1 Understanding IDEA and MOE The basics of maintenance of effort.

description

Special Education Maintenance of Effort

(MOE)

Objectives

Participants will learn:• What is MOE?• What are the parts of MOE?• How is MOE calculated?• What might count as exceptions?• What do we do if we get a letter from TEA?• How do we avoid the problem?

Definitions and Reports

MOE — What Is It?

“Except as provided in §§300.204 and 300.205, funds provided to an LEA under Part B of the Act must not be used to reduce the level of expenditures for the education of children with disabilities made by the LEA from local funds below the level of those expenditures for the preceding fiscal year.”

[ 34 CFR §300.203 (a) ]

MOE — What Is It?

• LEAs must spend . . . at least the same total or per capita amount from either of the following sources as the LEA spent for that purpose from the same source for the most recent prior year for which information is available:– Local funds only– The combination of State and local funds

[ § 300.203 (b) (1) ]

• Note: In Texas, local and state funds are all in Fund 199.

What Are Direct Services?

• TAC 89.1125 defines allowable expenditures

• 85% includes all allowable expenditures

• State special education funds may only be used for – Personnel, special materials, supplies and equipment– Directly related to the development and implementation

of the IEPs – Not ordinarily purchased for the regular classroom

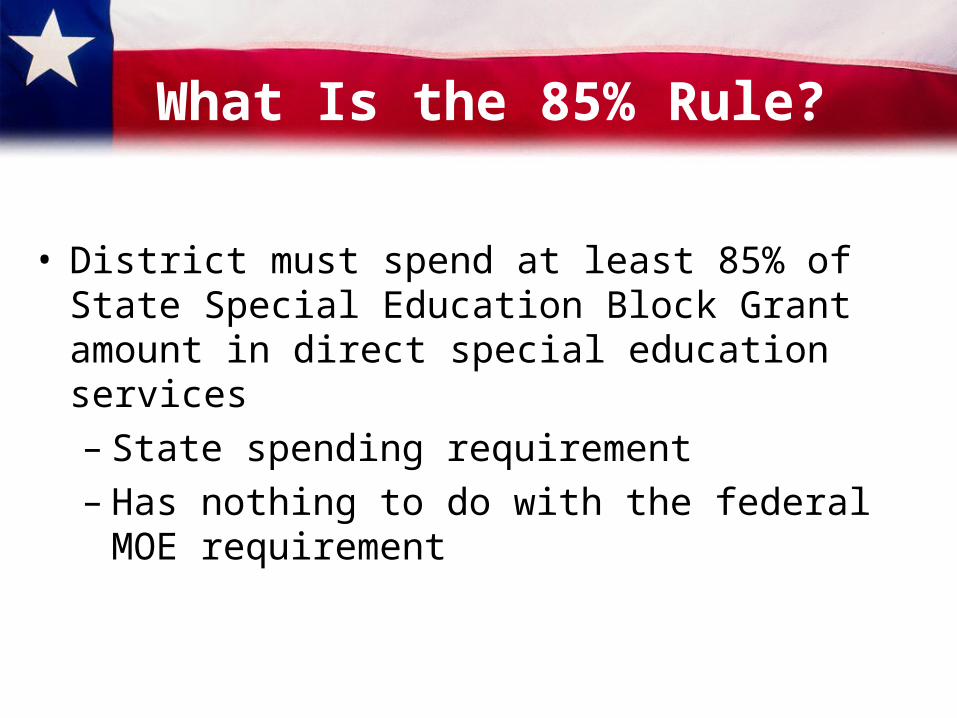

What Is the 85% Rule?

• District must spend at least 85% of State Special Education Block Grant amount in direct special education services– State spending requirement – Has nothing to do with the federal MOE

requirement

85% versus MOE?

Scenario #1

• FY03: LEA receives $100,000 in state special education dollars. They spent $95,000 in Fund 199, PIC 23, direct services

Result: Met 85%

• FY04: LEA receives $100,000 in state special education dollars. They spent $85,000 in Fund 199, PIC 23, direct services

Result: Met 85%, but not MOE

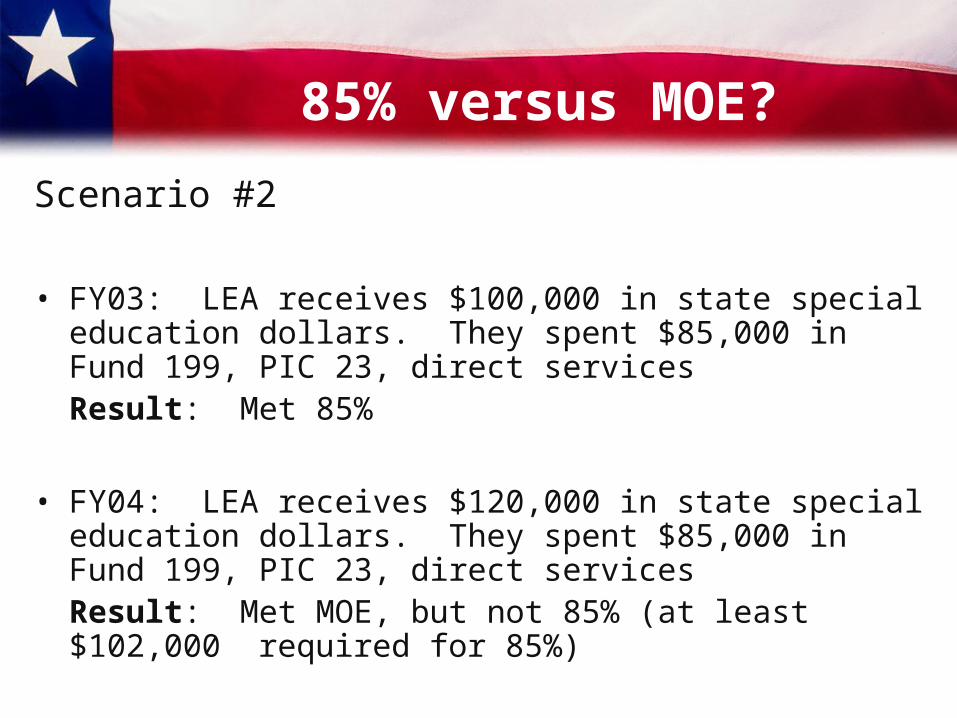

85% versus MOE?

Scenario #2

• FY03: LEA receives $100,000 in state special education dollars. They spent $85,000 in Fund 199, PIC 23, direct services

Result: Met 85%

• FY04: LEA receives $120,000 in state special education dollars. They spent $85,000 in Fund 199, PIC 23, direct services

Result: Met MOE, but not 85% (at least $102,000 required for 85%)

85% versus MOE?

Scenario #3

• FY03: LEA receives $100,000 in state special education dollars. They spent $85,000 in Fund 199, PIC 23, direct services

Result: Met 85%

• FY04: LEA receives $120,000 in state special education dollars. They spent $80,000 in Fund 199, PIC 23, direct services

Result: Did not meet MOE or 85%

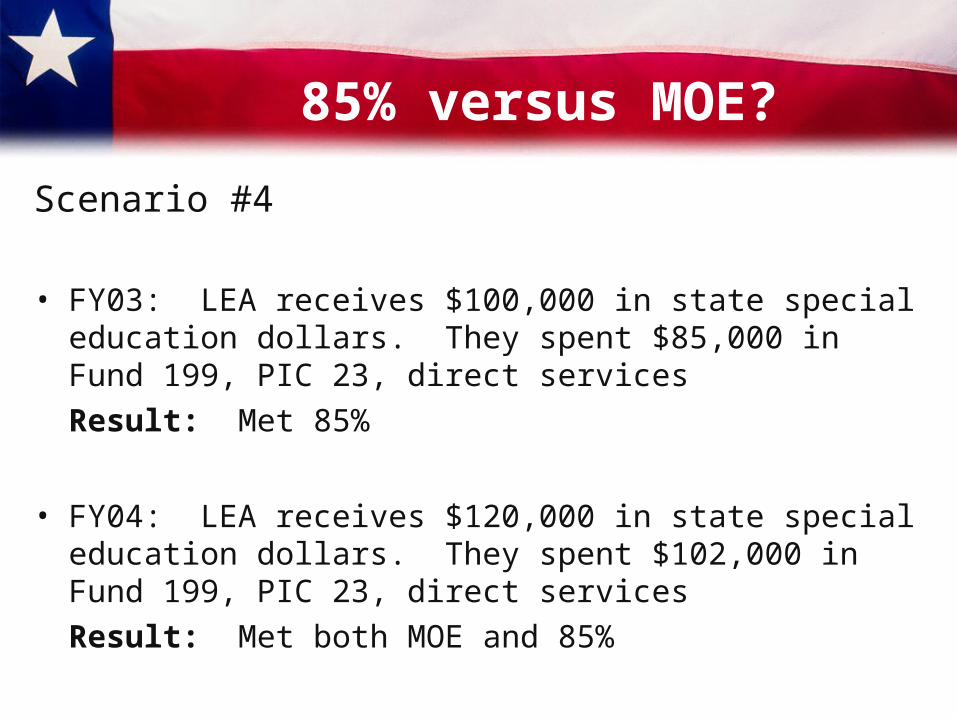

85% versus MOE?

