Some general concepts and the French experience on social responsibility and sustainable development...

19

Some general concepts and the French experience on social responsibility and sustainable development Cristian Brodhag Interministerial delegates for sustainable development, FRANCE ISO/TMB/WG SR : ISO 26000 Plenary meeting May 15-19, 2006, Lisbon see on brodhag.org

-

Upload

dina-kellie-parks -

Category

Documents

-

view

214 -

download

0

Transcript of Some general concepts and the French experience on social responsibility and sustainable development...

Some general concepts and the French experience on social responsibility

and sustainable development

Cristian BrodhagInterministerial delegates for

sustainable development, FRANCE

ISO/TMB/WG SR : ISO 26000Plenary meeting May 15-19, 2006,

Lisbonsee on brodhag.org

intégration difficulties

Amazon

Rio Negro

Rio Solimoes

two communities which have not the same historics references

?social and

environnemental responsibility

economic

social

environment

CSR

Community of ethics and social

responsibility

economic social

environment

PCPCommunity of

sustainable development

changing unsustainable patterns of consumption and production

European view of CSR• A common European understanding of what CSR means has

emerged on the basis of the Commission definition of CSR as a concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis.

• In its contribution to the March 2005 Spring Council, the Commission recognised that “voluntary business initiatives, in the form of corporate social responsibility (CSR) practices, can play a key role in contributing to sustainable development while enhancing Europe’s innovative potential and competitiveness”.

• In the Social Agenda, the Commission announced that it would, in co-operation with Member States and stakeholders, present initiatives to further enhance the development and transparency of CSR.

• In « Implementing the partnership for growth and jobs : making Europe a pole of excellence on corporate social responsibility », Communication from the Commission to the European Parliament, the Council and the European economic and social committee

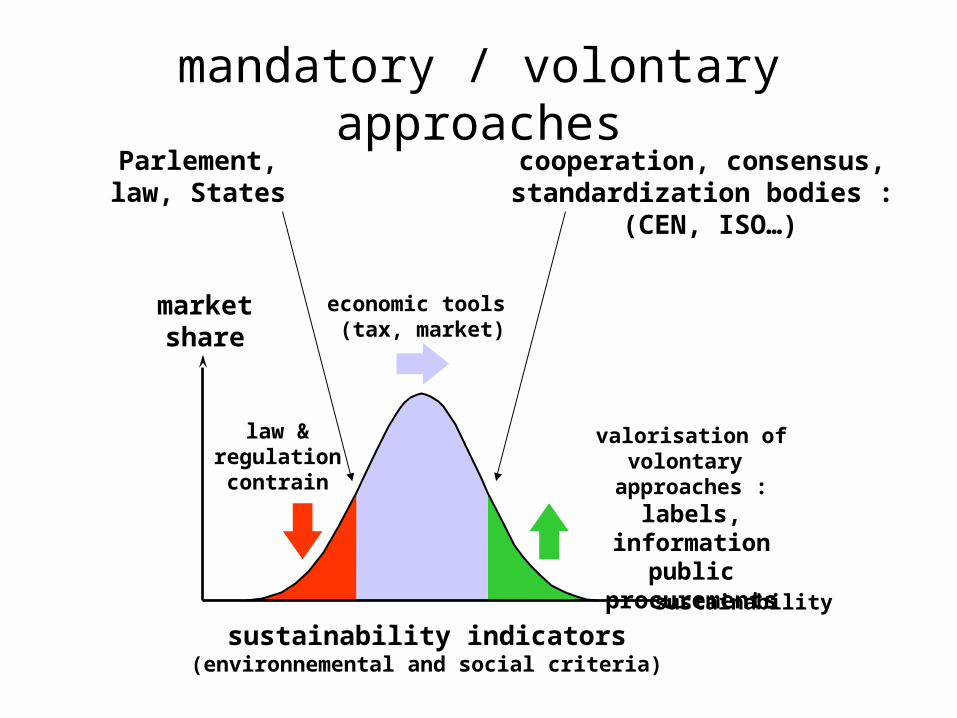

mandatory / volontary approachesParlement, law, States

cooperation, consensus, standardization bodies :

(CEN, ISO…)

valorisation of volontary approaches :

labels, informationpublic procurements

law & regulationcontrain

economic tools (tax, market)

market share

sustainability

sustainability indicators(environnemental and social criteria)

