Solo Growth Corp. - aldershotresources.com · In aggregate, more than 50 years of regulated...

19

Solo Growth Corp. June 2018

Transcript of Solo Growth Corp. - aldershotresources.com · In aggregate, more than 50 years of regulated...

Solo Growth Corp. June 2018

In aggregate, more than 50 years of regulated substance retail experience. Established Canada’s largest private liquor retailer, Solo Liquor.

A strong board of directors with extensive experience in building, growing and successfully monetizing public companies.

Competitive advantage from operating expertise in the regulated retail liquor market. Strong, collaborative and constructive relationships with municipalities and regulators across Alberta as well as landlords across Western Canada.

Selecting optimal locations in the most efficient manner based on a deep understanding of provincial demographics . Extensive expertise tailoring product brands and retail experience to area demographics while also marketing brands with a view to optimizing returns.

More than 20 years of consumer purchasing habits from customer transactions and real estate analytics.

Operational excellence: store sizing, site development, inventory management, staffing, training, cost structure and customer experience drive repeatable and sustainable platform.

$25MM in capital fully funds the opening of 60+ retail cannabis locations in the next 3 years.

2

Opportunity - Overview

Management

Market Expertise

Customer Intel

Sustainable Model

Long term value Creation

Board

Demographics & Brand Awareness

VisionUtilize our extensive expertise to become a sustainable retailer of recreational cannabis.

StrategyCapitalize on more than 50 years of aggregate experience in the controlled substance retail market, employ our understanding of consumer purchasing habits from historical data, and leverage our existing relationships (landlords, municipalities, and regulators) to grow a sustainable retail cannabis business in Western Canada.

3

Execution - Vision & Strategy

Competitive Advantage Customers: Established customer relationships since 1996 (>20,000 customers per day).

Retail and Real Estate Expertise: Rare to have both.

– Identified optimal retail Cannabis locations based on liquor performance and data.

– Relationship with Avison Young provides insight into new commercial developments. Pali Bedi is a multiple recipient of the Circle of Excellence designation as a top three performer for Avison Young in Commercial Real Estate in Alberta.

Regulatory Expertise: 20+ years of execution in a regulatory environment that mirrors retail cannabis framework.

Operational Excellence: Low cost operating model, leveraging data analytics, limited spoilage and inventory optimization.

Capital Allocation: Low cost approach to store CAPEX and OPEX while creating recognized leading retail platform. Quality not compromised.

Human Capital: Track record of lowest industry turnover; committed and loyal employee advantage.

– Proactive approach to employee training with onboarding and continuous education on the rapidly evolving Cannabis industry.

4

Execution

Operational Excellence Generates Returns in all Market & Competitive Environments

5

Opportunity – Canada Retail Market Size

Deloitte’s Recreational Marijuana Insights and Opportunities paper estimates that the base Canadian retail cannabis market could initially range from $4.9B to $8.7B CAD increasing to $12.7B to $22.6B CAD when ancillary markets such as testing labs, security, and various manufacturers are included.

