Spotlight on Decorative Paints Amsterdam, 1 December 2011

102

Spotlight on Decorative Paints Amsterdam, 1 December 2011 Keith Nichols Welcome Spotlight on Decorative Paints – 1 December 2011 2

Transcript of Spotlight on Decorative Paints Amsterdam, 1 December 2011

Spotlight on Decorative PaintsAmsterdam, 1 December 2011,

Keith Nichols

Welcome

Spotlight on Decorative Paints – 1 December 2011 2

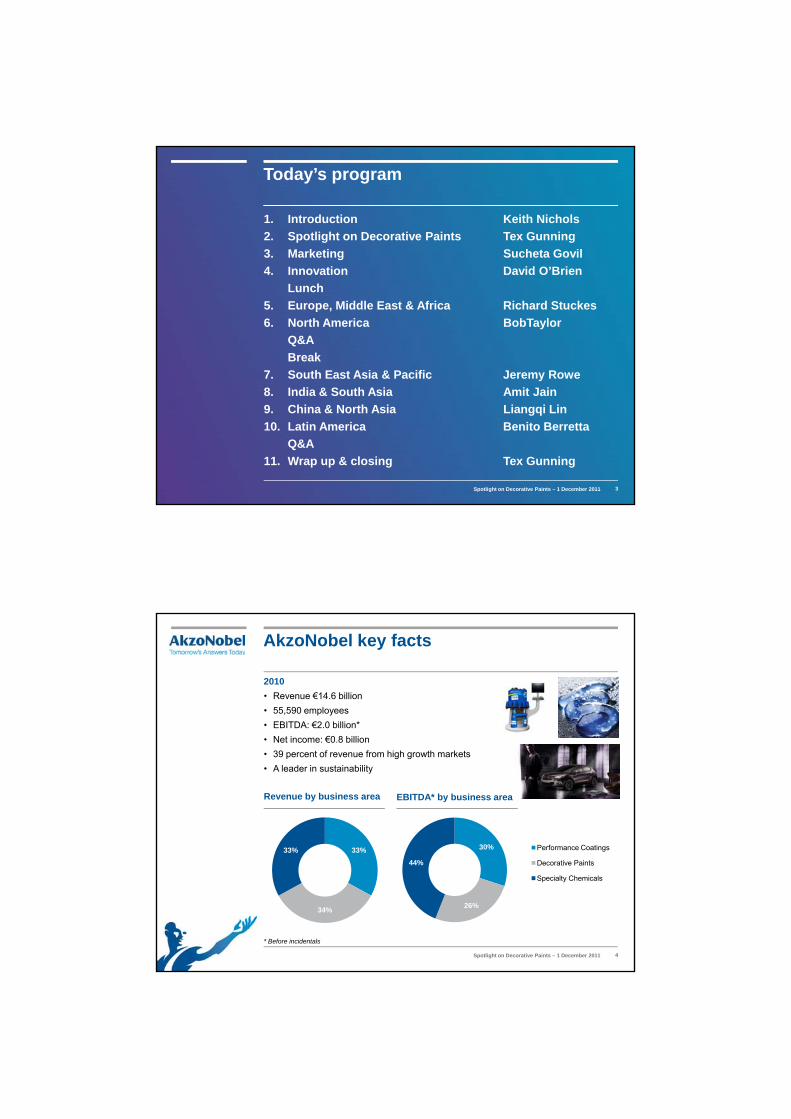

1. Introduction Keith Nichols2. Spotlight on Decorative Paints Tex Gunning3. Marketing Sucheta Govil

Today’s program

4. Innovation David O’BrienLunch

5. Europe, Middle East & Africa Richard Stuckes6. North America BobTaylor

Q&ABreak

7. South East Asia & Pacific Jeremy Rowe8. India & South Asia Amit Jain9. China & North Asia Liangqi Lin10. Latin America Benito Berretta

Q&A11. Wrap up & closing Tex Gunning

Spotlight on Decorative Paints – 1 December 2011 3

AkzoNobel key facts

2010• Revenue €14.6 billion• 55,590 employees• EBITDA: €2.0 billion*

33%33%

• Net income: €0.8 billion• 39 percent of revenue from high growth markets• A leader in sustainability

Revenue by business area EBITDA* by business area

30% Performance Coatings33%

34%

33%

* Before incidentals

26%

44% Decorative Paints

Specialty Chemicals

Spotlight on Decorative Paints – 1 December 2011 4

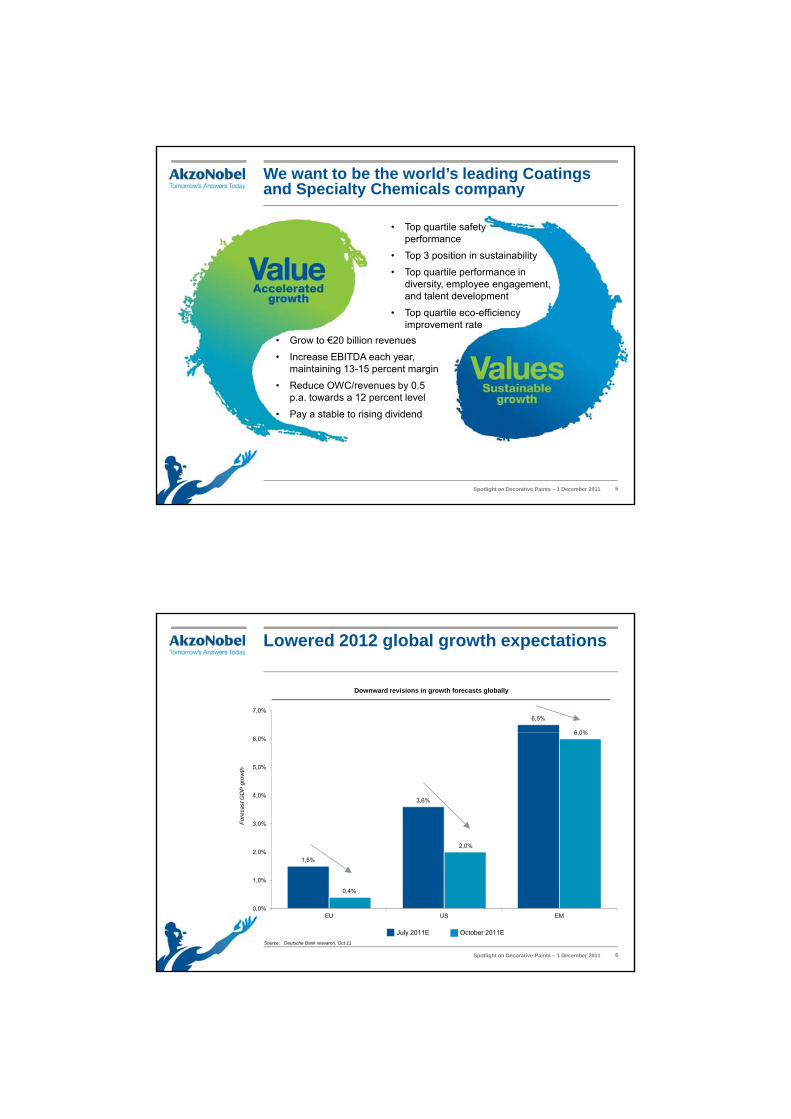

We want to be the world’s leading Coatings and Specialty Chemicals company

• Top quartile safetyperformance

• Top 3 position in sustainability

• Grow to €20 billion revenues

• Increase EBITDA each year, maintaining 13-15 percent margin

• Reduce OWC/revenues by 0 5

• Top quartile performance in diversity, employee engagement, and talent development

• Top quartile eco-efficiency improvement rate

• Reduce OWC/revenues by 0.5 p.a. towards a 12 percent level

• Pay a stable to rising dividend

Spotlight on Decorative Paints – 1 December 2011 5

Lowered 2012 global growth expectations

6,5%

6 0%

7,0%

Downward revisions in growth forecasts globally

3,6%

2,0%

6,0%

2 0%

3,0%

4,0%

5,0%

6,0%

Fore

cast

GD

P g

row

th

1,5%

0,4%

0,0%

1,0%

2,0%

EU US EM

Source: Deutsche Bank research, Oct-11

July 2011E October 2011E

Spotlight on Decorative Paints – 1 December 2011 6

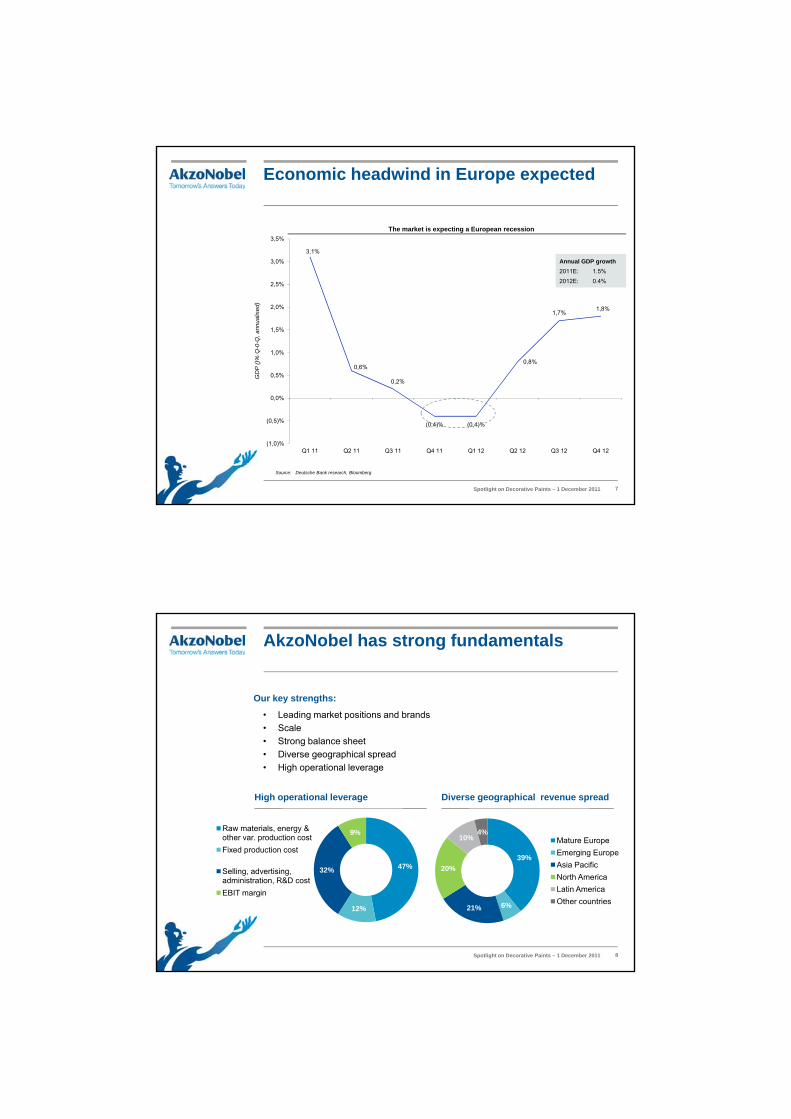

Economic headwind in Europe expected

3,1%

3,0%

3,5%The market is expecting a European recession

Annual GDP growth

0,6%

0,2%

0,8%

1,7%1,8%

0,5%

1,0%

1,5%

2,0%

2,5%

GD

P ()

% Q

-0-Q

, ann

ualis

ed)

2011E: 1.5%2012E: 0.4%

(0,4)% (0,4)%

(1,0)%

(0,5)%

0,0%

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

Source: Deutsche Bank research, Bloomberg

Spotlight on Decorative Paints – 1 December 2011 7

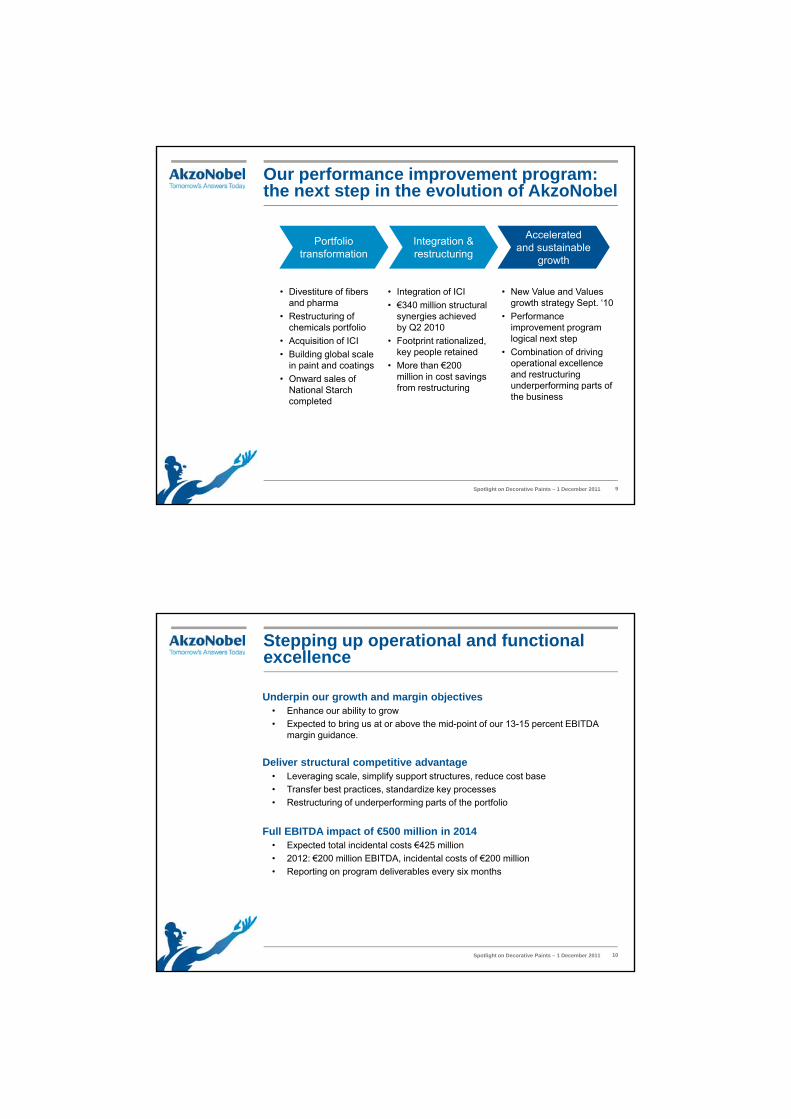

AkzoNobel has strong fundamentals

Our key strengths:

• Leading market positions and brands• Scale

10%4%

Mature EuropeEmerging Europe

• Strong balance sheet• Diverse geographical spread• High operational leverage

Diverse geographical revenue spread

9%Raw materials, energy & other var. production cost Fixed production cost

High operational leverage

39%

6%21%

20%

Emerging EuropeAsia PacificNorth AmericaLatin AmericaOther countries

47%

12%

32%

Fixed production cost

Selling, advertising, administration, R&D costEBIT margin

Spotlight on Decorative Paints – 1 December 2011 8

Our performance improvement program: the next step in the evolution of AkzoNobel

Portfolio transformation

Integration & restructuring

Accelerated and sustainable

growthg

• Divestiture of fibersand pharma

• Restructuring of chemicals portfolio

• Acquisition of ICI• Building global scale

in paint and coatings• Onward sales of

• Integration of ICI• €340 million structural

synergies achieved by Q2 2010

• Footprint rationalized, key people retained

• More than €200 million in cost savings f t t i

• New Value and Values growth strategy Sept. ‘10

• Performance improvement program logical next step

• Combination of driving operational excellence and restructuring underperforming parts ofNational Starch

completedfrom restructuring underperforming parts of

the business

Spotlight on Decorative Paints – 1 December 2011 9

Stepping up operational and functional excellence

Underpin our growth and margin objectives• Enhance our ability to grow• Expected to bring us at or above the mid-point of our 13-15 percent EBITDA

i idmargin guidance.

Deliver structural competitive advantage• Leveraging scale, simplify support structures, reduce cost base• Transfer best practices, standardize key processes• Restructuring of underperforming parts of the portfolio

Full EBITDA impact of €500 million in 2014• Expected total incidental costs €425 million• 2012: €200 million EBITDA, incidental costs of €200 million• Reporting on program deliverables every six months

Spotlight on Decorative Paints – 1 December 2011 10

A comprehensive program

• Comprehensive – all functions, all businesses

• Margin management, R&D and restructuring (~50%)

Decorative Paints

Perf. Coatings

Specialty Chemicals

• Supply Chain and Sourcing projects (~40%)

• Improvements implemented over three years (2012 to 2014)

• All business areas contribute to delivering the €500 million

• >40 percent Decorative Paints

Finance

Human Resources

Information Management

Research, Dev’t & Innov.

Integrated Supply Chain

Margin Management40 percent Decorative Paints

• >30 percent Performance Coatings

• Close to 25 percent Specialty Chemicals

Academy

Spotlight on Decorative Paints – 1 December 2011 11

Performance improvement initiatives examples

Supply Chain – Creating a sustainable, customer-driven supply chain thatoperates at world-class safety, operational and customer service levels:• Improve the efficiency of all of our 225 factories

R d th t f h i d t t ti• Reduce the cost of warehousing and transportation

RD&I – Delivering bigger, bolder, better and faster innovation by focusingon four key areas: • Rationalizing RD&I’s footprint in Europe and North America • Reducing the number of raw materials we use • Improving the efficiency of our manufacturing processes• Linking customers’ needs more effectively to our research activities

Decorative Paints – Restructuring will continue in mature markets:• In North America and Europe, focus will be placed on reducing product

complexity, optimizing distribution and increasing employee productivity

Spotlight on Decorative Paints – 1 December 2011 12

Organization and governance

• Joint responsibility of the Executive Committee, led by CEO• The Executive Committee Support Office (ESO) will operate the

implementation to track progress, intervene where necessary and support th ll

20Masterplans • Set priorities and identify improvement potential from design stages, build into a business case and action plan

• ExCo members to lead each plan

• Defined measures to address priority opportunities• Clear objectives and deliverables identified

the overall program

100Initiatives• Clear objectives and deliverables identified• Risks and dependencies identified• ExCo member still accountable, execution assigned to

operational management

Spotlight on Decorative Paints – 1 December 2011 13

Decorative Paints 2010 key financials and regional breakdown

2010• Revenue: €5.0 billion• 21,950 employees

EBITDA* €548 illi• EBITDA*: €548 million• 38 percent of revenue from high growth markets• Operating ROIC: 32%

7%6%4%

Europe, Middle East and Africa

Revenue by business area

* Before incidentals

52%

21%

10%Europe, Middle East and AfricaNorth AmericaLatin AmericaChina and North AsiaSouth East Asia and PacificIndia and South Asia

