South Africa – Major Banks Analysis - PwC Reporting Standards (IFRSs) (known as Treasury shares)...

32

Reinforcing collective strength and stability South Africa – Major Banks Analysis www.pwc.com/za PwC’s analysis of major banks’ results to 31 December 2010 March 2011

Transcript of South Africa – Major Banks Analysis - PwC Reporting Standards (IFRSs) (known as Treasury shares)...

Reinforcing collective strength and stability

South Africa – Major Banks Analysis

www.pwc.com/za

PwC’s analysis of major banks’ results to31 December 2010

March 2011

II South Africa – Major Banks Analysis

South Africa – Major Banks Analysis 1

Table of Contents

Overview 2

Combined results summary 4

Economic outlook 6

Net interest income 8

Non-interest income 9

Efficiency 10

Adaptingtonewrealitiesinapost-crisisenvironment 12

Assetquality 14

Capitalandfunding 18

Key banking statistics – Annual 22

Keybankingstatistics–Semi2010 23

Keybankingstatistics–Semi2009 24

Industry statistics 26

Contact details 29

2 South Africa – Major Banks Analysis

Overview

Bank results – overview

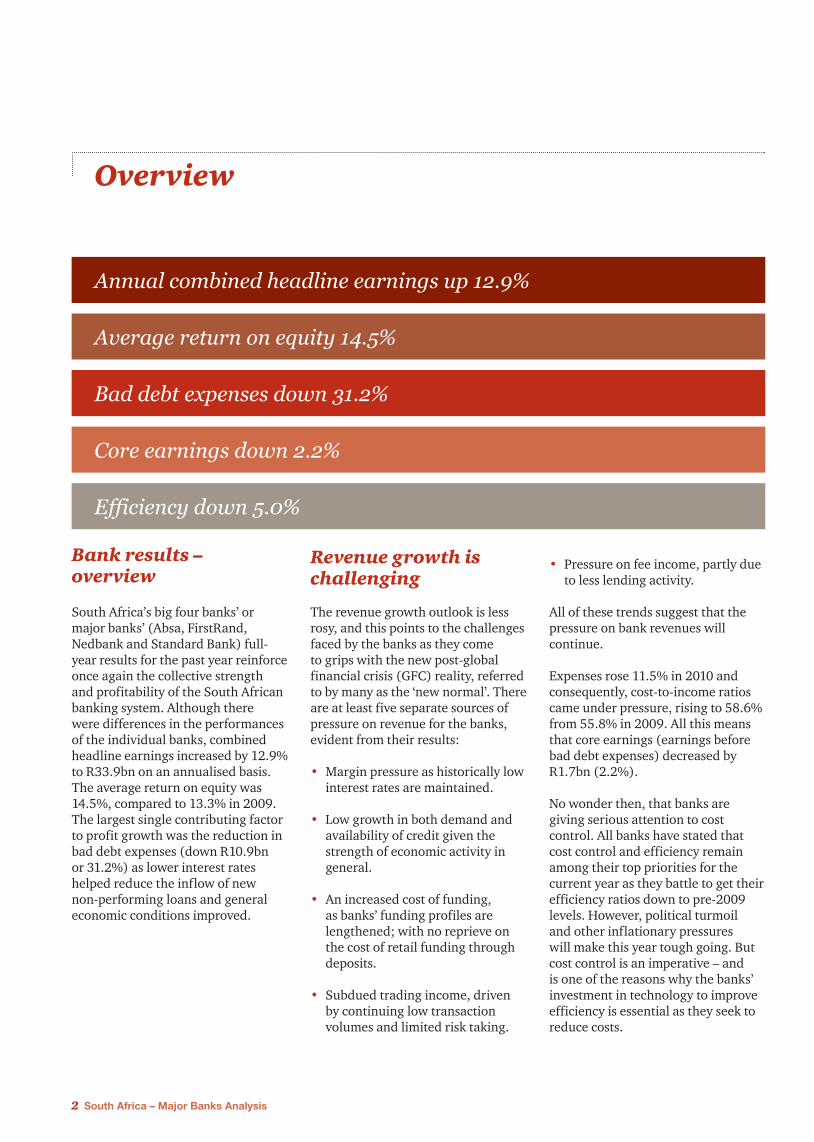

South Africa’s big four banks’ or major banks’ (Absa, FirstRand, Nedbank and Standard Bank) full-year results for the past year reinforce once again the collective strength and profitability of the South African banking system. Although there were differences in the performances of the individual banks, combined headline earnings increased by 12.9% to R33.9bn on an annualised basis. The average return on equity was 14.5%, compared to 13.3% in 2009. The largest single contributing factor to profit growth was the reduction in bad debt expenses (down R10.9bn or 31.2%) as lower interest rates helped reduce the inflow of new non-performing loans and general economic conditions improved.

Annual combined headline earnings up 12.9%

Average return on equity 14.5%

Bad debt expenses down 31.2%

Core earnings down 2.2%

Efficiency down 5.0%

Revenue growth is challenging

The revenue growth outlook is less rosy, and this points to the challenges faced by the banks as they come to grips with the new post-global financial crisis (GFC) reality, referred to by many as the ‘new normal’. There are at least five separate sources of pressure on revenue for the banks, evident from their results:

• Margin pressure as historically low interest rates are maintained.

• Low growth in both demand and availability of credit given the strength of economic activity in general.

• An increased cost of funding, as banks’ funding profiles are lengthened; with no reprieve on the cost of retail funding through deposits.

• Subdued trading income, driven by continuing low transaction volumes and limited risk taking.

• Pressure on fee income, partly due to less lending activity.

All of these trends suggest that the pressure on bank revenues will continue.

Expenses rose 11.5% in 2010 and consequently, cost-to-income ratios came under pressure, rising to 58.6% from 55.8% in 2009. All this means that core earnings (earnings before bad debt expenses) decreased by R1.7bn (2.2%).

No wonder then, that banks are giving serious attention to cost control. All banks have stated that cost control and efficiency remain among their top priorities for the current year as they battle to get their efficiency ratios down to pre-2009 levels. However, political turmoil and other inflationary pressures will make this year tough going. But cost control is an imperative – and is one of the reasons why the banks’ investment in technology to improve efficiency is essential as they seek to reduce costs.

South Africa – Major Banks Analysis 3

The regulatory environment continues to play an important role

The banks are also having to cope with a period of unprecedented regulatory change, together with levels of political scrutiny not seen before. Higher liquidity and capital requirements under Basel III will inevitably increase funding costs and put further pressure on returns on equity. In South Africa’s case in particular, it has been widely publicised that given the shortage of highly liquid instruments and the structural imbalances in the economy, many banks will likely be unable to meet the new liquidity requirements. As such, it is a positive step that the banks, regulators and National Treasury are working together to come up with the best possible solution for South Africa.

In addition to dealing with the requirements of Basel III, banks will have to contend with the new ‘Twin Peaks’ approach to financial regulation as announced by the Minister of Finance in the recent Budget Speech. Under the revised regulatory framework, the South African Reserve Bank (SARB) will be given lead responsibility for prudential regulation and the Financial Services Board (FSB) for consumer protection. As part of this redistribution of responsibility, the mandate of the FSB will be expanded to include the market conduct of retail banking services, including developing principles for how banks should set their fees, how these fees should be reported and what constitutes fair behaviour. Within the FSB, a retail banking services market conduct regulator will be established. This new regulator will focus on structural market issues and banking fees and will work closely with the National Credit Regulator, which has a complementary role in regulating the extension of credit. The SARB’s mandate for financial stability will be underpinned by a new Financial Stability Oversight Committee, co-chaired by the Governor of the SARB and the Minister of Finance.

Banks could have supposed that the new framework would be largely similar to what they have been accustomed to, but for the mention of bank fees in the new framework. Most banks rely increasingly on non-interest income (fees) to bolster their revenue lines and any regulatory changes on this front would be a severe blow.

Given the regulatory uncertainty, it is not surprising to see capital adequacy ratios creeping upwards, with the average for Tier 1 now at 12.8% (2009: 12.4%), which is well north of the minimum required. Most banks are cautious when dealing with the question of what will happen to their excess capital. This is likely to remain an issue until there is more clarity on what the new rules will be.

Looking ahead

South Africa has been fortunate in that our banks avoided much of the fallout from the GFC experienced by banks elsewhere. However, our consumers and households were similarly over-leveraged and as this slowly returns to normal, they are looking to be more cautious in relation to debt; which was a steady source of both revenue and profit growth for the banks over the past two decades. Increased demand for commercial and corporate borrowing may help offset this.

The Minister 0f Finance surprised some

by saying, “I have met with the chief

executives of our banks to take up this

issue (bank charges, the complexity of the

payment system) and I believe it is time

to put in place measures that will ensure

that banking charges are fairly set, are

transparent and do not create undue

hardship.”

In a deleveraging world, and with new capital and funding restrictions, South African banks will need to be more selective in finding new ways to connect with customers to drive revenue and profitable growth. Large investments in technology to improve efficiency are clearly one vehicle for this – and indeed the depth of customer information that will be available in a technologically–enabled banking system will enable extraordinary precision in both marketing and credit assessment. The banks are pushing the mobile handset revolution for the same reasons as this is seen as a potentially high growth area that does not require significant infrastructure investment, given that the target market was previously unbanked. In addition, the big four banks are increasing their focus on the lower income sectors as the battle for market share intensifies, given the importance of growth in this sector.

In the pursuit of growth, offshore expansion into Africa remains very much in play, with each bank taking a different approach. Suffice to say, history has shown that this is an area where a precise understanding of the chosen market - in contrast to ubiquity of scope and reach - is fundamentally important.