Scenario #4

• FY03: LEA receives $100,000 in state special education dollars. They spent $85,000 in Fund 199, PIC 23, direct services

Result: Met 85%

• FY04: LEA receives $120,000 in state special education dollars. They spent $102,000 in Fund 199, PIC 23, direct services

Result: Met both MOE and 85%

What Are the Parts of MOE?

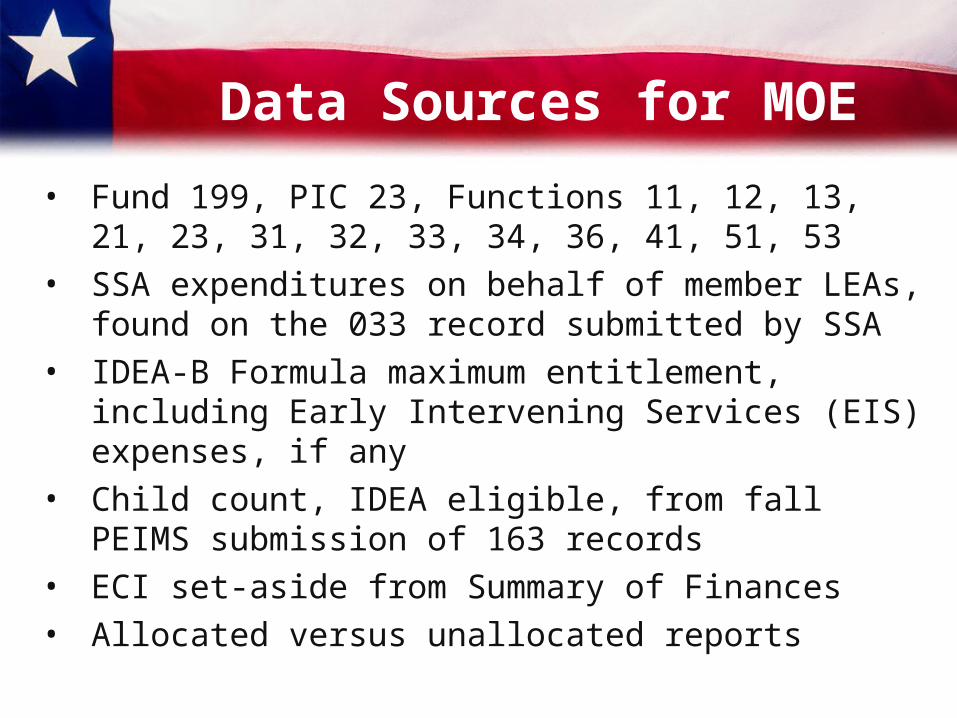

Data Sources for MOE

• Fund 199, PIC 23, Functions 11, 12, 13, 21, 23, 31, 32, 33, 34, 36, 41, 51, 53

• SSA expenditures on behalf of member LEAs, found on the 033 record submitted by SSA

• IDEA-B Formula maximum entitlement, including Early Intervening Services (EIS) expenses, if any

• Child count, IDEA eligible, from fall PEIMS submission of 163 records

• ECI set-aside from Summary of Finances• Allocated versus unallocated reports

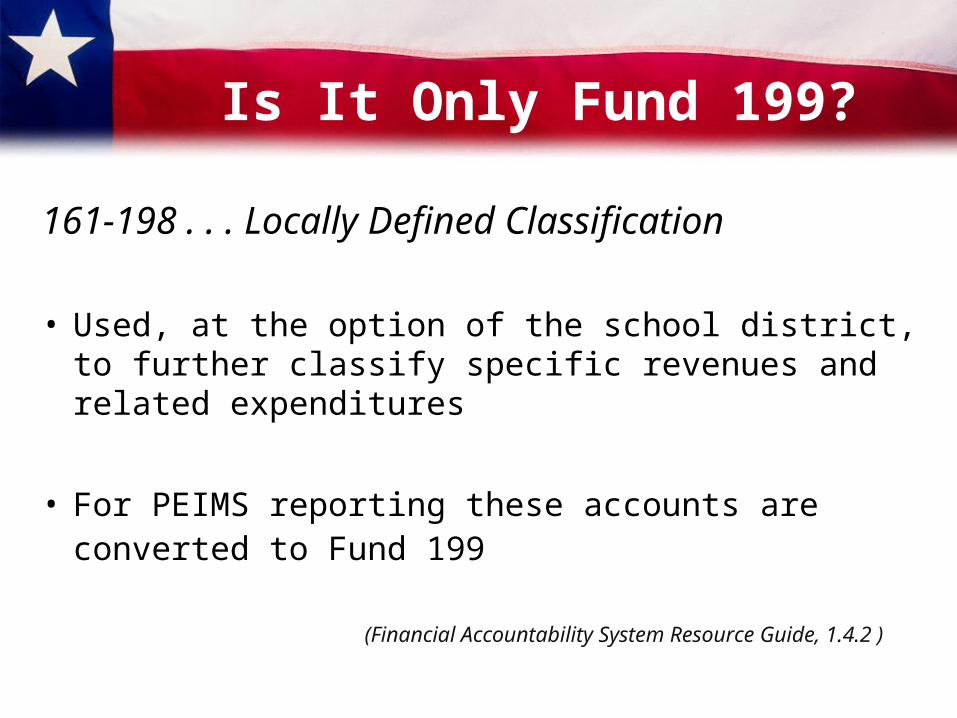

Is It Only Fund 199?

161-198 . . . Locally Defined Classification

• Used, at the option of the school district, to further classify specific revenues and related expenditures

• For PEIMS reporting these accounts are converted to Fund 199

(Financial Accountability System Resource Guide, 1.4.2 )

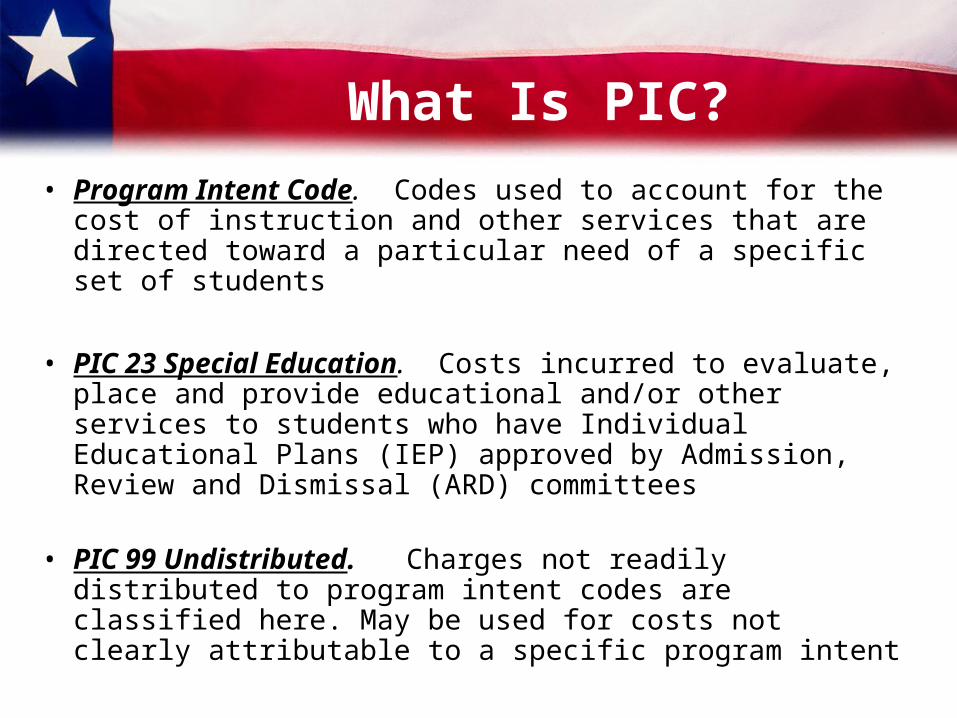

What Is PIC?

• Program Intent Code. Codes used to account for the cost of instruction and other services that are directed toward a particular need of a specific set of students

• PIC 23 Special Education. Costs incurred to evaluate, place and provide educational and/or other services to students who have Individual Educational Plans (IEP) approved by Admission, Review and Dismissal (ARD) committees

• PIC 99 Undistributed. Charges not readily distributed to program intent codes are classified here. May be used for costs not clearly attributable to a specific program intent

