SOLAR PV INDUSTRY JOBS REPORT - SAPVIA

27

APRIL 2021 SOLAR PV INDUSTRY JOBS REPORT PREPARED FOR South African PV Industry Association Eastgate Office Park, Block A South Boulevard Road | Bruma Johannesburg | 2198 | South Africa Office: +27(0)11 553 7264 SUBMITTED BY Ruan Fourie Energy Economist | Energy Industry Energy Centre | Smart Places | CSIR PO Box 395, Pretoria | 0001

Transcript of SOLAR PV INDUSTRY JOBS REPORT - SAPVIA

APRIL 2021

SOLAR PV INDUSTRY JOBS REPORT

PREPARED FOR South African PV Industry Association

Eastgate Office Park, Block ASouth Boulevard Road | Bruma

Johannesburg | 2198 | South AfricaOffice: +27(0)11 553 7264

SUBMITTED BY Ruan Fourie

Energy Economist | Energy IndustryEnergy Centre | Smart Places | CSIR

PO Box 395, Pretoria | 0001

PROUDLY SPONSORED BY:

LITERATURE REVIEW

ISSUING ORGANISATION: .........................................................................Council for Scientific and Industrial Research (CSIR)

Energy Centre

Smart Places

PO Box 395

Pretoria 0001

CONTRACT NAME: .........................................................................................CONSULTING AGREEMENT

SAPVIA SOLAR PV INDUSTRY JOBS REPORT

CONTACT DETAILS:........................................................................................ SAPVIA

Eastgate Office Park, Block A

South Boulevard Road, Bruma

Johannesburg

2198

South Africa

Office: +27(0)11 553 7264

APPROVED BY:

Responsibility Name Signature

Project Leader Ruan Fourie

Research Group leaders (Energy Systems)

Crescent Mushwana

Dr Brian North

Centre Manager Dr. Clinton Carter-Brown

Client representative Frank Spencer

DOCUMENT CONTROL

ISSUING ORGANISATION: .........................................................................Council for Scientific and Industrial Research (CSIR)

Energy Centre

Smart Places

PO Box 395

Pretoria 0001

Contract Name: ................................................................................................CONSULTING AGREEMENT

SAPVIA SOLAR PV INDUSTRY JOBS REPORT

Contact Details: SAPVIA

Eastgate Office Park, Block A

South Boulevard Road, Bruma

Johannesburg

2198

South Africa

Office: +27(0)11 553 7264

APPROVED BY:

Responsibility Name Signature

Project Leader Ruan Fourie

Research Group leader (Energy Systems) Crescent Mushwana

Centre Manager Dr. Clinton Carter-Brown

Client representative Frank Spencer

PROUDLY SPONSORED BY:

3

DOCUMENT CONTROL

ISSUING ORGANISATION: .........................................................................Council for Scientific and Industrial Research (CSIR)

Energy Centre

Smart Places

PO Box 395

Pretoria 0001

Contract Name: ................................................................................................CONSULTING AGREEMENT

SAPVIA SOLAR PV INDUSTRY JOBS REPORT

Contact Details: SAPVIA

Eastgate Office Park, Block A

South Boulevard Road, Bruma

Johannesburg

2198

South Africa

Office: +27(0)11 553 7264

APPROVED BY:

Responsibility Name Signature

Project Leader Ruan Fourie

Research Group leader (Energy Systems) Crescent Mushwana

Centre Manager Dr. Clinton Carter-Brown

Client representative Frank Spencer

PROUDLY SPONSORED BY:

3

DOCUMENT CONTROL

ISSUING ORGANISATION: .........................................................................Council for Scientific and Industrial Research (CSIR)

Energy Centre

Smart Places

PO Box 395

Pretoria 0001

Contract Name: ................................................................................................CONSULTING AGREEMENT

SAPVIA SOLAR PV INDUSTRY JOBS REPORT

Contact Details: SAPVIA

Eastgate Office Park, Block A

South Boulevard Road, Bruma

Johannesburg

2198

South Africa

Office: +27(0)11 553 7264

APPROVED BY:

Responsibility Name Signature

Project Leader Ruan Fourie

Research Group leader (Energy Systems) Crescent Mushwana

Centre Manager Dr. Clinton Carter-Brown

Client representative Frank Spencer

PROUDLY SPONSORED BY:

3

DOCUMENT CONTROL

ISSUING ORGANISATION: .........................................................................Council for Scientific and Industrial Research (CSIR)

Energy Centre

Smart Places

PO Box 395

Pretoria 0001

Contract Name: ................................................................................................CONSULTING AGREEMENT

SAPVIA SOLAR PV INDUSTRY JOBS REPORT

Contact Details: SAPVIA

Eastgate Office Park, Block A

South Boulevard Road, Bruma

Johannesburg

2198

South Africa

Office: +27(0)11 553 7264

APPROVED BY:

Responsibility Name Signature

Project Leader Ruan Fourie

Research Group leader (Energy Systems) Dr Brian North

Centre Manager Dr. Clinton Carter-Brown

Client representative Frank Spencer

PROUDLY SPONSORED BY:

5

TABLE OF CONTENTS1. Introduction ........................................................................................................................................................................................................................8

2. The Jobs Definition Conundrum................................................................................................................................................................................82.1. Background .................................................................................................................................................................................................................8

2.1.1. Green jobs as defined by the International Labour Organisation (ILO) ..................................................................................82.2. Job-years/full time equivalent (FTE) jobs ................................................................................................................................................... 92.3. Direct, indirect and induced jobs ...................................................................................................................................................................102.4. Jobs per standardised unit output .................................................................................................................................................................11

3. Global Solar PV Jobs Overview ................................................................................................................................................................................113.1. Renewable Energy and Jobs – Annual Review 2018/2019 (IRENA) ..................................................................................................113.2. Forecasting job creation from renewable energy deployment through a value-chain approach

(University of Zaragoza) ............................................................................................................................................................................................ 123.3. Job creation potential and skill requirements (Masdar Institute of Science and Technology) ........................................... 12

4. Solar PV Jobs Global Leading Markets (Case Studies) ................................................................................................................................ 134.1. Background .............................................................................................................................................................................................................. 134.2. Regional off grid solar prospects .................................................................................................................................................................. 134.3. China .......................................................................................................................................................................................................................... 134.4. Brazil ..........................................................................................................................................................................................................................144.5. United States ..........................................................................................................................................................................................................144.6. India ...........................................................................................................................................................................................................................144.7. Japan ..........................................................................................................................................................................................................................14

5. South African Solar PV Jobs Overview ...............................................................................................................................................................145.1. Photovoltaic Electricity: Localisation study ............................................................................................................................................... 155.2. Co-benefits job creation through renewable

energy in South Africa ................................................................................................................................................................................................165.3. South African employment potential estimation....................................................................................................................................16

6. Conclusions ...................................................................................................................................................................................................................... 17

Figures and Tables ...............................................................................................................................................................................................................18

References ..............................................................................................................................................................................................................................25

LIST OF TABLESTable 1: Stages that influence solar PV employment [12] .........................................................................................................................................20Table 2: Involved FTE jobs for the commissioning of a 1MWp PV facility in 2010 [9] .................................................................................20Table 3: Total full time direct jobs as per model results [9] .......................................................................................................................................21Table 4: Solar PV value chain employment factor summary from survey responses [13] ..........................................................................21Table 5: Job creation from several renewable energy technologies ....................................................................................................................22

LIST OF FIGURESFigure 1: Global Solar PV Installed Capacity [1] ...............................................................................................................................................................18Figure 2: South African Solar PV Installed Capacity (GW) [1] ..................................................................................................................................18Figure 3: Direct, Indirect and Induced Jobs[9] ................................................................................................................................................................19Figure 4: Global Employment by renewable energy technologies (IRENA, 2018; IRENA, 2019). ...........................................................19Figure 5: 2019 Chinese solar PV Jobs .................................................................................................................................................................................22Figure 6: Estimates of total and average number of FTE jobs created along the South African PV

industry value chain (2007, 2010, and 2020) ...............................................................................................................................................................23Figure 7: Forecasted Cumulative job years created during the construction phase in wind and solar PV

between the year 2018 and 2030 ..........................................................................................................................................................................................23Figure 8: Forecasted evolution of net employment in the power sector by the different technologies

(direct jobs) ..................................................................................................................................................................................................................................24

