UTILIZING SOLVENCY II TO IMPROVE INSURER SOLVENCY REGULATION IN

Upload

pankajguptaCategory

view

771download

1description

Solvency Margins

INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY (ASSETS,

LIABILITIES, AND SOLVENCY MARGIN OF INSURERS) REGULATIONS, 2000.

DETERMINATION OF SOLVENCY MARGINS

• LIFE INSURERS– Available Solvency Margin’ means the excess of value of assets

(furnished in IRDA- Form- AA) over the value of life insurance liabilities (furnished in Form H as specified in Regulation 4 of Insurance Regulatory and Development Authority (Actuarial Report and Abstract) Regulations, 2000) and other liabilities of policyholders’ fund and shareholders’ funds;

– “Solvency Ratio” means the ratio of the amount of Available Solvency Margin to the amount of Required Solvency Margin.

• GENERAL INSURERS – “Available Solvency Margin” means the excess of value of assets

(furnished in Form IRDA-Assets- AA) over the value of liabilities (furnished in Form HG), with further adjustments as shown in Table III of Form KG.

– “Solvency Ratio” means the ratio of the amount of Available Solvency Margin to the amount of Required Solvency Margin.

VALUATION OF ASSETS• The following assets should be placed with value zero,--

– Agent’s balances and outstanding premiums in India, to the extent they are not realised within a period of thirty days;

– Agents’ balances and outstanding premiums outside India, to the extent they are not realisable ;

– Sundry debts, to the extent they are not realisable;– Advances of an unrealisable character;– Furniture, fixtures, dead stock and stationery;– Deferred expenses; – Profit and loss appropriation account balance and any fictitious assets other

than pre-paid expenses;– Reinsurer’s balances outstanding for more than three months;– Preliminary expenses in the formation of the company;

• The value of computer equipment including software shall be computed as under:--

– seventy five per cent. of its cost in the year of purchase;– fifty per cent. of its cost in the second year; – twenty-five per cent. of its cost in the third year; and– zero per cent. thereafter.

Statement of Assets

Category of Asset Policyholders' funds:

Shareholders' funds: Amount ( in rupees lakhs) as per (a) below

Amount ( in rupees lakhs) as per (a) below

1 Approved Securities

2 Approved Investments

3 Deposits

4 Non-Mandated Investments

5 Other Assets, specify

6 Total

7 Fair Value Change Account

8 (6) - (7)

Valuation of Liabilities - Life Insurance

• Method of Determination of Mathematical Reserves• Prospective method of valuation :• to account for all prospective contingencies under which any

premiums (by the policyholder) or benefits (to the policyholder/beneficiary) may be payable under the policy, as determined by the policy conditions.

• to account for the cost of any options that may be available to the policyholder under the terms of the contract.

• the amount of liability under each policy tol be based on prudent assumptions of all relevant parameters. The value of each such parameter to based on the insurer’s expected experience and shall include an appropriate margin for adverse deviations (hereinafter referred to as MAD) that may result in an increase in the amount of mathematical reserves.

Valuation of Liabilities - Life Insurance

• Gross premium method of valuation:• premiums payable, if any, benefits payable, if any, on death; benefits

payable, if any, on survival; benefits payable, if any, on voluntary termination of contract, and the following, if any, :-

• basic benefits, • rider benefits,• bonuses that have already been vested as at the valuation date, • bonuses as a result of the valuation at the valuation date, and• future bonuses (one year after valuation date) including terminal

bonuses (consistent with the valuation rate of interest);• commission and remuneration payable, if any, in respect of a policy (This

shall be based on the current practice of the insurer). policy maintenance expenses, if any, in respect of a policy, as provided under sub-para (4) of para 5;

• allocation of profit to shareholders, if any, where there is a specified relationship between profits attributable to shareholders and the bonus rates declared for policyholders.

• Provided that allowance must be made for tax, if any.• Provision for Policy Options.

Valuation Parameters • The bases on which the future policy cash flows shall be computed and

discounted. Each parameter shall have to be appropriate to the block of business to be valued. An appointed actuary shall take into consideration the following,--

– The value(s) of the parameter shall be based on the insurer’s experience study, where available. If reliable experience study is not available, the value(s) can be based on the industry study, if available and appropriate. If neither is available, the values may be based on the bases used for pricing the product. In establishing the expected level of any parameter, any likely deterioration in the experience shall be taken into account;

– The expected level, as determined, shall be adjusted by an appropriate Margin for Adverse Deviations (MAD), the level of MAD being dependent on the degree of confidence in the expected level, and such MAD in each parameter shall be based on the Guidance Notes issued by the Actuarial Society of India, with the concurrence of the Authority.

– Valuation rates of interest shall be not higher than the rates of interest, for the calculation of the present value of policy cash flows determined from prudent assessment of the yields from existing assets attributable to blocks of life insurance business, and the yields which the insurer is expected to obtain from the sums invested in the future

Additional Requirements for Linked Business

• Reserves in respect of linked business shall consist of two components, namely, unit reserves and general fund reserves.

• Unit reserves shall be calculated in respect of the units allocated to the policies in force at the valuation date using unit values at the valuation date.

• General fund reserves (non-unit reserves) shall be determined using a prospective valuation method

Additional Requirements for Provisions

• The appointed actuary shall make aggregate provisions in respect of the following, where it is not possible to calculate mathematical reserves for each policy, in the determination of mathematical reserves:-

– Policies in respect of which extra premiums have been charged on account of underwriting of under-average lives that are subject to extra risks such as occupation hazard, over-weight, under-weight, smoking history, health, climatic or geographical conditions;

– Lapses policies not included in the valuation but under which a liability exists or may arise;

– Options available under individual and group insurance policies;– Guarantees available to individual and group insurance policies;– The rates of exchange at which benefits in respect of policies issued

in foreign currencies have been converted into Indian Rupees and what provision has been made for possible increase of mathematical reserves arising from future variations in rates of exchange;

– Other, if any.

