SMMT MOTOR INDUSTRY FACTS 2017 · CONTENTS UK AUTOMOTIVE AT A GLANCE 4-5 UK AUTOMOTIVE INDUSTRY 6...

30

SMMT MOTOR INDUSTRY FACTS 2017

Transcript of SMMT MOTOR INDUSTRY FACTS 2017 · CONTENTS UK AUTOMOTIVE AT A GLANCE 4-5 UK AUTOMOTIVE INDUSTRY 6...

SMMT MOTOR INDUSTRY FACTS 2017

WHAT IS SMMT?

The Society of Motor Manufacturers and Traders (SMMT) is one of the largest and most influential trade

associations in the UK. Its resources, reputation and unrivalled automotive data place it at the heart of

the UK automotive industry. It undertakes a variety of activities to support and represent the interests

of the industry and has a long history of achievement.

Working closely with member companies, SMMT acts as the voice of the UK motor industry, supporting

and promoting its interests at home and abroad to government, stakeholders and the media.

SMMT represents more than 700 automotive companies in the UK, providing them with a forum to voice

their views on issues affecting the automotive sector, helping to guide strategies and build positive

relationships with government and regulatory authorities.

To find out how to join SMMT and for more information,

visit www.smmt.co.uk/memberservices or e-mail [email protected]

WH

AT IS SMM

T?

02

CONTENTS

UK AUTOMOTIVE AT A GLANCE 4-5

UK AUTOMOTIVE INDUSTRY 6UK automotive employment 6UK Automotive: background 7

MANUFACTURING 8UK automotive manufacturing 8Global automotive manufacturing 9UK car manufacturing 10UK car exports 11Map: UK automotive manufacturing sites 12–14Commercial vehicles and engines 15UK automotive aftermarket 16

UK AUTOMOTIVE SUPPLY CHAIN 17

REGISTRATIONS 18New car registrations 18Registrations by colour 19 Registrations by sales type 20Registrations by segment 21–23Commercial vehicle registrations 24Global car registrations 25

CONNECTED CARS 26

DIGITALISATION OF AUTOMOTIVE MANUFACTURING 27

VEHICLES ON THE ROAD 28–29

ENVIRONMENT AND AIR QUALITY 30-31

UK AUTOMOTIVE AND THE EU 32

SMMT GROUP 33

CON

TENTS

03

UK AUTOMOTIVE AT A GLANCEU

K AUTO

MO

TIVE AT A GLAN

CE

Suppliers2,500

Commercial vehicle manufacturers

Cars built in 2016

1,722,698

Engines built in 2016

2,545,608

Commercial vehicles built in 2016

93,924

People employed across UK Auto

814,000

Countries importing UK-built vehicles

UK automotive turnover

£77.5 billion

Cars currently on UK roads

Over 34.4 million

Vehicles exported in 2016

1,354,216

New cars registered in 2016

2,692,237

160

Engine manufacturers

05

04

UK AUTOMOTIVE EMPLOYMENTU

K AU

TOM

OTIV

E EMPLO

YMEN

T

25,000new jobs to be

created in automotive manufacturing to

build connected and autonomous vehicles

41,000 people employed

in UK motorsport – 25,000 are engineers

(Motorsport Industry

Association)

169,000people employed in manufacturing

814,000 people employed

across UK Automotive

78,480 young people

began engineering and manufacturing

apprenticeships in 2015/6

(Semta)

06

UK A

UTO

MO

TIVE: B

ACKGR

OU

ND

UK AUTOMOTIVE: BACKGROUND

In 2016 the UK automotive manufacturing industry…

Turned over £77.5 billion

Invested £2.75 billion in R&D

Exported products worth £40.1 billion, accounting for 13% of the UK’s total export goods

