Special Accounting Procedures Chapter 5. What ratios I need to know 1.Gross profit margin 2.Net...

26

Special Accounting Procedures Chapter 5

-

Upload

maria-mcdonald -

Category

Documents

-

view

221 -

download

1

Transcript of Special Accounting Procedures Chapter 5. What ratios I need to know 1.Gross profit margin 2.Net...

Special Accounting Procedures

Chapter 5

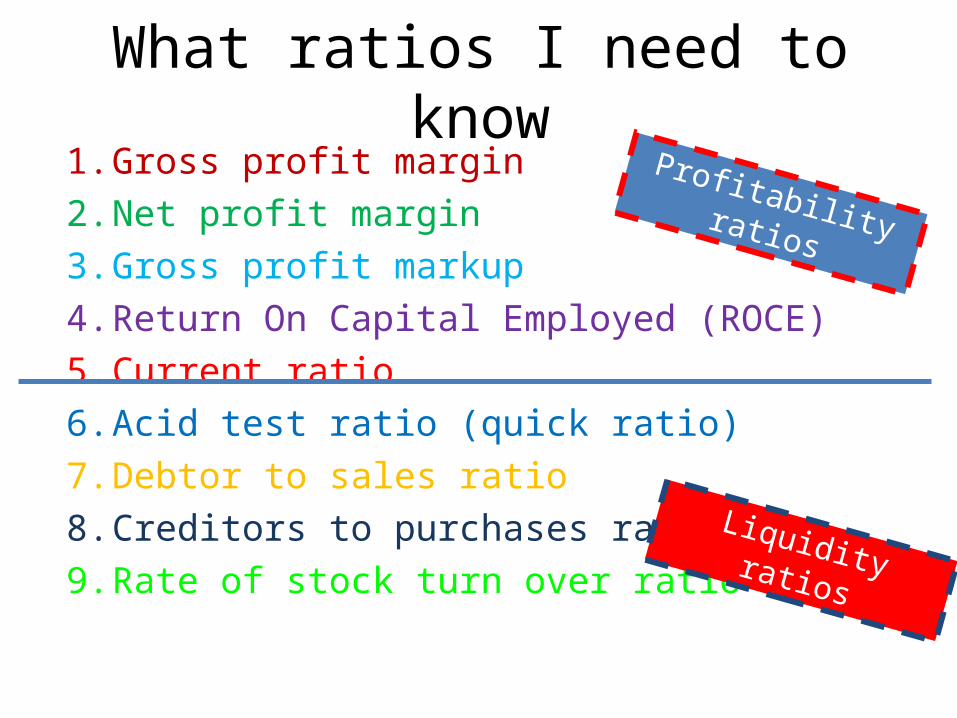

What ratios I need to know1. Gross profit margin2. Net profit margin3. Gross profit markup4. Return On Capital Employed (ROCE)5. Current ratio6. Acid test ratio (quick ratio)7. Debtor to sales ratio8. Creditors to purchases ratio9. Rate of stock turn over ratio

