SSE Financial Results - SSE Irelandireland.sse.com/media/5397/FINAL_RESULTS_PRESENTATION.pdf · SSE...

46

1 SSE Financial Results Year Ended 31 March 2013

Transcript of SSE Financial Results - SSE Irelandireland.sse.com/media/5397/FINAL_RESULTS_PRESENTATION.pdf · SSE...

1

SSE

Financial Results Year Ended 31 March 2013

2

Lord Smith of Kelvin Chairman

Continuing the 4 Ds

3

Today’s SSE team

Lord Smith of Kelvin

Chairman

Alistair Phillips-Davies

Deputy Chief Executive

Gregor Alexander

Finance Director

Ian Marchant

Chief Executive

Jim McPhillimy

MD Group Services

Alan Young

MD Corporate Affairs

Jim Smith

MD Renewables

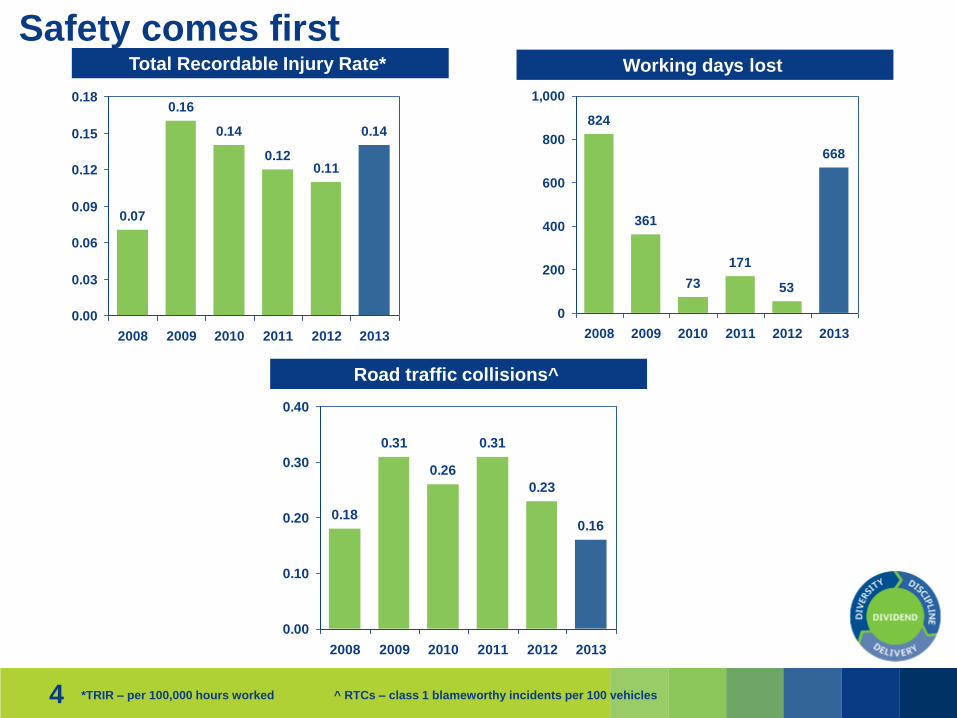

4

0.07

0.16

0.14

0.120.11

0.14

0.00

0.03

0.06

0.09

0.12

0.15

0.18

2008 2009 2010 2011 2012 2013

Safety comes first Total Recordable Injury Rate*

Road traffic collisions^

*TRIR – per 100,000 hours worked

^ RTCs – class 1 blameworthy incidents per 100 vehicles

0.18

0.31

0.26

0.31

0.23

0.16

0.00

0.10

0.20

0.30

0.40

2008 2009 2010 2011 2012 2013

Working days lost

824

361

73

171

53

668

0

200

400

600

800

1,000

2008 2009 2010 2011 2012 2013

5

Consistent management and governance (1)

Alistair Phillips-Davies

Deputy Chief Executive

Will Morris

MD Retail

Paul Smith

MD Generation Jim Smith

MD Renewables

Mark Mathieson

MD Networks

Alan Young

MD Corporate Affairs

Gregor Alexander

Finance Director

Martin Pibworth

MD EPM

Jim McPhillimy

MD Group Services

Rob McDonald

MD Regulation

Brandon Rennet

MD Finance

• Total combined service of Alistair Phillips-Davies and Gregor Alexander – 39 years

• Alistair Phillips-Davies and Gregor Alexander on SSE plc Board since 2002

• Total combined service of SSE Management Board – over 160 years

6

Consistent management and governance (2)