Spotlight on Decorative Paints – 1 December 2011 14

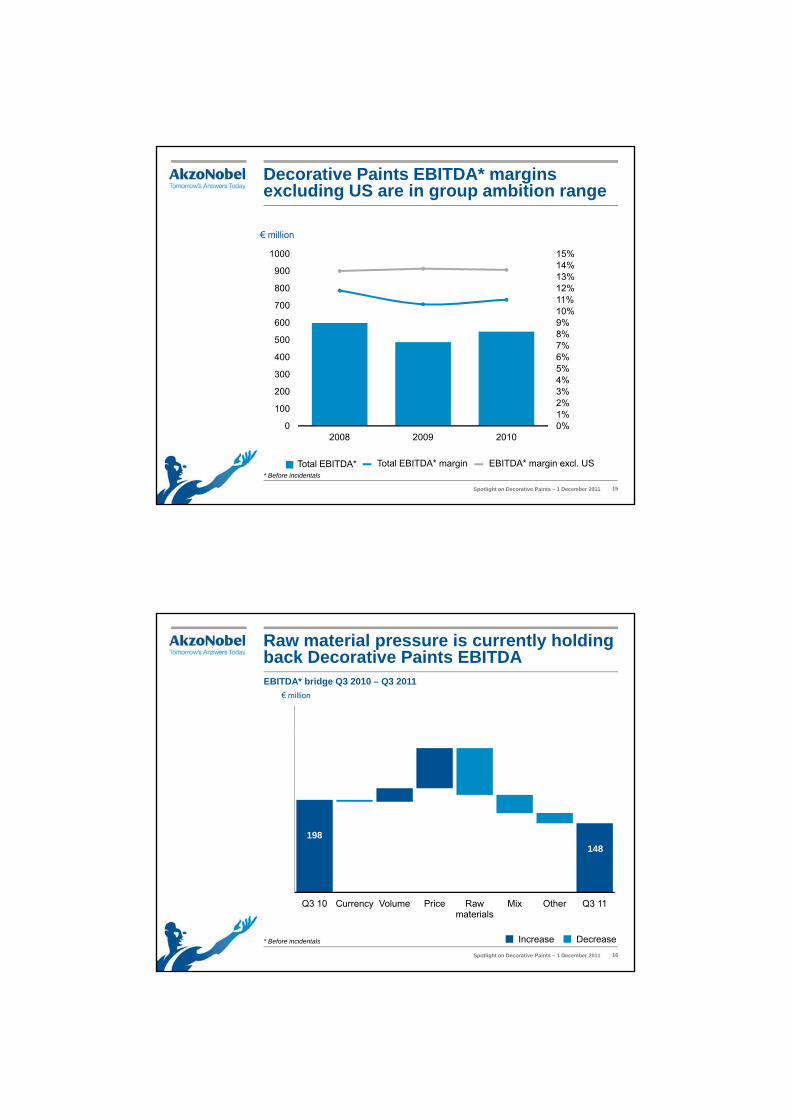

Decorative Paints EBITDA* margins excluding US are in group ambition range

14%15%1000

€ million

4%5%6%7%8%9%10%11%12%13%14%

300

400

500

600

700

800

900

0%1%2%3%

0

100

200

2008 2009 2010

Total EBITDA* Total EBITDA* margin* Before incidentals

EBITDA* margin excl. US

Spotlight on Decorative Paints – 1 December 2011 15

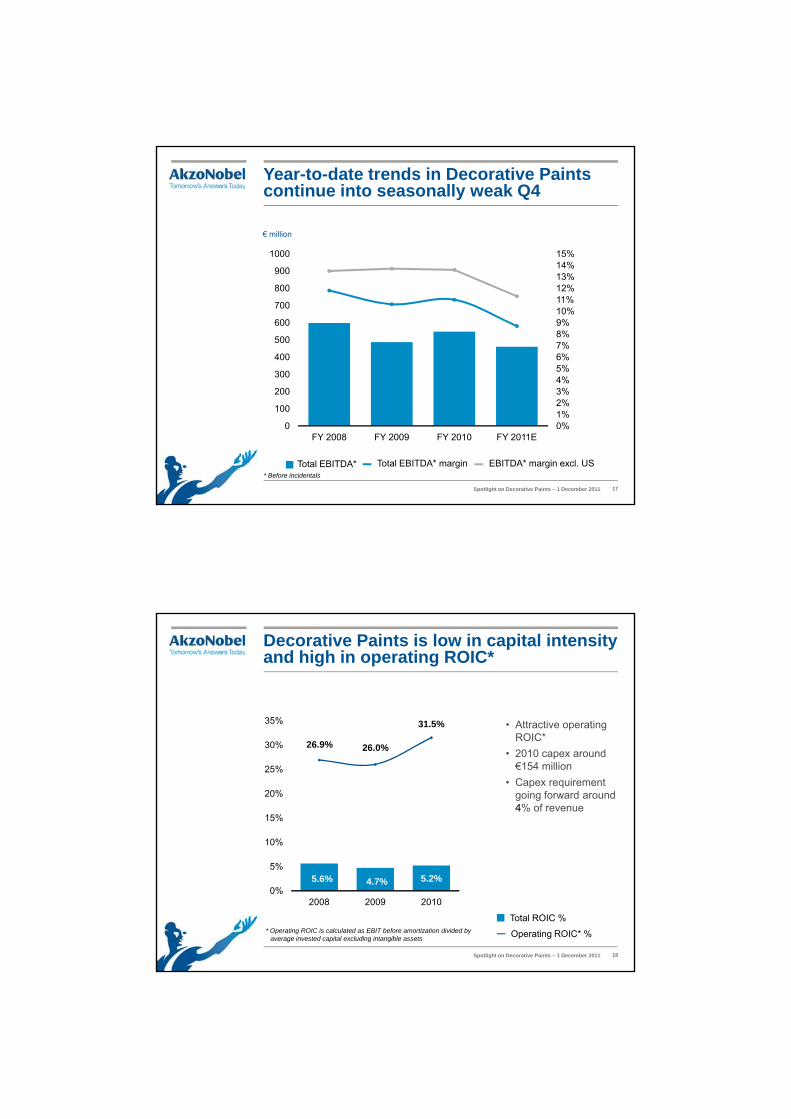

Raw material pressure is currently holding back Decorative Paints EBITDAEBITDA* bridge Q3 2010 – Q3 2011

€ million

(89)

1,964

98

198148

Q3 10 Currency Volume Price Raw materials

Mix Other Q3 11

Increase Decrease* Before incidentals

Spotlight on Decorative Paints – 1 December 2011 16

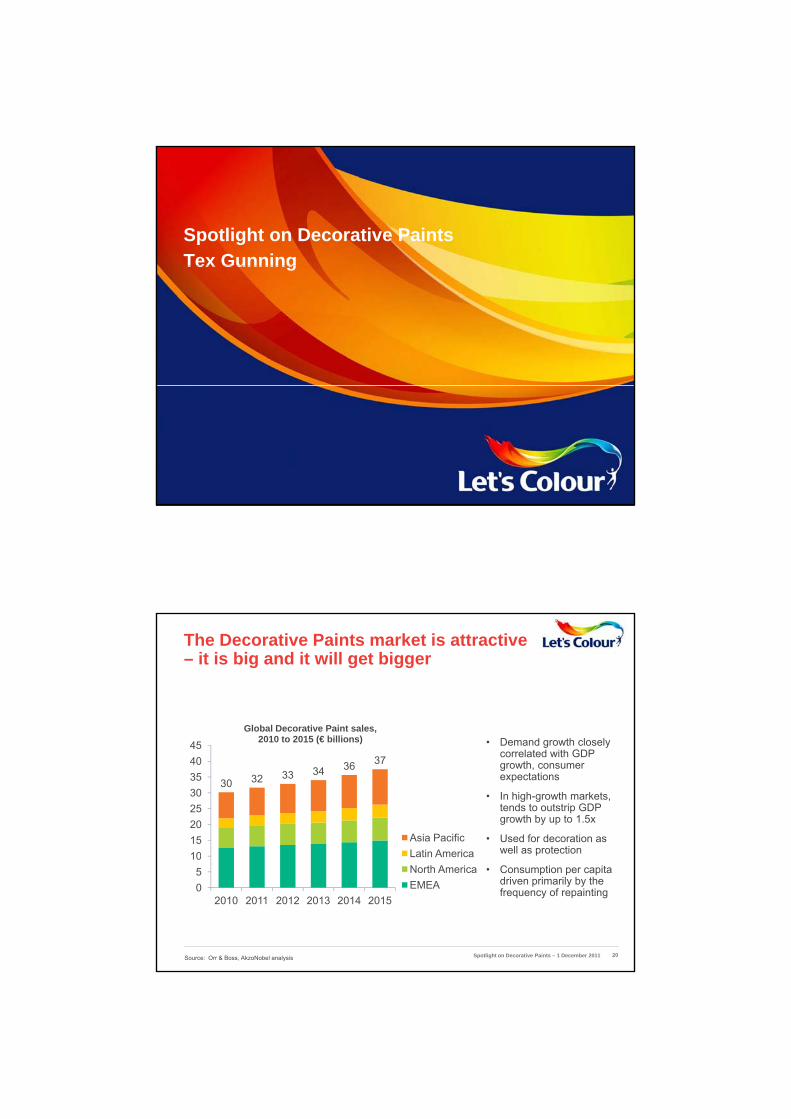

Year-to-date trends in Decorative Paints continue into seasonally weak Q4

14%15%1000

€ million

4%5%6%7%8%9%10%11%12%13%14%

300

400

500

600

700

800

900

0%1%2%3%

0

100

200

FY 2008 FY 2009 FY 2010 FY 2011E

Total EBITDA* Total EBITDA* margin* Before incidentals

EBITDA* margin excl. US

Spotlight on Decorative Paints – 1 December 2011 17

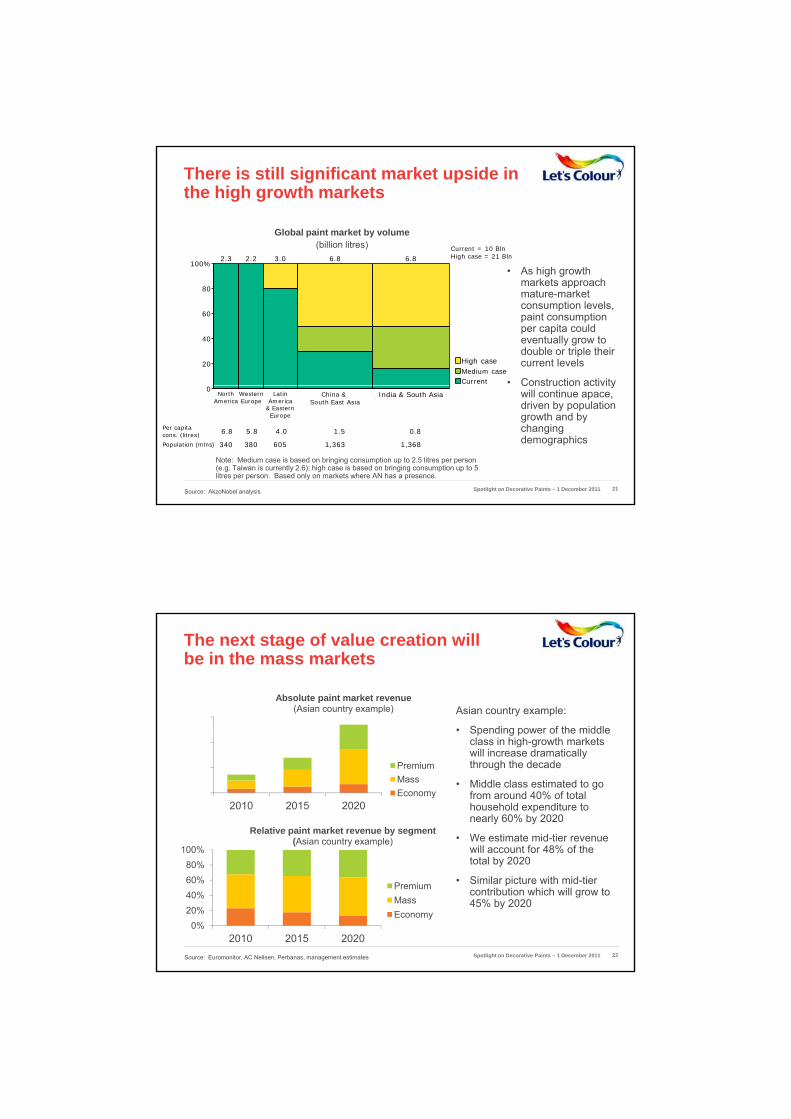

Decorative Paints is low in capital intensity and high in operating ROIC*

35% 31.5% • Attractive operating

10%

15%

20%

25%

30% 26.9% 26.0%ROIC*

• 2010 capex around €154 million

• Capex requirement going forward around 4% of revenue

0%

5%

2008 2009 2010

Total ROIC %

Operating ROIC* %

4.7%5.6%

9.7%

* Operating ROIC is calculated as EBIT before amortization divided by average invested capital excluding intangible assets

5.2%

Spotlight on Decorative Paints – 1 December 2011 18

Spotlight on Decorative PaintsTex GunningTex Gunning

The Decorative Paints market is attractive – it is big and it will get bigger

Global Decorative Paint sales,

30 32 33 34 36 37

1015202530354045

,2010 to 2015 (€ billions)

Asia PacificLatin America

• Demand growth closely correlated with GDP growth, consumer expectations

• In high-growth markets, tends to outstrip GDP growth by up to 1.5x

• Used for decoration as well as protection

05

10

2010 2011 2012 2013 2014 2015

Latin AmericaNorth AmericaEMEA

well as protection

• Consumption per capita driven primarily by the frequency of repainting

Source: Orr & Boss, AkzoNobel analysis Spotlight on Decorative Paints – 1 December 2011 20

There is still significant market upside in the high growth markets

100%2.3 2.2 3.0 6.8 6.8

Current = 10 BlnHigh case = 21 Bln

Global paint market by volume (billion litres)

20

40

60

80

100%

CurrentMedium caseHigh case

• As high growth markets approach mature-market consumption levels, paint consumption per capita could eventually grow to double or triple their current levels

• Construction activity

Source: AkzoNobel analysis

0North

AmericaWesternEurope

LatinAmerica

& EasternEurope

China &South East Asia

India & South Asia

6.8 5.8 4.0 1.5 0.8Per capitacons. (litres)

340 380 605 1,363 1,368Population (mlns)

Note: Medium case is based on bringing consumption up to 2.5 litres per person (e.g. Taiwan is currently 2.6); high case is based on bringing consumption up to 5 litres per person. Based only on markets where AN has a presence.

Construction activity will continue apace, driven by population growth and by changing demographics

Spotlight on Decorative Paints – 1 December 2011 21

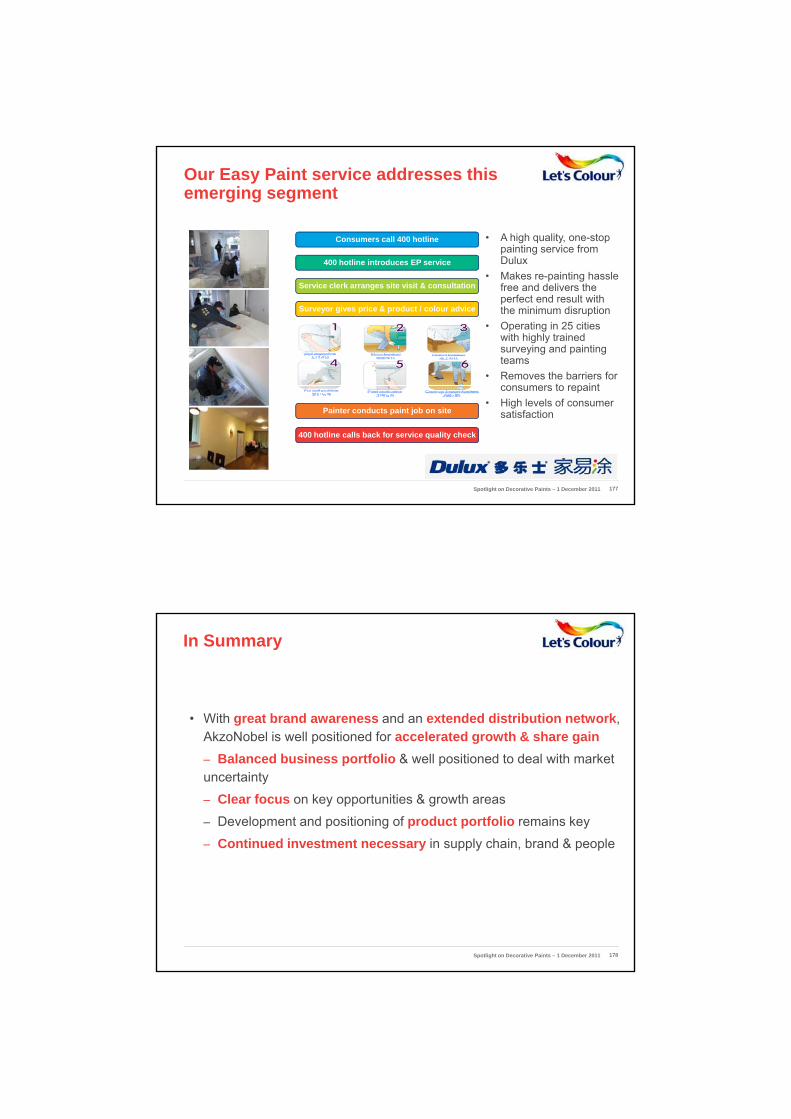

The next stage of value creation will be in the mass markets

Absolute paint market revenue(Asian country example) Asian country example:

• Spending power of the middle

2010 2015 2020

PremiumMassEconomy

100%

Relative paint market revenue by segment(Asian country example)

Spending power of the middle class in high-growth markets will increase dramatically through the decade

• Middle class estimated to go from around 40% of total household expenditure to nearly 60% by 2020

• We estimate mid-tier revenue will account for 48% of the

Source: Euromonitor, AC Neilsen, Perbanas, management estimates

0%20%40%60%80%

100%

2010 2015 2020

PremiumMassEconomy

will account for 48% of the total by 2020

• Similar picture with mid-tier contribution which will grow to 45% by 2020

Spotlight on Decorative Paints – 1 December 2011 22

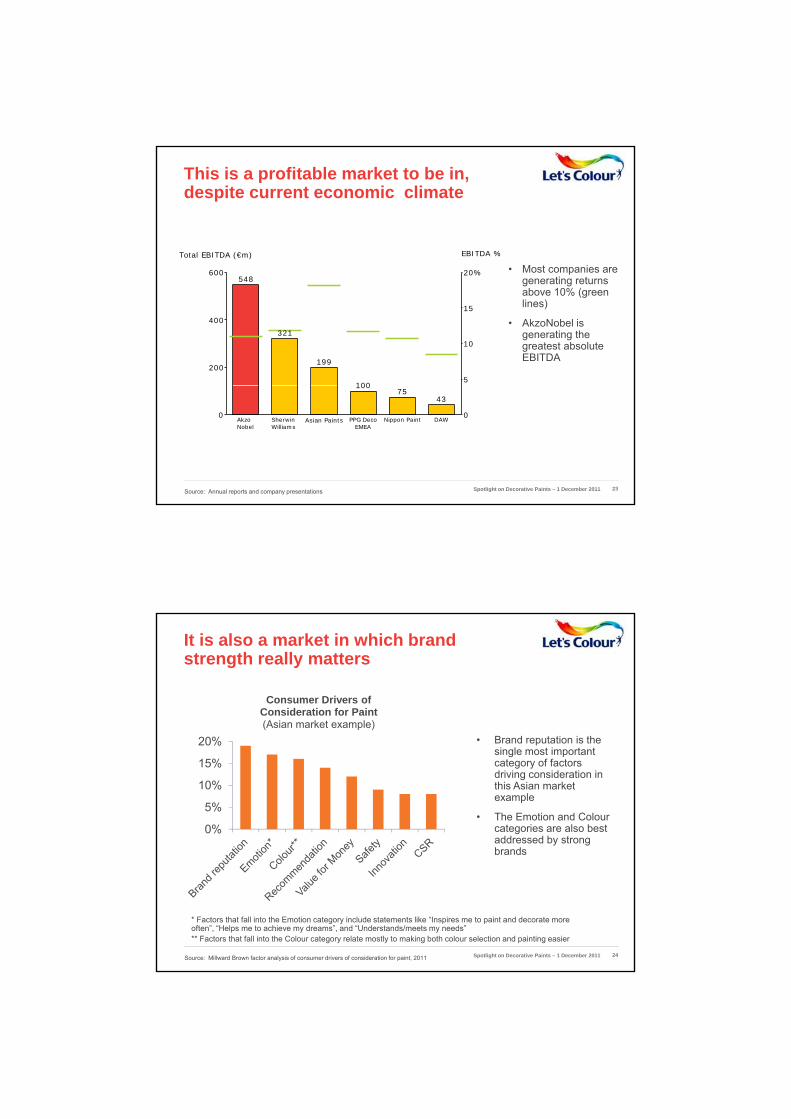

This is a profitable market to be in, despite current economic climate

M t iTotal EBITDA (€m) EBITDA %

• Most companies are generating returns above 10% (green lines)