Invested £4 billion net capital

Added £22 billion in value to the UK economy

07

UK A

UTO

MO

TIVE M

AN

UFA

CTURIN

GUK AUTOMOTIVE MANUFACTURING

Commercial vehicles by brandMake Volume

Vauxhall 73,615

Leyland Trucks 14,729

Alexander Dennis 2,228

Land Rover 1,820

Dennis Eagle 723

Cars by brandMake Volume

Jaguar Land Rover 544,401

Nissan 507,444

BMW 210,973

Toyota 180,425

Honda 134,146

Cars by modelModel Volume

Nissan Qashqai 309,893

Toyota Auris 144,674

Nissan Juke 109,968

Land Rover Evoque 96,498

Land Rover Discovery Sport 89,004

Top fives in production – 2016

08

GLOB

AL A

UTO

MO

TIVE M

AN

UFA

CTURIN

GGLOBAL AUTOMOTIVE MANUFACTURING

Top 10 European automotive manufacturers in 2016Rank Country Cars Commercial

Vehicles Total % change

1 Germany 5,746,808 315,754 6,062,562 0.50%

2 Spain 2,354,117 531,805 2,885,922 5.60%

3 France 1,626,000 456,000 2,082,000 5.60%

4 UK 1,722,698 93,924 1,816,622 8.00%

5 Czech Rep. 1,344,182 5,714 1,349,896 8.30%

6 Italy 713,182 390,334 1,103,516 8.80%

7 Slovakia 1,040,000 0 1,040,000 0.10%

8 Poland 554,600 127,237 681,837 3.20%

9 Hungary 472,000 0 472,000 -4.70%

10 Belgium 354,003 45,424 399,427 -2.40%

Source: OICA 2017

*See page 12 for 2016 UK car manufacturing data

Top 15 global automotive manufacturers in 2016Rank Country Cars Commercial

vehicles Total % change

1 China 24,420,744 3,698,050 28,118,794 14.50%

2 USA 3,934,357 8,263,780 12,198,137 0.80%

3 Japan 7,873,886 1,330,704 9,204,590 -0.80%

4 Germany 5,746,808 315,754 6,062,562 0.50%

5 India 3,677,605 811,360 4,488,965 7.90%

6 South Korea 3,859,991 368,518 4,228,509 -7.20%

7 Mexico 1,993,168 1,604,294 3,597,462 0.90%

8 Spain 2,354,117 531,805 2,885,922 5.60%

9 Canada 802,057 1,568,214 2,370,271 3.80%

10 Brazil 1,778,464 377,892 2,156,356 -11.20%

11 France 1,626,000 456,000 2,082,000 5.60%

12 Thailand 805,033 1,139,384 1,944,417 1.80%

13 UK 1,722,698 93,924 1,816,622 8.00%14 Turkey 950,888 535,039 1,485,927 9.40%

15 Czech Rep. 1,344,182 5,714 1,349,896 8.30%

09

UK CA

R MA

NU

FACTU

RING

UK CAR MANUFACTURING

10

UK car manufacturing

UK car manufacturing – 2016 vs 20152016 2015 % Change

Total 1,722,698 1,587,677 8.5%

Home 368,482 359,796 2.4%

Export 1,354,216 1,227,881 10.3%

% export 78.8% 77.3%

UK car production reached its HIGHEST LEVEL in

17 years in 2016

2,000,000

1972 2009 2012 2013 2014 2015 20160

1,000,000

500,000

1,500,000

RECO

RD H

IGH

UK CA

R EXPORTS

UK CAR EXPORTS

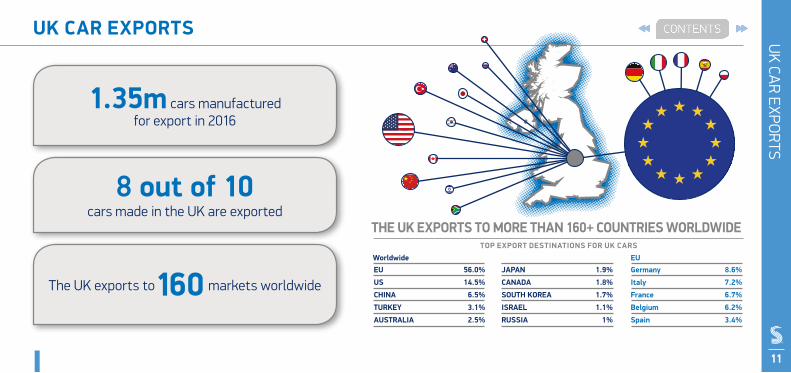

1.35m cars manufactured for export in 2016

8 out of 10 cars made in the UK are exported

The UK exports to 160 markets worldwide

11

TOP EXPORT DESTINATIONS FOR UK CARS

THE UK EXPORTS TO MORE THAN 160+ COUNTRIES WORLDWIDE

EU 56.0%

US 14.5%

CHINA 6.5%

TURKEY 3.1%

AUSTRALIA 2.5%

JAPAN 1.9%

CANADA 1.8%

SOUTH KOREA 1.7%

ISRAEL 1.1%

RUSSIA 1%

Germany 8.6%

Italy 7.2%

France 6.7%

Belgium 6.2%

Spain 3.4%

Worldwide EU

1

2 30 31

7

1220

23

8

99 10

21

5

4