7

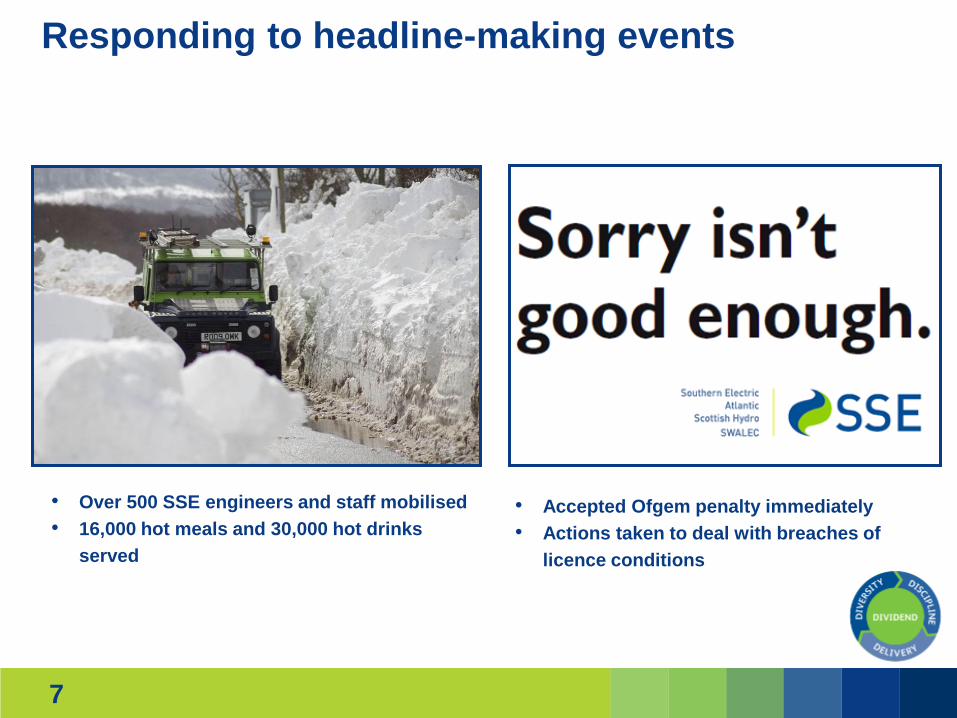

Responding to headline-making events

• Over 500 SSE engineers and staff mobilised

• 16,000 hot meals and 30,000 hot drinks

served

• Accepted Ofgem penalty immediately

• Actions taken to deal with breaches of

licence conditions

8

Ian Marchant Chief Executive

Delivering the dividend

9 9

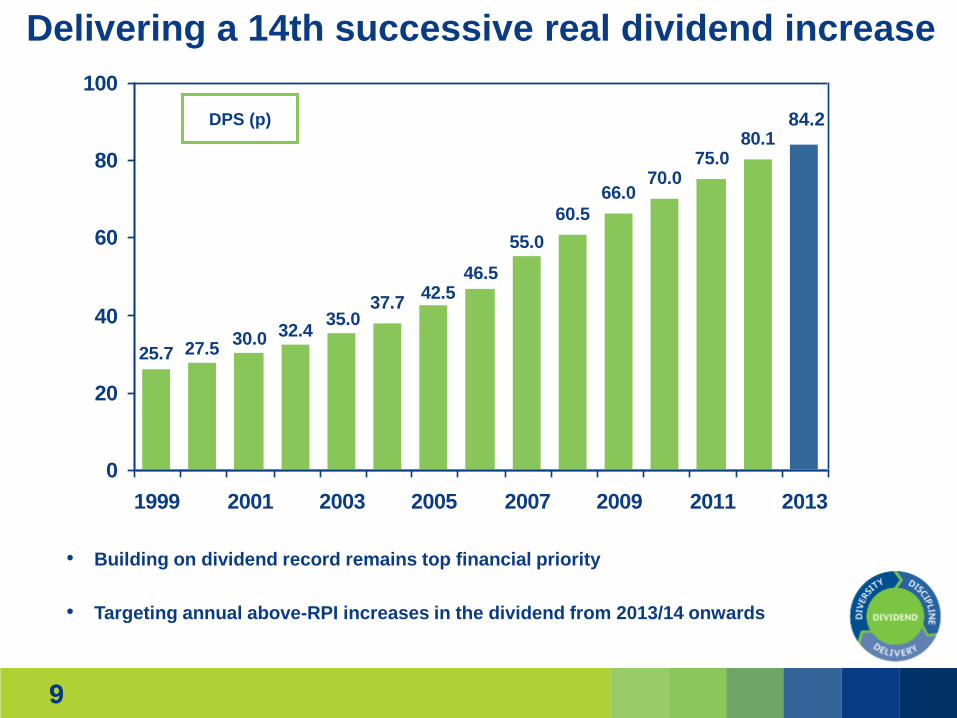

Delivering a 14th successive real dividend increase

60.5

66.070.0

75.080.1

25.7 27.530.0

46.5

55.0

42.537.7

35.032.4

0

20

40

60

80

100

1999 2001 2003 2005 2007 2009 2011 2013

84.2 DPS (p)

• Building on dividend record remains top financial priority

• Targeting annual above-RPI increases in the dividend from 2013/14 onwards

10

Delivering a 14th successive adjusted PBT increase

1,290.11,310.1

1,335.7

1,410.7

1,000

1,100

1,200

1,300

1,400

1,500

2010 2011 2012 2013

Increase in adjusted PBT, £m

110.2

112.3 112.7

118.0

100

104

108

112

116

120

2010 2011 2012 2013

Increase in adjusted EPS, pence

Year ended 31 March

2013 £m

2012 £m

Change

%

2011

£m

Adjusted profit before tax 1,410.7 1,335.7 5.6% 1,310.1

Fair value re-measurements (IAS 39) (199.7) (509.0) 1,423.3

Exceptional items (584.7) (551.6) (625.0)