• AkzoNobel is generating the greatest absolute EBITDA

200

400

600

5

10

15

20%548

321

199

100

Source: Annual reports and company presentations

0 0AkzoNobel

SherwinWilliams

Asian Paints PPG DecoEMEA

100

Nippon Paint

75

DAW

43

Spotlight on Decorative Paints – 1 December 2011 23

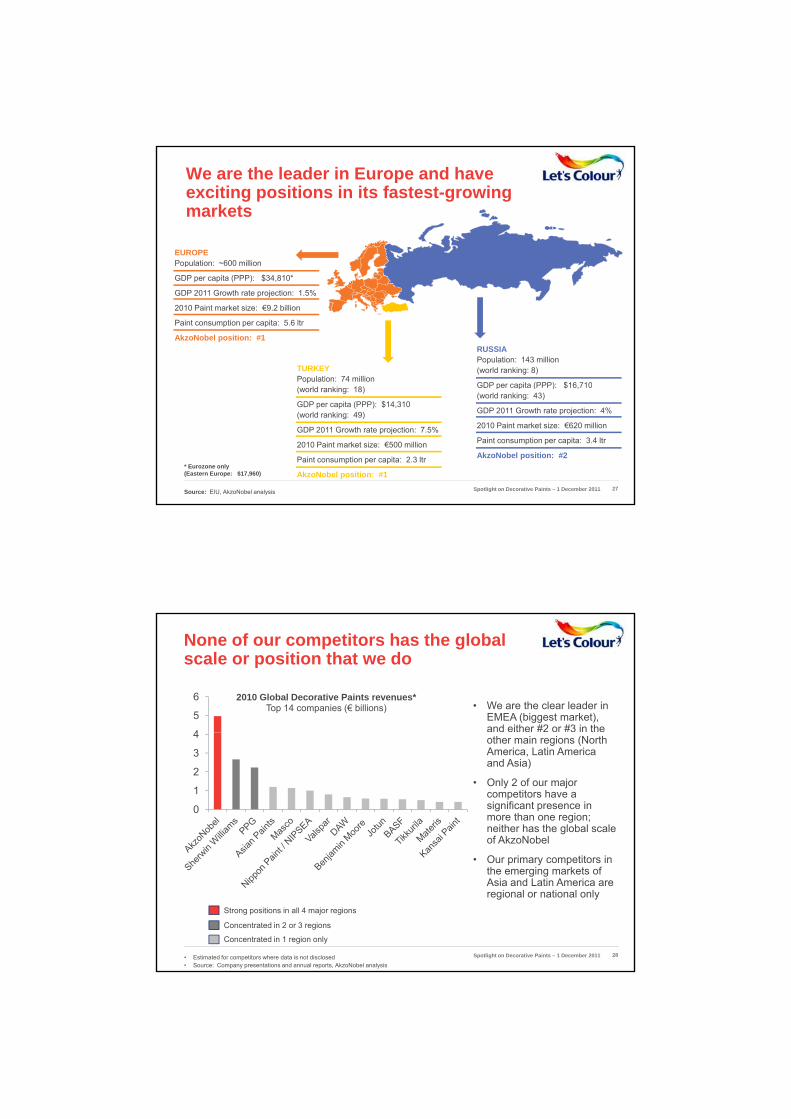

It is also a market in which brand strength really matters

Consumer Drivers of Consideration for Paint(Asian market example)

0%

5%

10%

15%

20% • Brand reputation is the single most important category of factors driving consideration in this Asian market example

• The Emotion and Colour categories are also best addressed by strong brands

Source: Millward Brown factor analysis of consumer drivers of consideration for paint, 2011

* Factors that fall into the Emotion category include statements like “Inspires me to paint and decorate more often”, “Helps me to achieve my dreams”, and “Understands/meets my needs”** Factors that fall into the Colour category relate mostly to making both colour selection and painting easier

brands

Spotlight on Decorative Paints – 1 December 2011 24

AkzoNobel has solid positions in some of the most exciting markets in Asia

CHINAPopulation: 1.34 billion(world ranking: 1)

GDP per capita (PPP): $8,620( ld ki 70)(world ranking: 70)

GDP 2011 Growth rate projection: 9%

2010 Paint market size: €3.4 billion

Paint consumption per capita: 1.4 ltr

AkzoNobel position: #2

INDONESIAPopulation: 238 million

VIETNAMPopulation: 86 million(world ranking: 13)

GDP per capita (PPP): $3 380

Source: EIU, AkzoNobel analysis

(world ranking: 4)

GDP per capita (PPP): $4,560(world ranking: 80)

GDP 2011 Growth rate projection: 6.5%

2010 Paint market size: €300 million

Paint consumption per capita: 1.1 ltr

AkzoNobel position: #1

GDP per capita (PPP): $3,380(world ranking: 84)

GDP 2011 Growth rate projection: 6%

2010 Paint market size: €150 million

Paint consumption per capita: 1.5 ltr

AkzoNobel position: #1

Spotlight on Decorative Paints – 1 December 2011 25

We have outpaced our competitors in the biggest market in Latin America

BRAZILPopulation: 191 million(world ranking: 5)

GDP per capita (PPP): $11,920(world ranking: 57)

GDP 2011 Growth rate projection: 3.6%

2010 Paint market size: €940 million

Paint consumption per capita: 4.6 ltr

AkzoNobel position: #1

ARGENTINAPopulation: 40 million

Source: EIU, AkzoNobel analysis

(world ranking: 31)

GDP per capita (PPP): $17,370(world ranking: 41)

GDP 2011 Growth rate projection: 8.5%

2010 Paint market size: €175 million

Paint consumption per capita: 3.2 ltr

AkzoNobel position: #1Spotlight on Decorative Paints – 1 December 2011 26

We are the leader in Europe and have exciting positions in its fastest-growing markets

EUROPEPopulation: ~600 million

RUSSIAPopulation: 143 million(world ranking: 8)

GDP per capita (PPP): $16 710

TURKEYPopulation: 74 million

p

GDP per capita (PPP): $34,810*

GDP 2011 Growth rate projection: 1.5%

2010 Paint market size: €9.2 billion

Paint consumption per capita: 5.6 ltr

AkzoNobel position: #1

GDP per capita (PPP): $16,710(world ranking: 43)

GDP 2011 Growth rate projection: 4%

2010 Paint market size: €620 million

Paint consumption per capita: 3.4 ltr

AkzoNobel position: #2

(world ranking: 18)

GDP per capita (PPP): $14,310(world ranking: 49)

GDP 2011 Growth rate projection: 7.5%

2010 Paint market size: €500 million

Paint consumption per capita: 2.3 ltr

AkzoNobel position: #1

Source: EIU, AkzoNobel analysis

* Eurozone only (Eastern Europe: $17,960)

Spotlight on Decorative Paints – 1 December 2011 27

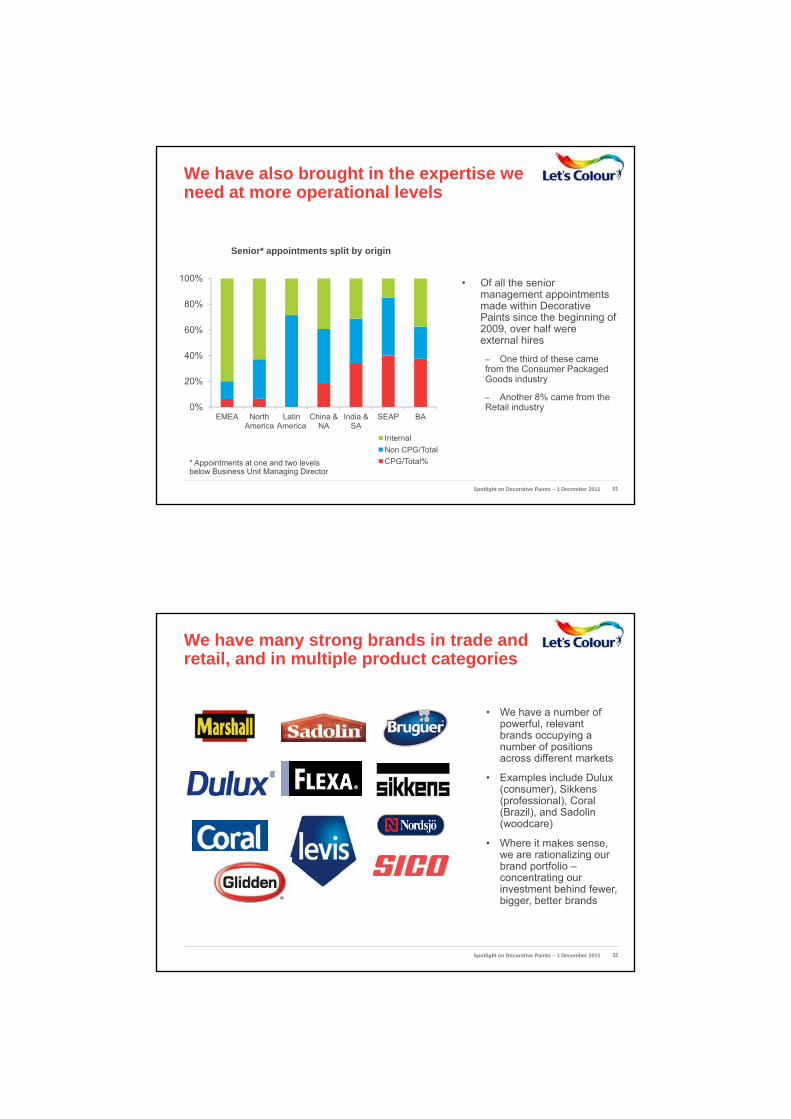

None of our competitors has the global scale or position that we do

4

5

6 2010 Global Decorative Paints revenues*Top 14 companies (€ billions) • We are the clear leader in

EMEA (biggest market), and either #2 or #3 in the

0

1

2

3

4 other main regions (North America, Latin America and Asia)

• Only 2 of our major competitors have a significant presence in more than one region; neither has the global scale of AkzoNobel

Concentrated in 2 or 3 regions

Concentrated in 1 region only

Strong positions in all 4 major regions

• Our primary competitors in the emerging markets of Asia and Latin America are regional or national only

• Estimated for competitors where data is not disclosed• Source: Company presentations and annual reports, AkzoNobel analysis

Spotlight on Decorative Paints – 1 December 2011 28

AkzoNobel has the people, brands and competencies to win globally

• We can offer the best development opportunities in the industry, helping us to Peopleattract and retain the best talent

• We can invest more to develop and support more powerful brands and global brand identities and industry-leading, game-changing innovations

Brands

• We can build and leverage experience and learning across markets and develop repeatable models to increase efficiency and effectiveness

Competencies

Spotlight on Decorative Paints – 1 December 2011 29

We have built a very strong leadership team at the top end

Amit JainIndia &

South Asia

Jeremy RoweSouth East

Asia & Pacific

Bob TaylorNorth America

Jaap KuiperLatin America

Liangqi LinChina &

North Asia

Richard StuckesEurope, Middle East & Africa

Sucheta GovilMarketing

David O’BrienBusiness Innovation

Spotlight on Decorative Paints – 1 December 2011 30

We have also brought in the expertise we need at more operational levels

Senior* appointments split by origin

• Of all the senior management appointments made within Decorative Paints since the beginning of 2009, over half were external hires

– One third of these came from the Consumer Packaged Goods industry20%

40%

60%

80%

100%

– Another 8% came from the Retail industry0%

EMEA North America

Latin America

China & NA

India & SA

SEAP BA

InternalNon CPG/TotalCPG/Total%* Appointments at one and two levels

below Business Unit Managing Director

Spotlight on Decorative Paints – 1 December 2011 31

We have many strong brands in trade and retail, and in multiple product categories

• We have a number of powerful, relevant b d ibrands occupying a number of positions across different markets

• Examples include Dulux (consumer), Sikkens(professional), Coral (Brazil), and Sadolin(woodcare)

• Where it makes sense, ti li iwe are rationalizing our

brand portfolio –concentrating our investment behind fewer, bigger, better brands

Spotlight on Decorative Paints – 1 December 2011 32

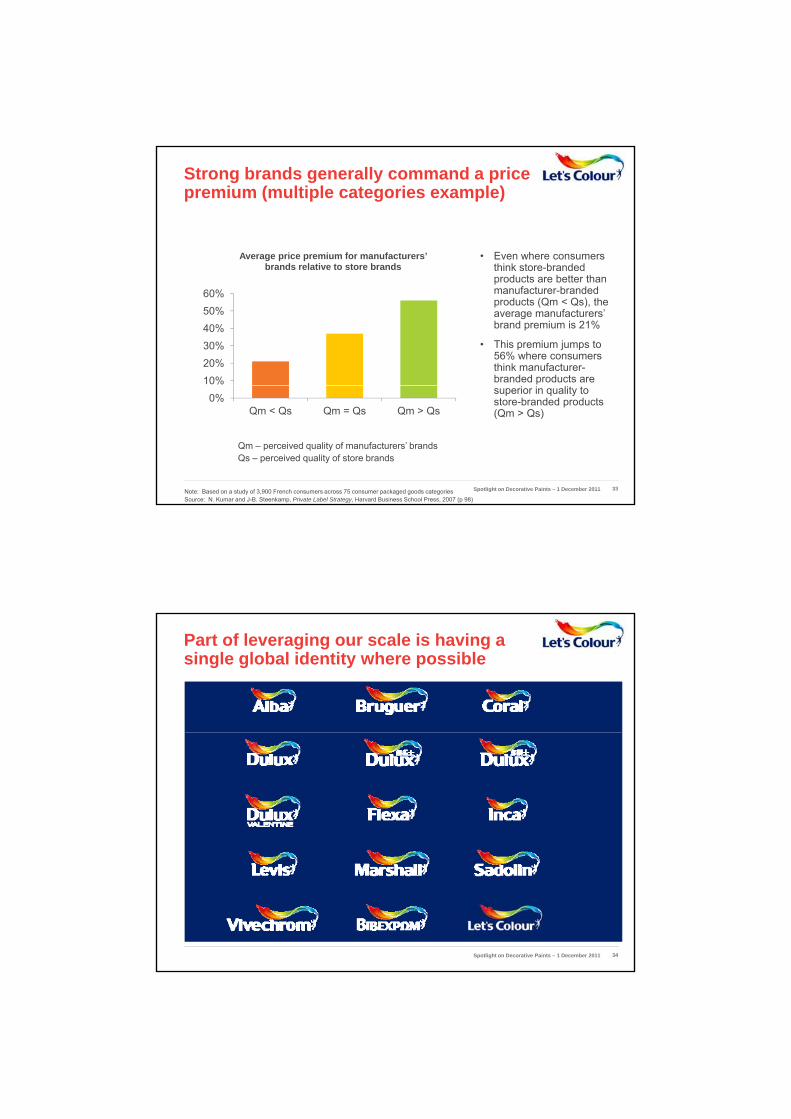

Strong brands generally command a price premium (multiple categories example)

Average price premium for manufacturers’ brands relative to store brands

• Even where consumers think store branded

10%20%30%40%50%60%

brands relative to store brands think store-branded products are better than manufacturer-branded products (Qm < Qs), the average manufacturers’ brand premium is 21%

• This premium jumps to 56% where consumers think manufacturer-branded products are

0%Qm < Qs Qm = Qs Qm > Qs

Note: Based on a study of 3,900 French consumers across 75 consumer packaged goods categoriesSource: N. Kumar and J-B. Steenkamp, Private Label Strategy, Harvard Business School Press, 2007 (p 98)

Qm – perceived quality of manufacturers’ brandsQs – perceived quality of store brands

superior in quality to store-branded products (Qm > Qs)

Spotlight on Decorative Paints – 1 December 2011 33

Part of leveraging our scale is having a single global identity where possible

Spotlight on Decorative Paints – 1 December 2011 34

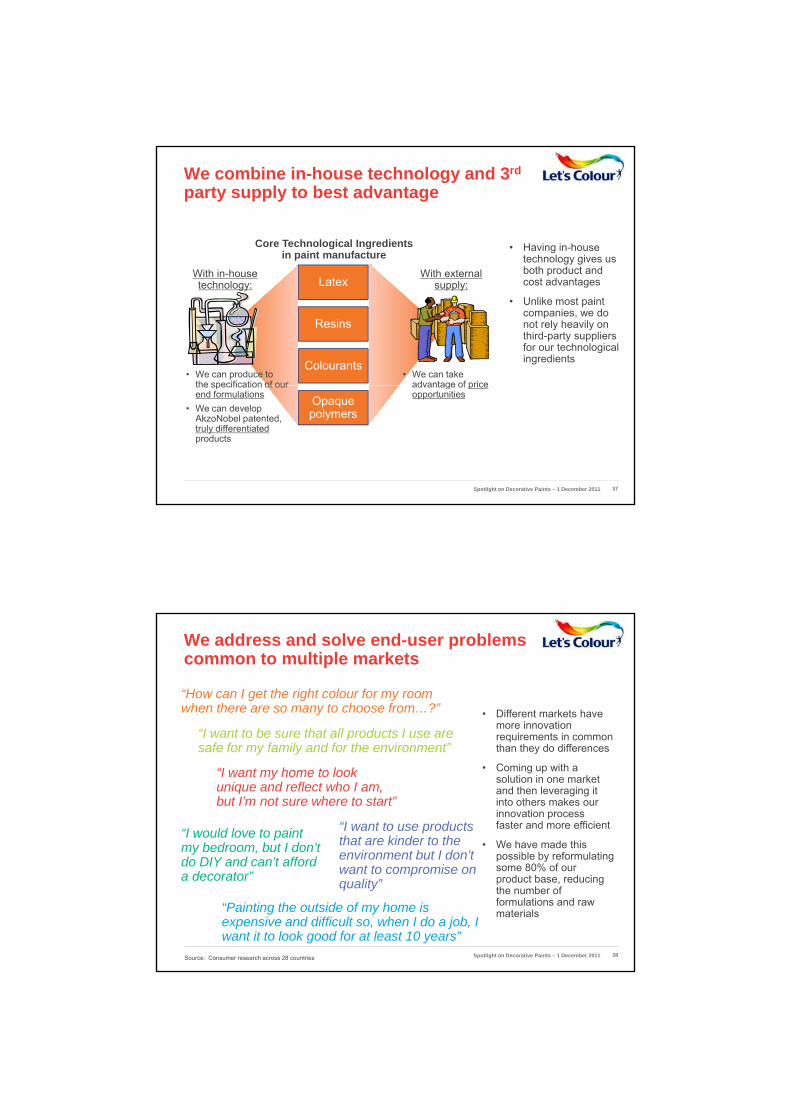

We are supporting our brand and growth ambitions with increased A&P spend

Advertising & Promotion spendas a percentage of revenue

• We have increased our overall A&P spend in

6%

8%

10%

12%as a percentage of revenue overall A&P spend in

proportion to revenue

• Higher spend % in the markets with the greatest growth potential

• Investing in the North American market as part of our US turnaround / Glidden

0%

2%

4%

EMEA NA LATAM ASIA Global

200920102011 (Est)2012 (Est)

turnaround / Glidden relaunch strategy

Spotlight on Decorative Paints – 1 December 2011 35

Our scale means we can outspend our competitors on Research and Development

Research & Development spend (total and %)

• AkzoNobel’s R&D spend in 2010 higher than that of our major competitors

• We leverage technological capabilities across Business Areas

Source: Company annual reports and presentations Spotlight on Decorative Paints – 1 December 2011 36

We combine in-house technology and 3rd

party supply to best advantage

Core Technological Ingredients in paint manufacture

• Having in-house technology gives us

Latex

Resins

Colourants

With in-house technology:

With external supply:

both product and cost advantages

• Unlike most paint companies, we do not rely heavily on third-party suppliers for our technological ingredients

• We can produce to the specification of our

• We can take advantage of price

Opaquepolymers

the specification of our end formulations

• We can develop AkzoNobel patented, truly differentiatedproducts

advantage of price opportunities

Spotlight on Decorative Paints – 1 December 2011 37

We address and solve end-user problems common to multiple markets

• Different markets have more innovation

“I want to be sure that all products I use are

“How can I get the right colour for my room when there are so many to choose from…?”

requirements in common than they do differences

• Coming up with a solution in one market and then leveraging it into others makes our innovation process faster and more efficient

• We have made this ibl b f l i

I want to be sure that all products I use are safe for my family and for the environment”

“I want my home to look unique and reflect who I am, but I’m not sure where to start”

“I would love to paint my bedroom, but I don’t

“I want to use products that are kinder to the

i t b t I d ’t possible by reformulating some 80% of our product base, reducing the number of formulations and raw materials

y bed oo , but do tdo DIY and can’t afford a decorator”

“Painting the outside of my home is expensive and difficult so, when I do a job, I want it to look good for at least 10 years”

Source: Consumer research across 28 countries

environment but I don’t want to compromise on quality”

Spotlight on Decorative Paints – 1 December 2011 38

We are building global competencies by codifying and rolling out our best practises

