Some Myths about the Chinese Economy - Hong Kong …€¦ · · 2012-11-16Some Myths about the...

55

Some Myths about the Chinese Economy Lawrence J. Lau, Ph. D. President and Ralph and Claire Landau Professor of Economics The Chinese University of Hong Kong and Kwoh-Ting Li Professor in Economic Development, Emeritus, Stanford University First Annual International Conference on the Chinese Economy Hong Kong Institute of Monetary Research Hong Kong, 11 January 2010 Phone: (852) 2609-8600; Fax: (852) 2603-5230 Email: [email protected] ; WebPages: HTTP://WWW.CUHK.EDU.HK/VC

Transcript of Some Myths about the Chinese Economy - Hong Kong …€¦ · · 2012-11-16Some Myths about the...

Some Myths about the

Chinese EconomyLawrence J. Lau, Ph. D.

President and Ralph and Claire Landau Professor of EconomicsThe Chinese University of Hong Kong

andKwoh-Ting Li Professor in Economic Development, Emeritus, Stanford University

First Annual International Conference on the Chinese EconomyHong Kong Institute of Monetary Research

Hong Kong, 11 January 2010

Phone: (852) 2609-8600; Fax: (852) 2603-5230Email: [email protected]; WebPages: HTTP://WWW.CUHK.EDU.HK/VC

Lawrence J. Lau, The Chinese University of Hong Kong 2

Preview

Introduction

The Seven Myths about the Chinese Economy

Concluding Remarks

Lawrence J. Lau, The Chinese University of Hong Kong 3

Introduction

There are many misunderstandings and myths about the Chinese economy. But repeated often enough, and by sufficiently respectable “authorities,” they tend to become accepted as truths.

However, accepting these misunderstandings and myths as truths has serious consequences: policy makers base their decisions on these assumed “truths.” And their policies will not have the expected effects if these assumed “truths” turn out to be false.

I hope to help dispel some of the common myths about the Chinese economy.

Lawrence J. Lau, The Chinese University of Hong Kong 4

The Seven Myths about the Chinese Economy

The Yuan is Under-Valued

Chinese Trade Surpluses Caused the Global Imbalances

Chinese Economic Growth Depends Critically on Exports

The Economies of China and East Asia Cannot be De- Coupled from the U.S. and Europe

Chinese Household Savings Rates Are Too High

China Faces Labour Shortages

The World Economy is Now Dominated by G-2 (Group of Two)—the United States and China

Lawrence J. Lau, The Chinese University of Hong Kong 5

Is the Yuan Under-Valued?

A country’s currency is considered under-valued if it runs persistent surpluses in trade in goods and services combined vis-à-vis the entire World. It is considered over-valued if it runs persistent trade deficits vis-a-vis the World.

A bilateral trade surplus, even a persistent one, says nothing about whether a country’s currency is under- valued because it may still have a near zero or even negative trade balance vis-à-vis the entire world. Most non-oil producing countries have persistent bilateral trade deficits with oil-exporting countries. And that does not necessarily mean the currencies of the oil-exporting countries are under-valued.

Lawrence J. Lau, The Chinese University of Hong Kong 6

Is the Yuan Under-Valued?

The statistics on Chinese trade balances over the past three decades indicate that China has had essentially balanced trade in goods and services combined with the World until 2005 and that its trade surplus is once again approaching zero in 2010.

In contrast, the large U.S. trade deficit with the world existed since at least 1998, long before 2005. What this means is that while there is evidence that the U.S. Dollar might have been over-valued, there is no evidence that the Renminbi was under-valued prior to 2005.

Lawrence J. Lau, The Chinese University of Hong Kong 7Lawrence J. Lau, The Chinese University of Hong Kong 7

Chinese Monthly Exports, Imports and Trade Balance, Goods Only, US$

Monthly Chinese Exports, Imports and Trade Balance of Goods, in U.S. Dollars

-10

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

Jan-

92A

pr-9

2Ju

l-92

Oct

-92

Jan-

93A

pr-9

3Ju

l-93

Oct

-93

Jan-

94A

pr-9

4Ju

l-94

Oct

-94

Jan-

95A

pr-9

5Ju

l-95

Oct

-95

Jan-

96A

pr-9

6Ju

l-96

Oct

-96

Jan-

97A

pr-9

7Ju

l-97

Oct

-97

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10

USD

bill

ions Exports, fob

Imports, cif

Trade Balance

Lawrence J. Lau, The Chinese University of Hong Kong 8

Monthly Chinese Surplus and U.S. Deficit with the World, Trade in Goods, Bill. US$