Tax on JCEs and associates (25.4) (6.6) 3.3

Reported profit before tax 600.9 268.5 2,111.7

Adjusted effective tax rate 15.9% 16.0% 20.5%

Adjusted earnings per share 118.0p 112.7p 4.7% 112.3p

• Dividend cover of 1.4

times

• Dividend cover

averaged 1.5 times

over last 4 years

• Exceptional charge

reflects tough

operating

environment

11

Movements in Networks’ operating profit Networks’ operating profit split

Gas

Distribution*

27%

Other

Networks

4%

Electricity

Transmission

11%

Electricity

Distribution

58%

Delivering good financial performance in Networks

• 49% of SSE adjusted operating profit

• Electricity Transmission operating profit up –

increase in asset base from capital invested

• Electricity Distribution operating profit up –

timing of allowed revenue recovery

• Gas Distribution operating profit flat

• Other Networks’ achieved operating profit similar

to that achieved in 2011

Year ended 31 March 2013

£m 2012

£m

Change

%

2011

£m

Electricity Transmission 93.3 73.7 26.6 47.7

Electricity Distribution 512.8 396.5 29.3 418.9

Gas Distribution* 234.1 234.8 -0.3 186.8

Other networks 35.9 32.1 11.8 37.1

Networks segment operating profit 876.1 737.1 18.9 690.5

*SSE share

12

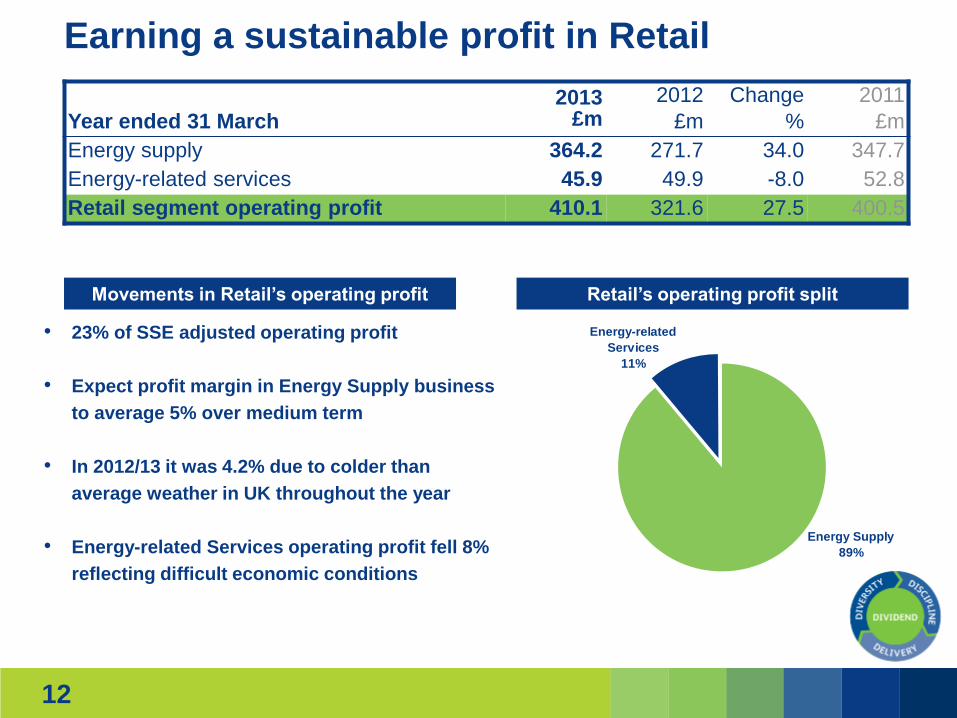

Movements in Retail’s operating profit Retail’s operating profit split

Energy Supply

89%

Energy-related

Services

11%

Earning a sustainable profit in Retail

• 23% of SSE adjusted operating profit

• Expect profit margin in Energy Supply business

to average 5% over medium term

• In 2012/13 it was 4.2% due to colder than

average weather in UK throughout the year

• Energy-related Services operating profit fell 8%

reflecting difficult economic conditions

Year ended 31 March 2013

£m 2012

£m

Change

%

2011

£m

Energy supply 364.2 271.7 34.0 347.7

Energy-related services 45.9 49.9 -8.0 52.8

Retail segment operating profit 410.1 321.6 27.5 400.5

13

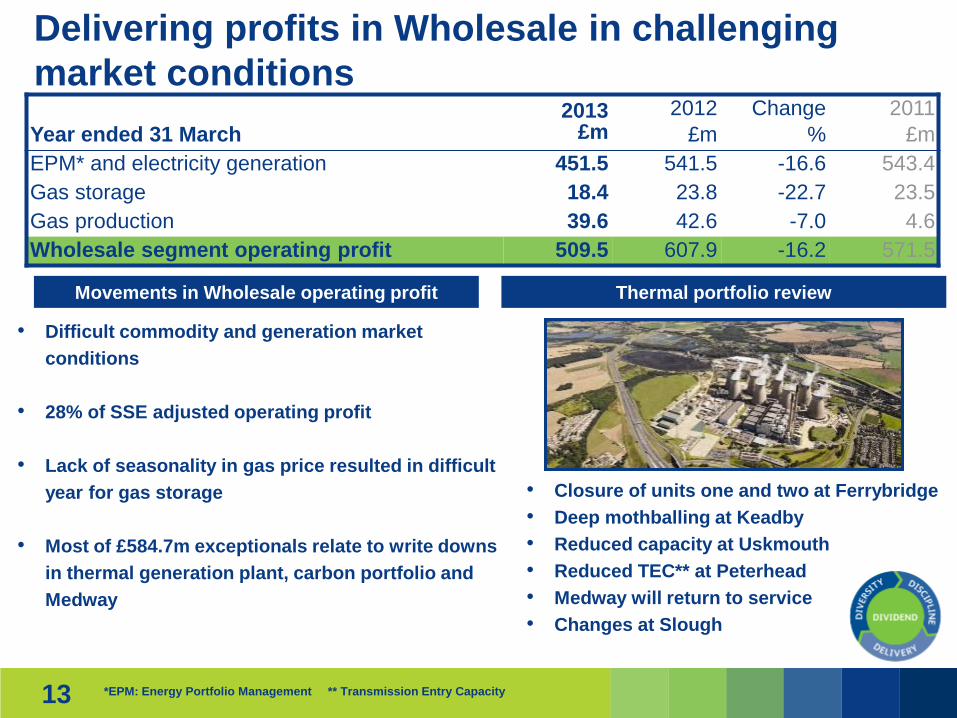

Movements in Wholesale operating profit

Delivering profits in Wholesale in challenging

market conditions

*EPM: Energy Portfolio Management ** Transmission Entry Capacity

• Difficult commodity and generation market

conditions

• 28% of SSE adjusted operating profit

• Lack of seasonality in gas price resulted in difficult

year for gas storage

• Most of £584.7m exceptionals relate to write downs

in thermal generation plant, carbon portfolio and

Medway

• Closure of units one and two at Ferrybridge

• Deep mothballing at Keadby

• Reduced capacity at Uskmouth

• Reduced TEC** at Peterhead

• Medway will return to service

• Changes at Slough

Thermal portfolio review

Year ended 31 March 2013

£m 2012

£m

Change

%

2011

£m

EPM* and electricity generation 451.5 541.5 -16.6 543.4

Gas storage 18.4 23.8 -22.7 23.5

Gas production 39.6 42.6 -7.0 4.6

Wholesale segment operating profit 509.5 607.9 -16.2 571.5

14 *Including corporation tax, rates, and NI **Capex ^Acquisitions

Business diversity delivering for our stakeholders

Employee numbers

Capex and acquisitions, £bn

Declared dividends of £5.6bn over last 10

years

Paid £3.5bn in tax over last ten years*

1 April 2003, SSE’s market cap was £5.5bn

15

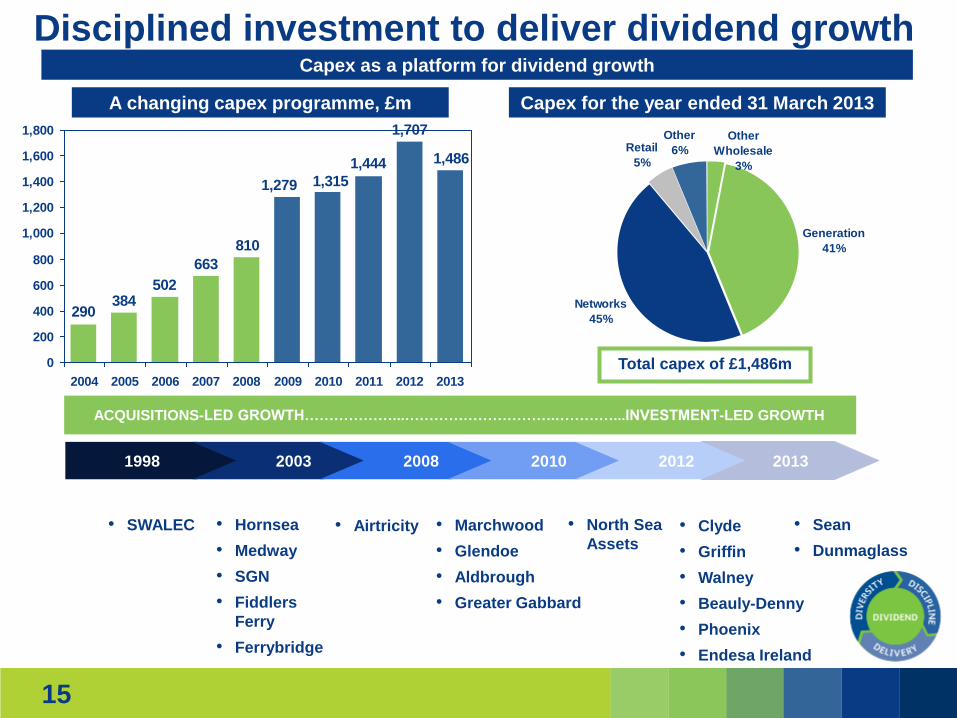

Capex as a platform for dividend growth

A changing capex programme, £m Capex for the year ended 31 March 2013

Generation

41%

Networks

45%

Retail

5%

Other

6%

Other

Wholesale

3%

Total capex of £1,486m

1,486

290384

502

1,444

1,707

1,3151,279

810

663

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Disciplined investment to deliver dividend growth