Source: Deloitte Recreational Marijuana Insights and Opportunities

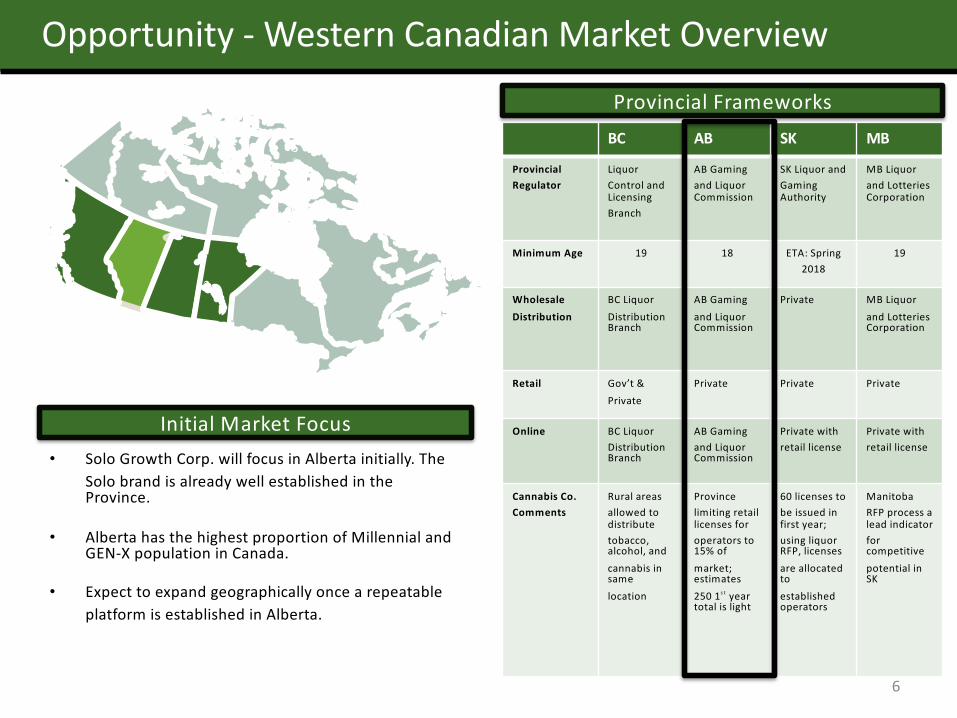

• Solo Growth Corp. will focus in Alberta initially. The

Solo brand is already well established in the Province.

• Alberta has the highest proportion of Millennial and GEN-X population in Canada.

• Expect to expand geographically once a repeatable

platform is established in Alberta.

6

Opportunity - Western Canadian Market Overview

BC AB SK MB

Provincial Regulator

Liquor

Control and Licensing

Branch

AB Gaming

and Liquor Commission

SK Liquor and

Gaming Authority

MB Liquor

and Lotteries Corporation

Minimum Age 19 18 ETA: Spring

2018

19

Wholesale Distribution

BC Liquor

Distribution Branch

AB Gaming

and Liquor Commission

Private MB Liquor

and Lotteries Corporation

Retail Gov’t &

Private

Private Private Private

Online BC Liquor

Distribution Branch

AB Gaming

and Liquor Commission

Private with

retail license

Private with

retail license

Cannabis Co. Comments

Rural areas

allowed to distribute

tobacco, alcohol, and

cannabis in same

location

Province

limiting retail licenses for

operators to 15% of

market; estimates

250 1s t year total is light

60 licenses to

be issued in first year;

using liquor RFP, licenses

are allocated to

established operators

Manitoba

RFP process a lead indicator

for competitive

potential in SK

Initial Market Focus

Provincial Frameworks

7

Opportunity - Alberta’s Demographic Advantage

16

1116

2126

3136

4146

5156

6166

7176

8186

9196

Alb er t a Can ada

U sage M illennials G en X B oom ers

D aily 11% 6% 4%

W eekly/ M onthly 12% 9% 4%

O ccasionally 11% 9% 6%

N ot at A ll 67% 77% 86%

Deloitte Cannabis Usage Survey Alberta & Canada Age Pyramid

A ctive M edical Registrants Total Population

% Registrants to Population

Canada 269,502 35 ,151,728 0 .8%

Alberta 104,272 4 ,067,175 2 .6%

B ritish Colum bia 9,985 4 ,648,055 0 .2%

Saskatchew an 8,466 1 ,098,352 0 .8%

M anitoba 6,650 1 ,278,365 0 .5%

O ntario 110,338 13 ,448,494 0 .8%

Registrants to Population

Alberta Market demographicsand Medicinal Registrants support preferred recreational market thesis

8

Opportunity – Inferred Alberta Retail Market SizeProv. Breakdown of Nat’l Alcohol Sales