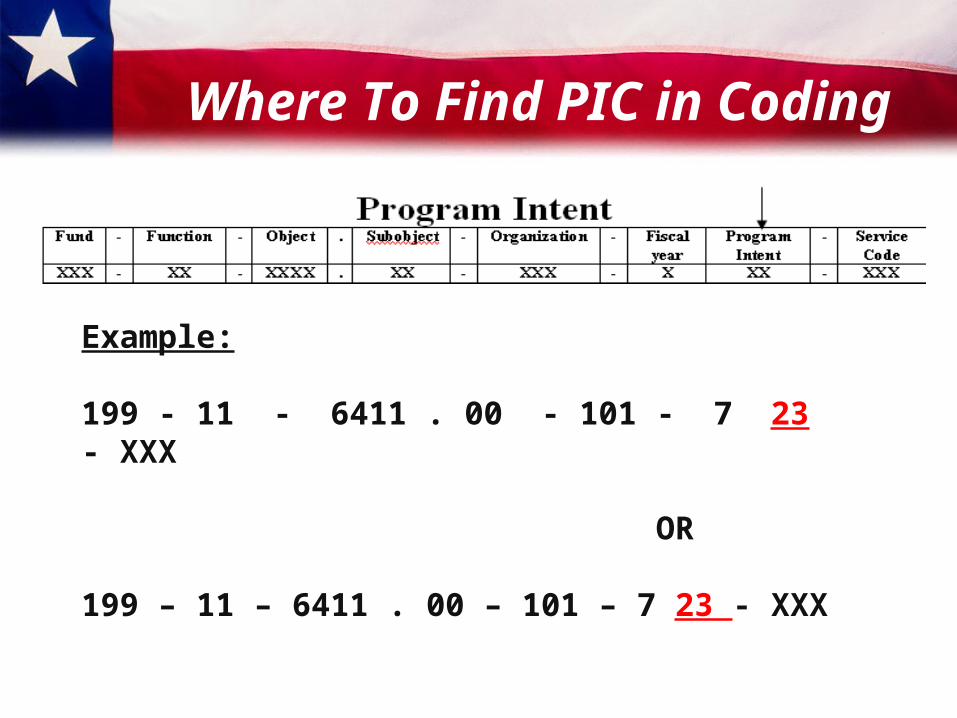

Where To Find PIC in Coding

Example:

199 - 11 - 6411 . 00 - 101 - 7 23 - XXX

OR

199 – 11 – 6411 . 00 – 101 – 7 23 - XXX

Are There Other PICs Besides 23?

Examples:

• 11 Basic Educational Services

• 21 Gifted and Talented

• 22 Career and Technology

• 24 Accelerated Education

• 25 Bilingual Education and Special Language

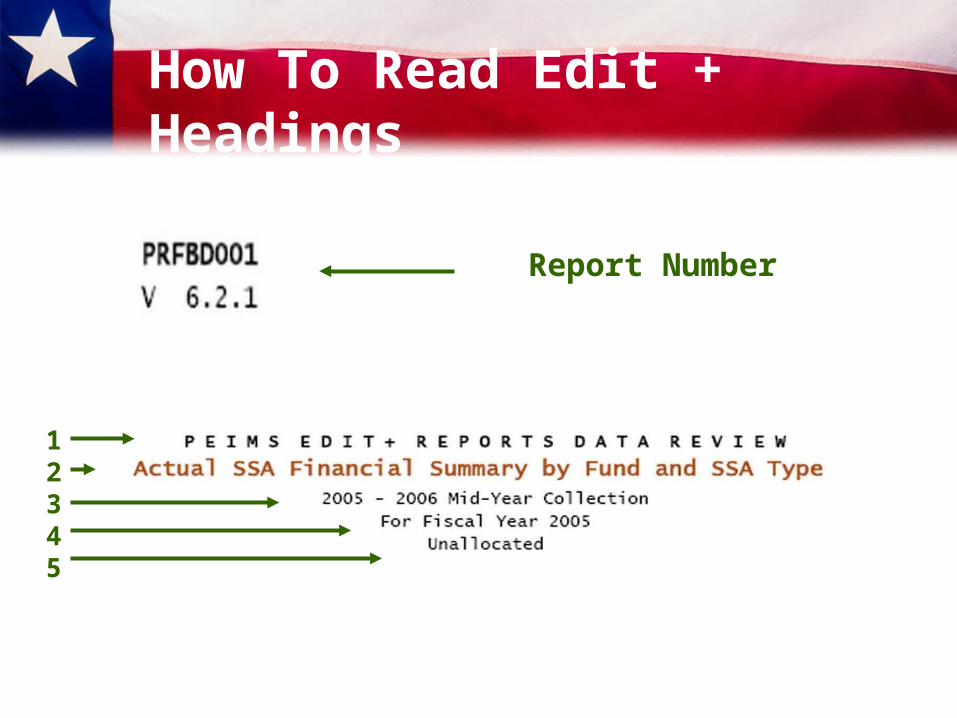

How To Read Edit + Headings

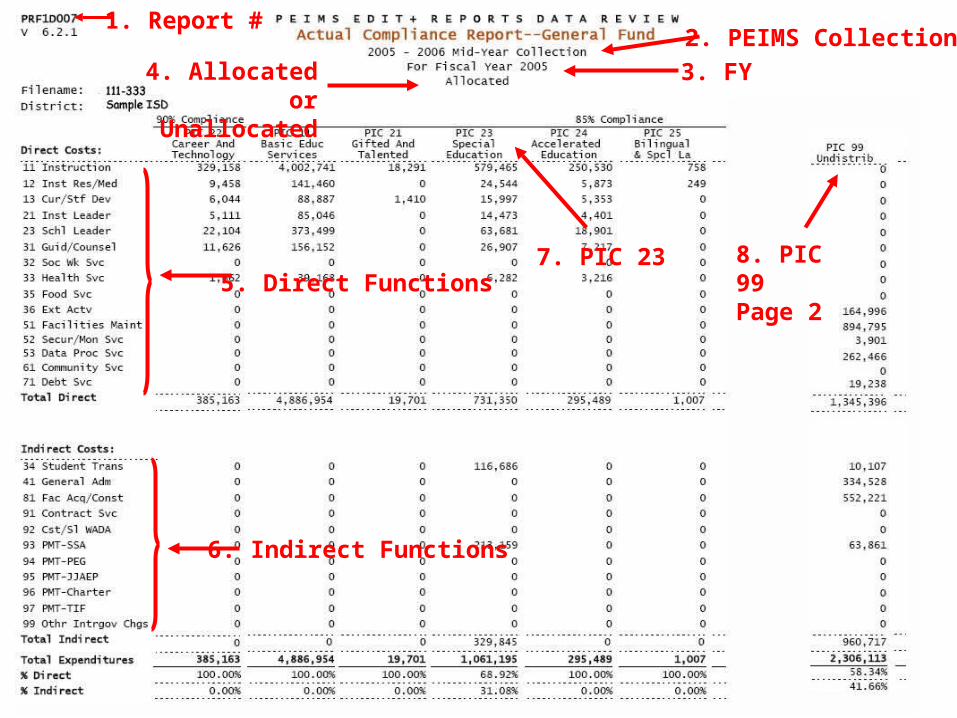

Report Number

12345

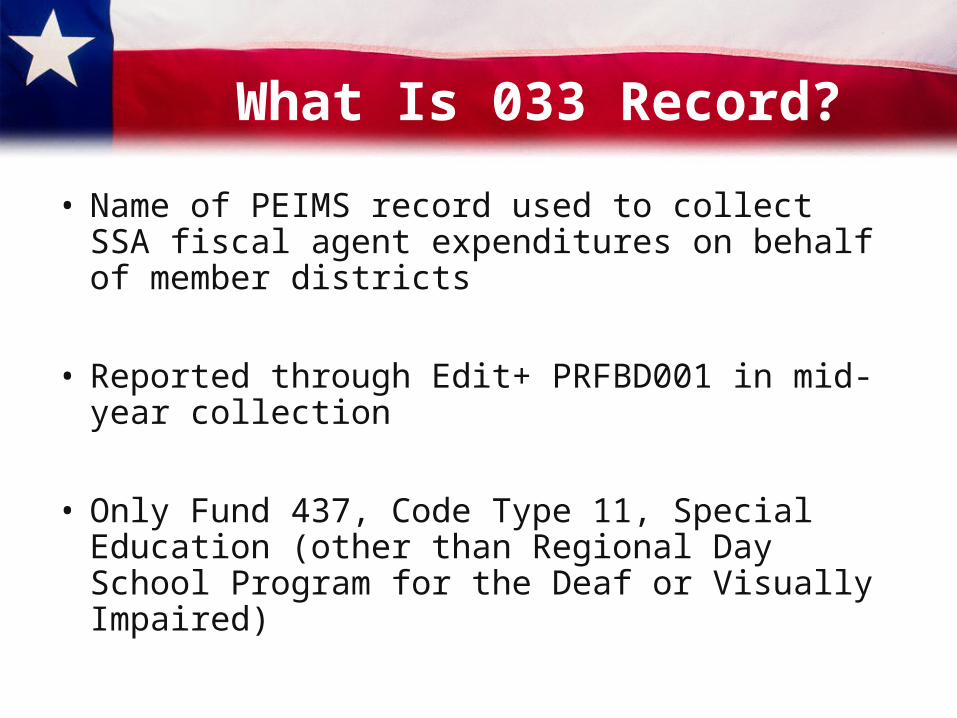

What Is 033 Record?

