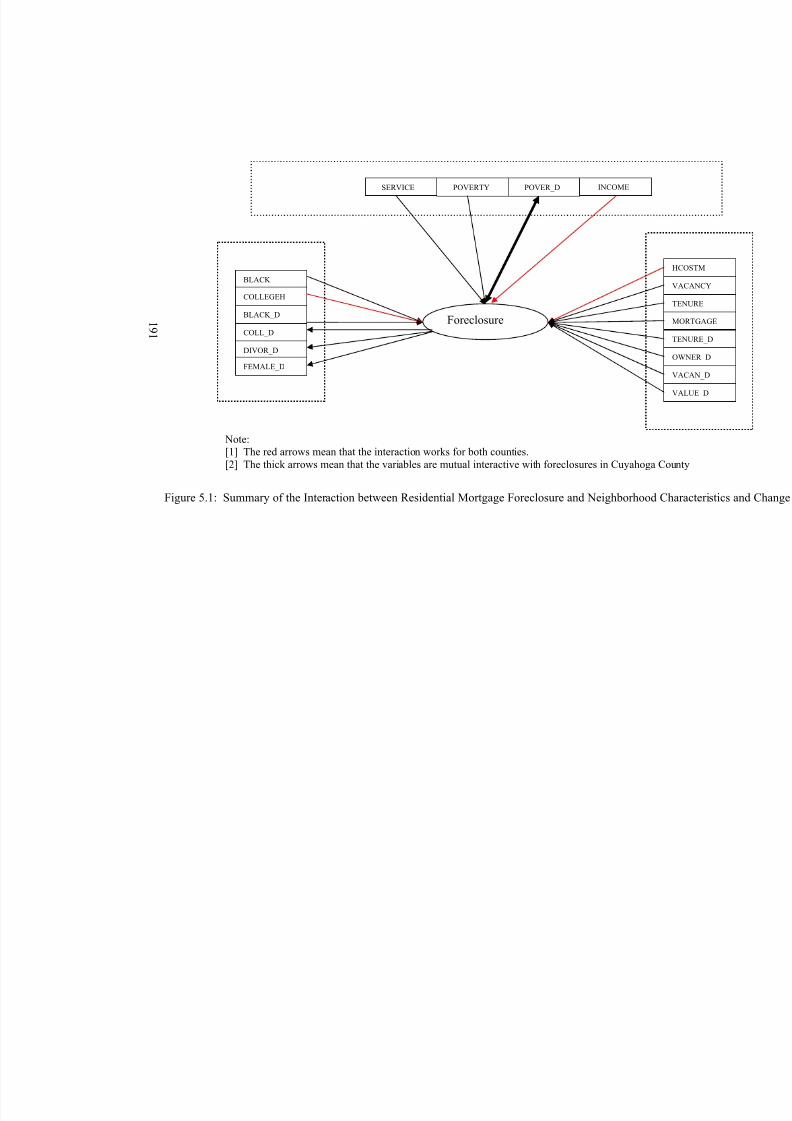

Spatial Lag Regression

268

THE DYNAMIC INTERACTION BETWEEN RESIDENTIAL MORTGAGE FORECLOSURE, NEIGHBORHOOD CHARACTERISTICS, AND NEIGHBORHOOD CHANGE DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Yanmei Li, M.A. ***** The Ohio State University 2006 Dissertation Committee: Professor Hazel Morrow-Jones, Adviser Professor Donald R. Haurin Professor Philip A. Viton Approved by Adviser Graduate Program in City and Regional Planning

Transcript of Spatial Lag Regression

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 1/268

THE DYNAMIC INTERACTION BETWEEN RESIDENTIALMORTGAGE FORECLOSURE, NEIGHBORHOOD

CHARACTERISTICS, AND NEIGHBORHOOD CHANGE

DISSERTATION

Presented in Partial Fulfillment of the Requirements for

the Degree Doctor of Philosophy in the Graduate

School of The Ohio State University

By

Yanmei Li, M.A.

*****

The Ohio State University

2006

Dissertation Committee:

Professor Hazel Morrow-Jones, Adviser

Professor Donald R. Haurin

Professor Philip A. Viton

Approved by

AdviserGraduate Program in City and Regional

Planning

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 2/268

Copyright by

Yanmei Li

2006

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 3/268

ii

ABSTRACT

Many factors lead to mortgage default and foreclosure, and neighborhood

characteristics are among the most important (Quercia and Stegman, 1992). However,

few scholars have examined how neighborhood characteristics contribute to mortgage

foreclosure (Cotterman, 2001; Baxter and Lauria, 2000; Lauria, 1998) and none of the

previous studies have systematically addressed the mutual interaction between

foreclosure and neighborhood characteristics and change. This research uses multiple

datasets from Ohio’s two most populous counties to examine some of these previously

omitted or understudied aspects of the issue. Particular attention has been paid to each

neighborhood’s racial composition, economic level, housing prices and other housing

stock characteristics as well as to the changes over time in those variables.

The analysis starts with simple descriptive statistics, spatial autocorrelation analysis,

and comparison of different foreclosure patterns in the two counties. Then spatial

regression models, H-Robust models and Iterated Seemingly Unrelated Regression

(ITSUR) are used to explain the interaction between mortgage foreclosure and

neighborhood characteristics and change. The study finds that foreclosures cluster in low-

income minority neighborhoods and inner cities, although suburban areas have seen an

increase. Educational attainment, median household income, and average housing cost

burden contribute to foreclosures in both counties. As expected there are similarities and

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 4/268

iii

disparities in the interaction of foreclosure and neighborhoods between the two counties.

The use of panel data, Robust OLS, spatial lag models and SUR has solved some

problems related to spatial dependence, heteroskedasticity and mutual non-recursive

interaction between foreclosure and neighborhoods.

The research not only contributes to the literate and methodology in related topics,

but also contributes to our understanding of the relationship between foreclosure and

neighborhoods, and will assist in the creation of better policies to deal with the issue of

foreclosure. The policy recommendations include a strong focus on neighborhood

foreclosure prevention, not just policies aimed at individual homeowners. These policies

might focus on neighborhoods with low educational attainment, an increasing percentage

black population, or a high female headship rate. This project suggests that foreclosure

prevention programs not be the same in all places.

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 5/268

iv

Dedicated to my father and mother

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 6/268

v

ACKNOWLEDGMENTS

I wish to thank my adviser, Professor Hazel Morrow-Jones, for her intellectual

support, encouragement, and enthusiasm that made this dissertation possible, and for her

patience in correcting my English, stylistic and scientific errors.

I thank Professor Jean M. Guldmann, Professor Phillip Viton, and Professor Donald

Haurin for their guidance which made the methodology more appealing.

I am grateful to Charlie Post from the Housing Research Center at Cleveland State

University to provide Cuyahoga County’s parcel data.

I wish to thank Katrin Anacker and Fang-Chi Hsu for their continuous

encouragement. I am indebted to Joe Gakenheimer for his support and suggestions in

writing and preparing this manuscript. I thank Eileen Frey, Cheryl Kaufman, and Donna

Fasnacht for their continuous prayers and love.

This research was supported by a grant from the Center for Urban and Regional

Analysis (CURA) at the Ohio State University. The financial support from the grant has

made this dissertation possible.

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 7/268

vi

VITA

December 25, 1975 ..……..…………...Born - Qujing, China

1998 ……………………….…………..B.S. Geography, East China Normal University,Shanghai, China

2001 …………………………………M.A. Regional Economics, Beijing Normal

University, Beijing, China

2001 – present ………………………Graduate Research Associate, The Ohio StateUniversity

PUBLICATIONS

1. Wu, Dianting, Yanmei Li, et. al. 2002. The Development of Intellectual Economy inChina. Economic Geography (Chinese). Vol. 22, No. 4

2. Wu, Dianting, Jie Tian, Yanmei Li, et. al. 2002. The Analysis of the Relationships

between Modernization, Industrialization, Urbanization, Intellectualization andEconomic Development in China. Systems Engineering – Theory and Practice

(Chinese). Vol.22. No. 11.3. Li, Yanmei, Dianting Wu, and Gang Zeng, 1999. The Characteristics and

Development Strategies of Hi-tech in Changjiang Delta, Areal Research and

Development (Chinese), Vol.18, No.34. Wu, Dianting, Shen Ji, and Yanmei Li. 1998. Dividing One Integrated Part to Three

Sections in Geographic Thoughts, Youth Geographer(Chinese), Vol.9, No.4

FIELDS OF STUDY

Major Field: City and Regional Planning

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 8/268

vii

TABLE OF CONTENTS

ABSTRACT ............................................................................................................. ii

ACKNOWLEDGMENTS................................................................................................ vVITA ................................................................................................................ vi

LIST OF TABLES........................................................................................................... ix

LIST OF FIGURES......................................................................................................... xi

CHAPTER 1 INTRODUCTION AND RESEARCH QUESTIONS......................... 1

Nature of the Problem..................................................................................................... 2Objective of the Research ............................................................................................... 3Research Questions......................................................................................................... 4Scope of the Research..................................................................................................... 6

CHAPTER 2 LITERATURE REVIEW...................................................................... 8Residential Mortgage Foreclosure .................................................................................. 8The Interaction between Neighborhood Characteristics, Neighborhood Change andResidential Mortgage Foreclosure ................................................................................ 31Major Problems in Neighborhood-Effects Research .................................................... 46Literature Summary and the Derivation of Research Questions .................................. 50

CHAPTER 3 RESEARCH METHODOLOGY........................................................ 52Hypotheses.................................................................................................................... 52Major Datasets Used in Foreclosure Research ............................................................. 56Summary of Datasets Used in this Research ................................................................ 62Variable Selection and Description .............................................................................. 64Research Methodology ................................................................................................. 73

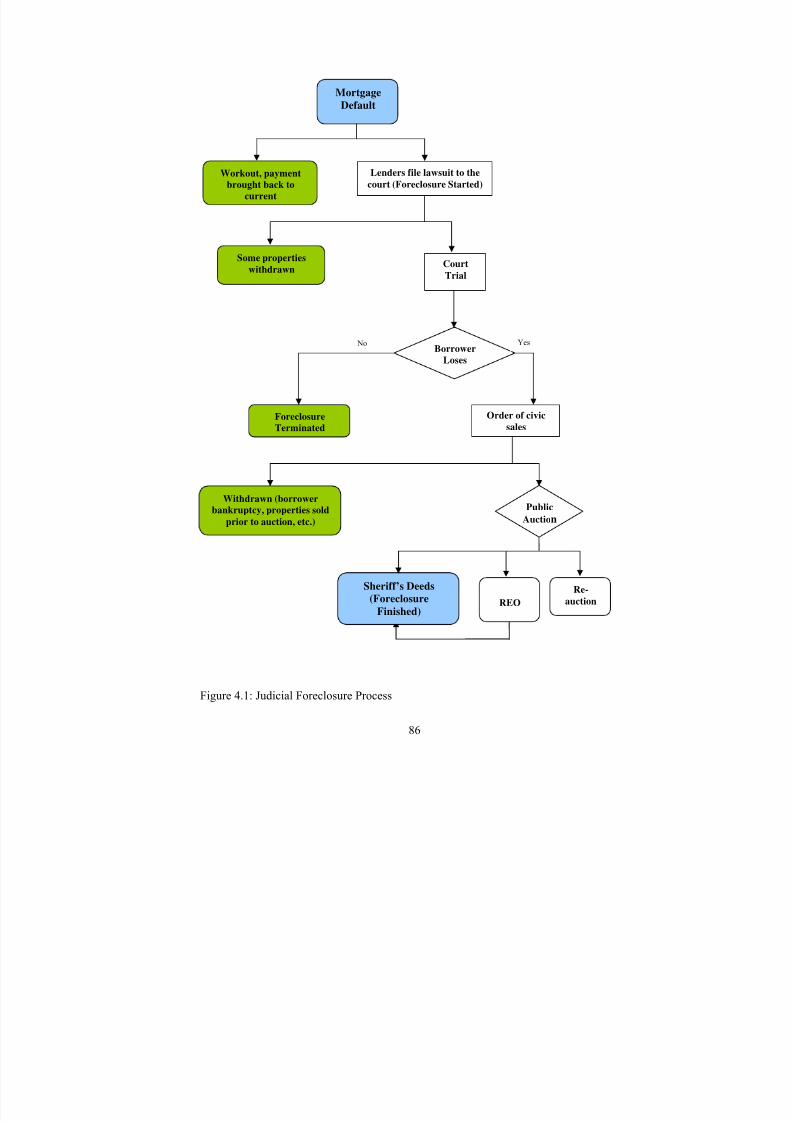

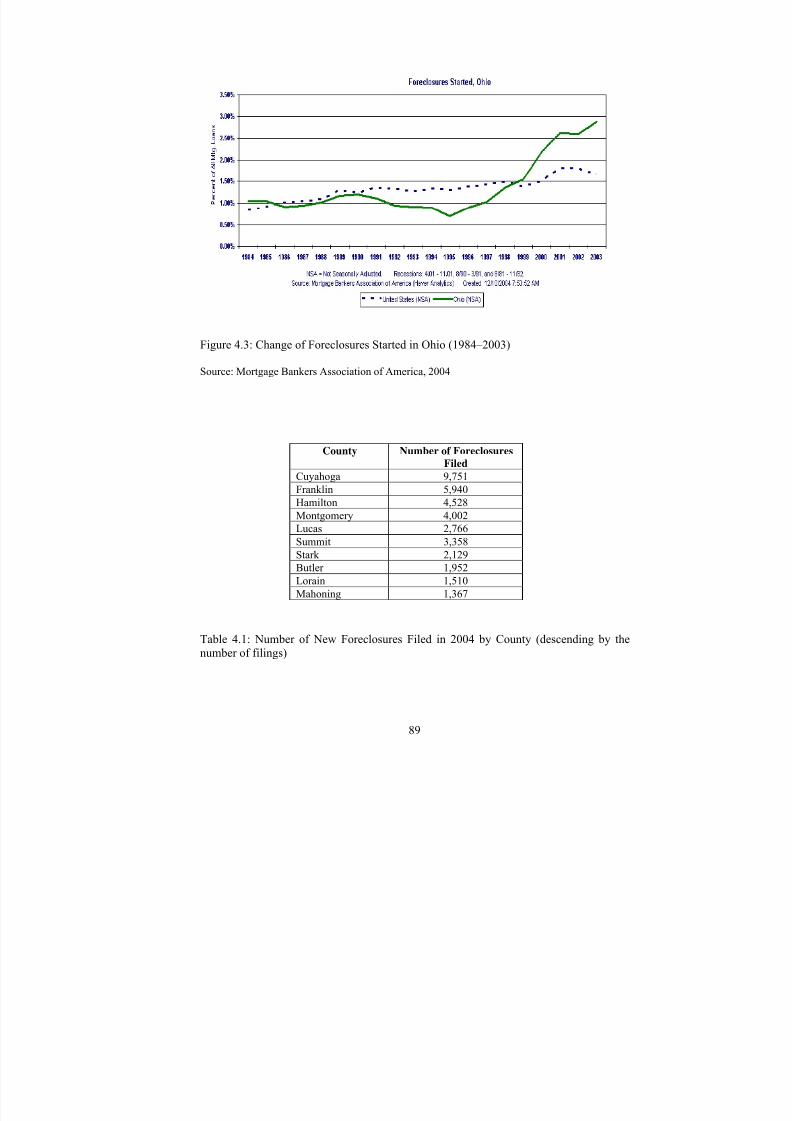

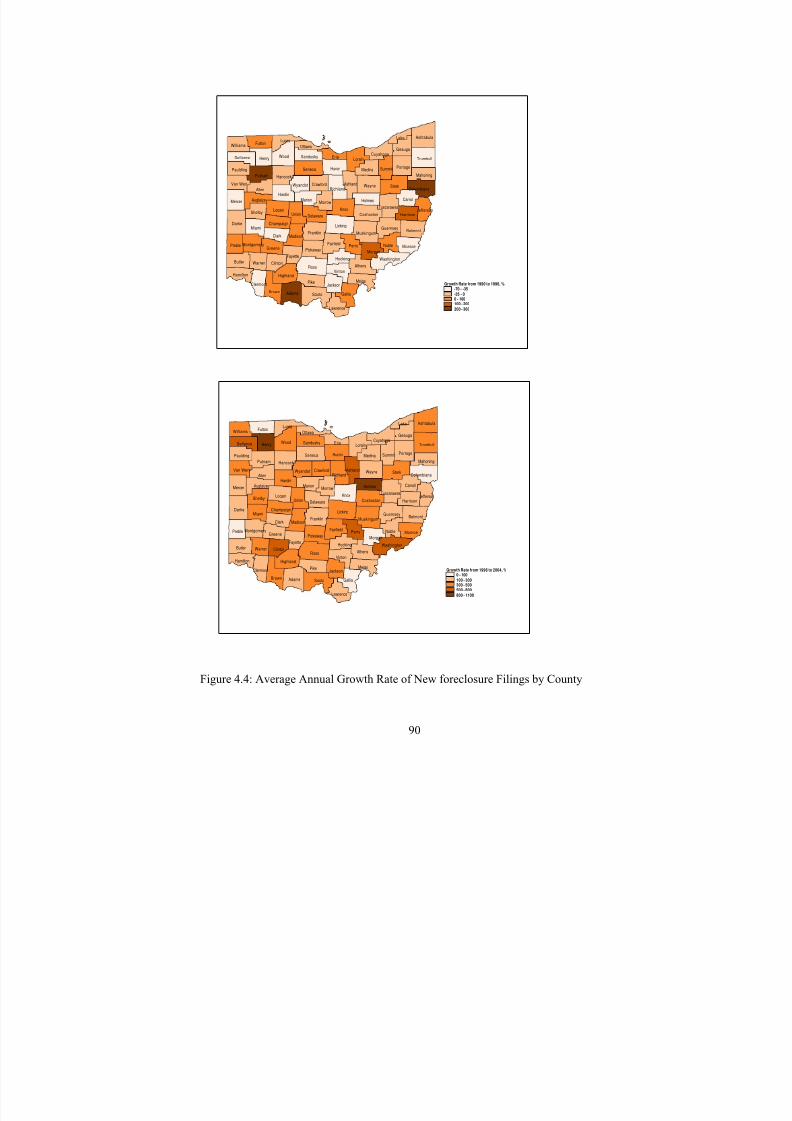

CHAPTER 4 DESCRIPTIVE AND SPATIAL ANALYSIS .................................. 84Judicial Foreclosure Process and Sheriff’s Deed Transfer Data................................... 84Ohio’s Foreclosure Situation ........................................................................................ 87

Research Area and Geographic Definition of Neighborhood....................................... 91Data Description for Each County................................................................................ 99Conclusions................................................................................................................. 139

CHAPTER 5 THE INTERACTION BETWEEN RESIDENTIAL MORTGAGE

FORECLOSURE, NEIGHBORHOOD CHARACTERISTICS,

AND NEIGHBORHOOD CHANGE.............................................. 141Effects of Neighborhoods on Foreclosure .................................................................. 145

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 9/268

viii

Summary: Effects of Neighborhood Characteristics on Residential MortgageForeclosure.................................................................................................................. 167The Impact of Residential Mortgage Foreclosure on Neighborhood Change: ASeemingly Unrelated Regression (SUR) Approach.................................................... 173Conclusion: The Interaction between Residential Mortgage Foreclosure, Neighborhood

Characteristics, and Neighborhood Change................................................................ 188

CHAPTER 6 CONCLUSIONS, POLICY IMPLICATIONS AND FUTURE

RESEARCH DIRECTIONS............................................................ 192

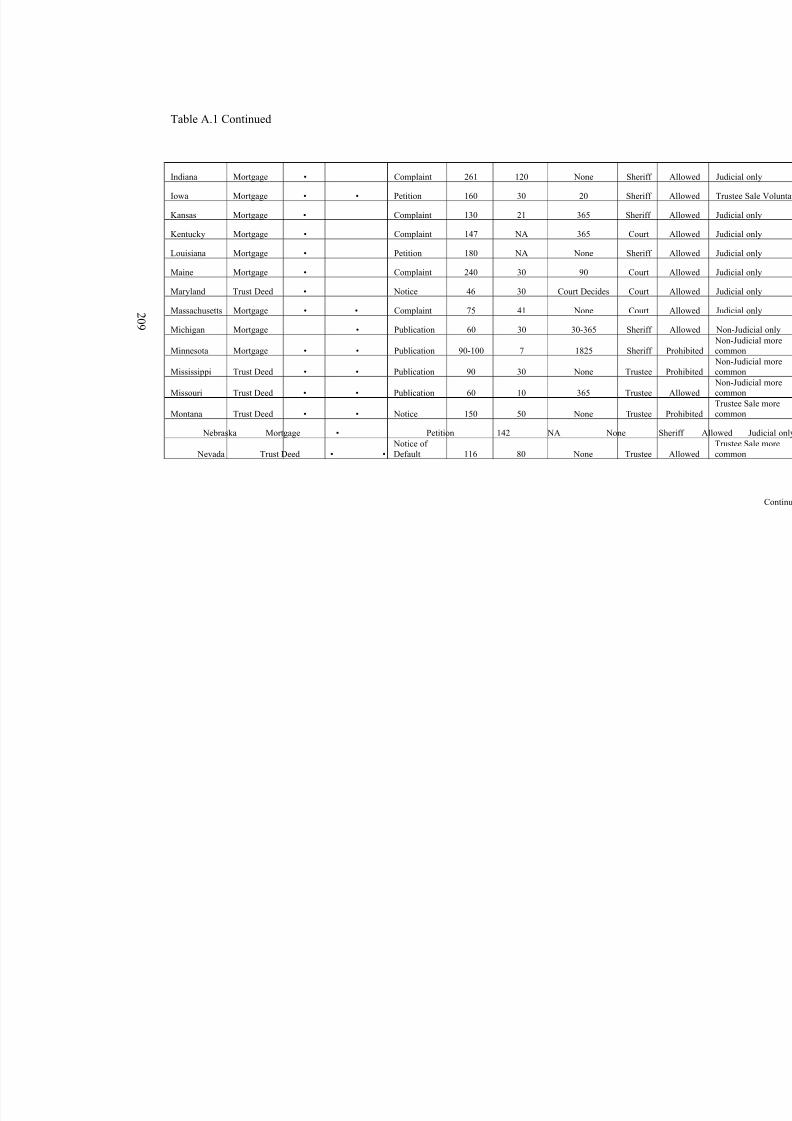

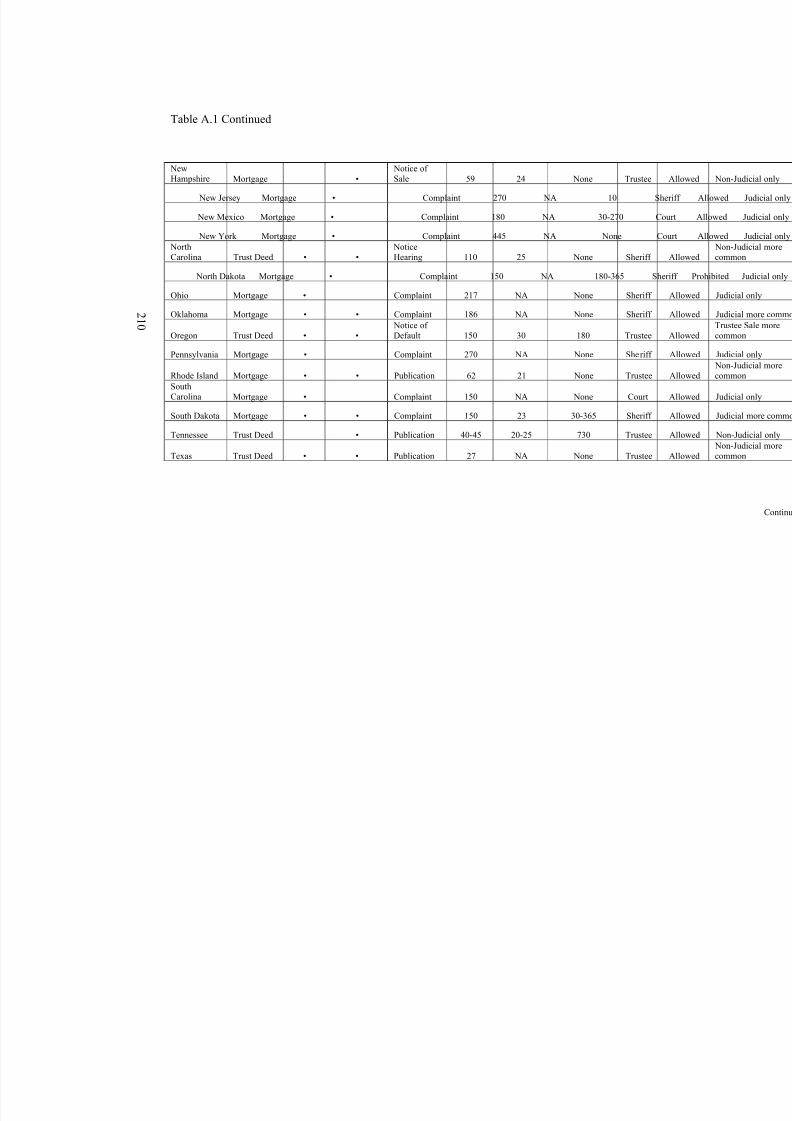

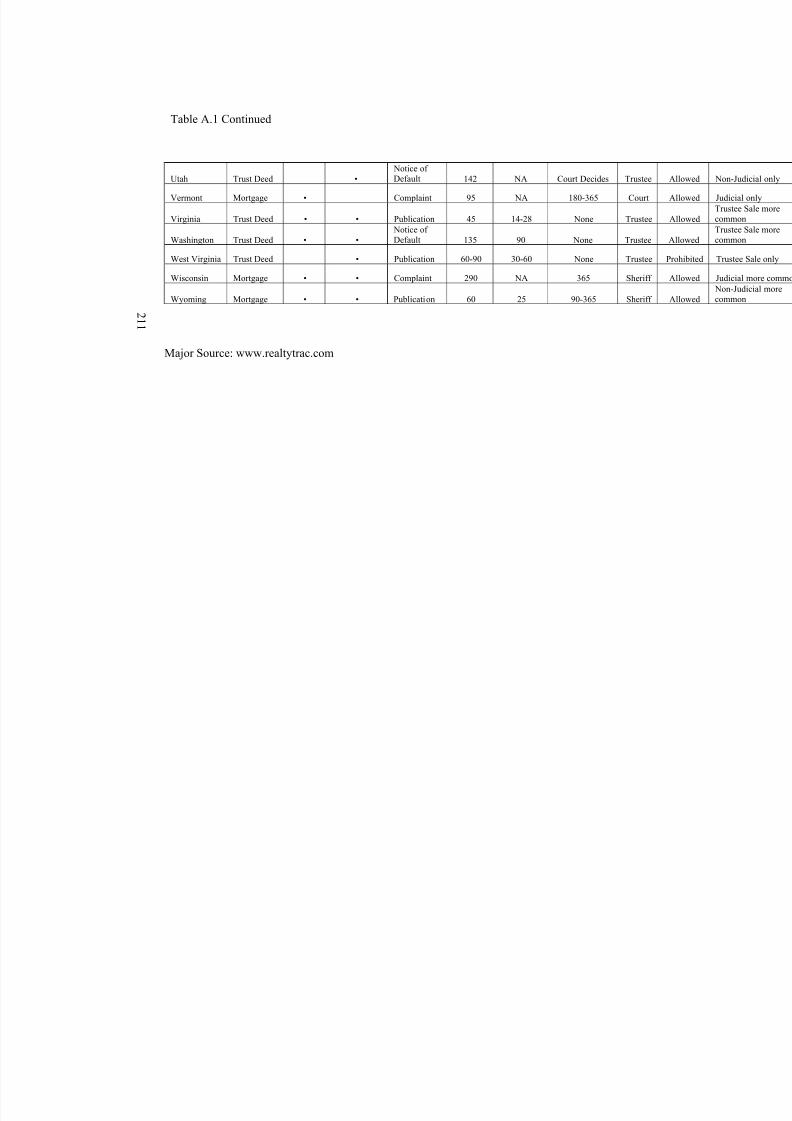

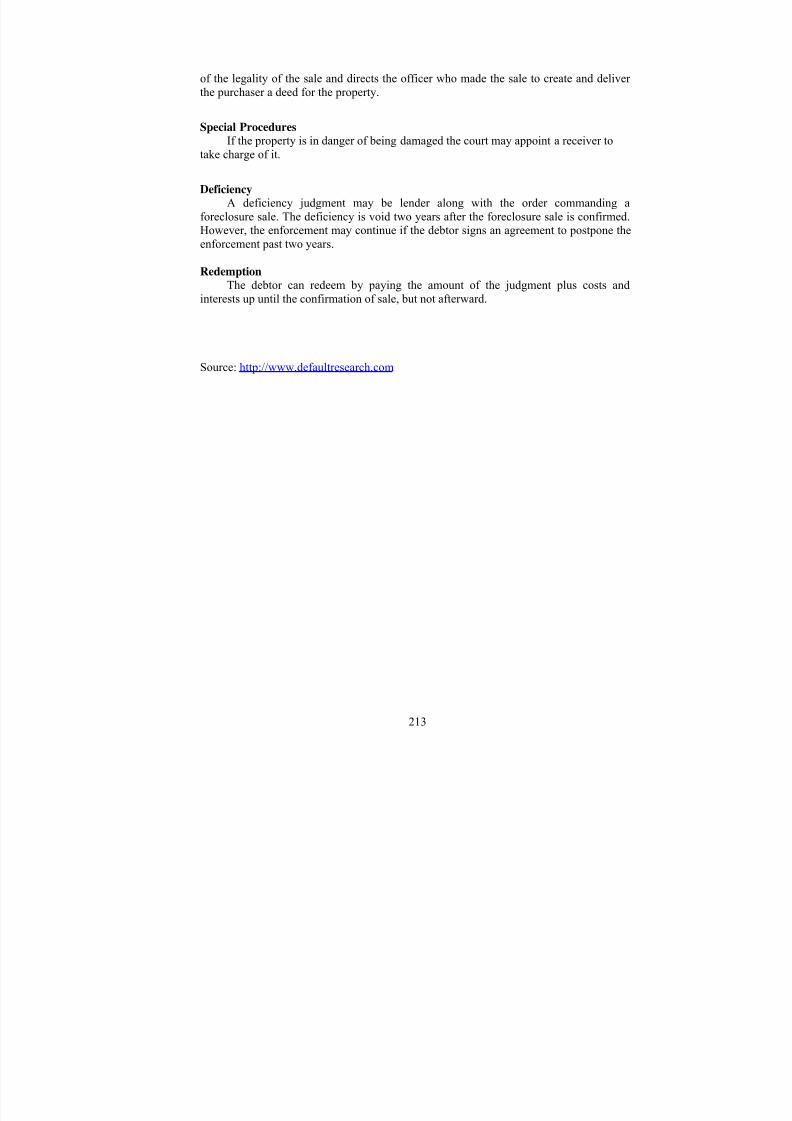

APPENDIX A FORECLOSURE PROCEDURES ................................................. 207

APPENDIX B TOTAL SHERIFF’S DEEDS AT THE SCHOOL DISTRICTLEVEL IN FRANKLIN COUNTY................................................. 214