Estimated Alberta Retail Cannabis Market Size: $811MM to $1.1B

Colorado vs Alberta

Population

Alberta 4.146m

Colorado 5.607m

Colorado Cannabis Sales - 2017 $1.5B

Source: Stats Canada, Colorado G ov’t

Source: Stats Canada

Deloitte’s Initial National Market Size = $4.9B to $8.7BMedian = $6.8B

11.93% x $6.8B = $811M

Alberta represents 11.9% of total Alcohol sales in Canada

Canada’s 2016 alcohol sales exceeded $22BThe Cannabis market is in its infancy

Pe r Capita 2016 % of Province 2015 Rank 2016 Rank S ale s Rank CAD

$000 $000Ontario $7,516,220 1 $7,926,079 1 $683 10 35.9%

Quebec $5,259,455 2 $5,336,962 2 $765 6 24.2%

Britis h Columbia $3,092,479 3 $3,155,568 3 $787 4 14.3%

Albe rta $2,540,264 4 $2,634,256 4 $772 5 11.9%

Manitoba $719,769 5 $752,882 5 $715 8 3.4%

S as katchewan $622,361 6 $641,069 6 $699 9 2.9%

Nova S cotia $591,729 7 $608,016 7 $750 7 2.8%

Newfoundland $443,165 8 $452,293 8 $997 3 2.0%

New Bruns wick $393,861 9 $410,390 9 $637 11 1.9%

P EI $70,155 10 $73,490 10 $594 12 0.3%

NWT $48,157 11 $49,239 11 $1,419 1 0.2%

Yukon $35,716 12 $36,149 12 $1,162 2 0.2%

Nunavut $5,370 13 $5,568 13 $221 13 0.0%

Canada $21,338,701 $22,081,961 $785 100%

Mr. Pali Bedi, President and CEO

Mr. Bedi has 22 years of experience in the controlled substance retail market having served as the Chief Executive Officer of Solo Liquor since 1996. Mr. Bedi was integral in growing Solo Liquor from 8 to 62 stores since 2010, which now sees over 20,000 customers per day in over 30

municipalities across Alberta. Mr. Bedi brings 30 years of commercial real estate experience and has been a Principal at Avison Young Real Estate Alberta for 18 years, specializing in retail development. Mr. Bedi has developed, leased and successfully sold in excess of 1.0 million square feet of retail, office and industrial real estate spanning five communities in Alberta throughout his career.

Mr. Jasbir “Jas” Hans, Vice President, Operations

Mr. Hans has served as the President of Solo Liquor since 1996, establishing 62 operating stores in 30 communities throughout Alberta. Mr. Hans has extensive experience in human resource management, the development and implementation of strategic direction and establishing

financial goals, budgets, corporate objectives and professional development.

Ms. Stephanie Bunch, CFO

Ms. Bunch is a Chartered Accountant with over 25 years industry experience with a focus on public company mergers and acquisitions and

capital markets. Ms. Bunch was the Vice President, Business Performance and Finance Lead, Mergers and Acquisitions of Centrica Energy (Direct Energy Marketing Limited) from 2013 to 2017 and the Chief Financial Officer and Vice President, Finance of Seaview Energy Inc., from 2006 to 2012. Prior to Seaview Energy Inc., Ms. Bunch held progressively senior roles including Controller, Acting CFO and Treasurer at Ketch

Energy Ltd., Acclaim Energy Trust and Canetic Resources Trust between 2000 and 2006. Beginning her career at a leading international accounting firm, KPMG LLP, Ms. Bunch has been directly involved in over $3 billion of public and private company mergers, acquisitions and

integrations throughout her career, from startups through to multi-national deals.

Mr. Sony Gill, Corporate Secretary

Mr. Gill is a partner at McCarthy Tétrault LLP, a national law firm. Mr. Gill has dealt with all aspects of a public and private company's creation, growth, restructuring and value maximization. Mr. Gill has extensive experience in the negotiation, structuring and consummation of a broad

range of corporate finance, securities and mergers and acquisitions. He serves on the board of directors of, and acts as corporate secretary to, numerous public and private companies. Mr. Gill was acknowledged as a Top 40 Under 40 by Lexpert.

Note: Solo Growth will see significant G&A savings as it will enter into a technical services agreement with Solo Liquor; pursuant to which it will be allocated G&A based on its build program

9

Execution - Management Team

Rick McHardyMr. McHardy has been a founder of several public companies and has extensive experience in leadership positions and over 20 years' experience in all aspects of securities and mergers and acquisitions. Mr. McHardy has been instrumental in a number of significant transactions including: (i) a founder and the President and Chief Executive Officer of Spartan Energy Corp. from December 10, 2013 to May 28, 2018 when it was acquired for

approximately $1.4 billion by Vermilion Energy Inc.; (ii) a founder and the President and Chief Executive Officer of Spartan Oil Corp. from March 2011 to January 2013 when it completed a business combination with Bonterra Energy Corp. for a total transaction value of approximately $480 million; (iii) a founder and the President and Chief Executive Officer of Spartan Exploration Ltd., from January 2008 to June 2011 when it completed

an arrangement with a public senior oil and gas company in a transaction valued at approximately $244 million; and (iv) a founder and the President of Titan Exploration Ltd. prior to its acquisition by Canetic Resources Trust for approximately $116 million. Mr. McHardy has served as corporate secretary for a number of public companies and was a partner at McCarthy Tétrault LLP, where he practiced securities and corporate law.