1998 2003 2008 2010 2012 2013

• Marchwood

• Glendoe

• Aldbrough

• Greater Gabbard

• SWALEC • Hornsea

• Medway

• SGN

• Fiddlers

Ferry

• Ferrybridge

• Airtricity

ACQUISITIONS-LED GROWTH………………...………………………….…………...INVESTMENT-LED GROWTH

• Clyde

• Griffin

• Walney

• Beauly-Denny

• Phoenix

• Endesa Ireland

• North Sea

Assets

• Sean

• Dunmaglass

16 16

60.5

66.070.0

75.080.1

25.7 27.530.0

46.5

55.0

42.537.7

35.032.4

0

20

40

60

80

100

1999 2001 2003 2005 2007 2009 2011 2013

84.2 DPS (p)

• One of only five FTSE100 companies to achieve greater than RPI growth in dividend

every year since 1999 – TSR of over 360%

• Building on dividend record remains top financial priority

• Targeting annual above-RPI increases in the dividend from 2013/14 onwards

Delivering sustained real dividend growth

17

Gregor Alexander Finance Director

Funding, Investment and Networks

18

Making sure SSE is well-financed

Mar 2013 Mar 2012

Adjusted net debt and hybrid capital - £m (7,347.7) (6,755.8)

Capital expenditure and investment 1,485.5 1,706.9

Average interest rate 5.26% 5.06%

Diverse sources of funding

Eurobonds

48%

US Private

Placement

6%

EIB

6%

Index-linked debt

3%

Other loans

9%

Hybrid securities

28%

• 33% Scrip uptake

• Wind asset sale (£131m net)

• Private US $ placement (£450m)

• Hybrid capital issued (£1.025bn)

• Interest cover of 5.4 times*

• c£5.4bn of medium to long-term borrowings**

• Average debt maturity of 10.6 years

• Secured £650m of additional bank facilities in

March 2013

*Excludes SGN **Excluding hybrid capital , also £1.5bn matures in next 12 months

Debt influenced by

• Three main acquisitions (£358m)

Remain committed to current criteria for single ‘A’ credit rating

19

Well-financed for future investment

• Forecasting spend of c£1.5bn in 2013/14

• Electricity networks and generation main components

• Economically regulated networks likely to require biggest proportion

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2011 2012 2013 2014 2015

Other Retail Networks Wholesale

Annual capex spend, £m

20

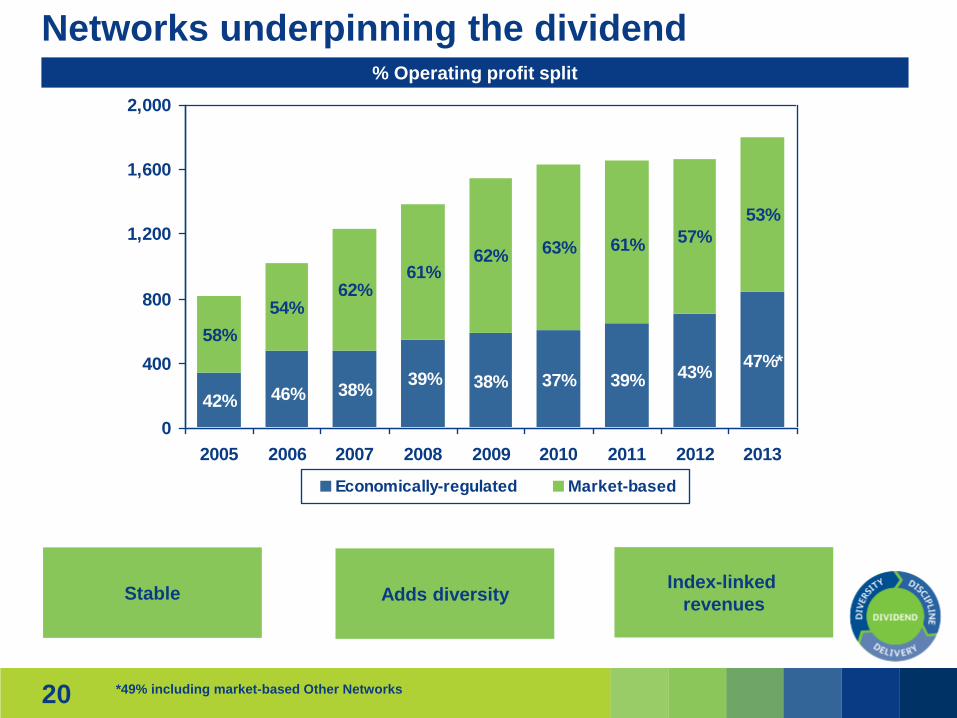

Networks underpinning the dividend

42% 46% 38%39% 38% 37% 39% 43%

47%*

58%

54%62%

61%62% 63% 61% 57%

53%

0

400

800

1,200

1,600

2,000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Economically-regulated Market-based

Stable Adds diversity Index-linked

revenues

% Operating profit split

*49% including market-based Other Networks

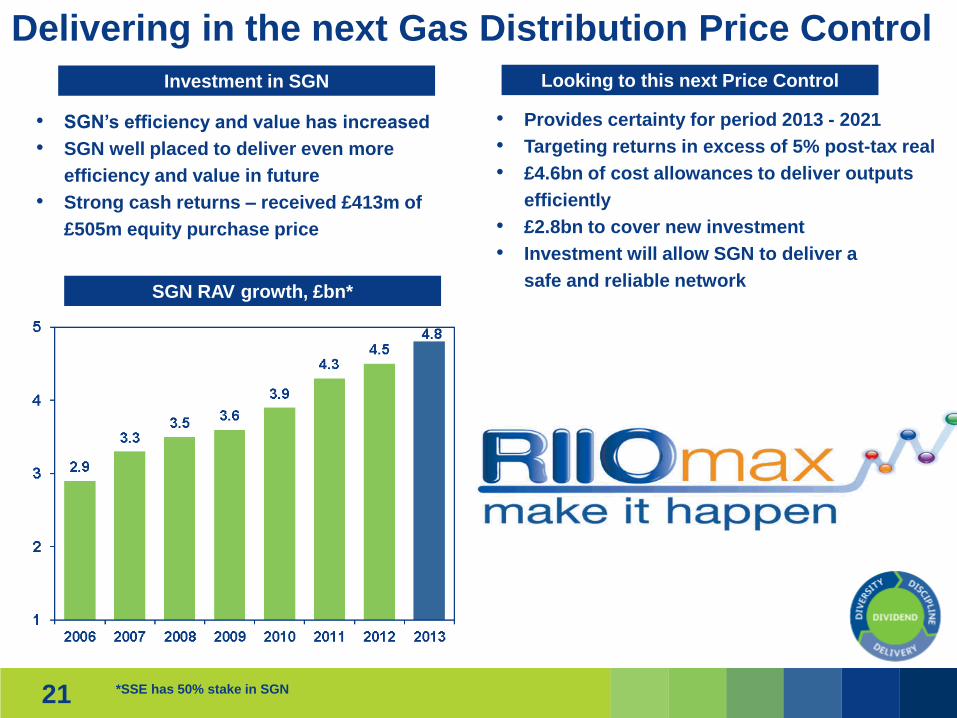

21

• SGN’s efficiency and value has increased

• SGN well placed to deliver even more

efficiency and value in future

• Strong cash returns – received £413m of

£505m equity purchase price

Delivering in the next Gas Distribution Price Control

Investment in SGN Looking to this next Price Control

• Provides certainty for period 2013 - 2021

• Targeting returns in excess of 5% post-tax real

• £4.6bn of cost allowances to deliver outputs

efficiently

• £2.8bn to cover new investment

• Investment will allow SGN to deliver a

safe and reliable network

*SSE has 50% stake in SGN

SGN RAV growth, £bn*

22

Maintaining an innovative approach in Gas Distribution

The new way to repair a joint

• Successful trials carried out in partnership with:

• Royal Borough of Kingston

• Croydon Council

• Glasgow City Council

• Approval from Transport for London and Glasgow City Council

• SGN now aim to use technique in all areas of operations

The coring device

Making the repair

using long handled

tools

Original core goes

back in and whole

process takes <5 hours

23

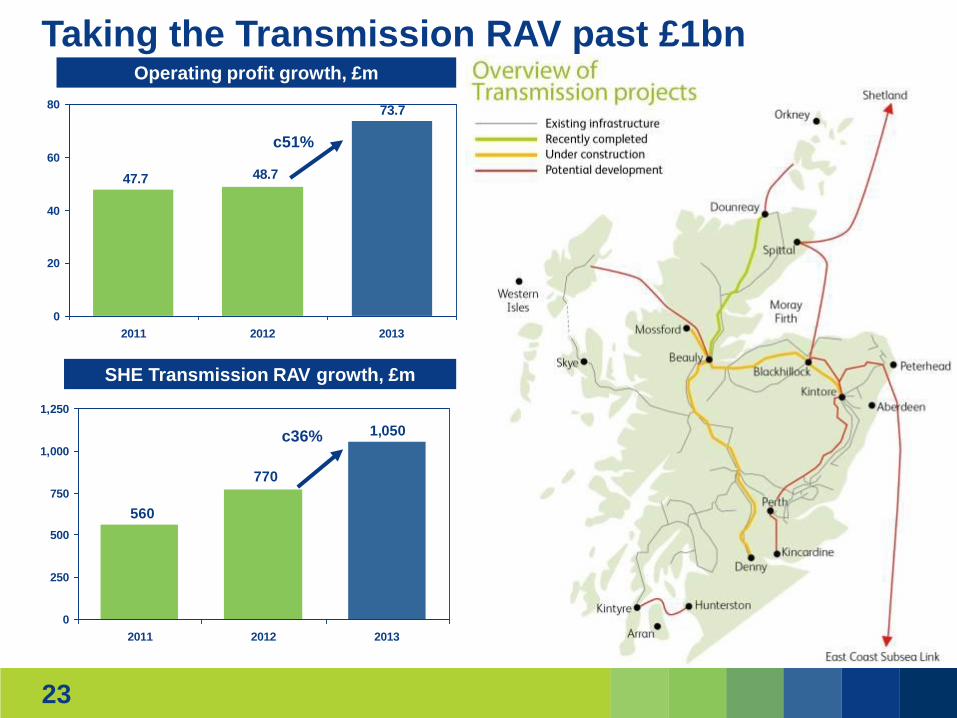

Taking the Transmission RAV past £1bn

47.7 48.7

73.7

0

20

40

60

80

2011 2012 2013

560

770

1,050

0

250

500

750

1,000

1,250

2011 2012 2013

SHE Transmission RAV growth, £m

Operating profit growth, £m

c36%

c51%

24

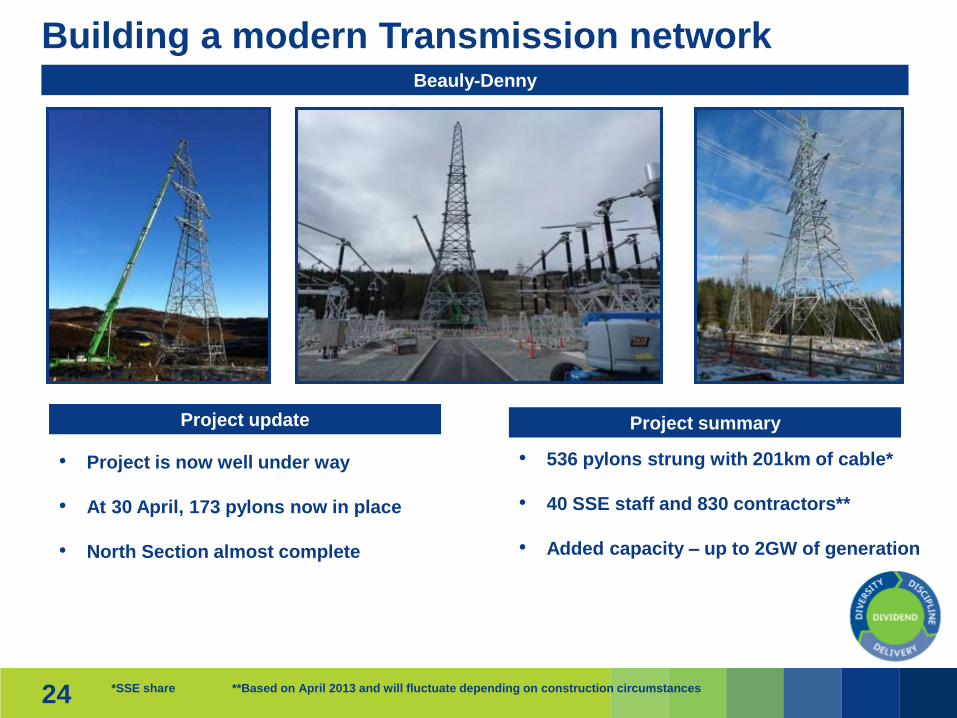

Building a modern Transmission network Beauly-Denny

Project update Project summary

• Project is now well under way

• At 30 April, 173 pylons now in place

• North Section almost complete

*SSE share **Based on April 2013 and will fluctuate depending on construction circumstances

• 536 pylons strung with 201km of cable*

• 40 SSE staff and 830 contractors**

• Added capacity – up to 2GW of generation

25

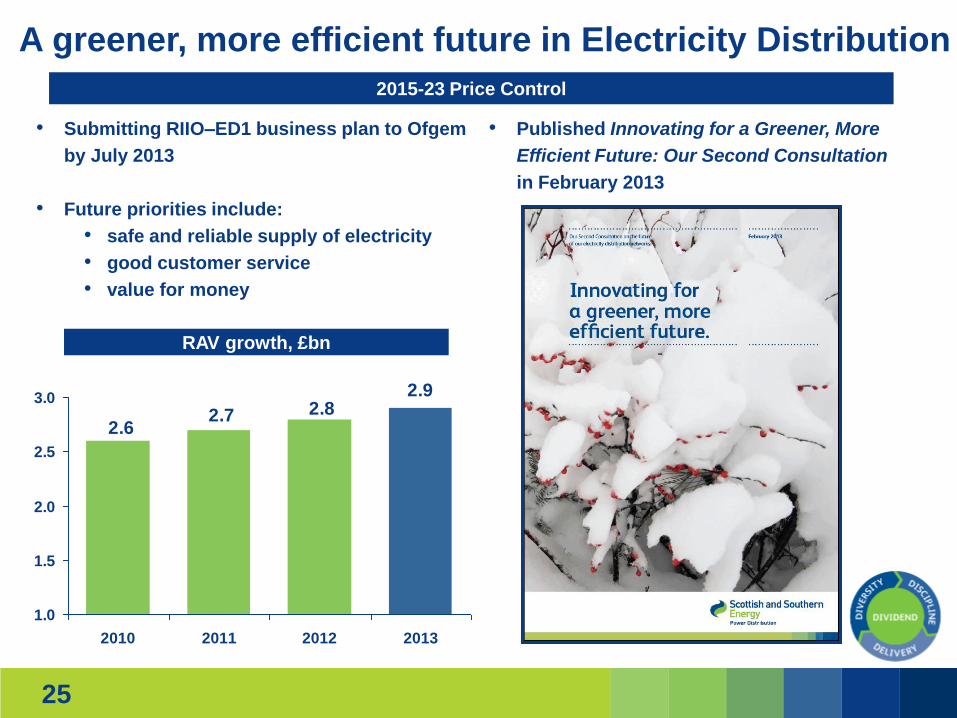

A greener, more efficient future in Electricity Distribution

2015-23 Price Control

• Submitting RIIO–ED1 business plan to Ofgem

by July 2013

• Future priorities include:

• safe and reliable supply of electricity

• good customer service

• value for money

• Published Innovating for a Greener, More

Efficient Future: Our Second Consultation

in February 2013

2.62.7 2.8

2.9

1.0

1.5

2.0

2.5

3.0

2010 2011 2012 2013

RAV growth, £bn

26

Dealing with storms – Kintyre and Arran

27

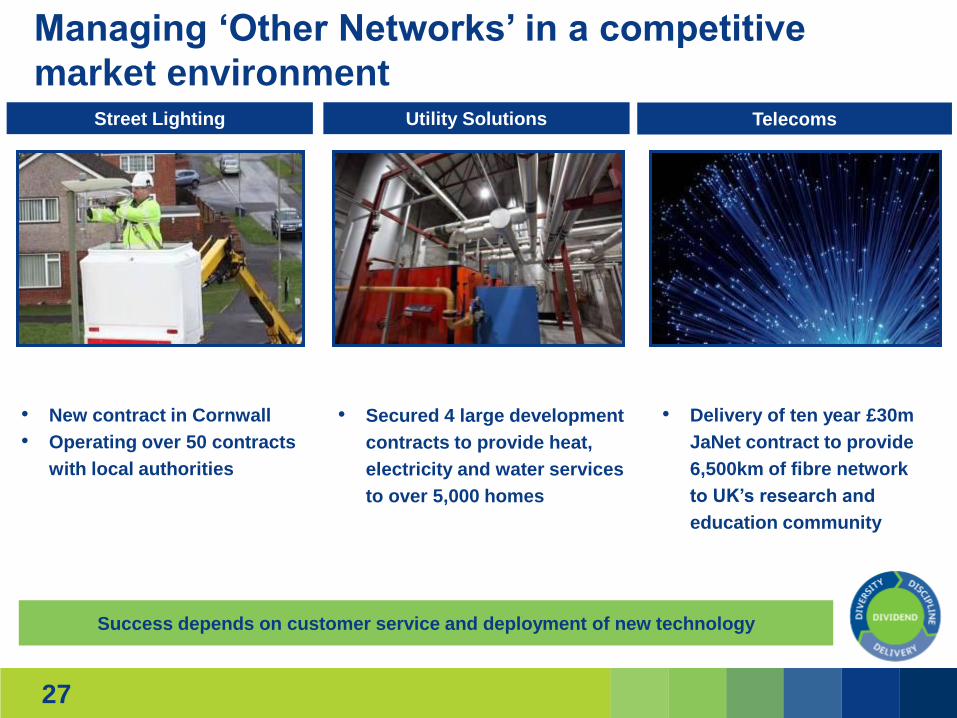

Utility Solutions Telecoms

Managing ‘Other Networks’ in a competitive

market environment Street Lighting

• New contract in Cornwall

• Operating over 50 contracts

with local authorities

• Secured 4 large development

contracts to provide heat,

electricity and water services

to over 5,000 homes

• Delivery of ten year £30m

JaNet contract to provide

6,500km of fibre network

to UK’s research and

education community

Success depends on customer service and deployment of new technology

28

60.566.0

70.075.0

80.1

25.7 27.530.0

46.5

55.0

42.537.7

35.032.4

0

20

40

60

80

100

1999 2001 2003 2005 2007 2009 2011 2013

84.2

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1999 2001 2003 2005 2007 2009 2011 2013

Distribution Transmission SGN*

28

Networks underpinning the dividend

Operational focus

on delivery

Demand operational

and financial

discipline

Lend real diversity to

SSE’s balanced group

of businesses

Dividend, pence Total Regulated Networks RAV, £m

*SSE share

Economically-regulated Networks really matter

Underpin financial principles and long-term commitment to the dividend

29

Alistair Phillips-Davies Deputy Chief Executive

Retail and Wholesale

30

SSE is a customer-focused company

Core purpose to provide the energy people need in a reliable and sustainable way

31

Rebuilding trust in Energy Supply (1)

• Only one of its kind in the industry

• Received 14,000 claims since Ofgem announcement

• Paid an average of £80 to over 5,000 customers

• Balance of the £5m to be given to energy related charities

Sales Guarantee

32

• Goes significantly beyond existing industry-wide

standards

• Promise to meet new set of customer service

commitments or give customers £20 off next bill

• Three core objectives of

• Helping customers save money

• Making life easier for customers

• Helping customers when they need it most

• Payments being made where standards not met

Rebuilding trust in Energy Supply (2)

Customer Service Guarantee

33

Supplying energy to customers in GB and Ireland

8.469.06 9.16

8.658.939.16

0.050.82

0.490.190.62

0.04

5

6

7

8

9

10

2008 2009 2010 2011 2012 2013

Total GB energy accounts Total Irish energy accounts

Customer accounts, million

Gain customers in the right way and retain them for the long term

80,000 net loss in

account numbers

130,000 gas customer

accounts from Phoenix

acquisition

Underlying fall of

210,000 accounts

Customer base only

3% smaller than peak

two years ago

• Mix of fair prices, simple products and excellent service – resilient Energy Supply business

• Energy Supply about gaining customers in right way and retaining them for long term

34

0%

1%

2%

3%

4%

5%

6%

2011 2012 2013*

0%

2%

4%

6%

8%

10%

Energy Supply

(2013)