Profitability ratios

Liquidity ratios

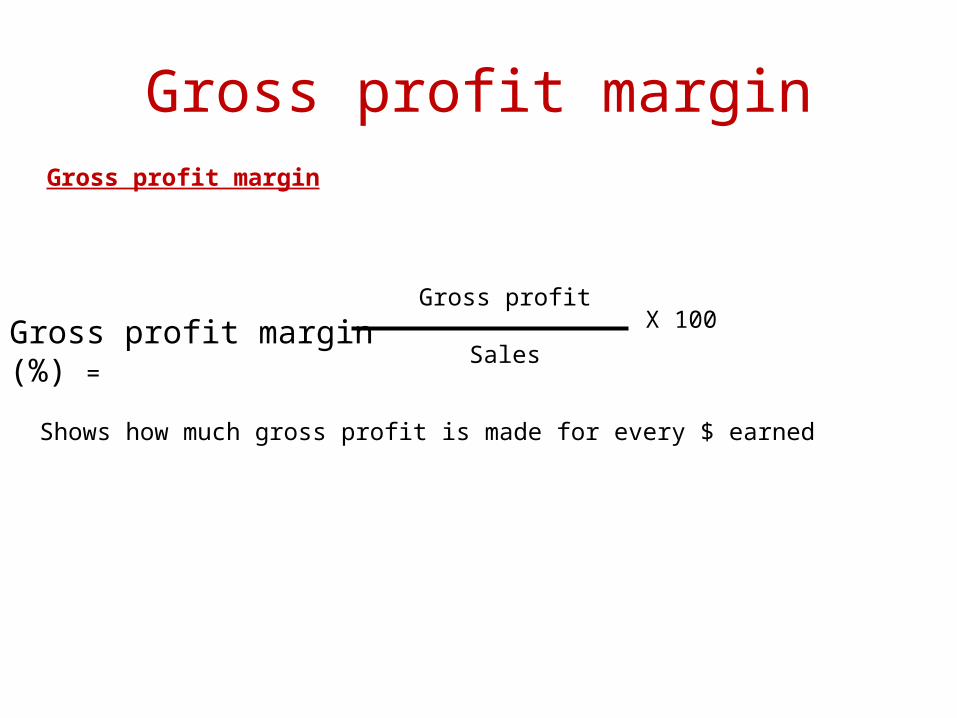

Gross profit marginGross profit margin

Gross profit margin (%) =

Gross profit

SalesX 100

Shows how much gross profit is made for every $ earned

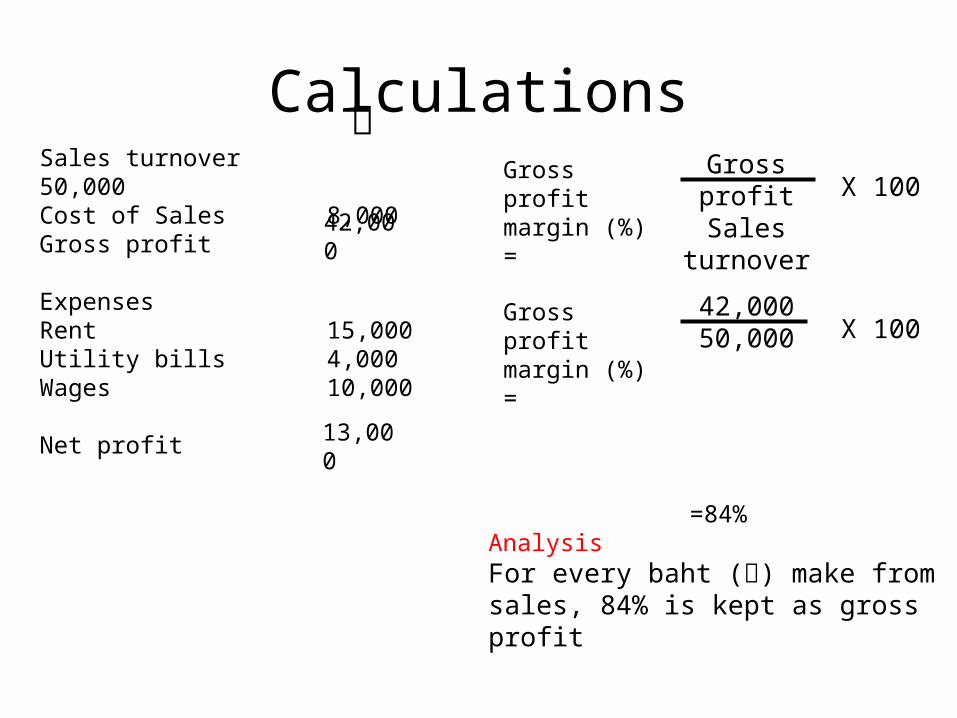

Calculations ฿Sales turnover 50,000Cost of Sales 8,000Gross profit

ExpensesRent 15,000Utility bills 4,000Wages 10,000

Net profit

42,000

13,000

Gross profit margin (%) =

Gross profitSales turnover X 100

Gross profit margin (%) =

42,00050,000 X 100

=84%Analysis For every baht (฿) make from sales, 84% is kept as gross profit

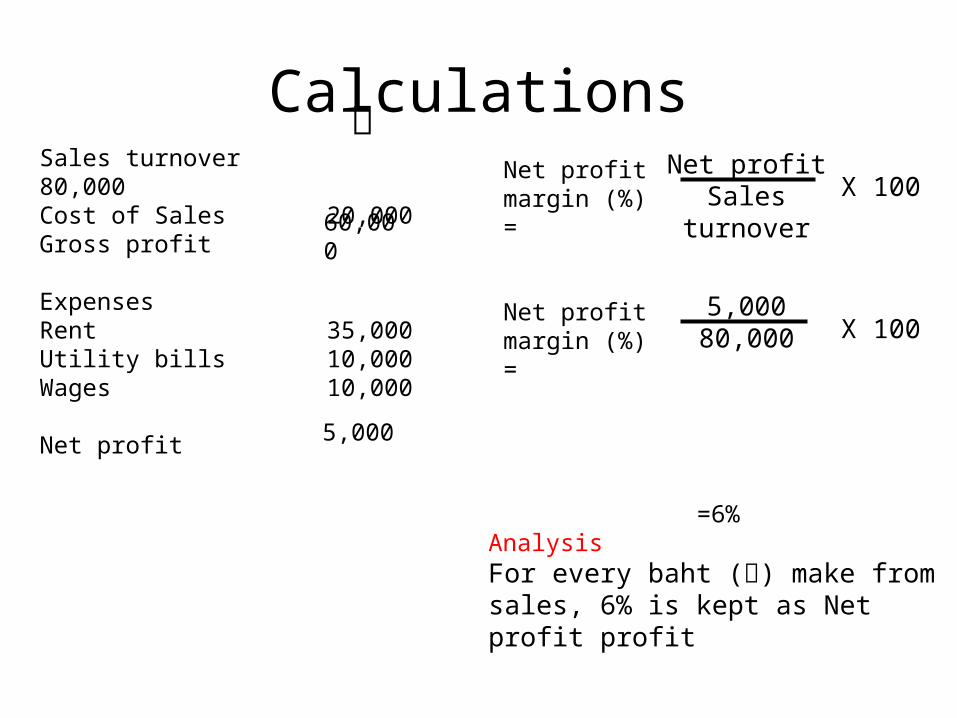

Net profit marginNet profit margin

Net profit margin (%) =

Net profit

Sales turnoverX 100

Shows how much Net profit is made for every $ earned

Calculations ฿Sales turnover 80,000Cost of Sales 20,000Gross profit

ExpensesRent 35,000Utility bills 10,000Wages 10,000

Net profit

60,000

5,000

Net profitmargin (%) =

Net profitSales turnover X 100

Net profitmargin (%) =

5,00080,000 X 100

=6%Analysis For every baht (฿) make from sales, 6% is kept as Net profit profit

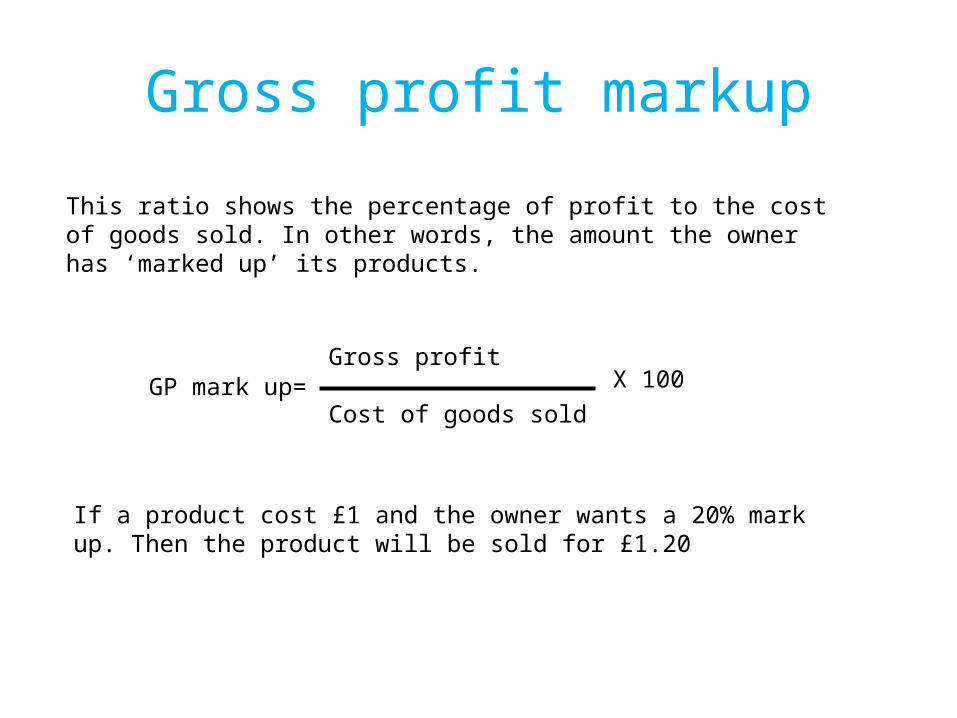

Gross profit markup

This ratio shows the percentage of profit to the cost of goods sold. In other words, the amount the owner has ‘marked up’ its products.

GP mark up= Gross profit

Cost of goods soldX 100

If a product cost £1 and the owner wants a 20% mark up. Then the product will be sold for £1.20

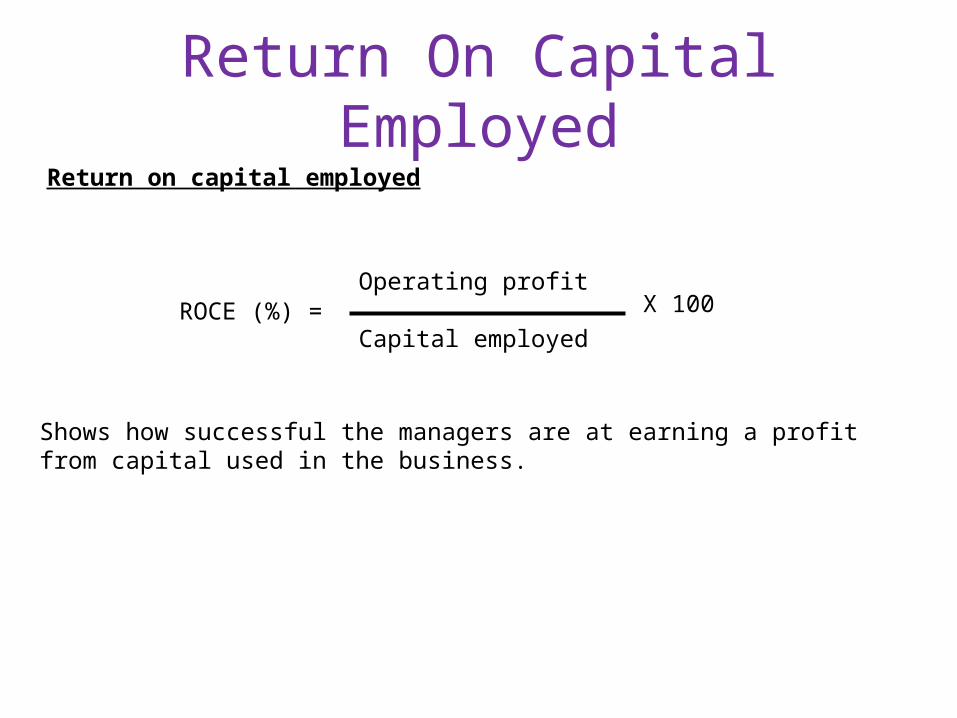

Return On Capital EmployedReturn on capital employed

ROCE (%) = Operating profit

Capital employedX 100

Shows how successful the managers are at earning a profit from capital used in the business.