Sales • Category management• Pricing excellence

S f ff

Research & Development

• Stage Gate process for pipeline management

Repeatable models within specific functions

• Sales force effectiveness• Global glossary

p

Marketing • Insight generation• Communications

development & evaluation• Point-of-Sale marketing

IntegratedSupply Chain

• LEAN methodology for manufacturing excellence

• Purchasing back-end processes

Storesoperations

• Stores management• Estate management

Support • Project management• Underlying culture of high

performance and employee engagementg g

• The multi-year implementation of a global ERP system, to be completed by early 2013 (70% rolled out already)

Key enablers

• Product Market Review process for prioritizing and reviewing innovation projects

• Integrated Business Planning for aligning short and medium term sales forecasts with manufacturing planning

Cross-functional repeatable models

Spotlight on Decorative Paints – 1 December 2011 39

These efforts are a critical aspect of the journey we have been on since our transformational merger in 2008

the ICI business (eliminate overlap reduceIntegrate the ICI business (eliminate overlap, reduce complexity, build a common culture)

underperforming businesses (e.g. US, Germany)

from our multi-local, fragmented history into a global company with global scale

Turnaround

Transform

By growing market share in both mature and emerging markets

Grow

Spotlight on Decorative Paints – 1 December 2011 40

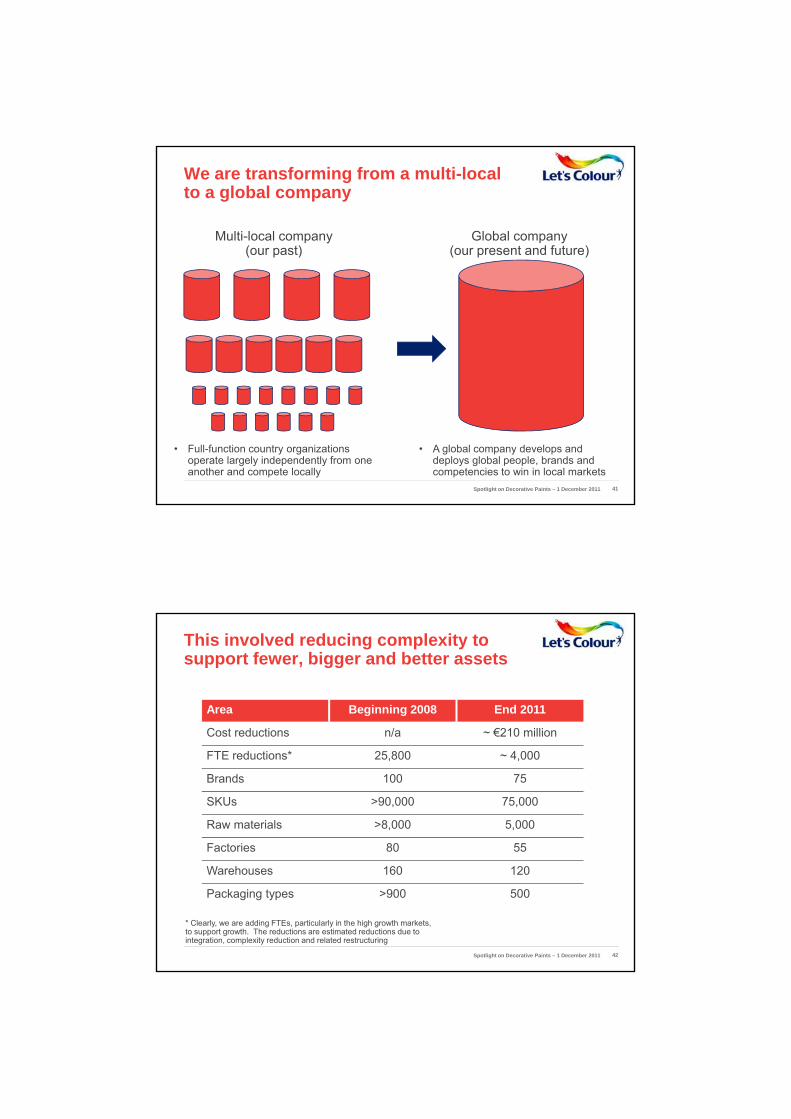

We are transforming from a multi-local to a global company

Multi-local company (our past)

Global company(our present and future)

• Full-function country organizations operate largely independently from one another and compete locally

• A global company develops and deploys global people, brands and competencies to win in local markets

Spotlight on Decorative Paints – 1 December 2011 41

This involved reducing complexity to support fewer, bigger and better assets

Area Beginning 2008 End 2011

Cost reductions n/a ~ €210 millionCost reductions n/a ~ €210 million

FTE reductions* 25,800 ~ 4,000

Brands 100 75

SKUs >90,000 75,000

Raw materials >8,000 5,000

Factories 80 55

Warehouses 160 120

Packaging types >900 500

* Clearly, we are adding FTEs, particularly in the high growth markets, to support growth. The reductions are estimated reductions due to integration, complexity reduction and related restructuring

Spotlight on Decorative Paints – 1 December 2011 42

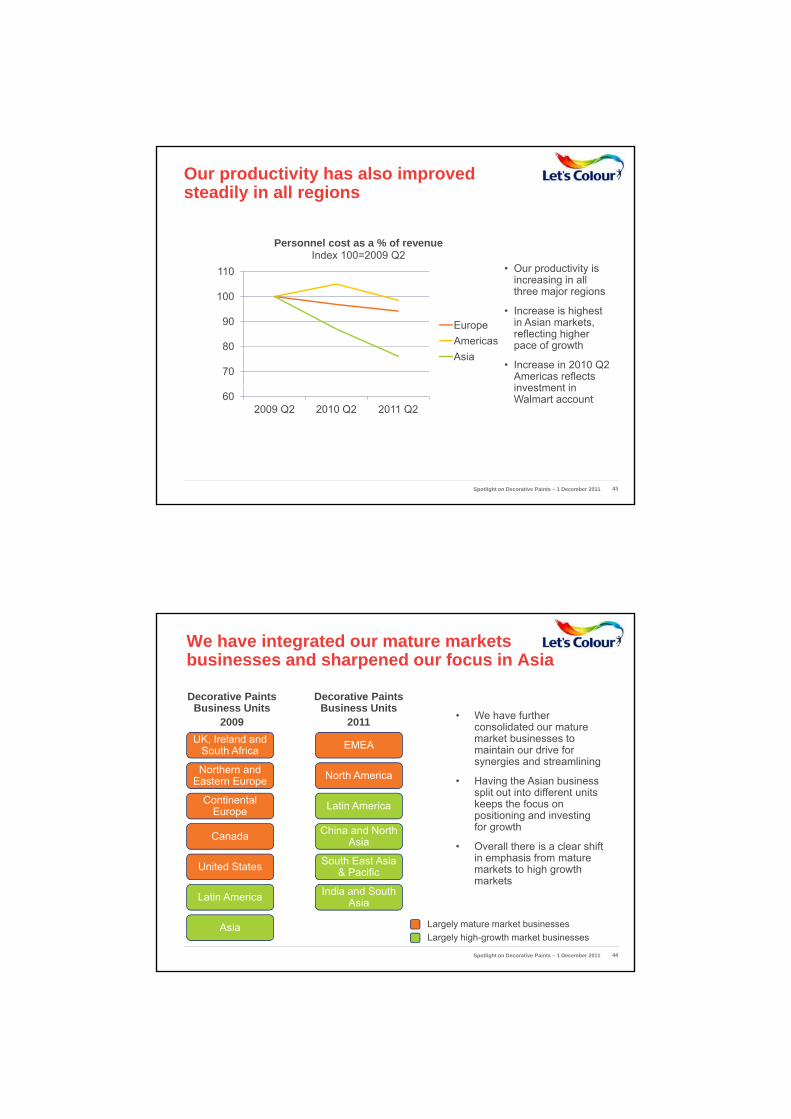

Our productivity has also improved steadily in all regions

Personnel cost as a % of revenueIndex 100=2009 Q2

O d ti it i

70

80

90

100

110

EuropeAmericasAsia

• Our productivity is increasing in all three major regions

• Increase is highest in Asian markets, reflecting higher pace of growth

• Increase in 2010 Q2 Americas reflects in estment in

602009 Q2 2010 Q2 2011 Q2

investment in Walmart account

Spotlight on Decorative Paints – 1 December 2011 43

We have integrated our mature markets businesses and sharpened our focus in Asia

• We have further consolidated our mature

Decorative Paints Business Units

2009

Decorative Paints Business Units

2011market businesses to maintain our drive for synergies and streamlining

• Having the Asian business split out into different units keeps the focus on positioning and investing for growth

• Overall there is a clear shift

UK, Ireland and South Africa

Northern and Eastern Europe

Continental Europe

Canada

EMEA

North America

Latin America

China and North Asia

in emphasis from mature markets to high growth markets

United States

Latin America

Asia

South East Asia & Pacific

India and South Asia

Largely mature market businessesLargely high-growth market businesses

Spotlight on Decorative Paints – 1 December 2011 44

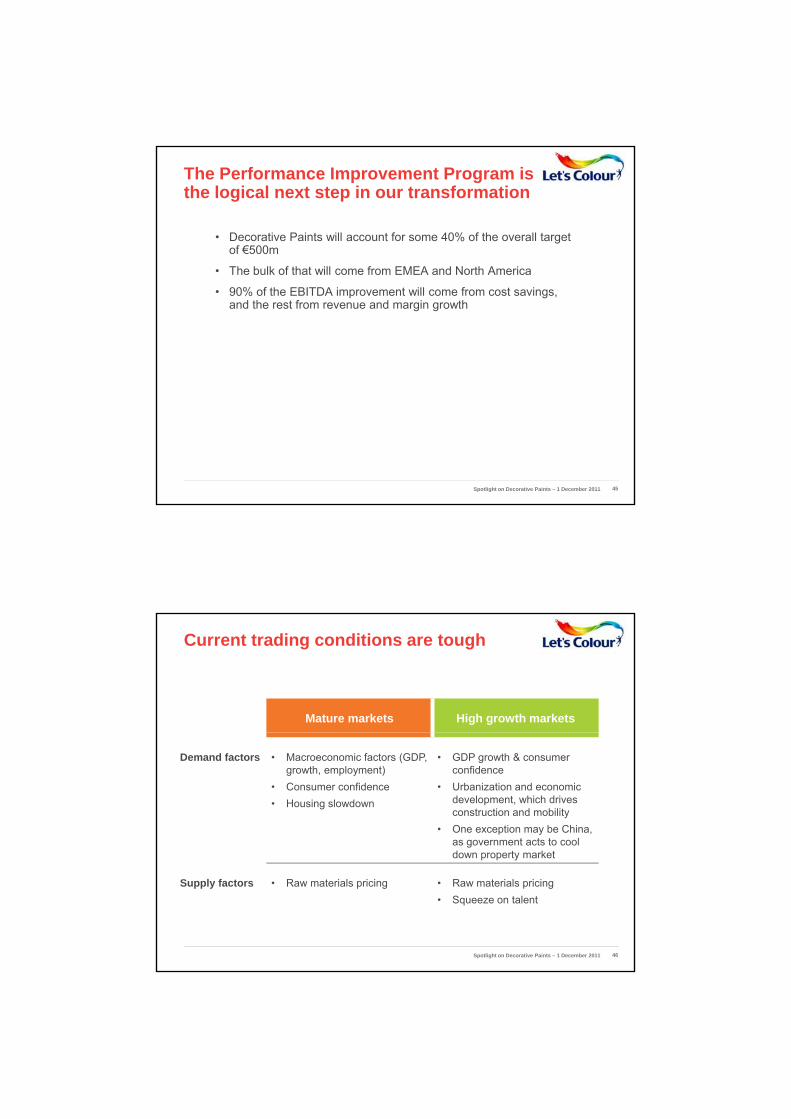

The Performance Improvement Program is the logical next step in our transformation

• Decorative Paints will account for some 40% of the overall target of €500m

• The bulk of that will come from EMEA and North America

• 90% of the EBITDA improvement will come from cost savings, and the rest from revenue and margin growth

Spotlight on Decorative Paints – 1 December 2011 45

Current trading conditions are tough

Mature markets High growth markets

Demand factors • Macroeconomic factors (GDP, growth, employment)

• Consumer confidence• Housing slowdown

• GDP growth & consumer confidence

• Urbanization and economic development, which drives construction and mobility

• One exception may be China,as government acts to cool d t k tdown property market

Supply factors • Raw materials pricing • Raw materials pricing• Squeeze on talent

Spotlight on Decorative Paints – 1 December 2011 46

Regional TiO2 Pricing – in USD/tonne

TiO2 prices are a challenge

4.000USD/Tonne

H1 2011 Decorative Paints raw material spend

(Total = €1.1 billion)

3.500

2.500

3.000 +91%

2.000

1.500

1.000

500Europe

Asia

North America

29%

17%20%

16%

8%10%

Resins & BindersPackaging MaterialsTitanium Dioxide

Source: ICIS Pricing

2003 20112009200720010

2005

• Pricing has gone up steadily in USD over the last decade, across all regions

• TiO2 accounts for 1/5th of our total raw materials spend (up from 17% in 2008)

Titanium DioxideAdditivesSolvents & DiluentsOther

Spotlight on Decorative Paints – 1 December 2011 47

There has been a lag in new extraction capacity coming onstream

Global supply & demand outlook for Ti mineral 2000 – 2020F

Alth h th i• Although there is no shortage of feedstock in the ground (mostly ilmenite and rutile), the market fears an expected shortage in TiO2 supply

• High current prices are bound to drive

Source: TZMI

new investment in capacity – we have already seen ample evidence of this, particularly in ChinaConsumption

Likely new projects (not yet approved)

Approved new projects

Existing production

Spotlight on Decorative Paints – 1 December 2011 48

We are actively working both to increase security of supply and reduce dependence

• Leveraging strong relationships with major suppliers, including the

• Using our formulating science expertise and our high-throughput experimentation

Sourcing Research & Development

major suppliers, including the emerging suppliers in China

• Maintaining a safety margin of stock

• Partnering with China-based Guangxi CAVA Titanium Industry to manufacture and distribute titanium dioxide

– With this deal a new titanium dioxide facility will be developed in Qinzhou with

g g p pcapability to reduce our TiO2 dependence in 3 ways:

– Using existing replacement technology

– Working with key suppliers to develop new technology

– Increasing efficiency of use through formulation improvements

• Combined, these initiatives mean we can d t t l TiO2 hilfacility will be developed in Qinzhou with

a production capacity of 100,000 tons, slated to begin operation in the beginning of 2014

– Further guarantees security of supply for the Asian market

reduce our total TiO2 usage while maintaining cost efficiency and product attributes

Spotlight on Decorative Paints – 1 December 2011 49

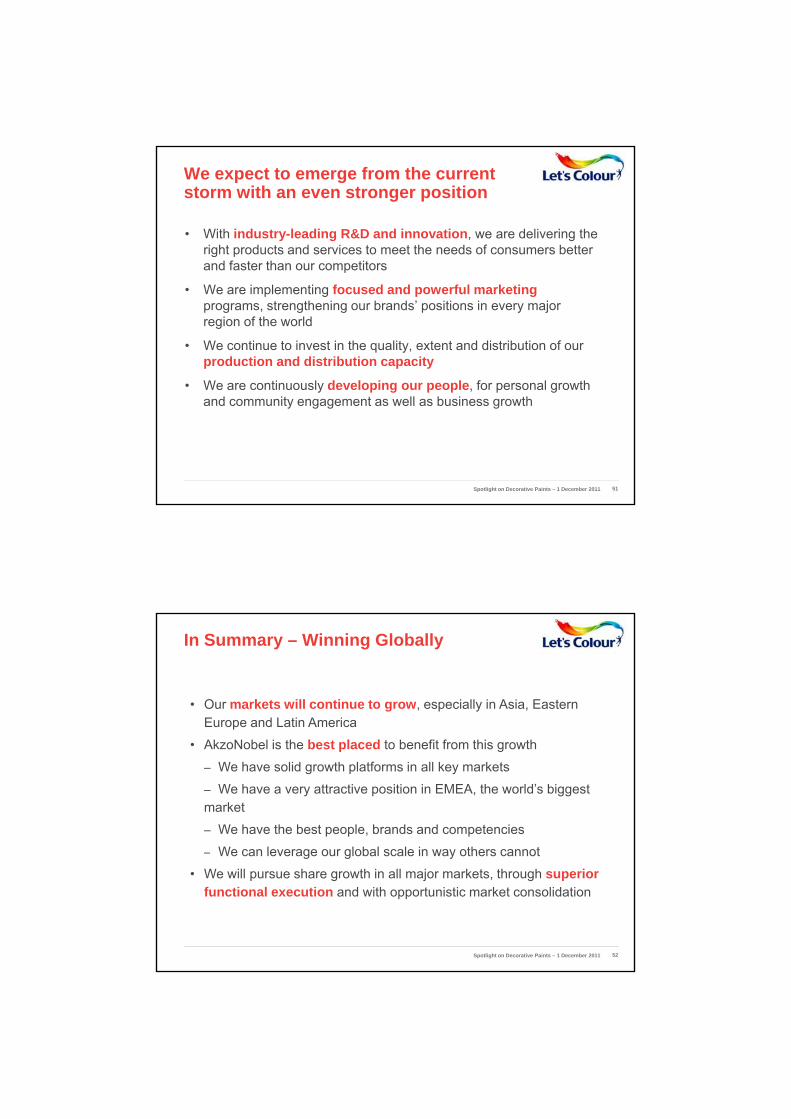

Raw material inflation drives price increases

10 Quarterly price development in % year-on-year(excluding mix effect)

2

0

2

4

6

8( g )

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3-2

2008

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2009 2010 2011

Spotlight on Decorative Paints – 1 December 2011 50

We expect to emerge from the current storm with an even stronger position

• With industry-leading R&D and innovation, we are delivering the right products and services to meet the needs of consumers better and faster than our competitorsand faster than our competitors

• We are implementing focused and powerful marketingprograms, strengthening our brands’ positions in every major region of the world

• We continue to invest in the quality, extent and distribution of our production and distribution capacity

• We are continuously developing our people for personal growth• We are continuously developing our people, for personal growth and community engagement as well as business growth

Spotlight on Decorative Paints – 1 December 2011 51

In Summary – Winning Globally

• Our markets will continue to grow, especially in Asia, Eastern Europe and Latin America

• AkzoNobel is the best placed to benefit from this growth

– We have solid growth platforms in all key markets

– We have a very attractive position in EMEA, the world’s biggest market

– We have the best people, brands and competencies

We can leverage our global scale in way others cannot– We can leverage our global scale in way others cannot

• We will pursue share growth in all major markets, through superior functional execution and with opportunistic market consolidation

Spotlight on Decorative Paints – 1 December 2011 52

MarketingSucheta GovilSucheta Govil

Our vision & plans

• Adding Colour to People’s Lives through inspiring and enabling decoration

• Fewer, Clearly Positioned Stronger brandsSpotlight on Decorative Paints – 1 December 2011 54

End the tyranny of grey, dull spaces

Spotlight on Decorative Paints – 1 December 2011 55

Adding Colour to People’s Lives

Spotlight on Decorative Paints – 1 December 2011 56

What business are we in?