4 South Africa – Major Banks Analysis

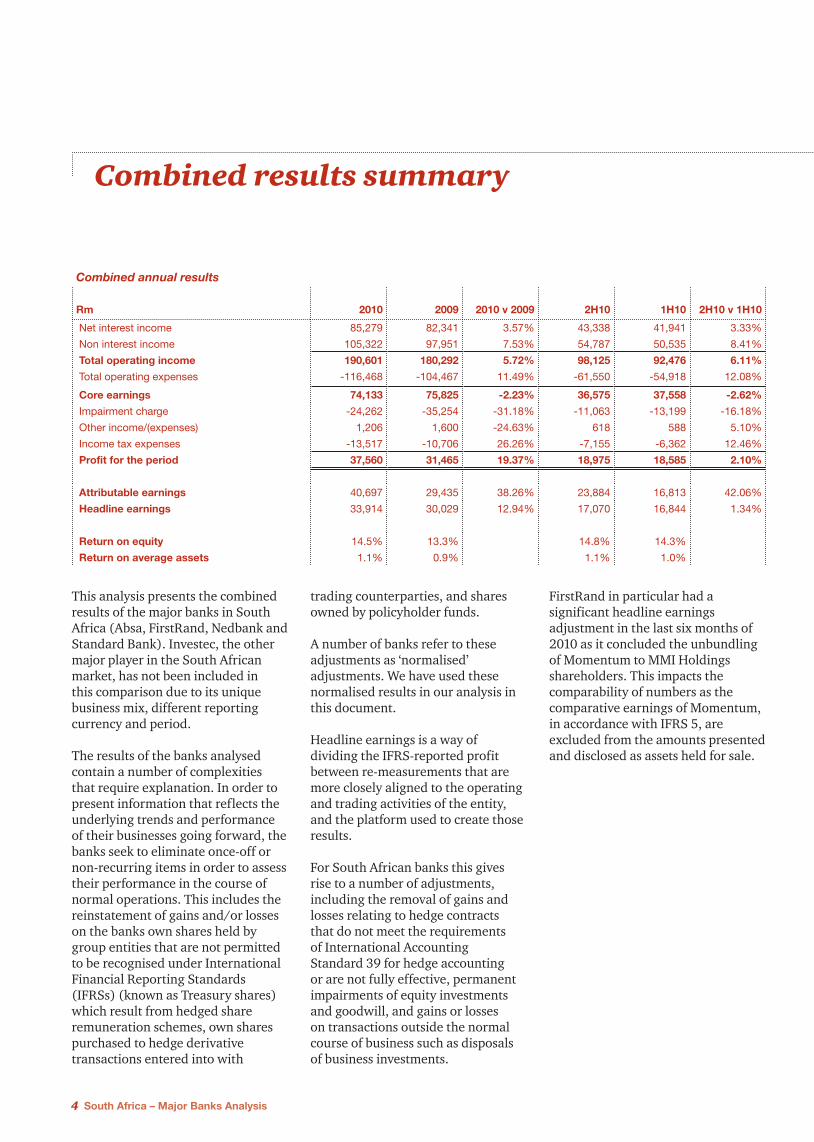

Combined results summary

This analysis presents the combined results of the major banks in South Africa (Absa, FirstRand, Nedbank and Standard Bank). Investec, the other major player in the South African market, has not been included in this comparison due to its unique business mix, different reporting currency and period.

The results of the banks analysed contain a number of complexities that require explanation. In order to present information that reflects the underlying trends and performance of their businesses going forward, the banks seek to eliminate once-off or non-recurring items in order to assess their performance in the course of normal operations. This includes the reinstatement of gains and/or losses on the banks own shares held by group entities that are not permitted to be recognised under International Financial Reporting Standards (IFRSs) (known as Treasury shares) which result from hedged share remuneration schemes, own shares purchased to hedge derivative transactions entered into with

trading counterparties, and shares owned by policyholder funds.

A number of banks refer to these adjustments as ‘normalised’ adjustments. We have used these normalised results in our analysis in this document.

Headline earnings is a way of dividing the IFRS-reported profit between re-measurements that are more closely aligned to the operating and trading activities of the entity, and the platform used to create those results.

For South African banks this gives rise to a number of adjustments, including the removal of gains and losses relating to hedge contracts that do not meet the requirements of International Accounting Standard 39 for hedge accounting or are not fully effective, permanent impairments of equity investments and goodwill, and gains or losses on transactions outside the normal course of business such as disposals of business investments.

FirstRand in particular had a significant headline earnings adjustment in the last six months of 2010 as it concluded the unbundling of Momentum to MMI Holdings shareholders. This impacts the comparability of numbers as the comparative earnings of Momentum, in accordance with IFRS 5, are excluded from the amounts presented and disclosed as assets held for sale.