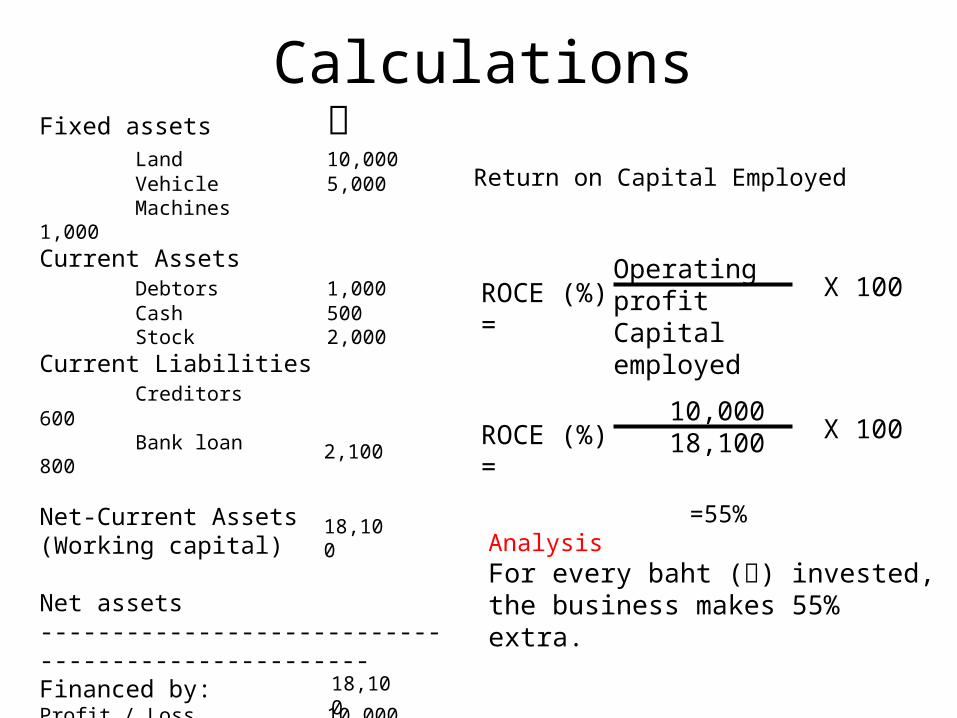

CalculationsFixed assets ฿

Land 10,000Vehicle 5,000Machines 1,000

Current AssetsDebtors 1,000Cash 500Stock 2,000

Current LiabilitiesCreditors 600Bank loan 800

Net-Current Assets(Working capital)

Net assets---------------------------------------------------Financed by:Profit / Loss 10,000Share capital 8,100

Capital employed

2,100

18,100

18,100

Return on Capital Employed

ROCE (%) = Operating profitCapital employed X 100

ROCE (%) = 10,00018,100 X 100

=55%Analysis For every baht (฿) invested, the business makes 55% extra.

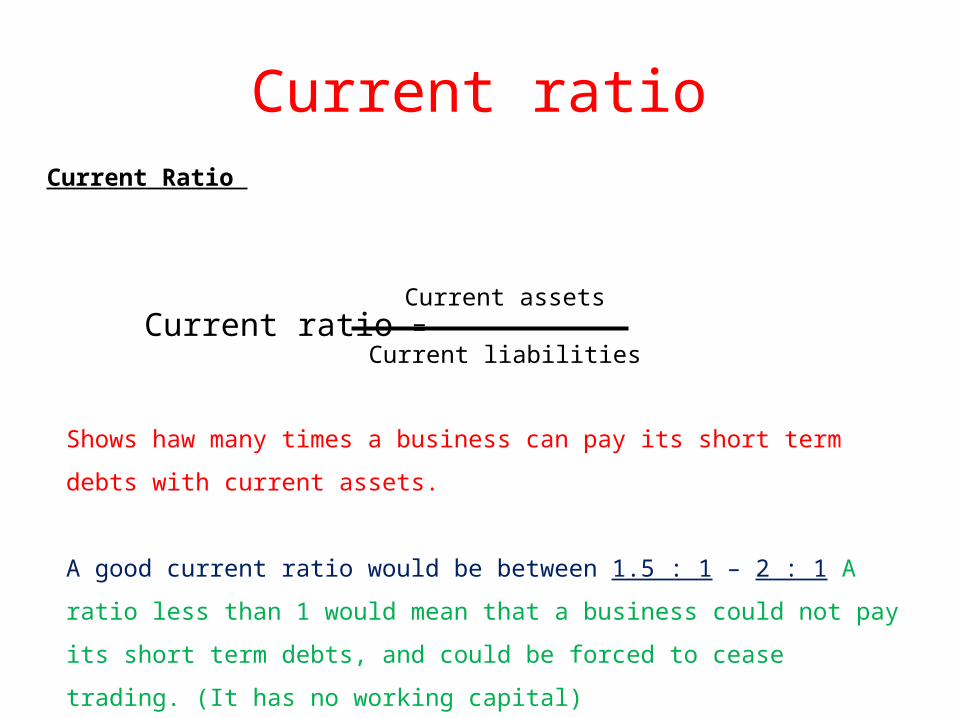

Current ratioCurrent Ratio

Current ratio = Current assets

Current liabilities

Shows haw many times a business can pay its short term debts with

current assets.

A good current ratio would be between 1.5 : 1 – 2 : 1 A ratio less

than 1 would mean that a business could not pay its short term

debts, and could be forced to cease trading. (It has no working

capital)

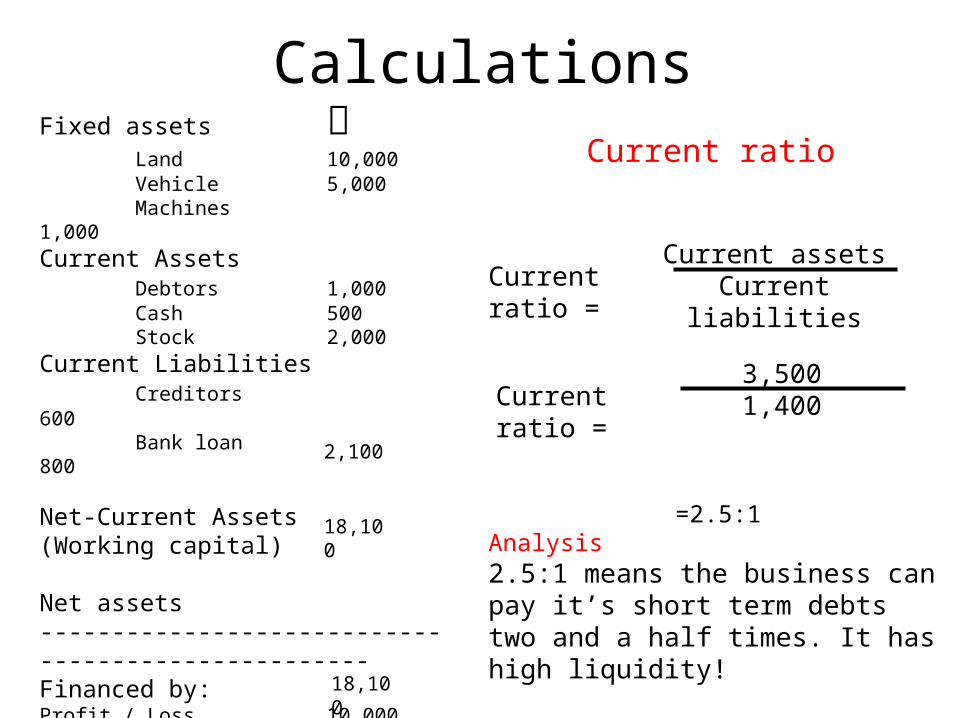

CalculationsFixed assets ฿

Land 10,000Vehicle 5,000Machines 1,000

Current AssetsDebtors 1,000Cash 500Stock 2,000

Current LiabilitiesCreditors 600Bank loan 800

Net-Current Assets(Working capital)

