Solvency II - Eversheds Sutherland · Solvency II EXPANDING THE VIEW Eversheds LLP, Pinwheel...

59

Solvency II EXPANDING THE VIEW Eversheds LLP, Pinwheel Consulting Limited and SmartControls 22 March 2011

Transcript of Solvency II - Eversheds Sutherland · Solvency II EXPANDING THE VIEW Eversheds LLP, Pinwheel...

Solvency II

EXPANDING THE VIEW

Eversheds LLP, Pinwheel Consulting Limited and SmartControls

22 March 2011

Legal Risk and Compliance Risk

Constantly spoiling surprises

Jeremy Irving, Eversheds LLP

22 March 2011

SCENARIO• De Shevers Group (DSG) is an insurance risk carrying

group

– a holding company, De Shevers Group (DSG), is domiciled inLiechtenstein

– a UK-domiciled subsidiary in the form of a limited company,Shed Verse Limited (SVL)

– a Miami-based subsidiary in the form of a limited company,Hed Severs Co (HSC) and

– a number of other risk-carrying subsidiaries in tax-efficientand emerging markets

• The De Shevers family is strongly influential within DSG,controlling a substantial proportion of DSG shares

SCENARIO• SVL is a substantial business

• 2 of SVL‟s NEDs are also directors of DSG

• DSG and SVL operate a calendar year financial year

• It is now February 2014, and the board of SVL is looking toapprove its Solvency Financial and Condition Report(SFCR) for public disclosure

– Within 14 weeks of 31.12 (as per CEIOPS, 2009)

– Assess the adequacy of its systems of governance, and

– Describe risk categories, exposures, concentration, mitigationand sensitivity, and the performance of the business

SCENARIO• HSC has a coverholder, Guata Boliv Hondur (GBH)

– Involvement in claims, but no decision-making

– Caribbean, and Central and South American markets

• Since 2011, GBH has written a portfolio of propertyinsurance risks for DSG, with HSC fronting for SVL

• GBH‟s marketing message to insureds

– „The cover you want, and the response you need‟

• A number of the De Shevers family are also directors ofGBH

SCENARIO• In February 2012, the first audit of GBH took place

– No material issues

• Audit for February 2013 was delayed for several months

– Freak weather

– Flooding

in the locale of GBH's headquarters and in many of its markets

• When the audit took place, it found that many of GBH'srecords were missing

SCENARIO• During 2013 GBH began to report large losses

• Adverse litigation decisions

– Emphasis on overall relationship, including pre-contract

– GBH directors agreed claim amounts

• GBH and DSG have struggled to deal with claims from therecent weather event

– Loss adjusters no longer allowed to access some sites andregions

• Requires a risk-carrier‟s “compliance function” to assess

– the “possible impact of any changes in the legal environment” and

– the “compliance risk”

• Insurers will need to establish methodologies to assess and challenge assumptions as to:

– where risk lies

– and the potential impact of such risk.

ARTICLE 46

COMPLIANCE RISK

• Not defined

• Compliance Risk can be taken to mean:

“the risk of legal or regulatory sanctions,material financial loss, or loss of reputation anundertaking may suffer as a result of its failureto comply with the laws, regulations andadministrative provisions.”

(“CEIOPS” - “Risk Management and Other Corporate Issues” )

LEGAL RISK

• Not defined but referred to in Article 101

• Legal Risk can be taken to mean:

“the possibility that lawsuits, adverse judgmentsfrom courts, or contracts that turn out to beunenforceable, disrupt or adversely affect theoperations or condition of an insurer”

(“Solvency II Glossary”, - Comité Européen des Assurances and the

Groupe Consultatif Actuariel Européen)

• Jurisprudence

– Contract, tort, equity etc

• Architecture

– Legislation, judicial decisions, regulator decisions etc

• GBH

– Judicial decisions

• Overall relationship and claim agreements

– Regulator decisions

• Loss adjusters no longer allowed to access some sites andregions

LEGAL ENVIRONMENT

• Due diligence

– Review of key legal features and risks in jurisdiction

– Review contracts and operational structures / procedures

• Monitoring

– Change-tracking legal / regulatory developments

• Occurred, Imminent, Probable, Possible

– Contracts and operational conduct / developments

• Compliance risk

– Legal / regulatory position in market and carrier‟s domicile

STATUS, CHANGES & IMPACT

GBH

• Due diligence

– Establish significance of „overall relationship‟

– Clarify scope of GBH‟s activities and rights

– Clear mechanisms for remediation

• Monitoring

– Track the new rules on loss adjusters

– Establish effect of director interference in claims

• Compliance risk

– What is SVL going to say in its SFCR?

