Sourcing trends and predictions for 2015 and beyond

15

Top trends and predictions for 2015 and beyond 1Q15 Global Sourcing Advisory Pulse Survey results

Transcript of Sourcing trends and predictions for 2015 and beyond

Top trends and

predictions for 2015

and beyond

1Q15 Global Sourcing Advisory

Pulse Survey results

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

1

KPMG’s shared services and outsourcing advisory practice

The Shared Services and Outsourcing Advisory practice brings a specialized global

team of more than 800 professionals within KPMG’s global network of independent

member firms operating in 155 countries. These professionals help clients design,

build, and manage information technology (IT) and business processes across the

enterprise.

We help clients align their business strategy, organization and execution to enable

them to manage the entire IT and business process life cycle, improving business

performance, and laying the groundwork for genuine business transformation.

We apply focused research, automating tools, proprietary data, clear business

acumen, and a forward-thinking mind-set to provide timely, objective, actionable

advice and practical approaches for clients.

Who we are

What we do

How we do it

KPMG has the ability to help member firms’ clients transform enterprise services to help improve

value, increase agility and create sustainable business performance.

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

2

KPMG Pulse Surveys

Focus on performance, trends, and futures

Launched in 2004 by EquaTerra*

Part of a growing family of KPMG Pulse market research studies

The Global Sourcing Advisory Pulse Surveys

The surveys are a quarterly review of global business services (GBS) market trends and individual

observations from the ‘front lines’.

800+ KPMG sourcing advisors

20 leading global business, IT, and cloud service providers

KPMG market research

HfS Research

The annual Top Trends and Predictions Pulse also polls 300+ additional KPMG executives globally across Audit, Tax and Advisory

Drivers for GBS usage

Demand and buying patterns

Deal attributes

Thematic topics for each Pulse survey

– Top Trends & Predictions for

2015

Call center/customer care

Finance and Accounting

Human Resources

Information Technology

Procurement

Real Estate and Facilities Management

Vertical Industry BPO

Emerging BPO/KPO functions

Input sources: Topics evaluated: Primary functional focus:

* KPMG LLP (US) KPMG Holdings Limited (UK) and KPMG International acquired the business and subsidiaries of advisory firm EquaTerra, Inc. in February 2011.

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

3

Summary – key findings

2

4

Top corporate initiatives in 2015

Changes to investment patters and overall market conditions

1 Top negative and positive trends for 2015

Top challenges and capabilities required for initiatives 3

Attracting, retaining and managing skilled talent will be the number one concern facing most

global companies for the foreseeable future. Even as these organizations are being forced

to wage an ongoing and fierce ‘War for Talent’, many will also be preoccupied with concerns

over precarious economic/market conditions and deciding which technologies to leverage.