APPENDIX C SPATIAL AUTOCORRELATION OF SELECTED VARIABLES

............................................................................................................. 216

APPENDIX D SUR MODEL RESULTS................................................................. 229

APPENDIX E THE GEOGRAPHIC DISTRIBUTION OF SELECTED

NEIGHBORHOOD CHANGE INDICATORS AT THE BLOCK

GROUP LEVEL IN FRANKLIN AND CUYAHOGA COUNTIES............................................................................................................. 233

BIBLIOGRAPHY…………………………………………………………….……….239

NOTES ……………………………………………………………………………….252

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 10/268

ix

LIST OF TABLES

Table 3.1: List of Selected Variables................................................................................ 70

Table 4.1: Number of New Foreclosures Filed in 2004 by County (descending by thenumber of filings) ..................................................................................................... 89

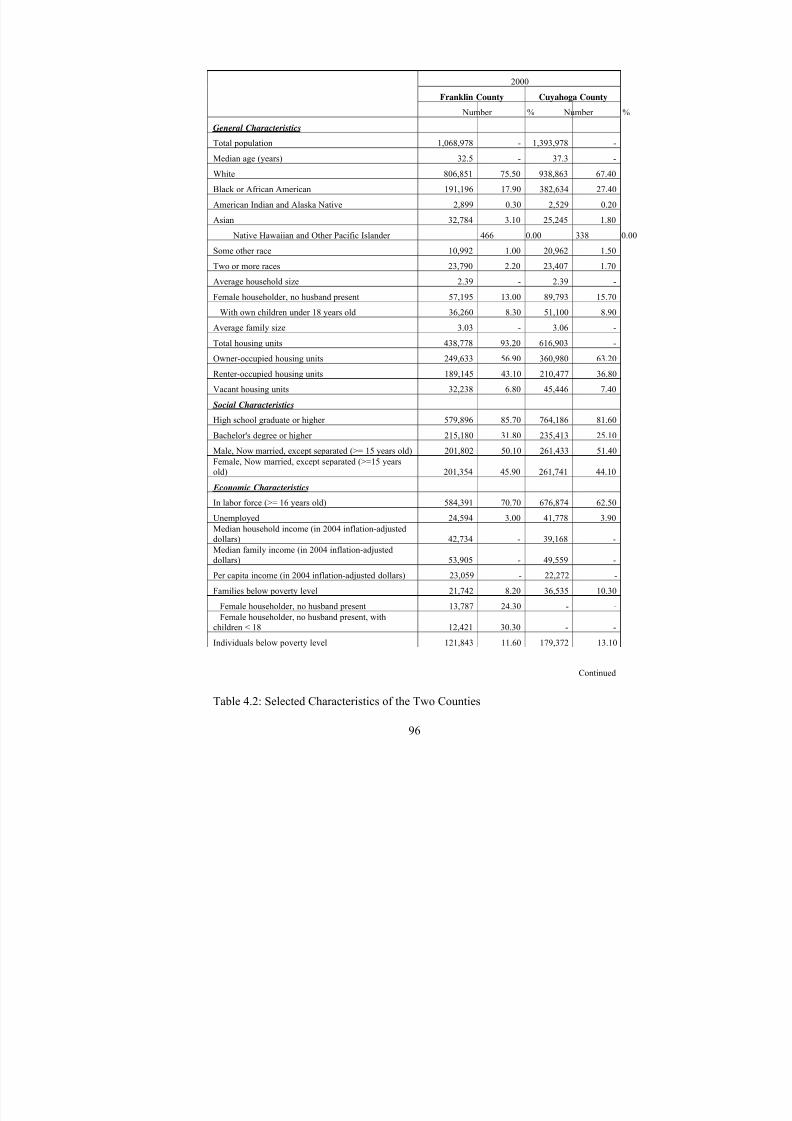

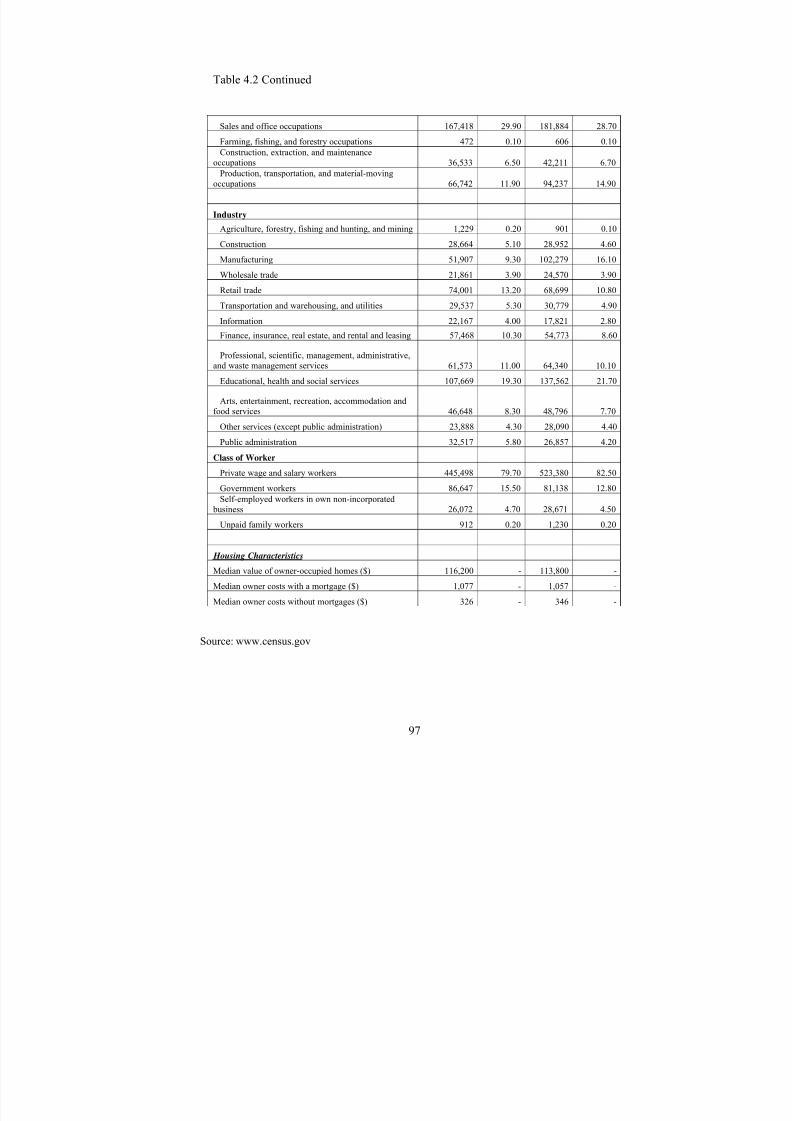

Table 4.2: Selected Characteristics of the Two Counties ................................................. 96

Table 4.3: New Foreclosure Filings, Terminated Foreclosure Cases and Sheriff’s Deeds(1997–2004, Franklin County).................................................................................. 99

Table 4.4: The Total Single-family Sheriff’s Deeds (1997–2004, Franklin County)..... 100

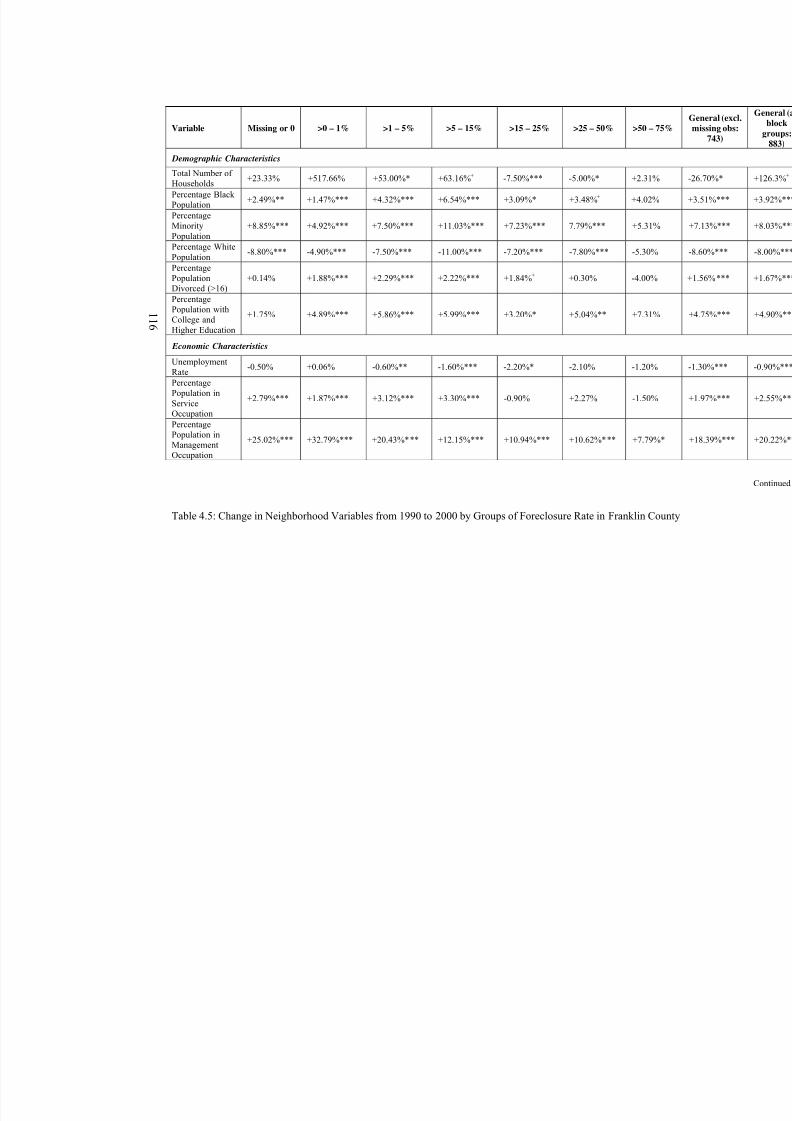

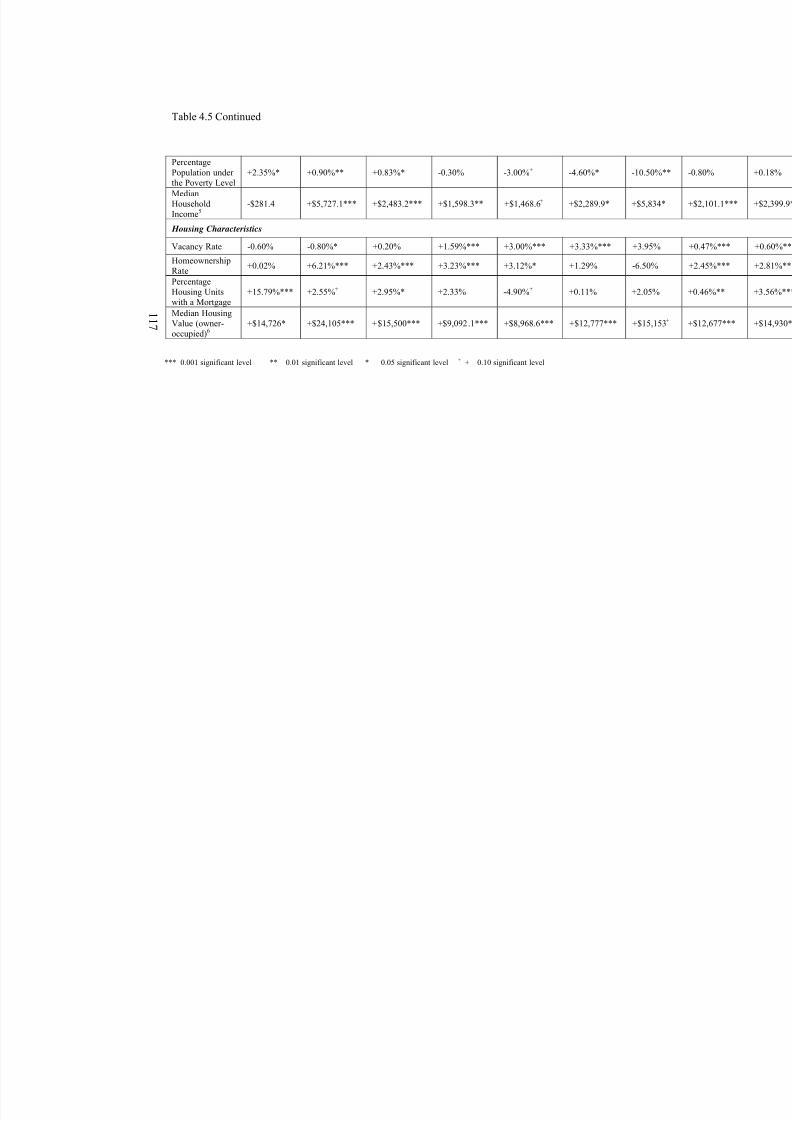

Table 4.5: Change in Neighborhood Variables from 1990 to 2000 by Groups of Foreclosure Rate in Franklin County...................................................................... 116

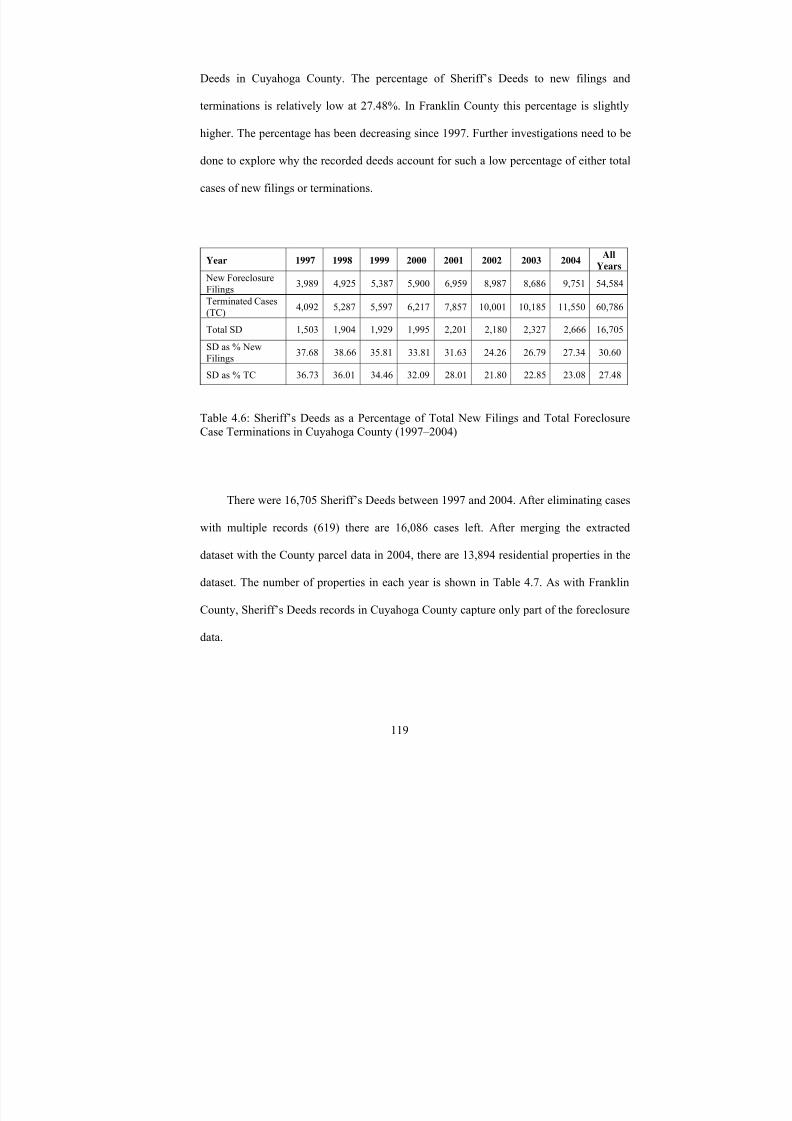

Table 4.6: Sheriff’s Deeds as a Percentage of Total New Filings and Total ForeclosureCase Terminations in Cuyahoga County (1997–2004)........................................... 119

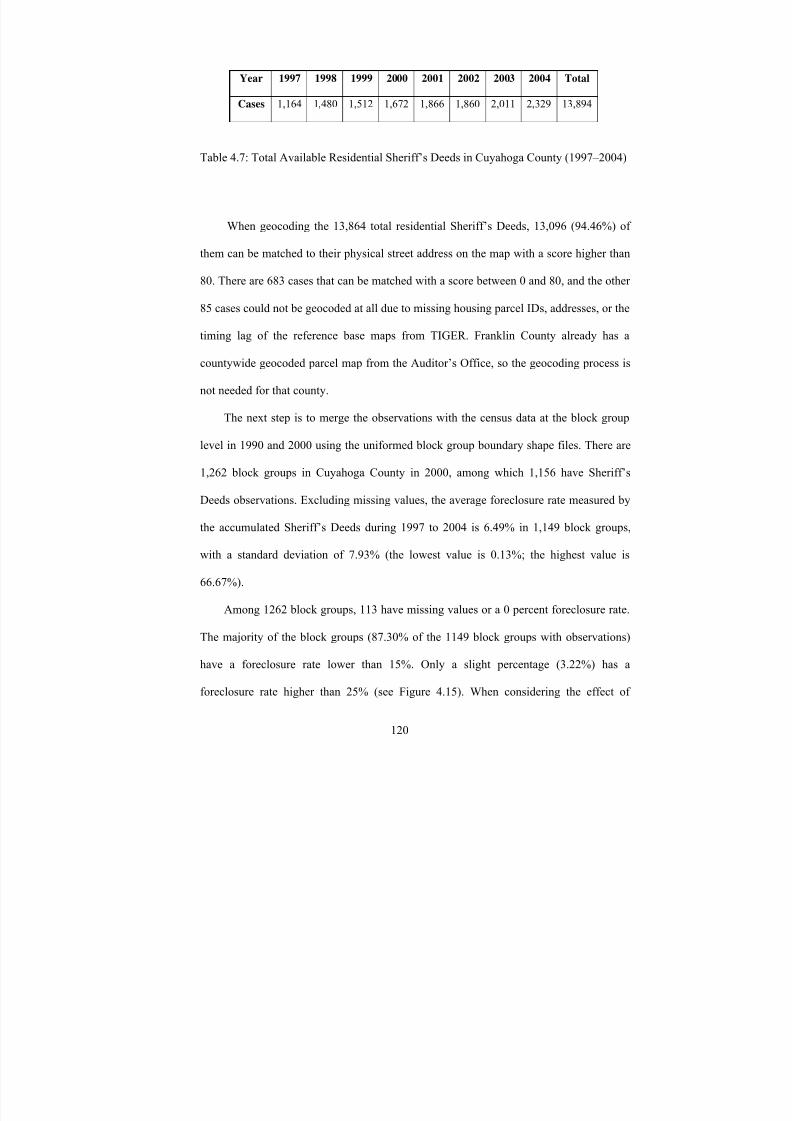

Table 4.7: Total Available Residential Sheriff’s Deeds in Cuyahoga County (1997–2004)................................................................................................................................. 120

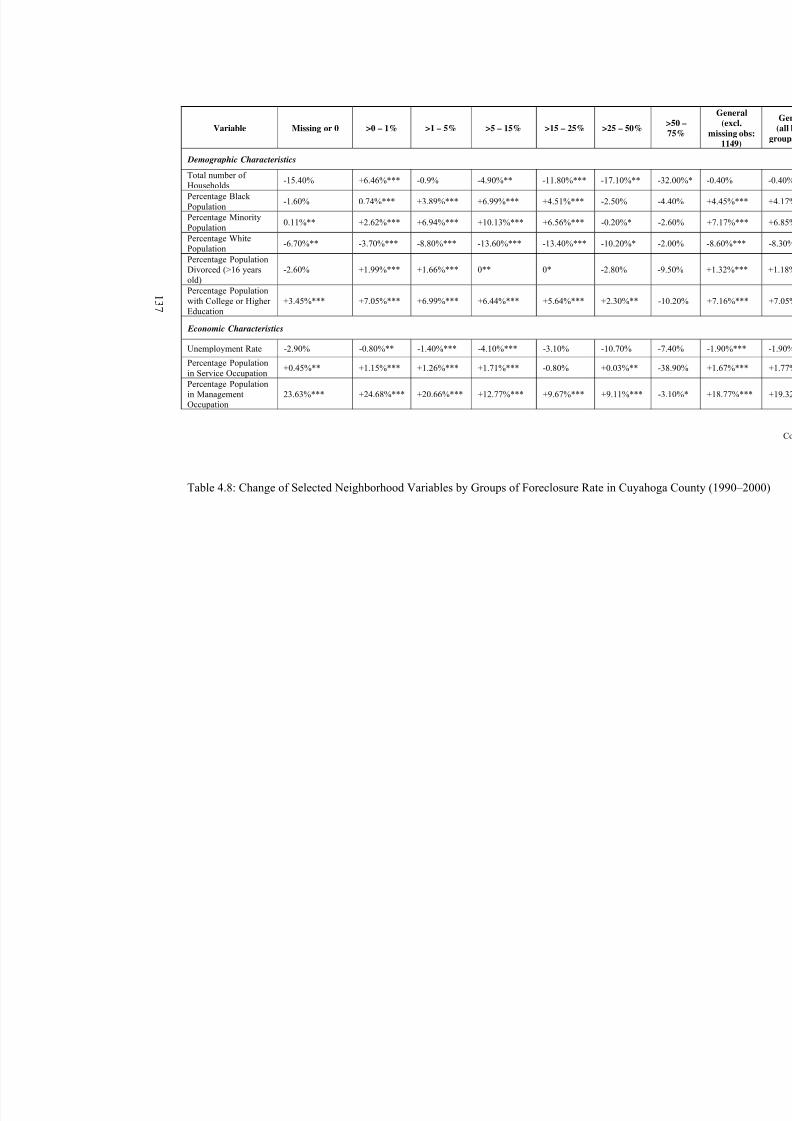

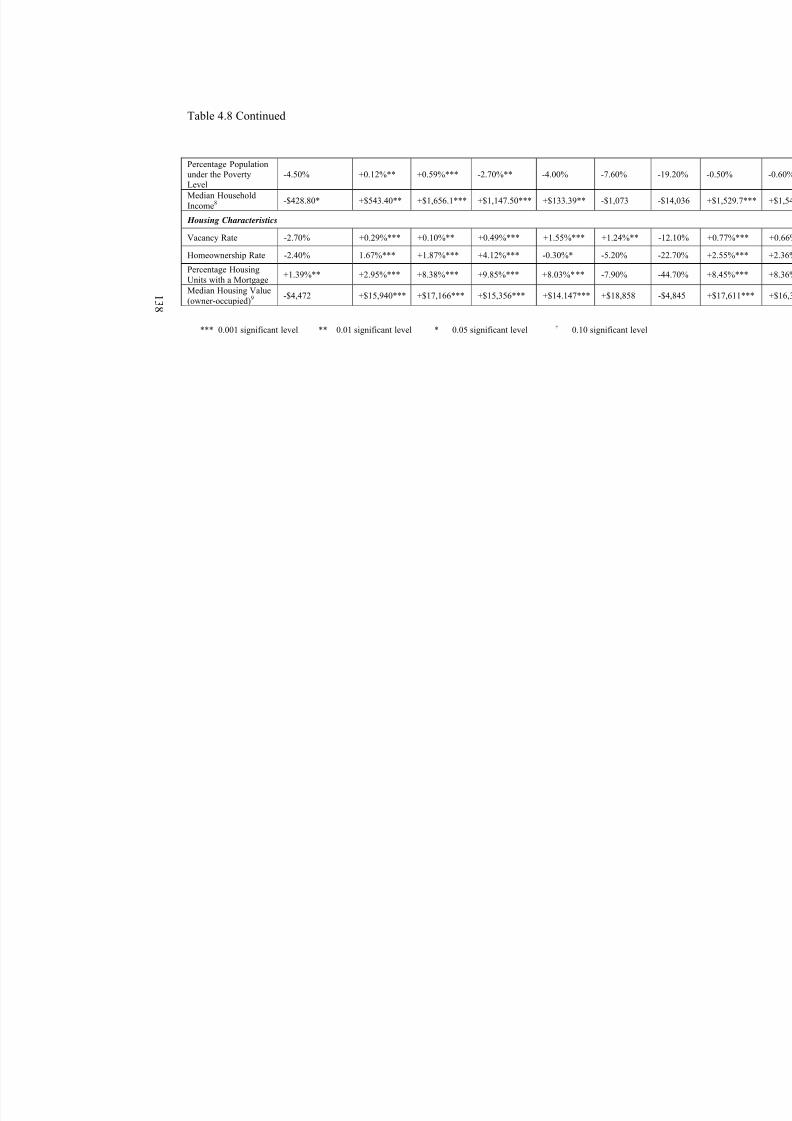

Table 4.8: Change of Selected Neighborhood Variables by Groups of Foreclosure Rate inCuyahoga County (1990–2000) .............................................................................. 137

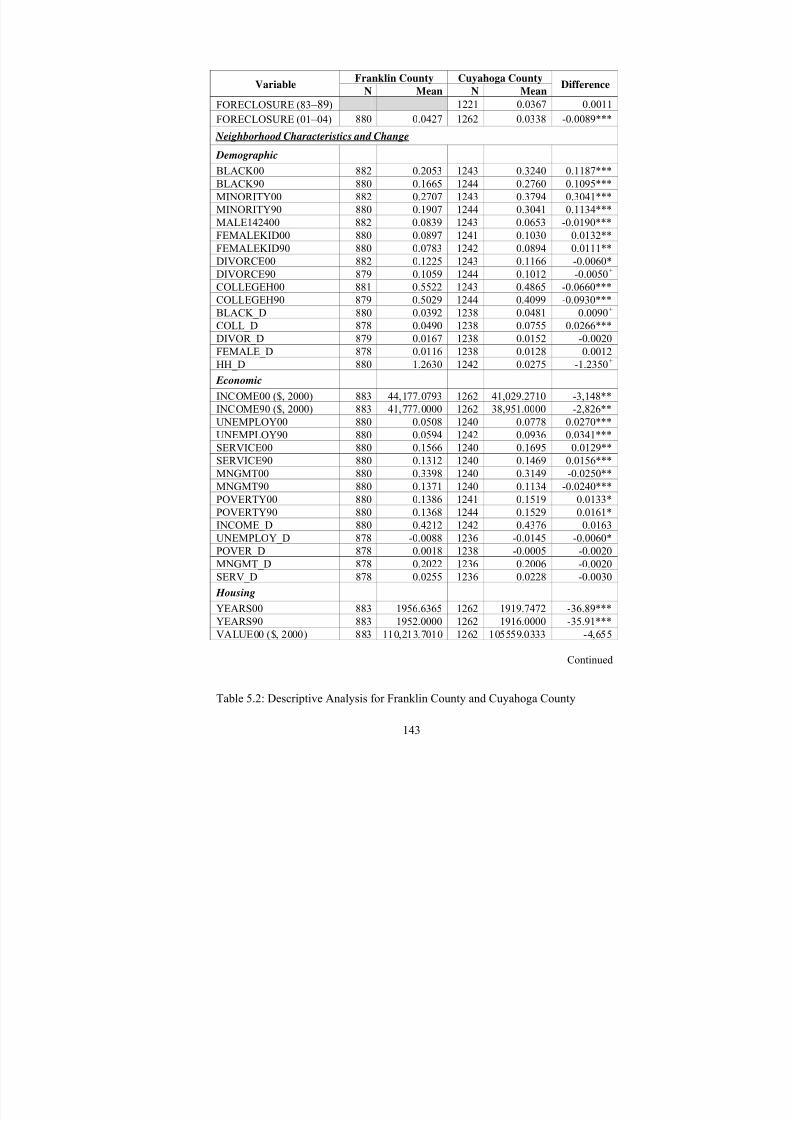

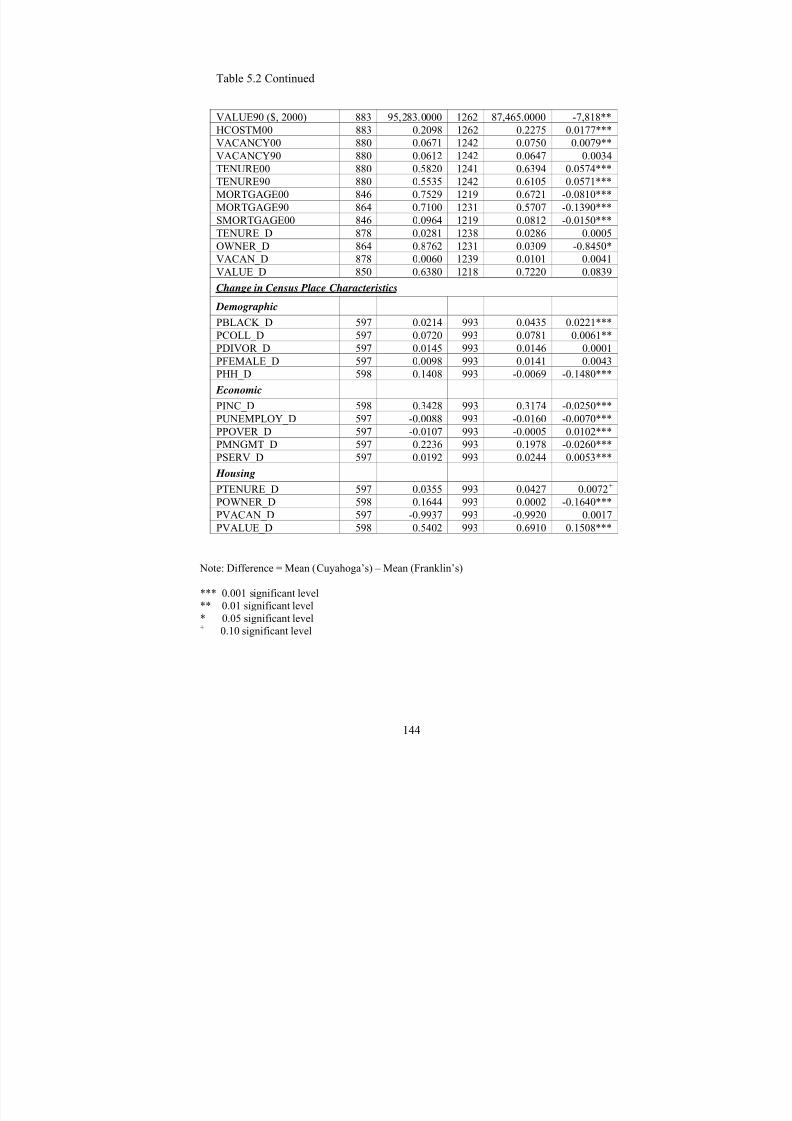

Table 5.1: Foreclosure Rate Characteristics for Franklin and Cuyahoga Counties........ 141