Group Supervision under Solvency II

Michael Wainwright, Eversheds LLP

Why is group supervision important?

• Risk to financial stability posed by groups

• Journey from the Insurance Groups Directive to Solvency II

– the objective – entire EEA Group supervised by a single supervisor

– pushback by smaller states – solo supervision and supervisory colleges

• Worldwide groups and equivalence

What does group supervision involve?

• Solvency II for groups includes

– Solvency calculation

– Own Risk and Solvency Assessment

– Disclosure and regulatory returns

– Risk concentrations and intra group deals

Triggers for group supervision

• Insurance group – one insurer owned by another or both owned by the same insurance holding company

• Rules apply at the level of the highest EEA group and the highest worldwide group

• Financial Conglomerates Directive covers mixed financial groups

• Mixed activity holding company covers non-financial groups

EEA and worldwide insurance groups

Ultimate non-EEA holding company

EEA holding company Non-EEA insurance companies

EEA insurers Non-EEA insurers

EEA Group Worldwide Group

DSG – HoldCo - Liechtenstein

HSC – Insurer - Miami SVL – Insurer - UK

GBH - Coverholder

De Shevers Group

Directors

DSG – HoldCo - Liech

HSC – Insurer - Miami SVL – Insurer - UK

De Shevers Group - alternatives

DSG – HoldCo - Liech

HSC – Insurer - Miami

SVL – Insurer - UK

New Parent - US

EEA group

• Rules to determine which EEA supervisor will carry out group supervision

• Other regulators will still regulate on a solo basis

• College of supervisors

• Calculation of group solvency

– Consolidation – diversification benefits

– Deduction and aggregation – needs supervisor consent

• Special rules for non-insurance entities

Group governance and risk management

• Solvency II requires that “risk management and internal control systems and reporting procedures shall be implemented consistently” across the group

• What arrangements are needed to deliver this?

Solvency II: Systems

in effective

governancesetting yourself apart

Presented by:

Jackie Pritchard

Director,

SmartControls

Eversheds

LondonMarch 2011

SmartControlsTM 2011 All rights reserved. ©

What you need

Use Test Guiding Principle (CP56) The undertaking’s use of the internal model shall be sufficiently material to result in pressure to improve the

quality of the internal model

It is equally important to understand where you are reluctant to use the model(due to model deficiencies)

and ensure this is factored into your model development plan

Nine Key Principles

1 Senior management and the administrative management or supervisory body shall be able to

demonstrate understanding of the internal model

2 The internal model shall fit the business model

3 The internal model shall be used to support and verify decision making in the undertaking

4 The internal model shall cover sufficient risks to make it useful for risk-management and

decision making

5 The undertaking shall design the internal model in such a way that it facilitates analysis of

business decisions

6 The internal model shall be widely integrated with the risk-management system

7 The internal model shall be used to improve the undertaking’s risk-management system

8 The integration into the risk-management system shall be on a consistent basis for all uses

9 The SCR shall be calculated at least annually from a full run of the internal model, and also when there

is a significant change to the undertaking’s risk profile

SmartControlsTM 2011 All rights reserved. ©

What you need (Sys of Gov L2 Paper (formerly CP33)

Effective 41(1) and proportionate(2) system of governance test

implemented written policies3 and ensure continuity and regularity in performance – apply appropriate and

proportionate systems, resources and procedures4

Effective internal control system46to include administrative and accounting

procedures, an internal control framework, appropriate reporting arrangements at all levels of the

undertaking46

Effective operation (under guidelines) of

Risk Management function44to identify, measure, monitor, manage and report, on a

continuous basis the risks, at an individual and at an aggregated level 44(1)

Internal audit function47effective, to evaluate the adequacy and effectiveness of the

internal control system and other elements of the system of governance 47(1) , independent and objective(2)

with direct reporting lines to an administrative, management or supervisory body (3)

