SOURCES OF GOVERNMENT REVENUE Chapter 9. TAXES ARE THE SINGLE MOST IMPORTANT WAY OF RAISING REVENUE...

25

SOURCES OF GOVERNMENT REVENUE Chapter 9

-

Upload

jasmine-stanley -

Category

Documents

-

view

217 -

download

0

Transcript of SOURCES OF GOVERNMENT REVENUE Chapter 9. TAXES ARE THE SINGLE MOST IMPORTANT WAY OF RAISING REVENUE...

SOURCES OF GOVERNMENT

REVENUE

Chapter 9

TAXES ARE THE SINGLE MOST IMPORTANT WAY OF RAISING REVENUE FOR THE GOVERNMENT

I. Economic Impact of Taxes

1. Increased Production Costs1. It now costs more to produce an item

2. This will decrease supply and increase price

A. Producer Paid Taxes

The person being taxed does not always bear the burden…

B. Consumer Paid Taxes

1. Changes incentives to save, invest and work 1. Mortgage rates, auto financing

2. Affects resource allocation

2. “Sin Tax” – manipulating taxes to discourage behavior1. Tax on socially undesirable goods

2. Alcohol, tobacco, gasoline

I. Economic Impact of Taxes

Sin Tax History Antismoking advocates tout this month's record increase

in the federal cigarette-tax rate, which on April 1 spiked from 39¢ to $1.01 per pack, as a move that will bolster the federal budget while saving an estimated 900,000 lives. Supporters say the measure will stop 2 million kids from lighting up and spur about 1 million adults to quit, but the sharp hike has some smokers fuming. Cigarette taxes, detractors argue, are a way for governments to line their coffers by legislating personal choice--and a prime example of a regressive "sin tax," the term often used for fees tacked on to popular vices like drinking, gambling and smoking.

Sin Tax

The sin tax is an established tactic. In the early 1500s, Pope Leo X underwrote his lavish lifestyle in part by taxing licensed prostitutes, and Peter the Great preyed on Russian vanity two centuries later by charging men who grew beards. In the Federalist papers, American patriot Alexander Hamilton proposed an excise tax on alcohol to boost revenues and curb consumption. The measure, enacted in 1791, sparked the Whiskey Rebellion, in which federal authorities were forced to quash an uprising by livid Pennsylvania settlers.

Sin Tax

The U.S. has taxed cigarettes since the Civil War. This month's increase--signed by a President who's trying to kick the habit himself--comes as recession-battered states are considering charges on everything from pornography to marijuana as a way to pad their budgets. Tobacco taxation enjoys broad public support, but other recent efforts to impose sin taxes have sputtered. Proof, perhaps, that in trying times, doing bad can feel really good.

http://www.time.com/time/magazine/article/0,9171,1889187,00.html

II. Criteria for Effective Taxes

EQUITY

SIMPLICITYEFFICIENCY

Equity

Fairness – Perceived What is fair? If Everyone Pays the same? If you make more you pay more? If you use more you pay more? Loopholes

Simplicity

Easily understood Individual Income Taxes

Tax on earnings Sales tax

General tax placed on items sold Food, Child Care, Rx

Efficiency

Easily Administered Payroll, Sales, Income, Road Toll

Serves its’ purpose Raises enough $ Example: 1991 Luxury tax on private aircraft

Raised $53,000 in tax revenue Caused job cuts and cost over $53,000 in

unemployment benefits. Congress repealed it

III. Principles of TaxationA. Benefit Principle

1. Those who benefit should pay an amount. proportionate to their benefit

Road toll, gas tax, sales tax

2. Limitationsa. Benefits are hard to measure

Do only those who own cars benefit from toll roads?

