Solvency II Breakfast Briefing 3 December 2015 - Deloitte · Solvency II Breakfast Briefing 3...

46

© 2015 Deloitte Solvency II Breakfast Briefing 3 December 2015 Leading business advisers

-

Upload

nguyenkhue -

Category

Documents

-

view

218 -

download

2

Transcript of Solvency II Breakfast Briefing 3 December 2015 - Deloitte · Solvency II Breakfast Briefing 3...

© 2015 Deloitte

Solvency II Breakfast Briefing3 December 2015

Leading business advisers

Solvency II and Internal Audit

Parameter Uncertainty

Aggregation and Dependency

Stress and Scenario Testing

Contract Boundaries – Non Life

Contract Boundaries - Life

Board Considerations

© 2015 Deloitte

Internal AuditAnlo Taylor, Senior Manager

© 2015 Deloitte4

• Impact of SII on Internal Audit

• To note…

• What are IA peers doing re SII

• SII areas to consider for 2016 Audit Plans

Solvency II Internal AuditOverview

© 2015 Deloitte5

Solvency II Internal Audit

Audit ‘requirement’ shift

‘Self’ Regulation

IIA Standards

Internal Audit

Best Practices

Stakeholder

Needs and

Expectations

Solvency II

Directive

IIA

recommendations

for Financial

Services Internal

audit

Law

© 2015 Deloitte6

Solvency II Internal Audit

Similarities between SII and IIA requirements

An internal audit function is a SII requirement (30) & to be appropriately

implemented as key function (guideline 5)

IA function can be outsourced (31) but have to allocate overall responsibility for

the outsourced key function in group. (guideline 50)

IA function can not be 'combined' with another function (32) & requires

independence at engagement performance level (guideline 32)

CBI should be informed prior to the outsourcing of internal audit function. (37)

(a49)

IA must have written policies for internal audit, implemented & reviewed at least

annually; prior approval by Board (a41)

IA function have to evaluate the adequacy and effectiveness of the internal

control system and other elements of the system of governance. IA function has to have a IA policy ie. charter/terms of reference.

(guidelines 9 & 33)

Minimum 'tasks' for IA function:

- establish, implement and maintain audit plan & report plan to Board;

- risk-based approach in deciding its priorities;

- issue an internal audit report to the board with findings, recommendations,

owner & implementation date;

- remediation testing (verify compliance with agreed action plans)

(guideline 34 on IA tasks)

© 2015 Deloitte7

• Internal Audit Assessment included in CP73 was not included in CP92, but in

practice the expectation is that it will be considered as part of the audit

universe. SII requires that u/takings must ensure that data used to calculate

technical provisions is accurate, appropriate and complete.

• The requirement for IA function automatically include requirement for PCF-13

• Most notable impact of SII is on insurance captives or subsidiaries of very large

insurance group, previously immaterial when group audit universe was defined

Solvency II Internal Audit To note…

© 2015 Deloitte8

Solvency II Internal Audit 2015 Internal Audit coverage of SII

© 2015 Deloitte9

Solvency II Internal Audit2016 Internal Audit Plans - coverage of SII

© 2015 Deloitte10

Pillar 1 Assessment of Reserving process (CP92/ CP73)

- Review of processes around preparation and submission of data provided to the

Actuarial Function and around the production of the booked reserves to provide

reasonable assurance that the data is accurate and complete

Model Risk Management

- Review processes and controls around operation of the model – including

governance, segregation of duties, model maintenance and updates, data checks,

controls over third party elements.

Pillar 2 High level review of ORSA governance and processes

- Review of ORSA Policy against Solvency II requirements and market best practice.

- Review of ORSA process – governance, processes and procedures in terms of

production of the ORSA.

- Review whether the methodology used the ORSA has been appropriately

documented.

- Review evidence of stress and scenario testing considered as part of the ORSA to

ensure all key risks are captured.

- Review of Board input into the ORSA process and evidence of appropriate challenge

of the assumptions and results of the solvency assessment and developing

appropriate response strategies.

Solvency II Internal AuditSII areas to consider for 2016 Audit Plans

© 2015 Deloitte11

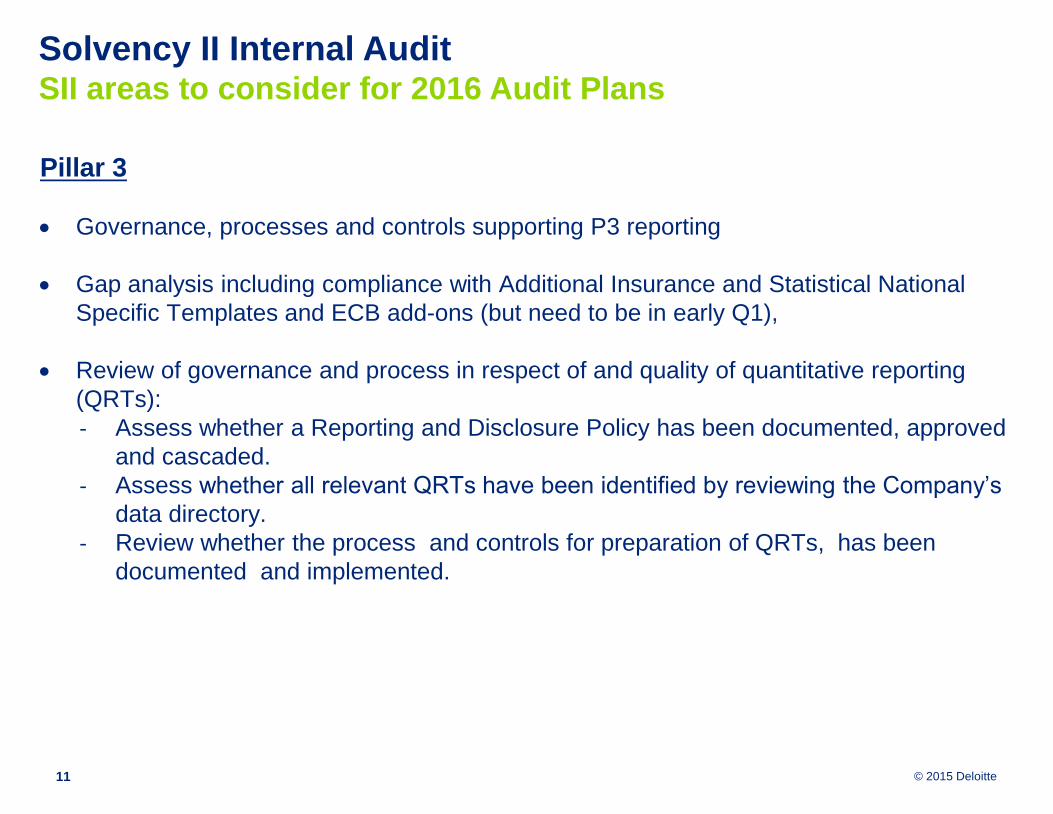

Pillar 3

Governance, processes and controls supporting P3 reporting

Gap analysis including compliance with Additional Insurance and Statistical National