3

14

27

12

13

28

32

29

15

2411

6

25

26

22

1617

1

18

11

19

UK AUTOMOTIVE MANUFACTURINGU

K AU

TOM

OTIV

E MA

NU

FACTU

RING

In 2016 UK automotive manufacturers produced

1,816,622 vehicles

In 2016 2,545,608 engines were built in the UK

There are more than 2,500 automotive component providers

in the UK

Key UK manufacturing sitesKey Manufacturer Location Sector Model

1 Alexander Dennis

Falkirk and Guildford

Bus and coach Enviro bus range

2 Aston Martin Gaydon CarComet, DB9, DB11, Rapide, Vantage, Vanquish.

3 Bentley Crewe Car and engine

Bentayga, Continental and Mulsanne

4 BMW Hams Hall Engine Engine range

5 Caterham Dartford Car Seven

6 Cummins Darlington Engine Engine range

7 Dennis Eagle Warwick CV N and W truck range

8 Euromotive Hythe Bus and coach Minibus range

9 Ford Bridgend and Dagenham Engine Engine range

10 Honda Swindon Car and engine Civic, CR-V and Jazz

11 Infiniti Sunderland Car Infiniti Q30

12 Jaguar Land Rover

Castle Bromwich & Wolver-hampton

Car and engine

Engine range Jaguar: F-Pace F-Type, XE, XJ and XF

13Jaguar Land Rover

Solihull and Halewood Car

Land Rover: Discovery, Discovery Sport, Range Rover, Range Rover Sport, and Evoque.

14John Dennis Coachbuilders

Guildford Bus and coach Fire vehicles

15 Leyland Trucks Leyland CV DAF CF, LF and XF truck range

16 Lotus Norwich Car Elise, Evora and Exige

17 LTC Coventry CV TX Taxi

18 McLaren Automotive Woking Car 540, 570, 650, 675

and P1

19 Mellor Rochdale Bus and coach

Accessible coach range

20 MG Motors Longbridge Car MG3 and MG GS

21 MINI Oxford Car

MINI 3-Door Hatch, MINI 5-Door Hatch, MINI Convertible, MINI Clubman, MINI Coupé, and MINI Roadster

22 Minibus Options Whaley Bridge Bus and

coach Minibus range

23 Morgan Malvern Car

Aero, Aero Supersport, Aero Coupe, 4/4, Plus 4, Plus 8, Roadster, 4 Seater and 3 Wheeler

24 Nissan Sunderland Car and engine

Juke, LEAF, Note and Qashqai, Infiniti Q30

25 Optare Leeds Bus and coach

Solo, Tempo and Versa bus range

26 Plaxton Scarborough Bus and coach

Cheetah, Elite, Panther, Paragon coach bodies and Enviro bus range

27 Rolls-Royce Goodwood Car Ghost, Phantom and Wraith

28 Toyota Burnaston Car and engine Auris and Avensis

29 Vauxhall Ellesmere Port

Car, CV and bus and coach

Astra 5-Door HatchAstra Sports Tourer

30 Vauxhall Luton CV Vivaro van

31 Warnerbus Dunstable Bus and coach Minibus range

32 Wrightbus Ballymena (NI) Bus and coach Bus range

14

13

12

2016 2015 % Change

Total 93,924 94,479 -0.6%

Home 39,102 47,300 -17.3%

Export 54,842 47,179 16.2%

% export 58.4% 49.9%

201388,110

201470,869

201594,479

201693,924

CV AN

D EN

GINE M

AN

UFA

CTURIN

GCV AND ENGINE MANUFACTURING

UK Commercial Vehicle manufacturing volumes:2013 to 2016

UK Commercial Vehicle manufacturing – 2016 vs 2015

15

UK engine manufacturing volumes – 2016

2,545,608 engines

built in 2016

10.1%

0.5%

25.9%

30.7%

5.2%

7.9%

9.4%

10.4%

JaguarLand Rover Toyota

NissanHondaFord (Bridgend)