Combined annual results

Rm 2010 2009 2010 v 2009 2H10 1H10 2H10 v 1H10

Net interest income 85,279 82,341 3.57% 43,338 41,941 3.33%

Non interest income 105,322 97,951 7.53% 54,787 50,535 8.41%

Total operating income 190,601 180,292 5.72% 98,125 92,476 6.11%

Total operating expenses -116,468 -104,467 11.49% -61,550 -54,918 12.08%

Core earnings 74,133 75,825 -2.23% 36,575 37,558 -2.62%

Impairment charge -24,262 -35,254 -31.18% -11,063 -13,199 -16.18%

Other income/(expenses) 1,206 1,600 -24.63% 618 588 5.10%

Income tax expenses -13,517 -10,706 26.26% -7,155 -6,362 12.46%

Profit for the period 37,560 31,465 19.37% 18,975 18,585 2.10%

Attributable earnings 40,697 29,435 38.26% 23,884 16,813 42.06%

Headline earnings 33,914 30,029 12.94% 17,070 16,844 1.34%

Return on equity 14.5% 13.3% 14.8% 14.3%

Return on average assets 1.1% 0.9% 1.1% 1.0%

South Africa – Major Banks Analysis 5

Combined results of six month periods

Combined results Comparative movement Rm 2H10 1H10 2H09 1H09 2H 1H

Net interest income 43,338 41,941 42,411 39,930 2.2% 5.0%

Non-interest income 54,787 50,535 52,611 45,340 4.1% 11.5%

Total operating income 98,125 92,476 95,022 85,270 3.3% 8.5%

Total operating expenses -61,550 -54,918 -55,023 -49,444 11.9% 11.1%

Core earnings 36,575 37,558 39,999 35,826 -8.6% 4.8%

Impairment charge -11,063 -13,199 -15,539 -19,715 -28.8% -33.1%

Other income 618 588 176 1,424 251.1% -58.7%

Income tax expenses -7,155 -6,362 -6,472 -4,234 10.6% 50.3%

Profit for the period 18,975 18,585 18,164 13,301 4.5% 39.7%

Attributable earnings 23,884 16,813 16,293 13,142 46.6% 27.9%

Headline earnings 17,070 16,844 16,750 13,279 1.9% 26.8%

Return on equity 14.8% 14.3% 14.8% 12.0% -0.4% 19.3%

Return on average assets 1.1% 1.0% 1.1% 0.8% 8.3% 28.2%

6 South Africa – Major Banks Analysis

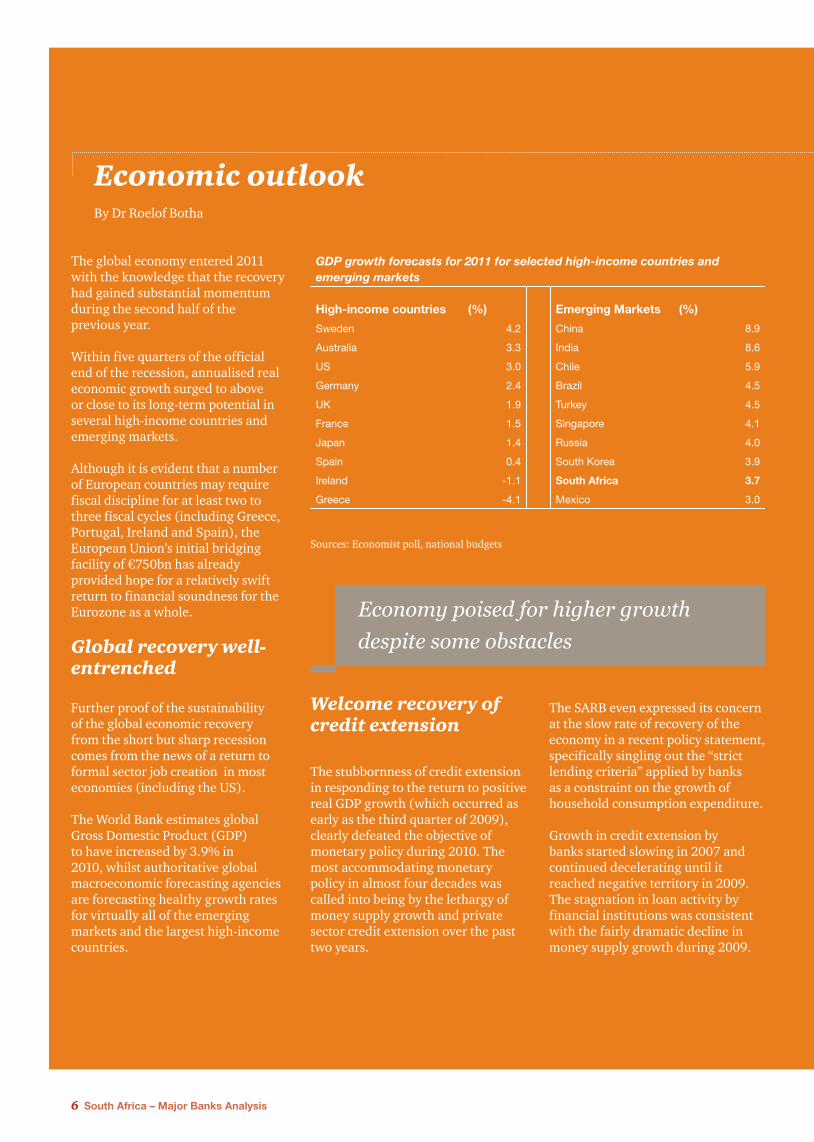

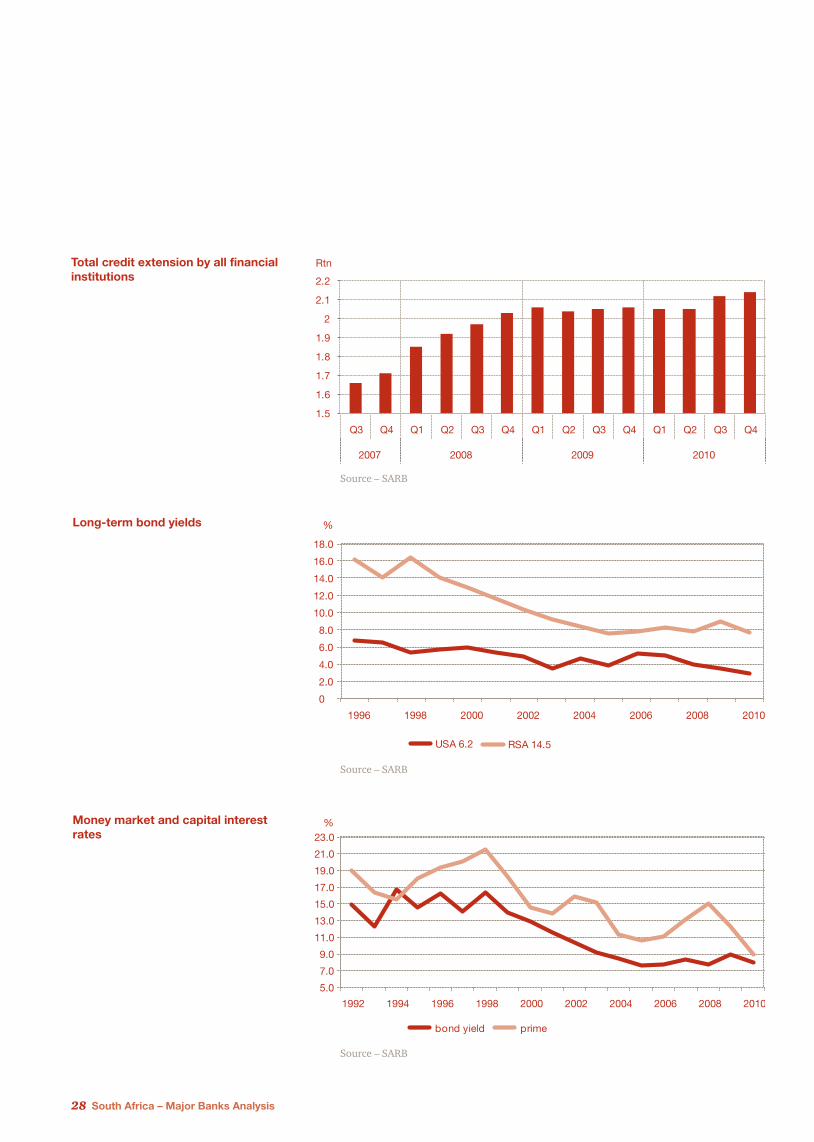

Economic outlookBy Dr Roelof Botha

Welcome recovery of credit extension

The stubbornness of credit extension in responding to the return to positive real GDP growth (which occurred as early as the third quarter of 2009), clearly defeated the objective of monetary policy during 2010. The most accommodating monetary policy in almost four decades was called into being by the lethargy of money supply growth and private sector credit extension over the past two years.

Economy poised for higher growth

despite some obstacles

The global economy entered 2011 with the knowledge that the recovery had gained substantial momentum during the second half of the previous year.

Within five quarters of the official end of the recession, annualised real economic growth surged to above or close to its long-term potential in several high-income countries and emerging markets.

Although it is evident that a number of European countries may require fiscal discipline for at least two to three fiscal cycles (including Greece, Portugal, Ireland and Spain), the European Union’s initial bridging facility of €750bn has already provided hope for a relatively swift return to financial soundness for the Eurozone as a whole.

Global recovery well-entrenched

Further proof of the sustainability of the global economic recovery from the short but sharp recession comes from the news of a return to formal sector job creation in most economies (including the US).

The World Bank estimates global Gross Domestic Product (GDP) to have increased by 3.9% in 2010, whilst authoritative global macroeconomic forecasting agencies are forecasting healthy growth rates for virtually all of the emerging markets and the largest high-income countries.

The SARB even expressed its concern at the slow rate of recovery of the economy in a recent policy statement, specifically singling out the “strict lending criteria” applied by banks as a constraint on the growth of household consumption expenditure.

Growth in credit extension by banks started slowing in 2007 and continued decelerating until it reached negative territory in 2009. The stagnation in loan activity by financial institutions was consistent with the fairly dramatic decline in money supply growth during 2009.

GDP growth forecasts for 2011 for selected high-income countries and emerging markets

High-income countries (%) Emerging Markets (%)

Sweden 4.2 China 8.9

Australia 3.3 India 8.6

US 3.0 Chile 5.9

Germany 2.4 Brazil 4.5

UK 1.9 Turkey 4.5

France 1.5 Singapore 4.1

Japan 1.4 Russia 4.0

Spain 0.4 South Korea 3.9

Ireland -1.1 South Africa 3.7

Greece -4.1 Mexico 3.0

Sources: Economist poll, national budgets

South Africa – Major Banks Analysis 7

0

5.0

10.0

15.0

20.0

25.0

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2008 2009 2010

According to the SARB, the continuation of subdued money market activity during the first half of 2010 was related, inter alia, to a low inflationary environment, relatively low returns on money market deposits and impaired balance sheets in both the corporate and household sectors.

A welcome return to positive growth in credit extension by the banking sector was made in the second quarter of 2010, although the rate of expansion has remained rather muted. All types of bank loans began recording positive growth during the third quarter of 2010.

Growth drivers

Since the second half of 2010, the equity market has also witnessed higher levels of activity, with its value of market capitalisation growing at healthy rates. This growth reflects the impact of lower bond yields, lower money market rates, higher profit expectations and progress in reducing the government’s budget deficit.

Prospects for a swift return to the pre-recession economic growth trajectory of above 4% have been buoyed by the presence of a number of rather impressive macroeconomic growth drivers, including the following:

• Prospectsforrelativelylowinflation during 2011

• Areturntohealthyrealgrowthrates for household disposable incomes

• Thelowestmoneymarketinterestrates in almost four decades

• Anupwardtrendincommodityprices (particularly metals, minerals and oil)

• Acontinuationoftherecoveryofinventory levels

• Continuedprogresswithgovernment infrastructure programmes

• Anexpansionaryfiscalpolicystance, particularly in terms of job creation initiatives

• Areturntoformalsectoremployment creation

Against these positives, however, the potential impact of higher oil and commodity prices fuelled by the political turmoil in the Middle East should be considered.

Source – SARB

Recovery of private sector credit extention (percentage annualised growth)

8 South Africa – Major Banks Analysis

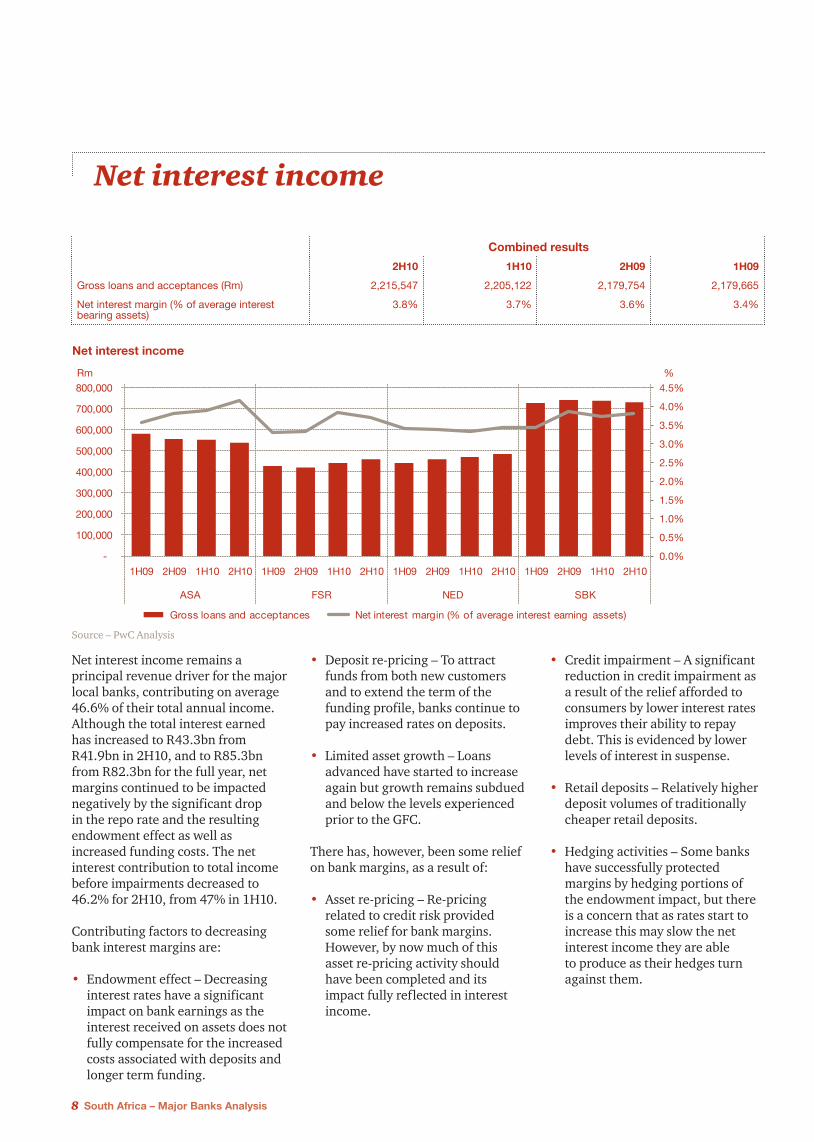

Net interest income

Net interest income remains a principal revenue driver for the major local banks, contributing on average 46.6% of their total annual income. Although the total interest earned has increased to R43.3bn from R41.9bn in 2H10, and to R85.3bn from R82.3bn for the full year, net margins continued to be impacted negatively by the significant drop in the repo rate and the resulting endowment effect as well as increased funding costs. The net interest contribution to total income before impairments decreased to 46.2% for 2H10, from 47% in 1H10.