BEAUTIFUL HOMESSpotlight on Decorative Paints – 1 December 2011 57

Our brands will inspire beautiful homes, spaces

To Increase Penetration and

Access for our Brands so Improving Spaces

becomes easy

To Increase Frequency of Painting and Decoration with

Our Brands

“We will Inspire Consumers and Painters to Create Beauty and fight the opportunity cost of grey and shabby”

Source: 3D qualitative research, July 2009 Spotlight on Decorative Paints – 1 December 2011 58

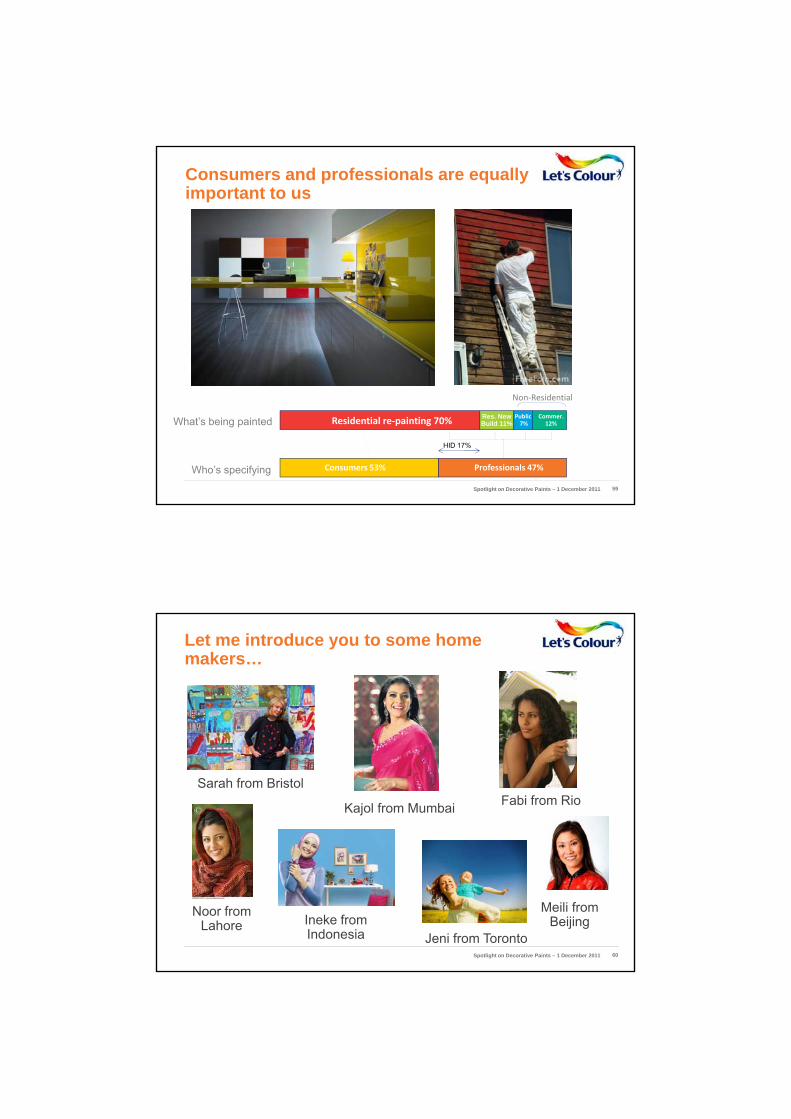

Consumers and professionals are equally important to us

Res. New Build 11%Residential re‐painting 70% Public

7%Commer.

12%

Non‐Residential

Consumers 53% Professionals 47%

What’s being painted

Who’s specifying

HID 17%

Spotlight on Decorative Paints – 1 December 2011 59

Let me introduce you to some home makers…

Sarah from Bristol

Kajol from Mumbai Fabi from Rio

Meili from Beijing

Noor from Lahore

Jeni from TorontoIneke from Indonesia

Spotlight on Decorative Paints – 1 December 2011 60

All say "me and my home are one"

Improving our home is important to feel better

Home is an extension of ourselves

“For all cultures, the home is an expression of the people who live there”

Source: 3D qualitative research, July 2009 Spotlight on Decorative Paints – 1 December 2011 61

Deep consumer insight: one universalpoint in the decorating journey For all:

pride/satisfaction in final end result

Decision to decorate

Finding inspiration,

gathering ideas exciting

Anticipatio

HO

PES

ARS

to decorate

PPR

DMVHMFMS

Satisfaction in doing something you’re good at or that appeals to

your nature

Anxiety about making the

right style/colour

Recognition that there is

physical work

Anticipation of a job well done

Source: Based on Global 3D qualitative research, July 2009

FEA y /

choice

Realisation of everything that could go wrong (buy the wrong product, bad colour choice, lack of

physical skill, disruption, family dissatisfaction)

More difficulties emerge as job starts:

prep, colour looks wrong, takes longer than anticipated, etc.

p ys ca o(boring/

difficult/disruptive) to do

Segment namesDMV: Deliver My VisionPPR: Perfect Professional ResultsHMFMS: Help Me Find My Style

Spotlight on Decorative Paints – 1 December 2011 62

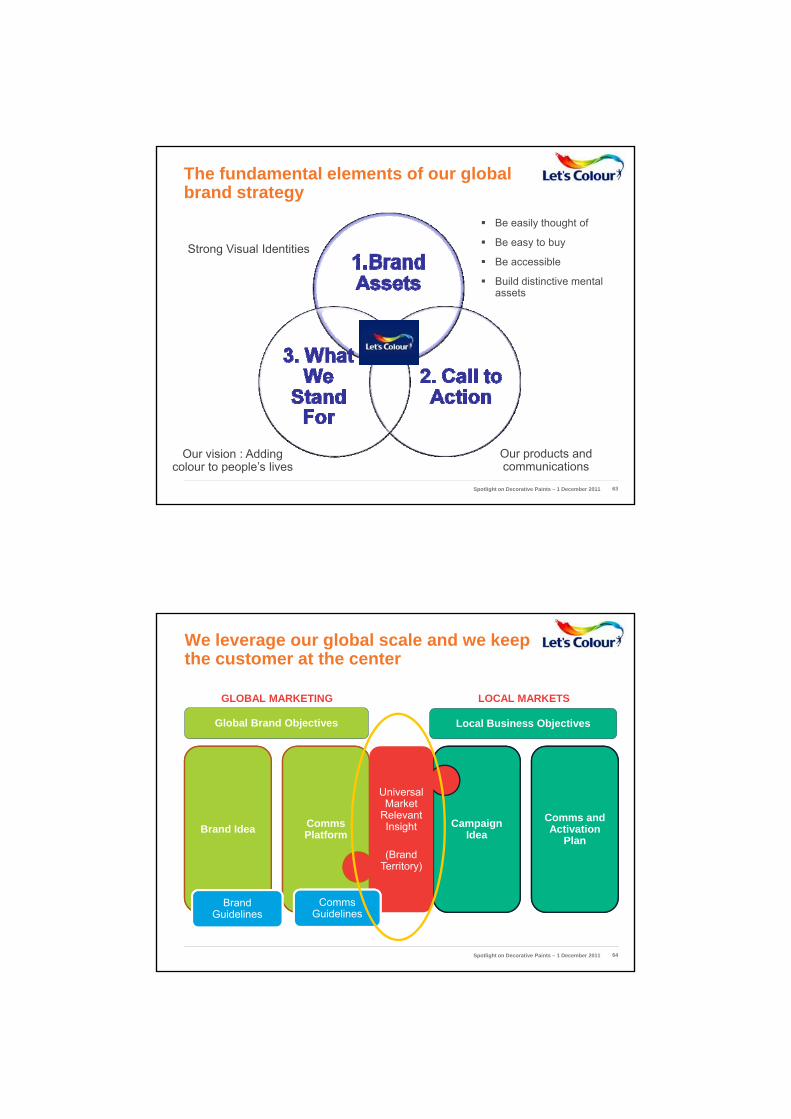

The fundamental elements of our global brand strategy

Strong Visual Identities

Be easily thought of

Be easy to buy

Be accessible

Build distinctive mental assets

Our vision : Addingcolour to people’s lives

Our products and communications

Spotlight on Decorative Paints – 1 December 2011 63

We leverage our global scale and we keepthe customer at the center

GLOBAL MARKETING LOCAL MARKETS

Global Brand Objectives Local Business Objectives

Brand Idea Comms Platform

Campaign Idea

Comms and Activation

Plan

Universal Market

Relevant Insight

(B d

Brand Guidelines

(Brand Territory)

Comms Guidelines

Spotlight on Decorative Paints – 1 December 2011 64

Our main competitive advantage: a greatglobal brand

• Dulux (cluster) sold in more than 50 countries in the world

A l b l b d lAs a global brand we can leverage:• A powerful positioning & strategy• Strong brand assets• Global Big Idea• Innovation products and concepts

Spotlight on Decorative Paints – 1 December 2011 66

Fewer powerful,

Our brands will also be the preferred partner of the professional painter

Fewer powerful, insight driven, business winning brands:• Sikkens

‘Sensations’• Dulux Trade ‘No.1• Herbol – ‘Schnell

Sicher Prod cti ’Sicher Productiv’

Spotlight on Decorative Paints – 1 December 2011 67

Our vision and plans

Adding Colour to People’s Lives through inspiring and enabling decoration• Leadership in Colour• The Art, Science, Delivery • Lock-in• Bigger innovations• Leveraged faster• Sustainability Leadership

Spotlight on Decorative Paints – 1 December 2011 68

InnovationDavid O’BrienDavid O Brien

Innovation will play a major part inachieving our growth objectives

• Growing our share through competitive advantage

• Growing our categories by encouraging frequency and penetration

• Locking professional users and specifiers into our brands

• Improving our margins by adding value and enabling us to compete

‘More people, More often, More money......’

Spotlight on Decorative Paints – 1 December 2011 70

Strategic context

• Consumer/user insight at the heart of innovation

• Major progress on leveraging our scale by moving f lti l l t l b l hfrom a multi-local to a global approach

• Focus of our resources on key initiatives (fewer, bigger, better and faster)

• Short term AND long term perspective

• Delivery of our sustainability objectives

Spotlight on Decorative Paints – 1 December 2011 71

Beautiful homes

Spotlight on Decorative Paints – 1 December 2011 72

Long lasting performance

Spotlight on Decorative Paints – 1 December 2011 73

Future Now

Spotlight on Decorative Paints – 1 December 2011 74

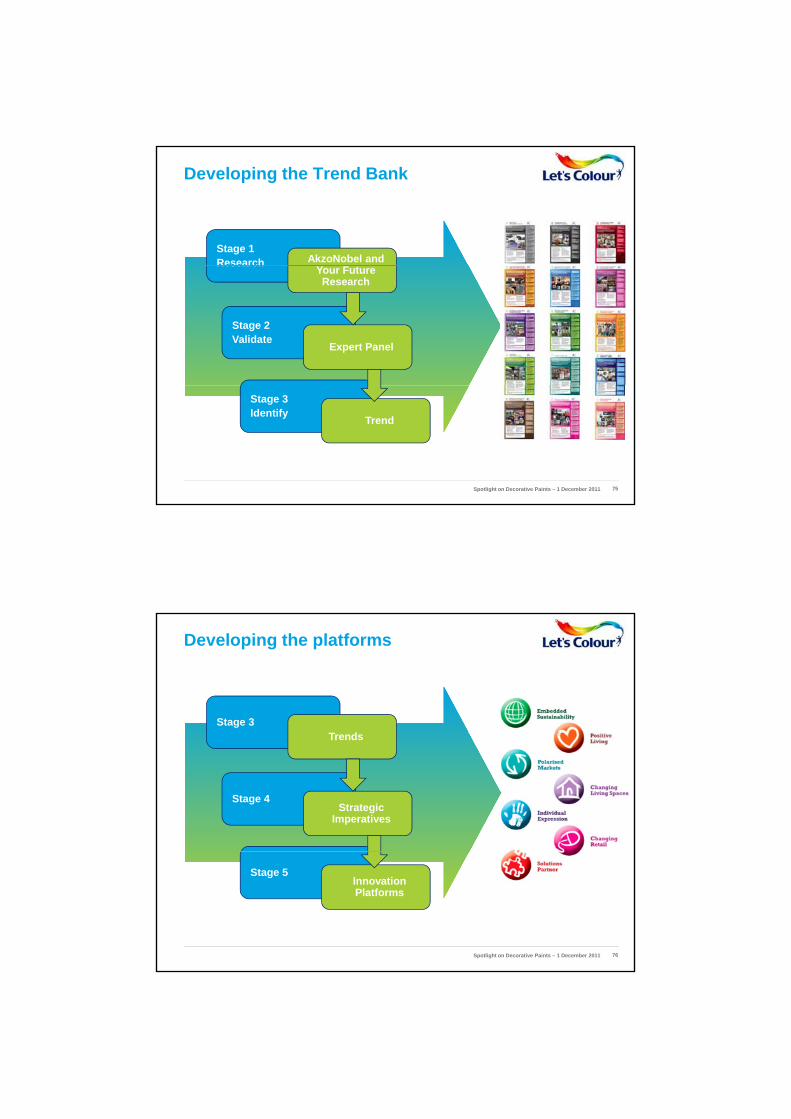

Developing the Trend Bank

Stage 1Research AkzoNobel and Research

Stage 2Validate

Your Future Research

Expert Panel

Stage 3Identify

Trend

Spotlight on Decorative Paints – 1 December 2011 75

Developing the platforms

Stage 3

Stage 4

Trends

Strategic Imperatives

Stage 5Innovation Platforms

Spotlight on Decorative Paints – 1 December 2011 76

Walk around

Three rooms:

1. Inspiring People Globally

2. Leading through Innovation

3. Winning in Professional Markets

Spotlight on Decorative Paints – 1 December 2011 77

Europe, Middle East & AfricaRichard StuckesRichard Stuckes

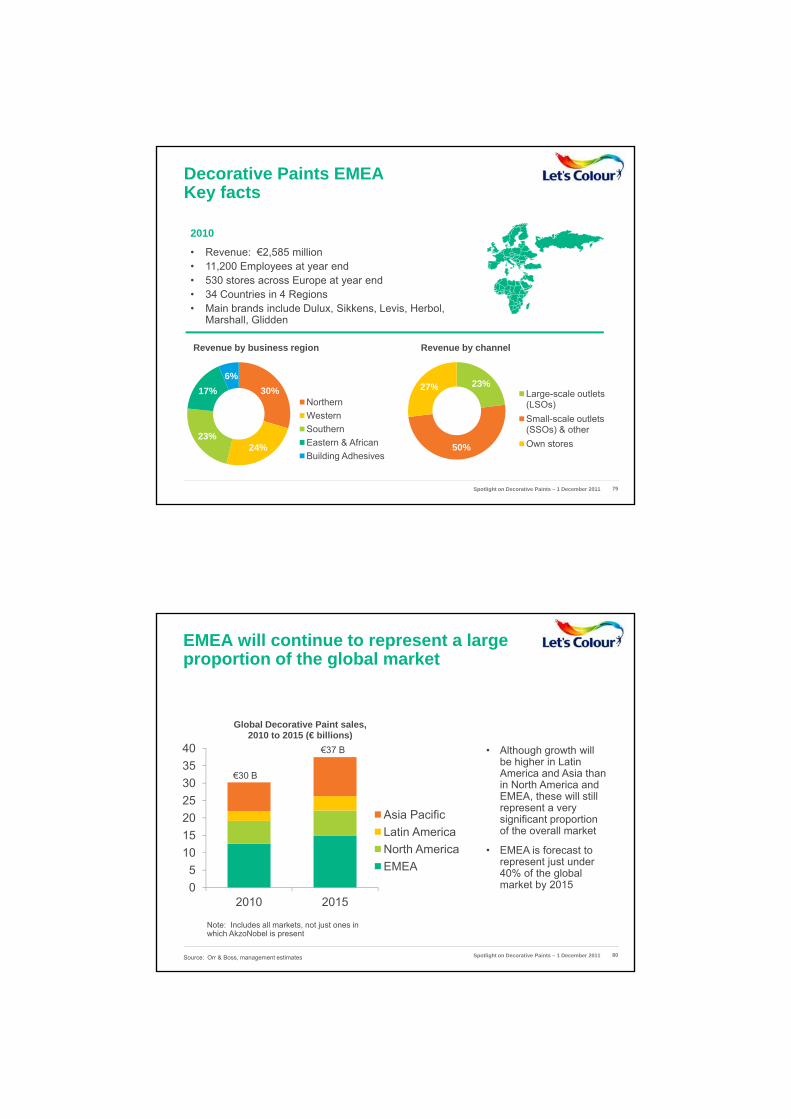

Decorative Paints EMEAKey facts

• Revenue: €2,585 million• 11 200 Employees at year end

2010

Revenue by business region

6%

• 11,200 Employees at year end• 530 stores across Europe at year end• 34 Countries in 4 Regions• Main brands include Dulux, Sikkens, Levis, Herbol,

Marshall, Glidden

Revenue by channel

23%27%30%

24%23%

17%NorthernWesternSouthernEastern & AfricanBuilding Adhesives

23%

50%

27%Large-scale outlets (LSOs)Small-scale outlets (SSOs) & otherOwn stores

Spotlight on Decorative Paints – 1 December 2011 79

EMEA will continue to represent a large proportion of the global market

Global Decorative Paint sales,2010 t 2015 (€ billi )

• Although growth will be higher in Latin America and Asia than in North America and EMEA, these will still represent a very significant proportion of the overall market

• EMEA is forecast to10152025303540

2010 to 2015 (€ billions)

Asia PacificLatin AmericaNorth America

€30 B

€37 B

EMEA is forecast to represent just under 40% of the global market by 20150

510

2010 2015

North AmericaEMEA

Note: Includes all markets, not just ones in which AkzoNobel is present

Source: Orr & Boss, management estimates Spotlight on Decorative Paints – 1 December 2011 80

There is still significant opportunity to grow share in EMEA

AkzoNobel’s Decorative Paints Market in 2010*100% = €12 billion

• Top 4 markets in pEurope represent 46% of the EMEA total

• Western Europe represents 77% of the EMEA total

• Only France and the UK are more than 50% consolidated to the top 3 players

* Markets where AkzoNobel is active. Does not include non-paints sales or integrated distribution

p y

• Opportunities to grow share include organic growth, distribution consolidation and potential opportunistic M&A

Source: Management estimates Spotlight on Decorative Paints – 1 December 2011 81

AkzoNobel have a solid overall leadership position in EMEA

2010 Decorative Paints revenues100% = €12 billion*

AkzoNobel

PPG

DAW

TikkurilaOthers

RMS = 2.4 • AkzoNobel is the largest paint manufacturer in EMEA, at more than double the size of our nearest competitor

• The top 6 competitors still only account for just under 40% of the total market

*Notes: Only includes markets where AkzoNobel is active.Does not include non-paints sales or integrated distribution.