Two roles of CSR

outwards looking– accountibility – formal communication to stakeholders– problem of the perimeter of the reports (range of

responsibility) – verification certification of information.

inwards looking– mobilizing company and staff to answer new issues– consider expectations of stakeholders and future market– allows the identification of way of progress (ie. informations

on best practices or techniques, in France SD 21000 guidelines)

sustainable development regulation and corporations

international institutionsinternational norms

principes

multinationalcorporations

Global Compact(volontary)

stakeholders ISO 26000? indicators

in stock exchangefrench law NRE

(mandatory sustainable development reporting)

GRInotation agencies

sensitization

national and local entities

SME’s

National strategies of SDLocal Agenda 21

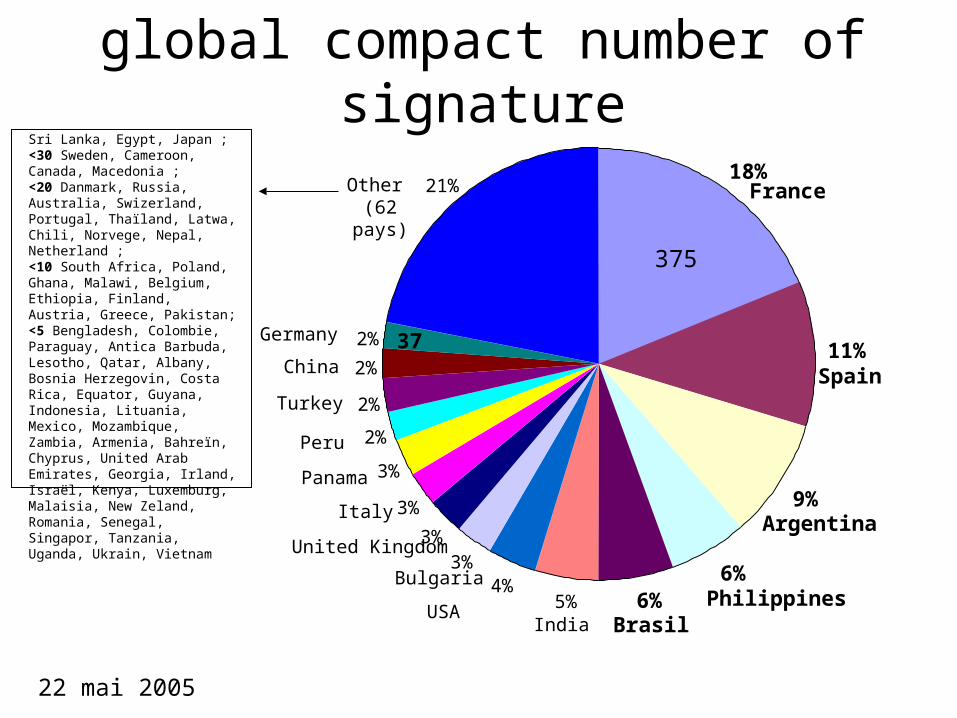

global compact number of signature

18%

11%

9%

6%6%5%

4%3%

3%

3%

3%

2%

2%

2%

2%

21% France

Spain

Argentina

PhilippinesBrasilIndia

USA

Bulgaria

United Kingdom

Italy

Panama

Peru

Turkey

China

Germany

Other (62 pays)

22 mai 2005

375

37

Sri Lanka, Egypt, Japan ; <30 Sweden, Cameroon, Canada, Macedonia ; <20 Danmark, Russia, Australia, Swizerland, Portugal, Thaïland, Latwa, Chili, Norvege, Nepal, Netherland ; <10 South Africa, Poland, Ghana, Malawi, Belgium, Ethiopia, Finland, Austria, Greece, Pakistan; <5 Bengladesh, Colombie, Paraguay, Antica Barbuda, Lesotho, Qatar, Albany, Bosnia Herzegovin, Costa Rica, Equator, Guyana, Indonesia, Lituania, Mexico, Mozambique, Zambia, Armenia, Bahreïn, Chyprus, United Arab Emirates, Georgia, Irland, Israël, Kenya, Luxemburg, Malaisia, New Zeland, Romania, Senegal, Singapor, Tanzania, Uganda, Ukrain, Vietnam