Ford (Dagenham)BMW

Bentley

UK A

UTO

MO

TIVE A

FTERM

AR

KE

TUK AUTOMOTIVE AFTERMARKET

£12.5 billion contribution to UK economy

347,000 jobs supported

£706.71average annual spend per car

£21.6 billion revenue of UK a�ermarket

Services more than

30 millionvehicles a year

The Importance of the Aftermarket to the UK Economy

16Source: Frost & Sullivan

UK A

UTO

MO

TIVE SU

PPLY CHA

INUK AUTOMOTIVE SUPPLY CHAIN

BODY PAINT POWERTRAIN ASSEMBLY INSPECTION

£4bn of unfulfilled opportunities for

domestic Tier 1 suppliers

18 of the world’s 20 biggest

automotive suppliers have a UK base

44% average UK content in British-built

cars – up from 36% since 2011 78,000 people

employed in the UK supply chain

£4.3bn added value generated by

UK automotive suppliers each year

17

2,500+ automotive

suppliers in the UK

REGISTRATIO

NS

NEW CAR REGISTRATIONS

Model Volume

1 Ford Fiesta 120,525

2 Vauxhall Corsa 77,110

3 Ford Focus 70,545

4 Volkswagen Golf 69,492

5 Nissan Qashqai 62,682

6 Vauxhall Astra 60,719

7 Volkswagen Polo 54,448

8 MINI 48,328

9 Mercedes-Benz C Class 44,184

10 Audi A3 43,808

3,000,000

’00 ’01 ’02 ’03 ’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’150

2,000,000

1,500,000

1,000,000

500,000

2,500,000

’16

2,692,786

Annual New Car Registrations – 2000 to 2016

Top 10 UK sellers in 2016

18

New car registrations by fuel type – 2016 vs 2007

2007

2016

1,285,160

1,318,707

88,919

16,641

DIES

ELPE

TROL

AFV

DIES

ELPE

TROL

AFV

967,413

1,419,953

REGISTRATIO

NS BY CO

LOU

RREGISTRATIONS BY COLOUR

Changing tastes in car colour: Top 5 1996-2016

19

The change in segment registrations – 2016 vs 2006

MINI +228.9%

UPPER MEDIUM-34.8%

SPECIALIST SPORTS -23.5%

SUPER MINI +15.8%

EXECUTIVE +27.4%

DUAL PURPOSE +149.1%

LOWER MEDIUM+5.8%

LUXURY SALOON -20.6%

MULTI PURPOSE+0.5%

1

2

34

5

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

REGISTR

ATION

S BY SA

LES TYPEREGISTRATIONS BY SALES TYPE

FleetModel Volume

Ford Fiesta 46,840

Volkswagen Golf 43,393

Vauxhall Astra 43,144

Ford Focus 43,037

Nissan Qashqai 36,381

PrivateModel Volume

Ford Fiesta 73,684

Volkswagen Polo 37,362

Vauxhall Corsa 32,072

MINI 28,483

Ford Focus 27,505

Top five new car registrations in 2016 by sales type

BusinessModel Volume

Vauxhall Corsa 15,373

Vauxhall Viva 7,840

Vauxhall Astra 5,881

Mitsubishi Outlander 3,919

Nissan Note 3,497Business

3.9%

51.3%

44.8%

2016 registrations by sales type

Business If the vehicle is being registered by a company that operates up to 24 vehicles, it is designated a business sale. This includes dealer demonstrators.

Fleet If the vehicle is being registered by a company that operates a fleet of 25 or more vehicles, it is designated a fleet sale. This includes dealer demonstrators and Motability-leased vehicles. Private If the vehicle is being registered primarily for the personal use of a private individual, it is designated a private sale.