Supermarkets High Street Retail Telecoms

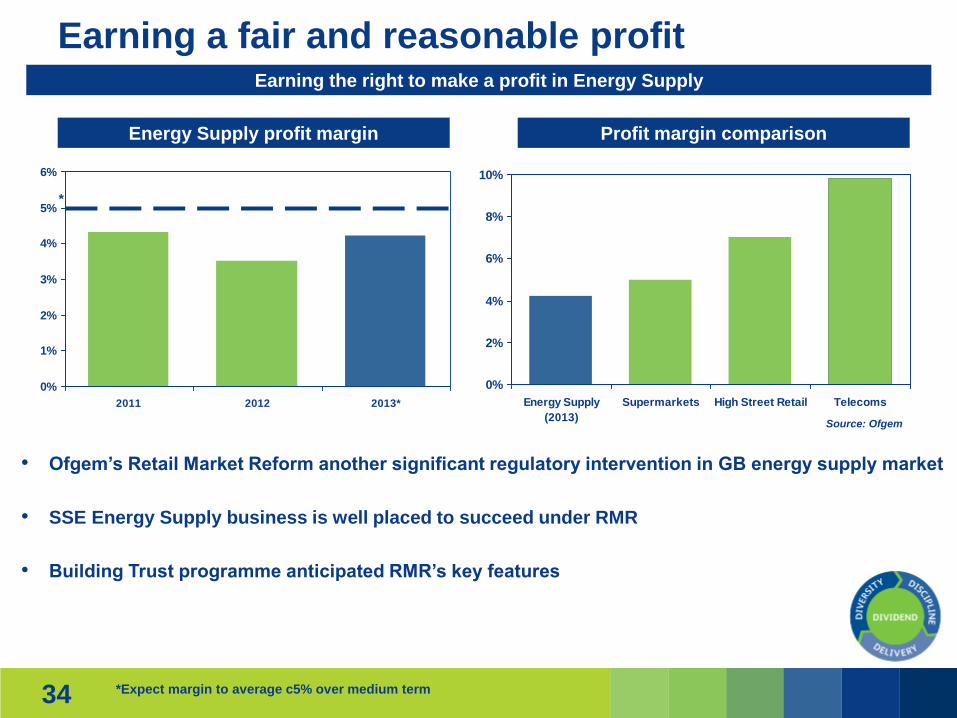

Earning a fair and reasonable profit

*

Profit margin comparison Energy Supply profit margin

• Ofgem’s Retail Market Reform another significant regulatory intervention in GB energy supply market

• SSE Energy Supply business is well placed to succeed under RMR

• Building Trust programme anticipated RMR’s key features

*Expect margin to average c5% over medium term

Earning the right to make a profit in Energy Supply

Source: Ofgem

35

Transforming our Retail business

Strong track record on

Customer Service

Broad range of energy-

related services

• Providing financial support for low income

customers

• Maintaining partnerships with key

organisations like Citizens’ Advice

• Practical steps to make vulnerable

customers’ lives easier – Careline

• Extensive product portfolio and high-potential

customer base

• Developing and deploying central proposition

to households and businesses

• Enabling customers to receive services from

SSE

Value Convenience Choice Quality

Building on the solid foundations we have through

36

0

4,000

8,000

12,000

16,000

20,000

24,000

2008 2009 2010 2011 2012 2013

Electricity consumption Gas consumption

A challenging GB Generation Market (1)

-10

0

10

20

30

40

Apr-08 Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14 Apr-15 Apr-16

-6

-4

-2

0

2

4

6

1999 2001 2003 2005 2007 2009 2011

Purpose of Wholesale is to secure the energy people and businesses need

Y-O-Y GDP growth, % Weather adjusted fuel demand, kWh

Spark spreads, £/MWh Diversity*

Renewable

capacity

25%

Coal-fired/solid

fuel capacity

33%

Gas- and oil-

fired capacity

42%

*Including Irish capacity

37

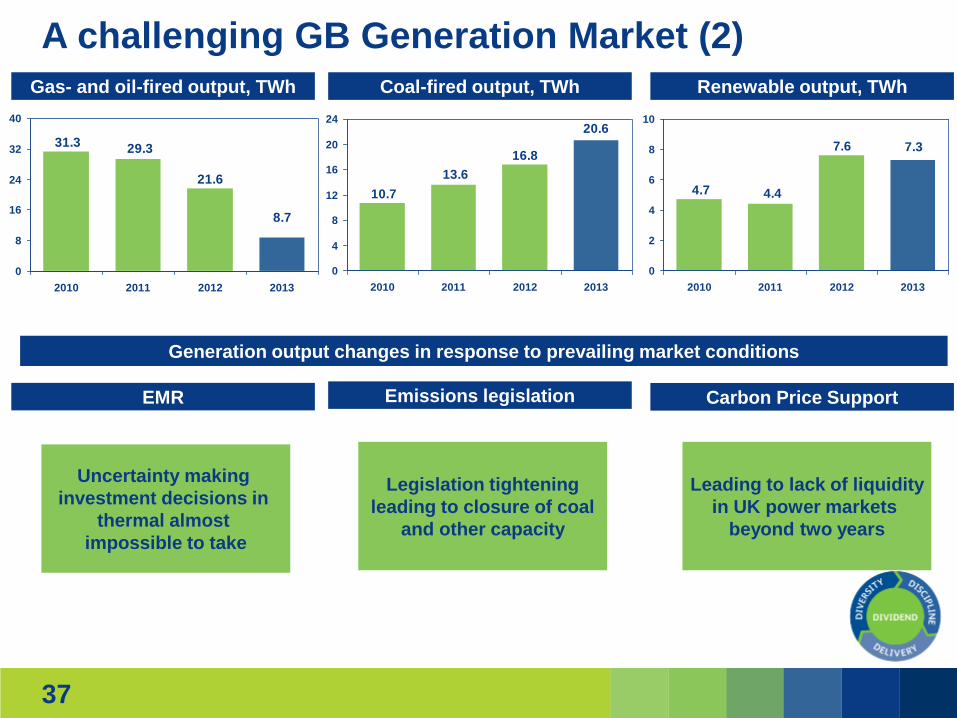

A challenging GB Generation Market (2)