• Name of PEIMS record used to collect SSA fiscal agent expenditures on behalf of member districts

• Reported through Edit+ PRFBD001 in mid-year collection

• Only Fund 437, Code Type 11, Special Education (other than Regional Day School Program for the Deaf or Visually Impaired)

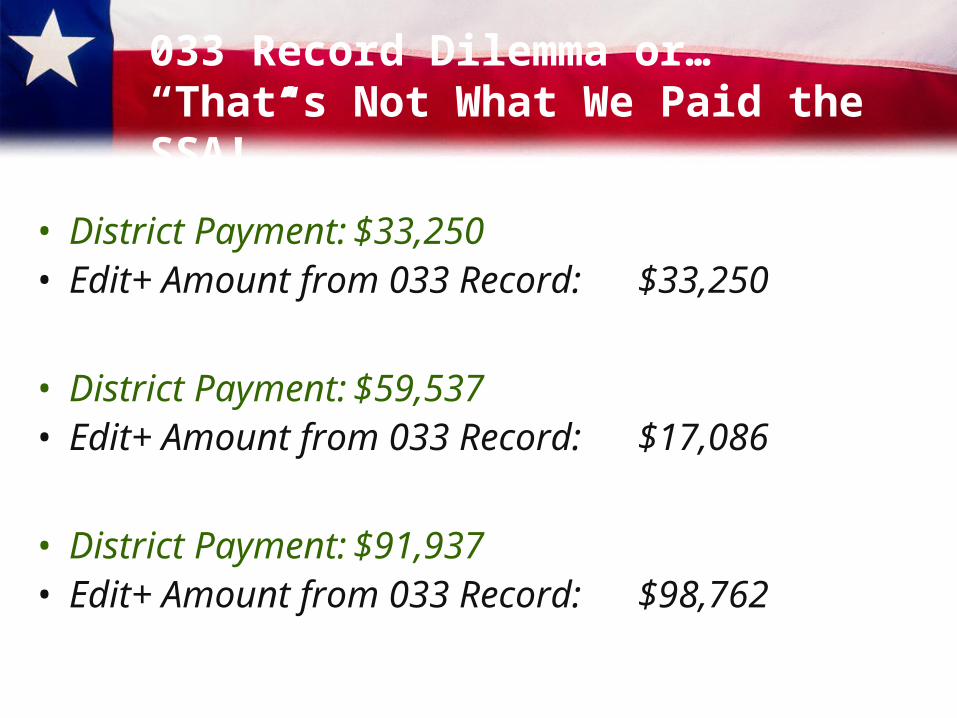

033 Record Dilemma or…“That’s Not What We Paid the SSA!”

• District Payment: $33,250• Edit+ Amount from 033 Record: $33,250

• District Payment: $59,537• Edit+ Amount from 033 Record: $17,086

• District Payment: $91,937• Edit+ Amount from 033 Record: $98,762

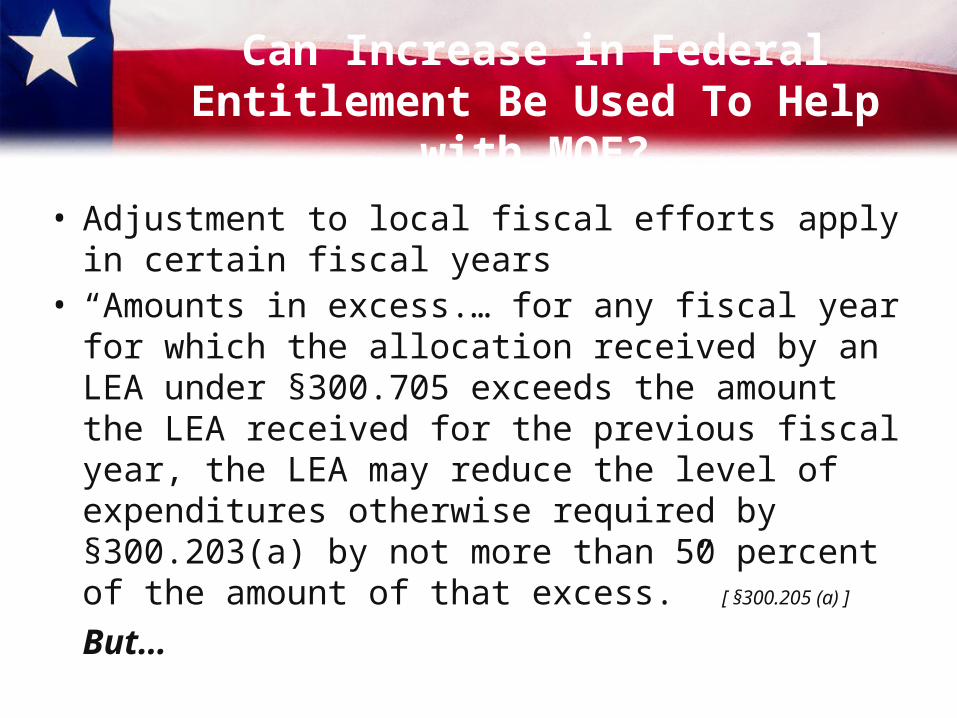

Can Increase in Federal Entitlement Be Used To Help with MOE?

• Adjustment to local fiscal efforts apply in certain fiscal years

• “Amounts in excess.… for any fiscal year for which the allocation received by an LEA under §300.705 exceeds the amount the LEA received for the previous fiscal year, the LEA may reduce the level of expenditures otherwise required by §300.203(a) by not more than 50 percent of the amount of that excess.” [ §300.205 (a) ]

But…

Early Intervening Services

Early intervening services may impact MOE…

“An LEA may not use more than 15 percent of the amount the LEA receives under Part B of the Act for any fiscal year, … to develop and implement coordinated, early intervening services, … for students … who are not currently identified as needing special education or related services, but who need additional academic and behavioral support to succeed in a general education environment.”

[ §300.226 (a) ]

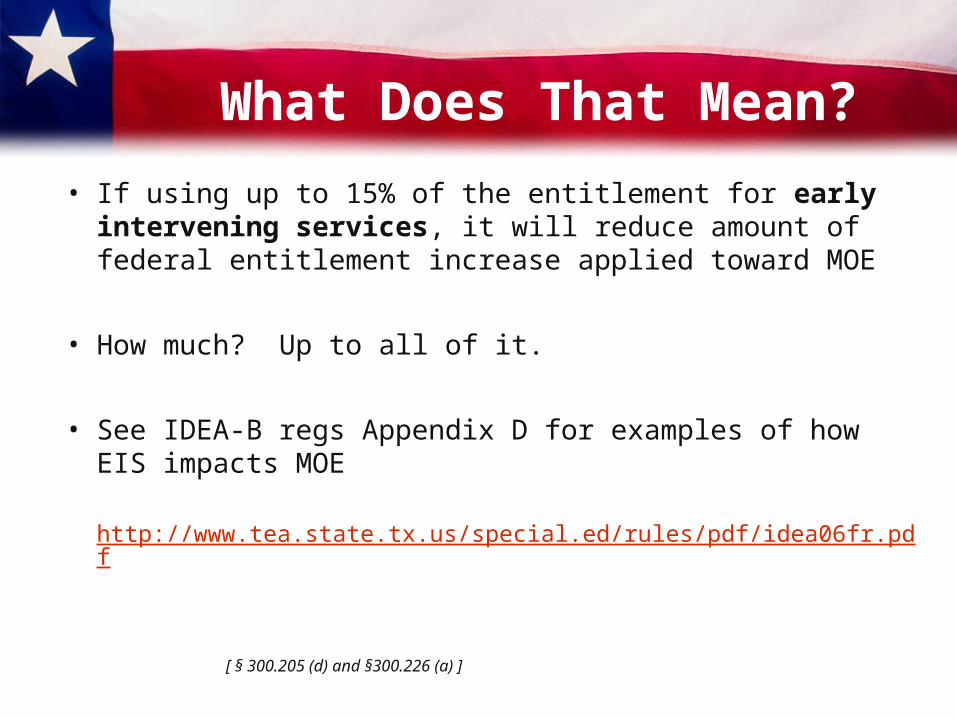

What Does That Mean?

• If using up to 15% of the entitlement for early intervening services, it will reduce amount of federal entitlement increase applied toward MOE

• How much? Up to all of it.

• See IDEA-B regs Appendix D for examples of how EIS impacts MOE

http://www.tea.state.tx.us/special.ed/rules/pdf/idea06fr.pdf

[ § 300.205 (d) and §300.226 (a) ]

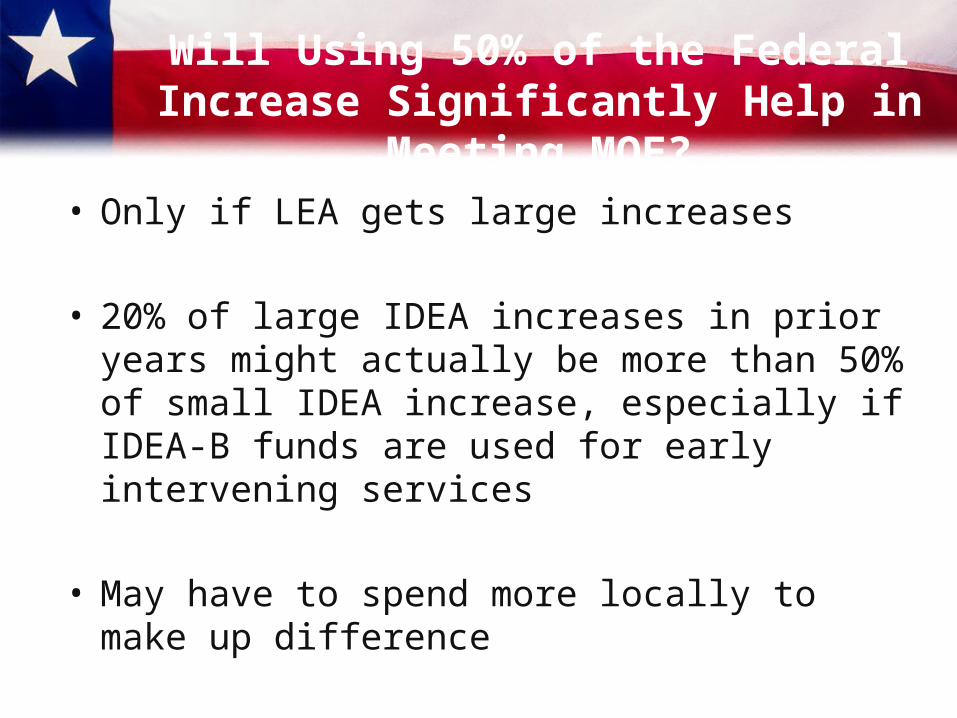

Will Using 50% of the Federal Increase Significantly Help in Meeting MOE?