Net assets---------------------------------------------------Financed by:Profit / Loss 10,000Share capital 8,100

Capital employed

2,100

18,100

18,100

Current ratio

=2.5:1Analysis 2.5:1 means the business can pay it’s short term debts two and a half times. It has high liquidity!

Current ratio = Current assets

Current liabilities

Current ratio = 3,5001,400

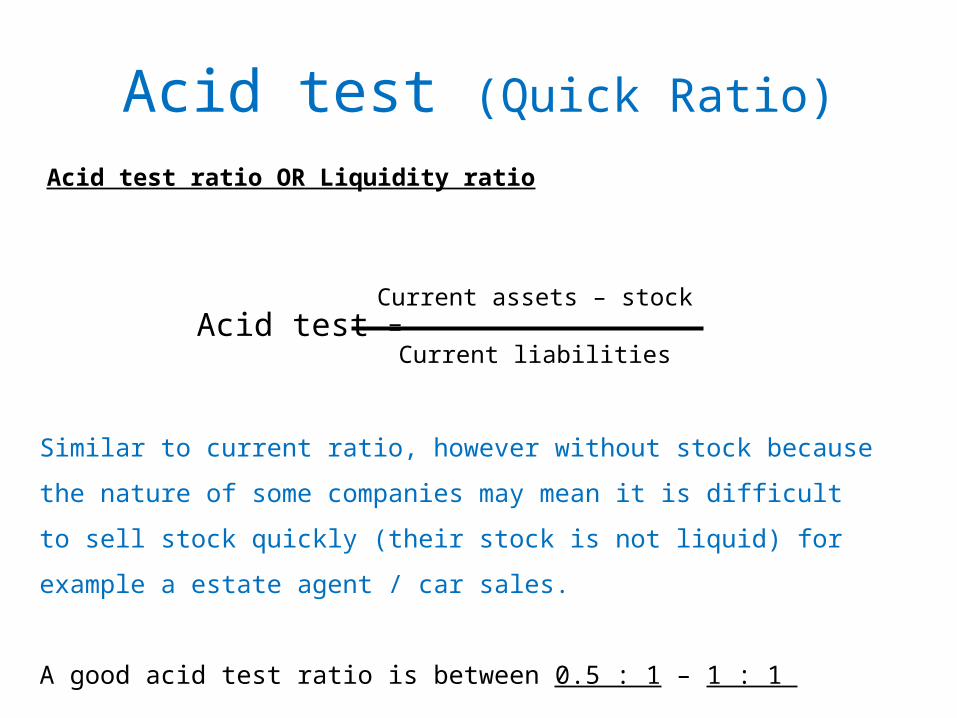

Acid test (Quick Ratio)

Acid test ratio OR Liquidity ratio

Acid test = Current assets – stock

Current liabilities

Similar to current ratio, however without stock because the

nature of some companies may mean it is difficult to sell stock

quickly (their stock is not liquid) for example a estate agent / car

sales.

A good acid test ratio is between 0.5 : 1 – 1 : 1

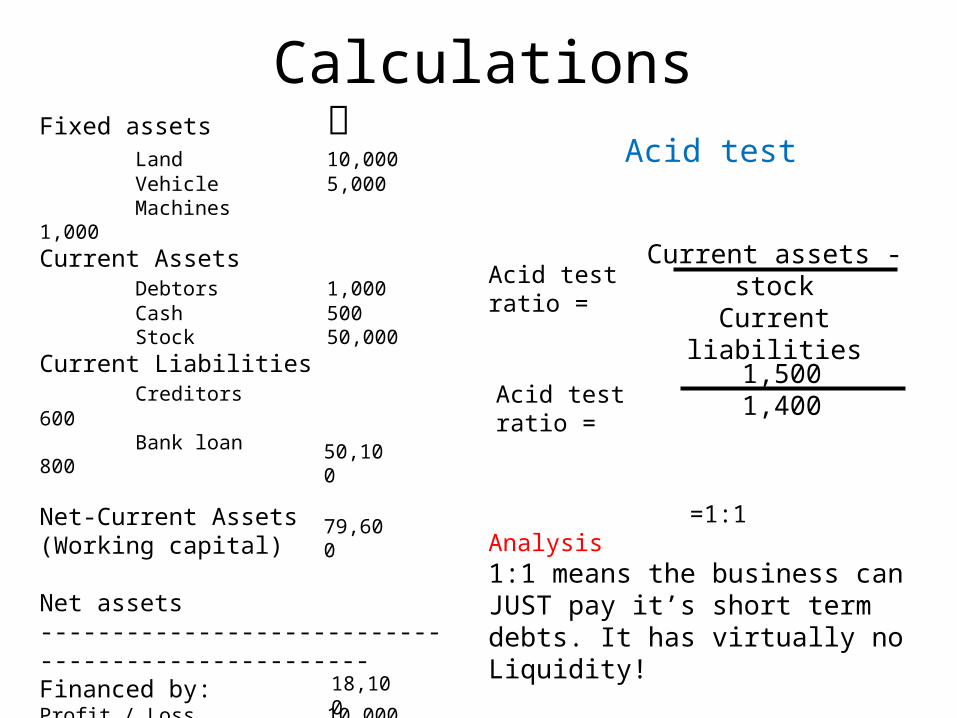

CalculationsFixed assets ฿

Land 10,000Vehicle 5,000Machines 1,000

Current AssetsDebtors 1,000Cash 500Stock 50,000

Current LiabilitiesCreditors 600Bank loan 800

Net-Current Assets(Working capital)

Net assets---------------------------------------------------Financed by:Profit / Loss 10,000Share capital 8,100

Capital employed

50,100

79,600

18,100

Acid test

=1:1Analysis 1:1 means the business can JUST pay it’s short term debts. It has virtually no Liquidity!