Specific Templates and ECB add-ons (but need to be in early Q1),

Review of governance and process in respect of and quality of quantitative reporting

(QRTs):

- Assess whether a Reporting and Disclosure Policy has been documented, approved

and cascaded.

- Assess whether all relevant QRTs have been identified by reviewing the Company’s

data directory.

- Review whether the process and controls for preparation of QRTs, has been

documented and implemented.

Solvency II Internal AuditSII areas to consider for 2016 Audit Plans

© 2015 Deloitte12

Pillar 3 (continued)

Review of governance and process in respect of and quality of narrative reporting:

- Assess whether a Reporting and Disclosure Policy has been documented, approved

and cascaded.

- Solvency and Financial Condition Report (SFCR)

• Review of structure and high level content to assess whether the SFCR is in line

with Solvency II requirements and market best practice.

• Assess whether the process for producing the SFCR has been appropriately

documented.

• Review of consistency with reporting and disclosure policy.

- Regular Supervisory Report (RSR)

• Review of structure and high level content to assess whether the RSR is in line

with Solvency II requirements and market best practice.

• Assess whether the process for producing the RSR has been appropriately

documented.

• Review of consistency with reporting and disclosure policy.

Solvency II Internal AuditSII areas to consider for 2016 Audit Plans

© 2015 Deloitte

Parameter UncertaintyEamon Howlin, Senior Manager

© 2015 Deloitte14

Prediction is very difficult – especially about

the future

‒ Niels Bohr*

*Disputed – also attributed to others

Parameter Uncertainty

© 2015 Deloitte15

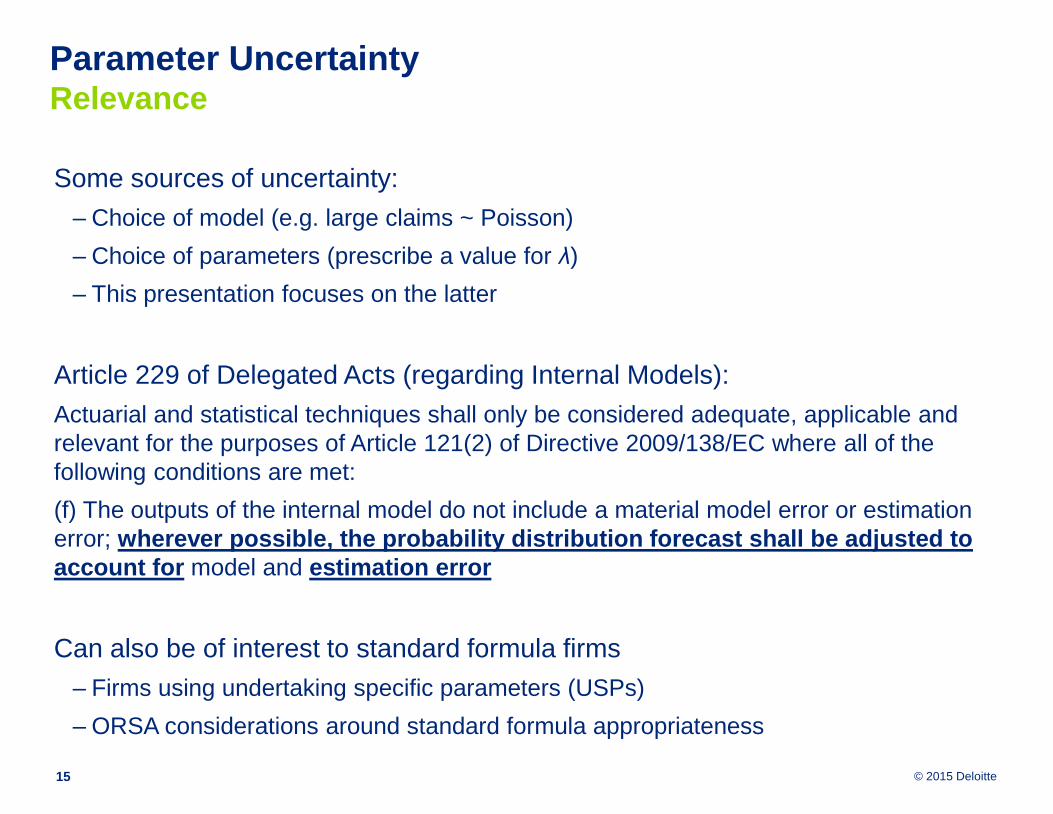

Some sources of uncertainty:

‒ Choice of model (e.g. large claims ~ Poisson)

‒ Choice of parameters (prescribe a value for λ)

‒ This presentation focuses on the latter

Article 229 of Delegated Acts (regarding Internal Models):

Actuarial and statistical techniques shall only be considered adequate, applicable and

relevant for the purposes of Article 121(2) of Directive 2009/138/EC where all of the

following conditions are met:

(f) The outputs of the internal model do not include a material model error or estimation

error; wherever possible, the probability distribution forecast shall be adjusted to

account for model and estimation error

Can also be of interest to standard formula firms

‒ Firms using undertaking specific parameters (USPs)

‒ ORSA considerations around standard formula appropriateness

Parameter UncertaintyRelevance

© 2015 Deloitte16

• Estimation error is the difference between an estimated value and the true

value of a parameter

• How can we be sure our parameters are appropriate?

• If we estimate parameters from (adjusted) data what would happen if we had

observed a different data sample?