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

4

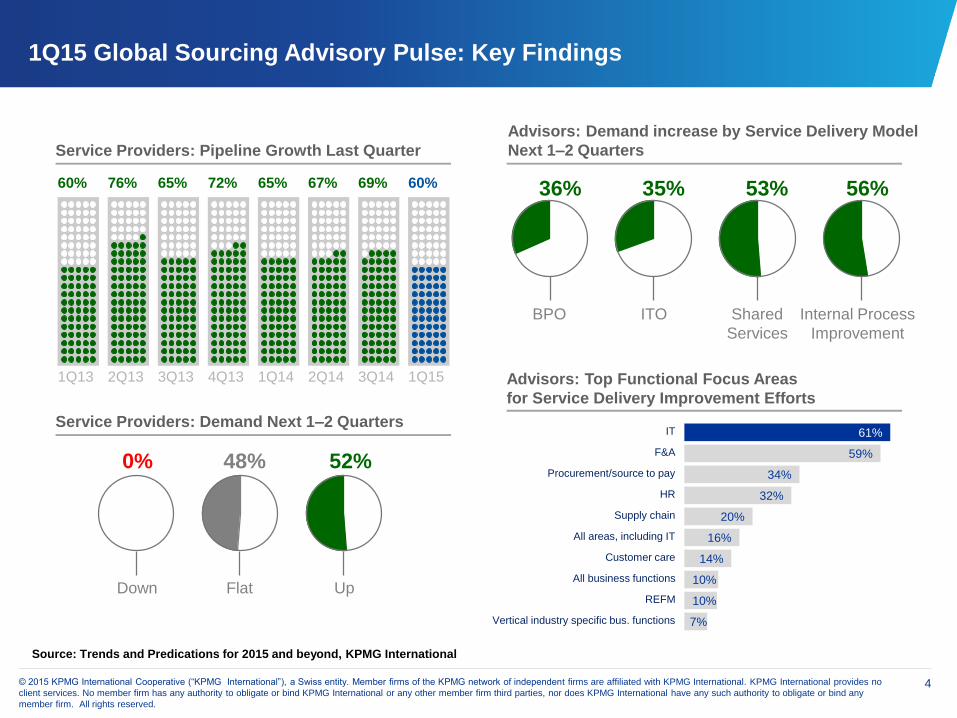

Shared

Services

53%

ITO

35%

BPO

36%

Internal Process

Improvement

56%

Flat

48%

Up

52%

Down

0%

60%

1Q13

76%

2Q13

65%

3Q13

72%

4Q13

65%

1Q14

67%

2Q14

60%

1Q15

69%

3Q14

Service Providers: Pipeline Growth Last Quarter

Advisors: Demand increase by Service Delivery Model

Next 1–2 Quarters

Advisors: Top Functional Focus Areas

for Service Delivery Improvement Efforts

Service Providers: Demand Next 1–2 Quarters

7%

10%

10%

14%

16%

20%

32%

34%

59%

61%

Vertical industry specific bus. functions

REFM

All business functions

Customer care

All areas, including IT

Supply chain

HR

Procurement/source to pay

F&A

IT

1Q15 Global Sourcing Advisory Pulse: Key Findings

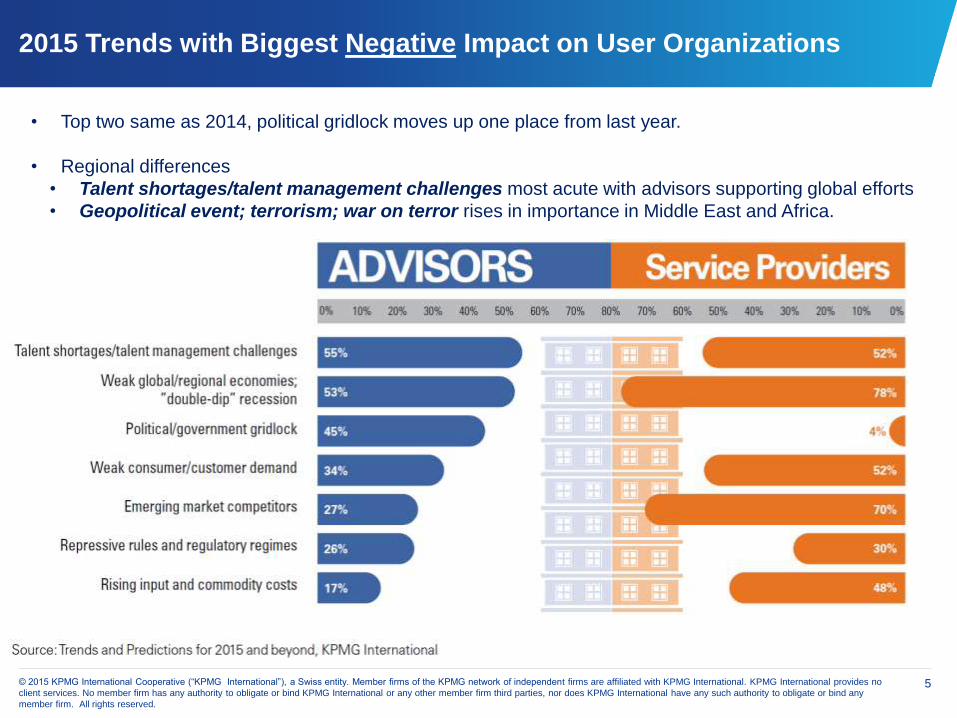

Source: Trends and Predications for 2015 and beyond, KPMG International

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

5

2015 Trends with Biggest Negative Impact on User Organizations

• Top two same as 2014, political gridlock moves up one place from last year.