• Only if LEA gets large increases

• 20% of large IDEA increases in prior years might actually be more than 50% of small IDEA increase, especially if IDEA-B funds are used for early intervening services

• May have to spend more locally to make up difference

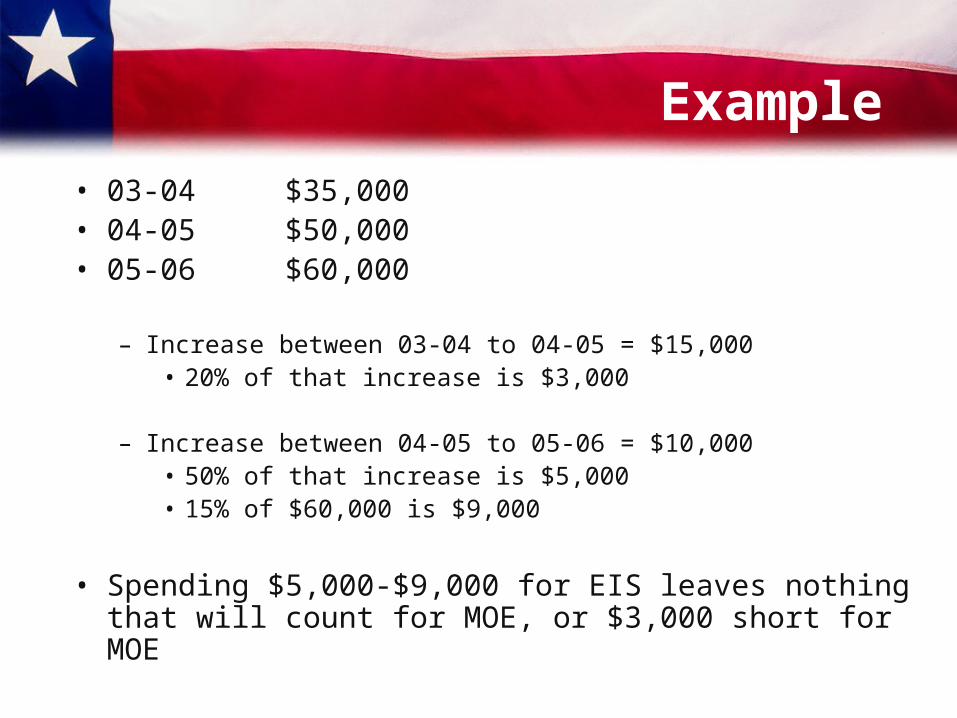

Example

• 03-04 $35,000 • 04-05 $50,000 • 05-06 $60,000

– Increase between 03-04 to 04-05 = $15,000• 20% of that increase is $3,000

– Increase between 04-05 to 05-06 = $10,000• 50% of that increase is $5,000• 15% of $60,000 is $9,000

• Spending $5,000-$9,000 for EIS leaves nothing that will count for MOE, or $3,000 short for MOE