20

Fleet

Private

REGISTR

ATION

S BY SEGM

ENT

REGISTRATIONS BY SEGMENT

Supermini

Lower M

edium

Model Volume Segment share

Hyundai i10 23,657 30.9%

Vauxhall Viva 14,297 18.7%

Volkswagen up! 13,245 17.3%

Suzuki Celerio 8,420 11.0%

Skoda Citigo 8,140 10.6%

Segment total: 76,616

Model Volume Segment share

Ford Fiesta 120,525 13.8%

Vauxhall Corsa 77,110 8.8%

Volkswagen Polo 54,448 6.2%

MINI 48,328 5.5%

Nissan Juke 38,803 4.5%

Segment total: 872,936

Model Volume Segment share

Ford Focus 70,545 9.6%

Volkswagen Golf 69,492 9.5%

Nissan Qashqai 62,682 8.5%

Vauxhall Astra 60,719 8.3%

Audi A3 43,806 6.0%

Segment total: 734,825

Mini

Top cars registered by segment

21

REGISTRATIONS BY SEGMENTR

EGISTRATIO

NS B

Y SEGMEN

T

Top cars registered by segment

Model Volume Segment share

Mercedes-Benz C Class 44,184 34.6%

Mercedes-Benz E Class 25,537 12.0%

BMW 5 Series 19,621 15.4%

Audi A6 18,698 14.6%

Jaguar XF 9,619 7.5%

Segment total: 127,804

Executive

Model Volume Segment share

BMW 3 Series 36,732 14.3%

Audi A4 26,686 10.4%

Vauxhall Insignia 25,095 9.8%

BMW 4 Series 23,479 9.1%

Skoda Octavia 23,068 9.0%

Segment total: 256,924

Upper M

edium

Model Volume Segment share

Mercedes-Benz S Class 3,339 31.8%

BMW 7 Series 2,076 19.8%

Jaguar XJ 1,206 11.5%

Audi A8 1,060 10.1%

Bentley Continental 1,033 9.8%

Segment total: 10,500

Luxury

22

REGISTR

ATION

S BY SEGM

ENT

REGISTRATIONS BY SEGMENT

Top cars registered by segment

Specialist Sports

Dual Purpose

MPV

23

Model Volume Segment share

Audi TT 9,836 19.8%

Volkswagen Scirocco 5,729 11.5%

Mazda MX-5 4,229 8.5%

Ford Mustang 3,257 6.5%

Other British 2,593 5.2%

Segment total: 49,774

Model Volume Segment share

Kia Sportage 40,083 9.2%

Ford Kuga 35,481 8.1%

Range Rover Evoque 27,161 6.2%

Hyundai Tucson 25,242 5.8%

Land Rover Discovery Sport 23,796 5.4%

Segment total: 437,931

Model Volume Segment share

Ford C-MAX 18,196 14.5%

Citroen C4 Picasso 15,773 12.6%

Vauxhall Zafira Tourer 12,444 9.9%

Ford S-MAX 7,794 6.2%

Ford B-MAX 7,468 6.0%

Segment total: 125,476

COM

MER

CIAL V

EHICLE R

EGISTRATIO

NS

COMMERCIAL VEHICLE REGISTRATIONS

Van registrations – 2010 to 2016 2016 commercial vehicle registrations

LCVs up to 3.5t Rigids Artics Bus and coach

Volume 375,687 26,882 19,346 8,779

% change on 2015

1.0% 17.0% -7.5% 8.0%

0

100,000

200,000

300,000

400,000375,687

20142013201220112010 2015 2016

19.6%

16.7%-7.9%

13.1%

18.7%

15.6% 1.0%

430,694 commercial vehicles

were registered in 2016

24

Country Volume

China 24,376,902

EU28 17,291,819

US 6,872,729

Japan 4,146,459

Germany 3,351,607

India 2,966,637

UK 2,692,786

France 2,015,177

Italy 1,824,968

Brazil 1,676,722

South Korea 1,533,813

Iran 1,320,300

GLOB

AL CA

R REGISTR

ATION

SGLOBAL CAR REGISTRATIONS

Source: OICA 2017 Figures include passenger cars only. LCVs (including pick-ups) are not included and may represent significant sales volumes in some markets

International new car registrations – 2016

69,464,432

new cars were registered globally in 2016

25

£51 BillionValue added annually

(at 2014 prices)

Top 5 benefits of CAVs

• Reduced stress of driving• Ability to rest on longer journeys• Fewer accidents• Lower insurance costs• Ability to travel at preferred times

320,000Additional jobs created

25,000Jobs in automotive

manufacturing created

2,500Lives saved

6/10 people*with limited mobility will have

an improved quality of life*when surveyed

1 millionmore people with access

to further education

25,000Serious accidents prevented

CONNECTED CARSCO

NN

ECTED CA

RS

UK social and economic impact of connected and autonomous vehicles

26

DIGITA

LISATION

OF M

AN

UFA

CTURIN

GDIGITALISATION OF AUTOMOTIVE MANUFACTURING

27

MACHINE DOWNTIMEREDUCED BY UP TO

40%

TIME TO MARKETREDUCED BY UP TO

30%

REDUCED PARTS INVENTORY BY UP TO

30%

INCREASED PRODUCTIVITY BY UP TO

5%

TOTAL CUMULATIVE ECONOMIC BENEFIT BY 2035

£74 billion

BENEFIT TO WIDER ECONOMY

£1.7 billion

BENEFIT TO VEHICLE MANUFACTURERS

£4.3 billion

BENEFIT TO SUPPLIERS

£2.6 billion

VEHICLES ON THE ROADV

EHICLES O

N TH

E RO

AD

2.5% 4.3% -0.5%2.4%

VANS4,178,733 BUS & COACH

87,778

TRUCKS595,542

CARS34,378,386

Year Cars (millions)