LIST OF ABBREVIATIONSCIM Construction, Installation and Manufacturing

CSIR Council for Scientific and Industrial Research

DBSA Development Bank of Southern Africa

DEFF Department of Environmental Affairs,

Fisheries and Forestry

DMRE Department of Mineral Resources

and Energy

DRE Decentralised Renewable Energy

EPC Engineering, Procurement and Construction

GW Gigawatt

GWh Gigawatt hour

IO Input-Output

IPPO Independent Power Producers Office

ILO International Labour Organisation

IRENA International Renewable Energy Agency

MW Megawatt

NREL National Renewable Energy Laboratory

O&M Operations and Maintenance

PAYG Pay-as-you-go

PV Photovoltaic

RE Renewable Energy

REI4P Renewable Energy Independent Power

Producers Procurement Program

SAPVIA South African Photovoltaic Industry

Association

SHS Solar Home System

SSEG Small-Scale Embedded GenerationUCT University of Cape Town

1 INTRODUCTION

Global installed renewable energy (RE) power generation capacity grew more than 170 GW in 2019 (mostly solar PV) to 2 532 GW [1]. For the fifth year in a row, net additions of RE power generation capacity clearly outpaced net installations of fossil fuel and nuclear power generation capacity combined. Global solar PV installations grew from 481 GW in 2018 to 579 GW in 2019, an increase of 98 GW [1], see Figure 1.

China was the global leader in new solar PV technology installations followed by the United States, India and Japan. Solar PV is clearly the global leader in new RE power sector generation development contributing 57,5% of total new RE generation capacity additions.

In contrast, South Africa has seen inconsistent growth over the last decade due to policy uncertainty, see Figure 2 for South African solar PV installed capacity evolution.

The inconsistent procurement of solar PV has seen variability in employment creation in the sector as local companies struggle to invest in a market with inconsistent demand for solar PV. Understanding the reason and implications of this variability in the market requires a brief overview of the market itself.

The solar PV market is divided in two market segments: utility and embedded generation. The latter spans residential, commercial and industrial applications and is often referred to as small scale embedded generation (SSEG), while the former mostly covers large utility scale ground mounted installations feeding power directly into the grid. Recent times have seen the introduction of ground mounted installations in the commercial and industrial space.

Job creation is a significant component of the socio-economic effects related to RE development in South Africa. The deployment of solar PV, in the utility and SSEG markets has created jobs for the South African economy as a whole.

The likely continued contribution of the solar PV industry in creating new jobs supports public policy and the allocation towards solar PV generation in the country’s Integrated Resource Plan (IRP). This literature review will cover the following aspects of jobs emanating from the solar PV sector:

n Analyzing the jobs definition conundrumn Global solar PV jobs research overview n Case Studies – solar PV jobs research overview in

various countriesn South African solar PV jobs research overview

The literature reviewed in the report identifies the number of jobs created as well as the chosen metric used to report said job numbers.

The literature review concludes with recommendations on what the best metrics are to report real job numbers as well as highlighting the results of the countries that report annual job numbers in the solar PV domain.

2 THE JOBS DEFINITION CONUNDRUM

2.1 BACKGROUND

The impact of RE jobs in South Africa is a complex issue that is highly contested by various groups in the country. It is essential to reach a common understanding of how jobs numbers are reported, although there are several studies conducted on this topic. These studies are investigated in this report and analyses work completed by the International Renewable Energy Agency (IRENA), International Labour Organisation (ILO), University of Zaragoza, CSIR and the University of Cape Town (UCT).

The uncertainty associated with selecting a consistent jobs metric to use creates confusion when reporting and engaging stakeholders on the number of jobs created by a technology in the South African power sector. A wide range of definitions of employment generated by energy sector activities have been proposed and a variety of methods have been used to construct such estimates. This study provides a comparison of how different countries or studies are using employment figures or how they arrive at certain estimates of jobs created by a specific technology deployment such as solar PV.

This section focuses on describing various approaches used in estimating employment created in the RE sector. The section will outline the following concepts:

n Job-years/full time equivalent (FTE) jobsn Direct, indirect and induced jobsn Jobs per standardised unit output

2.1.1 GREEN JOBS AS DEFINED BY THE INTERNATIONAL LABOUR ORGANISATION (ILO)

Green jobs are defined as jobs that help reduce the overall negative environmental impact, in the long run leading to environmentally, economically and socially sustainable enterprises and economies. Green jobs are decent jobs, which protect and restore ecosystems through reducing energy consumption and resources utilised, thus limiting the production carbon footprint and waste [2]. The Skills for Green Jobs: South Africa study by ILO [2] shows that the private sector stakeholder

plays a critical role in greening the economy, especially in terms of innovation and job creation opportunities. Moreover, job creation opportunities are central in the South African low carbon and climate-resilient growth path. The creation of green jobs is an important part of adopting solar PV and other RE technologies, it is also a key component of the Just Energy Transition. The South African Department of Environment, Forestry and Fisheries (DEFF) identified four areas that can create and promote green jobs [2]:[2]

n Development and growth of new green sectors and industries;

n Retrofitting industrial efficiency processes and clean production technologies in existing sectors and industries;

n Growing existing GE sectors such as renewable energy, waste recycling and biodiversity;

n Incentivising and accelerating private and public-sector investment in restoring critical ecosystem services and land productivity, water conservation, wetland rehabilitation and fire management.

These are some of the areas that can contribute to creating green jobs as identified by DEFF. Small and Medium Enterprises (SMEs) have a significant role to play in the country’s development objectives due to the economic impact they have in the South African Gross Domestic Product (GDP). SMEs created about 14% of employment opportunities which translates to approximately 42% economic contribution towards the GDP[2]. The prospects of SMEs in creating jobs in the energy value chain is minimal since most of them do not have the technical capacity in technologies like solar and wind [2]. Efforts to increase the labour absorption in various economic sectors (with the green economy receiving particular attention) have been undertaken since 2011.

The green economy is complex, extremely diverse and rapidly growing in many of its segments, particularly in an economy such as South Africa’s. The country will essentially be dealing with the progressive and simultaneous introduction of technologies that are either being improved, developed or commercialised. The economic merit of many of these technologies may only be fully established in years to come, opening up opportunities for the establishment of infant industries over time [3]. According to [3], the green economy sector has the potential to create approximately 98 000 new direct jobs on average in the short term, almost 255 000 in the medium term and around 462 000 employment opportunities in the formal economy in the long term.

2.2. JOB-YEARS/FULL TIME EQUIVALENT (FTE) JOBS

The reporting of job numbers in a standardised format is required due to the variable duration of different job opportunities created in the solar PV value chain. Construction, installation and manufacturing (CIM) jobs generally fall within one year while operation and maintenance (O&M) jobs span the lifetime of the plant and O&M jobs are generally lower than CIM jobs in the RE sector. Furthermore, some O&M jobs tend to periodically employ individuals which leads to underreporting of job numbers. Defining the different metrics currently used when reporting job numbers is critically important when undertaking a study that aims to collect and forecast job numbers for a specific technology.

The terms job-years or full-time equivalent (FTE) are often used loosely and are often misinterpreted as meaning the number of persons employed. The section that follows provides an elaboration into job-years and FTE metrics and how they are derived.

FULL TIME EQUIVALENT (FTE)

According to the ILO definition [4], an FTE job, “is a unit to measure employed persons in a way that makes them comparable although they may work a different number of hours per week”.

The FTE unit is obtained by comparing an employee's average number of hours worked to the average number of hours of a full-time worker. A full-time worker is therefore counted as one FTE, while a part-time worker gets a score in proportion to the hours he or she works.

This is a good way of measuring employment and is used to express the size of the workforce of an enterprise, activity or country. This metrics proves useful in cross value chain jobs assessments as part time employees can be standardised to annual FTE job numbers.

JOB-YEAR

The CSIR was unable to source a document from a reputable organisation that defines job-year apart from a document released by the United States Executive Office of the President Council of Economic Advisers. This document defines a job-year as one job for one year [5].

The lack of a reputable referenced document that clearly defines what a job year is, creates uncertainty around the metric itself and whether it would be prudent to use this metric in an analysis undertaken in the rest of this study.

98

The CSIR outlined its understanding on what a job-year is based on how this metric has been used in reporting jobs numbers in other reports. A job-year refers to a job that exists for a consecutive 40 hour per week for an undisturbed period of 12 months.