Monthly Chinese Surplus and U.S. Deficit with the World, Trade in Goods, Billion US$

-20

0

20

40

60

80

100

M1

1979

M7

1979

M1

1980

M7

1980

M1

1981

M7

1981

M1

1982

M7

1982

M1

1983

M7

1983

M1

1984

M7

1984

M1

1985

M7

1985

M1

1986

M7

1986

M1

1987

M7

1987

M1

1988

M7

1988

M1

1989

M7

1989

M1

1990

M7

1990

M1

1991

M7

1991

M1

1992

M7

1992

M1

1993

M7

1993

M1

1994

M7

1994

M1

1995

M7

1995

M1

1996

M7

1996

M1

1997

M7

1997

M1

1998

M7

1998

M1

1999

M7

1999

M1

2000

M7

2000

M1

2001

M7

2001

M1

2002

M7

2002

M1

2003

M7

2003

M1

2004

M7

2004

M1

2005

M7

2005

M1

2006

M7

2006

M1

2007

M7

2007

M1

2008

M7

2008

M1

2009

M7

2009

M1

2010

US$

Bill

ions

Chinese Trade Surplus in Goods

U.S. Trade Deficit in Goods

Lawrence J. Lau, The Chinese University of Hong Kong 9

Annual Chinese Surplus and U.S. Deficit with the World, Goods & Services, US$

Figure 2: Chinese Surplus and U.S. Deficit with the World, Trade in Goods and Services

-100

0

100

200

300

400

500

600

700

800

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

USD

bill

ions

Chinese Trade Surplus

U.S. Trade Deficit

Lawrence J. Lau, The Chinese University of Hong Kong 10

Is the Yuan Under-Valued?

In July 2005, the Renminbi was allowed to appreciate and rose 20 percent in nominal terms and 25 percent in real terms by the end of 2008.

The Chinese trade surplus vis-à-vis the world, which began rising in 2005, reached a peak in 2007 and began to decline in 2008. For 2009, it has declined more than 30%. It has continued to fall and has turned negative in 2010M3.

The long-term goal of the Chinese Government is to reduce the Chinese trade surplus vis-à-vis the World to zero. If the current trend continues, the goal of zero annual trade balance can probably be achieved by 2011, without necessarily any large adjustment in the nominal Yuan/U.S. Dollar exchange rate.

Lawrence J. Lau, The Chinese University of Hong Kong 11Lawrence J. Lau, The Chinese University of Hong Kong 11

The Nominal and Real Yuan/US$ Exchange Rates

The Nominal and Real Exchange Rates (1994 prices), Yuan/US$

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

Jan-

94A

pr-9

4Ju

l-94

Oct

-94

Jan-

95A

pr-9

5Ju

l-95

Oct

-95

Jan-

96A

pr-9

6Ju

l-96

Oct

-96

Jan-

97A

pr-9

7Ju

l-97

Oct

-97

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10

Yua

n pe

r U

.S. D

olla

r The Nominal Exchange Rate, Yuan/US$

The Real Exchange Rate, Yuan/US$

Lawrence J. Lau, The Chinese University of Hong Kong 12

Did the Chinese Trade Surpluses Cause the Global Imbalances ?

Global imbalances are blamed as a major cause of the current global financial crisis. However, the large U.S. trade deficit with the World existed since 1998, long before China began to have a significant trade surplus vis-à-vis the world. In 2000, U.S. trade deficit was US$380 billion whereas the Chinese trade surplus was only less than US$30 billion. Thus, the Chinese trade surpluses could not possibly have been the source of the global imbalances that supposedly fed the global liquidity that ultimately “enabled” the current global financial crisis.

Lawrence J. Lau, The Chinese University of Hong Kong 13

Did the Chinese Trade Surpluses Caused the Global Imbalances ?