Acid test ratio = Current assets - stock

Current liabilities

Acid test ratio = 1,5001,400

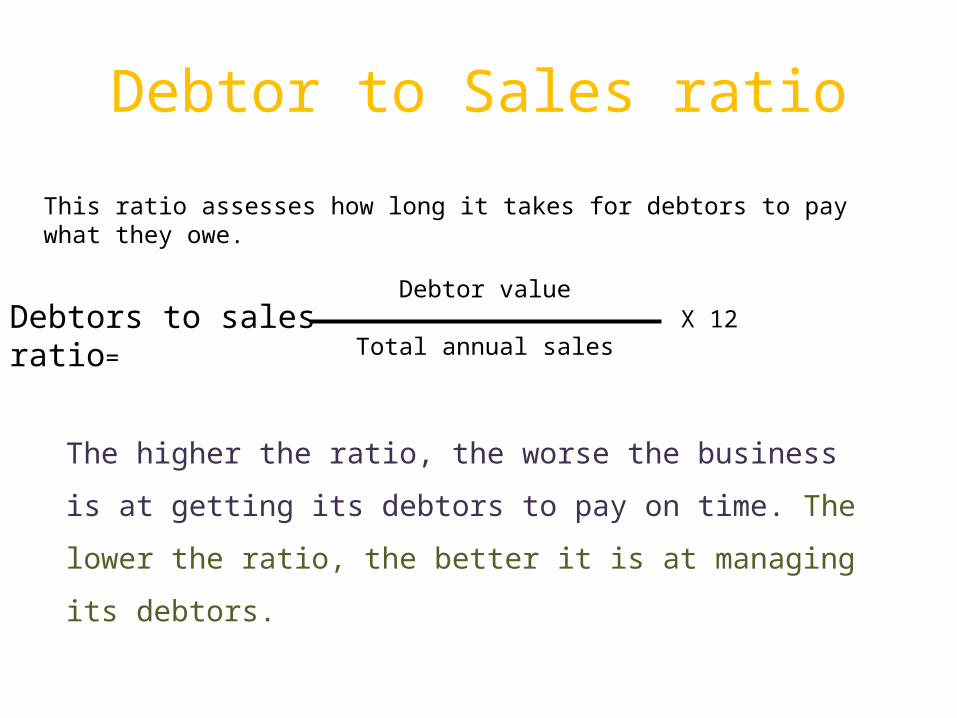

Debtor to Sales ratio

This ratio assesses how long it takes for debtors to pay what they owe.

Debtors to sales ratio= Debtor value

Total annual salesX 12

The higher the ratio, the worse the business is at

getting its debtors to pay on time. The lower the ratio,

the better it is at managing its debtors.

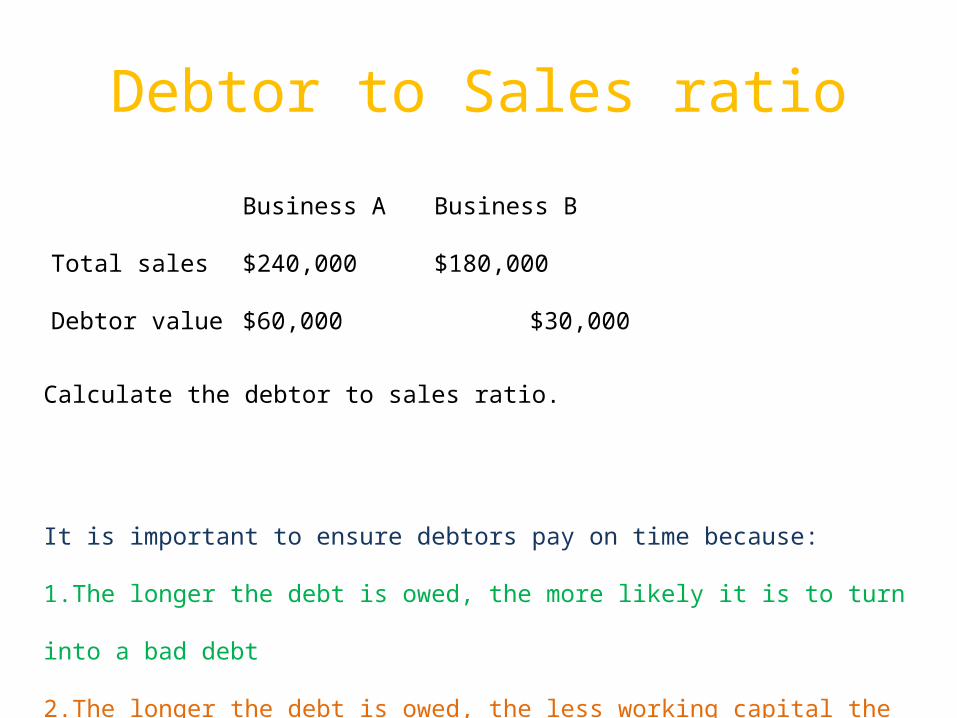

Debtor to Sales ratio

Business A Business B

Total sales $240,000 $180,000

Debtor value $60,000 $30,000

Calculate the debtor to sales ratio.

It is important to ensure debtors pay on time because:

1.The longer the debt is owed, the more likely it is to turn into a bad debt

2.The longer the debt is owed, the less working capital the business will

have

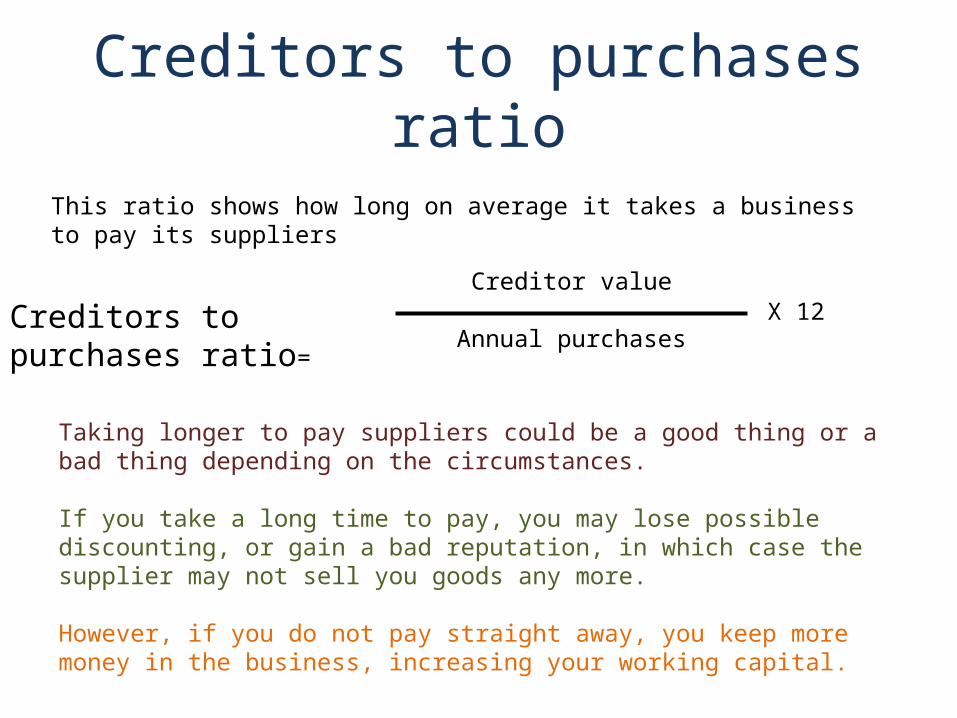

Creditors to purchases ratio

This ratio shows how long on average it takes a business to pay its suppliers

Creditors to purchases ratio=

Creditor value

Annual purchasesX 12

Taking longer to pay suppliers could be a good thing or a bad thing depending on the circumstances.

If you take a long time to pay, you may lose possible discounting, or gain a bad reputation, in which case the supplier may not sell you goods any more.

However, if you do not pay straight away, you keep more money in the business, increasing your working capital.