The concept of job-years becomes important when accounting for jobs created during the construction phase (18 to 24-month period) and O&M (20 years) phases of a typical lifetime of a solar PV (or other power generation) project. This enables comparison of jobs on a like for like basis. This metric format allows the user to specify how many people are employed in a specific year, which requires appropriate treatment of full-time and part-time jobs and the duration of activities that are time-bounded.

While others may argue that this is the best way to account for jobs created and supported by the industry others lean more towards accounting for jobs per energy concept without splitting the construction and O&M jobs.

EXAMPLES OF JOB-YEAR CALCULATIONS

If a job exists for 3 months employing one person, it is a quarter of a job-year, and therefore it would take four 3-month-long jobs to make one job-year or FTE. If a job exists for two years, it counts as two job-years.

So, in a 3-month example, if a road maintenance contract (for example) employs 100 people on a 3-month contract, that contract is actually creating 25 job-years, whereas a two-year project employing 100 people for a full period of 2 years is actually creating 200 job-years. So even though both projects were employing 100 people each, the actual number of job-years created is 225.

DIFFERENT APPROACHES TO BUILDING UP JOBS METRICS

According to World Bank (2011) [6] the time dimension of a job has to be fully articulated before aggregating employment created from different parts of a project or policy. A job is usually defined in terms of the number of job-years attached to the employment. This depends on how much time in each year a job is paid for (how long in a year does the person get paid for), and for how many years the job exists. Part-time jobs are converted to FTEs and then scaled by the number of years for which that particular job is required (e.g. construction for a few years, maintenance for several years).

Some studies have calculated the total number of job-years created over the lifetime of the project, which was the method initially used by the Independent Power Producers Office (IPPO) report [7] when reporting on

jobs, especially O&M jobs, which makes the number appear inflated if the basis for the definitions and calculations are not understood.

The World Bank references another report [8] published in Energy Policy journal which suggests that in order to compare different projects with different lifetimes, it is best to divide the total number of job-years created by the lifetime of the project to arrive at an annual equivalent. This means that the sector would then report on jobs per annum, rather than total job-years over the lifetime of the project, which can be misinterpreted. It should be noted that no single metric is likely to capture all the nuance of the job volumes and timing created over a project lifetime. Furthermore, the comparison metric numbers observed from different sources can only be meaningful to the extent that the same definitions and philosophies have been applied in calculating the numbers.

2.3. DIRECT, INDIRECT AND INDUCED JOBS

In addition to job-years and FTEs, there is the concept of direct, indirect and induced jobs [6]. This is explained further in the context of solar PV projects.

n Direct jobs are jobs created by the direct suppliers of solar PV projects (e.g. design, development, management, construction/installation, and maintenance phase of the project).

n Indirect jobs are jobs within the value chain of the direct suppliers to the project (e.g. the construction equipment manufacturers). The total employment created as the solar PV sector expands its outputs in order to supply the inputs required for the output of the solar PV sector. For example, the manufacture of glass or aluminium frames to supply solar PV manufacturer creates indirect employment.

n Induced jobs are created as a result of workers (directly and indirectly employed by the project value chains) spending earnings within the economy. These may include the jobs created or sustained in the hospitality sector in the Northern Cape as workers require accommodation, food and transport for the duration of the construction of solar plants.

The industry reports job numbers based on the industry codes specified by StatsSA for specific projects at a site. However, the job numbers collected in this way do not account for the indirect and induced jobs. Therefore, in order to account for indirect and induced jobs, additional information has to be collected from the industries impacted the new power generation project/facility. The job numbers reported by industry are assumed to be only representing new jobs created

by a project, and they do not account for the ripple effect that a project development like solar PV has on the rest of the economy. Within the solar PV market, direct jobs are those created by firms that are directly focused on solar PV project execution: solar developers, engineering, procurement and construction (EPC) firms, and solar PV component manufacturers.

In contrast, indirect jobs are created by businesses that are in the second tier of the solar PV industry value chain, such as suppliers of materials for manufacturing (such as glass), electricity suppliers, and public officers who deal with administration and finance. Figure 3 illustrates the examples of direct, indirect and induced effects of the solar PV industry.

Furthermore, it should be noted that indirect and induced jobs are normally sustained or supported jobs. This means that, for instance, for a logistics company to secure business in the solar PV sector for transportation of equipment and materials to site, they sustain their business and they manage to keep the people employed. These may not be new jobs created specifically for the solar PV industry but rather sustained jobs which enables the economy to maintain jobs that would have otherwise been lost if the logistics company did not have a pipeline of business to keep people employed.

While the method for defining different forms of jobs creation are mostly aligned across the globe to direct, indirect and induced effects, reporting is dependent on the ability of the industry to track and report on their numbers in such a manner. Further limitations include the fact that it is difficult to track indirect and especially induced job impacts as many of these business do not relate their activity to a specific technology.

2.4. JOBS PER STANDARDISED UNIT OUTPUT

When reporting and comparing jobs numbers in the energy value chain, it is important to make sure that job numbers across technologies/value chains use the same output metric. The previous 2 sections summarised metric options that provide a starting point on reporting job numbers. The issue with these metrics are that they do not allow for easy comparisons to be drawn across technology options with varying outputs and installed capacities.

In order to compare different technologies, or even value chain segments of technologies, one requires a unit output measurement. One potential approach is that the technologies are compared on employment (average job-years/FTE) per unit of energy output which would be defined as gigawatt-hours (GWh) of electricity generated per year.

Another approach is to assess employment per unit of capacity such as megawatt (MW), but a distinction must be made between the nameplate capacity of the plant (peak MW) and the expected capacity utilization of the plant (average MW). Because of the large variation in capacity factors between alternative technologies, the number of jobs created to produce a given number of GWh per year may vary substantially between technologies, while the cost for the same annual GWh will increase with reducing capacity factor of a plant. Employment would not decrease as the capacity factor of a specific plant reduces over time and as such the jobs/installed capacity would be a method for compensating for this inaccuracy. Therefore, for the purposes of this analysis, the metric that is most suitable is FTE jobs/MW/annum.

The South African RE market has not tracked real job creation in a standardised method that is publicly available apart from the IPPO process. This information is unfortunately not broken down to each value chain segment and the methodology by which this data is collected has also not been shared.

3. GLOBAL SOLAR PV JOBS OVERVIEW

3.1. RENEWABLE ENERGY AND JOBS – ANNUAL REVIEW 2018/2019 (IRENA)

The IRENA annual review does not quote the metric used to report job number nor the employment ratios1 used in calculating final figures. Technologies such as solar PV have a direct impact on jobs created through the production and installation of the solar cells and panels. The falling costs of RE technologies continue to drive the deployment of solar PV. According to the IRENA Annual Review, international RE employment reached 10.9 million jobs in 2017, a 5.3% increase compared with the previous year [10]. The jobs created in 2018 increased by 7% on 2016 levels, reaching a record high of 11 million jobs.

The international solar PV sector had 3.4 million jobs in 2017, representing a total installation of 94 GW, which is a 23% increase from the previous year. Figure 4 shows that in 2018 the jobs created in the solar PV sector grew to 3.6 million. The IRENA reports do not provide a metric used in reporting this information, which could be attributed to the misaligned approaches of large amounts of data that they are collecting across the globe.

1110

1 Employment ratio refers to the proportion of jobs created per unit of installed power throughout the solar PV value chain

Many countries derive socio-economic benefits from RE, but most of the employment benefits remain highly concentrated in countries such as China, Brazil, the United States, India, Germany and Japan with these countries having significant proportions of the manufacturing of solar energy components.

These benefits are created across the solar PV value chain. The overall employment numbers in 2018 increased in China and India, while South Africa, the United States, Japan and the European Union lost jobs in the RE sector. The main causes for these decreases can be attributed to political and policy changes within these nations. The employment outlook is shaped by a wide range of technical, economic and policy-driven factors.

Furthermore, the analysis takes an overall technology view in reporting the number of jobs created and does not delineate between different parts of the technology value chains. This extends from component design and manufacturing by O&M through to assembling, installation and commissioning/monitoring. As such the CSIR continued its literature review with the aim of identifying methods used internationally to capture and report on real job numbers collected across the value chain of solar PV.