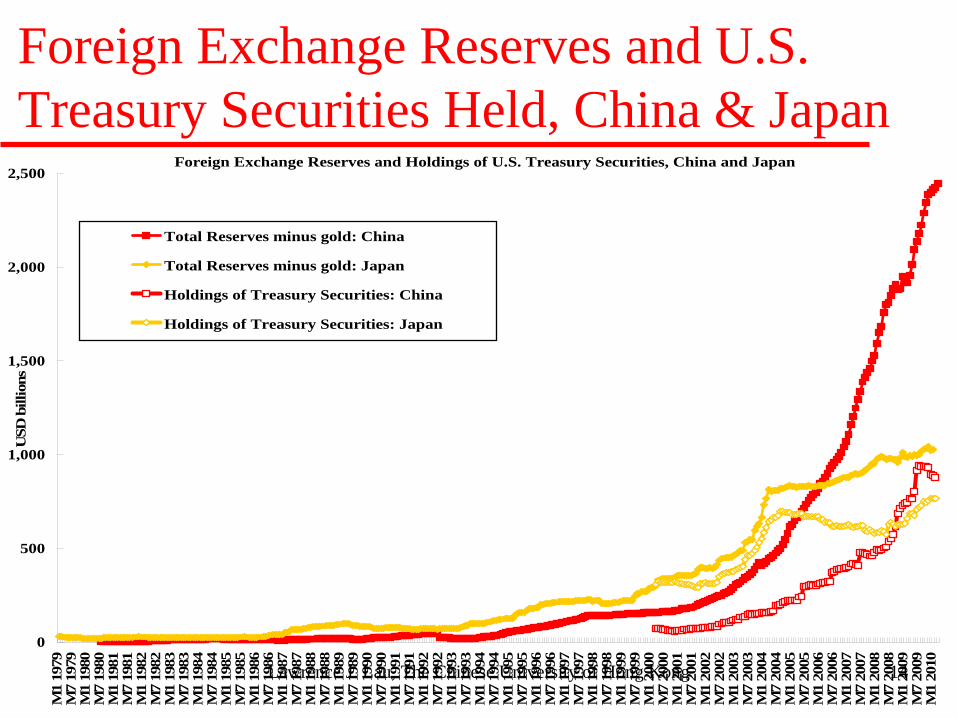

Japan and the oil exporting countries accounted for most of the trade surpluses vis-à-vis the world, and hence the global imbalances, since 2000. Japan had the largest foreign exchange reserves in the World until it was overtaken by China in 2006, and the Bank of Japan consistently held the largest amount of U.S. Treasury securities until the last quarter of 2008, when holdings of the People’s Bank of China exceeded the Bank of Japan’s for the first time.

In fact, the Case-Shiller U.S. Home Price Index, which can be taken as a proxy for the speculative asset price inflation caused by the growth of the sub-prime mortgage loans in the U.S., correlates almost perfectly with the U.S. trade deficit with the World but not with the Chinese trade surplus, demonstrating yet once again that the Chinese trade surpluses could not have been responsible for the global imbalances.

Lawrence J. Lau, The Chinese University of Hong Kong 14

Foreign Exchange Reserves and U.S. Treasury Securities Held, China & Japan

Foreign Exchange Reserves and Holdings of U.S. Treasury Securities, China and Japan

0

500

1,000

1,500

2,000

2,500

M1

1979

M7

1979

M1

1980

M7

1980

M1

1981

M7

1981

M1

1982

M7

1982

M1

1983

M7

1983

M1

1984

M7

1984

M1

1985

M7

1985

M1

1986

M7

1986

M1

1987

M7

1987

M1

1988

M7

1988

M1

1989

M7

1989

M1

1990

M7

1990

M1

1991

M7

1991

M1

1992

M7

1992

M1

1993

M7

1993

M1

1994

M7

1994

M1

1995

M7

1995

M1

1996

M7

1996

M1

1997

M7

1997

M1

1998

M7

1998

M1

1999

M7

1999

M1

2000

M7

2000

M1

2001

M7

2001

M1

2002

M7

2002

M1

2003

M7

2003

M1

2004

M7

2004

M1

2005

M7

2005

M1

2006

M7

2006

M1

2007

M7

2007

M1

2008

M7

2008

M1

2009

M7

2009

M1

2010

USD

bill

ions

Total Reserves minus gold: China

Total Reserves minus gold: Japan

Holdings of Treasury Securities: China

Holdings of Treasury Securities: Japan

Lawrence J. Lau, The Chinese University of Hong Kong 15

Case-Shiller U.S. Home Price Index, Chinese Trade Surplus & U.S. Trade Deficit, Bill. US$

Case-Shiller Home Price Index (2000Q1=100) , U.S. Trade Deficit and Chinese Trade Surplus