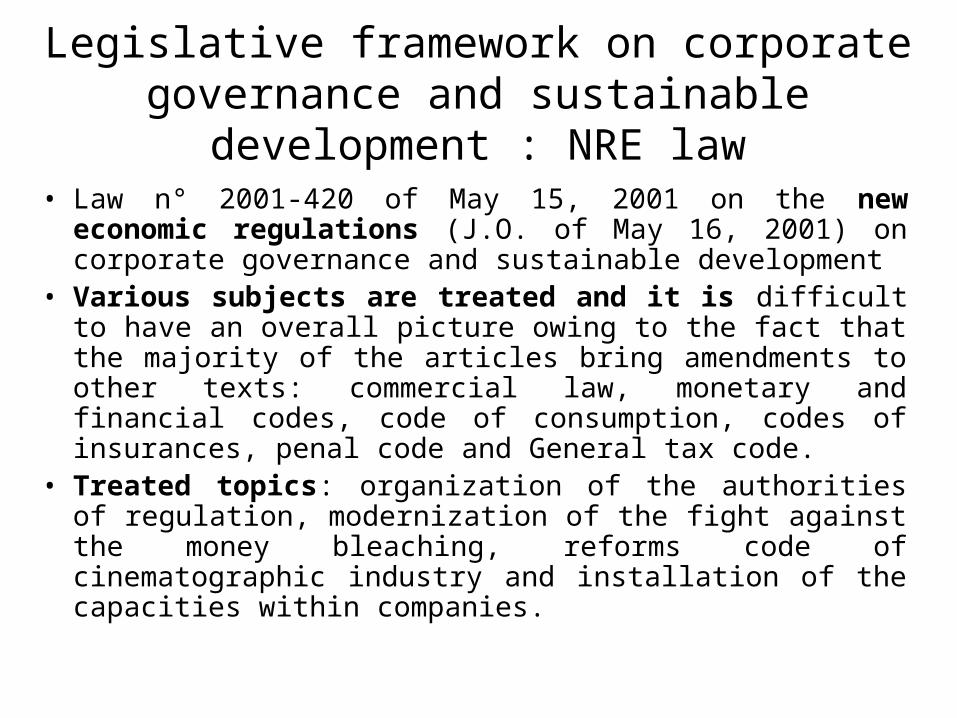

Legislative framework on corporate governance and sustainable development : NRE law

• Law n° 2001-420 of May 15, 2001 on the new economic regulations (J.O. of May 16, 2001) on corporate governance and sustainable development

• Various subjects are treated and it is difficult to have an overall picture owing to the fact that the majority of the articles bring amendments to other texts: commercial law, monetary and financial codes, code of consumption, codes of insurances, penal code and General tax code.

• Treated topics: organization of the authorities of regulation, modernization of the fight against the money bleaching, reforms code of cinematographic industry and installation of the capacities within companies.

Role of french guidelines SD 21000

• identify principal stakes, stakeholders and stakeholders’ expectation

• design a strategic vision on sustainable development

• define an action plan including external partnerships

• implemented in around two hundred SMEs (results on 80)

health security

work cond.

management system of

the entreprise

demonstration standards

etc…

Models of management

systèmes

environ- nment

ISO 14001

ISO 14004

quality ISO 9001

ISO 9004

OHSAS 18001

BS 8800

SA8000

AA1000

social/ societal

EMAS

excellence EFQM

Strategy / management systems

Guide for taking in account SD 21000 sustainable development

d’après Alain JOUNOT, Groupe de Travail « Entreprise et développement durable » AFNOR, document n°20, Cartographie des référentiels de management