• Regional differences

• Talent shortages/talent management challenges most acute with advisors supporting global efforts

• Geopolitical event; terrorism; war on terror rises in importance in Middle East and Africa.

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

6

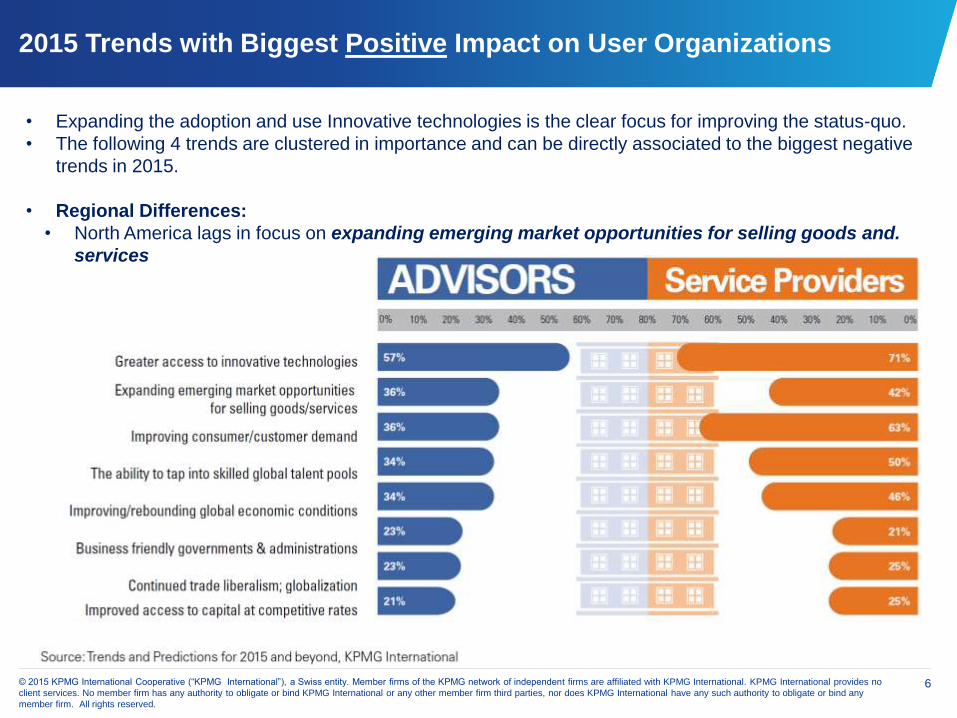

2015 Trends with Biggest Positive Impact on User Organizations

• Expanding the adoption and use Innovative technologies is the clear focus for improving the status-quo.

• The following 4 trends are clustered in importance and can be directly associated to the biggest negative

trends in 2015.

• Regional Differences:

• North America lags in focus on expanding emerging market opportunities for selling goods and.