2006 30.8

2007 31.1

2008 31.3

2009 31.0

2010 31.3

2011 31.4

2012 31.5

2013 31.9

2014 32.6

2015 33.5

2016 34.4

28

29

39,240,439 vehicles on UK roads

There are

69,755plug-in cars in

the UK

More than

8 million

used cars were sold in 2016

A UK RECORD

The Cotswolds and

Peterborough have the highest

proportion of

plug-in cars at 1.8%

The average car on

the road in the UK is

silver from the

Supermini segment and

7.8 years old

ENVIRONMENT – CO2EN

VIRO

NM

ENT

Emissions reduction

CO2 emissions from all cars in use

-7.6%

2015

2000

69

75

Mt CO2

-8.9%

CO2 emissions from all cars in use

-7.6%

2015

2000

69

75

Mt CO2

-8.9%

A new car in 2016

is typically

19.5% more fuel-efficient

than one bought in 2010

30

ENVIR

ON

MEN

TENVIRONMENT – AIR QUALITY

A Euro-VI bus emits

95% less NOx on the road than a

Euro-V busSource: Transport for London

0.5 g/km 0.08 g/km

Reduction in diesel car NOx emissions

31

UK AUTOMOTIVE AND THE EUU

K AU

TOM

OTIV

E AN

D TH

E EU

32

AT LEAST

10% OF PEOPLE

EMPLOYED IN THE UK

AUTOMOTIVE MANUFACTURING

SECTOR ARE FROM

ELSEWHERE IN THE EU

£2.7bnCOST

ON IMPORTScar imports from the EU only

WTOWORLD TRADE ORGANISATION

ON EXPORTS

£1.8bnCOST

car exports to the EU only

WTOWORLD TRADE ORGANISATION

The European automotive industry is deeply integrated with:

69% of UK car imports coming

from the EU

56% of UK car exports heading to the EU

79% of imported components

coming from the EU

65% of British-built components

exported to the EU

SMMT Industry ForumIndustry Forum was formed

in 1994, initially as a unique

collaboration between leading

vehicle manufacturers, SMMT

and government to improve the

performance and competitiveness of

the UK’s automotive supply chain.

Continued measurable success has led to

sustained growth into many other sectors including

aerospace, construction, domestic appliances,

electronics and food. Industry Forum now provides

support to blue chip organisations in more than 30

countries across five continents.

www.industryforum.co.uk

The Motor OmbudsmanThe Motor Ombudsman is the

automotive dispute resolution

body. Fully-impartial, it is the

first ombudsman to be focused

solely on the automotive

sector, and self-regulates

the UK’s motor industry through its comprehensive

Motor Industry Codes of Practice which have each

been approved by the Chartered Trading Standards

Institute’s Consumer Codes Approval Scheme (CCAS).

www.themotorombudsman.org

SMM

T GROU

PSMMT GROUP

33

DIS C L A IM E R

This publication contains general in for mat ion

a n d , a lt h o u g h S M M T endeavours to ensure

that the content is accurate and up-to-date

at the date of publication, no representation

or warranty, express or implied, is made as to

its accuracy or completeness and therefore

the infor mat ion in th is publ icat ion should

not be rel ied upon. Readers should always

seek appropr iate ad v ice f rom a su it ably

qualif ied expert before taking, or refraining

f rom tak ing, any ac t ion . The content s of

th is publ icat ion should not be constr ued

as advice or guidance and SMMT disclaims

l iabil i t y for any loss, howsoever caused,

ar is ing direc tly or indirec tly f rom rel iance

on the information in this publicat ion. Any

use of data should be credited to SMMT.

THE SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED71 Great Peter Street, London, SW1P 2BNTel: +44 (0)20 7235 7000E-mail: [email protected]

:@SMMT :SMMT

www.smmt.co.uk

July 2017