strategy and politicy of the

entreprise

economy

environment

society

liveable viable

fair

sustainable

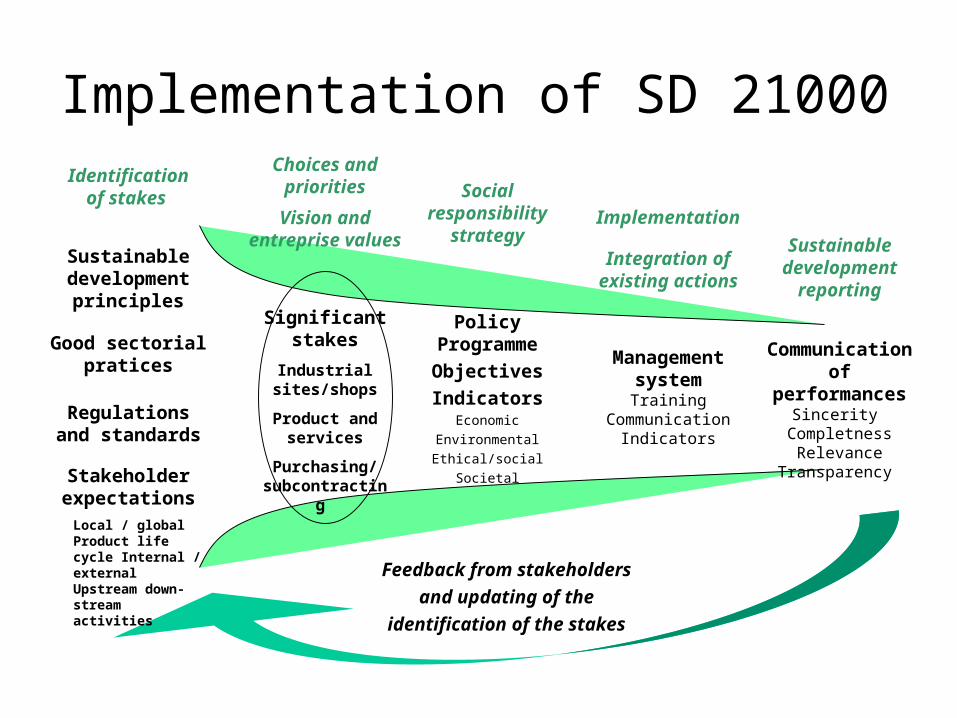

Feedback from stakeholders

and updating of the

identification of the stakes

Communication of performances

Sincerity Completness

RelevanceTransparency

Sustainable development

reporting

Regulations and standards

Good sectorial pratices

Stakeholder expectationsLocal / global Product life cycle Internal / external Upstream down- stream activities

Sustainable development

principles

Identification of stakes

Policy Programme

Objectives

IndicatorsEconomic

Environmental

Ethical/social

Societal

Social responsibility

strategy

Implementation of SD 21000

Implementation

Management systemTraining

CommunicationIndicators

Integration of existing actions

Choices and priorities

Significant stakes

Industrial sites/shops

Product and services

Purchasing/ subcontracting

Vision and entreprise values

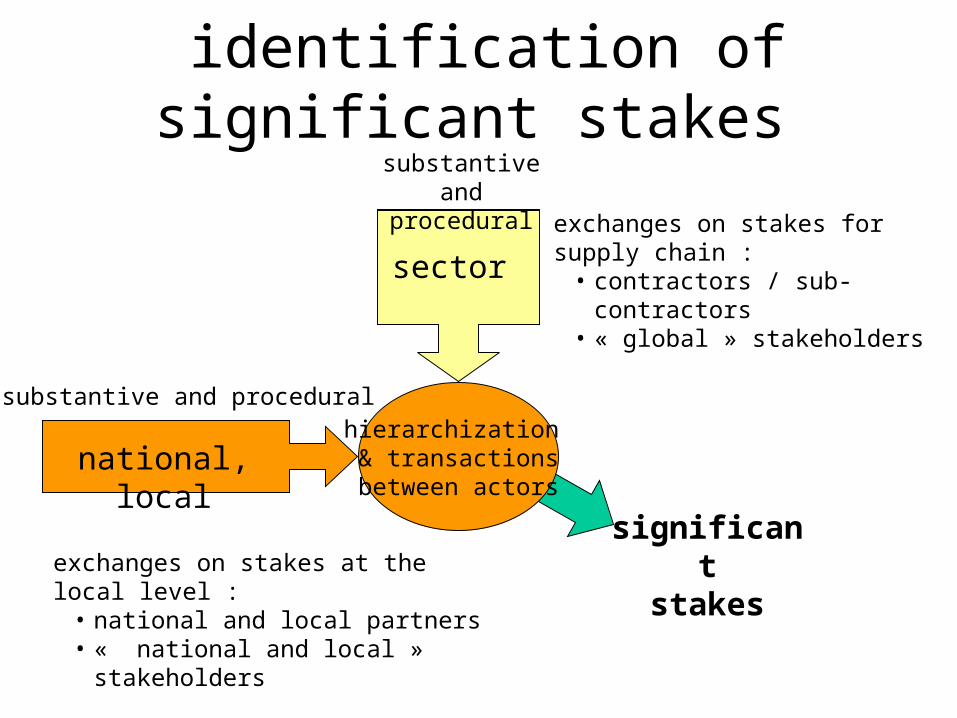

national, local

exchanges on stakes at the local level :• national and local partners• « national and local » stakeholders