TikkurilaJotun

Materis

total market

Source: Management estimates Spotlight on Decorative Paints – 1 December 2011 82

We hold a range of positions across individual markets

• Belgium• France retail• GreeceMarket leader

• Switzerland• Tunisia• Turkey

• AkzoNobel is the market leader in a number of countries,

• Italy trade• Netherlands

• Poland• Russia

Market leader

Competingvery closely

y• UK

• South Africa• Spain

,together accounting for nearly 40% of our total EMEA market

• Significant growth opportunities in key markets like Turkey, Poland and Russia

• In some markets we are up against strong,

• Germany• Middle East• Scandinavia

Challenger position

p g g,mostly local incumbents like Tikkurila in Russia, DAW (Caparol) in Germany and Jotun in Scandinavia and the Middle East

Spotlight on Decorative Paints – 1 December 2011 83

We are facing significant economic headwinds at the moment

Housing starts(Index 2005 = 100)

• Although construction is not the major driver of

6080

100120140160180200

(Index 2005 100)

BelgiumDenmarkFrancePolandSpain

paint demand, it reflects the broader economic environment including consumer sentiment

• Housing starts in a number of EMEA markets have yet to recover to their peak levels

• Other issues dampening

0204060 Spa

SwedenUK

consumer confidence are uncertainty about the Euro and expected cuts in government spending

Source: OECD Spotlight on Decorative Paints – 1 December 2011 84

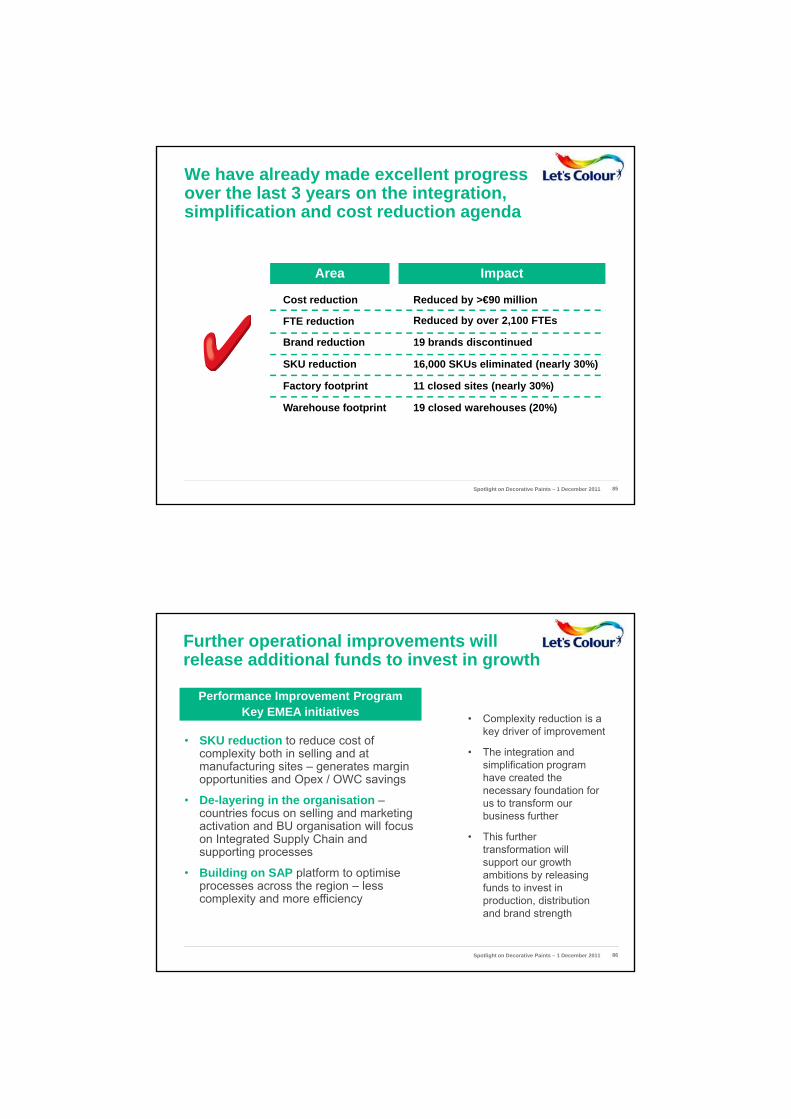

We have already made excellent progress over the last 3 years on the integration, simplification and cost reduction agenda

Cost reduction

FTE reduction

Brand reduction

SKU reduction

Factory footprint

Reduced by >€90 million

Reduced by over 2,100 FTEs

19 brands discontinued

16,000 SKUs eliminated (nearly 30%)

11 closed sites (nearly 30%)

ImpactArea

Factory footprint

Warehouse footprint

11 closed sites (nearly 30%)

19 closed warehouses (20%)

Spotlight on Decorative Paints – 1 December 2011 85

Further operational improvements will release additional funds to invest in growth

Performance Improvement ProgramKey EMEA initiatives • Complexity reduction is a

key driver of improvement• SKU reduction to reduce cost of

complexity both in selling and at manufacturing sites – generates margin opportunities and Opex / OWC savings

• De-layering in the organisation –countries focus on selling and marketing activation and BU organisation will focus on Integrated Supply Chain and supporting processes

key driver of improvement

• The integration and simplification program have created the necessary foundation for us to transform our business further

• This further transformation willsupporting processes

• Building on SAP platform to optimise processes across the region – less complexity and more efficiency

transformation will support our growth ambitions by releasing funds to invest in production, distribution and brand strength

Spotlight on Decorative Paints – 1 December 2011 86

We have world-class assets in EMEA, strengthened by our scale

People• Unparalleled industry depth combined with exciting new

hires that bring us critical category management expertise

Brands• Market leading brands in both the Trade and Retail

segments in several markets• Strong woodcare brands in UK, Scandinavia, Russia• Marketing organization restructured to leverage scale

Distribution infrastructure• 3 mega-sites (UK, Poland and France) to produce the bulk

of our volume at highly competitive rates of efficiency• Opportunity to find distribution synergies across the

AkzoNobel portfolio

Spotlight on Decorative Paints – 1 December 2011 87

A fantastic management team has brought great retail & consumer goods experience

Guy Williams (North)• 8 years in the business• Led UK Stores turnaround in 2005/6• Pre-AN experience at major retailers p j

including Woolworths and Aldi

Peter van Campen (South)• 1 year at AkzoNobel• Brings Category Management and

Kees Ekelmans (West)• New appointment, joining from Hunter

Douglas’ Division Components & Programs• Extensive finance, ops and management

experience from nearly 20 years at Unilever

branded consumer goods expertise from Shell, Heineken and LVMH

Jan-Piet van Kesteren (East)• 18 months in AkzoNobel• Brings emerging markets

marketing expertise from 14 years at Unilever in various international roles

Frank van Buchem (Marketing)• 6 months in AkzoNobel• Brings marketing and GM

experience at Unilever, Coca-Cola and Sara Lee

Spotlight on Decorative Paints – 1 December 2011 88

The phased roll-out of the new Let’s Colour brand identity is already underway

From: To:

• Phased rollout beginning in 2011 with Austria, France and the Netherlands

• Continuing though to Q1 2013

• Combination of modes: Launch, Phased and Hybrid

Spotlight on Decorative Paints – 1 December 2011 89

We continue to implement world-class technology in our mega-factories

Pilawa, 2006

Montataire

Ashington, 2014

Mobile vessels are moved to automatic dosing and mixing stations before progressing to filling

Montataire

A purpose-built, Agile plant in the North East of England making a complex range of products for the North West of Europe• Based on the Universal

Leading-edge technology ensures accuracy and reliability in quality

€4m of investments have nearly doubled the volume of product coming out of this site

Blending Plant design developed in Pilawa

• This £100m plant will represent a step change in technology, improving energy efficiency by 60% and reducing waste by 60%

Spotlight on Decorative Paints – 1 December 2011 90

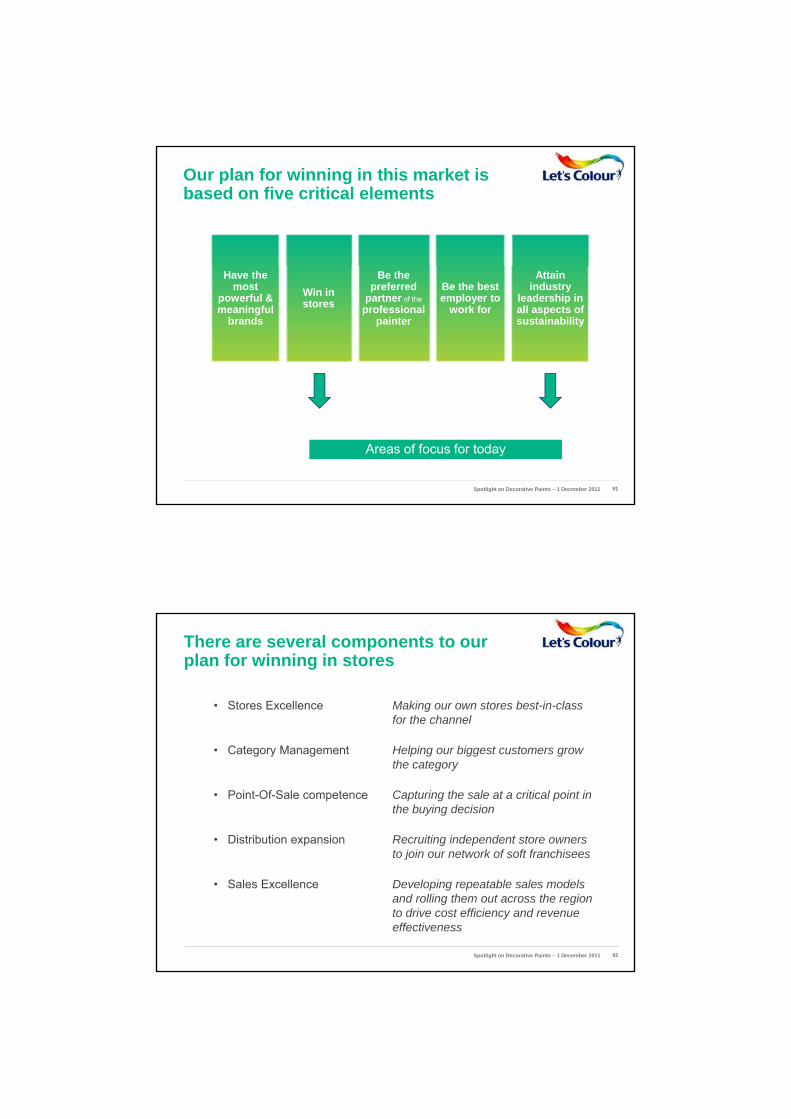

Our plan for winning in this market is based on five critical elements

Have the most

powerful & meaningful

brands

Win in stores

Be the preferred

partner of the professional

painter

Attain industry

leadership in all aspects of sustainability

Be the best employer to

work for

Areas of focus for today

Spotlight on Decorative Paints – 1 December 2011 91

There are several components to our plan for winning in stores

• Stores Excellence Making our own stores best-in-class for the channel

• Category Management Helping our biggest customers grow the category

• Point-Of-Sale competence Capturing the sale at a critical point in the buying decision

• Distribution expansion Recruiting independent store owners to join our network of soft franchiseesto join our network of soft franchisees

• Sales Excellence Developing repeatable sales models and rolling them out across the region to drive cost efficiency and revenue effectiveness

Spotlight on Decorative Paints – 1 December 2011 92

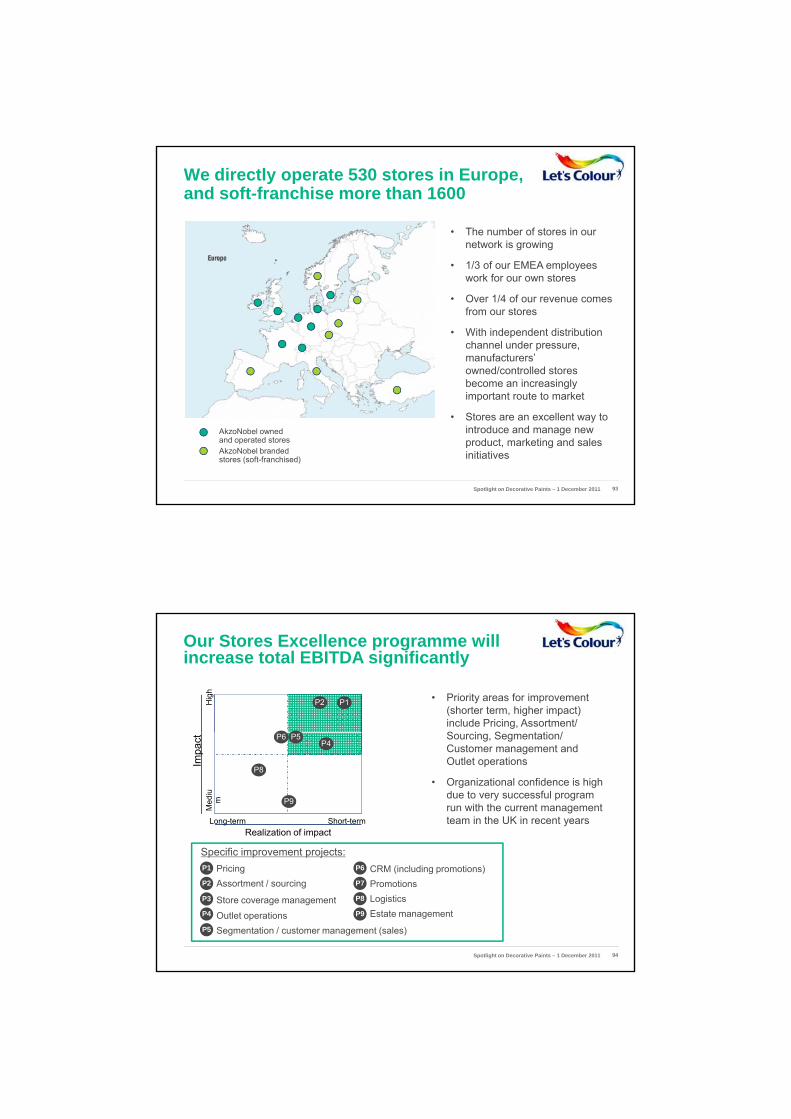

We directly operate 530 stores in Europe, and soft-franchise more than 1600

• The number of stores in our network is growing

• 1/3 of our EMEA employees• 1/3 of our EMEA employees work for our own stores

• Over 1/4 of our revenue comes from our stores

• With independent distribution channel under pressure, manufacturers’ owned/controlled stores become an increasingly

AkzoNobel owned and operated storesAkzoNobel branded stores (soft-franchised)

become an increasingly important route to market

• Stores are an excellent way to introduce and manage new product, marketing and sales initiatives

Spotlight on Decorative Paints – 1 December 2011 93

Our Stores Excellence programme will increase total EBITDA significantly

Hig

h

P1P2 • Priority areas for improvement (shorter term, higher impact)include Pricing, Assortment/ S i S t ti /

Short-term Long-termRealization of impact

Impa

ctM

ediu

m

P5P6P4

P8

P9

Specific improvement projects:

Sourcing, Segmentation/ Customer management and Outlet operations

• Organizational confidence is high due to very successful program run with the current management team in the UK in recent years

P9

Specific improvement projects:P1

P2

P5

P4

P3

P6

P7

P8

Estate managementLogisticsPromotionsCRM (including promotions)

Store coverage managementOutlet operationsSegmentation / customer management (sales)

Assortment / sourcingPricing

Spotlight on Decorative Paints – 1 December 2011 94

Turkey is a great growth platform for our business

• Total market size in 2010 of about €500m• Growing at approximately 2x GDP growthMarket

• Distribution to SSO via Wholesale is around 75% of the market• Other channels are LSOs and construction• SSOs are a competitive place without exclusivity• Mainly ready-mix paint, limited color variety

Distribution

• Extremely competitive: 5 players have between 10 and 25% share • Mainly ‘Buy-It-Yourself’

Market

• AkzoNobel operates with a single brand: Marshall• Marshall is the oldest and most well known paint brand• We are the market leader• Largely local supply chain, operated from Gebze (80 km from Istanbul)

AkzoNobel presence

Spotlight on Decorative Paints – 1 December 2011 95

We are pursuing an aggressive roll-out strategy with 1,000 stores in 2011 including in-store tinting equipment

From a fragmentedand messy look

To a revolutionary, exclusive store

Spotlight on Decorative Paints – 1 December 2011 96

Proven results will drive our momentum for further expansion through 2012

YTD Revenue uplift is significant, up to 50% whilst tinting sales in

Continuous upgrades of our concept provide even more strength

store increased by 500%

30

50

44

25

Realized %Target %

10

15

Corner StoresStore in StoresPerfect Stores

Spotlight on Decorative Paints – 1 December 2011 97

Operating sustainability across all aspects of our business is critically important to us

• Is the right thing to do, and protects the long-term health of the business

• Additional short-term benefits include:

• Top-line growth: revenue from our eco-premium products represent 22% of total sales and outgrew the market by a factor of 3

• Reduced costs: we have already reduced our energy use per tonne of production by 9% in two years, and by 4% in absolute terms

• Improved margins: eco-premiumImproved margins: eco premium R&D helps drive innovations

• Employee engagement:Employees have identified and pursued literally hundreds of small-scale improvement projects in every area of the business – these add up to big impact

Our ‘5 Pillar’ approach to Sustainability

Combines economic, environmental and social sustainability

Spotlight on Decorative Paints – 1 December 2011 98

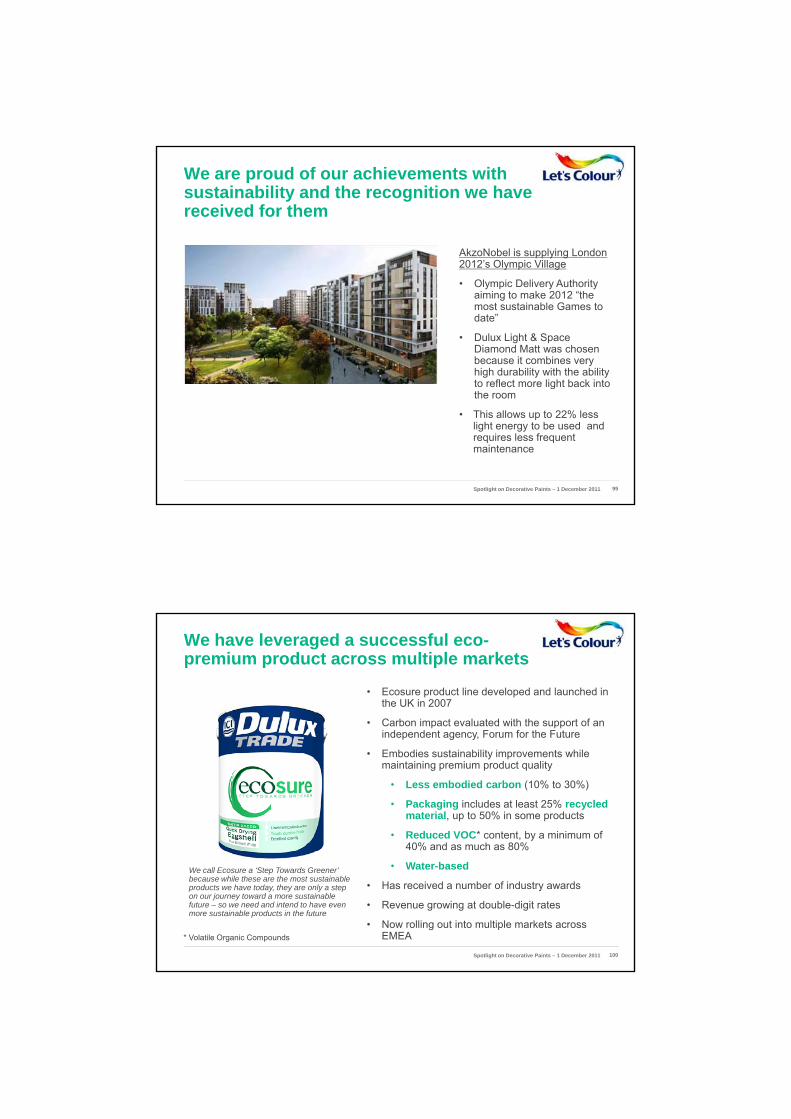

We are proud of our achievements with sustainability and the recognition we have received for them

AkzoNobel is supplying London 2012’s Olympic Village2012 s Olympic Village

• Olympic Delivery Authority aiming to make 2012 “the most sustainable Games to date”

• Dulux Light & Space Diamond Matt was chosen because it combines very high durability with the ability to reflect more light back intoto reflect more light back into the room

• This allows up to 22% less light energy to be used and requires less frequent maintenance

Spotlight on Decorative Paints – 1 December 2011 99

We have leveraged a successful eco-premium product across multiple markets

• Ecosure product line developed and launched in the UK in 2007

• Carbon impact evaluated with the support of an independent agency Forum for the Futureindependent agency, Forum for the Future

• Embodies sustainability improvements while maintaining premium product quality

• Less embodied carbon (10% to 30%)

• Packaging includes at least 25% recycled material, up to 50% in some products

• Reduced VOC* content, by a minimum of 40% and as much as 80%

• Water-based

• Has received a number of industry awards

• Revenue growing at double-digit rates

• Now rolling out into multiple markets across EMEA

We call Ecosure a ‘Step Towards Greener’ because while these are the most sustainable products we have today, they are only a step on our journey toward a more sustainable future – so we need and intend to have even more sustainable products in the future

* Volatile Organic Compounds

Spotlight on Decorative Paints – 1 December 2011 100

In Summary

• EMEA is the heartland of our business and will continue to be so• We will continue to pursue significant growth opportunities:

h i i t k t d b t ti l th i E tshare gain in mature markets and substantial growth in Eastern Europe, Turkey and Africa

• Tough trading conditions will generate opportunities to drive consolidation in the market

• We have everything we need to win here: the scale, the assets, the experience and the determination

• We will not only weather the storm of current market conditions – we will emerge stronger than many of our competitors

• We can do this while still protecting the best of our experience and our heritage in local markets

Spotlight on Decorative Paints – 1 December 2011 101

North AmericaBob TaylorBob Taylor

Decorative Paints North AmericaKey Facts

• Revenue: €1,029 million• 5,100 employees at year-end

13 f t i / di t ib ti f iliti

2010

• 13 manufacturing / distribution facilities• 550+ company-owned stores• 5,000 independent dealers

24%8%5%

Revenue* by business lineRevenue* by geography

24%

35%5%

11%

17%Home DepotCompany Owned StoresCaribbeanWalmartDiversified Brands - CanadaDiversified Brands - US

62%

33%

USACanadaCaribbean**

• Charts are based on 2011 Estimates** Including Puerto Rico. Charts are based on 2011 Estimates