31.329.3

21.6

8.7

0

8

16

24

32

40

2010 2011 2012 2013

10.7

13.6

16.8

20.6

0

4

8

12

16

20

24

2010 2011 2012 2013

Gas- and oil-fired output, TWh

4.7 4.4

7.6 7.3

0

2

4

6

8

10

2010 2011 2012 2013

Coal-fired output, TWh Renewable output, TWh

Generation output changes in response to prevailing market conditions

Uncertainty making

investment decisions in

thermal almost

impossible to take

Legislation tightening

leading to closure of coal

and other capacity

Leading to lack of liquidity

in UK power markets

beyond two years

EMR Emissions legislation Carbon Price Support

38

GRAIN OIL

Didcot A

Uskmouth

Tilbury Cockenzie

Fawley

Littlebrook

Kingsnorth

...partially

...partially

The 12/12/12 problem

39

Coal/Solid Fuel

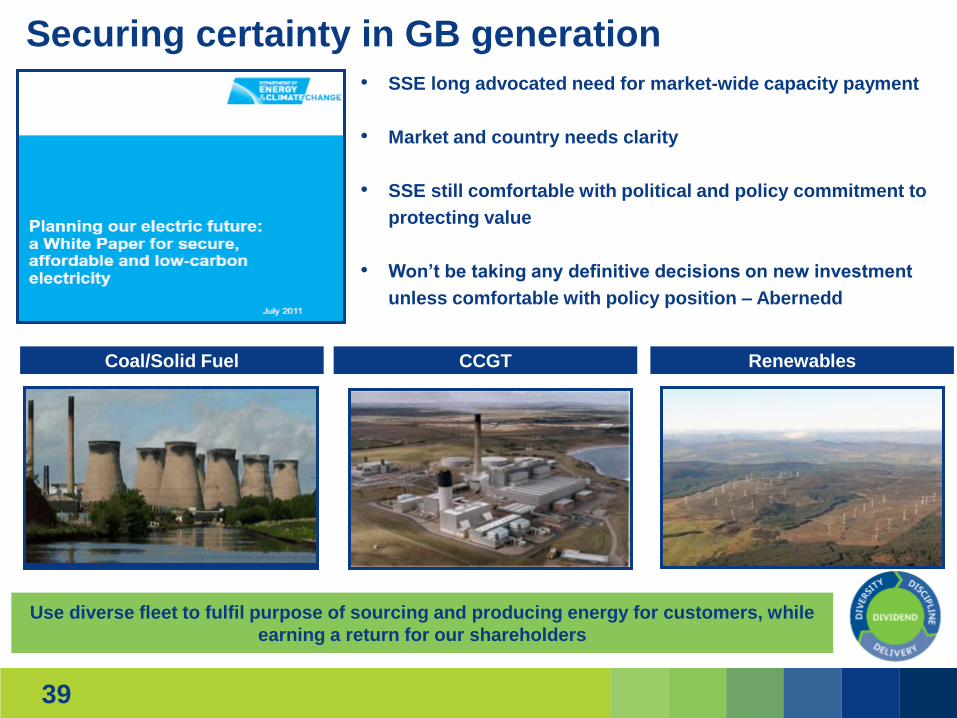

Securing certainty in GB generation

CCGT Renewables

• SSE long advocated need for market-wide capacity payment

• Market and country needs clarity

• SSE still comfortable with political and policy commitment to

protecting value

• Won’t be taking any definitive decisions on new investment

unless comfortable with policy position – Abernedd

Use diverse fleet to fulfil purpose of sourcing and producing energy for customers, while

earning a return for our shareholders

40

Optimising SSE’s thermal assets Areas of ongoing investment

Fiddlers Ferry Nox Abatement

Cleaner Gas Great Island CCGT

Ferrybridge Multifuel

• CCGT to support security of supply

• Need right market signals

• Valuable options in Abernedd 1, Keadby 2,

Seabank 3

• No investment decision on these until 2015

at earliest

41

Continuing to deliver renewable energy Hydro output, GWh

Wind farm output, GWh

Renewable generation capacity, MW

2,558

4,262

2,836

500

1,500

2,500

3,500

4,500

2011 2012 2013

1,653

3,199

4,281

200

1,000

1,800

2,600

3,400

4,200

5,000

2011 2012 2013

2,450

3,0203,240

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012 2013

Invested £383m in renewables

Renewable portfolio

Priorities for 2013/14

• 138MW new onshore wind

• 162MW net offshore wind

• 87% of availability at Greater Gabbard –

expected to be over 90% in 2013/14

• Now have total of 3,240MW*

• Capacity generating electricity includes

Glendoe – returned to service last August

• Onshore wind developments at Calliachar,

Keadby, Strathy North and Dunmaglass

• Capex spend expected to be similar

in 2013/14

*

*Net of 79.6MW wind sale

42

Renewables in GB and Ireland CCGT in GB and Ireland

SSE has options Solid fuel with NOX abatement

Diversity will be the hallmark of our generation portfolio

43

Continuing to build up a good position in gas Sean gas field

• Purchased Sean gas field (£117m)

• Total portfolio of gas production assets represents

approximately 3bn therms of 2P reserves

• Expect volume/production profile of assets to

provide secure and fixed-price supply of gas to

meet c25% of forecast demand from domestic

customers over next three years

42.6

39.6

5

15

25

35

45

2012 2013

Gas production operating profit, £m Long-term fuel supply contracts

• Will cover significant portion of future gas

needs with fair pricing structure and minimal

risk

• Have further opportunities to build on asset

base and will do so provided value

can be secured

84.2p

RPI +2% increase

Discipline

Sticking to SSE’s four Ds (1)

• Balance between

three segments

• Diversity within

segments through

different assets,

customer bases

and different

markets

Diversity

• Strong financial

management

• Sale of non-core

assets and close

cost control

whether they are

revenue or capital

Delivery

• Delivered biggest increase in adjusted PBT for five years

• Unbroken record of annual profit increases against difficult background

44

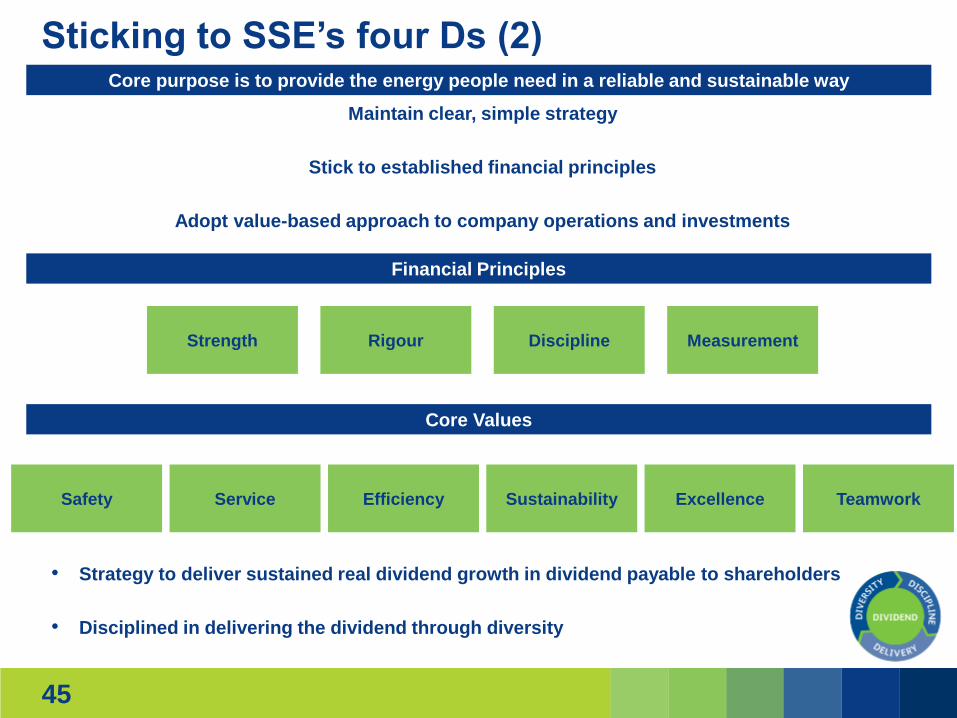

Sticking to SSE’s four Ds (2) Core purpose is to provide the energy people need in a reliable and sustainable way

• Strategy to deliver sustained real dividend growth in dividend payable to shareholders

• Disciplined in delivering the dividend through diversity

Financial Principles

Maintain clear, simple strategy

Stick to established financial principles

Adopt value-based approach to company operations and investments

Core Values

Safety Service Efficiency Sustainability Excellence Teamwork

45

Strength Rigour Discipline Measurement

46 46

• Building on dividend record remains top financial priority

• Targeting annual above-RPI increases in the dividend from 2013/14 onwards

All delivering dividend growth for the long-term

60.5

66.070.0

75.080.1

25.7 27.5 30.0

46.5

55.0

42.537.7

35.032.4

0

20

40

60

80

100

1999 2001 2003 2005 2007 2009 2011 2013

84.2 DPS (p)

Forecast

84.2p +

RPI plus