b. Government Services Those who benefit the most can least afford the taxes (low-

income housing) Recovery and Reinvestment Act

B. Ability-To-Pay Principle1. Those who make more money pay more in taxes

IV. Types of Taxes

1. Proportional1. Directly related to value of item taxes2. Such as Property Tax

2. Progressive1. Income goes up…taxes go up2. Federal Income Tax

3. Regressive 1. Income goes up % of total goes down2. Sales Tax, FICA

V. Categories of Taxes

1. Individual Income Tax2. FICA3. Corporate Income Tax4. Other Federal Taxes

a) Exciseb) Estatec) Giftd) Customs dutye) User fees

Individual Income Tax 1913 – 16th Amendment

Allows Congress to impose an income tax Tax on individual, personal earnings 45% of Federal Revenue

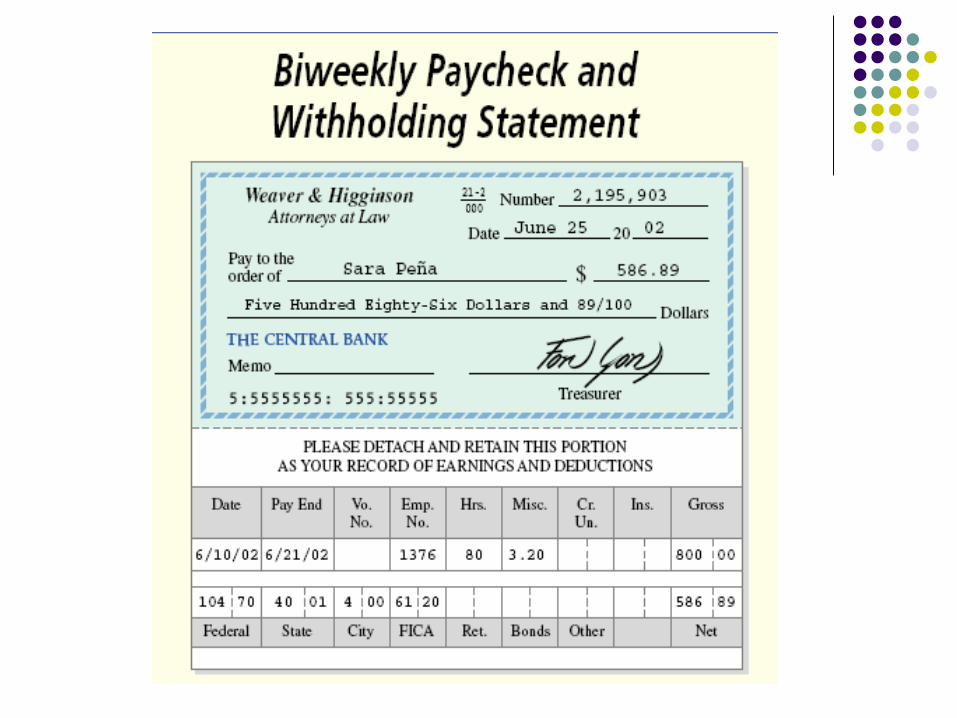

Individual Income Tax

Via payroll deductions Automatically deducted Paid directly to the

government by employers Tax Returns

Between Dec 31st – April 15th

Summarizes annual activity (+/-) (paid v. owed) THIS IS YOUR MONEY

FICA Federal Insurance Contributions Act Also known as “payroll tax” Pays for Social Security (6.2%)

6.2% of gross income ($84,900. cap)

Pays for Medicare Medicare – Federal health-care program available to senior

citizen, regardless of income 1.45% of gross income (no cap)

Employer/Employee share in this equally TOTAL tax is 15.3% (employer pays 6.2% we pay 6.2 %

plus Medicare of 1.45)