Table 5.2: Descriptive Analysis for Franklin County and Cuyahoga County ................ 143

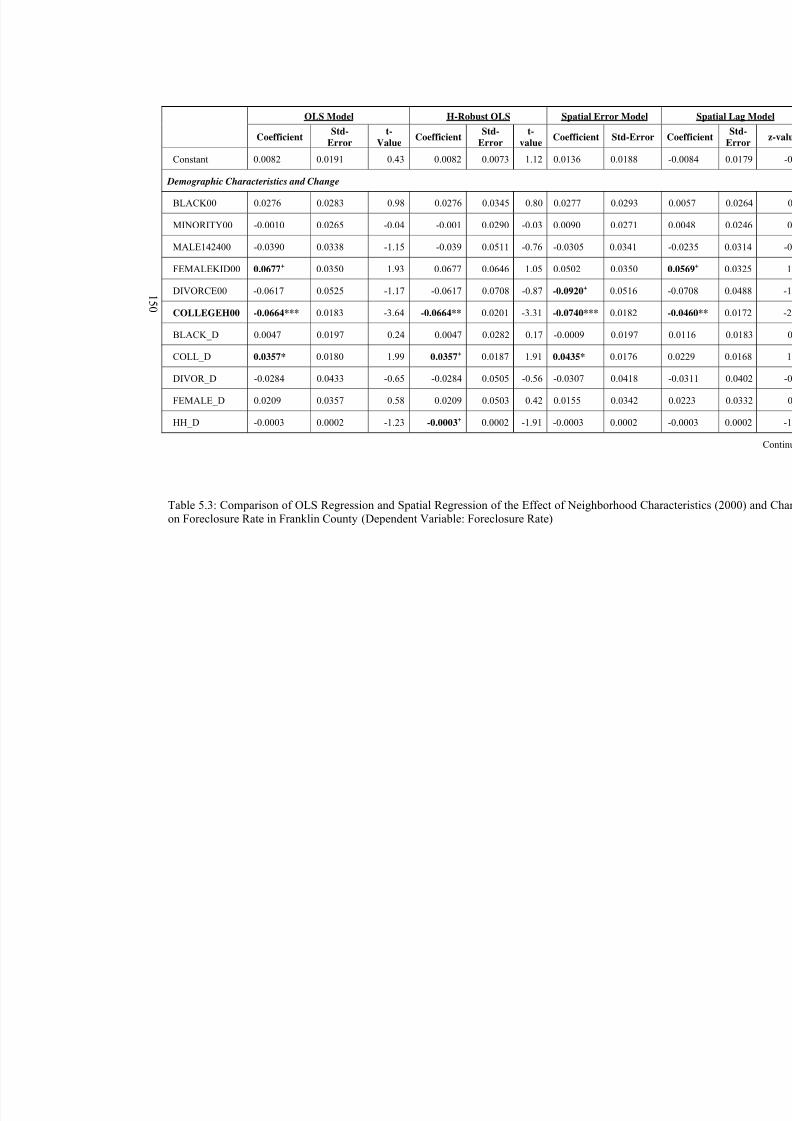

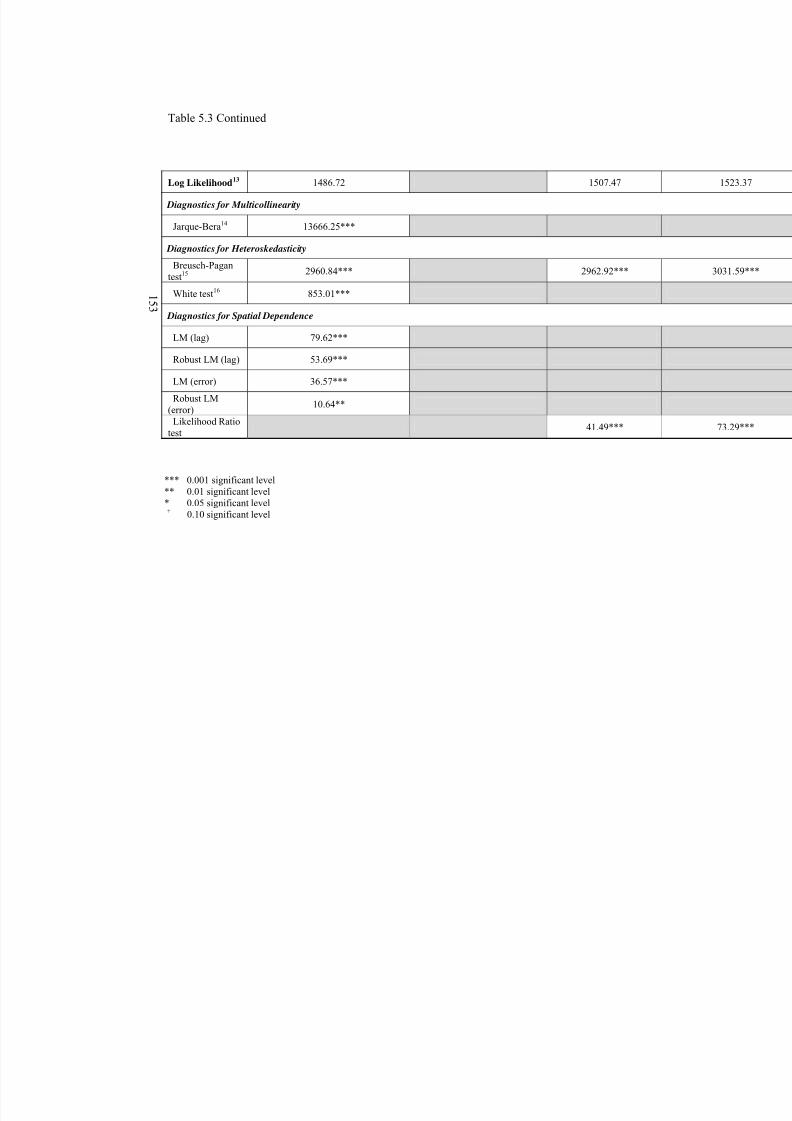

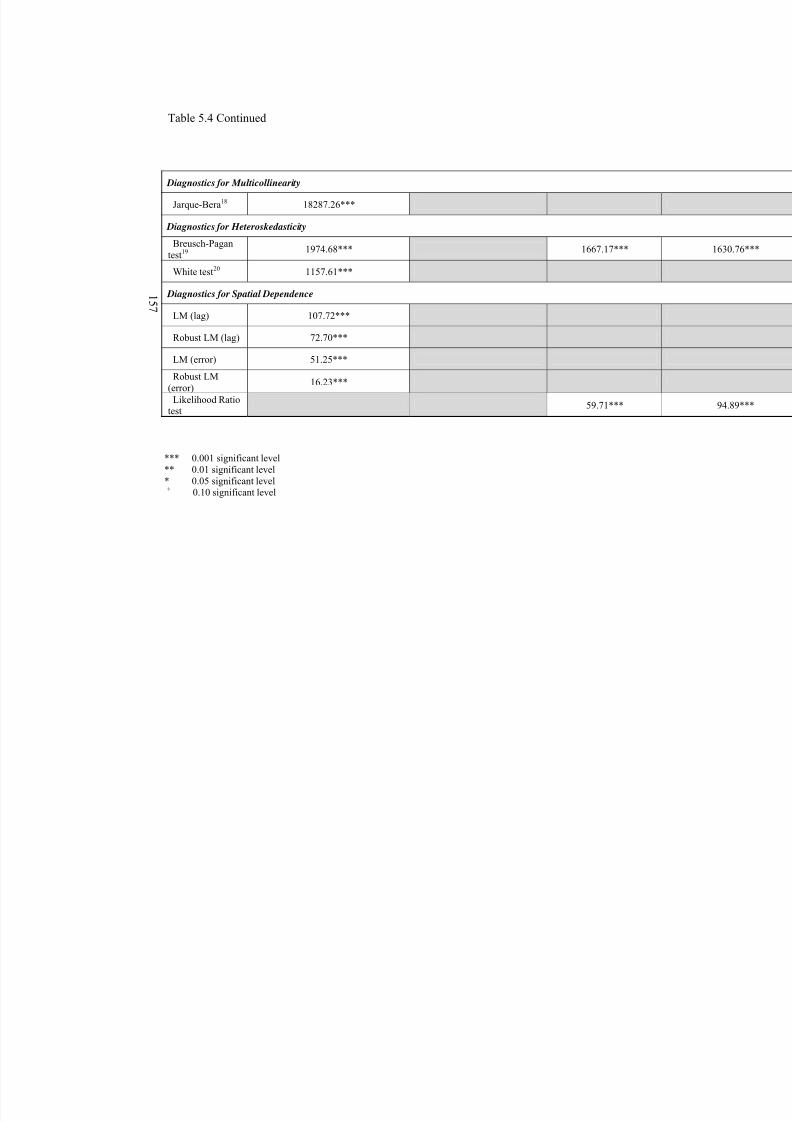

Table 5.3: Comparison of OLS Regression and Spatial Regression of the Effect of

Neighborhood Characteristics (2000) and Change on Foreclosure Rate in FranklinCounty (Dependent Variable: Foreclosure Rate).................................................... 150

Table 5.4: Comparison of OLS Regression and Spatial Regression of the Effect of Neighborhood Characteristics (2000) and Change on Foreclosure Rate in CuyahogaCounty (Dependent Variable: Foreclosure Rate).................................................... 154

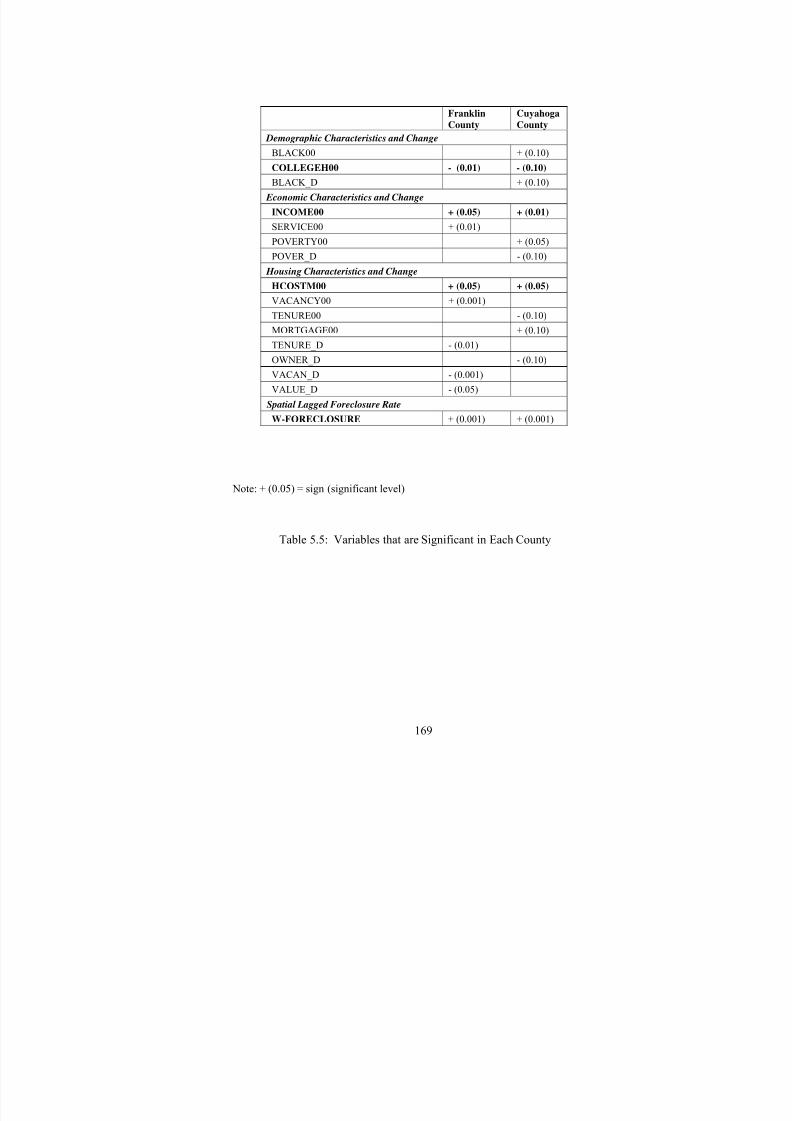

Table 5.5: Variables that are Significant in Each County.............................................. 169

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 11/268

x

Table 5.6: Cross Model Covariance Matrix for Cuyahoga County ................................ 175

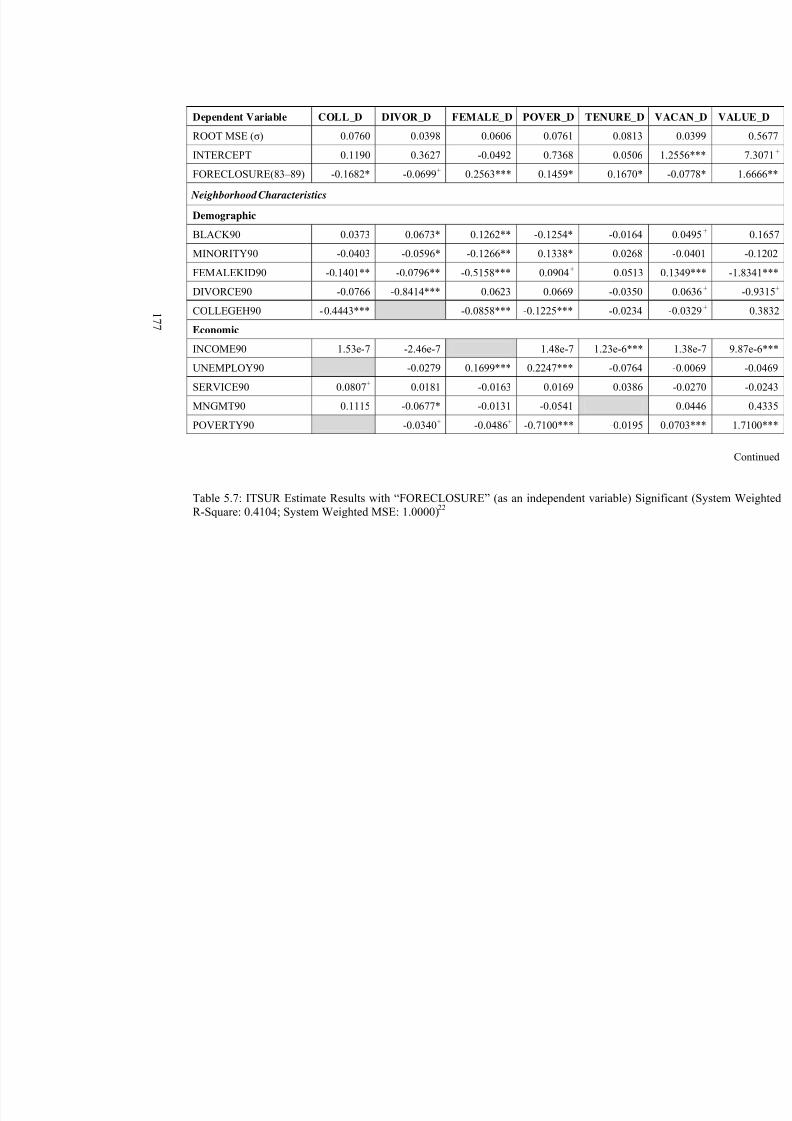

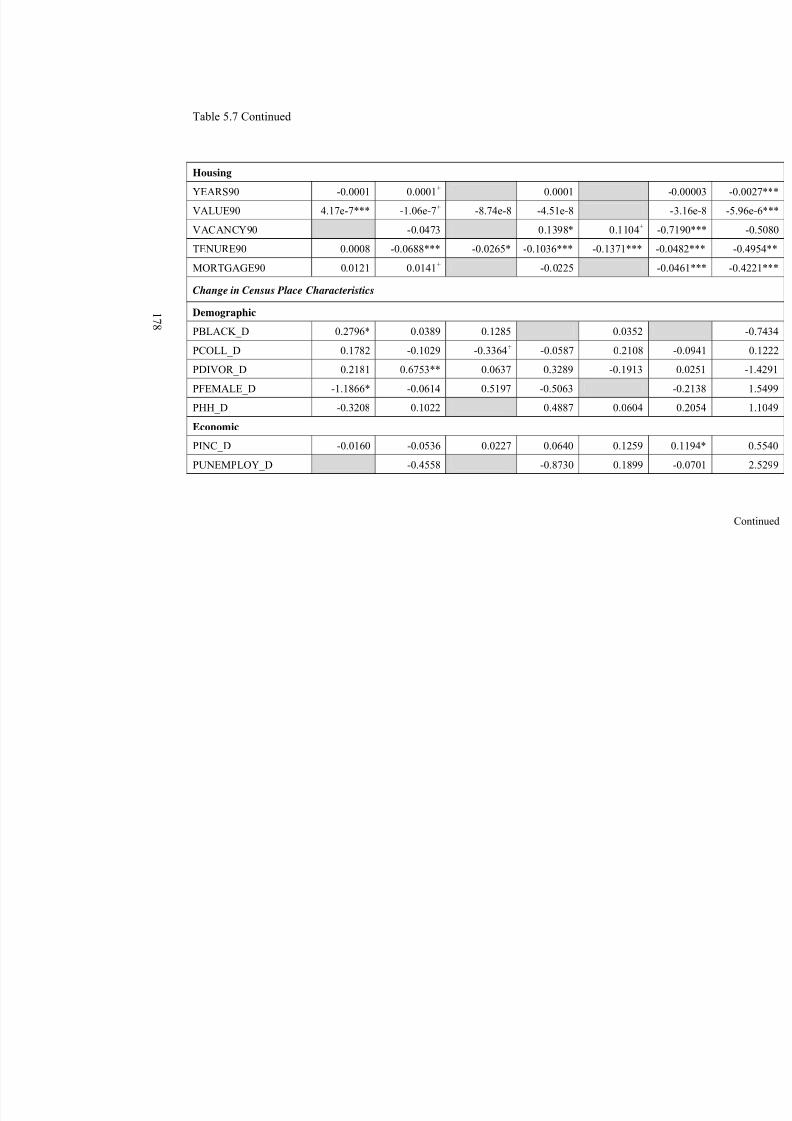

Table 5.7: ITSUR Estimate Results with “FORECLOSURE” (as an independent variable)Significant (System Weighted R-Square: 0.4104; System Weighted MSE: 1.0000)................................................................................................................................. 177

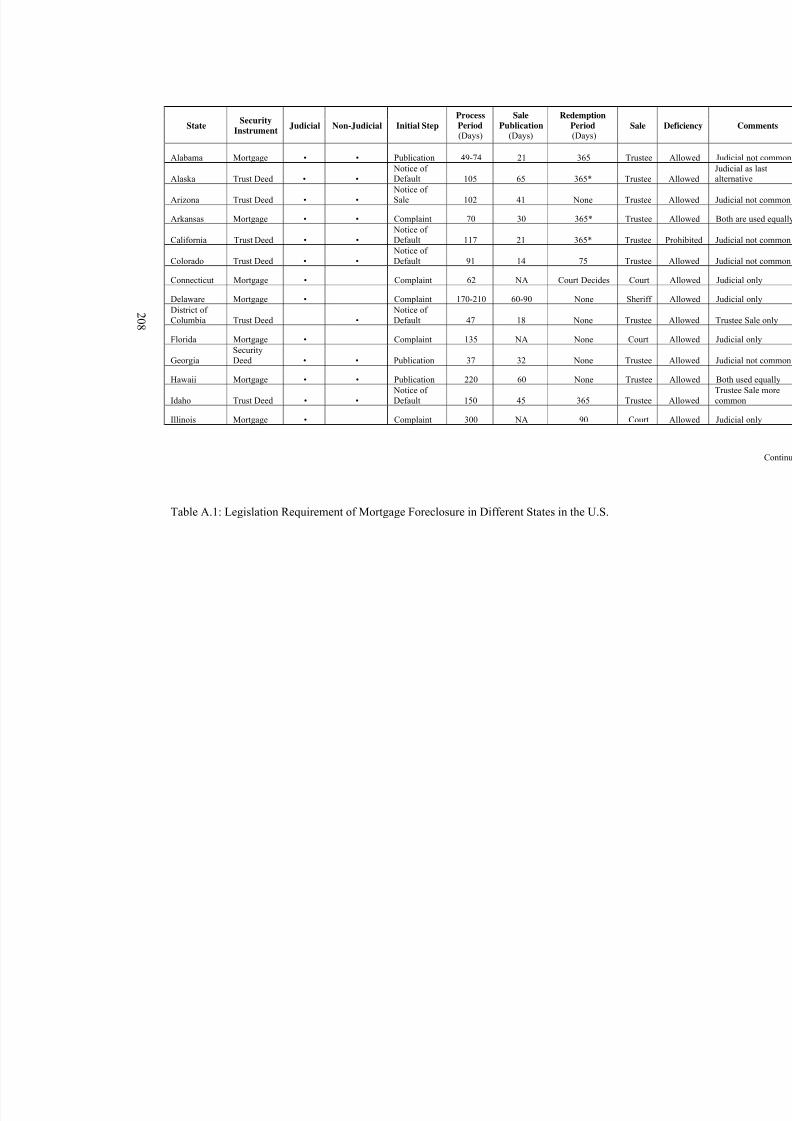

Table A.1: Legislation Requirement of Mortgage Foreclosure in Different States in theU.S. ......................................................................................................................... 208

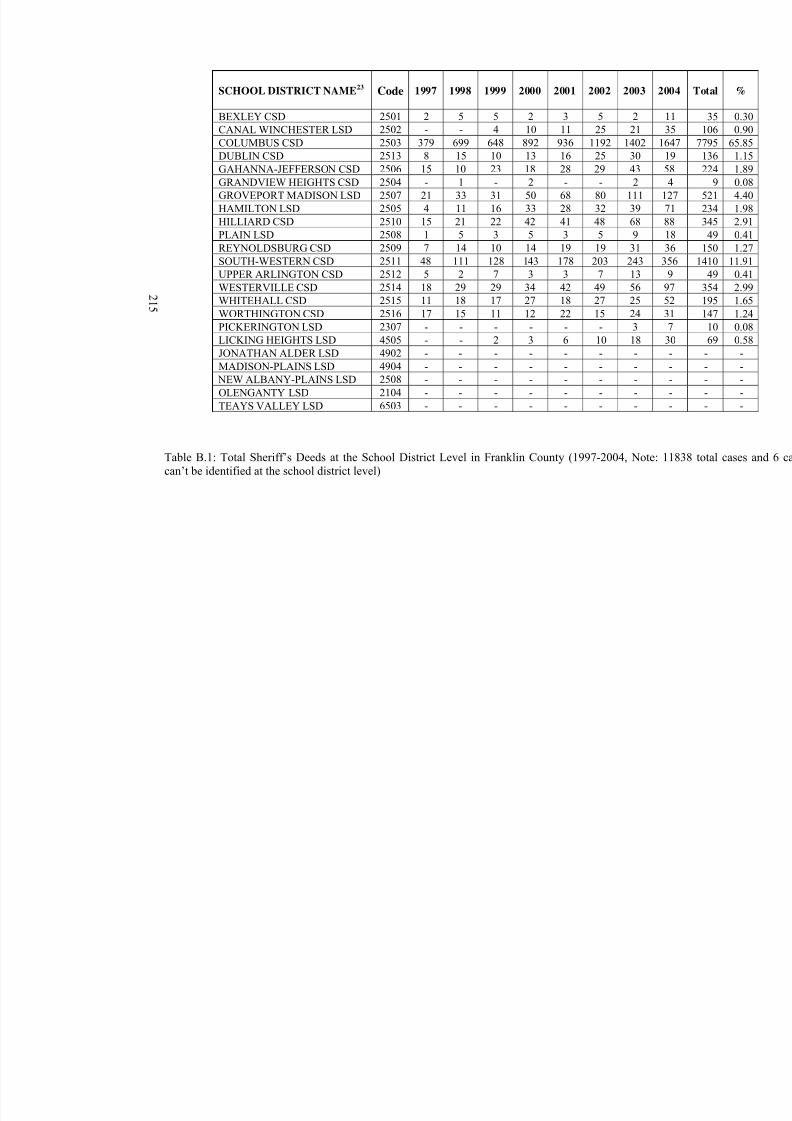

Table B.1: Total Sheriff’s Deeds at the School District Level in Franklin County (1997-2004, Note: 11838 total cases and 6 cases can’t be identified at the school districtlevel) ....................................................................................................................... 215

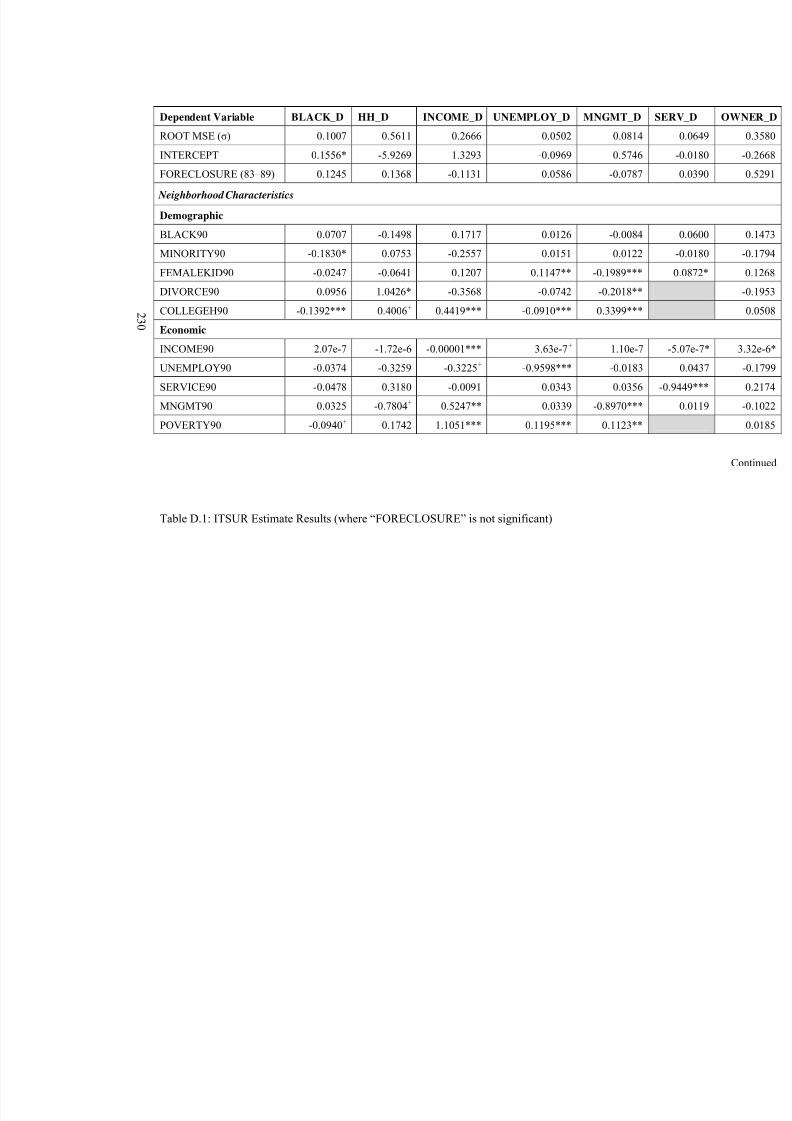

Table D.1: ITSUR Estimate Results (where “FORECLOSURE” is not significant) ..... 230

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 12/268

xi

LIST OF FIGURES

Figure 2.1: The Interaction between Residential Mortgage Foreclosure, and Neighborhood Characteristics and Change............................................................... 30

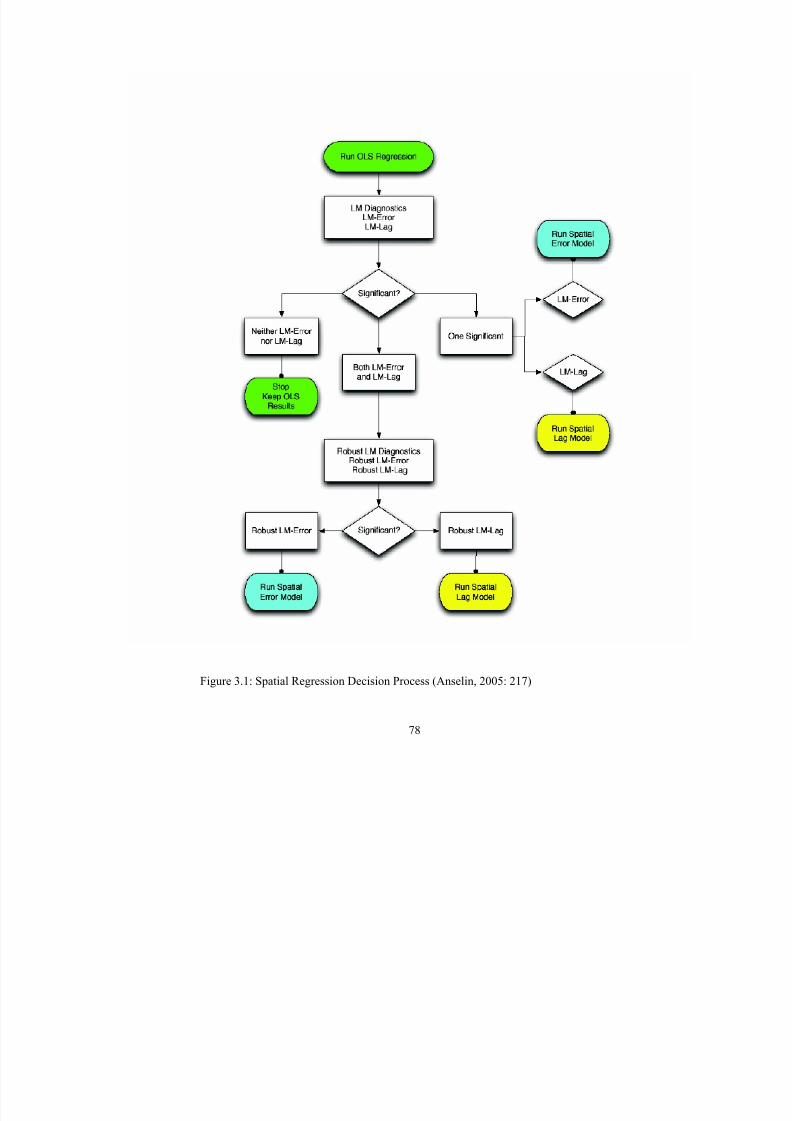

Figure 3.1: Spatial Regression Decision Process (Anselin, 2005: 217) ........................... 78

