Social Discount Rate 12-706 / 19-702. Admin Issues zSchedule changes: yNo Friday recitation – will...

43

Social Discount Rate 12-706 / 19-702

-

date post

21-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Social Discount Rate 12-706 / 19-702. Admin Issues zSchedule changes: yNo Friday recitation – will...

Social Discount Rate

12-706 / 19-702

Admin Issues

Schedule changes: No Friday recitation – will do in class Monday

Pipeline case study writeup – still Monday

Format expectations: Framing of problem (see p. 7!), Answer/justify with preliminary calculations Don’t just estimate the answer! Do not need to submit an excel printout, but feel free to paste a table into a document

Length: Less than 2 pages.

Real and Nominal Values

Nominal: ‘current’ or historical data

Real: ‘constant’ or adjusted data Use deflator or price index for real

Generally “Real” has had inflation/price changes factored in and nominal has not

For investment problems: If B&C in real dollars, use real disc rate If B&C in nominal dollars, use nominal rate Both methods will give the same answer

Similar to Real/Nominal : Foreign Exchange Rates / PPP

Big Mac handoutCommon Definition of inputsShould be able to compare cost across countries

Interesting results? Why?What are limitations?

Is it worth to spend $1 million today to save a life 10 years from now?

How about spending $1 million today so that your grandchildren can have a lifestyle similar to yours?

RFF Discounting Handout

How much do/should we care about people born after we die?

Ethically, no one’s interests should count more than another’s: “Equal Standing”

Social Discount Rate

Rate used to make investment decisions for society

Most people tend to prefer current, rather than future, consumption Marginal rate of time preference (MRTP)

Face opportunity cost (of foregone interest) when we spend not save Marginal rate of investment return

Intergenerational effects

We have tended to discuss only short term investment analyses (e.g. 5 yrs)

Economists agree that discounting should be done for public projects Do not agree on positive discount rate

Government Discount Rates

US Government Office of Management and Budget (OMB) Circular A-94 http://www.whitehouse.gov/omb/circulars/a094/a094.html

Discusses how to do BCA and related performance studies

What discount, inflation, etc. rates to use

Basically says “use this rate, but do sensitivity analysis with nearby rates”

OMB Circular A-94, Appendix C

Provides the current suggested values to use for federal government analyses

http://www.whitehouse.gov/omb/circulars/a094/a94_appx-c.html

Revised yearly, usually “good until January of the next year”

How would the government decide its discount rates?

What is the government’s MARR?

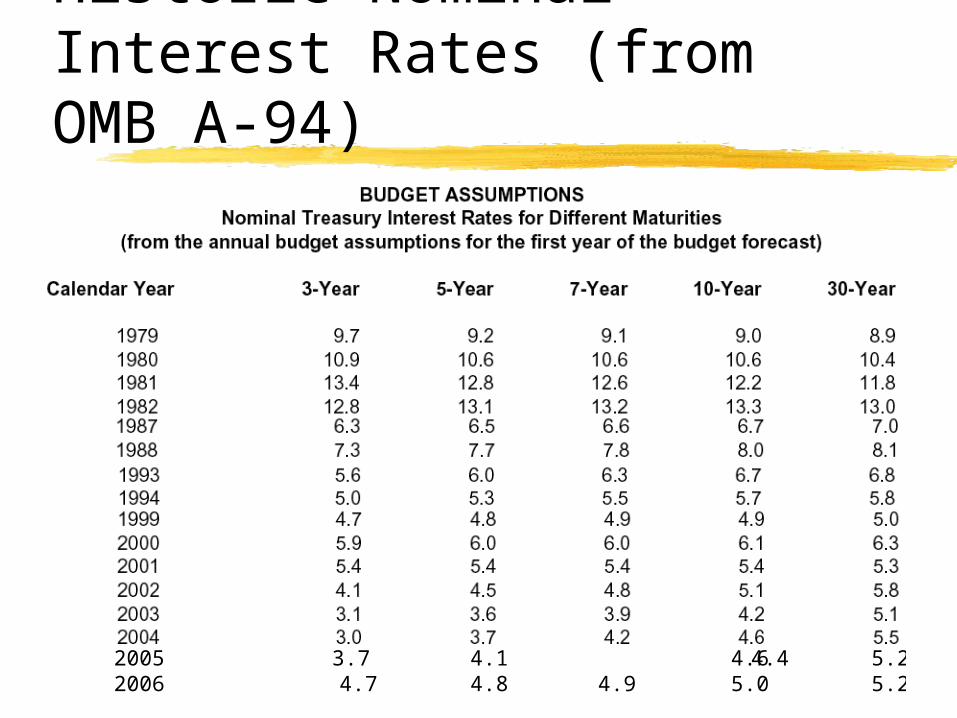

Historic Nominal Interest Rates (from OMB A-94)

2005 3.7 4.1 4.4 4.6 5.2 2006 4.7 4.8 4.9 5.0 5.2

Real Discount Rates (from A-94)

2005 1.7 2.0 2.3 2.5 3.12006 2.5 2.6 2.7 2.8 3.0

What do people think

Cropper et al surveyed 3000 homes Asked about saving lives in the future

Found a 4% discount rate for lives 100 years from now

Hume’s Law

Discounting issues are normative vs. positive battles

Hume noted that facts alone cannot tell us what we should do Any recommendation embodies ethics and judgment

E.g. focusing on ‘highest NPV’ implies net benefits is only goal for society

If future generations will be better off than us anyway Then we might have no reason to make additional sacrifices

There might be ‘special standing’ in addition to ‘equal standing’ Immediate relatives vs. distant relatives Different discount rates over time Why do we care so much about future and ignore some present needs (poverty)

A Few More Questions

Current government discount rates are ‘effectively zero’

What does this mean for projects and project selection decisions?