3.2. FORECASTING JOB CREATION FROM RENEWABLE ENERGY DEPLOYMENT THROUGH A VALUE-CHAIN APPROACH

In 2013, the team at the University of Zaragoza in Spain identified the same issue outlined in the previous section and set out to develop a methodology to capture real data across the RE technologies value chains. The method proposed is based on the collection, critical analysis and presentation of the results obtained using primary information sources. The main focus for reviewing this literature is to draw insights from the methodology rather than the results as the data is dated.

The study states that quantifying total jobs involved in the deployment of solar PV and other RE technologies can give varying results as technology deployment differs across off-grid, grid-connected, ground or rooftop-mounted PV [12].

These differences are caused by varying labour intensity of each stage in the solar PV value chain for different applications and scale. Jobs and employment characteristics are different depending on the nature of the projects.

Table 1 shows the various categories of jobs created across the solar PV value chain and provides details regarding their stability, level of specialisation and volumes.

For example, construction and installation, and dismantling, creates more jobs, but for a shorter period of time. Most stable jobs are generated in categories 1, 2 and 4, however, they are mainly located where the actual manufacturing takes place. However, construction and O&M employment opportunities are not dependent on the component manufacturing location.

The Zaragoza study continues by developing specific metrics for a 1MWp facility across the PV value chain. The metrics used in their assessment is Jobs/MW as seen in Table 2. The study added another layer of complexity by including the professional level2 of the type of job.

The study concludes by using these metrics to calculate the number of jobs created by the Spanish PV industry between 2001 and 2010 based on the MW installed. Results can be seen in Table 3 above. Results were aggregated to differentiate between manufacturing, installation and O&M jobs and provides a breakdown of jobs created across the PV value chain that cannot be viewed in the IRENA reports.

3.3. JOB CREATION POTENTIAL & SKILLS REQUIREMENTS

The Masdar Institute of Science and Technology in the United Arab Emirates conducted a similar study [13] to that of the University of Zaragoza with the aim of quantifying job creation potential of RE across their respective value chains. This study builds on the “jobs per unit measure of energy” principle by conducting interviews and surveys with key industry stakeholders to obtain the required metrics across different technology value chains.

This study, at the start, applied a high-level approach which provides simplicity that is not provided by classic input-output (IO) models when estimating job impacts, since analytical models generally ignore jobs that are less indirectly associated with an industry.

As such the results are likely to under-report overall employment impacts [14]. Such more concise models often use employment factors illustrated in Table 4 from interviews or questionnaires from industry partners to link RE technology diffusion employment estimations. Interview specifics are used to develop job intensities or employment factors, defined as the number of jobs derived from a certain RE technology investment or capacity. The metrics listed in the table below differ in their energy units and employment type grouping as the survey allowed respondents to reply on their own chosen energy unit.

Lastly, the study shows that a variable that needs to be considered is the degree of development in the solar PV sector and above all the maturity of the technology considered from the industrial development prospects. The study used a learning rate to artificially increase the number of real jobs created over time.

4. SOLAR PV JOBS3 GLOBAL LEADING MARKETS (CASE STUDIES)

4.1. BACKGROUND

The case studies in this section have been primarily adopted from the IRENA Renewable Energy and Jobs Annual Review [10] with supplementary sources from other reports . The case studies below will provide insights into the number of jobs created as well as recent trends in various nations, however, it will not speak to the metrics used as IRENA does not define the metric they employ nor the methodology in gathering said information in their studies. This is indicative of a global challenge in quantifying job numbers in the RE sector.

4.2. REGIONAL OFF GRID SOLAR PROSPECTS

Solar PV will continue to play an important role in improving energy access. The global renewable off- grid capacity more than doubled in the past decade to 8.8 GW in 2018; off-grid solar PV expanded 10-fold to 2.9 GW [10]. In South Asia, public sector programmes have had a strong role in improving energy access. On the contrary, private sector “Pay-as-you-go” (PAYG) business models are common in Sub-Saharan Africa. Investment in private off-grid projects grew from $10 million in 2010 to $511.5 million in 2018, accounting for a cumulative investment of $ 1.7 billion over that period.

Businesses operating under the PAYG model played a significant role in growing jobs created in developing countries. A recent case study known as “BBOXX’s” in the Democratic Republic of Congo’s “Energie pour Tous” rural electrification initiative intended to provide energy access through solar home systems (SHS) and mini-grids to 2.5 million people by 2020 projected nearly 10 000 jobs that could be created through solar PV deployment.

According to [15], approximately 80% of global investments in off-grid solar PV projects were in Sub-Saharan Africa, while 15% in South Asia and 5% in Latin America. A group of key participating firms, including Zola, M-KOPA, d.light, Mobisol, BBOXX, and others, secured two-thirds of the total investment. The solar PV

sector created jobs in distributed off-grid installations. Information remains relatively scarce on the full employment impacts of off-grid renewable projects.

However, a total of 130 million off-grid solar lanterns, SHS, and other products had been sold worldwide by 2017. Over 40 companies that participated in the survey conducted by [16] projected off-grid solar employment in parts of Sub-Saharan Africa and South Asia at 372 000 FTE jobs. Almost 56% of these jobs are in rural areas and 27% are occupied by women. This estimate is comprised of sales and distribution, installation and maintenance, and customer support. According to IRENA (2019), “Power for All” launched an annual jobs census on the decentralised renewable energy (DRE) sector in low-energy access countries.

This census involves a wide range of solar technologies. Originally the project focused on Kenya, India and Nigeria, however, the geographic scope will broaden to 10 countries in 2019 and 25 in 2020. The study examines approximately 150 DRE businesses and conducts focus group discussions with stakeholders from government, skills development and training sector, civil society, finance, and industry.

The research analysis, which is still pending, is set to yield valuable insights on total DRE employment permanency of jobs, levels of compensation, current skills demand, recruitment challenges, and gender and youth representation.

The study maps areas of indirect employment impacts in upstream activities such as equipment suppliers, or service providers such as training and education [10].

4.3. CHINA

China remains the clear leader in renewable energy employment worldwide, accounting for 39% of the world’s total RE jobs. Overall, a drop in solar PV from 2.216 million jobs to 2.194 million has been recorded in 2019. This is due to a notice by the government of China that it was suspending advantageous arrangements for utility-scale solar, imposing a cap on subsidised distributed solar, and reducing feed-in-tariffs in response to continuous growth in solar subsidies. Subsidies had grown largely because the authority that approves solar farms was delegated to the local level in 2013, making policy coordination difficult. China installed 43 GW of solar PV in 2018, which is an 18% decline as compared to 2017. Rooftop solar PV saw gains, although utility-scale deployment dropped significantly.

Largely, the production of solar PV modules grew by 21% in 2018 to 87 GW, however, significant overcapacities in the supply chain led to some factory

1312

2 The authors do not provide a detailed description of what professional level jobs entail

3 The solar PV jobs consulted in this literature include utility-scale as well as distributed solar system

closures and layoffs. Offsetting lower domestic sales to a large extent, exports rose by 30%, to 41 GW, during 2018. PV exports to emerging markets are being promoted through China’s newly unveiled International Investment Alliance for Renewable Energy. Chinese PV manufacturers are also increasing their global footprint, with production facilities in close to 20 countries [10]. The solar PV employment numbers created in China are shown in Figure 5.

4.4. BRAZIL

IRENA Renewable Energy and Jobs Annual Review of 2019 reported that Brazil is increasing activities in solar PV, installing 828 MW of large-scale capacity and 318 MW of distributed capacity during 2018. In operation since mid-2018, the country’s 399 MW Pirapora solar complex in Minas Gerais is one of Latin America’s larger domestic modules users (Power Technology, 2018). IRENA’s employment factor calculations suggest that Brazil presently has close to 15 600 jobs in solar PV, mostly in construction and installation. According to [10], the industry group Associação Brasileira de Energia Solar Fotovoltaica, will likely install about 1 GW of capacity during 2019, and 15 000 new jobs could be created from this initiative.

4.5. UNITED STATES

According to the IRENA Renewable Energy and Jobs Annual Review of 2019, in the US solar PV experienced a second successive year of job losses, down to 242 300 [10]. This was due to the uncertainty surrounding US import tariff policy that resulted in several utility-scale projects being delayed. The policy amendments in California and Massachusetts also reduced solar PV activities. Once the uncertainty over tariffs was lifted, new projects started construction and project announcements surged.