Compliance function46

Actuarial function48details listed

Outsourced functions of any insurance or reinsurance

activities49

remain fully responsible for discharging all of their obligations under this Directive for 49(1) .

materially impairing the quality of the system of governance of the undertaking concerned

49.2(a) or unduly increasing the operational risk 2(b);

SmartControlsTM 2011 All rights reserved. ©

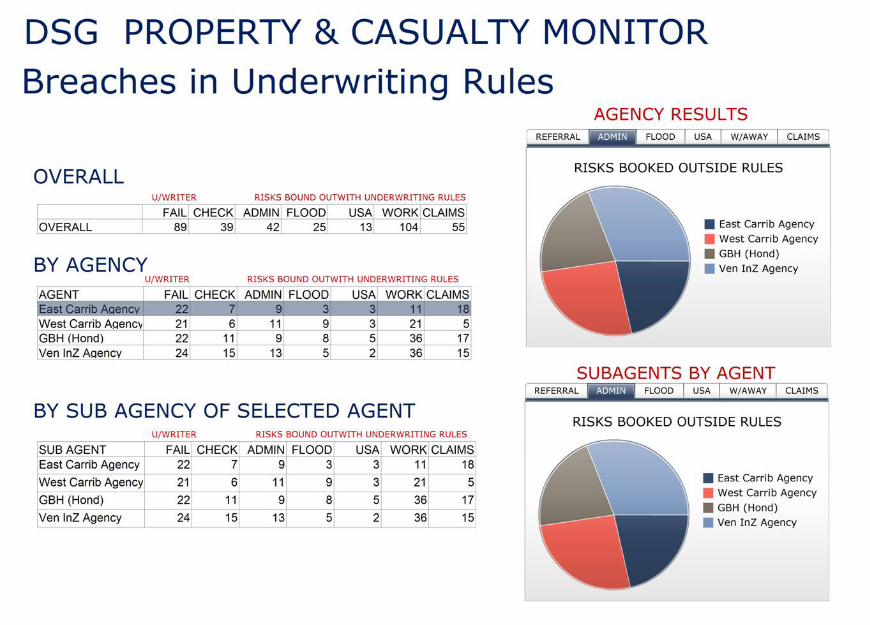

Identifying failure and its impact

20 concerns

20 tests

36 additional pieces of information

None of them reported

All of them available

6 breaches in 32 lines

Property

&

Casualty

SmartControlsTM 2011 All rights reserved. ©

Identifying failure and its impact

1 concern

2 tests

1 additional piece of information

1,500 breaches in 31,000 lines

Household

SmartControlsTM 2011 All rights reserved. ©

Risk based proportionate reporting

Who hasn’t done what you agreed

Who tried but failed (competences)

Who didn’t do it within tolerances

What value is at risk

What is effort to fix it

Working Capital client money - your money – their money

SmartControlsTM 2011 All rights reserved. ©

Risk based proportionate reporting

Who hasn’t done what you agreed

Who tried but failed (competences)

Who didn’t do it within tolerances

What value is at risk

What is effort to fix it

Worldwide

financial

controls

Solvency II

Risk Assessment and

Communication

Rosanne Bachman CPCU

Pinwheel Consulting Ltd

www.pinwheelconsulting.com

5 Key Elements

I. Risk Has Changed

II. Risks Have Changed

III. Losses Happening More Violently

IV. Loss Potential in Insured Areas

V. Drive With a Clear View to the

Future

2003 Losses Happening More Violently

Total Economic Losses„04 $123b, „05 $230b, „08 $269b

Total Economic Losses

2009 $63b & 2010 $222b

Economic & Insured Losses 1950 -2008

Economic and Insured losses „80-

‟10

Number of Great & Devastating

Events ‟80 -‟10

Source: Munich Re

Total Number of Nat Cats „80-‟10

Correlation of EventsHurricane Mitch 1998

Past Data

Anticipating risk and change

Measuring what has changed

Questioning what is in and not in the

models

Seeking out additional knowledge -

correlating the uncorrelated

Worse case and realistic disaster

scenarios

WHAT IF…..

“Pay all claims” Cuthbert Heath

1906

QUESTIONS?