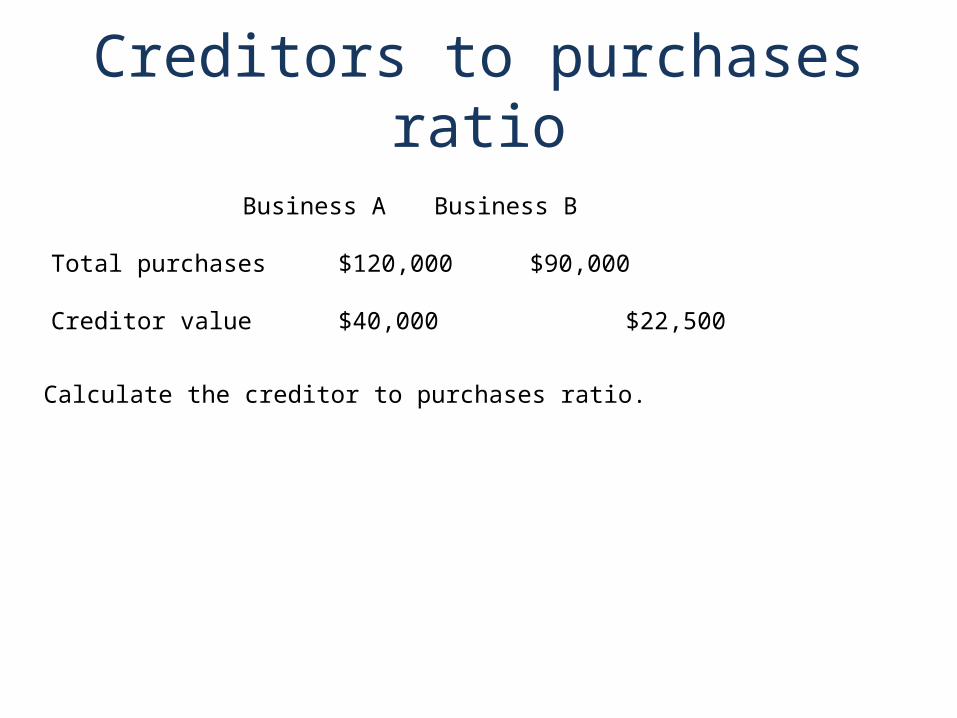

Business A Business B

Total purchases $120,000 $90,000

Creditor value $40,000 $22,500

Calculate the creditor to purchases ratio.

Creditors to purchases ratio

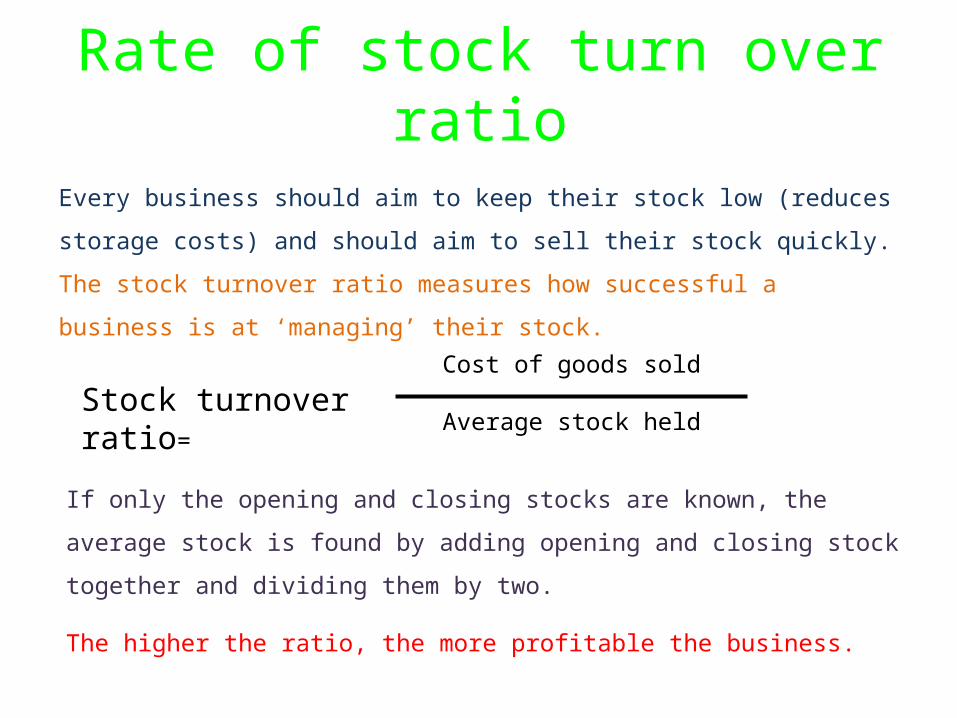

Rate of stock turn over ratio

Every business should aim to keep their stock low (reduces storage

costs) and should aim to sell their stock quickly. The stock turnover

ratio measures how successful a business is at ‘managing’ their

stock.

Stock turnover ratio=

Cost of goods sold

Average stock held

If only the opening and closing stocks are known, the average stock is

found by adding opening and closing stock together and dividing

them by two.

The higher the ratio, the more profitable the business.