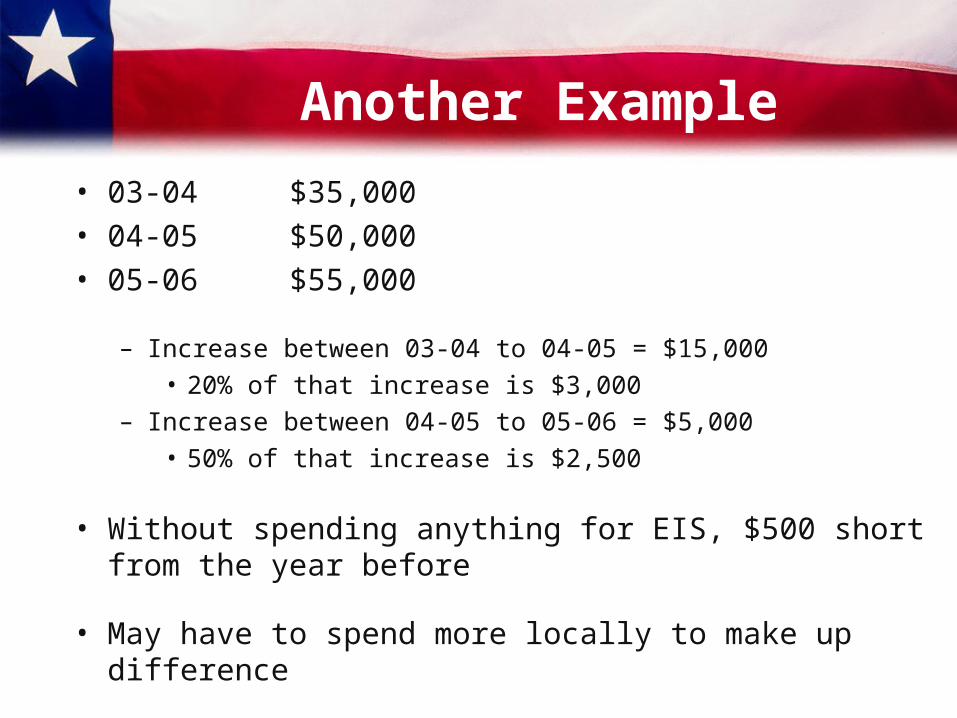

Another Example

• 03-04 $35,000 • 04-05 $50,000 • 05-06 $55,000

– Increase between 03-04 to 04-05 = $15,000• 20% of that increase is $3,000

– Increase between 04-05 to 05-06 = $5,000• 50% of that increase is $2,500

• Without spending anything for EIS, $500 short from the year before

• May have to spend more locally to make up difference

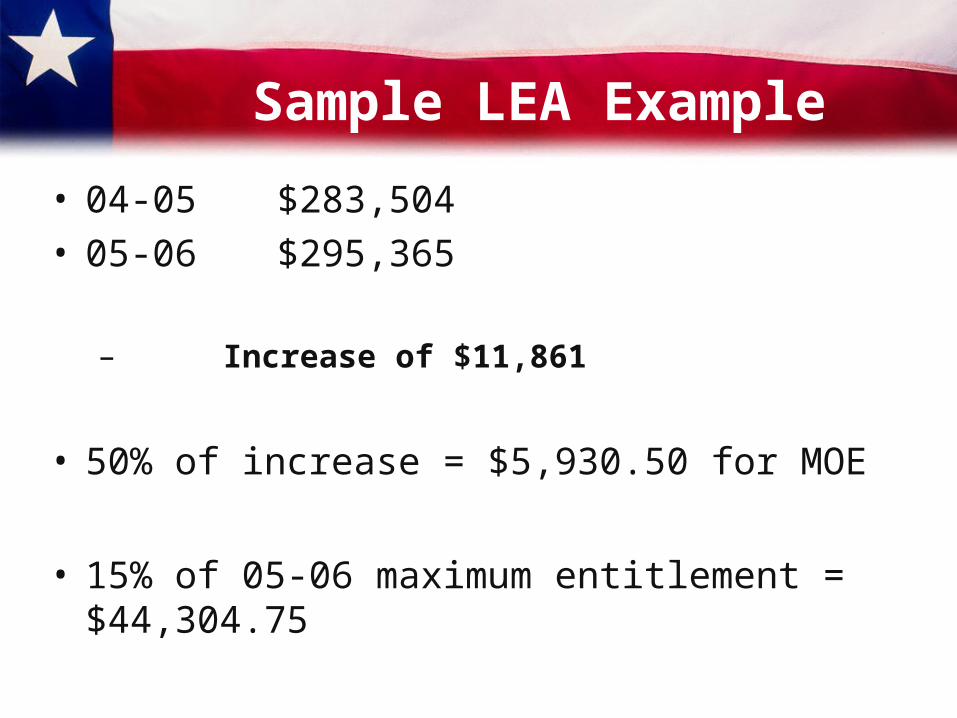

Sample LEA Example

• 04-05 $283,504 • 05-06 $295,365

– Increase of $11,861

• 50% of increase = $5,930.50 for MOE

• 15% of 05-06 maximum entitlement = $44,304.75

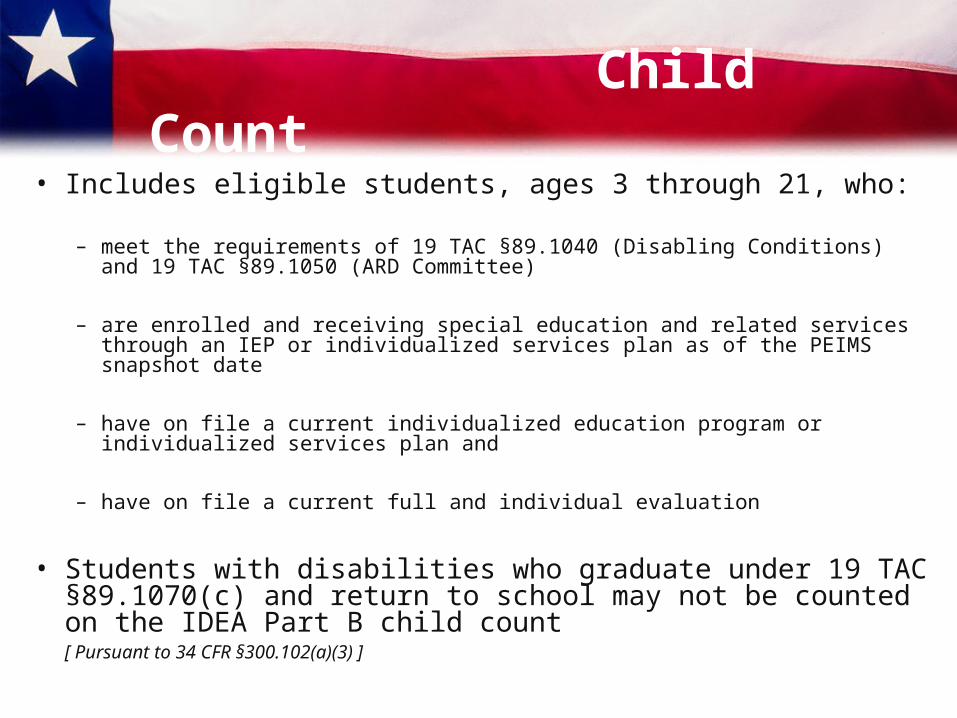

Child Count

• Includes eligible students, ages 3 through 21, who:

– meet the requirements of 19 TAC §89.1040 (Disabling Conditions) and 19 TAC §89.1050 (ARD Committee)

– are enrolled and receiving special education and related services through an IEP or individualized services plan as of the PEIMS snapshot date

– have on file a current individualized education program or individualized services plan and

– have on file a current full and individual evaluation

• Students with disabilities who graduate under 19 TAC §89.1070(c) and return to school may not be counted on the IDEA Part B child count [ Pursuant to 34 CFR §300.102(a)(3) ]

What Is ECI Set-Aside?

• Found on the District’s Summary of Finances http://www.tea.state.tx.us/school.finance/funding/sofweb7.html

• Shown as negative number

• Adjustment taken “off the top” or “set aside” at state level

What Is the Most Confusing Part of

Understanding MOE?

ALLOCATION…

Or, how to decide how much of PIC 99 belongs to special education?

Unallocated Report vs. Allocated Report

What is the difference between an unallocated reportand an allocated report?

• Unallocated matches the “books,” or general ledger

• Allocated is what is on the general ledger for PIC 23, PLUS part of what had been in PIC 99

What Is Allocation?

• Allocation process – Is a report type of template– Does not change transaction information within the

general ledger system – Uses payroll and staff data for instructional FTEs (full time

equivalents of staff), as recorded under function 11, Instruction, as a basis to allocate costs from PIC 99

• Full use of specific program intent codes in function 11 is essential for the optimum functionality of the allocation process

• Undistributed Program Intent Code 99 used when a school district elects not to allocate costs

What Allocates?

• Amounts dispersed from the General Fund, PIC 99

(Note: The use of PIC 99 is district choice in most instances)

• Fund 199 (including local use of 161-198)

• Objects 6XXX

• DC Functions 11, 12, 13, 21, 23, 31, 32, 33

• IC Functions None

• Not Org 998 or 7XX

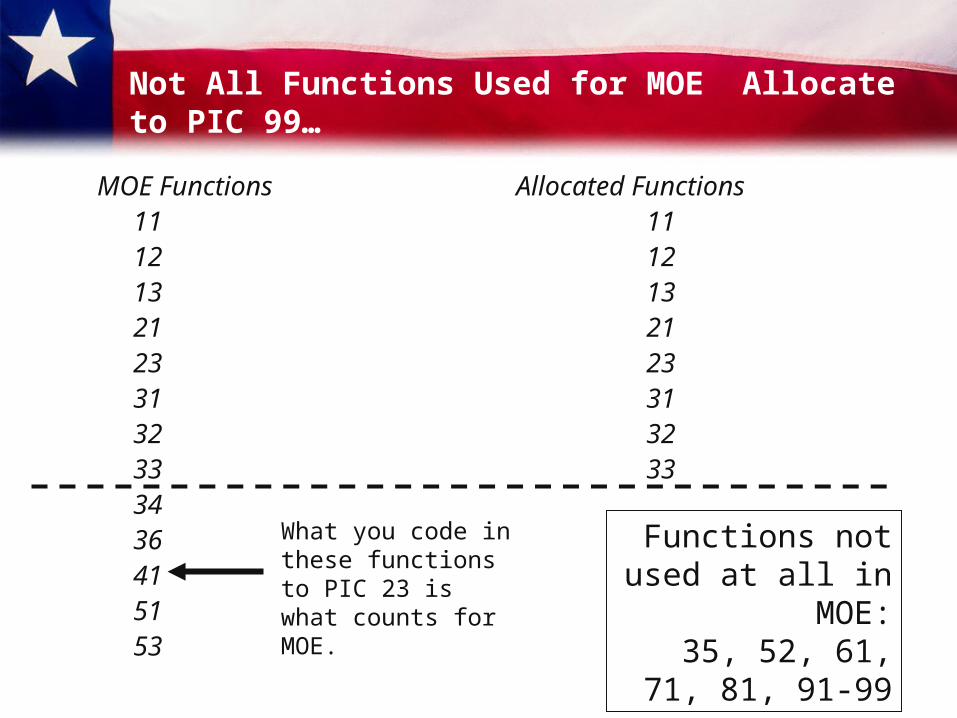

Not All Functions Used for MOE Allocate to PIC 99…

MOE Functions Allocated Functions11 1112 1213 1321 2123 2331 3132 3233 333436415153

What you code in these functions to PIC 23 is what counts for MOE.

Functions not used at all in MOE:

35, 52, 61,71, 81, 91-99

1 36

5. Direct Functions

6. Indirect Functions

7. PIC 23 8. PIC 99Page 2

4. Allocated or Unallocated

3. FY

2. PEIMS Collection1. Report #

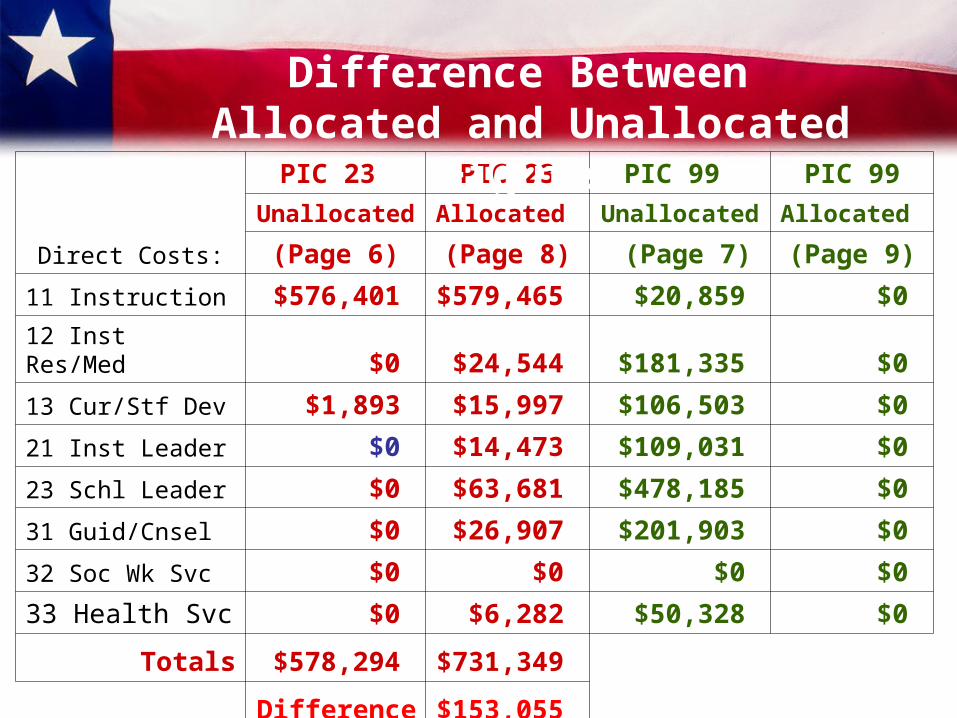

Difference Between Allocated and Unallocated Figures

Is there a lot of difference between the allocated and unallocated figures?

It depends on your district’s financial accounting and how much PIC 99 is used.