Ron HozjanMr. Hozjan has been Vice President, Finance and Chief Financial Officer of Tamarack Valley Energy Ltd. ("Tamarack"), a public company listed on the Toronto Stock Exchange, since 2010. Mr. Hozjan is a Chartered Professional Accountant with over 30 years of oil and gas experience and over 20

years of experience as a senior financial officer. Prior to Tamarack, Mr. Hozjan served as the Chief Financial Officer of Vaquero Resources Ltd., which was acquired by RMP Energy Ltd. Prior thereto, he was the Vice President, Finance and Chief Financial Officer at a predecessor firm, Vaquero Energy Ltd., which grew successfully before merging with Highpine Oil & Gas Limited. Previously, Ron held various senior finance positions at Storm Energy Ltd., Beau Canada Exploration Ltd. and Renaissance Energy Ltd.

Sonny MottahedMr. Mottahed is the co-founder and Chief Executive Officer of 51st Parallel Life Sciences Ltd. ("51st Parallel"), an Alberta-based, pre-production

applicant to become a licensed provider of cannabis focused on the recreational market. 51st Parallel has a strategic relationship and technical services agreement with LivWell Enlightened Health LLC, a vertically integrated cannabis company. Mr. Mottahed is also the President and Chief Financial Officer of Target Capital Inc. d.b.a. CBi2 Capital, a publicly listed company that develops and manages a diversified portfolio of predominantly early stage cannabis investment opportunities. Mr. Mottahed brings significant senior leadership and financial expertise to the

Canadian cannabis market. Mr. Mottahed is currently the Chief Executive Officer and Managing Partner of Black Spruce Merchant Capital, a corporate finance advisory firm based in Calgary. Prior thereto, Mr. Mottahed was the Managing Director, Investment Banking at Raymond James Ltd. in Calgary where he was instrumental in raising $4.0 billion in capital over 4 years.

10

Execution – Board of Directors

Michael StarkMr. Stark is an independent businessman and previously a certified financial planner. He was the Chairman of Spartan Energy Corp. from December 10, 2013 to May 28, 2018. Prior thereto, Mr. Stark was the Chairman of Spartan Oil Corp. from June 2011 to January 2013 and the Chairman of Spartan Exploration Ltd. from January 2008 to June 2011. Mr. Stark was also the Chairman of Titan Exploration Ltd. from August 2004 until December 2007. Mr. Stark has served on the audit committee of several public issuers.

James MillerMr. Miller is the President of Boarder Capital Inc., a commercial real estate focused private equity firm. Mr. Miller has over 25 years' experience in the investment and commercial real estate business, starting his career at CBRE Group where he achieved the title of Vice President and Top Producer very early in his career. Mr. Miller joined an international private equity fund from 1998 to 2002 focused on commercial and multi-residential real estate assets. During his time at the private equity fund, Mr. Miller assisted in redeveloping and repositioning value add assets throughout Canada and the United States. Mr. Miller has directly participated in over $1.5 billion worth of commercial real estate transactions including foreign, pension fund, REIT and private capital investments. Mr. Miller joined Avison Young in 2004 becoming "Top Producer of the Year" in 2005, 2006, 2007 and 2011. During his tenure with Avison Young, Mr. Miller led the Calgary Capital Markets Group, and was active as a senior leader of the company's national Capital Markets Group as well as sitting on the National Executive Committee.

11

Execution – Board of Directors

12

Execution - Corporate Success Factors

Location

Minimize New Build Costs

Low Employee Turnover

Priced Competitive & Profitably

Inventory Management

Store Hours

Same Store Result Must Deliver

The Alberta Gaming and Liquor Commission (“AGLC”)

ensures products are sold to retailer by distributors at

identical price

RELATIONSHIPS,CAPITAL AND OPERATIONAL EXCELLENCE A

MUST

Real Estate Expertise - Right Leases

Ca

pit

al

Allo

cati

on

Op

era

tio

na

l

Minimize Operational Costs

Ind

ust

ry

Re

lati

on

ship Regulators

Municipalities

Landlords

13

Execution – Operating Milestones

Year New Stores Communities

2018 3 – 5 1 – 3

2019 15 – 25 6 – 10

2020 25 – 30 15+

Total 60+ 15+

Execution - Case Study: Solo Liquor

14

Fort McMurrayGrande Prairie

Edmonton

Red Deer

Calgary

Lethbridge

Solo Growth's leadership team has, in aggregate, 50+ year history of successful expansion within the Alberta liquor market

• Solo Liquor was established in 1996. Since 2010, Solo Liquor has grown from 8 to 62 stores.