services

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

7

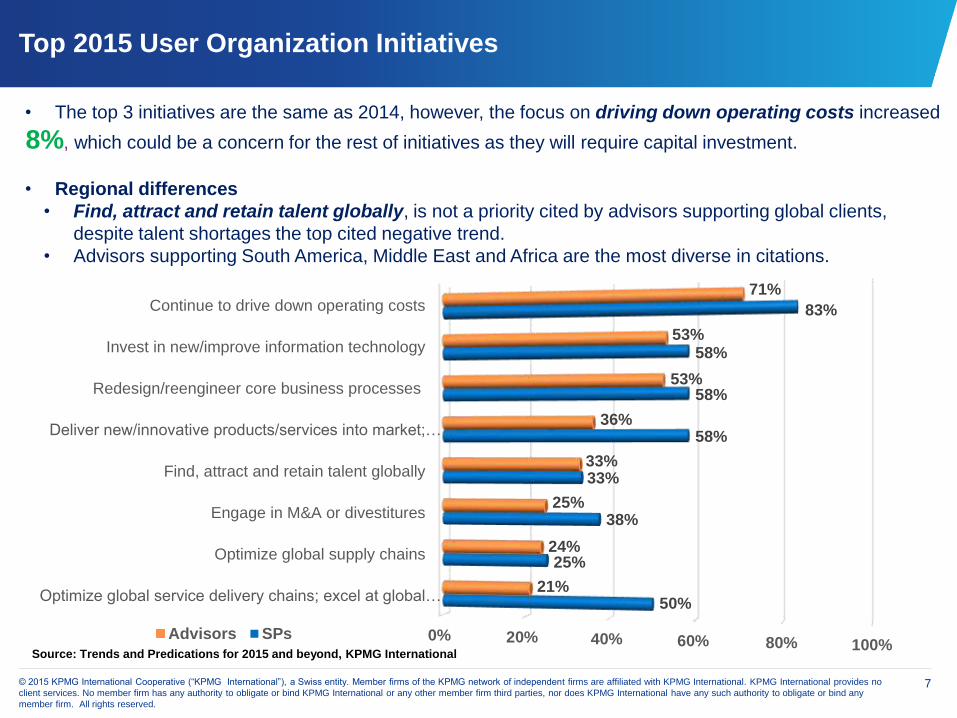

Top 2015 User Organization Initiatives

0% 20% 40% 60% 80% 100%

Optimize global service delivery chains; excel at global…

Optimize global supply chains

Engage in M&A or divestitures

Find, attract and retain talent globally

Deliver new/innovative products/services into market;…

Redesign/reengineer core business processes

Invest in new/improve information technology

Continue to drive down operating costs

50%

25%

38%

33%

58%

58%

58%

83%

21%

24%

25%

33%

36%

53%

53%

71%

Advisors SPs

• The top 3 initiatives are the same as 2014, however, the focus on driving down operating costs increased

8%, which could be a concern for the rest of initiatives as they will require capital investment.

• Regional differences

• Find, attract and retain talent globally, is not a priority cited by advisors supporting global clients,

despite talent shortages the top cited negative trend.

• Advisors supporting South America, Middle East and Africa are the most diverse in citations.

Source: Trends and Predications for 2015 and beyond, KPMG International

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

8

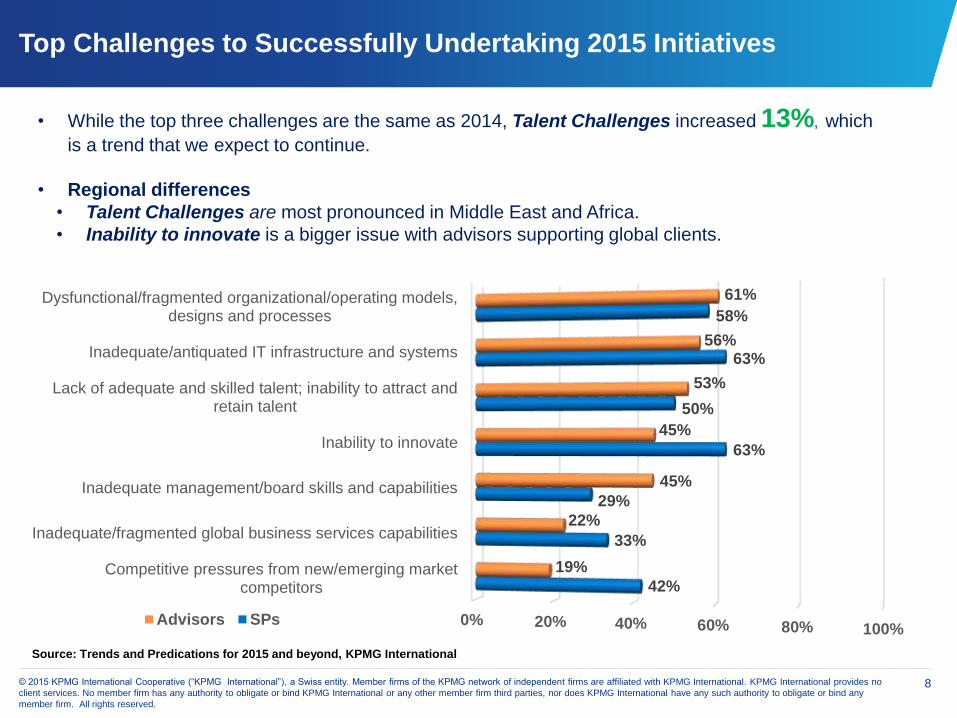

Top Challenges to Successfully Undertaking 2015 Initiatives

0% 20% 40% 60% 80% 100%

Competitive pressures from new/emerging marketcompetitors

Inadequate/fragmented global business services capabilities

Inadequate management/board skills and capabilities

Inability to innovate

Lack of adequate and skilled talent; inability to attract andretain talent

Inadequate/antiquated IT infrastructure and systems

Dysfunctional/fragmented organizational/operating models,designs and processes

42%

33%

29%

63%

50%

63%

58%

19%

22%

45%

45%

53%

56%

61%

Advisors SPs

• While the top three challenges are the same as 2014, Talent Challenges increased 13%, which

is a trend that we expect to continue.