• Different data samples (observed from the same distribution) may lead to very

different parameter estimates

Parameter UncertaintyIntroduction

© 2015 Deloitte17

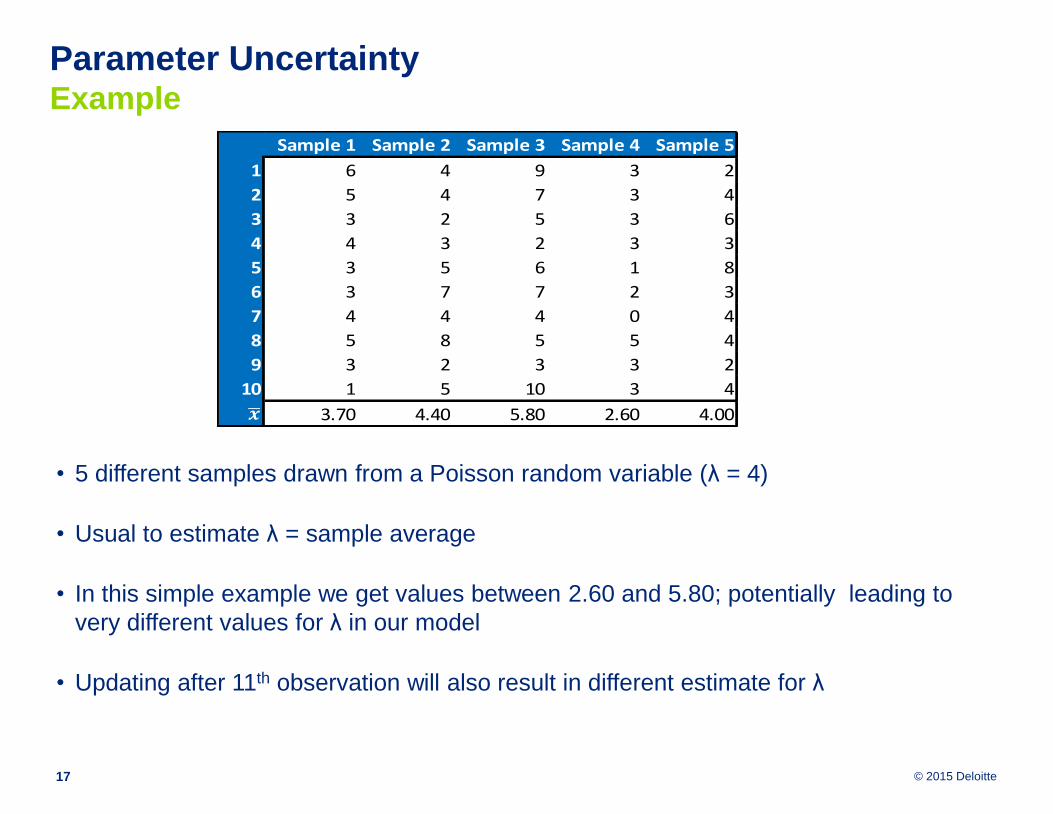

• 5 different samples drawn from a Poisson random variable (λ = 4)

• Usual to estimate λ = sample average

• In this simple example we get values between 2.60 and 5.80; potentially leading to

very different values for λ in our model

• Updating after 11th observation will also result in different estimate for λ

Sample 1 Sample 2 Sample 3 Sample 4 Sample 5

1 6 4 9 3 2

2 5 4 7 3 4

3 3 2 5 3 6

4 4 3 2 3 3

5 3 5 6 1 8

6 3 7 7 2 3

7 4 4 4 0 4

8 5 8 5 5 4

9 3 2 3 3 2

10 1 5 10 3 4

3.70 4.40 5.80 2.60 4.00

Parameter UncertaintyExample

© 2015 Deloitte18

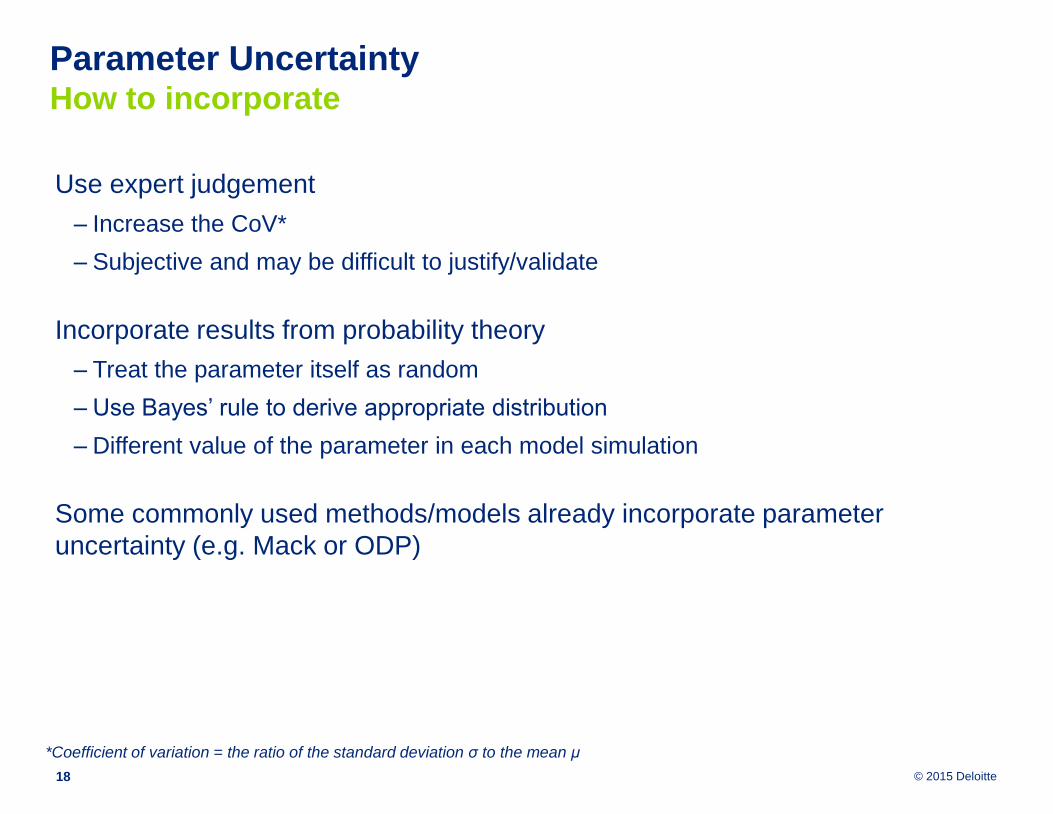

Use expert judgement

‒ Increase the CoV*

‒ Subjective and may be difficult to justify/validate

Incorporate results from probability theory

‒ Treat the parameter itself as random

‒ Use Bayes’ rule to derive appropriate distribution

‒ Different value of the parameter in each model simulation

Some commonly used methods/models already incorporate parameter

uncertainty (e.g. Mack or ODP)

*Coefficient of variation = the ratio of the standard deviation σ to the mean μ

Parameter UncertaintyHow to incorporate

© 2015 Deloitte19

Depends on number of data points, “spread” of data points etc. but….