What does it say about intergenerational effects?

What are implications of zero or negative discount rates?

Comprehensive Everglades Restoration Project

Comprehensive project to restore natural water flow to the Florida Everglades.

Enhance water supply to South Florida region.

Provide continuous flood protection.

See more info at http://www.evergladesplan.org/

Indian River Lagoon-South (IRLS)

Part of Everglades Restoration Project.

Total Cost of $1.21 billion.

Annual Benefits of $159 million after project is completed in 2015.

Find NPV of first 25 years of project.

IRLS Cash Schedule

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

15 16 17 18 19 20 21 22 23 24 25

$0.425

$748.3

$2.043

$447.3

$12.62

$159 per year

All values are in millions

NPV of Project

-$700

-$600

-$500

-$400

-$300

-$200

-$100

$0

3% 7% 20%

(Millions)

Discount Rate

NPV of Project

What would NPV be if we used a negative discount rate?

-$800

-$600

-$400

-$200

$0

$200

$400

$600

$800

$1,000

3% 7% 20% 0% -1%(Millions)

Discount Rate

NPV of Project

NPV of Project

Borrowing, Depreciation, Taxes in Cash Flow Problems

H. Scott Matthews12-706 / 19-702

Theme: Cash Flows

Streams of benefits (revenues) and costs over time => “cash flows”

We need to know what to do with them in terms of finding NPV of projects

Different perspectives: private and public We will start with private since its easier Why “private..both because they are usually of companies, and they tend not to make studies public

Cash flows come from: operation, financing, taxes

Without taxes, cash flows simple

A = B - C Cash flow = benefits - costs Or.. Revenues - expenses

Notes on Tax deductibilityReason we care about financing and depreciation: they affect taxes owed

For personal income taxes, we deduct items like IRA contributions, mortgage interest, etc.

Private entities (eg businesses) have similar rules: pay tax on net income Income = Revenues - Expenses

There are several types of expenses that we care about Interest expense of borrowing Depreciation (can only do if own the asset) These are also called ‘tax shields’

Goal: Cash Flows after taxes (CFAT)

Master equation conceptually:CFAT = -equity financed investment + gross income - operating expenses + salvage value - taxes + (debt financing receipts - disbursements) + equity financing receipts

Where “taxes” = Tax Rate * Taxable IncomeTaxable Income = Gross Income - Operating Expenses - Depreciation - Loan Interest - Bond Dividends Most scenarios (and all problems we will look at) only deal with one or two of these issues at a time

Investment types

Debt financing: using a bank or investor’s money (loan or bond) DFD:disbursement (payments)

DFR:receipts (income)

DFI: portion tax deductible (only non-principal)

Equity financing: using own money (no borrowing)

Why Finance?

Time shift revenues and expenses - construction expenses paid up front, nuclear power plant decommissioning at end.

“Finance” is also used to refer to plans to obtain sufficient revenue for a project.

Borrowing

Numerous arrangements possible: bonds and notes (pay dividends) bank loans and line of credit (pay interest)

municipal bonds (with tax exempt interest)

Lenders require a real return - borrowing interest rate exceeds inflation rate.

Issues

Security of loan - piece of equipment, construction, company, government. More security implies lower interest rate.

Project, program or organization funding possible. (Note: role of “junk bonds” and rating agencies.

Variable versus fixed interest rates: uncertainty in inflation rates encourages variable rates.

Issues (cont.)

Flexibility of loan - can loan be repaid early (makes re-finance attractive when interest rates drop). Issue of contingencies.

Up-front expenses: lawyer fees, taxes, marketing bonds, etc.- 10% common

Term of loanSource of funds

Sinking Funds

Act as reverse borrowing - save revenues to cover end-of-life costs to restore mined lands or decommission nuclear plants.

Low risk investments are used, so return rate is lower.

Recall: Annuities (a.k.a uniform values) Consider the PV of getting the same amount ($1) for many

years Lottery pays $A / yr for n yrs at i=5%

----- Subtract above 2 equations.. -------

When A=1 the right hand side is called the “annuity factor”

€

PV = A1+i +

A(1+i)2 + A

(1+i)3 + ..+ A(1+i)n

€

PV * (1+ i) = A + A(1+i)

+ A(1+i)2 + ..+ A

(1+i)n−1

€

PV * (1+ i) − PV = A − A(1+i)n

€

PV * (i) = A(1− 1(1+i)n

) = A(1− (1+ i)−n )

€

PV = A (1−(1+i)−n )i

Uniform Values - Application

Note Annual (A) values also sometimes referred to as Uniform (U) ..