Figure 4.1: Judicial Foreclosure Process .......................................................................... 86

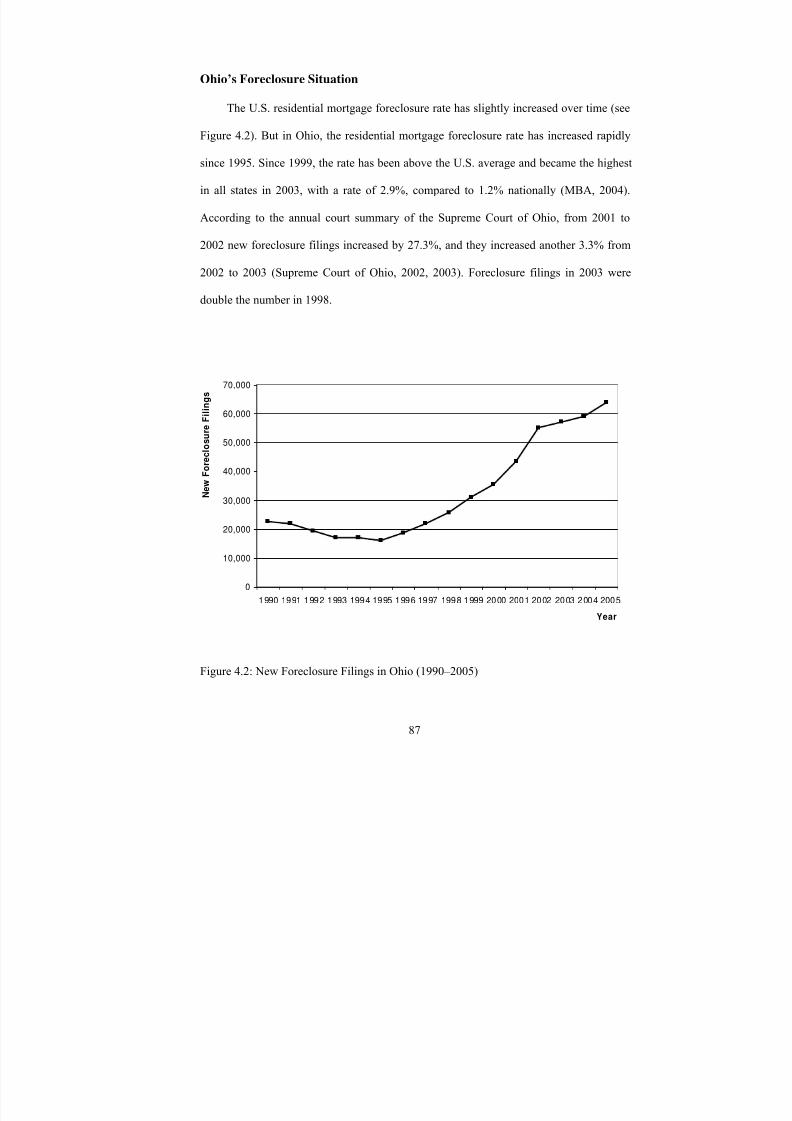

Figure 4.2: New Foreclosure Filings in Ohio (1990–2005).............................................. 87

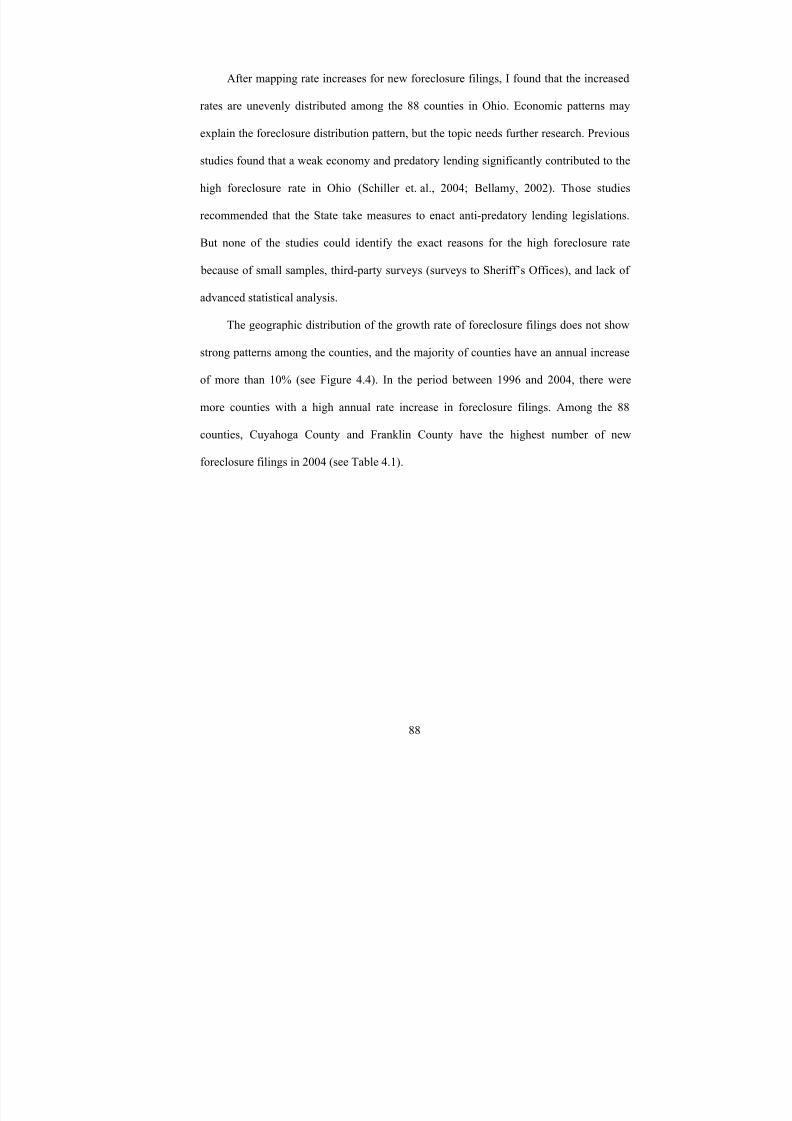

Figure 4.3: Change of Foreclosures Started in Ohio (1984–2003)................................... 89

Figure 4.4: Average Annual Growth Rate of New foreclosure Filings by County .......... 90

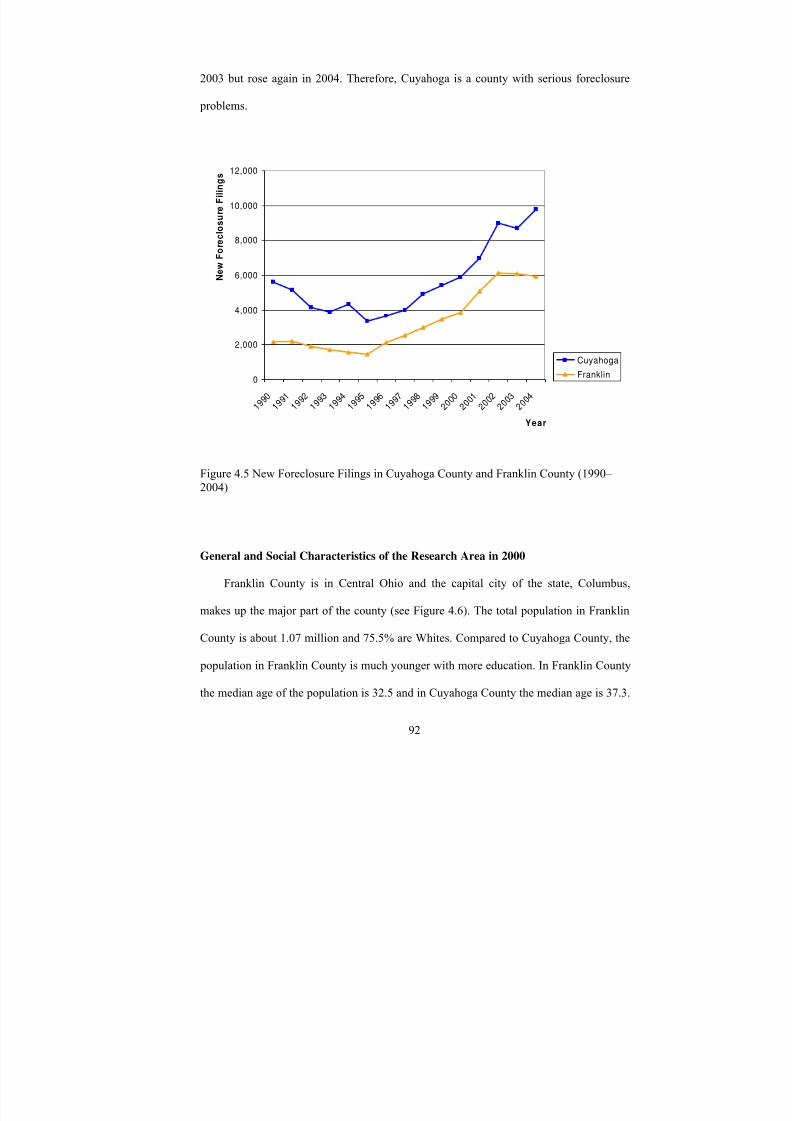

Figure 4.5 New Foreclosure Filings in Cuyahoga County and Franklin County (1990– 2004) ................................................................................................................................. 92

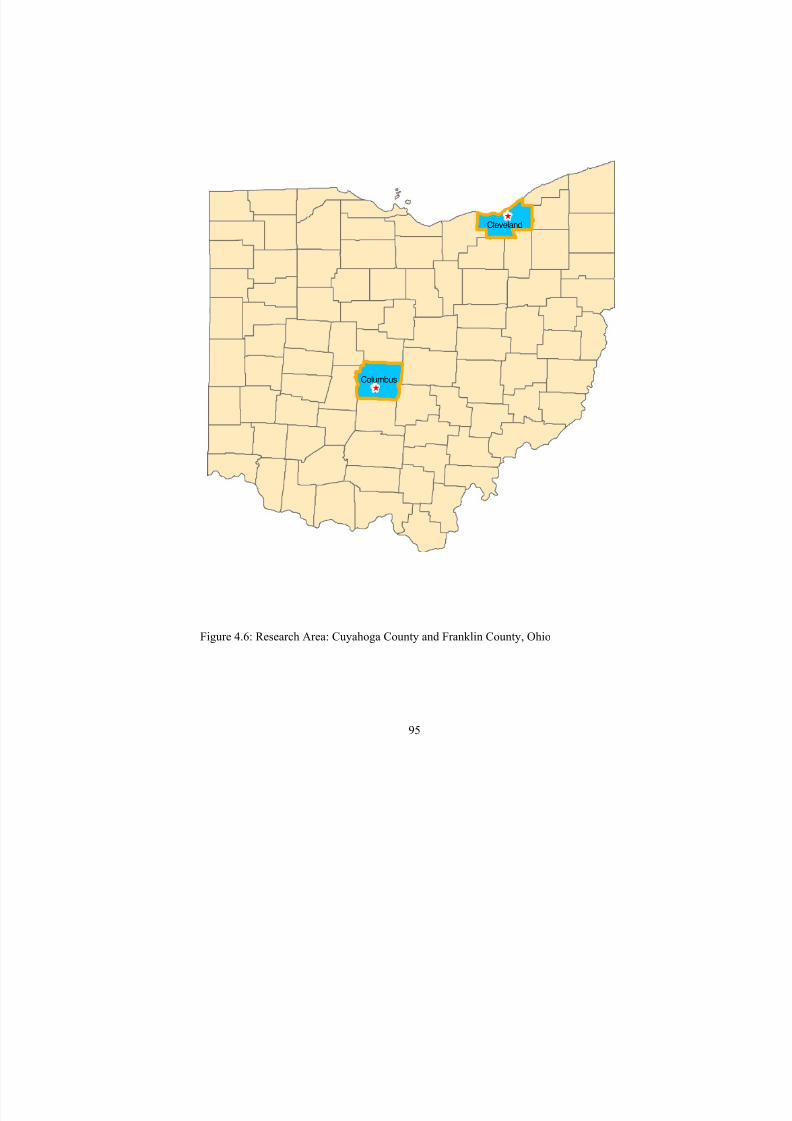

Figure 4.6: Research Area: Cuyahoga County and Franklin County, Ohio ..................... 95

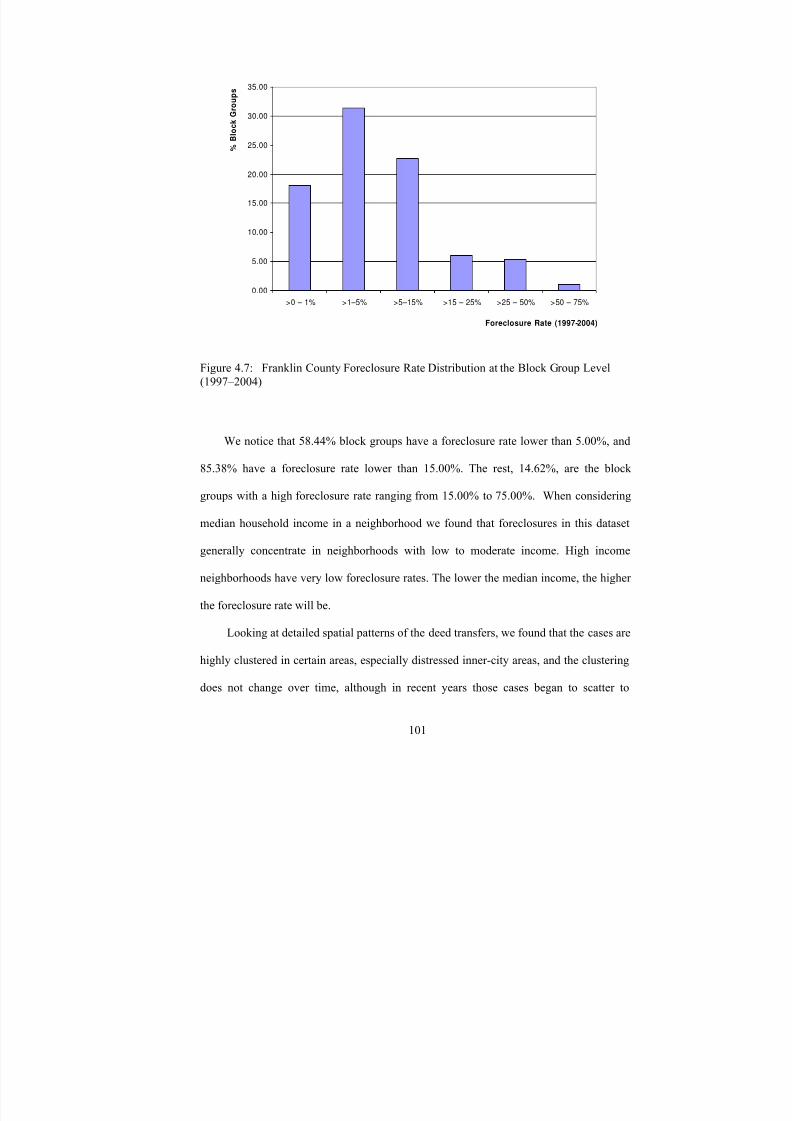

Figure 4.7: Franklin County Foreclosure Rate Distribution at the Block Group Level(1997–2004)............................................................................................................ 101

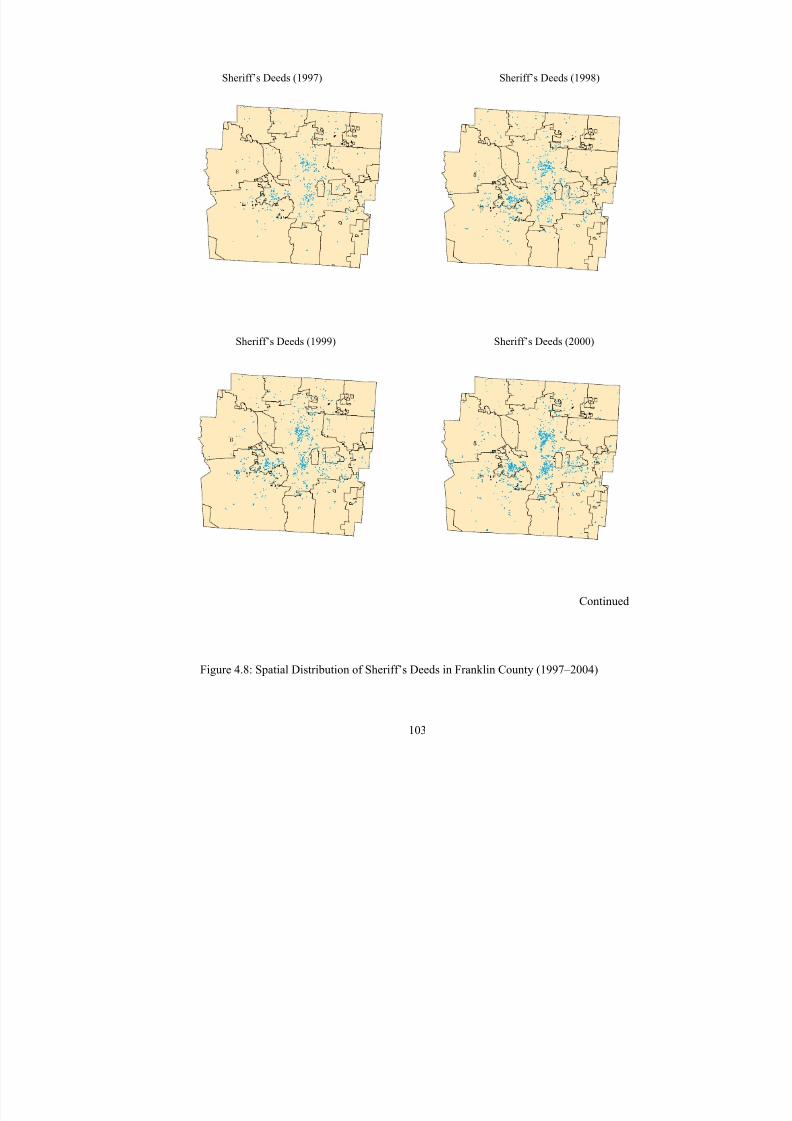

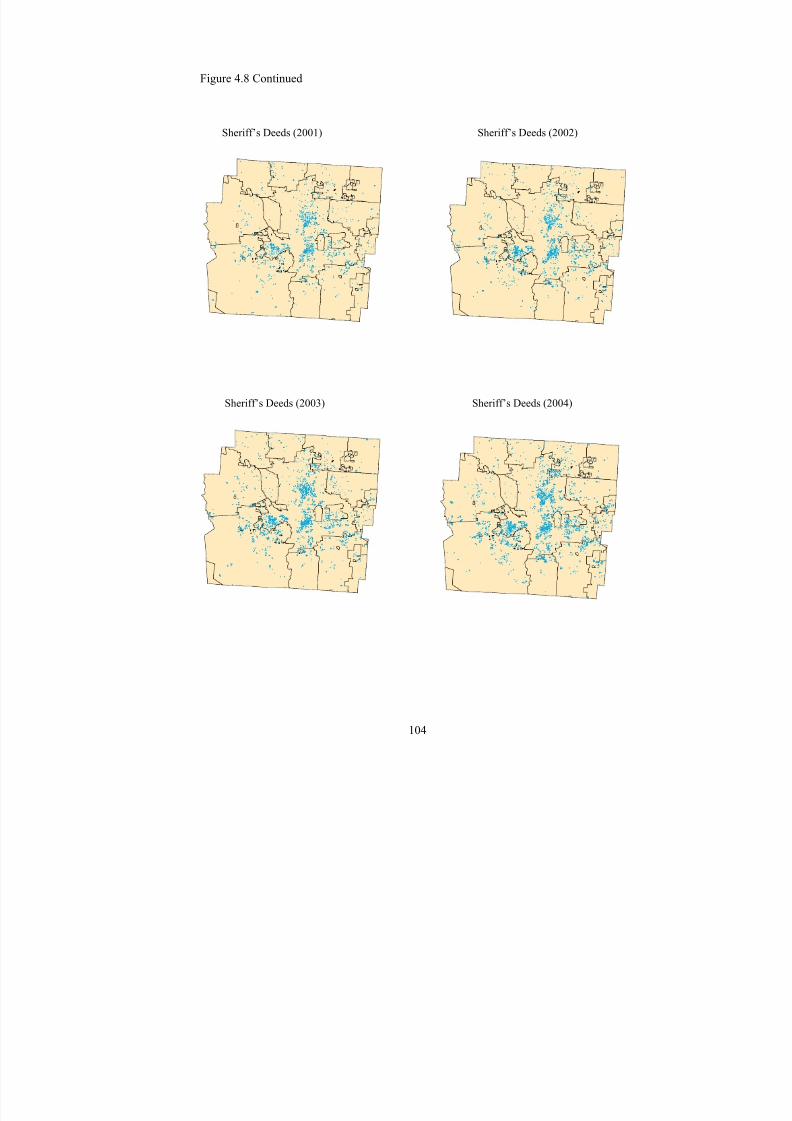

Figure 4.8: Spatial Distribution of Sheriff’s Deeds in Franklin County (1997–2004) ... 103

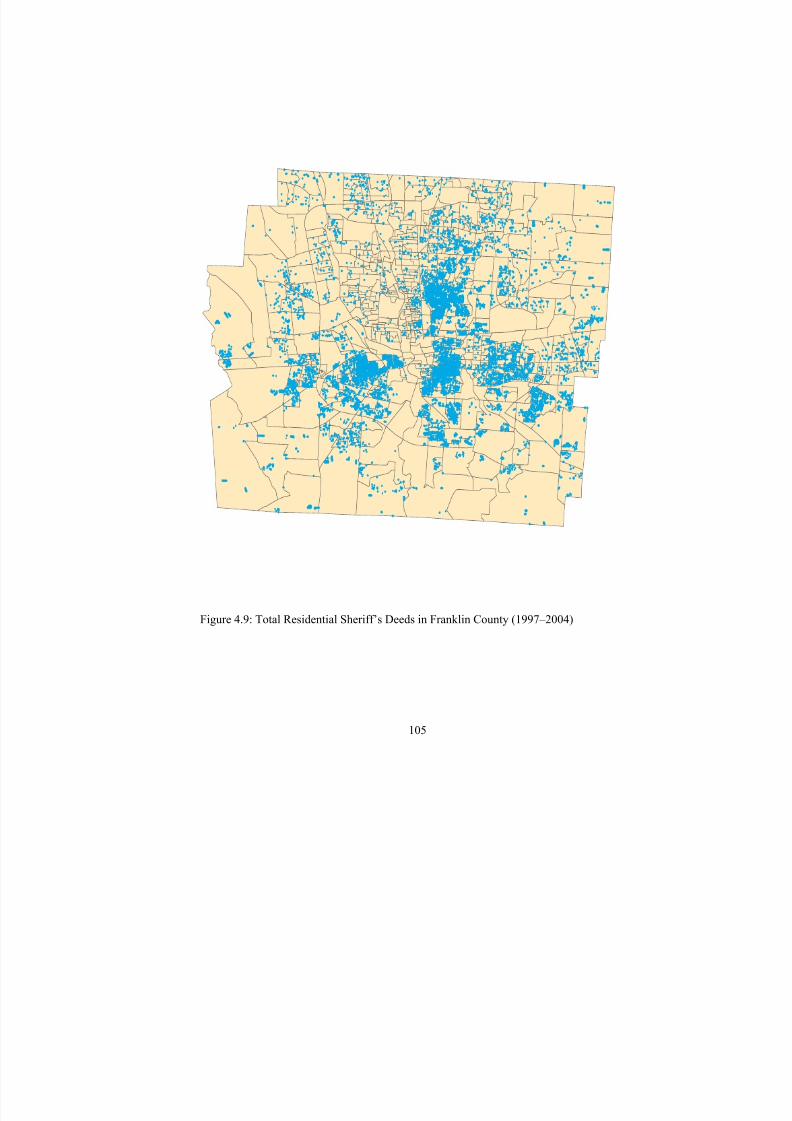

Figure 4.9: Total Residential Sheriff’s Deeds in Franklin County (1997–2004) ........... 105

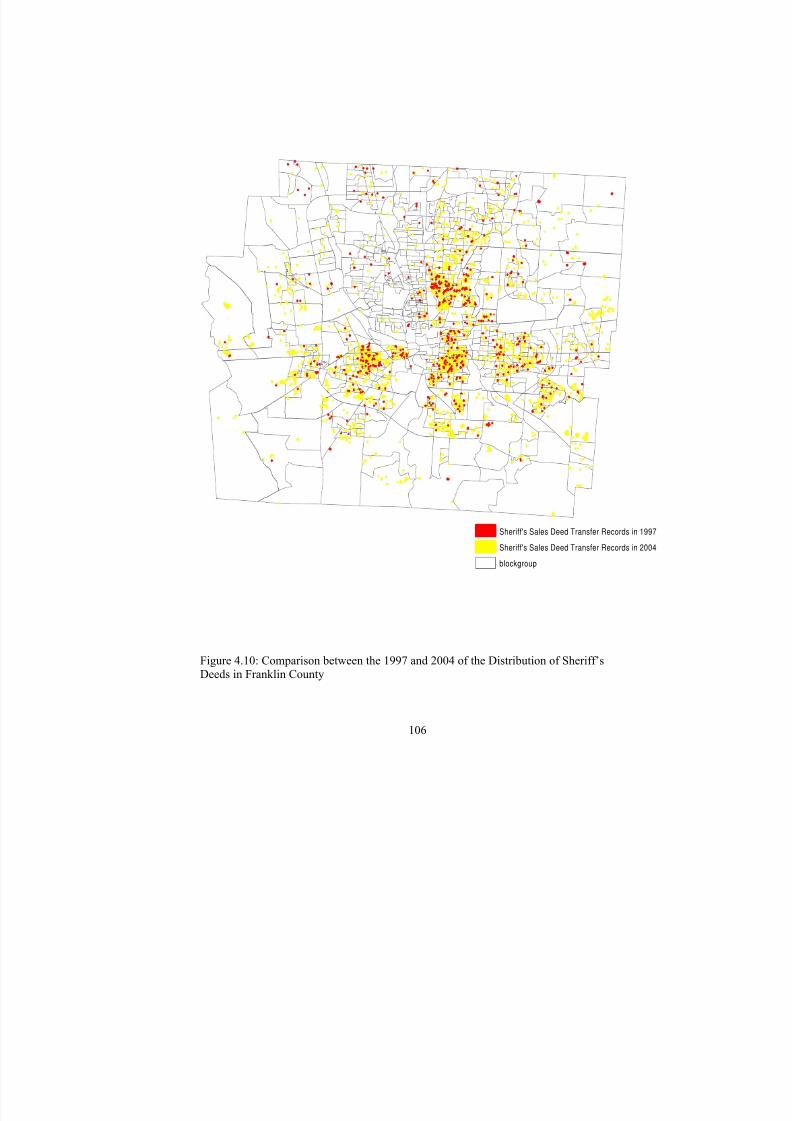

Figure 4.10: Comparison between the 1997 and 2004 of the Distribution of Sheriff’sDeeds in Franklin County ....................................................................................... 106

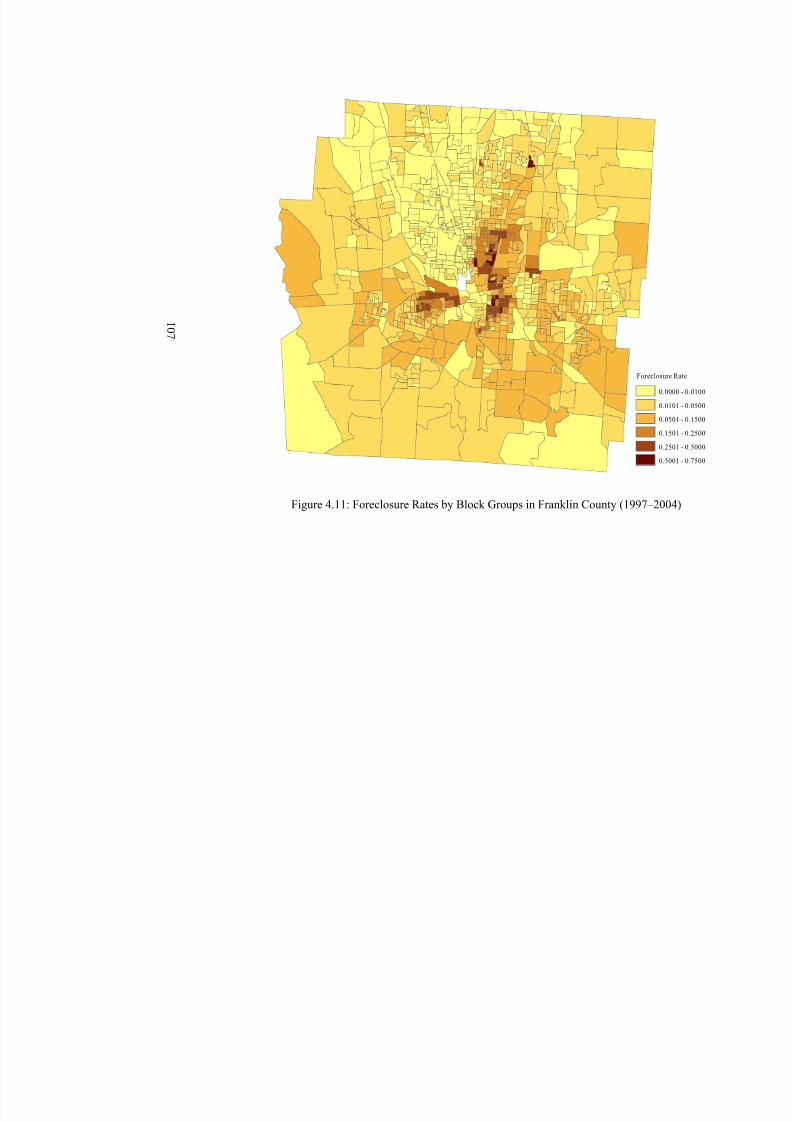

Figure 4.11: Foreclosure Rates by Block Groups in Franklin County (1997–2004)...... 107