Here are some (standalone) examples:

Parameter UncertaintyImpact

*for illustrative purposes only

% increase

in CoV

Poisson - Sample 3 4.0%

Irish Motor Claims 2005-14* 49.2%

Reserve USP based on Taylor/Ashe data 9.7%

© 2015 Deloitte

Aggregation and DependencyEamon Howlin, Senior Manager

© 2015 Deloitte21

Dependency describes the relationship between two or more variables

Dependency assumptions a key input into any model

‒ Will impact diversification benefit

‒ Key focus of regulatory scrutiny

Implicit dependency

‒ Inflation

‒ Impact of CATs

‒ Shocks/Binary Events/ENIDS

Explicit dependency

‒ Usually via a copula

‒ Need to choose a copula and parameters

‒ Commonly use Gaussian Copula (“the formula that killed Wall Street”)

Aggregation and dependencyIntroduction

© 2015 Deloitte22

• Correlation and dependency often (incorrectly)

used interchangeably

• Correlation is a measure of linear dependency

• Dependency is not always linear

• Not all dependent variables are correlated

• In the following examples correlation = 0

• Do you think they’re independent?

Graph source: Wikipedia

Gaussian Copula

Aggregation and dependencyCorrelation vs dependency

© 2015 Deloitte23

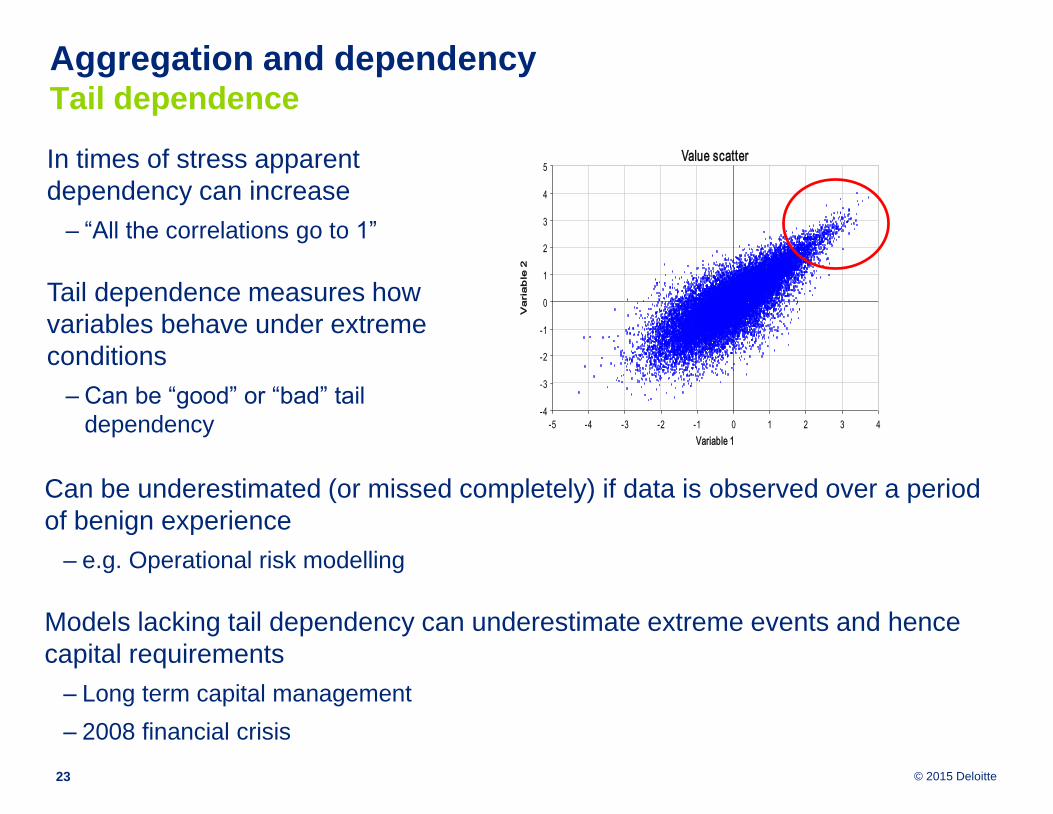

In times of stress apparent

dependency can increase

‒ “All the correlations go to 1”

Tail dependence measures how

variables behave under extreme

conditions

‒ Can be “good” or “bad” tail

dependency

Can be underestimated (or missed completely) if data is observed over a period

of benign experience

‒ e.g. Operational risk modelling

Models lacking tail dependency can underestimate extreme events and hence

capital requirements

‒ Long term capital management

‒ 2008 financial crisis

Value scatter

-4

-3

-2

-1

0

1

2

3

4

5

-5 -4 -3 -2 -1 0 1 2 3 4

Variable 1

Va

ria

ble

2

Aggregation and dependencyTail dependence

© 2015 Deloitte24

All models are wrong, but some models are

useful

‒ George Box

A word of warning…….

……is yours one of the useful ones?

© 2015 Deloitte

Stress and Scenario TestingMaaz Mushir, Manager

© 2015 Deloitte

Sensitivity Testing - Straightforward and common technique to assess financial impact

of adverse changes in a single risk parameter (single factor analysis) relative to a best

estimate view. Sensitivity testing can be used to highlight whether a risk or assumption is

material.

Stress Testing - In a stress test, a single or a small number of connected risk factors are

stressed in isolation from other risk factors and the effect on the economic balance sheet is

calculated. A stress test can therefore serve to analyse the exposure of a company to

specific (individual) risk factors.

Scenario Testing - A scenario tries to define and include all risk factors to which a

company may be exposed. Scenarios do not predict future development, but rather

illuminate extreme but still possible situations.