$1000 / year for 5 years exampleP = U*(P|U,i,n) = (P|U,5%,5) = 4.329

P = 1000*4.329 = $4,329

Relevance for loans?

Borrowing

Sometimes we don’t have the money to undertake - need to get loan

i=specified interest rateAt=cash flow at end of period t (+ for loan receipt, - for payments)

Rt=loan balance at end of period tIt=interest accrued during t for Rt-1

Qt=amount added to unpaid balanceAt t=n, loan balance must be zero

Equations

i=specified interest rateAt=cash flow at end of period t (+ for loan receipt, - for payments)

It=i * Rt-1

Qt= At + It

Rt= Rt-1 + Qt <=> Rt= Rt-1 + At + It

Rt= Rt-1 + At + (i * Rt-1)

Annual, or Uniform, payments

Assume a payment of U each year for n years on a principal of P

Rn=-U[1+(1+i)+…+(1+i)n-1]+P(1+i)n

Rn=-U[((1+i)n-1)/i] + P(1+i)n

Uniform payment functions in Excel

Same basic idea as earlier slide

Example

Borrow $200 at 10%, pay $115.24 at end of each of first 2 years

R0=A0=$200

A1= -$115.24, I1=R0*i = (200)*(.10)=20

Q1=A1 + I1 = -95.24

R1=R0+Qt = 104.76

I2=10.48; Q2=-104.76; R2=0

Various Repayment Options

Single Loan, Single payment at end of loan

Single Loan, Yearly PaymentsMultiple Loans, One repayment

Notes

Mixed funds problem - buy computer Below: Operating cash flows At Four financing options (at 8%) in At section below

t At(Operation)

0 -22,000 10,000 10,000 10,000 10,0001 6,000 -2,505 -800 -2,8002 6,000 -2,505 -800 -2,6403 6,000 -2,505 -800 -2,4804 6,000 -2,505 -800 -2,3205 6,000 -14,693 -2,505 -10,800 -2,160

2,000

At(Financing)

Further Analysis (still no tax)

t At8% (Operation)

0 -22,000 10,000 10,000 10,000 10,000 -12,000 -12,000 -12,000 -12,0001 6,000 -2,505 -800 -2,800 6,000 3,495 5,200 3,2002 6,000 -2,505 -800 -2,640 6,000 3,495 5,200 3,3603 6,000 -2,505 -800 -2,480 6,000 3,495 5,200 3,5204 6,000 -2,505 -800 -2,320 6,000 3,495 5,200 3,6805 6,000 -14,693 -2,505 -10,800 -2,160 -8,693 3,495 -4,800 3,840

2,000 2,000 2,000 2,000 2,000NPV 3317.427 0.1911 -1.7386 0 1E-12 3317.62 3315.69 3317.4 3317.43

At(Financing at 8%)

A*(Total pre-tax)

MARR (disc rate) equals borrowing rate, so financing plans equivalent.

When wholly funded by borrowing, can set MARR to interest rate

Effect of other MARRs (e.g. 10%)t At

10% (Operation)0 -22,000 10,000 10,000 10,000 10,000 -12,000 -12,000 -12,000 -12,0001 6,000 -2,505 -800 -2,800 6,000 3,495 5,200 3,2002 6,000 -2,505 -800 -2,640 6,000 3,495 5,200 3,3603 6,000 -2,505 -800 -2,480 6,000 3,495 5,200 3,5204 6,000 -2,505 -800 -2,320 6,000 3,495 5,200 3,6805 6,000 -14,693 -2,505 -10,800 -2,160 -8,693 3,495 -4,800 3,840

2,000 2,000 2,000 2,000 2,000NPV 1986.563 876.8 504.08 758.16 483.69 2863.37 2490.64 2744.7 2470.25

At A*(Financing at 8%) (Total pre-tax)

‘Total’ NPV higher than operation alone for all options All preferable to ‘internal funding’ Why? These funds could earn 10% ! First option ‘gets most of loan’, is best

Effect of other MARRs (e.g. 6%)

t At6% (Operation)

0 -22,000 10,000 10,000 10,000 10,000 -12,000 -12,000 -12,000 -12,0001 6,000 -2,505 -800 -2,800 6,000 3,495 5,200 3,2002 6,000 -2,505 -800 -2,640 6,000 3,495 5,200 3,3603 6,000 -2,505 -800 -2,480 6,000 3,495 5,200 3,5204 6,000 -2,505 -800 -2,320 6,000 3,495 5,200 3,6805 6,000 -14,693 -2,505 -10,800 -2,160 -8,693 3,495 -4,800 3,840

2,000 2,000 2,000 2,000 2,000NPV 4768.699 -979.46 -551.97 -842.5 -525.1 3789.23 4216.73 3926.2 4243.61

At A*(Financing at 8%) (Total pre-tax)

Now reverse is true Why? Internal funds only earn 6% ! First option now worst