Also, the Chinese government’s decision in May 2018 to cut domestic solar incentives which support the domestic Chinese solar PV industry had the effect of reducing global demand for modules as Chinese solar prices decreased; the resulting over-supply lowered prices worldwide and counteracted the impact of the tariffs [17]. Two-thirds of these jobs are in installations and project development, mainly in the residential areas. Manufacturing accounts for 14% of solar PV jobs created in the solar PV sector [10]. Domestic US module production has been volatile over the years, and most of the solar PV technology is imported. Uncertainty about the US tariff policy hindered investments in the utility-scale solar PV projects. The US example illustrates the negative effect that policy uncertainty and rapid changes can have on solar PV job creation potential.

4.6. INDIA

India’s employment in grid-connected solar PV, as estimated by IRENA using employment factors, increased to 115 000 jobs in 2018, a gain of more than 20 000 additional jobs over 2017. Jobs in off-grid solar applications cannot be calculated with precision since jobs are quantified by employment factors and some off-grid systems are small in size therefore it is not always feasible to use employment factors. Moreover, the indirect jobs for off-grid solar systems are diverse throughout the world.

However, the jobs creation may well double total solar PV employment. Seven of India’s top 10 module suppliers are Chinese firms. Indian manufacturers cannot compete on cost due to a number of factors such as incentives that the Chinese companies receive for manufacturing, cheap labour costs, technology development knowhow and automated production. Imports, principally from China and Malaysia, but increasingly also from Thailand, Vietnam, and Singapore, dominate the Indian market. In the fiscal year 2018, domestic manufacturers had a market share of just 7% [18].

4.7. JAPAN

Japan’s solar PV installations reached a cumulative 55.5 GW in 2018, the second-largest installations after China. The pace of new installations declined for the third year in a row. The reasons for slowdown in solar PV installations were lower feed-in-tariffs, land shortages and grid constraints. Close to 300 solar firms have declared bankruptcy since 2015, with the number rising year on year.

According to [11] in Japan employment is estimated to be approximately 250 000 jobs, a reduction of 22 000 from 2017. A new driver is expected to be activated by the larger installations and more jobs may come from the government’s “Zero Energy Homes” policy, which requires all new buildings to integrate solar PV and energy efficiency technologies by 2030. This initiative is specific to Japan.

5. SOUTH AFRICAN SOLAR PV JOBS OVERVIEW

The Department of Minerals Resources and Energy (DMRE) Renewable Energy Independent Power Producers Procurement Programme (REI4P) was established at the end of 2010 as one of the South African government’s urgent interventions to enhance South Africa’s power generation capacity. The South African government adopted a framework consisting

of 18 Strategic Infrastructure Projects that is intended to transform the economic landscape of South Africa, create a significant number of new jobs, strengthen the delivery of basic services to the people of South Africa and support the integration of African economies.

The section below will provide a high level assessment of the amount of jobs that solar PV created in SA according to a different research reports.

5.1. SOLAR PV ELECTRICITY: LOCALISATION STUDY

The South African Photovoltaic Industry Association (SAPVIA) in collaboration with South Africa’s Trade, Industry and Competition (the DITC) and the World Wildlife Fund for Nature commissioned a research study into the localisation potential of solar PV and the strategy needed to support a large scale roll-out in South Africa in 2012/2013. The reports content is based on a much earlier report completed in 2006 using 2001 data.

A detailed breakdown of the methodology employed during the study is not represented in the report which makes it difficult to compare the results of the study to other research pieces.

5.1.1 UTILITY MARKET

According to this 2017 study completed on the Solar PV market in South Africa [19], the utility market is projected to lead in terms of installed capacities in the near to medium-term and is anticipated to procure 1.1 GW between 2017-2020. Construction of utility-scale projects are expected to create 5.83 FTE jobs per MW per annum, and this can be strengthened through improved local content policy. Additionally, O&M are expected to create 0.35 FTE jobs per MW over the lifetime of the facility. PV components like inverters, mounting hardware and modules account for the biggest expenditure of the total project cost.

Continuous job creation opportunities are dependent on market certainty and government commitments to continue procuring solar PV. The FTE/MW figures mentioned in this study is based on theoretical modelling framework which provides context of metrics that can be expected but does not provide a methodology for collecting and reporting on real jobs data.

5.1.2 COMMERCIAL AND INDUSTRIAL MARKET AND SMALL RESIDENTIAL MARKETS

The commercial and industrial market share increased rapidly in the past few years in South Africa, with rooftop applications accounting for the largest number of installations, although ground-mounted plants

have a higher installed capacity. The payback period of rooftop systems is between 5 and 7 years. The construction and installation of solar PV systems for commercial and industrial applications is estimated to create between 5.3 and 8.0 FTE jobs per MW.

Comparing these metrics to those on a utility scale it can be seen that the number of jobs per MW increase as time progresses. Grid-tied and autonomous off-grid PV systems that deploy batteries through hybrid systems are used for household PV systems.

Most of these applications are found in rural areas. The adoption of PV systems in South Africa has been dominated by applications in rural households, however, in the past few years the recent amendments of the Electricity Act of 2006 has increased residential and commercial solar PV systems adoption[19]. Moreover, the application of solar PV systems in industrial sector and mining areas has increased significantly.

The jobs created during the installation of residential solar PV systems differ depending on whether it is a rooftop or a mono pole grounded solar PV system. Rooftop systems have been adopted predominantly, and they are projected to create between 6.1 and 9.2 FTE jobs per MW (i.e. 7.7 FTE jobs per MW on average) during construction and installation [19]. Most solar PV systems for households are being installed on rooftops; however, ground mounting or mono pole systems can also be installed, nevertheless, their cost is approximately 5-10% more expensive.

Solar PV modules and inverters are among the top three biggest cost items for household solar PV systems. Table 5 shows that solar PV technology can create up to 17 times more FTE jobs per average MW over the life of the facility during the establishment phase [19] than wind power or solar thermal technologies. At the operational phase, solar PV impact on employment is smaller since it requires minimal operation supervision and maintenance. Furthermore, employment created during production and installation of solar PV technology has the potential to create employment in other sectors that are not in the value chain. These may include the financial services sector and security services, among others.

Figure 6 shows that 3.5 FTE jobs/MW and 1.2 FTE jobs/MW can be created by the supply and services value chain segments respectively. Solar PV panels suppliers that provide the link between producers and installers benefit from solar PV projects by achieving approximately 2.9 FTE jobs/MW [19]. The ability of South Africa to realise employment opportunities created through the development of the local solar PV energy capacity is dependent on the country’s industry

1514

and market structure. This especially relates to the jobs created during the first few stages of the value chain, i.e. Research and Development (R&D), supply, and production that are generally concentrated in the global solar PV production hubs.

Therefore, the realisation of employment potential associated with the first few stages of the value chain in any given country would be subject to numerous factors, including localisation capabilities. Installation of solar PV also creates employment opportunities for the local labour force.

5.2. CO-BENEFITS JOB CREATION THROUGH RENEWABLE ENERGY IN SOUTH AFRICA

The Co-benefit of climate change mitigation study [20] conducted a detailed theoretical modelling exercise to calculate the number of jobs being created in the RE space within South Africa. This study analyses the employment impacts of different plans for expanding electricity generation in South Africa’s power sector; this was carried out in the context of the Co-benefits project with the aim of assessing the co-benefits of a low-carbon energy transition in the country. It is important to note that the studies compared power sector modelling scenarios and not technologies specifically.

As such, PV specific information is limited in the review of this study as the growth in jobs takes into account all technologies being deployed. Furthermore, job numbers are reported in job years and cover direct, indirect and induced job impacts.

Four scenarios for the future development of the electricity sector in South Africa were analysed: Council for Scientific and Industrial Research Least Cost planning scenario (CSIR_LC); Department of Environmental Affairs Rapid Decarbonisation scenario (DEA_RD); draft Integrated Resource Plan 2016 (IRP 2016); and draft Integrated Resource Plan Policy Adjusted scenario 2018 (IRP 2018) collect real job information. Gross employment research utilising IJEDI to determine gross job impacts focused on all scenarios except the DEA rapid decarbonisation scenario.