Contributing factors to decreasing bank interest margins are:

• Endowment effect – Decreasing interest rates have a significant impact on bank earnings as the interest received on assets does not fully compensate for the increased costs associated with deposits and longer term funding.

• Deposit re-pricing – To attract funds from both new customers and to extend the term of the funding profile, banks continue to pay increased rates on deposits.

• Limited asset growth – Loans advanced have started to increase again but growth remains subdued and below the levels experienced prior to the GFC.

There has, however, been some relief on bank margins, as a result of:

• Asset re-pricing – Re-pricing related to credit risk provided some relief for bank margins. However, by now much of this asset re-pricing activity should have been completed and its impact fully reflected in interest income.

• Credit impairment – A significant reduction in credit impairment as a result of the relief afforded to consumers by lower interest rates improves their ability to repay debt. This is evidenced by lower levels of interest in suspense.

• Retail deposits – Relatively higher deposit volumes of traditionally cheaper retail deposits.

• Hedging activities – Some banks have successfully protected margins by hedging portions of the endowment impact, but there is a concern that as rates start to increase this may slow the net interest income they are able to produce as their hedges turn against them.

Combined results

2H10 1H10 2H09 1H09

Gross loans and acceptances (Rm) 2,215,547 2,205,122 2,179,754 2,179,665

Net interest margin (% of average interest bearing assets)

3.8% 3.7% 3.6% 3.4%

%Rm

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10

ASA FSR NED SBK

Gross loans and acceptances Net interest margin (% of average interest earning assets)

Source – PwC Analysis

Net interest income

South Africa – Major Banks Analysis 9

Non-interest income

Increased reliance on non-interest income

Non-interest income for 2H10 was up 8.4% on 1H10 and 4.1% up on 2H09. It now represents 53.8% of total income, up from 53.0% in 1H10. This demonstrates the increased reliance of banks on non-interest income as a source of earnings.

Net fee and commission income

Net fee and commission income increased by 9.0% on 1H10 and increased by 5.8% on 2H09. This growth is largely attributable to transactional volume growth, coupled with inflationary increases offset by lower knowledge-based fees on the back of reduced deal flow in Investment Banking.

Of particular interest is the strong growth in electronic banking fees, generally considered to be a cheaper alternative to other transaction channels. The continued migration of customers to electronic banking channels could significantly impact the net fee and commission income earned in future periods.

Fair value income

air value income decreased by 1.9% on 1H10 and by 12.5% on 2H09. Proprietary trading and customer demand for Interest Rate and Foreign Exchange risk management products remained relatively low. Uncertainty regarding the market direction, especially following the sovereign debt crisis in Europe in 1H10,

significantly impacted earnings. Competition for derivative flows in emerging markets remains intense, and has increased as international banks seek to grow in emerging markets, resulting in a compression of margins. Equity markets have however been buoyant as fears over the GFC abated.

Insurance and Bancassurance income

Insurance and Bancassurance income increased by 64.7% in 2H10 against 1H10 and by 19.1% on 2H09, albeit from a relatively low base. This dramatic increase is primarily attributable to strong premium growth as a result of stronger cross-selling and the launch of more innovative products. Increased investment returns following the recovery of the global financial markets have also significantly contributed to this growth.

-10,000

-

10,000

0

20,000

30,000

40,000

50,000

60,000

1H09 2H09 1H10 2H10

Net fee and commission income Fair value income

Insurance & Bancassurance income Other income

Rm

Source – PwC Analysis

Non-interest income

10 South Africa – Major Banks Analysis

Efficiency

Compared to the prior period, banks’ operating expenses increased by 12.1 % while total operating income increased by 6.1%. Consequently the banks’ combined cost-to-income ratio deteriorated from 57.1% in 1H10 to 59.9% in 2H10. The banks have continued to place significant emphasis on tightly managing their expense base. Given the subdued growth in total operating income, these cost containment strategies have paid dividends and limited the impact on the cost-to-income ratio. All of the banks have stated at their results presentations that this will remain a strategic priority in 2011.

Of particular interest is the continued significant investment made in information technology, from an already high base in prior periods. The banks have cited several reasons for this:

• There has been ongoing upward pressure on banking technology costs in terms of security, business continuity, and recoverability. The complexity and threats in these areas have risen exponentially in recent years, alongside the cost of staying ahead of the game.

• The importance of technology to the banks’ operations has been on a long-term upward trend. While this has generated efficiencies in many areas, it has also consequentially increased technology costs.

• Most importantly of all in the

-

47%

7%5%

41%

Total staf f costs

Information Technology

Depreciation, amortisation and impairments

Other

-

47%

7%6%

40%

Total staf f costs

Information Technology

Depreciation, amortisation and impairments

Other

Combined results

2H10 1H10 2H09 1H09

Cost-to-income ratio 59.9% 57.1% 55.7% 56.1%

FY10 – Operating expenditure

FY09 – Operating expenditure

Source – PwC Analysis

Source – PwC Analysis

most recent year banks have made investments to replace or enhance core banking systems both locally and abroad. Changes in regulatory and risk requirements have also necessitated, and will continue to necessitate, various system enhancements as banks require access to more historic and detailed data on a more regular basis.

Staff costs, which represented 47% of total expenses, continue to grow at levels well above inflation, reflecting an 11.8% increase in 2010 from 2009. As a result, staff costs are the subject of more and more discussion in boardrooms. Banks have begun to respond to external pressures on staff costs by increasing amounts paid in shares and extending vesting periods.

South Africa – Major Banks Analysis 11

Operating expenses were also favourably impacted by the strong Rand during the period. The average USD/ZAR rate strengthened from 8.42 in 2009 to 7.32 in 2010. As South African banks continue to expand into Africa and other emerging markets, currency fluctuations are having a more pronounced impact on earnings.

Banks will continue to place considerable focus on reducing their cost base over the next few years. Because we expect that margins will remain compressed, and beyond 2011 lending volumes may improve only modestly, we expect that cost management will rise further in terms of relative importance and may well be a distinguishing factor between the relative performances of the banks.

12 South Africa – Major Banks Analysis

Adapting to new realities in a post-crisis environment

Confidence is back – this is the overwhelming message from CEOs in PwC’s 14th Annual Global CEO survey released in the first quarter of this year. More specifically, CEOs are nearly as confident of growth this coming year, as they have ever been in the history of our survey. Realising growth aspirations will not be easy; however, as companies will have to respond to new challenges in the post-crisis environment. PwC explored some of these new realities and the mega trends that will affect the Global and South African banking industry in a study called Project Blue.

Top-line growth main concern for South African banks

As mentioned earlier, South African banks are struggling to grow top-line revenue as consumers are reluctant to borrow due to over-indebtedness, inflation fears and anticipated interest rate increases. As a result, many believe South African banks will have to tap into the rapidly increasing emerging-to-emerging market trade flows if they want to realise their growth aspirations. It is therefore not surprising to see the banks focusing their attention on expansion into Africa to capture these trade flows.

This is supported by our economic forecast, which suggests that the GDP of E7 emerging economies could be bigger than that of the G7 economies by 2020, and that China may overtake the US before the end of the decade. Many Western banks are looking to offset slow growth in their home markets by strengthening their presence in South America, Africa, Asia and the Middle East. Most of the

banking and capital markets CEOs are clearly in this camp. 61% think that emerging markets will be more important to their organisation’s future than developed markets. However, success will be hard won as emerging economies respond to international interest. For example, interest in the African continent from international players has not been lost on African CEOs: 28% have changed their strategy because of competitive threats, compared to a global average of 10%.

Responding to changing customer requirements

More CEOs are responding to the rise of middle-class consumers in emerging economies by developing products and services tailored to those high-growth markets, while also looking to serve the changing needs of more mature markets. Our CEO Survey reveals that CEOs are placing a higher premium on innovation today. Since 2007, business leaders have consistently

reported that their single best opportunity for growth lay in better penetration of their existing markets. Now they are just as likely to focus on the innovation needed for new products and services.

We believe that changing customer behaviour and accessible banking are two of the key drivers that will fundamentally influence the business models of South African banks.

South African banks

Many believe the previously unbanked market represents a significant opportunity for revenue growth in South Africa. To date this market has largely been serviced by Tier 2 banks, with limited inroads being made by the bigger banks. However, these large banks have now started to tailor their service offerings to enable them to provide banking services to the mass market. Inability to do so will result in a loss of market share and stagnating revenue growth over the long term.

“In the same way, for the younger people

who went through this recession, it will

forever have an impact on the way they

behave, the way they incur debt, the way

they spend, the way they save. It will be a

permanent change”

– Richard K. Davis,

President and CEO of U.S. Bancorp

South Africa – Major Banks Analysis 13

“We expect that governments will not

only be looking to the private sector

for the provision of capital, but for

increasing the delivery of a whole

range of social services. For example,

in the UK the government is looking at

different ways to provide services from

the private sector in terms of meeting the

government’s objectives.”

Nicholas Moore,

CEO of the Macquarie Group

It is notable that 87% percent of global banking and capital market CEOs believe that innovations will lead to operational efficiencies and provide them with a competitive advantage. 64% also believe that their IT investments will help them tap into new marketing and transactional opportunities such as mobile devices and social media. With more than 40 million mobile devices in operation in South Africa, this is clearly a distribution channel that will be explored further by South African banks as they penetrate the mass market.