60

80

100

120

140

160

180

200

220

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10

2000

Q1=

100

-10

0

10

20

30

40

50

60

70

80

90

100

USD

bill

ions

Case-Shiller Home Price Index

U.S. Trade Deficit with the World

Chinese Trade Surplus with the World

Lawrence J. Lau, The Chinese University of Hong Kong 16

Chinese Surplus and U.S. Deficit with the World, Trade in Goods and Services

Chinese Surplus and U.S. Deficit with the World, Trade in Goods and Services

-100

0

100

200

300

400

500

600

700

800

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

USD

bill

ions

Chinese Trade Surplus

U.S. Trade Deficit

Lawrence J. Lau, The Chinese University of Hong Kong 17Lawrence J. Lau, The Chinese University of Hong Kong 17

The Nominal and Real World Prices of Oil (2009 prices)

Nominal and Real Price of Oil

0

10

20

30

40

50

60

70

80

90

100

110

120

130

Jan-

74Ju

l-74

Jan-

75Ju

l-75

Jan-

76Ju

l-76

Jan-

77Ju

l-77

Jan-

78Ju

l-78

Jan-

79Ju

l-79

Jan-

80Ju

l-80

Jan-

81Ju

l-81

Jan-

82Ju

l-82

Jan-

83Ju

l-83

Jan-

84Ju

l-84

Jan-

85Ju

l-85

Jan-

86Ju

l-86

Jan-

87Ju

l-87

Jan-

88Ju

l-88

Jan-

89Ju

l-89

Jan-

90Ju

l-90

Jan-

91Ju

l-91

Jan-

92Ju

l-92

Jan-

93Ju

l-93

Jan-

94Ju

l-94

Jan-

95Ju

l-95

Jan-

96Ju

l-96

Jan-

97Ju

l-97

Jan-

98Ju

l-98

Jan-

99Ju

l-99

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10

U.S

. Dol

lars

per

Bar

rel

Nominal Price of Oil

Real Price of Oil, in 2009M1 price

Lawrence J. Lau, The Chinese University of Hong Kong 18

Is Chinese Economic Growth Critically Dependent on Exports?

It should be clear from the fact that the Chinese economy has been growing at an average real rate of growth of approximately 10 percent per annum since 1979, and that a significant Chinese trade surplus vis-a-vis the World only began to occur in 2005, that Chinese economic growth could not possibly have been critically dependent on running export surpluses.

Chinese exports as a ratio of GDP has been heading downwards from its peak of almost 40 percent in 2006 to approximately 25 percent in 2009. While this ratio appears large, it actually exaggerates the importance of exports in the Chinese economy.

Lawrence J. Lau, The Chinese University of Hong Kong 19Lawrence J. Lau, The Chinese University of Hong Kong 19

Real Chinese GDP in US$ Since 1952 (2009 Prices)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Billi

ons U

S$

Chinese Real GDP, in 2009 prices

Lawrence J. Lau, The Chinese University of Hong Kong 20

Chinese Exports of Goods and Services as a Ratio of GDP, 1970-present

Chinese Exports of Goods and Services as a Ratio of GDP since 1970

0

5

10

15

20

25

30

35

40

45

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

Lawrence J. Lau, The Chinese University of Hong Kong 21

Is Chinese Economic Growth Critically Dependent on Exports?

The domestic value-added content of Chinese exports is no more than 30 percent, that is: for every dollar of goods exported, less than 30 cents, on average, consist of domestic value-added. If we multiply the Exports/GDP ratio of say 40 percent (it is actually much lower) to the domestic value-added content of 30 percent, we obtain 12 percent, which is the maximum percentage of Chinese GDP attributable to exports.

Now, 12 percent of GDP is a large number, and no economy can afford to lose 12 percent of its GDP overnight. However, if 12 percent of GDP does not grow, or even declines by 25 percent, as long as the other 88 percent of the economy continues to grow, the economy as a whole should do all right, especially if appropriate compensatory economic stimulus measures are taken.

Lawrence J. Lau, The Chinese University of Hong Kong 22

Is Chinese Economic Growth Critically Dependent on Exports?

A 25 percent decline in Chinese exports should result in a 25 percent times 12 percent or 3 percent maximum decline in Chinese GDP, other things being equal. Thus, the reduction in exports caused by the global financial crisis should be expected to reduce the Chinese real rate of growth from 9 percent in 2008 to 6 percent in 2009. However, the 4-trillion economic stimulus programme launched by the Chinese Government in November 2008 should help make up the short-fall in aggregate demand.