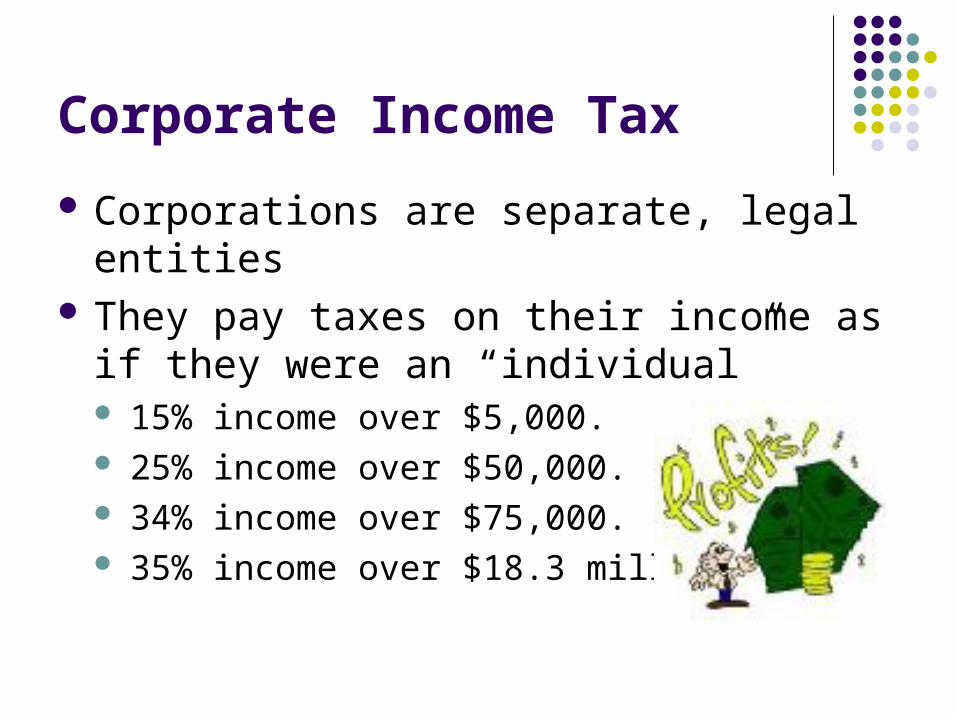

Corporate Income Tax

Corporations are separate, legal entities They pay taxes on their income as if they

were an “individual” 15% income over $5,000. 25% income over $50,000. 34% income over $75,000. 35% income over $18.3 million.

Other Federal Taxes

Excise – Taxes on the production, transportation, sale, or purchase of

certain goods gas, liquor, telephone, coal, luxury goods

Estate – Death Tax Transfer of property when a person dies (18%-50%)

Gift – Gifts of cash or items in excess of a certain amt. Customs duty – Imports

Tax on certain items brought into the country

User fees – Fee paid when fed government items are used (national parks, animal grazing on Fed. land, etc.)

Some Criticisms of our Current Tax System

Too complex – the Federal Tax Code is 18,500 pages!

Too many loopholes – do the wealthiest Americans pay their fair share?

Too bureaucratic – the IRS costs too much!