Spotlight on Decorative Paints – 1 December 2011 103

Executive Summary

• Relentless Focus:

− Drive profitable growth with an intense focus on margin, cost and innovation

• How:− New management team with clear priorities− Margin management – price, procurement, formulations− Capitalize on robust innovation pipeline− Drive cost synergies across North America− Invest in portfolio of strong brands− Leverage cross channel presence− Continue delivering solid Canadian performance

• Build upon strong customer relationships & retail partnerships

• A culture change underpinned by AkzoNobel’s core values

Spotlight on Decorative Paints – 1 December 2011 104

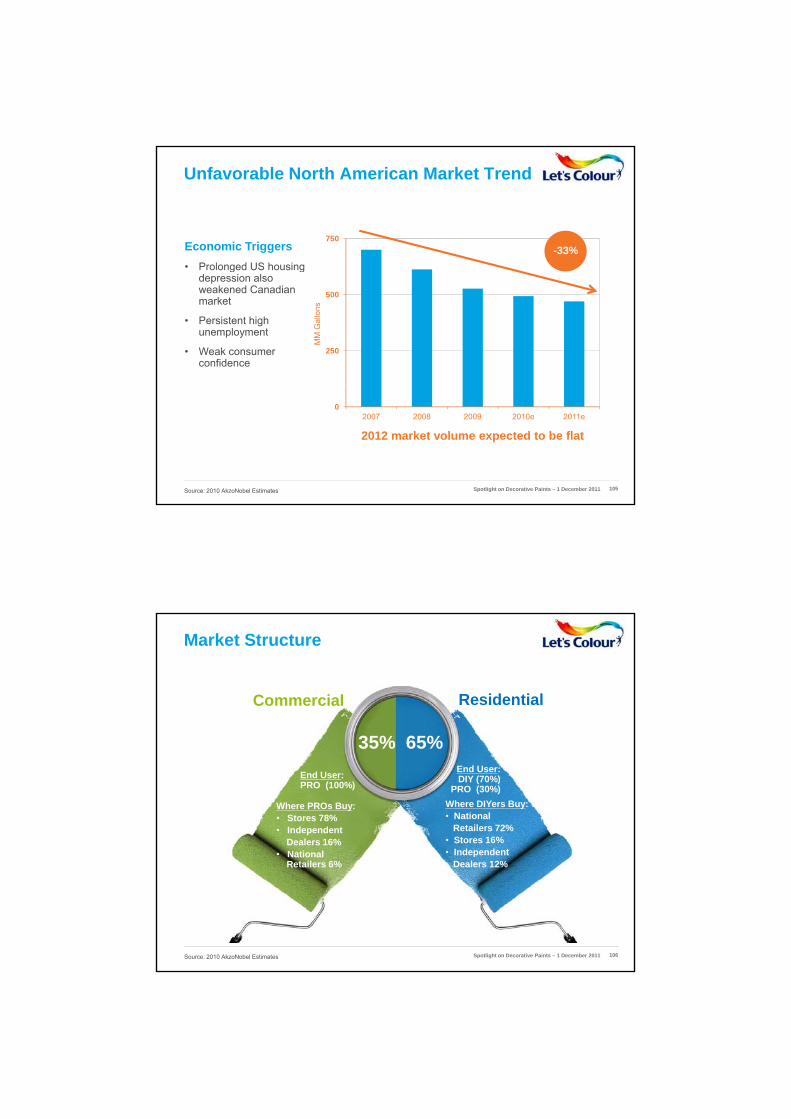

Unfavorable North American Market Trend

Economic Triggers• Prolonged US housing

750-33%

• Prolonged US housing depression also weakened Canadian market

• Persistent high unemployment

• Weak consumer confidence

250

500

MM

Gal

lons

Source: 2010 AkzoNobel Estimates

02007 2008 2009 2010e 2011e

2012 market volume expected to be flat

Spotlight on Decorative Paints – 1 December 2011 105

Market Structure

ResidentialCommercial

35% 65%

Where PROs Buy:• Stores 78%• Independent

Dealers 16%N ti l

End User: PRO (100%)

End User: DIY (70%)

PRO (30%)Where DIYers Buy: • National

Retailers 72%• Stores 16%• Independent• National

Retailers 6%

Source: 2010 AkzoNobel Estimates

• Independent Dealers 12%

•

Spotlight on Decorative Paints – 1 December 2011 106

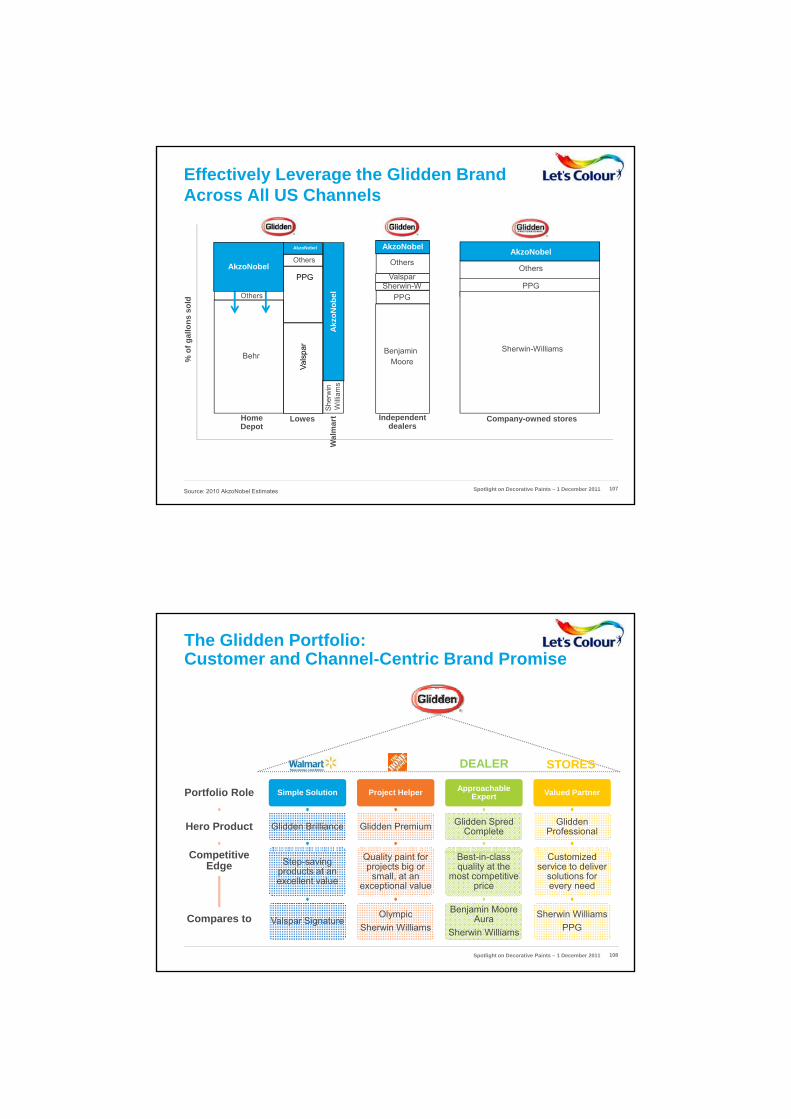

Effectively Leverage the Glidden Brand Across All US Channels

Others

AkzoNobel

Oth

AkzoNobelOthers

AkzoNobel

AkzoNobel

SWPPG

BenjaminMoore

Valspar

BenjaminMoore

Others

PPG

Sherwin-Williams

PPG

Sherwin-WilliamsBehr

PPG

Vals

par

Behr

n sAk

zoN

obel

Sherwin-W

% o

f gal

lons

sol

d Others

AkzoNobel

Independent dealers

Company-owned stores

Sher

win

Willi

ams

Home Depot

Lowes

Wal

mar

t

Source: 2010 AkzoNobel Estimates Spotlight on Decorative Paints – 1 December 2011 107

The Glidden Portfolio:Customer and Channel-Centric Brand Promise

Portfolio Role

Hero Product

C titi

Simple Solution

Glidden Brilliance

Project Helper

Glidden Premium

Approachable Expert

Glidden SpredComplete

Valued Partner

Glidden Professional

DEALER STORES

Competitive Edge

Compares to

Step-saving products at an excellent value

Valspar Signature

Quality paint for projects big or

small, at an exceptional value

OlympicSherwin Williams

Best-in-class quality at the

most competitive price

Benjamin Moore Aura

Sherwin Williams

Customized service to deliver

solutions for every need

Sherwin WilliamsPPG

Spotlight on Decorative Paints – 1 December 2011 108

Relative Market Position - Canada

obel

Others

% o

f gal

lons

sol

d

AkzoNobel

Home Hardware

BenjaminMoore

BenjaminMoore

OthersPPG

Sherwin Williams

AkzoNobel

Behr

Oth

Akzo

Nob

el

General Paint

Cloverdale

Akzo

Nob

el

Akzo

Nob

el

Akzo

No

Independent dealers

MooreMoore

Company-owned stores

General PaintOthers

Masco

Home Depot

Rona

Wal

mar

t

Source: 2010 AkzoNobel Estimates

Can

adia

n Ti

re

Spotlight on Decorative Paints – 1 December 2011 109

Our Journey To Date

Rebuild brand

2008-2011

position

Spotlight on Decorative Paints – 1 December 2011 110

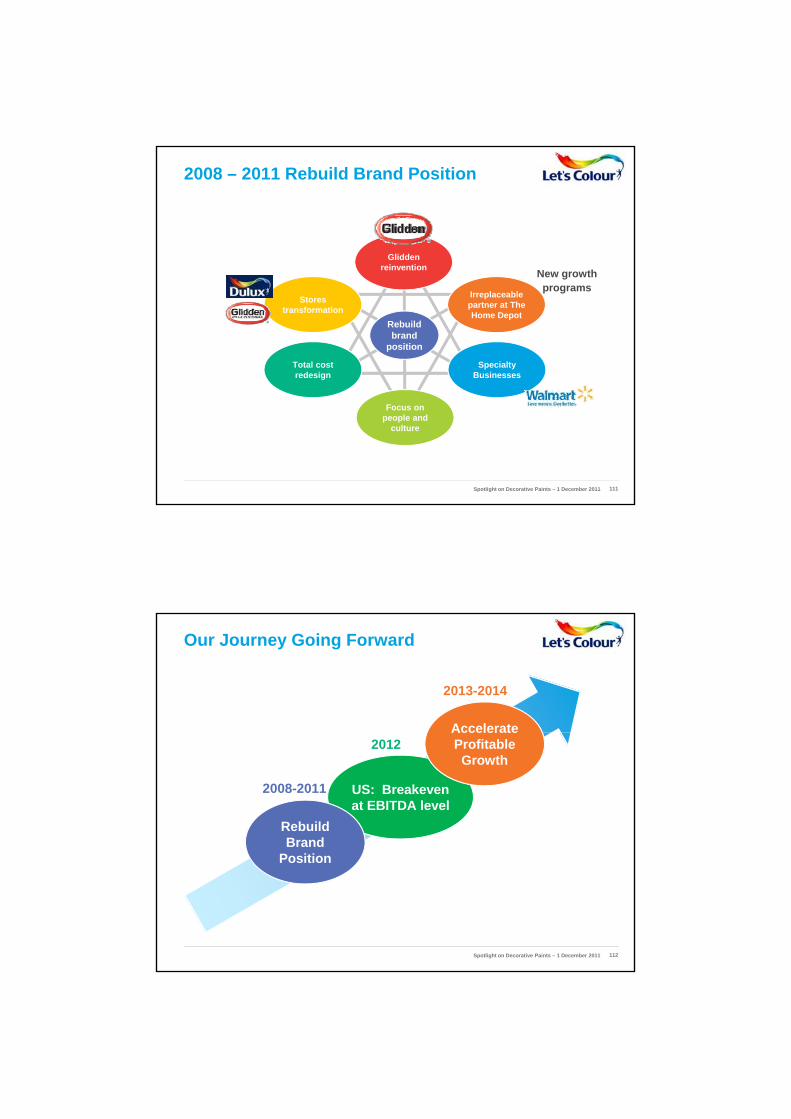

2008 – 2011 Rebuild Brand Position

Glidden reinventionreinvention

Irreplaceable partner at The Home Depot

Specialty Businesses

Stores transformation

Total cost redesign

Rebuild brand

position

New growthprograms

Focus on people and

culture

Spotlight on Decorative Paints – 1 December 2011 111

Our Journey Going Forward

Accelerate

2013-2014

US: Breakeven at EBITDA level

Rebuild Brand

Accelerate Profitable Growth

2008-2011

2012

Position

Spotlight on Decorative Paints – 1 December 2011 112

2012 – 2014 Strategy:Leverage Scale & Scope to Accelerate Profitable Growth

Changeculture

• Clear priorities & accountability

• Sense of urgency

• New management team

Protect investment

in our brands and

innovate

Drive growth

• New growth programs at The Home Depot

• Target core Walmart shopper

• Expand retail partner base• Drive PRO strategy• Expand Dulux stores in

Improve margin

• Aggressive margin management

• Improve mix• Commercialize new

products

team

• Expand Dulux stores in Canada

• Drive Caribbean growth

Reduce cost base

• Deliver supply chain & back office efficiencies

• Reduce product complexity

• Improve processes and systems productivity

• Drive North American synergies

Spotlight on Decorative Paints – 1 December 2011 113

Solution:

A collection of new Glidden programs that simplify painting for

Provide The Home Depot with industry-leading innovation

programs that simplify painting for the DIY & PRO end user

Color Palette

Spotlight on Decorative Paints – 1 December 2011 114

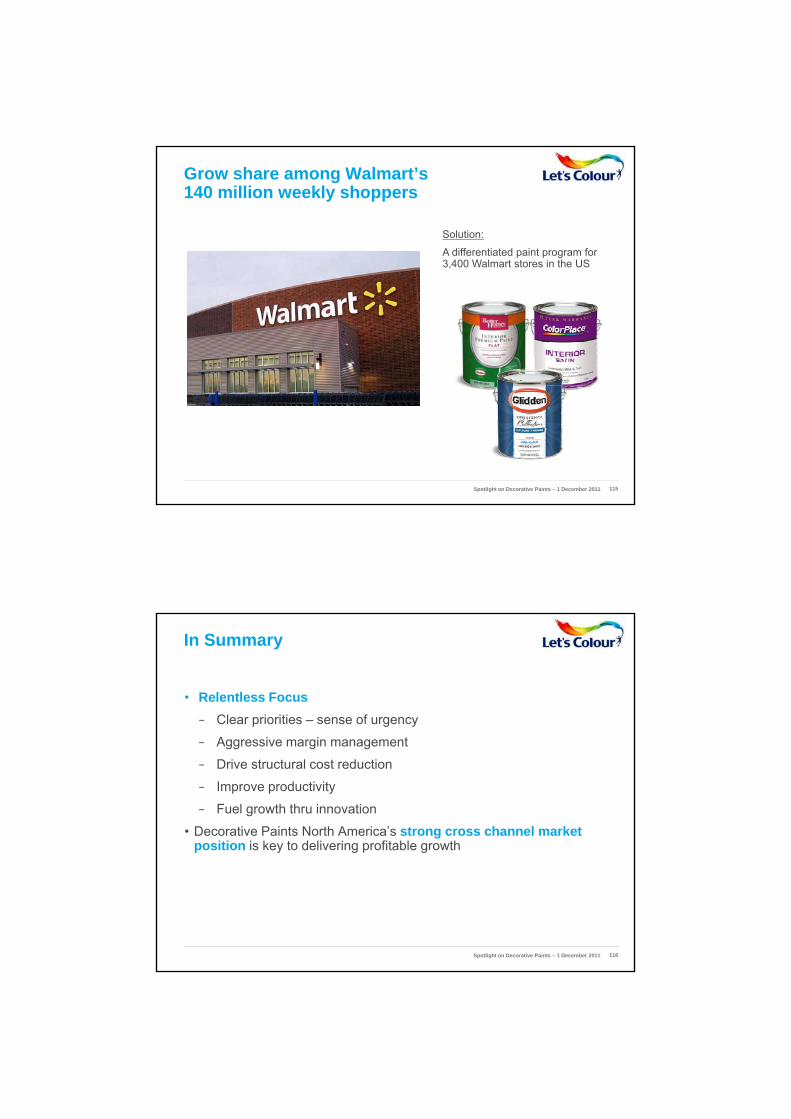

Solution:

A differentiated paint program for 3 400 Walmart stores in the US

Grow share among Walmart’s 140 million weekly shoppers

3,400 Walmart stores in the US

Spotlight on Decorative Paints – 1 December 2011 115

In Summary

• Relentless Focus− Clear priorities – sense of urgency

− Aggressive margin management

− Drive structural cost reduction

− Improve productivity

− Fuel growth thru innovation

• Decorative Paints North America’s strong cross channel market position is key to delivering profitable growthp y g p g

Spotlight on Decorative Paints – 1 December 2011 116

Spotlight on Decorative Paints – 1 December 2011 117

Q&A:Keith NicholsKeith NicholsTex GunningRichard StuckesBob Taylor

South East Asia & PacificJeremy RoweJeremy Rowe

Decorative Paints South East Asia & Pacific – Key Facts

• Revenue: €279 million• 1,400 Employees at year end

7 f t i it d 15 000 t il i t d

2010

Revenue by BrandRevenue By Country

• 7 manufacturing sites and 15,000 retail points served• #1 or #2 in every market served and #1 overall• High profitability• A Dulux business• JV’s in Indonesia with PT DWI Satrya Utama (AN share 55%) and in Malaysia with

Amanah Raya Berhad/Skim Amnanah Saham Bumiputra (AN share 60%)

10% I d i

70%

30%

DuluxNon-Dulux

30%

25%20%

15%

10% IndonesiaVietnamMalaysiaThailandOthers

Spotlight on Decorative Paints – 1 December 2011 120

A large, growing region

• Over 600m people, growing at around 1% per annumaround 1% per annum

• Almost 30% of the population <14 years old

• Historic GDP growth of 7-8% likely to continue in the medium-term

• Wide range of incomes, with GDP/Capita ranging from US$800 to US$43

Spotlight on Decorative Paints – 1 December 2011 121

A dynamic, colourful region

• A dynamic, fast developing iregion

• Where colour is ingrained in the spirit of many diverse cultures

• With a short painting cycle of 3-5 years due to factors including the climate andincluding the climate and the importance of home renewal for festive events

Spotlight on Decorative Paints – 1 December 2011 122

A large and profitable paints market

Market Value By Category

15% • A market of around 1 billion litres and €1.5 billion value

Market Value By Country

6%

40%

30%

15%InteriorExteriorTrimOthers

• 70%+ of the market in Decorative Paints

• Relatively low consumption of ~ 1.7 litres/capita and pricing of ~ €1.50/litre

• High proportion of exteriors due to habits and climate

28%

20%16%

17%

13%6%

IndonesiaThailandMalaysiaPhilippinesVietnamSingapore & Others

• Five countries represent more than 90% of the region

• A profitable market

Spotlight on Decorative Paints – 1 December 2011 123

A market that is expected to grow in the medium term

10%• More urban households

6%

• A move from non-permanent to permanent, and unpainted to painted houses

• Increased percentage of disposable income spent on decoration

• Continued development and infrastructure investment

Inflation & price gro th

Volume Value

Expected Market Growth2010 – 2015 CAGR

• Inflation & price growth

• Highest growth in the mass market

• Growth spread across Tier 1, 2 & 3 cities

Spotlight on Decorative Paints – 1 December 2011 124

But challenged in the shorter-term

• Flood situation in Thailand will take 6 th t6 months or more to recover

• Political instability remains a feature of the region, but is improving

• Vietnam’s recovery from economic overheating will reduce growth prospects in 2012prospects in 2012

• Continued raw material price inflation

• Indonesia is best placed to weather any global recession

Spotlight on Decorative Paints – 1 December 2011 125

A consumer-driven, colour-loving but fragmented market

Market Value By Channel

21%

• A market of mostly “Buy It Yourself” (BIY) and “Have It Done” (HID) consumers

Consumer By Type

49%

19%

11%

TraditionalWholesaleModern RetailProjects & Others

( )