Figure 7 shows the cumulative job years created by both wind power and solar PV technologies for each of the scenarios analysed during the period 2018 – 2030. More jobs are created in the wind sector under the CSIR_LC and IRP 2018_PA scenarios. This can be attributed to the larger shares of wind power capacities added in comparison to solar PV in both scenarios over the analysed time horizon. The figures attributed to solar PV are relatively high but includes induced job creation which cannot be easily quantified in terms of real jobs.

The study further developed a net employment impacts analysis that reported direct FTE jobs only utilising a SATIMCGE model that calculated economic gains and losses across all sectors and quantified job gains and losses in the power sector. The analysis differs from the gross assessment as only direct FTE jobs are reported from the modelling exercise.

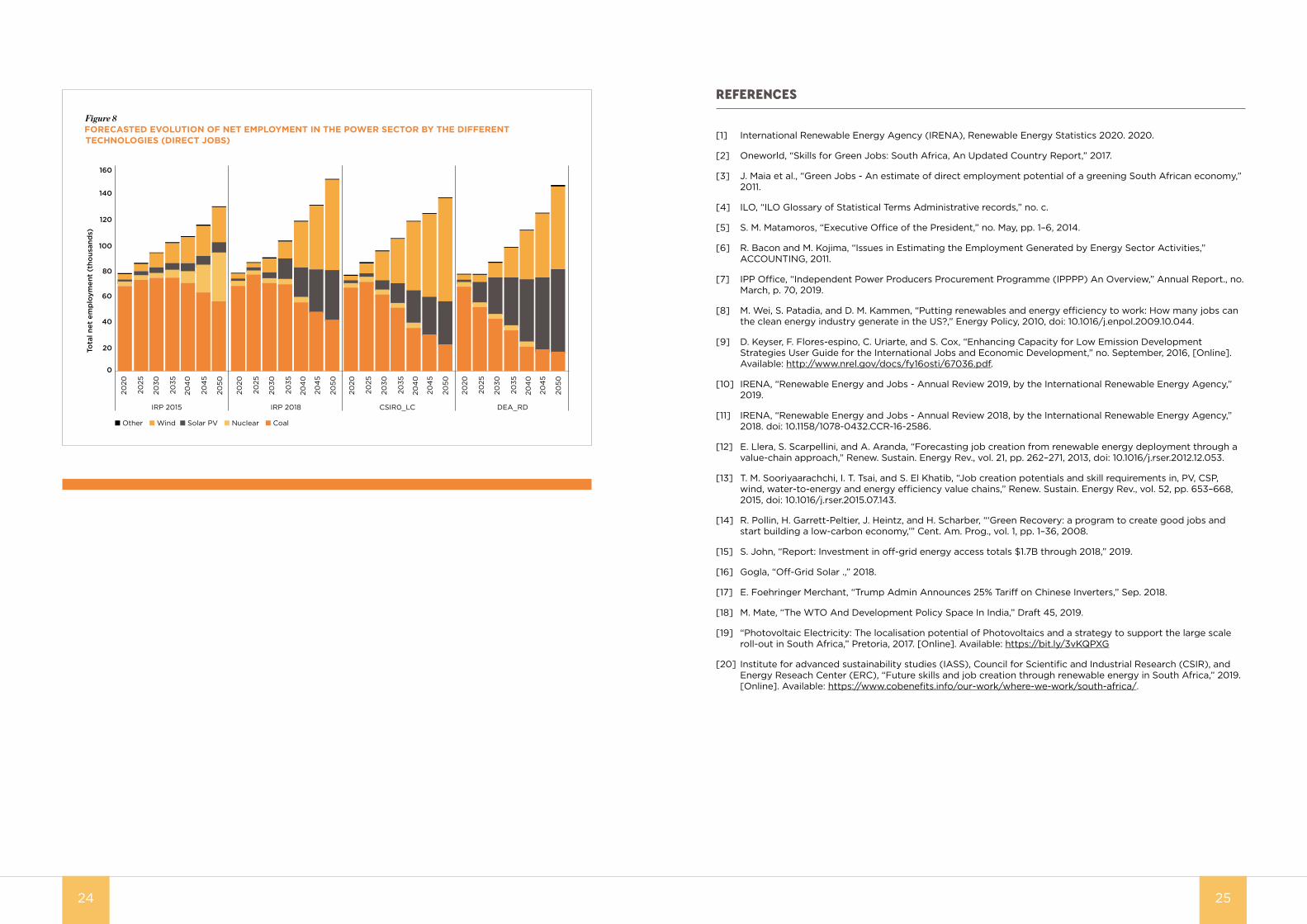

Figure 8 indicates that in the medium term, coal continues to play an important role in the power sector as a major employer, but this decreases over time as coal-fired power plants are decommissioned and replaced with other emerging technologies, most notably solar PV and wind.

5.3. SOUTH AFRICAN EMPLOYMENT POTENTIAL ESTIMATION

The study analysis by TIPS in 2011 shows that over 15 years (where the short term refers to 2011 and 2012; the medium-term refers to the subsequent five-year period up to and including the year 2017; and the long term refers to the subsequent eight-year period up to and including the year 2025) employment opportunities that will be created from the adoption of the green economy will continue to increase. The projection of employment potential was based on the expected number of jobs per year (on a non-cumulative basis).

Therefore, for construction employment to be sustained from one year to the next, the construction activity would need to be sustained, while an increase in employment would have to be associated with a higher level of construction activity [3]. This means that for green jobs to be sustained for a long period, policy certainty is required so that the deployment of RE is predictably undertaken.

Nonetheless, external opportunities, whether in the rest of Africa or elsewhere, could sustain employment levels through initiatives such as local manufacturing of energy components. The lifespan of the facilities/equipment was, where necessary, taken into account in the employment calculations as it has replacement implications.

Employment estimates for O&M activities, in turn, capture the number of people needed to operate the plants already constructed and commissioned, implying that the workers employed in year one would still be employed in year two and so on [3]. This means that an increase in the number of plants will also increase the quantum of employment associated with O&M requirements.

The jobs are also calculated on an FTE basis. For instance, if a crew of ten people can build a plant in three months, it would have to build four plants per

year to be considered fully employed. However, should the crew build only one plant, the employment creation would be reflected as 2.5 jobs created.

6. CONCLUSIONS

The literature review has explored job creation reporting by reviewing:

n Job creation defining reports, n Global reports that share best practice for reporting

on jobs numbers, n Cases studies on nations that create substantial

amounts of solar PV jobs and, n A review of South African reports that pertain to RE

job creation numbers

This review has highlighted the following key points listed below:

n Jobs created vary substantially between the asset construction and O&M phases. Reporting of jobs in a particular timeframe (such as in a particular year) needs to be assessed in relation to the portfolio of projects and the cycle of implementation.

n The concept of FTEs is critical. Substantial differences will arise when reporting on the number of people employed versus FTEs. A lack of clarity on these specifics is likely to result in large differences in reported numbers and will render comparison of numbers largely invalid.

n As mentioned above, proportionally more jobs are created in the construction phase as compared to O&M for solar PV. The concept of an average FTEs employed per annum over the lifetime of the plant (or total FTEs over all years) is valid but will result in a substantially different number as compared to looking at jobs in any particular year.

n The FTE metric alone does not provide the necessary flexibility to compare job creation potential across technologies nor value chain segments. A standardized unit of output is required to create a metric that mitigates against technologies differences in capacity factors and provides the ability to forecast future job creation potential as more MW’s are deployed.

n The concept of job categories of direct, indirect and induced jobs is critical. Study results need to be clear as to which of these categories have been included. Comparing total numbers will be misleading if studies are not consistently including the same job categories. This should be considered when developing the value chain that the data collection wants to explore as this can be a method to exclude induced jobs which are extremely difficult to collect and quantify

n Surveying of companies within the technologies value chain can be hampered by how said companies choose to track their employment generation figures. Surveying for direct, indirect and induced effects when companies choose to track their employees based on their payroll could create a lower response rate to surveys. To mitigate these negative effects, it is suggested to use simpler metrics that align best with how companies track their employment and generation figures and capture direct and indirect effects in the value chain breakdown itself.

n The fact that the majority of the jobs in solar PV are created in the initial construction phase requires a continuous rollout of annual solar PV installations to sustain the existing construction jobs. This will allow the creation of a sustainable industry and an industry that will replenish itself every 20-25 years when a solar PV facility reaches end of life and needs to be replaced.