• Solo’s lower SG&A cost allows it to offer customers lower prices while still delivering a comparable EBITDA margin– Solo Liquor 12.9% SG&A vs. 20%+ of competitors

• ~350 average customers per store per day (20,000 total per day)

• Weekly management meetings to discuss financial and operational performance and inventory allocation

FY 2016 Solo LIQ RU M

G ross Profit 16 .9% 25.3% 24.2%

SG & A 12.9% 20.4% 23.7%

EB ITD A M argin 4.0% 4.9% 1.5%

Industry Performance Benchmark

Solo Liquor – Same Store EBITDA FY2017

FY 2017 EB ITD A

90% of stores open > 12 months generate positive EBITDA

15

Execution - Branding

Comparable Retail Focus Companies / Deals

16

Transaction Indicative Valuation Highlights

MedMen $50MM private placement & RTO transaction

C$1.0 Billion Retail Implied

C$2.1 Billion total value reduced by implied value of WEED

cultivation valuation(~$20,000 / kg/yr)

- Vertically integrated Cannabis company with ~50,000 kg/year cultivation capacity, ~6,000 kg/year extraction capacity & 20 retails locations in California, New York, Nevada & Massachusetts

- Projecting $110MM in 2018 retail revenue ($5.5MM / store)

Fire & Flowerrecent equityinvestments fromstrategic partners

C$50 Million

- Fire & Flower is a lifestyle branding company that has applied for 37 cannabis retail licenses in Alberta

- EMC acquired 5.0% equity for $2.5MM, TER acquired 5.0% equity for $2.5MM, MMJ Phytotech acquired 1.6% for $1.0MM

Aurora equity investment into Liquor Stores NA

C$84.5 Million Implied Value

Based on premium paid by Aurora ($15/sh.) to LIQ’s market price ($11.96/sh) to secure an equity

interest in LIQ

- LIQ is the largest liquor store retailer in Canada with stores in Alberta, B.C. and Saskatchewan, as well as in Alaska

- ACB subscribed to 8.2mm (~20%) shares and sub. receipts at a price of $15.00 (24% prem.) and will receive 12mm in warrants exercisable at $15.00-$15.75 per share (additional ~20%)

C$280 Million

- Vertically integrated cannabis company focused on the production, branding and retail distribution of cannabis and related products

- Brands include DOJA, Tokyo Smoke, Van der Pop and Maitri - 2 indoor cannabis production facilities in Kelowna (5,160 Kg/yr)- Hiku operates 7 retail cafes in Canada (5 in ON; 1 in AB & B.C.)

Market OpportunityCanadian retail cannabis market projected to be $4.9B to $8.7B. Inferred Alberta market size is $811M to $1.1B.

Favorable demographics in Alberta suggest significant adoption and above average usage.

Track RecordMore than 50 years of regulated substances retail experience.

Proven operational excellence.

Robust customer analytics.

Strong, collaborative and constructive relationships.

Milestones2018 – Open 3 - 5 stores, Operating in 1 -3 communities across Alberta (subject to date of legalization).

2019 – Open 15 - 25 stores, Operating more than 18 locations across 6-10 communities in Alberta.

2020 – Open 25 - 30 stores, Operating more than 50 locations across more than 15 communities in Alberta.

17

Conclusion

This presentation does not constitute an offer to sell or solicitation of an offer to buy any of the securities described herein. The sole purposeof this presentation, in paper or electronic form, is strictly for information purposes. Neither Aldershot Resources Ltd. d.b.a. “Solo GrowthCorp.” (“Solo” or the “Company”) nor any of its current or proposed directors, officers, owners, managers, partners, consultants, employees,affiliates or representatives, make any warranty or representation, whether express or implied, or assume any legal liability or responsibilityfor any action taken in reliance upon this presentation, or for the accuracy, completeness, or usefulness of any information disclosed,includinganypro-forma financial statements included in this presentation.