Growth opportunities, especially in emerging markets, prompt changes to talent strategies

As they look to expand globally, CEOs recognise that they require a more diverse workforce, including more women and different geographic leaders as they look to expand globally. Filling the skills gaps in emerging markets begins with banks making themselves more attractive to potential and current employees; as well as looking for better ways to develop and deploy staff globally. Becoming the employer of choice is a vital advantage in dynamic markets where top talent has the pick of jobs from domestic and foreign employers.

We have noted in Project Blue that South African banks will have to reconsider the remuneration policies and development opportunities they offer in order to attract and retain key talent. The role that organisational culture plays in talent retention should also not be underestimated.

Overregulation continues to rank amongst the top 3 risks on CEOs’ minds

Nearly three quarters of CEOs told us they would actively support new government policies that promote growth that is economically, socially and environmentally sustainable. However, overregulation remains

a concern for global CEOs. For South African banks, changes to Basel III, particularly the proposed new liquidity requirements, could fundamentally change the business models of the banks and may negatively impact on banks’ ability to grow. However, it is the positive step that the National Treasury is leading a task force investigating how best to deal with the challenges of Basel III.

The majority of global banking CEOs regard political instability as the most significant global risk

Western banks will need to adjust to governments exerting greater control over their activities and the real economy. In developed markets, the crisis necessitated a rapid increase in state intervention and, in many people’s eyes, has legitimised ongoing intervention. Project Blue highlights the rise of state-directed capitalism as one of the mega trends that will have an impact on banking globally. Western banks’ ability to respond to opportunities in emerging markets will largely depend on the risk appetite of governments of the jurisdictions from which they operate. This creates opportunities for emerging market banks to capture market share if they are able to

respond to opportunities quickly.

Political interference in banking is much less common in South Africa, given that none of its banks had to be bailed out. However, there has been ongoing support by the South African government for community banks and the Postbank to ensure access to banking services for the unbanked market. Although the debate around nationalisation currently focuses on mines, banks have also been mentioned in this context not too long ago. All of these factors could profoundly change the South African banking environment in future.

It is clear that South African banks will have to contend with a number of new realities if they wish to remain relevant in the post-crisis environment. The most successful banks are likely to be those which can respond to the opportunities, while at the same time making the most of their principal competitive strengths. This will accelerate the move towards precision as banks become ever more ruthless in the defence and optimisation of their core franchises. As one CEO put it, the bank that can implement its strategy in the most efficient way will be the winner.

14 South Africa – Major Banks Analysis

Asset quality

Levels of gross advances

Given the subdued global sentiment and the strained economic environment in 2010, it is not surprising that there was limited overall growth in advances for the full year 2010.

The growth in total advances across the Corporate and Retail sectors for 2010 was 2.2%.

Total advances as at 2H10 increased to R2.2tn compared to R2.1tn as at 2H09. This increase was made up of an increase in total advances of approximately 5.1% in the Retail sector (total retail advances as at 2H10 amounted to R1.4tn compared to R1.3tn as at 2H09), a 0.3% marginal decrease in the Corporate Banking sector, and a decrease in the ‘Other’ advances category amounting to R18bn during the year.

Total non-performing loans (NPLs)

An analysis of NPLs as a percentage of gross advances at 2H10 follows:

- 3.0

- 2.0

- 1.0

0

1.0

2.0

3.0

4.0

5.0

6.0

2,100,000

2,150,000

2,200,000

2,250,000

2,300,000

2,350,000

2,400,000

Rm %

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2008 2009 2010

Loans and advances (LHS) Loans and advances – year-on-year growth (RHS)

Source – SARB (all banks)

Growth in NPL

advances (%)

NPLs/Advances (%)

2010 2009

Personal and Business Banking/ Retail

-1.2% 7.5% 7.9%

Mortgage loans -1.5% 9.4% 9.7%

Instalment sale and finance leases 5.8% 5.5% 5.3%

Card debtors -6.9% 8.8% 9.5%

Other loans and advances -4.2% 3.7% 4.6%

Corporate and Investment Banking -1.4% 3.0% 3.0%

Corporate lending -0.5% 3.0% 3.0%

Commercial property finance 1.7% 3.0% 3.1%

Central and Other -130.7% 0.3% 2.5%

Total -1.3% 5.9% 6.1%

South Africa – Major Banks Analysis 15

Although the levels of inflows into the early arrears categories seem to have decreased, the level of NPLs in the banks’ balance sheets remains sticky with a marginal decrease in NPL levels across the banks. Total NPLs amounted to R130bn, around 5.9% of total gross advances (R2.2tn) in 2H10 (compared to a ratio of 6.2% in 2H09). The marginal decrease in NPL levels was made up of growth in ABSA’s NPL book by 9.8%, offset by decreases in the NPL books of the other banks (Nedbank’s and FirstRand’s NPL books decreased by 1% and 8.7% respectively, and Standard Banks’ decreased by 11.7%).

The high NPL levels are as a result of the large number of client accounts that were previously in arrears, which are now working their way through the banks’ legal departments. The combined level of NPLs now stands at R76bn for the Mortgage Portfolio’s alone. The number and value of loans subject to legal remedy will no doubt increase the workloads of the collections, legal and recovery teams

within banks. Given the volumes of loans designated as NPLs, banks will need to reassess their expectations of when these properties will be recovered. This may have an impact on the timing of these recoveries and ultimately Loss Given Default (LGD) assumptions used in estimating mortgage book impairments.

The numbers of debt counselling clients in the non-performing categories seem to have reached a peak in 2010. We saw inflows into the debt counselling process starting to show a more stable trend in 2H10. During 2010, banks across the industry placed an emphasis on terminating clients that had not stuck to their debt counselling terms. The incentive for banks to terminate clients and place them back into the legal recovery process is that recoveries are made sooner by this means, which positively impacts impairments.

The manner in which banks terminate clients was recently called into question, where a full bench in

the Western Cape High Court ruled that a credit provider could not terminate the debt review process where an application for a debt re-arrangement had been lodged by the debt counsellor with the magistrate court and was still pending. The High Court judgement demonstrated that if consumers and debt counsellors fulfilled their duties by submitting an application for debt review to the magistrate’s court within 60 days of receiving such application, the credit provider could not unilaterally terminate the debt review process.

The High Court stated in its judgement that “to allow a credit provider to unilaterally terminate the consumer’s protection at the precise moment when he or she may need it the most can only be construed as absurd. It would be like providing the consumer with an umbrella and then snatching it back the moment it starts raining.” The High Court implied that a typical debt review often takes longer than 60 business days before it results in an order by the magistrate’s court.

0

5

10

15

20

25

30

35

40

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10

ASA FSR NED SBK

NPLs (LHS) Specif ic impairment of NPLs (RHS)

Rm %

Source – PwC Analysis

The High Court stated in its judgement that “to allow a credit

provider to unilaterally terminate the consumer’s protection at

the precise moment when he or she may need it the most can only

be construed as absurd. It would be like providing the consumer

with an umbrella and then snatching it back the moment it starts

raining.”

16 South Africa – Major Banks Analysis

The press suggests that the National Credit Regulator has a large backlog of unresolved cases due to capacity constraints in the court system. This is not good news for banks as an extension of this process means higher LGD percentages as a result of potentially lower recovery rates in the future.

How banks resolve the current levels of NPLs and those NPLs in the debt review process needs to be monitored in 2011.

Analysis of gross advances and non-performing loans in the mortgage loan portfolio

Mortgage loan advance growth has been 2.2% for the year since 2009.

NPL as a percentage of advances is 9.4% and has decreased slightly for 2H10 compared to 2H09, when it was 9.7%. Coverage ratios have increased as the average age of accounts with NPL status has increased. The implied LGD (calculated by dividing the specific impairment amounts by the NPL book) remained relatively consistent at 18.6% across all banks, compared to approximately 18.5% as at 2H09.

Analysis of gross advances and non-performing loans in the vehicle and asset finance portfolio

Certain South African banks include their Corporate or Business vehicle asset finance books within the

Retail vehicle and asset finance categories for financial reporting purposes, whilst other banks include the Business and Corporate vehicle asset finance business under their Corporate operations. This means that direct comparisons of key Retail vehicle and asset portfolio ratios is not always possible.

Notwithstanding the above, it appears that vehicle and asset finance advance growth was approximately 1.8% for the year since 2H09, with most of the growth coming from retail advances as car sales increased in 2H10. NPLs as a percentage of advances are close to 5.5% and have increased slightly in 2H10 compared to 2H09, when they were 5.3%. Coverage ratios have generally increased as the average age of the accounts with NPL status has increased. The implied LGD decreased to approximately 46.5% across all of the banks (from approximately 48.8% during 2H09).

Analysis of gross advances and non-performing loans in the card portfolio

Card advances growth has been 0.1% for the year since 2H09.

NPLs as a percentage of card advances are 8.8% and have decreased slightly for 2H10 compared to 2H09, when they were 9.5%. Coverage ratios have increased as the average age of accounts with NPL status has increased. The implied LGD decreased to approximately 75.6% across all of the banks (from approximately 77.7% as at 2H09). The improvement in LGDs in this portfolio implies that banks have had

some success in realising outstanding balances. Our industry experience shows that post-write-off recoveries in the current year have been more favourable across this portfolio compared to previous years and would most likely taper off in the future.

Analysis of gross advances and non-performing loans in the wholesale portfolio

Corporate advances decreased slightly by 0.3% for the year since 2H09.

NPLs as a percentage of advances were 3.0% for 2H10 and were at similar levels for 2H09. The implied LGD rate increased to approximately 40.3% across all of the banks (from approximately 26.4% for 2H09).