• High use of colour

• >55% on residential repainting

• A highly fragmented, mostly traditional channel

• In-store tinting established and growing strongly

60%

40%

BIY & HID (Use a Painter)DIY

• Modern retail only growing slowly

Spotlight on Decorative Paints – 1 December 2011 126

A market where AkzoNobel is the leader

Estimated Value Market Size and ShareTop 6 markets in South East Asia

100%

Th Th Th

28%

18%12%

42%AkzoNobelNippon PaintsTOAAll Others20

40

60

80

#1 #2 Joint#1 #1

Joint#1

#2Player

#1Player

Joint#1 #1

Player

#2Player Joint

#1

The Rest

The Rest

The Rest

The Rest

The Rest

The Rest

0Indonesia Thailand Malaysia Philippines Vietnam

Singapore

# #1

AkzoNobel

AkzoNobel also has #1 position in Brunei, Joint #1 in Papua New Guinea, and #3 in Cambodia

Spotlight on Decorative Paints – 1 December 2011 127

Leadership built on the Dulux brand

• 70% of business behind Dulux

• A well-known and highly regarded brand in terms of:- Leading- Premium- Quality

• Especially strong in- Premium segmentPremium segment- Exteriors market

• Well-know Dulux propositions such as Dulux Weathershield, the leading brand for exteriors in the region

Spotlight on Decorative Paints – 1 December 2011 128

Our winning objectives

• Ensure volume and revenue growth > 10%> 10% per annum

• Build to a Relative Market Share of 2.5x to the nearest competitor

• Continued superior profitability from brand, scale, mix and global leverageleverage

• Strong ROIC

Spotlight on Decorative Paints – 1 December 2011 129

Investment centered around the brand and winning the consumer

Mass Market Penetration Embedded Sustainability

Product Offer & Portfolio

Deep Distribution

Brand Visibility

Advertising

Partners & Advocates

One-on-One Interaction

Activation

Colour Delivery

Deep Distribution

Society

Partners & Advocates

Investment

Spotlight on Decorative Paints – 1 December 2011 130

A renewed and focused product offerand portfolio

• Focused product portfolio aligned toportfolio aligned to consumer needs

• Renewed livery across the range

• Regular innovation and renovation

• Simplification and harmonisation of product, positioning and execution

Spotlight on Decorative Paints – 1 December 2011 131

A dramatic and successful entry into the mass market

• Mass market shaped historically by competitorscompetitors

• Benchmarking to find the right price and positioning for entry

• Invest in product quality at the right price

• Leverage the Dulux brand

• “Beauty that lasts” and “easy choice” for consumers

• Dramatic success in Indonesia and Thailand to date

Spotlight on Decorative Paints – 1 December 2011 132

Embedded sustainability in all of our major products

• Low-Odour Low VOC implemented across the productimplemented across the product range and underpinned by the Singapore Green Label Standard

• Weathershield Keep Cool for exteriors

• Dulux Pure air-purifying concept for interiorsfor interiors

• Water-based versions of trim and woodcare products

• Eco-premium % well above 30%

Spotlight on Decorative Paints – 1 December 2011 133

Supported by locally-relevant and specific advertising and activation

• Increased brand investment levels towards 10% oflevels towards 10% of revenue

• Brand campaigns based on global position within a local context

• Deep local activations paround festive painting occasions

Spotlight on Decorative Paints – 1 December 2011 134

Including significant one-on-one consumer interaction

• One-on-one colour design and cons lting ser ices inand consulting services in many markets provide individualised brand experiences

• Rolled-out at scale, visiting and producing consultations for tens of thousands of consumer perthousands of consumer per year with high conversion rates

• Measurable brand and sales impact

Spotlight on Decorative Paints – 1 December 2011 135

LiveryOutdoor Shops

Brand visibility across all touch points

Shops

TintingMachines

Events

TVClubs

Collaterals

Machines

Web Sites Facebook

Clothes

Design CentresSpotlight on Decorative Paints – 1 December 2011 136

Increasing distribution depth and capability

• Increasing numeric and weighted distrib tion be ond o r c rrentdistribution beyond our current 15,000 end points

• Engaging professional distribution partners for large geographies –increasing numeric reach by 15% and weighted reach by 10%

• Improvements see in market shareImprovements see in market share, customer service, distributor stock, range completion, and overdues

• Creating enhanced in-store experiences

Spotlight on Decorative Paints – 1 December 2011 137

Deep delivery of colour through theDiscovery low-cost tinting machine

• Superior colour marketing, le eraging global capabilitiesleveraging global capabilities such as ColourFutures

• Conversion to tinting for colourdelivery, Already over 5,000 tinting machines in place across the region

• The Discovery tinting machine isThe Discovery tinting machine is an important enabler of deep rural penetration into small shops

Spotlight on Decorative Paints – 1 December 2011 138

Building professional partners & brand advocates

• Continued investment in:

- Painters

- Architects

- Professional Specifiers

- Interior Designers

- Developers

Spotlight on Decorative Paints – 1 December 2011 139

And taking the brand into society

Spotlight on Decorative Paints – 1 December 2011 140

An engaged, creative, local team supported by global capabilities

Spotlight on Decorative Paints – 1 December 2011 141

In summary

• The South East Asian and Pacific markets are attractive and offer significant growth potentialsignificant growth potential

• We are the leading Decorative Paints company in the region, with a #1 position in key markets such as Indonesia and Vietnam

• We are re-launching and further developing the Dulux brand to secure long-term leadership for AkzoNobel

• This is an integrated investment program covering our brands, capabilities and people and leveraging on global capabilities for

i i dcompetitive advantage

Spotlight on Decorative Paints – 1 December 2011 142

India & South AsiaAmit JainAmit Jain

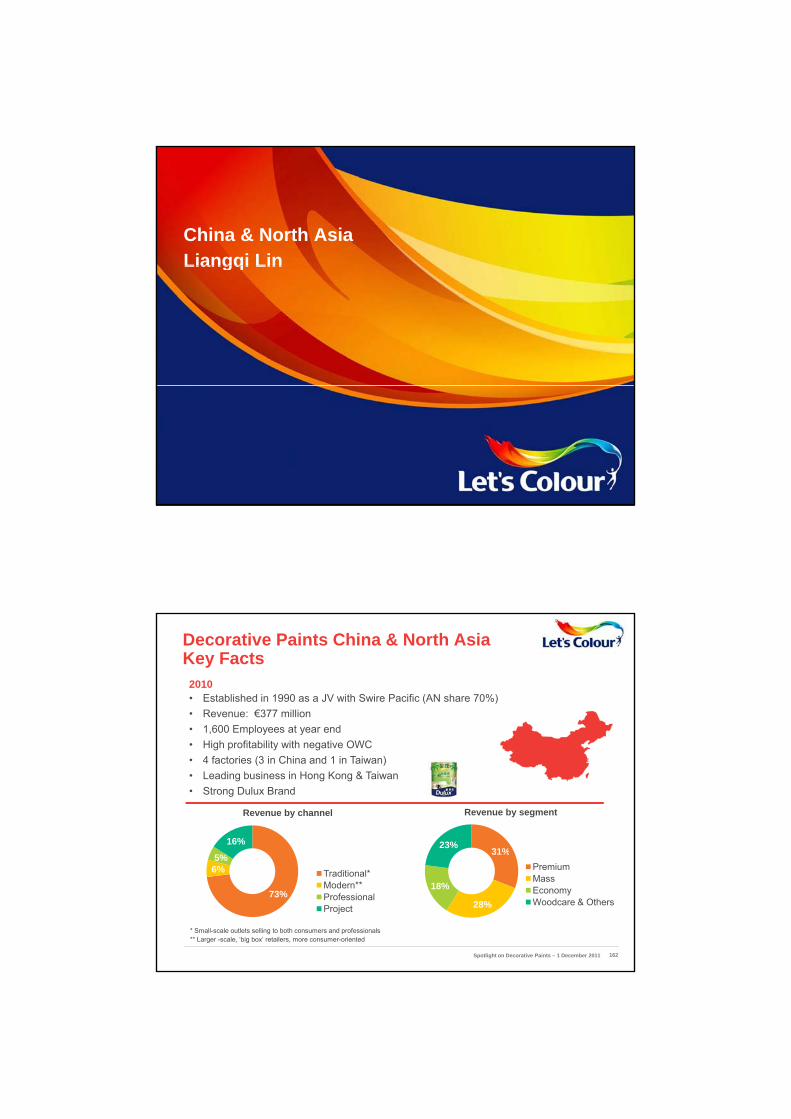

Decorative Paints India & South AsiaKey facts

• Revenue: €185 million• 900 Employees at year end• Production Units : 3

2010

16%

Revenue by price tier

• 75 warehouses servicing 7500 retailers nationwide • Strong position in premium segment• Undisputed market leader in Sri Lanka• Main brands Dulux and ICI Paints• India : Publicly listed, AN holding 56.4%, 3 Business Units (Decorative Paints largest)

16%

Revenue by country

62%22%

PremiumMassEconomy

84%

Sri Lanka

India

Spotlight on Decorative Paints – 1 December 2011 144

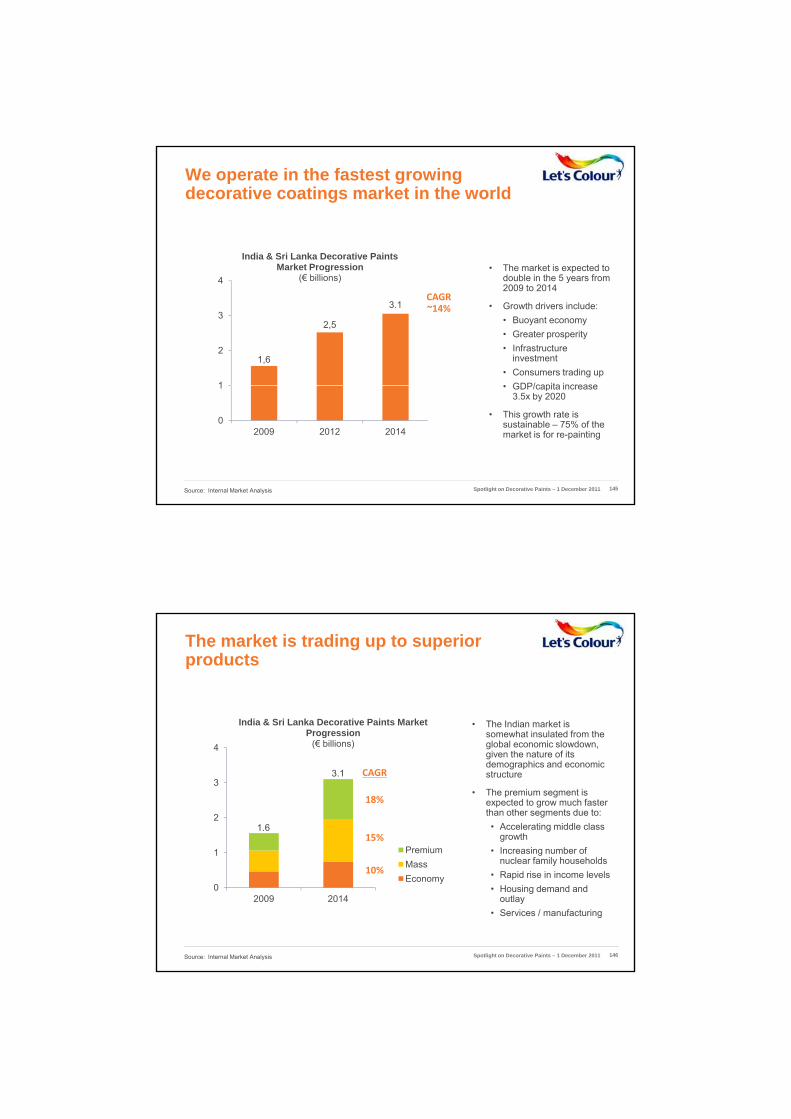

We operate in the fastest growing decorative coatings market in the world

India & Sri Lanka Decorative Paints Market Progression Th k t i t d t

1,6

2,5

3.1

1

2

3

4Market Progression

(€ billions)• The market is expected to

double in the 5 years from 2009 to 2014

• Growth drivers include:• Buoyant economy• Greater prosperity• Infrastructure

investment• Consumers trading up• GDP/capita increase

CAGR ~14%

0

1

2009 2012 2014

• GDP/capita increase 3.5x by 2020

• This growth rate is sustainable – 75% of the market is for re-painting

Source: Internal Market Analysis Spotlight on Decorative Paints – 1 December 2011 145

The market is trading up to superior products

India & Sri Lanka Decorative Paints Market Progression

• The Indian market is some hat ins lated from the

1

2

3

4Progression

(€ billions)

Premium

somewhat insulated from the global economic slowdown, given the nature of its demographics and economic structure

• The premium segment is expected to grow much faster than other segments due to:• Accelerating middle class

growth• Increasing number of

18%

15%

CAGR

1.6

3.1

0

1

2009 2014

PremiumMassEconomy

Increasing number of nuclear family households

• Rapid rise in income levels• Housing demand and

outlay• Services / manufacturing

10%

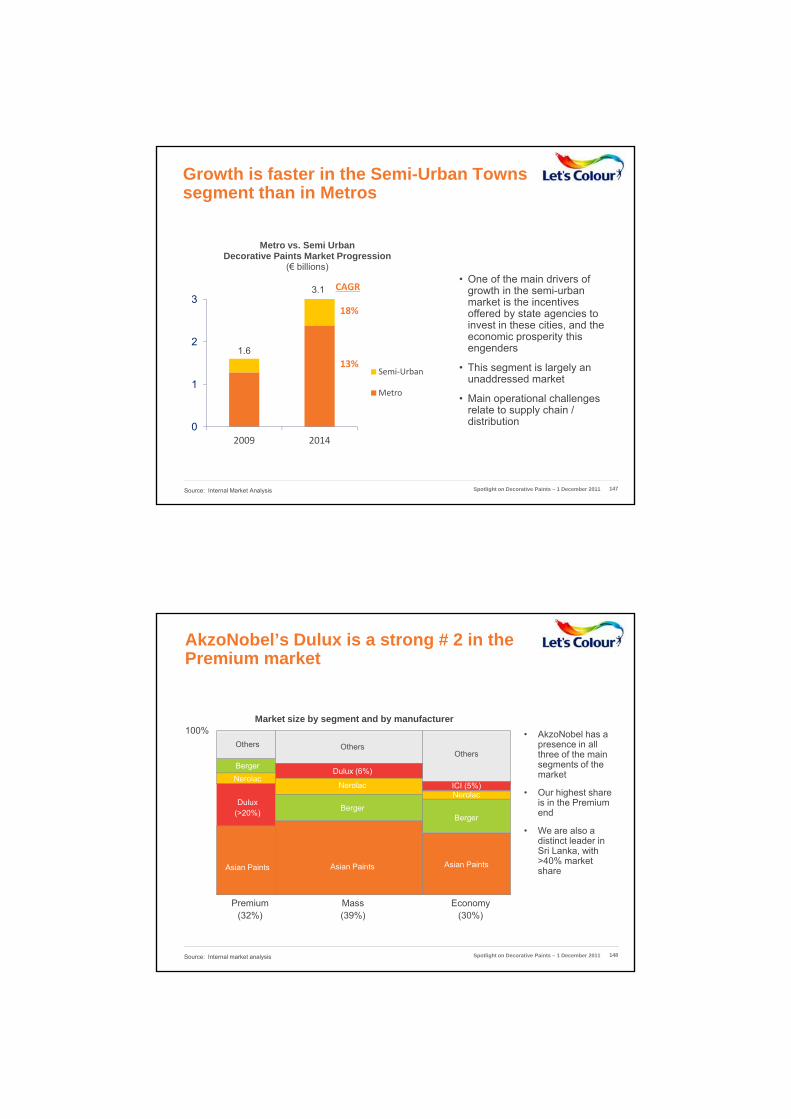

Source: Internal Market Analysis Spotlight on Decorative Paints – 1 December 2011 146

Metro vs. Semi UrbanDecorative Paints Market Progression

(€ billions)

Growth is faster in the Semi-Urban Towns segment than in Metros

• One of the main drivers of growth in the semi-urban market is the incentives offered by state agencies to invest in these cities, and the economic prosperity this engenders

• This segment is largely an unaddressed market1

2

3

(€ billions)

Semi‐Urban

18%

CAGR

13%1.6

3.1

• Main operational challenges relate to supply chain / distribution0

1

2009 2014

Metro

Source: Internal Market Analysis Spotlight on Decorative Paints – 1 December 2011 147

100%Market size by segment and by manufacturer

AkzoNobel’s Dulux is a strong # 2 in the Premium market

Ak N b l h100%

Dulux(>20%)

ICI (5%)

Dulux (6%)

BergerBerger

Others OthersOthers

NerolacNerolac

NerolacBerger

• AkzoNobel has a presence in all three of the main segments of the market

• Our highest share is in the Premium end

• We are also a distinct leader in Sri Lanka with

Economy(30%)

Mass(39%)

Premium(32%)

Asian Paints Asian Paints Asian Paints

Source: Internal market analysis

Sri Lanka, with >40% market share

Spotlight on Decorative Paints – 1 December 2011 148

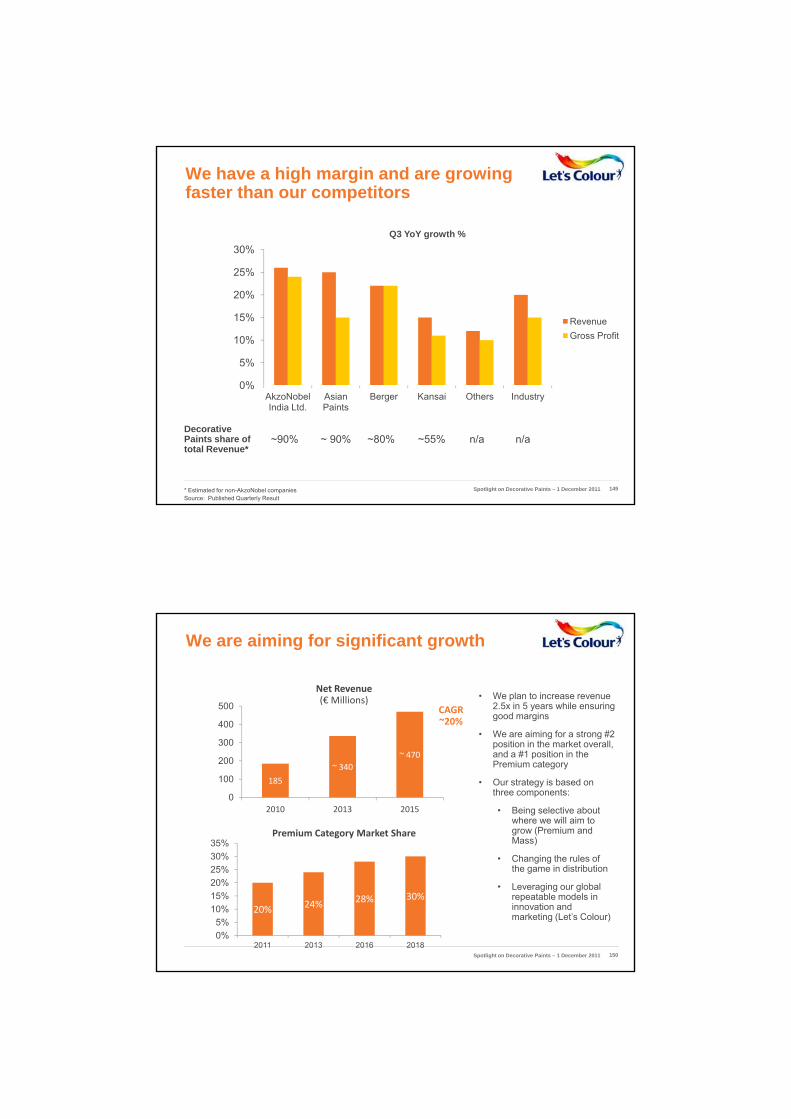

We have a high margin and are growing faster than our competitors

30%Q3 YoY growth %

0%

5%

10%

15%

20%

25%

RevenueGross Profit

* Estimated for non-AkzoNobel companiesSource: Published Quarterly Result

0%AkzoNobel India Ltd.

Asian Paints

Berger Kansai Others Industry

Decorative Paints share of total Revenue*

~90% ~ 90% ~80% ~55% n/a n/a

Spotlight on Decorative Paints – 1 December 2011 149

We are aiming for significant growth