Forward Looking Statements. Certain information included in this presentation constitutes forward-looking information under applicablesecurities legislation. Forward-looking information typically contains statements with words such as “will”, “anticipate”, “believe”, “expect”,“plan”, “intend”, “estimate”, “propose” or similar words suggesting future outcomes or statements regarding an outlook. Forward-lookinginformation in this presentation includes, but is not limited to, statements relating to: Solo’s business, strategies, expectations, plannedoperations or future actions, including future retail cannabis locations; the performance of the Company’s business and operations; thecompetitive conditions of the industry in which the Company operates and the competitive advantages of the Company; and the Company’sfutureproduct offerings.

The forward-looking statements contained in this presentationarebasedoncertain key expectations andassumptionsmadeby Solo, includingexpectations and assumptions concerning: the availability of sufficient capital; the availability of and access to qualified personnel; Solo’sability to protect its intellectual property; the expected growth in the cannabis market; themedical benefits, viability, safety, efficacy, dosingand social acceptance of cannabis; the securities markets and the general economy; the legalization of cannabis for adult-use in Canada,including federal and provincial regulations pertaining thereto and the timing related thereof and the Company’s intentions to participate insuchmarket, if andwhen legalized; the legalization of the use of cannabis for medical and/or adult use in jurisdictions outside of Canada; andapplicable lawsnot changing inamanner that is unfavorable toSolo.

Although Solo believes that the expectations and assumptions on which the forward-looking statements are based are reasonable, unduereliance should not be placed on the forward-looking statements because Solo can give no assurance that they will prove to be correct. Sinceforward-looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties. Actualresults coulddiffermaterially fromthose currently anticipateddue toanumber of factors and risks. These include, but are not limited to, risksassociated with the cannabis industry in general; actions and initiatives of federal and provincial governments and changes to governmentpolicies and the execution and impact of these actions, initiatives and policies, including the fact that adult-use cannabis is currently illegalunder federal and provincial law; import/export restrictions for cannabinoid-based operations; the size of the medical-use and adult-usecannabismarket; andcompetition fromother industry participants.

18

Disclaimers

Forward Looking Statements (continued). Readers are cautioned that the assumptions used in the preparation of forward-lookinginformation, although considered reasonable at the time of preparation, may prove to be imprecise. Solo’s actual results, performance orachievement could differ materially fromthose expressed in, or implied by, these forward-looking statements and accordingly there can be noassurance that such expectations will be realized and/or what benefits Solo will derive therefrom. The forward-looking information containedin this presentation is made as of the date hereof and Solo undertakes no obligation to update or revise any forward-looking information,whether as a result of new information, future events or otherwise, unless required by applicable securities laws. The forward lookinginformation contained in this presentation is expressly qualified by this cautionary statement.

Certain information contained herein has been obtained from published sources prepared by independent industry analysts and third-partysources (including industry publications, surveys and forecasts). While such information is believed to be reliable for the purpose used herein,none of the directors, officers, owners, managers, partners, consultants, shareholders, employees, affiliates or representatives assumes anyresponsibility for the accuracy of such information. None of the sources cited in this presentation have consented to the inclusion of any datafromtheir reports, nor has Solo sought their consent.

FOFI Disclosure. This presentation contains future-oriented financial information and financial outlook information (collectively, “FOFI”) aboutSolo’s prospective retail locations, revenue, expenses, profit and components thereof, all of which are subject to the same assumptions, riskfactors, limitations and qualifications as set forth in the above paragraphs. FOFI contained in this presentation was made as of the date of thispresentation and was provided for the purpose of providing further information about Solo’s anticipated future business operations. Solodisclaims any intention or obligation to update or revise any FOFI contained in this presentation, whether as a result of new information,future events or otherwise, unless required pursuant to applicable law. Readers are cautioned that the FOFI contained in this presentationshould not be used for purposes other than for which it is disclosed herein.

U.S. Registration. This presentation is not an offer of the securities for sale in the United States. The securities have not been registered underthe U.S. Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an exemption fromregistration. This presentation shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of thesecurities in any state in which such offer, solicitation or sale would be unlawful.

19

Disclaimers (continued)