identification of significant stakes

sector

hierarchization & transactionsbetween actors

exchanges on stakes for supply chain :

• contractors / sub-contractors• « global » stakeholders

significantstakes

substantive and procedural

substantive and procedural

state of the art path

1 2

3

first stage:correction of pathimplementation of state of

the art (in context)

Per

form

ance

Choice of significant stakes : combining importance and performance

second stage:towards a new production

and consumer model, innovative approach in rupture

5 innovation path

Need to identify « best practices »

4

http://www.brodhag.org

Importance of stakes1 – low importance2 – medium importance 3 – no mastership will impede some

processes of the enterprise 4 – no mastership will impede important

and strategic process of the enterprise

5 – no mastership will impede the existence of the enterprise

Performance

Impo

rtan

ce

5

4

3

2

1

54321

react

act

enhance

no prioritySD and long term stackes

Correction through stakeholders expectations

Stakes # indicators

• Avoid a “carpet bombing” of information, to many information kills information.

• To work on the significant stakes with tools allowing the adaptation of their hierarchisation and the levels of performance in the context with stakeholders involvement (SD 21000).

• Quantitative indicators and qualitative information on mechanism: according to the stakes and contexts' one has either or others. SD 21000 approach propose to use a single scale of performance (1 to 5 : 3 is state of the art, 4 innovative approaches and 5 excellence).

• It is a “universal” notation that can be openly discused in different context

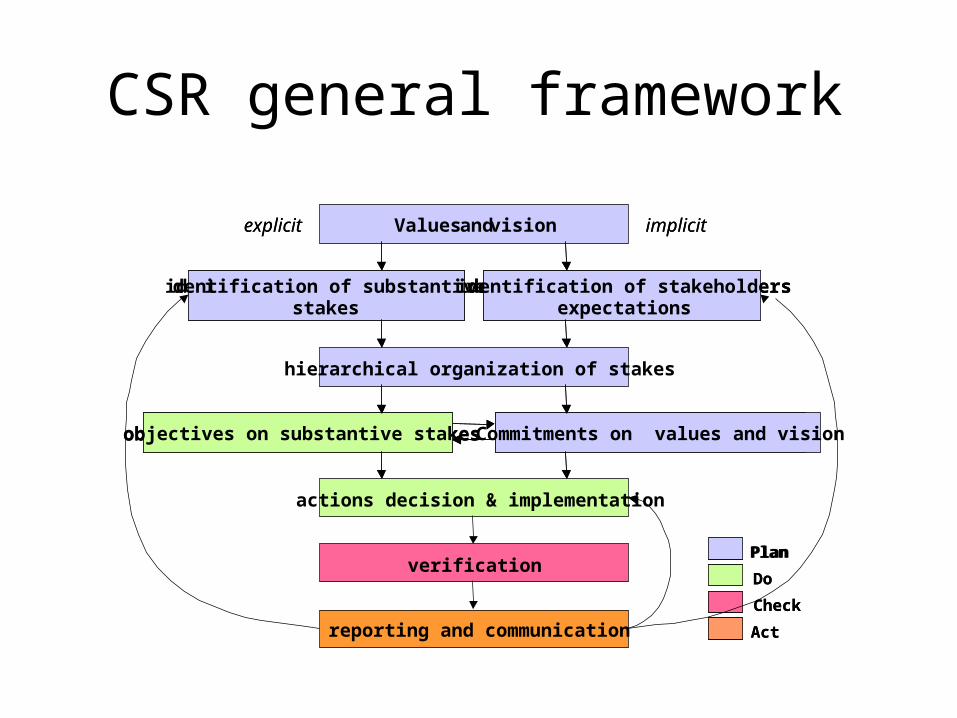

four key elements of any CSR strategy and management system

• Values and Principles for CSR – the guiding principles shaping an organisation’s overall approach to CSR and orientating its decision-making processes;

• CSR Management Process – an overall organisation process linking together values and principles for CSR, CSR Management Tools and the organisation’s core strategy, policies and procedures;

• CSR Management Tools – a number of management tools helping the organisation to address specific issues and ‘themes’ linked with CSR performance, e.g. stakeholder engagement, reporting etc.; and

• Assurance – procedures of internal audit (self-governed by the organisation) and external verification (provided by independent third parties) aimed to raise the credibility of the system.