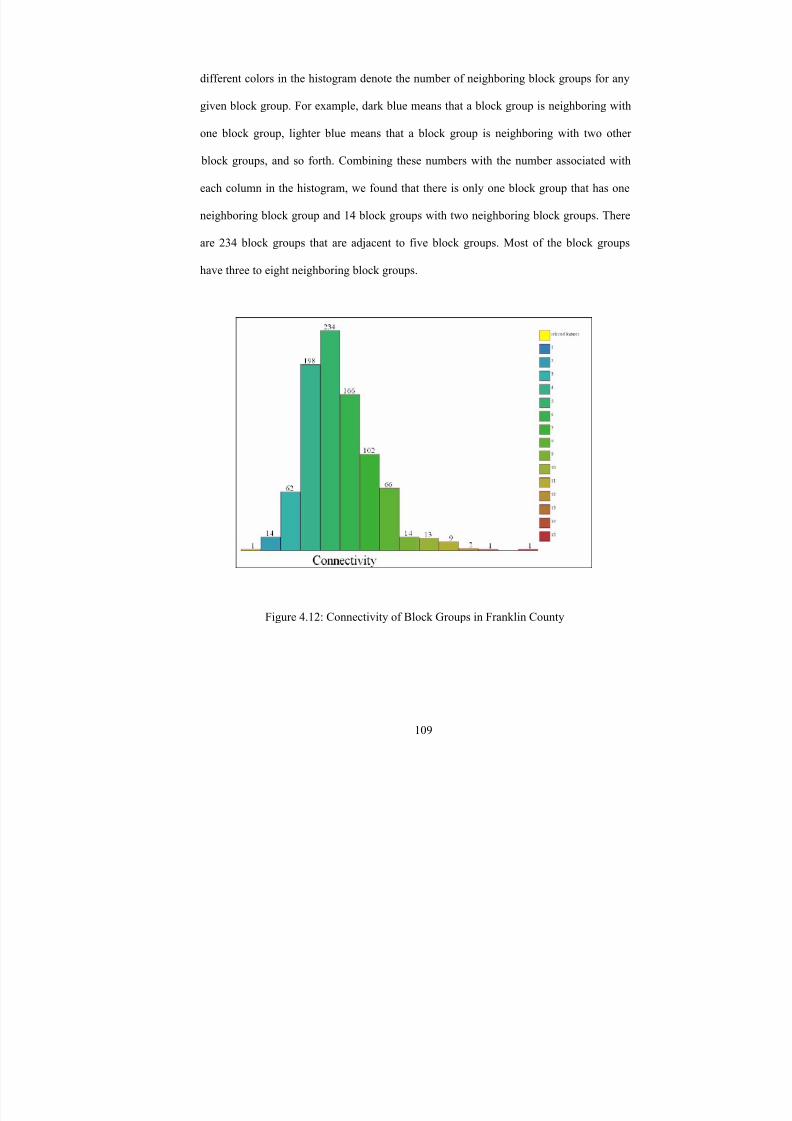

Figure 4.12: Connectivity of Block Groups in Franklin County .................................... 109

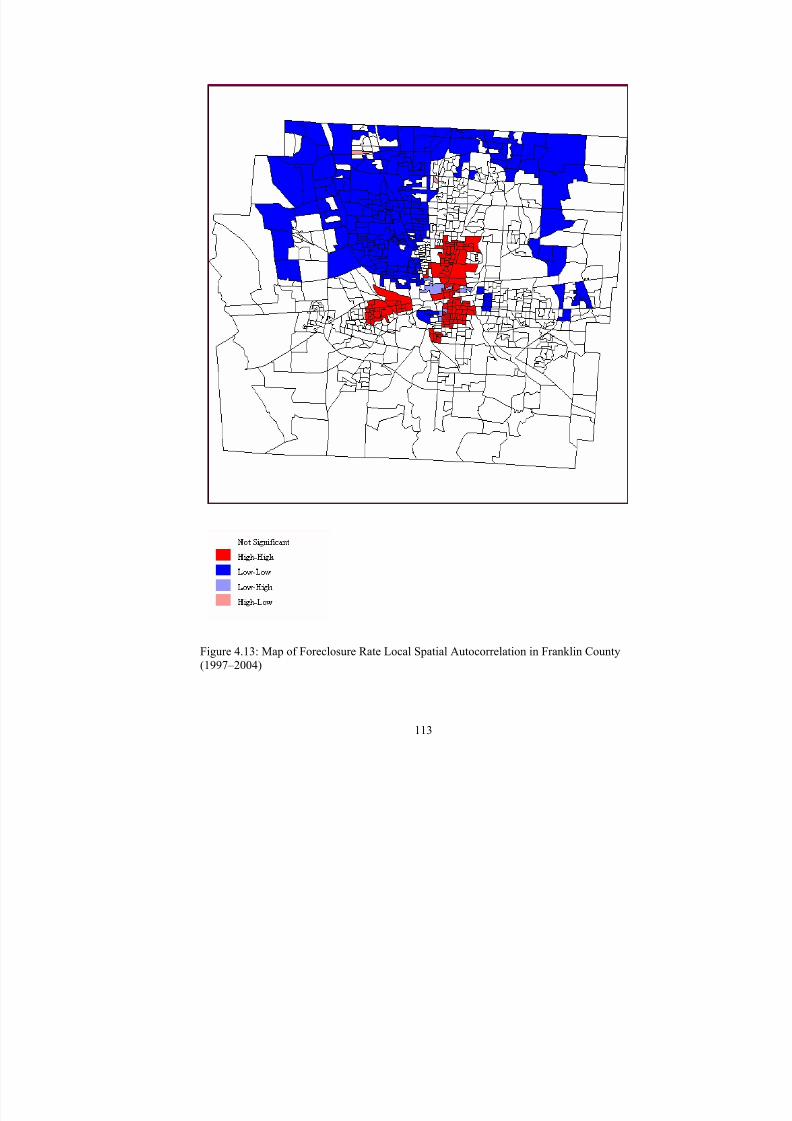

Figure 4.13: Map of Foreclosure Rate Local Spatial Autocorrelation in Franklin County(1997–2004)............................................................................................................ 113

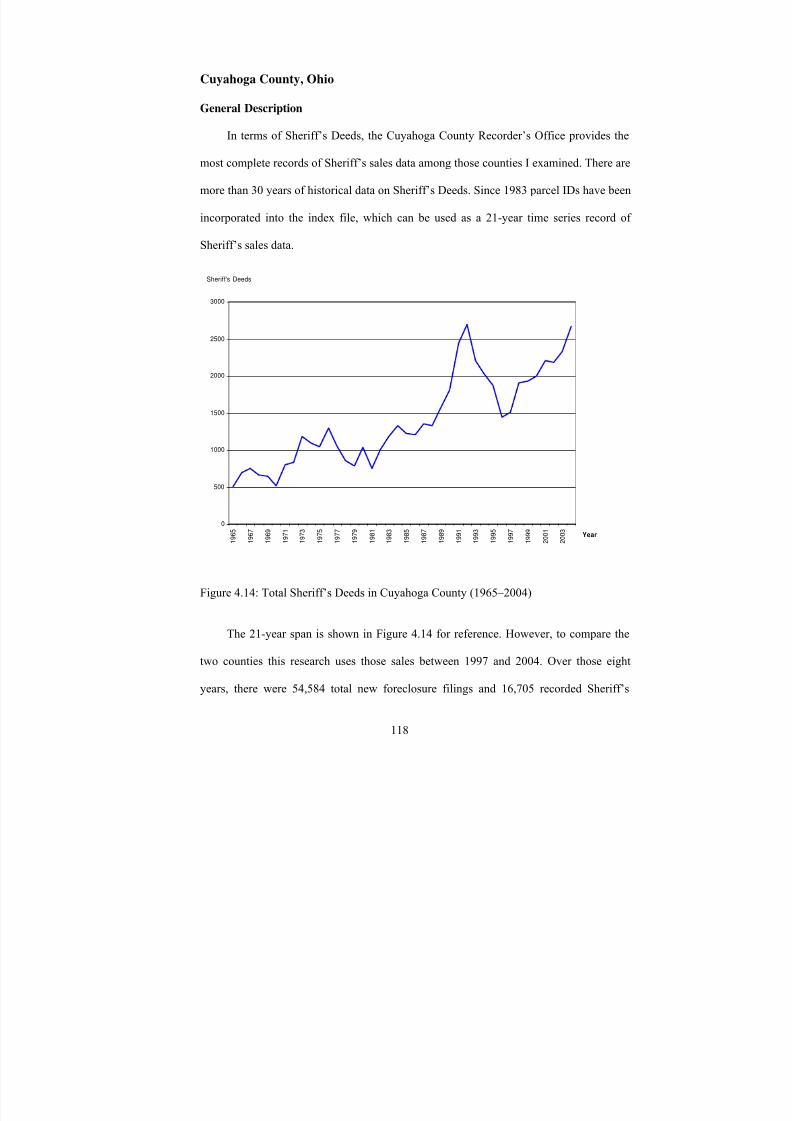

Figure 4.14: Total Sheriff’s Deeds in Cuyahoga County (1965–2004).......................... 118

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 13/268

xii

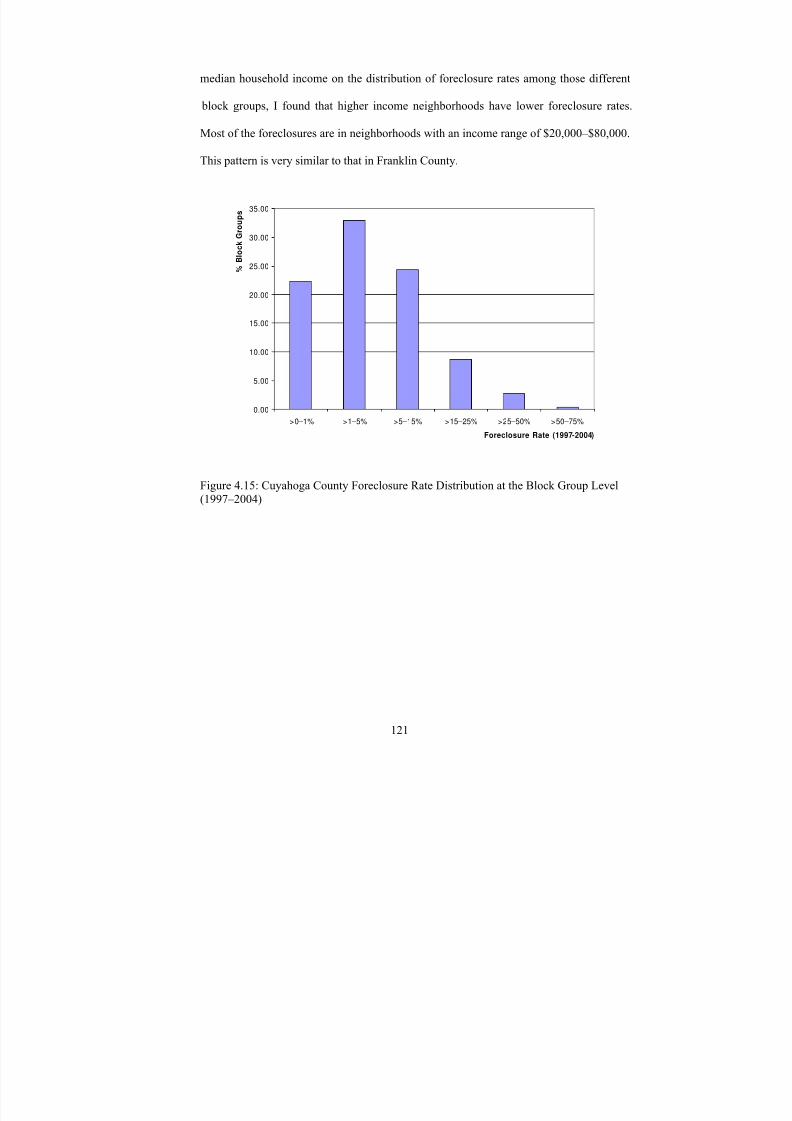

Figure 4.15: Cuyahoga County Foreclosure Rate Distribution at the Block Group Level(1997–2004)............................................................................................................ 121

Figure 4.16: Spatial Distribution of Sheriff’s Deeds in Cuyahoga County (1997–2004)................................................................................................................................. 122

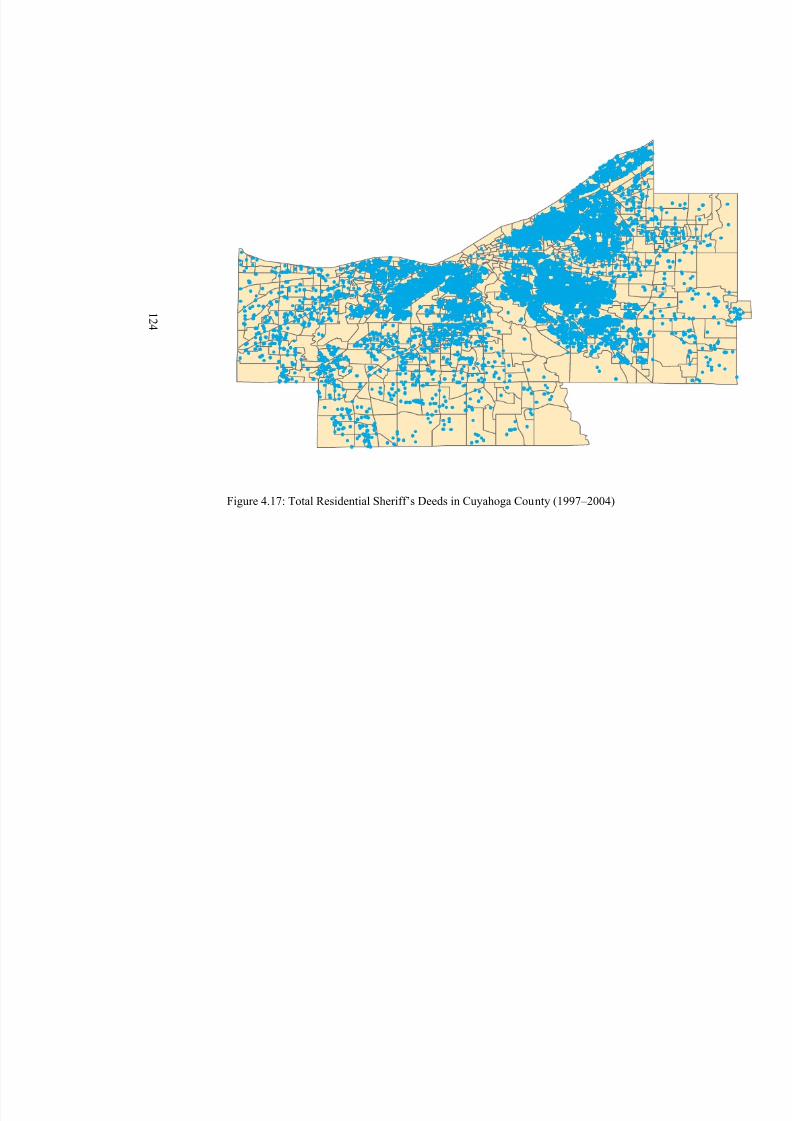

Figure 4.17: Total Residential Sheriff’s Deeds in Cuyahoga County (1997–2004)....... 124

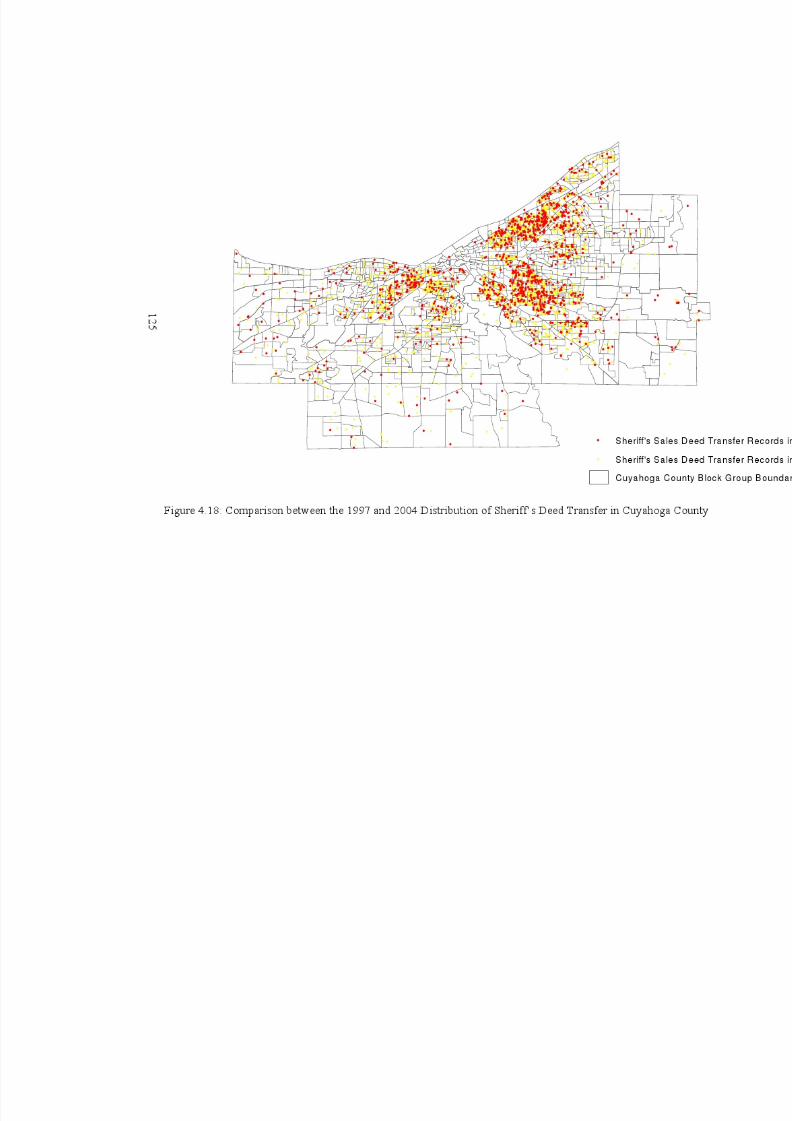

Figure 4.18: Comparison between the 1997 and 2004 Distribution of Sheriff’s DeedTransfer in Cuyahoga County................................................................................. 125

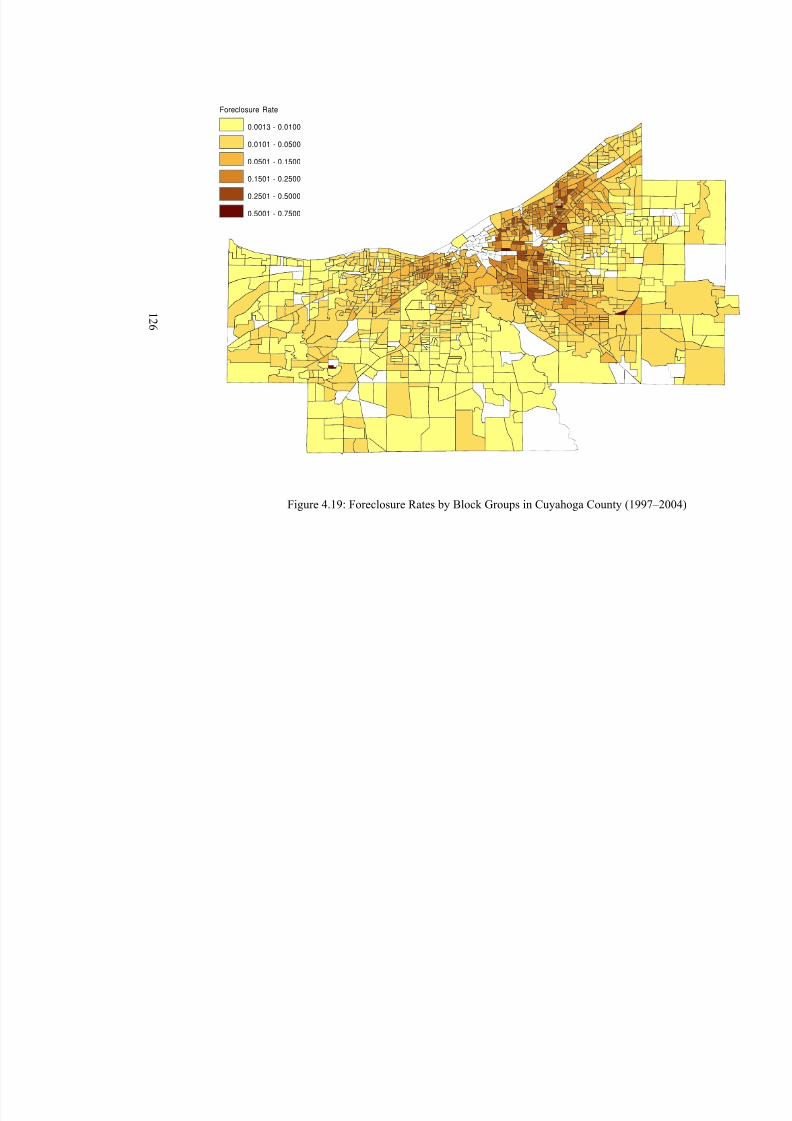

Figure 4.19: Foreclosure Rates by Block Groups in Cuyahoga County (1997–2004) ... 126

Figure 4.20: Foreclosure Rates by Block Groups in Cuyahoga County (1983-1989).... 128

Figure 4.21: Connectivity of Block Groups in Cuyahoga County.................................. 130

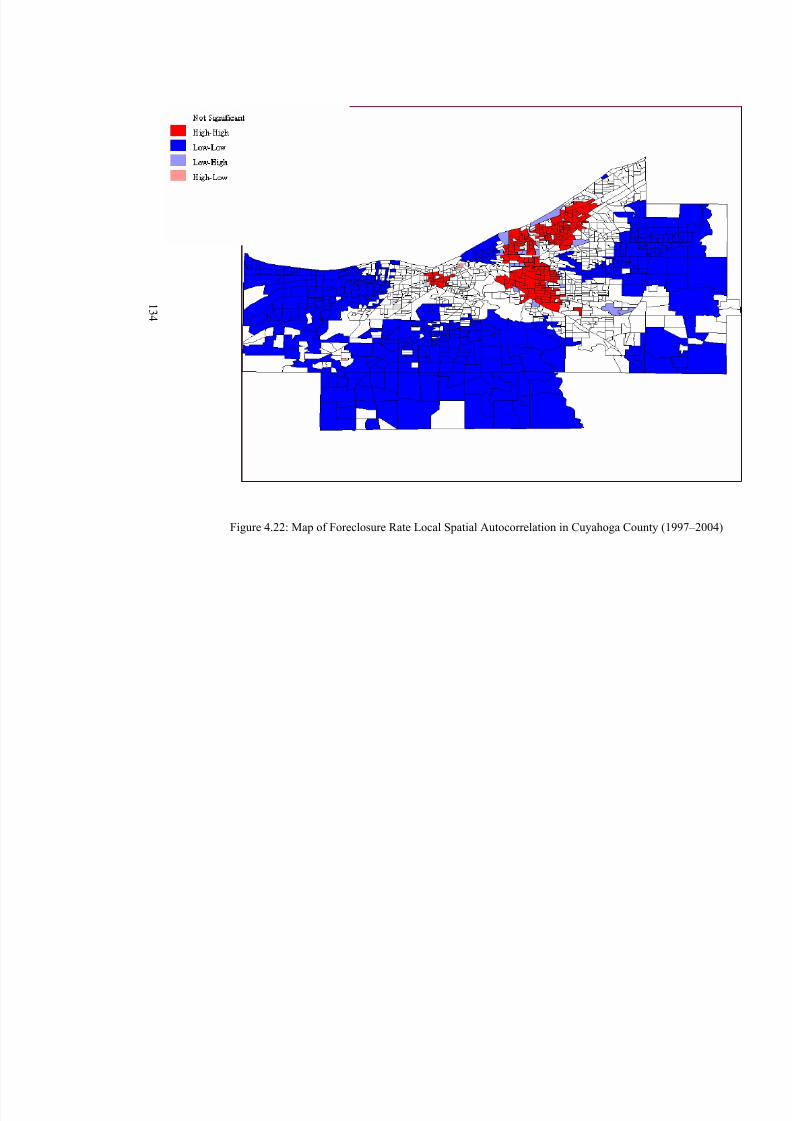

Figure 4.22: Map of Foreclosure Rate Local Spatial Autocorrelation in Cuyahoga County(1997–2004)............................................................................................................ 134

Figure 5.1: Summary of the Interaction between Residential Mortgage Foreclosure and Neighborhood Characteristics and Change............................................................. 191

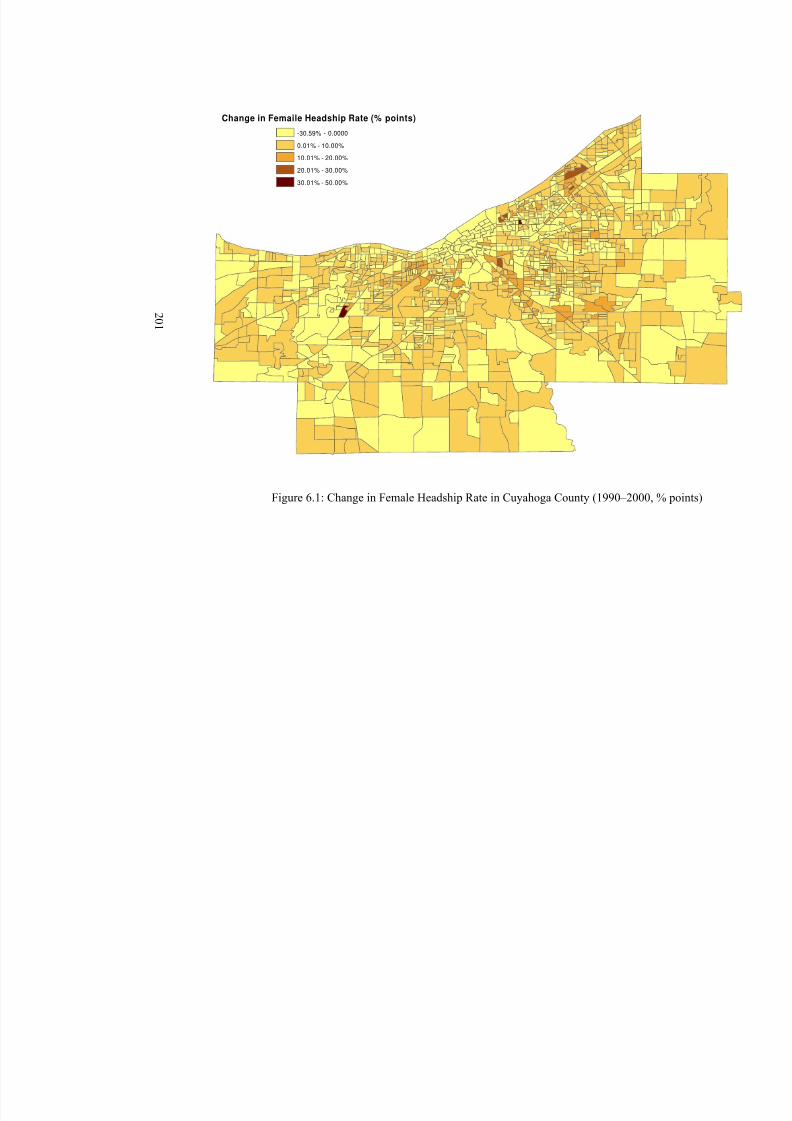

Figure 6.1: Change in Female Headship Rate in Cuyahoga County (1990–2000, % points)................................................................................................................................. 201

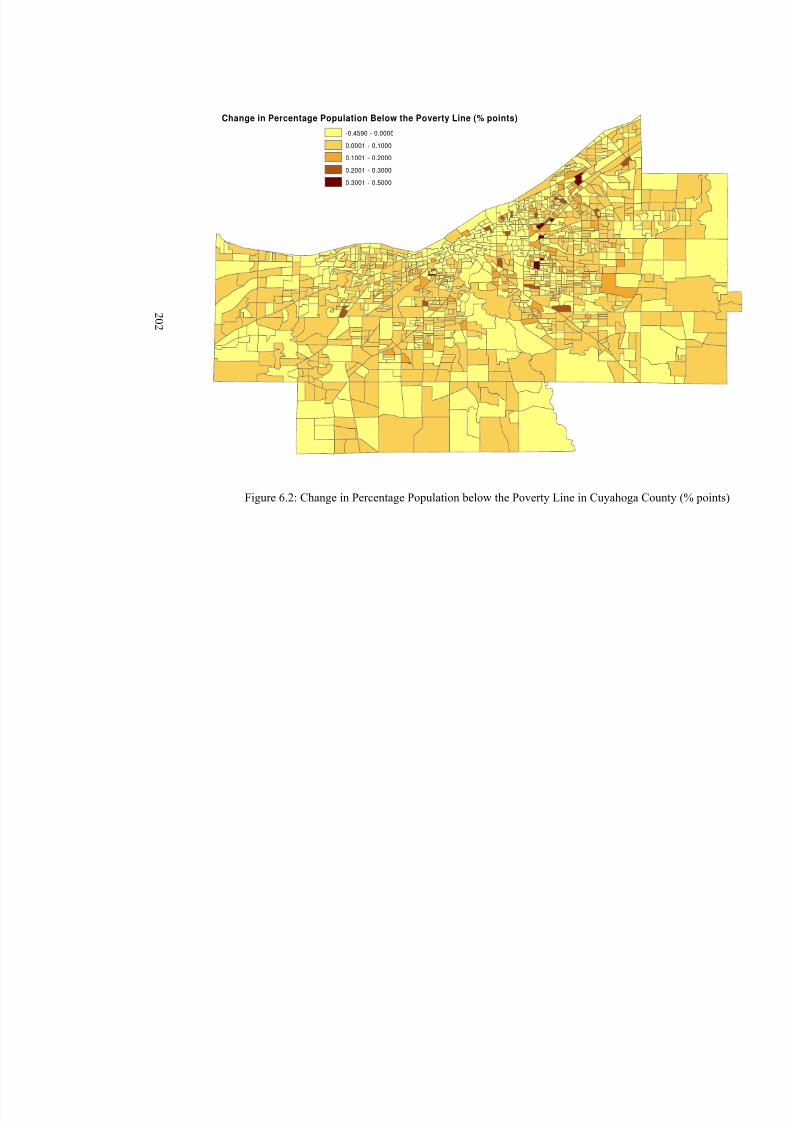

Figure 6.2: Change in Percentage Population below the Poverty Line in CuyahogaCounty (% points) ................................................................................................... 202