Back-testing - A comparison of the actual observed (historical) values of key financial

variables with the predictions generated by the stress-testing models. Back-testing can be

used to validate the robustness of stress testing models.

Reverse Stress Testing – These are stress tests that require a firm to assess scenarios

and circumstances that would render its business model unviable, thereby identifying

potential business vulnerabilities.

Stress and Scenario TestingDefinitions

26

© 2015 Deloitte

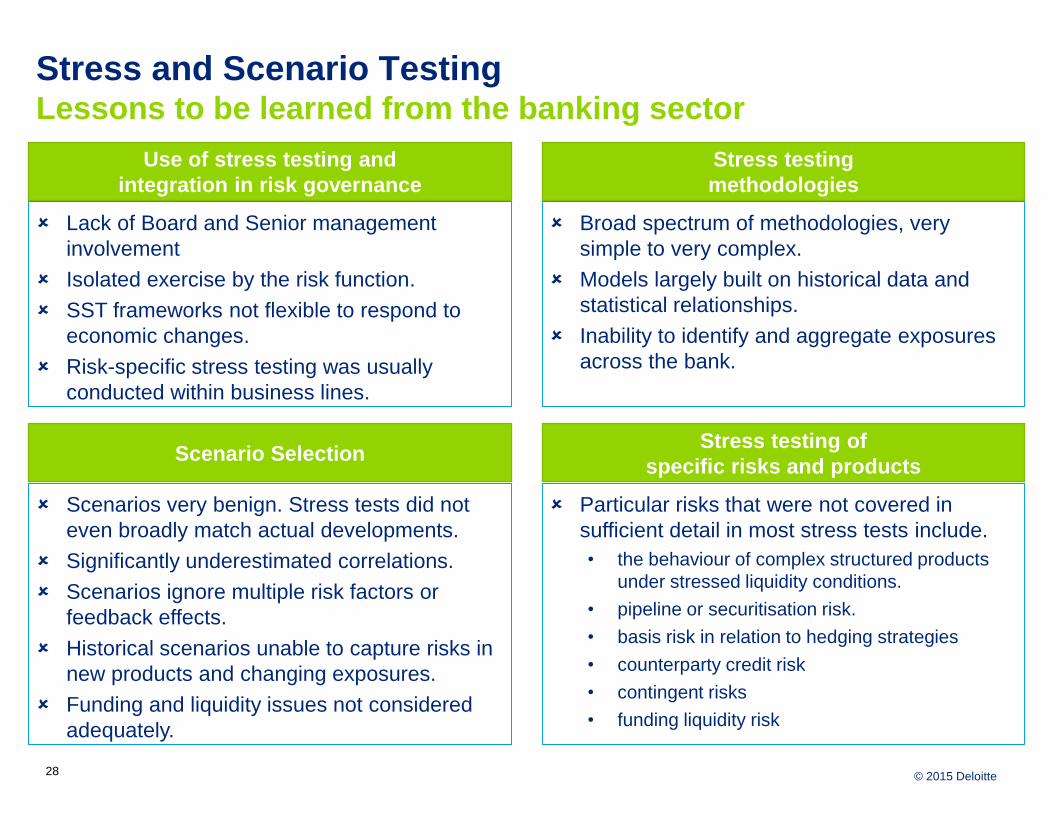

Stress and Scenario TestingLessons to be learned from the banking sector

Paper highlighted weaknesses in stress

testing practices employed prior to the crisis

in 4 key areas:

i. Use of stress testing and integration in

risk governance;

ii. Stress testing methodologies;

iii. Scenario selection; and

iv. Stress testing of specific risks and

products.

Performance of stress testing

during the crisis

May

2009

27

© 2015 Deloitte

Stress and Scenario TestingLessons to be learned from the banking sector

Stress testing

methodologies

Broad spectrum of methodologies, very

simple to very complex.

Models largely built on historical data and

statistical relationships.

Inability to identify and aggregate exposures

across the bank.

Use of stress testing and

integration in risk governance

Lack of Board and Senior management

involvement

Isolated exercise by the risk function.

SST frameworks not flexible to respond to

economic changes.

Risk-specific stress testing was usually

conducted within business lines.

Stress testing of

specific risks and products

Particular risks that were not covered in

sufficient detail in most stress tests include.

• the behaviour of complex structured products

under stressed liquidity conditions.

• pipeline or securitisation risk.

• basis risk in relation to hedging strategies

• counterparty credit risk

• contingent risks

• funding liquidity risk

Scenario Selection

Scenarios very benign. Stress tests did not

even broadly match actual developments.

Significantly underestimated correlations.

Scenarios ignore multiple risk factors or

feedback effects.

Historical scenarios unable to capture risks in

new products and changing exposures.

Funding and liquidity issues not considered

adequately.

