public Support In-Kind

Total Revenues