Work sheet

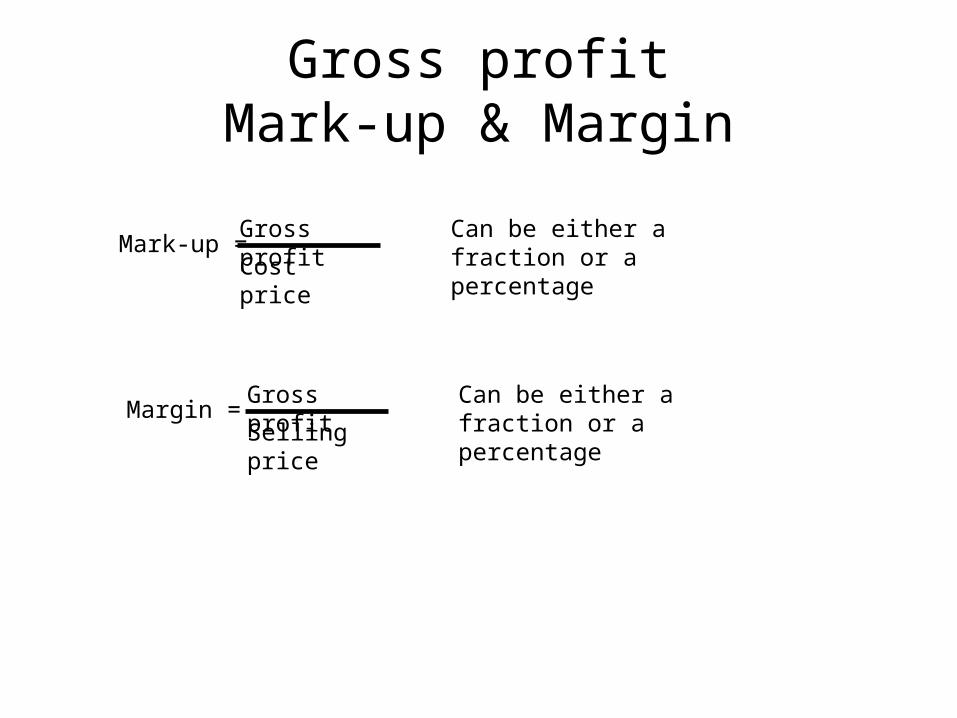

Gross profitMark-up & Margin

Mark-up = Gross profitCost price

Can be either a fraction or a percentage

Margin = Gross profitSelling price

Can be either a fraction or a percentage

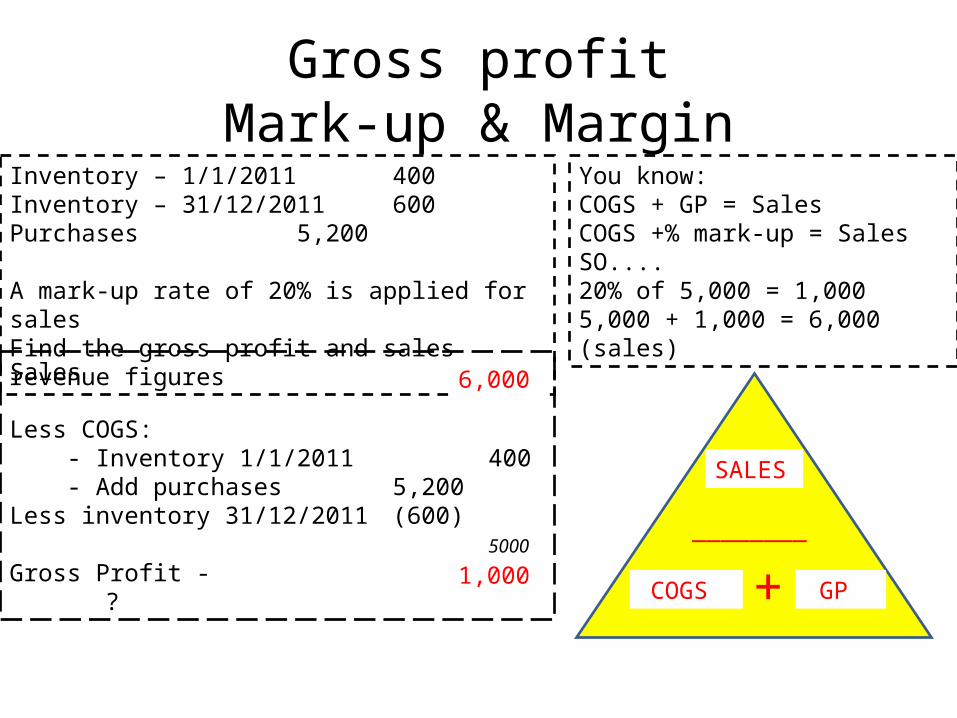

Gross profitMark-up & Margin

Inventory – 1/1/2011 400Inventory – 31/12/2011 600Purchases 5,200

A mark-up rate of 20% is applied for salesFind the gross profit and sales revenue figuresSales ?

Less COGS: - Inventory 1/1/2011 400 - Add purchases 5,200Less inventory 31/12/2011 (600)

5000

Gross Profit - ?

You know:COGS + GP = SalesCOGS +% mark-up = SalesSO....20% of 5,000 = 1,0005,000 + 1,000 = 6,000 (sales)

6,000

1,000

SALES

COGS GP

________

+

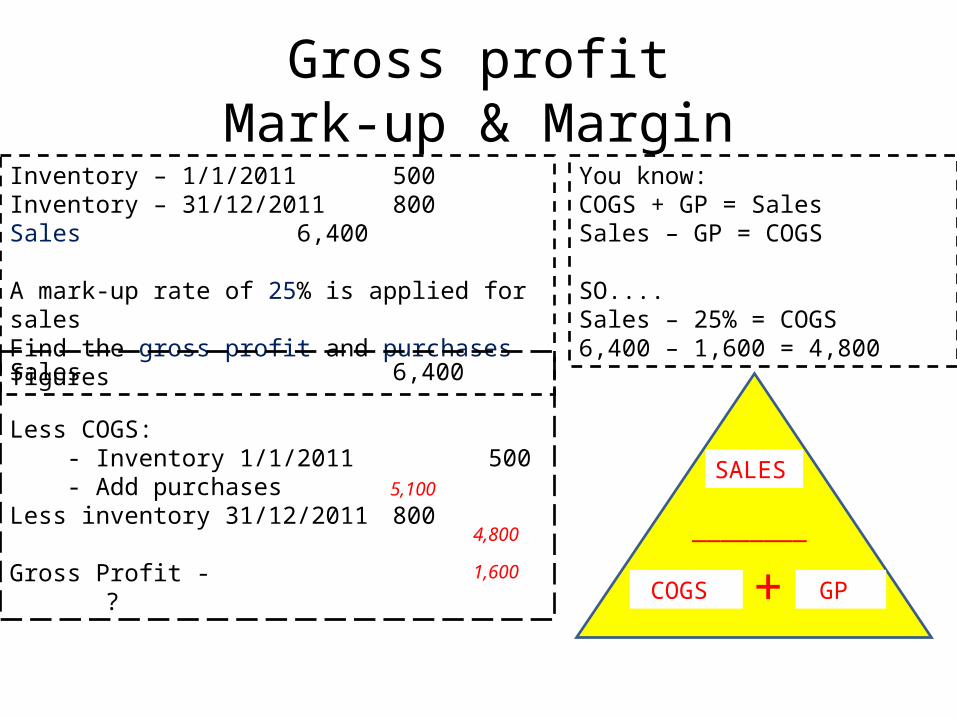

Gross profitMark-up & Margin

Inventory – 1/1/2011 500Inventory – 31/12/2011 800Sales 6,400

A mark-up rate of 25% is applied for salesFind the gross profit and purchases figures

Sales 6,400

Less COGS: - Inventory 1/1/2011 500 - Add purchases ?Less inventory 31/12/2011 800

Gross Profit - ?

You know:COGS + GP = SalesSales – GP = COGS

SO....Sales – 25% = COGS6,400 – 1,600 = 4,800

4,800

5,100

1,600

SALES

COGS GP

________

+

Gross profitMark-up & Margin

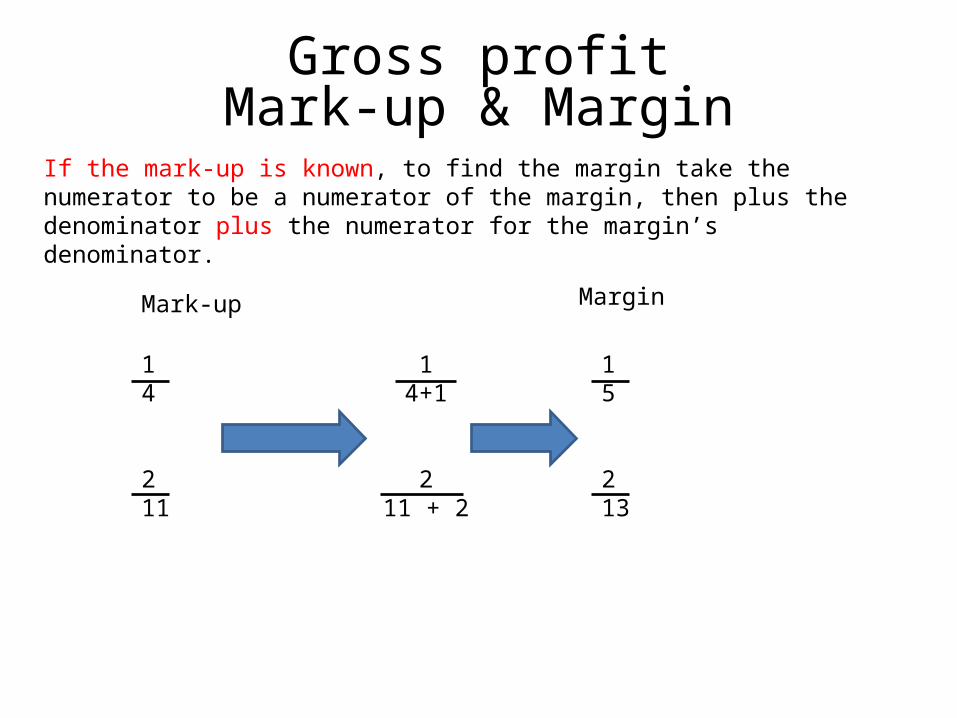

If the mark-up is known, to find the margin take the numerator to be a numerator of the margin, then plus the denominator plus the numerator for the margin’s denominator.