Lawrence J. Lau, The Chinese University of Hong Kong 23

Is Chinese Economic Growth Critically Dependent on Exports?

Moreover, even if Chinese exports manage to grow by 25 percent per year going forward (which is most unlikely), it will lead to only 3 percent overall economic growth, which is by itself hardly enough. That is why China cannot, and will not, rely on exports as a primary source of its future economic growth.

If there were any lingering doubts on the degree of export-dependence of the Chinese economy, they should have been dispelled by the fact that the Chinese economy managed to achieve a real rate of growth of 8.7 percent in 2009, with exports down by 25 percent from 2008 and the U.S. and European economies still mired in recession.

Lawrence J. Lau, The Chinese University of Hong Kong 24

External Dependence of Mainland China

An important implication of the relatively low external dependence of Chinese GDP is that the rate of growth of Chinese real GDP is relatively stable even as Chinese exports and imports fluctuate as widely as the exports and imports of other East Asian economies. (see the following charts on the rates of growth of the exports, imports and real GDP of East Asian economies).

Lawrence J. Lau, The Chinese University of Hong Kong 25Lawrence J. Lau, The Chinese University of Hong Kong 25

Quarterly Rates of Growth of Exports of Goods: Selected East Asian Economies

Year-over-Year Quarterly Rates of Growth of Exports of Goods in US$ (Percent)

-50

-40

-30

-20

-10

0

10

20

30

40

50

Q1

1997

Q2

1997

Q3

1997

Q4

1997

Q1

1998

Q2

1998

Q3

1998

Q4

1998

Q1

1999

Q2

1999

Q3

1999

Q4

1999

Q1

2000

Q2

2000

Q3

2000

Q4

2000

Q1

2001

Q2

2001

Q3

2001

Q4

2001

Q1

2002

Q2

2002

Q3

2002

Q4

2002

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Ann

ualiz

ed P

erce

nt p

er a

nnum

China,P.R.:Hong Kong IndiaIndonesia KoreaMalaysia PhilippinesSingapore ThailandChina,P.R.: Mainland JapanTaiwan Prov.of China

Lawrence J. Lau, The Chinese University of Hong Kong 26Lawrence J. Lau, The Chinese University of Hong Kong 26

Quarterly Rates of Growth of Imports of Goods: Selected East Asian Economies

Year-over-Year Quarterly Rates of Growth of Imports of Goods in US$ (Percent)

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Q1

1997

Q2

1997

Q3

1997

Q4

1997

Q1

1998

Q2

1998

Q3

1998

Q4

1998

Q1

1999

Q2

1999

Q3

1999

Q4

1999

Q1

2000

Q2

2000

Q3

2000

Q4

2000

Q1

2001

Q2

2001

Q3

2001

Q4

2001

Q1

2002

Q2

2002

Q3

2002

Q4

2002

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Ann

ualiz

ed P

erce

nt p

er a

nnum

China,P.R.:Hong Kong IndiaIndonesia KoreaMalaysia PhilippinesSingapore ThailandChina,P.R.: Mainland JapanTaiwan Prov.of China

Lawrence J. Lau, The Chinese University of Hong Kong 27Lawrence J. Lau, The Chinese University of Hong Kong 27

Quarterly Rates of Growth of Real GDP, Y-o-Y: Selected East Asian Economies

Quarterly Rates of Growth of Real GDP, Year-over-Year, Selected East Asian Economies

-20

-15

-10

-5

0

5

10

15

20

Q1

1994

Q2

1994

Q3

1994

Q4

1994

Q1

1995

Q2

1995

Q3

1995

Q4

1995

Q1

1996

Q2

1996

Q3

1996

Q4

1996

Q1

1997

Q2

1997

Q3

1997

Q4

1997

Q1

1998

Q2

1998

Q3

1998

Q4

1998

Q1

1999

Q2

1999

Q3

1999

Q4

1999

Q1

2000

Q2

2000

Q3

2000

Q4

2000

Q1

2001

Q2

2001

Q3

2001

Q4

2001

Q1

2002

Q2

2002

Q3

2002

Q4

2002

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Ann

ualiz

ed R

ates

in P

erce

nt

China,P.R.:Hong Kong IndiaIndonesia KoreaMalaysia PhilippinesSingapore ThailandChina,P.R.: Mainland JapanTaiwan Prov.of China

Lawrence J. Lau, The Chinese University of Hong Kong 28

Can the Economies of East Asia/China be De-Coupled from the U.S. and Europe?