1716

FIGURES AND TABLES

Figure 4GLOBAL EMPLOYMENT BY RENEWABLE ENERGY TECHNOLOGIES (IRENA, 2018; IRENA, 2019)

0 500 1000 1500 2000 2500 3000 3500 4000

Tide, Waveand Ocean Energy

CSP

Municipal andindustrial waste

SolarPhotovoltaic

Liquid Biofuels

Hydropower

Wind Energy

Solar Heating/Cooling

Solid Biomass

Biogas

GeothermalEnergy

Jobs (thousands)

3605O�-grid solar for

energy access

1160

801

787

334

94

41

34

1

2054

2063

Figure 2SOUTH AFRICAN SOLAR PV INSTALLED CAPACITY (GW)

2010

0

2011

0.01

2012

0.01

2013

0.26

2014

1.06

2015

1.25

2016

1.97

2017

2.19

2018

2.56

2019

2.56

+3 GW

0GW

Figure 1GLOBAL SOLAR PV INSTALLED CAPACITY

2010

40

2011

72

2012

102

2013

136

2014

172

2015

217

2016

291

2017

384

2018

481

2019

579

+98 GW

+538 GW

XX XX

XX XX

1918

DIRECT INDIRECT INDUCEDn On-site construction workersn Equipment manufacturersn Design servicesn Maintenance workersn Security personneln Replacement part

manufactureres

n Legal servicesn Natural resource suppliersn Construction equipment

suppliersn Whole businesses that sell

replacement partsn Accounting services

n Housingn Retailersn Restaurantsn Health care providersn Agriculture, food

providers

Figure 3DIRECT, INDIRECT AND INDUCED JOBS

Table 3TOTAL FULL TIME DIRECT JOBS AS PER MODEL RESULTS

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Manufacturing 963 1224 1447 2417 1713 1633 2145 9714 3598 11,075

Installation 372 594 581 1033 1539 3935 9149 18,040 475 2494

O&M 242 287 332 419 561 1020 2423 5863 5933 6296

Total jobs 1577 2105 2360 3869 3813 6588 13,717 33,617 10,006 19,865

Table 4 TOTAL FULL TIME DIRECT JOBS AS PER MODEL RESULTSTechnology type Employment opportunity Employment Factor Direct/ Indirect/Induced

Solar PV

Manufacturing, construction, Installation 5.76–6.21 jobs/MWp Direct

O&M 1.2–4.8 jobs/MWp Direct

PV module manufacturing

3–7 jobs/MWp

12–20 jobs/MWp Indirect

PV panel production 10 jobs/MWp Direct

Wholesale, retail, installation & maintenance 36 jobs/MWp Direct

Installation 346 jobs/MWp Direct

O&M 2.7 jobs/MWp Direct

Construction

17.2 man-years/MW Direct

9.4 man-years/MW Indirect

7.2 man-years/MW Induced

Operations

4.1 man-years/MW Direct

1.6 man-years/MW Indirect

2.7 man-years/MW Induced

Project construction 33–39 job-years/MWp Direct and Indirect

Table 1STAGES THAT INFLUENCE SOLAR PV EMPLOYMENT

Category number Category description

Volume of job creation generation

Location (from higher to lower numbers of jobs)

Sustainability of job

Level of specialisation

1 Research, design and development Medium From foreign to local Stable Very high

2 Manufacturing Medium From foreign to local Stable Very high

3 Transport, installation and commissioning High From local to foreign Temporary High

4 Operation and maintenance Low Local Stable Medium

5 Renovation, modernization, uprating or de-commissioning High From local to foreign Temporary High

Table 2INVOLVED FTE JOBS FOR THE COMMISSIONING OF A 1MWP PV FACILITY IN 2010

Jobs/MW Managers Technical consulters Salesmen Installers Operators Maintenance

staffAdministrative

staff Total jobs

Projects/studies 0.08 0.17 0.03 0.05 0.33

Silicon 0.05 0.80 0.13 0.98

Cells 1.01 0.50 0.70 0.20 2.41

Module assembly 2.01 1.01 4.02 2.01 9.05

Solar tracker 0.97 1.04 0.84 2.55 0.97 6.37

Elect. components & inverters 0.68 0.45 0.82 0.65 2.60

Installation 1.06 1.35 0.67 2.31 0.67 6.06

Operation 0.30 0.35 0.21 0.47 0.32 1.65

Total 6.16 4.41 2.20 2.31 8.90 0.47 5.00 29.46

XX XX

XX XX

2120

Figure 52019 CHINESE SOLAR PV JOBS

39% of global

renewable

energy jobs

Solar PV2.2 million jobs

Solar Water Heating670 000 jobs

Figure 6ESTIMATES OF TOTAL AND AVERAGE NUMBER OF FTE JOBS CREATED ALONG THE SOUTH AFRICAN SOLAR PV INDUSTRY VALUE CHAIN (2007, 2010, AND 2020)

0 5 10 15 20 25 30 35 40 45 50

2007

2010

2020

Average number of jobs created per MW of installed PV systems at di�erent stages of the value chain

0.9 2.6

3.4

3.4

7.0

9.0

9.6

2.1

2.7

2.9

29.1

31.7

32.4

0.9

1.2

0 50

2007

2010

2020

■ Research ■ Supply ■ Production ■ Wholesaler ■ Installation

Total jobs/MW

■ Entire Value Chain

47.9

49.6

41.8

Figure 7FORECASTED CUMULATIVE JOB YEARS CREATED DURING THE CONSTRUCTION PHASE IN WIND AND SOLAR PV BETWEEN THE YEAR 2018 AND 2030

Cum

ulat

ive

job

yea

rs, 2

018

-20

30(t

hous

and

s)

800

700

600

500

400

300

200

100

0

IRP 2016 IRP 2018 CSIR_LC

■ PV ■ Wind

Table 5JOB CREATION FROM SEVERAL RENEWABLE ENERGY TECHNOLOGIES

TechnologyEmployment per MW Average employment over life of the

facility

CIM (FTE jobs/MW)

O&M (FTE jobs/MW)

CIM (FTE jobs/MWa)

O&M (FTE jobs/MWa)

2001

Solar PV 30.0-32.3 0.25-1.0 5.76-6.21 1.2-4.8

Wind power 2.57-3.8 0.1-0.29 0.29-0.43 0.27-0.83

Biomass 4.29-8.5 0.04-1.53 0.13-0.4 0.38-1.8

Coal 8.5 0.18 0.27 0.74

2006

Solar PV 32.34-37.0 0.37-1.0 6.47-7.40 1.85-5.0

Wind Power 3.80-10.96 0.14-0.18 0.43-1.25 0.41-0.50

Solar Thermal 4.55 0.38 0.45 0.95

XX

XX

XX

2322

REFERENCES

[1] International Renewable Energy Agency (IRENA), Renewable Energy Statistics 2020. 2020.

[2] Oneworld, “Skills for Green Jobs: South Africa, An Updated Country Report,” 2017.

[3] J. Maia et al., “Green Jobs - An estimate of direct employment potential of a greening South African economy,” 2011.

[4] ILO, “ILO Glossary of Statistical Terms Administrative records,” no. c.

[5] S. M. Matamoros, “Executive Office of the President,” no. May, pp. 1–6, 2014.

[6] R. Bacon and M. Kojima, “Issues in Estimating the Employment Generated by Energy Sector Activities,” ACCOUNTING, 2011.

[7] IPP Office, “Independent Power Producers Procurement Programme (IPPPP) An Overview,” Annual Report., no. March, p. 70, 2019.

[8] M. Wei, S. Patadia, and D. M. Kammen, “Putting renewables and energy efficiency to work: How many jobs can the clean energy industry generate in the US?,” Energy Policy, 2010, doi: 10.1016/j.enpol.2009.10.044.

[9] D. Keyser, F. Flores-espino, C. Uriarte, and S. Cox, “Enhancing Capacity for Low Emission Development Strategies User Guide for the International Jobs and Economic Development,” no. September, 2016, [Online]. Available: http://www.nrel.gov/docs/fy16osti/67036.pdf.

[10] IRENA, “Renewable Energy and Jobs - Annual Review 2019, by the International Renewable Energy Agency,” 2019.

[11] IRENA, “Renewable Energy and Jobs - Annual Review 2018, by the International Renewable Energy Agency,” 2018. doi: 10.1158/1078-0432.CCR-16-2586.