28

© 2015 Deloitte

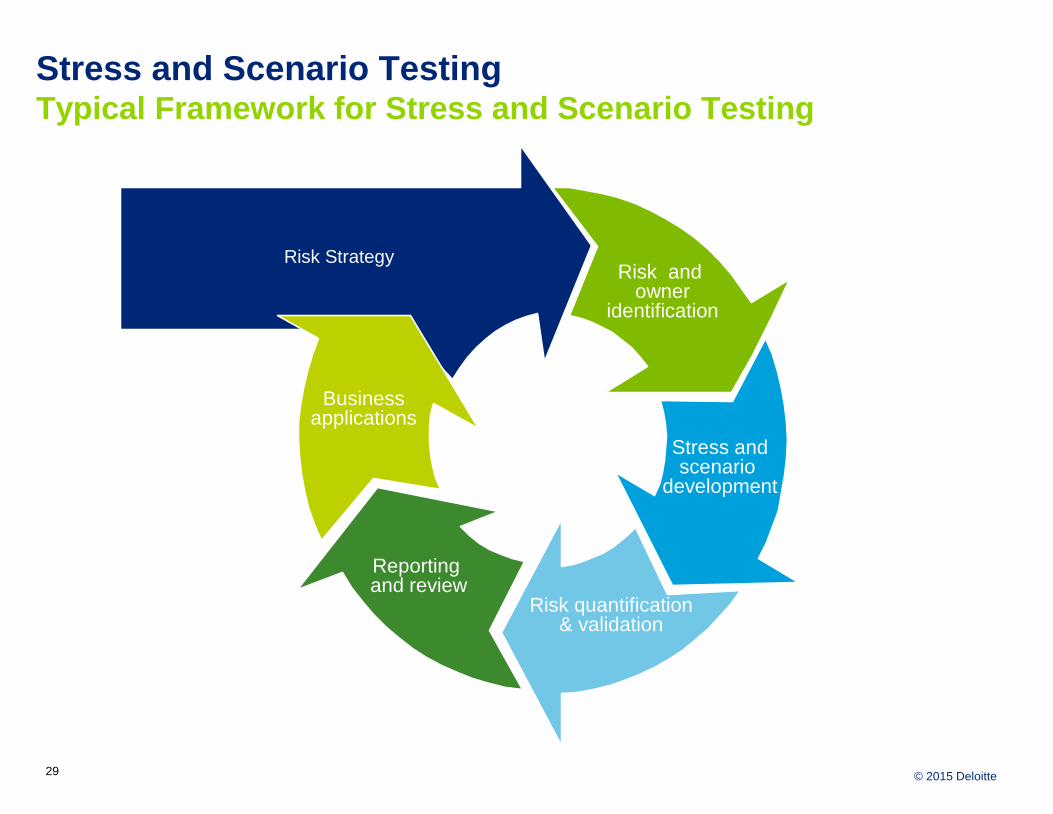

Stress and Scenario TestingTypical Framework for Stress and Scenario Testing

Risk StrategyRisk and

owneridentification

Risk quantification& validation

Reporting and review

Businessapplications

Stress andscenario

development

29

© 2015 Deloitte

Stress and Scenario TestingMaturity Ladder

Risk StrategyRisk and

owneridentification

Risk quantification& validation

Reporting and review

Businessapplications

Stress andscenario

development

- Clear governance, and well

developed frameworks.

- Business functions engaged in

identifying risks and developing

scenarios.

- SST linked to business plan

and changes in risk profile.

- Complimentary and

independent risk perspective to

Economic Capital Models.

- Reasonable evidence of

embedding in decision making.

- Stresses based on a 1-in-200

event from the EC model.

- Additional focus on risks not

covered in SCR.

- SST focussed on one metric

only (SCR).

- SST treated as a compliance

exercise.

- Very technical output.

- Attention to emerging risks and

changing risk profile.

- Wider range of scenarios,

including control failures.

- Peer analysis, and industry

benchmarking,

- Wide range of metrics used,

IFRS, EEV, SCR, Liquidity.

- Mitigating actions developed

for different scenarios.

- Perform reverse stress testing

and back-testing.

- Strong evidence of embedding

in decision making.

- SST performed at different

confidence levels and multi-

period time horizons.

- Developing early warning

indicators and trigger points for

management actions.

- Realistic contingency actions

through techniques such as

war-gaming.

- Views from internal and

external experts on scenarios

and contingency plans.

- Wide range of reverse stress

tests, extended to disaster

management and recovery

planning.

- Reporting and communication

tailored to different audience.

Primitive Basic Advanced Leading

30

© 2015 DeloitteSolvency II

Stress and Scenario TestingGeneral Insurance Stress Tests

• In July 2015 the PRA sent a request to the UK’s

largest general insurers to participate in a stress

test exercise.

• The GIST have 9 scenarios guided by the

regulator, plus two additional insurer specific

scenarios.

• These stress tests have been

designed to complement the

ongoing work of the PRA in

assessing the resilience of UK

insurers and in monitoring how

insurers are developing their

Own Risk and Solvency

Assessment.

• The full document on GIST can

be found here:

• http://www.bankofengland.co.uk/

pra/Documents/supervision/activ

ities/generalinsurancestresstesti

ngjuly2015.pdf

• http://www.bankofengland.co.uk/

pra/Documents/supervision/activ

ities/gist2015.xlsx

31

© 2015 Deloitte

Contract Boundaries – Non LifeDarren Shaughnessy, Manager

© 2015 Deloitte33

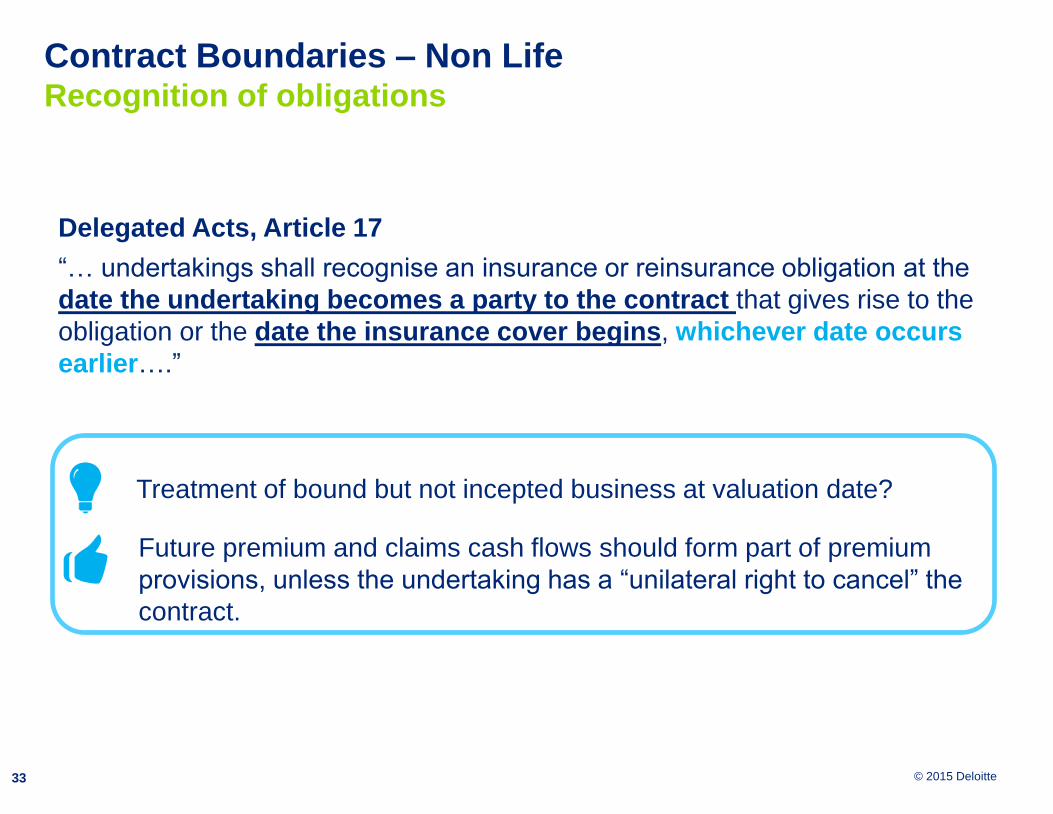

Contract Boundaries – Non LifeRecognition of obligations

Delegated Acts, Article 17

“… undertakings shall recognise an insurance or reinsurance obligation at the

date the undertaking becomes a party to the contract that gives rise to the

obligation or the date the insurance cover begins, whichever date occurs

earlier….”