A review of the latest liquidation numbers shows that Corporate clients may not be out of the woods yet. More companies closed their doors in January this year compared to the same month in 2010, Statistics SA said recently. “A year-on-year increase of 24.8% (from 206 to 257) in company liquidations was recorded for January 2011 compared with January 2010”. Over the same period, closed corporation liquidations rose from 110 to 143, and company liquidations increased from 96 to 114.

“A year-on-year increase of 24.8% (from 206 to

257) in company liquidations was recorded for

January 2011 compared with January 2010”.

– Statistics SA

South Africa – Major Banks Analysis 17

Total income statement impairment charge ratio (impairments to the income statement divided by average advances)

The total income statement impairment charge across the major banks was R24.3bn for 2010 compared to R35.3bn for 2009. There is therefore a noticeable improvement in the impairment credit charge ratio, which varied from 0.9% to 1.4% for 2010. This varied from 1.3% to 1.7% in 2009.

The levels of income statement impairment seem to have reached its highs in 2009 and are now starting to decline, albeit at a much slower rate than many had anticipated. The low interest rate environment coupled with relatively strong salary increases left consumers with more disposable income in 2010, which resulted in fewer inflows into the arrears categories. As noted earlier, external inflationary pressure and rises in interest rates will have a negative impact which may possibly result in new NPL volumes increasing over time.

Total coverage ratios

The coverage ratios (calculated as specific impairment divided by NPL book) across all products decreased slightly during the year. This trend is not surprising given that the average age of loans included in the NPL category has not decreased substantially.

The average NPL coverage ratios across certain products were as follows:

• Mortgage loans – 18.6% (FirstRand was the highest at 19.64% and Standard Bank the lowest at 17.43%).

• Instalment sales business – 46.5% (Standard Bank was the highest at 57.91% and FirstRand the lowest at 41.19%).

• Cards – 75.6% (Nedbank was the highest at 96.53% and Standard Bank the lowest at 67.16%).

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10

ASA FSR NED SBK

Specif ic impairment % Portfolio impairment %

%

Source – PwC Analysis

18 South Africa – Major Banks Analysis

Capital and funding

Deposits

Optimising the mix of the deposit book remains a key focus in reducing the high cost of wholesale and longer term funding. This is critical as banks compete more aggressively for lower-cost deposit pools with longer behavioural duration and as they start to work towards the potential Basel III liquidity ratios.

Low interest rates, coupled with low domestic savings levels and the deleveraging of consumers, led to modest growth in retail deposits during 2010. As noted above, the increased competition and duration negatively impacted on net interest margins earned during 2H10.

Capital

The individual Capital Adequacy Ratios (‘CAR’) for the major banks continued to improve in 2H10. The average CAR increased from 15.2% to 15.3% over the comparable period, reinforcing the upward trend on higher capital ratios. Slightly more pronounced, however, is the rise in Tier 1 capital where the combined average ratio increased from 12.5% to 12.8%.

Basel III – a significant concern for banks

One of the main issues that has been preoccupying many banks is the impact of Basel III and other local regulatory changes to the capital structure of South African banks. The banks’ conservative approach has set them up well to face the challenges of compliance with the new rules. However, their dependence on short-term wholesale funding and the limited supply of South African government securities will make compliance with the liquidity rules more challenging.

This latter challenge is well recognised, to the extent that the Basel Committee is now developing a separate standard for jurisdictions which do not have sufficient high quality government securities available.

05101520253035404550

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Government Wholesale Corporate Retail Other

% Government % Wholesale % Corporate % Retail % Other

%Rm

Source – SARB

South Africa – Major Banks Analysis 19

Fundamental to the Basel III rules are the requirements for the banks to hold more capital of higher quality. In particular:

• All banks must hold a minimum common equity (common shares and retained earnings less deductions, some of which were previously taken against lower forms of capital) of 4.5% of risk weighted assets, which may be supplemented by Pillar 2 requirements (set by SARB based on individual bank risk profiles)

• A ‘conservation buffer’ of 2.5%, above the 4.5% minimum, must be created to absorb losses during periods of financial and economic stress. Drawing on this buffer during times of stress will result in constraints on earnings distributions

• A ‘counter-cyclical buffer’ ranging from 0 – 2.5% of common equity, determined by SARB as required, for instance in times of excessive credit growth.

The result of all these measures is that the new common equity (core Tier 1) ratio will be at least 7%. In addition, the banks will want to hold their own internal buffer, over and above this regulatory minimum, as part of normal risk management; particularly as the sanctions for going under 7% will involve restrictions on their ability to pay dividends. We suspect that banks may view the buffers as de facto minima due to the negative market signals associated with holding less capital than the required buffers.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10 1H09 2H09 1H10 2H10

ASA FSR NED SBK Combined results

Total Tier 2 capitalTotal Tier 1 capital

%

As well as these requirements for common equity, the banks are also required to hold Tier 1 capital to a minimum of 8.5% (i.e. including the conservation buffer, of which at least 7% is common equity) and total capital (i.e. Tier 1 and Tier 2) of at least 10.5%. In South Africa, additional capital requirements could push the total minimum capital requirement to 12% due to the Pillar 2 (a) add-on of 1.5% for banks.

Source – PwC Analysis

20 South Africa – Major Banks Analysis

Banks adopting the internal rating based (IRB) approach to credit risk would be particularly concerned about the proposed re-introduction of the 6% scaling factor to credit risk weighted assets. This is not strictly a Basel III amendment but has been proposed in draft amendments to the South African regulations to the Banks Act and will be implemented along with the other Basel III amendments. This proposed 6% scaling factor could drastically increase the capital requirement of banks that apply IRB approaches to credit risk. It is estimated that the 6% scaling factor could result in a reduction of 45 to 60 basis points in the capital adequacy ratio of the banks adopting this approach.

In addition to being a reminder of how much common equity the banks have raised in recent years, the table shows that the major banks are in good shape in relation to the requirements. Based on our estimates, collectively the banks would meet the 7% ratio for common equity as at 31 December 2010 and even the 11 % minimum Tier 1 ratio (including the counter-cyclical buffer of 2.5%). The major banks have an average of 12.75% Tier 1 ratio based on the current Basel II regulations. This has prompted many commentators to suggest that the banks are currently over-capitalised. The results presentations of the major banks have all addressed this issue in varying levels of detail. What is clear is that given the uncertainty as to how the Basel III rules will be implemented in South Africa, the major banks have been cautious in returning capital to shareholders or in setting their capital targets for the years ahead. Our analysis of the issue is that the apparent “surplus” of Tier 1 capital above the minimum does

not take into consideration the fact that the CAR under the current Basel II rules is not the same as the Basel III CAR, as the Basel III rules are stricter. It also does not take into account the additional capital requirements from Pillars 2(a) or (b) or indeed what these add-on ratios may be. Therefore it would appear to be premature to suggest that the banks should return capital to their shareholders.

We also suspect that there will be some upward pressure on equity levels globally. For instance, Switzerland has announced capital requirements on its banks in the high teens. We believe that the Basel III requirements represent something of a compromise on the part of regulators in order to minimise any adverse impact on economic growth.

Will the new liquidity rules bite credit growth?

The new liquidity rules are aimed to ensure that banks’ funding is on a more sustainable, long-term basis, thus enabling better liquidity during times of market turbulence. They involve two ratios:

• The net stable funding requirement (NSFR) will target better duration matching of assets and liabilities. This will be introduced from 2018, following an observation period starting in 2012.

• The liquidity coverage ratio (LCR) will require banks to hold sufficient high quality assets to survive periods of severe market stress. This will be introduced from 2015, following an observation period starting in 2011.

Both these measures create challenges for the South African banks. The stable funding requirement is a challenge because it allows minimal funding of assets through short-term liabilities, whereas in the years leading up to these new rules, the banks relied fairly heavily on short-term funding.

Analysts’ research reports suggested that as of July 2010 (and before recently announced modifications), the South African banks had a net NSFR range of 40% to 60%, short of the benchmark of 100%.

The liquidity coverage ratio is a challenge in South Africa because the assets most liquid during periods of market stress are government securities, and the strong financial position of South Africa’s public sector means there is a small pool of government securities relative to the size of bank balance sheets.

The challenge for the South African banks in meeting these requirements has been made somewhat less daunting in the past few months by Basel Committee announcements which make the requirements less onerous to meet.

As Lord Turner (Chairman of the UK’s Financial Standards

Authority) is reported to have said, “If we were philosopher

kings designing a banking system entirely anew for a

greenfield economy, should we have set still higher capital

ratios than in the Basel III regime? Yes I believe we should.”

South Africa – Major Banks Analysis 21

For instance, for the LCR:

• The run-off rates of certain retail and small and medium enterprise deposits during periods of market stress have been reduced.

• Likewise, assumed outflows of certain funding from central banks and government have also been reduced.

• A new category of ‘level 2’ liquid assets (e.g. bonds of certain public sector enterprises and covered bonds of other banks) has been introduced and may account for up to 40% of the requirement.

Despite these changes, the core issue for the South African banks regarding the LCR is the shortage of South African Government Bonds. The Basel Committee is currently determining its response to this challenge for jurisdictions such as South Africa.

The position regarding the NSFR is much the same. Recent announcements have eased the impact of the proposals in relation to jurisdictions such as South Africa, for instance in how mortgages are treated.

Nonetheless the postponement of their application until 2018 (following an observation phase) is an indication of the extent of transition required.

One of the major contributors to the challenges in meeting the NSFR in South Africa is that a large portion of the savings pool is being held within pension funds and other fund managers. This, together with the structural challenges to unlocking such liquidity, has exacerbated this

issue for South African banks. For example, pension funds are currently limited in terms of Regulation 28 of the Pension Funds Act in terms of investing in bank debt instruments. They are currently limited to allocating 20% of their total assets to banks debt instruments. In many cases this 20% already includes the liquid assets required by the pension funds for operational purposes, thereby further limiting the amount of longer term investment in banks liabilities. This has the effect of reducing the availability of additional longer term funding to banks, exacerbating the problem for the NSFR.