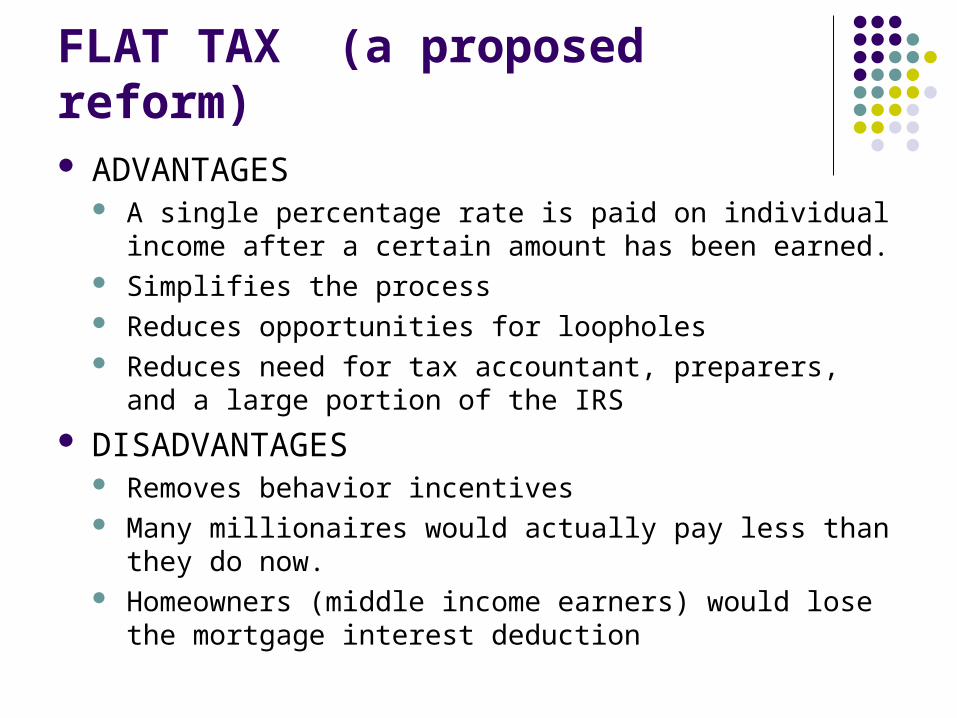

FLAT TAX (a proposed reform) ADVANTAGES

A single percentage rate is paid on individual income after a certain amount has been earned.

Simplifies the process Reduces opportunities for loopholes Reduces need for tax accountant, preparers, and a large

portion of the IRS

DISADVANTAGES Removes behavior incentives Many millionaires would actually pay less than they do

now. Homeowners (middle income earners) would lose the

mortgage interest deduction

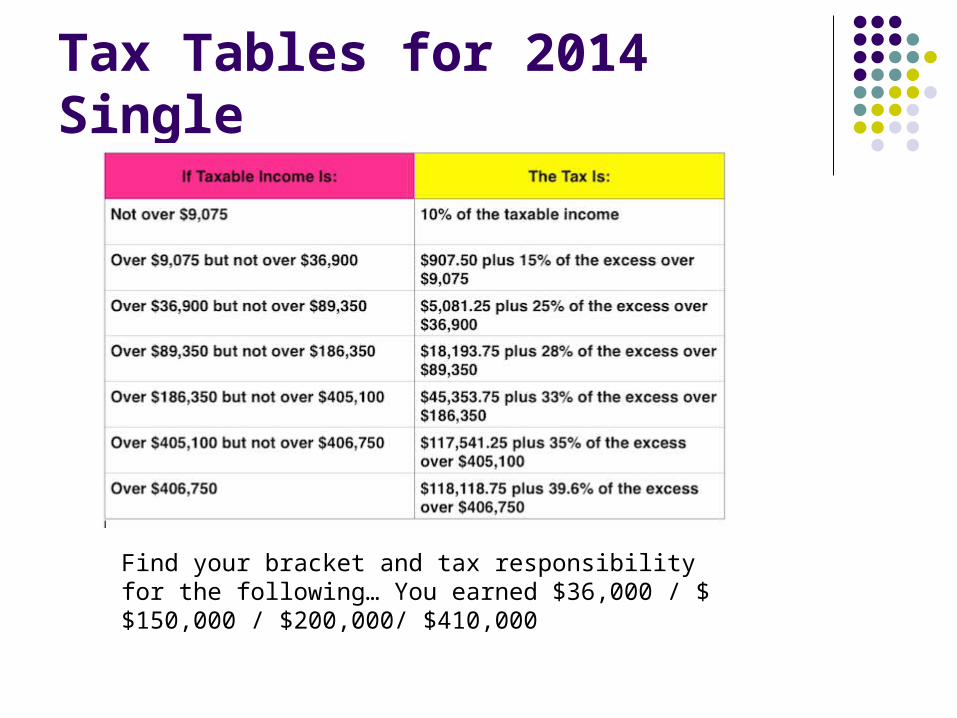

Tax Tables for 2014 Single

Find your bracket and tax responsibility for the following… You earned $36,000 / $$150,000 / $200,000/ $410,000

Think about this!

If you were an elected official who wanted to increase tax revenues for Michigan to cover the deficit, which of the following taxes would you prefer to use: individual income, sales, sin tax, property, corporate income, user fees, or flat? Use support for your answerThink Pair Share