East Asia is taken to mean the 10 ASEAN countries (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam) + 3 (China (including Hong Kong, Macao and Taiwan), Japan, and South Korea), that is, approximately, everything east of Bangladesh and west of the Pacific Ocean.

The “Partial De-Coupling Hypothesis” says that while East Asia is not immune from the effects of the economic recession in North America and Europe, it can nevertheless continue growing, albeit at somewhat lower rates, even with economic contraction in North America and Europe.

Partial de-coupling is a consequence of the economic centre of gravity of the World gradually shifting to East Asia from the United States and Western Europe and within East Asia from Japan to China (but the shifts are not yet completed).

Lawrence J. Lau, The Chinese University of Hong Kong 29

The Shifting Economic Centre of Gravity

In the following charts, East Asian and Chinese GDP as percentages of World GDP are respectively presented. Both show very strong trends of growth over the past half a century.

In 1960, East Asian GDP, comprising of the GDPs of ASEAN (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam) + 3 (China (Mainland only), Japan, and South Korea) was just over 10 percent of World GDP.

Today, East Asian economies account for approximately a quarter of World GDP, comparable to the size of the U.S. economy and that of the Euro Zone.

Lawrence J. Lau, The Chinese University of Hong Kong 30Lawrence J. Lau, The Chinese University of Hong Kong 30

East Asian Share of World GDP, 1960-present

East Asian Share of World GDP, 1960-present

10

12

14

16

18

20

22

24

26

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Perc

ent

Lawrence J. Lau, The Chinese University of Hong Kong 31

The Shifting Economic Centre of Gravity

These figures and percentages are sensitive to the exchange rates used for the conversion, but the general conclusions below are reasonably robust to the exchange rates used.

(1) The contribution of East Asia to total World GDP has increased significantly to approximately a quarter, approximately the same as the contributions of the United States and the Euro Zone;

(2) The contribution of East Asia other than Japan, especially that of China, to East Asian GDP has also increased significantly; and

(3) Japan remains for the time being the leading economy within East Asia in both aggregate and per capita terms, but China (Mainland only) will likely surpass Japan in terms of aggregate GDP around 2015.

Lawrence J. Lau, The Chinese University of Hong Kong 32

Can the Economies of East Asia/China be De-Coupled from the U.S. and Europe?

Given the current trends in rates of economic growth, East Asia will surpass the United States in terms of aggregate GDP with China perhaps contributing the highest proportion of the total by 2015.

This is what gives credence to the idea of partial “de- coupling” of the World economies—that the Chinese and East Asian economies can continue to do reasonably well despite the current economic problems in the U.S. and elsewhere.

However, China, with its GDP accounting for only 7% of the World total, and East Asia are not large enough to turn around the whole World. The talk about G-2 is pre- mature.

Lawrence J. Lau, The Chinese University of Hong Kong 33Lawrence J. Lau, The Chinese University of Hong Kong 33

China’s Share of World GDP, 1960-present

China's GDP as a Percentage of World GDP, 1960-present

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

Lawrence J. Lau, The Chinese University of Hong Kong 34

The Shifting Economic Centre of Gravity

East Asian shares of World exports, imports, and international trade have also grown from approximately 10 percent in 1960 to a quarter in 2008, paralleling the growth of East Asian share of World GDP (see the following chart).

Similarly, Chinese shares of World exports, imports and international trade have also grown.

Chinese exports and imports have risen from approximately 1 percent of World exports and imports in 1960 to approximately 10 percent of World exports and imports in 2008.

China has overtaken Japan to become the largest exporting country in East Asia. China has also overtaken Japan to become the largest importing country in East Asia and the most important export market for almost all East Asian economies and runs trade deficits vis-à-vis almost every one.

Lawrence J. Lau, The Chinese University of Hong Kong 35Lawrence J. Lau, The Chinese University of Hong Kong 35

The Rising Ratio of East Asian Trade in Total World Trade, 1960-present

East Asian Share of Total World Trade, 1960-present

0

5

10

15

20

25

30

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

Share of World Exports

Share of World Imports

Share of Total World Trade

Lawrence J. Lau, The Chinese University of Hong Kong 36

Rising Intra-East Asian Interdependence

The emergence of the Chinese economy on the global market was the one most important new development during the past three decades. Japan has been China’s largest trading partner for the past decade and a half and China became Japan’s largest source of imports in 2002. The recent pick-up in economic activities in Japan is due in no small parts to the Chinese demand for Japanese exports.