Treatment of bound but not incepted business at valuation date?

Future premium and claims cash flows should form part of premium

provisions, unless the undertaking has a “unilateral right to cancel” the

contract.

© 2015 Deloitte34

Contract Boundaries – Non LifeRecognition of obligations – impact on premium volume

measure

Premium risk volume measure at t=0

IRD ------------- ----------------------

IRD ------------

IRD -----

t-1 t t+1 t+2

IRD Initial recognition date of contract

P(last,s)

Ps

FP(existing,s)

FP(future,s)

Premium excluded

© 2015 Deloitte35

Contract Boundaries – Non LifeBoundary of a recognised contract

Undertakings should consider the boundary of a contract to be the point in time in the

future which the undertaking has a unilateral right to cancel the contract, reject the

premium or amend the premium or benefits (“unilateral right to cancel”).

Treatment of multi-year contracts (technical provisions)?

• All future premium and claims cash flows for the whole of the multi-year

contract should form part of technical provisions, unless the undertaking has

a “unilateral right to cancel” the contract.

• Any obligations which relate to cover provided after the date in which the

undertaking has “unilateral right to cancel” do not belong to the contract

unless the undertaking can compel the policyholder to pay the premium for

those obligations.

© 2015 Deloitte36

Contract Boundaries – Non LifeBoundary of a recognised contract - impact on premium volume

measure

EIOPA Q&A set 8 on the Preparatory Phase Technical Specification (10/07/2014)

There should not be a link between the contract boundary and the premium and

reserve risk modules, as it is factor based.

Technical Provisions

No profits / losses are recognised

beyond this point defined as the

contract boundary.

Premium volume measure (SCR)

The premium volume measure is the

expected value of premiums

irrespective of what point in time is

defined as the contract boundary.

© 2015 Deloitte

Contract Boundaries - LifeColin Murphy, Senior Manager

© 2015 Deloitte38

Contract Boundaries – LifeReviewable products & unit-linked savings

Reviewable products

• General Irish market practice is that the contact boundary is the date of

review and the policy is assumed to become paid-up after that date.

Regular premium savings products

• General Irish market practice is that the contract boundary is assumed to

be immediately and no future premiums from the valuation date forward, in

most cases.

Solvency II rules prevent the recognition of future premiums

unless there is a future material insurance event or financial

guarantee.

© 2015 Deloitte39

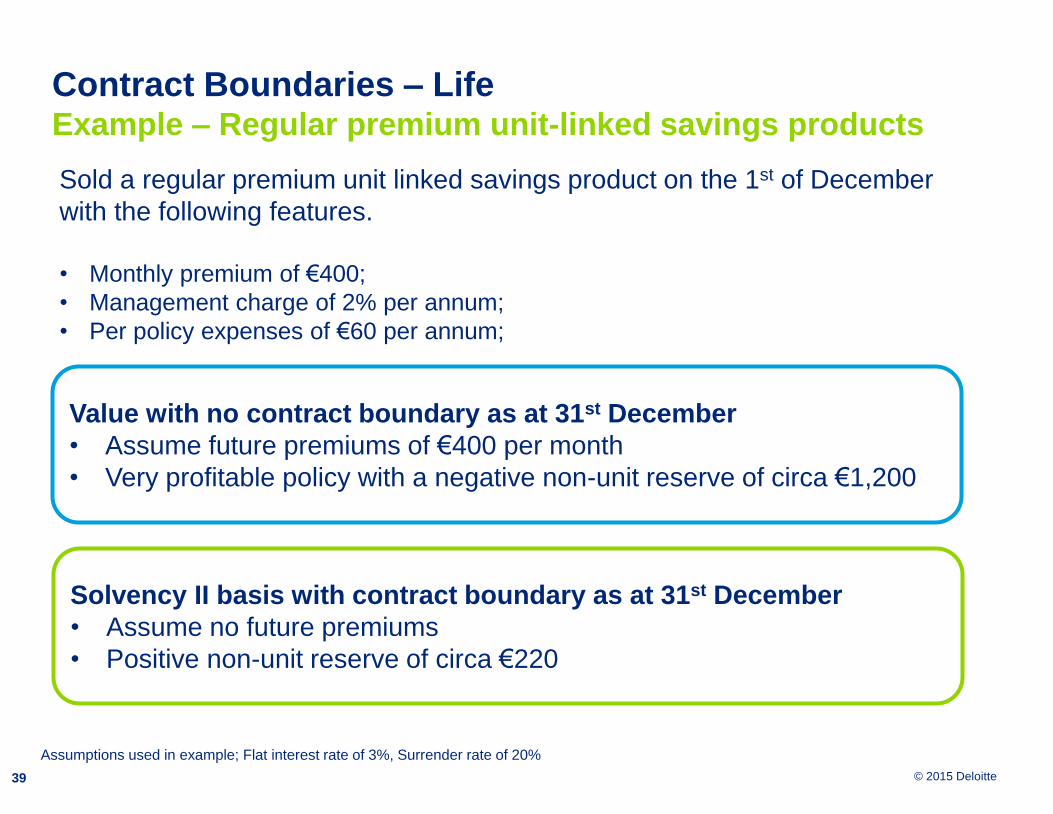

Contract Boundaries – LifeExample – Regular premium unit-linked savings products

Sold a regular premium unit linked savings product on the 1st of December

with the following features.