• Regional differences

• Talent Challenges are most pronounced in Middle East and Africa.

• Inability to innovate is a bigger issue with advisors supporting global clients.

Source: Trends and Predications for 2015 and beyond, KPMG International

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

9

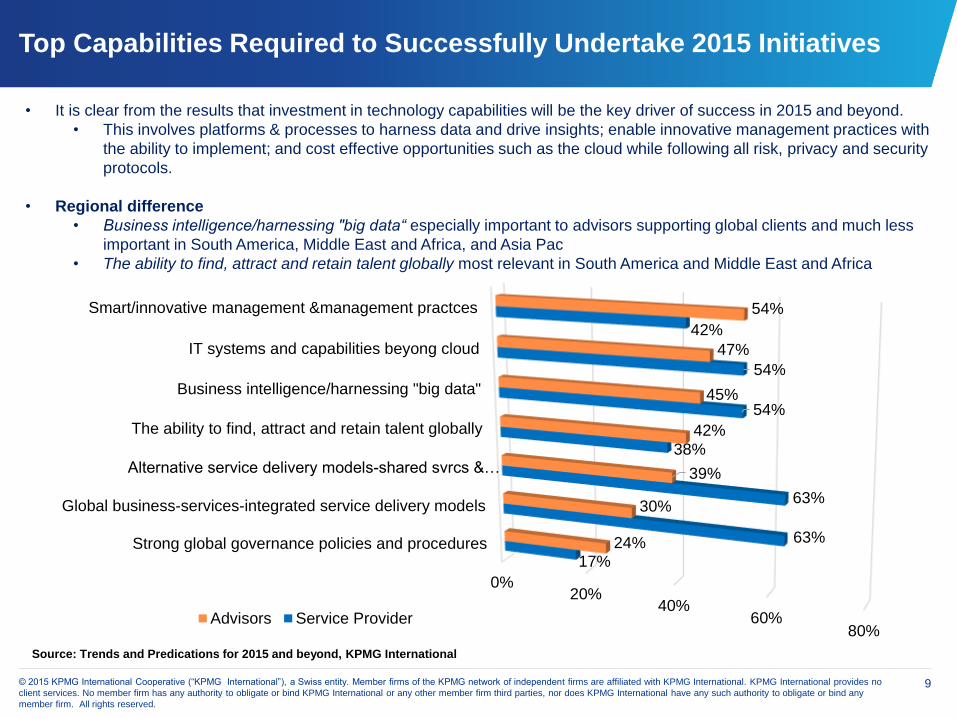

Top Capabilities Required to Successfully Undertake 2015 Initiatives

• It is clear from the results that investment in technology capabilities will be the key driver of success in 2015 and beyond.

• This involves platforms & processes to harness data and drive insights; enable innovative management practices with

the ability to implement; and cost effective opportunities such as the cloud while following all risk, privacy and security

protocols.

• Regional difference

• Business intelligence/harnessing "big data“ especially important to advisors supporting global clients and much less

important in South America, Middle East and Africa, and Asia Pac

• The ability to find, attract and retain talent globally most relevant in South America and Middle East and Africa

0%20%

40%60%

80%

Strong global governance policies and procedures

Global business-services-integrated service delivery models

Alternative service delivery models-shared svrcs &…

The ability to find, attract and retain talent globally

Business intelligence/harnessing "big data"