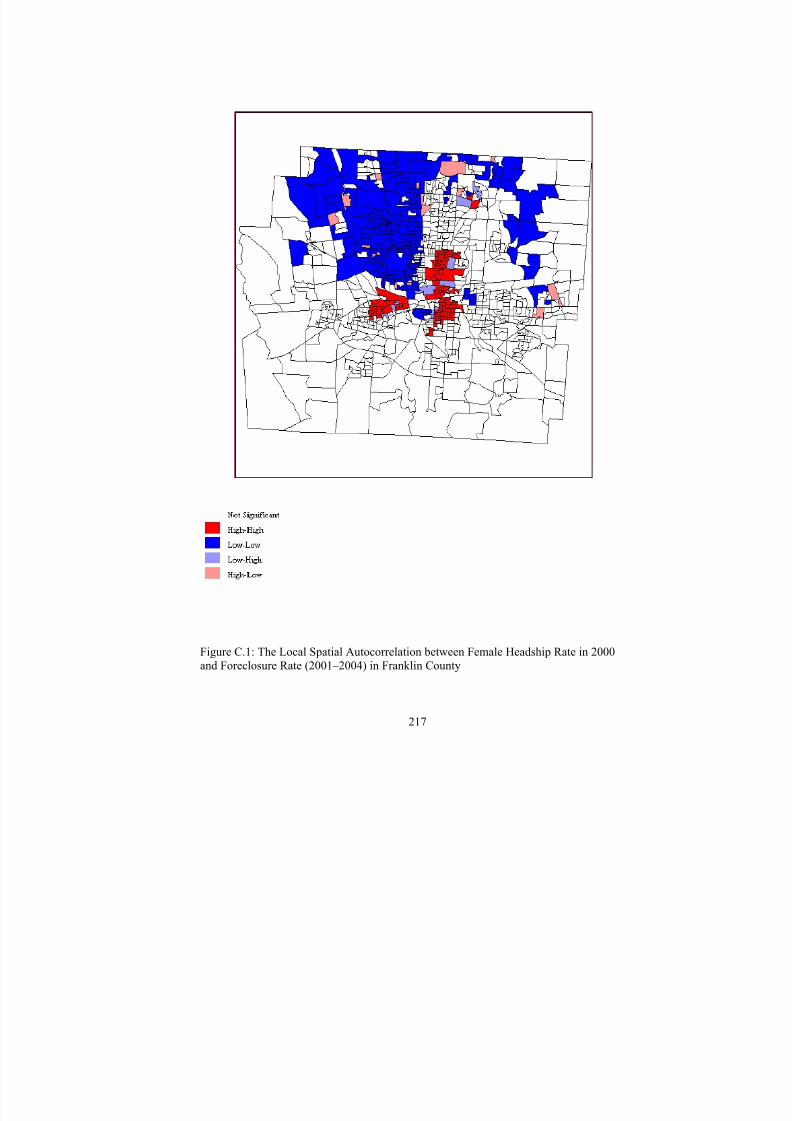

Figure C.1: The Local Spatial Autocorrelation between Female Headship Rate in 2000and Foreclosure Rate (2001–2004) in Franklin County ......................................... 217

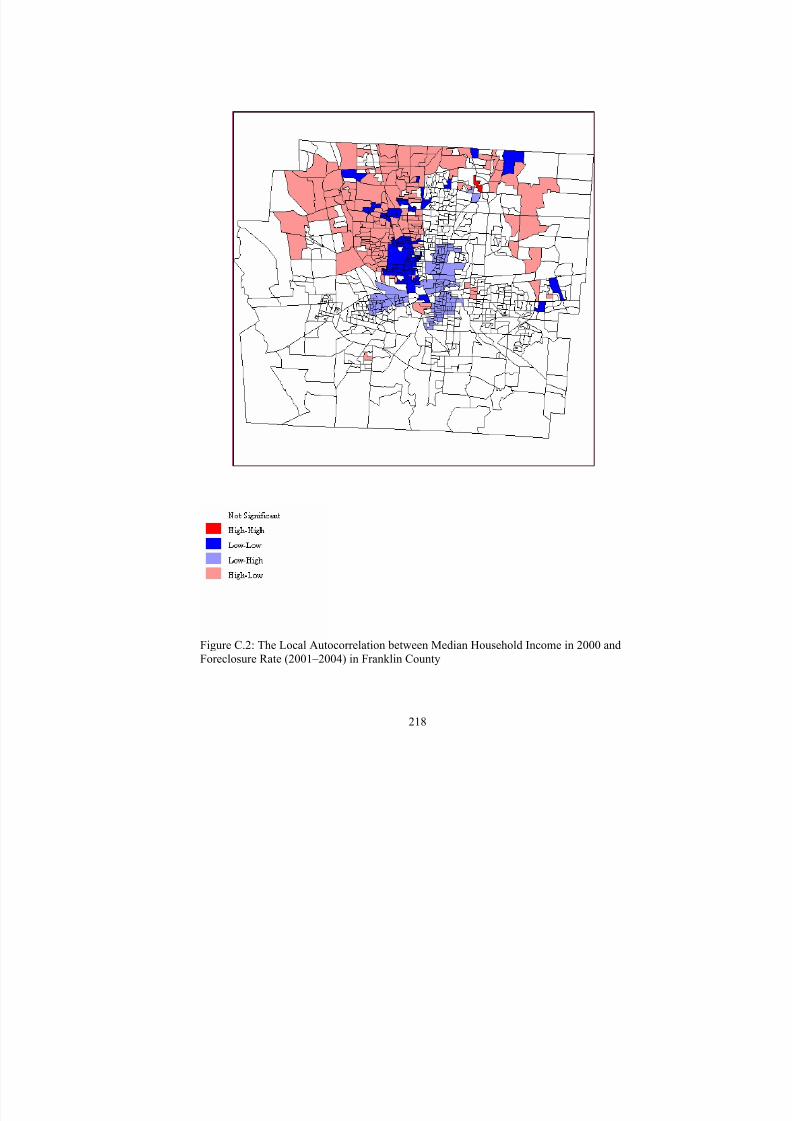

Figure C.2: The Local Autocorrelation between Median Household Income in 2000 andForeclosure Rate (2001–2004) in Franklin County ................................................ 218

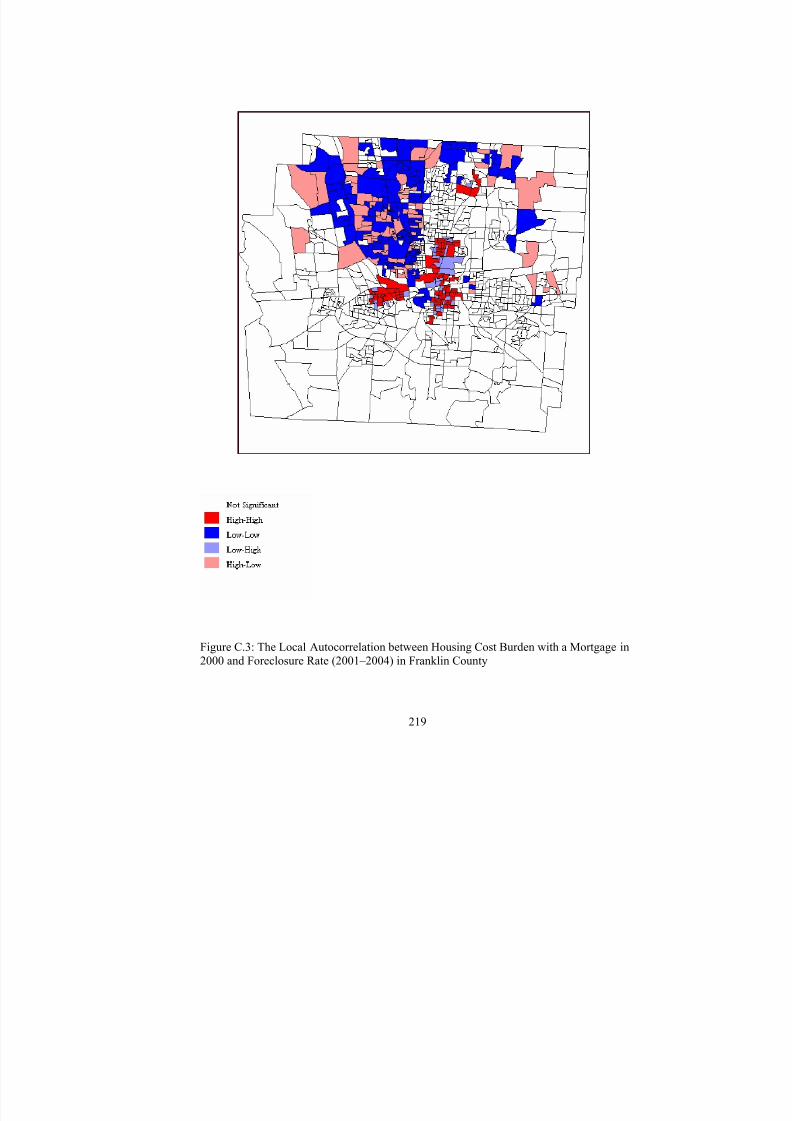

Figure C.3: The Local Autocorrelation between Housing Cost Burden with a Mortgage in2000 and Foreclosure Rate (2001–2004) in Franklin County ................................ 219

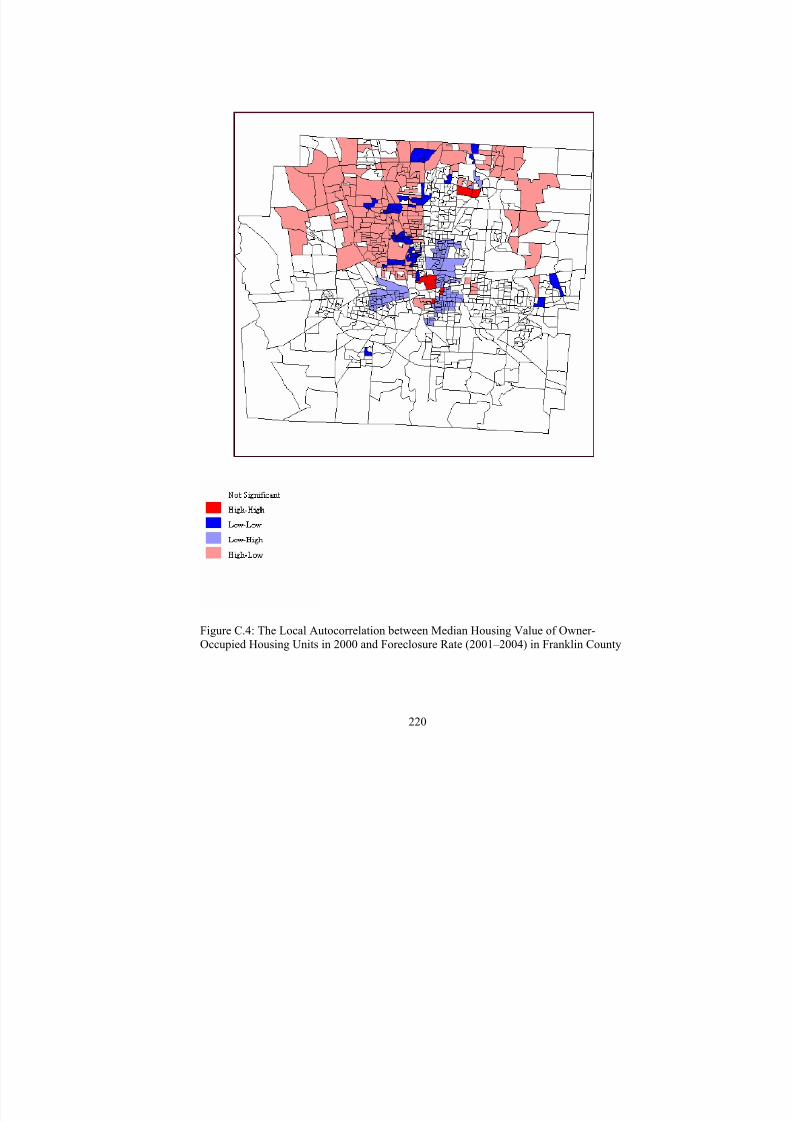

Figure C.4: The Local Autocorrelation between Median Housing Value of Owner-Occupied Housing Units in 2000 and Foreclosure Rate (2001–2004) in FranklinCounty..................................................................................................................... 220

Figure C.5: The Local Autocorrelation between Housing Vacancy Rate in 2000 andForeclosure Rate (2001–2004) in Franklin County ................................................ 221

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 14/268

xiii

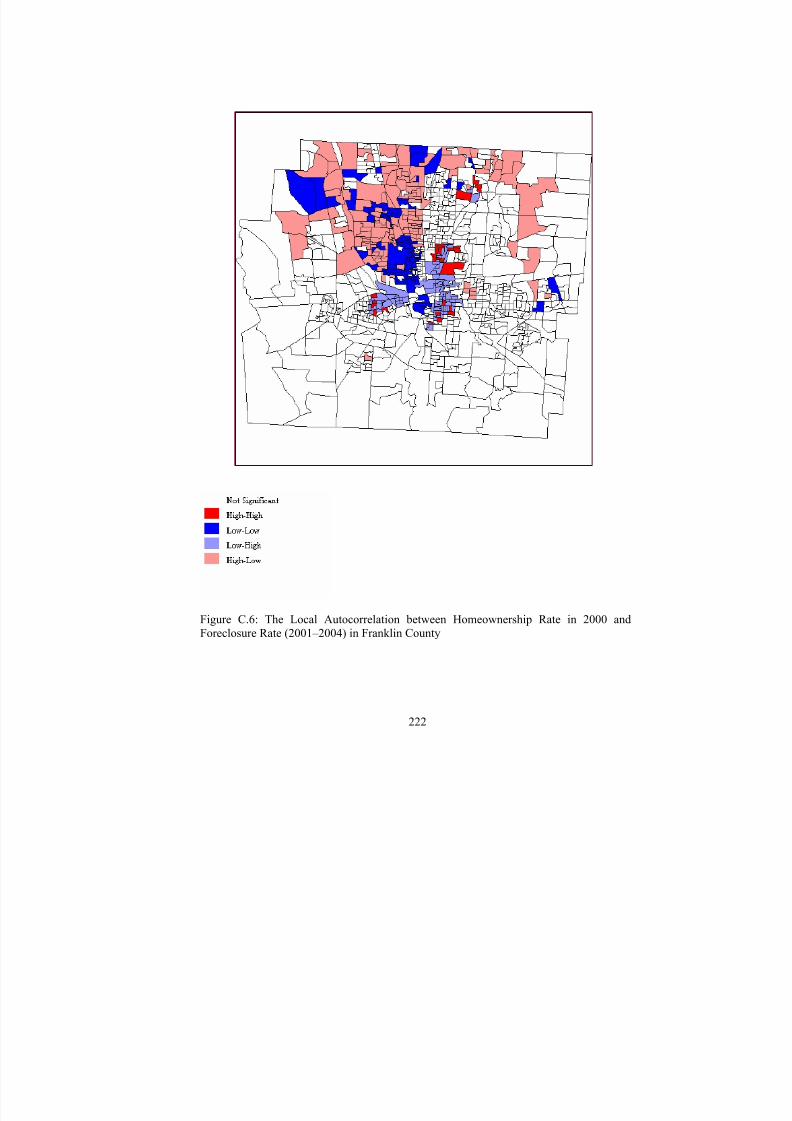

Figure C.6: The Local Autocorrelation between Homeownership Rate in 2000 andForeclosure Rate (2001–2004) in Franklin County ................................................ 222

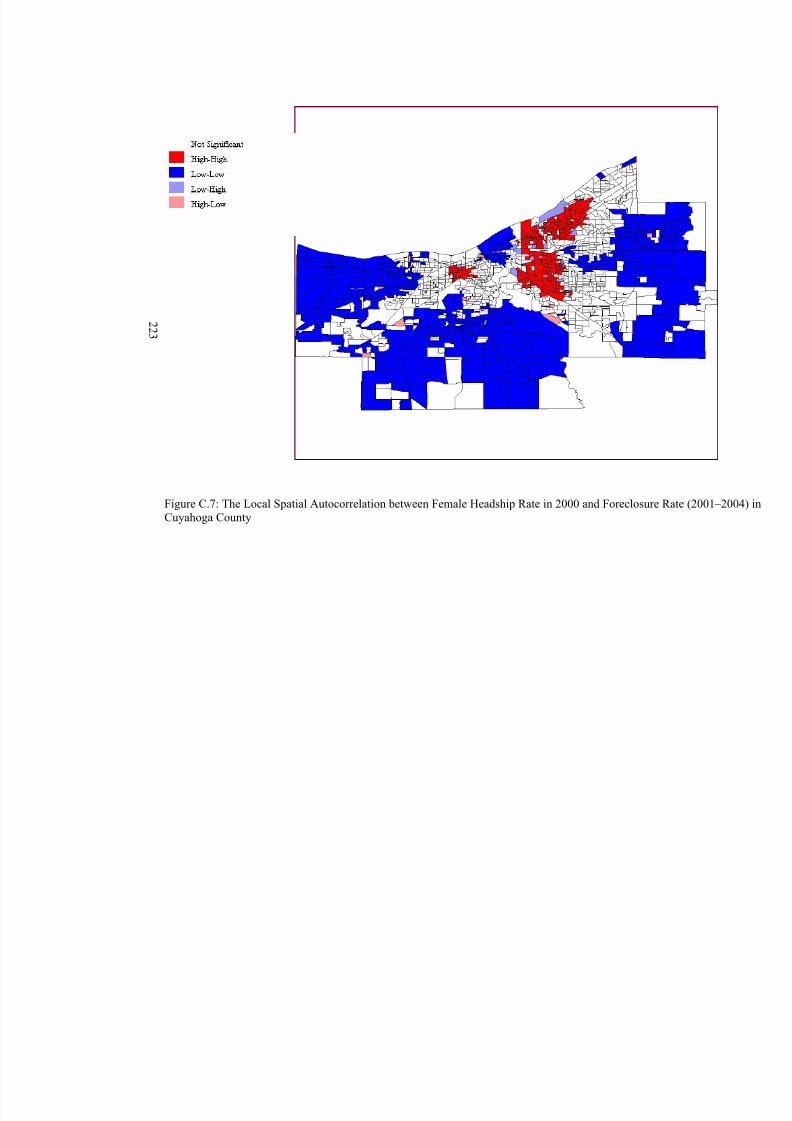

Figure C.7: The Local Spatial Autocorrelation between Female Headship Rate in 2000and Foreclosure Rate (2001–2004) in Cuyahoga County....................................... 223

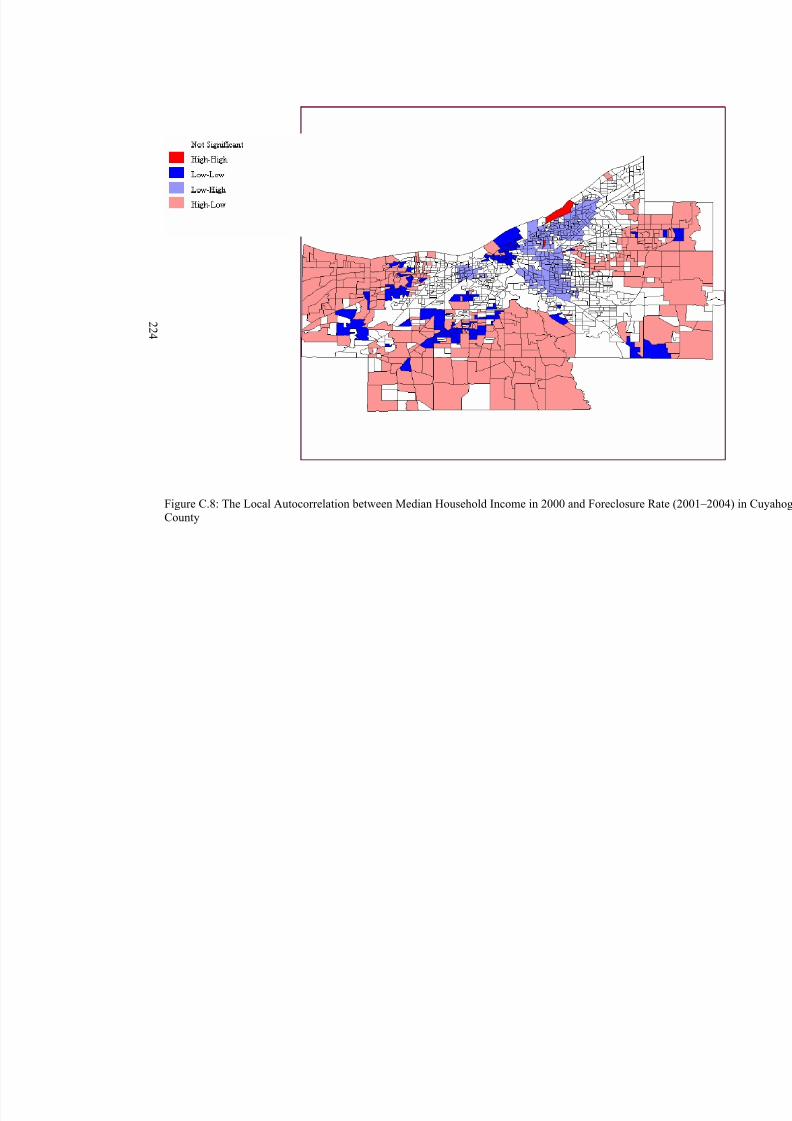

Figure C.8: The Local Autocorrelation between Median Household Income in 2000 andForeclosure Rate (2001–2004) in Cuyahoga County.............................................. 224

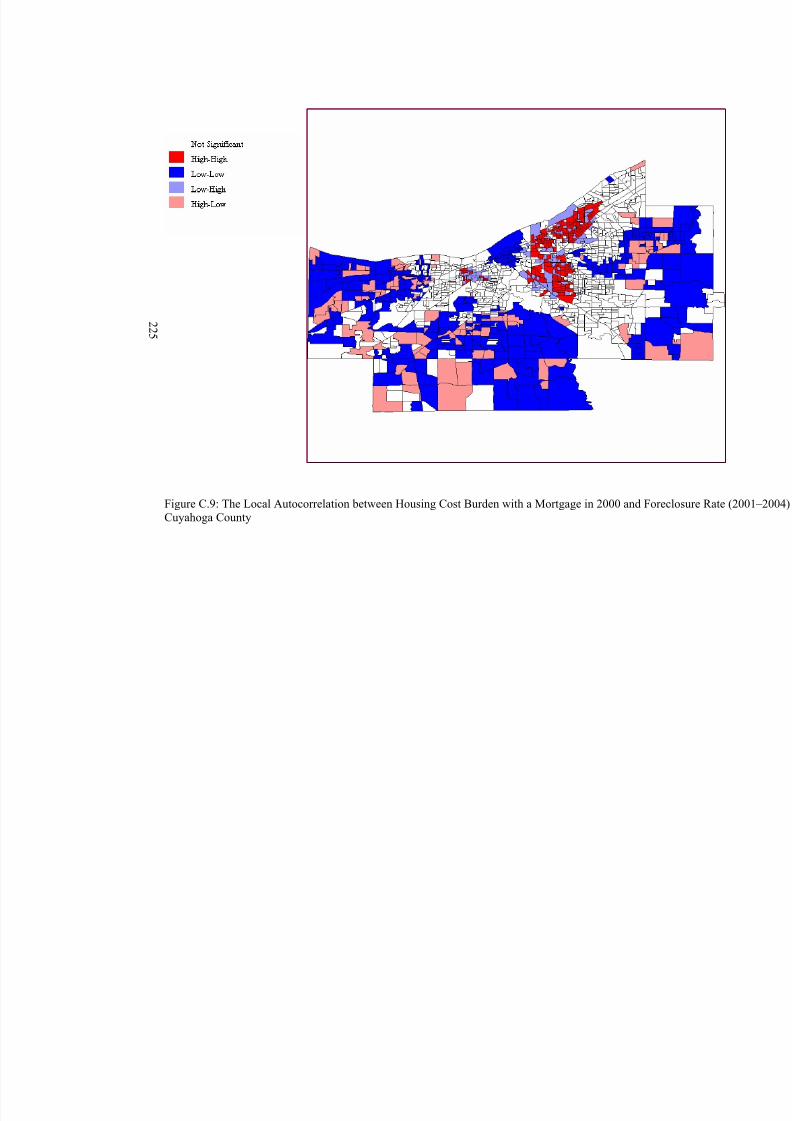

Figure C.9: The Local Autocorrelation between Housing Cost Burden with a Mortgage in2000 and Foreclosure Rate (2001–2004) in Cuyahoga County.............................. 225

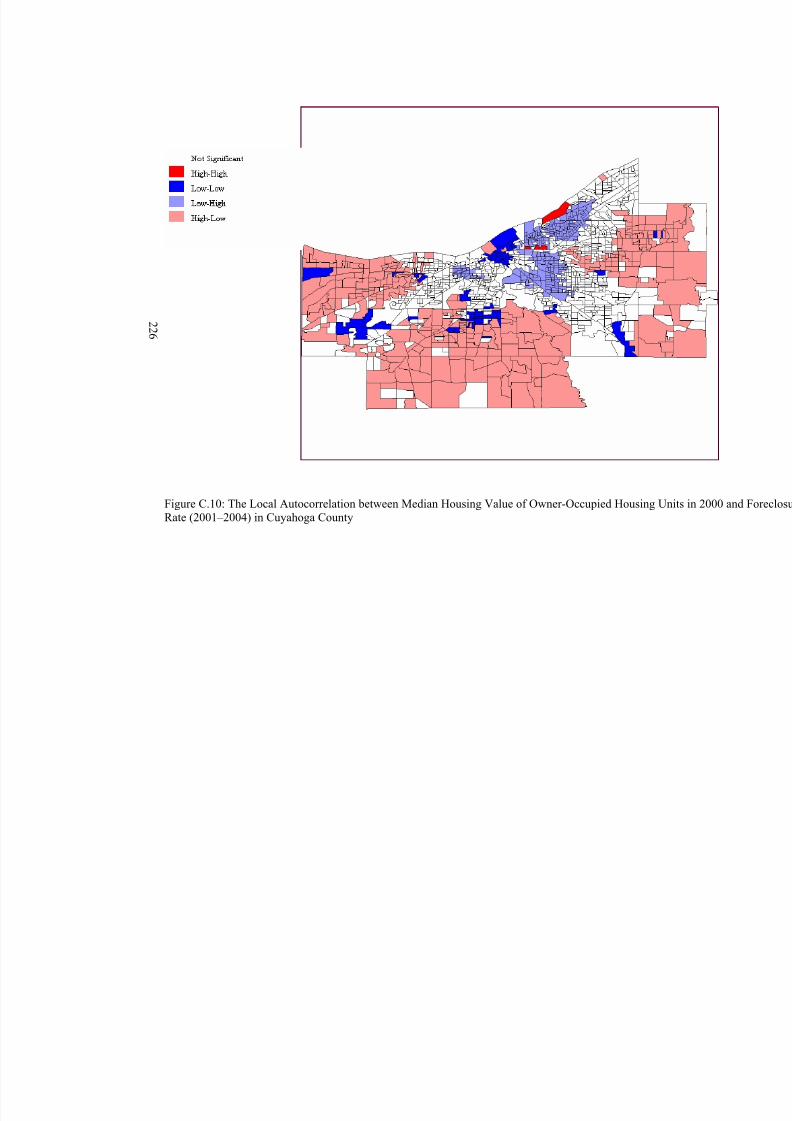

Figure C.10: The Local Autocorrelation between Median Housing Value of Owner-Occupied Housing Units in 2000 and Foreclosure Rate (2001–2004) in CuyahogaCounty..................................................................................................................... 226

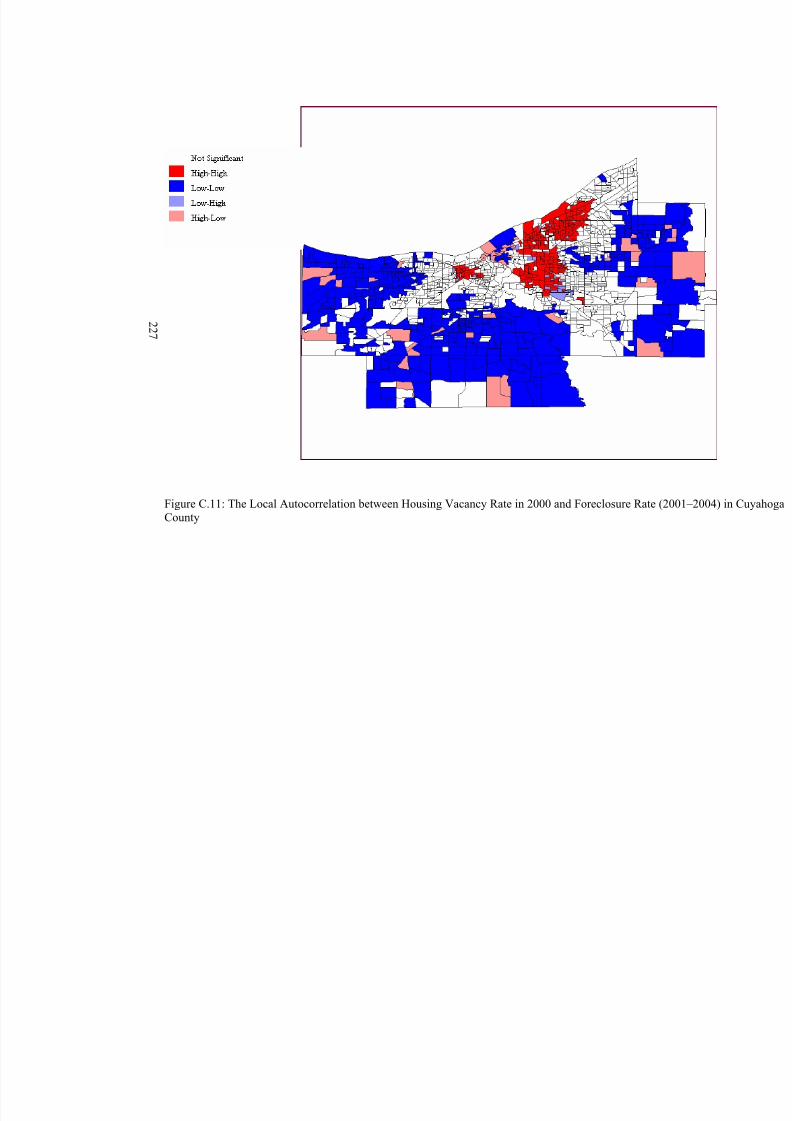

Figure C.11: The Local Autocorrelation between Housing Vacancy Rate in 2000 andForeclosure Rate (2001–2004) in Cuyahoga County.............................................. 227