• Monthly premium of €400;

• Management charge of 2% per annum;

• Per policy expenses of €60 per annum;

Assumptions used in example; Flat interest rate of 3%, Surrender rate of 20%

Value with no contract boundary as at 31st December

• Assume future premiums of €400 per month

• Very profitable policy with a negative non-unit reserve of circa €1,200

Solvency II basis with contract boundary as at 31st December

• Assume no future premiums

• Positive non-unit reserve of circa €220

© 2015 Deloitte40

Contract Boundaries - LifeConsiderations

Expenses after the contract boundary

• Do you use full expenses, paid-up expenses or another expense

assumption after the contract boundary?

Extending the contract boundary

• Some insurers are considering adding free benefits to insurance

contracts to extend the contract boundary.

Preference for higher own funds

• Depending on your preference for higher own funds and potentially a

lower coverage ratio or vice versa could influence how companies

approach the application of the contract boundary.

© 2015 Deloitte

Board ConsiderationsSinéad Kiernan, Director

© 2015 Deloitte42

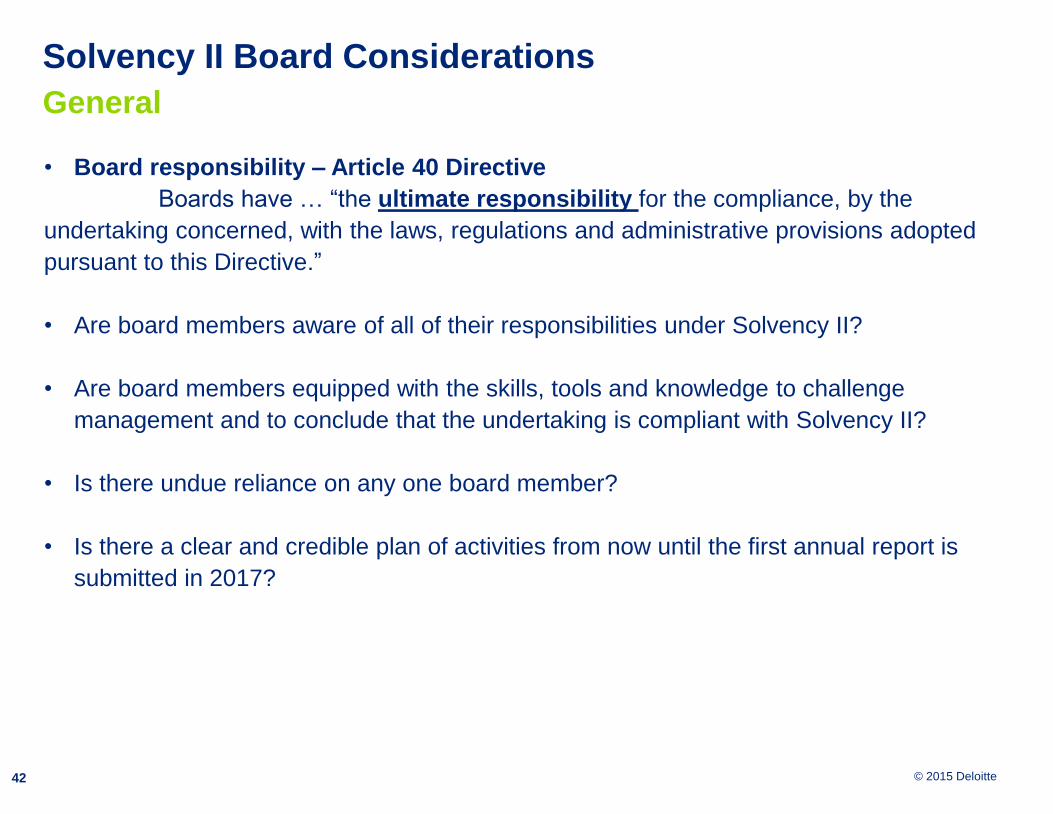

Solvency II Board Considerations

General

• Board responsibility – Article 40 Directive

Boards have … “the ultimate responsibility for the compliance, by the

undertaking concerned, with the laws, regulations and administrative provisions adopted

pursuant to this Directive.”

• Are board members aware of all of their responsibilities under Solvency II?

• Are board members equipped with the skills, tools and knowledge to challenge

management and to conclude that the undertaking is compliant with Solvency II?

• Is there undue reliance on any one board member?

• Is there a clear and credible plan of activities from now until the first annual report is

submitted in 2017?

© 2015 Deloitte43

Solvency II Board Considerations

Pillar 1

• Is there a clear understanding of the differences between the Solvency II balance sheet

and financial statements / Solvency I balance sheets?

• Solvency II risk margin is a very different concept to Solvency I margin for uncertainty

(non-life undertakings)

• Capital coverage ratio on a Solvency I vs Solvency II basis

• What are the drivers of SCR? What might cause it to fluctuate?

© 2015 Deloitte44

Solvency II Board Considerations

Pillar 2

ORSA:

• Have board members been actively involved in identifying risks and stresses?

• How have board members steered the ORSA process?

• Has ORSA been used in any board level decisions?

Standard formula appropriateness: Have board members challenged the analysis and

any resulting actions?

Key control functions:

• Risk management: Is there sufficient challenge from risk management, including at

board level?

• Compliance function: Advises board on compliance with Solvency II

• Actuarial Function Report: Is the board aware of changes to the role of the actuary

under Solvency II?

© 2015 Deloitte45

Solvency II Board Considerations

Pillar 3

• Board is responsible for approving annual QRTs, narrative reports and Day 1 QRTs

• Do board members have a good understanding of the QRTs?

• Has there been a dry run to populate QRTs and test the CBI portal?

• Can management provide sufficient evidence to the board of the controls around the

population of QRTs / narrative reports and the quality of data in the reports?

• Is there sufficient time in the 2016 plan for Board review and challenge of regulatory

submissions?

© 2015 Deloitte© 2015 Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company limited by guarantee, and its network of

member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/ie/about for a detailed

description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

With nearly 2,000 people in Ireland, Deloitte provide audit, tax, consulting, and corporate finance to public and private clients

spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings

world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex

business challenges. With over 210,000 professionals globally, Deloitte is committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, Deloitte Global Services

Limited, Deloitte Global Services Holdings Limited, the Deloitte Touche Tohmatsu Verein, any of their member firms, or any of

the foregoing’s affiliates (collectively the “Deloitte Network”) are, by means of this publication, rendering accounting, business,

financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional

advice or services, nor should it be used as a basis for any decision or action that may affect your finances or your business.

Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified

professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person

who relies on this publication.

© 2015 Deloitte. All rights reserved