IT systems and capabilities beyong cloud

Smart/innovative management &management practces

17%

63%

63%

38%

54%

54%

42%

24%

30%

39%

42%

45%

47%

54%

Advisors Service Provider

Source: Trends and Predications for 2015 and beyond, KPMG International

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

10

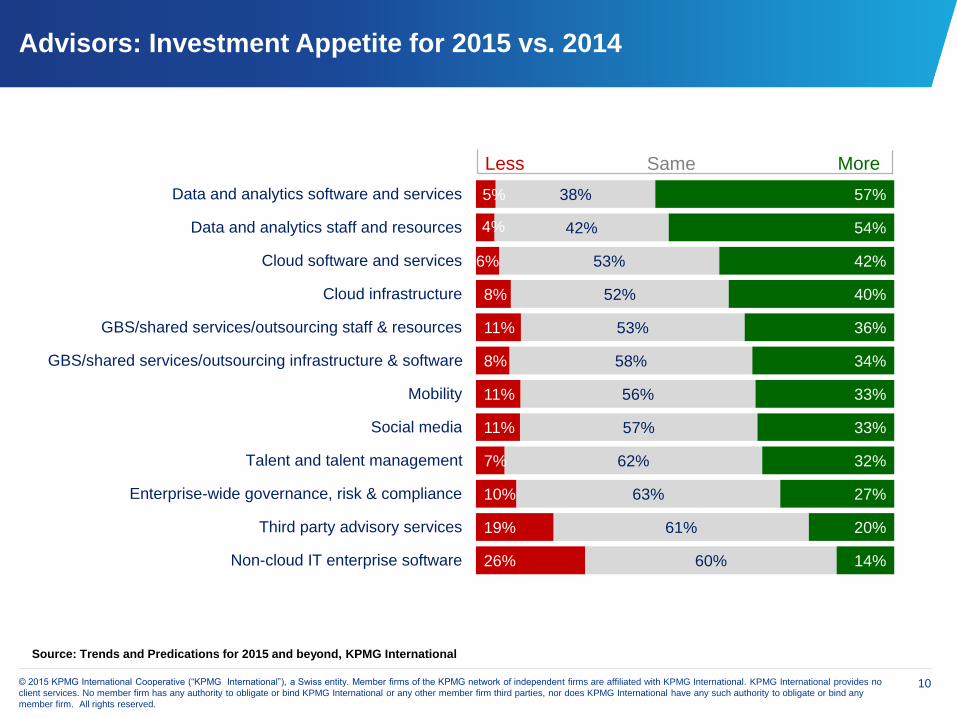

Advisors: Investment Appetite for 2015 vs. 2014

26%

19%

10%

7%

11%

11%

8%

11%

8%

6%

4%

5%

60%

61%

63%

62%

57%

56%

58%

53%

52%

53%

42%

38%

14%

20%

27%

32%

33%

33%

34%

36%

40%

42%

54%

57%

Non-cloud IT enterprise software

Third party advisory services

Enterprise-wide governance, risk & compliance

Talent and talent management

Social media

Mobility

GBS/shared services/outsourcing infrastructure & software

GBS/shared services/outsourcing staff & resources

Cloud infrastructure

Cloud software and services

Data and analytics staff and resources

Data and analytics software and services

Less Same More

Source: Trends and Predications for 2015 and beyond, KPMG International

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

11

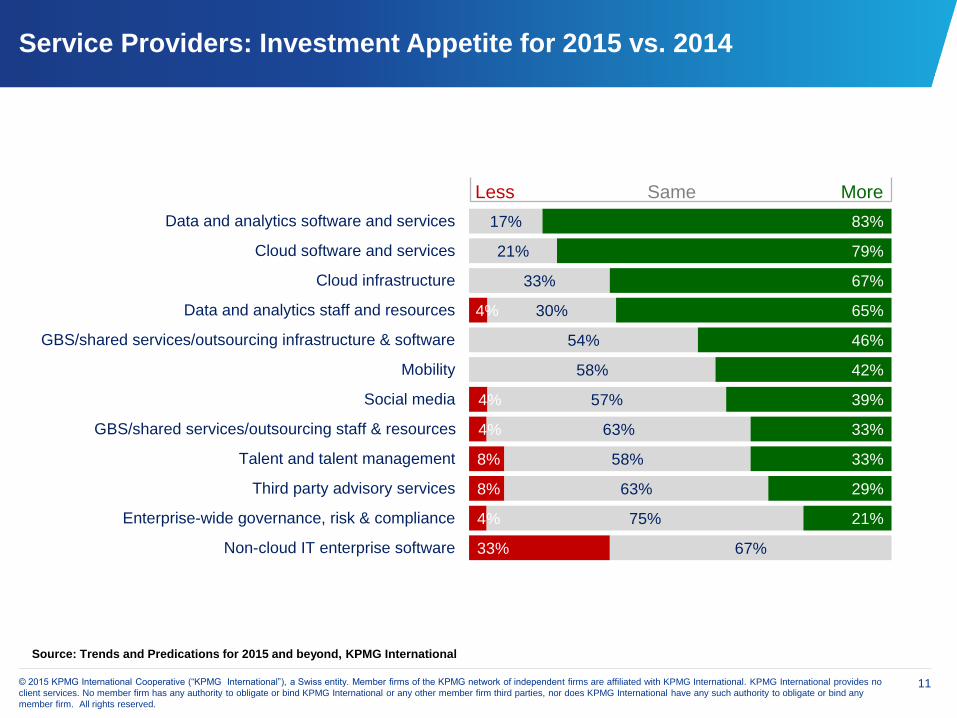

Service Providers: Investment Appetite for 2015 vs. 2014

33%

4%

8%

8%

4%

4%

4%

67%

75%

63%

58%

63%

57%

58%

54%

30%

33%

21%

17%

21%

29%

33%

33%

39%

42%

46%

65%

67%

79%

83%

Non-cloud IT enterprise software

Enterprise-wide governance, risk & compliance

Third party advisory services

Talent and talent management