[12] E. Llera, S. Scarpellini, and A. Aranda, “Forecasting job creation from renewable energy deployment through a value-chain approach,” Renew. Sustain. Energy Rev., vol. 21, pp. 262–271, 2013, doi: 10.1016/j.rser.2012.12.053.

[13] T. M. Sooriyaarachchi, I. T. Tsai, and S. El Khatib, “Job creation potentials and skill requirements in, PV, CSP, wind, water-to-energy and energy efficiency value chains,” Renew. Sustain. Energy Rev., vol. 52, pp. 653–668, 2015, doi: 10.1016/j.rser.2015.07.143.

[14] R. Pollin, H. Garrett-Peltier, J. Heintz, and H. Scharber, “‘Green Recovery: a program to create good jobs and start building a low-carbon economy,’” Cent. Am. Prog., vol. 1, pp. 1–36, 2008.

[15] S. John, “Report: Investment in off-grid energy access totals $1.7B through 2018,” 2019.

[16] Gogla, “Off-Grid Solar .,” 2018.

[17] E. Foehringer Merchant, “Trump Admin Announces 25% Tariff on Chinese Inverters,” Sep. 2018.

[18] M. Mate, “The WTO And Development Policy Space In India,” Draft 45, 2019.

[19] “Photovoltaic Electricity: The localisation potential of Photovoltaics and a strategy to support the large scale roll-out in South Africa,” Pretoria, 2017. [Online]. Available: https://bit.ly/3vKQPXG

[20] Institute for advanced sustainability studies (IASS), Council for Scientific and Industrial Research (CSIR), and Energy Reseach Center (ERC), “Future skills and job creation through renewable energy in South Africa,” 2019. [Online]. Available: https://www.cobenefits.info/our-work/where-we-work/south-africa/.

Figure 8FORECASTED EVOLUTION OF NET EMPLOYMENT IN THE POWER SECTOR BY THE DIFFERENT TECHNOLOGIES (DIRECT JOBS)

2020

2025

2030

2035

204

0

204

5

2050

Tota

l net

em

plo

ymen

t (t

hous

and

s)

160

140

120

100

80

40

20

0

■ Other ■ Wind ■ Solar PV ■ Nuclear ■ Coal

IRP 2015 IRP 2018 CSIR0_LC DEA_RD

60

2020

2025

2030

2035

204

0

204

5

2050

2020

2025

2030

2035

204

0

204

5

2050

2020

2025

2030

2035

204

0

204

5

2050

XX

2524

FORENSICS SCENARIO ANALYSIS

TABLE OF CONTENTS1. Introduction ..................................................................................................................................................................................................................31

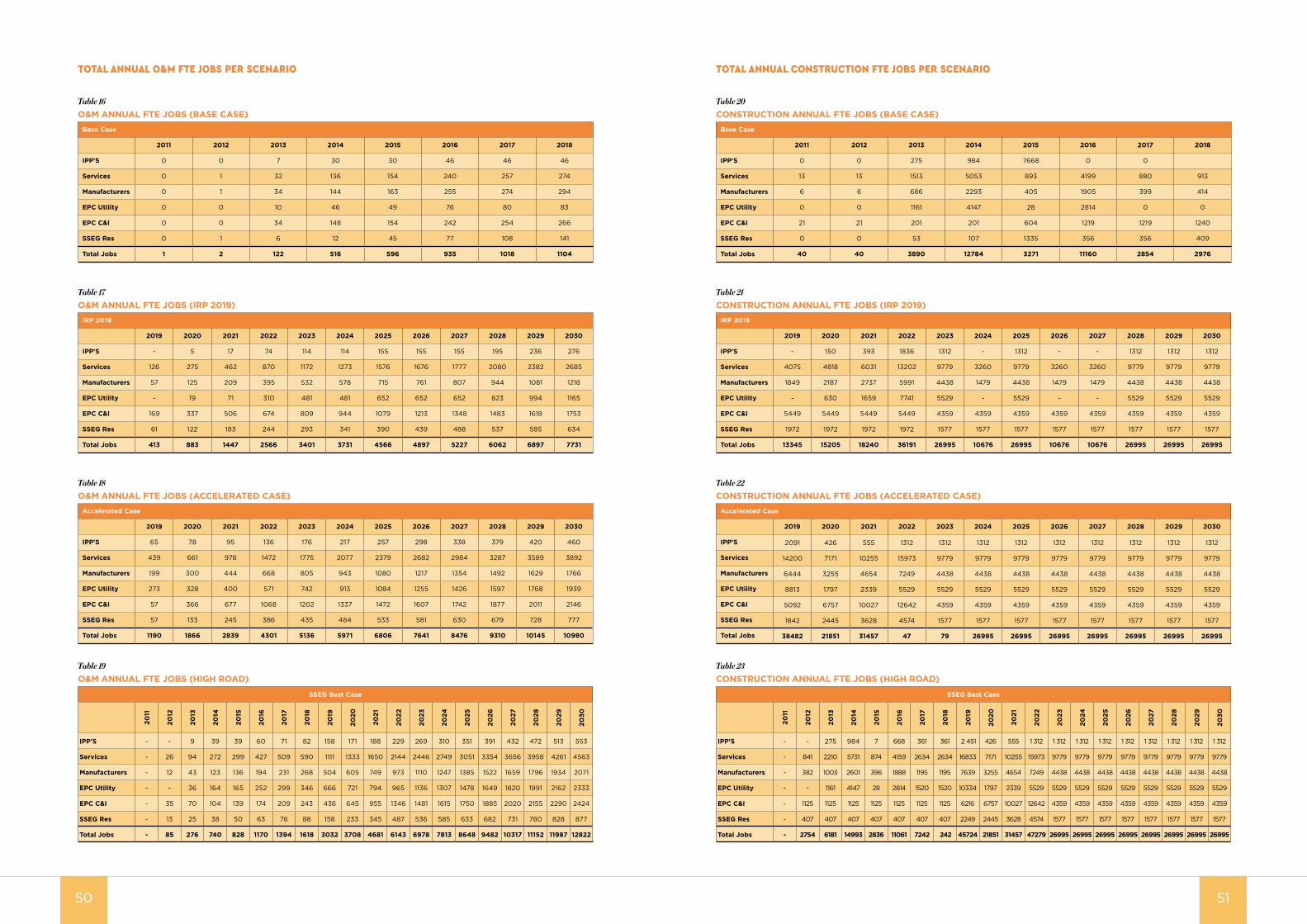

2. Methodology ................................................................................................................................................................................................................312.1. Overview.................................................................................................................................................................................................................312.2. Identification Of Preferred Metric .............................................................................................................................................................312.3. Contact List Construction And Sorting ..................................................................................................................................................312.4. Data Collection And Calculation Of Metrics .......................................................................................................................................322.5. Scenario Forecasting Utilising Real Job Number Calculated Metrics .....................................................................................32

3. Local Solar PV Jobs Survey ................................................................................................................................................................................343.1. Survey Stratification ........................................................................................................................................................................................343.2. Survey Responses ...........................................................................................................................................................................................343.3. Survey Results ..................................................................................................................................................................................................34

4. Scenario Configuration and Assumed Solar PV Capacities .................................................................................................................35

5. Scenario Job Analysis Results ............................................................................................................................................................................355.1. General ...................................................................................................................................................................................................................355.2. Base Case Scenario .........................................................................................................................................................................................355.3. IRP 2019 Scenario ............................................................................................................................................................................................355.4. Accelerated Scenario .....................................................................................................................................................................................365.5. High Road Scenario ........................................................................................................................................................................................365.6. O&M And Construction Jobs......................................................................................................................................................................36

6. Validation of Study Results ..................................................................................................................................................................................376.1. General ...................................................................................................................................................................................................................376.2. REI4P Job Statistics ........................................................................................................................................................................................376.3. I-Jedi Model Projections ...............................................................................................................................................................................376.4. International Benchmarks ............................................................................................................................................................................37

7. Summary and Conclusion .....................................................................................................................................................................................38

Figures and Tables ..........................................................................................................................................................................................................40

8. References ....................................................................................................................................................................................................................47

Annexure A1 .......................................................................................................................................................................................................................48A1.1: Questionnaires ................................................................................................................................................................................................48A1.2: Job Number Tables ......................................................................................................................................................................................50