Mark-up Margin

14

211

14+1

211 + 2

15

213

Gross profitMark-up & Margin

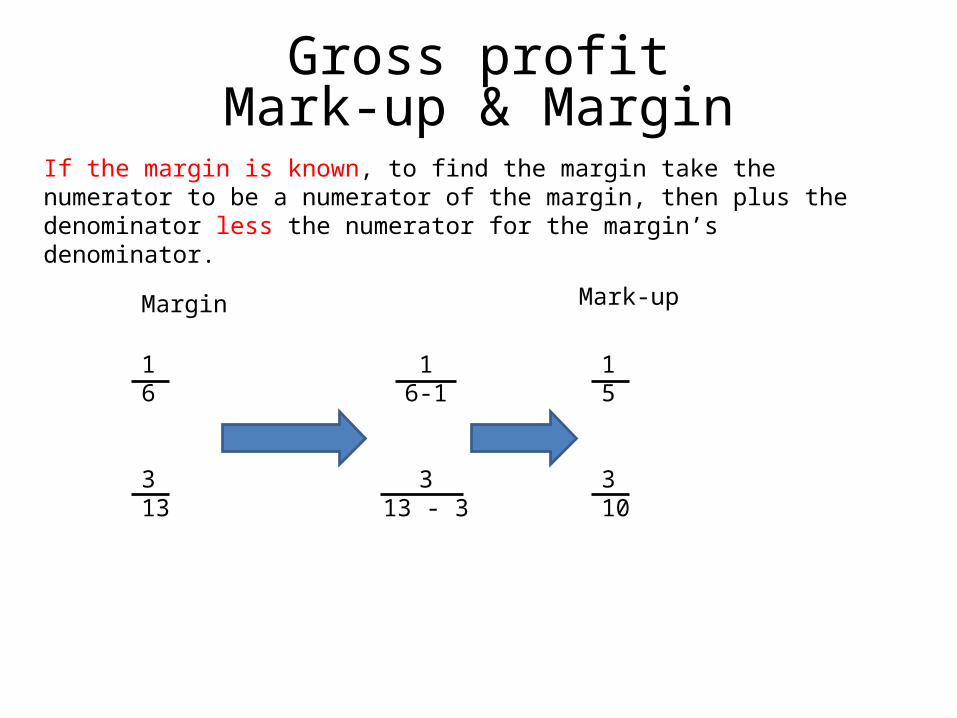

If the margin is known, to find the margin take the numerator to be a numerator of the margin, then plus the denominator less the numerator for the margin’s denominator.

Margin Mark-up

16

313

16-1

313 - 3

15

310

Gross profitMark-up & Margin

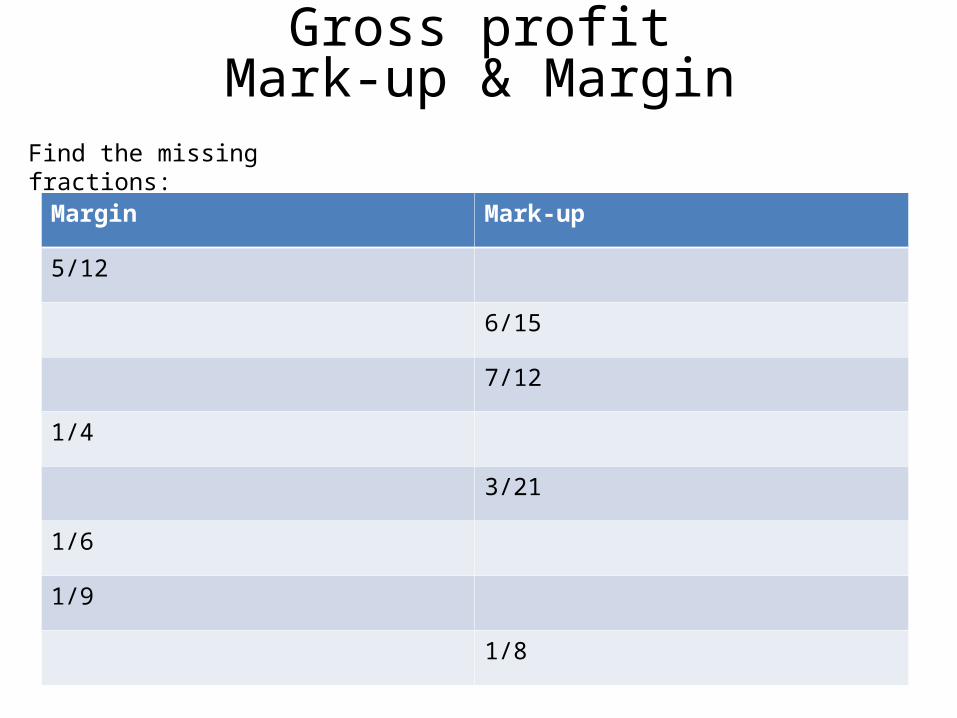

Find the missing fractions:

Margin Mark-up

5/12

6/15

7/12

1/4

3/21

1/6

1/9

1/8

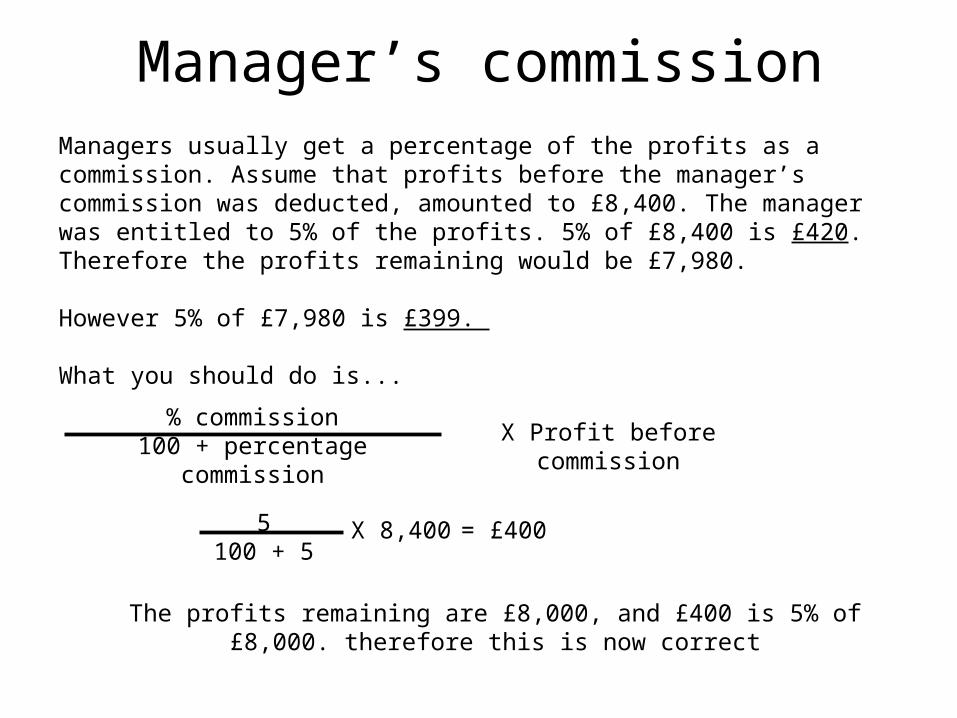

Manager’s commissionManagers usually get a percentage of the profits as a commission. Assume that profits before the manager’s commission was deducted, amounted to £8,400. The manager was entitled to 5% of the profits. 5% of £8,400 is £420. Therefore the profits remaining would be £7,980.

However 5% of £7,980 is £399.

What you should do is...

% commission100 + percentage commission X Profit before

commission

5100 + 5

X 8,400 = £400

The profits remaining are £8,000, and £400 is 5% of £8,000. therefore this is now correct