The project by the National Treasury to investigate potential reforms to various regulations such as those relating to pension funds, collective investment schemes and tax regulations could potentially unlock some of the liquidity that is not currently available to banks.

Another potential source of liquidity for South African banks that has not received much public debate is covered bonds, i.e. banks issuing bonds secured by ring-fenced (inevitably very high quality) assets on their balance sheet. Covered bonds have received a lot of attention and debate in countries such as New Zealand and Australia. Covered bonds could provide South African banks with another option to access long-duration wholesale funding, and additionally the bonds could potentially be treated as ‘eligible securities’ for LCR purposes.

The worst-case scenario would be where the NSFR requirements can only be met through the banks rationing credit (assets) to less than, say, the rate of growth in nominal

GDP. On current specifications, this risk cannot be ruled out, but we believe in practice it is a low risk – the National Treasury and the SARB are acutely aware of this risk and, given the long lead times, the transition can be managed.

22 South Africa – Major Banks Analysis

Key

ba

nk

ing

sta

tist

ics

– A

nn

ua

lRm

Gro

wth

2010

2009

2010

2009

2010

2009

2010

2009

2010

2009

09/1

0

Tota

l ass

ets

716,

470

71

0,79

6

69

5,80

9

80

2,38

9

608,

718

570,

703

1,

341,

420

1,

297,

788

3,

362,

417

3,

381,

676

-0

.57%

Gro

ss L

oans

and

acc

epta

nces

537,

414

55

5,35

3

46

1,50

3

42

2,12

9

486,

499

460,

099

73

0,13

1

742,

173

2,

215,

547

2,

179,

754

1.

64%

Tota

l dep

osit

s39

3,51

7

392,

906

543,

713

487,

929

49

0,44

0

46

9,35

5

796,

635

768,

548

2,

224,

305

2,

118 ,

738

4.

98%

Risk

wei

ghte

d as

sets

413,

013

38

6,26

4

37

8,49

0

34

6,04

9

323,

681

326,

466

62

0,06

4

59

9,82

2

1,73

5,24

8

1,65

8,60

1

4.62

%

Non

-per

form

ing

loan

s39

,641

36

,089

21

,117

23

,121

26

,765

27

,045

42

,701

48

,376

13

0,22

4

134,

631

-3

.27%

Impa

irm

ents

-13,

902

-1

3,15

8

-9

,844

-1

0,99

1

-11,

226

-9,7

98

-17,

106

-18,

666

-5

2,07

8

-52,

613

-1

.02%

Colle

ctive

pro

visi

ons

-2,0

87

-3,2

22

-3,1

17

-3,7

03

-2,1

54

-1,9

68

-4,8

84

-5,5

88

-12,

242

-14,

481

-15.

46%

Indi

vidu

ally

ass

esse

d pr

ovis

ions

-11,

815

-9

,936

-6

,727

-7

,288

-9

,072

-7

,830

-1

2,22

2

-1

3,07

8

-3

9,83

6

-3

8,13

2

4.

47%

Non

-per

form

ing

loan

s (%

of a

dvan

ces)

7.4%

6.5%

4.6%

5.5%

5.5%

5.9%

5.8%

6.5%

5.8%

6.1%

-4.3

9%Im

pair

men

t cha

rge

(% o

f ave

rage

adv

ance

s)1.

2%1.

7%0.

9%1.

5%1.

4%1.

5%1.

0%1.

3%1.

1%1.

5%-2

5.78

%Im

pair

men

t cov

erag

e ratio

35.1

%36

.5%

46.6

%47

.5%

41.9

%36

.2%

40.1

%38

.6%

40.9

%39

.7%

3.07

%Im

plie

d lo

ss g

iven

def

ault

29.8

%27

.5%

31.9

%31

.5%

33.9

%29

.0%

28.6

%27

.0%

31.0

%28

.8%

7.94

%

Net

inte

rest

inco

me

23,3

40

21,8

54

16,4

04

12,6

88

16,6

08

16,3

06

28,9

27

31,4

93

85,2

79

82,3

41

3.57

%N

on in

tere

st in

com

e19

,474

2 0

,232

28

,579

24

,193

13

,215

11

,906

44

,054

41

,620

10

5,32

2

97

,951

7.

53%

Tota

l ope

rati

ng in

com

e42

,814

42

,086

44

,983

36

,881

29

,823

28

,212

72

,981

73

,113

19

0,60

1

180,

292

5.

72%

Tota

l ope

ratin

g ex

pens

es-2

4,94

9

-23,

227

-26,

955

-2

2,11

3

-1

7,04

5

-15,

538

-47,

519

-4

3,58

9

-1

16,4

68

-104

,467

11

.49%

Core

ear

ning

s17

,865

18

,859

18

,028

14

,768

12

,778

12

,674

25

,462

29

,524

74

,133

75

,825

-2

.23%

Impa

irm

ent c

harg

e-6

,005

-8

,967

-4

,545

-7

,556

-6

,188

-6

,634

-7

,524

-1

2,09

7

-2

4,26

2

-35,

254

-31.

18%

Oth

er in

com

e/(e

xpen

ses)

-9 -5

0

816

98

0

-90

67

9

489

-9

1,20

6

1,60

0

-24.

63%

Inco

me

tax

expe

nses

-3,2

62

-2,3

40

- 3,9

26

-2,4

39

-1,3

64

-1,3

07

-4,9

65

-4,6

20

-13,

517

-1

0,70

6

26

.26%

Profi

t fo

r th

e pe

riod

8,58

9

7,50

2

10,3

73

5,75

3

5,13

6

5,41

2

13,4

62

12,7

98

37,5

60

31,4

65

19.3

7%

Attri

buta

ble

earn

ings

8,11

8

6,84

0

16,9

94

6,71

5

4,81

1

4,82

6

10,7

74

11,0

54

40,6

97

29,4

35

38.2

6%H

eadl

ine

earn

ings

8,04

1

7,62

1

10,0

04

6,87

8

4,90

0

4,27

7

10,9

69

11,2

53

33,9

14

30,0

29

12.9

4%

Oth

er o

peratin

g in

com

e (%

of t

otal

inco

me)

45.5

%48

.1%

63.5

%65

.6%

44.3

%42

.2%

60.4

%56

.9%

53.4

%53

.2%

0.42

%N

et in

tere

st m

argi

n (%

of t

otal

ass

ets)

3.2%

2.9%

2.1%

1.5%

2.9%

2.9%

2.6%

3.2%

2.7%

2.6%

3.16

%N

et in

tere

st m

argi

n (%

of a

vera

ge in

tere

st e

arni

ng a

dvan

ces)

4.0%

3.7%

3.6%

2.5%

3.4%

3.4%

3.8%

4.5%

3.7%

3.5%

4.52

%St

anda

rdis

ed effi

cien

cy r

atio

56.5

%53

.0%

59.1

%59

.3%

55.7

%53

.5%

63.1

%57

.3%

58.6

%55

.8%

4.99

%

Retu

rn o

n e

quit

y14

.3%

15.1

%19

.9%

13.8

%11

.1%

10.8

%12

.6%

13.4

%14

.5%

13.3

%9.

09%

Retu

rn o

n av

erag

e as

sets

1.1%

1.0%

1.3%

0.8%

0.8%

0.8%

1.0%

1.0%

1.1%

0.9%

17.9

2%

Tota

l num

ber

of s

taff

*36

,770

36

,150

38

,657

38

,760

27

,525

27

,037

48

,125

45

,937

15

1,07

7

147,

884

2.16

%

Tier

1

12.8

0%12

.80%

13.6

0%13

.50%

11.7

0%11

.50%

12.9

0%11

.80%

12.7

5 %12

.40%

2.82

%Ti

er 2

2.70

%2.

70%

1.70

%2.

10%

3.30

%3.

30%

2.40

%2.

80%

2.53

%2.

73%

-7.3

4%To

tal

15.5

0%15

.50%

15.3

0%15

.60%

15.0

0%14

.80%

15.3

0%14

.60%

15.2

8%15

.13%

* - S

taff

num

bers

for

Firs

tran

d w

ere

not r

epea

ted

in D

ecem

ber

2H10

Bala

nce

shee

t

Ass

et q

ualit

y &

pro

visi

onin

g

Profi

t &

loss

ana

lysi

s (i)