Practically every other East Asian economy has a trade surplus vis-à-vis China.

Lawrence J. Lau, The Chinese University of Hong Kong 37Lawrence J. Lau, The Chinese University of Hong Kong 37

The Ratio of Chinese Trade in Total World Trade, 1950-present

The Ratio of Chinese Trade to World Trade

0

1

2

3

4

5

6

7

8

9

10

1950

1951

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

The ratio of Chinese Exports to World Exports

The ratio of Chinese Imports to World Imports

The ratio of Chinese Total Trade to World Total Trade

Lawrence J. Lau, The Chinese University of Hong Kong 38Lawrence J. Lau, The Chinese University of Hong Kong 38

The Ratio of Chinese Trade in Total East Asian Trade, 1952-present

The Ratio of Chinese Trade to East Asian Trade

0

5

10

15

20

25

30

35

40

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

The Ratio of Chinese Exports to East Asian Exports

The Ratio of Chinese Imports to East Asian Imports

The Ratio of Chinese Total Trade to East Asian Total Trade

Lawrence J. Lau, The Chinese University of Hong Kong 39

The Shifting Economic Centre of Gravity

Because of the rapid economic growth of China and the rest of East Asia outside of Japan, and the demand and supply that such economic growth has generated, the East Asian economies now trade more with one another than with economies outside of East Asia, including the United States. By the late 1990s, approximately half of East Asian trade is among East Asian economies (see the following charts).

And while much of the trade consists of raw materials, components, and semi-finished goods which are further processed for exports to developed economies ultimately, much of it has also found itself into the final demands of the domestic markets.

This is a sea change compared to say thirty years ago when most of the East Asian trade was between East Asia and the United States and Western Europe and not within East Asia itself.

Lawrence J. Lau, The Chinese University of Hong Kong 40Lawrence J. Lau, The Chinese University of Hong Kong 40

The Share of East Asian Exports Destined for East Asia

The Share of East Asian Exports Destined for East Asia

35

37

39

41

43

45

47

49

51

53

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10

%

Lawrence J. Lau, The Chinese University of Hong Kong 41Lawrence J. Lau, The Chinese University of Hong Kong 41

The Share of East Asian Imports Originated from East Asia

The Share of East Asian Imports Originated from East Asia

45

47

49

51

53

55

57

59

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

%

Lawrence J. Lau, The Chinese University of Hong Kong 42

The Changing Pattern of World Trade

Interdependence of the East Asian economies has been rising sharply over the years and East Asian dependence on the United States and Western Europe has declined. Interdependence of the East Asian economies will rise even further within the next five to ten years as East Asia becomes the only region with a high rate of economic growth.

The ASEAN Free Trade Area as well as its variations (+1 (China); + 3 (China, Japan and South Korea)) are rapidly becoming a reality. (There is also the more recently concluded Indo-ASEAN Free Trade Agreement.)

Lawrence J. Lau, The Chinese University of Hong Kong 43

The Savings Rates of East Asian Economies

The savings rates of East Asian economies (with the possible exception of the Philippines) have always been high and are sufficient to supply the necessary investment to enable the continued growth of these economies even as the inflows of both foreign direct and portfolio investment and of foreign loans from outside of East Asia decline.

This is in part what gives credence to the idea of “partial de-coupling” of the World economies—that the Chinese and East Asian economies can continue to do reasonably well despite the current economic problems in the U.S. and elsewhere.

Lawrence J. Lau, The Chinese University of Hong Kong 44Lawrence J. Lau, The Chinese University of Hong Kong 44

Savings Rates of Selected Asian Economies (1952-2008)

Savings Rates of Selected Asian Economies

0

10

20

30

40

50

60

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Year

Perc

ent

China, Mainland Hong KongIndia IndonesiaJapan KoreaMalaysia PhilippinesSingapore TaiwanThailand

Lawrence J. Lau, The Chinese University of Hong Kong 45Lawrence J. Lau, The Chinese University of Hong Kong 45

Savings Rates of Selected Asian Economies (1980-2008)

Savings Rates of Selected Asian Economies

10

15

20

25

30

35

40

45

50

55

60

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Year

Perc

ent

China, Mainland Hong KongIndia IndonesiaJapan KoreaMalaysia PhilippinesSingapore TaiwanThailand

Lawrence J. Lau, The Chinese University of Hong Kong 46

Chinese Household Savings RatesChinese Household Savings Rates

20

22

24

26

28

30

32

34

36

38

40

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Perc

ent

Lawrence J. Lau, The Chinese University of Hong Kong 47

Savings Rates of Urban and Rural Households

Savings Rates of Urban and Rural Households

0

5

10

15

20

25

30

35

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Perc

ent

Household Savings Rates: Rural

Household Savings Rates: Urban

Lawrence J. Lau, The Chinese University of Hong Kong 48

Are Chinese Households Saving Too Much?