Valuation of Liabilities (General Insurance)

• Reserve for claims incurred but not reported (IBNR") means the reserve for claims incurred but not reported on the balance sheet date, and includes reserve for claims which may be inadequately reserved;

• Reserve for outstanding claims: shall be determined in the following manner:-

– where the amounts of outstanding claims of the insurers are known, the amount is to be provided in full;

– where the amounts of outstanding claims can be reasonably estimated according to the insurer, he may follow the 'case by case method' after taking into account the explicit allowance for changes in the settlement pattern or average claim amounts, expenses and inflation;

• Reserve for unexpired risks, shall be, in respect of,---– Fire business, 50 per cent, – Miscellaneous business, 50 per cent, – Marine business other than marine hull business, 50 per cent; and– Marine hull business, 100 per cent,

of the premium, net of re-insurances, received or receivable during the preceding twelve months

STATEMENT OF LIABILITIES Description Reserves for

unexpired risks

Reserve for Outstanding Claims

IBNR Reserves Total Reserves

1 Fire

2 Marine

Sub class:

Marine Cargo

Marine Hull

3 Miscellaneous

Sub class:

Motor

Engineering

Aviation

Liabilities

Rural insurance

Others

5 Total Liabilities

STATEMENT OF SOLVENCY MARGIN

• REQUIRED SOLVENCY MARGIN BASED ON NET PREMIUM AND NET INCURRED CLAIMS

• RSM means Required Solvency Margin and shall be the higher of the amounts of RSM-1 and RSM-2

• RSM-1 in the table means Required Solvency Margin based on net premiums, and shall be determined as twenty per cent. of the amount which is the higher of the Gross Premiums multiplied by a Factor A and the Net Premiums.

• RSM-2 in the table means Required Solvency Margin based on net incurred claims, and shall be determined as thirty per cent. of the amount which is the higher of the Gross Net Incurred Claims multiplied by a Factor B and the Net Incurred Claims.:

AVAILABLE SOLVENCY MARGIN AND SOLVENCY RATIO

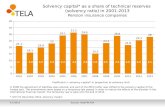

• As per excel sheet

• Solvency ratio• The solvency ratio of an insurance company is the size

of its capital relative to premium written. The solvency ratio is (most often) defined as:

• net assets ÷net premium written The solvency ratio is a measure of the risk an insurer faces of claims that it cannot absorb. The amount of premium written is a better measure than the total amount insured because the level of premiums is linked to the likelihood of claims.

• It is a basic measure of how financially sound an insurer is, but this simple calculation that does not take into account the types of business the company does.

• The solvency margin is a minimum excess on an insurer's assets over its liabilities set by regulators. It can be regarded as similar to capital adequacy requirements for banks. It is essentially a minimum level of the solvency ratio, but regulators usually use a slightly more complex calculation. The current EU requirement is the greatest of:

• 18% of premium written up to €50m plus 16% of premiums above €50m.

• 26% of claims up to €35m plus 23% of claims above €35m. • Some other adjustments are also made. Premiums for high risk

classes of business are increased for the purpose of this calculation, an adjustment is made for reinsurance, etc.

• This requirement is being replaced by "Solvency II". This is a development that is very similar to the Basel II capital adequacy requirements for banks, as it will mean a move to more complex risk models.

• The free asset ratio is net assets adjusted for the solvency margin.

• A solvency measure used by British life insurance companies, the free asset ratio is:

• (available assets - required minimum margin of solvency) ÷admissible assets The exact definition varies and the numbers disclosed by different companies as headline free asset ratios may not be comparable. For example, some companies include future profits. The ratio will also depend on the assumptions made in valuing liabilities.

• In general, the higher the ratio, the more surplus capital a company has available.

• Embedded Value• The embedded value of a life insurance business is an estimate of

the value of both its net assets and the income stream expected from policies already in force.

• E = PV + NAV where E is the embedded value,PV is the present value of future cash flows on policies already in force andNAV is the company's NAV with investments valued at market value.

• The future profits do not include the value of policies that the company will sell in the future, only those already sold. Policies that the company can expect to sell in the future are an important component of the difference between the embedded value and the actual value of the business to investors.

• European embedded value• European Embedded Value (EEV) is a standardised calculation of

embedded value and related numbers that is being adopted by European insurance companies to make their results more meaningfully comparable.

• The EEV principles provide consistent definitions, actuarial assumptions and disclosure requirements for EEV.

• Although EEV provides a tighter set of rules and more consistency between companies, it still leaves a number of important decisions (such as risk premiums to be used) to individual companies. Given the complex nature of insurance accounts, investors should not expect this to mean that comparisons are now easy.

• A key part of EEV is a uniform method of comparing new business premiums: PVNBP.

• PVNBP• Present value of new business premiums (PVNBP) is a measure of sales that forms

part of the European Embedded Value accounting principles that have been adopted in order to provide uniform measures for all European insurers.

• PVNBP is, like annual premium equivalent (APE), a way in which the values of single and regular premium new business sold during a financial period can be combined to give a single sales number. It is:

• value of single premiums + present value of regular premium streams There are two major differences between PVNBP and APE:

• PVNBP adjusts regular premiums to make them comparable with single premiums, APE does the opposite.

• APE uses a simple adjustment factor, PVNBP uses a more sophisticated discounted value.

• The first of these is not of great importance. The APE way of doing things gives a number that is more like the sales number of a trading company and that therefore may be more intuitive.

• In using a DCF PVNBP is more correct, but it introduces more uncertainties and more room for manipulation because it requires choosing an appropriate discount rate.