GBS/shared services/outsourcing staff & resources

Social media

Mobility

GBS/shared services/outsourcing infrastructure & software

Data and analytics staff and resources

Cloud infrastructure

Cloud software and services

Data and analytics software and services

Less Same More

Source: Trends and Predications for 2015 and beyond, KPMG International

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

12

What we think

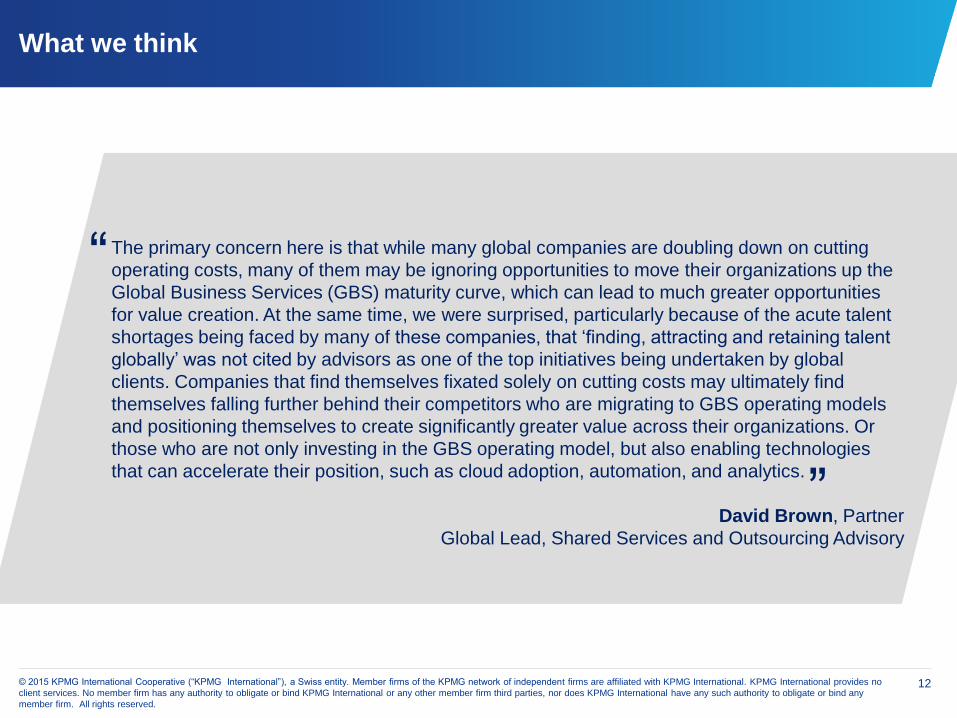

The primary concern here is that while many global companies are doubling down on cutting

operating costs, many of them may be ignoring opportunities to move their organizations up the

Global Business Services (GBS) maturity curve, which can lead to much greater opportunities

for value creation. At the same time, we were surprised, particularly because of the acute talent

shortages being faced by many of these companies, that ‘finding, attracting and retaining talent

globally’ was not cited by advisors as one of the top initiatives being undertaken by global

clients. Companies that find themselves fixated solely on cutting costs may ultimately find

themselves falling further behind their competitors who are migrating to GBS operating models

and positioning themselves to create significantly greater value across their organizations. Or

those who are not only investing in the GBS operating model, but also enabling technologies

that can accelerate their position, such as cloud adoption, automation, and analytics.