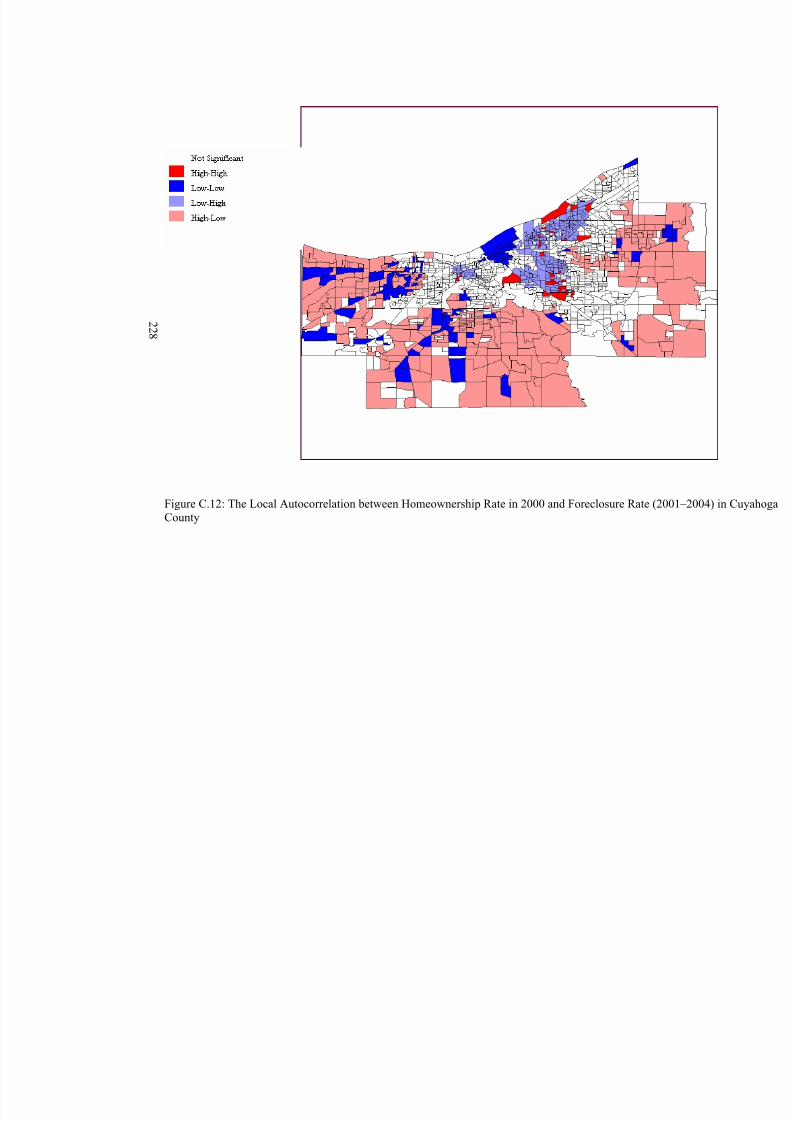

Figure C.12: The Local Autocorrelation between Homeownership Rate in 2000 andForeclosure Rate (2001–2004) in Cuyahoga County.............................................. 228

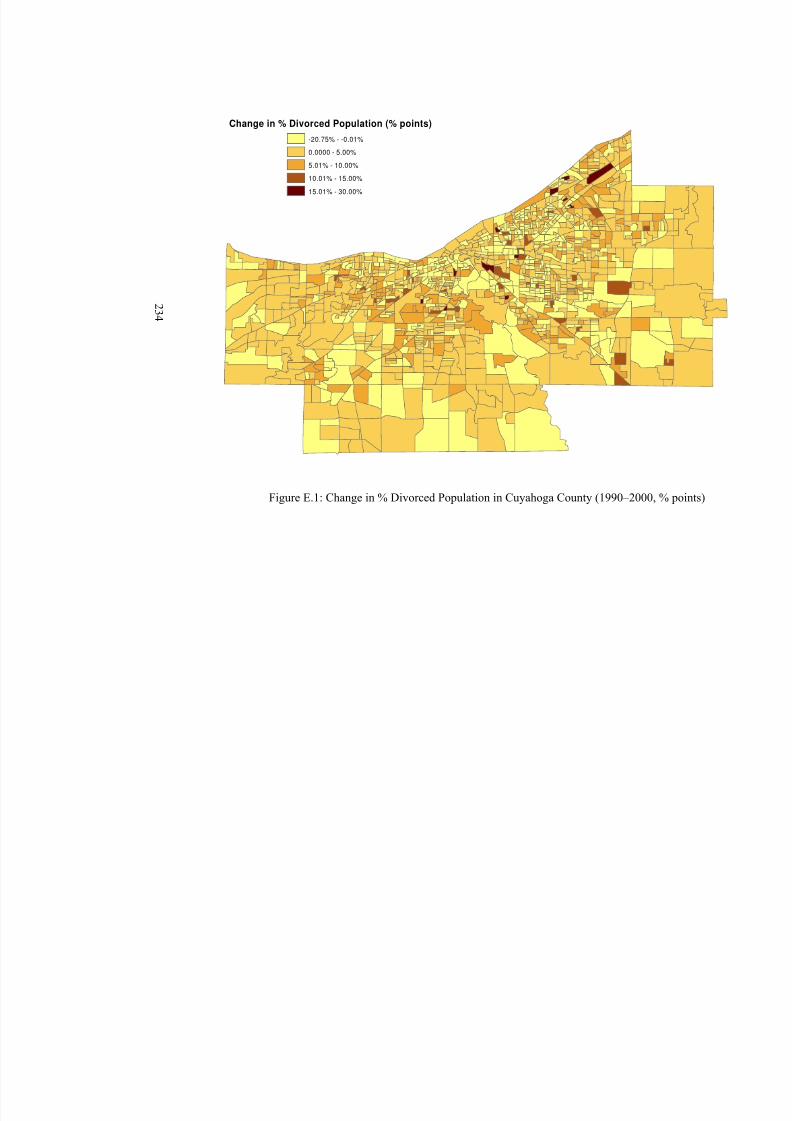

Figure E.1: Change in % Divorced Population in Cuyahoga County (1990–2000, % points) ..................................................................................................................... 234

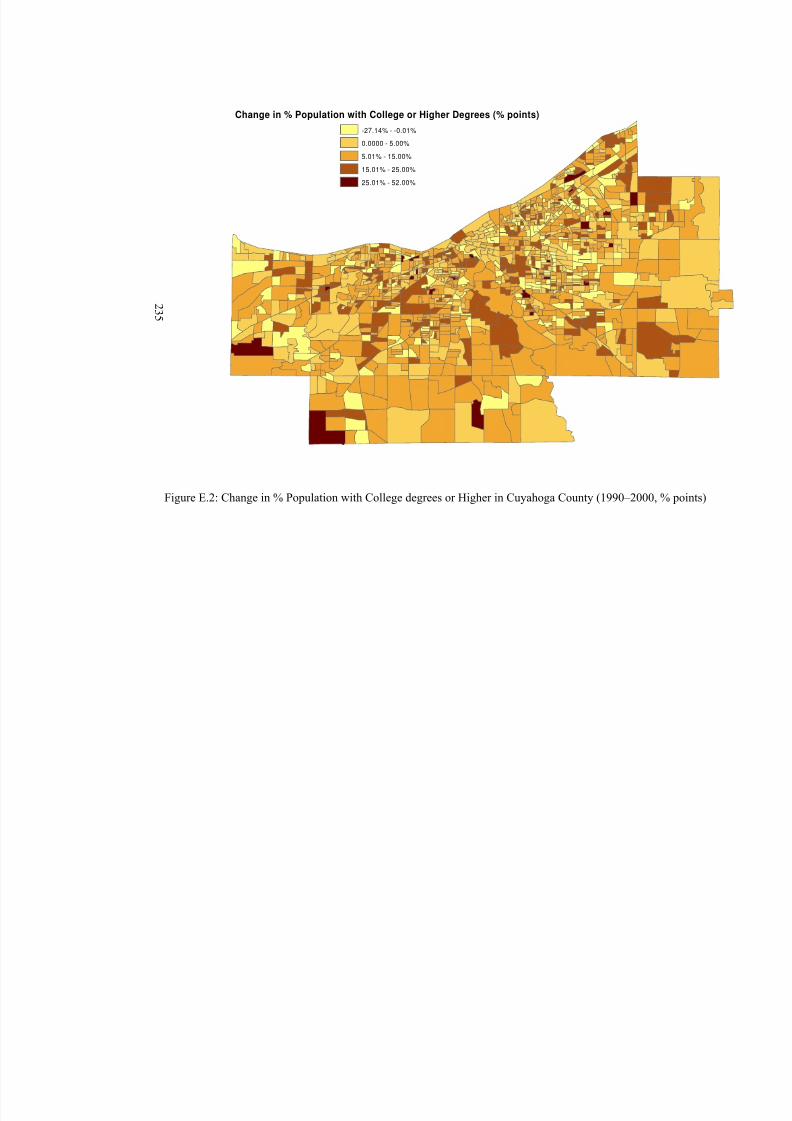

Figure E.2: Change in % Population with College degrees or Higher in Cuyahoga County(1990–2000, % points)............................................................................................ 235

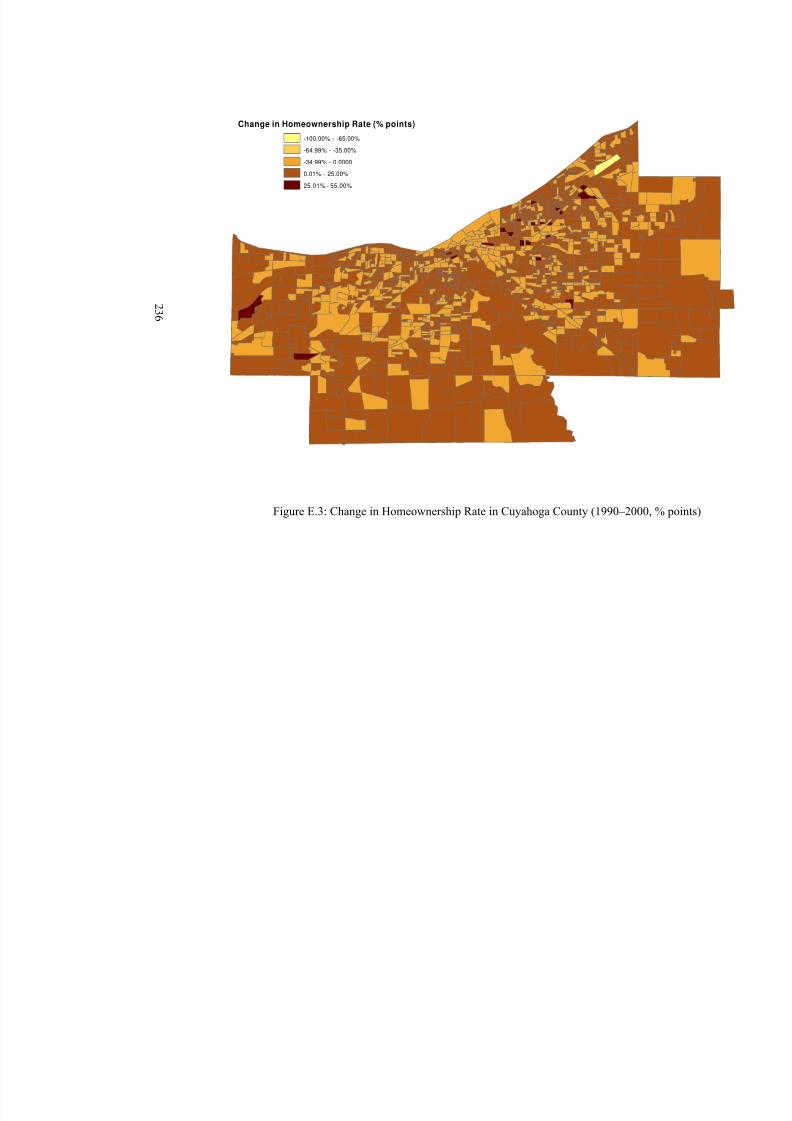

Figure E.3: Change in Homeownership Rate in Cuyahoga County (1990–2000, % points)................................................................................................................................. 236

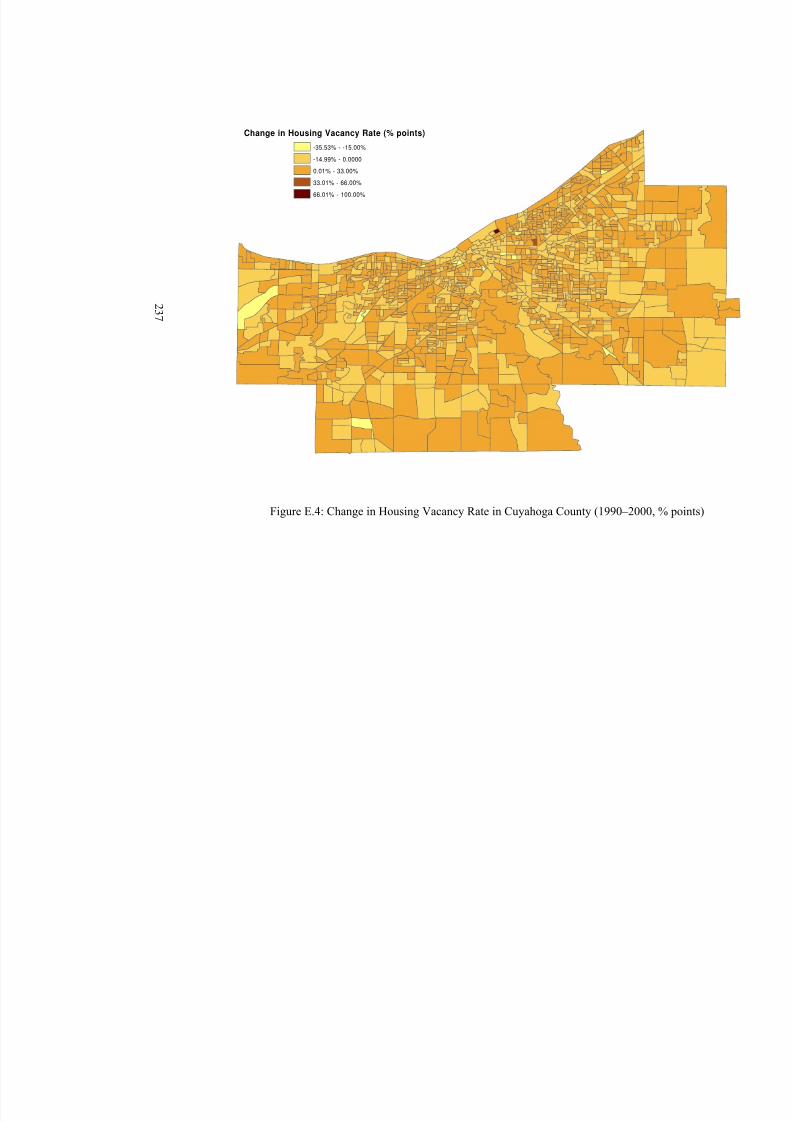

Figure E.4: Change in Housing Vacancy Rate in Cuyahoga County (1990–2000, % points) ..................................................................................................................... 237

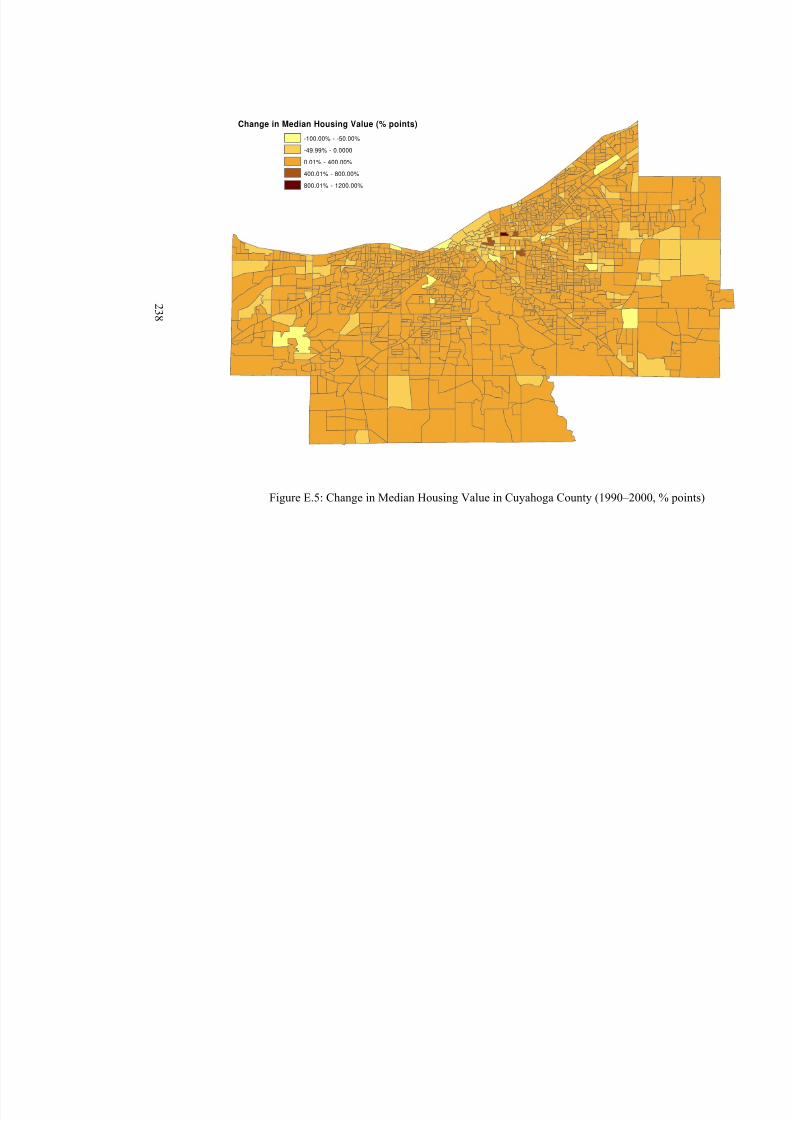

Figure E.5: Change in Median Housing Value in Cuyahoga County (1990–2000, % points) ..................................................................................................................... 238

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 15/268

1

CHAPTER 1

INTRODUCTION AND RESEARCH QUESTIONS

Residential mortgage foreclosures are the processes that homeowners are legally

forced to foreclose on their properties because they default on their mortgage payment.

There are many factors contributing to foreclosures. Foreclosures have profound impacts

on individual homeowners, neighborhoods, mortgage lenders, and policies. As the first

step of a research agenda this project focuses on the interaction between residential

mortgage foreclosures, neighborhood characteristics, and neighborhood change.

Residential mortgage default and foreclosure issues did not attract much attention

until the mid 1970s, when the single-family foreclosure rate in the U.S. began to increase.

Most of the studies since then focused on the factors contributing to mortgage default and

foreclosure, with an emphasis on what financial institutions could do better to manage

their credit risk (Quercia and Stegman, 1992). Since 2000, there has been a dramatic rise

in foreclosure rates, especially in Ohio and Indiana, and it has caused great concern

among policy makers, citizen advocacy groups, fair housing agencies, and other

concerned individuals. This means that many more stakeholders are showing an interest

in mortgage default and foreclosure. The complexity of this issue has increased with the

advent of flexible financial products, along with increasing ethical and legal challenges

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 16/268

2

facing the real estate profession (such as mortgage fraud, incomplete disclosure of costs

associated with mortgages, using a “teaser rate” to confuse loan borrowers, etc.).

Nature of the Problem

There is abundant literature on factors contributing to mortgage default and

foreclosure. Many of the previous studies focused on measuring default risk using

various factors and models, in order to provide more accurate mortgage pricing and risk

management for financial institutions. Neighborhood characteristics are one of the

important sets of factors that should be considered in these models of residential

mortgage foreclosure. But only a few scholars have paid attention to the impact of

neighborhood characteristics on residential mortgage foreclosure (Cotterman, 2001; von

Furstenburg and Green, 1974; Williams et. al., 1974; Sandor and Sosin, 1975).

Residential mortgage foreclosure is an issue in housing markets, and housing

markets are geographically bounded. So mortgage foreclosure, neighborhood

characteristics and neighborhood change are related to each other in complex ways. But,

just as with the studies of neighborhood effects on mortgage default and foreclosure, the

impacts of foreclosure on neighborhood characteristics and change have not been fully

explored, with the notable exception of the studies conducted by Lauria and Baxter in

New Orleans (Lauria, 1998; Lauria and Baxter, 1999; Baxter and Lauria, 2000), and

Immergluck and Smith in Chicago (Immergluck and Smith, 2005a, 2005b).

The interaction between mortgage foreclosure and neighborhood change is very

complicated and is related to many different aspects of housing market equilibrium,

economic development, lender and borrower decision theory and social transition, among

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 17/268

3

other things. In order to examine the interactive relationships between residential

mortgage foreclosure and neighborhood characteristics and change, this study uses

Sheriff’s foreclosure sales data in the two most populous counties in Ohio, Cuyahoga

County and Franklin County, the central counties of the Cleveland and Columbus

metropolitan areas, respectively.

Ohio has one of the highest residential mortgage foreclosure rates in the United

States, where the foreclosure rate is defined as the number of mortgages in foreclosure as

a percentage of all mortgage loans outstanding (Krumkin, 2000). There has been a

tremendous increase in foreclosures in Ohio since 1995. These two Ohio counties provide

good case studies for testing hypotheses about the interaction between mortgage

foreclosure and neighborhood characteristics and change. The Sheriff’s Sales data are

combined with other datasets, such as census demographic data, housing and economic

data, and real property parcel data in each county, to develop a deeper understanding of

the complexities than has been previously available (Cotterman, 2001; Baxter and Lauria,

2000).

Objective of the Research

The objective of this research is to improve our understanding of the complex

relationship between neighborhood characteristics, foreclosure and neighborhood change.

In addition, I hope to make a significant contribution to housing and foreclosure policy in

Ohio. The findings will contribute to both theory and policy on foreclosure and

neighborhood change. The research results will also help target community-based

foreclosure prevention programs to the most at-risk neighborhoods. The document

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 18/268

4

includes suggestions for ways to intervene to reduce foreclosure concentration and the

impacts of such concentration on neighborhoods. The research will contribute to the

limited academic literature on this topic by adding significant work over time and across

space, allowing an analysis of the context within which foreclosure occurs. The explicit

consideration of racial issues and the problem of house price depreciation incorporated in

this analysis will also enhance the existing models.

Research Questions

There are three primary questions that the research tries to answer. Following each

question are more detailed hypotheses.

1. Do neighborhood characteristics and changes affect residential mortgage default and

foreclosure? If so, how?

If the answer to this question is yes, several subsidiary questions need to be

addressed. For example, what neighborhood factors contribute to mortgage default risk

and rising mortgage foreclosure rates? What kinds of neighborhoods have seen the

highest increase in foreclosure sales? Why do different neighborhoods have different

foreclosure rates? Do the phenomena follow certain patterns over time in different

metropolitan areas?

2. Do mortgage foreclosures affect neighborhoods? How and under what circumstances?

According to previous research, mainly by Lauria and Baxter (1998, 1999, 2000),

the impact of mortgage foreclosure on neighborhoods in which foreclosed properties are

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 19/268

5

located is very significant. They found important impacts on racial transition and general

economic condition of the neighborhoods.

Properties in some neighborhoods tend to have a lower price appreciation (Oliver

and Shapiro, 1995; Raffalovich, 2002; Shapiro, 2004), which in turn makes it more likely

that people will default on mortgages because a lower appreciation rate or depreciation

will decrease the property’s real value, and that leads to less equity. If values depreciate

enough, the property could end up with negative equity. Negative equity is one of the

leading reasons for people to default on mortgage payments (Case and Shiller, 1996;

Cunningham and Capone, 1990). Higher foreclosure rates in a neighborhood can

decrease housing values in the neighborhood and make price appreciation even lower,

thus making more people likely to default. On the other hand, the characteristics of the

residents of these neighborhoods must also be taken into account as those characteristics

could tend to lead to higher default rates. Thus, the complexity of the geographic

relationships, as well as the interdependencies of the people and the neighborhoods,

requires special attention. In this research, in addition to the racial composition and

general economic condition of neighborhoods, housing price appreciation and other

housing stock characteristics of neighborhoods are explored to find out whether and how

mortgage foreclosure affects housing price appreciation and neighborhood stability.

3. Can we model the cyclical nature of the relationship between neighborhood

characteristics, neighborhood change and foreclosure rates?

The first two research questions indicate that separating the impact of

neighborhoods on foreclosures from the impact of foreclosures on neighborhoods is a

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 20/268

6

crucial methodological problem. Thus, in order to address these two substantive

questions, the research must address the methodological question that is relevant to many

neighborhood-effects studies. Neighborhood-effects research is a controversial area of

inquiry in social sciences (Dietz, 2002), although there is abundant literature addressing

research methods in the area. There are several difficult problems in this area of research,

including endogenous effects, omitted variables, and reflection problems (Dietz, 2002;

Manski, 2001). My research develops a model to deal with the nonrecursive nature of the

relationship between neighborhood characteristics, neighborhood change and foreclosure

rates, taking into account the possibility of endogenous effects, omitted independent

variables and the reflection problem (Dietz, 2002).

Scope of the Research

The major datasets used for this research are the Sheriff’s deed transfer data from

1997 to 2004 (in Cuyahoga County the data from 1983 to 1989 are also used), the census

block group data from 1990 and 2000, the census designated place data from 1990 and

2000, and real property parcel data from 2004 and 2005. These datasets were merged for

analysis purposes. More details in the data sets and the methodologies are included in the

relevant chapters. The second chapter of this dissertation provides the literature review

and conceptual models. Then I turn to the results.

The first section of results provides the descriptive and spatial analyses of the

foreclosure patterns in each county, and their relationships with selected neighborhood

characteristics.

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 21/268

7

The second results section reports the outcomes of the advanced spatial analysis and

the spatial modeling. Spatial autocorrelation analysis measures how spatial

autocorrelation affects the regression results and how the spatial lag and error models

differ from the Ordinary Least Square (OLS) regression models when using

neighborhood variables to predict foreclosure rate.

The third section of the results formulates a Seemingly Unrelated Regression (SUR)

system to measure how foreclosure rates and other neighborhood and place-characteristic

variables affect each selected neighborhood change variable in each county.

In the final chapter of the dissertation, the major findings from the research will be

used as the basis for policy suggestions to help policy makers be aware of the spatial

patterns of foreclosure, the mutual impact of neighborhood variables and foreclosure, and

the specific neighborhood factors that are highly related to foreclosure. Targeted policies

can be created to manage neighborhood variables identified in this research in order to

break the cyclic nature of the relationship between neighborhood characteristics and

foreclosure. The establishment of spatial analysis and models and SUR models in the

research will provide an effective method for analyzing similar research questions, and

the combination of these spatial and quantitative models will contribute to foreclosure

research.

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 22/268

8

CHAPTER 2

LITERATURE REVIEW

Residential Mortgage Foreclosure

Concepts of Mortgage Delinquency, Mortgage Default and Foreclosure

Mortgage foreclosure is “the process by which the mortgage originators claim legal

rights to the property by foreclosing the mortgage in the event of mortgage default”

(Frumkin, 2000). A mortgage delinquency, which usually means a mortgage repayment is

overdue 30 days or more, becomes a mortgage default when it is overdue by more than

90 days. When the mortgage is in default, the lender may choose to work with the

borrower to see if the loan can be modified or brought back to a normal balance. When

these efforts fail, the lender will usually file a foreclosure with the court to claim its legal

rights under the mortgage. Many studies treat “default” and “foreclosure” as synonymous

(Goering and Wienk, 1996), but in fact, default is incurred and affected by borrowers’

choices, while foreclosure is one of the options available to lenders to enforce the

repayment of a mortgage in default. This research will treat default and foreclosure as

two related but different processes.

A civic real estate sale is the final procedure in a judicial foreclosure process. The

property can be withdrawn from this process if the borrower(s) file for bankruptcy, bring

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 23/268

9

the back payments up to date, sell the property, legally cancel the mortgage, or resume

the mortgage repayments.

In contemporary U.S. society, with its mature financial markets and innovative and

flexible financial products, buying a home has become much easier. Homebuyers do not

need to accumulate large amounts of savings in order to purchase a house. When certain

conditions are met, they can readily obtain a mortgage to finance a home purchase,

although different financial agencies might have different underwriting standards.

When a borrower obtains a mortgage to buy a house, a scheduled repayment of the

mortgage is incurred. This schedule is determined by the loan-to-value ratio, loan term,

mortgage interest rate, and interest compounding factors. But the mortgage performances

of borrowers differ greatly and are related to the differences in household characteristics,

such as income, family structure, and mobility decisions, and to the general economic

context, including recessions, interest rates and so forth. Mortgage performance includes

timely submission of mortgage payments, prepayment behavior, refinancing behavior,

mortgage delinquency and mortgage default. Of these behaviors only mortgage

delinquency and default are related to a possible change of homeownership status of

borrowers and the risk of borrowers losing their homes if they are not able to resume the

mortgage repayment.

Mortgage delinquency usually means missing one scheduled payment. At that time,

lenders cannot tell whether the payment will be continued or stopped in the next payment

cycle. But if several payments are missed, usually three (Quercia and Stegman, 1992),

lenders will consider borrowers to have defaulted. The criteria that determine a default

vary among financial institutions. When a loan defaults, lenders will choose either to use

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 24/268

10

loss-mitigation techniques to work with the borrowers to resolve the issue and resume the

payments, or foreclose the mortgage by auctioning the mortgage property to cover the

loan balances of the borrowers (Capone Jr., et. al., 1996). Lenders choose the option that

costs the least to process. If the costs of working out the troubled loan are much larger

than foreclosure costs, lenders prefer to choose foreclosure. On the other hand, many

lenders are willing to work with borrowers first to find ways to resolve the issue. If this

cooperation fails, a foreclosure action will be filed in the local civic court or a non-

judicial trustee’s sales process will be initiated. A civic real estate sale is the final

procedure in a judicial foreclosure process.