Key

data

Capi

tal r

atios

SBK

Com

bine

d A

SA

FSR

NED

South Africa – Major Banks Analysis 23

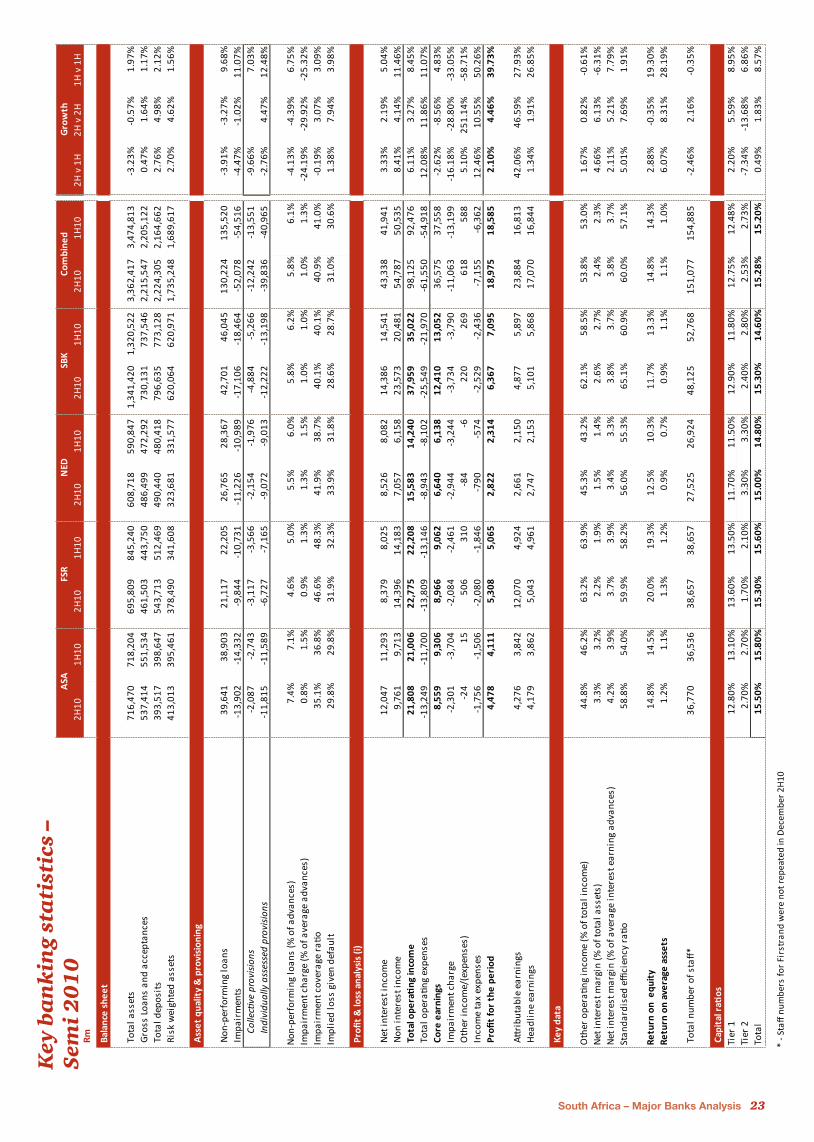

Rm2H

101H

102H

101H

102H

101H

102H

101H

102H

101H

102H

v 1

H2H

v 2

H1H

v 1

H

Bala

nce

shee

t

Tota

l ass

ets

716,

470

71

8,20

4

69

5,80

9

84

5,24

0

608,

718

590,

847

1,

341,

420

1,

320,

522

3,

362,

417

3,

474,

813

-3

.23%

-0.5

7%1.

97%

Gro

ss L

oans

and

acc

epta

nces

537,

414

55

1,53

4

46

1,50

3

44

3,75

0

486,

499

472,

292

73

0,13

1

73

7,54

6

2,21

5,54

7

2,20

5,12

2

0.47

%1.

64%

1.17

%To

tal d

epos

its

393,

517

39

8,64

7

54

3,71

3

51

2,46

9

490,

440

480,

418

79

6,63

5

77

3,12

8

2,22

4,30

5

2,16

4,66

2

2.76

%4.

98%

2.12

%Ri

sk w

eigh

ted

asse

ts41

3,01

3

395,

461

378,

490

341,

608

32

3,68

1

33

1,57

7

620,

064

620,

971

1,

735,

248

1,

689,

617

2.

70%

4.62

%1.

56%

Ass

et q

ualit

y &

pro

visi

onin

g

Non

-per

form

ing

loan

s39

,641

38

,903

21

,117

22

,205

26

,765

28

,367

42

,701

46

,045

13

0,22

4

13

5,52

0

-3

.91%

-3.2

7%9.

68%

Impa

irm

ents

-13,

902

-1

4,33

2

-9

,844

-1

0,73

1

-1

1,22

6

-10,

989

-17,

106

-1

8,46

4

-5

2,07

8

-5

4,51

6

-4

.47%

-1.0

2%11

.07%

Colle

ctive

pro

visi

ons

-2,0

87

-2,7

43

-3,1

17

-3,5

66

-2,1

54

-1,9

76

-4,8

84

-5,2

66

-12,

242

-1

3,55

1

-9

.66%

7.03

%In

divi

dual

ly a

sses

sed

prov

isio

ns-1

1,81

5

-11,

589

-6,7

27

-7,1

65

-9,0

72

-9,0

13

-12,

222

-13,

198

-39,

836

-4

0,96

5

-2

.76%

4.47

%12

.48%

Non

-per

form

ing

loan

s (%

of a

dvan

ces)

7.4%

7.1%

4.6%

5.0%

5.5%

6.0%

5.8%

6.2%

5.8%

6.1%

-4.1

3%-4

.39%

6.75

%Im

pair

men

t cha

rge

(% o

f ave

rage

adv

ance

s)0.

8%1.

5%0.

9%1.

3%1.

3%1.

5%1.

0%1.

0%1.

0%1.

3%-2

4.19

%-2

9.92

%-2

5.32

%Im

pair

men

t cov

erag

e ratio

35.1

%36

.8%

46.6

%48

.3%

41.9

%38

.7%

40.1

%40

.1%

40.9

%41

.0%

-0.1

9%3.

07%

3.09

%Im

plie

d lo

ss g

iven

def

ault

29.8

%29

.8%

31.9

%32

.3%

33.9

%31

.8%

28.6

%28

.7%

31.0

%30

.6%

1.38

%7.

94%

3.98

%

Profi

t &

loss

ana

lysi

s (i)

Net

inte

rest

inco

me

12,0

47

11,2

93

8,37

9

8,02

5

8,52

6

8,08

2

14,3

86

14,5

41

43,3

38

41,9

41

3.33

%2.

19%

5.04

%N

on in

tere

st in

com

e9,

761

9,71

3

14,3

96

14,1

83

7,05

7

6,15

8

23,5

73

20,4

81

54,7

87

50,5

35

8.41

%4.

14%

11.4

6%To

tal o

perati

ng in

com

e21

,808

21

,006

22

,775

22

,208

15,5

83

14,2

40

37,9

59

35,0

22

98,1

25

92,4

76

6.11

%3.

27%

8.45

%To

tal o

peratin

g ex

pens

es-1

3,24

9

-11,

700

-13,

809

-13,

146

-8,9

43

-8,1

02

-25,

549

-21,

970

-6

1,55

0

-5

4,91

8

12.0

8%11

.86%

11.0

7%Co

re e

arni

ngs

8,55

9

9,

306

8,

966

9,

062

6,

640

6,

138

12

,410

13

,052

36

,575

37

,558

-2

.62%

-8.5

6%4.

83%

Impa

irm

ent c

harg

e-2

,301

-3

,704

-2

,084

-2

,461

-2

,944

-3

,244

-3

,734

-3

,790

-1

1,06

3

-1

3,19

9

-16.

18%

-28.

80%

-33.

05%

Oth

er in

com

e/(e

xpen

ses)

-24

15

50

6

310

-8

4

-6 22

0

269

61

8

588

5.

10%

251.

14%

-58.

71%

Inco

me

tax

expe

nses

-1,7

56

-1,5

06

-2,0

80

-1,8

46

-790

-574

-2

,529

-2

,436

-7

,155

-6

,362

12

.46%

10.5

5%50

.26%

Profi

t fo

r th

e pe

riod

4,47

8

4,

111

5,

308

5,

065

2,

822

2,

314

6,

367

7,

095

18

,975

18

,585

2.

10%

4.46

%39

.73%

Attri

buta

ble

earn

ings

4,27

6

3,

842

12

,070

4,

924

2,

661

2,

150

4,

877

5,

897

23

,884

16

,813

42

.06%

46.5

9%27

.93%

Hea

dlin

e ea

rnin

gs4,

179

3,86

2

5,04

3

4,96

1

2,74

7

2,15

3

5,10

1

5,86

8

17,0

70

16,8

44

1.34

%1.

91%

26.8

5%

Key

data

Oth

er o

peratin

g in

com

e (%

of t

otal

inco

me)

44.8

%46

.2%

63.2

%63

.9%

45.3

%43

.2%

62.1

%58

.5%

53.8

%53

.0%

1.67

%0.

82%

-0.6

1%N

et in

tere

st m

argi

n (%

of t

otal

ass

ets)

3.3%

3.2%

2.2%

1.9%

1.5%

1.4%

2.6%

2.7%

2.4%

2.3%

4.66

%6.

13%

-6.3

1%N

et in

tere

st m

argi

n (%

of a

vera

ge in

tere

st e

arni

ng a

dvan

ces)

4.2%

3.9%

3.7%

3.9%

3.4%

3.3%

3.8%

3.7%

3.8%

3.7%

2.11

%5.

21%

7.79

%St

anda

rdis

ed effi

cien

cy r

atio

58.8

%54

.0%

59.9

%58

.2%

56.0

%55

.3%

65.1

%60

.9%

60.0

%57

.1%

5.01

%7.

69%

1.91

%

Retu

rn o

n e

quit

y14

.8%

14.5

%20

.0%

19.3

%12

.5%

10.3

%11

.7%

13.3

%14

.8%

14.3

%2.

88%

-0.3

5%19

.30%

Retu

rn o

n av

erag

e as

sets

1.2%

1.1%

1.3%

1.2%

0.9%

0.7%

0.9%

1.1%

1.1%

1.0%

6.07

%8.

31%

28.1

9%

Tota

l num

ber

of s

taff

*36

,770

36

,536

38

,657

38

,657

27

,525

26

,924

48

,125

52

,768

15

1,07

7

154,

885

-2.4

6%2.

16%

-0.3

5%

Capi

tal r

atios

Tier

1

12.8

0%13

.10%

13.6

0%13

.50%

11.7

0%11

.50%

12.9

0%11

.80%

12.7

5%12

.48%

2.20

%5.

59%

8.95

%Ti

er 2

2.70

%2.

70%

1.70

%2.

10%

3.30

%3.

30%

2.40

%2.

80%

2.53

%2.

73%

-7.3

4%-1

3.68

%6.

86%

Tota

l15

.50%

15.8

0%15

.30%

15.6

0%15

.00%

14.8

0%15

.30%

14.6

0%15

.28%

15.2

0%0.

49%

1.83

%8.

57%

Gro

wth

Com

bine

d A

SA

FSR

NED

SBK

* - S

taff

num

bers

for

Firs

tran

d w

ere

not r

epea

ted

in D