The high Chinese national savings rate, which sometimes approaches 50%, is also blamed as a cause of the Chinese trade surplus and hence the global imbalances and ultimately the global financial crisis.

It is true that China has excessive domestic savings, but China also has excessive domestic investment. China both saves too much and invests too much. The excessive savings and excessive investment were in approximate balance and thus there was no excess savings, until 2005, when China began to have a trade surplus vis-à-vis the world, but not before that time.

More recently, the Chinese trade surplus has declined significantly, reflecting the decline in export demand and the increase in domestic demand as a result of its economic stimulus programme.

Lawrence J. Lau, The Chinese University of Hong Kong 49

Are Chinese Households Saving Too Much?

The savings behaviour of Chinese households on the Mainland are no different from those in Hong Kong and Taiwan at the same level of per capita household income, with an average savings rate of approximately 30%.

The high Chinese national savings rate of almost 50% is due to (1) the much higher corporate savings rates and (2) the much lower share of GDP received by households as income; in particular, the share of labour is low in China, less than 50 percent compared to approximately 70 percent in developed economies of the West.

Lawrence J. Lau, The Chinese University of Hong Kong 50

Does the Chinese Economy Face Labour Shortages?

As long as the percentage of labour force in the primary sector (agriculture and mining) exceeds the percentage of GDP originating from the primary sector, there is little or no upward pressure on the real wage rate of unskilled, entry-level labour in the secondary and tertiary sectors.

It is exactly what Nobel Laureate in Economic Sciences Prof. Arthur Lewis said in his famous paper on surplus labour more than fifty years ago.

Lawrence J. Lau, The Chinese University of Hong Kong 51Lawrence J. Lau, The Chinese University of Hong Kong 51

The Distribution of Chinese GDP by Sector Since 1952

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1952

19

53

1954

19

55

1956

19

57

1958

19

59

1960

19

61

1962

19

63

1964

19

65

1966

19

67

1968

19

69

1970

19

71

1972

19

73

1974

19

75

1976

19

77

1978

19

79

1980

19

81

1982

19

83

1984

19

85

1986

19

87

1988

19

89

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

The Distribution of GDP by Sector

Primary Sector Secondary Sector Tertiary Sector

Lawrence J. Lau, The Chinese University of Hong Kong 52Lawrence J. Lau, The Chinese University of Hong Kong 52

The Distribution of Chinese Employment by Sector Since 1952

The Distribution of Employment by Sector

0%

20%

40%

60%

80%

100%

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Primary Sector Secondary Sector Tertiary Sector

Lawrence J. Lau, The Chinese University of Hong Kong 53

Is China Ready for G-2?

The United States accounts for approximately a quarter of World GDP.

China, with its GDP accounting for only 7 percent of the World total, and East Asia, with its total GDP (including China) accounting for less than 20 percent of the World total, and still very low GDP per capita, are not large enough to turn around the whole World. The talk about G-2 is pre-mature.

Lawrence J. Lau, The Chinese University of Hong Kong 54Lawrence J. Lau, The Chinese University of Hong Kong 54

China’s Share of World GDP, 1960-present

China's GDP as a Percentage of World GDP, 1960-present

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

Lawrence J. Lau, The Chinese University of Hong Kong 55

Concluding Remarks

If the World is going to emerge from the global financial crisis, there must be global cooperation and coordination of economic policies. And these policies must be based on facts, not myths.

Despite very substantial progress during the past thirty years, the Chinese economy still faces formidable challenges ahead but it cannot and will not solve these problems with a beggar thy neighbour policy.

Countries around the World should collectively refrain from finger- pointing and scape-goating. The global financial crisis was clearly brought about by easy money in the U.S. and serious regulatory failure in the developed economies. But let us not waste time in laying blame but devote our efforts in restoring economic health of the World.