David Brown, Partner

Global Lead, Shared Services and Outsourcing Advisory

“

”

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no

client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

13

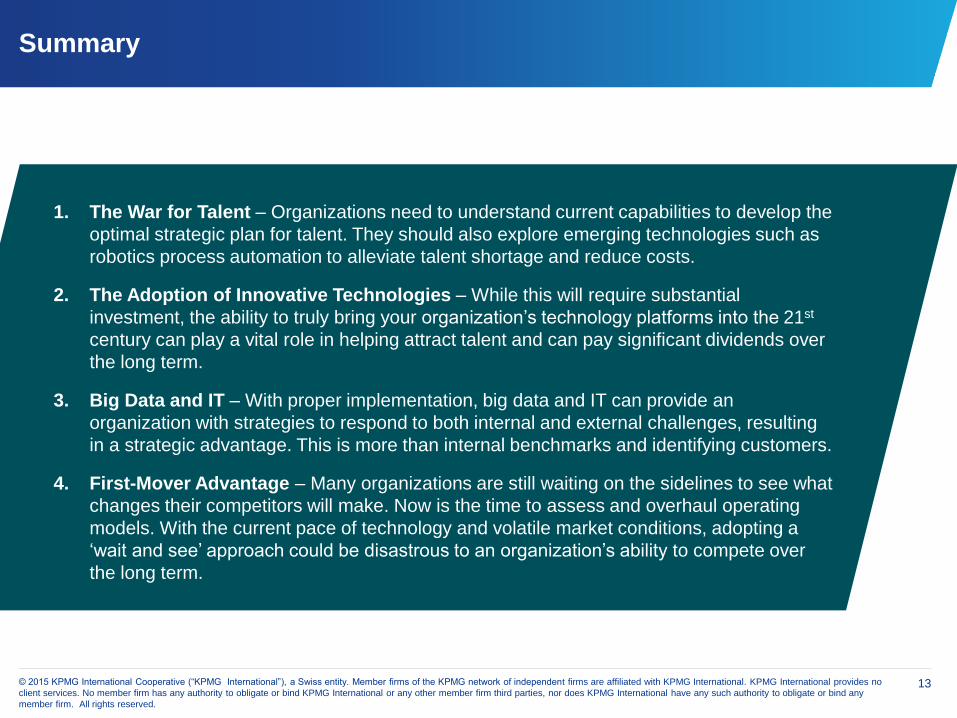

Summary

1. The War for Talent – Organizations need to understand current capabilities to develop the

optimal strategic plan for talent. They should also explore emerging technologies such as

robotics process automation to alleviate talent shortage and reduce costs.

2. The Adoption of Innovative Technologies – While this will require substantial

investment, the ability to truly bring your organization’s technology platforms into the 21st

century can play a vital role in helping attract talent and can pay significant dividends over

the long term.

3. Big Data and IT – With proper implementation, big data and IT can provide an

organization with strategies to respond to both internal and external challenges, resulting

in a strategic advantage. This is more than internal benchmarks and identifying customers.

4. First-Mover Advantage – Many organizations are still waiting on the sidelines to see what

changes their competitors will make. Now is the time to assess and overhaul operating

models. With the current pace of technology and volatile market conditions, adopting a

‘wait and see’ approach could be disastrous to an organization’s ability to compete over

the long term.

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms

of the KPMG network of independent firms are affiliated with KPMG International. KPMG

International provides no client services.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide

accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No

one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia kpmg.com/app

Contact Us:

David BrownPartner

Global Lead, Shared Services

and Outsourcing Advisory

T: +1 314 803 5369

Visit www.kpmg.com/2015SourcingTrends

for more information on the 2015 Sourcing

Trends Survey.