Direct Costs:

PIC 23 PIC 23 PIC 99 PIC 99

Unallocated Allocated Unallocated Allocated

(Page 6) (Page 8) (Page 7) (Page 9)

11 Instruction $576,401 $579,465 $20,859 $0

12 Inst Res/Med $0 $24,544 $181,335 $0

13 Cur/Stf Dev $1,893 $15,997 $106,503 $0

21 Inst Leader $0 $14,473 $109,031 $0

23 Schl Leader $0 $63,681 $478,185 $0

31 Guid/Cnsel $0 $26,907 $201,903 $0

32 Soc Wk Svc $0 $0 $0 $0

33 Health Svc $0 $6,282 $50,328 $0

Totals $578,294 $731,349

Difference $153,055

Difference Between Allocated and Unallocated Figures

PIC 99 Lesson

• Use PIC 99 as little as possible

(Then more direct control over meeting MOE with direct expenses)

• Remember, use of PIC 99 is optional in most cases

• Not all PIC 99 coding affects MOE. Review the slide “What Allocates”

Estimating How Much PIC 99 Will Allocate to PIC 23

Is there a spreadsheet we can use for estimating how much PIC 99 will allocate to PIC 23?

• No . . . but . . .

• PEIMS EDIT+ User Technical Documentation: Tips for the Allocation Process for PEIMS (EDIT+) Reports

http://www.tea.state.tx.us/peims/editplus/documents/tips_allocproc.pdf

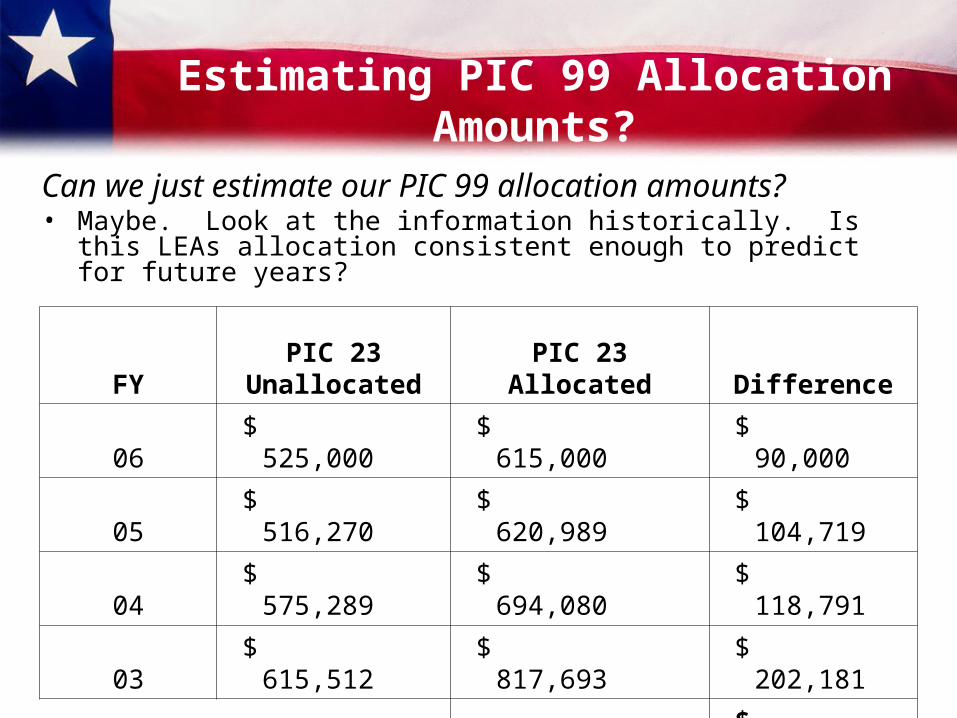

Estimating PIC 99 Allocation Amounts?

Can we just estimate our PIC 99 allocation amounts?• Maybe. Look at the information historically. Is this LEAs allocation

consistent enough to predict for future years?

FYPIC 23

UnallocatedPIC 23

Allocated Difference

06 $ 396,500 $ 445,000 $ 48,500

05 $ 382,539 $ 442,355 $ 59,816

04 $ 355,206 $ 404,543 $ 49,337

03 $ 373,396 $ 427,684 $ 54,288

4 year average $ 52,985

Estimating PIC 99 Allocation Amounts?

Can we just estimate our PIC 99 allocation amounts?• Maybe. Look at the information historically. Is this LEAs allocation

consistent enough to predict for future years?

FYPIC 23

UnallocatedPIC 23

Allocated Difference

06 $ 525,000 $ 615,000 $ 90,000

05 $ 516,270 $ 620,989 $ 104,719

04 $ 575,289 $ 694,080 $ 118,791

03 $ 615,512 $ 817,693 $ 202,181

4 year average $ 128,923

How Is MOE Calculated?

1 44

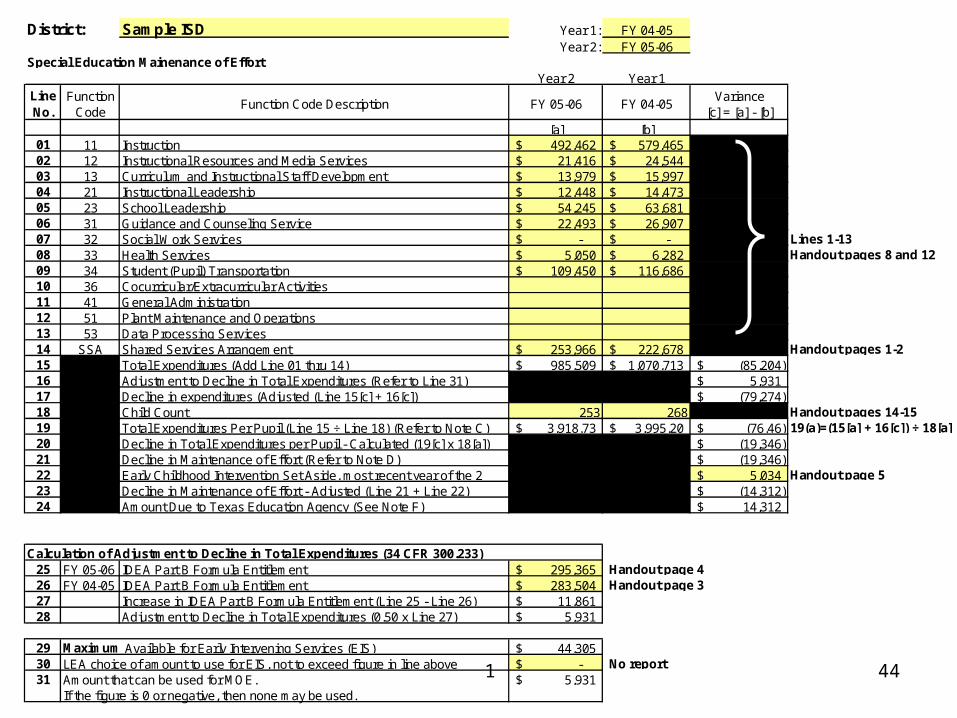

District: Sample ISD Year 1: FY 04-05Year 2: FY 05-06

Special Education Mainenance of EffortYear 2 Year 1

Line No.

Function Code

Function Code Description FY 05-06 FY 04-05Variance

[c] = [a] - [b][a] [b]

01 11 Instruction 492,462$ 579,465$ 02 12 Instructional Resources and Media Services 21,416$ 24,544$ 03 13 Curriculum and Instructional Staff Development 13,979$ 15,997$ 04 21 Instructional Leadership 12,448$ 14,473$ 05 23 School Leadership 54,245$ 63,681$ 06 31 Guidance and Counseling Service 22,493$ 26,907$ 07 32 Social Work Services -$ -$ Lines 1-1308 33 Health Services 5,050$ 6,282$ Handout pages 8 and 1209 34 Student (Pupil) Transportation 109,450$ 116,686$ 10 36 Cocurricular/Extracurricular Activities11 41 General Administration12 51 Plant Maintenance and Operations13 53 Data Processing Services14 SSA Shared Services Arrangement 253,966$ 222,678$ Handout pages 1-215 Total Expenditures (Add Line 01 thru 14) 985,509$ 1,070,713$ (85,204)$ 16 Adjustment to Decline in Total Expenditures (Refer to Line 31) 5,931$ 17 Decline in expenditures (Adjusted (Line 15[c] + 16[c]) (79,274)$ 18 Child Count 253 268 Handout pages 14-1519 Total Expenditures Per Pupil (Line 15 ÷ Line 18) (Refer to Note C) 3,918.73$ 3,995.20$ (76.46)$ 19(a)=(15[a] + 16[c]) ÷ 18[a]20 Decline in Total Expenditures per Pupil - Calculated (19[c] x 18[a]) (19,346)$ 21 Decline in Maintenance of Effort (Refer to Note D) (19,346)$ 22 Early Childhood Intervention Set Aside, most recent year of the 2 5,034$ Handout page 523 Decline in Maintenance of Effort - Adjusted (Line 21 + Line 22) (14,312)$ 24 Amount Due to Texas Education Agency (See Note F) 14,312$

Calculation of Adjustment to Decline in Total Expenditures (34 CFR 300.233)25 FY 05-06 IDEA Part B Formula Entitlement 295,365$ Handout page 426 FY 04-05 IDEA Part B Formula Entitlement 283,504$ Handout page 327 Increase in IDEA Part B Formula Entitlement (Line 25 - Line 26) 11,861$ 28 Adjustment to Decline in Total Expenditures (0.50 x Line 27) 5,931$

29 Maximum Available for Early Intervening Services (EIS) 44,305$ 30 LEA choice of amount to use for EIS, not to exceed figure in line above -$ No report31 Amount that can be used for MOE. 5,931$

If the figure is 0 or negative, then none may be used.