CSR general framework

implicit explicit implicit explicit

identification of substantive stakes

identification of stakeholders expectations

identification of substantive stakes

identification of stakeholders expectations

commitments values visions Commitments on values and vision objectives on substantive stakes objectives on substantive stakes

hierarchical organization of stakes

Plan

Act Check Do Plan

Act Check Do

Values and vision

actions decision & implementation

verification

reporting and communication

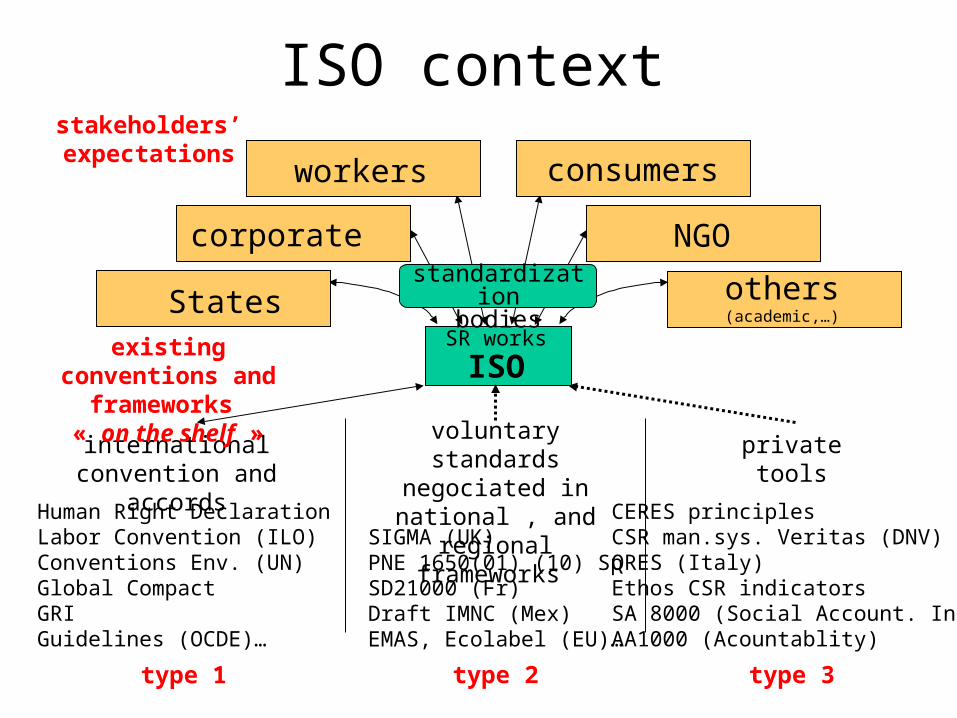

ISO context

SR works

ISO

States

corporate

workers consumers

NGO

others (academic,…)

stakeholders’ expectations

standardizationbodies

private tools

CERES principlesCSR man.sys. Veritas (DNV)QRES (Italy)Ethos CSR indicatorsSA 8000 (Social Account. Int.)AA1000 (Acountablity)

type 3

voluntary standards negociated in national ,

and regional frameworks

SIGMA (UK)PNE 1650(01) (10) SpSD21000 (Fr)Draft IMNC (Mex)EMAS, Ecolabel (EU)…

type 2

Human Right Declaration Labor Convention (ILO)Conventions Env. (UN)Global CompactGRIGuidelines (OCDE)…

international convention and accords

existing conventions and frameworks « on the shelf »

type 1

Coherence between strategies

local Agenda 21

vertical integration

national sustainable development strategies

international governanceconventions, accords…

peer review

corporate sustainable development strategies

mandatory regulations