The decision of whether to choose foreclosure depends greatly on state legislation

(Clauretie, 1987). In a non-judicial process, when loans are in default a notice of default

will be issued to the borrower. Then, if the borrower cannot repay the back payments, a

trustee’s sale will be initiated to sell the foreclosed properties. Thus a non-judicial

foreclosure does not need the involvement of courts and Sheriff’s Offices. But the

judicial process starts with foreclosure filings to the local court. Then, if the borrower

cannot walk out of the foreclosure process (e.g. cannot sell the property before the

auction, or get a bankruptcy), the court will order a Sheriff’s sale. Both judicial and non-

judicial processes have advantages and disadvantages. The biggest advantage of the

judicial process is the legal guarantee that helps the involved parties avoid disputes in

titles and other real estate claims. However, judicial foreclosure is much more expensive

in terms of legal fees and is more time consuming than non-judicial processes. Many

states in the U.S. allow both judicial and non-judicial processes, but Ohio only allows a

judicial process (see Appendix A for a detailed description of the process).

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 25/268

11

According to research conducted by Clauretie (1987), states without judicial

foreclosure usually see a higher foreclosure rate because of the low foreclosure costs,

controlling the time span of the foreclosure process. This makes Ohio’s high foreclosure

rate even more surprising.

Previous Research on Mortgage Default and Foreclosure

Studies on residential mortgage default have changed over time. Many have focused

on lenders’ and financial institutions’ need to understand the mechanisms in mortgage

default. Using these studies, financial institutions have sought to minimize mortgage

default risk and losses associated with the risk. Only in recent years has research on the

social impacts of mortgage default and foreclosure begun to appear in the academic

literature. But the recent research still has not resolved some essential issues related to

foreclosure, such as whether there are racial differences in mortgage default decisions,

how and where the households move after they lose their homes due to the foreclosure

process, and how those changes affect the structure of a neighborhood.

Three Generation’s Research on Mortgage Default

In the early 1990s, Quercia and Stegman (1992) summarized the literature on

residential mortgage default. They provided a comprehensive analysis of mortgage

default risk from three different perspectives, that of lenders, borrowers, and institutions,

each of which is associated with a research generation. These perspectives have

contributed to the mortgage default literature either theoretically or empirically. Their

research also tried to seek different indicators to measure mortgage default risk, such as

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 26/268

12

default rates, expected mortgage losses, and interest rate premiums (Quercia and

Stegman, 1992).

The first generation’s studies were from the lender’s perspective. Minimizing credit

risk is one of the essential activities in the daily management of financial institutions

(Saunders and Cornett, 2003). The goal of lenders facing mortgage default by borrowers

is to lower the costs associated with defaults and foreclosures. This stream of research

found that mortgage default rates are correlated with loan characteristics, borrower

characteristics and property characteristics. For example, loans with higher loan-to-value

ratios, higher interest rates and longer terms are much more likely to be in default

compared to the reverse characteristics of those indicators. Higher initial payment-to-

income ratio, properties with poor conditions and unstable neighborhoods usually are also

associated with a higher default risk.

The second generation’s research was from the borrower’s perspective and probed

borrower payment models. The models are based on utility (net wealth) optimization in

consumer theories and option-based choices. The utility (net wealth) optimization

theories indicate that when borrowers make decisions (timely payment, prepay, refinance,

or default) in their mortgage performance they base those decisions on the maximization

of their net wealth. The option-based models view default as a put option, where the

borrowers can sell the property back to the lender for the value of the mortgage at the

beginning of each payment period. Those mortgage performance choices are determined

by many factors, such as transaction costs, family crises and mobility decisions.

The third generation’s research was from the perspective of large financial

institutional loan pools and financial regulators. The research explored, for example, how

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 27/268

13

default happens on an FHA-insured mortgage or on a fixed-interest mortgage, and how

some regulations (e.g., capital requirements) affect mortgage default. But the studies of

the third generations are more complete and have considered the roles of all three sectors:

lenders, large financial institutions and regulators, and borrowers.

Quercia and Stegman concluded that there are still some obstacles in the research.

One of the greatest is the lack of data about changes to borrower, lender and property

information over time, which limits the research to some extent. But the most difficult

problem is the lack of data about borrower’s issues and decisions. They also indicate that

mortgage default models need to incorporate not only the role of borrowers but also the

mobility decision of borrowers.

Mortgage Default and Foreclosure Factors

There are many factors determining the possible mortgage default risk of certain

loans, but loan-to-value ratio, payment-to-income ratio, householder’s occupation (with

or without volatile income), property and neighborhood condition, regional

unemployment rate, transaction costs, crisis events, and borrowers’ expectations are some

of the major elements contributing to the risk of mortgage default and foreclosure

(Quercia and Stegman, 1992; HUD, 1992; Vandell and Tribodeau, 1985).

Among those factors, the macro economic situation, housing price appreciation and

neighborhood characteristics are macro spatial factors that help determine borrower

characteristics in certain geographical areas and, therefore, the loan characteristics

associated with those borrowers. Using those factors, loan default risk in certain

geographical areas can be measured. According to previous literature on mortgage default

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 28/268

14

and foreclosure, the following is a list of major factors contributing to mortgage default

and foreclosure, although some of them are correlated to others:

• Macro economic situation

• Mortgage loan characteristics

• Types of Mortgage Products

• Borrower characteristics and default decisions

• Mortgage lending legislation and foreclosure legislation

• Lender decisions in mortgage foreclosure

•

Housing attributes

• Housing appraisal

• Housing price appreciation

• Mortgage fraud

• Neighborhood characteristics.

I will discuss each of these briefly, though they are not the focus of this dissertation.

Macro economic situation

Studies have found that mortgage default is largely related to macro economic

changes over time. The most obvious indexes that are associated with mortgage default

are the unemployment rate, interest rate, and housing price index.

Bellamy (2002) found that in Ohio between 1994 and 2001 the unemployment rate

fell consistently, with minor volatility, but foreclosure filings increased consistently.

Therefore, he suggested that the increasing foreclosure rates in Ohio are not solely

dependent on the economic situation. A report from Policy Matters Ohio in 2004 assumes

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 29/268

15

a weak economy since 2001 to be one of the leading reasons for the high foreclosure rate

in Ohio in recent years. Case and Shiller (1996) found that high mortgage default rates

“strongly follow” real estate price declines or interruptions of real estate price increases.

Also, mortgage delinquency and foreclosure rates themselves are important economic

indicators (Frumkin, 2000).

Mortgage Loan Characteristics

Loan characteristics are important factors that can affect mortgage defaults and

foreclosures. In early research there were many interesting findings, such as that the

interest risk is one indicator of mortgage risk, and a higher loan-to-value ratio means

more default risk.

Many studies found that the initial loan-to-value (LTV) ratio has a significant

influence on mortgage default (Von Fustenberg, 1969, 1970a, 1970b; Deng and Gabriel,

2002; Calhoun and Deng, 2002; Ambrose et. al. 2002). The LTV ratio directly

determines the equity position of a borrower (HUD, 2004), and HUD found that a high

LTV ratio is associated with a high default rate by examining FHA-insured and GSE

(Government Sponsored Enterprises: Fannie Mae, Freddie Mac and Ginnie Mae)-

purchased loans. Von Furstenberg (1969, 1970a, 1970b) thought that home equity at the

time of loan origination is highly related to mortgage default. When the LTV ratio is

raised by seven percentage points from 90% to 97%, default rates for new homes increase

by seven times. But research found that in subprime mortgages the LTV has little effect

on loan performance (OCC, 2003). Quercia et.al. found that LTV ratio does not affect

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 30/268

16

default in their panel data of rural low-income mortgage borrowers (Quercia et. al.,

1995).

Interest rates that financial institutions charge to loan borrowers reflect the

expectations from the lenders about default potential. The lenders are hedging possible

losses from credit risk, so interest rate should be related to mortgage default risk (Jung,

1962). The yield curve slope therefore should be a factor contributing to mortgage

defaults (HUD, 2004). This hypothesis was later proven by other research. For example,

Page (1964) found that default risk was related to property values; financial institutions

are willing to issue loans with a lower interest rate to borrowers purchasing a high-value

property. A borrower who caught a loan to buy an expensive house probably has good

credit so their interest rate is low. In a situation of burnout1, where borrowers passed up

some previous good opportunities to refinance the mortgage at a more favorable interest

rate, they have a higher tendency to default because of the high interest rates (HUD,

2004). Ambrose and Sanders (2003) also found that the change in yield curve has a direct

impact on the probability of mortgage default.

Besides interest rates and LTV ratios, loan term length and the age of the mortgage

are also important factors (von Furstenberg, 1969). Von Furstenberg (1969) found that

mortgage default risk positively correlates with the term of the mortgage and a mortgage

younger than 3 or 4 years is at higher risk as well.

HUD (2004) found that loan size is also a factor in determining loan default risk by

exploring both PMI (Private Mortgage Insurance) and FHA loan data. Smaller loan sizes

usually are associated with a higher default rate, which might be because that low-income

borrowers, low-liquid-asset borrowers, or borrowers with high income-volatility tend to

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 31/268

17

have smaller loans. That can also indicate high housing price volatility in low-priced

houses.

Quercia and Stegman (1992) stated that default patterns for adjustable rate

mortgages (ARMs) were not comprehensively studied before. With ARMs, payment

shock due to unexpected interest rate increase is one of the important reasons for people

to default. Early ARM payment accounts for the impact of the change of payment coupon

from an initial low rate (“teaser rate”) to an index-adjusted rate during the first year of the

loan. Therefore, early ARM payment can also explain some of the default risk.

Another factor contributing to mortgage delinquency and default is the presence and

holding status of junior or subordinate loans and liens (Herzog and Earley, 1970; LaCour-

Little, 2004). Their research found that junior or subordinate loans and liens might

increase the default risk of primary loans.

Types of Mortgage Products

Product types such as FHA-insured, VA-insured, Conventional, ARM, FRM (Fixed

Rate Mortgage), GRM (Graduated Rate Mortgage) and subprime loans affect mortgage

default risk due to their own characteristics. According to the Mortgage Bankers’

Association, FHA loans usually have a higher foreclosure rate than conventional

mortgages. But determinants of delinquency rates in different types of loans are different,

especially for some non-profit community lending organizations in which social

networks, business culture, funding sources, composition of the board and loan

committees, staff structure, loan intake, and collection tools are major organizational

factors affecting loan delinquency rate (Baku and Smith, 1998).

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 32/268

18

The role of subprime and predatory lending on increasing mortgage foreclosures is

addressed by many previous studies and in different states such as Ohio, Indiana and

Arizona (Realtors, 2003; Goldstein, 2004; Rhey and Posner, 2004; Stock et. al., 2001). A

study of the differences in mortgage default rates of prime and non prime mortgages

indicates that these mortgages are significantly different in many aspects, such as

different risk levels at the loan origination. They both default at elevated levels but

respond differently to incentives to prepay or default (Pennington-Cross, 2003). The

study also found that mortgage default is less responsive to the amount of equity when

credit scores are included in the analysis.

Borrower Characteristics and Default Decisions

Default decisions made by borrowers are determined by many factors. A default is

usually due to two situations: inability to pay and/or unwillingness to pay. Those two

scenarios should be separated when exploring mortgage default decisions. In addition to

factors described in the preceding section on borrower characteristics in mortgage default

risk models, certain events such as changes in borrower characteristics and life crises can

also make borrowers choose default. The most important such factors are job loss, family

structure change (such as divorce, children going to college, or decease of a financially

supportive adult), and moving.

When terminating a mortgage, the decision of a household to default is determined

by the borrower’s perception of the value of the mortgage versus the value of the home.

When the house is perceived to be less valuable than the outstanding mortgage balance, a

decision to default might be made and this is a voluntary default decision. Another

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 33/268

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 34/268

20

and credit history on mortgage default risk, recent research has begun to focus more on

comprehensive loan characteristics, borrower characteristics, and property and

neighborhood characteristics.

The payment-to-income ratio is thought to have a significant effect on mortgage

default, but empirical studies show mixed results. Therefore, we cannot say that its

impact on mortgage default is significant (HUD, 2004).

Earlier research found that the effect of income on mortgage default was ambiguous

(HUD, 1992). However, Van Order and Zorn (2002), in a recent study of competing risk

of mortgage termination, found that borrower income is an important determinant for

mortgage default decisions when the borrower’s property has negative equity. Although

few studies have focused on income levels, many have tried to examine the impact of

income variability (stability and growth) on mortgage default. Van Order and Zorn

(2002) also found a positive relationship between income variability and the mortgage

default rate. This means that high volatility of income is usually associated with a high

default rate. Borrowers with certain occupations, such as those who are self employed,

those whose major income depends on commissions, and those with low-skilled jobs

(HUD, 2004), have high income volatility. Research also found that borrowers with low

liquid assets have a higher mortgage default probability (HUD, 2004).

In several studies the impact of a borrower’s ethnic background was greatly reduced

by controlling other characteristics, such as down payment and credit history (Cotterman,

2002; Van Order and Zorn, 2002). Therefore, many researchers believe that loan default

differences among different racial groups can be better explained by down payment

amount and credit history of the borrowers. Some think that racial minorities are more

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 35/268

21

likely to become targets of predatory lending, but little attention has been paid to possible

racial disparities in mortgage performances, mortgage default and mortgage foreclosures.

Only in recent years have some scholars noticed this issue (Lauria and Baxter, 1999;

Lauria, 1998; Baxter and Lauria, 2000).

Mortgage default will affect the future credit worthiness of a borrower. But for some

borrowers, repeated mortgage decisions can be observed. Ambrose and Capone (2000)

found that borrowers with a first default have a greater risk for a second default, and the

risk is also greater when the time difference between two defaults is shorter than two

years. They also found that the economic factors affecting the first default have no effect

on the second default. The findings of this study imply that the ability of borrowers to

obtain another mortgage will be lower since they have been found to have a higher

default probability in their second mortgage.

Mortgage Lending Legislation and Foreclosure Legislation

The impact of mortgage lending legislation on foreclosure is under-investigated

because of the difficulty of evaluating how legislation contributes to foreclosure. But

recently, with the increasing awareness of mortgage foreclosure, some non-profit

organization and concerned citizen groups have begun to question whether loose

mortgage lending legislation and regulations are an important factor affecting

foreclosure. They might especially affect the geographically clustered distribution of

foreclosure in low-to-moderate-income neighborhoods. The major agenda that these

groups propose is to enact anti-predatory lending legislation and require real estate and

mortgage brokers/agents and real estate appraisers to pass stricter licensing exams. At the

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 36/268

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 37/268

23

State bankruptcy laws also have some impact on default decisions of borrowers. Lin

and White (2001) found that in states with higher bankruptcy exemptions borrowers have

greater tendencies to choose default.

Lender Decisions in Mortgage Foreclosure

There are three possible outcomes when a mortgage is defaulted: (1) resumption of

payments, (2) termination by prepayment, or (3) foreclosure (Phillips and VanderHoff,

2004). The value of termination options and local economic and housing market

conditions affect default resolution probabilities greatly. After a study of loan pools in a

large national savings and loan institution, Phillips and VanderHoff (2004) found that

judicial procedure and tenancy statutes decrease the probability of foreclosure by 25%,

due to the increasing costs of foreclosure. They also indicate a possibility of adjusting

mortgage rate premiums to compensate the added costs to lenders.

For FHA-insured loans, lenders do not bear many foreclosure costs when

foreclosures occur (Realtors, 2003). This could be one of the reasons why FHA loans

have a high foreclosure rate.

The amount of time between mortgage default and foreclosure is different

depending upon the mortgage interest rate and home equity values (Lauria, 2004). Lauria

found that lower interest rate loans and loans with an outstanding balance below the

median value of the home were given a longer time from default to foreclosure. Whether

there is racial discrimination in the foreclosure process is still unclear.

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 38/268

24

Housing Attributes

Housing attributes, such as the number of bedrooms in a dwelling and the units in

the building, building type, and building year, are important factors in loan approval in

the automated mortgage scoring system of many types of mortgages, and this is where

home equity values could go. Therefore they can be important indirect factors affecting

mortgage default risk (Sandor and Sosin, 1975).

Housing Appraisal

In research on the role of real estate appraisal on mortgage lending and performance

in Alaska’s housing market, Lacour-Little and Malpezzi (2003) found that if the appraisal

value of a property is higher than the estimated price from a hedonic model they

developed, the mortgage against this property is exposed to more default risk. In other

research, Lacour-Little and Green (1998) found that minorities and minority

neighborhoods are much more likely to get low appraisals, which increases the loan

application rejection rates of racial minorities. But they found that the low appraisal is

related to poor neighborhood and housing quality. Noordewier et. al. (2001) found that

properties with a higher appraisal value than similar recently sold properties are related to

higher default risk of the borrowers.

Housing Price Appreciation

Housing price change is a very important factor in determining mortgage default

probabilities. This is true, first, because of the possibility of negative equity, which

affects mortgage default decisions greatly (Quigley et. al., 1993), is largely determined by

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 39/268

25

housing price changes (Case and Shiller, 1996). Second, as housing prices fall, the loss

severity followed by a default increases, and loss severity increases non-linearly and

faster than the decline of housing prices (Case and Shiller, 1994). Third, the research on

housing price appreciation in low-income and/or minority neighborhoods should help

explain the disparities among mortgage foreclosure rates in different neighborhoods

(Raffalovich, 2002). By examining neighborhood effects on FHA-insured loans,

Cotterman (2001) found that low housing price appreciation in minority neighborhoods is

an important factor in the higher default rates in those neighborhoods.

Housing price appreciation is also an important motivation for people to move

(Kiel, 1993). When a moving decision is made, borrowers will choose either to sell or

default on the property in which they currently reside (Pavlov, 2001). When the equity

value is positive they will usually choose to sell the property and prepay the mortgage.

But when the equity value is negative and cannot offset default costs, they will choose to

default. However, only a small percentage of borrowers actually choose to default in this

situation. Their decision might be more determined by life crisis events because choosing

default is costly for borrowers in regard to its negative impact on borrower credit scores

(HUD, 1992; Foster and Van Order, 1985).

Mortgage Fraud

Foreclosure cases because of mortgage fraud are few and there is no literature

related to the relationship between mortgage fraud and foreclosures. Hence there are no

empirical studies conducted to see how mortgage fraud affects foreclosure. The definition

of mortgage fraud can be very broad, but here it means that lenders use some illegal

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 40/268

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 41/268

27

and other minorities are required to have a higher standard than Whites in loan approval,

and thus Blacks and other minorities have a lower tendency to default because those who

can have a loan are those who meet the higher standards; also “minorities tend to have

less attractive distributions of factors leading to default” compared to whites because of

the more strict underwriting standards (Cotterman, 2004). But a study by Berkovee et. al.

(1994, 1995) found that black homeowners have a higher default rate than white

homeowners, which contradictorily indicates that mortgage default has no relationship to

lending discrimination. Anderson and VanderHoff (1999) also found that Black

homeowners have a higher marginal default rate than white households, controlling for

borrower and property characteristics. Other scholars found that there are flaws with

using mortgage default to predict mortgage lending discrimination (Ross, 1996;

Anderson and VanderHoff, 1999). Controlling credit history reduces the effect of races

on mortgage default (Cotterman, 2002). Deng and Gabriel (2003) and Van Order and

Zorn (2001) found that minorities have higher default probabilities, but the losses from

their high default risk can be offset by their low tendency for prepayment. They

recommend that financial institutions should have similar pooling and risk-based

mortgage pricing for all borrowers, which will benefit more racial minorities and

therefore improve their homeownership rate. Cotterman (2004) concluded that Blacks

and Hispanic borrowers incur a larger loan loss rate than Whites in FHA-insured loans,

but he did not explore whether the loss could be offset by the lower prepayment tendency

of racial minorities.

Therefore, many researchers think that racial disparities in mortgage default can be

explained by other factors, such as down payment amount and credit history, which

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 42/268

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 43/268

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 44/268

3 0

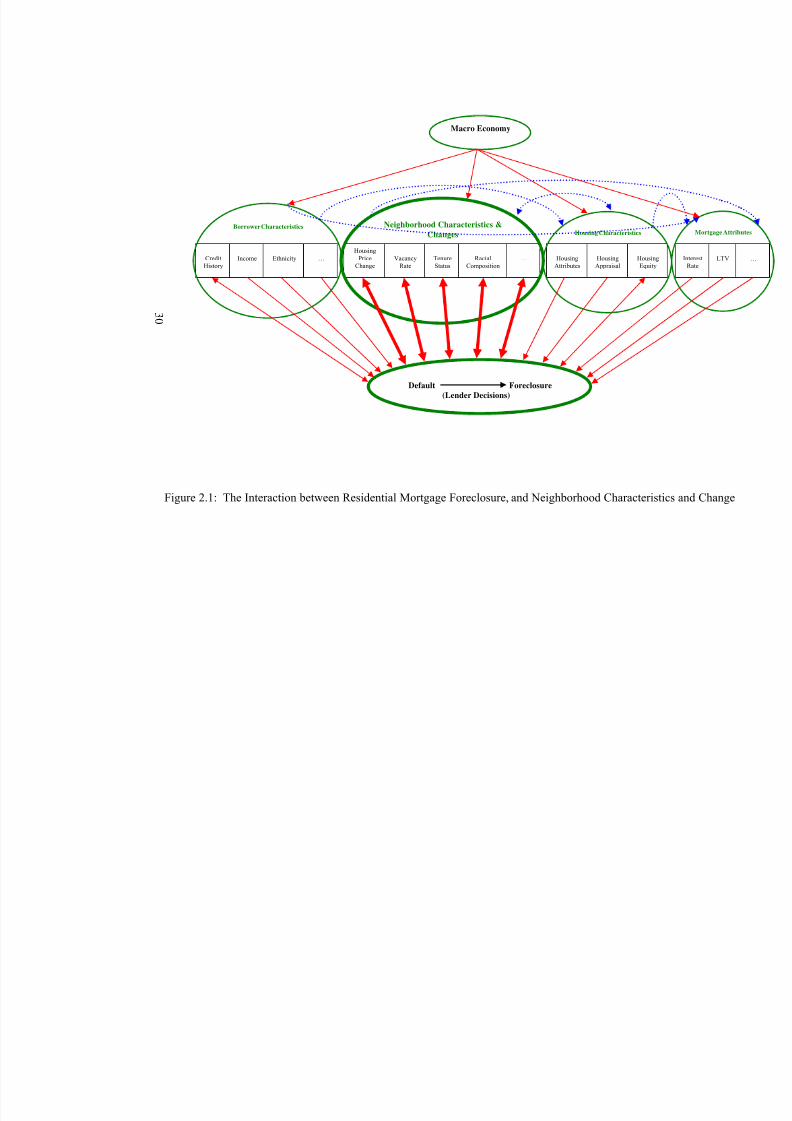

Figure 2.1: The Interaction between Residential Mortgage Foreclosure, and Neighborhood Characteristi

Macro Economy

CreditHistory

Income Ethnicity …Housing

PriceChange

VacancyRate

TenureStatus

RacialComposition

… HousingAttributes

HousingAppraisal

HousingEquity

Default Foreclosure

(Lender Decisions)

Neighborhood Characteristics &

Changes Housing CharacteristicsBorrower Characteristics

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 45/268

31

The Interaction between Neighborhood Characteristics, Neighborhood

Change and Residential Mortgage Foreclosure

General Theories of Neighborhood Change

As mentioned earlier, the development of neighborhood change theory can be

summarized into three generations and research concentrations (Galster and Krall, 2003).

Because these generations have temporal overlap, it is not appropriate to conclude that

they have specific temporal orders. Many contemporary scholars still use the theories

formulated in the first generation in their research. Many conduct their research on

neighborhood change based on the theories of one of the three generations, or the

combined theories from two or three generations.

1. The first generation: descriptive, cartographic and causal analysis (1950 – )

Simple descriptive, cartographic and causal analysis dominates in this generation.

The major theoretical bases are the invasion-succession model that was proposed by the

Chicago School of Sociology (Park, 1952; Duncan and Duncan, 1957; Taeuber and

Taeuber, 1965), the life-cycle model (Hoover and Vernon, 1959), the

demographic/ecological model, the social-cultural/organizational model, the social

movement model (Downs, 1981; Bradbury, et. al., 1982; Schwirian, 1983), the stage

model, and the political-economy model. These theories have been followed by

Maclenna(1982), Taub, et. al. (1984), Grigsby, et. al. (1987), Rothenburg et. al. (1991),

Temkin and Rohe (1996), Lauria (1998), and Galster (2003). All these theories have

formed the fundamental basis of neighborhood change theory by describing how

neighborhoods change, the push and pull factors of the change, and what factors are

affected the most in the neighborhood-succession process. Some of the theories use

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 46/268

32

mechanisms in other disciplines, for example, ecology, to explain the dynamic processes

of a neighborhood. This research will use some of the aforementioned methodology, such

as cartography and descriptive and causal analysis to explain how foreclosures and

neighborhood characteristics and change interact with each other. Some of the terms

developed in this generation, such as racial transition and exogenous variables, will be

used extensively in this research.

2. The second generation: regression and predictive models (1970 – )

Regression and predictive models are used to explore how exogenous variables

affect neighborhood outcome indicators and estimate-related indicators (Galster and

Krall, 2003). Examples of those indicators are population density (Guest, 1972, 1973;

Fogarty, 1977), income or social class (Guest, 1974; Vandel, 1981; Coulson and Bond,

1990; Galster and Mincy, 1993; Galster et. al., 1997; Carter et. al., 1998),

homeownership rate (Baxter and Lauria, 2000), female headship rates (Krivo et. al.,

1998), and racial composition changes (Guest and Weed, 1976; Schwab and Marsh,

1980; Ottensmann et. al., 1990; Galster, 1990; Denton and Massey, 1991; Ottensmann

and Gleeson, 1992; Lauria and Baxter, 1999; Crowder, 2000; Ellen, 2000; Baxter and

Lauria, 2000). There are mixed findings in the studies, but all these indicators provided

the basis for this research when selecting variables. Similarly, when exploring the impact

of foreclosure on neighborhood characteristics and change, foreclosure rate is the

exogenous variable that affects the neighborhood indicators and their change. Only a few

scholars have paid attention to this matter. This research will also use regression and

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 47/268

33

predictive models to find out how foreclosures and neighborhood characteristics and

change interact.

3. The third generation: threshold effect, endogenous neighborhood theory,

neighborhood tipping and complexity models (1990 – )

In more recent neighborhood-change literature, Quercia and Galster (1997, 2000)

proposed a new theory that is called the “Threshold Effect”, which is defined as “a

dynamic process in which the magnitude of the response changes significantly as the

triggering stimulus exceeds some critical value” (Quercia and Galster, 1997: 409). They

advocate using non-linear regression models to predict threshold effects of the change in

neighborhood indicator outcomes caused by exogenous variables. Spline and quadratic

regressions are used in their studies of the threshold effects and neighborhood change.

Galster et. al. (2000) empirically tested the theory by analyzing some exogenous

variables on neighborhood quality-of-life indicators.

Many people have explored how exogenous variables affect the change in

neighborhood outcome indicators, but little has been done to explain how these indicators

change endogenously after the breakdown in stability by the exogenous variable.

Schelling (1971, 1972), and Galster and Krall (2003) are among several people who have

explored the endogenous dynamic change of the neighborhood outcome indicators

affected by exogenous variables. They named the model “Neighborhood Tipping”.

“Complexity Models” evolved from the neighborhood tipping theory.

This generation’s study of neighborhood change has created a new and interesting

scenario. The proposed methodology can be used to determine the extent that

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 48/268

34

foreclosures (the exogenous variable) affect the change in neighborhood indicators

(endogenous variables). Then, the threshold points at which the endogenous variables

change from stability to instability will be calculated. When foreclosures have

contributed to homogenous racial composition, the effect is very similar to the

“Neighborhood Tipping” theory.

Major Neighborhood Indicators Estimated

In these three generations of research, many neighborhood indicators have been

explored for their potential importance to the dynamics of neighborhood change:

• Income or Social Class (Guest, 1974; Vandel, 1981; Coulson and Bond, 1990;

Galster and Mincy, 1993; Galster et. al., 1997; Carter et. al., 1998)

• Homeownership Rate (Baxter and Lauria, 2000)

• Female Headship Rates (Krivo et. al., 1998)

• Racial Composition Changes (Guest and Weed, 1976; Schwab and Marsh,

1980; Ottensmann et. al., 1990; Galster, 1990; Denton and Massey, 1991;

Ottensmann and Gleeson, 1992; Lauria and Baxter, 1999; Crowder, 2000;

Ellen, 2000; Baxter and Lauria, 2000)

• Median Value of Homes (Galster and Krall, 2003)

• Property Delinquency Rate (Galster and Krall, 2003)

• Poverty Rates (Carter et. al., 1998; Galster and Mincy, 1993; Galster et. al.,

1997; Vandell, 1981; Krivo et. al. 1998)

These studies have found that some of the variables have complicated endodynamic

and exodynamic changes (e.g., poverty rate and change). Others are affected by

8/6/2019 Spatial Lag Regression

http://slidepdf.com/reader/full/spatial-lag-regression 49/268

35

exogenous variables, such as foreclosures or metropolitan economic restructuring

affecting the racial transition of a neighborhood. This research will continue to test how

foreclosures and these selected variables interact with each other because all these

variables are very important indicators of neighborhood quality.

Theories of Neighborhood Change

Neighborhood change is an important focus in urban theory and social science. The

literature on neighborhood change, which is quite abundant, mainly focuses on social or

economic explanations of change.

The economic explanation of neighborhood change “focuses on residential

preferences and the interplay of supply-demand relationships in local housing markets”

(Baxter and Lauria, 2000). A simplified version of this idea says that many industries and

jobs moved out to the suburbs because of the development of the transportation network,

the universal use of automobiles, and land price differences inside and outside of the city

center. The process is followed by the out-movement of residents and workers who can

afford both the transit and housing costs in the suburbs and who prefer a less dense living

environment. Those residents who cannot afford those costs are left behind, and many of

them lose their jobs. With the decline of economic activities and household income in

those neighborhoods, housing demand decreased due to lack of housing appreciation,