Edit + PRF3D022

• New Edit+ report available in mid-year PEIMS

found in the Edit+ Turnaround Reports

Source of Excel Spreadsheet

• For a prediction of how the spreadsheets will look for 05-06 and following years, Region 8 ESC has developed an Excel spreadsheet

• Available at following link:

http://www.reg8.net/docs/14-MOE%20FY05%20to%20FY06.xls

MOE Exceptions

Allowable Exceptions to MOE

• §300.204 Exception to maintenance of effort

“Notwithstanding the restriction in § 300.203(a), an LEA may reduce the level of expenditures by the LEA under Part B of the Act below the level of those expenditures for the preceding fiscal year if the reduction is attributable to any of the following:” – The voluntary departure, by retirement or

otherwise, or departure for just cause, of special education or related services personnel

– A decrease in the enrollment of children with disabilities

– The termination of the obligation of the agency, consistent with this part, to provide a program of special education to a particular child with a disability that is an exceptionally costly program, as determined by the SEA, because the child—

(1) Has left the jurisdiction of the agency

(2) Has reached the age at which the obligation of the agency to provide FAPE to the child has terminated; or

(3) No longer needs the program of special education

Allowable Exceptions to MOE

– The termination of costly expenditures for long-term purchases, such as the acquisition of equipment or the construction of school facilities

– The assumption of cost by the high cost fund operated by the SEA under § 300.704(c)

Allowable Exceptions to MOE

State Enforcement

“If an SEA determines that an LEA is not meeting the requirements of Part B of the Act, including the targets in the State’s performance plan, the SEA must prohibit the LEA from reducing the LEAs maintenance of effort under § 300.203 for any fiscal year.”

[ § 300.608 (a) ]

What Records Do We Need To Keep for Each

Exception?

The voluntary departure, by retirement or otherwise, or departure for just cause, of special education or related services personnel.

• All staff must be properly certified, and TEA may check SBEC records prior to approving this exception

• This exception is LEA employees only, not contract

Exception A: Voluntary Departure

Does this exception apply if we reduce staff by reassigning outside of the special education program? In other words, if the teacher is still in the district, just no longer in the special education program, does it count under this exception?

• No. The law and the rule clearly state departure, not transfer or reassignment.

Exception A: Voluntary Departure

Special Education Staff Records To Keep Each Year

• List of special education staff assigned to and paid from special education funds

• List of special education staff who leave• Changes in special education staff in the middle

of the year• Staff schedules, time and effort documentation,

and job descriptions or other record of assigned job duties

Special Education Staff Records To Keep Each Year

• Documentation of appropriate certification or licensure, including emergency and temporary permits

• Rationale for not replacing leaving staff, – Reduction in the # of special education students– High cost student leaves

Exception B: Decrease in Special Education Enrollment

• Reduction in # of special education students will not be accepted as exception if district actually earned more state special education block grant funds in second year– Year 1 $200,000, 525 students– Year 2 $240,000, 498 students

• Only eligible IDEA-B student counts were used in letters mailed in 2006

Special Ed Student Enrollment Records To Keep Each Year

• Edit+ PRF5D010 Special Education Child/Counts by Funding Type

• Roster of the students in the Edit+ report. Could be Edit+ PRF5D027 Special Education Roster by Grade or list from your district software

• Notes about high cost students or any other special circumstances that could impact MOE

The termination of the obligation of the agency… to provide a program of special education to a particular child with a disability that is an exceptionally costly program,… because the child—(1) Has left the jurisdiction of the agency;(2) Has reached the age at which the obligation of the agency to provide FAPE to the child has terminated; or(3) No longer needs the program of special education.

• Interpret these exceptions literally

Exception C: Termination of Exceptionally Costly Program

High Cost Records To Keep Each Year

• List of high cost students who leave during or at end of the year, or who do not return to school in fall, and the documentation proving this list

• Copies of student ARDs/IEPs documenting requirement of services

• POs and other records proving high cost expenses, such as special equipment

• Costs of related services to an individual student, which may also require payroll or contracted services costs, logs or other documentation of services provided, etc.

The termination of costly expenditures for long-term purchases, such as the acquisition of equipment or the construction of school facilities.

• Payment of a large obligation limited to LEAs definition of capitalization (6600). So, if LEA only capitalizes individual items >$5,000, then large purchases of <$5,000 per item will not count

• Long-term means taking 2 or more years to pay the debt

AND

• Item must have an anticipated life span of >12 months

• Supplies and consumable items won’t count

Exception D: Termination ofLong-Term Purchase Expenditures

Long-term Purchase RecordsTo Keep Each Year

• POs and other records proving long-term purchases, and records to show payment took more than one year

• LEA policies or guidelines on capitalization of equipment

• TEA may ask you to explain how item(s) purchased is/are directly attributable to and necessary for provision of special education services

Exception E: High Cost Fund

The assumption of cost by the high cost fund operated by the SEA under § 300.704(c).

What does this mean?

Another good example of what we don’t know yet about the new regs.

What Do We Do If We Get an MOE Letter from TEA?

MOE Letter from TEA

What do we do if we get a letter from TEA?

• Read the letter carefully

• Verify the data

• See if you qualify for exceptions

• Submit only what they want, in the format requested, by the deadline set

What If We Owe Money?

• Don’t send a check until TEA asks you to do so.

• What if we owe more than we received in federal dollars? – It is lesser of the absolute value of decline in MOE or

IDEA-B maximum entitlement for the year

• Who writes the check if the district is an SSA member? – LEA, from local funds, not the SSA – Repayment also from local funds for single member

district

How Do We Avoid an MOE Problem?

How Do We Avoid MOE Problem?

• Give Special Education staff access to budget and expenditure information to assist in catching errors—at budgeting and during the fiscal year

• Give Special Education staff access to PEIMS reports prior to final submission deadlines

• These sharing practices are important for all special populations, not just special education

What If We Had Bad Data?

• Bad data, bad data, bad data!– Staff or expenses miscoded in budgets

• That’s between you and TEA as to whether they accept it as an MOE explanation

MOE: What We Have (and Haven’t) Learned

• Districts can be in a grey area—where total expenditures increase or remain the same and expenditures per pupil decline, or visa versa

• SSVI and Medicaid Administrative Claiming (MAC) are NOT coded to the general fund (199)

• SHARS should be coded to the general fund (199)

MOE: What We Have (and Haven’t) Learned

• Bad data in 033 record– 033 record is hand entered data, not extracted– Errors in entering wrong fiscal year or amount– LEAs being left off

• Mismatch between child count year and expenditure year on 033 records

• Share with member districts

MOE: Where Do We Go from Here?

Where Do We Go from Here?

• Devise a record keeping system and systematically keep anything that might possibly apply to MOE

• Let everyone know where those records are filed

General Records To Collect

• Independent audit reports

• Spending trends analysis

• Spreadsheets run to track MOE

• Copies of Edit+ reports

• Maximum entitlements

• Any board policies that impact MOE (capitalization, voluntary retirements/resignations, etc.)

Times To Check MOE

When you:

• Propose a new budget

• Prepare to close a fiscal year

• Review the real figures for the prior fiscal year after the mid-year PEIMS collection

Next Steps

• When fiscal agent closes books for year, member districts should be provided with amount that will be reported on 033 record

• When mid-year collection is submitted, fiscal agent should give copy of Edit+ PRFBD001 to each member district

• After mid-year submission, each LEA should run MOE figures as pre-look at MOE status before TEA letters are mailed

Next Steps

• Fiscal agent should provide amount of the maximum IDEA-B Formula entitlement to SSA members

• Documentation system should be developed for any potential MOE issue

- Should be collected at that time since letters will be months later coming from TEA

- Should be collected in such a way to answer directly one or more of allowable reasons for reduction of MOE

Next Steps

• Foster strong working relationship among special education director, PEIMS coordinator, and business manager

• Establish who keeps what records and makes what decisions

• Make sure all know what affects MOE

• Make sure new business managers understand MOE implications before they change bookkeeping and/or coding procedures

MOE Reference Documents

• Individuals With Disabilities Education Act http://www.tea.state.tx.us/special.ed/rules/

• WebSAS or eGrants Program Guidelineshttp://www.tea.state.tx.us/special.ed/funding/

• IDEA-B Formula Maximum Entitlementshttp://barton.tea.state.tx.us/websas/Pg_Admin_Pub_Login.asp

MOE Reference Documents

• Financial Accounting and Reporting Module, TEA Financial Accountability System Resource Guide http://www.tea.state.tx.us/school.finance/audit/resguide12/index.html

• Texas laws and regulations on spending state special education funds, such as TEC §21.003, TAC § 89.1125, 89.1131, 230.501, 230.551http://www.tea.state.tx.us/special.ed/rules/sbs.html

MOE Reference Documents

• PEIMS Data Standards http://www.tea.state.tx.us/peims/standards/index.html

• Edit+ Reports

http://www.tea.state.tx.us/peims/editplus/index.html

• August 2006 TEA PowerPoint on MOE:

http://www.tea.state.tx.us/school.finance/audit/2006_0824_resc_iv_idea_moe.ppt

Disclaimer

• There are some variations to this content for charter schools

• Call your ESC for more assistance if needed

Summary

During this module, participants learned:• What is MOE?• What are the parts of MOE?• How is MOE calculated?• What might count as exceptions?• What do we do if we get a letter from TEA?• How do we avoid the problem?